Embed Size (px)

Citation preview

Investor Meeting

June 21, 2007

2 June 21, 2007

Today’s Schedule

Time Topic Speaker

11:00 - 11:30am Registration & Display of RR Donnelley Offerings

11:30 - 11:45am Welcome and Introduction Dan Leib

11:45 - 12:00pm One RR Donnelley Tom Quinlan

12:00 - 1:00pm Industry Dynamics & RR Donnelley Strategy

John Paloian Dan Knotts

1:00 - 1:30pm Financial Review Dan Leib Tom Quinlan

Q&A

3 June 21, 2007

Safe Harbor Statement

Use of Forward-Looking Statements This presentation contains "forward-looking statements" as defined in the U.S. Private Securities Litigation Reform Act of 1995. Readers are cautioned not to place undue reliance on these forward-looking statements and any such forward-looking statements are qualified in their entirety by reference to the following cautionary statements. All forward-looking statements speak only as of the date of this presentation and are based on current expectations and involve a number of assumptions, risks and uncertainties that could cause the actual results to differ materially from such forward-looking statements. The company does not undertake to and specifically declines any obligation to publicly release the results of any revisions to these forward-looking statements that may be made to reflect future events or circumstances after the date of such statement or to reflect the occurrence of anticipated or unanticipated events.

The factors that could cause material differences in the expected results of RR Donnelley include, without limitation, the following: the successful execution and integration of acquisitions and the performance of the company's businesses following acquisitions; the ability to implement comprehensive plans for the execution of cross-selling, cost containment, asset rationalization and other key strategies; competitive pressures in all markets in which the company operates; factors that affect customer demand, including changes in postal rates and postal regulations, changes in the capital markets, changes in advertising markets, the rate of migration from paper-based forms to digital format, customers' budgetary constraints and customers' changes in short-range and long-range plans; shortages or changes in availability, or increases in costs of, key materials (such as ink, paper and fuel); and other risks and uncertainties described in RR Donnelley's periodic filings with the Securities and Exchange Commission (SEC). Readers are strongly encouraged to read the full cautionary statements contained in RR Donnelley's filings with the SEC. RR Donnelley disclaims any obligation to update or revise any forward-looking statements.

4 June 21, 2007

Non-GAAP Financial Information

The company believes that certain non-GAAP measures, when presented in conjunction with comparable GAAP measures, are useful because that information is an appropriate measure for evaluating the company’s operating performance. Internally, the company uses this non-GAAP information as an indicator of business performance, and evaluates management’s effectiveness with specific reference to these indicators. These measures should be considered in addition to, not a substitute for, or superior to, measures of financial performance prepared in accordance with GAAP.

A reconciliation of GAAP net earnings to non-GAAP net earnings and further descriptions are presented in the tables attached to our Earnings Releases, which are available in the investors section of our website, rrdonnelley.com. Also available in the investors section of our website, rrdonnelley.com, is a description of additional non-GAAP financial measures referred to in this presentation.

Twelve Months Ended December 31,

In $ millions, except EPS 2003 2004 2005 2006

Income from Cont. Ops EPS

Income from Cont. Ops EPS

Income from Cont. Ops EPS

Income from Cont. Ops EPS

GAAP results $292.7 $1.54 $459.2 $0.88 $450.4 $0.63 $750.7 $1.83

AdjustmentsRestructuring and impairments - net 12.5 0.07 107.4 0.31 419.8 1.83 206.1 0.79 Integration charges - - 80.8 0.23 8.3 0.02 - - Income Tax adjustment - (0.44) - (0.16) - - - (0.11) Net (income) from Discontinued Operations - 0.13 - 0.39 - (0.19) - 0.01 Cumulative effect of change in accounting principle - - - 0.03 - - - - Other non-GAAP adjustments - 0.01 - (0.03) - - - 0.03 Total Adjustment 12.5 (0.23) 188.2 0.77 428.1 1.66 206.1 0.72

Non-GAAP results 305.2 $1.31 647.4 $1.65 878.5 $2.29 956.8 $2.55

Depreciation and amortization 270.3 385.5 425.0 463.3 EBITDA (non-GAAP) $575.5 $1,032.9 $1,303.5 $1,420.1

5 June 21, 2007

Agenda

One RR Donnelley

Industry Dynamics & RR Donnelley Strategy

Financial Review

Q&A

6 June 21, 2007

Building RR Donnelley to Succeed

Note: (1) In addition, RRD completed the acquisition of Ad-Plex Rhodes Charlestown facility in August, 2005, Spencer Press in November, 2005, CMCS in December, 2005 and Canadian Bank Note in October, 2006

May 2003February 2004

June 2005

April 2006

Acquisitions(1)Divestitures

December 2005

October 2004Package Logistics

July 2005

Sept 2005Poligrafia

January 2007

May 2007

7 June 21, 2007

Product and Related Services Opportunity

PREPARE PRODUCE DELIVER

Premedia ServicesStudio PhotographyColor ServicesPage Layout & ProcessingFacilities ManagementAd ManagementDigital Asset ManagementOffshore Service Offering

Broadest Product PortfolioCatalogsMagazinesRetail InsertsDirectoriesBooksCommercialDirect MailStatementsFinancialFormsLabelsBPO

Print LogisticsPrint DistributionFulfillment and KittingExpedited Services

2006: $374 Billion Print Market Worldwide, $172 Billion in the U.S.

Gravure, Offset and Digital Capabilities

8 June 21, 2007

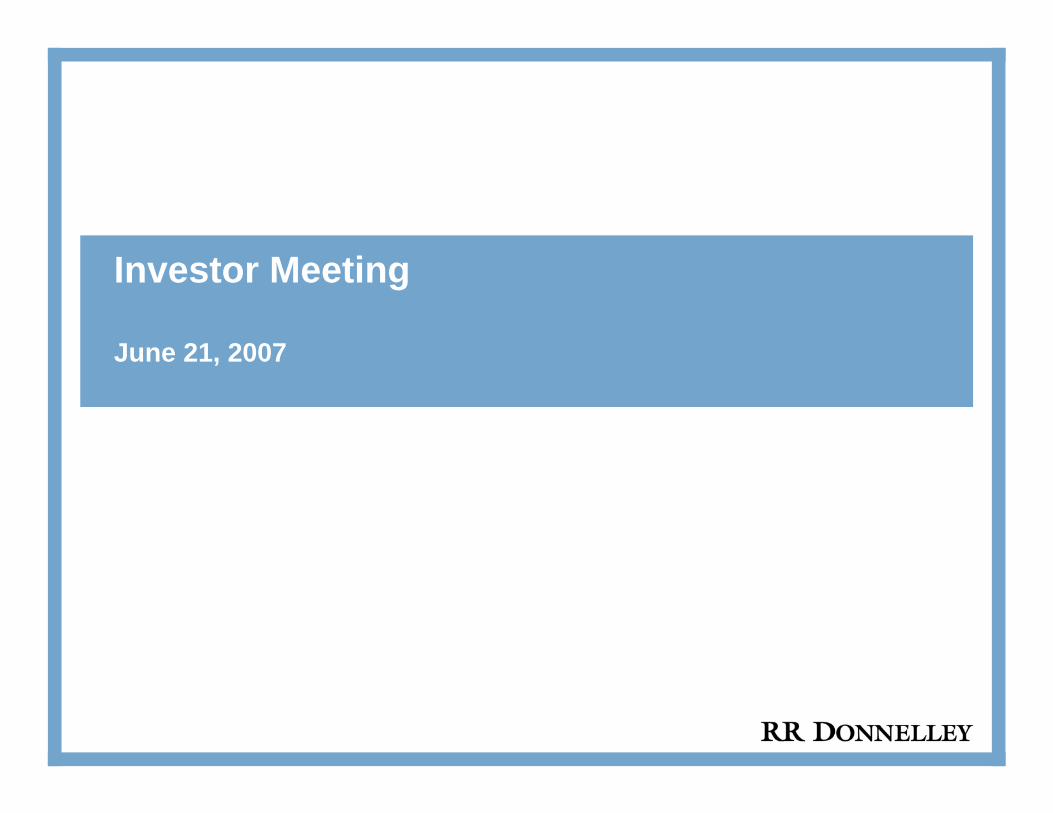

The World’s Premier Print and Related Services Company

Brand Strength

Distinct ServiceOffering

Delivers on Promises

Over 600 locations in

35+ countries

Serve > 90% of the

Fortune 500

Scale Advantages

Financial Flexibility

Low Cost Provider

Product Line

Breadth

Recurring Revenue

Strategic Operational Financial

Over 40,000 Customers

Platform Flexibility

9 June 21, 2007

Simplified Branding

Rebrand Moore Wallace and certain other trade names as RR Donnelley

Effective Q3 2007, we will realign the management and reporting structure

Simplifies client and internal interactions

Results in an approximately $315 million non-cash impairment charge

10 June 21, 2007

10

Deep Customer Relationships

Blue Chip Customer Relationships

And many others…

Total of 40,000 Customers

125 customers with revenue > $10 million (1)

950 customers with revenue > $1 million (1)

Serve over 90% of Fortune 500 and have approximately 15% of their print spend

• Opportunity to continue to grow our Fortune 500 Relationships

(1) Includes only revenue generated in North America

11 June 21, 2007

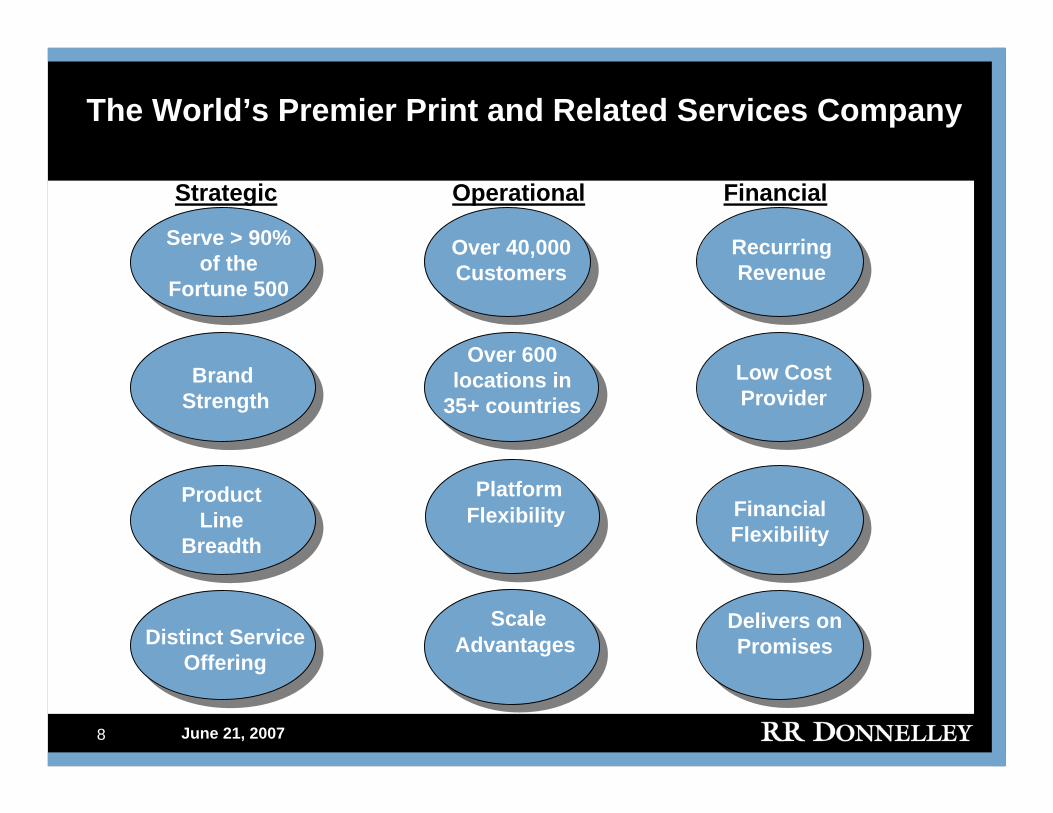

Plenty of Opportunity to Expand Relationships

We offer 15 core products and services

150 customers purchase 7 or more products/services

(1) Includes only products/services provided in North America

Multi-offering purchasers66

38

27

105 6

0

10

20

30

40

50

60

70

7 8 9 10 11 12+# of products/services purchased from RR Donnelley

# of

Cus

tom

ers

12 June 21, 2007

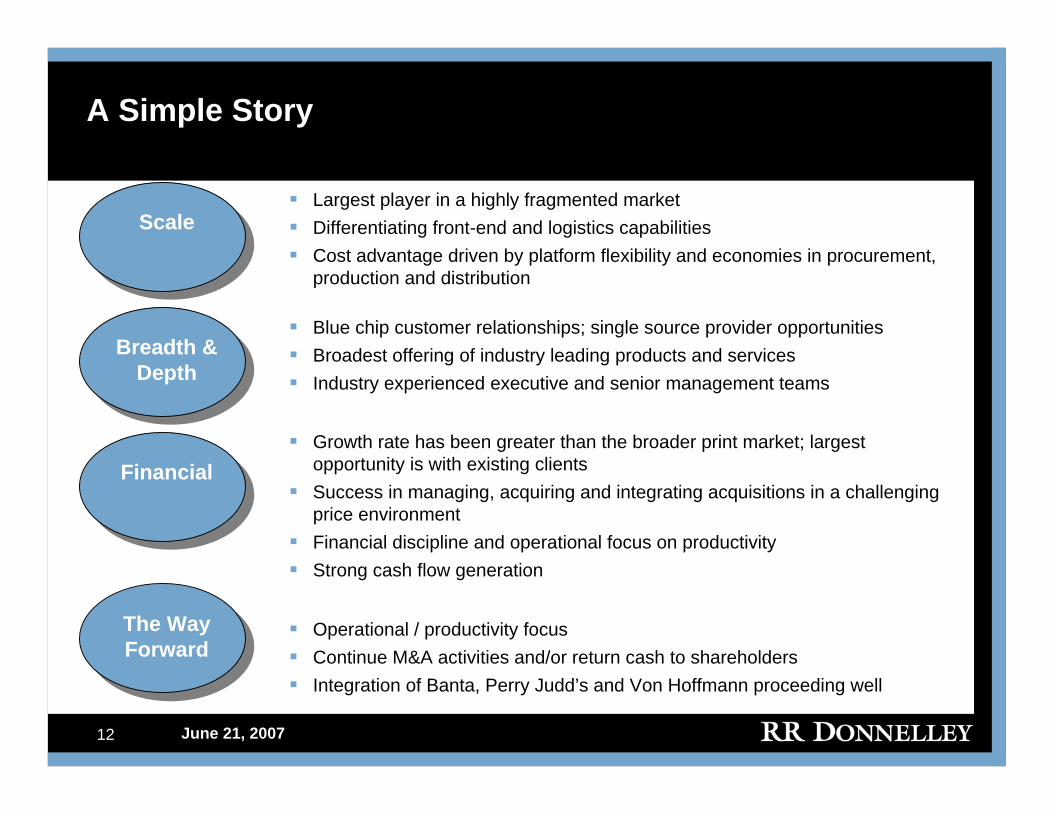

A Simple Story

Largest player in a highly fragmented marketDifferentiating front-end and logistics capabilitiesCost advantage driven by platform flexibility and economies in procurement, production and distribution

Scale

Breadth & Depth

Blue chip customer relationships; single source provider opportunitiesBroadest offering of industry leading products and servicesIndustry experienced executive and senior management teams

FinancialGrowth rate has been greater than the broader print market; largest opportunity is with existing clientsSuccess in managing, acquiring and integrating acquisitions in a challenging price environmentFinancial discipline and operational focus on productivityStrong cash flow generation

The Way Forward

Operational / productivity focusContinue M&A activities and/or return cash to shareholdersIntegration of Banta, Perry Judd’s and Von Hoffmann proceeding well

13 June 21, 2007

Agenda

One RR Donnelley

Industry Dynamics & RR Donnelley Strategy

Financial Review

Q&A

14 June 21, 2007

Trends Shaping Industry

Customer Relationship Management

Consolidation(Printers, Suppliers

& Customers)

Electronic Substitution

Trends generally continuing at same paceImpact differs by print sector: results in new products / services

Total System Cost Focus

Regulatory Changes

Shift toward variable (customized), higher value-add printIT / data management capabilities increasingly importantto customers

Pricing pressureLarge / diversified printers are better positioned to be successfulPrivate equity presence changing buying dynamics

Positive and negative implicationsPrinters’ ability to offer compliance assurance / secure environment increasingly important

Printers who are able to offer lowest total print / document management cost and higher ROI are advantaged

15 June 21, 2007

Consolidating Industry*

*Sample representation – estimated total of 39,088 printing facilities in the United States at the end of 2006 (PIA/GATF, April 3, 2007). Source: RR Donnelley management estimates

16 June 21, 2007

Consolidating Supplier Base

Flint/NAPIC + Continental BASF Graphics + Alper Ink Group + SICPA + Day

Flint acquired by XSYS European

Source: RR Donnelley management estimates

1980

2007

Paper Suppliers

Stora/Enso

Bowater/Avenor

Domtar/WeyerhaeuserAbitibi/BowaterMead/WestvacoUPM/KymmeneIP/ChampionGeorgia Pacific/Ft. James

Ink Suppliers

Dai Nippon/SunINX/Acme + Midland

17 June 21, 2007

Consolidation Runs Across Business Spectrum

Media Companies

Retailers

Catalogers

Magazine & Book Publishers

Pharmaceuticals

Automotive

Bank/Financial Institutions

Food Industry

18 June 21, 2007

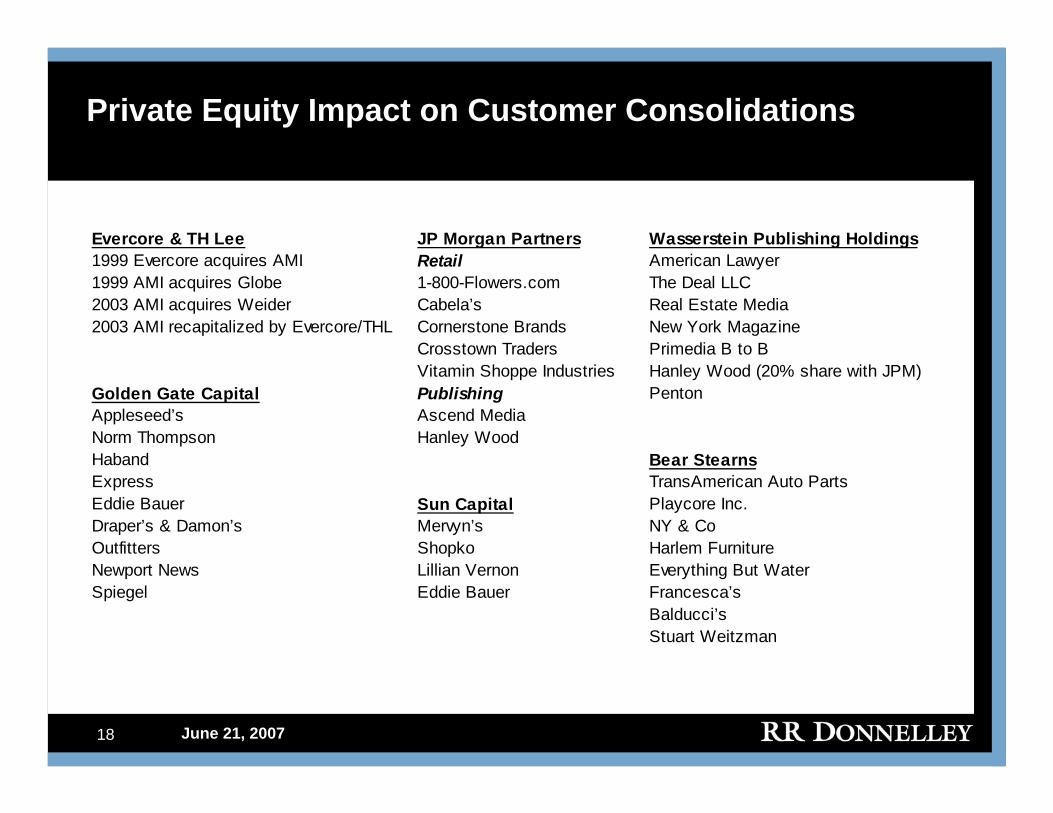

Private Equity Impact on Customer Consolidations

Evercore & TH Lee JP Morgan Partners Wasserstein Publishing Holdings1999 Evercore acquires AMI Retail American Lawyer 1999 AMI acquires Globe 1-800-Flowers.com The Deal LLC 2003 AMI acquires Weider Cabela’s Real Estate Media 2003 AMI recapitalized by Evercore/THL Cornerstone Brands New York Magazine

Crosstown Traders Primedia B to B Vitamin Shoppe Industries Hanley Wood (20% share with JPM)

Golden Gate Capital Publishing Penton Appleseed’s Ascend MediaNorm Thompson Hanley WoodHaband Bear StearnsExpress TransAmerican Auto Parts Eddie Bauer Sun Capital Playcore Inc. Draper’s & Damon’s Mervyn’s NY & Co Outfitters Shopko Harlem Furniture Newport News Lillian Vernon Everything But Water Spiegel Eddie Bauer Francesca’s

Balducci’s Stuart Weitzman

19 June 21, 2007

Change in Ownership has Driven Change in Buying Dynamics

From… To…

Focus on lowest total document management costs and also on achieving highest ROI

Contractual relationship

Fragmented print procurement across different functions / divisions / geographies

Focus on lowest print cost

In-house print / document management

Transactional relationships

Consolidated print procurement,centrally managed

Outsourcing non-core processes including print / document process management

20 June 21, 2007

The Evolution of Print Relationships

Source: Derived from InfoTrends/Cap Ventures

Single Product Relationships

Time

Cus

tom

er R

elat

ions

hips

Outsourced print andValue-Added Services

Multiple Product Relationships

Total Cost of Process/Procurement

Function

100% of Core Product(s)

1864 2000 2006 2007+

Client’s focus on print supply chain, not just print

RRD reaches across total value chain

Ability to bring scale• Procurement• Distribution• Production

Leverage the relationship• 100% Positions• Trust in place• Vested Interest

21 June 21, 2007

The Evolution of RR Donnelley’s Strategy

ManagementPut “World Class” team together

Built support infrastructure

• Admin/Finance/Ops

InvestmentDeveloped and implemented new strategy

Built, through organic investments and acquisitions, flexible full-service platform

OperationalFocused on continual productivity improvements

Absorbed equipment installs

Absorbed and integrated acquisitions

Asserted disciplines/metrics (cost compression culture)

22 June 21, 2007

The RR Donnelley Strategy – Profitable Growth

Targeted sales strategy• Winners/consolidators in their space• Contractual opportunities – opening the window• 100% positions

Disciplined investment approach• Organic investment• Targeted acquisitions

Trade-off with capital expenditures

Productivity and waste reduction

Building a Global Platform for Global Customer Needs

23 June 21, 2007

The RR Donnelley Strategy – A Disciplined Approach

Key Elements

Market / platform versus business unit approach

Window of opportunity - prioritization

Standardized capital investment approach

Flexibility to adapt to evolving customer needs

24 June 21, 2007

One RR Donnelley (Illustrative)

Magazine Publisher

Book Publisher

Directory Publisher

Healthcare Financial Retail

Internal Process (Pricing, Production Planning)

One Global Platform

Sales and Marketing

Sheetfed

PREPARE PRODUCE DELIVERGravure Offset

DigitalBindery

25 June 21, 2007

The RR Donnelley Strategy - Driving Profitable Growth

Sales growth targets

Platform optimization• Asset utilization

• Productivity focus

Organic investment• Expand and upgrade base platform

• Equipment balance

Acquisitions• Targeted for customers, equipment, capacity, capabilities, people

• Disciplined analysis

26 June 21, 2007

Platform Optimization - Asset Utilization

36%64%

1st Half 2nd Half

Off peak (1H) growth has exceeded peak (2H) growth by over $100 million from 2004 to 2006

% of Revenue Growth (2004 – 2006)*

* 2004-06 growth in most historically seasonal offerings (magazines, catalogs, retail inserts, books and directories)

27 June 21, 2007

Platform Optimization – Productivity Focus

Leverage RR Donnelley scale• Supply chain

• Shared services

• One platform

Targeted investment• Quality and service

• Waste, throughput and cost takeout

28 June 21, 2007

Organic Investment

Capacity investment• 50+ presses and binding lines installed• Assortment of standardized asset types to optimize platform• Overall increase in capacity utilization

Capability investment• Targeted to meet market and customer requirements• Standardization to drive flexibility

Productivity / Compliance / Maintenance investment• Relentless approach to cost takeout and waste reduction• Safety focused• Infrastructure requirements

29 June 21, 2007

The RR Donnelley Strategy – A Living Process

Keys to Success

Industry and market knowledge

Sales planning

Leveraging scale as one platform

Investment prioritization

Sales Growth Targets

Platform Optimization

Organic Investment

Acquisitions

30 June 21, 2007

RR Donnelley - An Unmatched Portfolio

Books

Statements BPO & Document

ManagementCatalogs

Commercial Printing

Direct Mail

Directories

In-Box & Global Turnkey

Solutions

Logistics/Fulfillment Services

Magazines

Labels & Label SystemsRetail Inserts

Financial Services

eCommerce Tools

Forms

Premedia Services

2006: $374 Billion Market Worldwide, $172 Billion in the U.S.

31 June 21, 2007

RR Donnelley International Presence

32 June 21, 2007

New Customers and Expansion of Relationships

Since February 2004, the contract value of our largest new business wins and renewals…

Totals over $6.5 billion

33 June 21, 2007

RRD Existing Global Customers

34 June 21, 2007

RR Donnelley is Differentiated to Drive Growth

Comprehensive global printing & print-related services platform• Reaches across total value chain• Allows for maximum cost compression

Global outsourcing / procurement capabilityScale associated with leveraged buying

• Materials• Logistics

Leveraging long-term customer relationships/contracts• 100% positions in place• Trust is already earned• “Vested interest”

Financial strength and stability

35 June 21, 2007

Agenda

One RR Donnelley

Industry Dynamics & RR Donnelley Strategy

Financial Review

Q&A

36 June 21, 2007

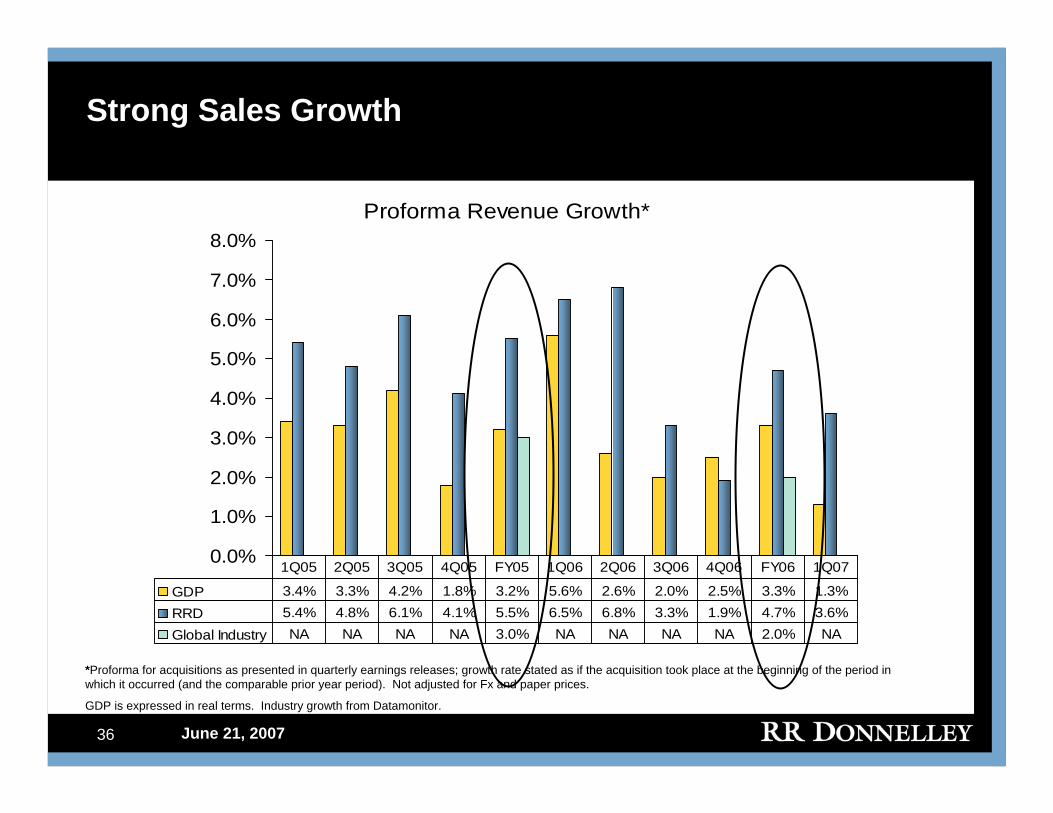

Strong Sales Growth

Proforma Revenue Growth*

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

GDP 3.4% 3.3% 4.2% 1.8% 3.2% 5.6% 2.6% 2.0% 2.5% 3.3% 1.3%RRD 5.4% 4.8% 6.1% 4.1% 5.5% 6.5% 6.8% 3.3% 1.9% 4.7% 3.6%Global Industry NA NA NA NA 3.0% NA NA NA NA 2.0% NA

1Q05 2Q05 3Q05 4Q05 FY05 1Q06 2Q06 3Q06 4Q06 FY06 1Q07

*Proforma for acquisitions as presented in quarterly earnings releases; growth rate stated as if the acquisition took place at the beginning of the period in which it occurred (and the comparable prior year period). Not adjusted for Fx and paper prices.

GDP is expressed in real terms. Industry growth from Datamonitor.

37 June 21, 2007

4,183

7,156

8,430

9,317

0

2,000

4,000

6,000

8,000

10,000

2003 2004 2005 2006

Rev

enue

($m

m)

EBITDA Growth has Exceeded Sales Growth

CAGR = 35%

576

1,033

1,304

1,420

0

400

800

1,200

1,600

2003 2004 2005 2006

EBIT

DA

($m

m)

CAGR = 31%

38 June 21, 2007

0%

100%

Revenue Cost of Sales SG&A D&A Earnings fromCont. Ops

% o

f Rev

enue

Materials Labor Other Semi-variable Fixed D&A

2006 Profitability and Cost Detail

39 June 21, 2007

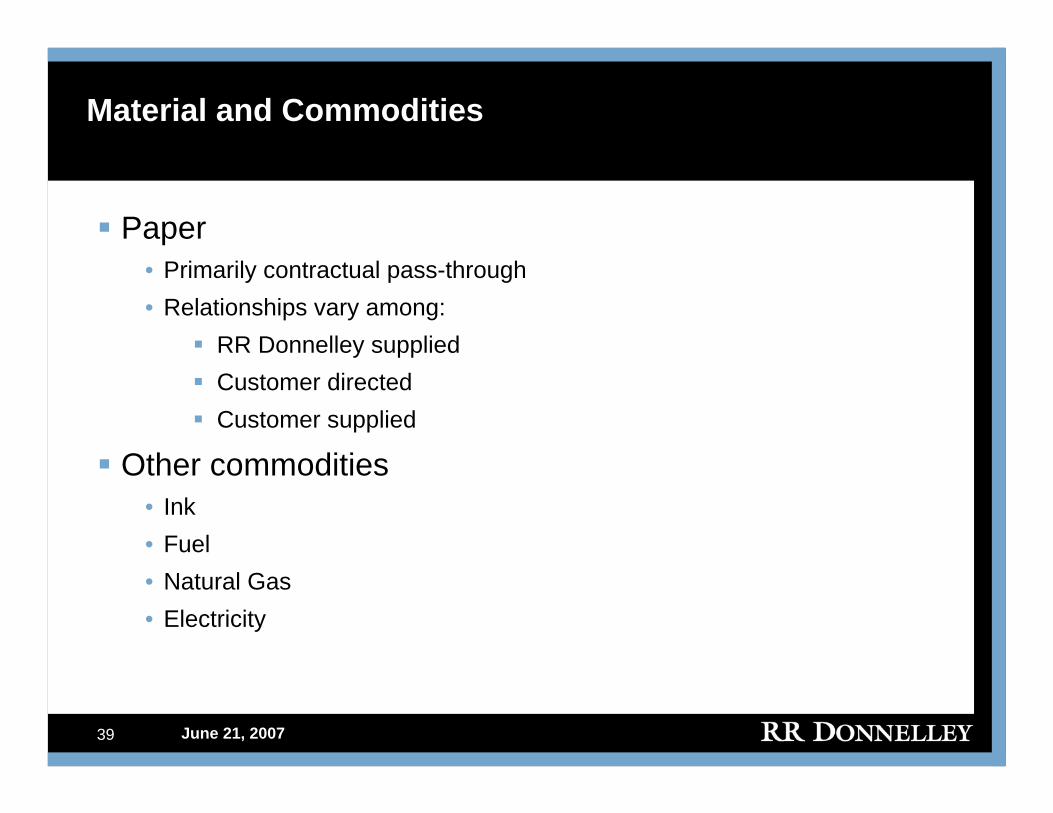

Material and Commodities

Paper• Primarily contractual pass-through• Relationships vary among:

RR Donnelley suppliedCustomer directedCustomer supplied

Other commodities• Ink• Fuel• Natural Gas• Electricity

40 June 21, 2007

270

386425

463

595

193

265

471

374

450-475

4.6%3.7%

5.6%

4.0% 4.0%

0

100

200

300

400

500

600

700

2003 2004 2005 2006 2007

Depreciation & AmortizationCapexCapex as % Revenue

Historically, D&A has exceeded Capital Expenditures

$ in Millions

Capital expenditure as a % of Revenue is expected to decrease in 2008

2008 capex expected to decrease to 3.5% to 4.0% of revenue

Platform refresh investments

41 June 21, 2007

$1.31

$1.65

$2.29$2.55

$0.11

$0.18

$0.23

$0.35

$2.70 - 2.75

$0.00

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

2003 2004 2005 2006 2007

Strong Non-GAAP Earnings per Share Growth

CAGR = 20%

CAGR = 24%, adjusted for purchasing accounting amortization

Non-GAAP EPS Dilutive Impact of Purchasing Accounting

Note: Dilutive impact of Purchase Accounting amortization calculated using amortization of intangibles, tax effected at the company’s non-GAAP effective tax rate.

42 June 21, 2007

Business Generates Substantial Cash Flow

$376

$759

$972$904

$183

$494 $501 $530

0

200

400

600

800

1,000

1,200

2003 2004 2005 2006

Cash Flow from Continuing Ops (CFFCO)CFFCO - Capex

$mm

43 June 21, 2007

Debt Maturity Profile

$ in millions

400499

624 598499

969

$0

$200

$400

$600

$800

$1,000

$1,200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016+

Weighted average interest rate of ~5.50% on existing long-term debt• Most outstanding debt at fixed rate

Few near-term maturities

3.75% 4.95% 4.95% 5.50% 6.65%Interest Rate 5.63%

44 June 21, 2007

Cash

Internal

Investment

Share

BuybackDividend Acquisition Debt Repay

• Organic Growth

• Cost Management

• Maintenance

Multiple Avenues to Value Creation

• Topline growth in line with GDP• Productivity to offset price• Cash flow and capital allocated to

drive value

• Discount to intrinsic value

• Accretive use of cash

• Furthers customer relationship

• Cost synergies

• Excess capacity

• Investor preference for distribution

• ST cash management

• Strong credit metrics

45 June 21, 2007

Balanced Capital Deployment

Very strong balance sheet and cash position

Strong investment grade credit ratings• Moody’s = Baa2• S&P = BBB+

Prioritization of cash flows• Dividend maintained at $1.04 per share/year• Internal capital to support growth/productivity• Continued M&A and/or return cash to shareholders

46 June 21, 2007

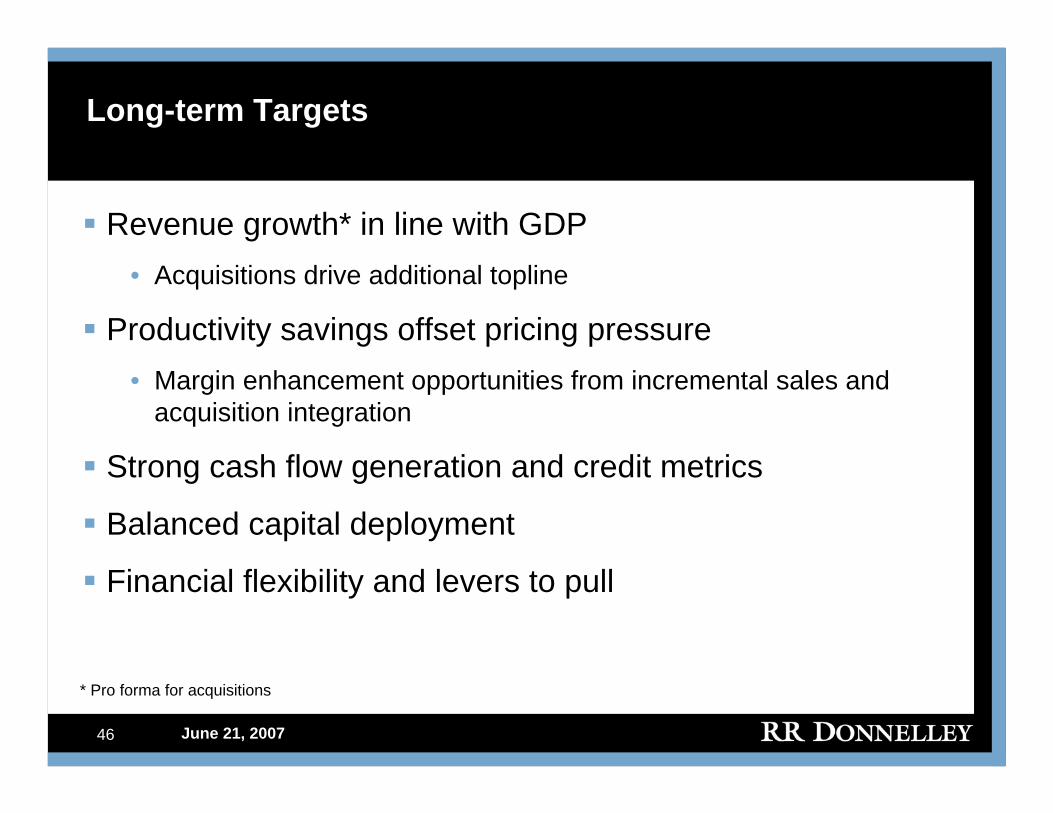

Long-term Targets

Revenue growth* in line with GDP• Acquisitions drive additional topline

Productivity savings offset pricing pressure• Margin enhancement opportunities from incremental sales and

acquisition integration

Strong cash flow generation and credit metrics

Balanced capital deployment

Financial flexibility and levers to pull

* Pro forma for acquisitions

47 June 21, 2007

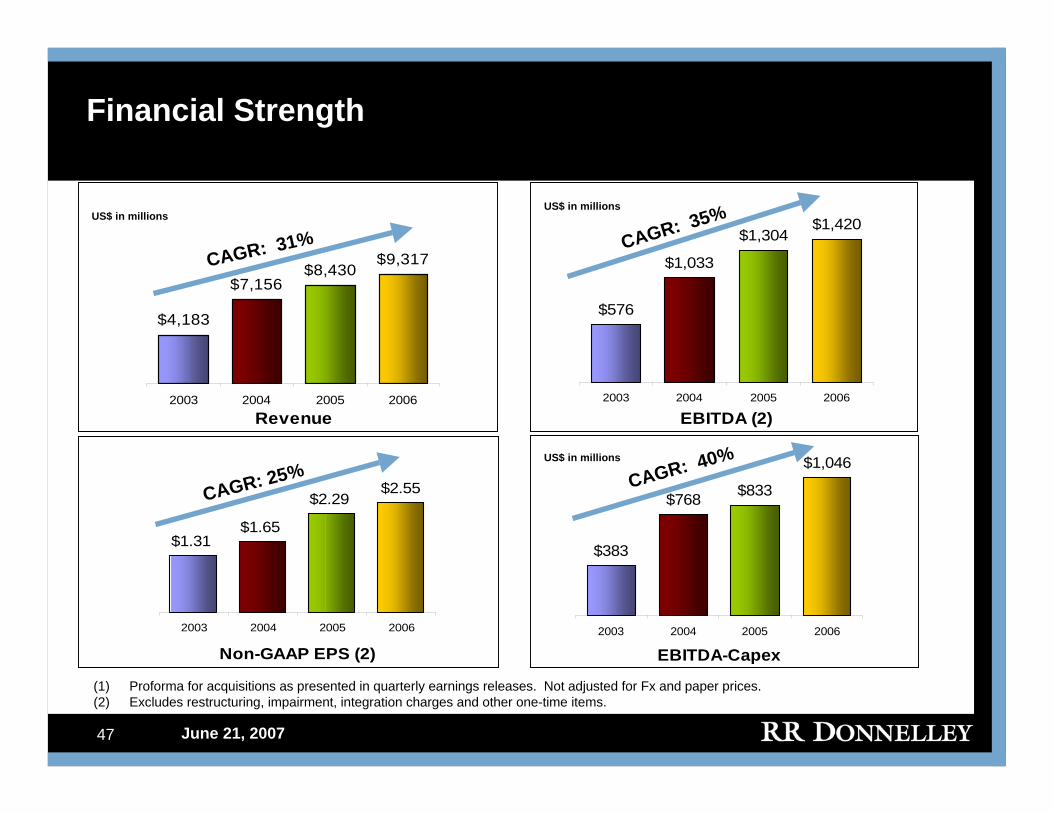

Financial Strength

$576

$1,033

$1,304$1,420

2003 2004 2005 2006

EBITDA (2)

$1.31$1.65

$2.29$2.55

2003 2004 2005 2006

Non-GAAP EPS (2)

$383

$768 $833

$1,046

2003 2004 2005 2006

EBITDA-Capex

CAGR: 25% CAGR: 40%

CAGR: 35%

(1) Proforma for acquisitions as presented in quarterly earnings releases. Not adjusted for Fx and paper prices.(2) Excludes restructuring, impairment, integration charges and other one-time items.

US$ in millions

US$ in millions

$4,183

$7,156$8,430

$9,317

2003 2004 2005 2006Revenue

CAGR: 31%US$ in millions

48 June 21, 2007

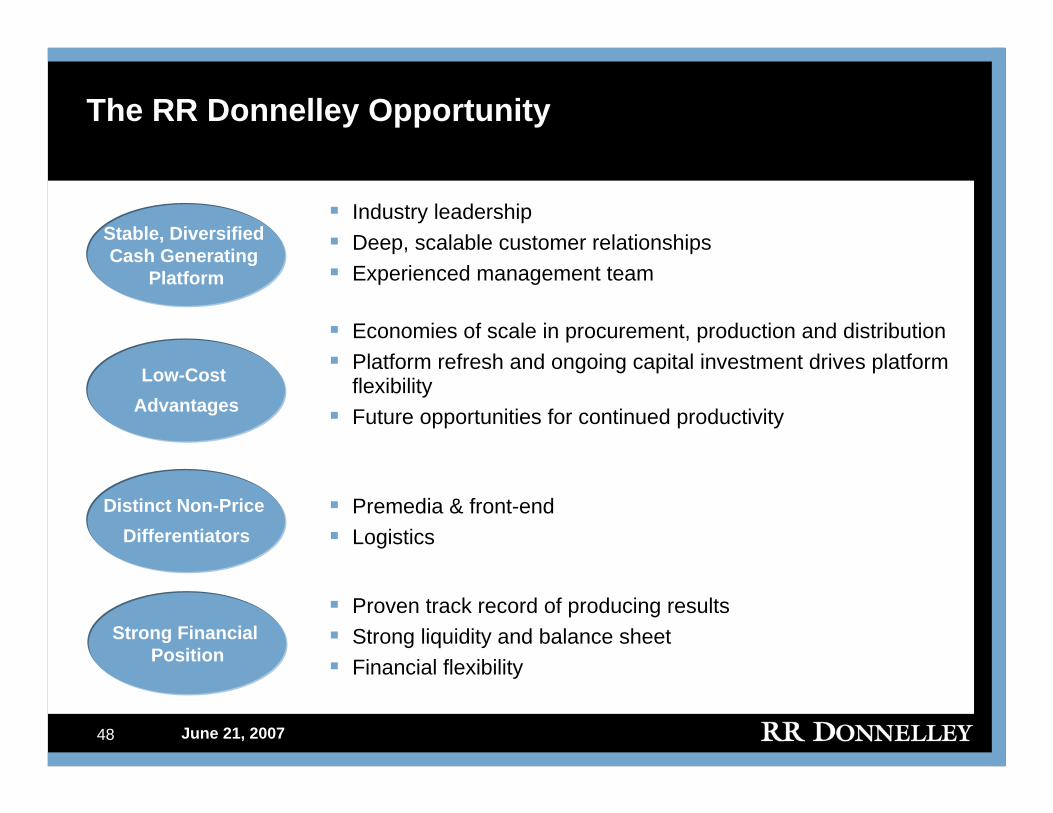

Distinct Non-Price Differentiators

Low-Cost Advantages

Stable, Diversified Cash Generating

Platform

Industry leadership Deep, scalable customer relationshipsExperienced management team

Economies of scale in procurement, production and distributionPlatform refresh and ongoing capital investment drives platform flexibilityFuture opportunities for continued productivity

Premedia & front-endLogistics

Strong Financial Position

The RR Donnelley Opportunity

Proven track record of producing resultsStrong liquidity and balance sheetFinancial flexibility

49 June 21, 2007

Agenda

One RR Donnelley

Industry Dynamics & RR Donnelley Strategy

Financial Review

Q&A

Investor Meeting

June 21, 2007