JUNE 2019

INVESTOR PRESENTATIONBUILDING A TOP 10 GLOBAL RESTAURANT BRAND

FORWARD-LOOKING STATEMENTS

This presentation contains forward-looking statements that are subject to risks and uncertainties.

All statements other than statements of historical fact or relating to present facts or current

conditions included in this presentation are forward-looking statements. Forward-looking statements

give Wingstop Inc.’s (the “Company”) current expectations and projections relating to its financial

condition, results of operations, plans, objectives, future performance and business. You can identify

forward-looking statements by the fact that they do not relate strictly to historical or current facts.

These statements may include words such as “anticipates,” “believes,” “continues,” “estimates,”

“expects,” “goal,” “objectives” “intends,” “may,” “opportunity,” “plans,” “potential,” “near-term,”

“long-term,” “projections,” “assumptions,” “projects,” “guidance,” “forecasts,” “outlook,” “target,”

“trends,” “should,” “could,” “would,” “will” and similar expressions and terms of similar meaning in

connection with any discussion of the timing or nature of future operating or financial performance or

other events.

The forward-looking statements contained in this presentation are based on assumptions that the

Company has made in light of its industry experience and perceptions of historical trends, current

conditions, expected future developments and other factors it believes are appropriate under the

circumstances. As you read and consider this presentation, you should understand that these

statements are not guarantees of performance or results. They involve risks, uncertainties (many

of which are beyond the Company’s control) and assumptions. Although the Company believes

that these forward-looking statements are based on reasonable assumptions, you should be

aware that many factors could affect its actual operating and financial performance and cause its

performance to differ materially from the performance anticipated in the forward-looking

statements. The Company believes these factors include, but are not limited to, those described

under the sections “Risk Factors” and “Management’s Discussion and Analysis of Financial

Condition and Results of Operations” in its Annual Report on Form 10-K and subsequent periodic

reports filed with the Securities and Exchange Commission (the “SEC”). Should one or more of

these risks or uncertainties materialize, or should any of these assumptions prove incorrect, the

Company’s actual operating and financial performance may vary in material respects from the

performance projected in these forward-looking statements.

Any forward-looking statement made by the Company in this presentation speaks only as of the

date on which it is made. Factors or events that could cause the Company’s actual operating and

financial performance to differ may emerge from time to time, and it is not possible for the

Company to predict all of them. The Company undertakes no obligation to publicly update any

forward-looking statement, whether as a result of new information, future developments or

otherwise, except as may be required by law.

NON-GAAP FINANCIAL MEASURES

This presentation contains certain non-GAAP financial measures. A “non-GAAP financial

measure” is defined as a numerical measure of a company’s financial performance that excludes

or includes amounts so as to be different than the most directly comparable measure calculated

and presented in accordance with GAAP in the statements of income, balance sheets or

statements of cash flow of the company. The Company has provided a reconciliation of Adjusted

EBITDA, a non-GAAP financial measure, to net income in the Appendix to this presentation.

Adjusted EBITDA is presented because management believes that such financial measure, when

viewed with the Company’s results of operations presented in accordance with GAAP and the

reconciliation of Adjusted EBITDA to net income, provides additional information to investors

about certain material non-cash items and about unusual items that the Company does not expect

to continue at the same level in the future. Adjusted EBITDA is used by investors as a

supplemental measure to evaluate the overall operating performance of companies in the

Company’s industry, but you should not consider it in isolation, or as a substitute for analysis of

results as reported in accordance with GAAP. The Company’s calculation of Adjusted EBITDA

may not be comparable to that reported by other companies. For additional information about the

Company’s non-GAAP financial measures, see the Company’s filings with the SEC.

FORWARD-LOOKING STATEMENTS

Wingstop Investor Presentation1

Corporate Overview2

OUR MISSION: TO SERVE THE

WORLD FLAVOR

OUR VISION: TO BECOME A TOP 10

GLOBAL RESTAURANT BRAND

OUR CORE VALUES:

• SERVICE-MINDED

• AUTHENTIC

• FUN

• ENTREPRENEURIAL

THE WINGSTOP BRAND

Wingstop operates and franchises a global

network of restaurants with the mission of

serving the world FLAVOR.

With a menu of 11 bold, distinctive flavors of

classic and boneless chicken wings,

Wingstop is the destination for made-to-crave

wings and sides.

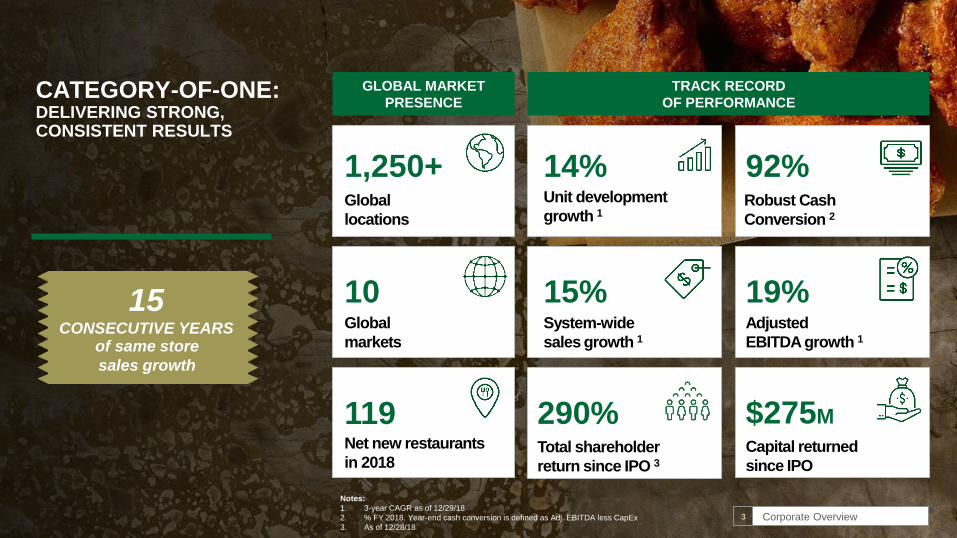

CATEGORY-OF-ONE: DELIVERING STRONG, CONSISTENT RESULTS

Notes:

1. 3-year CAGR as of 12/29/18

2. % FY 2018. Year-end cash conversion is defined as Adj. EBITDA less CapEx

3. As of 12/28/18

GLOBAL MARKET

PRESENCE

1,250+Global

locations

Corporate Overview3

10Global

markets

119Net new restaurants

in 2018

TRACK RECORD

OF PERFORMANCE

14%Unit development

growth 1

15%System-wide

sales growth 1

Capital returned

since IPO

$275M

19%Adjusted

EBITDA growth 1

92%Robust Cash

Conversion 2

Total shareholder

return since IPO 3

290%

15 CONSECUTIVE YEARS

of same store

sales growth

Corporate Overview4

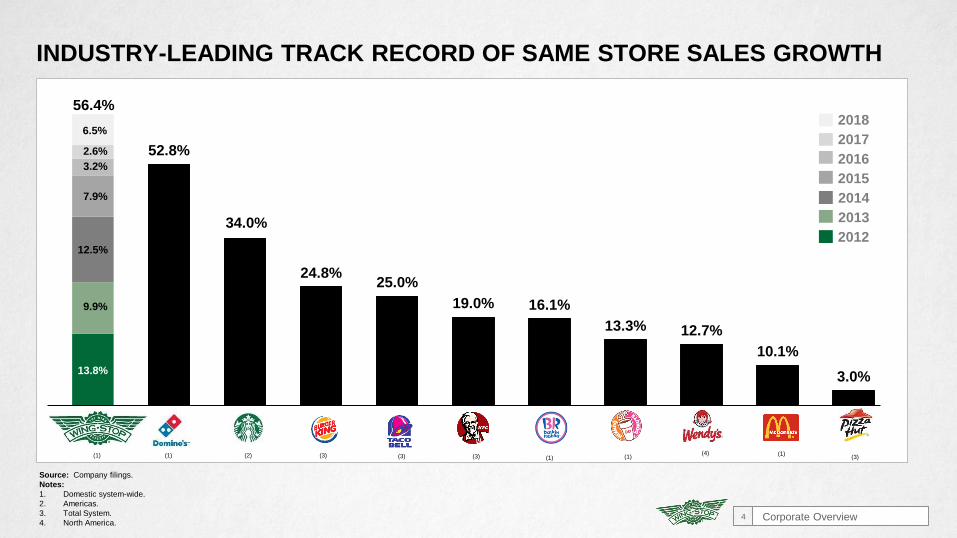

INDUSTRY-LEADING TRACK RECORD OF SAME STORE SALES GROWTH

13.8%

9.9%

12.5%

7.9%

3.2%

2.6%

56.4%

52.8%

34.0%

24.8%25.0%

19.0% 16.1%

13.3% 12.7%

10.1%

3.0%

Source: Company filings.

Notes:

1. Domestic system-wide.

2. Americas.

3. Total System.

4. North America.

2014

2013

2012

2015

2016

2017

(1) (1)(3) (1)(1)(3)(4)(3)(1) (2) (3)

20186.5%

Long-term Growth Strategy5

INVEST IN PEOPLE AND INFRASTRUCTURE TO BUILD THE ORGANIZATION FOR THE NEXT LEVEL

PATH TO BECOMING A TOP 10 GLOBAL RESTAURANT BRAND

National

Advertising

Digital

Delivery

Cost of Goods

Mitigation

Operating

Efficiencies

Advantages

of Scale

Fortress Key

U.S. Markets

Continue International

Expansion

Enter Non-Traditional

Restaurant Locations

SUSTAIN SSS VIA BRAND

AWARENESS AND INNOVATION

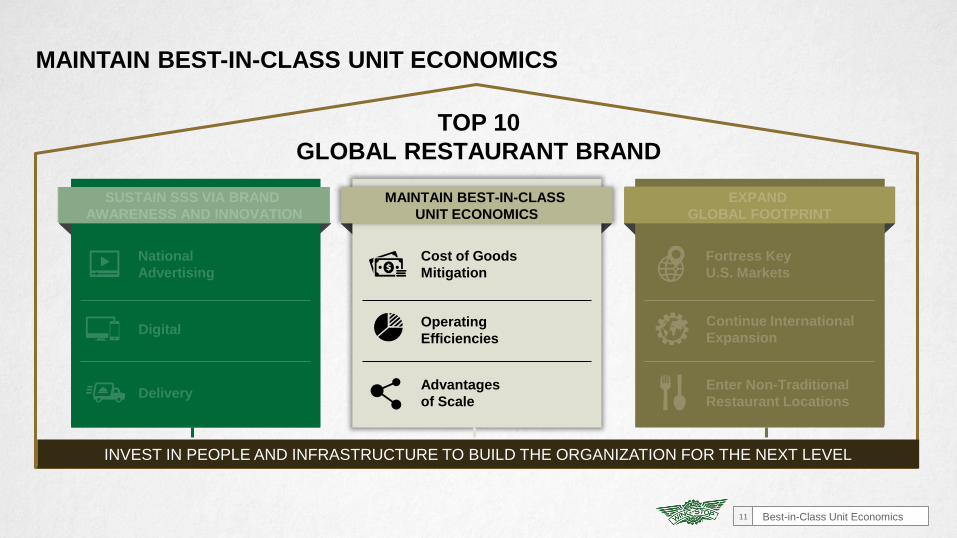

MAINTAIN BEST-IN-CLASS

UNIT ECONOMICS

EXPAND

GLOBAL FOOTPRINT

TOP 10

GLOBAL RESTAURANT BRAND

Brand Awareness & Innovation6

SUSTAIN SSS GROWTH VIA BRAND AWARENESS AND INNOVATION

INVEST IN PEOPLE AND INFRASTRUCTURE TO BUILD THE ORGANIZATION FOR THE NEXT LEVEL

National

Advertising

Digital

Delivery

Cost of Goods

Mitigation

Operating

Efficiencies

Advantages

of Scale

Fortress Key

U.S. Markets

Continue International

Expansion

Enter Non-Traditional

Restaurant Locations

SUSTAIN SSS VIA BRAND

AWARENESS AND INNOVATION

MAINTAIN BEST-IN-CLASS

UNIT ECONOMICS

EXPAND

GLOBAL FOOTPRINT

TOP 10

GLOBAL RESTAURANT BRAND

6%

29%

2017 2018 2019

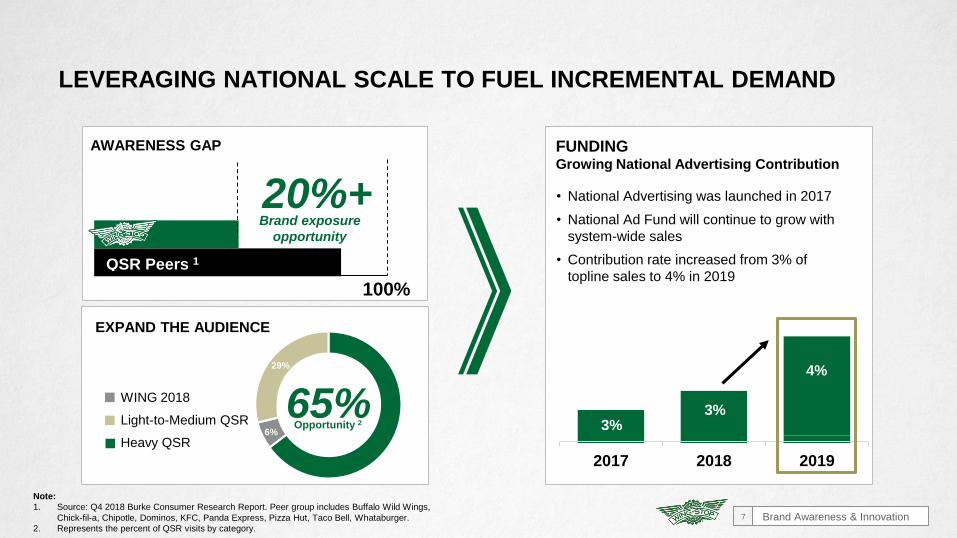

FUNDING Growing National Advertising Contribution

• National Advertising was launched in 2017

• National Ad Fund will continue to grow with

system-wide sales

• Contribution rate increased from 3% of

topline sales to 4% in 2019

AWARENESS GAP

QSR Peers 1

Note:

1. Source: Q4 2018 Burke Consumer Research Report. Peer group includes Buffalo Wild Wings,

Chick-fil-a, Chipotle, Dominos, KFC, Panda Express, Pizza Hut, Taco Bell, Whataburger.

2. Represents the percent of QSR visits by category.

Brand exposure

opportunity

20%+

LEVERAGING NATIONAL SCALE TO FUEL INCREMENTAL DEMAND

Brand Awareness & Innovation7

3% 3%

4%

65%Opportunity 2

EXPAND THE AUDIENCE

100%

WING 2018

Light-to-Medium QSR

Heavy QSR

Brand Awareness & Innovation8

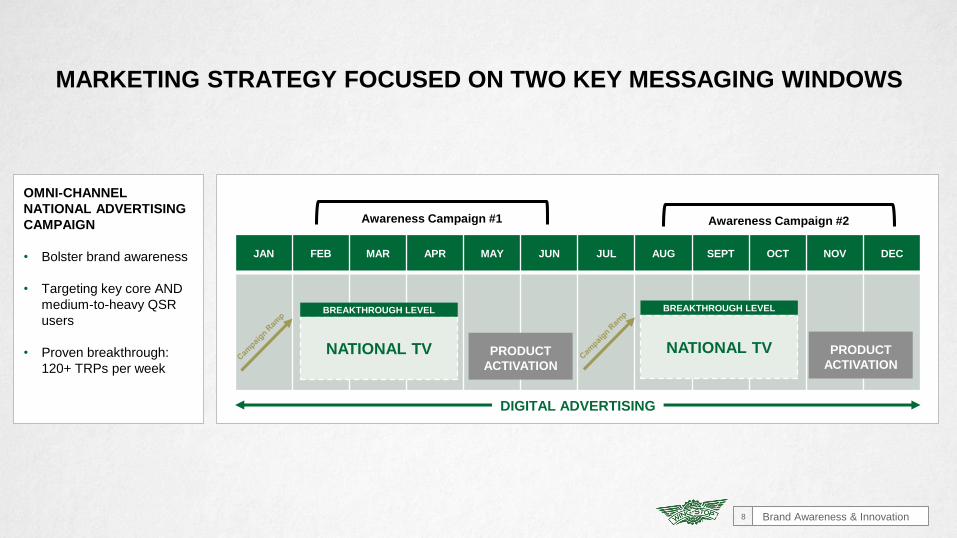

JAN FEB MAR APR MAY JUN JUL AUG SEPT OCT NOV DEC

Awareness Campaign #2

PRODUCT

ACTIVATION

Awareness Campaign #1

OMNI-CHANNEL

NATIONAL ADVERTISING

CAMPAIGN

• Bolster brand awareness

• Targeting key core AND

medium-to-heavy QSR

users

• Proven breakthrough:

120+ TRPs per week

NATIONAL TV PRODUCT

ACTIVATION

NATIONAL TV

DIGITAL ADVERTISING

BREAKTHROUGH LEVEL BREAKTHROUGH LEVEL

MARKETING STRATEGY FOCUSED ON TWO KEY MESSAGING WINDOWS

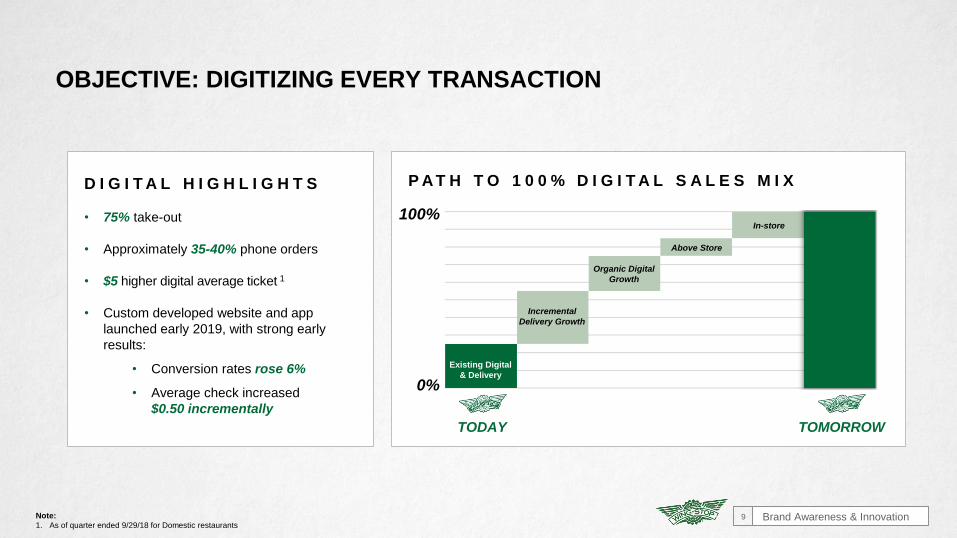

D I G I T A L H I G H L I G H T S

• 75% take-out

• Approximately 35-40% phone orders

• $5 higher digital average ticket 1

• Custom developed website and app

launched early 2019, with strong early

results:

• Conversion rates rose 6%

• Average check increased

$0.50 incrementally

Note:

1. As of quarter ended 9/29/18 for Domestic restaurants

OBJECTIVE: DIGITIZING EVERY TRANSACTION

Brand Awareness & Innovation9

Existing Digital

& Delivery

Incremental

Delivery Growth

Organic Digital

Growth

Above Store

In-store100%

0%

TODAY TOMORROW

P A T H T O 1 0 0 % D I G I T A L S A L E S M I X

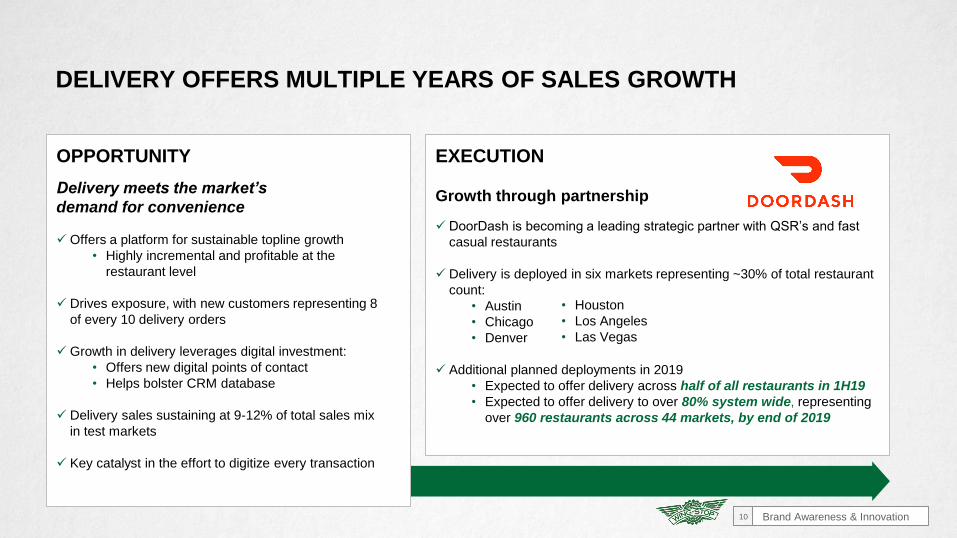

DELIVERY OFFERS MULTIPLE YEARS OF SALES GROWTH

EXECUTION

Growth through partnership

DoorDash is becoming a leading strategic partner with QSR’s and fast

casual restaurants

Delivery is deployed in six markets representing ~30% of total restaurant

count:

• Austin

• Chicago

• Denver

Additional planned deployments in 2019

• Expected to offer delivery across half of all restaurants in 1H19

• Expected to offer delivery to over 80% system wide, representing

over 960 restaurants across 44 markets, by end of 2019

OPPORTUNITY

Delivery meets the market’s

demand for convenience

Offers a platform for sustainable topline growth

• Highly incremental and profitable at the

restaurant level

Drives exposure, with new customers representing 8

of every 10 delivery orders

Growth in delivery leverages digital investment:

• Offers new digital points of contact

• Helps bolster CRM database

Delivery sales sustaining at 9-12% of total sales mix

in test markets

Key catalyst in the effort to digitize every transaction

Brand Awareness & Innovation10

• Houston

• Los Angeles

• Las Vegas

Best-in-Class Unit Economics11

MAINTAIN BEST-IN-CLASS UNIT ECONOMICS

INVEST IN PEOPLE AND INFRASTRUCTURE TO BUILD THE ORGANIZATION FOR THE NEXT LEVEL

National

Advertising

Digital

Delivery

Cost of Goods

Mitigation

Operating

Efficiencies

Advantages

of Scale

Fortress Key

U.S. Markets

Continue International

Expansion

Enter Non-Traditional

Restaurant Locations

SUSTAIN SSS VIA BRAND

AWARENESS AND INNOVATION

MAINTAIN BEST-IN-CLASS

UNIT ECONOMICS

EXPAND

GLOBAL FOOTPRINT

TOP 10

GLOBAL RESTAURANT BRAND

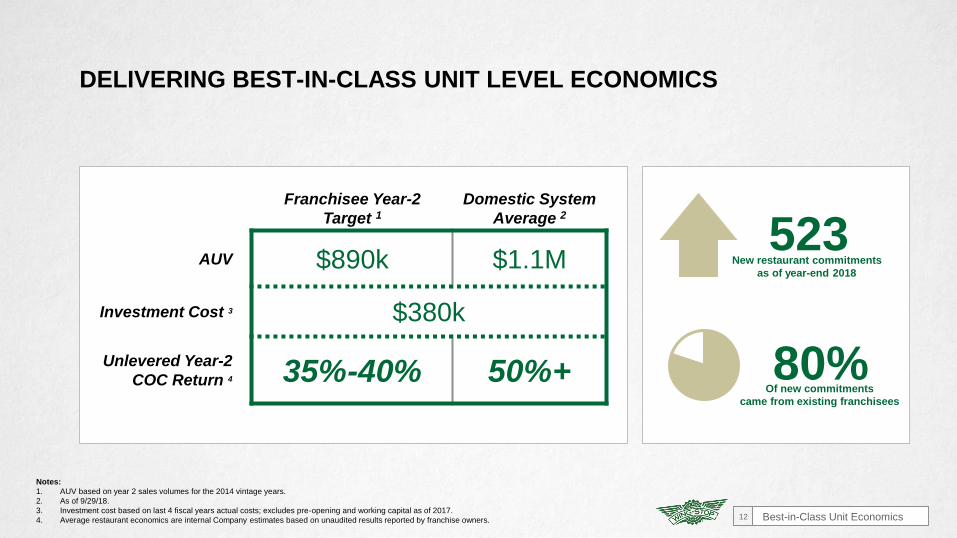

Franchisee Year-2

Target 1Domestic System

Average 2

AUV $890k $1.1M

Investment Cost 3 $380k

Unlevered Year-2

COC Return 4 35%-40% 50%+

Notes:

1. AUV based on year 2 sales volumes for the 2014 vintage years.

2. As of 9/29/18.

3. Investment cost based on last 4 fiscal years actual costs; excludes pre-opening and working capital as of 2017.

4. Average restaurant economics are internal Company estimates based on unaudited results reported by franchise owners.

DELIVERING BEST-IN-CLASS UNIT LEVEL ECONOMICS

Best-in-Class Unit Economics12

523New restaurant commitments

as of year-end 2018

80%Of new commitments

came from existing franchisees

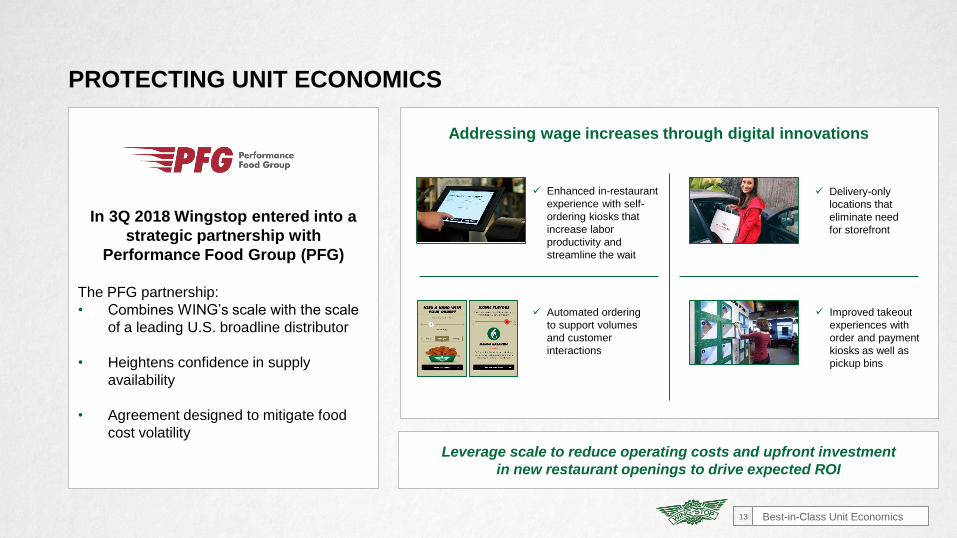

PROTECTING UNIT ECONOMICS

Best-in-Class Unit Economics13

In 3Q 2018 Wingstop entered into a

strategic partnership with

Performance Food Group (PFG)

The PFG partnership:

• Combines WING’s scale with the scale

of a leading U.S. broadline distributor

• Heightens confidence in supply

availability

• Agreement designed to mitigate food

cost volatility

Addressing wage increases through digital innovations

Leverage scale to reduce operating costs and upfront investment

in new restaurant openings to drive expected ROI

Enhanced in-restaurant

experience with self-

ordering kiosks that

increase labor

productivity and

streamline the wait

Improved takeout

experiences with

order and payment

kiosks as well as

pickup bins

Automated ordering

to support volumes

and customer

interactions

Delivery-only

locations that

eliminate need

for storefront

Global Expansion14

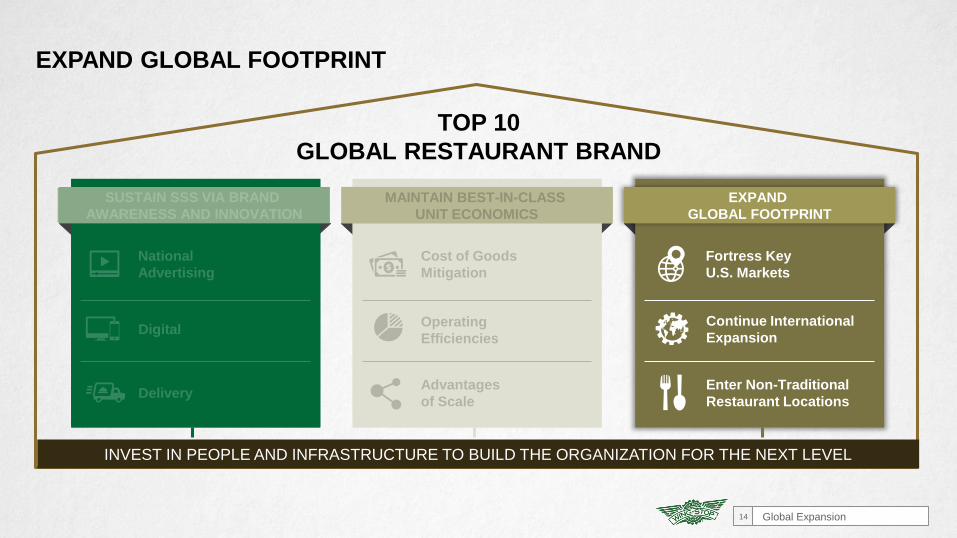

EXPAND GLOBAL FOOTPRINT

INVEST IN PEOPLE AND INFRASTRUCTURE TO BUILD THE ORGANIZATION FOR THE NEXT LEVEL

Cost of Goods

Mitigation

Operating

Efficiencies

Advantages

of Scale

Fortress Key

U.S. Markets

Continue International

Expansion

Enter Non-Traditional

Restaurant Locations

MAINTAIN BEST-IN-CLASS

UNIT ECONOMICS

EXPAND

GLOBAL FOOTPRINT

National

Advertising

Digital

Delivery

TOP 10

GLOBAL RESTAURANT BRAND

SUSTAIN SSS VIA BRAND

AWARENESS AND INNOVATION

DOMESTIC

3x

NON-TRADITIONAL

90%Domestic

50/50

Long-term

Goal of

Split

INTERNATIONAL

1,252 units ~6,000 units

Currently 1

1,124 units128 units

3,000 units3,000 units

IN CORE AND

EMERGING US MARKETS

Global Expansion15

THREE-PRONGED STRATEGY TO REACH 6,000 GLOBAL LOCATIONS

Note:

1. As of 12/29/18.

FORTRESS

Stadiums & Sport

Complexes

Airports Colleges &

Universities

Food Courts Travel Centers Casinos

25 MARKETS x 150 DEEP

Domestic International

Global Expansion16

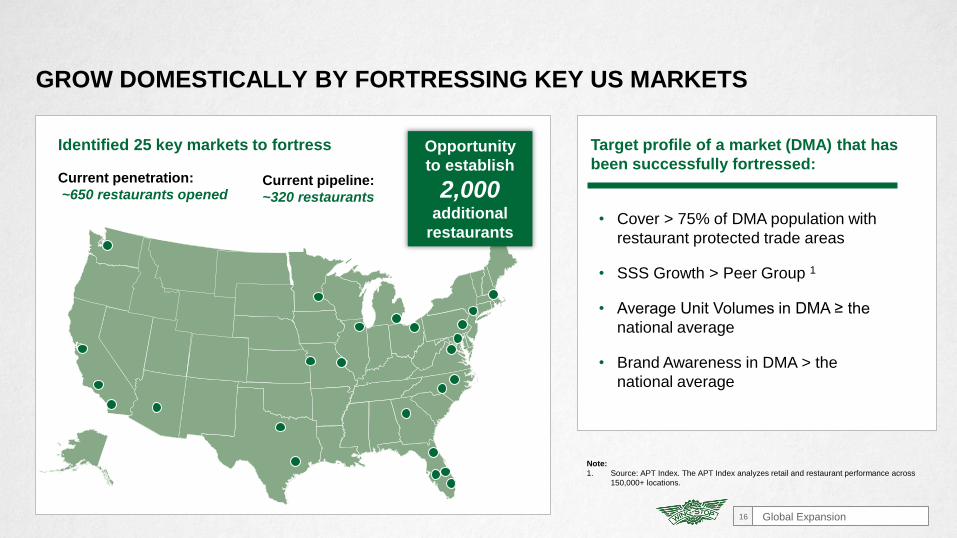

GROW DOMESTICALLY BY FORTRESSING KEY US MARKETS

• Cover > 75% of DMA population with

restaurant protected trade areas

• SSS Growth > Peer Group 1

• Average Unit Volumes in DMA ≥ the

national average

• Brand Awareness in DMA > the

national average

Target profile of a market (DMA) that has

been successfully fortressed:

Identified 25 key markets to fortress Opportunity

to establish

2,000additional

restaurants

Current pipeline:

~320 restaurants

Current penetration:

~650 restaurants opened

Note:

1. Source: APT Index. The APT Index analyzes retail and restaurant performance across

150,000+ locations.

Global Expansion17

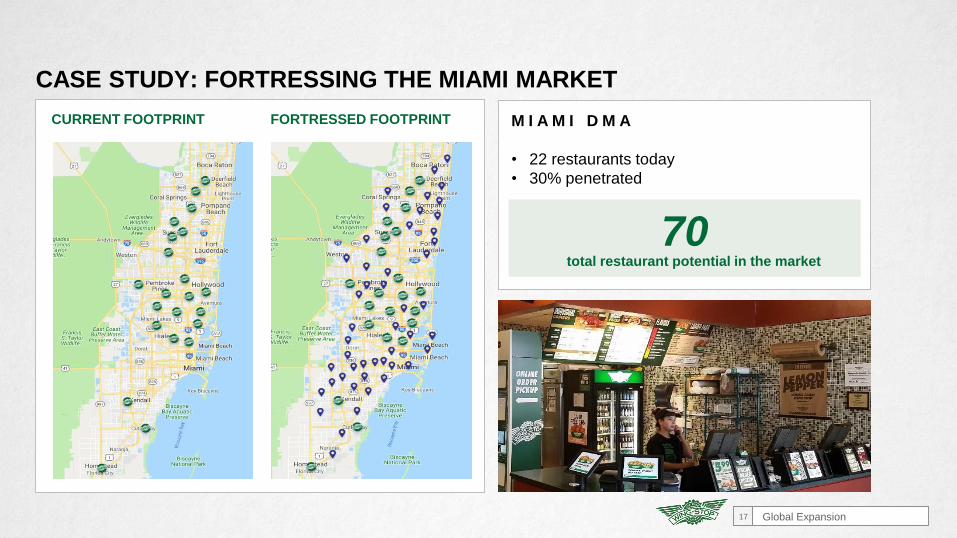

CASE STUDY: FORTRESSING THE MIAMI MARKET

M I A M I D M A

• 22 restaurants today

• 30% penetrated

CURRENT FOOTPRINT FORTRESSED FOOTPRINT

70total restaurant potential in the market

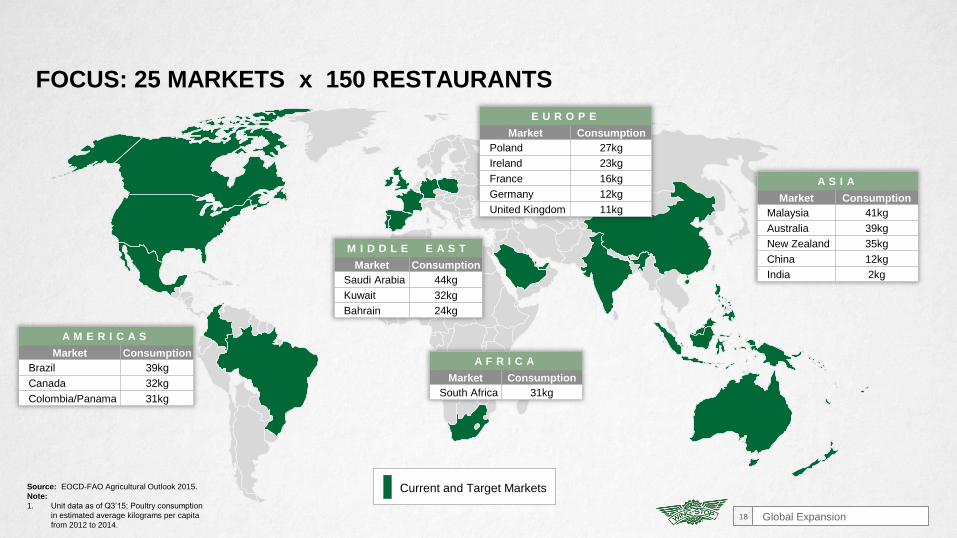

A M E R I C A S

Market Consumption

Brazil 39kg

Canada 32kg

Colombia/Panama 31kg

Source: EOCD-FAO Agricultural Outlook 2015.

Note:

1. Unit data as of Q3’15; Poultry consumption

in estimated average kilograms per capita

from 2012 to 2014.

A F R I C A

Market Consumption

South Africa 31kg

A S I A

Market Consumption

Malaysia 41kg

Australia 39kg

New Zealand 35kg

China 12kg

India 2kg

E U R O P E

Market Consumption

Poland 27kg

Ireland 23kg

France 16kg

Germany 12kg

United Kingdom 11kg

M I D D L E E A S T

Market Consumption

Saudi Arabia 44kg

Kuwait 32kg

Bahrain 24kg

Global Expansion18

FOCUS: 25 MARKETS x 150 RESTAURANTS

Current and Target Markets

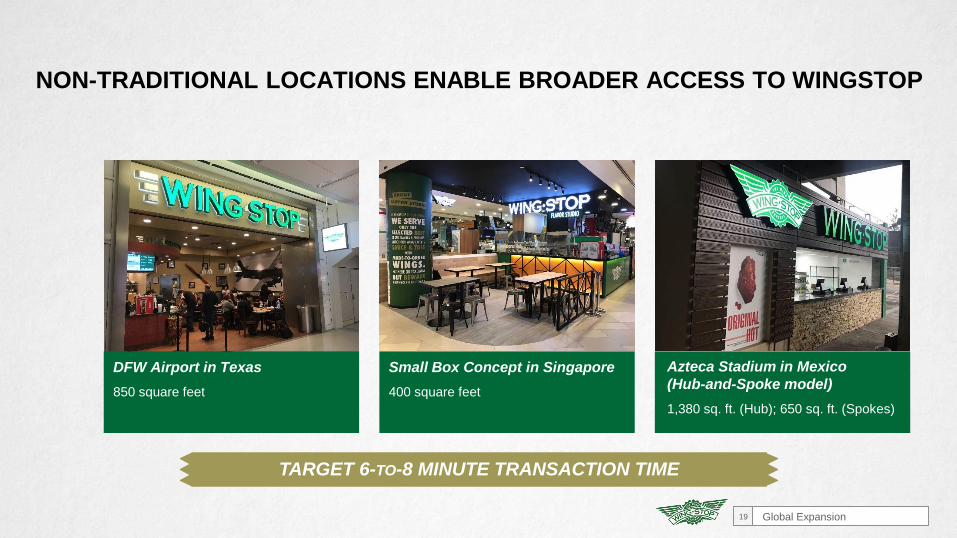

NON-TRADITIONAL LOCATIONS ENABLE BROADER ACCESS TO WINGSTOP

Global Expansion19

DFW Airport in Texas

850 square feet

Small Box Concept in Singapore

400 square feet

Azteca Stadium in Mexico

(Hub-and-Spoke model)

1,380 sq. ft. (Hub); 650 sq. ft. (Spokes)

TARGET 6-TO-8 MINUTE TRANSACTION TIME

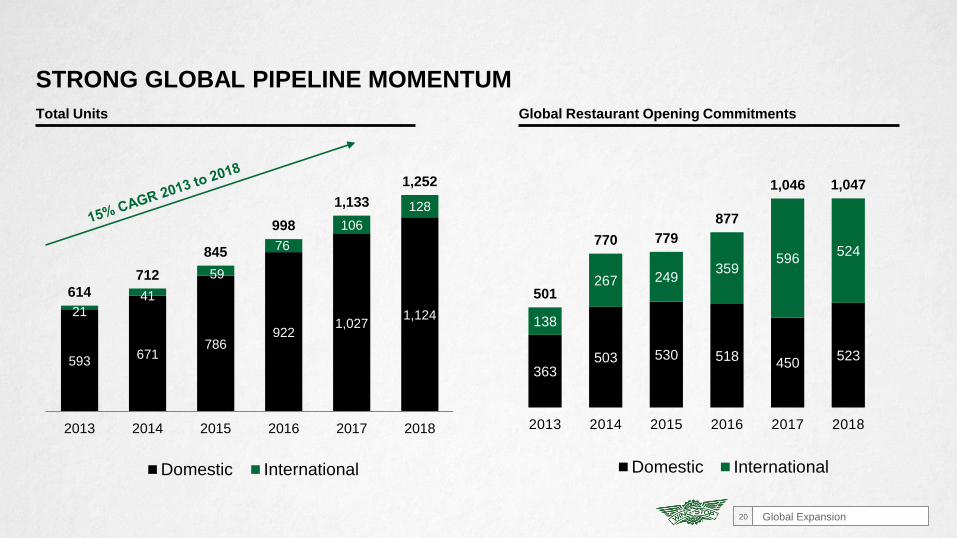

363503 530 518

450523

138

267 249359

596524

501

770 779

877

1,046 1,047

2013 2014 2015 2016 2017 2018

Domestic International

Total Units Global Restaurant Opening Commitments

STRONG GLOBAL PIPELINE MOMENTUM

Global Expansion20

593 671

786 922

1,027 1,124 21

41

59

76

106

128

614

712

845

998

1,133

1,252

2013 2014 2015 2016 2017 2018

Domestic International

LONG-TERM GROWTH MODEL

Wingstop Investor Presentation21

Long-term Growth Strategy22

PATH TO TOP 10

GLOBAL RESTAURANT BRAND

MAXIMIZE FREE CASH FLOW CONVERSION AND BEST-IN-CLASS

SHAREHOLDER RETURNS

ACHIEVING LONG-TERM GROWTH TARGETS

10%+ Annual Unit Growth

EXPAND

GLOBAL FOOTPRINT

MAINTAIN BEST-IN-CLASS

UNIT ECONOMICS

Low Single Digit

Same Store Sales Growth

SUSTAIN SSS VIA BRAND

AWARENESS AND INNOVATION

Appendix23

APPENDIX

Appendix24

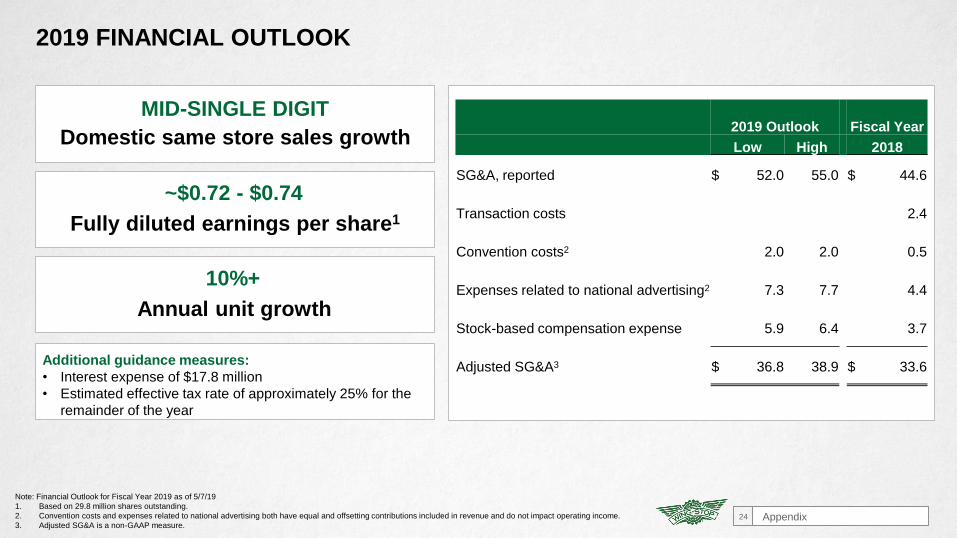

2019 FINANCIAL OUTLOOK

MID-SINGLE DIGIT

Domestic same store sales growth2019 Outlook Fiscal Year

Low High 2018

SG&A, reported $ 52.0 55.0 $ 44.6

Transaction costs 2.4

Convention costs2 2.0 2.0 0.5

Expenses related to national advertising2 7.3 7.7 4.4

Stock-based compensation expense 5.9 6.4 3.7

Adjusted SG&A3 $ 36.8 38.9 $ 33.6

Note: Financial Outlook for Fiscal Year 2019 as of 5/7/19

1. Based on 29.8 million shares outstanding.

2. Convention costs and expenses related to national advertising both have equal and offsetting contributions included in revenue and do not impact operating income.

3. Adjusted SG&A is a non-GAAP measure.

~$0.72 - $0.74

Fully diluted earnings per share1

Additional guidance measures:

• Interest expense of $17.8 million

• Estimated effective tax rate of approximately 25% for the

remainder of the year

10%+

Annual unit growth

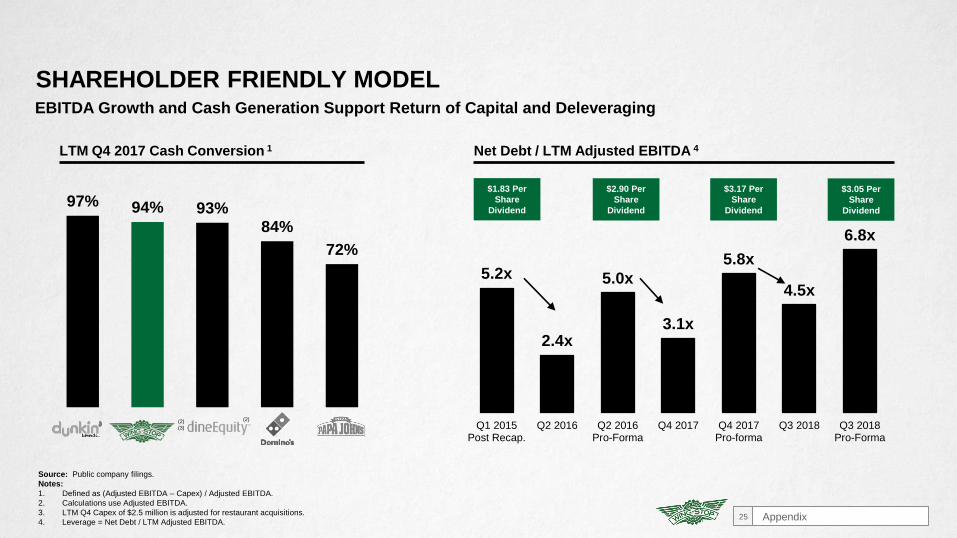

97% 94% 93%84%

72%

5.2x

2.4x

5.0x

3.1x

5.8x

4.5x

6.8x

Q1 2015Post Recap.

Q2 2016 Q2 2016Pro-Forma

Q4 2017 Q4 2017Pro-forma

Q3 2018 Q3 2018Pro-Forma

EBITDA Growth and Cash Generation Support Return of Capital and Deleveraging

(2)(2)

(3)

LTM Q4 2017 Cash Conversion 1

$2.90 Per

Share

Dividend

Net Debt / LTM Adjusted EBITDA 4

Source: Public company filings.

Notes:

1. Defined as (Adjusted EBITDA – Capex) / Adjusted EBITDA.

2. Calculations use Adjusted EBITDA.

3. LTM Q4 Capex of $2.5 million is adjusted for restaurant acquisitions.

4. Leverage = Net Debt / LTM Adjusted EBITDA.

$1.83 Per

Share

Dividend

$3.17 Per

Share

Dividend

SHAREHOLDER FRIENDLY MODEL

Appendix25

$3.05 Per

Share

Dividend

(1)

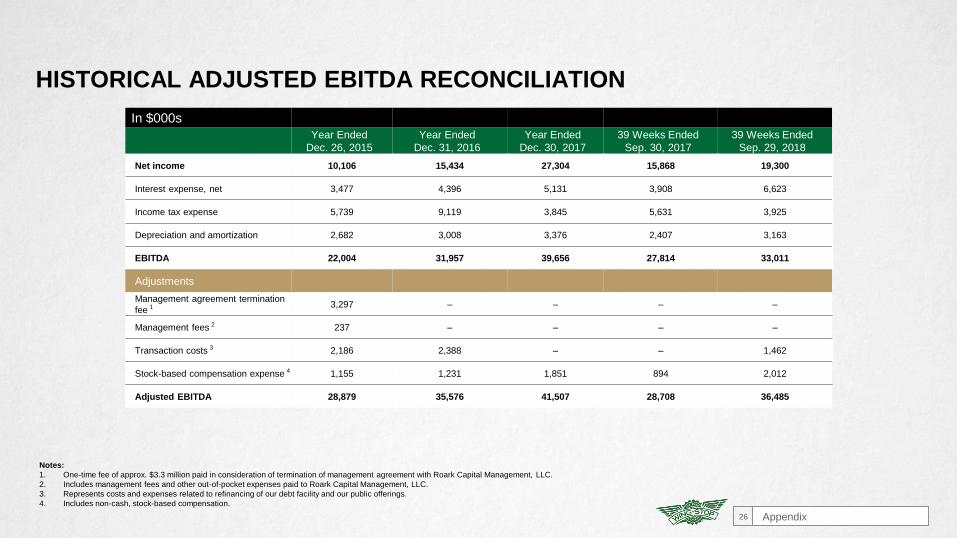

In $000s

Year Ended

Dec. 26, 2015

Year Ended

Dec. 31, 2016

Year Ended

Dec. 30, 2017

39 Weeks Ended

Sep. 30, 2017

39 Weeks Ended

Sep. 29, 2018

Net income 10,106 15,434 27,304 15,868 19,300

Interest expense, net 3,477 4,396 5,131 3,908 6,623

Income tax expense 5,739 9,119 3,845 5,631 3,925

Depreciation and amortization 2,682 3,008 3,376 2,407 3,163

EBITDA 22,004 31,957 39,656 27,814 33,011

Adjustments

Management agreement termination

fee 1 3,297 – – – –

Management fees 2 237 – – – –

Transaction costs 3 2,186 2,388 – – 1,462

Stock-based compensation expense 4 1,155 1,231 1,851 894 2,012

Adjusted EBITDA 28,879 35,576 41,507 28,708 36,485

Notes:

1. One-time fee of approx. $3.3 million paid in consideration of termination of management agreement with Roark Capital Management, LLC.

2. Includes management fees and other out-of-pocket expenses paid to Roark Capital Management, LLC.

3. Represents costs and expenses related to refinancing of our debt facility and our public offerings.

4. Includes non-cash, stock-based compensation.

HISTORICAL ADJUSTED EBITDA RECONCILIATION

Appendix26

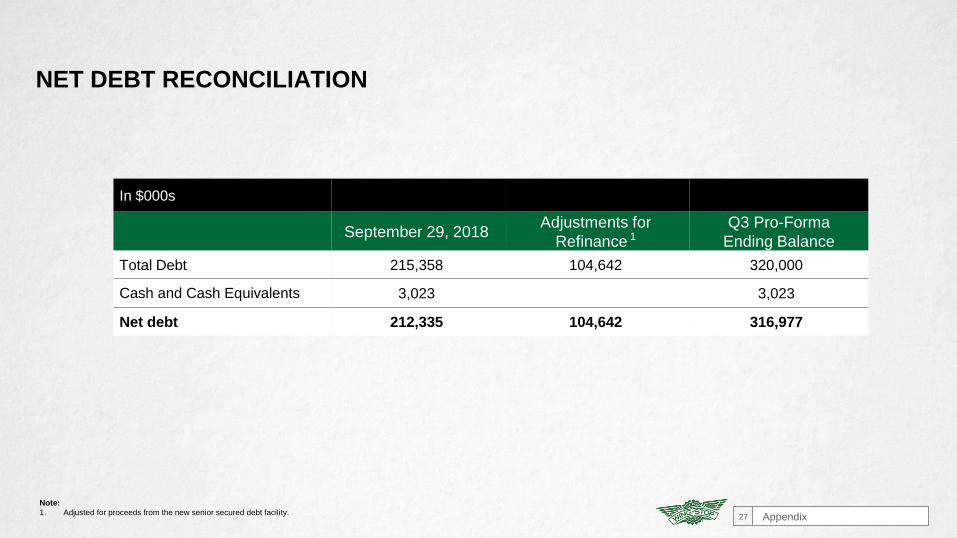

NET DEBT RECONCILIATION

In $000s

September 29, 2018Adjustments for

Refinance 1Q3 Pro-Forma

Ending Balance

Total Debt 215,358 104,642 320,000

Cash and Cash Equivalents 3,023 3,023

Net debt 212,335 104,642 316,977

Note:

1. Adjusted for proceeds from the new senior secured debt facility.Appendix27

Recommended