Embed Size (px)

Citation preview

Why Do Firms Go Public? Why Do Firms Go Public? Welch and Ritter (2002)

•Desire to raise capital for a growing firm.

•Create liquidity for founders and other shareholders.

Questions•Why are IPOs the best way to raise capital?•Why are these reasons stronger in some times than others?

Welch and Ritter (2002): Table 1

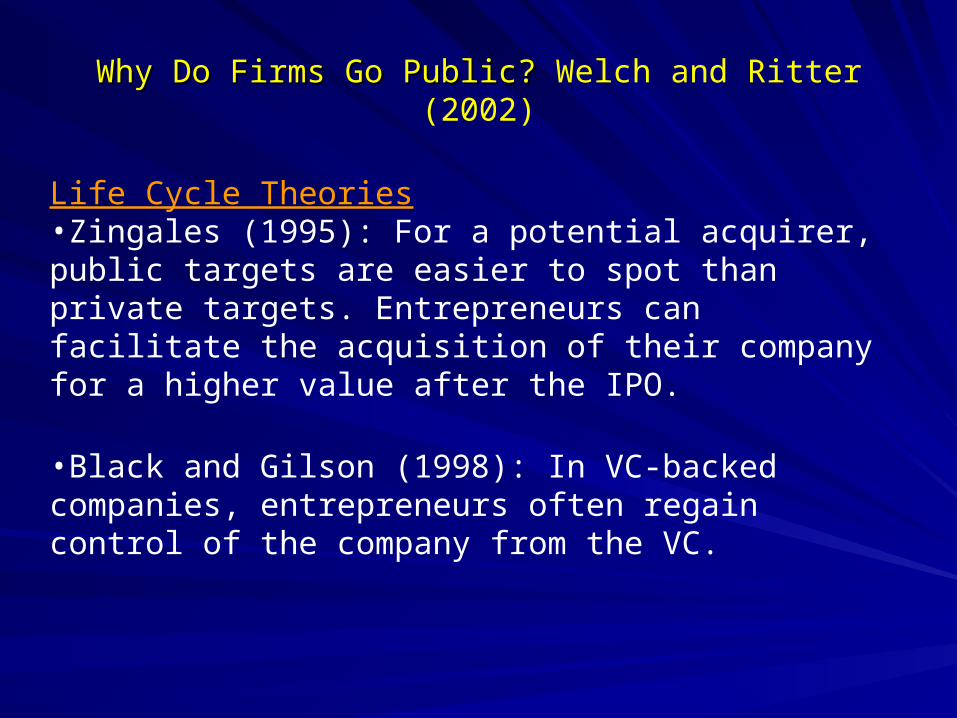

Why Do Firms Go Public? Why Do Firms Go Public? Welch and Ritter (2002)

Life Cycle Theories•Zingales (1995): For a potential acquirer, public targets are easier to spot than private targets. Entrepreneurs can facilitate the acquisition of their company for a higher value after the IPO.

•Black and Gilson (1998): In VC-backed companies, entrepreneurs often regain control of the company from the VC.

Why Do Firms Go Public? Why Do Firms Go Public? Welch and Ritter (2002)

Life Cycle Theories•Chemmanur and Fulghieri (1999):

•To allow for greater dispersion of ownership. Pre-IPO angel investors and VCs hold undiversified portfolios (hence, bear systematic and unsystematic risk) and, therefore, are not willing to pay as high a price as diversified public-market investors.•Fixed costs of going public.•Early in its lifecycle a firm will be private. As it grows and faces profitable investment opportunities, the costs of going public are worth incurring.•Public trading can itself add value to the firm as it inspires confidence from investors, customers, suppliers, and employees.•IPO capital allows for first-mover advantages.(1998-99 IPOs)

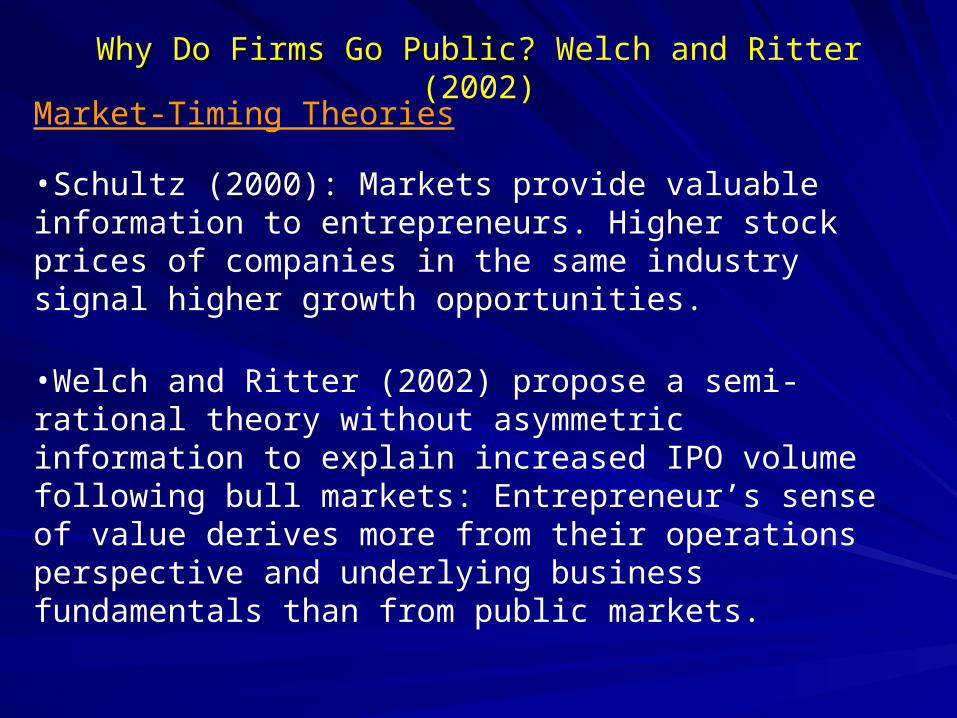

Why Do Firms Go Public? Why Do Firms Go Public? Welch and Ritter (2002)

Market-Timing Theories

•Schultz (2000): Markets provide valuable information to entrepreneurs. Higher stock prices of companies in the same industry signal higher growth opportunities.

•Welch and Ritter (2002) propose a semi-rational theory without asymmetric information to explain increased IPO volume following bull markets: Entrepreneur’s sense of value derives more from their operations perspective and underlying business fundamentals than from public markets.

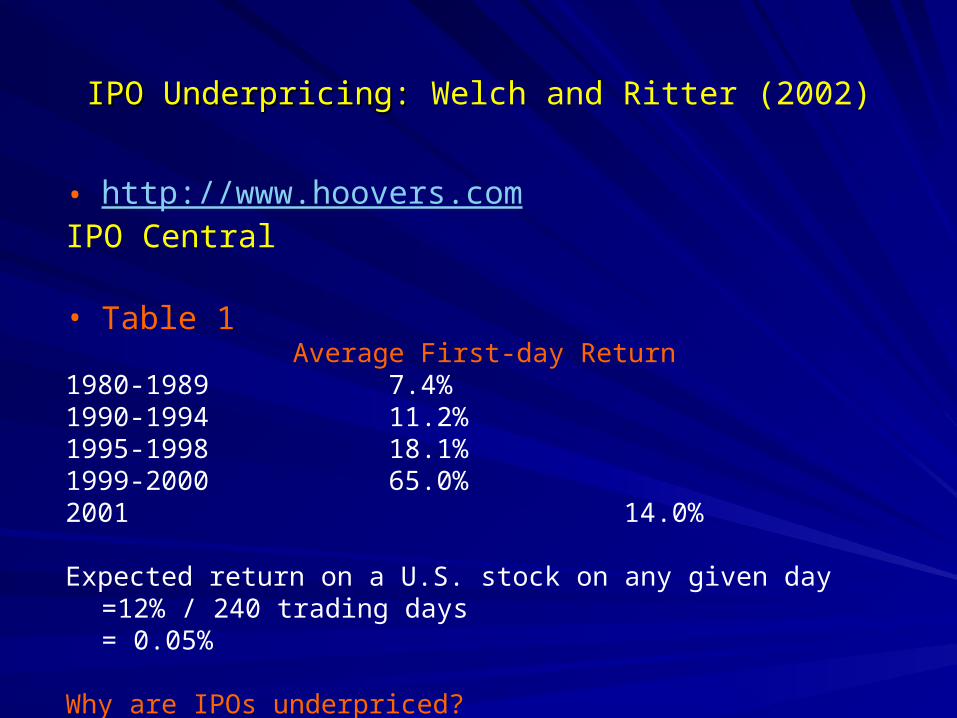

IPO Underpricing: IPO Underpricing: Welch and Ritter (2002)

• http://www.hoovers.comIPO Central

• Table 1Average First-day Return

1980-1989 7.4%1990-1994 11.2%1995-1998 18.1%1999-2000 65.0%2001 14.0%

Expected return on a U.S. stock on any given day =12% / 240 trading days = 0.05%

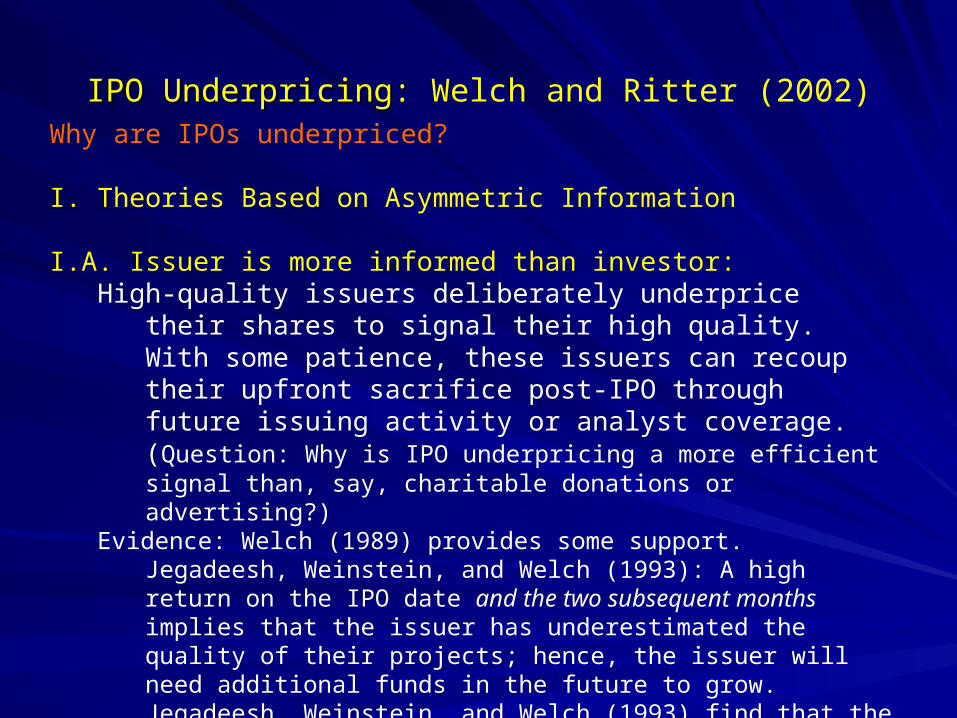

Why are IPOs underpriced?

IPO Underpricing: IPO Underpricing: Welch and Ritter (2002)Why are IPOs underpriced?

I. Theories Based on Asymmetric Information

I.A. Issuer is more informed than investor:High-quality issuers deliberately underprice their shares to signal their

high quality. With some patience, these issuers can recoup their upfront sacrifice post-IPO through future issuing activity or analyst coverage. (Question: Why is IPO underpricing a more efficient signal than, say, charitable donations or advertising?)

SharePrice

Months

High Quality Issuer

Low Quality Issuer

Offer Day

IPO Underpricing: IPO Underpricing: Welch and Ritter (2002)Why are IPOs underpriced?

I. Theories Based on Asymmetric Information

I.A. Issuer is more informed than investor:High-quality issuers deliberately underprice their shares to signal

their high quality. With some patience, these issuers can recoup their upfront sacrifice post-IPO through future issuing activity or analyst coverage. (Question: Why is IPO underpricing a more efficient signal than, say, charitable donations or advertising?)

Evidence: Welch (1989) provides some support. Jegadeesh, Weinstein, and Welch (1993): A high return on the IPO date and the two subsequent months implies that the issuer has underestimated the quality of their projects; hence, the issuer will need additional funds in the future to grow. Jegadeesh, Weinstein, and Welch (1993) find that the return in the two subsequent months is more strongly (compared to IPO date return) related to the probability and timing of subsequent seasoned equity offerings.

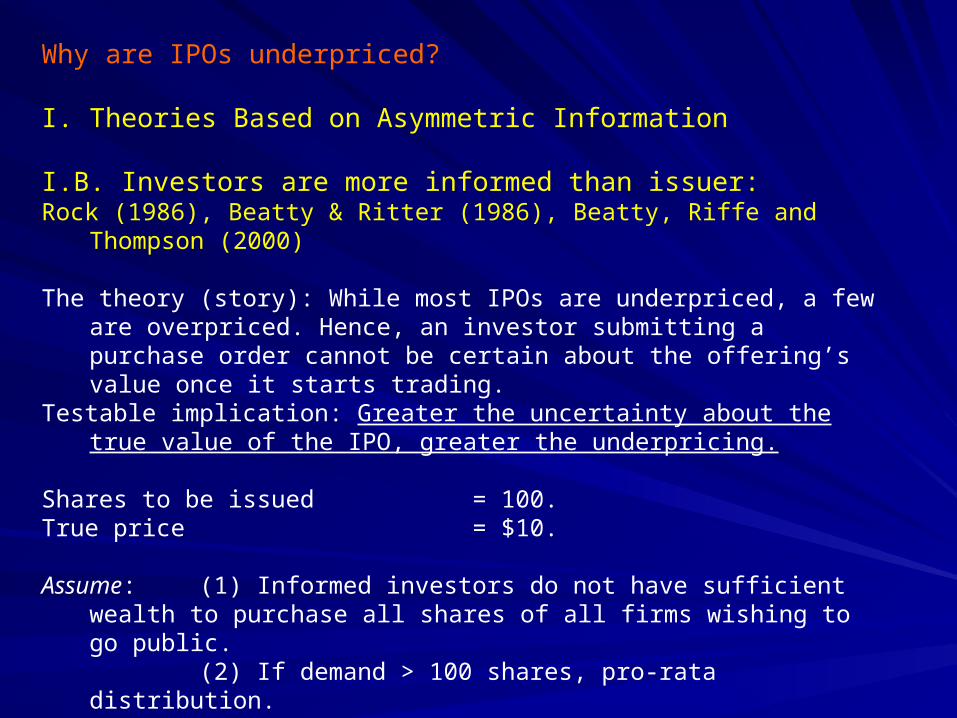

Why are IPOs underpriced?

I. Theories Based on Asymmetric Information

I.B. Investors are more informed than issuer:Rock (1986), Beatty & Ritter (1986), Beatty, Riffe and Thompson (2000) The theory (story): While most IPOs are underpriced, a few are overpriced.

Hence, an investor submitting a purchase order cannot be certain about the offering’s value once it starts trading.

Testable implication: Greater the uncertainty about the true value of the IPO, greater the underpricing.

Shares to be issued = 100.True price = $10. Assume: (1) Informed investors do not have sufficient wealth to purchase

all shares of all firms wishing to go public. (2) If demand > 100 shares, pro-rata distribution.

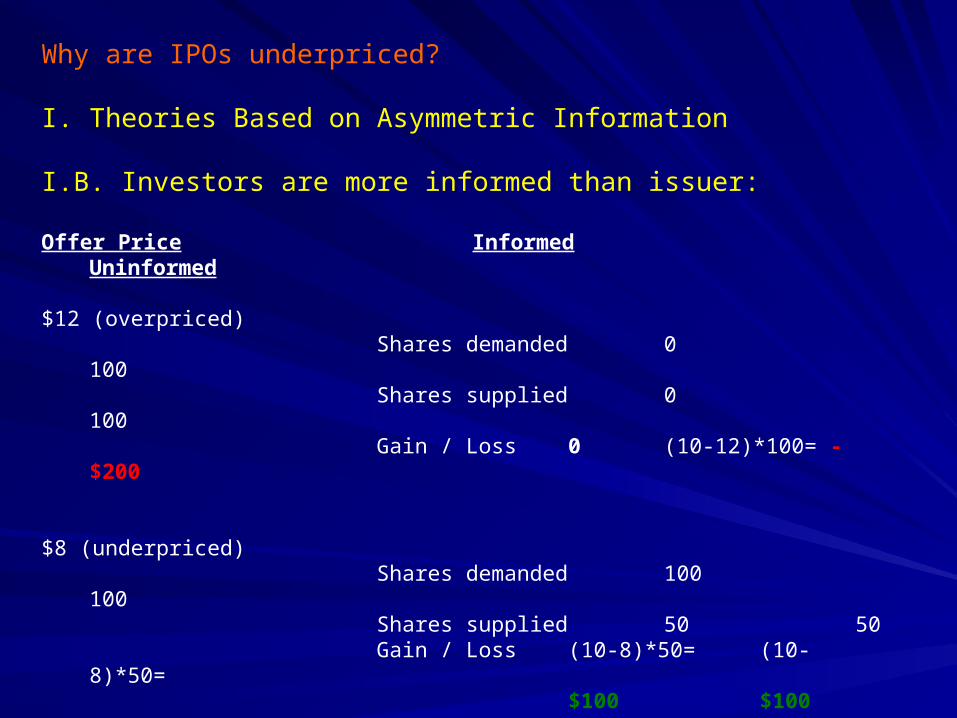

Why are IPOs underpriced?

I. Theories Based on Asymmetric Information

I.B. Investors are more informed than issuer:

Offer Price Informed Uninformed $12 (overpriced)

Shares demanded 0 100Shares supplied 0 100Gain / Loss 0 (10-12)*100= -$200

$8 (underpriced)Shares demanded 100 100Shares supplied 50 50Gain / Loss (10-8)*50= (10-8)*50=

$100 $100

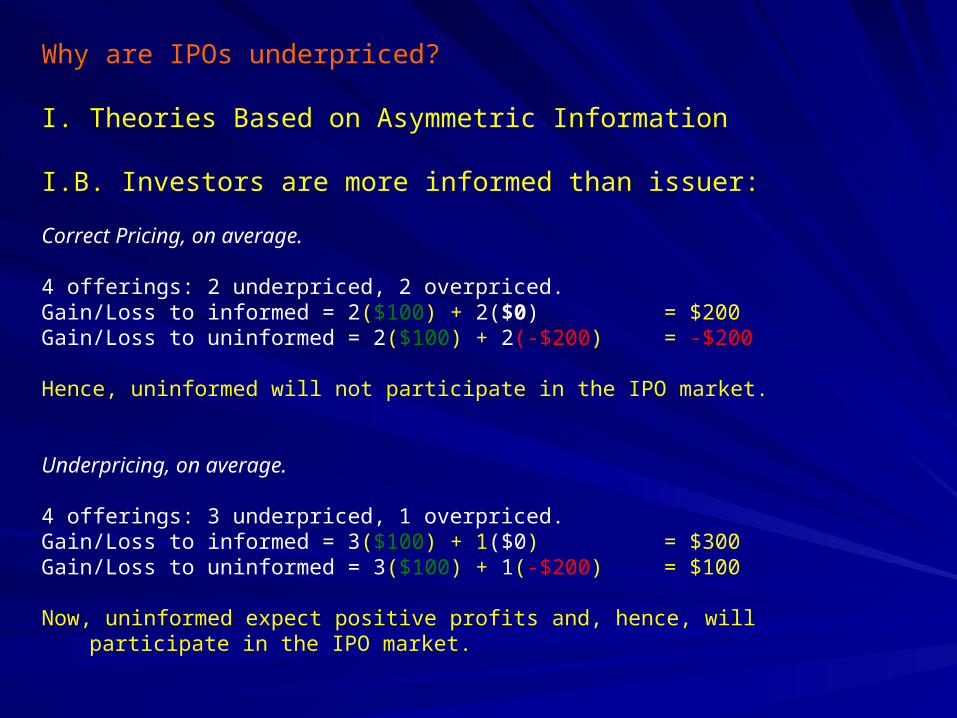

Why are IPOs underpriced?

I. Theories Based on Asymmetric Information

I.B. Investors are more informed than issuer:

Correct Pricing, on average. 4 offerings: 2 underpriced, 2 overpriced.Gain/Loss to informed = 2($100) + 2($0) = $200Gain/Loss to uninformed = 2($100) + 2(-$200) = -$200 Hence, uninformed will not participate in the IPO market. Underpricing, on average. 4 offerings: 3 underpriced, 1 overpriced.Gain/Loss to informed = 3($100) + 1($0) = $300Gain/Loss to uninformed = 3($100) + 1(-$200) = $100

Now, uninformed expect positive profits and, hence, will participate in the IPO market.

Why are IPOs underpriced?

I. Theories Based on Asymmetric Information

I.B. Investors are more informed than issuer:

Fly in the ointment: If informed are making abnormal profits then over time they should have sufficient wealth to purchase all shares of all firms wishing to go public.

Perhaps a different set of investors are the informed investors for different IPOs depending on the industry of the IPO.

Empirical evidence is consistent with the above model: Beatty, Riffe

and Thompson (2000) find that IPOs for which there is greater uncertainty about their value are underpriced more. Additionally, underwriters that underprice too much or too little lose their market share.

Why are IPOs underpriced?

I. Theories Based on Asymmetric Information

I.B. Investors are more informed than issuer:Book-Building Theory/StoryIn the preliminary IPO prospectus underwriters note the range for the

future offer price. Underwriters then canvass potential investors regarding their demand for the IPO shares. Underwriters seem reluctant to fully adjust their pricing upward to keep IPO underpricing constant. When underwriters revise the share price upward from the original range, underpricing tends to be higher. Perhaps this extra underpricing is necessary to induce investors to reveal their high demand for the IPO shares.

Table 3:Mean first-day return when offer price is below range: 3.3% Mean first-day return when offer price is within range: 12.0%Mean first-day return when offer price is above range: 52.7%

Why are IPOs underpriced?

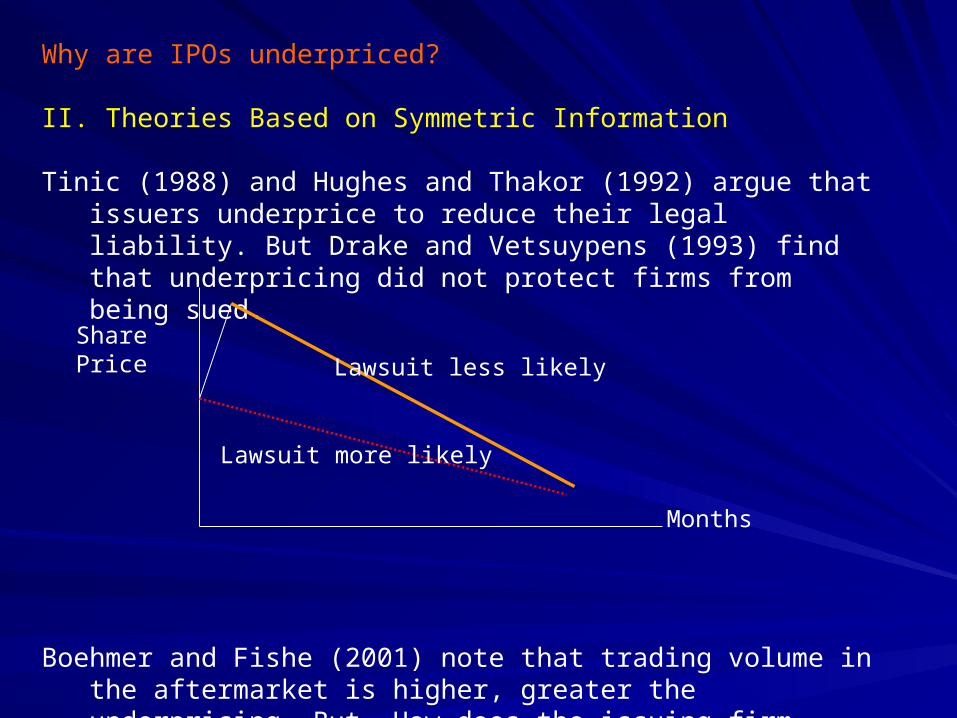

II. Theories Based on Symmetric Information

Tinic (1988) and Hughes and Thakor (1992) argue that issuers underprice to reduce their legal liability. But Drake and Vetsuypens (1993) find that underpricing did not protect firms from being sued.

Boehmer and Fishe (2001) note that trading volume in the aftermarket is higher, greater the underpricing. But… How does the issuing firm benefit from underpricing unless the increased liquidity is persistent?

SharePrice

Months

Lawsuit less likely

Lawsuit more likely

Why are IPOs underpriced?

III. Theories Focusing on Allocation of Shares

If IPOs are underpriced on average, then the opportunity to purchase them at the offering price would be quite attractive.

Table 1: 1999-2000: 65% return on the first day!

Underwriters have the opportunity to allocate such underpriced shares to their “preferred customers.”

How does one become a “preferred customer?”Provide underwriter with economic benefits (other business).Provide underwriter with political benefits.

Selling Out to Public Firms vs. IPOsSelling Out to Public Firms vs. IPOsPoulsen-Stegemoller (2006)Poulsen-Stegemoller (2006)

Determinants of the Choice between Selling Out to Public Determinants of the Choice between Selling Out to Public Firms vs. IPOsFirms vs. IPOs

A. Growth and the Need for CapitalA. Growth and the Need for Capital

– IPO: Private firm raises public capital and allocates it to projects IPO: Private firm raises public capital and allocates it to projects the managers deem most worthy.the managers deem most worthy.

– Sellout: Capital allocated by managers of acquiring company. Sellout: Capital allocated by managers of acquiring company. Sellout firm has to compete with other divisions of the acquiring Sellout firm has to compete with other divisions of the acquiring company for new capital.company for new capital.

Companies with greater growth potential more likely to go Companies with greater growth potential more likely to go public through an IPO.public through an IPO.

Selling Out to Public Firms vs. IPOsSelling Out to Public Firms vs. IPOsPoulsen-Stegemoller (2006)Poulsen-Stegemoller (2006)

Determinants of the Choice between Selling Out to Public Determinants of the Choice between Selling Out to Public Firms vs. IPOsFirms vs. IPOs

A. Growth and the Need for CapitalA. Growth and the Need for Capital

Companies with greater growth potential more likely to go Companies with greater growth potential more likely to go public through an IPO.public through an IPO.

Proxies for growth: Proxies for growth: – Increase in assets, capital expenditures, revenues over the past year.Increase in assets, capital expenditures, revenues over the past year.– Capital expenditure / Assets, Capital expenditure / Assets, – R&D / Assets,R&D / Assets,– Market value of assets / Book value of assets. Market value of assets / Book value of assets.

(Market = Book + Growth Opportunities.(Market = Book + Growth Opportunities.

Market / Book = 1+ Growth Opportunities.)Market / Book = 1+ Growth Opportunities.)

Selling Out to Public Firms vs. IPOsSelling Out to Public Firms vs. IPOsPoulsen-Stegemoller (2006)Poulsen-Stegemoller (2006)

Determinants of the Choice between Selling Out to Public Determinants of the Choice between Selling Out to Public Firms vs. IPOsFirms vs. IPOs

A. Growth and the Need for CapitalA. Growth and the Need for Capital

Companies with greater growth potential more likely to go Companies with greater growth potential more likely to go public through an IPO.public through an IPO.

Myers (1984) Underinvestment Problem: Myers (1984) Underinvestment Problem: With risky debt With risky debt outstanding, shareholders will sometimes pass up positive NPV projects.outstanding, shareholders will sometimes pass up positive NPV projects.

Companies that have Companies that have – lots of growth opportunities,lots of growth opportunities,– have some debt, andhave some debt, and– cash constrainedcash constrained

are more likely to do an IPO to gain access to equity capital.are more likely to do an IPO to gain access to equity capital.

Selling Out to Public Firms vs. IPOsSelling Out to Public Firms vs. IPOsPoulsen-Stegemoller (2006)Poulsen-Stegemoller (2006)

Determinants of the Choice between Selling Out to Public Determinants of the Choice between Selling Out to Public Firms vs. IPOsFirms vs. IPOs

B. Asymmetric InformationB. Asymmetric Information

IPOs offered by investment bankers to mostly mutual/pension funds.IPOs offered by investment bankers to mostly mutual/pension funds.

Investment bankers and mutual/pension fund managers may not be Investment bankers and mutual/pension fund managers may not be able to value the assets of a private company as well asable to value the assets of a private company as well as

Another company in the same industry.Another company in the same industry.

Additionally, firm-specific information may retain its value only when it Additionally, firm-specific information may retain its value only when it is not accessible to outside competitors.is not accessible to outside competitors.

Selling Out to Public Firms vs. IPOsSelling Out to Public Firms vs. IPOsPoulsen-Stegemoller (2006)Poulsen-Stegemoller (2006)

Determinants of the Choice between Selling Out to Public Firms Determinants of the Choice between Selling Out to Public Firms vs. IPOsvs. IPOs

B. Asymmetric InformationB. Asymmetric Information

Investment bankers and mutual/pension fund managers may not be able to Investment bankers and mutual/pension fund managers may not be able to value the assets of a private company as well asvalue the assets of a private company as well as

Another company in the same industry.Another company in the same industry.

What type of companies may be more difficult to value?What type of companies may be more difficult to value?– More intangible assets.More intangible assets.– Less developed.Less developed.– Smaller.Smaller.– Less profitable.Less profitable.– No VC backing.No VC backing.