Embed Size (px)

Citation preview

THREE ESSAYS ON COMPETITION AND PRODUCTIVITY IN THE U.S.

AIRLINE INDUSTRY

A dissertation presented

by

Tuvshintulga Bold

to

The Department of Economics

Submitted in partial fulfillment of the requirements for the degree of

Doctor of Philosophy

in the field of

Economics

Northeastern University

Boston, MA

November, 2013

THREE ESSAYS ON COMPETITION AND PRODUCTIVITY IN THE U.S.

AIRLINE INDUSTRY

by

Tuvshintulga Bold

ABSTRACT OF DISSERTATION

Submitted in partial fulfillment of the requirements

for the degree of Doctor of Philosophy in Economics

in the Graduate School of Social Sciences and Humanities of

Northeastern University

November, 2013

2

Abstracts

Chapter 1: The Effect of Wright Amendment on Consumer Welfare

This paper analyses effect of the Wright Amendment on airline ticket price and

ultimately consumer welfare for passengers flying to and from the Dallas metropolitan

area. The Wright Amendment is a law that was implemented in 1979 to restrict

passenger air travel to and from Dallas Love Field airport in order to encourage growth

at then the newly constructed Dallas Fort-Worth airport. Today, Dallas Fort-Worth has

become one of the busiest airports in the U.S., but the Wright Amendment continues to

suppress competition by prohibiting long distance flights to and from Dallas Love Field

airport. While supporters and opponents of the Wright Amendment have been debating

for some time, to date no economic study has measured the effect of the law on air fares

and consumer welfare. I use data from the U.S. Department of Transportation’s Ticket

and Origin and Destination Survey from 1996 to 2011 to produce estimations of the

effect of the Wright Amendment. Series of three relaxations to the amendment created

an opportunity to use the difference-in-difference econometric method to precisely

measure the fare distortion brought by the law. Of the three relaxations, the third and

the last change introduced a major alteration in the law by allowing airlines to fly

anywhere in the country from Dallas Love Field airport. As a result, fares decreased on

average by 13.88% while certain destinations experienced as much as 36% of fare

decrease during the five years following the implementation of the change.

Consequently, passengers of the Dallas area saved $1.31 billion from 2007 to 2011 on

flights to and from the Dallas region.

Chapter 2: The Effect of Bankruptcy on Productivity in the Airline Industry

This study tracks major airlines in the U.S. during the past 20 years to determine

whether bankruptcies of the biggest airlines affect their productivity under financial

stress. The U.S. airline industry has seen an incredible amount of volatility ever since

the deregulation of 1978 with every major carrier declaring bankruptcy at least once.

Business cycles surely affect airlines’ health, but not evenly. During economic

expansionary periods industry profits can be modest, but during recessions the biggest

3

airlines start declaring bankruptcies one after another. Yet after so many bankruptcies,

the industry still remains very vulnerable. In common practice, Chapter 7 bankruptcy

declaration is a way for an organization to reorganize and is a golden opportunity to

improve by getting rid of its inefficiency. However, to date there has been no previous

study in the airline industry looking into the relationship between bankruptcy and

productivity. Using data of the 14 biggest airlines in the U.S., I empirically explore how

bankruptcy affects productivity. Both partial and total factor productivity methods were

used to provide a detailed presentation of the evolution of airline productivity. I find

that bankruptcy does not have any impact on productivity as some of the major airlines

declare bankruptcy multiple times indicating lack of improvement in employee and

aircraft productivity. The results were consistent under different variations of post-

bankruptcy periods where short term and long term effects were tested.

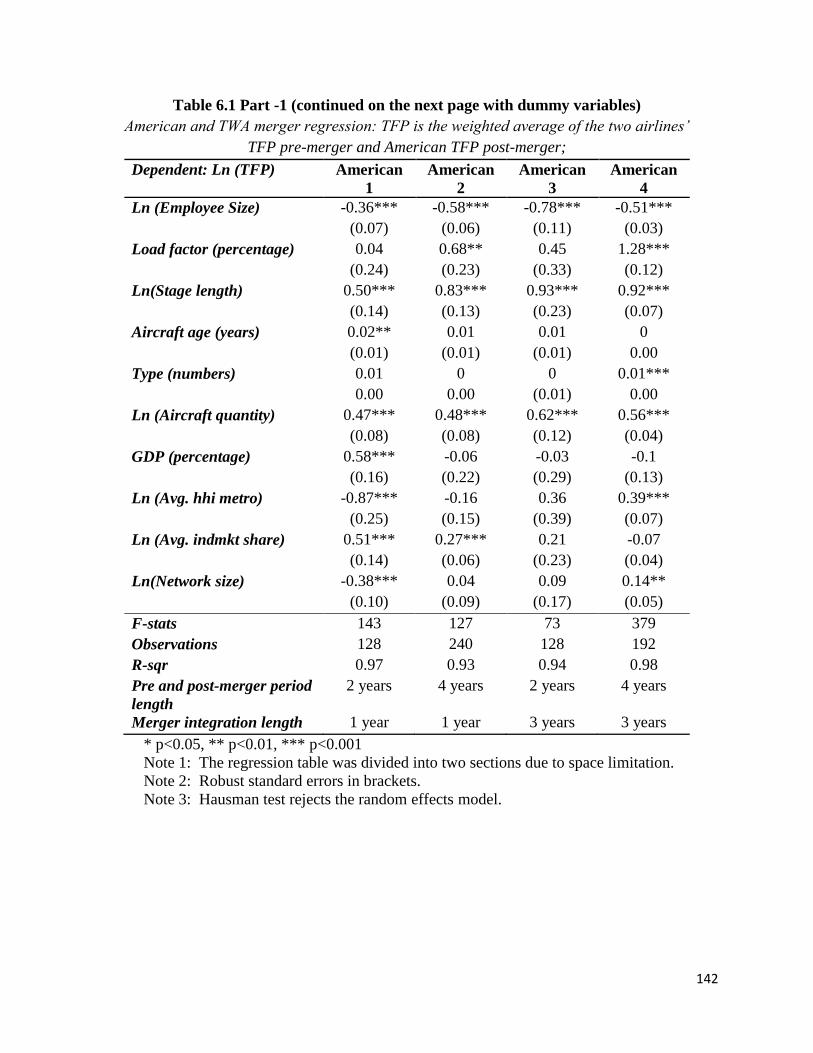

Chapter 3: The Effect of Mergers on Productivity in the Airline Industry

In this study, I examine the effect of mergers in the U.S. airline industry on

productivity. Chapter 7 bankruptcies and mergers are the two major types of strategies

a vulnerable airline can pursue in order to secure its survival in its immediate future. A

merger deal can offer several major benefits including increased market power,

availability of new financing source by merging with a healthier airline, reduced cost

and improved productivity through synergy. The airline industry has witnessed a

significantly increased level of mergers in the last decade, especially among its biggest

players who enter mega-sized mergers to create the world’s biggest airlines one after

another. Airlines highlight cost savings and improved efficiency as their primary

merger motivations. Yet, to date no study exists has examined the relationship between

merger and productivity in the airline industry. Similar to bankruptcies mergers can

offer short term survival solutions, but long term viability comes from improvements in

productivity. I use data of the 14 biggest airlines in U.S. during the past 20 years to

track productivity of airlines going through mergers. For the 14 airlines, I construct

partial and total factor productivity in order to estimate merger effects. Using the

available data, I identify three mergers where is there is sufficient ex-ante and ex-post

data exist. Using the difference-in-difference econometric technique, I find that mergers

4

do improve productivity as promised by the airlines. However, the extent of

improvements depended on whether the acquiring airline was more productive than the

target airlines prior to the merger. The results were consistent with previous findings of

studies on mergers and productivity outside the airline industry.

5

Acknowledgements

I express my deepest gratitude to my dissertation committee. Without their

contribution, encouragement and dedication, this dissertation would not have been

possible. I thank my advisor Professor Steven Morrison for his invaluable advice,

patience and support. I feel most fortunate to have met him, to be able to benefit from

his constant encouragement and mentorship. I am thankful to Professor John Kwoka

and Professor James Dana whose insightful comments, points of view enriched my

thinking and whose ever present support made this work possible.

I thank Prof. Neil Alper for patiently mentoring me to deal with students, carrying a

course load and teaching me how to teach. I am also indebted to the other faculty for

their advice, the staff and my fellow graduate students at the Department of Economics

for their support and kindness.

I am thankful to my father Kh.Bold and my mother M.Tsetsegmaa for dedicating

themselves so that I could pursue my education in America.

Finally, I dedicate this dissertation to my daughter, T.Nandin, who puts a smile on my

face every single day.

6

TABLE OF CONTENTS

Abstract

Acknowledgments

Table of Contents

Chapter 1: The Effect of Wright Amendment

on Consumer Welfare

Introduction

History of Airport Restrictions

Econometric Identification

Data

Regression Results

Conclusion

References

Tables

Chapter 2: The Effect of Bankruptcy on Productivity

in the Airline Industry

Introduction

Literature Review

Data

Airline bankruptcy background

Measuring Productivity

2

5

6

8

8

11

17

19

22

28

30

32

44

44

46

48

51

57

7

Econometric Methodology

Regression Results

Conclusion

References

Tables

Figures

Appendix

Chapter 3: The Effect of Mergers on Productivity in

the Airline Industry

Introduction

Literature Review

Data

Background on Mergers in the U.S. Airline Industry

Measuring Productivity

Econometric Methodology

Regression Results

Conclusion

References

Tables

Figures

64

67

70

72

75

85

97

99

99

101

102

105

112

118

121

124

127

130

148

8

Chapter 1: The effect of Wright Amendment on Consumer Welfare

I. Introduction

Deregulation of the airline industry in 1978 marked the beginning of an era of

market competition for commercial aviation. Ever since, airlines have been competing

fiercely using all their resources by any means without the kind of regulation that

restricted their action before 1978: some have prospered, some ceased to exist and the

rest are still trying to find ways to survive. While airlines may have differing opinions

on whether deregulation has brought them prosperity, one particular stakeholder in the

industry who has benefited substantially from deregulation is consumers. Market

competition based pricing in the airline industry has made flying so inexpensive that

the gain in consumer welfare has been large.1

Today airlines can enter and exit to serve any airport pair market at their will

and set the level of fares and frequency of flights as they see fit. As such, passenger

fares have become heavily dependent on two aspects of market structure: the level of

competition that exists on a particular route and the extent of hub dominance at origin

or destination airports of a specific flight. Though most routes are open to free entry

and exit, laws that suppress market competition still exist, causing a significant

decrease in consumer welfare in affected regions.

These laws exist in the form of limiting airlines’ ability to fly to and from

certain airports. The two major airport restrictions are the perimeter rules and slot

1 See Morrison and Winston (1995) Estimation of annual benefits to the consumers were $12.4 billion in

1993 dollars, which is $19.9 billion in 2012 dollars.

9

rules.2 This paper aims to measure the effect of Wright Amendment, which is a form of

a perimeter rule, on consumer welfare for passengers who travel to and from the Dallas

Fort-Worth metropolitan area.

The Wright Amendment directly suppresses airline competition at the fourth

busiest airport in the United States, puts restrictions on flights out of Dallas Love Field

(DAL), which is the other major airport for commercial service in metropolitan Dallas

besides Dallas Fort-Worth (DFW).3 DAL is one-third as far from downtown Dallas as

DFW airport.

The Wright Amendment has gone through several changes, but the original

Wright Amendment prohibited any airline serving DAL to sell long-haul flight tickets

that used airplanes with more than 56 seats. Specifically, an airline at DAL could not

sell tickets, connecting or direct, to any destinations beyond Texas and its neighboring

states, Louisiana, Arkansas, Oklahoma and New Mexico. For example, if passengers

wished to fly to Los Angeles from DAL, not only were they not able to fly directly to

Los Angeles but they could not even purchase a flight ticket with a connection either in

Texas or its four neighboring states. They would have to purchase two tickets

separately, one for a flight to a connecting city within the Wright Amendment

perimeter and another one for the flight between the connecting city and final

2 A fourth, long-term exclusive gate leases are another form of restriction on competition at the airport

level. Such long-term leases allow incumbent airlines to employ a majority of the gates at a certain

airport for 20 years at a time. If an entrant wishes, it has to purchase the rights to use those gates usually

at undesired hours for higher prices. (“Slot-Controlled Airports” United States General Accounting

Office Report, 2012). 3 DFW ranks fourth in passenger enplanement and deplanement after Hartsfield-Jackson Atlanta (92

million), Chicago O’Hare (66 million) and Los Angeles International (61 million) according to Airport

Council International North America as of Q3 of 2012 (http://aci-na.org/).

10

destination. A more detailed background on the Wright Amendment comes in Section

II.

Because of the Wright Amendment, fares for flights to and from the Dallas

metropolitan area (DFW + DAL) have been potentially higher than what they would

have been due to the following factor. The higher the route level competition between

the airlines on a particular route, the lower the fares have been for passengers. In the

last three decades, Southwest has been the pioneer of increased route-level competition

that results in low fares wherever it chooses to serve. When Southwest enters a route

(airport pair) fares have declined on average by 46% (Morrison 2001). This is known as

the actual effect of Southwest. When Southwest serves a route by serving airports

adjacent to a specific airport pair, fares have declined on average by 26% (Morrison

2001). This is termed the effect of adjacent competition. As such, passengers flying to

or from the Dallas metropolitan area on routes outside of Texas and its neighboring

states have been paying higher for fares due to Southwest’s inability to serve out of

DAL.4 This paper aims to measure the effect of the Wright Amendment on the

consumer welfare of the Dallas metropolitan area.

The paper is organized as follows. Section II provides background on the

Wright Amendment and one other form of airport restriction. Section III discusses the

econometric model used to capture the effect of Wright Amendment. Section IV

4 Another potential cause for higher fares at DFW is the hub premium effect. Borenstein (1989) finds that

a carrier with at least 50% of the traffic at an airport charged about 12% higher fares than those with

about 10% traffic. Currently, Dallas Fort-Worth is American Airline’s hub airport as it handles 82% of

all flights originating or ending at the airport. Naturally, on routes outside of Texas and its contiguous

states American Airlines aims to charge a hub-premium on fares on its customers which it will not be

able to if faced with competition from Southwest out of DAL. Again, the Wright Amendment has

preserved American Airlines’ ability to charge a hub-premium fare by prohibiting Southwest from

serving the affected markets.

11

provides a description of the data used for the estimates. Section V presents and

interprets the results. Section VI provides the paper’s summary.

II. History of airport restrictions

Currently there are two types of airport restrictions that legally limit

competition in the airline industry. They are the slot rule and the perimeter rule.5 The

Wright Amendment is a form of a perimeter rule where the perimeter is defined by

state borders instead of a constant distance.

Slot rules were introduced in 1969 as means of controlling rapidly increasing

traffic at four airports: New York LaGuardia, New York JFK, Chicago O’Hare and

Washington National (now Reagan National). Slot controls functions by putting limits

on the number of landings and take offs within a given hour mainly during peak

periods. The limitation on the number of take offs and landings translates into reduced

competition, but only if the traffic is high enough that the limitations are binding, which

is indeed the case generally.

The general perimeter rules and Wright Amendment were implemented to

encourage growth at nearby newly built airports, while the slot rules were targeted at

reducing airport congestion. A perimeter rule at an airport restricts all carriers serving

that airport from offering flights outside the indicated perimeter. For example, La

Guardia Airport’s (LGA) perimeter, formalized in 1984, is 1,500 miles and it was

instituted to reduce congestion at LGA by forcing long-haul flights to John F. Kennedy

Airport (JFK). If someone wishes to fly non-stop from New York to Los Angeles, for

5 Slot rules are also known as “High Density Rule.”

12

example, the passenger would have to fly either from Newark or JFK since Los

Angeles lies outside of La Guardia’s 1,500-mile perimeter. For Reagan National in

Washington D.C., the perimeter rule was instituted in 1986.

The origin of the Wright Amendment dates back to the pre-deregulation era of

the airline industry and is a very interesting case of a law that has come to suppress

competition at one of the nation’s busiest metropolitan areas. As passenger traffic in the

airline industry grew in the 1960s in the metropolitan Dallas area, competition for air

service among airports surrounding the city intensified. These airports included Love

Field, Greater Southwest Airport, Red Bird Airport and Meacham Field. Concerned

with duplication of services, Federal officials drafted a proposal to build a single airport

to serve both the regions surrounding Dallas and Fort-Worth6. The proposal was

accepted by the relevant local government bodies and all the airlines agreed to relocate

to the new regional airport once construction was complete, except Southwest Airlines.

Southwest Airlines began service on June 18, 1971 operating intra-state flights within

the state of Texas. As Southwest flourished at Love Field, it expressed its intention to

remain at Love Field even after completion of construction at Dallas Fort-Worth

International Airport. As a result, Southwest Airlines was sued by the DFW Airport

board and by the cities of Dallas and Fort-Worth, who tried to decommission DAL and

force Southwest to move to DFW. Southwest Airlines won in court and was allowed to

operate from DAL offering intrastate flights while DFW officially opened in 1974.

Southwest continued to grow successfully out of DAL offering intrastate services until

1978. However, the beginning of airline industry deregulation in 1978 opened a whole

6 Love Terminal Partners, et al., Plaintiffs, v. THE UNITED STATES, Defendant. No. 08-536 L.

13

new level of opportunities for the airline to capitalize on its successful business model

on national level. In 1979, Southwest received a ruling from the Civil Aeronautics

Board that gave it permission to offer interstate services from DAL. Naturally, the

CBA’s ruling was not welcomed at all by the supporters of DFW as they quickly took

counter measures by turning to U.S. House of Representatives Speaker Jim Wright (D-

Texas) to include an amendment to the International Air Transportation Competition

Act of 1979 that would protect DFW from any competition by DAL. The result, after

some modifications, became what is known as the Wright Amendment of 1980, which

enforced three major points: a) it became illegal for any airline at DAL to offer flights

to destinations beyond Texas and its four neighboring states, Louisiana, Arkansas,

Oklahoma and New Mexico (the Wright perimeter), b) airlines were prohibited to offer

or advertise the availability of any connecting flights between DAL and any city

outside the Wright perimeter and c) airlines at DAL may not use aircraft with more

than 56 seats for commercial purposes to destinations outside the Wright perimeter.7

Today the annual enplanements and deplanements at DFW are 57.7 million

passengers, making them fourth largest in the country.8 At DAL it had stayed constant

around 6 million until 2006 and grew to 7.9 million by 2011.9 Considering the traffic

had reached 6.3 million in 1973 the growth at the airport was severely constrained by

the Wright Amendment. For many of the 57.7 million passengers who are forced to use

DFW, the Wright Amendment is potentially a major setback preventing them from the

choice of experiencing lower fares. As such, over the years there has been heavy

7 Love Terminal Partners, et al., Plaintiffs, v. THE UNITED STATES, Defendant. No. 08-536 L.

8 Dallas Fort-Worth Airport statistics of 2011 (http://www.dfwairport.com/stats/P1_058942.php).

9 Dallas Love Field Airport statistics of 2011 (http://www.dallas-lovefield.com/pdf/statistics).

14

campaigning resulting in a series of relaxations and an agreement to fully repeal the

amendment in 2014 was reached in 2006 among the stake holders. These sequences of

relaxations present an opportunity to measure what fares could be in the absence of the

amendment. Arguably, the Wright Amendment has outlived its original purpose and

stands in the way of all the benefits that can be brought by increased competition to the

Dallas metropolitan area consumers of air service.

The first exemption, passed in October of 1997, was sponsored by Senator

Richard Shelby of Alabama and was consequently named the Shelby Amendment.10

The Shelby Amendment allowed for non-stop flights to Alabama, Mississippi and

Kansas from DAL.11

Citing lack of demand at DAL, Southwest did not begin non-stop

service immediately, though Southwest did take the opportunity to start selling tickets

for connecting flights to two major cities in these states: Birmingham, Alabama and

Jackson, Mississippi. As Southwest did not increase its service due to low demand, it is

expected that no major statistically significant change in fare would take place. Table 1

provides a comparison of fares and passenger quantity before and after the Shelby

Amendment took effect.

Even though Southwest did not begin non-stop service immediately, fares

decreased by 23% for the Birmingham route, but increased by 12% over the next four

10

“Dallas Love field: The Wright and Shelby Amendments” CRS Report for Congress (2005). 11

The Shelby Amendment also introduced a more relaxed version of the 56-seat restriction stating that as

long as the airplane contained, including reconfigured or originally manufactured, fewer than 56-seats

and weighted less than 300,000 pounds, it could be flown anywhere in the country. The previous version

of the 56-seat rule stipulated that the aircraft originally must have been produced with fewer than 56

seats. Legend Airlines used the opportunity to offer service using re-configured 56-seat airplanes to long-

distance destinations such as Washington D.C. and New York. American Airlines immediately began

offering the same service to the same destinations even occasionally at lower prices while at the same

time suing Legend Airlines to halt their service out of DAL. Just a few months after beginning operation,

Legend Airlines went out of business.

15

quarters for the Jackson route. The increase in Jackson fares will be explained in the

results section. In addition, the number of passengers who flew to these destinations

saw a big increase for the Birmingham route and a mild 10% increase for the Jackson

route.

The second relaxation came in December 2005 when Senator Christopher ‘Kit’

Bond of Missouri successfully added another exemption (Bond Amendment) to the

Wright Amendment to allow flights to his state from DAL.12

Southwest immediately

began service to Kansas City and St. Louis. At the same time, American Airlines also

started serving those two cities from DAL. Table 2 provides a comparison of fares and

passenger traffic before and after the Bond Amendment took effect.

Here, we observe much bigger changes in both fare and traffic due to

Southwest’s immediate entrance into the new markets. The market concentration level

drops significantly as well.

The third and the most significant alteration was realized in 2006 after years of

heavy campaigning by Southwest to repeal the amendment in its entirety. An

agreement, which eventually became a public law named the Wright Amendment

Reform Act of 2006, was reached between American Airlines, the city of Dallas, the

city of Fort-Worth and Southwest. The agreement was that the original Wright

Amendment would be partially repealed beginning in October 2006 and fully repealed

in 2014. There were two major conditions that were agreed upon for the Reform-Act to

be realized. First, beginning October 2006 until October 2014, airlines operating at

12

Wright Amendment Reform Act (2006).

16

DAL were now permitted to sell tickets to any destination in the country as long as the

flights make a stopover (or a connection) within the Wright perimeter. Second, once the

stop-over requirement expires and airlines would be allowed to make non-stop flights

from DAL to anywhere in the country, the number of gates at DAL would be reduced

from 32 to 20.13

Under the Reform-Act from October 2006 till October 2014, an airline

could begin selling tickets from DAL to fly anywhere in the country, unlike previously,

but the itinerary would have to make a stop-over (or a connection) within the Wright

perimeter. Within a few days of passing of the Reform-Act, Southwest announced its

plan to immediately start selling tickets to 25 metropolitan areas from Love Field with

connections at various points inside the Wright perimeter. Table 3 presents a

comparison of fares before and after the third relaxation was introduced allowing

Southwest to begin selling tickets to 25 cities:14

The simple comparison of before-and-after average fares for the 25 markets

show significant reduction in fares for the most part as expected. 16 out of 25 markets

experience fare decreases of more than 10%. Of the remaining nine markets, seven

experience fare decrease, one shows no change and another one shows an increase in

13

Even though by 2014 all airlines could begin selling non-stop tickets to anywhere from Dallas Love

Field, the cap of twenty gates at Dallas Love Field will remain and has been causing some controversy.

The gate usage has been divided as 16 for Southwest, 2 for American and 2 for Continental (now

United). JetBlue has opposed the reform act. The cap will become a binding restriction for further growth

at DAL if demand increases significantly, which is expected. To remedy the situation at least partially,

the airport is investing in modernizing the airport’s twenty gates to handle passenger traffic more

efficiently. (http://www.dallas-lovefield.com/) 14

It must be noted that flights to these cities had been already available from Love Field prior to the

reform act. However, it was illegal for Southwest and other airlines at Love Field to sell tickets to these

long-haul destinations. There are reports of consumers who went through the task of booking two

roundtrip tickets on their own, one to a destination within the Wright perimeter and second to the final

destination from the connecting airport. Considering the additional task passengers had to complete to fly

on Southwest, their fares must have been low enough to offset the extra hurdle. For example, if a

passenger needs to fly from DAL to Chicago, he/she would comb through all the possible connecting

points within the Wright perimeter using Southwest’s website. Then, he/she would need to determine

flights with best matching connection times. Only, then he/she could begin to compare prices. It was

known as the “Texas two-step fare and ticketing” among the local fliers (flyerguide.com, flyertalk.com).

17

fares of 7%. Aggregate calculation of all the 25 markets show a 14% fare decrease and

a 13% increase in traffic.

III. Econometric Identification

The main estimation used for capturing the airport restriction effect is the OLS

difference-in-difference (DD) model. It has become a common practice to employ the

difference-in-differences methodology to estimate the effect of a natural experiment by

observing changes in two groups: treatment and control. To employ the difference-in-

differences method, we must have observations on both groups before and after the

event. Once the timing of the event and the two groups are identified, the DD model

works by observing the differences within the simultaneous changes in two groups as

both groups evolve through time.

Each of the three stages of the Wright Amendment serves as the external event

that affects the treatment group. With each relaxation, new routes that are no longer

subject to the Wright Amendment open up for service. These new routes will serve as

the treatment group, while all the other routes from the Dallas metropolitan area will

serve as the control group.

Furthermore, we implement a market-level fixed effect to account for all the

different routes that are being regressed at the same time.

The main assumption of the DD method is that no major change takes place

between the treatment and the control group other than the event in question. That is to

say if there were some other external causes affecting the treatment group differently

than the control group besides the event in question, then the control group can no

18

longer serve the purpose it is designed for. No event has been detected that could

influence the routes affected by the Shelby, Bond and the Reform-Act other than the

rest of the routes to/from the Dallas metropolitan area.

As I am only concerned with flights to and from the Dallas metropolitan area, I

make no distinction between flights to and from DFW or DAL. Therefore, flights to

and from DFW and DAL are regarded to be the same.

The following regression is used for the estimation:

ln (fare)it itit treatmentpostextreatmentpostexX )*.(**.** 4320

Dependent variable:

Log of fare:

For one-way trip flights: log of the fare for passengers in route i in time t (year-

quarter);

For roundtrip flights: log of half of the fare for a single passenger on a flight to

or from the Dallas metropolitan area in a given year-quarter;

Explanatory variables X:

Distance:

Distance between DAL and either the originating or the destination airport;

the coefficient is expected to be positive as longer trips are more expensive;

Quarterly Effect dummies:

1st quarter: 1 for all 1

st quarter observations regardless of year; 0 otherwise;

2nd

quarter: 1 for all 2nd

quarter observations regardless of year; 0 otherwise;

3rd

quarter: 1 for all 3rd

quarter observations regardless of year; 0 otherwise;

Roundtrip dummy:

1 for roundtrips flights and 0 otherwise; the coefficient is expected to be

negative as roundtrip flights are usually much cheaper than one way flights

distance held constant;

Time dummy:

19

1 for all observations after the event and 0 otherwise;

Treatment dummy:

The treatment dummy is 1 for routes where the Wright Amendment restriction

previously applied but was removed due to a particular relaxation and 0

otherwise. A route is consider a specific airport pair, but because this paper

aims to measure effect on consumers of the Dallas metropolitan area, containing

both DFW and DAL, DFW and DAL are considered to be the same point of

origin/destination.

Treatment Regional dummy:

This dummy further extends the Treatment Dummy by including other airports

in the nearby region, where a route is defined to exist between the Dallas

metropolitan area and another metropolitan area; for example, under this

definition, Dallas-Chicago, Midway and Dallas-Chicago, O’Hare are regarded

as one route; while it is expected that the Wright Amendment caused higher

fares when routes are defined at the airport level, it is interesting to see how far

the effect extends when the routes are defined at the metropolitan level.

Time*Treatment dummy (or Treatment Regional):

1 for all observations that are in the treatment group for the time period after

each relaxation and 0 otherwise; this is the main coefficient that will indicate

the impact of the Wright Amendment and it is expected to be negative as we

expect that restriction on competition results in higher fares;

Table 4 presents the treatment groups for each case of the exemptions.

Once a relaxation is introduced, I wait till the beginning of the next quarter to

implement the time dummy since the quarter in which the event takes place will have

undistinguishable mix of affected and unaffected fares by the treatment. The same goes

for the ex-ante time period that excludes the quarter in which the event takes place.

IV. Data

The data for this study come from the U.S. Department of Transportation’s

Ticket Origin and Destination Survey (Databank 1B), which consists of a 10% sample

of the tickets provided by domestic airlines to the Department of Transportation on a

20

quarterly basis. The data contains collection of tickets where one observation (a row) is

a ticket containing the following information:

Fare paid for one passenger

Number of passengers with the same itinerary and same fare

Number of segments in a given ticket15

Segment-specific variables: carrier airline, distance of segment, beginning and

ending airports,

Origin and destination airports of a ticket

Fare basis: first, business or coach economy class;16

Reporting year and quarter

Change in trip direction (used for identifying round trip tickets)

The following filters were applied to the 10 percent ticket sample to obtain

relevant observations for this study:

Only the tickets with trips either beginning or ending at DFW/DAL were

selected; this means all tickets that do not involve DFW/DAL as origins or

destinations were dropped.

Tickets with more than four segments (5% of the sample), which means tickets

that involve two or more stop-overs, were dropped.

Tickets with more than two trip breaks (1% of the sample), which means multi-

destination tickets, were dropped. A trip break indicates either a turn-around

15

One segment represents one leg of a flight. 16

In addition, the complete class of service types include variations of the above three which are first

class discounted, coach class discounted, business class discounted, thrift, thrift discounted, first class

premium, supersonic, standard class and coach economy premium.

21

point or the final destination of a ticket. The destination airport becomes

ambiguous for a ticket with more than two trip breaks when the ticket is for a

round-trip flight.

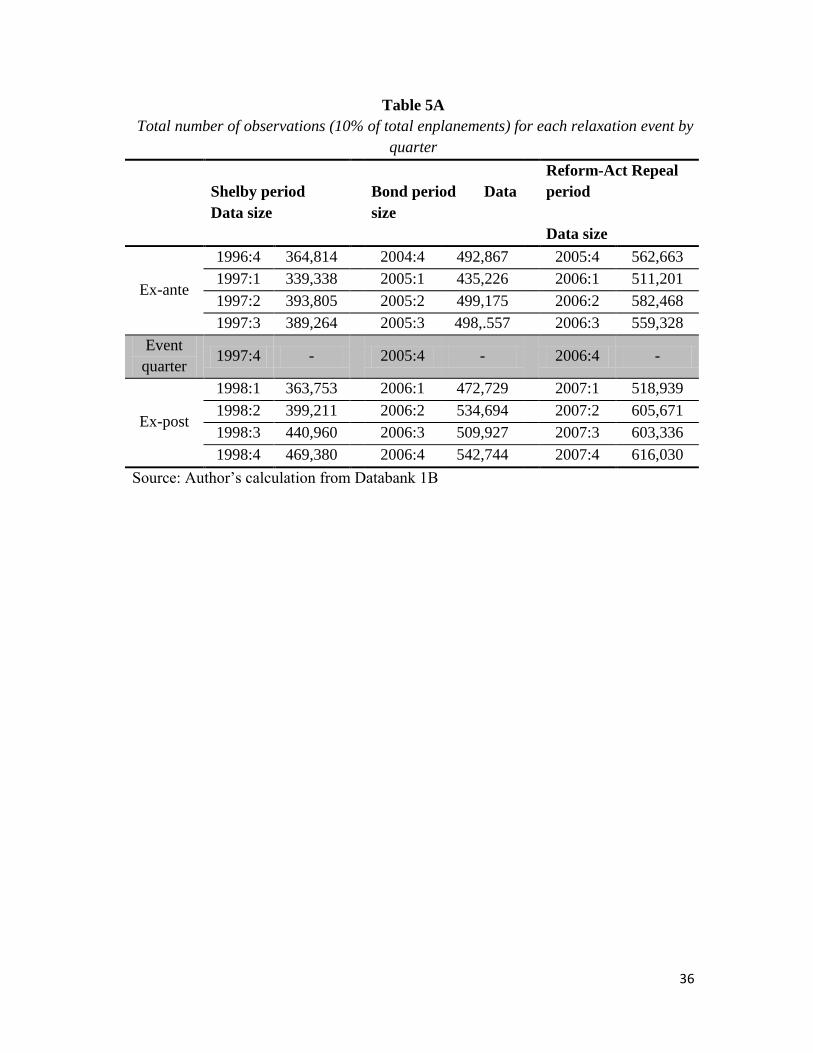

Table 5 presents the number of observations in each quarter for each relaxation

event after all irrelevant parts of the data have been filtered out. In addition, the

remaining data have been expanded by passenger number. In the original data set one

observation meant one itinerary at a specific price with one or multiple passengers in

the same itinerary. In other words, if multiple people paid the same and traveled exactly

the same itinerary, during the given quarter, all the passengers were grouped into one

observation. Expanding by passengers means converting that one observation into

multiple observations where one observation represents one person the same as one

enplanement. In doing so, the number of observations directly translates into number of

enplanements, which means it now reports 10% of traffic on a given route. We will use

traffic information to calculate the welfare effect in Section V.

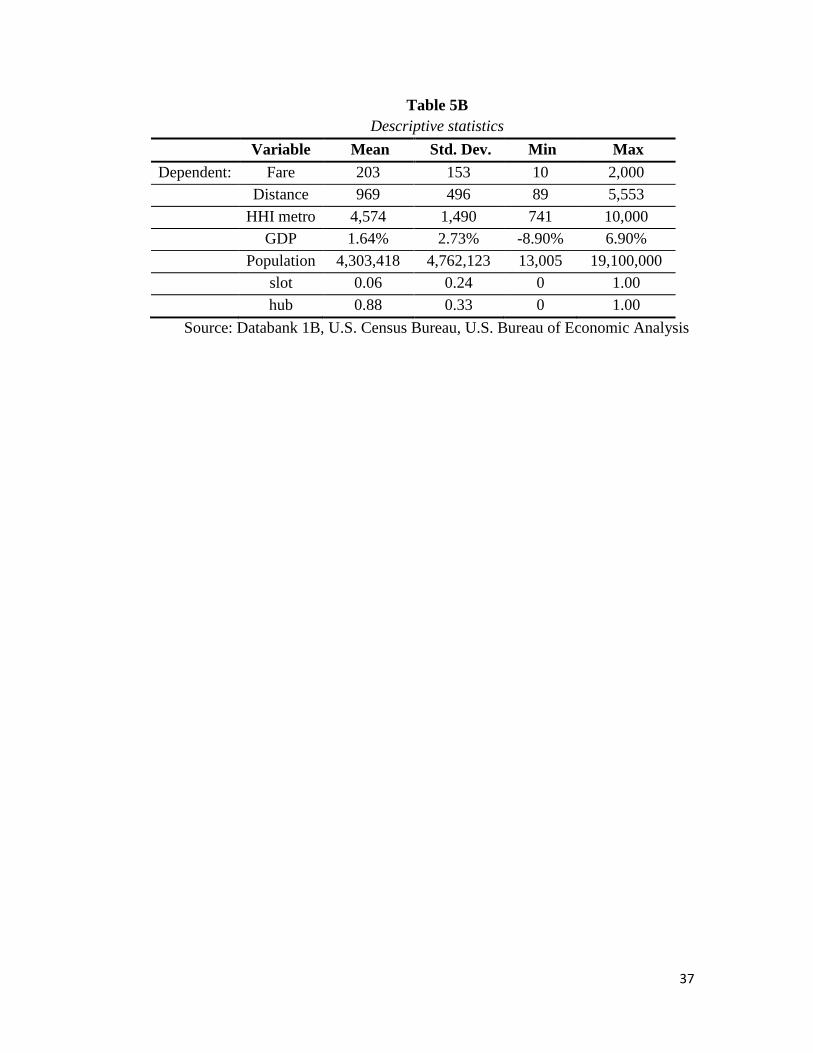

Additional control variable data consist of population at destination airports

where the origin is the Dallas metropolitan area and quarterly percentage change in

U.S. GDP. The population data comes from the U.S. Census Bureau and the GDP data

comes from the U.S. Bureau of Economic Analysis. Table 5B provides descriptive

statistics of the final data set.

22

V. Regression Results

1. Shelby Amendment

Table 6A presents the regression results for the routes affected by the Shelby

Amendment. The Shelby Amendment took place in the fourth quarter of 1997, thus that

particular quarter is excluded from regression data. Three different regressions have

been run covering three different frames of time. The first result covers the third quarter

of 1997 and the first quarter of 1998 which are the immediate quarter before and after

the Shelby relaxation takes effect. The second result covers the first quarter of 1997 and

the first quarter of 1998 which are three quarters before and the quarter after the

relaxation event, allowing for same quarter comparisons. The third result covers the

twelve month period prior the relaxation, from 1996:4 to 1997:3 and the twelve month

period after the event, from 1998:1 to 1998:4. This helps us to look at the effect of the

relaxation on a twelve-month aggregated time frame. The treatment dummy includes

both of the cities of Birmingham, AL and Jackson, MS for which Southwest began

selling tickets for connecting flights following the enactment of the Shelby

Amendment.

We observe that for all three instances, all signs of the coefficients are the same.

However, we find the coefficients to be insignificant for the Time*Treatment dummy,

the main variable capturing the change in fares, for the immediate before and after

quarter and the twelve-month period regressions. It is significant for the same quarter

analysis, which confirms that the fares decreased by 25% compared with the previous

23

year’s same quarter.17

For the immediate quarter before and after analysis, fares

decreased by 11% and for the twelve month period fares decreased by 7%; however,

since both of them are insignificant when the errors are clustered at the route level, they

will not be used for calculating the welfare effect.

For the twelve-month period, the time dummy indicates a 4% increase in fares,

statistically significant, as is the case for the same quarter analysis. All three

regressions agree that round-trip flights cost 37% less than one-way flights when

controlled for distance. Connecting flights do not display statistically different figures

when everything else is the same as direct flights. This makes sense for the Shelby

amendment as Southwest announced no intention of offering direct flights from DAL

citing lack of demand and only began to sell connecting tickets on services that were

already available.

An inquiry into the changes in traffic in Table 6B reveals that majority of the

increase in traffic is attributable to Southwest’s connecting services to these

destinations. It is likely that as Southwest offered only connecting services to compete

against American and Delta’s non-stop services to the destinations affected by the

Shelby Amendment, Southwest’s entry into these markets did not result in statistically

significant major reductions in fares.

17

The percentage change in fares is calculated by the formula of (e^(coefficient)-1)*100. It is roughly

equal to the coefficient when the value is small enough, but the difference grows drastically for bigger

values. Thus, 0.224 in percentage is (e^0.224-1)*100=25%.

24

2. Bond Amendment

Table 7A presents the effect of changes caused by Senator Bond’s amendment

to the Wright Amendment. Once the changes took effect, Southwest immediately began

non-stop service to Kansas City and St. Louis as they were lucrative markets in which

American had enjoyed a great deal of market power. The Bond amendment was

enacted in 2005:4 and thus that period has been excluded from the data.

We observe some major differences and similarities between the Bond and the

Shelby Amendment regressions.

First, the Time*Treatment dummies across regressions, which capture the

change in fares due to Southwest’s entrance allowed by the Bond Amendment, are not

only much larger than in the Shelby Amendment but all are significant. The coefficients

for one quarter before-and-after, same quarter and four quarter regressions are -0.45, -

0.53 and -0.49 respectively. In percentage terms these translate to fare reduction of

56%, 69% and 63% respectively. Second, the time dummy coefficient displays around

4% increase in fares over the twelve-month period captured in the regressions, the same

as in the Shelby Amendment. Third, just as in the Shelby Amendment, the value the

coefficients of the dummies on the connecting flights are small and statistically

insignificant.

The increase in traffic is 53% for the Bond effect while for the Shelby effect the

increase was 24%, signaling a much larger entry. During the four quarters after the

enactment of the Bond Amendment, Southwest’s market share rose from 4% to 32%.

25

Using the data on change in traffic and fares from the regressions, the total gain

in welfare brought to passengers can be calculated as follows. The mean fare for

twelve-months prior to the amendment on the affected routes was $219. The twelve-

month period following the amendment saw a 63% decrease in fares, which translates

to $137. The number of passengers flying on the affected routes prior to the

amendment was 489,980, with an increase of 261,640 passengers during the following

twelve-month period. Lower bound of the total gain to the passengers then would be

$137*489,980=$67,127,260 or $67 million per year.18

This is the total savings realized

for the existing passengers. The approximate total gain in welfare is $137*489,980 +

$137*261,640/2 = $85,049,600 or $85 million for the twelve months following the

Bond amendment.

3. The Reform Act

Table 8 presents results from the Reform-Act regression. Contrary to the time

frames of the Shelby and Bond Amendment regressions results, the Reform-Act

regression looks at a long term change in fares on the 25 destinations, represented by

the five year ex-ante and ex-post periods. Additional set of regressions for each three

different time periods have been conducted where the destinations are considered to be

metropolitan areas rather than airports to see the extent to which Southwest’s entry

impacts as implied in Morrison (2000). The results of airport destinations fare nearly

identical with the results of metropolitan destinations.

18

This is the welfare gain to the existing number of passengers, not including any gains brought by new

passengers who are flying due to fare decrease. With an assumption that there has been no shift in the

demand curve and that these passengers have a linear demand curve, the additional gain in consumer

surplus from new passengers can be calculated as (∆p * ∆q) / 2. We will make these assumptions for

future calculations for approximately assessing total gain in welfare.

26

Distance and market concentration level have positive effect on fares as longer

flights cost more and bigger concentration also results in higher fares. GDP and

Population have no effect on fares as GDP is significant only in the one year time frame

and Population is dropped due to lack of variation.

Fares at airport with slots are on average 5% (the coefficient is 0.05) lower than

non-slot airports and fares at hubs are about 13% (the coefficient is 0.12) higher than

non-hub airports. Hub premiums are consistent with previous empirical studies

(Borenstein (1989)). The negative effect of the slot controlled airport could be logical if

the extent of competition at these airports outweighs the degree to which traffic is

constrained by the slot control. Roundtrip fares are on average 13% cheaper than one-

way fares when controlled for distance. Quarter dummies bear significance when there

is enough variation and get dropped otherwise. Where they are significant we observe

that fares in Q2 and Q3 are slightly more expensive than fares in Q1 and Q4. This

difference is related to the high tourism season.

The main variable of interest that captures the effect of the Wright Amendment

is Time*Treatment. The coefficient of this variables is big at first when 1 quarter before

and after fares are compared, 17%, but decreases to about 11%-13% when 1 year and 5

year periods are introduced. The decrease of fare difference between Wright affect and

non-affected markets from 17% to 13% is plausible as American Airlines and those

serving out of DFW cannot continuously keep charging higher amount for fares. What

is surprising is that while the 13% difference is reached within a year, it doesn't change

much from that level during the next four years. There are two possible explanations

27

that complement each other for airlines at DFW that continue to charge somewhat

higher fares in the long run. First, DAL is capacity constrained where it has only 20

gates. Even though Southwest can offer lower fares, compared to DFW, capacity

constraint will limit the extent to which consumers can benefit Southwest's new service.

Second, many consumers could be willing to pay 13% more for fares just to experience

the non-stop feature offered from DFW. Even though Southwest now can fly to any

destinations it wants from DAL, the law still enforces all flights out of DAL to have a

connection inside the Wright perimeter.

For the final result, this study focuses on the 13.88% of fare reduction affecting

the 25 metropolitan consumers for the five years following the Reform-Act.

The consumer welfare is calculated as follows. During the five years prior to the

Reform-Act, average fare between Dallas and the 25 affected metropolitan areas was

$215 per enplanement. 13.88% change in fare translates to $29.85. Total number of

traffic to the five metropolitan areas prior to the Reform-Act was 41,730,860. This

translates into $1,245,586,983 or $1.24 billion in savings to existing passengers alone.

Assuming the price elasticity of demand of -0.7 as the lower bound as done in

Morrison (1994), we can calculate the additional benefit to consumer surplus brought

by new passengers who are flying from Dallas due to the lower price. We already know

that price decreased by 14%, which means quantity demanded increased by

(-14)*(-0.7)=9.8 or 9.8% due to the lower price. If we apply the 9.8% increase in

quantity demanded to the 41,730,860 enplanements five years preceding the Reform-

Act, then increase in quantity is 4,086,624 or about 4 million enplanements. Assuming

28

a linear demand curve, the added consumer surplus brought by new passengers is

(4,086,624*$29.85)/2 or $61 million. The combined gain in consumer surplus is

$1,245+$61 million or $1.31 billion.

The higher bound assumption of price elasticity of demand at -1.5 brings the

added consumer surplus brought by new passengers to $131 million. The total gain in

consumer surplus in this case is $1,245+$131=$1.37 billion which is not very different

from the previous result.

VI. Conclusion.

In this essay, I measured the effect of airport competition restrictions on

consumer welfare by identifying changes in fares and traffic. A law that prohibits long

distance flights out of Dallas Love Field experienced three changes during its lifetime

has made it possible to estimate its effect on fares using the difference-in-difference

model. The regressions from three different time frames have produced fairly similar

results all pointing in the same direction if not with equal weight. The Shelby

amendment caused a decrease in fares, though statistically insignificant, with an

increase in quantity. This was expected as Southwest announced its intention to not

offer any new services and instead simply begin selling tickets on existing flights. The

Bond amendment saw a significant decrease in fares as Southwest immediately began

non-stop service to two destinations, Kansas City and St. Louis. The Reform-Act

finally allowed Southwest and other carriers at DAL to sell tickets to any destination

outside the Wright perimeter from DAL on the condition that the flights make a stop-

over. A 13.88% decrease in fares has been observed due to Southwest’s entry into

29

multiple markets. Based on the fare reduction and number of passengers flying long-

distance from DAL, the gain in consumer surplus over the five years following the last

change to the Wright Amendment has been estimated to be $1.31 billion.

It is worthy to note that the 13.88% reduction is occurring even though

Southwest is still being forced to make a connection within the Wright perimeter while

having to compete against those carriers at DFW that offer non-stop flights. Thus, the

price could fall even further once Southwest becomes eligible to offer the same service

from DAL.

The above results clearly display the scale of the negative welfare impact the

Wright Amendment brings to passengers of the Dallas metropolitan area. After 2014,

the Wright Amendment will be lifted, but not entirely due to gate capping, to allow

Southwest to offer non-stop flights and the region’s passengers and the economy can

finally begin enjoy everything that is brought by low airfares.

30

References:

Airport Council International – North American Q3, 2012 Traffic statistics (2012)

http://aci-na.org.

Borenstein, S. (1989) “Hubs and High Fares: Dominance and Market Power in the US

Airline Industry,” RAND Journal of Economics, 20, 344-65.

Cherny, A.I., D.Gillen, H.M. Niemeier and P.Forsyth (2008) “Airport Slots,” Ashgate

Publishing Company, London.

Dallas Fort-Worth International Airport Traffic report (2012)

http://www.dfwairport.com/stats/index.php.

Dallas Love Field Airport Traffic report (2012) http://www.dallas-

lovefield.com/pdf/statistics.

Dallas Love Field: The Wright and Shelby Amendments (2005) Congressional

Research Service report for Congress, 109th

Congress; H.R. 2932, H.R. 2646, H.R.

3058, H.R. 3383, S. 1424, and S. 1425.

Farris, M.T.II., and S.M.Swartz (2005) “Repeal or Retain? The Wright Amendment

Debate” University of North Texas.

Morrison, S.A. and C. Winston (1994) “The Evolution of the Airline Industry,” The

Brookings Institution Press, Washington, D.C.

Morrison, S.A. (2001) “Actual, Adjacent, and Potential Competition: Estimating the

Full Effect of Southwest Airlines,” Journal of Transport Economics and Policy,

Volume 35, Part 2, May 2001, pp. 239-256.

LOVE TERMINAL PARTNERS, et al., Plaintiffs, v. THE UNITED STATES,

Defendant. (2011) United States Court of Federal Claims, No. 08-536 L.

Reforming the Wright Amendment (2006) Hearing before the Subcommittee on

Aviation of the Committee on Transportation and Infrastructure House of

Representations, 109th

Congress, 2nd

session.

Slot-Controlled Airports: Report to the Committee on Commerce, Science, and

Transportation, U.S. Senate (2012) United States Government Accountability Office,

GAO-12-902.

31

Southwest Airlines New Release (2006) “Wright Amendment Reform Act of 2006

Enacted Into Law; Southwest Airlines Offers Customers $99 One-Way Fares and

Increased Travel Options From Dallas Love Field,” http://www.southwest.com.

“That Long Drive Out to the Airport: Why the Wright Amendment is bad for Dallas”

(2005) Dallas Magazine, August, 2005.

The Repeal of the Wright Amendment (2005) The Legacy Center for Public Policy

Wright Amendment Reform Act (2006) Public Law 109-352, 109th

Congress

“We’re talking about the Wright amendment and short-haul flights,” (2011) Dallas

Morning News, Jan 11, 2011.

32

Tables:

Table 1

Comparison of average fares and traffic for the Shelby Amendment affected

routes for four quarters before (1996:4 - 1997:3) and four quarters after (1998:1 -

1998:4) the event quarter (1997:4)*

Before Relaxation Percentage Change after relaxation

Average

Fare)

Traffic

(Enplanements)

HHI Average

Fare

Traffic

(Enplanements)

HHI

Birmingham,

AL $213 67,380 3754 -23% +37%

-

12%

Jackson, MS $120 59,660 5210 12% +10%

-

10%

Source: Author’s calculation from Databank 1B

* The event quarter is the quarter in which the law changes takes place and is

always excluded from analysis due to having some fares that were affected by

the law and some that are not.

33

Table 2

Changes to the Bond Amendment affected routes; four quarters before (2004:4 -

2005:3) and after (2006:1 - 2006:4) the event quarter (2005:4)

Before Relaxation

Percentage Change after

relaxation

Average

Fare

Traffic

(Enplanements) HHI

Average

Fare

Traffic

(Enplanements) HHI

Kansas,

MO $220 241,370

788

0 -50% +52% -32%

St. Louis,

MO $217 248,510

733

4 -50% +55% -23%

Source: Author’s calculation from Databank 1B

34

Table 3

Comparison of average fares and traffic for the 25 Reform-Act affected routes

1 year before (2005:4 – 2006:3) and 1 year after (2007:1 - 2007:4)*

Before Relaxation Percentage Change after

relaxation

Averag

e Fare

Traffic

(Enplanement

s)

HHI Averag

e Fare

Traffic

(Enplanement

s)

HHI

Louisville $268 70,280 3281 -34% 59% 14%

Omaha $239 81,830 6753 -30% 50% 2%

Columbus $269 132,690 5077 -29% 30% 21%

Detroit $252 271,660 3923 -27% 24% 2%

Nashville $236 146,180 7612 -26% 46% -

13%

Philadelphia $264 350,920 3954 -26% 22% 2%

Phoenix $232 394,410 3673 -23% 31% -2%

Oakland $274 117,910 5338 -22% 20% -

13%

San Diego $267 242,970 5062 -21% 33% -6%

Cleveland $263 131,190 3371 -20% -11% 30%

Denver $194 574,910 3208 -20% 8% 0%

Tampa $226 230,210 7044 -19% 24% -

15%

Salt Lake City $241 18,230 2713 -18% 19% -3%

Tucson $240 85,900 6714 -16% 3% 3%

Jacksonville $210 122,420 5997 -13% 15% -4%

Portland $253 161,360 3777 -10% 11% 5%

Sacramento $244 151,600 3841 -9% 8% 6%

Seattle/Tacoma $245 334,910 4281 -8% 8% -2%

Los Angeles, $227 590,490 5017 -7% 11% -1%

Indianapolis $204 169,580 6312 -7% 5% 11%

Baltimore/Washingto

n D.C.

$187 372,810 5776 -7% -1% -9%

Orlando $174 504,560 5108 -2% 14% -8%

Las Vegas $186 587,460 3781 -2% 8% 2%

Chicago Midway $131 328,220 4003 0% -25% 45%

Fort

Lauderdale/Hollywo

od

$175 271,840 7005 7% -11% -9%

All 25 markets

combined $217 6,608,610 4671 -14% 13% -1%

Source: Author’s calculation from Databank 1B

*the quarter in which the law takes place, 2006:4, is excluded

35

Table 4

Date of relaxations and affected treatment groups

Relaxation

name

Date of

Event Treatment routes

Control

routes

Shelby

Amendment 1997:4

To/From Dallas

metropolitan area to

Birmingham, AL and

Jackson, MS all other

routes to/from

the Dallas

metropolitan

area

Bond

Amendment 2005:4

To/From Dallas

metropolitan area to

Kansas and St. Louis,

MO

Reform-Act

repeal 2006:4

To/From Dallas

metropolitan area to the

25 new routes

Southwest entered

Source: Author’s calculation

36

Table 5A

Total number of observations (10% of total enplanements) for each relaxation event by

quarter

Shelby period

Data size

Bond period Data

size

Reform-Act Repeal

period

Data size

Ex-ante

1996:4 364,814

2004:4 492,867

2005:4 562,663

1997:1 339,338

2005:1 435,226

2006:1 511,201

1997:2 393,805

2005:2 499,175

2006:2 582,468

1997:3 389,264

2005:3 498,.557

2006:3 559,328

Event

quarter 1997:4 -

2005:4 -

2006:4 -

Ex-post

1998:1 363,753

2006:1 472,729

2007:1 518,939

1998:2 399,211

2006:2 534,694

2007:2 605,671

1998:3 440,960

2006:3 509,927

2007:3 603,336

1998:4 469,380

2006:4 542,744

2007:4 616,030

Source: Author’s calculation from Databank 1B

37

Table 5B

Descriptive statistics

Variable Mean Std. Dev. Min Max

Dependent: Fare 203 153 10 2,000

Distance 969 496 89 5,553

HHI metro 4,574 1,490 741 10,000

GDP 1.64% 2.73% -8.90% 6.90%

Population 4,303,418 4,762,123 13,005 19,100,000

slot 0.06 0.24 0 1.00

hub 0.88 0.33 0 1.00

Source: Databank 1B, U.S. Census Bureau, U.S. Bureau of Economic Analysis

38

Table 6A

Shelby Amendment regression results*

1 quarter before

(1997:4) and 1

quarter after

(1998:1)

Same quarter,

(1997:1) to

(1998:1)

Four quarters before

(1996:4 – 19997:3)

and four quarters

after (1998:1 – 1998:4)

Coeff.**

Clustered

t-stat*** Coeff.

Clusered

t-stat Coeff.

Clustered

t-stat

Time

dummy 0.070 (4.78) 0.044 (1.91) 0.048 (3.7)

Time *

Treatment -0.106 (-0.89) -0.224 (-7.73) -0.073 (-0.83)

Roundtrip -0.307 (-9.15) -0.322 (-10.6) -0.328 (-11.37)

Connecting -0.024 (-0.84) -0.002 (-0.09) -0.031 (-1.35)

1st quarter

effect 0.033 (2.1)

2nd

quarter

effect 0.027 (2.53)

3rd

quarter

effect 0.020 (2.48)

R-sq 0.23

0.24

0.25

Observations 753,017

703.091

3,160,525

* For all three regressions (Shelby, Bond and the Reform-Act), Hausman test

has been performed to test for random fixed effects. The results indicate there is

no statistically significant difference between the fixed and random effect

approaches in this case.

** For the Shelby and Bond amendments, control variables HHI, GDP,

population, slot dummy and hub dummy have been excluded due to lack of

variation as the treatment group consists only of two destinations. The Reform-

Act regression includes these variables.

*** Given the large number of observations, a regression clustered at the route

level has been performed to ensure robust results.

39

Table 6B

Changes in market share and traffic on routes affected by the Shelby

Amendment

American Delta Continental Southwest Remaining Combined

Traffic*

1996:3 –

1997:3

44% 44% 8% 1% 3% 127,040

1998:1 –

1998:4

41% 41% 2% 14% 2% 157,480

Source: Author’s calculation from Databank 1B

* Birmingham and Jackson traffic data are combined.

40

Table 7A

Bond Amendment regression results

1 quarter before

(2005:3) and 1

quarter after

(2006:1)

Same quarter,

(2005:3) to (2006:3)

Four quarters before

(2004:4 – 2005:3) and

four quarters after

(2006:1 – 2006:4)

Coeff.

Clustered

t-stat. Coeff.

Clustered

t-stat. Coeff.

Clustered t-

stat.

Time

dummy 0.030 (4.73) 0.046 (5.77) 0.047 (6.08)

Time *

Treatment -0.454 (-71.72) -0.539 (-27.86) -0.491 (-25.54)

Roundtrip -0.022 (-2.46) -0.017 (-2.10) -0.119 (-1.55)

Connecting -0.018 (-1.62) -0.015 -(1.35) -0.017 (-1.85)

1st quarter

effect 0.033 (5.52)

2nd

quarter

effect 0.049 (9.57)

3rd

quarter

effect 0.052 (10.24)

R-sq 0.27

0.25

0.27

Observations 971,286

907,955

3,985.919

41

Table 7B

Changes in market share and traffic on routes affected by the Bond Amendment

American Southwest Remaining Combined

Traffic

Q3,04 – Q3,05 87% 4% 9% 489,980

Q1,06 – Q4,06 66% 32% 2% 751,620

Source: Author’s calculation from Databank 1B

42

Table 8

Reform-Act Regression results for three different time frames to airport and metropolitan destinations

Dependent: Ln Fare Treatment=25 airport destinations Treatment=25 metropolitan destinations

Before/After time length 1 quarter 1 year 5 years 1 quarter 1 year 5 years

Ln Distance 0.43*** 0.44*** 0.42*** 0.43*** 0.44*** 0.42***

(0.05) (0.04) (0.04) (0.05) (0.04) (0.04)

Ln HHI metro (0.16) 0.04 0.13*** -0.14 0.03 0.13***

(0.08) (0.03) (0.04) (0.08) (0.04) (0.04)

GDP - 0.34* 0.03 - 0.35* 0.03

(.) (0.15) (0.09) (.) (0.15) (0.09)

Ln Population - - - - - -

(.) (.) (.) (.) (.) (.)

Slot dummy -0.06*** -0.04*** -0.05*** -0.06*** -0.04*** -0.05***

0.00 0.00 0.00 0.00 0.00 0.00

Hub dummy 0.18*** 0.18*** 0.12*** 0.18*** 0.18*** 0.12***

(0.02) (0.02) (0.02) (0.02) (0.02) (0.02)

Roundtrip dummy -0.12*** -0.12*** -0.12*** -0.12*** -0.12*** -0.12***

(0.01) (0.01) (0.01) (0.01) (0.01) (0.01)

Q1 dummy -0.05** 0.00 0.01*** -0.02 0 0.01***

(0.01) (0.01) 0.00 (0.01) (0.01) 0.00

Q2 dummy - 0.04*** 0.02*** - 0.04*** 0.02***

(.) (0.01) 0.00 (.) (0.01) 0.00

Q3 dummy - 0.04*** 0.02*** - 0.04*** 0.02***

(.) (0.01) 0.00 (.) (0.01) 0.00

Time dummy - -0.02 0.13*** - - 0.15***

(.) (0.01) (0.02) (.) (0.01) (0.02)

Time*Treatment -0.16*** -0.13*** -0.11*** -0.17*** -0.12*** -0.13***

(0.03) (0.03) (0.03) (0.03) (0.02) (0.02)

Observation 1,005,367 4,259,388 19,992,921 1,005,367 4,259,388 19,992,921

R-squared 0.07 0.06 0.06 0.07 0.06 0.06

* p<0.05, ** p<0.01, *** p<0.001

Note 1: Robust standard clustered errors are reported.

43

Note 2: Hausman test rejects the random effects model

44

Chapter 2: The Effect of Bankruptcy on Productivity in the Airline Industry

1. Introduction

Rising costs due to over expansion and increasing input prices combined with stagnant

revenue growth due to market competition is a theme that has plagued the U.S. airline industry

ever since deregulation in 1978. The vulnerable states of the biggest airlines manifest themselves

in waves of bankruptcies during economic downturns. The latest of such waves occurred from

2002 to 2007 following the recession caused by the tech-bubble and the September 11 attacks.19

During that time, four of the seven largest airlines in the country filed and were approved for

Chapter 11 reorganization bankruptcy protection plans.20

In the last decade, the majority of firms in the airline industry have gone through a

bankruptcy procedure. Every time an airline announces a bankruptcy, it cites the reason is to

become a more competitive and leaner organization.21

Can airlines really become more

competitive and efficient by declaring a bankruptcy? It is evident that at least in the short to

medium term the airlines reduce their costs (Government Accountability Study (2005)) by

getting out of contracts and renegotiating better terms through means of leveraging their

bankruptcy status. However, airline could benefit greatly in the long run from improvement in

efficiency and productivity rather than a mere short term cost reduction. Ultimately, increased

productivity of an organization is what surviving amid competition demands in the long term.

Judging from the industry’s fragile state, this paper hypothesizes that bankruptcies do not

19

The first wave took place just after the deregulation in the 80s. The second wave took place after the 1990

recession and the gulf war in 1991 that hurt air travel. 20

TWA in 2001, US Airways in 2002, United Airlines in 2003, Delta Air Lines and Northwest Airlines in 2005. 21

“US Airways Enters bankruptcy to emerge as a leaner, more competitive airlines” (http://www.usairways.com/en-

US/aboutus/pressroom/history/chronology.html); “AMR Files for Bankruptcy to Achieve Industry Competitiveness”

(http://www.aa.com/i18n/amrcorp/newsroom/fp_restructuring.jsp)

45

improve airline productivity and aims to empirically test this hypothesis using multiple cases of

airline bankruptcies.

Indeed, some industry insiders claim that Chapter 11 protection does not help firms

become more productive in the long run.22

Such claims are not without merit given the behavior

of repetitively declaring bankruptcy is observed. For instance, Trans World Airlines (TWA) went

into bankruptcy in 1992, 1995 andother one again in 2001. Also, U.S. Airways came out of

bankruptcy in 2003 only to go back in 2004. It could be that airlines simply use bankruptcy

protection to get out of unpleasant financial obligations and that is all. That, of course, is not

desirable market equilibrium for the long term as the inefficient incumbents remain by declaring

bankruptcy over and over again whenever they are under financial stress. Of course, as long as

there are enough lenders who are willing to keep the fund flowing into the airline industry

regardless of its state, airlines can maintain their status quo and simply keep declaring

bankruptcy. From the policy side, it becomes a question of how the bankruptcy courts can go

about imposing requirements as far as productivity and efficiency improvements go to ensure

that the bankrupt airlines are not simply “gaming” the system and that they are actually

becoming better organizations as a whole. Hence, this paper sets out to empirically determine

what happens to an airline’s overall productivity when it goes through a bankruptcy protection.

This paper uses bankruptcies of four legacy airlines to examine the effect of bankruptcy

on airline productivity. I use quarterly input and output data for each airline and use them to

22

“What is wrong with Chapter 11? It may keep ailing businesses going, but it distorts the airline industry: Chapters

11 businesses end up with unfair competitive advantages over competitors, thanks to their ability to renegotiate

contracts, cut costs and dump debts.” A quote by Simon Wilson in MoneyWeek, Dec 12, 2005.

46

create the total-factor-productivity index for each airline. After running fixed-effects regressions,

I find that bankruptcy does not improve productivity.

The paper is organized as follow. Section 2 looks at the literature on the subject of

bankruptcy and productivity in the airline industry. Section 3 discusses source of data and

provides a summary of descriptive statistics. Section 4 provides discussion on bankruptcies in the

airline industry since the deregulation. Section 5 elaborates on the ways in which productivity

can be measured. Section 6 discusses the econometric method used for identifying the effect of

bankruptcy on productivity. Section 7 covers regressions results and Section 8 provides

concluding remarks.

2. Literature Review

Many articles on the topic of bankruptcy in the airline industry exist where the focus is

mainly on the effect of bankruptcy on pricing, quality or capacity. Many articles also involve

various aspects of airline productivity, but none involve bankruptcy effects. The following

section provides a brief summary of the literature in bankruptcy and productivity respectively.

Bankruptcy and financial stress literature concerning the airline industry:

Borenstein and Rose (1995) focus on airline bankruptcies between 1989 and 1992 to

examine the effect of bankruptcy on pricing behavior. Their study finds that bankrupt airlines do

not change their own price dramatically and do not force competitors to reduce their price.

Borenstein and Rose (2003) look at whether airline bankruptcies affect supply quantity at the

airport level. The paper finds no evidence of significant effects of bankruptcy on flight quantity

at large and small airports. The effect on medium sized airports was small. The government

Accountability Office (2005) study investigates the effect of bankruptcy on aggregate costs of

47

airlines. The study determined that only some were able to reduce costs while others could not.

Hofer (2009) finds that financial distress causes airlines to reduce prices based on lowered costs

and demands. Waite (2009) focuses on airline bankruptcy and contracts between airlines and

airports to discover that airlines use bankruptcy status to avoid airport fees while continuing to

use airport facilities. Jayanti (2009) finds that airline bankruptcies result in decreasing own

market share and increasing rivals market presence. Lee (2010) finds that LCC capacity grew by

16% as legacy carriers when legacies reduce their capacity while undergoing a bankruptcy

procedure. Ciliberto and Schenone (2012a) find that bankrupt airlines on average drop 25% of

their pre-bankruptcy capacity. In addition, Ciliberto and Schenone (2012b) find that service

quality increases during bankruptcy and return to pre-bankruptcy lower levels once airlines exit

bankruptcy status.

Airline productivity literature:

The literature on the topic of airline productivity is rich. Caves et al. (1982a) was one of

the first studies to look at productivity aspect of the airline industry using the Total Factor

Productivity (TFP) indexing method. A more detailed look into this method comes in Section 5

as this section will provide findings of empirical productivity studies. Cave et al. (1982b), using

TFP, produces a comparison of airline industry productivity between 1970-1975 and 1976-1980.

They find that airline industry productivity increased by about 80% between those two periods.

Windle (1991) compares productivity of global airlines. The study uses TFP methodology to

determine that US airlines were 19% more productive than European airlines, but Asian airlines

were 45% more productive than US airlines in 1983. Good et al. (1993) conducts productivity

comparisons of eight US airlines to four European airlines from 1976 to 1986 and determines

that while the productivity growth rate between 1976 and 1986 were almost identical between

48

US and European carriers, US carriers were more productive. Distexhe and Perelman (1994)

finds that the biggest carriers, on a global scale, were better positioned to take advantage of

technological development and in turn showed more technical efficiency than the others between

1977 and 1986. Oum and Yo (1997) provide an extensive study of productivity and cost

competitiveness of world airlines employing the TFP index methodology. Ng and Seabrigth

(2001) perform productivity comparison of twelve European and seven major US airlines to find

that state ownership has a large impact on costs. Specifically the study finds that privatization

could reduce costs by as much as 20% for European airlines. Oum, et al. (2001) shows that

horizontal alliances of international airlines induce a significantly positive effect on productivity,

but there was no effect on profit. Swelbar (2007) compares partial productivity of legacy and low

-cost carriers US carriers from 1995 to 2006. The study shows that both aircraft and employee

productivity for legacy carriers declined sharply for three to four years and began improving

while low cost carrier partial productivity kept steadily increasing. Mark Greer (2008) looks at

changes in productivity of major US airlines from 2000 to 2004 using the Malmquist

productivity index, which is the same as the TFP index used in Caves et al. (1982), and finds that

there was significant improved in productivity during this period. The study discusses the overall

productivity trend in the industry from 1970 to 1980.

The main findings of the above studies were that over the years airlines’ productivity

have been increasing significantly as output grew much faster than input.

3. Data

The data for this study come from several different sources. The final database includes

detailed domestic US airline data on input/output quantity, cost/revenue statistics and market

concentration data for 11 airlines in Table 3.1 from 1992 to 2011 on quarterly basis. The

49

procedure for selecting these airlines is related to finding airline bankruptcy cases where pre and

post-bankruptcy data were available and determining suitable control group airlines for each

instance. This procedure is discussed in detail in Section 4. All data used in this study only

include the domestic portion of the 11 airlines.

The first part of the database consists of constructing necessary data for calculating the

TFP index and partial productivity ratios both of which come from the Department of

Transportation Form 41. Form 41 is a financial reports data where air carrier submit detailed

revenue, cost and operational statistics to the Department of Transportation. The TFP index uses

four input (labor, fuel, aircraft and miscellaneous) and three output (revenue passenger mile,

revenue-ton mile and incidental) to calculate productivity. As such, detailed database containing

both quantities of input/output components and respective dollar amount spent/earned on them

was assembled on quarterly basis between 1992 and 2011.

Input data: The quantitative part of the input index includes data on the number of

employees, gallons consumed for fuel and the average number of aircraft. Data on miscellaneous

quantity of inputs (all other material input besides aircraft and fuel such as amount of passenger

meals, various equipment, etc.) is not available. Instead, the miscellaneous material quantity

index was calculated by dividing miscellaneous materials cost by the quarterly US GDP deflator

as done in Oum, et al. (2001). The cost sharing part includes data on labor cost, fuel cost and

aircraft cost. Miscellaneous was cost was calculated by subtracting the previous three main costs

from total cost. The cost-share part of the input data was available from Form 41 on a quarterly

50

basis. It includes the dollar amount spent on labor, aircraft and fuel. The material cost (or

miscellaneous cost) was computed by subtracting labor, aircraft and fuel cost from Total Cost.23

Output data: The quantitative section of the output index includes revenue passenger

miles, revenue-ton miles and miscellaneous revenue earning quantity index (such as baggage

fees, meal service, etc.). While the former two are available, the miscellaneous revenue earning

quantity index is not available. Instead, it was replaced by an index computed by dividing

miscellaneous revenue by the quarterly US GDP deflator as was done previously. The revenue-

share section of the output index was computed by dividing each of ticket sale revenue, mail and

freight revenue and incidental revenue by the total revenue.

Once the output and input data indexed are calculated, the TFP index is calculated by

dividing output by input. Table 3.2 illustrates a sample of input, output and TFP index data.

The second part of the database consists of creating the independent variable data. The

data for fleet size, fleet age and fleet type were calculated come from Department of

Transportation’s data on airline fleet statistics section from its website which is available only

post 1992. Quarterly data for stage length and load factor come from Form 41. Quarterly GDP

growth and GDP deflator data were collected from the U.S. Bureau of Economic Analysis. The

quarterly HHI index, market share and network size for each airline was computed from

Databank 1B, the U.S. Department of Transportation’s Ticket Origin and Destination Survey, on

quarterly basis.

23

Total Cost and Total Revenue excludes Transport Related Costs and Transport Related Revenues. Transport

related revenues/costs report the amount earned/spent from purchasing airline service from regional feeder airlines

and thus do not directly take part in an airline’s own production of goods and services.

51

The finished database consists of an unbalanced panel consisting of 612 combined

observations where each observation is quarter-carrier unique data consisting of ln(TFP) as the