Embed Size (px)

Citation preview

JKAU: Islamic Econ., Vol. 34 No. 1, pp: 25-43 (January 2021)

DOI:10.4197/Islec.34-1.2

25

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan

Ejaz Aslam

Assistant Professor and researcher at the School of Islamic Economics Banking & Finance, Minhaj University Pakistan

Khuram Mobusher Azam

Credit Manager, Habib Bank Ltd., Pakistan

Anam Iqbal

PhD scholar at IIUM Institute of Islamic Banking and Finance International Islamic University Malaysia

ABSTRACT. Ṣukūk is an innovative financial instrument with a flexible structure based

on Sharīʿah, unlike a bond which is based on an interest-based structure. With the

notion that ṣukūk contracts are significantly different from ordinary bonds, it is in high

demand especially in Muslim countries to overcome liquidity problems. Ṣukūk has a

key importance in the financial market, and literature is lacking on how to predict the

trend and volatility of ṣukūk in the case of Pakistan, where debt instruments are high in

demand. Thus, this investigation intends to inspect the volatility and trends analysis of

the ṣukūk industry in Pakistan. The study sample consists of six ṣukūk issued in

Pakistan, for which the daily data was collected. For this purpose, this study employed

the ARCH, GARCH, EGARCH, and TGARCH models to analyze the risk behavior of

the ṣukūk industry in Pakistan. Results revealed that Engro Corporation ṣukūk yield is

higher and less volatile among other ṣukūk returns. The results testify that there is

volatility in all corporate ṣukūk returns of different maturities. Additionally, it is found

that smaller tenure ṣukūk had high volatility as compared to larger tenure ṣukūk, and

that bad news and events have larger effects on volatility of the ṣukūk return than good

news. The findings of this study shall be beneficial for investors, portfolio managers,

and decision-making authorities to invest in the low-risk profile ṣukūk as debt

instruments in Pakistan.

KEYWORDS: ARCH, GARCH, Islamic finance, Ṣukūk, Volatility.

JEL CLASSIFICATION: G02, G14, P51

KAUJIE CLASSIFICATION: K16, I10

26 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

1. Introduction

Shortage of money is the major issue faced by gov-

ernments and corporate bodies all over the globe. To

overcome the issue of shortage of money, the finan-

cial bodies massively borrow to amass their required

capital expenditures (Shiau, Chang, & Yang, 2018, p.

176). Since the last two decades, Islamic certificates

have been used extensively as a prolific alternative to

conventional bonds, especially in Muslim majority

countries because of its unique nature and resilience

to alleviate liquidity problems. Thus, Islamic certifi-

cates (ṣukūk) are based on Islamic rules, which pro-

hibit ribā, gharar, and other attributes that exploit

and/or undermine the rights of any party involved

(Salman, Amjad, & Aslam, 2017, p. 8; Smaoui,

Mimouni, & Temimi, 2020, p. 807).

The development of ṣukūk in financial markets

was seen as an opportunity to provide new financing

and investing dimension for corporates and investors,

respectively. Thus, ṣukūk was considered as an alter-

native to other long-term funding and investing op-

tions (Nasir & Farooq, 2017, p. 375). Ṣukūk’s struc-

ture is based on Sharīʿah, and it could be used for the

establishment of Islamic economies in society (Alam,

Bhatti, & Wong, 2018, p. 665). Usmani (2007, p. 3)

documented that there is a need to strictly evaluate

the development of ṣukūk structure in concurrence

with the fundamental principles of the Islamic eco-

nomic system which distinguish it from the conven-

tional system.

Ṣukūk is a financial instrument which represents

the ownership of an underlying real/tangible asset to

its holder and is considered as an alternative for tradi-

tional bonds. It is based on Islamic law which allows

the sale or lease of an actual asset; and the generated

income is considered a form of profit on sale or rent-

als for a lease on assets (Smaoui & Ghouma, 2020, p.

807). Additionally, “Investment Sukuk are certifi-

cates of equal value representing undivided shares in

ownership of tangible assets, usufruct and services or

(in the ownership of) the assets of particular projects

or special investment activity” (AAOIFI, 2015, p.

468).

The basic concept behind the issuance of ṣukūk is

to enable the holders of ṣukūk to share in the profits

and revenues of large enterprises, and not just act as

the lender of the fund and collect fix interest pay-

ments. Thus, ṣukūk provides an opportunity to invest

in a Sharīʿah compliant manner and facilitate the

institutions to meet their liquidity problems without

resorting to speculation and resource exploitation as

well as to get an equitable return (Hassan, 2012, p. 1).

Apart from Sharīʿah compliance, Islamic financial

instruments also fascinate as an active business op-

portunity. Therefore, ṣukūk is attracting both Mus-

lims and non-Muslims as a financing and investment

source despite the fact that ṣukūk markets are facing

economic, financial, legal, and regulatory challenges

(Jobst, Kunzel, Mills, & Sy, 2008, p. 341). Perhaps,

ṣukūk has a vital role to play in the development of

the real Islamic banking system, and this will con-

tribute to the achievement of the noble objectives

sought by the Sharīʿah (Usmani, 2007, p. 2).

1.1 Overview of Ṣukūk Market in Pakistan

As per the Securities and Exchange Commission of

Pakistan (SECP)(1)

, a total of ninety-nine domestic

corporate, privately placed ṣukūk had been issued as

of 31st December 2016. The total raised amount was

worth about Rs. 1173.11 billion out of which ṣukūk

of worth Rs. 613.78 billion had been redeemed, and

total outstanding ṣukūk were worth about Rs. 559.34

billion. Among these ṣukūk, Pakistan Water and

Power Development Authority (WAPDA) issued

three ṣukūk till December 2016. The very first ṣukūk,

worth Rs. 8 billion, was issued on 5th January 2006

based on the ijārah ṣukūk, and was issued for a peri-

od of seven years. The second WAPDA ṣukūk was

issued on 13th July 2007. This was based on the di-

minishing mushārakah model, having a worth of Rs.

8 billion, and was issued for a period of ten years.

The third ṣukūk was issued in continuation of the first

ijārah ṣukūk that was redeemed in January 2013.

This ṣukūk was issued on 14th October 2013, having a

worth of Rs. 10 billion, and was issued for a period of

eight years. These ṣukūk were non-listed, and had an

AAA rating by the Pakistan Credit Rating Agency

(PACRA). The securities provided against these

ṣukūk were twelve power generation turbines at the

Mangla & Tarbela Power Station.

(1) www.psx.com.pk

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 27

Karachi Electric Supply Company Limited (K-

Electric) issued Pakistan’s first listed ṣukūk named

AZM ṣukūk that provided a rate of return and flexible

options like early purchase/redemption option, and

was traded in all three stock exchanges of Pakistan.

The AZM ṣukūk had a rating of A+ by the JCR-VIS

credit rating company and the Islamic International

Rating Agency. This ṣukūk was utilized to meet the

working capital requirement of K-Electric. The secu-

rities provided against these ṣukūk were the forty-

seven grid stations of the company. Moreover, Engro

Corporation Ltd. issued two ṣukūk named Engro Is-

lamic Rupiya-1 and Engro Islamic Rupiya-2 that had

a tenure of three and five years, respectively. The

instrument rating was AA and entity rating AA- is-

sued by PACRA. The amount raised from Engro

Islamic Rupiya-1 was Rs. 3 billion at 13% expected

annual rate of return. While Engro Islamic Rupiya-2

raised Rs. 1 billion, with 13.5% expected annual rate

of return.

The present research evaluates the risk and trend

analysis of the ṣukūk market in Pakistan. The more

significant part of the previous literature used theoret-

ical justification and trend analysis to justify their

idea. Thus, the present research tests their proposed

hypotheses by using the autoregressive conditional

heteroscedasticity (ARCH) and the generalized auto-

regressive conditional heteroskedasticity (GARCH)

approaches, utilizing ṣukūk data in Pakistan.

Pakistan is a developing country, and its bond

market is less productive when contrasted with its

financial exchange and debt base instruments like

bonds that depend on bank borrowings to fund their

operations (Ghafoor, Saba, & Kouser, 2018, p. 161).

Therefore, ṣukūk is considered as the best alternative

which provides more return at low risk as compared

to conventional bonds. Thus, the outcome of this

research can stretch positive ramifications to both the

debtor and the creditor, particularly in Pakistan.

This study consists of five sections. After the in-

troduction, the next section discusses the available

literature on ṣukūk and its background in Pakistan.

The third section explores the methodology, while

section four presents and discusses the results of this

study. In the last section, the conclusion and limita-

tions of this research are presented.

2. Literature Review

Ṣukūk has an alternate structure and arrangement

from regular bonds (Abdul Rauf & Ibrahim, 2014, p.

146). It is a certificate of trust that represents the fi-

nancial ownership in an underlying asset, for exam-

ple, processing plant inventories, vehicles, specula-

tion venture like property advancement projects,

hydropower projects, and motorways projects (Lah-

sasna & Lin, 2012, p. 496). Moreover, it gives the

premise of Islamic financial framework, which de-

pends on an impartial conveyance of riches, risk-

reward sharing, and riches fixation (Bhuiyan, Puspa,

Saiti, & Ghani, 2020, p. 1251). However, in compari-

son with customary bonds, ṣukūk is considered a

diverse mode of financing (Hassan, 2012, p. 4).

Some of the researchers contended that both

ṣukūk and ordinary bonds are similar. For example,

Miller, Challoner, and Atta (2007, p. 24) mention that

ṣukūk are structured such that they offer similar prof-

its as conventional bonds. Similarly, Ahmad and

Abd. Rahim (2014, p. 278) believe that ṣukūk reflect

ordinary bonds, particularly for financial specialists

who are unfamiliar with the investment.

However, on the other hand, some researchers be-

lieve that ṣukūk offer particular and interchange secu-

rity to customary bonds, particularly regarding risk.

For instance, Godlewski, Turk-Ariss, and Weill

(2013, p. 746) considered the declaration impacts of

the issuance of Islamic and ordinary bonds. They

utilized an occasion study system and inferred that

the market did not respond as much towards the issu-

ance of the traditional securities.

In this regard, Tariq and Dar (2007, p. 221) put

forth their attempts to discover the risk associated

with the fundamental structure of ṣukūk. They at-

tempted to relieve these risks with the assistance of

ideas and endorsements. They examined the develop-

ment of ṣukūk, their underlying principals, structures,

risks, and competitiveness versus the traditional bond

framework. Thus, they found that ṣukūk provides

motivating forces and strength to money related mar-

kets and result in asset deployment to both the private

and public sectors.

Abdul Rauf and Ibrahim (2014, p. 145) identified the risk embedded in ṣukūk structure and determined a positive relationship between risk and ṣukūk return.

28 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

Similarly, Kostandyan (2015, p. 36) concludes ṣukūk to be an advantageous part of the portfolio in diversi-fying risk in the case of Bahrain, Pakistan, Qatar, Malaysia, and the UAE.

Ariff and Safari (2012, p. 101) noted that ṣukūk securities yield was different from the traditional bond yield, though the tenure of issue and issuer of securities was the same. The mean yield of ṣukūk securities was drastically different from the conven-tional bond, and with some exceptions, there was no causal relationship between these two debt instru-ments.

Abdalla and Winker (2012, p. 166) studied the trend of investment bonds (IBs) of different maturi-ties by employing the ARCH and GARCH model to measure the volatility. They observed that investors were taking a higher profit/loss on their investment in the five years IBs due to their high volatility. Where-as ten years maturity IBs returns volatility was in between the volatility of IBs with five years and three years maturity. Al-Amine (2011, p. 344) documented that any positive change in the interest rate resulted in a decrease in the fixed return ṣukūk values. Fathu-rahman and Fitriati (2013, p. 162) studied the yields of conventional coupon payment bonds and ṣukūk listed on the Indonesian stock market. Their findings showed that the yield on ṣukūk was different from the yield of conventional bonds. Additionally, the yields on ṣukūk were more massive than the yield on tradi-tional bonds in at least three of the ten groups studied. Similarly, Bhuiyan et al. (2020, p. 1245) documented that ṣukūk risk is lower than the risk in bond.

Raees, Raheem, and Zakir (2017, p. 103) noted that knowledge and Islamic spirit have a positive relationship with investment in ṣukūk. Nagano (2017, p. 142) stated that ṣukūk is utilized more when firms experience high data asymmetry and have a large funding demand. Zulkhibri (2015, p. 239) stated that lack of harmonization, fewer markets, non-active trading, lack of regulatory support, and different Sharīʿah interpretations are the main constraints to investment in ṣukūk. Nasreen, Naqvi, Tiwari, Ham-moudeh, and Shah (2020, p. 17) mention in their study that VAR analysis demonstrates that benefits from the Islamic assets portfolio vary within the time/scale. Al-Swaidan, Daynes, and Pasgas (2017, p. 389) documented that ṣukūk risk profiles are di-rectly related to ṣukūk structures.

Abd. Rahim and Ahmad (2015, p. 581) estimated

volatility of ṣukūk using Moving Centerline Expo-

nentially Weighted Moving Average (MCEWMA)

volatility forecasting model applied to get the daily

return information about the ijārah ṣukūk issuance

from 2008 to 2011. They found that bootstrap meth-

ods of MCEWMA perform better to evaluate the

ṣukūk issuance volatility. Maghyereh and Awartani

(2016, p. 252) compare the ṣukūk and bond based on

return and volatility with equities. They observed that

ṣukūk have higher returns and standard deviation as

compared to world bond index. Malikov (2017, p.

34) concludes that sovereign ṣukūk issuances have a

positive impact on the economic development of

Malaysia and Saudi Arabia.

Ariff and Safari (2012, p. 103) examined the av-

erage yields of ṣukūk and ordinary bonds traded in

Malaysia and observed that yields for ṣukūk are high-

er as well as that ṣukūk with low tenure maturity re-

main more volatile. Likewise, Saeed and Izzeldin

(2016, p. 150) inferred that dissimilar to common

bonds, the exchange off among risk and proficiency

does not exist in Islamic bonds, for example, ṣukūk.

Meanwhile, El Mosaid and Boutti (2014, p. 226)

found that the ṣukūk index outperforms the bond and

market index. The outcomes likewise affirmed a

positive and noteworthy correlation among ṣukūk and

bond portfolios, proposing that ṣukūk does not con-

trast from regular bonds as far as their Sharīʿah struc-

ture is concerned.

As aforesaid, the discussion and/or study of the

risk and return of ṣukūk is an important issue. There-

fore, it is interesting to explore further the volatility

and trends of the ṣukūk industry in Pakistan. Thus,

the proposed research hypotheses of the present study

are constructed as follows:

H1: Yield of Engro Corporation ṣukūk is higher than

the yield of other ṣukūks in Pakistan.

H2: Returns of different maturities corporate ṣukūk

are volatile.

H3: There exists a clustering effect in all corporate

ṣukūk returns of different maturities.

H4: Corporate ṣukūk, which have a short maturity

period/tenure have high volatility.

H5: GARCH effect exists in all corporate ṣukūk returns.

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 29

3. Methodology

To achieve the objective of the study, data of the

daily market prices of six ṣukūk index of different

maturities is selected from the period 2006-2016 in

Pakistan. This time period is selected in order to col-

lect a reasonable number of ṣukūk instruments and

their trading to compare the ṣukūk based on the same

credit rating and maturity period of the financial in-

struments. Thus, the present study selected WAPDA,

K-Electric and Engro Corporation ṣukūk across three

years, five years, eight years, and ten years maturity

periods because it is available in the Pakistan Stock

Exchange (PSX) database. The choice of our sample

is motivated by the availability of statistical data and

the difficulty of accessing databases that provide a

wide range of index types. The present study em-

ployed the Augmented Dickey-Fuller test to identify

the stationarity in data and autoregressive conditional

heteroscedasticity (ARCH) and its variants; general-

ized autoregressive conditional heteroscedasticity

(GARCH); exponential generalized autoregressive

conditional heteroscedasticity (EGARCH); and

threshold generalized autoregressive conditional het-

eroscedasticity (TGARCH) model, in order to cap-

ture volatility clustering, volatility persistence and

asymmetric effect of ṣukūk in Pakistan (Agwu &

Godfrey, 2019, p. 268; Maqsood, Safdar, Shafi, &

Lelit, 2017, p. 373). This research used a parametric

approach to measure the current period yield, which

is calculated with the help of the below-mentioned

equation (1).

Current yield =𝐹 × r

𝑃 (1)

Where F is the face value of the ṣukūk, r is the cou-

pon rate, and P is the selling price/current price in the

market.

Whereas yield to maturity is calculated with the

help of the below-mentioned formula. The returns are

derived from the yield of ṣukūk in equation 2. The

return of t day is derived from the difference in yield

of t day minus the yield of t-1 day. The formula for

calculation of return is given below.

Ṣ𝑢𝑘ū𝑘 Return (Rt) = Yt - Yt−1 (2)

ARCH model was developed by Engle (1982).

ARCH models are used for financial time series with

time-varying volatility, such as bond returns. For

modelling the volatility, this model is very helpful

and describes volatility as a function of the error

term. These errors occur due to the shocks or news by

financial analysis in the financial market. These

shocks may be of positive or negative nature depend-

ing on the good news or bad news. According to this

model, the larger the shock, the greater will be the

volatility. Thus, before applying the model and its

variants, there should be clustered volatility in the

variance, and there should be heteroskedasticity in

the residuals of the ṣukūk return data (Maqsood et al.,

2017, p. 376). ARCH model is given below in equa-

tion 3.

t2 = + 2

t-1 + t (3)

A generalized autoregressive conditional heterosce-

dasticity (GARCH) model was developed by

Bollerslev (1986). This model captures the long-

legged effects in the shocks with few parameters; this

made it popular among the experts. The GARCH

model is presented in equation 4.

σ2t = ω + α σ

2t – 1 + β ε

2t – 1 (4)

An exponential GARCH (EGARCH) model was

proposed by Nelson (1991). This model was particu-

larly formulated to allow asymmetric effect between

positive and negative return. The EGARCH model is

presented in equation 5.

𝑙𝑛𝜎𝑡2 = 𝜔 + ∑ 𝛼𝑖

𝑞𝑖=1 [|

𝜀𝑡−1

𝜎𝑡−1|] + ∑ 𝛽𝑖

𝑝𝑡=1 𝑙𝑛(𝜎𝑡−1

2 ) +

∑ 𝛾𝑖𝑞𝑡=1

𝜀𝑡−1

𝜎𝑡−1 (5)

Threshold GARCH (TGARCH) model was present-

ed by Glosten, Jagannathan, and Runkle (1993). The

equation of the TGARCH model is given in equation 6.

𝜎𝑡2

= 𝜔

+ ∑ 𝛼𝑖𝜀𝑡−12

𝑞

𝑖−1

+ ∑ 𝛼𝑖𝜎𝑡−12

𝑝

𝑖−1

+ ∑ 𝛾𝑖𝜀𝑡−12

𝑞

𝑡=1𝐼𝑡−1 (6)

Where σ2t symbolizes the conditional variance that is

the measure of volatility, conditional variance sug-

gests that the forecast of variation in period t is based

on the previous values of variables. ω denotes the

intercept. It−1=1, if εt−1 < 0, otherwise It−1 = 0,

30 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

and γi is the parameter of leverage effect. The value

of conditional variance will be positive even if the

parameters are negative because it models the log of

conditional variance. σ2t – 1 is the GARCH term that is

prior to conditional variance. ε2t – 1 is the ARCH term

that is the squared error term from the previous peri-

od, whereas α and β are the coefficients.

4. Results and Discussions

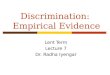

4.1 Ṣukūk Yield

First and foremost, the present study graphically de-

scribes the data to show the behavior of ṣukūk yield

and return in Pakistan. Thus, figure 1 shows the yield

of eight- and ten-year maturities of WAPDA ṣukūk,

and three- and five-years maturities of K-Electric and

Engro ṣukūk. There was a continuous fluctuation and

downward trend in all ṣukūk except the three-year

maturity Engro Corporation ṣukūk yield. Due to the

changing trend, the graph is considered as nonlinear.

The downward trend can be seen from Jan 2014 to

May 2015 in the yield of eight-year maturity

WAPDA ṣukūk that decreased from 12% to 9%, and

after that, from May 2015 to January 2016 the yield

was moderately stable at 9% approximately. While

the yield of ten-year maturity WAPDA ṣukūk re-

mained between 10%-11% from Jan 2014 to Nov

2014, but after November 2014 till May 2015 the

yield of ten-year WAPDA ṣukūk dropped to 7% and

then after that from May 2015 to Jan 2016, it re-

mained at 7% approximately.

The downward trend can also be seen from Octo-

ber 2014 to May 2015 in the yield of three-year ma-

turity K-Electric ṣukūk that decreased from 12% to

9% approximately, and after that from May 2015 to

Aug 2015, it was moderately stable at approximately

9%. From August 2015 to January 2016, it decreased

to almost 8.5%. The same trend was found in the

yield of five-year maturity K-Electric ṣukūk. From

October 2014 till May 2015, the yield of five-year

maturity K-Electric ṣukūk dropped to 9% and then,

after that from May 2015 to January 2016, it re-

mained at approximately 9% with minor fluctuations.

Additionally, the downward trend can be seen

from October 2014 to April 2015 in yield of three-

year maturity Engro ṣukūk that decreased from

12.5% to 11.75% approximately, and after that from

May 2015 to January 2016, it increased and reached

almost 12.25%. While the yield of five-year maturity

Engro Corporation ṣukūk rose from 12.5% to 13%

from Oct 2014 to May 2015, and after May 2015 till

Aug 2015 the yield dropped by approximately 1%.

However, it recovered from Aug 2015 to Dec 2015,

but it again declined, and at the end of Jan 2016 the

yield of five-year Engro ṣukūk was 11.25% approxi-

mately. It can be seen from figure 1 that the yield of

both Engro Corporation ṣukūk are higher than the

yield from K-Electric and WAPDA ṣukūk due to the

high rate of return offered by the organization. There-

fore, we accept H1 that the Engro Corporation ṣukūk

yield is higher than the other ṣukūk of the study.

Figure (1) Line Graph of Ṣukūk Yield

Line graph of ten- and eight-year WAPDA sukuk yield

0.0000

2.0000

4.0000

6.0000

8.0000

10.0000

12.0000

14.0000

Yie

ld

10 Year

WAPDA

Sukuk Yield

8 Year

WAPDA

Sukuk Yield

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 31

Line graph of three- and five-year K- Electric sukuk yield

Line graph of three- and five-year Engro Corporation sukuk yield

Source: Developed by authors (results exacted from Microsoft Excel)

4.2 Ṣukūk Return

Figure 2 shows the first difference in the yield data

of all six ṣukūk. It can be viewed that all ṣukūk re-

turn series are stationary, while the spikes in the

graph indicate the high volatility in the data. The

graphs show, as in case of WAPDA ten-year ma-

turity ṣukūk, for the first 150 days, a period of low

volatility, followed by a period of high volatility

from 200 to 340 days, then there are periods of low

volatility from 340 to 399 days, followed again by

some period of high volatility and then a period of

0.0000

2.0000

4.0000

6.0000

8.0000

10.0000

12.0000

14.0000

Yie

ld

3 Year K-

Electric-

Sukuk Yield

5 Year K-

Electric-

Sukuk Yield

10

10.5

11

11.5

12

12.5

13

13.5

Yie

ld

3 Year Engro

Corporation

Sukuk Yield

5 Year Engro

Corporation

Sukuk Yield

32 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

low volatility. Hence, volatility clustering gives the

reason of applying ARCH, GARCH, EGARCH,

and TGARCH models. Similar is the case of the

remaining ṣukūk that also show the same pattern of

clustering. The graphs show that the eight-year ma-

turity ṣukūk return is more volatile than any other

ṣukūk in this study. The figure also verifies the yield

trend that was downward, by showing that majority

of the return as negative due to the downward trend

in the pricing of the instrument except for the three-

year maturity Engro corporation ṣukūk.

Figure (2) Line Graph of Ṣukūk Return

-.5

-.4

-.3

-.2

-.1

.0

.1

.2

.3

50 100 150 200 250 300 350 400 450

RETURNWAPDA8

-.5

-.4

-.3

-.2

-.1

.0

.1

.2

50 100 150 200 250 300 350 400 450

RETURNWAPDA10

-.6

-.5

-.4

-.3

-.2

-.1

.0

.1

.2

25 50 75 100 125 150 175 200 225 250 275 300

RETURNKE3

-.6

-.5

-.4

-.3

-.2

-.1

.0

.1

.2

.3

25 50 75 100 125 150 175 200 225 250 275 300

RETURNKE5

-.20

-.15

-.10

-.05

.00

.05

.10

.15

25 50 75 100 125 150 175 200 225 250 275 300

ECL3

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

25 50 75 100 125 150 175 200 225 250 275 300

ECL5

Source: Results extracted from EViews 8 software.

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 33

4.3 Stationarity, Autocorrelation, and Hetero-

scedasticity Test

In order to analyze the volatility in ṣukūk, this study

first verifies the stationary in data by using the

Augmented Dickey-Fuller (ADF) test. Table 1

shows that the p-value of the ADF test is significant

in all series; thus, we reject the null hypothesis of a

unit root. This signifies that stationarity exists in all

series of ṣukūk. In order to test the presence of auto

correlation, this study employed the Durbin Watson

test, which is also presented in Table 1. All Durbin

Watson values are near to 2, so there is no issue of

autocorrelation (Gujarati & Porter, 2009. p. 436).

Moreover, Lagrange Multiplier (LM) is used to ex-

amine whether the standardized residuals show

ARCH behavior. The results of the LM test, pre-

sented in table 2, evidently show that the variance of

the returns of ṣukūk is non-constant for all periods

specified.

Table (1) Unit Root and Autocorrelation Test

Time Series Test Statistics P-Value Critical values Durbin

Watson

test 1% 5% 10%

WAPDA 8 -24.75563 0.0000 -3.4433 -2.8671 -2.5698 2.052

WAPDA 10 -22.63298 0.0000 -3.4433 -2.8671 -2.5698 2.126

K-Electric 3 -19.41356 0.0000 -3.1212 -2.1322 -2.4321 1.953

K-Electric 5 -18.06651 0.0000 -3.2565 -2.2554 -2.5656 1.976

Engro 3 -17.95931 0.0000 -3.4570 -2.2732 -2.3214 2.043

Engro 4 -17.79921 0.0000 -3.3239 -2.4568 -2.5717 2.011

Source: Estimated by authors.

Table (2) ARCH-LM Test for Different Values of q

Time Series Arch Order 2 Test Statistics TR2 Probability

WAPDA 8 q1 156.952 0.0001

WAPDA 8 q2 226.532 0.0000

WAPDA 10 q1 196.190 0.0000

WAPDA 10 q2 283.165 0.0000

K-Electric 3 q1 166.762 0.0000

K-Electric 3 q2 240.690 0.0001

K-Electric 5 q1 141.747 0.0000

K-Electric 5 q2 204.587 0.0001

Engro 3 q1 120.485 0.0000

Engro 3 q2 173.899 0.0000

Engro 4 q1 148.197 0.0000

Engro 4 q2 213.895 0.0000

Source: Estimated by authors.

There are two preconditions to apply the ARCH

model. First, there should be clustered volatility in

residuals, and second, there should be an ARCH ef-

fect in the residuals. Both conditions were fulfilled in

all the ṣukūk return data incorporated in this study.

Moreover, as shown in figure 3, the p-value of the

heteroskedasticity test of all ṣukūk returns is 0.00,

which is less than 0.05, meaning that ARCH effect

exists. Thus, the ARCH model can be tested on this

ṣukūk return.

34 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

Figure (3) Residual Graph of Ṣukūk Return

Wapda 8

-.6

-.4

-.2

.0

.2

.4

-.6

-.4

-.2

.0

.2

.4

50 100 150 200 250 300 350 400 450

Residual Actual Fitted

Wapda 10

-.6

-.4

-.2

.0

.2

-.6

-.4

-.2

.0

.2

50 100 150 200 250 300 350 400 450

Residual Actual Fitted

KE3

-.6

-.4

-.2

.0

.2

.4

-.6

-.4

-.2

.0

.2

25 50 75 100 125 150 175 200 225 250 275 300

Residual Actual Fitted

KE5

-.6

-.4

-.2

.0

.2

.4

-.6

-.4

-.2

.0

.2

.4

25 50 75 100 125 150 175 200 225 250 275 300

Residual Actual Fitted

ECL3

-.20

-.15

-.10

-.05

.00

.05

.10

.15

-.20

-.15

-.10

-.05

.00

.05

.10

.15

25 50 75 100 125 150 175 200 225 250 275 300

Residual Actual Fitted

ECL5

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

25 50 75 100 125 150 175 200 225 250 275 300

Residual Actual Fitted

Source: Results extracted from EViews 8 software.

In figure 4, the graphs of conditional standard devia-tion and the conditional variance of ṣukūk return are presented. The values of the conditional standard deviation are calculated by taking the square root of the conditional variance. The conditional variance spikes are lesser as compared to the conditional standard deviation graph. Thus, we accept H3

because it clearly shows the presence of variance that shows high volatility clustering in this series. The extraordinary spikes indicate the high volatile periods in the series. Further, it is noted that the values of the ARCH LM test and correlogram for all ṣukūk returns in this study showed that the GARCH (1,1) model is a good model.

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 35

Figure (4) Plot for Conditional Standard Deviation and Conditional Variance of Ṣukūk Return

Wapda 8

.0

.1

.2

.3

.4

.5

.6

.7

50 100 150 200 250 300 350 400 450

Conditional standard deviation

.00

.05

.10

.15

.20

.25

.30

.35

.40

50 100 150 200 250 300 350 400 450

Conditional variance Wapda 10

.0

.1

.2

.3

.4

.5

.6

50 100 150 200 250 300 350 400 450

Conditional standard deviation

.00

.04

.08

.12

.16

.20

.24

.28

.32

50 100 150 200 250 300 350 400 450

Conditional variance KE3

.0

.1

.2

.3

.4

.5

.6

.7

25 50 75 100 125 150 175 200 225 250 275 300

Conditional standard deviation

.0

.1

.2

.3

.4

.5

25 50 75 100 125 150 175 200 225 250 275 300

Conditional variance

36 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

KE5

.0

.1

.2

.3

.4

.5

.6

.7

.8

25 50 75 100 125 150 175 200 225 250 275 300

Conditional standard deviation

.0

.1

.2

.3

.4

.5

.6

25 50 75 100 125 150 175 200 225 250 275 300

Conditional variance ECL3

ECL5

4.4 Analysis and Discussion

The results of the ARCH (1) model in table 3 illus-

trate that all coefficients are positive and statistically

significant at the 5% level. The results indicate that

every past value of ṣukūk returns significantly pre-

dicts the current value of ṣukūk return. Moreover, the

ARCH (1) model results of all ṣukūk are significant

as p-value is less than 0.05, except Engro 5Y, which

did not give a significant result by testing the ARCH

(1) model. Thus, we applied the ARCH (2) model

and results are statistically significant at the 1% level,

in which there are two ARCH terms that explain the

varying volatility of the five years Engro Corporation

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 37

ṣukūk return. The finding clearly establishes the pres-

ence of time-varying conditional volatility of all

ṣukūk returns. Thus, returns of different maturities

corporate ṣukūk are volatile, supporting the findings

of Abdul Rauf and Ibrahim (2014, p. 145). Moreover,

results indicate that the persistence of volatility in

ṣukūk, as represented by the signs of the ARCH and

GARCH parameters (α, β), is large. It denotes that

the effects of today’s shock remain in the forecasts of

variance for many periods in the future.

Table (3) Summary of The Results of ARCH and GARCH Models

WAPDA 10Y WAPDA 8Y K-Electric 3Y K-Electric 5Y ENGRO 3Y ENGRO 5Y

ARCH Effect

0.000396 0.000478 0.003515 0.000487 0.000591 0.000306

0.384722 0.184937 0.128925 0.091033 0.4245 0.004353

(0.0000) -0.0001 -0.0471 -0.0277 -0.0003 -0.7553

0.004494

(0.0000)

GARCH Effect

- 0.000255 - 0.000548 0.000154 0.000931

0.009838 0. 442981 0.008152 -0.011554 -0.020148 -0.008991

(0.0000) (0.0000) (0.0000) (0.0000) (0.0000) -0.0083

β 0.990162 0.290698 0.991848 0.870366 0.745251 0.850294

(0.0000) (0.0000) (0.0000) (0.0000) (0.0000) (0.0000)

E-GARCH Effect

0.001713 0.004166 -0.002089 -0.000621 -0.001448 -0.007837

C4 -0.034036 0.245613 -0.471532 -0.932125 0.151768 -0.164966

-0.7098 (0.0000) (0.0000) (0.0000) -0.0086 -0.0353

T-GARCH Effect

0.014506 0.107648 0.094017 1.076242 0.659524 -0.073835

-0.7722 -0.2082 -0.4117 -0.0032 -0.0012 (0.0000)

γ1 1.11083 1.094793 2.731196 1.404857 -0.017594 0.210222

(0.0000) (0.0000) (0.0000) -0.001 -0.8467 (0.0000)

Source: Estimated by authors.

It is evident from this research that volatility is found

in all different maturities corporate ṣukūk returns,

similar to the finding of Abdalla and Winker (2012,

p. 172). This confirms our hypothesis H2 that there is

volatility in all corporate ṣukūk returns of different

maturities. The WAPDA ṣukūk returns are more vol-

atile as compared to K-Electric and Engro Corpora-

tion ṣukūk returns. The first reason for the volatility

of WAPDA ṣukūk returns is that it has been in the

ṣukūk market for more than a decade, implying that it

is among the pioneers of this sector. Whereas, K-

Electric and Engro Corporation ṣukūk are relatively

new entrants in the market. Secondly, WAPDA

ṣukūk is an AAA rated instrument as compared to

K-Electric, and Engro Corporation ṣukūk, which are

rated AA and A+ respectively.

Furthermore, the rate of return was much higher

in both K-Electric and Engro Corporation, which was

the result of investors retaining their holdings and not

selling their ṣukūk securities, that in turn, ultimately

affects the volatility pattern. Another reason for low

volatility in ṣukūk returns could be that in an Islamic

secondary market, there is no speculation like deriva-

tives, futures, and hedging. This means that there

would be less volatility in this market. The principles

of Islamic economics prohibit any speculation on the

prices, which is for the benefit of the people and to

save them from losses.

38 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

Comparing the volatility of three- and five-years maturity K-Electric ṣukūk returns with three, and five-years maturity Engro Corporation ṣukūk returns, it is discovered that K-Electric ṣukūk returns are more volatile than Engro Corporation ṣukūk returns. As for the K-Electric ṣukūk, the rate of return was varying, as it was linked with the KIBOR, and it was highly traded. However, Engro Corporation ṣukūk was less volatile as compared to WAPDA and K-Electric ṣukūk, because people did not want to sell their ṣukūk due to the higher rate of return offered by the Engro Corporation in the market. Thus, Engro Corporation ṣukūk is best for risk-averse customers who want a safe investment along with high profit.

It is shown that the tenure of ṣukūk affects the volatility of its return, as ṣukūk returns of three-year maturity period are more volatile than the ṣukūk re-turns of five-year maturity. Similarly, ṣukūk returns for eight-years maturity period are more volatile than ṣukūk returns of ten-year maturity. The results sup-port the findings of Ariff and Safari (2012, p. 101), who found that short period maturity ṣukūk are more volatile. Thus, we accept H4 because the results showed that the smaller the tenure of the ṣukūk, the higher its volatility. However, other factors like credit rating of the issuer, the credit rating of the instrument, rate of return, issue amount, and other market conditions would also affect the volatility behavior of all ṣukūk.

It is found that WAPDA eight and ten-year ma-turity ṣukūk has high volatility, which means that investors are more interested in this ṣukūk. Thus, investors who are willing to take a high risk in order to gain high profits can include ten and eight-year WAPDA ṣukūk in their portfolio. While the return volatility of both K-Electric ṣukūks lies between the volatility of the ṣukūk returns for the two WAPDA ṣukūks and the two Engro Corporation ṣukūks. Also, the results of ṣukūk return predicted that WAPDA ṣukūk returns with a maturity of eight years will rise more than other corporate ṣukūk returns.

The z statistic is used to test for a normal distribu-tion. As per the results, the hypothesis that the pa-rameter coefficients are approximately zero is reject-ed; conditional variance and ARCH term are showing significant value at the 5% level. Thus, we accept H5 because it is proven that there is a GARCH effect founded in all corporate ṣukūk returns as per GARCH (1,1).

EGARCH model is the advance family member

of ARCH model. Referring to the EGARCH table,

the C4 coefficient is negative and significant, which

clearly denotes that there is a leverage effect. The

finding indicates that a negative correlation exists

between the past return and the future volatility of the

return. This indicates that if there is higher leverage

than there is higher volatility in return. The higher

leverage occurs due to the negative returns which

translate to low equity prices, meaning a higher debt

to equity ratio. Whereas a positive shock has less

effect on conditional variance, compared to negative

news. This means that good news and shock gener-

ates less variance than bad news (economics condi-

tions like inflation, unemployment, etc.) for Pakistan

ṣukūk returns.

Moreover, events, news, incidents, etc., have a

strong and powerful influence on the decision mak-

ing of financial investors, and it has an asymmetric

impact on financial markets. A standard ARCH and

GARCH model treats both kinds of good and bad

news symmetrically, and their impact on ṣukūk vola-

tility is the same. However, as a matter of fact, the

good and bad news may be asymmetric. Therefore,

the threshold GARCH model captures the asymme-

tries in terms of positive and negative shocks that hit

the financial markets. Thus, the multiplicative dum-

my variable was introduced into the variance equa-

tion to check whether there is a statistically signifi-

cant difference when shocks are negative.

Lastly, the results of TGARCH show that for all

ṣukūk returns, except Engro three-year ṣukūk return

where γ1 is significant and positive, negative shocks

have larger effects on conditional variance than posi-

tive shocks. The results indicate that news and events

are very significant determinants of ṣukūk return vol-

atility. The bad news has a larger effect than the good

news as 1+ γ1> 1. The above finding of news and

events gives useful information to investors and

speculators about the risk attached with investment in

ṣukūk returns.

5. Conclusions and Recommendations

This research analyzes the trends and volatility of the

different corporate domestic ṣukūk across various

maturities. It was observed during all stages of the

analysis, i.e., identification stage, estimation, diag-

nostic checking, and evaluation stage, that ARCH,

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 39

GARCH, EGARCH, and TGARCH models are best

suited to identifying the trends and volatility in six

ṣukūks issued in Pakistan. The yield of both the En-

gro Corporation ṣukūks is higher than the K-Electric

and WAPDA ṣukūks as evident from the yield curve

given in the results and discussion section. The yield

of Engro corporation three-year maturity ṣukūk is

highest, as its yield increased when all other ṣukūk

yields were decreasing.

It is evident from this research that volatility is

found in all different maturities corporate ṣukūk re-

turns. The WAPDA ṣukūk returns are more volatile

as compared to K-Electric and Engro Corporation

ṣukūk returns. While comparing the volatility of

three- and five-years K-Electric ṣukūk returns with

three- and five-year Engro Corporation ṣukūk returns,

it is discovered that K-Electric ṣukūk returns are more

volatile than Engro Corporation ṣukūk returns. This

study also showed that the smaller the tenure of the

ṣukūk, the higher its volatility. It was also found that

WAPDA eight and ten-year maturity ṣukūk have

higher volatility, meaning that investors are more

interested in these ṣukūk. This indicates that investors

who are willing to take a higher risk to gain higher

profits should include ten and eight-year WAPDA

ṣukūk in their portfolio. Moreover, TGARCH results

show that for all ṣukūk returns, except Engro three-

year ṣukūk, bad news will have a larger effect on the

volatility of the ṣukūk return than good news.

5.1 Significance of Research and Future Outlook

Volatility forecasting is a fascinating subject to both academics and practitioners for investment, security valuation, risk management, and monetary policy-making. This research shall also prove beneficial for the issuers, investors, and security managers in Paki-stan as well as abroad to identify the risk by calculat-ing the volatility of ṣukūk issued domestically. By assessing the whole situation of the risk, investors will take initiatives for safe and profit-taking invest-ments in domestic corporate ṣukūk released in Paki-stan. Besides this, it shall help portfolio managers to pick the appropriate ṣukūk by analyzing the risk ap-petite of their clients as well. In addition, the finding of this study shall help the policymakers to under-stand the ups and downs in the secondary capital market for making policies to safeguard the invest-ment of the general public.

This research will provide a platform to the other researchers to further investigate the ṣukūk sector and bring up new concepts and elaborate upon previous ones in a more precise manner. Moreover, future studies can extend the present research by analyzing the volatility of other corporate domestic and sover-eign ṣukūk issued in Pakistan as well as around the world. In addition, future studies can also compare the ṣukūk return volatility with other fixed income securities present in the capital market. Future studies can also further extend the analysis by applying dif-ferent research models.

40 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

References

Abd. Rahim, S., & Ahmad, N. (2015). Asymmetric mar-ket reactions to sukuk issuance. International Journal of Novel Research in Humanity and Social Sciences, 2(3), 581-589.

Abdalla, S.Z.S., & Winker, P. (2012). Modelling stock market volatility using univariate GARCH models: Ev-idence from Sudan and Egypt. International Journal of Economics and Finance, 4(8), 161-176.

Abdul Rauf, A.L., & Ibrahim, Y. (2014). A sectorial analysis of sukuk market based on determinants of risk and return performances. European Journal of Ac-counting Auditing and Finance Research, 2(2), 145-161.

Accounting and Auditing Organization for Islamic Financial Institutions [AAOIFI]. (2015). Shari’ah Standards. Manama, Bahrain: Author.

Agwu, E.C., & Godfrey, O.U. (2019). Modeling volatility and daily exchange rate movement in Nigeria. Interna-tional Journal of Economics and Financial Research, 5(11), 264-275.

Ahmad, N., & Abd. Rahim, S. (2014). CAAR estimations by sectors of sukuk issuance. In K.A. Mkhitaryan & M. Plaisent (Eds.), Proceedings of International Confer-ence on Economics, Education and Humanities (ICEEH'14) (pp. 276-282). Bali, Indonesia: Interna-tional Center of Economics, Humanities & Manage-ment.

Alam, N., Bhatti, M., & Wong, J.T.F. (2018). Assessing sukuk defaults using value-at-risk techniques. Manage-rial Finance, 44(6), 665-687.

al-Amine, M.A.M. (2011). Global sukūk and Islamic securitization market: Financial engineering and product innovation. Leiden, the Netherlands: Brill.

Ariff, M., & Safari, M. (2012). Are sukuk securities the same as conventional bonds? Afro Eurasian Studies, 1(1), 101-125.

Bhuiyan, A.R., Puspa, M., Saiti, B., & Ghani, G.M. (2020). Comparative analysis between global sukuk and bond indices: Value-at-risk approach. Journal of Islamic Accounting and Business Research, 11(6), 1245-1256.

Bollerslev, T. (1986). Generalized autoregressive condi-tional heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

Engle, R.F. (1982). Autoregressive conditional heterosce-dasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50(4), 987-1007.

Fathurahman, H., & Fitriati, R. (2013). Comparative analysis of return on sukuk and conventional bonds. American Journal of Economics, 3(3), 159-163.

Ghafoor, S., Saba, I., & Kouser, R. (2018). Sukuk issu-

ance in Malaysia: Lessons for Pakistan. Journal of Ac-

counting and Finance in Emerging Economies, 4(2),

159-176.

Glosten, L.R., Jagannathan, R., & Runkle, D.E. (1993).

On the relation between the expected value and the

volatility of the nominal excess return on stocks. The

Journal of Finance, 48(5), 1779-1801.

Godlewski, C.J., Turk-Ariss, R., & Weill, L. (2013).

Sukuk vs. conventional bonds: A stock market perspec-

tive. Journal of Comparative Economics, 41(3), 745-

761.

Gujarati, D.N., & Porter, D. (2009). Basic Econometrics

(5th ed.). New York, USA: McGraw-Hill.

Hassan, K.A. (2012). Comparison between sukuk and

conventional bonds: Value at risk approach (Universi-

ty of Westminster working paper). Retrieved from:

https://bit.ly/356HqiB

Jobst, A., Kunzel, P., Mills, P., & Sy, A. (2008). Islamic

bond issuance: What sovereign debt managers need to

know. International Journal of Islamic and Middle

Eastern Finance and Management, 1(4), 330-344.

Kostandyan, B. (2015). Sukuk vs conventional bonds: A

value-at-risk based comparative analysis. Russian Re-

view, 2(3), 36-49.

Lahsasna, A., & Lin, L.S. (2012). Issues in Islamic capital

markets: Islamic bond/sukuk. In 3rd International Con-

ference on Business and Economic Research (3rd

ICBER 2012) Proceeding (pp. 495–512). Retrieved

from: https://bit.ly/38hTb7T

Maghyereh, A.I., & Awartani, B. (2016). Dynamic

transmissions between sukuk and bond markets. Re-

search in International Business and Finance, 38, 246-

261.

Malikov, A. (2017). How do sovereign sukuk impact on

the economic growth of developing countries? An

analysis of the infrastructure sector. In V. Efendić, F.

Hadžić, & H. Izhar (Eds.), Critical issues and chal-

lenges in Islamic economics and finance development

(pp. 1-37). Cham, Switzerland: Springer Nature.

Maqsood, A., Safdar, S., Shafi, R., & Lelit, N. J. (2017).

Modeling stock market volatility using GARCH mod-

els: A case study of Nairobi Securities Exchange

(NSE). Open Journal of Statistics, 7(2), 369-381.

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 41

Miller, N.D., Challoner, J., & Atta, A. (2007). UK wel-

comes the sukuk: How the UK finance bill should

stimulate Islamic finance in London, much to the de-

light of the city’s banks. International Financial Law

Review, 26(5), 24-25.

el-Mosaid, F., & Boutti, R. (2014). Sukuk and bond per-

formance in Malaysia. International Journal of Eco-

nomics and Finance, 6(2), 226-234.

Nagano, M. (2017). Sukuk issuance and information

asymmetry: Why do firms issue sukuk? Pacific-Basin

Finance Journal, 42, 142-157.

Nasir, A., & Farooq, U. (2017). Analysis of value at risk

of sukuk and conventional bonds in Pakistan. Journal

of Islamic Accounting and Business Research, 8(4),

373-388.

Nasreen, S., Naqvi, S.A.A., Tiwari, A.K., Hammoudeh,

S., & Shah, S.A.R. (2020). A Wavelet-Based Analysis

of the Co-Movement between ṣukūk Bonds and

Sharīʿah Stock Indices in the GCC Region: Implica-

tions for Risk Diversification. Journal of Risk and Fi-

nancial Management, 13(4), 1-21.

Nelson, D.B. (1991). Conditional heteroskedasticity in

asset returns: A new approach. Econometrica, 59(2),

347-370.

Raees, S., Raheem, Z., & Zakir, A. (2017). Sukuk bond

in Pakistan: An analysis of Islamic mode of financing

for investors. Archives of Business Research, 5(10),

103-117.

Saeed, M., & Izzeldin, M. (2016). Examining the relation-

ship between default risk and efficiency in Islamic and

conventional banks. Journal of Economic Behavior &

Organization, 132, 127-154.

Salman, A., Amjad, M., & Aslam, E. (2017). Types of

interest in Islamic law: Analysis and application. Paki-

stan Journal of Islamic Research, 18(2), 1-14.

Shiau, H.-L., Chang, Y.-H., & Yang, Y.-J. (2018). The

cash holdings and corporate investment surrounding

financial crisis: The cases of China and Taiwan. The

Chinese Economy, 51(2), 175-207.

Smaoui, H., & Ghouma, H. (2020). Sukuk market devel-

opment and Islamic banks’ capital ratios. Research in

International Business and Finance, 51, 1-17.

Smaoui, H., Mimouni, K., & Temimi, A. (2020). The

impact of sukuk on the insolvency risk of conventional

and Islamic banks. Applied Economics, 52(8), 806-824.

al-Swaidan, M.W., Daynes, A., & Pasgas, P. (2017).

Understanding and evaluation of risk in sukuk struc-

tures. Journal of Islamic Accounting and Business Re-

search, 8(4), 389-405.

Tariq, A.A., & Dar, H. (2007). Risks of sukuk structures:

Implications for resource mobilization. Thunderbird In-

ternational Business Review, 49(2), 203-223.

Usmani, M.T. (2007). Sukuk and their contemporary ap-

plications. Retrieved from: https://bit.ly/2IeRI76

Vishwanath, S. R., & Azmi, S. (2009). An overview of

Islamic sukuk bonds. The Journal of Structured

Finance, 14(4), 58–67.

Zulkhibri, M. (2015). A synthesis of theoretical and em-

pirical research on sukuk. Borsa Istanbul Review,

15(4), 237-248.

42 Ejaz Aslam, Khuram Mobusher Azam and Anam Iqbal

Ejaz Aslam is currently an Assistant Professor and researcher at the School of Islamic

Economics, Banking & Finance, Minhaj University Pakistan. He specialises in

corporate finance, corporate governance, and financial management. He has published

in journals like Corporate Governance: The International Journal of Business in

Society, Borsa Istanbul Review, Environmental Science and Pollution Research,

Global Business Review, International Journal of Business Excellence, Islamic

Economic Studies, and Asian Journal of Accounting Research. E-mail:

Khuram Mobusher Azam is currently credit manager at Habib Bank Ltd. in Pakistan.

He holds a master’s degree in Islamic Banking and Finance from the University of

Management and Technology, Lahore. His research interests include global financial

system, financial risk management, monetary and financial theory, international

investment, corporate finance, corporate governance, portfolio analysis, financial

engineering, and ṣukūk/mutual fund market. E-mail: [email protected]

Anam Iqbal is a PhD scholar at the IIUM Institute of Islamic Banking and Finance,

International Islamic University Malaysia. She got her master’s degree in Finance,

University of Management & Technology, Lahore-Pakistan. Her areas of research are

corporate governance, earning management, and financial management. She has

published in journals like Islamic Economic Studies, International Transaction Journal

of Engineering, Management, & Applied Sciences & Technologies, and Islamic

Banking and Finance Review.

The Risk Analysis of Ṣukūk: An Empirical Evidence from Pakistan 43

تحليل مخاطر الصكوك: أدلة تجريبية من باكستان

إعجاز أسلم

باكستان، جامعة منهاج، تمويلالاقتصاد الإسلامي والبنوك والأستاذ مساعد وباحث في كلية

خرم مبشر أعظم

باكستان، مدير بنك حبيب

إقبالم عأن

الإسلامية بماليزياالجامعة العالمية ، تمويلفي معهد البنوك الإسلامية وال دكتوراه ةطالب

عد المستخلص.ُمبادئ الشريعة الإسلامية مرنة تعتمد على هيكلةالصكوك أداة مالية مبتكرة ذات ت

حرمة على أساس الفوائد ات التي تقوم، على عكس السندالتي تربط العائد بنتيجة المشروعُ. الربوية الم

خاصة في البلدان عليها، الطلببسبب هذه التركيبة والمرونة التي تتمتع بها صيغة الصكوك تزايد

تمتع الصكوك بأهمية رئيسة في السوق المالية، ولا توجد تالسيولة. تالإسلامية للتغلب على مشكلا

التي حالة باكستان، يلهذه الأداة المالية كما هو الشأن فأدبيات حول كيفية التنبؤ بالاتجاه والتقلبات

البحث التّجريبي إلى فحص التقلبات يهدف هذاكبيرة على أدوات الدين. تعرف أسواق المال فيها طلبات

صادرة في صكوك وتحليل الاتجاهات في صناعة الصكوك في باكستان. تتكون عينة الدراسة من ستة

، (EGARCH( و )GARCH( و )ARCH) باكستان. ولهذا الغرض، استخدمت الدراسة نماذج

لتحليل سلوك الخطر لصناعة الصكوك في باكستان. كشفت النتائج أن عائد شركة (TGARCH) و

(Engroإنغرو )ًا الأخرى. وتشهد النتائج على أن هناك تقلبً من عوائد صكوك الشركات أعلى وأقل تقلبا

تبين أن الحيازة الأصغر ائد الشركات في الصكوك من آجال مختلفة. بالإضافة إلى ذلك،و في جميع ع

للًوك كانت ذات تقلبات عالية مقارنة بالحيازة الأكبر، وأن الأخبار والأحداث السيئة لها آثار صّكحجما

فيد نتائج . جيدةمن الأخبار ال عوائد الصكوكأكبر على تقلب ُعددًا هذه الدراسة يأمل الباحثون أن ت

للاستثمار في ؛وسلطات صنع القرارالمالية، المحافظومديري ،لمستثمرينمن الأطراف ذات الصلة، كا

.المنخفضة المخاطر كأدوات للديون في باكستان صكوكسوق ال

الة: .التمويل الإسلامي، تقلب الصكوك الكلمات الدَّ

JEL :G02, G14, P51 تصنيف

KAUJIE :K16, I10 تصنيف