Embed Size (px)

Citation preview

The Honorable Marsha J. Pechman 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

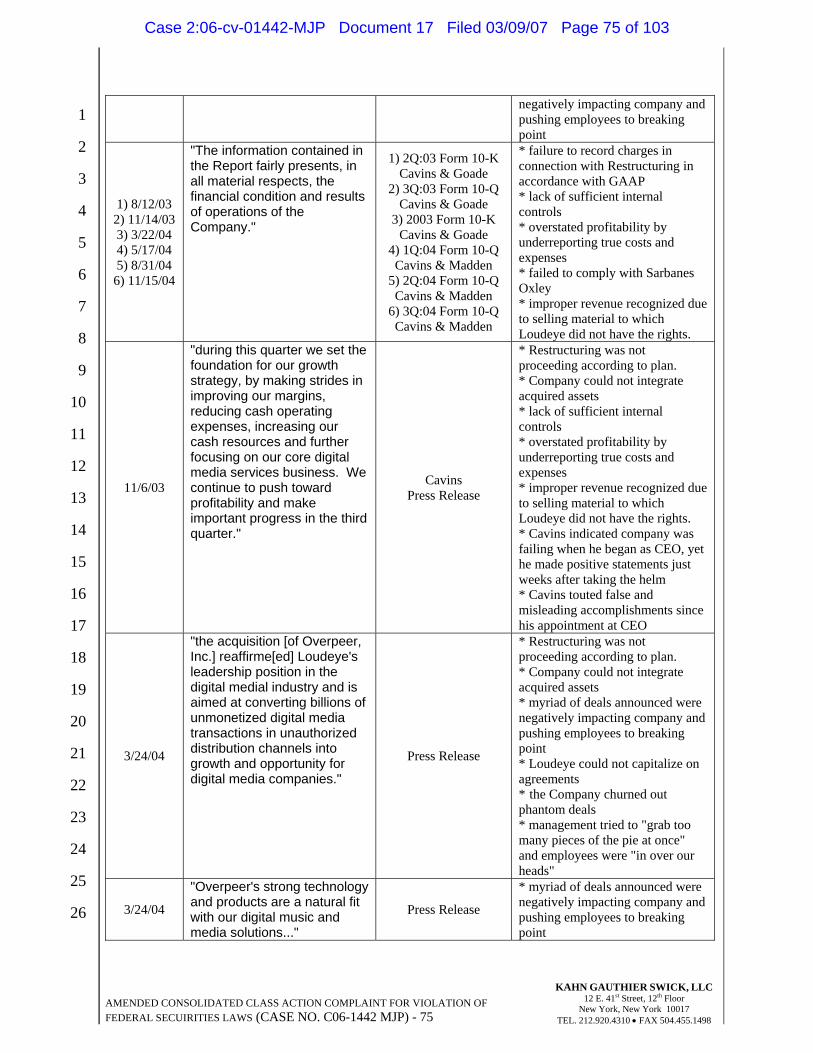

20

21

22

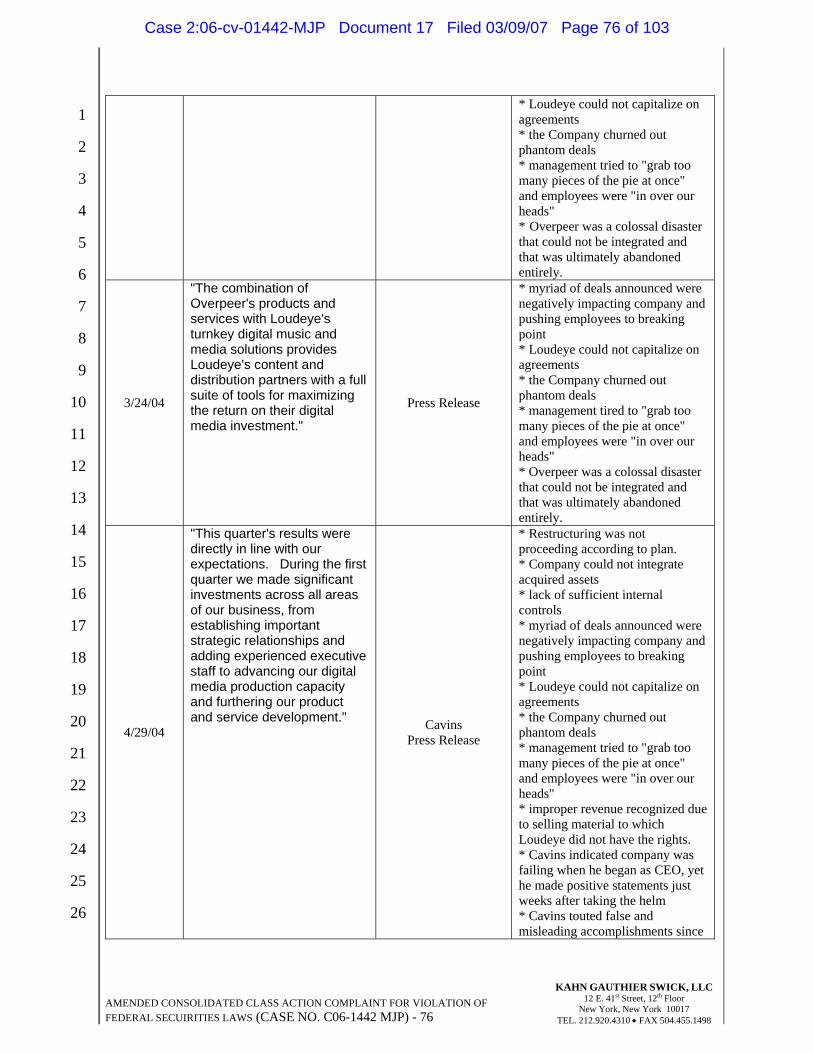

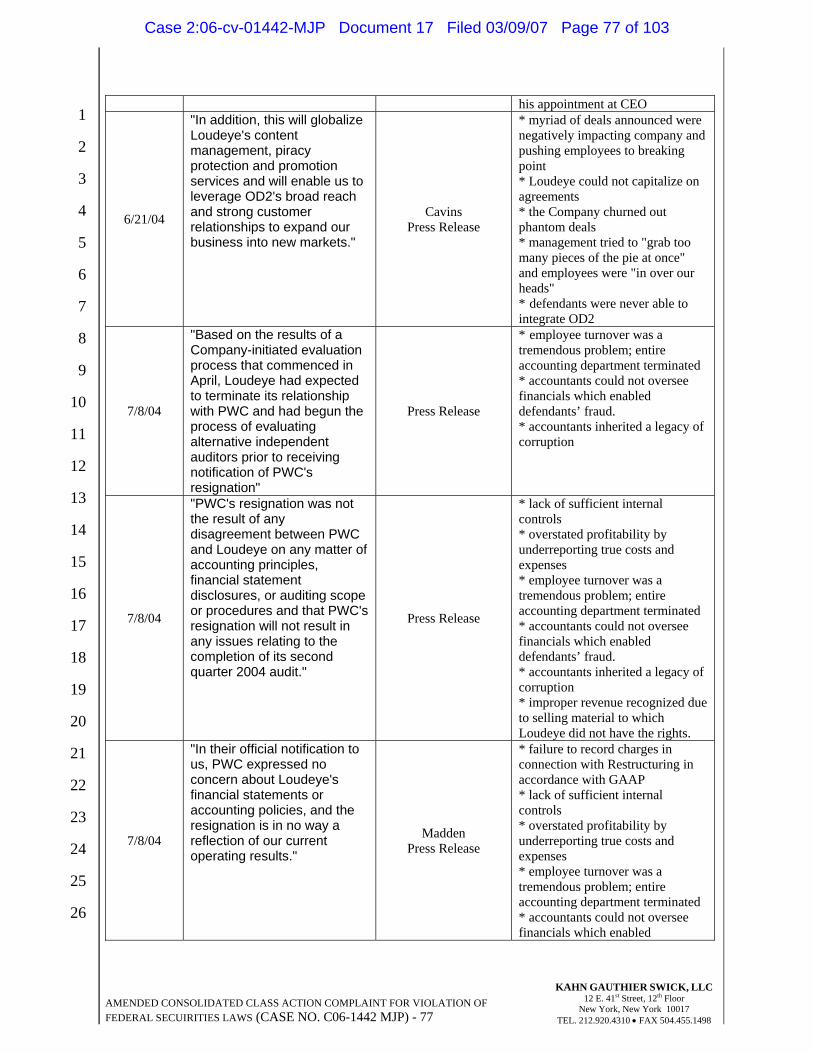

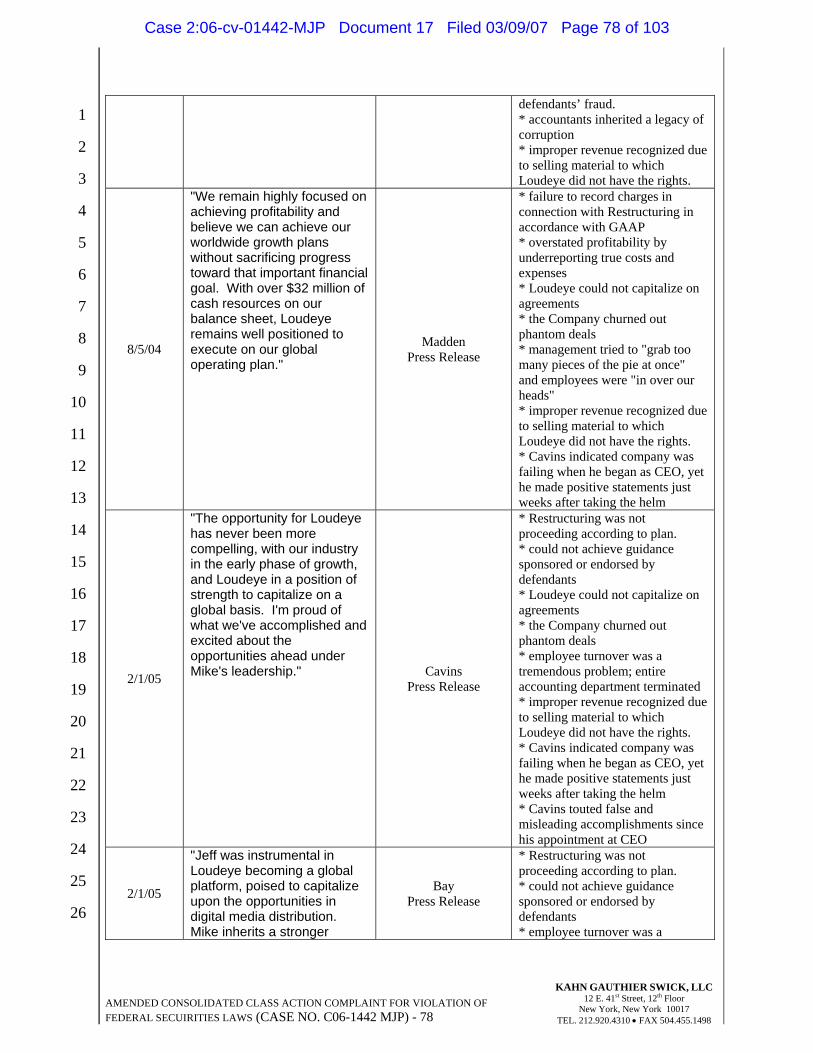

23

24

25

26

UNITED STATES DISTRICT COURT

WESTERN DISTRICT OF WASHINGTON

IN RE LOUDEYE CORPORATION SECURITIES LITIGATION

CASE NO. C06-1442 MJP

AMENDED CONSONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF FEDERAL SECURITIES LAWS JURY TRIAL DEMANDED

INTRODUCTION

This is a federal class action on behalf of purchasers of the common stock of Loudeye

Corp. (“Loudeye” or the “Company”) between May 14, 2003 and November 9, 2005, inclusive

(the “Class Period”), seeking to pursue remedies under the Securities Exchange Act of 1934

(the “Exchange Act”). As alleged herein, defendants published a series of materially false and

misleading statements that defendants knew to be and/or deliberately disregarded the fact that

they were materially false and misleading at the time of such publication, and that omitted to

reveal material information necessary to make defendants’ statements, in light of such material

omissions, not materially false and misleading.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 1

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 1 of 103

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

JURISDICTION AND VENUE

1. The claims asserted herein arise under and pursuant to Sections 10(b) and 20(a)

of the Exchange Act [15 U.S.C. §§ 78j(b) and 78t(a)] and Rule 10b-5 promulgated thereunder

by the United States Securities and Exchange Commission (“SEC”) [17 C.F.R. § 240.10b-5].

2. This Court has jurisdiction over the subject matter of this action pursuant to 28

U.S.C. §§ 1331 and 1337, and Section 27 of the Exchange Act [15 U.S.C. § 78aa].

3. Venue is proper in this District pursuant to Section 27 of the Exchange Act, and

28 U.S.C. § 1391(b). During the Class Period, Loudeye maintained its principal place of

business in this District and many of the acts and practices complained of herein occurred in

substantial part in this District.

4. In connection with the acts alleged in this complaint, defendants, directly or

indirectly, used the means and instrumentalities of interstate commerce, including, but not

limited to, the mails, interstate telephone communications and the facilities of the national

securities markets.

PARTIES

5. Lead Plaintiffs Maria Corso, Steven Corso, and Louise Rehling (the “Corso

Group”) were appointed Lead Plaintiffs pursuant to a January 23, 2007 Order of the Court.

6. Lead Plaintiff Maria Corso resides in Palm Beach, Florida. As set forth in the

certification attached to her initial complaint against defendants, and incorporated by reference

herein, Maria Corso purchased the common stock of Loudeye at artificially-inflated prices

during the Class Period and has been damaged thereby.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 2

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

7. Lead Plaintiff Steven Corso, Maria Corso’s spouse, also resides in Palm Beach,

Florida. As set forth in the certification attached to his initial complaint against defendants, and

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 2 of 103

incorporated by reference herein, Steven Corso purchased the common stock of Loudeye at

artificially-inflated prices during the Class Period and has been damaged thereby.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

8. Lead Plaintiff Louise Rehling resides in Chicago, Illinois. As set forth in the

certification attached to the Lead Plaintiff Motion of the Corso Group, and incorporated by

reference herein, Louise Rehling purchased the common stock of Loudeye at artificially-

inflated prices during the Class Period and has been damaged thereby.

9. During the Class Period, Defendant Loudeye Corporation was a Delaware

corporation, founded in 1997, with its principal place of business and chief executive offices

located in Seattle, Washington. According to the Company’s profile, during the Class Period,

Loudeye provided business-to-business digital media services that facilitate the distribution,

promotion, and sale of digital media content for media and entertainment, mobile

communications, consumer products, consumer electronics retail, and ISP customers

worldwide. The Company’s services included purported “turn-key,” outsourced digital media

distribution and promotional services, such as private-labeled digital media store services,

including mobile music services; and digital media content services, such as encoding, music

samples services, hosting, and Web casting, as well as Internet radio services. The Company’s

digital media store services included hosting, publishing, and managing digital media content,

and delivering such content to end-consumers on behalf of its customers; and digital rights

management and licensing, usage reporting, digital content royalty settlement, customer

support, and publishing-related services.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 3

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

10. Defendant Jeffrey M. Cavins (“Cavins”) was during the Class Period, Chief

Executive Officer and President of the Company, having served in this capacity from early

2003 until on or about February 1, 2005 when he was forced to resign from the Company.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 3 of 103

During the Class Period, defendant Cavins signed and/or certified the Company’s SEC filings,

including but not limited to Loudeye’s Form(s) 10-Q and Form(s) 10-K, and made and/or was

responsible for numerous additional false and misleading statements and omissions.

1

2

3

4

5

6

7

8

9

10

11

12

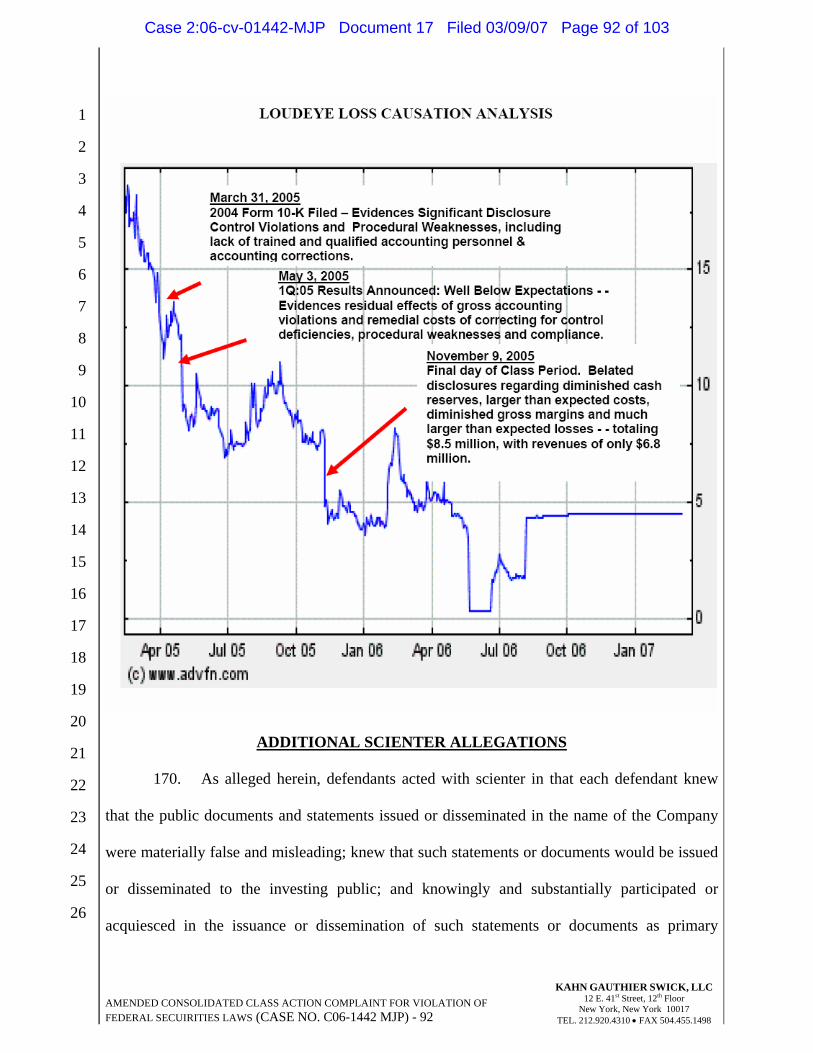

13

14

15

16

17

18

19

20

21

22

23

24

25

26

11. Defendant Andrew Bay (“Bay”) was, during the Class Period, the chairman of

the Company. During the Class Period, Bay made and/or was responsible for numerous false

and misleading statements and omissions.

12. Defendant Michael A. Brochu (“Brochu”) was, beginning on or about February

1, 2005, Chief Executive Officer and President of the Company. During the Class Period,

defendant Brochu signed and/or certified the Company’s SEC filings, including but not limited

to Loudeye’s Form(s) 10-Q and made and/or was responsible for numerous additional false and

misleading statements and omissions.

13. Defendant Jerold J. Goade (“Goade”) was, prior to and during the Class Period

until on or around April 9, 2004, Interim Chief Financial Officer and Principal Accounting

Officer of the Company. Throughout the rest of the Class Period, Goade was Senior Vice

President of Finance. During the Class Period, defendant Goade signed and/or certified the

Company’s SEC filings, including but not limited to Loudeye’s Form(s) 10-Q and Form(s) 10-

K and made and/or was responsible for numerous additional false and misleading statements

and omissions. Goade is currently prohibited from practicing public accounting by the State of

Washington.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 4

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

14. Defendant Lawrence J. Madden (“Madden”) was between April 9, 2004, and

April 7, 2005, Chief Financial Officer and Principal Accounting Officer of the Company.

During the Class Period, defendant Madden signed and/or certified the Company’s SEC filings,

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 4 of 103

including but not limited to Loudeye’s Form(s) 10-Q and Form(s) 10-K and made and/or was

responsible for numerous additional false and misleading statements and omissions.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

15. The defendants referenced above in ¶¶ 1-14 are referred to herein as the

“Individual Defendants.”

SUBSTANTIVE ALLEGATIONS Background

16. Throughout the Class Period, Loudeye purported to be a provider of business-to-

business digital media services that facilitate the distribution, promotion, and sale of digital

media content for media and entertainment, mobile communications, consumer products, retail

consumer electronics, and Internet service provider customers worldwide. Loudeye’s primary

products and services allowed its customers to outsource their digital media distribution and

promotional services - - such as private-labeled digital media store services, mobile music

services and Internet radio services.

17. In light of recent growing demand for the delivery of digital music across

different platforms and delivered to different devices, Loudeye’s promotion of itself as a

“worldwide leader in business-to-business digital media solutions” and services brought the

Company to investors’ attention and caused Loudeye shares to accelerate radically from the

inception of the Class Period.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 5

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

18. Prior to the inception of the Class Period, on February 4, 2003, John T. Baker,

the former Chairman and Chief Executive Officer of Loudeye resigned, and the Board of

Directors of the Company engaged Regent Pacific Management Corporation to help Loudeye

find new senior management. On or about March 7, 2003, Regent Pacific’s engagement

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 5 of 103

concluded and Jeffrey M. Cavins was elected President and Chief Executive Officer of the

Company.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

19. At the time that Cavins was brought in, defendants’ goal was to have Cavins

rescue a failing enterprise and turn it around. According to Cavins’ own resume, attached

hereto as Exhibit A, defendants knew the Company was failing prior to the inception of the

Class Period and the objective was to take “the business from the brink of bankruptcy” and

make it “a leader in the digital media space.” While Cavins’ resume and defendants’ Class

Period representations touted Cavins’ alleged successes, the true adverse facts discussed herein

– concealed from investors during the Class Period – paint a very different picture.

20. In fact, throughout the Class Period, the Company was failing and Cavins’

“business model” of boosting gross margins and profits while representing that he had the

ability to control costs when in fact he failed to make essential expenditures to build

necessary infrastructure had no chance to succeed, particularly given that the Company was

growing at an exponential rate and needed to make significant investments and expenditures in

order to build necessary infrastructure and synergize its constantly-increasing assets --

including its major acquisitions.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 6

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

21. In light of the foregoing failed strategy, defendants’ numerous statements

regarding successful cost-cutting measures were false and misleading when made; e.g.: “The

Company implemented an operational restructuring at the end of the first quarter of 2003 which

is expected to reduce future operating costs” (¶ 36); “restructuring plan which has already

resulted in significant cost savings” (¶37); “improvements in our cost structure, and building

on our progress to drive revenue, cash flow and profitability” (¶37); “improving our margins,

reducing cash operating expenses” (¶58); “Gross margins as a percentage of revenue increased

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 6 of 103

to 46%...This is the company’s best performance as a public company.” (¶57) “We were

successful in 2003 in achieving the goals we set for ourselves. We significantly improved our

gross margins, reduced our cost structure and improved our balance sheet.” (¶66); “We

remain highly focused on achieving profitability and believe we can achieve our worldwide

growth plans without sacrificing progress toward that important financial goal” (¶80).

[Emphasis added].

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

22. Rather than acknowledging to the marketplace that its strategy was an abject

failure, defendants instead engaged in a scheme and course of conduct to artificially inflate the

price of Loudeye stock during the Class Period by issuing false and misleading positive

statements to investors – set forth in detail herein below -- and omitting to disclose the material,

adverse true facts, which enabled defendants, inter alia, to raise money through Private

Investment in Public Equity Stock Sales (“PIPE” sales), whereby the Company sold stock to a

group of private investors, usually with warrants provided as part of the deal.

23. Moreover, through their scheme and course of conduct, while defendants were

unable to salvage the Company, they ultimately saved themselves by selling the Company’s

assets to Nokia in exchange for complete indemnification for all defendants for the conduct as

issue in this case, as well as obtaining sweetheart deals for those executives who stayed at

Loudeye until the end, including defendant Brochu, who personally pocketed hundreds of

thousands of dollars in the Nokia deal, according to the Merger Prospectus, in addition to the

indemnification and other perks and benefits.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 7

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

24. Up until the time the Company announced Cavins’ abrupt resignation in

February 1, 2005, and beyond, defendants vigorously stayed “on message” with respect to their

fraudulent scheme to conceal the fact that their strategy had failed utterly from the get-go under

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 7 of 103

Cavins’ “leadership.” E.g., “an aggressive restructuring plan which has already resulted in

significant cost savings (¶37); “During this quarter we set the foundation for our growth

strategy, by making strides in improving our margins, reducing cash operating expenses,

increasing our cash resources and further focusing on our core digital media services business

(¶58); “We were successful in 2003 in achieving the goals we set for ourselves.” (¶66);

Overpeer’s strong technology and products are a natural fit with our digital music and media

solutions” (¶68); “Beginning next quarter, we expect improving results for the remainder of

2004 as we deliver upon the opportunity in front of us (¶71); “The combination [with OD2]

approximately doubles Loudeye’s revenues on a pro forma basis and creates the largest

business to business focused digital media company in the world” (¶75).

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

25. Throughout the Class Period, defendants falsely touted Mr. Cavins’ successes in

putting the pieces in place that would enable Loudeye to reach greater profitability and success

in the future, which defendants knew at the time would not happen, as they were already

searching for strategic alternatives to abandon the Company and enable defendants to save

themselves. The February 1, 2005 press release also stated:

“Mr. Cavins was appointed chief executive officer in March 2003 to develop and execute on a strategic plan that included focusing on a growing opportunity in digital media distribution and related services, and restructuring Loudeye's financial and operating performance. During his tenure, Loudeye developed its product offering significantly to offer online and mobile private-labeled digital music store solutions and expanded its reach to over 20 countries worldwide. In addition, Loudeye strengthened its balance sheet and grew revenue significantly, delivering successive record quarters of revenue performance in the third and fourth quarters of 2004…. Defendant Bay added: "Jeff was instrumental in Loudeye becoming a global platform, poised to capitalize upon the opportunities in digital media distribution. Mike inherits a stronger company due to Jeff's efforts and leadership."

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 8

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 8 of 103

26. The above statements were false and misleading when made because defendants

knew the business had been failing prior to and throughout the Class Period, knew that Cavins

had not successfully executed a strategic plan to grow the Company but rather had pushed the

Company to the breaking point, leading to the terminations of the entire accounting department

and ensuring that adequate internal controls were not possible and the Company could not

comply with GAAP, knew that the countless acquisitions by the Company were not and could

not be successfully integrated into the Loudeye platform, knew that Loudeye would never

become a global platform, and knew that the Company inherited by defendant Brochu as the

new CEO was not “stronger” due to “Jeff’s efforts and leadership” but rather required an

emergency change in direction in order to enable the Company to limp along just long enough

to sell off its assets in exchange for a golden ticket for the individual defendants: complete

indemnification for their fraudulent scheme and course of conduct as alleged herein by their

eventual merger partner, Nokia.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27. Defendants also used the February 1, 2005 transition of leadership as an

opportunity to then explain to investors that this change followed the Company’s growth and

evolution after its Restructuring. Defendants used this release to condition investors to believe

that the Company was also successfully proceeding along its plan to develop a single, global

delivery platform, falsely noting that the future for Loudeye looked bright when defendants

knew that the Company could not survive, and further touting Cavins’ “several notable

successes” which were in fact complete failures, particularly the Overpeer, Inc. (“Overpeer”)

and OD2 acquisitions that could never be synergized or integrated into Loudeye:

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 9

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

"The opportunity for Loudeye has never been more compelling, with our industry in an early phase of growth, and Loudeye in a position of strength to capitalize on a global basis. I'm proud of what we've accomplished and excited about the opportunities ahead under Mike's leadership," said Mr. Cavins.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 9 of 103

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Mr. Cavins leaves Loudeye after leading the company to achieve several notable successes during his tenure at Loudeye. Under Mr. Cavins' direction Loudeye positioned itself as a key player in the rapidly growing market for legitimate digital distribution of music, video and games. [Emphasis added]. 28. In stark contrast to prior statements made by the Company under Cavins’

leadership regarding platform integration, on May 3, 2005, during an Earnings Conference Call

for Q1:05, defendant Brochu – no longer able to fully hide the fact that gross margins were

being rapidly eroded by all the necessary expenditures that Cavins failed to undertake while at

the helm – stated in part:

“We are investing heavily in our platform and operational infrastructure and ahead of our current revenues [and indicate the Company] would move aggressively on areas such as integrating our U.S. and International operations, which have been running autonomously, resulting in higher costs.” [Emphasis added].

These statements -- while continuing to conceal the full scope of the effects of defendants’

scheme that were revealed on the last day of the Class Period, November 9, 2005 -- directly

contradicted prior statements by defendants that the Company’s acquisitions had been

integrated and had already resulted in immediate synergies.

The Highly-Touted Restructuring

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 10

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

29. According to the Company, during and subsequent to Regent Pacific’s

engagement, the Board of Loudeye also undertook a “strategic and operational analysis” of its

business and product lines. This analysis resulted in the development of a new strategic and

operational plan (the “Restructuring”), under which Loudeye purported to rationalize its

business and operations. In connection with the Restructuring, defendants also provided new

near-term forward-looking guidance for revenues, earnings, profits and margins.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 10 of 103

30. In connection with these revised estimates, defendants also performed a

reassessment of the carrying value of all of its assets, both tangible and intangible, as well as

the value of its goodwill and other assets. As a result of the analysis that was purported to have

occurred in connection with the Restructuring, the Company recorded impairment charges for

goodwill, intangible assets, and property and equipment related to its enterprise communication

services and media restoration services businesses of $5.3 million, $685,000, and $601,000,

respectively.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

31. Loudeye’s alleged focused dedication to electronic music delivery coincided

with the Company’s major Restructuring – purported to have taken place immediately prior to

the inception of the Class Period. As “evidence” that the Company’s restructuring plan was

already showing early signs of success, Company CEO, defendant Cavins, stated in a May 14,

2003 Company press release announcing results for the first quarter of 2003 that the Company

had “implemented an aggressive restructuring plan which has already resulted in significant

cost savings. We are encouraged by our progress, as we took steps to reduce our cost

structure, reduce cash burn and tightly focus our business to deliver better financial results

in future quarters.” [Emphasis added].

32. Thereafter, throughout the Class Period, the Company repeatedly assured

investors that the Restructuring was effective and that Loudeye was operating according to its

revised plan, as discussed in detail below.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 11

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

33. Moreover, throughout that time, defendants repeatedly stated that Loudeye

maintained adequate financial controls and operational procedures so as to reasonably assure

investors that the Restructuring was proceeding properly, that the Company was poised for

growth through acquisitions as well as organic growth, and that the Company was achieving

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 11 of 103

operational improvements and financial success; e.g., “our disclosure controls and procedures

are effective in timely alerting us to material information relating to the Company required to

be included in our periodic SEC filings (¶39); “Subsequent to the date of that evaluation, there

have been no significant changes in our internal controls or in other factors that could

significantly affect internal controls, nor were any corrective actions required” (¶40); “the

financial statements…fairly present …the financial condition, results of operations and cash

flows” (¶41); “Loudeye has assembled a strong asset base and has built a digital media

distribution infrastructure which I believe will be a vital component to the rising online digital

media business” (¶42); “We are focused intently on execution and are pleased to see the results

in our operating metrics and improved financial performance in the second quarter (¶45);

“the acquisition [of Overpeer] reaffirm[ed] Loudeye’s leadership position in the digital media

industry and is aimed at converting billions of unmonetized digital media transactions in

unauthorized distribution channels into growth and opportunity (¶67); (“the combination

[with OD2] ...creates the largest business-to-business focused digital media company in the

world” (¶75) [Emphasis added].

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 12

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

34. For the reasons described in detail herein, the material, affirmative

representations and material omissions concerning Loudeye’s Restructuring, the integration of

its acquired assets, and the effectiveness of the Company’s systems and controls were patently

untrue when made, and Defendants, throughout the Class Period, knew and/or deliberately

disregarded the true, material, adverse facts that starkly contrasted with the material, positive

Class Period statements concerning the Company, which facts are discussed in detail herein.

As investors would ultimately learn, there were true but undisclosed adverse facts about the

Company which are discussed directly below.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 12 of 103

MATERIAL, ADVERSE FACTS KNOWN AND CONCEALED BY DEFENDANTS 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Background Concerning Material, Adverse Facts

35. As investors ultimately learned on November 9, 2005, throughout the Class

Period, Loudeye was suffering from a host of undisclosed material adverse factors that were

negatively impacting Loudeye’s business. These issues would ultimately cause it to report

dramatically declining financial results -- materially less than the market expectations

defendants had caused and cultivated.

36. These concealed, adverse facts ultimately forced defendants to admit that

previously-reported financials were not true, accurate, or reliable and required adjustments; and

finally acknowledge that the financial and operation status of Loudeye was so dire that the

Company was forced to consider strategic alternatives. In truth, according to confidential

witness #4, defendants – knowing they were at the end of the road -- had already hired a

consultant no later than July of 2005 to propose strategic alternatives.

37. On May 1, 2006, Loudeye announced its agreement to sell all of its US

operations to Muze Media (“Muze”).

38. On August 8, 2006, the Company announced that it had agreed to sell what was

left of Loudeye to Nokia, a Finnish mobile phone and electronics manufacturer. The Nokia

deal struck by the defendants was their knight in shining armor: Nokia agreed to indemnify the

defendants for any claims – including securities fraud claims – for a six year period (longer

than the statute of limitations for an Exchange Act case), as well as to provide the Company’s

remaining executives, including defendant Brochu, with sweetheart stock and severance

packages (amounting to hundreds of thousands of dollars for defendant Brochu).

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 13

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 13 of 103

The Restructuring Was Not Proceeding According To Plan 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

39. Loudeye’s purported restructuring was not proceeding according to plan and

defendants were not seeing early signs of success. The restructuring was not “already resulting

in significant cost savings” (¶5) and defendants were not, or should not have been,

“encouraged” by those results. (¶5).

40. In truth, in connection with the Restructuring, defendants failed to record all

proper and necessary charges and materially understated the true costs associated with building

the necessary and adequate internal controls and procedures so as to reasonably assure that the

Company’s financial statements and operational reports were prepared in accordance with

Generally Accepted Accounting Principles (“GAAP”) and Securities and Exchange

Commission (“SEC”) rules.

As Defendants Eventually Admitted, the Company Utterly Lacked Adequate Internal Controls and Its Financial

Statements Failed to Comply with GAAP and SEC Rules

41. With respect to internal controls, Loudeye had grossly inadequate systems of

internal operational or financial controls in place. In fact, as defendants would eventually

admit, reporting controls and operational procedures were so woefully deficient that Loudeye’s

financial and operational reporting was not true, accurate or reliable during the Class Period.

For example, material control weaknesses included:

-- “Insufficiently skilled personnel compounded by a lack of human resources” (¶82);

--“Insufficient analysis, documentation and review of the selection and application of [GAAP] to significant, non-routine transactions (¶82);

-- “Deficiencies related to insufficient review and approval and documentation of the review and approval of the work being performed by employees within our accounting and finance department” (¶99);

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 14

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 14 of 103

--“Loudeye does not have sufficient internal control over financial reporting to ensure underlying transactions are being appropriately and timely accounted for” (¶ 99);

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

--“Insufficient number of effectively designed controls or there are ineffectively designed controls” (¶99);

-- Failure to appropriately assess and monitor the effectiveness of controls executed by third party service providers, and to adequately implement and/or maintain customer level controls” (¶99);

--“Inadequate entity-level controls” (¶99); -- Defendants materially overstated the Company’s profitability by underreporting Loudeye’s true financial and operational costs and expenses during the Class Period;

-- As noted by a former employee who worked in the accounting department during the Class Period (“Former Employee #1”), the Company failed to comply with the Sarbanes-Oxley Act;

-- After the abrupt resignation of PricewaterhouseCoopers LLP (“PWC”) as the Company’s auditors after completion of services related to review of Loudeye’s interim financial statements for the quarter ended June 30, 2004, the Company was forced, in its 2004 Form 10-K, to include a series of “adjustments” that revealed that the control deficiencies were not only operational but fiscal as well, including: (i) improper accounting for minority interest in OD2; (ii) improper accounting for OD2 escrow consideration, (iii) material weaknesses resulting in “deficiencies in the processes, procedures and competencies within our accounting and financial reporting functions”; and (iv) management’s assessment that “there were eight material weaknesses in Loudeye’s internal control over financial reporting [and] financial reporting was not effective as of December 31, 2004.” [Emphasis added]; and

-- PWC had chosen to “fire” Loudeye, according to Former Employee #2. [Emphasis added].

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 15

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

42. As a result of the severe limitations on the Company’s operations and its

significant lack of operational and financial controls, the myriad of deals announced regularly

by defendants during the Class Period were negatively impacting the Company and pushing

the Company and its employees to the breaking point, according to a former employee who

worked as a systems engineer during the class period (“Former Employee #2”).

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 15 of 103

43. Because of the numerous, serious internal deficiencies within the Company,

Loudeye could not capitalize upon these agreements and, accordingly, the publication of each

successive agreement was nothing more than a method used by defendants to deceptively

instill investors with confidence in Loudeye.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

The Acquisitions of OD2 and Overpeer Were Never Integrated or Synthesized into the Company

44. In part, as a result of the Company’s significant control deficiencies and other

technological, fiscal, and logistical problems, defendants could not integrate the Company’s

acquired assets, including, in particular, its highly-touted acquisitions of OD2 and Overpeer.

45. Despite defendants’ statements that the Company was achieving growth and

profitability, Loudeye utterly lacked the ability to integrate its assets – logistically, fiscally,

and technologically -- or to support them as non-integrated businesses, in part because of the

Company’s lack of sufficient cash flow from operations and organic internal growth and in

part because some of the acquisitions were incompatible with existing operations, due to

geographically disparate location of operations, and in part because the assets of the

acquisitions were fundamentally flawed.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 16

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

46. The fact that OD2 was never synergized with Loudeye’s platform is confirmed

by reports from two sources. According to OD2 Former Employee #1 who worked at OD2

prior to and after Loudeye’s acquisition, “the OD2 platform was really good. I was never

really sure what Loudeye did to screw it up.” According to OD2 Former Employee #2,

“[i]nitially, after the merger, there was not much impact on OD2 employees. Over time, there

were some “frustrations because processes were not changed for the better soon enough. As

a result, there was poor cooperation between OD2 and Loudeye.” Loudeye “was not doing

well.”

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 16 of 103

47. As further revealed in the Merger Prospectus for the Nokia deal, described

herein below, defendants were never able to integrate OD2, and the combination of the

different technology platforms and content libraries was never possible. Because Loudeye

could not integrate both its platform and its acquired system platforms and because they could

never generate sufficient revenues to support both, Loudeye could not generate sufficient cash

from operations to sustain the Company over the long term. Further, the logistics of running

one half of the incompatible platform in Seattle, Washington and the other half of the

operations in the United Kingdom also proved impossible. In fact, defendants had begun

looking for strategic alternatives well before they belatedly disclosed that they were doing so.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

48. Overpeer, Loudeye’s alleged “anti-piracy/content protection unit” was a colossal

disaster and complete legal and technological liability. Instead of providing the anti-piracy

protections touted by defendants, Overpeer was responsible for poisoning some of the world’s

biggest P2P networks with useless digital audio files that often just play 5 second loops of

songs over and over (or intentionally corrupted files). As noted by PC World in a December

29, 2004 article entitled “Risk Your PC’s Health for a Song,” “by flooding file sharing services

with spoofed files, Overpeer makes finding real music files more difficult.” The Company

abruptly abandoned Overpeer entirely by shutting it down lock, stock, and barrel, exactly one

month after the end of the Class Period. In short, Overpeer’s technology was never able to

function properly independent of Loudeye, thus, defendants knew during the Class Period they

could not successfully integrate Overpeer’s technical platforms with its own.

Employee Turnover and Termination of Entire Accounting Department

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 17

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

49. Employees were surprised by the constant shift in directions, the number of new

ventures, and management’s insistence on pursuing many diverse markets and trying to “grab

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 17 of 103

too many pieces of the pie at once.” Each time after listening to management’s constantly

changing plan, employees would hold water cooler discussions wondering how management

was going to pull off the latest idea. Former Employee #2 noted, “we were way over our

heads” and “employees were very afraid of losing their jobs or of being worked to death.”

There was an “insane amount of work,” according to Former Employee #2.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

50. According to Former Employee #2, employee turnover was a tremendous

problem for the Company as a whole. The average term of employment at Loudeye was just

three months. Management regularly “ramped up” groups, only to fire them all later – at one

point, the entire Company consisted of just 30 employees. A manager named Joe Baldini

participated in the ramping up process. (F.E.#2). During the Class Period, the entire

accounting department was terminated by management and/or resigned. During one point

during the Class Period, Loudeye management “laid off almost the entire company with only

30 people remaining,” according to Former Employee #2. The building was “nearly

vacant.” Later, they “regrew the Company to 150 employees.” (F.E. #2).

51. As a result, it was impossible for trained accounting professionals to properly

oversee the Company’s financial statements and ensure compliance with GAAP and SEC rules,

further enabling defendants’ fraud through the simple removal of proper and adequate

accounting oversight.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 18

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

52. While the accounting department, which used Great Plains Software, consisted

of talented employees, including Fred Angeles, Vonnie Vo, Jenifer Lopez, and Tom Lo, they

were in a situation in which they could not succeed because there was a “legacy of corruption”

that they had inherited. (F.E. #2) There was also an “old boy network” among management.

(F.E. #2). Management was “unethical” (F.E. #1).

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 18 of 103

Phantom Deals 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

53. The Company churned out “phantom deals.” (F.E. #3). For example, the

Company would issue press releases or make statements to the press regarding big names and

touting positive changes for Loudeye when in fact the deals that had been struck were so small

as to be immaterial. (F.E. #3). For example, one “phantom deal” involved Gibson Audio, a

division of Gibson Guitars. (F.E. #3). Another involved a deal with Starbucks Coffee to allow

customers to acquire downloadable music in the physical store. With respect to this deal,

defendant Cavins stated that “"We’re at a tipping point. You are going to see a lot of well-

recognized brands make investments in digital music this year." However, the “investment” by

Starbucks Coffee and touted by defendant Cavins was worth only about $200 dollars to

Loudeye. (F.E. #3).

Defendant Cavins’ Improper Revenue Recognition and False and Misleading Resume, Which Reveals Defendants Knew the Company Was

a Near-Bankrupt Failure Prior To the Inception of the Class Period

54. Defendant Cavins was a “liar” (F.E. #1, who reported directly to Cavins), so

desperate to increase revenue recognition that he actually sold material to which the Company

did not have the rights, according to a Former Employee who worked in sales and business

development during the Class Period (“Former Employee #3). Therefore, improper revenue

was recognized during the Class Period in violation of GAAP and SEC rules.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 19

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

55. Defendant Cavins’ resume, dated October 2, 2005 (just a few weeks after the

end of the Class Period) and obtained by plaintiffs’ counsel in the course of its investigation,

reveals that at the time of his appointment as CEO of Loudeye in March 2003, Cavins knew

that the Company was failing utterly and yet Cavins was responsible for numerous highly

positive, public statements touting the Company beginning no later than May 19, 2003 – just

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 19 of 103

weeks after taking the helm! The resume, attached hereto as Exhibit A, states that Cavins

“[t]ook the business from the brink of bankruptcy and turned it into a leader in the digital

media space. When I arrived, the company had $8M in cash on hand, was burning $6.5M

per quarter, had $13M in long term lease obligations, was being delisted from NASDAQ, had

no strategy, producing $2.7M in quarterly revenue with negative gross margins, very low

employee morale and was experiencing rapid customer flight.”

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

56. Like his false and misleading public statements regarding the Company during

the Class Period, defendant Cavins’ resume also contains the following false description of his

purported accomplishments at Loudeye, which “facts” are belied by the true state of the

Company at the end of the Class Period as described herein: “Since my appointment as CEO

in March 2003, we set strategy, right sized the business fiscally, raised $57M, completed two

strategic acquisitions, expanded the company globally, grew the market capitalization by

more than 1,200% and drove share price increase by more than 775%. The company is now

a highly liquid NASDAQ traded company with a leadership position in the digital media

space.” Despite these representations in Cavins’ resume, Cavins did not right the sinking ship.

In dramatic contrast to the resume’s characterization, instead, after Cavins’ departure, the

Company promptly closed Overpeer (one of the “strategic acquisitions” touted in the resume)

and by the following summer had sold all of its U.S. assets to Muze and merged with Nokia.

The Truth Is Revealed

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 20

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

57. It was only at the end of the Class Period, however, that investors ultimately

learned that the Company was operating well below expectations, that Loudeye could not

support its operations with its cash flow, that Loudeye could not integrate its acquisitions, that

the Company’s restructurings had failed miserably, and that Loudeye was operating without

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 20 of 103

financial and operational controls such that its financial reports and results of operations were

unreliable and untrue. These sudden and shocking disclosures had a material and immediate

impact on the price of Loudeye stock, and following each of these disclosures shares of the

Company declined precipitously - - falling from a Class Period high of almost $30.00 per share

in late-2004, to less than $2.00 per share by the time that defendants announced that the

remaining assets of the Company would be sold to Nokia.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

58. Defendants were motivated to and did conceal the true operational and financial

condition of Loudeye, and materially misrepresented and failed to disclose the conditions that

were adversely affecting Loudeye throughout the Class Period, because: (i) it deceived the

investing public regarding Loudeye’s business, operations, management and the intrinsic value

of Loudeye common stock; (ii) it enabled defendants to raise almost $60 million through the

sale of stock and warrants to private equity investors during the Class Period; (iii) it enabled

defendants also to use almost $25 million of Loudeye’s artificially-inflated shares to purchase

the once-valuable assets of companies such as Overpeer and OD2 during the Class Period; and

(iv) it caused plaintiffs and other members of the Class to purchase Loudeye common stock at

artificially-inflated prices.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 21

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

59. Moreover, in furtherance of this unlawful scheme, plan and course of conduct,

defendants, jointly and individually (and each of them) took the actions set forth herein. These

actions ultimately included negotiating the sale of the Company’s remaining assets to Nokia on

terms that were preferential to the Company’s insiders and under an agreement that provided

Loudeye’s management and former management with freedom from liability for any and all of

the illegal acts and practices complained of herein.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 21 of 103

Defendants’ Materially False and Misleading Statements and Omissions During the Class Period1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

60. On May 14, 2003, at the inception of the Class Period, Loudeye published a

release announcing results for the first quarter ended March 31, 2003, with “Improved

revenues, gross margins and cash usage.” This release stated, in part, the following:

Revenues. Revenues increased by 28% compared to the fourth quarter of 2002 and 2% compared to the year earlier quarter;

Gross Margins. Gross margins as a percentage of revenue improved to 23% in the first quarter of 2003;

Cash and Investments. The Company reported $8.9 million in cash, short-term and restricted investments as of March 31, 2003. The $4.5 million decrease in cash, short-term and restricted investments in the first quarter was a 32% improvement compared to the $6.6 million change in cash, short-term and restricted investments in the fourth quarter 2002. The first quarter 2003 change was primarily due to restructuring items including severance, legal, consulting and lease settlement fees; and

Operational Restructuring and Special Charges. The Company implemented an operational restructuring at the end of the first quarter of 2003 which is expected to reduce future operating costs. Associated with the restructuring, the company recorded special charges of $8.4 million, of which $6.6 million were non-cash. [Emphasis added]. 61. As “evidence” that the Company’s aggressive restructuring plan was purported

to be showing early signs of success, Loudeye’s May 14, 2003 release also quoted the

Company’s CEO, as follows:

“In the first quarter we achieved improved sales bookings and billings and implemented an aggressive restructuring plan which has already resulted in significant cost savings,” said Jeff Cavins, Loudeye’s president and chief executive officer. “We are encouraged by our progress, as we took steps to reduce our cost structure, reduce cash burn and tightly focus our business to deliver better financial results in future quarters.” [Emphasis added.]

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 22

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 22 of 103

62. On or about May 20, 2003, defendants filed with the SEC the Company’s 1Q:03

Form 10-Q for the quarter ended March 31, 2003, signed and certified by defendants Cavins

and Goade. In addition to making statements concerning the Company’s operations and

financial condition the same as or substantially similar to those statements published previously

in the Company’s May 14, 2003 release, the 1Q:03 Form 10-Q also stated, in part, the

following:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Unaudited Interim Financial Data …. The financial information included herein reflects all adjustments (consisting only of normal recurring adjustments) that are, in the opinion of management, necessary for a fair presentation of the results for interim periods. The results of operations for the quarters ended March 31, 2003 and 2002 are not necessarily indicative of the results to be expected for the full years. [Emphasis added.]

63. The Company’s 1Q:03 Form 10-Q also contained representations that attested to

the purported effectiveness and sufficiency of the Company’s controls and procedures. In this

regard, the 1Q:03 Form 10-Q stated, in part, the following:

Item 4 DISCLOSURE CONTROLS AND PROCEDURES We maintain a set of disclosure controls and procedures designed to ensure that information required to be disclosed by us in the reports filed under the Securities Exchange Act, is recorded, processed, summarized and reported within the time periods specified by the SEC’s rules and forms. Disclosure Controls are also designed with the objective of ensuring that this information is accumulated and communicated to our management, including our Chief Executive Officer and Chief Financial Officer, as appropriate to allow timely decisions regarding required disclosure.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 23

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Within 90 days prior to the date of filing this report, we carried out an evaluation of our disclosure controls and procedures under the supervision and with the participation of management including the Chief Executive Officer and Chief Financial Officer. Based upon that evaluation, the Chief Executive Officer and the Chief Financial Officer concluded that our disclosure controls and procedures are effective in timely alerting us to material information relating to the Company required to be included in our periodic SEC filings.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 23 of 103

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

64. At that time, defendants did state that Loudeye would be unable to timely file its

year end 2002 Form 10-K for the year ended December 31, 2002, and its Form 10-Q for the

quarter ended March 31, 2003, however, defendants indicated that the filing delay was not a

significant cause for investor concern. Accordingly, the 1Q:03 Form 10-Q stated, in part, that:

Subsequent to the date of that evaluation, there have been no significant changes in our internal controls or in other factors that could significantly affect internal controls, nor were any corrective actions required with regard to significant deficiencies and material weaknesses. [Emphasis added.]

65. As noted above, the Company’s 1Q:03 Form 10-Q also contained Certifications

by each of defendants Cavins and Goade that attested to the purported accuracy and sufficiency

of Loudeye’s financial and operational controls and procedures, in relevant part as follows:

--Based on my knowledge, this quarterly report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this quarterly report; --Based on my knowledge, the financial statements, and other financial information included in this quarterly report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this quarterly report; --The registrant’s other certifying officer and I … have:

…evaluated the effectiveness of the registrant’s disclosure controls and procedures as of a date within 90 days prior to the filing date of this quarterly report …and

presented in this quarterly report our conclusions about the effectiveness of the disclosure controls and procedures based on our evaluation as of the Evaluation Date;

--The registrant’s other certifying officer and I have disclosed…to the registrant’s auditors and the audit committee of registrant’s board of directors …):

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 24

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 24 of 103

all significant deficiencies in the design or operation of internal controls which could adversely affect the registrant’s ability to record, process, summarize and report financial data and have identified for the registrant’s auditors any material weaknesses in internal controls; and

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

..any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal controls; and

--The registrant’s other certifying officer and I have indicated in this quarterly report whether or not there were significant changes in internal controls or in other factors that could significantly affect internal controls subsequent to the date of our most recent evaluation, including any corrective actions with regard to significant deficiencies and material weaknesses.

66. On June 9, 2003, when defendants announced the addition of President of

Digital Distribution and Development at EMI Recorded Music, Jay Samit, to the Loudeye

Board of Directors, defendants provided more information about the success of the Company’s

purported restructuring. At that time, defendants also stated, in part, the following:

“For years, Loudeye has assembled a strong asset base and has built a digital media distribution infrastructure which I believe will be a vital component to the rising online digital media business,” said EMI’s Jay Samit. “I am pleased to become a member of Loudeye’s board of directors, and look forward to helping guide the Company’s direction and growth as a key outsourced provider of digital media services and infrastructure.” [Emphasis added.]

67. During the second quarter of 2003, defendants also announced the following

deals that were purported to further drive the foreseeable growth and performance of the

Company:

05/21/03 EMI Expands Relationship With Loudeye In Europe For Digital Music Fulfillment

05/28/03 Loudeye Provides Digital Media Services for AOL Online Radio

Products

05/22/03 Loudeye Providing Instant-On Music Samples Using Microsoft’s Windows Media 9 Series

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 25

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 25 of 103

06/03/03 The Orchard Selects Loudeye For Global Digital Music Fulfillment 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

06/16/03 DMI Chooses Loudeye to Enable Digital Music Downloads and

Video Distribution In Japan 07/10/03 Loudeye Announces Strategy to Expand Into Wireless Digital

Music Distribution Market in North America, Europe and Japan 07/09/03 Loudeye Announces QuickClips with Real-Time Analytics

68. The statements contained in Loudeye’s May 14, 2003 release and those

statements contained in the Company’s 1Q:03 Form 10-Q, referenced above, were each

materially false and misleading when made, and were known by defendants to be false at that

time or were deliberately disregarded as such thereby, for the following reasons, among others:

• Loudeye’s Restructuring was not proceeding according to plan and

defendants were not seeing early signs of success. The restructuring was not “already

resulting in significant cost savings” and defendants were not, or should not have been,

“encouraged” by those results.

• Defendants failed to record all proper and necessary charges in

connection with the Restructuring and materially understated the true costs associated with

building the necessary and adequate internal controls and procedures so as to reasonably

assure that the Company’s financial statements and operational reports were prepared in

accordance with Generally Accepted Accounting Principles (“GAAP”) and Securities and

Exchange Commission (“SEC”) rules.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 26

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

• Defendants could not integrate the Company’s acquired assets. Despite

defendants’ statements that the Company was achieving growth and profitability, that the

acquisitions were being synthesized into the Loudeye platform, Loudeye utterly lacked the

ability either to integrate and synthesize these assets or to support them as non-integrated

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 26 of 103

businesses, in part because of the Company’s dramatic lack of sufficient cash flow from

operations and organic internal growth and in part because some of the acquisitions were

incompatible with existing operations, due to location of operations or other hurdles.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

• Loudeye had grossly inadequate systems of internal operational or

financial controls in place. In fact, as defendants would ultimately admit, reporting controls

and operational procedures were so woefully deficient such that Loudeye’s financial and

operational reporting was not true, accurate or reliable. Ultimately, no fewer than eight

material control weaknesses were identified, and PWC, the Company’s auditors, “fired”

Loudeye.

• Defendants materially overstated the Company’s profitability by

underreporting Loudeye’s true financial and operational costs and expenses.

• The Company failed to comply with Sarbanes Oxley.

• Loudeye could not achieve guidance sponsored or endorsed by

defendants.

• As a result of the severe limitations on the Company’s operations and its

significant lack of operational and financial controls, the myriad of deals announced

regularly by defendants during the Class Period were negatively impacting the Company

and pushing the Company and its employees to the breaking point.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 27

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

• Because of the numerous, serious internal deficiencies within the

Company, Loudeye could not capitalize upon these agreements and, accordingly, the

publication of each agreement was nothing more than a method used by defendants to

deceptively instill investors with confidence in Loudeye.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 27 of 103

• The Company churned out “phantom deals.” For example, the

Company would issue press releases or make statements to the press regarding big names

and touting positive changes for Loudeye when in fact the deals that had been struck were so

small as to be immaterial. For example, one “phantom deal” involved Gibson Audio, a

division of Gibson Guitars. Another involved a deal with Starbucks Coffee to allow

customers to acquire downloadable music in the physical store. With respect to this deal,

defendant Cavins stated that “"We’re at a tipping point. You are going to see a lot of well-

recognized brands make investments in digital music this year." However, the “investment”

by Starbucks Coffee and touted by defendant Cavins was worth only about $200 dollars to

Loudeye.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

• Employees were surprised by the constant shift in directions, the number

of new ventures, and management’s insistence on pursuing many diverse markets and trying

to “grab too many pieces of the pie at once.” Each time after listening to management’s

constantly changing plan, employees would hold water cooler discussions wondering how

management was going to pull off the latest idea. One former employee noted, “we were

way over our heads.”

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 28

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

• Employee turnover was a tremendous problem for the Company as a

whole. The average term of employment at Loudeye was just three months. Management

regularly “ramped up” groups, only to fire them all later – at one point, the entire Company

consisted of just 30 employees. During the Class Period, the entire accounting department

was terminated by management and/or resigned. During one point during the Class

Period, Loudeye management “laid off almost the entire company with only 30 people

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 28 of 103

remaining. The building was “nearly vacant.” Later, they “regrew the Company to 150

employees.”

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

• As a result, it was impossible for trained accounting professionals to

properly oversee the Company’s financial statements and ensure compliance with GAAP and

SEC rules, further enabling defendants’ fraud through the simple removal of proper and

adequate accounting oversight.

• While the accounting department consisted of talented employees, they

were in a situation in which they could not succeed because there was a “legacy of

corruption” that they had inherited. There was an “old boy network” among management.

Management was “unethical.”

• Defendant Cavins was so desperate to increase revenue recognition that

he actually sold material to which the Company did not have the rights. Therefore, improper

revenue was recognized during the Class Period in violation of GAAP and SEC rules.

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 29

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

• As revealed in the Merger Prospectus for the Nokia deal, described

herein, defendants were never able to integrate OD2, and the combination of the different

technology platforms and content libraries was never possible. Because Loudeye could not

integrate both its platform and its acquired system platforms and because they could never

generate sufficient revenues to support both, Loudeye could not generate sufficient cash

from operations to sustain the Company over the long term. Further, the logistics of running

one half of the incompatible platform in Seattle, Washington, and the other half of the

operations in the United Kingdom also proved impossible. In fact, defendants had begun

looking for strategic alternatives well before they belatedly disclosed that they were doing

so, and had hired a consultant to find such alternatives no later than July 2005.

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 29 of 103

• Overpeer, Loudeye’s alleged “anti-piracy/content protection unit” was a

colossal disaster and complete legal and technological liability from the start. Instead of

providing the anti-piracy protections touted by defendants, instead Overpeer was responsible

for poisoning some of the world’s biggest P2P networks with useless digital audio files that

often just play 5 second loops of songs over and over (or intentionally corrupted files). The

Company abruptly abandoned Overpeer entirely by shutting it down lock, stock, and barrel,

exactly one month after the end of the Class Period.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

• Defendant Cavins’ resume, dated October 2, 2005 (just a few weeks after

the end of the Class Period) and obtained by plaintiffs’ counsel in the course of its

investigation, reveals that at the time of his appointment as CEO of Loudeye in March

2003, Cavins knew that the Company was failing utterly and yet he was responsible for

numerous highly positive, public statements touting the Company beginning no later than

May 19, 2003 – a mere five weeks after taking the helm! The resume, attached hereto as

Exhibit A, states that Cavins “[t]ook the business from the brink of bankruptcy and turned it

into a leader in the digital media space. When I arrived, the company had $8M in cash on

hand, was burning $6.5M per quarter, had $13M in long term lease obligations, was being

delisted from NASDAQ, had no strategy, producing $2.7M in quarterly revenue with

negative gross margins, very low employee morale and was experiencing rapid customer

flight.

• Like his false and misleading public statements regarding the Company

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 30

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

during the Class Period, defendant Cavins’ resume also contains the following description of

his purported accomplishments at Loudeye, which “facts” are belied by the true state of the

Company at the end of the Class Period as described herein: “Since my appointment as CEO

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 30 of 103

in March 2003, we set strategy, right sized the business fiscally, raised $57M, completed

two strategic acquisitions, expanded the company globally, grew the market capitalization

by more than 1,200% and drove share price increase by more than 775%. The company is

now a highly liquid NASDAQ traded company with a leadership position in the digital

media space.”

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

69. On July 7, 2003, Loudeye published a release announcing that the Company

had achieved purported “Record First Half Operating Metrics.” This release also stated, in

part, the following:

Loudeye Achieves Record First Half Operating Metrics and Expects Improved Second Quarter 2003 Financial Results Anticipates its Best Quarterly Performance in Net Loss and Net Loss Per Share as a Public Company Loudeye Corp. LOUD, a leading provider of services for the management, promotion and distribution of digital media, today announced record first half operating metrics serving more than 370 million digital music samples and 6.5 million encoded files to its customers. Additionally, the Company announced it expects second quarter 2003 financial results to include improved net loss and net loss per share results.

* * * As a result of this record operating performance in combination with a focused strategic plan, for the second quarter 2003 Loudeye anticipates that it will report its best quarterly financial performance as a public company in terms of net loss and net loss per share. This anticipated performance primarily reflects improvement in gross margins and reductions in operating expenses and special charges. In addition, the company expects to report that its total cash, short-term and restricted investments at the end of the second quarter 2003 increased from the end of the first quarter 2003, due primarily to its focused cost savings initiatives, improvements in gross margins, working capital financing and cash management programs….

AMENDED CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATION OF FEDERAL SECUIRITIES LAWS (CASE NO. C06-1442 MJP) - 31

KAHN GAUTHIER SWICK, LLC 12 E. 41st Street, 12th Floor

New York, New York 10017 TEL. 212.920.4310 • FAX 504.455.1498

The financial and operating results reflect the increasing demand for outsourced digital media services and the growing use of digital media among online retailers, music subscription and download services, record labels,

Case 2:06-cv-01442-MJP Document 17 Filed 03/09/07 Page 31 of 103

portals, wireless carriers and other companies building a business or brand around digital music or film. 1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16