Embed Size (px)

Citation preview

The Cyclical Behavior of Net Interest Margins:

Evidence from the United States Banking Sector

Roger Aliaga-Dıaz∗and Marıa Pıa Olivero†

Preliminary version, comments welcome.

July 2005

AbstractThe paper studies the cyclical behavior of net interest margins

(NIMs) in the United States banking sector, using time series quarterlydata for the period 1979-2005. It documents the countercyclicality ofNIMs and offers potential explanations for this behavior.

Even controlling for important changes in banking regulation thattook place in this period, monetary policy certainly plays a role in ex-plaining the countercyclical behavior. Other determinants are interestrate risk and the economy’s financial depth. At the bank-level, banksliquidity, capital holdings and the share of total assets held by big banksalso exert a significant impact on margins over the cycle. These con-clusions are consistent across several alternative definitions used forNIMs and three different business cycle indicators.

Our results provide support to the bank lending channel of mon-etary policy and to the hypothesis that the effects of monetary policyare weaker in more concentrated banking sectors.

JEL Classification: C32, E32, E44, G21

∗North Carolina State University, Raleigh, NC, 27695. [email protected]†LeBow College of Business, Drexel University, 3141 Chestnut Street, Philadelphia,

PA, 19104. [email protected]

1

1 Introduction

Total loans and leases granted by commercial banks in the United States

averaged almost 45% of gross domestic product in 2004 and the first quarter

of 2005. This figure has been steadily increasing over time1. The ratio of

loans to total bank assets has fluctuated around 60% since 1973. Therefore,

financial sector deepening, if any, does not seem to have lowered the impor-

tance of loans in banks’ portfolios. Both facts are indicative of the relevance

of studies focusing on the market for bank credit in the American economy

and particularly, on its macroeconomic impact.

This paper studies the cyclical behavior of net interest margins (NIMs)

in the United States banking industry, using time series quarterly data for

the period 1979-2005. Our results document the countercyclicality of NIMs.

The contemporaneous sample raw correlation between NIMs and alternative

business cycle indicators is significantly negative in our data. This negative

negative relationship is robust to the inclusion of controls related to monetary

policy, default risk and banking regulation, which are suggested to be the

main determinants of this cyclical behavior.

The paper also offers alternative explanations for the observed behavior.

The business cycle measure loses its explanatory power after an expanded set

of controls is included in the regression of NIMs against a business cycle indi-

cator. This set consists of both macroeconomic and bank-level determinants,

and it completely explains the cyclical behavior of NIMs. Interest rate risk,

the economy’s degree of financial deepening, banks liquidity, capital holdings

and the share of total assets held by big banks all exert a significant impact

on margins.

These conclusions are robust to several alternative definitions for the mar-

1The figure was around 10% in 1947, the first year for which we have data. It was 38%

in 1980.

2

gins and the cycle measure.

Our results have interesting policy implications due to their macroeco-

nomic impacts. When markups vary endogenously in response to aggregate

productivity shocks, which have no direct relation to market structure, their

variation becomes an additional channel through which such shocks can affect

economic activity (Rotemberg and Woodford (1995)). With spreads in the

market for credit being countercyclical according to our results, a financial

accelerator seems to be operating in the American economy. Credit becomes

more expensive in bad times; firms may as a result delay investment and

production decisions and the recession may be made even worse. This may

call for stabilization policies to be made more effective in economies where

these spreads are more countercyclical.

The determinants of margins in the banking sector have been theoreti-

cally studied before. Ho and Saunders (1981) and Saunders and Schumacher

(2000) model procyclical spreads in the market for bank credit. Theirs is a

microeconomic model of banks operating as risk averse dealers. The NIM is

composed of two elements: a producer’s surplus or monopoly rent term, and

a risk adjustment term2. Allen (1988) extends the Ho and Saunders (1981)

model by studying a banks portfolio effect on spreads. She looks at how the

cross-price elasticities of demand among various bank products affect that

pure interest spreads. Wong (1997) develops a model with both credit and

interest rate risk to determine optimal bank NIMs.

Other papers study the empirical determinants of NIMs. Angbazo (1997)

studies the relationship between default and interest rate risk and net interest

margins. Demirguc-Kunt and Huizinga (2000) analyze the effect of financial

development and bank performance on profitability and margins. Angelini

and Cetorelli (2003) look at the impact of regulatory reforms, large scale

2The latter is a function of the banks’ coefficient of absolute risk aversion, the volume

of transactions and the variability of interest rates on deposits and loans.

3

consolidation and competitive pressure on the structure of the Italian bank-

ing industry. Demirguc-Kunt, Laeven and Levine (2004)) study the impact

of bank regulations, market structure and institutions on banks’ efficiency

measured by both NIMs and overhead expenditures.

However, to our knowledge the cyclical behavior of NIMs has been previ-

ously analyzed only by Dueker and Thornton (1997). Thus, we believe this

study is an important empirical contribution. Dueker and Thornton’s frame-

work is significantly different from ours. They build a model with switching

costs for customers and risk averse banks that lead to countercyclical markups

in the pricing of bank loans. They find evidence for loan rates exhibiting a

countercyclical spread over the marginal cost of funds for banks3.

The paper is also closely related to the theoretical literature that mod-

els oligopolistic markets and how various types of strategic interaction may

lead to different patterns for prices and markups. In this work, dynamic

general equilibrium models are used to study the cyclicality of price-cost

margins. The reasons for markups being countercyclical there are, among

others, implicitly colluding oligopolies that find collusion more difficult when

their demand is relatively high (Rotemberg and Saloner (1986)), demand

composition effects such that some types of increases in aggregate demand

imply a procyclical elasticity faced by oligopolistic firms (Gali (1994)), and

“deep habit” formation that allows the demand faced by each individual

producer to depend on past consumption levels, and the price elasticity of

demand to be procyclical (Ravn, Schmitt-Grohe and Uribe (2005)).

Last, our work is related to the vast empirical literature developed after

3Angelini and Cetorelli (2003) include the growth rate of GDP among their regressors

and find a negative impact on both price-cost margins and Lerner indexes in Italy. In

their cross-country study of the impact of bank regulations, market structure and institu-

tions, Demirguc-Kunt, Laeven and Levine (2004) find that economic growth is negatively

(although only weakly) associated with NIMs.

4

Rotemberg and Saloner’s first contribution that measures the cyclicality of

markups in goods markets (Domowitz et al. (1986), Lebow (1992), Chevalier

and Scharfstein (1995 and 1996), Galeotti and Schiantarelli (1998), Bloch and

Olive (2001), Campello (2003), among others).

There are of course explanations for the countercyclical behavior of NIMs

alternative to those offered in this paper. These are more difficult to quan-

tify but future work could try to incorporate them. The first relates to the

banks owners’ preference structure. When adjusting interest rates down-

wards during recessions, banks face the trade-off between profits and market

share. As explained in Dueker and Thornton (1997), if firms with market

power have preferences for smoother profit streams, in recessions they may

smooth profits by charging relatively high prices. The second involves issues

of asymmetric information in the lender-borrower relationship. Banks face

adverse selection when they increase their market share during downturns:

they are faced to borrowers with bigger default probabilities. Therefore, they

may need to increase markups over their marginal costs. Third, the “degree

of market power” may be countercyclical in itself. Forbes and Mayne (1989)

present evidence on the procyclicality of the elasticity of the demand for

credit faced by banks. Fourth, Allen (1988) studies a banks portfolio effect

and extends the Ho and Saunders (1981) model. She shows that pure in-

terest spreads can be reduced when considering the cross-price elasticities of

demand among various bank products. Last, costs of collusion may increase

during economic expansions, as in Rotemberg and Saloner (1986).

The paper proceeds as follows. A review of background literature is pre-

sented in Section 2. A reduced form model for margins is discussed in Section

3. Section 4 describes the econometric methodology and the data used. The

results are shown in Section 5. The last section concludes and outlines some

directions for further research. A detailed description of the data and ex-

tended results are provided in the appendices. The results of some robustness

5

checks can be found in Appendix C.

2 Background Literature

The traditional industrial organization approach states that price wars occur

in recessions. Markups are procyclical as a result. For example, in the

customer market model of Phelps and Winter (1970), a firm that lowers its

current price not only sells more to its current customers, but also expands

its customer base. An increase in aggregate demand implies that profits

rely mainly on current sales and that increasing market shares is relatively

unimportant. Therefore, firms raise their prices in periods of high aggregate

demand, and price-cost margins are directly related to the level of economic

activity.

Rotemberg and Saloner (1986) challenge this view on both theoretical and

empirical grounds. They study the response of oligopolies to fluctuations in

the demand for their goods. The strength of their paper is in their model

that can account for firms behaving more competitively in periods of high

demand. They study implicitly colluding oligopolies4, that find this collusion

more difficult when their demand is relatively high. In booms, there is a larger

gain for a particular firm from lowering the price from the profit maximizing

price for the group. The firm can work with a bigger market by doing so.

The punishment for not cooperating is less affected if it is in the future,

when demand returns to its normal level. The authors also examine the

macroeconomic effects of a shift in demand towards the oligopolistic sector.

In a two-sector model where the other sector is competitive and uses the

4James Friedman (1971) first modeled this type of oligopolistic market where price is

the strategic variable, and where firms threat to revert to competitive behavior whenever

a single firm deviates from oligopolistic pricing. This threat induces cooperation by all

firms.

6

oligopolistic sector’s output as an input, the competitive sector’s output also

increases in periods of high demand5.

Theoretically, countercyclical markups also arise in Gali (1994) and Ravn,

Schmitt-Grohe and Uribe (2005).

Gali (1994) models demand composition effects. Both households and

firms purchase the goods produced by an oligopolistic sector, but they have

different elasticities of substitution between various goods. In this model,

some kinds of increases in aggregate demand, those that imply a change

in its composition, may imply countercyclical markups and have additional

expansionary impacts as a result6.

In Ravn, Schmitt-Grohe and Uribe (2005) agents exhibit “deep habit

formation”. They form habits over individual varieties of goods as opposed

to over a composite consumption good. This allows the demand function

faced by each individual producer to depend on past consumption levels,

and the price elasticity of demand to be procyclical7.

Ho and Saunders (1981) and Saunders and Schumacher (2000) model

margins in the market for bank credit. NIMs are procyclical in their frame-

work. Theirs are microeconomic models of banks operating as risk averse

dealers. The NIM there is composed of two elements: a producer’s surplus

or monopoly rent term, and a risk adjustment term. The latter is a function

of the banks’ coefficient of absolute risk aversion, the volume of transactions

and the variability of interest rates on deposits and loans. The larger the size

of transactions, the bigger NIMs are according to their specification. How-

ever, in their empirical estimation they concentrate on the effects on margins

of market structure and volatility. They do not look at the impacts of risk

5Rotemberg and Woodford (1992) also work with the implicit collusion model.6In Gali (1994) the inefficiency wedge is a monotonically decreasing function of the

share of investment spending in value added.7The demand is composed by both an elastic term (Ct) and an inelastic term (Ct−1).

The share of the latter falls in expansions.

7

aversion and transaction size because of problems in estimating these two.

Ho and Saunders (1981) do show that smaller banks have a one third of a

percent larger spread than bigger banks. However, they argue that this is

due to market structure conditions that allow smaller banks to earn some

additional monopoly profits, and not due to differences in the size of trans-

actions. Allen (1988) studies a banks portfolio effect and extends the Ho and

Saunders (1981) model. She shows that pure interest spreads can be reduced

when considering the cross-price elasticities of demand among various bank

products. Wong (1997) develops a theoretical model with both credit and

interest rate risk to determine optimal bank NIMs. He shows that the op-

timal margin is positively related to market power, operating costs and the

degree of both interest rate and credit risk. The effect of the Federal funds

rate depends on the bank’s net position in the interbank market.

In Olivero (2004) countercyclical price-cost margins in an oligopolistic

market for bank credit arise from a procyclical interest rate elasticity of the

demand for loans.

In Aliaga (2005) the countercyclicality of spreads in bank credit arises

there as result of capital adequacy regulations becoming more binding in

periods of depressed aggregate demand, when higher default lowers banks’

equity. Due to the fact that the cost of equity financing exceeds that of

deposits, this makes the financial cost of funds and the margin increase in

recessions. The spread charged by banks behaves countercyclically as a re-

sult.

A vast empirical literature has evolved after Rotemberg and Saloner’s first

contribution. Several papers have developed thorough econometric analyses

of the cyclical behavior of markups in industrial sectors (Domowitz et al.

(1986), Lebow (1992), Chevalier and Scharfstein (1995 and 1996), Galeotti

and Schiantarelli (1998), Bloch and Olive (2001) and Campello (2003), among

others).

8

However, a big gap in the literature is discovered when looking for this

type of evidence on cyclicality in financial markets. The only exception is

Dueker and Thornton (1997) who find evidence for loan rates exhibiting a

countercyclical spread over the marginal cost of funds for banks. Based on

Klemperer (1995), they outline a model with switching costs for customers

and risk averse banks, which both lead to countercyclical markups in the

pricing of bank loans. They use the spread between the prevailing prime rate

and the 180-day certificate of deposit rate. As business cycle indicators they

use both the spread between the commercial paper and the Treasury bill rate8

and the slope of the yield curve. However, they do not provide explanations

for the countercyclicality, nor do they control for macroeconomic or bank-

level factors that might affect spreads.

Some papers explore the determinants of NIMs in general. Angbazo

(1997) uses Call Report data over the period 1989-19939 to study the re-

lationship between default and interest rate risk and net interest margins10.

He also investigates the impact of credit market cycles on net interest mar-

gins. The motivation in this case is that credit contractions may affect mar-

gins because of either loan or deposit rate stickiness. Last, he studies the

effect of off-balance sheet instruments on the size and volatility of margins

and on the portfolio risk of banking organizations. His results indicate that

bank interest margins reflect both default and interest rate risk premium,

although significantly differently across bank sizes. Off-balance sheet activ-

ities generate higher margins to compensate for the increased interest-rate

and liquidity risks that they imply. To study the impact of credit cycles on

margins, he evaluates the coefficient on a dummy variable for a particular

subperiod characterized by an increase in charge-offs rates and by a credit

8They argue that this spread is a useful predictor of economic activity.9Their sample includes 286 commercial banks with assets of $1 billion or more.

10The used measure is constructed to reflect a bank’s repricing or maturity gap.

9

contraction in bank lending. The coefficient indicates a significant negative

effect of bank lending contraction on margins.

Demirguc-Kunt and Huizinga (2000) study the relationship between fi-

nancial development and bank performance, profitability11 and margins. They

use bank level data for a large cross-section of countries differing widely in

the extent to which their firms rely on bank-based or market-based financing.

In their analysis of net interest margins, they find no statistically significant

impact of macroeconomic variables, except for inflation12.

Demirguc-Kunt, Laeven and Levine (2004) use data on commercial banks

for 72 countries averaged over the 1995-1999 period to study the impact of

bank regulations, market structure and institutions on banks’ efficiency mea-

sured by both net interest margins and overhead expenditure ratios to total

assets. They control for both bank specific factors13 and macroeconomic

conditions. They control for inflation and the level of equity market develop-

ment since equity may be considered as a substitute to bank lending. Based

on the conjecture that there may exist a positive relationship between the

cycle and business opportunities available to banks, they also include GDP

growth among their controls arguing that business cycle fluctuations might

affect the cost of intermediation. They also use GDP per capita as a general

indicator of institutional development. Among other things, they find that

bank concentration raises margins when controlling for bank-specific factors14

11They measure profitability as the ratio of banks profits to assets.12Their macroeconomic controls include GNP per capita, the growth rate, the tax rate

on banks profits and inflation.13They control for cross-country differences in the banks ability to conduct securities

market, insurance, and real estate operations, and whether banks can own nonfinancial

firms, the degree of state-ownership of commercial banks, bank size, the liquidity of as-

sets, the degree to which banks raise income through fees and commissions, the standard

deviation of each banks return on assets, and the market share of each bank.14This relationship breaks down when controlling for regulatory restrictions on banks

and macroeconomic stability.

10

and that regulatory restrictions increase margins15. Regarding the macroe-

conomic determinants of spreads, their results are as follows. First, higher

inflation is associated with higher margins. Second, economic growth is neg-

atively (although only weakly) associated with net interest margins. Third,

the total value of domestic equity traded enters negatively and significantly

in the regression. Fourth, the degree of state ownership of the banking in-

dustry is positively linked with net interest margins. As a robustness check,

they include all the macroeconomic and financial sector indicators simulta-

neously with bank concentration and bank-specific controls. There inflation

stays as a significant determinant of margins, while the other macroeconomic

controls are no longer significantly correlated with net interest margins.

Angelini and Cetorelli (2003) look at the impact of regulatory reforms,

large scale consolidation and competitive pressure on the structure of the

Italian banking industry. They include the growth rate of GDP as one of

the controls in their estimation of both price-cost margins and Lerner in-

dexes16, and show its negative impact on both, even after controlling for

other variables that might influence competitive conditions in financial mar-

kets, inflation, countercyclical monetary policy and default risk of loans.

This paper looks in the banking sector for evidence of the countercyclical

price-cost margins modeled in the theoretical literature. It also seeks to

complement the empirical work that studies the cyclicality in goods markets

and to document a stylized fact with important macroeconomic implications.

Last, it offers some potential explanations to this countercyclical behavior.

15However, this is no longer true when controlling for factors related to broader national

institutions.16The Lerner index is defined as the ratio of the difference between price and marginal

cost to the price.

11

3 A Reduced Form Model for NIMs

The regression specification for NIMs that will be used in the empirical sec-

tion is shown in equation (1).

yt = α + βlog(Xt) +K1∑i=1

γiZi,t +K2∑i=1

δiRi,t +3∑

i=1

θiQi,t + εt (1)

where y is the NIM measure and X is the business cycle indicator. Both

macroeconomic and bank-level controls are included in the Z matrix, banking

regulations dummies are measured by the R matrix, and seasonal dummies,

by Q.

The set of controls in Z is conjectured as potential determinants of the

countercyclical behavior of NIMs evidenced by the sample correlations shown

in Table 1 below. They are all introduced next in subsections 3.1 and 3.2.

Table A.5 in Appendix A shows the correlations of each of these controls

with GDP per capita and both total and C&I loans.

12

3.1 Explaining the Countercyclicality: Macroeconomic

Determinants

Monetary Policy:

Several measures for the stance of monetary policy have been suggested

in the literature. The “Romer dates” type of measures (Romer and Romer,

1990 and Boschen and Mills, 1991) look at the monetary authority decisions

through its Federal Open Market Committee minutes. However, as pointed

out in Kashyap, Stein and Wilcox (1993), this implies looking at just a few

isolated episodes and valuable information can be lost this way. Alternatively,

Bernanke and Blinder (1992) argue that the federal funds rate is a fairly good

indicator. Thus, this last measure is used here.

The expected effect of the federal funds rate on NIMs needs to be assessed

first. As suggested in Angelini and Cetorelli (2003), interest rates on banks

liabilities are characterized by more inertia than those on assets, so that

monetary policy shocks to interest rates should be associated with increased

margins. Hannan and Berger (1991) and Neumark and Sharpe (1992) also

find evidence for the rigidity of deposit rates.

Another rationale for a positive coefficient on the federal funds rate is

given by the bank lending channel of monetary policy (Kashyap, Stein and

Wilcox, 1993; Kashyap and Stein, 1997 and Kashyap and Stein, 2000). Banks

can react to a fall in reserves due to a contractionary monetary policy by

relying more on non-reservable liabilities, such as certificate of deposits, to

finance loans. However, these alternative funds are not covered by deposit

insurance17 and thus, banks may choose to not fully offset the effects of the

policy, and they may let lending fall as a result. This effect occurs on top

of the contraction in loans derived from a lower demand for credit. Spreads

can be expected to increase with lending falling. Kashyap and Stein (2000)

17Leaving the bank exposed to credit risk

13

argue that under the lending view of monetary policy, the Federal Reserve

can affect not only Treasury bill rates but also the effective NIM.

Next, with this positive effect of the federal funds rate on NIMs in mind,

the role played by monetary policy in determining the cyclicality of NIMs

has to be considered. Changes to the quantity of money and hence to the in-

terest rate exert two opposing forces on the cyclical behavior of spreads. On

the one hand, the level of economic activity is partly the result of monetary

policy. When output is high (low) as a result of an expansionary (contrac-

tionary) monetary policy, the federal funds rate and NIMs are low (high),

and monetary policy explains the countercyclicality of the spreads. On the

other hand, with monetary policy playing a stabilization role, an increase (a

fall) in the federal funds rate during a boom (recession) will cause NIMs to

increase (decrease). In this case, the countercyclicality of NIMs should be

explained with the help of factors other than monetary policy, as it would

imply procyclical NIMs.

While the level of economic activity is expected to respond with lags to

monetary changes, the federal funds rate is likely to react instantaneously

to the cyclical movements of the economy. Thus, to thoroughly account for

the effects of monetary policy, both the current and the lagged values of the

federal funds rate are used as controls. Up to four lags of the federal funds

rate were also included in the regression as a robustness check. This implied

no important changes in our results18.

Additionally, two different interaction variables are constructed with the

goal of appropriately measuring the total impact of monetary policy on bank

margins.

The first is built as the product of a measure of the liquidity of banks

balance sheets19 and the federal funds rate. Gibson (1996) finds that the

18See Appendix C for a discussion of this robustness check.19The liquidity measure used is the same that is included later as a bank-level determi-

14

macroeconomic effects of monetary policy are stronger when banks in the

aggregate hold less liquid portfolios. In their cross-sectional study, Kashyap

and Stein (2000) find that the impact of monetary policy on lending is weaker

for banks with more liquid balance sheets, as they can react to a fall in re-

serves due to a contractionary monetary policy and protect their loan port-

folios by drawing from the buffer of cash and securities. They find this to

happen mainly for small banks that do not have access to alternative unin-

sured external financing. For them the liquidity of the balance sheet is key

to determine their response to the policy shock. Conversely, for larger banks,

they find a positive and significant effect of liquidity on the strength of mon-

etary policy. Aggregate data for the entire size distribution of banks is used

in this study, and bigger banks with almost to perfect access to uninsured

sources of finance are more heavily weighted. Therefore, our results can be

expected to reproduce theirs for the case of big banks.

The second variable is the interaction between a concentration measure

given by the Herfindahl-Hirschman index in the market for total loans and

the federal funds rate. Peltzman (1969) develops a theoretical model that

relates market structure in banking to the transmission of monetary policy.

Cottarelli and Kourelis (1994) find that entry barriers slow policy transmis-

sion, although they do not find significant effects from differences in market

concentration. More recently, Adams and Amel (2005) study the relation-

ship between banking competition and the transmission of monetary policy

through the bank lending channel, and find that the impact of monetary

policy is weaker in more concentrated markets. Of course, the structure of

the banking industry does not change dramatically on a quarterly basis or

even at business cycle frequencies. Therefore, while we do expect a negative

sign for the coefficient on this regressor, we think it might be not significant.

nant of the cyclicality of NIMs.

15

Default or Credit Risk:

The lagged value of the net charge-off rate defined as loan charge-offs20

net of loan recoveries as a percentage of total loans is used as a measure of

the degree of default or credit risk in the economy.

Optimally chosen margins should be enough to cover the cost of increasing

the bank’s capital as risk exposure increases. Thus, an increase in the econ-

omy’s default rate on loans should imply an increase in the spread charged

by commercial banks. If, as expected, a higher credit risk is associated with

periods of low economic activity, default is a very important candidate to

explain the countercyclical behavior of spreads21.

However, we are not particularly concerned about risk with any of our

margin measures. All our margins use ex-post interest rates on loans, cal-

culated using the actual income obtained by banks after accounting for bad

loans. Actually, for these measures, a negative sign can be expected for the

coefficient on the risk variable. Angelini and Cetorelli (2003) use price-cost

margins similar to ours for the Italian banking sector and expect a negative

sign for the coefficient on the ratio of bad and doubtful loans to total assets.

An increase in the share of these loans can imply a fall in the income measure

used to compute ex-post NIMs. The spread between the bank prime and the

Treasury bill rates, also used as one of our margin measures, is an ex-ante

variable22. However, credit risk should not play an important role even in

20Charge-offs are the value of loans removed from the books and charged against loss

reserves.21The contemporaneous correlation of GDP per capita (GDPpc), total loans and com-

mercial and industrial (C&I) loans with the default measure are -0.21, 0.05 and 0.13,

respectively. With the lagged value of the charge-off they are -0.22, -0.13 and -0.01. See

Table A.5 in Appendix A.22It is calculated using cited interest rates series as opposed to banks actual interest

income.

16

this case. Both rates used to calculate this spread include only a small risk

premium, if any.

Alternative regressions were run where the delinquency rate23, the loss

rate24 and the Baa-Treasury bond spread25 were used as measures of default

risk. This implied no important qualitative differences with our results.

Interest Rate Risk:

Previous studies have shown both theoretically and empirically the impor-

tance of accounting for interest rate risk (Ho and Saunders (1981), Saunders

and Schumacher (2000) and Demirguc-Kunt, Laeven, and Levine (2004)).

The idea is that banks may charge a premium to hedge against this type of

risk.

Thus, the volatility of short-term interest rates is included among the

regressors as a proxy for the interest rate risk faced by banks. Following

Saunders and Schumacher (2000), the measure used is the standard deviation

over each quarter of the weekly series for the 3-month Treasury bill rate. If

the risk measure and NIMs are positively correlated, a countercyclical risk

measure can explain the countercyclicality of margins.

Both the contemporaneous and the lagged values are included based on

the fact that the lagged measure is the one that is negatively correlated at

business cycle frequencies with our business cycle indicators26. The volatility

of interest rates has been suggested as a useful leading indicator of economic

23According to the Federal Reserve’s definition, delinquent loans and leases are those

past due thirty days or more and still accruing interest as well as those in non-accrual

status.24Defined here as the ratio of loans loss allowances to total loans.25Stock and Watson (1990) suggest that this spread is a useful indicator of the default

risk prospects on private debt.26The volatility of the Treasury Bill rate is negatively correlated with GDP contempo-

raneously too.

17

activity. Interest rate volatility hampers investment and lowers consumer

confidence, exerting a negative effect on GDP levels. Thus, high volatility

increases the probability of a future recession. This explains the counter-

cyclicality of the volatility measure.

The Economy’s Financial Deepening:

An indicator of the degree of financial depth in the economy is included

among the controls.

A negative sign is expected for the coefficient on this regressor because

a deeper financial sector should imply a bigger availability of substitutes to

bank credit. Banks should therefore need to charge lower spreads.

Demirguc-Kunt and Huizinga (2000) show evidence that countries with

underdeveloped financial systems that move towards more development see

bank profitability and margins fall. However, once they control for bank

and market development, they cannot find independent effects on margins of

financial structure per se.

Following Kashyap, Stein and Wilcox (1993), this degree is measured as

the ratio of commercial paper issued by the nonfarm nonfinancial corpo-

rate business sector to the sum of commercial paper and bank loans for the

nonfarm nonfinancial corporate business and nonfarm noncorporate business

sectors. The lagged value of the variable is used, based on this measure

being more procyclical than the contemporaneous counterpart. With this

procyclicality and with a negative expected coefficient, the inclusion of fi-

nancial depth as a control should help in explaining the countercyclicality of

NIMs.

One explanation for the procyclicality can be found in Kashyap, Stein

and Wilcox (1993). They show that a monetary contraction makes this

financial deepening indicator increase as bank lending decreases by more

than commercial paper. Thus, high federal funds rates in periods of high

18

output levels (i.e. a countercyclical monetary policy) can explain the cyclical

pattern of this variable.

Supply of Funds:

The supply of deposits available to banks is used as a proxy for their

marginal cost of funds. Given that deposits are procyclical, the marginal cost

can be expected to be countercyclical. If costs and margins are positively

related, this can provide an explanation for countercyclical NIMs27.

Inflation:

Banks might require higher risk premia when inflation or nominal interest

rates are high. Huybens and Smith (1999) argue that inflation may make

informational asymmetries stronger and lead to higher NIMs. Boyd, Levine

and Smith (2001) find a significant, economically important and negative re-

lationship between inflation and banking sector development. In turn, lower

development can be conjectured to derive in increased net interest margins.

Saunders and Schumacher (2000) present evidence for margins increasing

with higher interest rate volatility, which can be associated with high and

variable inflation. Demirguc-Kunt and Huizinga (2000) provide support to

the fact that banks profits increase in inflationary environments. Demirguc-

Kunt, Laeven and Levine (2004) show that inflation has a robust, positive

impact on bank margins and overhead costs. For Italy, Angelini and Cetorelli

(2003) document a negative effect of inflation on price-cost margins, though.

Therefore, changes in the consumer price index (CPI) are included as a

regressor even though all our variables are measured in real terms. Given

27It would be interesting to extend the paper by including alternative measures of the

operative costs of banks. Data on non-interest expenses, banks’ spending on furniture and

equipment and salaries and benefits are available from the Call Reports on Condition and

Income data.

19

the negative correlation between economic activity and inflation at business

cycle frequencies, a direct relationship between inflation and margins might

provide another explanation for the countercyclical behavior of the latter.

3.2 Explaining the Countercyclicality: Bank-Level Ex-

planations

Liquidity:

The ratio between cash and total investment securities to total assets

is introduced among our regressors as a measure of aggregate liquidity for

banks28.

Demirguc-Kunt, Laeven and Levine (2004) find evidence that banks with

more liquid assets have lower net interest margins. The intuition there is that

banks with high levels of liquid assets in cash and government securities may

receive lower interest income than banks with less liquid assets. If the market

for deposits is reasonably competitive, then greater liquidity will tend to be

negatively associated with interest margins. Angbazo (1997) finds that as

the proportion of funds invested in cash or cash equivalents increases, banks

liquidity risk29 declines and leads to a lower liquidity premium in net interest

margins.

On the contrary, it could also be argued that when banks choose to hold

28See data appendix for definition. Kashyap and Stein (1997) define liquidity for each

bank as the ratio of cash plus securities plus federal funds sold to total assets. Due to

the lack of data on federal funds for several periods, we depart slightly from them and

define it as cash plus securities over total assets. The aggregate measure is calculated as

the weighted average across banks, with the weights given by each bank’s share in total

assets for each period.29This is the risk of not having sufficient cash or borrowing capacity to meet deposit

withdrawals or new loan demand, thereby forcing banks to borrow emergency funds at

excessive cost. The analysis uses the ratio of liquid assets to liabilities to proxy for liquidity

risk.

20

more liquid portfolios, they pay for the cost of that liquidity by raising their

margins. Ho and Saunders (1981) and Saunders and Schumacher (2000) de-

velop a model where banks charge spreads that are mainly fees in order to

provide what they call “immediacy services”. Theirs is a dealership frame-

work where risk-averse banks charge a cost for the immediate provision of

deposits and loans. In their model banks have to temporarily invest funds

in the money market whenever a deposit arrives at a time different from a

new loan demand, and they face a reinvestment risk if the short term rate

falls. If banks face a demand for a new loan without a contemporaneous

supply of new deposits, they need to borrow temporarily in the money mar-

ket, facing a refinancing risk should the short term interest rate go up. The

spread compensates banks for bearing this risk. Holding more liquid assets

can be viewed as an alternative to having to resort to the money market to

provide these “immediacy services”. Therefore, we think this model provides

a rationale for a positive relationship between margins and banks liquidity.

If the positive effect of liquidity on NIMs is stronger, cyclical changes in

liquidity can provide another explanation for the countercyclicality of mar-

gins. This is because all our measures of economic activity and our liquidity

measure are negatively correlated. Therefore, more economic activity which

is related to lower liquidity, lowers the cost of it for banks and allows NIMs

to shrink.

The countercyclicality of balance sheet liquidity can be easily explained

by the fact that, in recessions, credit risk increases more for risky and illiquid

assets, such as loans, than for more liquid assets such as government securi-

ties. It is natural then to think that these risk-return considerations result

in banks shifting their asset portfolio toward more liquid assets during bad

times. Also, banks opportunity cost of holding more liquid and less profitable

assets falls in recessions when there are fewer investment opportunities.

21

Banks Capital Holdings:

Another control is the ratio of total equity capital to total loans. The

goal here is to control for the effect of capital requirements for banks. After

the Basle Accords of 1988 banks are required to hold a minimum of capital

as a percentage of risk weighted assets. However, the lack of data on risk

weighted assets for each bank prevent the use of that measure30. Total loans

are used instead bearing in mind that loans are one of the riskiest assets in

banks’ portfolios.

There is empirical evidence that banks hold capital against credit risk

in excess of the minimum 8% of total risk weighted assets required by the

Accords. In our sample equity represents 14% of loans. According to the

Bank of International Settlements, with the adoption of the Basle standards,

the average ratio of capital to risk-weighted assets of major banks in G-10

countries rose from 10% in 1988 to 11% in 1996.

Given that due mainly to taxation issues, holding equity is costly relative

to debt, banks may need to charge higher margins to finance this extra cost.

Hellman, Murdock and Stiglitz (2000) present a context that provides an

alternative story for capital requirements to increase margins. They show

that when capital requirements increase banks cost of funding, they lower

the franchise value of banks and this increases the incentives to excessive

risk-taking. Last, Demirguc-Kunt, Laeven and Levine (2004) argue that

highly capitalized banks have lower bankruptcy risks and lower funding costs

and that they therefore charge higher NIMs when interest rates on loans are

insensitive to equity.

The capital to assets ratio is countercyclical in our sample period. Thus, if

as expected an increase in the ratio implies an increase in margins, the inclu-

sion of this regressor in our set of controls can explain the countercyclicality

30Data on risk capital and risk-adjusted assets are available from the Report of Condition

and Income data only after 1991.

22

of margins.

The cyclical pattern of capital to assets ratio is the result of two opposing

forces. On the one hand, since loan default and delinquency rates tend

to increase during recessions, and since they both negatively affect banks

equity, the numerator of the ratio moves in a procyclical fashion. On the

other, demand for credit is highly procyclical and thus the ratio should move

countercyclically. As stated above, the second effect seems to dominate in

our sample.

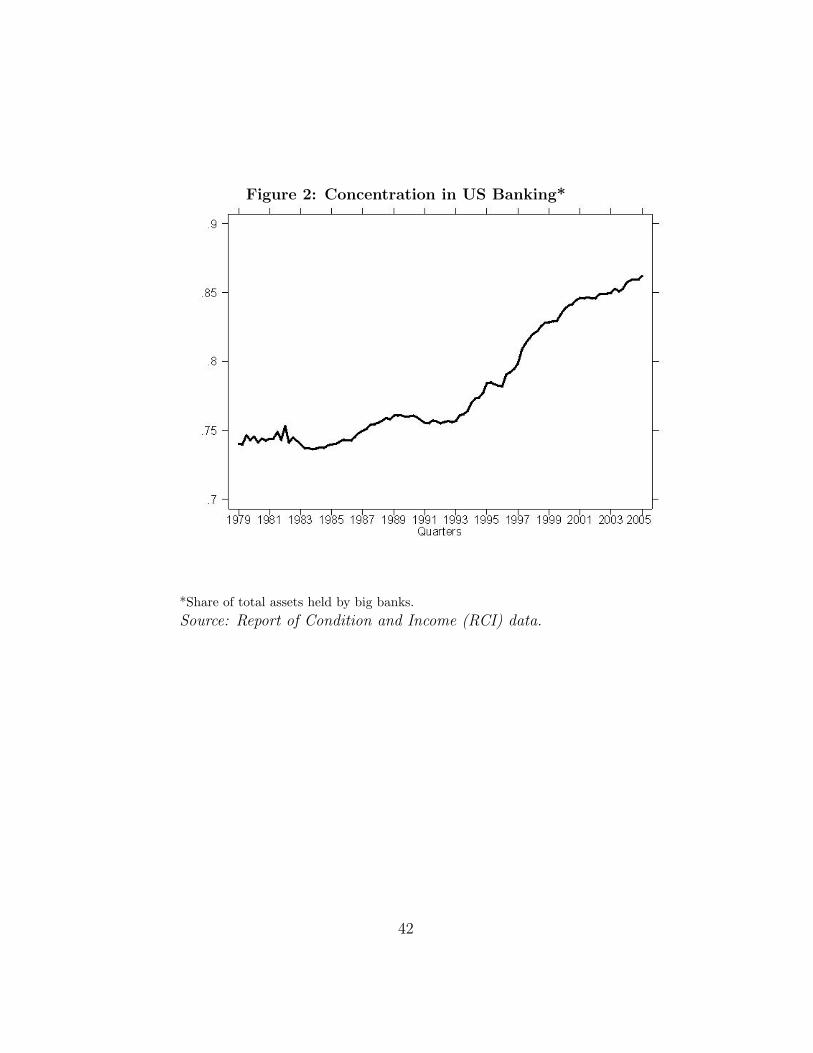

The Share of Total Assets Held by Big Banks:

The share of total assets held by big banks is included among our controls

as a measure of concentration. The Herfindahl-Hirschman index (HHI) for

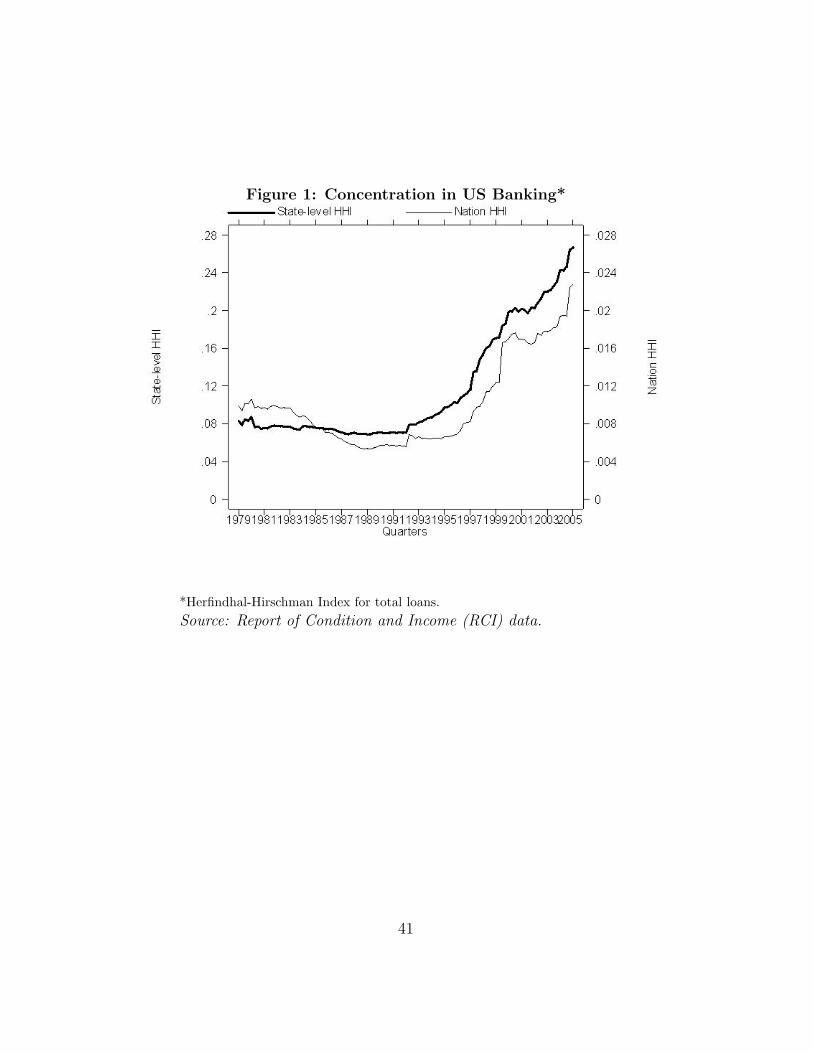

the market for loans is an alternative measure of concentration. Figures 1

and 2 show the comovement of the two measures. Two different measures for

the Herfindahl index are shown there: an aggregate measure and a weighted

average of states indexes. This distinction becomes specially relevant for

the pre-1997 period when interstate branching was not allowed in the US31.

Worthy of note is the important increase in all concentration measures over

the last years.

If higher market concentration is a good proxy for less competition, there

should be a positive relationship between market concentration and price-

31To understand the need for this adjustment, consider an economy where banks are

restricted to operate in only one state and where there is only one bank in each state. The

aggregate HHI in that economy would be∑

(1/N2) = 1/N with N being the number of

states. With the transformed measure, the weighted HHI would equal∑

(1 ∗ 1/N) = 1.

Therefore, the aggregate measure would be underestimating the concentration measure in

an economy where banks are perfect monopolies in each of their areas of operation. The

variability over time of these two measures can be expected to be different if the shares of

each state in total assets change significantly at business cycle frequencies. However, we

do not expect these changes to be very important.

23

cost margins. Also, for a given interest rate on loans, concentration will

increase NIMs if it allows banks to offer lower deposit rates. Berger and

Hannan (1989) provide strong evidence of a negative relationship between

market concentration and deposit rates. Hannan and Berger (1991) find that

banks in more concentrated markets have more rigid deposit rates, and that

deposit rates are stickier upwards than downwards. Neumark and Sharpe

(1992) find that in more concentrated markets deposit rates rise more slowly

and fall faster after a change in input costs. They also find that banks in

concentrated markets offer lower rates on deposits than more competitive

banks.

However, Jackson (1992 and 1997), Rhoades (1995) and Hannan (1997)

present models of oligopolistic competition alternative to Cournot, accord-

ing to which there might be an inverse relationship between spreads and

concentration indexes32. Jackson (1992) finds that the negative price (de-

posit interest rate)-concentration relationship in Berger and Hannan (1989)

is not consistent over the full range of observed market concentration values.

Smirlock (1985) argues that market concentration is not random, but the

result of more efficient banks “endogenously” gaining larger market shares.

Therefore, he tests the hypothesis that there is no causal relationship be-

tween concentration and profitability in banking, but rather between market

share and profits. He does find a link of profits to market share, but no

positive relationship with concentration once this is controlled for.

32The basic idea in these models is that banks operate in a perfectly competitive market

for loans, but have market power when getting deposits from savers in the economy and

they choose the interest rate on deposits. Their model of consumer deposit pricing is

represented by a general rational distributed lag function. The change in the rate of

deposits is a function of the changes in the six-month Treasury bill rate at 0,...,N lags.

In this model, more concentrated markets should have higher spreads, but they would

also exhibit relatively more deposit rate rigidity. Jackson (1997) provides evidence of a

non-monotonic relationship between market concentration and price rigidity.

24

Also, the share of total bank assets held by big banks is not only a measure

of concentration, but one of the relative importance of bigger banks in the

economy. It can therefore capture differences, if any, in the behavior of these

banks relative to the rest. Flannery (1981) provides evidence that larger

banks charge lower margins. He shows that large banks effectively hedge

themselves against market rate risk by holding assets and liabilities of similar

average maturities. This provides a rationale why larger banks might charge

smaller margins. Ho and Sunders (1981) also show that smaller banks have

a one third of a percent larger spread than bigger banks.

Thus, it is not clear what sign to expect for this coefficient. If the negative

effect is stronger, the high procyclicality of the share observed in our sample

provides an alternative explanation for a countercyclical behavior of margins.

Two explanations for the high procyclicality of this variable are based on

the non-competitive behavior of large banks over the cycle. First, in a setting

of imperfect competition originated in product differentiation, we can think

of big banks being more aggressive than smaller banks in capturing most

of the increased demand for credit in booms. This can be done by invest-

ing more aggressively in advertising or differentiating from smaller banks by

offering other banking services together with loans, for example. A second

explanation can be found in a setting of strategic behavior of big banks as in

a colluding oligopoly along the lines of Rotemberg and Saloner (1986). Dur-

ing booms players revert to the non-collusion equilibrium with lower prices

and higher quantities. If the larger banks in the industry are the ones that

implicitly collude while smaller banks do not have such a strategic behavior,

then big banks will expand their share of the market during booms when the

collusion is more difficult to sustain.

25

3.3 Banking Regulation

A set of dummy variables is included in the regression specification to control

for three important regulatory changes that have taken place in the United

States banking sector during our sample period.

First, in 1980 the Depository Institutions Deregulation and Monetary

Control Act of 1980 eliminated the deposit interest rate ceilings imposed by

Regulation Q33 and increased the limit of deposit insurance by the FDIC

from $40,000 to $100,000 per account.

Second, in 1994 the Riegle-Neal Interstate Banking and Branching Effi-

ciency Act repealed the Douglas Amendment. It allowed national banks to

operate branches across state lines after June 1, 1997. The Riegle-Neal Act

specified that state law continues to control intrastate branching for both

national and state banks.

Third, the Gramm-Leach-Bliley Act (GLBA) enacted in November of

1999 increased the activities allowed for banks and their holding companies.

Before 1999 commercial banks were prevented from expanding into a wide

range of financial services such as investment banking. Specifically, they

could not hold corporate equity, and the underwriting of securities was left

to investment banks. The GLBA repealed the parts of the Banking Act of

1933 that separated commercial banking from the securities business, which

have come to be known as “Glass-Steagall”. It also repealed the parts of the

Bank Holding Company Act of 1956 that separated commercial banking from

the insurance business. Thus, the GLBA permits single holding companies

to offer banking, securities, and insurance, as they had before the Great

Depression (Barth et al., 2000).

33The prohibition against payment of interest on demand deposits is the last vestige of

Regulation Q that is still valid.

26

4 Empirical Methodology

4.1 The Data

The study uses time series quarterly data for the period 1979:I-2005:I. Bank-

level balance sheet and income data is taken from the Call Reports on Con-

dition and Income data, available for all banks regulated by the Federal Re-

serve System, Federal Deposit Insurance Corporation, and the Comptroller

of the Currency. These data are available from the Federal Reserve Bank

of Chicago. Details on variable definitions and sources can be found in Ap-

pendix A.

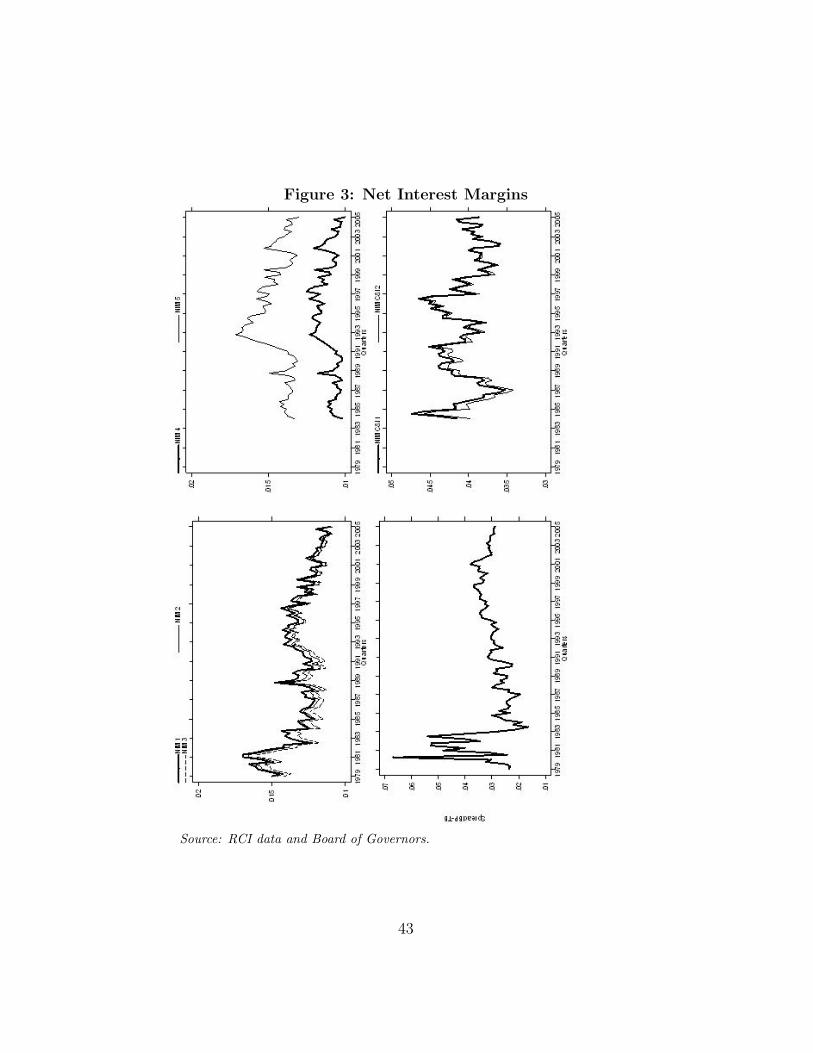

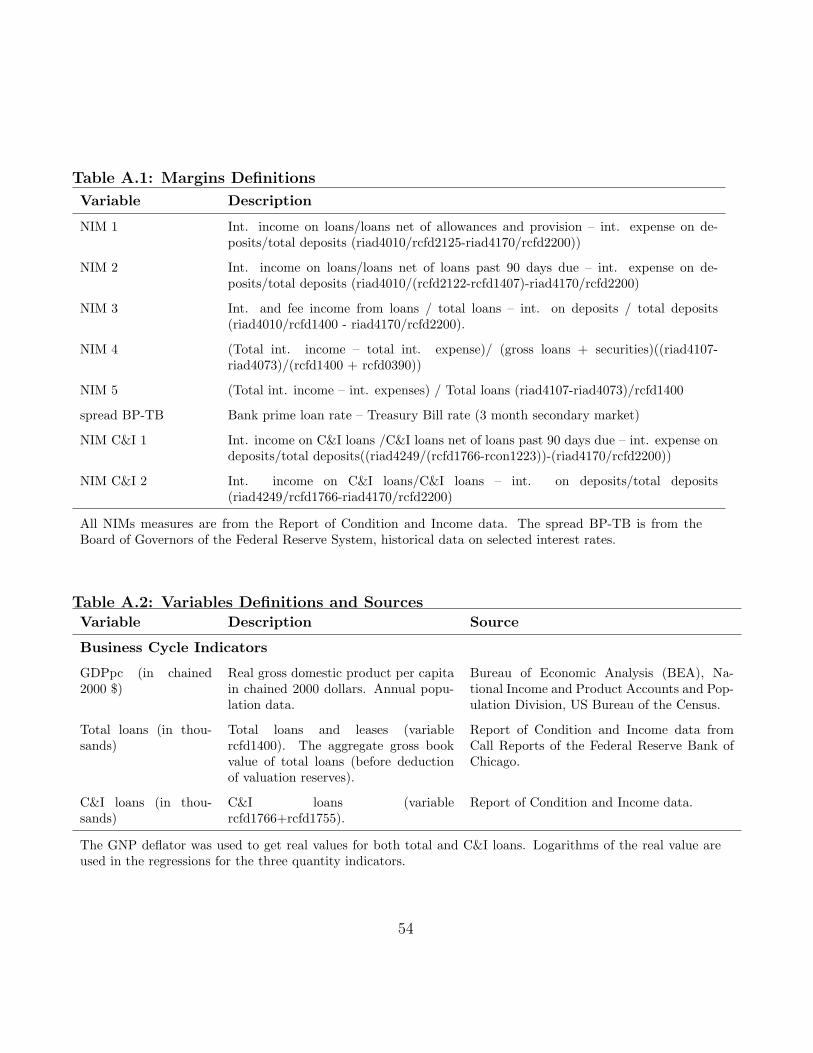

Eight alternative definitions are used here for NIMs. All the series are

shown in Figure 3. In only one case macro data is used to calculate the spread

as the difference between the bank prime and the Treasury bill rates. The

latter is taken as a proxy for the interest rate on deposits paid by commercial

banks. Dueker and Thornton (1997) also use the bank prime as the lending

rate in their study of markups in the banking sector. They argue that a

change in the prime rate is indicative of a general shift in lending rates.

It is important to state here the distinction between spreads and net

interest margins. The pure spread is the rate spread between loan and deposit

rates. NIMs are calculated as the ratio of the difference between interest

revenues and interest expenses to assets, whereas spreads are obtained as

the difference between interest returns (i.e., interest revenues/earning assets)

and interest costs (i.e., interest expenses minus provisions for loans losses,

divided by interest bearing liabilities) (Angbazo, 1997). In this sense, our

NIMs 1,2 and 3 as well as C&I 1 and 2 more closely measure spreads, while

NIM 4 and 5 are strictly “margins” and comparable to the measures that the

previous literature has worked with34.

34Demirguc-Kunt, Laeven and Levine (2004) define the net interest margin as interest

income minus interest expense divided by interest-bearing assets. In Angbazo (1997) the

27

Three alternative definitions for the business cycle measure are used here:

GDP per capita and both total and C&I loans. The sample correlation of

these two loan definitions with GDP is 0.57 and 0.78, respectively. Adding

loans as an alternative measure is useful because they may be even more

sensible to the cycle than GDP. It is also conjectured here that they may

more closely reflect the behavior of other aggregates that are key to study

the cyclicality of spreads, such as investment and production of firms that

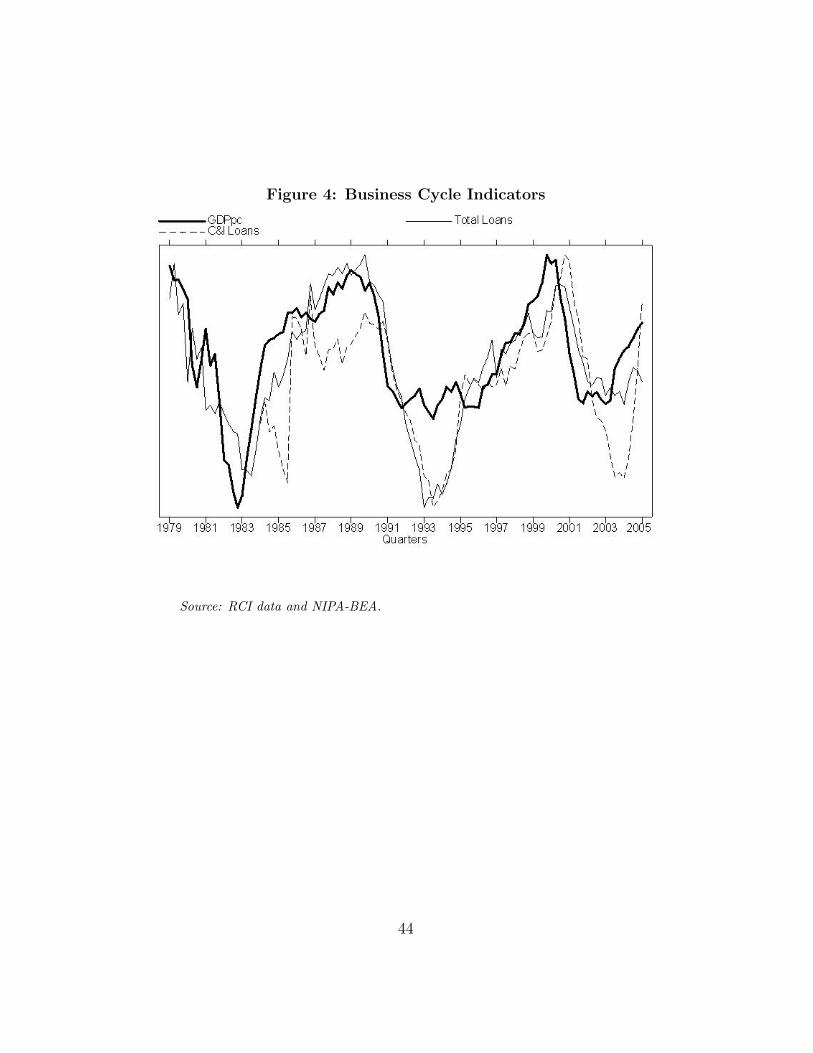

depend critically on bank financing. Figure 4 plots the three business cycle

indicators together.

Table 1: Sample Correlations of NIMs with Cycle MeasuresNIM 1 NIM 2 NIM 3 NIM 4 NIM 5 BP/TB C&I 1 C&I 2

GDPpc -0.20 -0.23 -0.21 -0.26 -0.34 -0.24 -0.07 -0.07(0.040) (0.016) (0.029) (0.016) (0.001) (0.012) (0.549) (0.503)

Total loans -0.35 -0.42 -0.40 -0.31 -0.52 -0.11 0.14 0.13(0.000) (0.000) (0.000) (0.004) (0.000) (0.283) (0.202) (0.222)

C&I loans -0.34 -0.40 -0.39 -0.35 -0.53 0.01 0.03 0.02(0.002) (0.000) (0.000) (0.001) (0.000) (0.938) (0.810) (0.851)

GDPpc: GDP per capita. Significance levels shown in parentheses.

To provide a first insight on the cyclicality of net interest margins, sample

raw correlations between alternative measures of the detrended margin and

detrended business cycle indicators are shown in Table 1. The contempo-

raneous correlation with GDP per capita is always negative for all spread

measures. Correlations are very low and become not significant in the few

cases in which they are positive.

It is relevant to highlight that the non-significance of the correlations for

the last three spreads is not evidence against the countercyclicality of NIMs.

NIM is calculated as the spread between interest revenues and interest expenses (before

loan loss provisions) divided by average earning assets. Demirguc-Kunt and Huizinga

(2000) define margins as banks’ net interest income / total assets, where net interest

income is banks profits plus operating costs and loan loss provisions - non-interest income.

28

Several forces like changes in banking regulation and seasonality of the data

not accounted for in these raw correlations may be distorting the picture. It

will be shown below that when controlling for the effects of banking regulation

and seasonality as well as monetary policy and default risk, the coefficient on

the business cycle indicator becomes negative and significant in all 24 cases.

4.2 Estimation Strategy

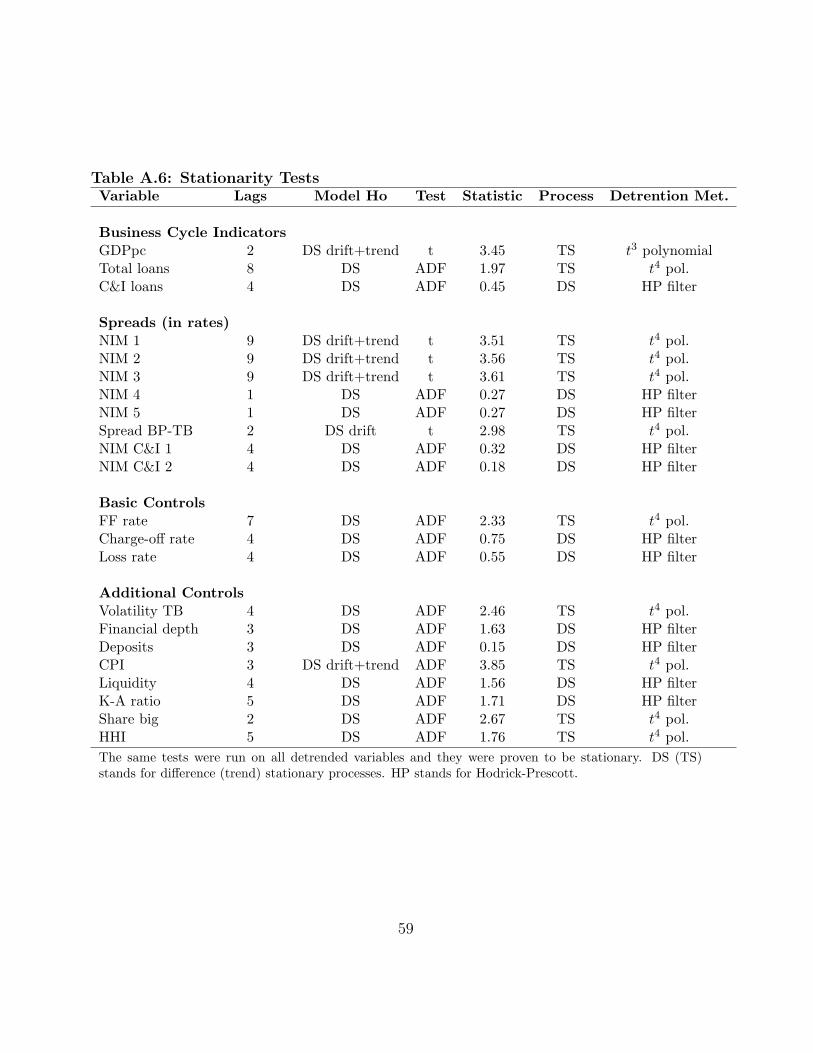

Augmented Dickey-Fuller (ADF) tests were run for all the variables in our

sample to test for the presence of unit roots. Except in a few cases, we do

not have a priori on the process followed by each variable under the null of a

unit root. Thus, we preferred to follow the methodology put forth by Dolado,

Jenkinson and Sosvilla-Rivero (1990)35. The optimal lag length for the ADF

regressions was based on the Akaike Information Criterion and the Schwartz

Bayesian criterion as well as on the Box-Pierce Q test for white noise of the

errors of the regression. Table A.5 in Appendix A shows the results of the

stationarity checks performed.

When detected, non-stationarity was dealt with by transforming the orig-

inal series into stationary processes. Trend stationary (TS) variables were

detrended by regressing them on a constant and a polynomial of time36. Dif-

ference stationary (DS) variables were also “detrended” using the Hodrick-

Prescott filter with a smoothing parameter of 1600 to separate the cyclical

component from trend. All detrended variables were proven to be stationary

35In short, the methodology starts with an unrestricted model that includes a constantand trend and then tests sequentially for the validity of the trend first and for the constantlater. If in any of the three possible models the null of unit root is not rejected, thenthe variable is difference stationary (DS) with drift plus trend, DS with drift or DS,respectively. If the null is rejected at some stage, then we can conclude the variable beingtrend stationary (TS). The advantage of this method is that once the “true” model isknown under the null, the power of the unit root test can be increased by using the usualt-test instead of the values tabulated by Dickey and Fuller (this result is due to Sims,Stock and Watson, 1990).

36The order of the polynomial was chosen based on fit.

29

by rejecting Dickey-Fuller tests. The original model was thus redefined in

terms of these detrended stationary variables.

DS variables were not first-differenced because we think that including

the first-differenced variables in the model would both be methodologically

incorrect and lack economic meaning. From the point of view of econometric

theory, it would be wrong to try to estimate the original parameters from

the model in levels by first-differencing all the variables when some of them

are TS rather than DS. An alternative would be to redefine the original

model in terms of a mixture of first-differenced DS variables and detrended

TS variables. However, for the purpose of measuring the cyclical pattern

followed by spreads it is necessary to isolate the business cycle frequency

component of the explanatory variables. Quarterly changes in GDPpc or in

total loans may or may not be related to the phase of the business cycle.

That is, the estimated coefficients on these first-difference variables could

not clearly be interpreted as measures of the countercyclicality of spreads.

The specification includes lags of some of the independent variables.

Lagged dependent variables are not included because we consider they do

not belong to the econometric model. Of course, important autocorrelation

in the disturbances is expected, so two tests for autocorrelation are imple-

mented here. Durbin-Watson (DW) test for first-order autocorrelation and

also Breusch-Godfrey (BG) test for possible autocorrelation of up to order

4. It has been suggested that an AR(4) model is appropriate for quarterly

data because of seasonal autocorrelation. Indeed, in several cases the null

of no autocorrelation cannot be rejected with the DW statistic, but it is re-

jected when using the BG test (see Table 4 and tables B.1-B.6 in Appendix

B). In all cases in which some form of autocorrelation was found, standard

errors were obtained by using the Newey-West robust, consistent estimator

for autocorrelated disturbances of unspecified structure.

Our specification also presents potential endogeneity problems. A system

30

of equations bias can be affecting our results if, as expected, some of the ex-

planatory variables in the basic specification are simultaneously determined

with the dependent variable. Specially prone to this bias are the business

cycle indicator and the share of total assets held by big banks37.

To account for endogeneity, the models were also estimated by two-stage

least squares (2SLS)38. Since IV methods are relatively inefficient compared

to OLS, a Hausman specification test was run in order to evaluate the com-

promise between efficiency and consistency of our estimations.

Finally, variance inflation factor (VIF) tests were run on our regressions

to check for the existence of multicollinearity.

5 Results

The results for the estimations obtained following the methodology outlined

in Section 4 are presented in this section.

Monetary policy and default risk are the two main candidates to explain

the countercyclicality indicated by the sample correlations shown in Table 1.

In order to study if the cyclicality of margins is robust to these important

determinants, they are both introduced as controls in our basic specification.

The basic specification also includes dummies to control for the effect of

regulatory changes in the banking sector that took place during our sample

period. Also, since most of our data is not seasonally adjusted, quarterly

dummies are included to capture any seasonality affecting banks margins.

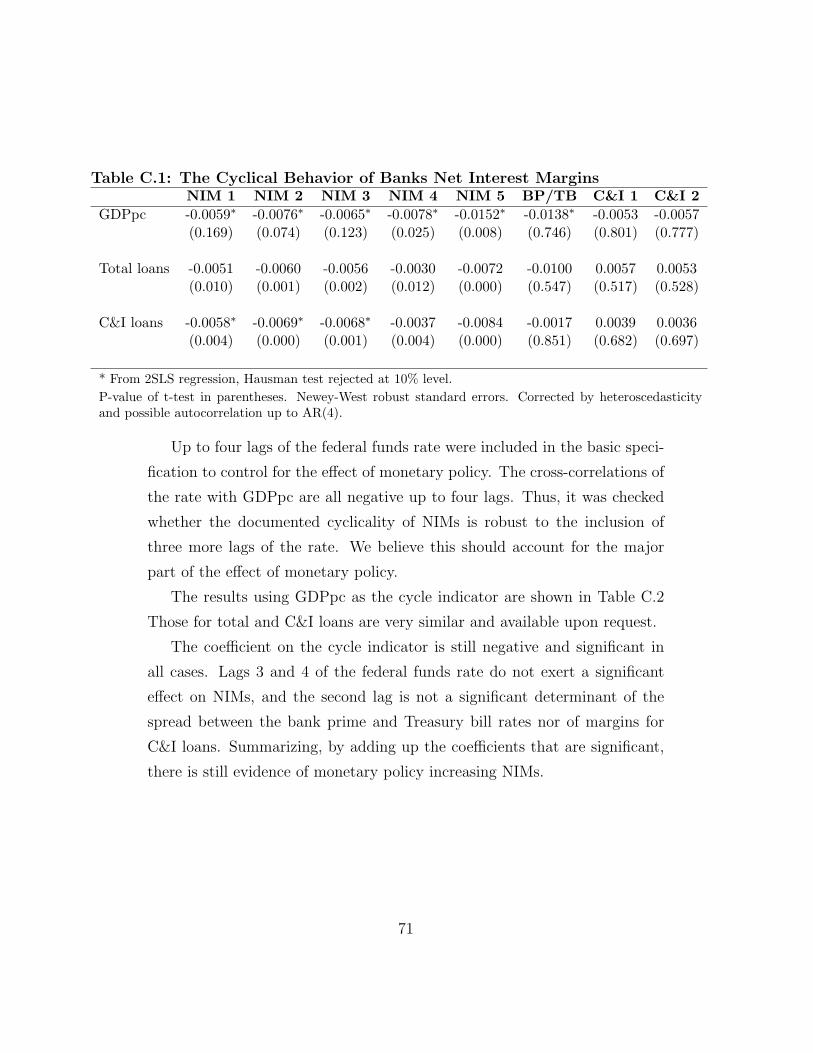

As a robustness check, the cyclical behavior of NIMs was also studied

37When thought of as a measure of concentration, this share might itself be a functionof the spread.

38Three-stage least squares (3SLS) would have allowed for correlation among the errorterms of the three equations: the margin, the cycle indicator and the share of big banksin total assets. 3SLS gives more efficient estimates, but 2SLS ones are still consistent.Moreover, 3SLS would pose the risk that a wrongly specified equation bias the estimatorsof interest in the NIM equation.

31

when not controlling for monetary policy and default risk. All the NIMs

measures were regressed against each of the three alternative business cycle

indicators and just the dummies controlling for regulations and seasonality

in the data. The results can be found in Appendix C. Overall, the counter-

cyclicality of NIMs is robust to this change in the econometric specification.

A set of additional regressors is added later to the basic specification.

The main goal there is to try to explain the actual channels through which

macroeconomic aggregates such as GDP affect the microeconomic behavior

of banks, and generate countercyclical NIMs. Thus, no explanatory power

should be left to the cycle measure after including this expanded set of con-

trols.

5.1 Regressions with Basic Controls

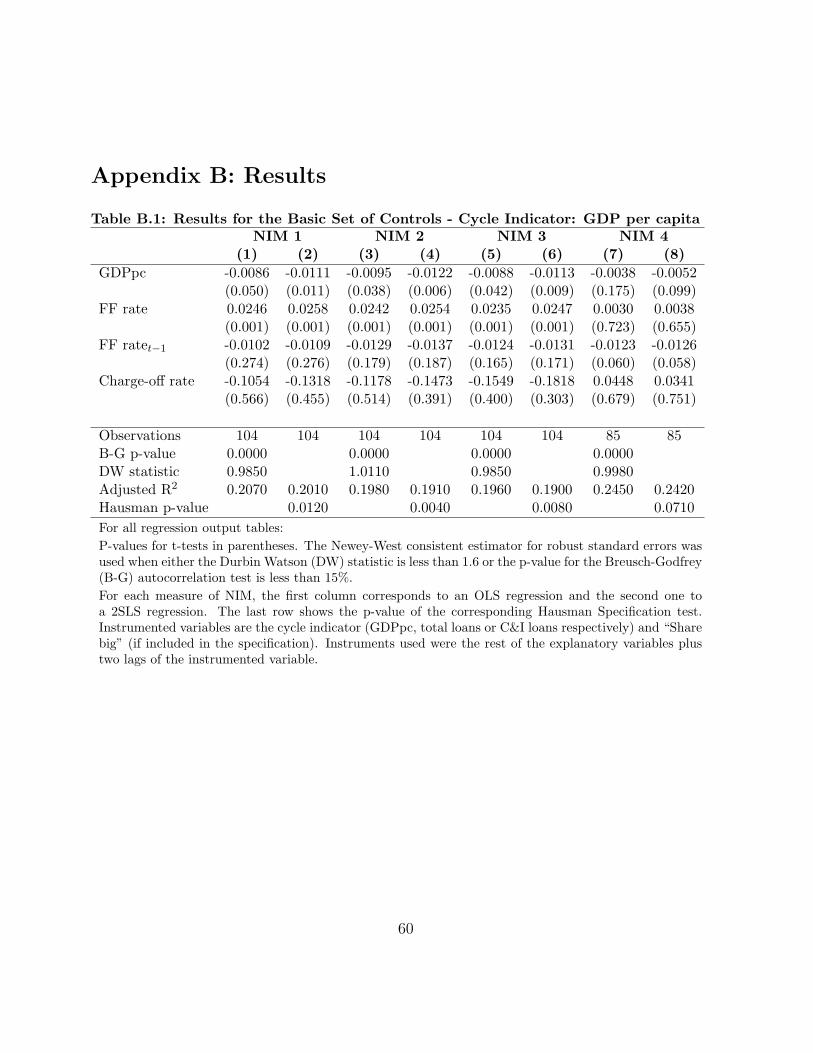

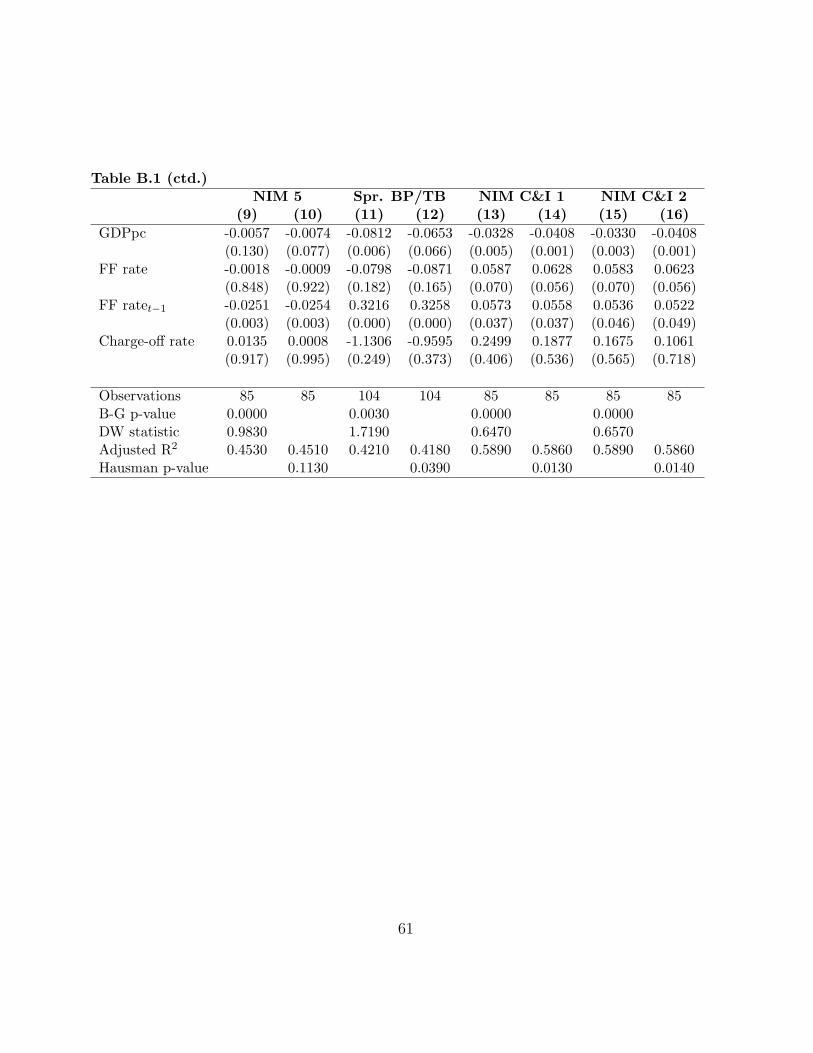

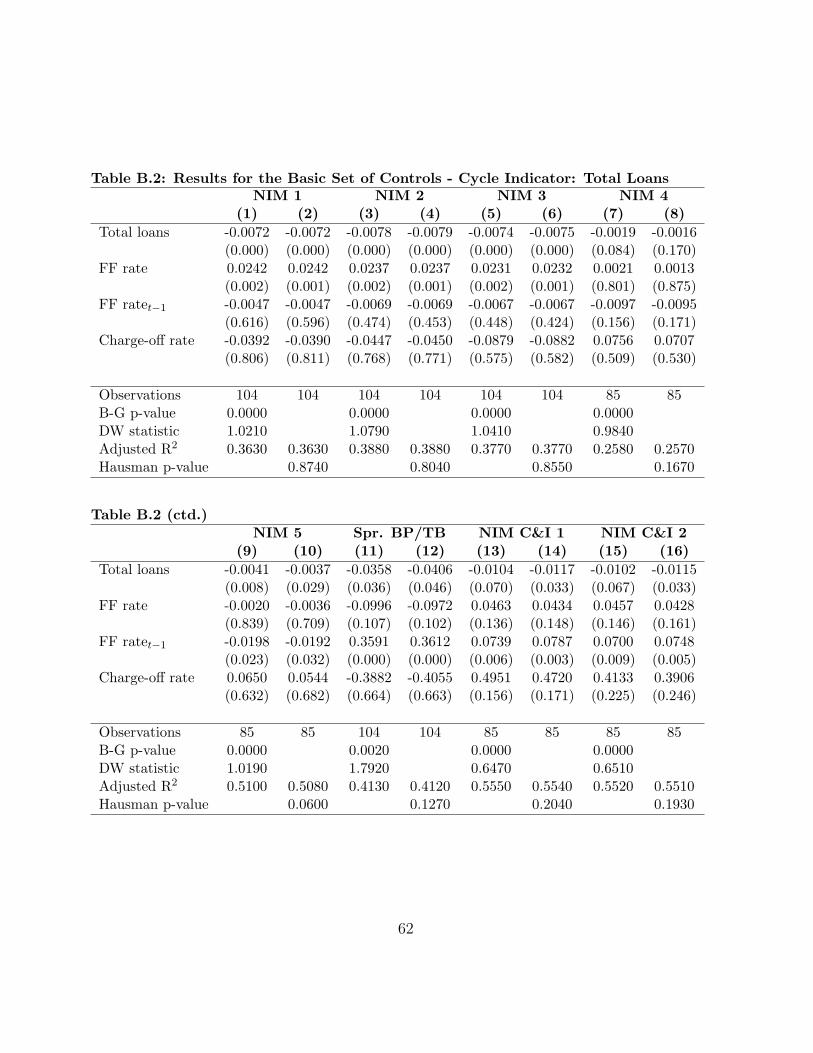

Results for the basic specification are summarized in Table 2. The counter-

cyclicality of spreads is documented with a negative and significant coefficient

on all business cycle indicators and for all definitions of NIMs. The result is

robust to the inclusion of dummy variables to control for both banking regu-

lation issues and seasonality in the data. This is true even after controlling for

the effects of countercyclical monetary policy and default risk. Importantly,

the coefficients on the margins on C&I loans and the bank prime-Treasury

bill spread become significantly different from zero, even when the sample

raw correlations presented in Table 1 are not.

The full regression output along with several important regression diag-

nostic statistics are shown in Tables B.1 to B.3 of Appendix B. The coeffi-

cients for seasonal and regulation dummies were not included in those tables.

The stance of monetary policy is measured with the federal funds rate, in-

cluding both the current rate and a lagged value. Credit risk was accounted

for with a lagged value of the net charge-off rate.

32

Table 2: The Cyclical Behavior of Banks Net Interest MarginsNIM 1 NIM 2 NIM 3 NIM 4 NIM 5 BP/TB C&I 1 C&I 2

GDPpc −0.0111∗ −0.0122∗ −0.0113∗ −0.0052∗ −0.0074∗ −0.0653∗ −0.0408∗ −0.0408∗

(0.011) (0.006) (0.009) (0.099) (0.077) (0.066) (0.001) (0.001)

Total loans -0.0072 -0.0078 -0.0074 -0.0019 −0.0037∗ −0.0406∗ -0.0104 -0.0102(0.000) (0.000) (0.000) (0.084) (0.029) (0.046) (0.070) (0.067)

C&I loans -0.0063 -0.0071 -0.0064 -0.0023 -0.0041 -0.0275 -0.0222 -0.0216(0.002) (0.000) (0.001) (0.131) (0.031) (0.006) (0.000) (0.000)

* From 2SLS regression, Hausman test rejected at 10% level.P-value of t-test in parentheses. Newey-West robust standard errors. Corrected by heteroscedasticity andpossible autocorrelation up to AR(4).

A positive effect of the federal funds rate is obtained for all specifica-

tions for the margins and business cycle indicators, except for NIM 4 and 5

measures39. Monetary policy affects interest rates and spreads in the same

direction. It is of particular importance to control for countercyclical policy

here. If expansionary policies help the economy and lower spreads at the

same time, not including the federal funds rate among the controls may bias

the coefficient on the cycle indicator downwards. We interpret the positive

and significant coefficient found as evidence of the bank lending channel of

monetary policy being at work in the US economy for our sample period.

According to our results the credit risk measure has no significant impact

on NIMs. As in Angelini and Cetorelli (2003), a potential explanation is that

a higher realized value of charge-offs results in lower effective income earned

by banks.

5.1.1 Economic Importance of the Results

Having already discussed the statistical significance of our results, it is in-

teresting to assess their quantitative importance and also to compare the

39The coefficients on the current and lagged values are added for this assessment.

33

sensitivity of each spread definition to changes in the cycle indicator.

The importance of the coefficients shown in Table 2 can be better under-

stood by comparing the standard deviation of the spreads with the implied

change after a one standard deviation increase of the cycle indicator40. For

example, the coefficient of -0.011 of NIM 1 on the logarithm of GDP per

capita shows that a one standard deviation increase of output from its trend

(roughly a 2% increase) is associated to a fall of approximately 1/3 of a stan-

dard deviation of the spread relative to its own trend (around 0.02 percentage

points fall in the spread). The coefficients shown in Table 2 can be mislead-

ing if one omits the standard deviations from the analysis. For example, the

coefficient of -0.0072 on the logarithm of total loans, although lower than

that on GDP per capita, actually implies a fall of 1/2 of standard deviation

of NIM 1 relative to its own trend. With this interpretation in mind, Table

3 shows the number of standard deviations by which NIMs fall after a one

standard deviation increase in the cycle measure.

Table 3: Economic Significance of the CoefficientsNIM 1 NIM 2 NIM 3 NIM 4 NIM 5 BP/TB C&I 1 C&I 2

GDPpc -0.36 -0.41 -0.38 -0.30 -0.29 -0.23 -0.46 -0.47Total loans -0.48 -0.54 -0.52 -0.23 -0.30 -0.30 -0.24 -0.24C&I loans -0.35 -0.41 -0.37 -0.23 -0.27 -0.17 -0.43 -0.43

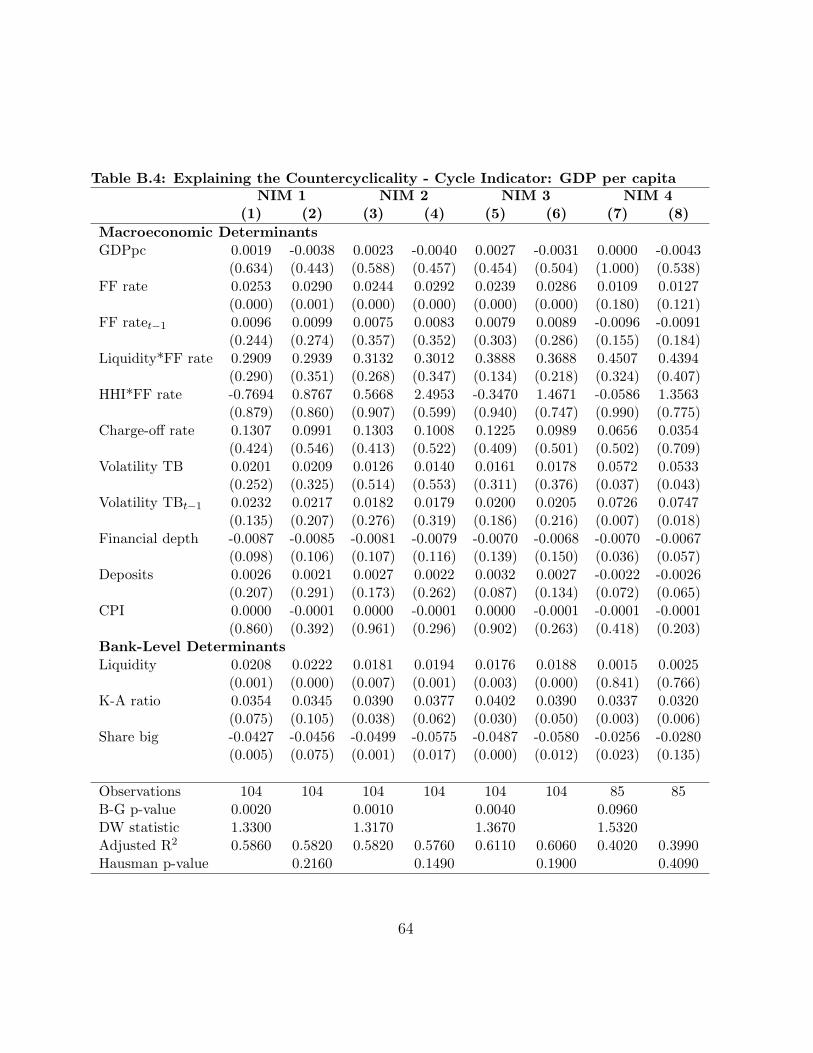

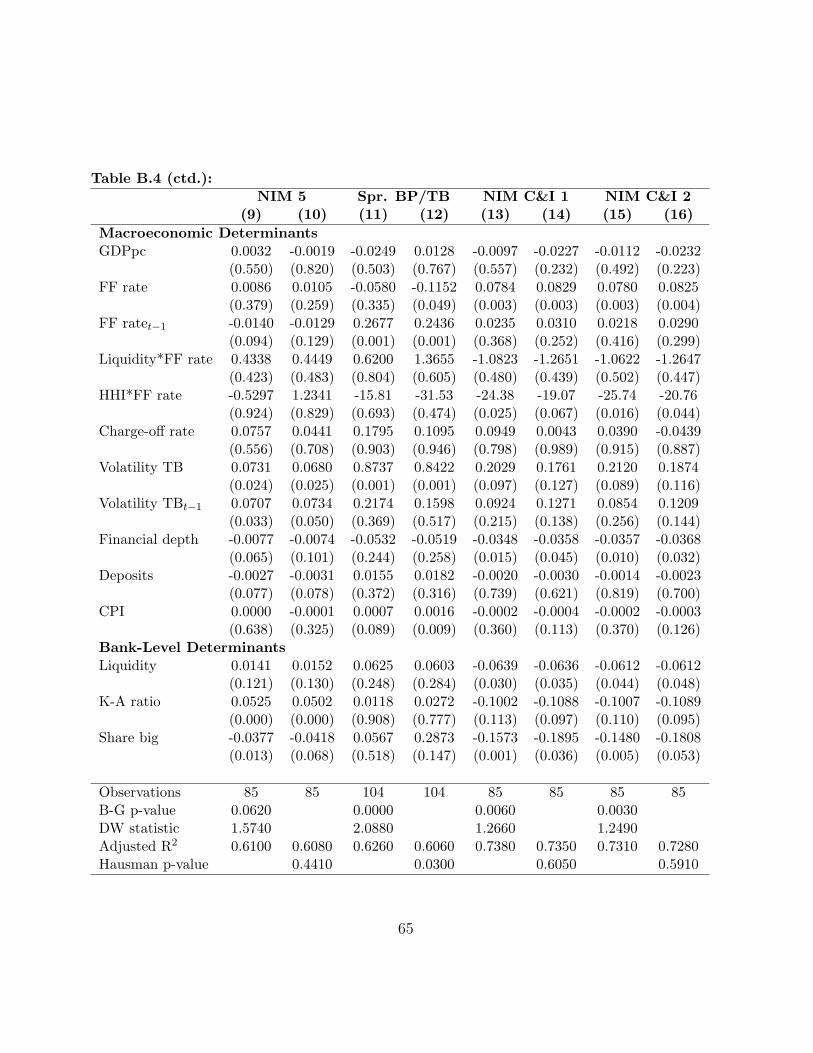

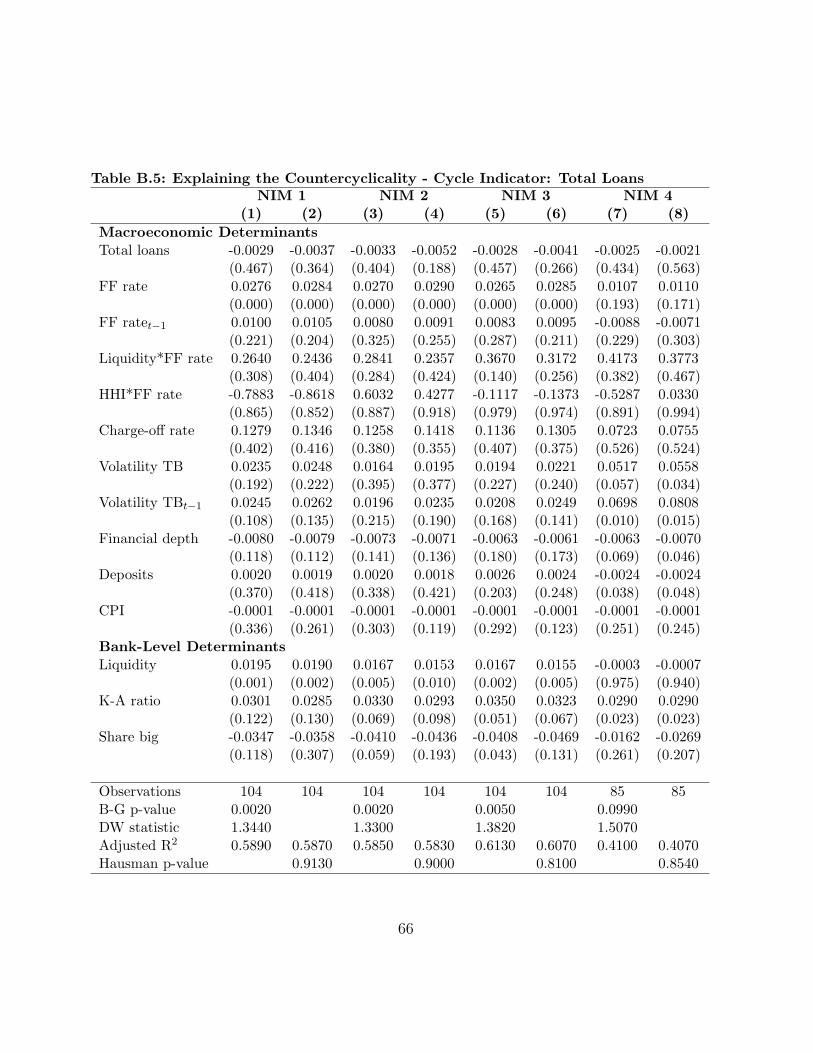

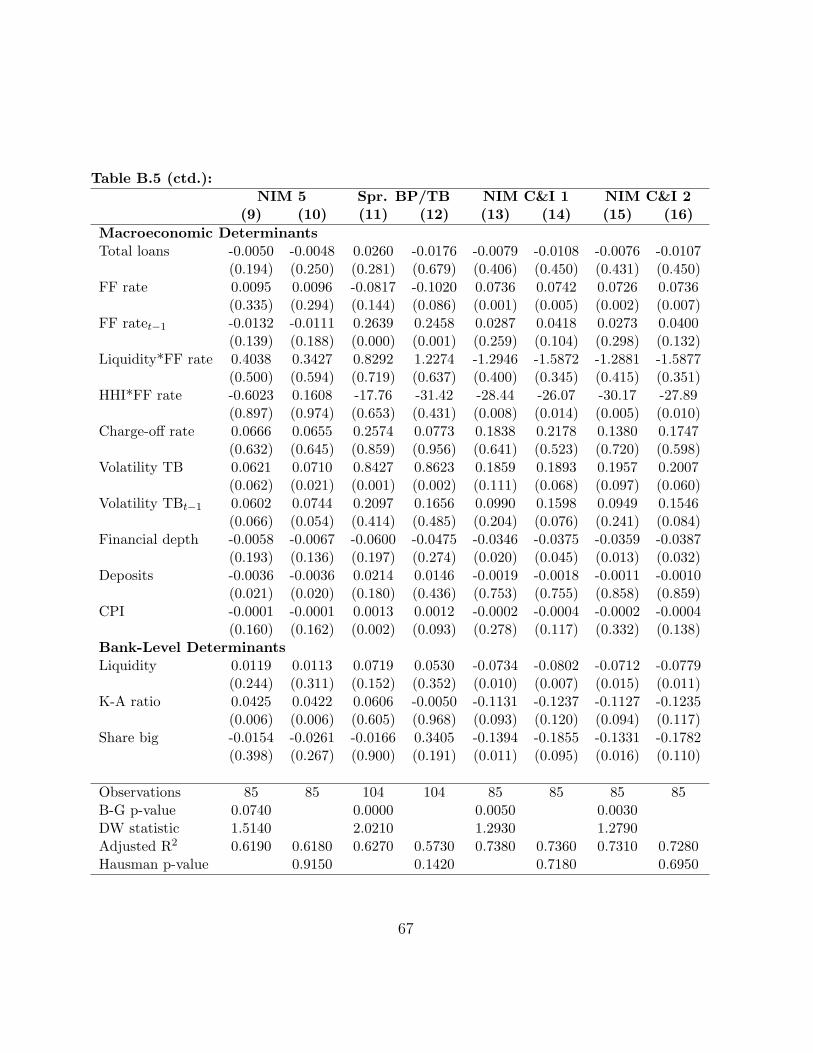

5.2 Additional Controls

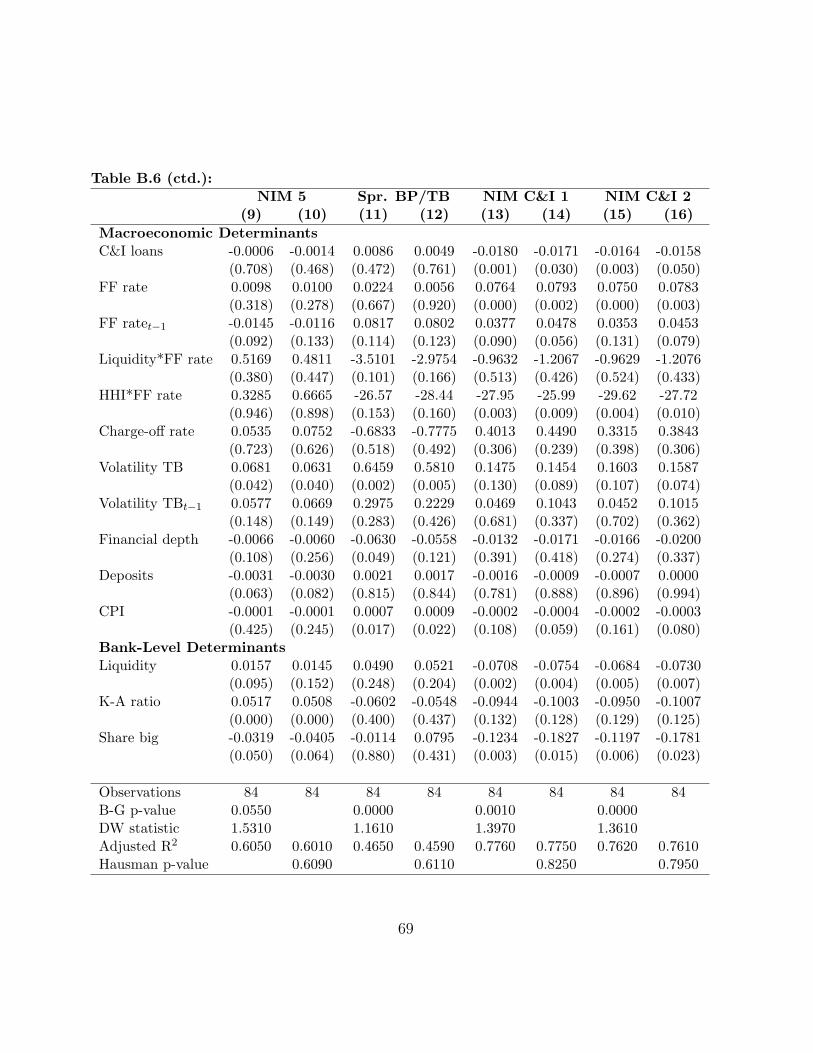

The additional set of controls presented in Section 3 are added next to find

potential explanations to the countercyclicality of NIMs. With the purpose

of saving space and given the similarity in the qualitative results, Table 4

includes the regression outputs of just four selected margins and only for

GDP and total loans. Results for the rest of margins and for C&I loans as

40See Table A.4 in the appendix for standard deviations of detrended business cyclemeasures and NIMs.

34

well as a number of regression diagnostic tests are all included in Tables B.4

to B.6 of Appendix B.

For all regressions in Table 4 and also in Tables B.4 to B.6, the cycle

measure completely loses its explanatory power41. This evidence suggests

that at least a subset of the included controls are important channels through

which fluctuations in the economy translate into cyclical movements of the

spreads.

Overall, the federal funds rate retains its positive and significant impact

on spreads even after introducing the additional controls. Moreover, in the

case in which the coefficient on the contemporaneous rate is negative, the

total effect of monetary policy on NIMs is still positive when considering the

rate’s lagged value42.

41The only exception corresponds to the particular case of NIMs C&I 1 and C&I 2 withC&I loans, for which the quantity indicator keeps its significance and negative sign.

42The only exception is given by the combinations of NIM 5 with GDP and with C&Iloans. Monetary policy exerts a negative effect on NIMs in these two cases.

35

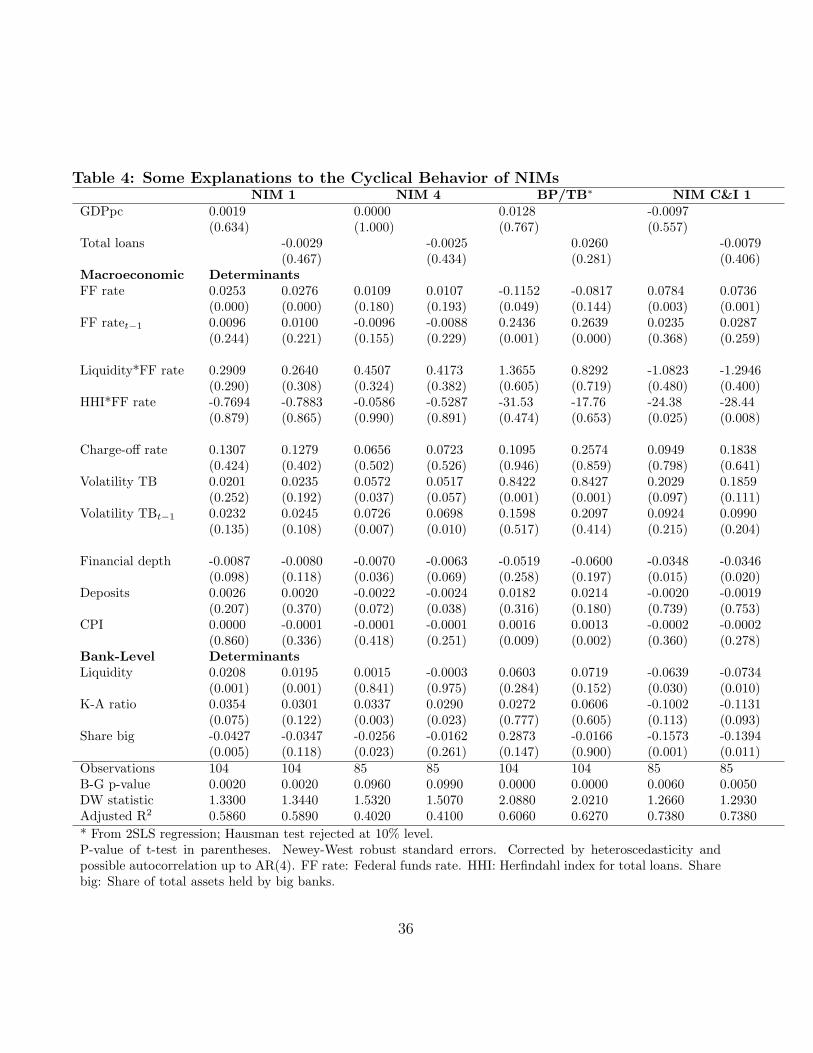

Table 4: Some Explanations to the Cyclical Behavior of NIMsNIM 1 NIM 4 BP/TB∗ NIM C&I 1

GDPpc 0.0019 0.0000 0.0128 -0.0097(0.634) (1.000) (0.767) (0.557)

Total loans -0.0029 -0.0025 0.0260 -0.0079(0.467) (0.434) (0.281) (0.406)

Macroeconomic DeterminantsFF rate 0.0253 0.0276 0.0109 0.0107 -0.1152 -0.0817 0.0784 0.0736

(0.000) (0.000) (0.180) (0.193) (0.049) (0.144) (0.003) (0.001)FF ratet−1 0.0096 0.0100 -0.0096 -0.0088 0.2436 0.2639 0.0235 0.0287

(0.244) (0.221) (0.155) (0.229) (0.001) (0.000) (0.368) (0.259)

Liquidity*FF rate 0.2909 0.2640 0.4507 0.4173 1.3655 0.8292 -1.0823 -1.2946(0.290) (0.308) (0.324) (0.382) (0.605) (0.719) (0.480) (0.400)

HHI*FF rate -0.7694 -0.7883 -0.0586 -0.5287 -31.53 -17.76 -24.38 -28.44(0.879) (0.865) (0.990) (0.891) (0.474) (0.653) (0.025) (0.008)

Charge-off rate 0.1307 0.1279 0.0656 0.0723 0.1095 0.2574 0.0949 0.1838(0.424) (0.402) (0.502) (0.526) (0.946) (0.859) (0.798) (0.641)

Volatility TB 0.0201 0.0235 0.0572 0.0517 0.8422 0.8427 0.2029 0.1859(0.252) (0.192) (0.037) (0.057) (0.001) (0.001) (0.097) (0.111)

Volatility TBt−1 0.0232 0.0245 0.0726 0.0698 0.1598 0.2097 0.0924 0.0990(0.135) (0.108) (0.007) (0.010) (0.517) (0.414) (0.215) (0.204)

Financial depth -0.0087 -0.0080 -0.0070 -0.0063 -0.0519 -0.0600 -0.0348 -0.0346(0.098) (0.118) (0.036) (0.069) (0.258) (0.197) (0.015) (0.020)

Deposits 0.0026 0.0020 -0.0022 -0.0024 0.0182 0.0214 -0.0020 -0.0019(0.207) (0.370) (0.072) (0.038) (0.316) (0.180) (0.739) (0.753)

CPI 0.0000 -0.0001 -0.0001 -0.0001 0.0016 0.0013 -0.0002 -0.0002(0.860) (0.336) (0.418) (0.251) (0.009) (0.002) (0.360) (0.278)

Bank-Level DeterminantsLiquidity 0.0208 0.0195 0.0015 -0.0003 0.0603 0.0719 -0.0639 -0.0734

(0.001) (0.001) (0.841) (0.975) (0.284) (0.152) (0.030) (0.010)K-A ratio 0.0354 0.0301 0.0337 0.0290 0.0272 0.0606 -0.1002 -0.1131

(0.075) (0.122) (0.003) (0.023) (0.777) (0.605) (0.113) (0.093)Share big -0.0427 -0.0347 -0.0256 -0.0162 0.2873 -0.0166 -0.1573 -0.1394

(0.005) (0.118) (0.023) (0.261) (0.147) (0.900) (0.001) (0.011)Observations 104 104 85 85 104 104 85 85B-G p-value 0.0020 0.0020 0.0960 0.0990 0.0000 0.0000 0.0060 0.0050DW statistic 1.3300 1.3440 1.5320 1.5070 2.0880 2.0210 1.2660 1.2930Adjusted R2 0.5860 0.5890 0.4020 0.4100 0.6060 0.6270 0.7380 0.7380* From 2SLS regression; Hausman test rejected at 10% level.P-value of t-test in parentheses. Newey-West robust standard errors. Corrected by heteroscedasticity andpossible autocorrelation up to AR(4). FF rate: Federal funds rate. HHI: Herfindahl index for total loans. Sharebig: Share of total assets held by big banks.

36

Our results cannot provide full support to the effect studied in Kashyap

and Stein (2000) related to the interaction between monetary policy and

banks liquidity. This hypothesis would imply a negative sign for the in-

teraction between liquidity and the federal funds rate. Coefficients are not

significant in all possible combinations of NIMs and cycle indicators. More-

over, consistently across business cycle measures, they are positive for all

NIMs except for the ones on C&I loans. However, our findings can be easily

reconciled with theirs recalling that their hypothesis is specially relevant for

small banks that typically have less than perfect access to uninsured sources

of finance. For larger banks they also find a positive and even significant

effect of this interaction on banks loan supply. In our aggregate data, large

banks43 weight more heavily than small and medium size banks, so we expect

the coefficient on this interaction to be at least positive and insignificant.

The coefficient obtained for the interaction between our measures of mon-

etary policy and concentration is negative and significant for the case of NIMs

on C&I loans. This provides support to the hypothesis on the weaker effect of

monetary policy when concentration increases in the banking industry. The

evidence found is weak though, because although the coefficients are still

negative, they are not significant any more for most other spread variables.

Concerning credit risk, although positive, the coefficients on the lagged

value of the charge-off rate are not significant. However, as discussed before,

we are not particularly concerned about risk with any of our ex-post margins.

Moreover, the spread between the bank prime and the Treasury Bill rates is

calculated using two interest rate measures that should, by definition, include

a very small risk premium, if any. Thus, even in this case we do not expect

a significantly positive effect of our credit risk measure.

Interest rate risk has a positive and in most cases significant impact on

43Bank size was determined in the same way than in Kashyap and Stein, 1997. Largebanks are those in the 99-100th percentile of total asset distribution, medium size banksare those in the 95-99th percentiles and the rest are small banks.

37

NIMs. Therefore, our conclusions are consistent with Ho and Saunders (1981)

theoretical model and with previous empirical studies that show NIMs in-

cluding an interest rate risk premium.

Although not significant in some cases, the financial depth measure exerts

a negative effect on the dependent variable, as expected.

The supply of deposits faced by banks and used as a proxy for the

marginal cost of funds for them does not have a consistently significant im-

pact on margins. Nevertheless, in some cases the sign is negative and signif-

icant as expected. Future research could try to incorporate more accurate

microeconomic measures of operative costs for banks.

Inflation rates do not seem to significantly affect banks price-cost margins.

However, significantly across cycle indicators, inflation has a positive and

significant impact on the spread between the bank prime and the treasury

bill rates.

The liquidity of banks portfolios increases margins for the case of NIMs 1-

3. In this sense, our results are consistent with those in Angbazo (1997) and

Demirguc-Kunt, Laeven and Levine (2004). However, no conclusive evidence

can be found as the coefficient is insignificant for other spreads and it is even

negative and significant for NIMs C&I.

The coefficient on the capital to assets ratio is positive and significant

across the different alternative specifications, except again for the case of the

spread on C&I loans. In general, banks seem to charge higher spreads to

cover the costs of capital holdings.

One explanation we can exercise for the fact that both banks liquidity

and capital holdings have a different impact on C&I margins is related to