Embed Size (px)

Citation preview

THAILAND: Your Partner for growing market in ASIA

Chanin khaochanDirector- Frankfurt Office

Thailand Board of [email protected]

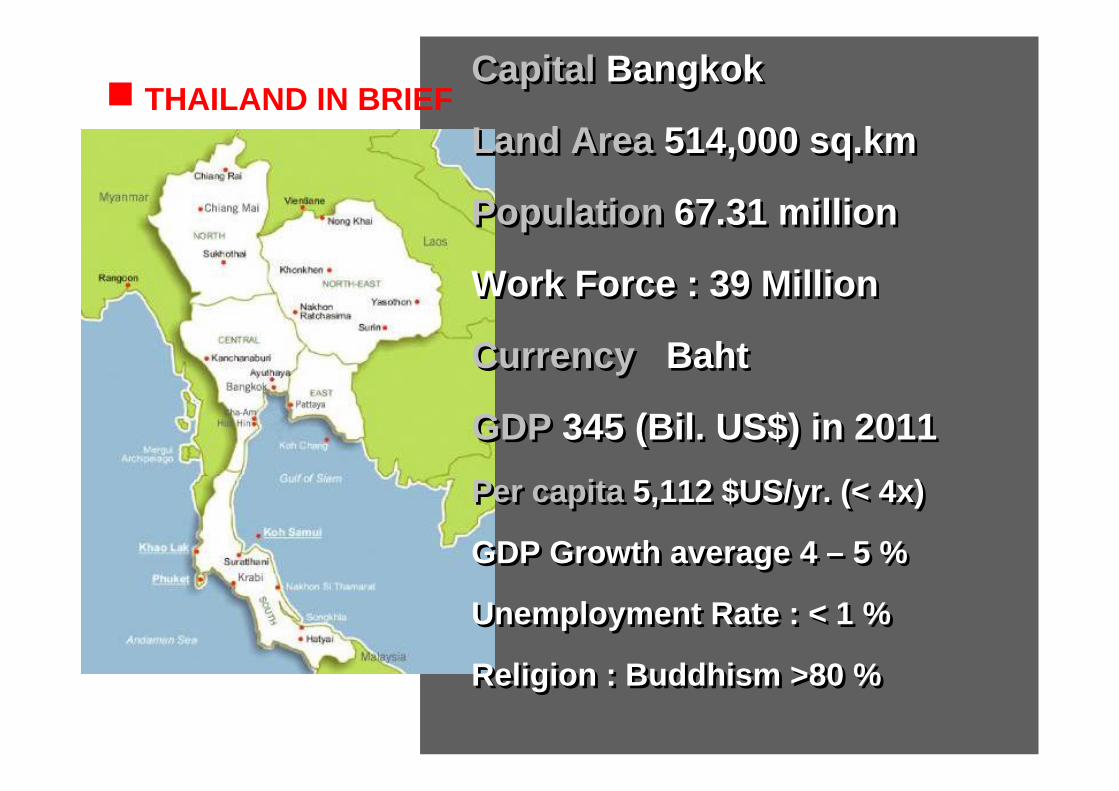

Capital Bangkok

Land Area 514,000 sq.km

Population 67.31 million

Work Force : 39 Million

Currency Baht

GDP 345 (Bil. US$) in 2011Per capita 5,112 $US/yr. (< 4x)

GDP Growth average 4 – 5 %

Unemployment Rate : < 1 %

Religion : Buddhism >80 %

Capital Bangkok

Land Area 514,000 sq.km

Population 67.31 million

Work Force : 39 Million

Currency Baht

GDP 345 (Bil. US$) in 2011Per capita 5,112 $US/yr. (< 4x)

GDP Growth average 4 – 5 %

Unemployment Rate : < 1 %

Religion : Buddhism >80 %

THAILAND IN BRIEF

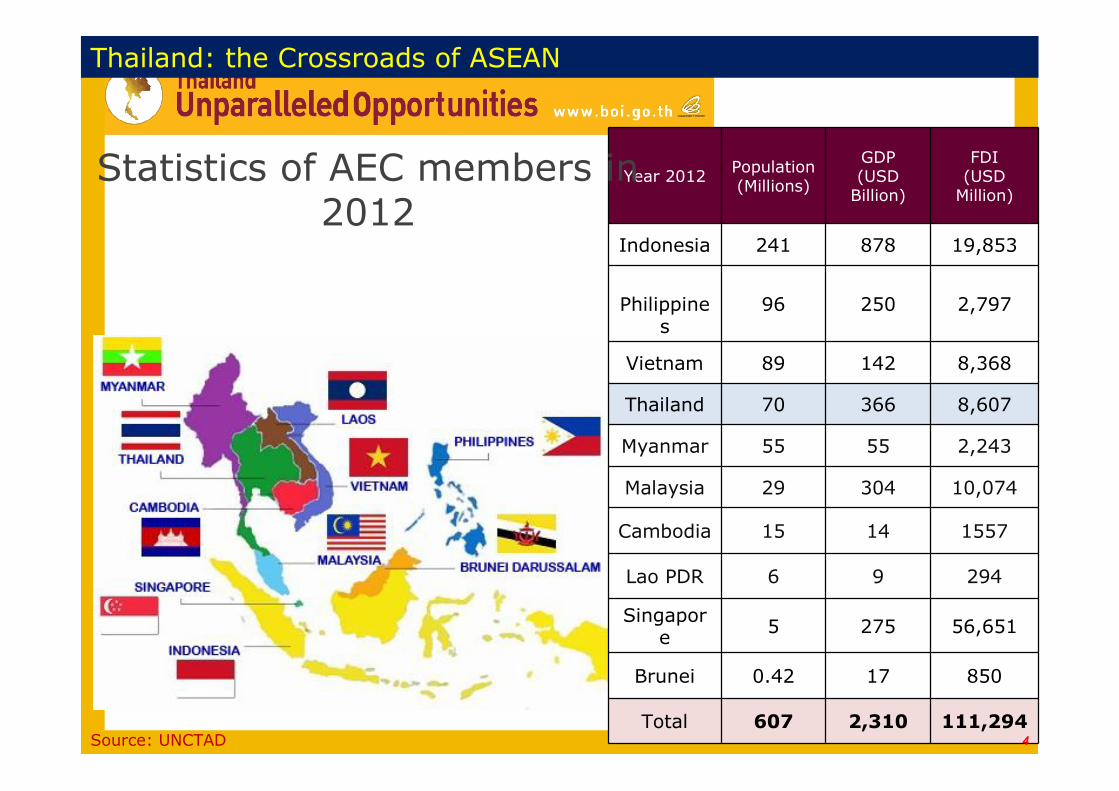

Thailand: the Crossroads of ASEAN

ASEAN Economic Community Compared to

Population 607 million > Europe Union (507 Million)

GDP size $ 2.31 trillion ≈ UK ($2.44 trillion)(1/7 of EU’s $16.6

trillion) International trade$ 1.6 trillion = 6 times of Thailand

FDI $ 111.3 billion ≈ China ($ 111.7 Billion)

International tourists Ranked 2nd globally65 million = next to France

3

Year 2012 Population(Millions)

GDP(USD

Billion)

FDI(USD

Million)

Indonesia 241 878 19,853

Philippines

96 250 2,797

Vietnam 89 142 8,368

Thailand 70 366 8,607

Myanmar 55 55 2,243

Malaysia 29 304 10,074

Cambodia 15 14 1557

Lao PDR 6 9 294

Singapore 5 275 56,651

Brunei 0.42 17 850

Total 607 2,310 111,294

Statistics of AEC members in 2012

Source: UNCTAD 4

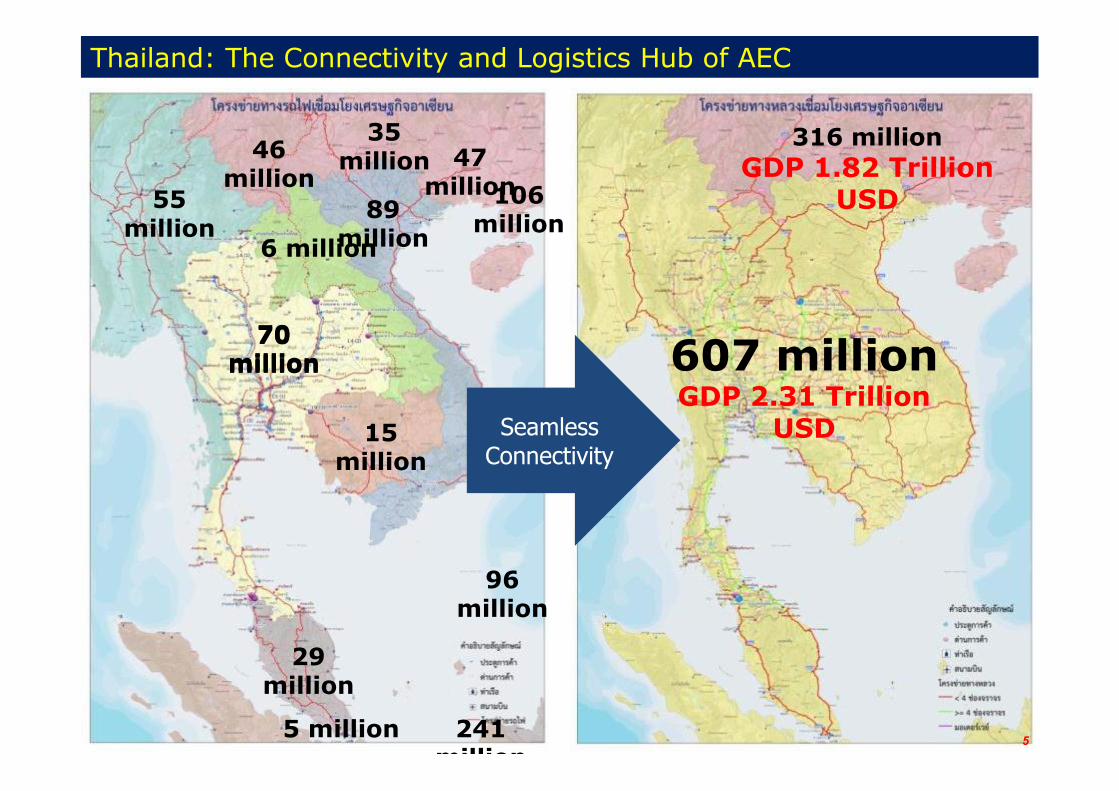

Thailand: the Crossroads of ASEAN

Seamless Connectivity

5

70 million

55 million

6 million89

million

46 million

47 million

15 million

29 million

241 million

96 million

35 million

106 million

5 million

70 million 607 million

GDP 2.31 Trillion USD

316 millionGDP 1.82 Trillion

USD

Thailand: The Connectivity and Logistics Hub of AEC

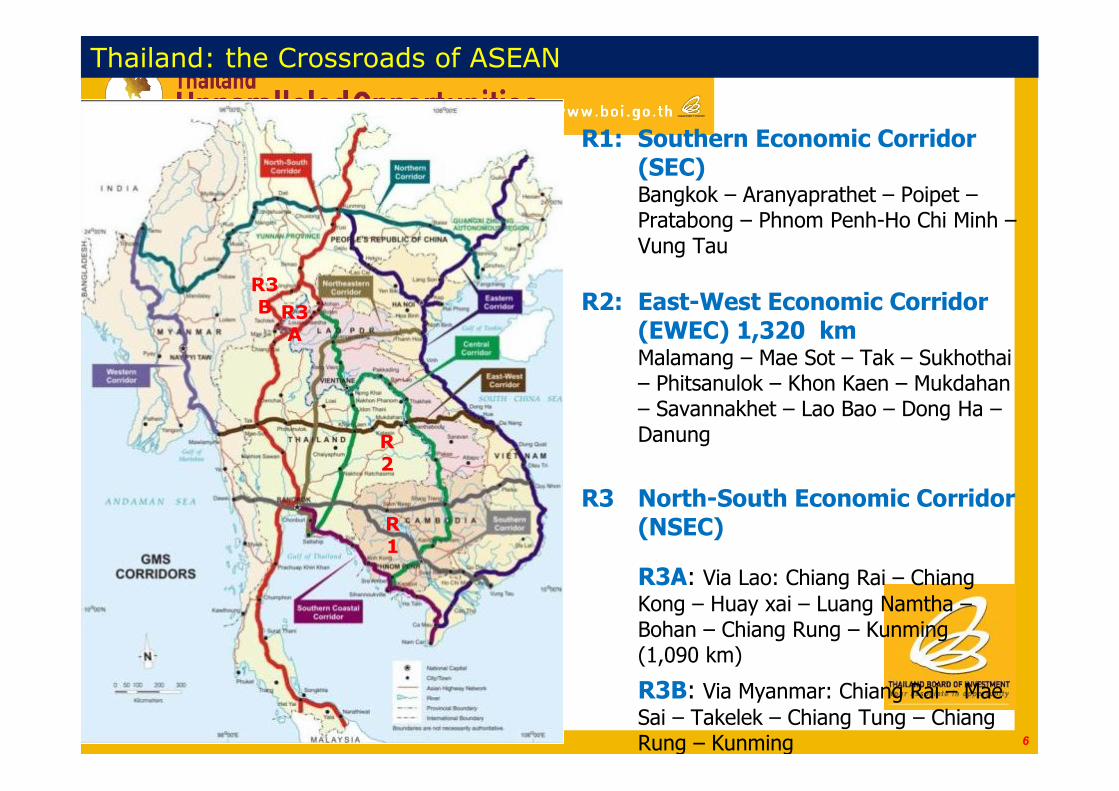

RR11

R1: Southern Economic Corridor (SEC)Bangkok – Aranyaprathet – Poipet –Pratabong – Phnom Penh-Ho Chi Minh –Vung Tau

R2: East-West Economic Corridor (EWEC) 1,320 kmMalamang – Mae Sot – Tak – Sukhothai– Phitsanulok – Khon Kaen – Mukdahan– Savannakhet – Lao Bao – Dong Ha –Danung

R3 North-South Economic Corridor (NSEC)

R3A: Via Lao: Chiang Rai – Chiang Kong – Huay xai – Luang Namtha –Bohan – Chiang Rung – Kunming (1,090 km)

R3B: Via Myanmar: Chiang Rai – Mae Sai – Takelek – Chiang Tung – Chiang Rung – Kunming

R2

R3A

R3B

6

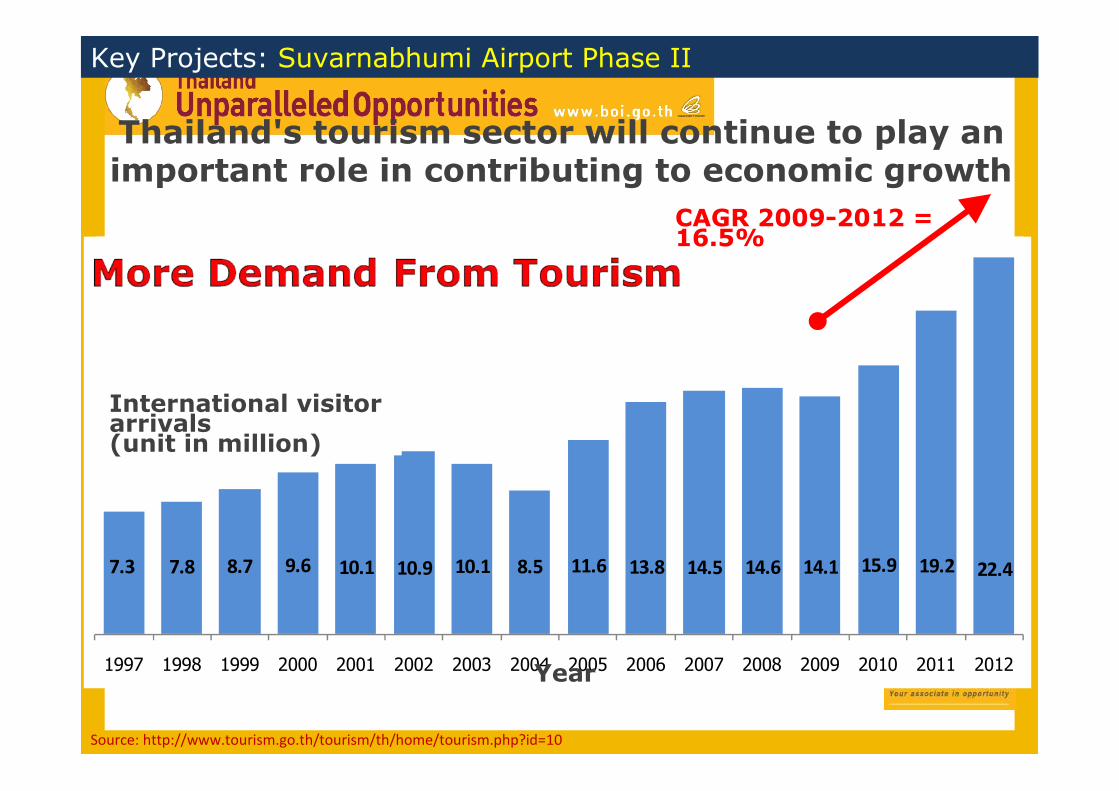

Thailand: the Crossroads of ASEAN

Thailand's tourism sector will continue to play an important role in contributing to economic growth

Source: http://www.tourism.go.th/tourism/th/home/tourism.php?id=10

7.3 7.8 8.7 9.6 10.1 10.9 10.1 8.5 11.6 13.8 14.5 14.6 14.1 15.9 19.2 22.4

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

International visitor arrivals(unit in million)

CAGR 2009-2012 = 16.5%

Year

Key Projects: Suvarnabhumi Airport Phase II

Free Trade Agreement

Note: * Thailand, Malaysia, Indonesia, Philippines, Singapore anNote: * Thailand, Malaysia, Indonesia, Philippines, Singapore and Brunei only.d Brunei only.

ASEAN•+570 million pop.•US$1.3 trillion GDP (2007)

ASEAN+3•+2 billion pop.(1/3 world pop.)•US$9trillion GDP(16% of world GDP)

ASEAN+6•3.3 billion pop.(>50% world pop.)•US$12.25 trillion GDP

Automotive Industry“Thailand: Automotive Hub of Asia”

As of Feb 14, 2013

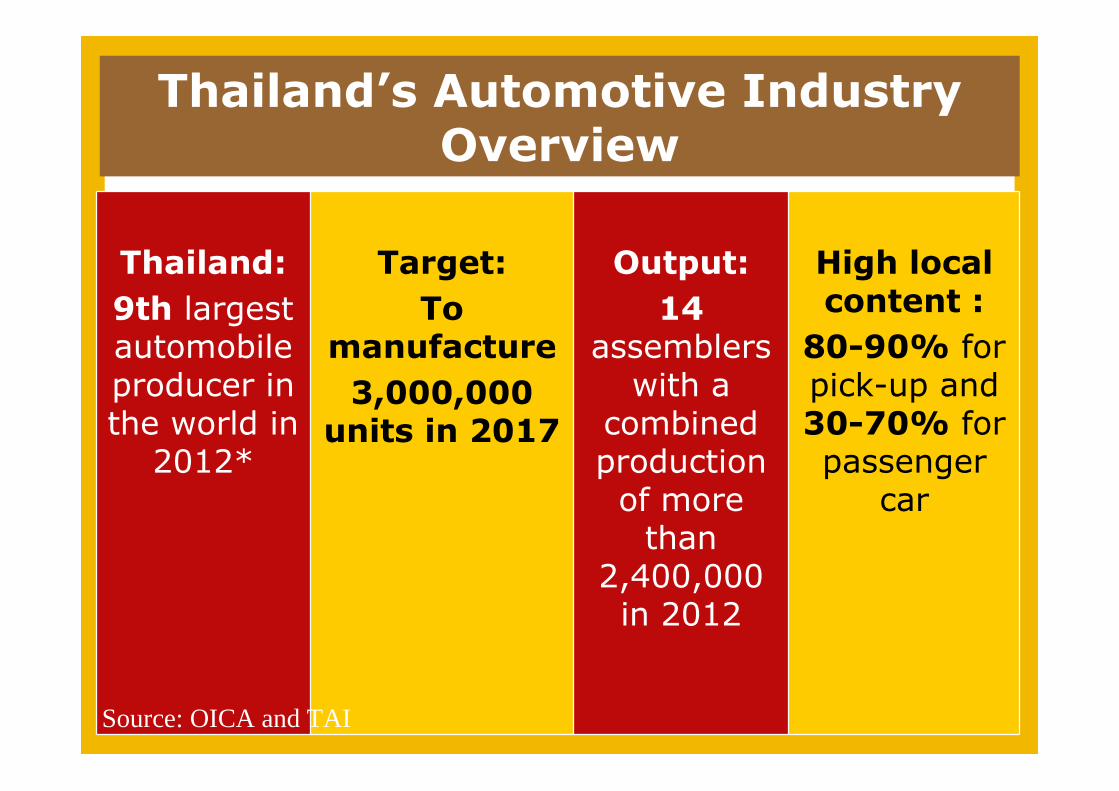

Thailand:9th largest automobile producer in the world in

2012*

Target: To

manufacture3,000,000

units in 2017

Output:14

assemblers with a

combined production

of more than

2,400,000 in 2012

High local content :

80-90% for pick-up and 30-70% for passenger

car

Source: OICA and TAI

Thailand’s Automotive Industry Overview

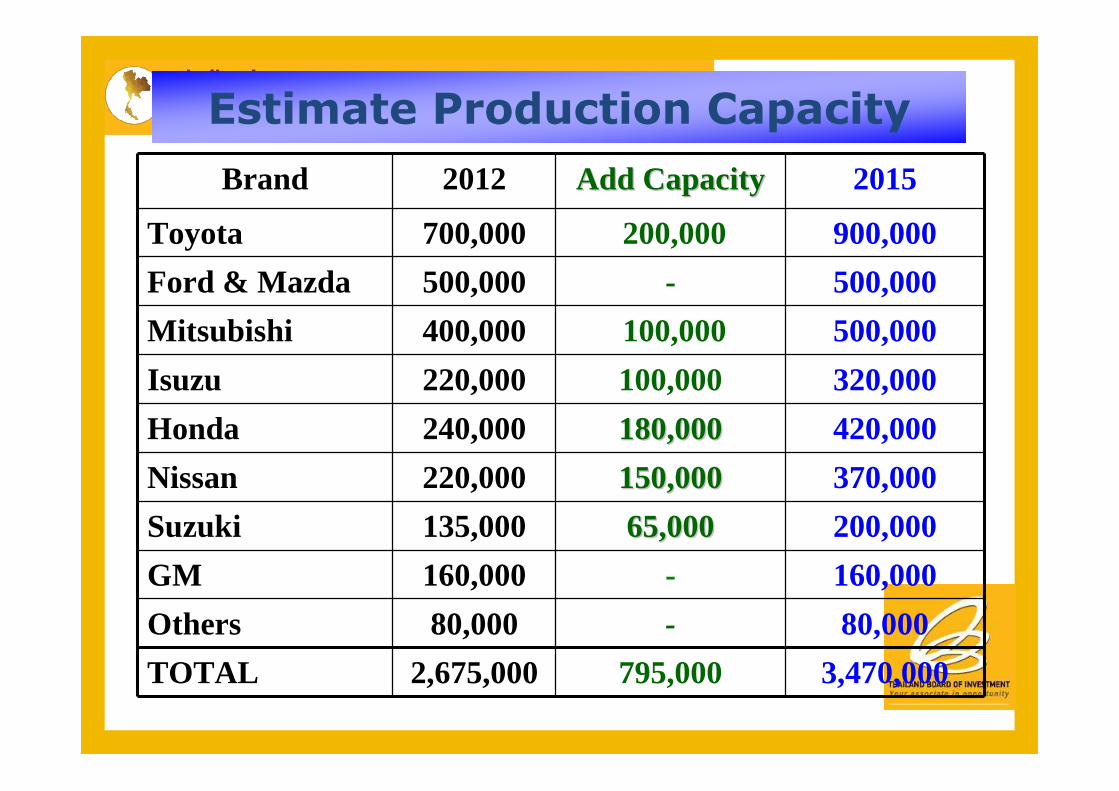

Brand 2012 Add CapacityAdd Capacity 2015

Toyota 700,000 200,000 900,000Ford & Mazda 500,000 - 500,000Mitsubishi 400,000 100,000 500,000Isuzu 220,000 100,000 320,000Honda 240,000 180,000180,000 420,000Nissan 220,000 150,000150,000 370,000Suzuki 135,000 65,00065,000 200,000GM 160,000 - 160,000Others 80,000 - 80,000TOTAL 2,675,000 795,000 3,470,000

Estimate Production Capacity

Need more suppliers capacity to support

3 Million cars Year 2017

Want more machinery, Tooling, Automation

Thailand: Auto Hub of Asia

• Thailand continues to industrialize, but is dependent

on foreign industrial machinery for immediate future.

• High demand for:– Food and farm machinery– Alternative energy/energy conservation machinery– Automotive production machinery– Mould & Die Industry–– Industrial AutomationIndustrial Automation– Logistic Equipment

Opportunities in Machinery

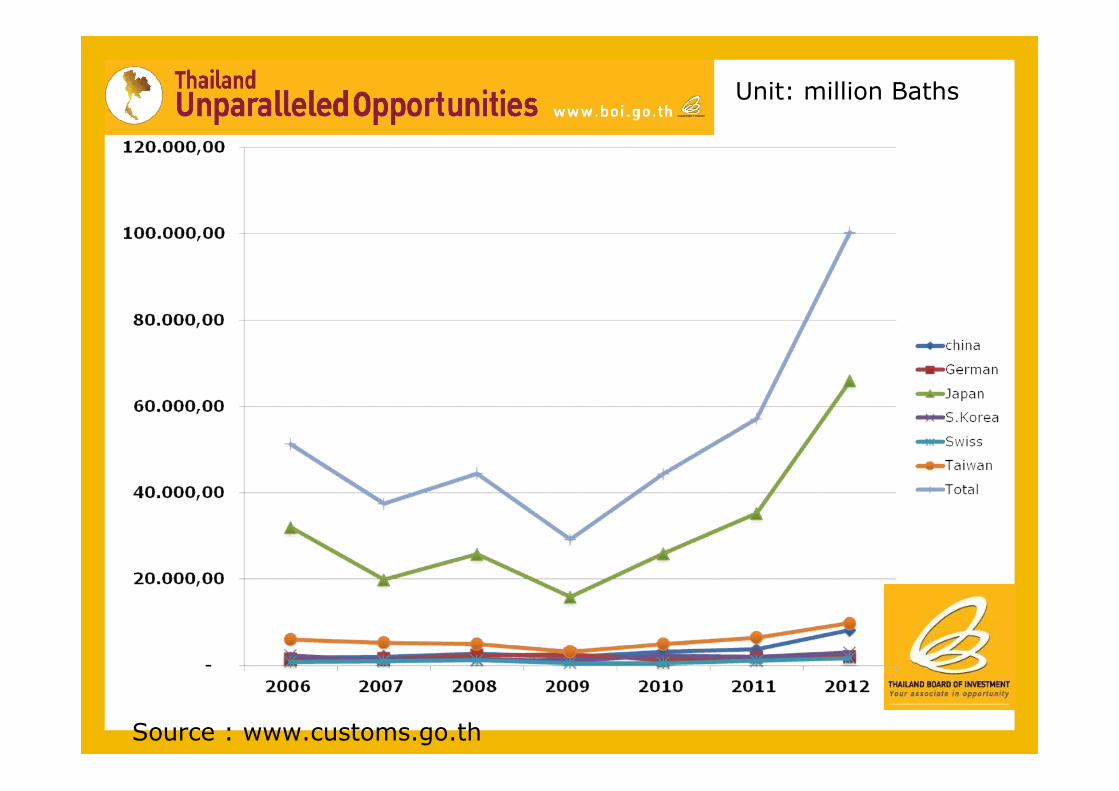

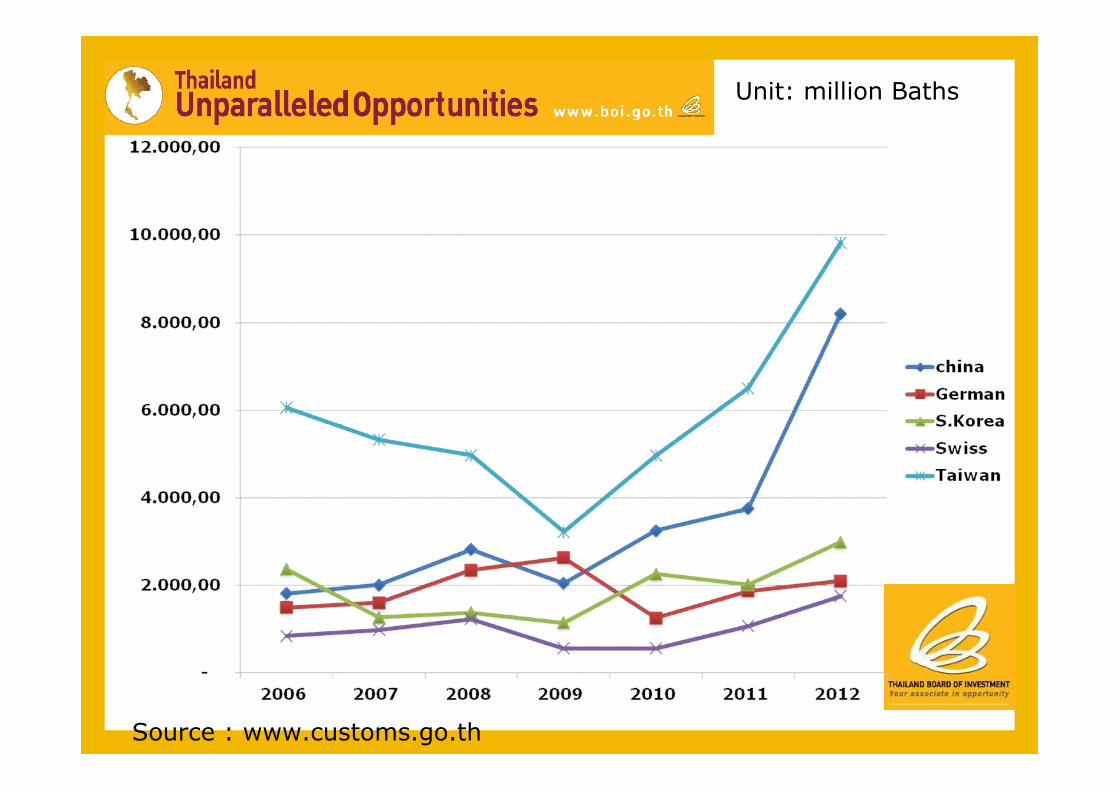

Thailand Import statistic : Metal Machinery + Machine Tool

Metal Processing Machine , Mold &Die and Machine Tool Import Statistic

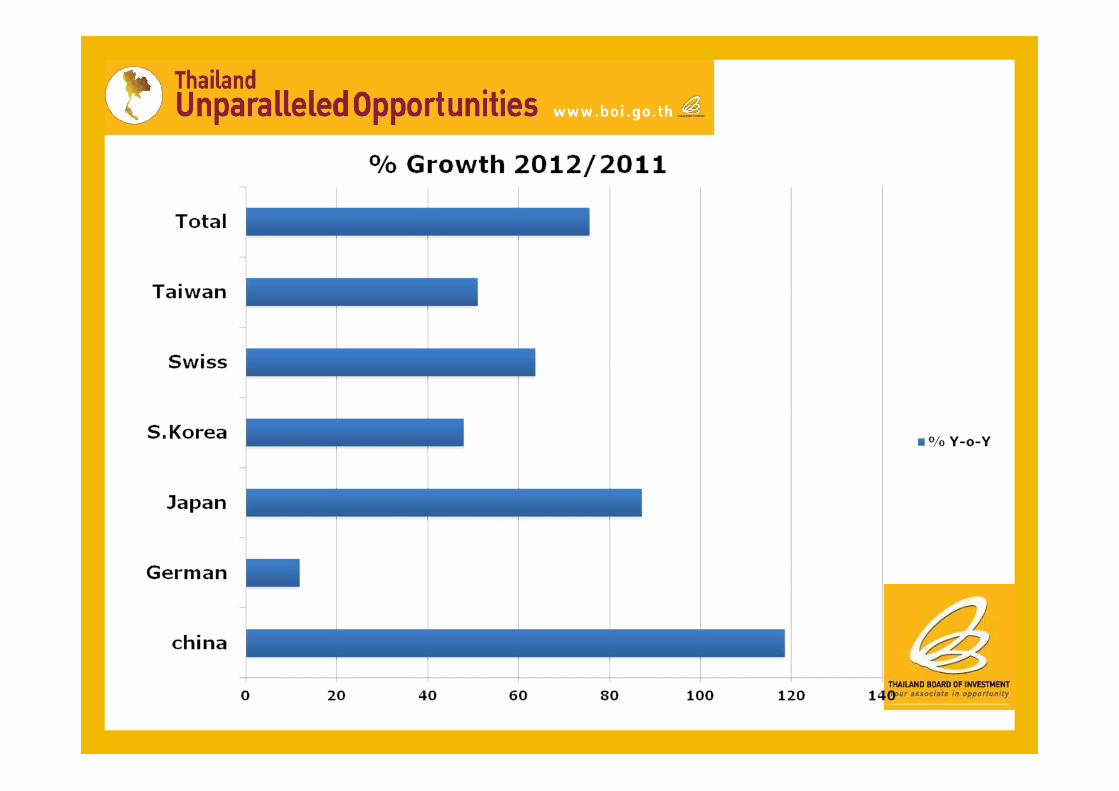

china Germany Japan Korea SWITZERLAND Taiwan Total All Country2006 1,817,707,833 1,495,390,403 32,002,610,692 2,368,576,319 849,234,285 6,061,836,460 51,258,486,828 2007 2,013,176,041 1,603,814,384 19,889,696,940 1,268,607,820 983,916,342 5,329,174,346 37,439,804,438 2008 2,825,446,015 2,348,128,285 25,766,509,552 1,381,417,247 1,233,637,189 4,974,587,621 44,514,989,582 2009 2,050,544,011 2,633,764,639 15,905,290,950 1,150,087,837 566,954,034 3,221,480,293 29,183,766,912 2010 3,255,462,370 1,254,082,684 25,940,584,570 2,261,161,942 561,176,209 4,963,106,209 44,408,077,167 2011 3,756,059,469 1,857,269,893 35,231,926,169 2,021,352,004 1,076,860,821 6,501,652,246 57,135,090,325 2012 8,211,376,157 2,098,159,555 65,926,832,780 2,992,518,450 1,762,295,840 9,824,584,395 100,343,159,310

Plastic and Rubber Import statistic

2007 1,895,742,206 2,073,774,537 7,367,361,739 351,355,687 85,477,663 1,959,733,853 17,117,834,292 2008 2,337,398,315 2,397,286,534 7,188,024,311 709,528,202 74,967,138 2,055,538,286 17,167,123,104 2009 2,387,982,864 1,406,448,829 6,637,853,627 640,395,562 77,648,213 2,608,151,733 15,902,755,226 2010 3,254,251,665 1,797,187,769 6,926,650,103 417,844,714 237,138,967 2,810,064,542 17,930,852,116 2011 4,966,637,263 2,575,144,679 9,992,709,236 775,714 324,655,170 2,841,162,617 24,448,138,157 2012 7,865,882,052 3,098,172,373 20,227,147,487 1,031,151,416 126,172,355 4,170,073,961 40,302,632,841

Unit : Thai Baths

Source : www.customs.go.th

Why Thailand

19

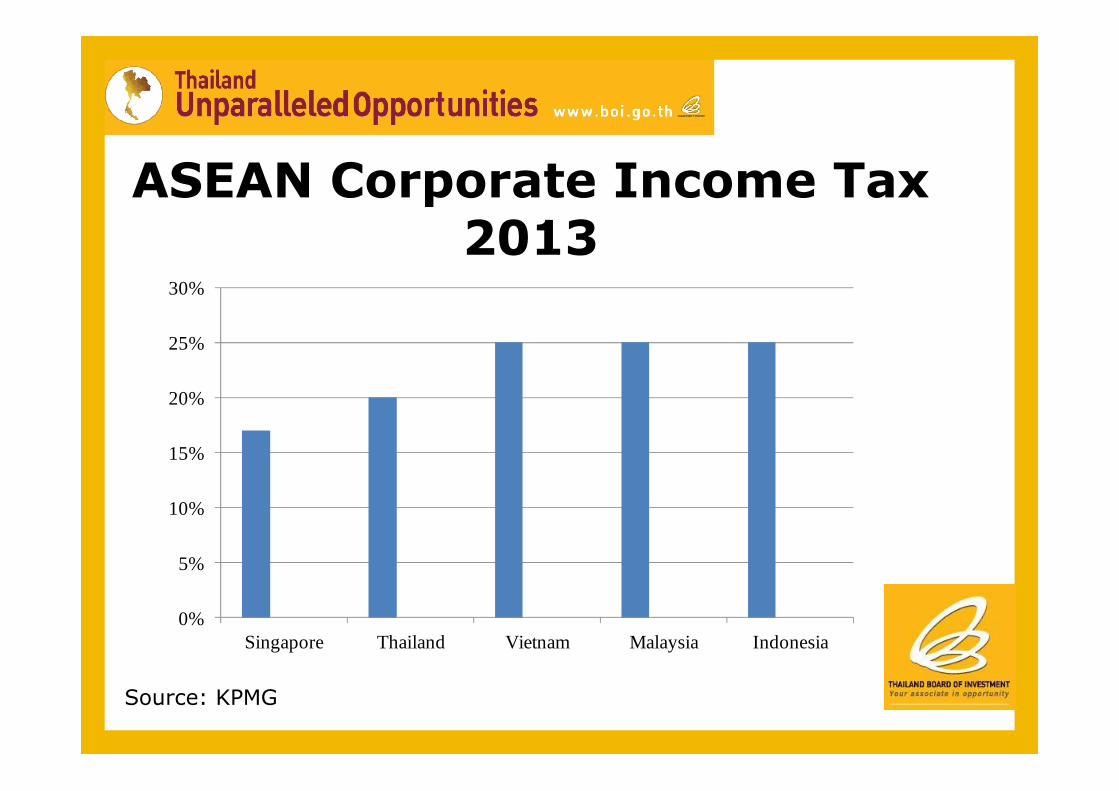

ASEAN Corporate Income Tax 2013

0%

5%

10%

15%

20%

25%

30%

Singapore Thailand Vietnam Malaysia Indonesia

Source: KPMG

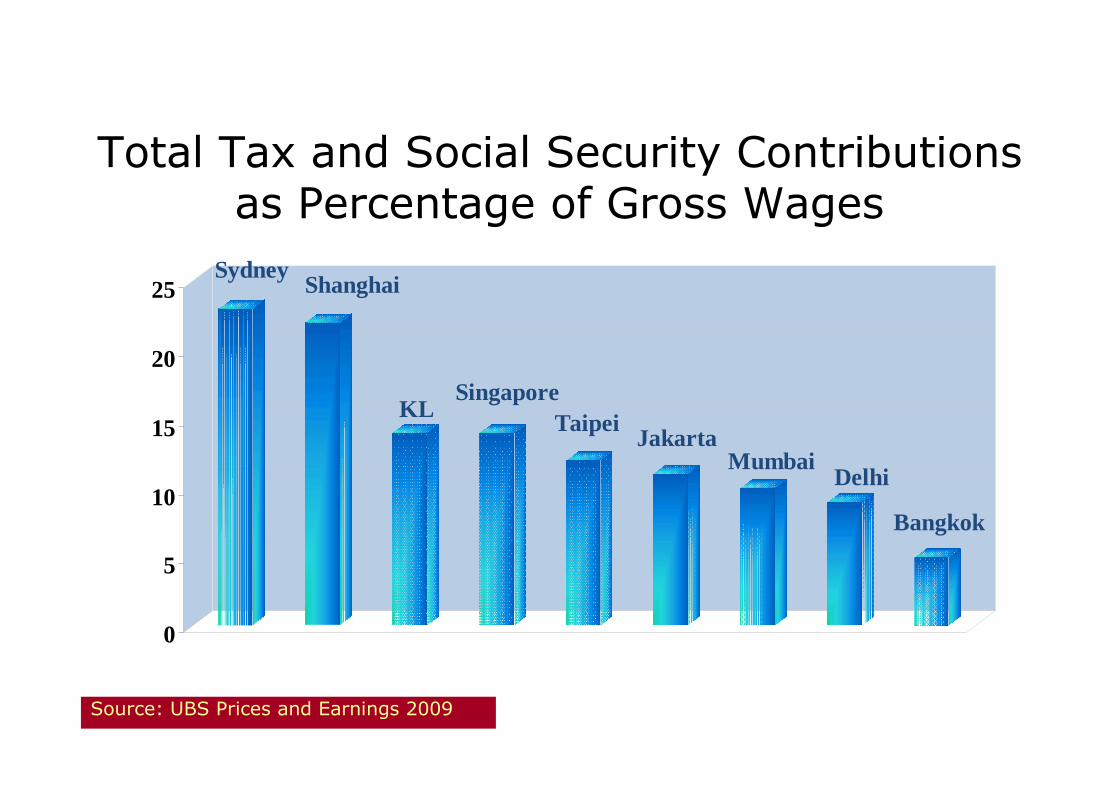

Sydney Shanghai

KLSingapore

Taipei JakartaMumbai Delhi

Bangkok

0

5

10

15

20

25

Source: UBS Prices and Earnings 2009

Total Tax and Social Security Contributions as Percentage of Gross Wages

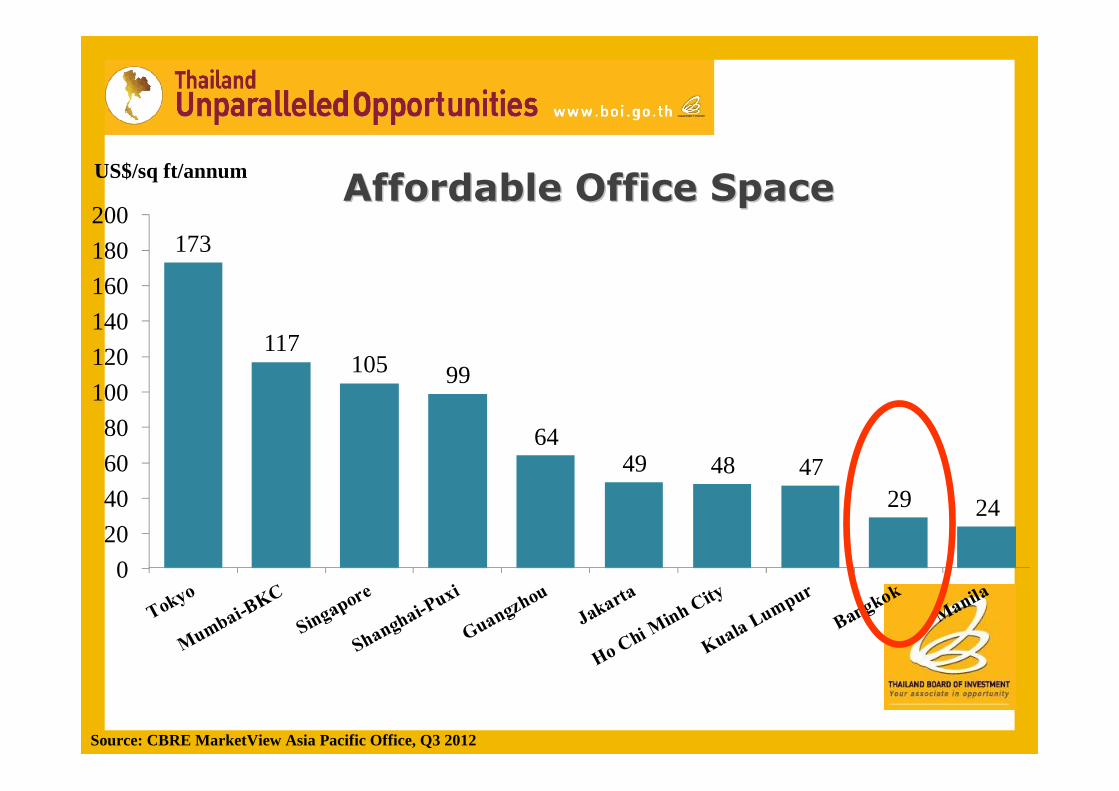

Affordable Office SpaceAffordable Office Space173

117105 99

6449 48 47

29 24

020406080

100120140160180200

US$/sq ft/annum

Source: CBRE MarketView Asia Pacific Office, Q3 2012

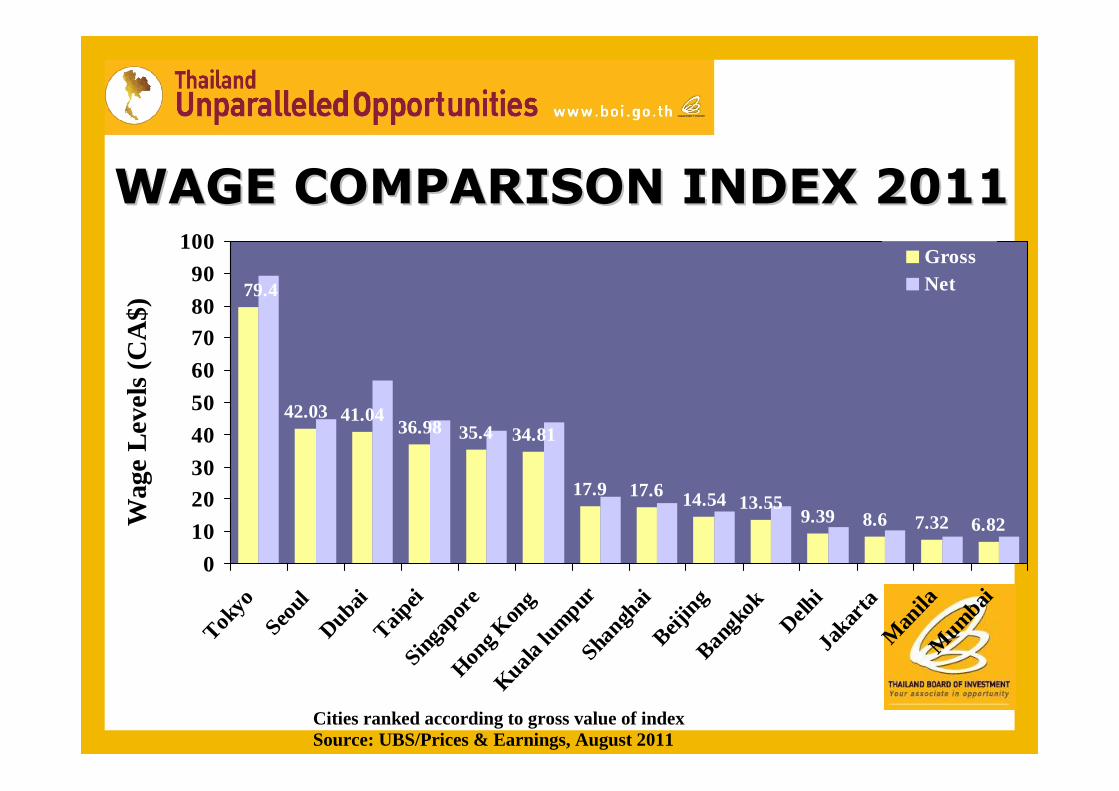

WAGE COMPARISON INDEX 2011WAGE COMPARISON INDEX 2011

42.03 41.0436.98 35.4 34.81

17.9 17.6 14.54 13.559.39 8.6 7.32 6.82

79.4

0102030405060708090

100

Tokyo

Seoul

DubaiTaip

eiSing

apor

eHon

g Kon

gKuala

lumpur

Shangh

aiBeij

ingBan

gkok

Delhi

Jakar

taM

anila

Mumbai

Wag

e Le

vels

(CA

$)

GrossNet

Cities ranked according to gross value of index Source: UBS/Prices & Earnings, August 2011

ØThailand has over 60 Industrial estates, zones and parks nationwide

Modern Industrial EstatesModern Industrial Estates

(25)

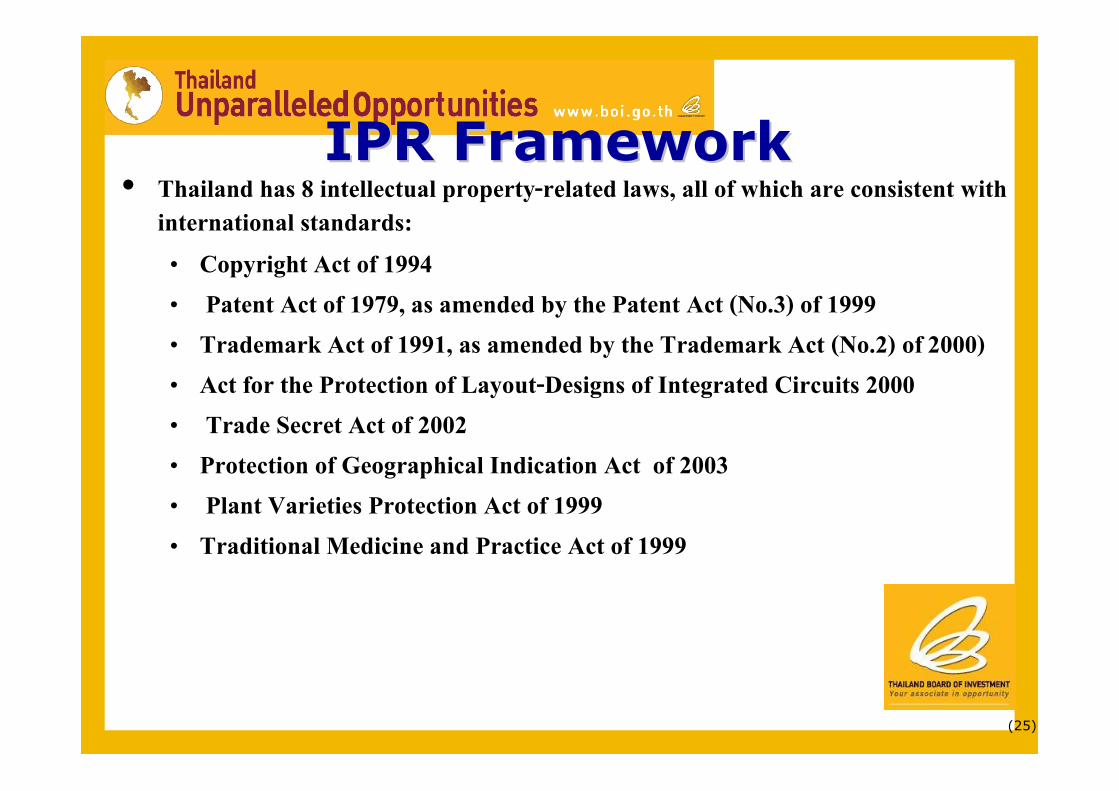

IPR FrameworkIPR Framework• Thailand has 8 intellectual property-related laws, all of which are consistent with

international standards: • Copyright Act of 1994• Patent Act of 1979, as amended by the Patent Act (No.3) of 1999• Trademark Act of 1991, as amended by the Trademark Act (No.2) of 2000) • Act for the Protection of Layout-Designs of Integrated Circuits 2000• Trade Secret Act of 2002 • Protection of Geographical Indication Act of 2003• Plant Varieties Protection Act of 1999 • Traditional Medicine and Practice Act of 1999

Country Rankings

Thailand 1

Canada 2South Africa 3Malaysia 4

Philippines 5Australia 6Spain 7New Zealand 8Belgium 9United States 10

Expat Experience 2011Expat Experience 2011

Source: Expat Explorer Survey 2011, HSBC as of Nov 28, 2011 (3,385 respondents)

“For those looking for the best overall expat experience, our findings this year show Thailand as the top expat destination, being ranked as number one by our expats for ease of organizing healthcare, finding accommodation and the work environment. Last year this destination was ranked highly as a retirement hotspot so it’s great to see the country develop in terms of its economic appeal.

Lisa Wood, head of marketing at HSBC Bank

International

Thailand has been chosen as the best

country in the world for expats

to live

Market Access : Exhibition

Know Local customer

• service

• Training

• Loan Support

Service and support from Service and support from GovernmentGovernment

Roles of the BOIRoles of the BOI• Facilitating market entry—100% foreign ownership

in manufacturing and most services eligible for BOI promotion

• Reducing initial investment costs through provision of tax incentives

• Providing business-related services– Information – Site visits– Subcontracting development

• Facilitating business operations– Right to own land– Visas and work permits– Help Desk

Thailand and the BOI offer:

• Facilitating market entry—100% foreign ownership in manufacturing and most services eligible for BOI promotion

• Reducing initial investment costs through provision of tax incentives

• Providing business-related services– Information – Site visits– Subcontracting development

• Facilitating business operations– Right to own land– Visas and work permits– Help Desk

Roles of the BOIRoles of the BOI

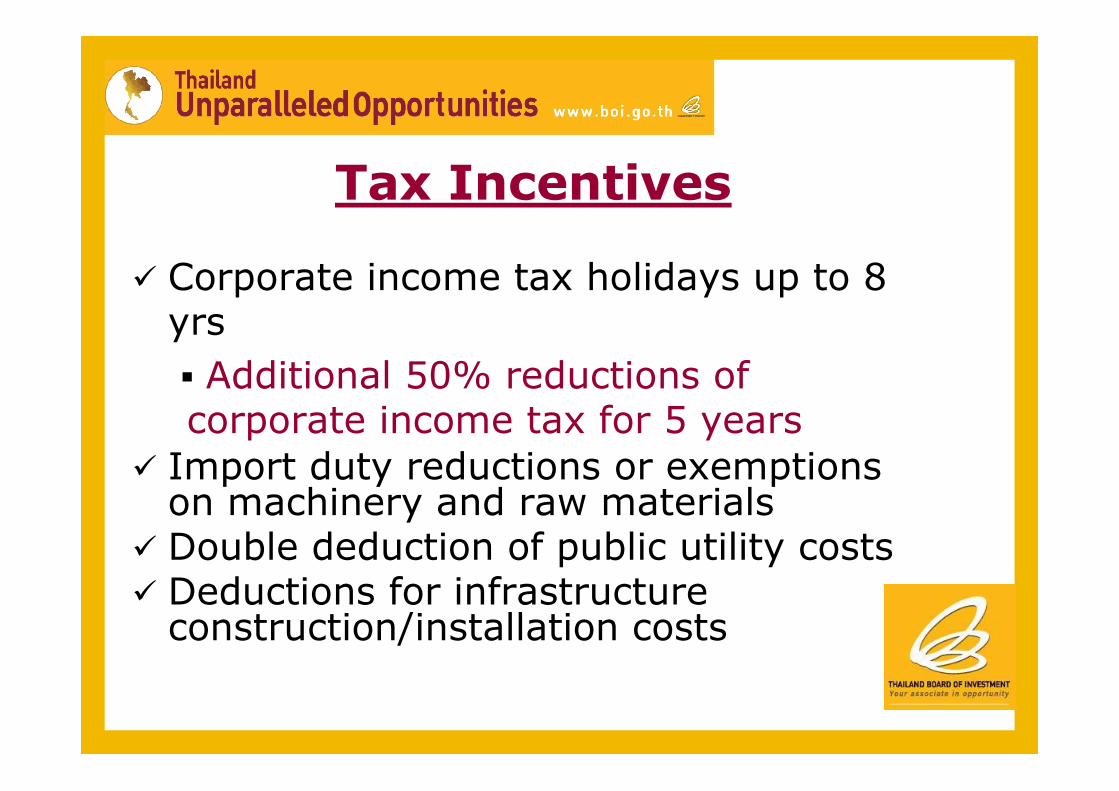

Tax Incentives

ü Corporate income tax holidays up to 8 yrs§ Additional 50% reductions of corporate income tax for 5 years

ü Import duty reductions or exemptions on machinery and raw materials

ü Double deduction of public utility costsü Deductions for infrastructure

construction/installation costs

Roles of the BOIRoles of the BOI• Facilitating market entry—100% foreign ownership in

manufacturing and most services eligible for BOI promotion

• Reducing initial investment costs through provision of tax incentives

• Providing business-related services– Information – Site visits– Sourcing

• Facilitating business operations– Right to own land– Visas and work permits– Help Desk

• Facilitating market entry—100% foreign ownership in manufacturing and most services eligible for BOI promotion

• Reducing initial investment costs through provision of tax incentives

• Providing business-related services– Information – Site visits– Subcontracting development

• Facilitating business operations– Right to own land– Visas and work permits– Help Desk

Roles of the BOIRoles of the BOI

36

18th Floor, Chamchuri Square Building319 Phayathai Road, PathumwanDomestic Call: 0 2209 1100, Inter. Call: (66 2) 209 1100Email: [email protected]

More Convenience, less time,more efficiency!

More Convenience, less time,more efficiency!

One Start One Stop Investment Center

37373737

Mr. Chanin KhaochanDirectorThailand Board of Investment, Frankfurt OfficeBethmannstrasse 58, 60311 Frankfurt am Main, Germany

Tel.: +49 69 929 1230Fax: +49 69 929 123 20Email: [email protected]: www.boi.go.th

BOI OFFICE IN GERMANYBOI OFFICE IN GERMANY

THANK YOUTHANK YOU

Frankfurt• Thailand Board of Investment• Bethmannstr 58, 60311 Frankfurt am Main Germany• Telephone: (49 69) 92 91 230 Fax: (49 69) 92 91 232• Email: [email protected]