Embed Size (px)

Citation preview

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 1

BDI/WEC workshop on ETP 2014

Technology as a basis for the

transformation of the energy system

Dr. Frank-Detlef Drake, RWE AG

Berlin, May 22nd, 2014

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 2

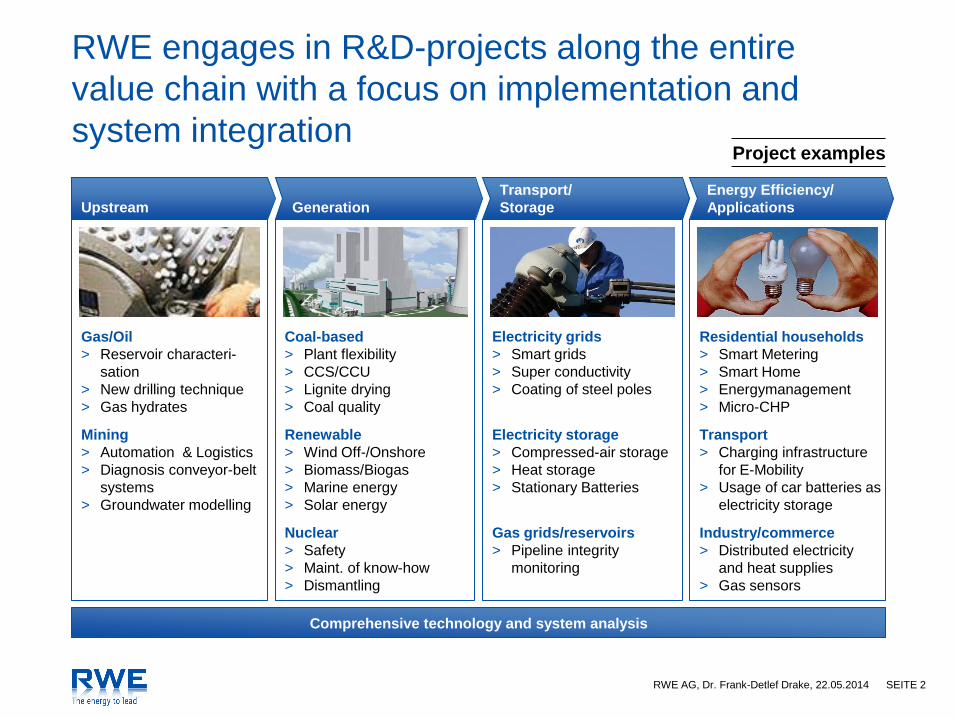

RWE engages in R&D-projects along the entire

value chain with a focus on implementation and

system integration

Upstream Generation

Transport/

Storage

Energy Efficiency/

Applications

Comprehensive technology and system analysis

Gas/Oil

> Reservoir characteri-

sation

> New drilling technique

> Gas hydrates

Mining

> Automation & Logistics

> Diagnosis conveyor-belt

systems

> Groundwater modelling

Coal-based

> Plant flexibility

> CCS/CCU

> Lignite drying

> Coal quality

Electricity grids

> Smart grids

> Super conductivity

> Coating of steel poles

Residential households

> Smart Metering

> Smart Home

> Energymanagement

> Micro-CHP

Renewable

> Wind Off-/Onshore

> Biomass/Biogas

> Marine energy

> Solar energy

Electricity storage

> Compressed-air storage

> Heat storage

> Stationary Batteries

Transport

> Charging infrastructure

for E-Mobility

> Usage of car batteries as

electricity storage

Nuclear

> Safety

> Maint. of know-how

> Dismantling

Gas grids/reservoirs

> Pipeline integrity

monitoring

Industry/commerce

> Distributed electricity

and heat supplies

> Gas sensors

Project examples

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 3

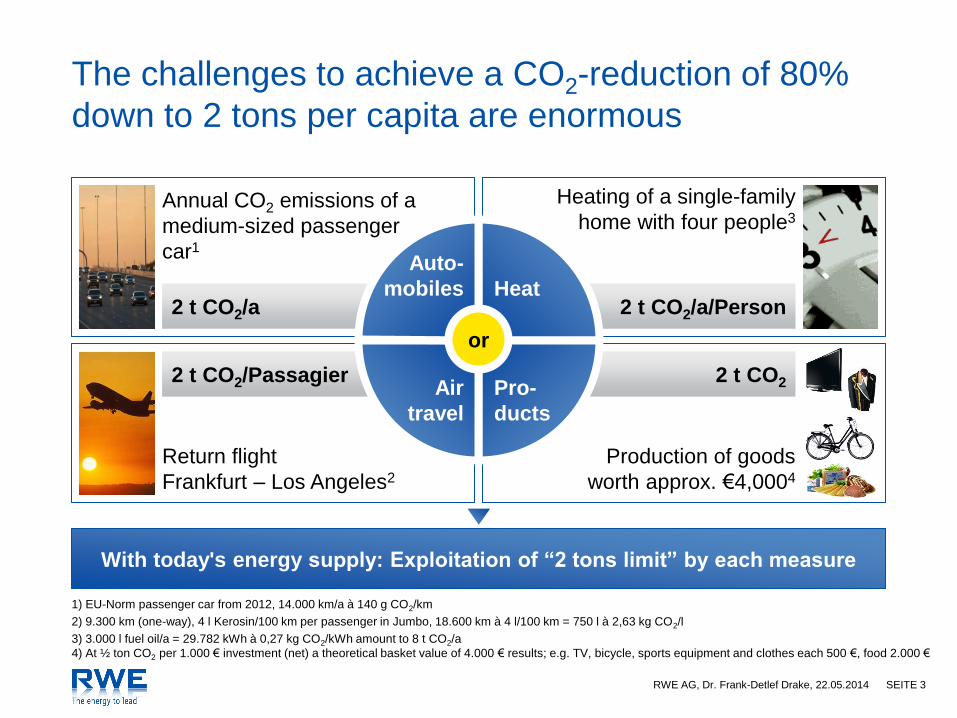

Return flight

Frankfurt – Los Angeles2

2 t CO2/Passagier

Annual CO2 emissions of a

medium-sized passenger

car1

2 t CO2/a

The challenges to achieve a CO2-reduction of 80%

down to 2 tons per capita are enormous

Heating of a single-family

home with four people3

Production of goods

worth approx. €4,0004

With today's energy supply: Exploitation of “2 tons limit” by each measure

2 t CO2

2 t CO2/a/Person

or

Auto-

mobiles Heat

Air

travel

Pro-

ducts

1) EU-Norm passenger car from 2012, 14.000 km/a à 140 g CO2/km

2) 9.300 km (one-way), 4 l Kerosin/100 km per passenger in Jumbo, 18.600 km à 4 l/100 km = 750 l à 2,63 kg CO2/l

3) 3.000 l fuel oil/a = 29.782 kWh à 0,27 kg CO2/kWh amount to 8 t CO2/a

4) At ½ ton CO2 per 1.000 € investment (net) a theoretical basket value of 4.000 € results; e.g. TV, bicycle, sports equipment and clothes each 500 €, food 2.000 €

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 4

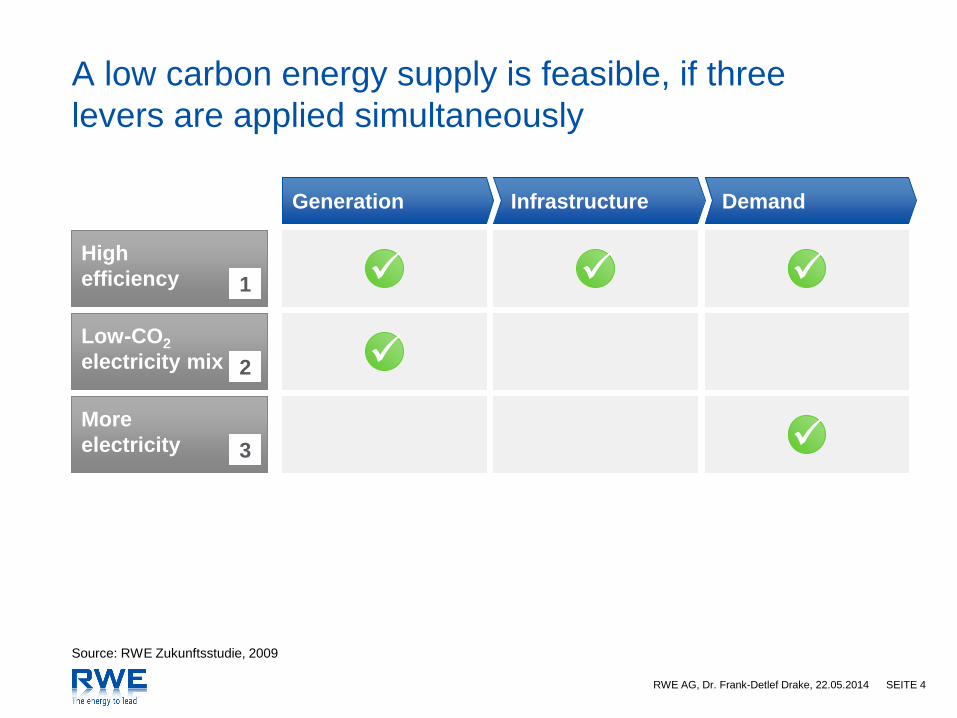

A low carbon energy supply is feasible, if three

levers are applied simultaneously

High

efficiency

More

electricity

Low-CO2

electricity mix

Generation Infrastructure Demand

1

2

3

Source: RWE Zukunftsstudie, 2009

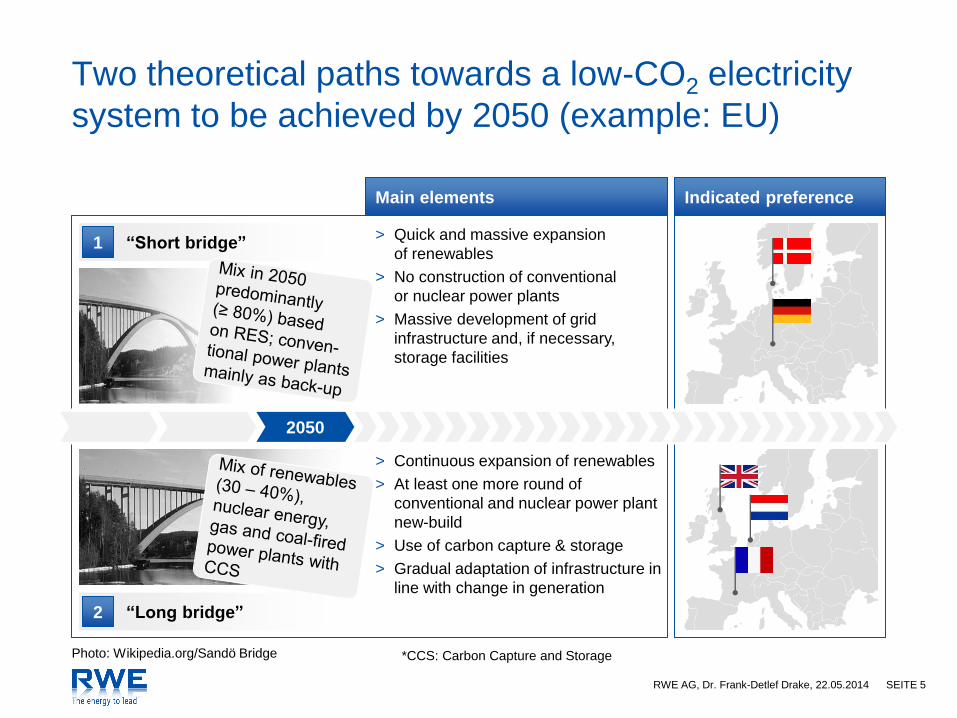

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 5

Two theoretical paths towards a low-CO2 electricity

system to be achieved by 2050 (example: EU)

Photo: Wikipedia.org/Sandö Bridge

2050

“Short bridge” > Quick and massive expansion

of renewables

> No construction of conventional

or nuclear power plants

> Massive development of grid

infrastructure and, if necessary,

storage facilities

> Continuous expansion of renewables

> At least one more round of

conventional and nuclear power plant

new-build

> Use of carbon capture & storage

> Gradual adaptation of infrastructure in

line with change in generation

“Long bridge”

Main elements Indicated preference

1

2

*CCS: Carbon Capture and Storage

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 6

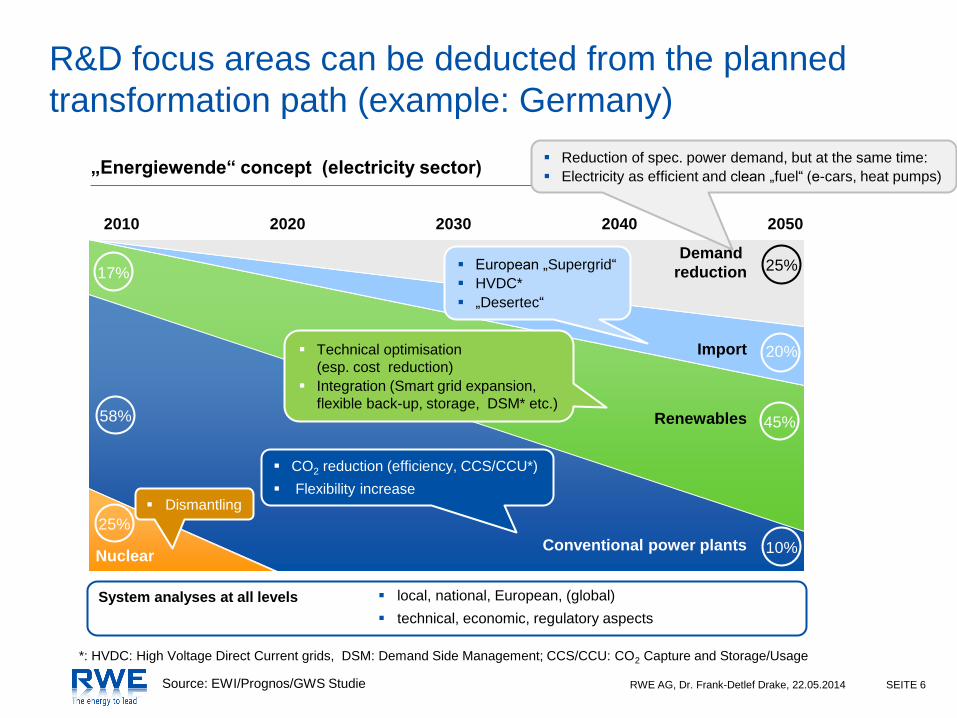

R&D focus areas can be deducted from the planned

transformation path (example: Germany)

„Energiewende“ concept (electricity sector)

Source: EWI/Prognos/GWS Studie

2010 2020 2050 2030 2040

Nuclear Conventional power plants

Renewables

Import

Demand

reduction 17%

25%

58% 45%

10%

20%

25%

System analyses at all levels local, national, European, (global)

technical, economic, regulatory aspects

Dismantling

CO2 reduction (efficiency, CCS/CCU*)

Flexibility increase

Technical optimisation

(esp. cost reduction)

Integration (Smart grid expansion,

flexible back-up, storage, DSM* etc.)

European „Supergrid“

HVDC*

„Desertec“

Reduction of spec. power demand, but at the same time:

Electricity as efficient and clean „fuel“ (e-cars, heat pumps)

*: HVDC: High Voltage Direct Current grids, DSM: Demand Side Management; CCS/CCU: CO2 Capture and Storage/Usage

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 7

View on important ETP 2014 findings (1/2)

> ETP presents an encompassing and highly valuable work with a global as well as

clear system perspective and many important findings: Congratulation!

> Importance of system analysis cannot be overemphasized regarding the intricate

interplay of technology, economy, regulation and society. Future market design

needs to take these interdepencies into account (presently often not the case!)

> In light of fast technological developments, long-term goals, size of the challenge

and complexity of the energy system, a non-dogmatic, supra-national and

technology-open approach is of utmost importance

> Key levers for a cost-efficient and sustainable future energy system are efficiency,

decarbonisation of the power sector and a shift towards electricity in all sectors

o A cap and trade system such as the ETS ensures already today that

electrification of e.g. mobility or heating does not lead to higher emissions.

o With pressure on CO2-emissions, we will see again more coal-to-gas shift in

conventional generation. But, as ETP points out rightfully, also gas is a bridge.

o Word of caution: the realistic economic potential of efficiency might be lower

than postulated in many studies – so we should not rely on it and take rebound

effects into account

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 8

View on important ETP 2014 findings (2/2)

> On RES: cost will come down further and competetiveness with conventional

plants “in sight” in many regions of the world, but “LCOE” and real cost (including

risk-adjusted cost of capital) differ largely. Financing is a key issue.

> On RES-integration:

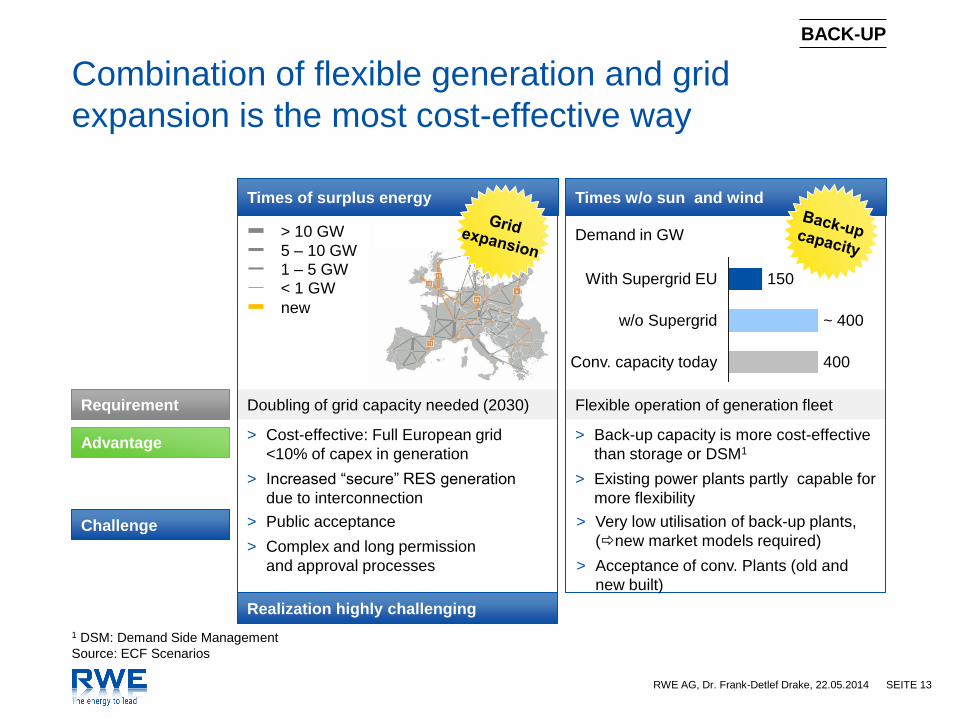

> Combination of (smart) grid expansion and flexible back-up power plants is most

cost-efficient, but requires acceptance!

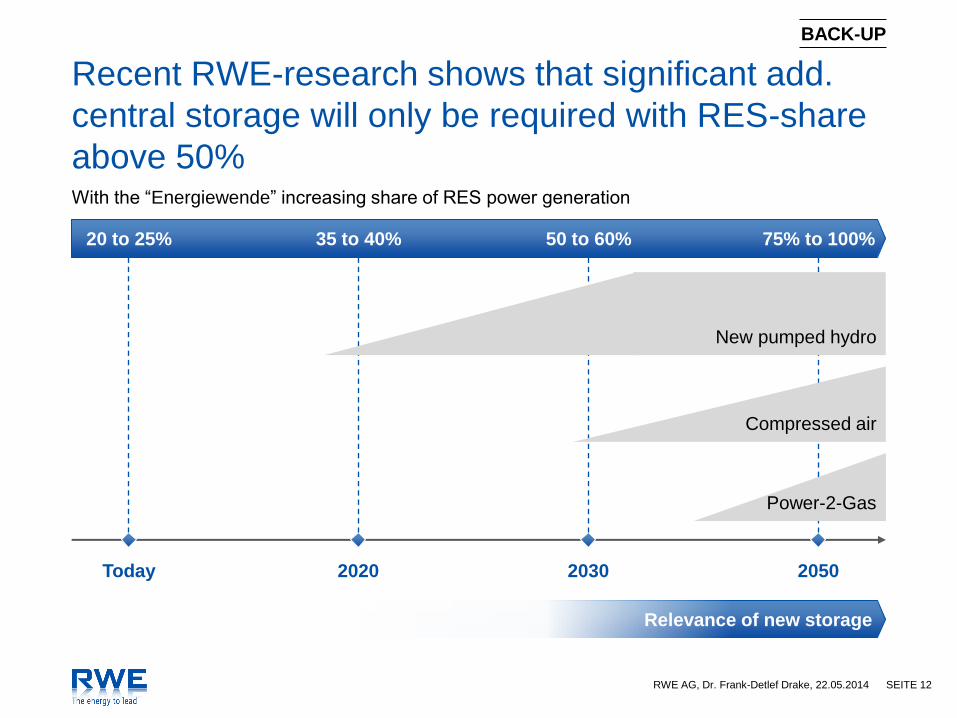

> Storage is not the “golden bullet” (yet): RWE research also shows that

significant additional central storage will only be needed beyond RES shares of

50%. Intense and diverse R&D is needed to develop options and bring down

cost. Battery developments with potential to be “game-changing”.

> On CCS: from a global perspective it looks indispensable, but the more

concrete/local you go, the higher the hurdles. We cannot count on it.

> On Smart Grid: the more volatile and the more decentral generation becomes, the

more smartness we need. There are “before the meter” and “beyond the meter”

measures (e.g DSM, smart charging…), which need effective coordination

(especially in unbundled markets)

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 9

BACK-UP

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 10

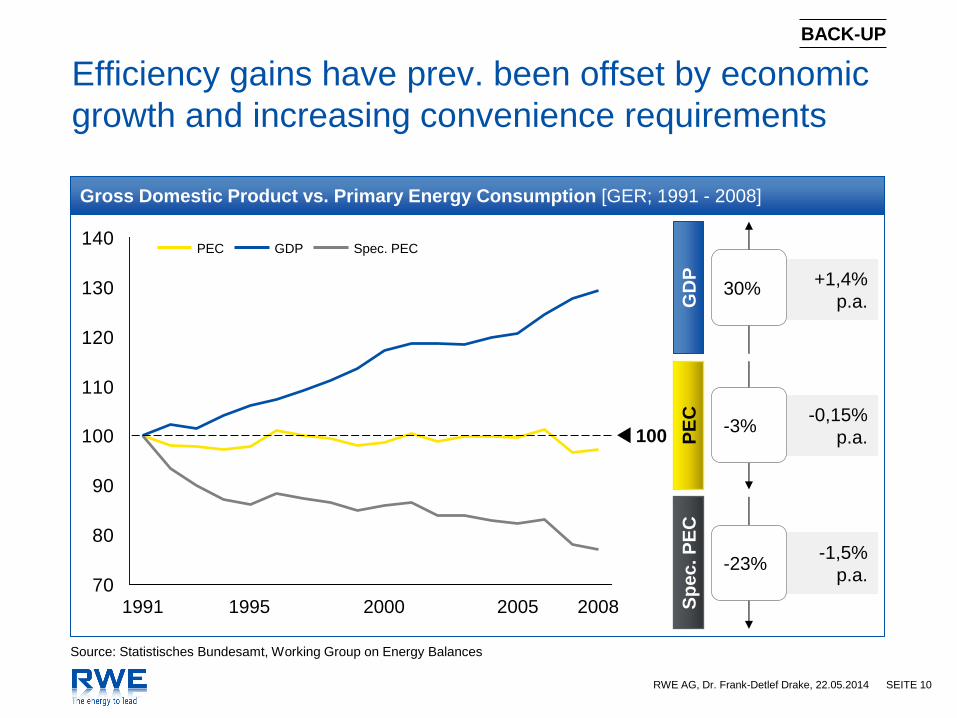

Efficiency gains have prev. been offset by economic

growth and increasing convenience requirements

BACK-UP

Gross Domestic Product vs. Primary Energy Consumption [GER; 1991 - 2008]

70

80

90

100

110

120

130

140

2005 2008

100

1991 1995 2000

GDP Spec. PEC PEC

GD

P

PE

C

Sp

ec

. P

EC

+1,4%

p.a.

-0,15%

p.a.

-1,5%

p.a.

30%

-3%

-23%

Source: Statistisches Bundesamt, Working Group on Energy Balances

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 11

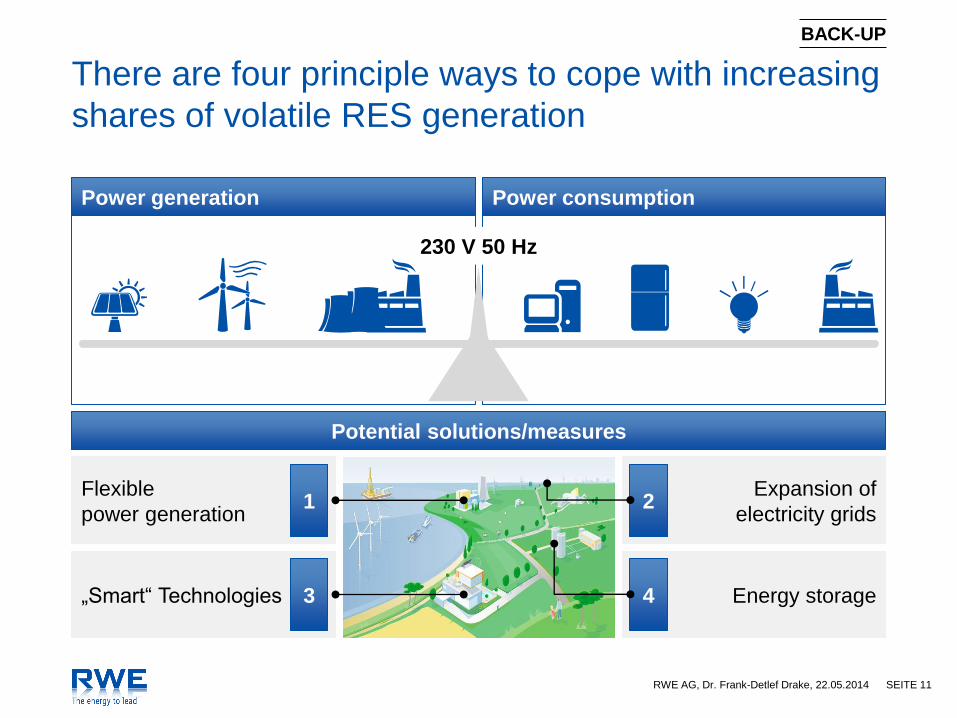

There are four principle ways to cope with increasing

shares of volatile RES generation

Power generation Power consumption

Potential solutions/measures

Flexible

power generation

„Smart“ Technologies

Expansion of

electricity grids

Energy storage 3

1

4

2

230 V 50 Hz

BACK-UP

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 12

Recent RWE-research shows that significant add.

central storage will only be required with RES-share

above 50%

Today

With the “Energiewende” increasing share of RES power generation

20 to 25%

2020

35 to 40%

2030

50 to 60%

2050

75% to 100%

Relevance of new storage

New pumped hydro

Compressed air

Power-2-Gas

BACK-UP

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 13

Combination of flexible generation and grid

expansion is the most cost-effective way

1 DSM: Demand Side Management

Source: ECF Scenarios

Times of surplus energy Times w/o sun and wind

Conv. capacity today 400

w/o Supergrid ~ 400

With Supergrid EU 150

> 10 GW

5 – 10 GW

1 – 5 GW

< 1 GW

Requirement

Advantage

Challenge

Doubling of grid capacity needed (2030) Flexible operation of generation fleet

Demand in GW

> Cost-effective: Full European grid

<10% of capex in generation

> Increased “secure” RES generation

due to interconnection

> Public acceptance

> Complex and long permission

and approval processes

> Back-up capacity is more cost-effective

than storage or DSM1

> Existing power plants partly capable for

more flexibility

> Very low utilisation of back-up plants,

(new market models required)

> Acceptance of conv. Plants (old and

new built)

Realization highly challenging

new

BACK-UP

RWE AG, Dr. Frank-Detlef Drake, 22.05.2014 SEITE 14

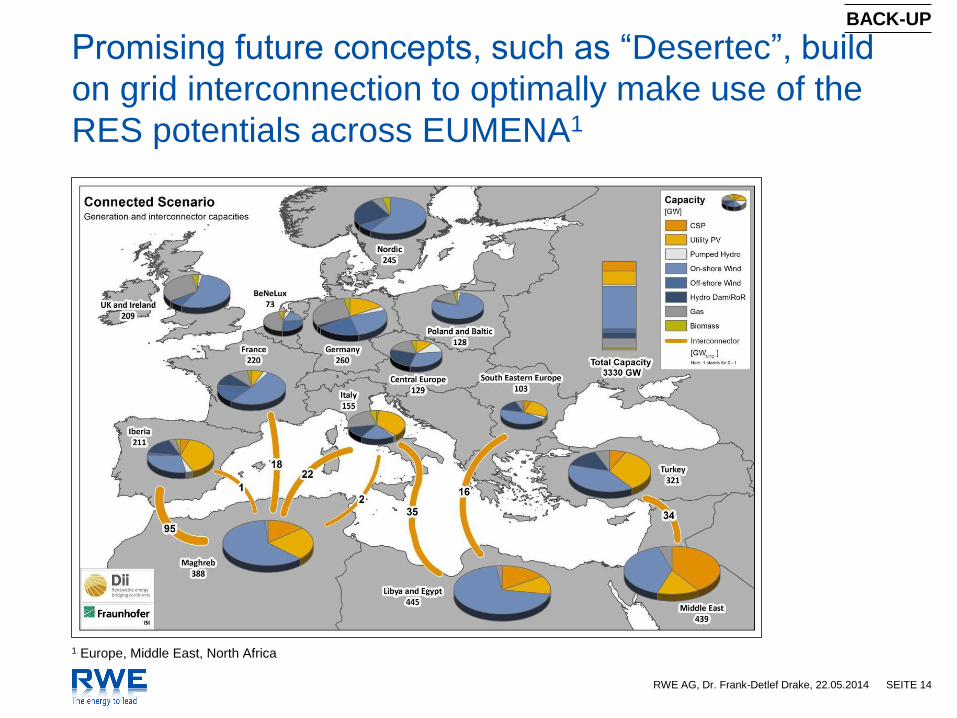

Promising future concepts, such as “Desertec”, build

on grid interconnection to optimally make use of the

RES potentials across EUMENA1

1 Europe, Middle East, North Africa

BACK-UP

![Sheet 07.5: Matrices II: Inverse, Basis Transformation · PDF file · 2016-08-16... Gaussian elimination and matrix inversion [4] ... Find the matrix T =1, and use the inverse transformation](https://img.pdfslide.us/doc/110x75/5ab9033d7f8b9ad3038d7e1c/sheet-075-matrices-ii-inverse-basis-transformation-gaussian-elimination.jpg)