Embed Size (px)

Citation preview

Helvea Swiss Equites Conference 2013

Bad Ragaz, January 18, 2013

Michael Buscher (CEO)

Andreas Schwarzwälder (Head of Investor Relations)

Oerlikon’s Transformation

save space

3 pillars as basis for Oerlikon’s Transformation

January 2013_Investor Presentation

PORTFOLIO REFINANCING OPERATIONAL EXCELLENCE

OERLIKON’S TRANSFORMATION

Page 2

save space

4.00

6.00

8.00

10.00

12.00

Oerlikon Portfolio – Streamlined portfolio with reduced volatility

Apr 16, 2012 Divestment of Pilatus stake

Mar 23, 2012 Sale of Arbon

property

Page 3

Oerlikon

Textile

Drive Systems

Vacuum

Coating

Advanced Technologies

Jun 29 & Oct 29, 2012 Streamlining of manufacturing

footprint of Drive Systems

Dec 3, 2012 Announcement Natural Fibers / Textile Components divestment

Nov 27, 2012 Closing Solar divestment

Mar 2, 2012 Announcement

Solar divestment

Jul 2, 2012 Divestment of Melco

in Textile Segment

January 2013_Investor Presentation

save space

Balanced Oerlikon Portfolio

Page 4

BALANCED SEGMENT

SALES

Divestment of Natural Fibers / Textile Components business

reduces Textile exposure from over 50 % to some 30 %

Potential: Portfolio adjustments and accelerated growth to

further balance Segment sales

BALANCED GEOGRAPHIC

SALES

Balanced geographic portfolio

Growth providing Asian region to account for 43 % of total

sales (preliminary HY 2012 figures)

CURRENCY EXPOSURE

No major currency mismatch between sales, COGS and

overhead costs – natural hedge in place

Limited Swiss Franc exposure

Limited transaction risk

SERVICE Service & spare parts to account for 21 % of total sales

Potential: Strengthening of service business to increase

proportion of recurring revenue

12%

Other

RMB 7%

USD

17%

EURO

60%

CHF

4%

January 2013_Investor Presentation

RoW

6%

Asia / Pacific

43%

North America

20%

Europe

32%

Service & Spare Parts

21%

79%

18% Coating

Vacuum

15%

30%

Drive Systems

Textile 33%

4%

Adv. Techn.

Goods, Equipment & Components

save space

Oerlikon Portfolio – Textile Segment Focus on manmade fiber business

HIGH- PERFORMING

BUSINESS

Profitability and growth of manmade fiber

business twice as high as of natural

fiber business (substitution and

new applications)

Order books already filled until

beginning of 2015

Manmade fiber business with less cyclicality

STRONG CUSTOMER

BASE

Strong and concentrated customer base with around 15 customers to account for 50 %

of Segment sales

Long-term investment horizon of customers

Strong balance sheets and access to financing

Customers also invest in upstream capacities

COMPETITIVE ADVANTAGE

Technological leadership

Focus on energy efficiency/e-save (e.g. Wings FDY energy

consumption reduced by up to 25 %)

Provider of process equipment

Page 5

* 2011 figures

Medical clothes

Home Automotive

Sports

Smart clothes

Construction

January 2013_Investor Presentation

save space

Oerlikon Portfolio – Textile Segment Overview

STRATEGIC POSITION &

PROFITABILITY

Focus on high-performing manmade fiber business with high profitable growth potential

and less cyclicality

Focus on high-end textile machines as demand for low-end products will shrink over time

due to objectives of the Chinese 5-Year-Plan

Focus on growing end markets as construction, automotive, home textiles, clothing,

geo / agro textiles and sports

EBIT-Margin of 14-16 % over the cycle

PRODUCT OFFERING &

MARKET SEGMENTS

Spinning plants and line equipment for

filaments, carpet yarn, staple fibers and

nonwovens and engineering services

OERLIKON’S STRENGTH

Market leader in manmade fiber industry

Solution provider (full range of products)

Strong R&D, playing to the strength of German Technology and precision engineering

Global footprint with strategic production sites in Asia and Europe

Technological leadership and know how to leverage in new applications and markets

Page 6

5%

6% 2% 12%

4%

71%

CHF 893m*

Nonwoven

Staple Fiber

Carpet Yarn (BCF)

Plastic Processing (BSZ)

Industrial Filament

Textile Filaments

* 2011 figures

Process equip.

January 2013_Investor Presentation

Line equip.

save space

Oerlikon Portfolio – Drive Systems Segment Overview

STRATEGIC POSITION &

PROFITABILITY

Focus on high growth segments of energy and on/off highway market while maintaining a

strong presence in other served areas

Niche applications with limited exposure to more commoditized gear component market

Focus on difficult-to-produce, high performance products in high-end applications

Adjustment of global production network (streamline in I and expansion in IN and CN)

Access to local markets in China and India

EBIT-Margin of 10 % as initial milestone, targeting for current Group average

PRODUCT OFFERING &

MARKET SEGMENTS

OERLIKON’S STRENGTH

Solution provider of true drive systems (joint development and engineering)

Most comprehensive support to customers in terms of product range, solutions and

geographical coverage

Highly advanced engineering and application expertise in gear and power transmission

Global footprint and network as increased technology demands will threaten smaller

independent firms

Potential to further expand in Emerging Marktes and new applications

Page 7

15%

8%

40%

20%

17%

Energy/Mining/Specialty Industrial

High-end Automotive

Agriculture

Construction

Off-Highway / Transportation

Gear components Clutches

Axles Transmissions

CHF 821m*

* 2011 figures

January 2013_Investor Presentation

save space

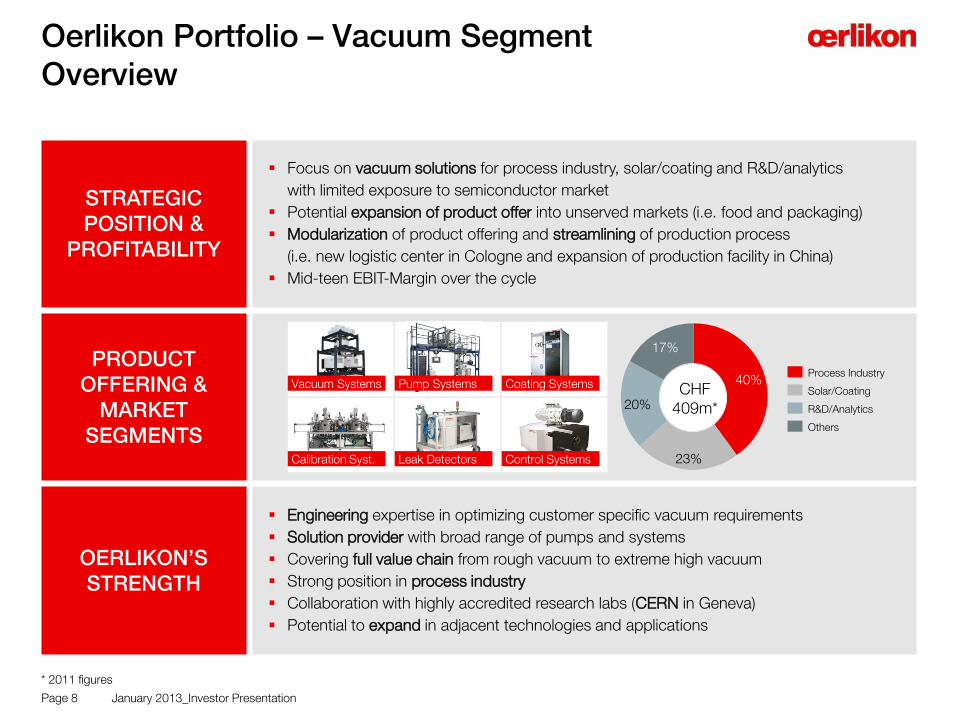

STRATEGIC POSITION &

PROFITABILITY

Focus on vacuum solutions for process industry, solar/coating and R&D/analytics

with limited exposure to semiconductor market

Potential expansion of product offer into unserved markets (i.e. food and packaging)

Modularization of product offering and streamlining of production process

(i.e. new logistic center in Cologne and expansion of production facility in China)

Mid-teen EBIT-Margin over the cycle

PRODUCT OFFERING &

MARKET SEGMENTS

OERLIKON’S STRENGTH

Engineering expertise in optimizing customer specific vacuum requirements

Solution provider with broad range of pumps and systems

Covering full value chain from rough vacuum to extreme high vacuum

Strong position in process industry

Collaboration with highly accredited research labs (CERN in Geneva)

Potential to expand in adjacent technologies and applications

Oerlikon Portfolio – Vacuum Segment Overview

Page 8

20%

23%

40%

17%

R&D/Analytics

Solar/Coating

Process Industry

Others

CHF 409m*

Vacuum Systems Pump Systems Coating Systems

Calibration Syst. Leak Detectors Control Systems

* 2011 figures

January 2013_Investor Presentation

save space

Oerlikon Portfolio – Coating Segment Overview

STRATEGIC POSITION &

PROFITABILITY

Undisputed technology and market leader in Physical Vapor Deposition (PVD)

Continues expansion of Components business

Automotive industry represents around 40 % (direct and indirect). Coating to benefit

from efforts to further reduce weight and fuel consumption (structural growth)

Extension of product offer to new coatings and services

Sustainable profitability level with EBIT-Margin of around 20 %

PRODUCT OFFERING &

MARKET SEGMENTS

OERLIKON’S STRENGTH

Market leader in PVD coating

Global presence with ~90 coating centers worldwide

Organic growth by implementing 3-5 new coating centers every year

Coating systems to be implemented in the client’s production process

Potential to expand in adjacent technologies and applications

Page 9

9%

20%

51%

8%

12%

Forming Tools

Cutting Tools

Precision Components

Automotive Components

Equipment

CHF 484m*

ePD interior PVD/PECVD

Equipment

* 2011 figures

ePD exterior

January 2013_Investor Presentation

save space

Oerlikon Portfolio – Advanced Technologies Overview

STRATEGIC POSITION &

PROFITABILITY

Focus on high growth and high value added applications in cleantech, semiconductors

and mobile device markets

Incubator for new technologies and applications predominantly in deposition technology

EBIT-Margin mid-term in the range of 10 %

PRODUCT OFFERING &

MARKET SEGMENTS

OERLIKON’S STRENGTH

Core competence in industrializing thin film coating applications for Advanced Packaging,

and Energy Management

Highest productivity PVD tools for semi, mobile and clean tech applications

Excellent reputation confirmed by independent market surveys

Strong customer base in Asia

R&D capabilities – Incubator function

Page 10

77%

3%

18%

2%

Photovoltaic

Others

Touch Panel

Semi

CHF 108m*

Thin-film Deposit.

Thin-film Coating

* 2011 figures

January 2013_Investor Presentation

save space

3 pillars as basis for Oerlikon’s Transformation

PORTFOLIO REFINANCING OPERATIONAL EXCELLENCE

OERLIKON’S TRANSFORMATION

Page 11 January 2013_Investor Presentation

save space

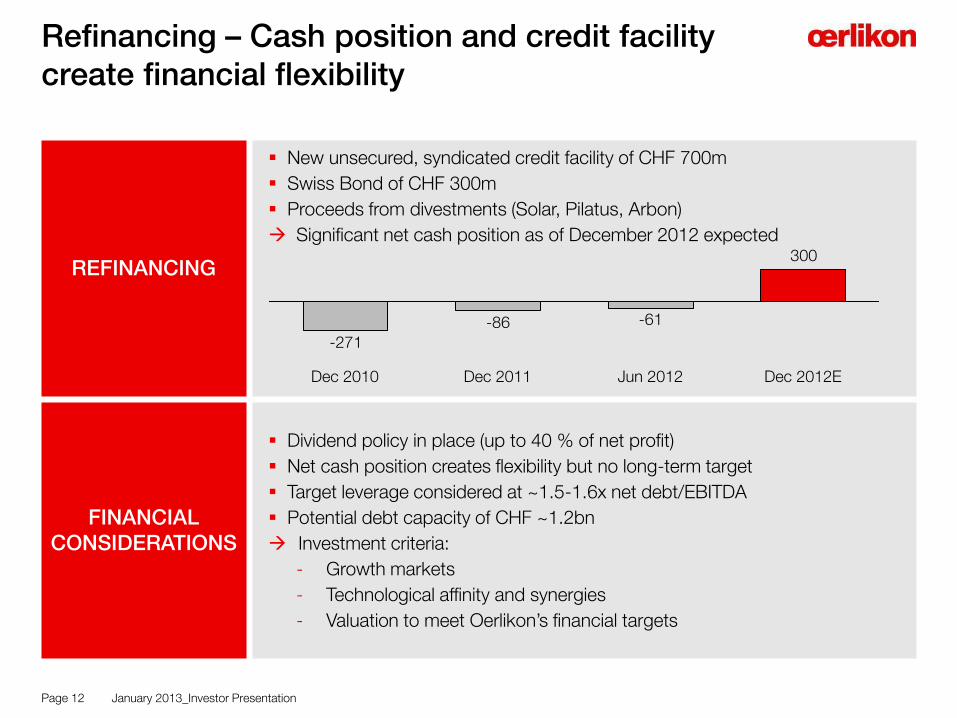

Refinancing – Cash position and credit facility create financial flexibility

REFINANCING

New unsecured, syndicated credit facility of CHF 700m

Swiss Bond of CHF 300m

Proceeds from divestments (Solar, Pilatus, Arbon)

Significant net cash position as of December 2012 expected

FINANCIAL CONSIDERATIONS

Dividend policy in place (up to 40 % of net profit)

Net cash position creates flexibility but no long-term target

Target leverage considered at ~1.5-1.6x net debt/EBITDA

Potential debt capacity of CHF ~1.2bn

Investment criteria:

- Growth markets

- Technological affinity and synergies

- Valuation to meet Oerlikon’s financial targets

Page 12

300

-61-86-271

Dec 2012E Jun 2012 Dec 2011 Dec 2010

January 2013_Investor Presentation

save space

3 pillars as basis for Oerlikon’s Transformation

PORTFOLIO REFINANCING OPERATIONAL EXCELLENCE

OERLIKON’S TRANSFORMATION

Page 13 January 2013_Investor Presentation

save space

Operational Excellence – Basis for improvement of underlying performance

MANAGEMENT

Changes in management to acquire and ensure necessary know how and

capabilities for transformation process

New Segment CEOs in Textile, Vacuum and Drive Systems

Introduction of Country Representatives for China, India, Russia

and the Americas to identify growth potential across all Segments

OPERATIONAL EXCELLENCE

Significant improvement of On-Time Delivery (OTD)

Manufacturing footprint alignment

Production process improvement

Cross Segment procurement

Platform strategies (i.e. in Textile and Vacuum)

Sustained Innovation is crucial to meet and exceed customer expectation

Continued invest in R&D to deliver groundbreaking innovations

Innovations to decrease operating costs, increase production efficiency,

reduce environmental impact and increase performance

GROWTH

Portfolio shaping to accelerate growth

Continued CapEx in the magnitude of depreciation level

Addressing growth regions in emerging markets

Expansion in growth applications and technologies

Page 14 January 2013_Investor Presentation

save space

Outlook Oerlikon Group 2012

Natural Fibers and Textile Components Business Units reported as «discontinued operations»

Based on the current assessment of the effects from Natural Fibers and Textile Components Business Units reported as discontinued, we updated our guidance:

- sales growth of more than 5 % (prior: to be at 2011 levels)

- order intake to be close to previous year’s level (prior: up to minus 5 %)

- EBIT margin to increase by 1 percentage point on prior guidance (prior: around 12.5 % reported)

Guidance FY 2012 based on current currency exchange rates

Financial flexibility to further capture organic and inorganic growth opportunities as well as continued focus on Operational Excellence to further increase value creation of Oerlikon

Page 15 January 2013_Investor Presentation

save space

Question and Answers

Page 16 January 2013_Investor Presentation

save space

Oerlikon divests Natural Fibers and Textile Components Business Units – Summary

Page 17

TRANSACTION

Oerlikon to divest Natural Fibers and Textile Components Business Units

(including certain real estate) to Jinsheng Group of China

Enterprise Value of around CHF 650 million

Subject to merger control approval in a number of countries

Closing expected for Q3 2013

RATIONALE

Manmade and natural fiber markets different in terms of industry dynamics,

technologies, customers and regions – limited overlap and synergies incl.

manufacturing footprint

Focus on manmade fibers – fastest growing area in the global fiber industry

Reduces complexity / cyclicality and overall textile exposure of Group portfolio

Focus on technological leadership and value creation of Oerlikon Group

TRANSFORMATION PROCESS 2012

Disciplined execution of Operational Excellence

Disposal of non-operating assets (Pilatus Flugzeugwerke AG, Arbon property)

Divestment of Solar Segment and announced reduction of textile exposure

Repositioning of Balance Sheet (net cash positive, unsecured CHF 700m

credit facility and CHF 300m Swiss Bond)

January 2013_Investor Presentation

save space

Group Sales Group Order Intake Group EBIT

20

11

excl. S

ola

r

FY 2011 Group EBIT Margin excluding Solar Segment at 11.1 %

20

11

p

relim

inary

resta

ted

Divestment will be accretive on restated FY 2011 EBIT margin by 50 to 60 bps dependent on cost allocation and deconsolidation impacts

Oerlikon Portfolio – Segment split more balanced

53%

21%

13%

11% 3%

CHF 3.9 bn 53%

24%

11%

11% 2%

CHF 3.8 bn

33%

30%

18%

15% 4%

CHF 2.7 bn

36%

32%

15%

14% 3%

CHF 2.9 bn

Textile Drive Systems Coating Vacuum Advanced Technologies

Page 18 January 2013_Investor Presentation

save space

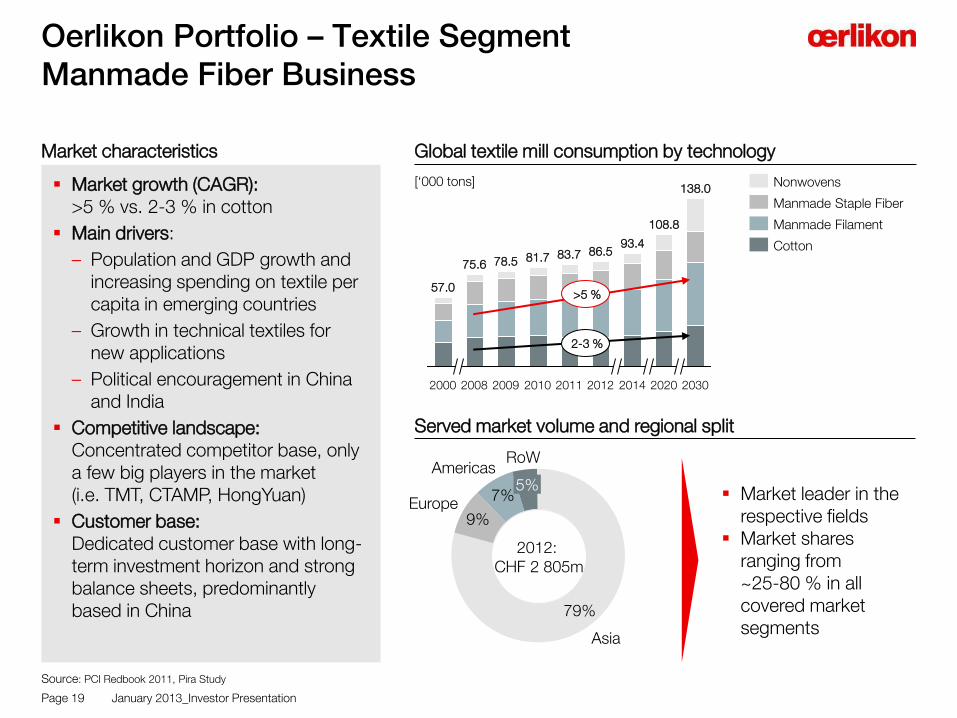

Market growth (CAGR): >5 % vs. 2-3 % in cotton

Main drivers:

– Population and GDP growth and increasing spending on textile per capita in emerging countries

– Growth in technical textiles for new applications

– Political encouragement in China and India

Competitive landscape: Concentrated competitor base, only a few big players in the market (i.e. TMT, CTAMP, HongYuan)

Customer base: Dedicated customer base with long-term investment horizon and strong balance sheets, predominantly based in China

Oerlikon Portfolio – Textile Segment Manmade Fiber Business

2030

138.0

2020

108.8

2014

93.4

2012

86.5

2011

83.7

2010

81.7

2009

78.5

2008

75.6

2000

57.0

[‘000 tons]

Global textile mill consumption by technology

Cotton

Manmade Filament

Manmade Staple Fiber

Nonwovens

Market characteristics

Served market volume and regional split

Source: PCI Redbook 2011, Pira Study

>5 %

2-3 %

Page 19

7%

9%

RoW

5% Americas

Europe

Asia

79%

2012: CHF 2 805m

Market leader in the respective fields

Market shares ranging from ~25-80 % in all covered market segments

January 2013_Investor Presentation

save space

Oerlikon Portfolio – Drive Systems Segment Agriculture and Construction as drivers

Construction & Agricultural Equipment Market 2008-2014E* Market characteristics

Served market volume and regional split

Page 20

Source: IHS Global Insight, CNH, BaB estimates

Market growth (CAGR): GDP correlated

Main drivers:

– Population growth, rising middle class and increased mobility

– Migration towards higher technology/systems in agriculture in emerging markets

– Construction and infrastructure build-up in developing countries

Competitive landscape: Many competitors worldwide competing in the niche gear and drives market. Competitors include both global players as well as smaller regional producers

Customer base: Concentrated customer base of global OEMs and producers (CNH, John Deere, Caterpillar)

Americas 40%

Europe

25%

Asia 35%

2012: CHF 9 200m

Drive Systems Segment No. 2 or 3 in addressable markets

Market shares ranging from ~5-15 % in all covered market segments

2012 2014E

2 000

2013E

1 900 2 000

2011

1 900

2010

1 600

2009

1 600

2008

1 700

Tractors Light Equipment Heavy Equipment Combines

[‘000 units]

January 2013_Investor Presentation

save space

Oerlikon Portfolio – Vacuum Segment Process industry and China

Cyclicality and growth in the vacuum business Market characteristics

Served market volume and regional split

Page 21

Americas

21%

Europe 25%

Asia 54% 2012:

CHF 3 450m

Oerlikon Leybold No. 3 in addressable markets

Market shares ranging from ~10-15 % in all covered market segments

Market growth (CAGR): GDP correlated

Main drivers:

– Aging population with growing demand for health care and pharma

– Demographics and middle class development driving process industry growth

– Construction and infrastructure with coating of glass and solar panels

Competitive landscape: Big global competitors (Edwards, Pfeiffer, Busch) as well as regional competitors

Customer base: Reliable partner for more than 18 000 customers

CAGR

Cyclicity

Chemical F&P / PP

SEMI

Coating

Solar

R&D

Analytics Process Industry

Stable Highly cyclical

Oerlikon involved

January 2013_Investor Presentation

save space

Oerlikon Portfolio – Coating Segment Automotive and Components Business

Oerlikon’s global network Market characteristics

Served market volume and regional split

Page 22

* Source: OICA 2012

Americas

21%

Europe

41%

Asia 38%

2012: CHF 1 400m

Market leader in the respective fields

Market shares ranging from ~25-45 % in all covered market segments

Market growth (CAGR): ~7-8 % organic growth (incl. build-up of new coating centers)

Main drivers:

– High increase in automotive sales in emerging markets

– Usage of adv. surface solutions in various sub-segments for functional and decorative enhancements (watches, medical, aerospace etc.)

– Substitution of chrome-plating technology on automotive

Competitive landscape: Undisputed market and technology leader

Customer base: Broad customer base worldwide

Americas: 21 Centres

Asia: 30 Centres

Europe: 38 Centres

January 2013_Investor Presentation

Consistent high level of profitability in Q3 2012 Group EBIT margin at 11.6 %

With an EBIT margin of 11.6 %, Oerlikon operates on a continued high level

Strong margin improvements in the Textile and Drive Systems Segment

Positive currency impact

Growth in Europe +13 % and Asia +9% (whereof China +12 %)

Execution of Operational Excellence programs and portfolio adjustments

Consistent high level of profitability

in 2012

Page 23

Oerlikon net cash positive after strong operational and financial performance

and based on completion of comprehensive refinancing in July 2012

Order intake Sales*

837 +7%

Q3 2012 cont. op.

898

Q3 2011 restated

939 +2%

Q3 2012 cont. op.

957

Q3 2011 restated

EBIT

123 -10%

Q3 2012 cont. op.

111

Q3 2011 restated

Order backlog

1,485

-16%

Q3 2012 cont. op.

1,240

Q3 2011 restated

EBIT margin

13.1

-1.5% pts.

Q3 2012 cont. op.

11.6

Q3 2011 restated

* Sales to third parties

in CHF million in CHF million in CHF million in CHF million in %

January 2013_Investor Presentation

Key figures by Segment Q3 2012

Order intake Δ to Q3 2011

Order backlog Δ to Q3 2011

Sales* Δ to Q3 2011

EBIT % of sales

in CHF m Vacuum

93 +9.4 %

74 -1.3 %

92 -8.9 %

8 8.3 %

Page 24

Textile

486 +17.1 %

970 -20.0 %

524 +3.6 %

57 10.9 %

Coating

126 +5.0 %

n/a

126 +5.0 %

25 20.0 %

Adv.Tech.

28 +40.0 %

33 +50.0 %

20 -13.0 %

-1 n.a.

Drive

165 -16.2 %

163 -7.4 %

195 +3.2 %

18 9.3 %

Group**

898 +7.3 %

1 240 -16.5 %

957 +1.9 %

111 11.6 %

** restated

* Sales to third parties

January 2013_Investor Presentation

FX impact on Sales, EBIT and EBIT margin

+68+2

+887

+8%

Q3 2012 reported

+957

Translation effects

Transaction effect

Q3 2012 FX impact adj.

+10+4

+97

+14%

Q3 2012 reported

+111

Translation Effects

Transaction Effects

Q3 2012 FX impact adj.

11.6 10.9

Currency impact driven by strong development of USD and CNY

EBIT margin disproportionate affected due to currency mix in global network

EBIT margin in %

Page 25

* Sales to third parties

in CHF m

Oerlikon Group Sales* Q3 2012

in CHF m

Oerlikon Group EBIT Q3 2012

January 2013_Investor Presentation

Return On Capital Employed (ROCE) ROCE = NOPAT / Capital Employed

17.3%17.5%17.6%

Q3 2012 continuing operations

Q2 2012 continuing operations

Q1 2012 continuing operations

FY 2011 restated

16.5%

FY 2011 reported

14.9%

Page 26

in %

ROCE

9M 2012: improvement in 12-month rolling NOPAT and disproportionate increase in Capital Employed

Oerlikon Group creates value by earning premium over cost of capital

January 2013_Investor Presentation

Successful closing of Solar divestment will allow to further reduce debt (drawing of Facility A)

Oerlikon net cash positive by end of Q3 2012

483 486

345

196

-56%

Others

Bond

Facility C (old)

Facility B (old)

Facility A (new)

9M 2012

368

4

298*

66*

HY 2012

687

5

FY 2011

832

4

Page 27

Development of debt position FY 2011 – 9M 2012

* Including capitalized financing costs (Bond CHF 2 million, Facility A CHF 14 million)

January 2013_Investor Presentation

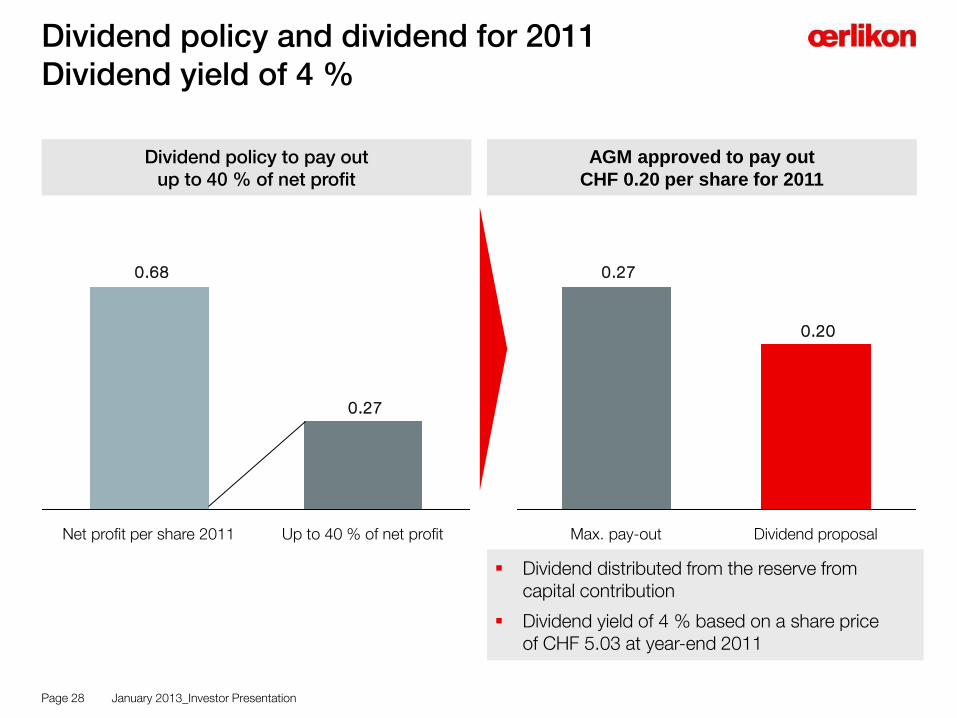

Dividend policy and dividend for 2011 Dividend yield of 4 %

0.27

0.68

Up to 40 % of net profit Net profit per share 2011

0.20

0.27

Max. pay-out Dividend proposal

Dividend distributed from the reserve from capital contribution

Dividend yield of 4 % based on a share price of CHF 5.03 at year-end 2011

Page 28

Dividend policy to pay out up to 40 % of net profit

AGM approved to pay out

CHF 0.20 per share for 2011

January 2013_Investor Presentation

Oerlikon Shares

Listed on Swiss Exchange (SIX) since 1975

Securities symbol: OERL

Securities number 81 682

ISIN: CH0000816824

No. of shares outstanding: 325 547 970 shares*

Re-entry to Swiss SMIM on April 17, 2012

Addition to STOXX Europe 600 as of June 18, 2012

48,86% Free Float 51,14%

Treasury Shares (part of Free Float)

0,15%

Renova Group

Page 29

* as of September 30, 2012

(as of June 14, 2012)

Oerlikon Shares Oerlikon Shareholder Structure

(as of December 31, 2012, Indexed; 100 percent = Closing price per December 31, 2011

Oerlikon Share Price Development

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

220.0

30.1

2.1

1

06.0

1.1

2

13.0

1.1

2

20.0

1.1

2

27.0

1.1

2

03.0

2.1

2

10.0

2.1

2

17.0

2.1

2

24.0

2.1

2

02.0

3.1

2

09.0

3.1

2

16.0

3.1

2

23.0

3.1

2

30.0

3.1

2

06.0

4.1

2

13.0

4.1

2

20.0

4.1

2

27.0

4.1

2

04.0

5.1

2

11.0

5.1

2

18.0

5.1

2

25.0

5.1

2

01.0

6.1

2

08.0

6.1

2

15.0

6.1

2

22.0

6.1

2

29.0

6.1

2

06.0

7.1

2

13.0

7.1

2

20.0

7.1

2

27.0

7.1

2

03.0

8.1

2

10.0

8.1

2

17.0

8.1

2

24.0

8.1

2

31.0

8.1

2

07.0

9.1

2

14.0

9.1

2

21.0

9.1

2

28.0

9.1

2

05.1

0.1

2

12.1

0.1

2

19.1

0.1

2

26.1

0.1

2

02.1

1.1

2

09.1

1.1

2

16.1

1.1

2

23.1

1.1

2

30.1

1.1

2

07.1

2.1

2

14.1

2.1

2

21.1

2.1

2

28.1

2.1

2

OC OERLIKON CORP SWISS MARKET INDEX SMIM PRICE INDEX STXE 600 € Pr

January 2013_Investor Presentation

Coverage 8 Buy/Accumulate – 2 Hold/Neutral

Page 30

Broker (as of December 31, 2012)

Analyst Recommendation Date of last update

Target Price

AlphaValue Pierre-Yves Gauthier Buy 06.12.2012 12.50

Bank am Bellevue Michael Studer Hold 20.12.2012 10.50

Berenberg Bank Benjamin Glaeser Buy 03.12.2012 11.00

Credit Suisse Patrick Laager Outperform 10.01.2013 14.20

Helvea SA Reto Amstalden Accumulate 10.12.2012 11.20

Kepler CM Christoph Ladner Buy 04.12.2012 11.00

MainFirst Resumption of coverage planned for 2013

Société Générale Jean Baptiste Roussille Hold 04.12.2012 11.00

UBS Torsten Wyss Buy 05.12.2012 12.00

Vontobel Michael Foeth Buy 04.12.2012 12.50

Zürcher Kantonalbank Armin Rechberger Overweight 04.12.2012 -

Consensus 11.99

January 2013_Investor Presentation

save space

Investor Relations Contact

OC Oerlikon Management AG Churerstrasse 120 CH-8808 Pfäffikon SZ Switzerland Andreas Schwarzwälder Head of Investor Relations Phone: +41-58-360-9622 Mobile: +41-79-810-8211 E-mail: [email protected]

Page 31 January 2013_Investor Presentation

save space

Oerlikon has made great efforts to include accurate and up-to-date information in this document. However, we make no representation or warranties, expressed or implied, as to the accuracy or completeness of the information provided in this document and we disclaim any liability whatsoever for the use of it.

This presentation is based on information currently available to management. The forward-looking statements contained herein could be substantially impacted by risks and influences that are not foreseeable at present, so that actual results may vary materially from those anticipated, expected or projected. Oerlikon is under no obligation to (and expressly disclaims any obligation to) update or alter its forward-looking statements, whether as a result of new information, future events or otherwise.

All information provided in this document is not intended as, and may not be construed as, an offer or solicitation for the purchase or disposal, trading or any transaction in any Oerlikon securities. Investors must not rely on this information for investment decisions.

Disclaimer

December 2012_Investor Presentation Page 32