Embed Size (px)

Citation preview

TAXATION for COOPERATIVES

Presented by:

Ms. Yesa p. yap

Revenue officer

Rdo 113-west davao

1

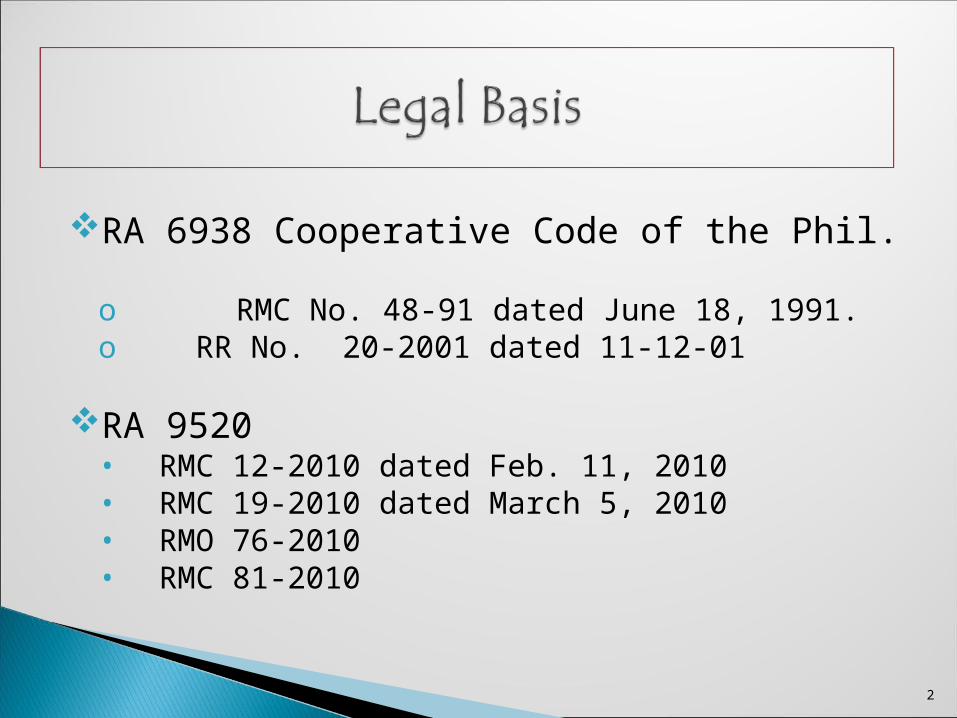

RA 6938 Cooperative Code of the Phil. o RMC No. 48-91 dated June 18, 1991. o RR No. 20-2001 dated 11-12-01

RA 9520• RMC 12-2010 dated Feb. 11, 2010• RMC 19-2010 dated March 5, 2010 • RMO 76-2010• RMC 81-2010

2

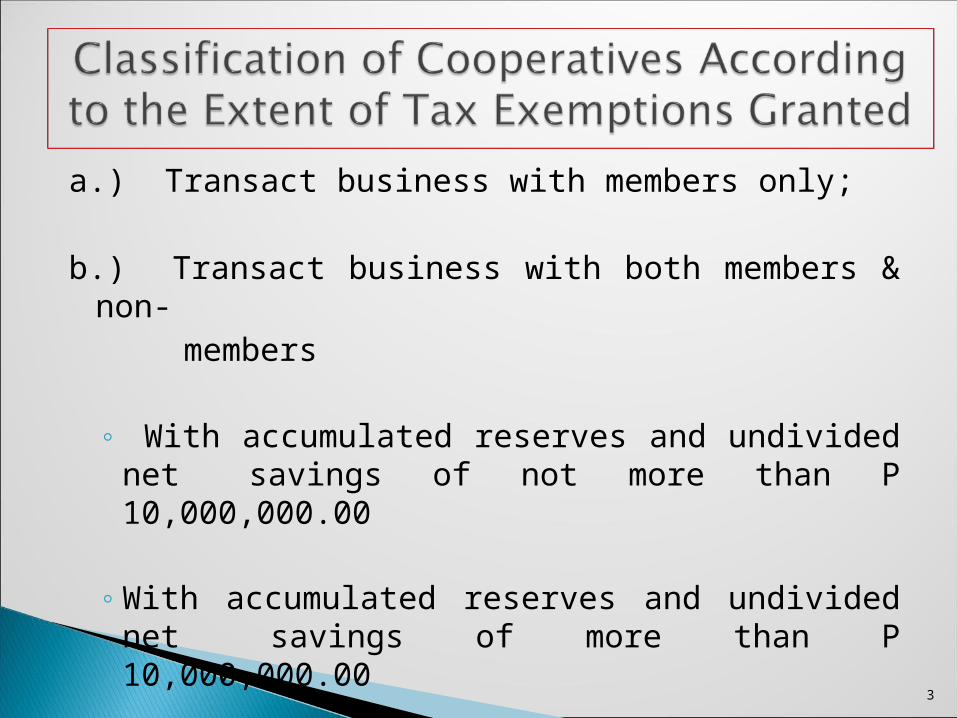

a.) Transact business with members only;

b.) Transact business with both members & non- members

◦ With accumulated reserves and undivided net savings of not more than P 10,000,000.00

◦ With accumulated reserves and undivided net savings of more than P 10,000,000.00

3

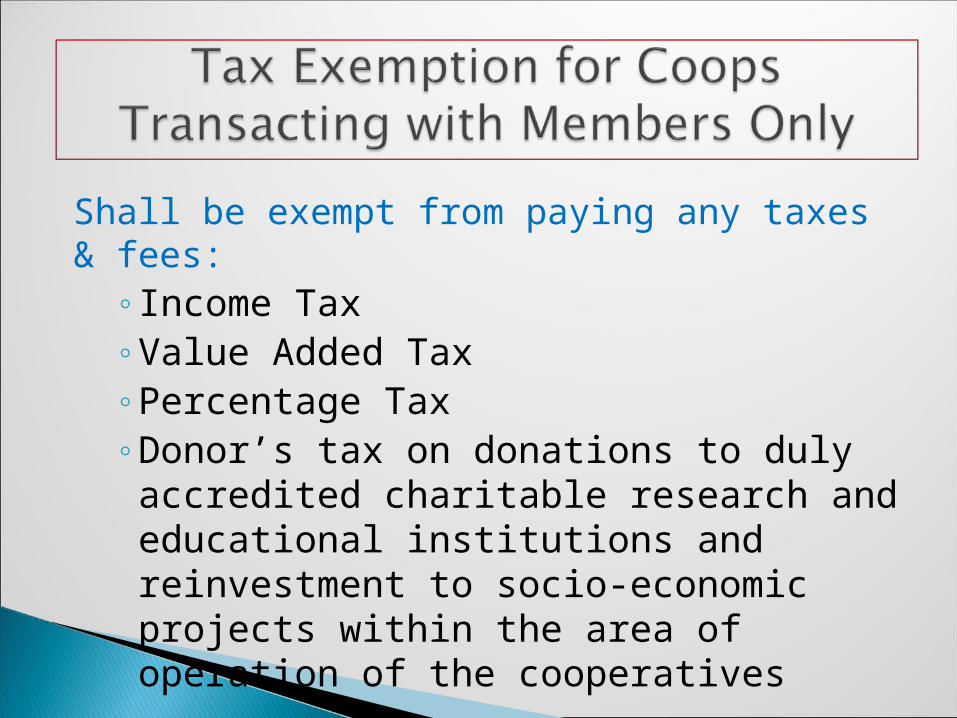

Shall be exempt from paying any taxes & fees:

◦Income Tax◦Value Added Tax◦Percentage Tax◦Donor’s tax on donations to duly

accredited charitable research and educational institutions and reinvestment to socio-economic projects within the area of operation of the cooperatives

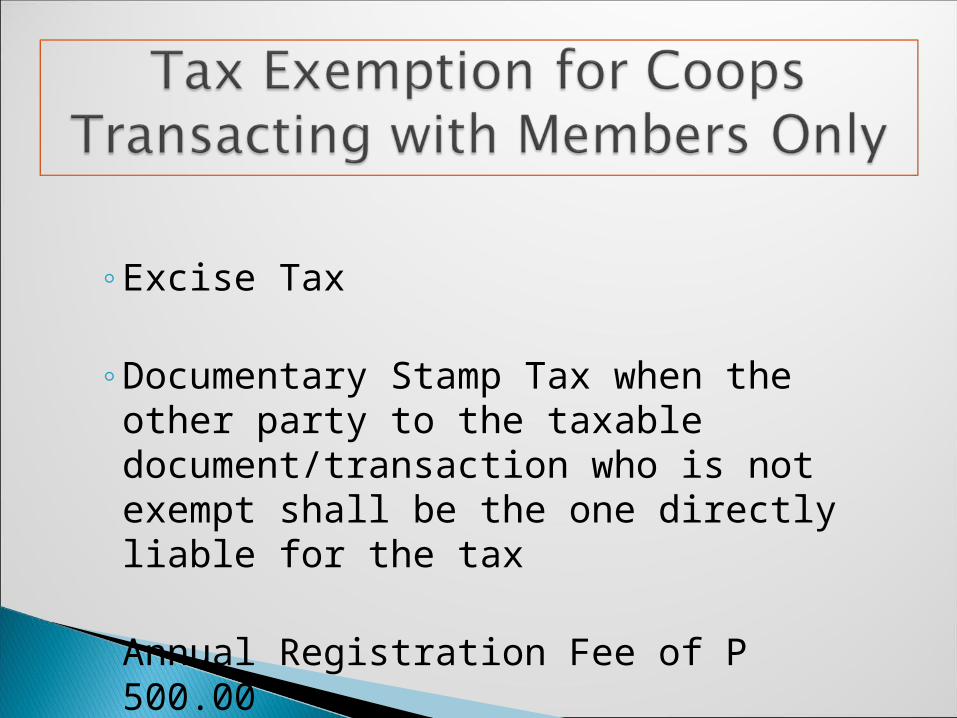

◦Excise Tax

◦Documentary Stamp Tax when the other party to the taxable document/transaction who is not exempt shall be the one directly liable for the tax

◦Annual Registration Fee of P 500.00

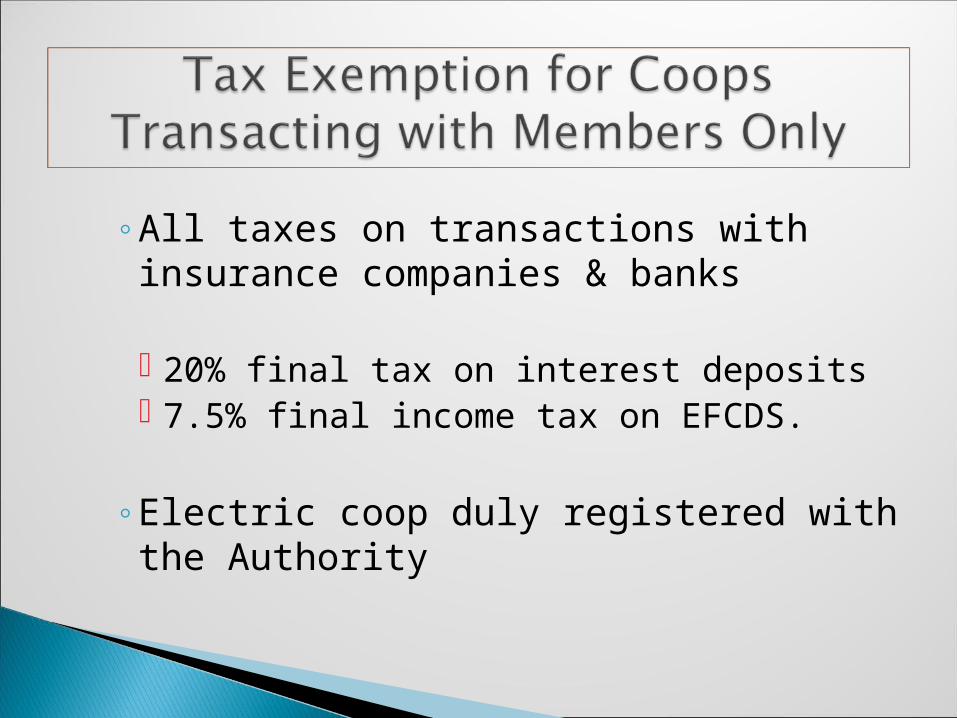

◦All taxes on transactions with insurance companies & banks

20% final tax on interest deposits 7.5% final income tax on EFCDS.

◦Electric coop duly registered with the Authority

Same exemption from all national internal revenue taxes for which these cooperatives are liable as enumerated under Sec. 7 of this Joint Rules & Regulations.

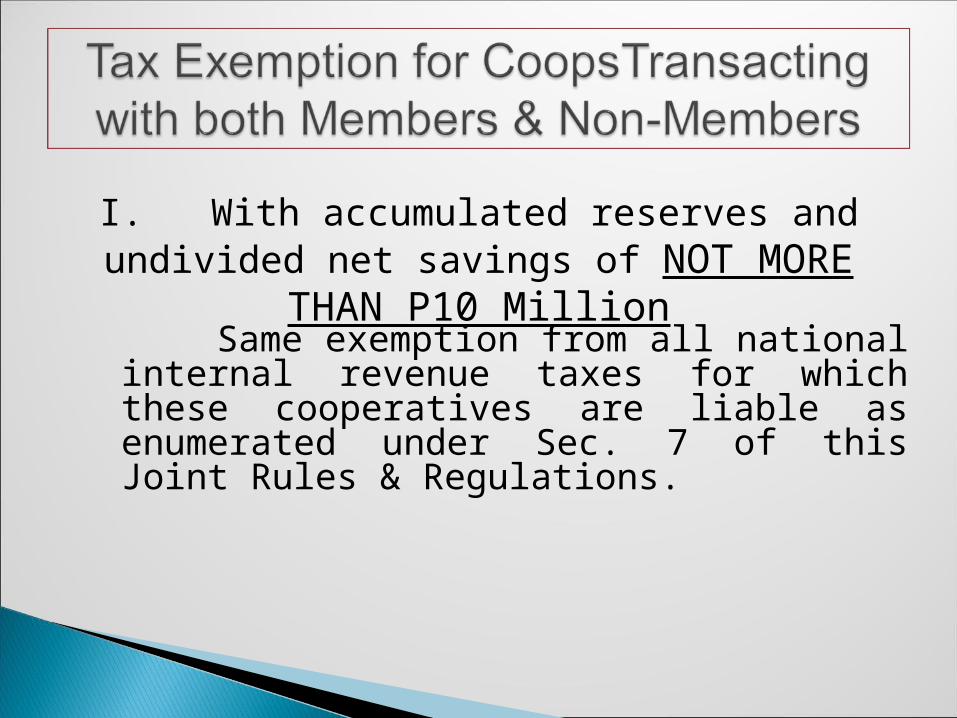

I. With accumulated reserves and undivided net savings of NOT MORE THAN P10 Million

Classified again into two:

1. Business transactions with members – exempt from all National Internal Revenue Taxes for which it is liable as enumerated in Sec. 7 of this Joint Rules & Regulations.

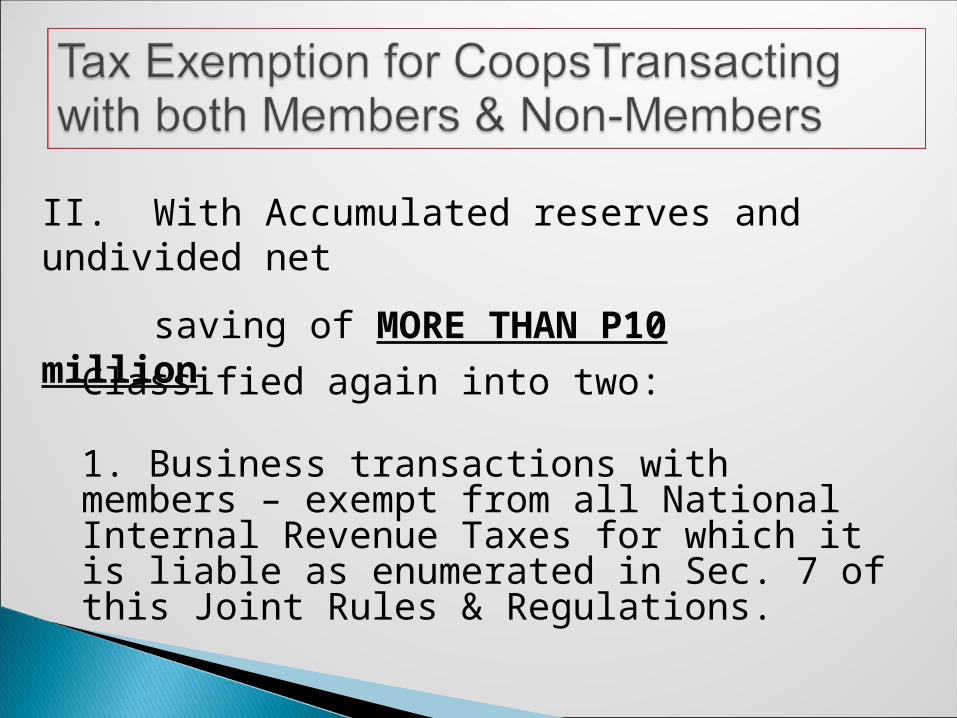

II. With Accumulated reserves and undivided net

saving of MORE THAN P10 million

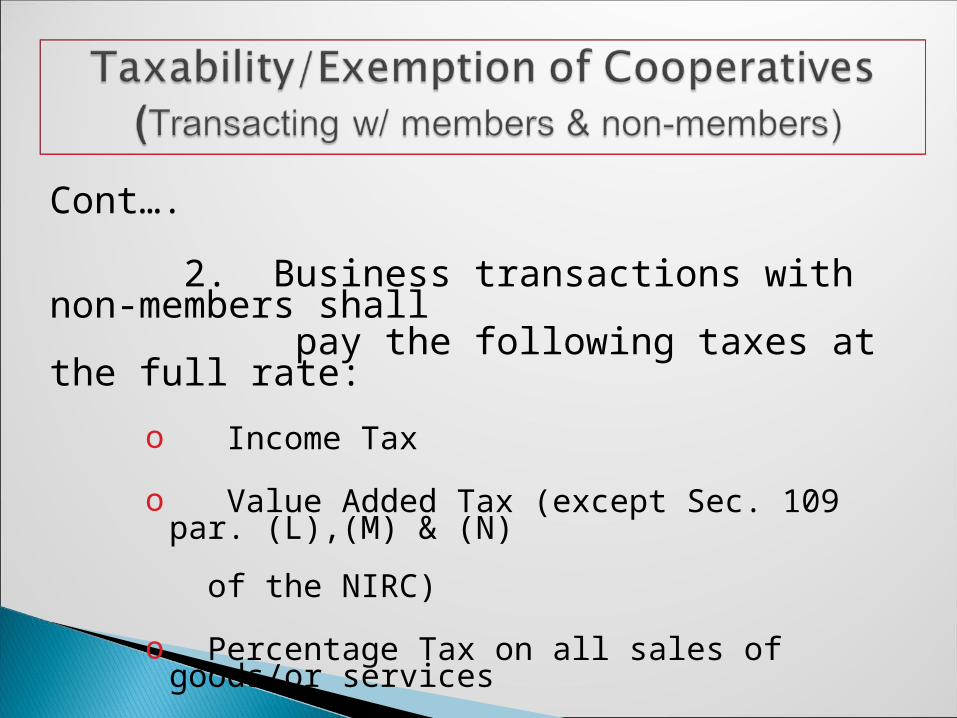

Cont…. 2. Business transactions with non-members shall pay the following taxes at the full rate:

o Income Tax

o Value Added Tax (except Sec. 109 par. (L),(M) & (N) of the NIRC)

o Percentage Tax on all sales of goods/or services

o All other internal revenue taxes unless otherwise provided by the law.

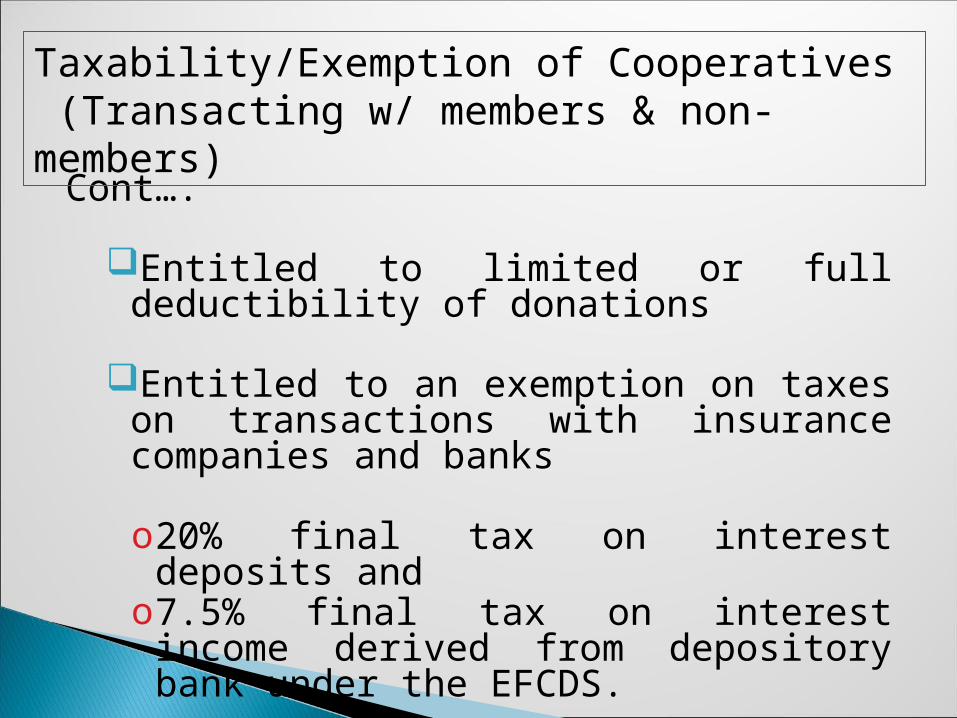

Cont….

Entitled to limited or full deductibility of donations

Entitled to an exemption on taxes on transactions with insurance companies and banks

o20% final tax on interest deposits and o7.5% final tax on interest income derived from

depository bank under the EFCDS.

Taxability/Exemption of Cooperatives (Transacting w/ members & non-members)

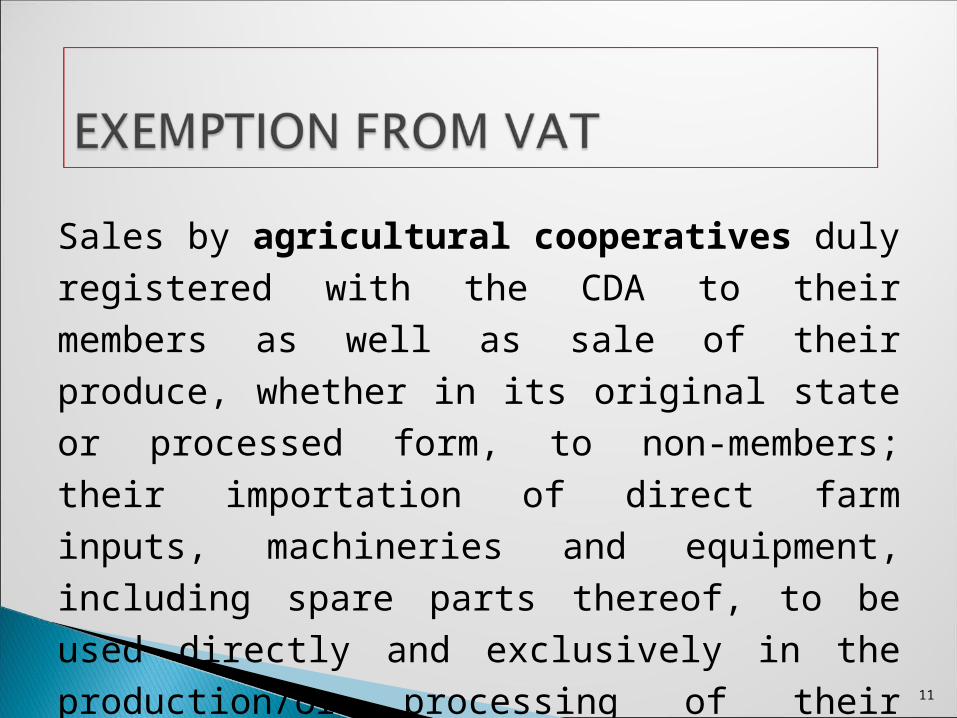

Sales by agricultural cooperatives duly registered with the CDA to their members as well as sale of their produce, whether in its original state or processed form, to non-members; their importation of direct farm inputs, machineries and equipment, including spare parts thereof, to be used directly and exclusively in the production/or processing of their produce. (Sec. 109 (L))

11

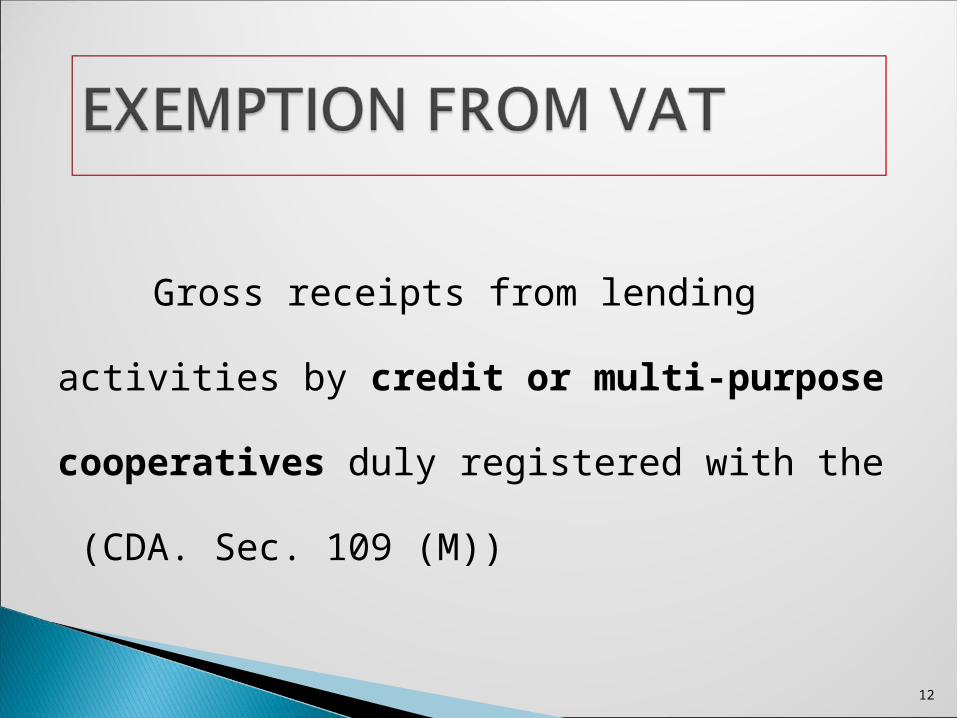

Gross receipts from lending activities

by credit or multi-purpose cooperatives

duly registered with the (CDA. Sec. 109 (M))

12

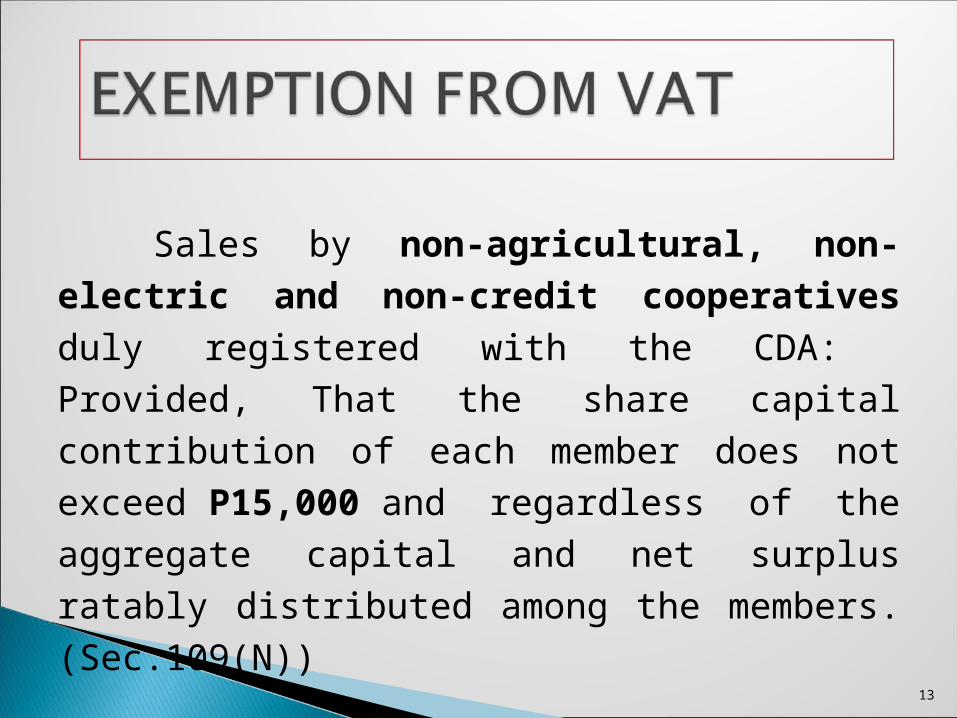

Sales by non-agricultural, non-electric and non-credit cooperatives duly registered with the CDA: Provided, That the share capital contribution of each member does not exceed P15,000 and regardless of the aggregate capital and net surplus ratably distributed among the members. (Sec.109(N))

13

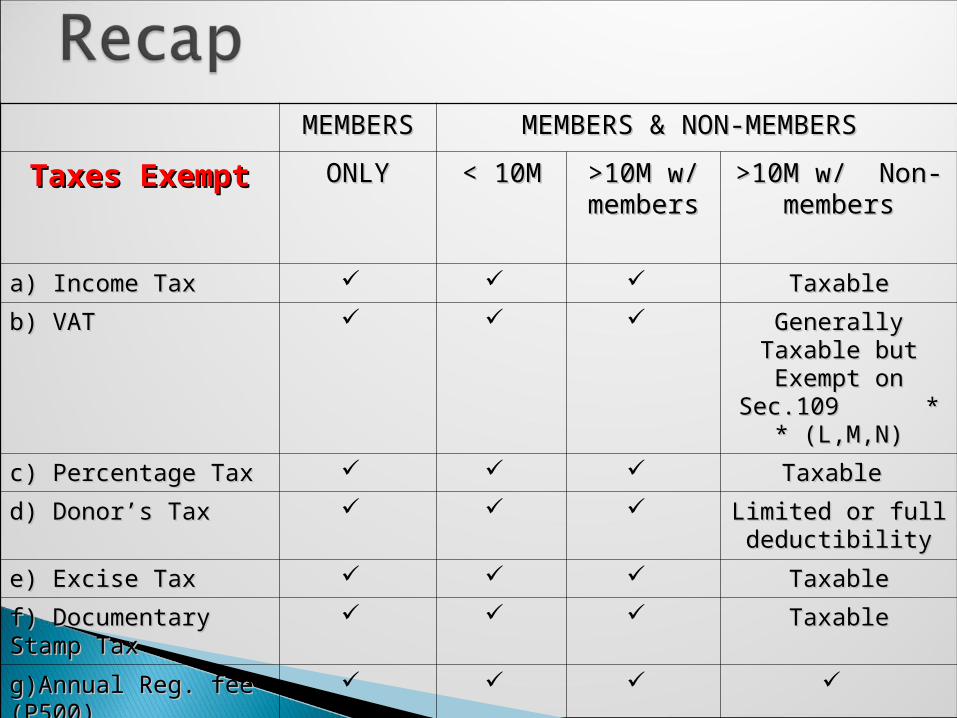

MEMBERSMEMBERS MEMBERS & NON-MEMBERS MEMBERS & NON-MEMBERS

Taxes ExemptTaxes Exempt ONLYONLY < 10M< 10M >10M w/ >10M w/ membersmembers

>10M w/ Non->10M w/ Non-membersmembers

a) Income Taxa) Income Tax TaxableTaxable

b) VAT b) VAT Generally Taxable but Generally Taxable but Exempt on Sec.109 * Exempt on Sec.109 *

* (L,M,N)* (L,M,N)

c) Percentage Taxc) Percentage Tax Taxable Taxable

d) Donor’s Taxd) Donor’s Tax Limited or full Limited or full deductibilitydeductibility

e) Excise Taxe) Excise Tax TaxableTaxable

f) Documentary Stamp Taxf) Documentary Stamp Tax TaxableTaxable

g)Annual Reg. fee (P500)g)Annual Reg. fee (P500)

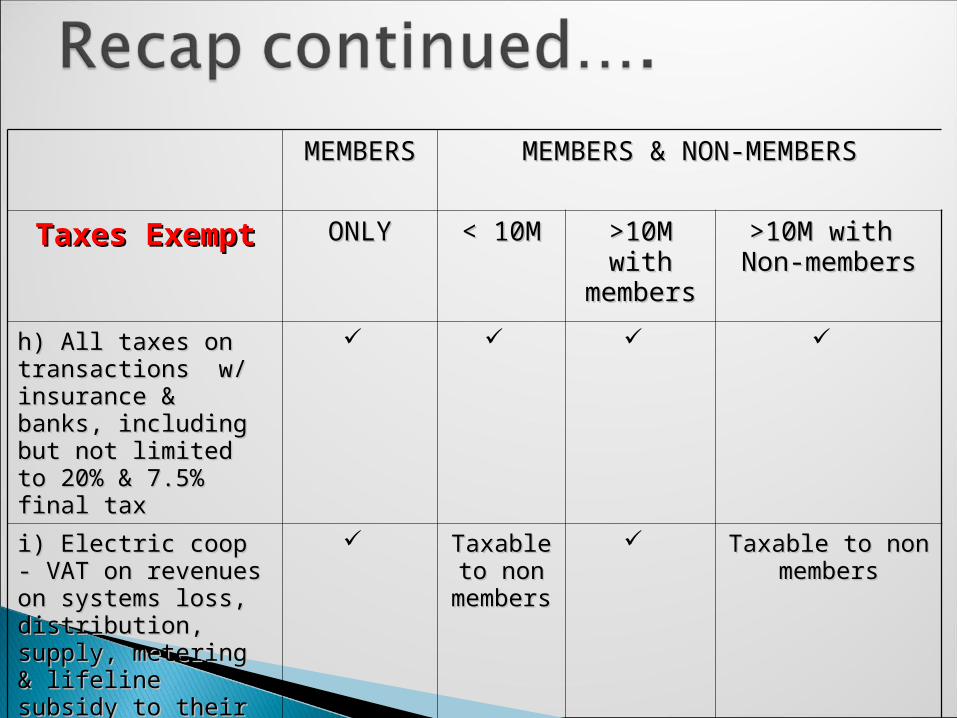

MEMBERMEMBERSS

MEMBERS & NON-MEMBERSMEMBERS & NON-MEMBERS

Taxes ExemptTaxes Exempt ONLYONLY < 10M< 10M >10M >10M with with

membersmembers

>10M with >10M with Non-membersNon-members

h) All taxes on h) All taxes on transactions w/ transactions w/ insurance & banks, insurance & banks, including but not including but not limited to 20% & limited to 20% & 7.5% final tax7.5% final tax

i) Electric coop - i) Electric coop - VAT on revenues on VAT on revenues on systems loss, systems loss, distribution, supply, distribution, supply, metering & lifeline metering & lifeline subsidy to their subsidy to their membersmembers

Taxable Taxable to non to non

membermemberss

Taxable to non Taxable to non membersmembers

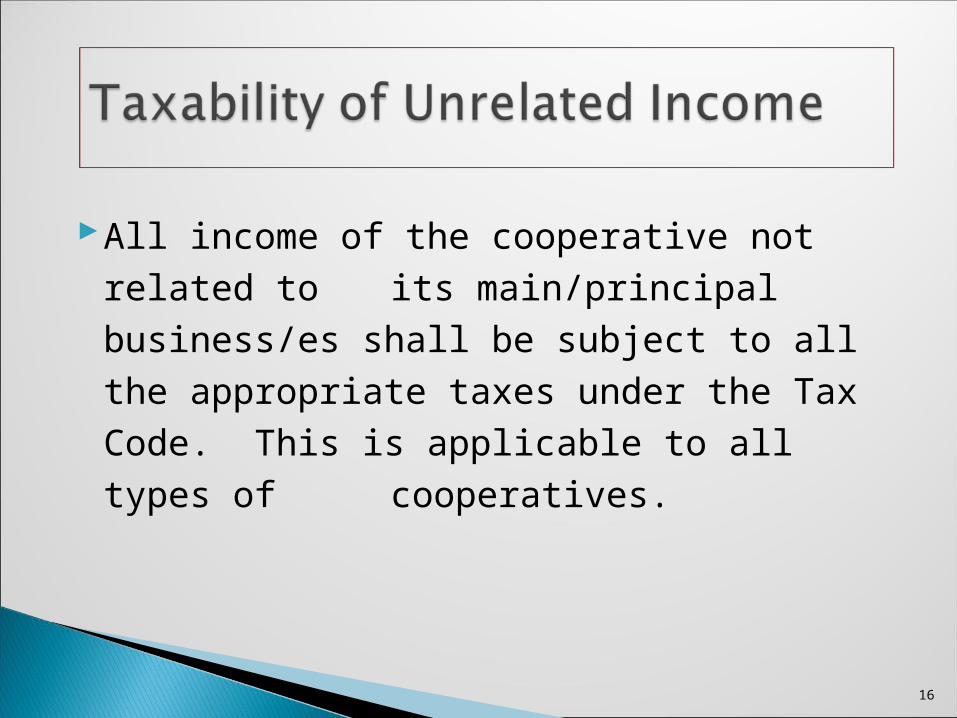

All income of the cooperative not related to its main/principal business/es shall be subject to all the appropriate taxes under the Tax Code. This is applicable to all types of cooperatives.

16

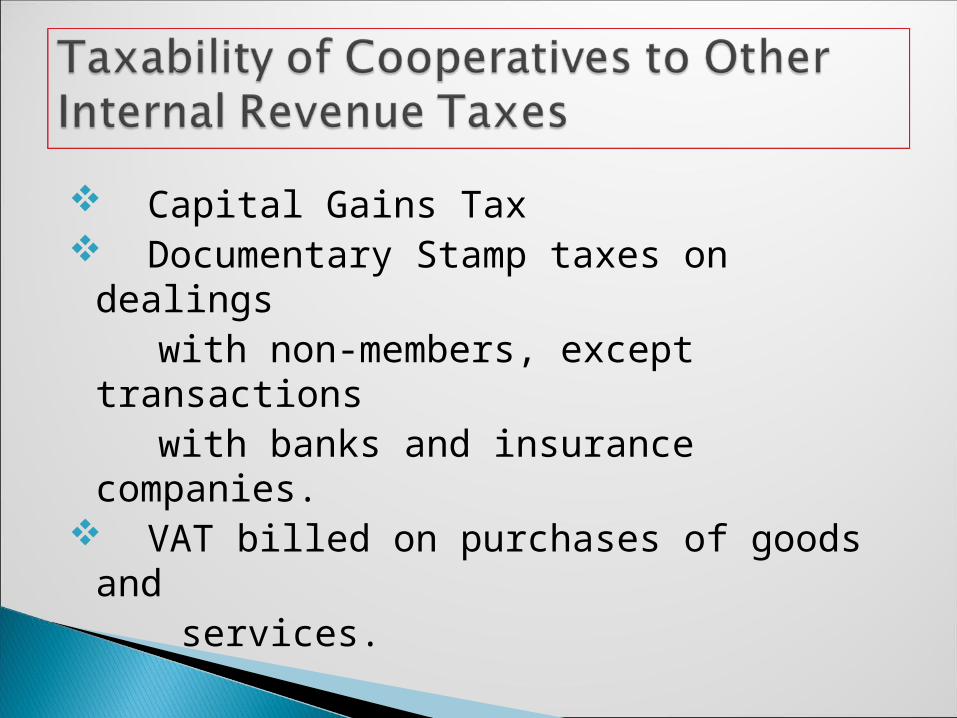

Capital Gains Tax Documentary Stamp taxes on dealings with non-members, except transactions with banks and insurance companies. VAT billed on purchases of goods and services.

Cont….

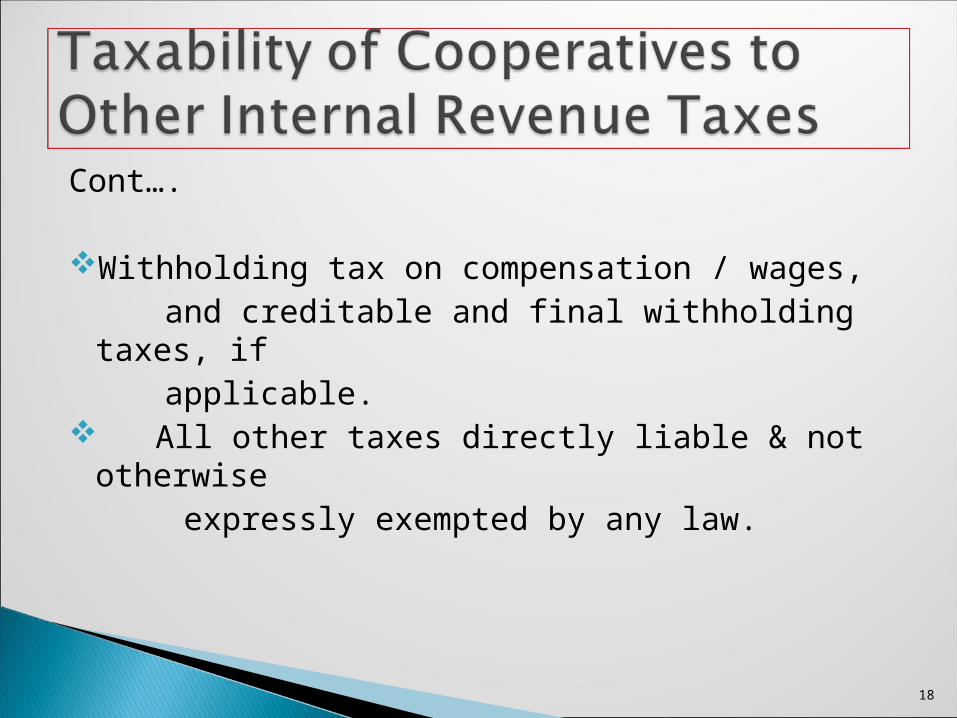

Withholding tax on compensation / wages, and creditable and final withholding taxes, if applicable. All other taxes directly liable & not otherwise

expressly exempted by any law.

18

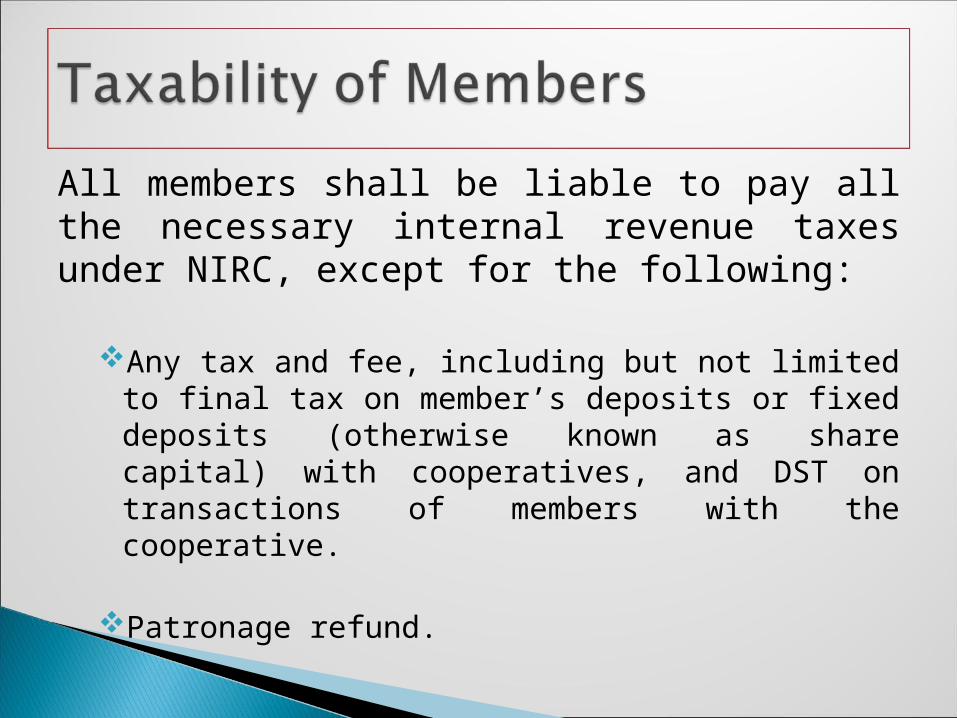

All members shall be liable to pay all the necessary internal revenue taxes under NIRC, except for the following:

Any tax and fee, including but not limited to final tax on member’s deposits or fixed deposits (otherwise known as share capital) with cooperatives, and DST on transactions of members with the cooperative.

Patronage refund.

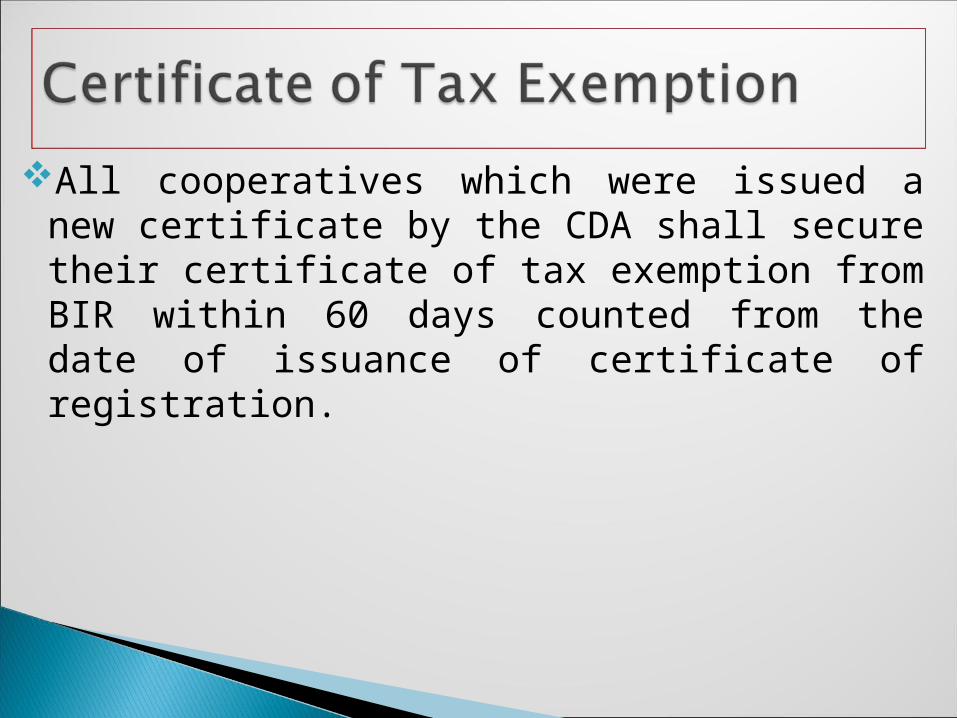

All cooperatives which were issued a new certificate by the CDA shall secure their certificate of tax exemption from BIR within 60 days counted from the date of issuance of certificate of registration.

Application for tax exemption of cooperatives whose Accumulated Reserves and Undivided Net Savings do not exceed 10M shall be acted upon within 45days upon submission of all the required documents.

21

Policies & Guidelines in the Issuance of Certificate of

Tax Exemption of Cooperatives and Monitoring thereof

(RMO 76-2010)

General Guidelines All cooperatives previously registered by

CDA under RA 6938 and 6939 are deemed registered under RA 9520 and a New Certificate of Registration shall be issued by CDA.

General Guidelines It is only after a cooperative has secured a

new certificate of registration that it becomes eligible to apply for a Certificate of Tax Exemption with the BIR.

General Guidelines

• All coops are mandated to update their registration information with the BIR with issuance of Certificate of Tax Exemption

The cooperative's application for Registration Update may be processed simultaneously with the cooperative's application for tax exemption.

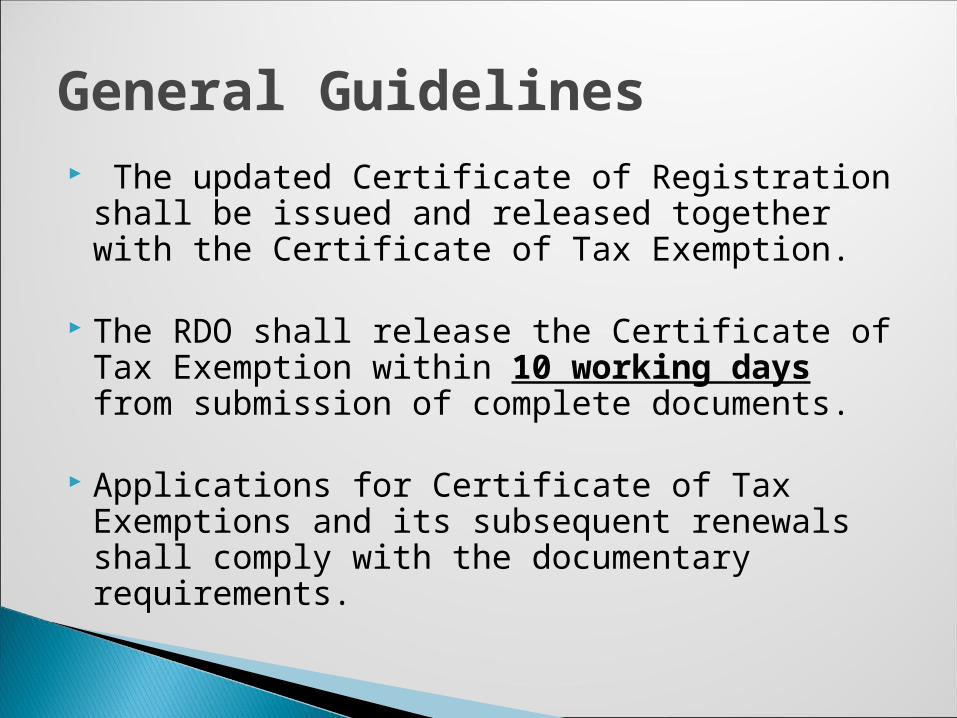

General Guidelines The updated Certificate of Registration shall

be issued and released together with the Certificate of Tax Exemption.

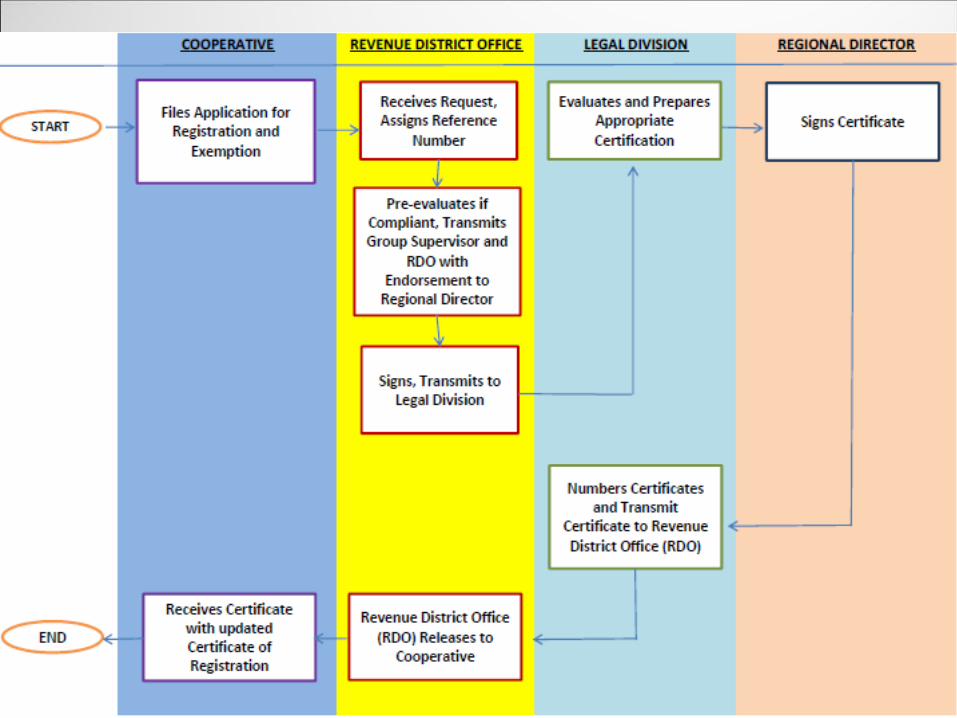

The RDO shall release the Certificate of Tax Exemption within 10 working days from submission of complete documents.

Applications for Certificate of Tax Exemptions and its subsequent renewals shall comply with the documentary requirements.

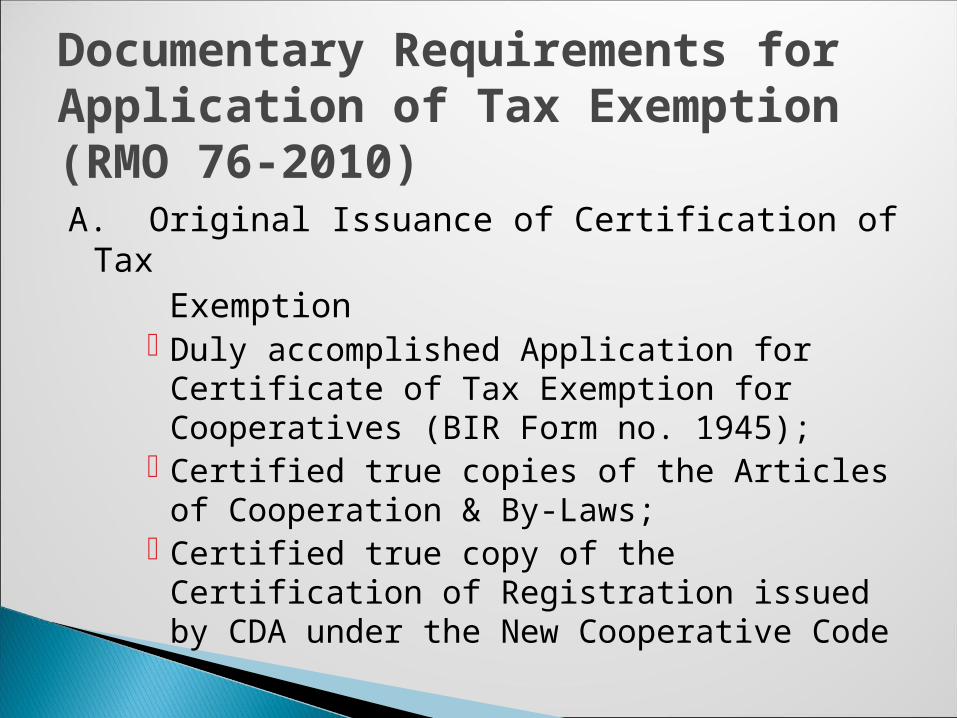

Documentary Requirements for Application of Tax Exemption(RMO 76-2010)A. Original Issuance of Certification of Tax Exemption

Duly accomplished Application for Certificate of Tax Exemption for Cooperatives (BIR Form no. 1945);

Certified true copies of the Articles of Cooperation & By-Laws;

Certified true copy of the Certification of Registration issued by CDA under the New Cooperative Code

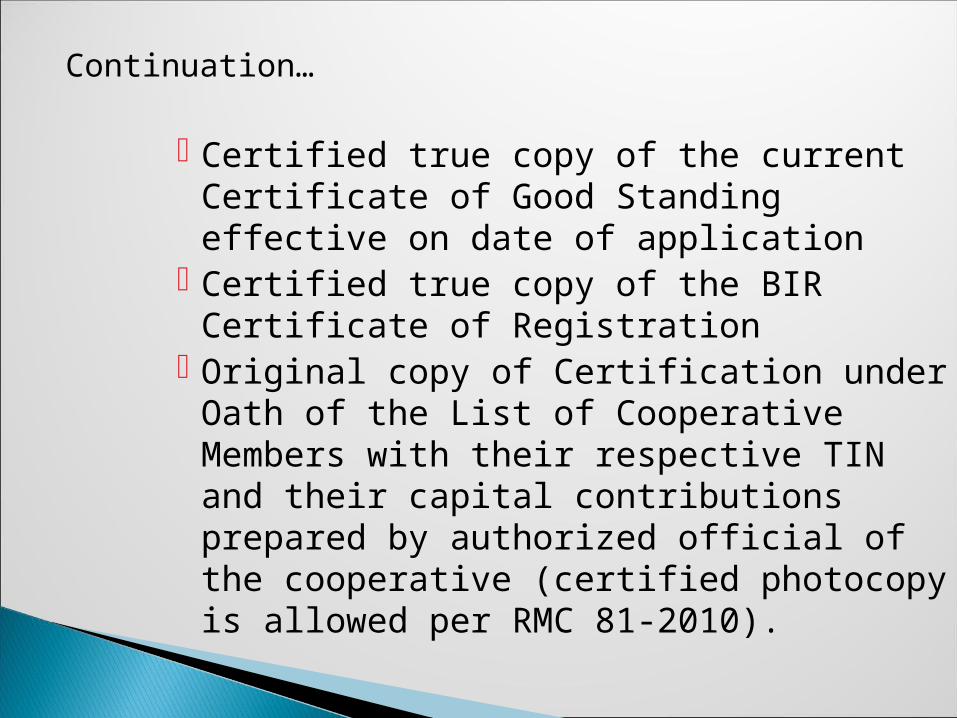

Certified true copy of the current Certificate of Good Standing effective on date of application

Certified true copy of the BIR Certificate of Registration

Original copy of Certification under Oath of the List of Cooperative Members with their respective TIN and their capital contributions prepared by authorized official of the cooperative (certified photocopy is allowed per RMC 81-2010).

Continuation…

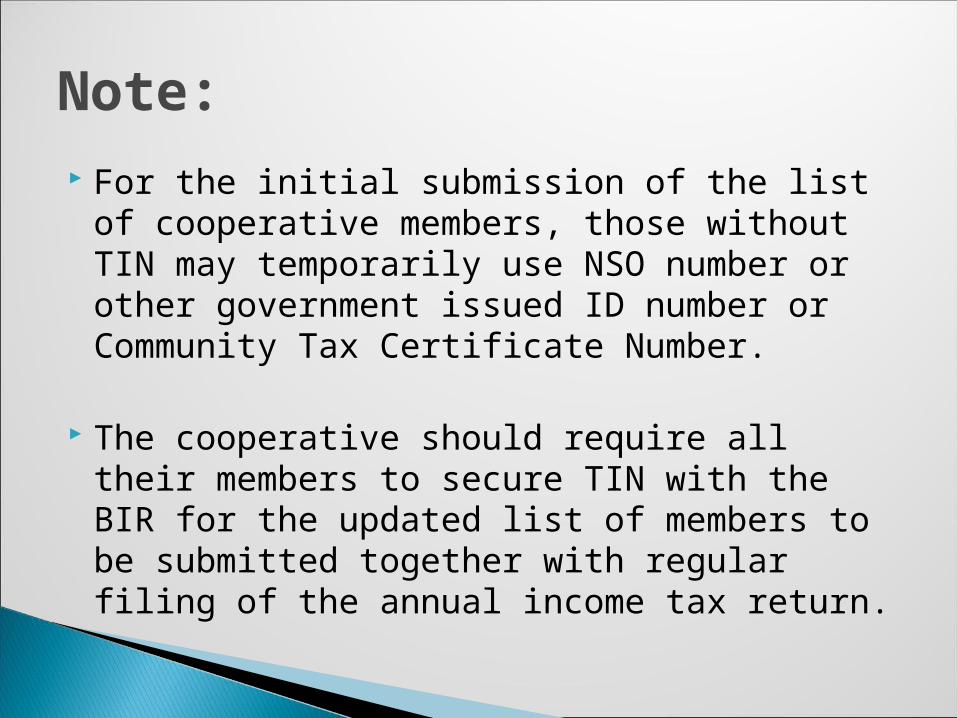

Note: For the initial submission of the list of

cooperative members, those without TIN may temporarily use NSO number or other government issued ID number or Community Tax Certificate Number.

The cooperative should require all their members to secure TIN with the BIR for the updated list of members to be submitted together with regular filing of the annual income tax return.

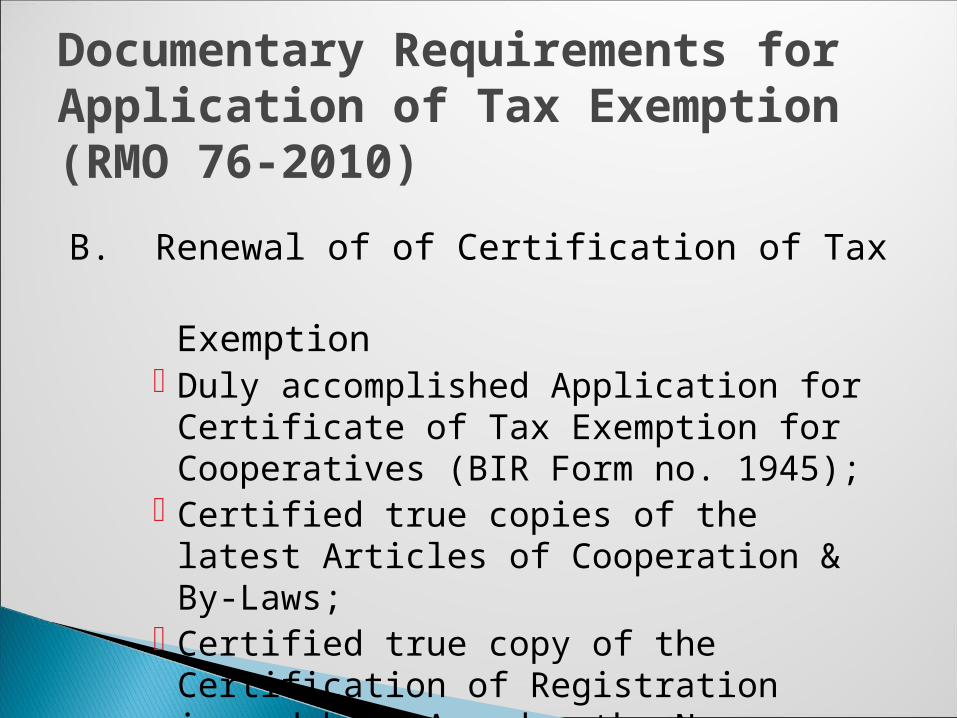

Documentary Requirements for Application of Tax Exemption(RMO 76-2010)

B. Renewal of of Certification of Tax Exemption

Duly accomplished Application for Certificate of Tax Exemption for Cooperatives (BIR Form no. 1945);

Certified true copies of the latest Articles of Cooperation & By-Laws;

Certified true copy of the Certification of Registration issued by CDA under the New Cooperative Code

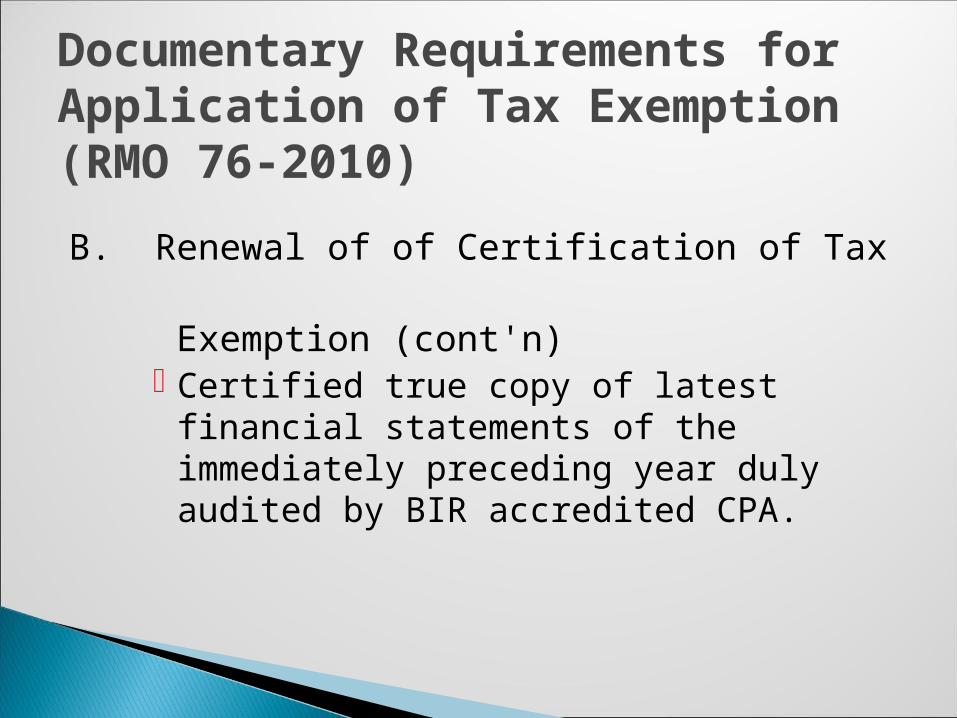

Documentary Requirements for Application of Tax Exemption(RMO 76-2010)

B. Renewal of of Certification of Tax Exemption (cont'n)

Certified true copy of latest financial statements of the immediately preceding year duly audited by BIR accredited CPA.

Shall be valid for the period of 5 years from the date of issue or date of effectivity

Cooperative is in good standing as ascertained by the CDA on an annual basis

• Renewed at least 2 months prior to the date of expiration of the existing Certificate of Tax Exemption/Ruling.

• Renewal certificate shall be good for another period of five (5) years.

Monitoring of Cooperative Cooperatives shall annually file its Annual

Information Return (Form 1702) with the following documents:◦Certified true copy of the current and

effective Certificate of Good Standing from CDA;

◦Certified true copy of Certificate under oath by the chairperson/General Manager

Monitoring of Cooperative◦Original copy of yearly summary of records

of transactions clearly showing which transactions correspond to members, yearly summary of records of transactions clearly showing which transactions correspond to members and non-members

Monitoring of Cooperative

◦ Original copy of certification under oath by the chairperson/general manager of list of members, their respective TIN and the share capital contribution as of the year end concerned. (certified photocopy is now allowed under RMC 81-2010)

Certificate under oathThe type/category of cooperative and the

principal activities/business transactions it is engaged in;

That the cooperative is transacting business with members only or both members and non-members;

The amount of accumulated reserves as of the year end; and

That at least 25% of the net surplus is returned to the members – interest or patronage refund.

Note Failure of the cooperatives to comply with

the documentary requirements shall be a ground for cancellation/revocation of the Certificate of Tax Exemption.

The books of accounts and there pertinent records may be examined by the BIR annually

after prior authorization by the CDA within 20 days from receipt of the request from BIR.

1. For the cases existing prior to the effectivity date of RA 9520 last March 22, 2009, the old cooperative code RA 6938 shall apply, since the new law (RA 9520) did not provide for the retroactive effect;

1. For the audit/investigation of 2008 internal revenue tax returns of Cooperatives, including tax returns of fiscal period taxpayers whose taxable year ended before March 22, 2009, all BIR Offices are authorized to issue notices of investigation following the procedures under the applicable Audit Program;

All unpaid/unsettled assessments as of the effectivity of RA 9520 shall be qualified to avail of the compromise settlement at a compromise rate equivalent to 20% of the basic tax assessed.

if the financial position of a cooperative demonstrates a clear inability to pay the assessed tax, Sec. 204(A)(2) of the NIRC as amended, shall apply.

end

44