Embed Size (px)

Citation preview

Tax policy and inequality

Robert Joyce, Institute for Fiscal Studies

Presentation at HMT/HMRC tax policy school

21st September 2016

© Institute for Fiscal Studies

© Institute for Fiscal Studies

Introduction

• Not for economists to specify strength of preference for equality or philosophies of ‘fairness’

– But given these judgements, how should tax policy be made?

• This talk is in broadly two parts:

1. General points about how to make policy, with links to examples

2. Comments on specific parts of tax system

• Political feasibility of suggestions will vary greatly, but:

– What is feasible depends on time horizon

– Need clear benchmark for what a good system looks like before you try to approximate it or move towards it

• See Mirrlees Review: www.ifs.org.uk/publications/mirrleesreview

© Institute for Fiscal Studies

Tax policy and fairness / distribution General points

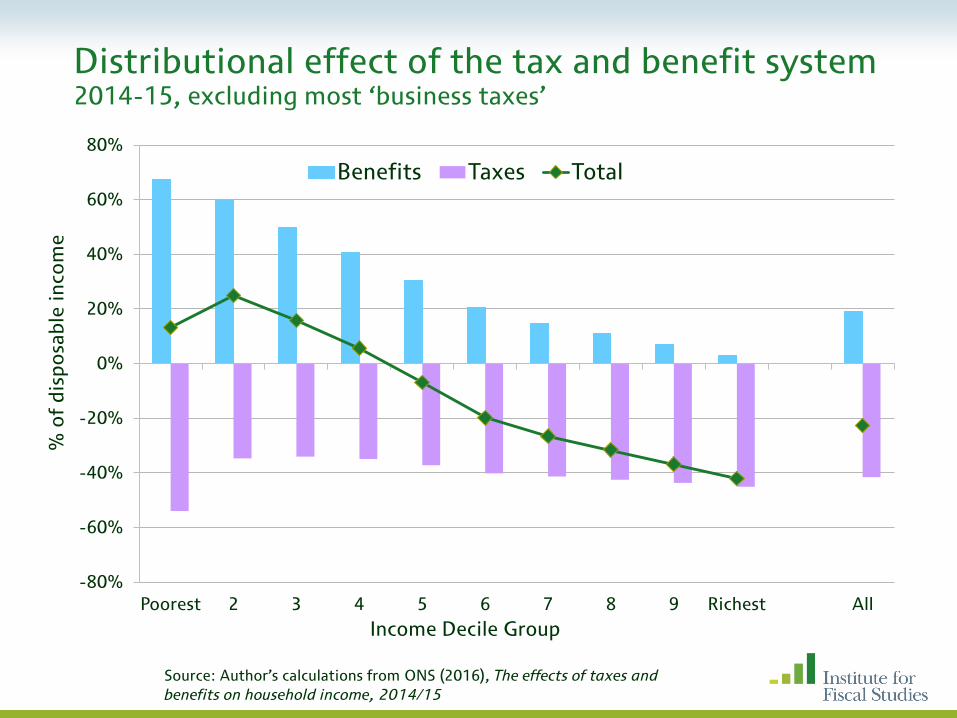

1. Consider effects of tax and welfare system as a whole

– Much of the redistribution is done by benefits/tax credits

Distributional effect of the tax and benefit system 2014-15, excluding most ‘business taxes’

© Institute for Fiscal Studies

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Poorest 2 3 4 5 6 7 8 9 Richest All

% o

f d

isp

osa

ble

in

com

e

Income Decile Group

Benefits Taxes Total

Source: Author’s calculations from ONS (2016), The effects of taxes and

benefits on household income, 2014/15

© Institute for Fiscal Studies

Tax policy and fairness / distribution General points

1. Consider effects of tax and welfare system as a whole

– Much of the redistribution is done by benefits/tax credits

– Trying to get every part of system to achieve every objective can lead to bad policy, e.g. indirect taxes are ill-suited for use as a means of redistribution (see Mirrlees Review on differential VAT rates)

– Coherence, fairness and avoidance opportunities: is the system treating similar activities similarly?

© Institute for Fiscal Studies

Tax policy and fairness / distribution General points

1. Consider effects of tax and welfare system as a whole

2. Take a long term (ideally lifetime) view of who gets what

© Institute for Fiscal Studies

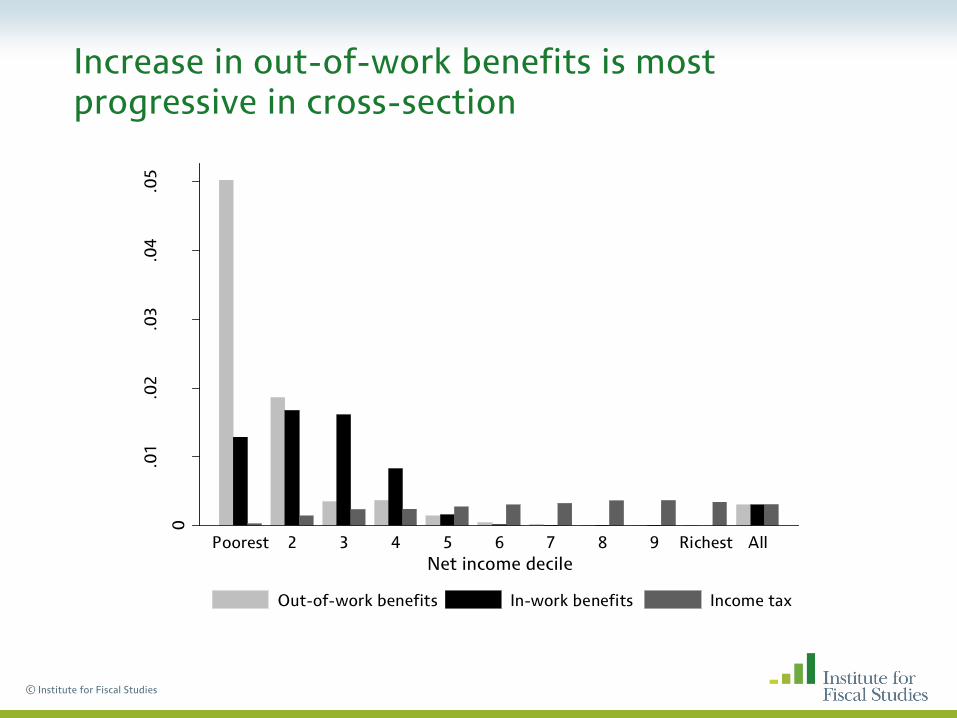

Increase in out-of-work benefits is most progressive in cross-section

0

.01

.02

.03

.04

.05

Pro

po

rtio

na

l ch

an

ge

in

ne

t in

com

e

Poorest 2 3 4 5 6 7 8 9 Richest All

Net income decile

Out-of-work benefits In-work benefits Income tax

© Institute for Fiscal Studies

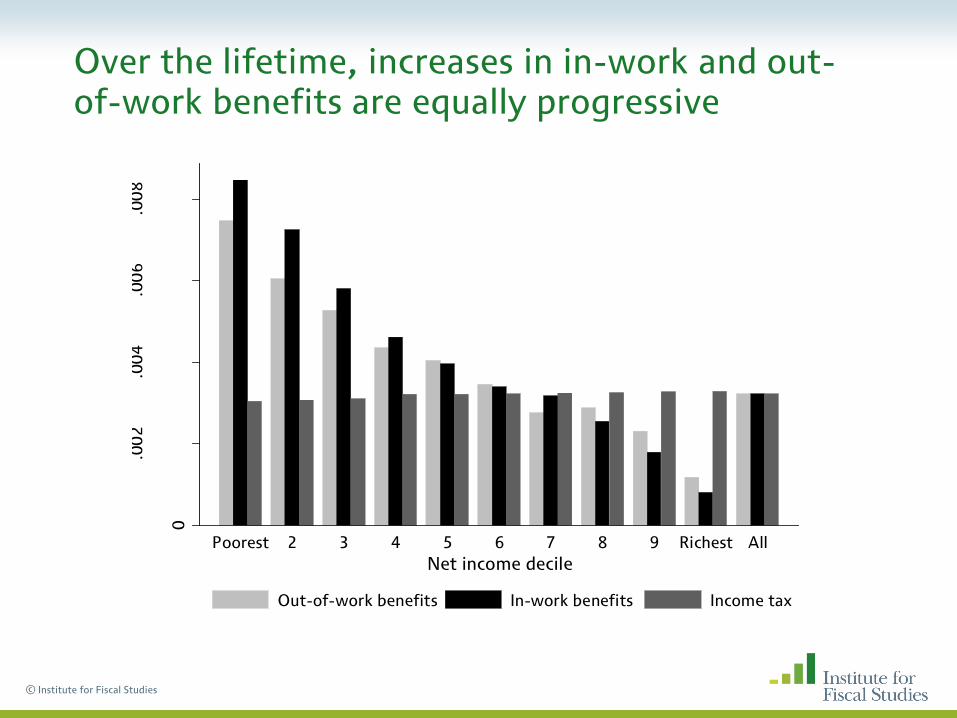

Over the lifetime, increases in in-work and out-of-work benefits are equally progressive

0

.00

2.0

04

.00

6.0

08

Pro

po

rtio

na

l ch

an

ge

in

ne

t in

com

e

Poorest 2 3 4 5 6 7 8 9 Richest All

Net income decile

Out-of-work benefits In-work benefits Income tax

© Institute for Fiscal Studies

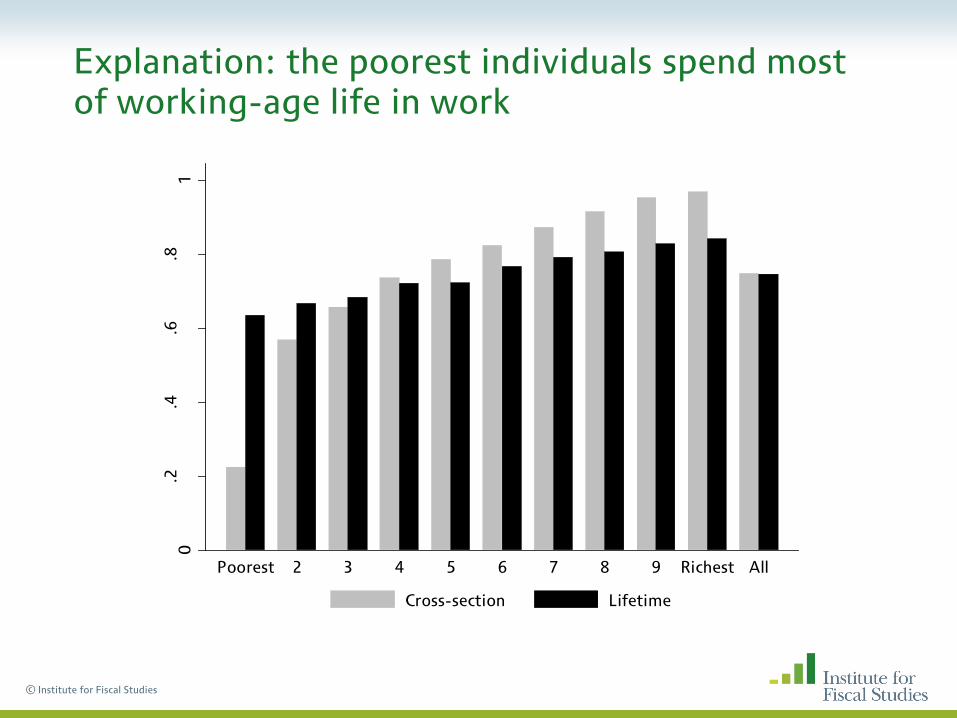

Explanation: the poorest individuals spend most of working-age life in work

0.2

.4.6

.81

Pro

po

rtio

n e

mp

loy

ed

Poorest 2 3 4 5 6 7 8 9 Richest All

Cross-section Lifetime

© Institute for Fiscal Studies

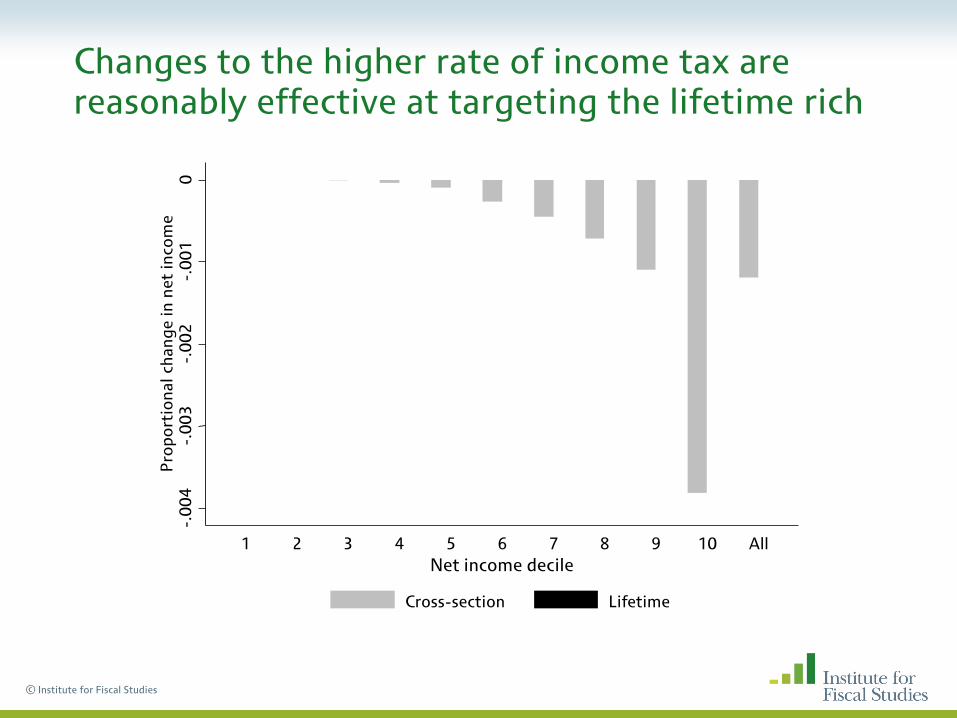

Changes to the higher rate of income tax are reasonably effective at targeting the lifetime rich

-.0

04

-.

00

3

-.0

02

-.

00

1

0

Pro

po

rtio

na

l ch

an

ge

in

ne

t in

com

e

1 2 3 4 5 6 7 8 9 10 All

Net income decile

Cross-section Lifetime

© Institute for Fiscal Studies

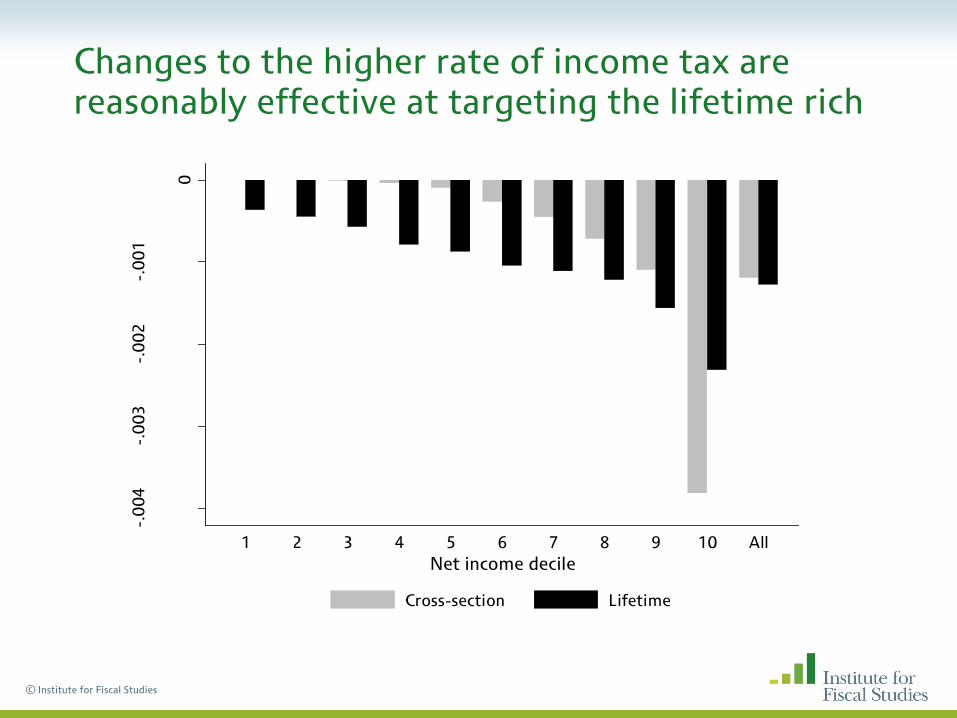

Changes to the higher rate of income tax are reasonably effective at targeting the lifetime rich

-.0

04

-.0

03

-.0

02

-.0

01

0

Pro

po

rtio

na

l ch

an

ge

in

ne

t in

com

e

1 2 3 4 5 6 7 8 9 10 All

Net income decile

Cross-section Lifetime

© Institute for Fiscal Studies

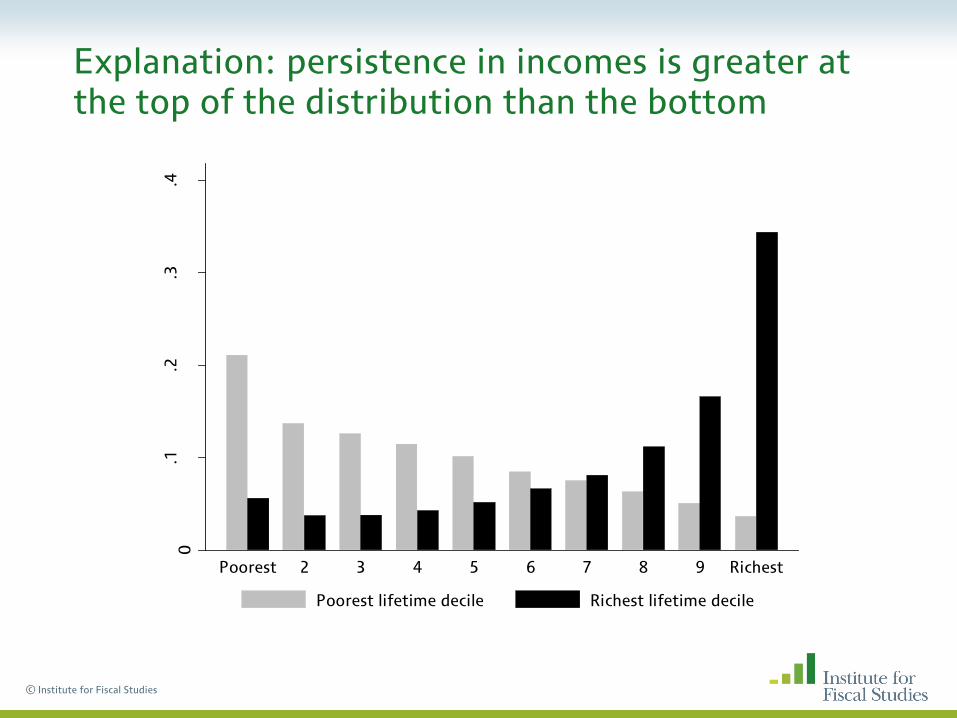

Explanation: persistence in incomes is greater at the top of the distribution than the bottom

0.1

.2.3

.4

Pro

po

rtio

n o

f li

fe i

n e

ach

cro

ss-s

ect

ion

al

de

cile

Poorest 2 3 4 5 6 7 8 9 Richest

Poorest lifetime decile Richest lifetime decile

© Institute for Fiscal Studies

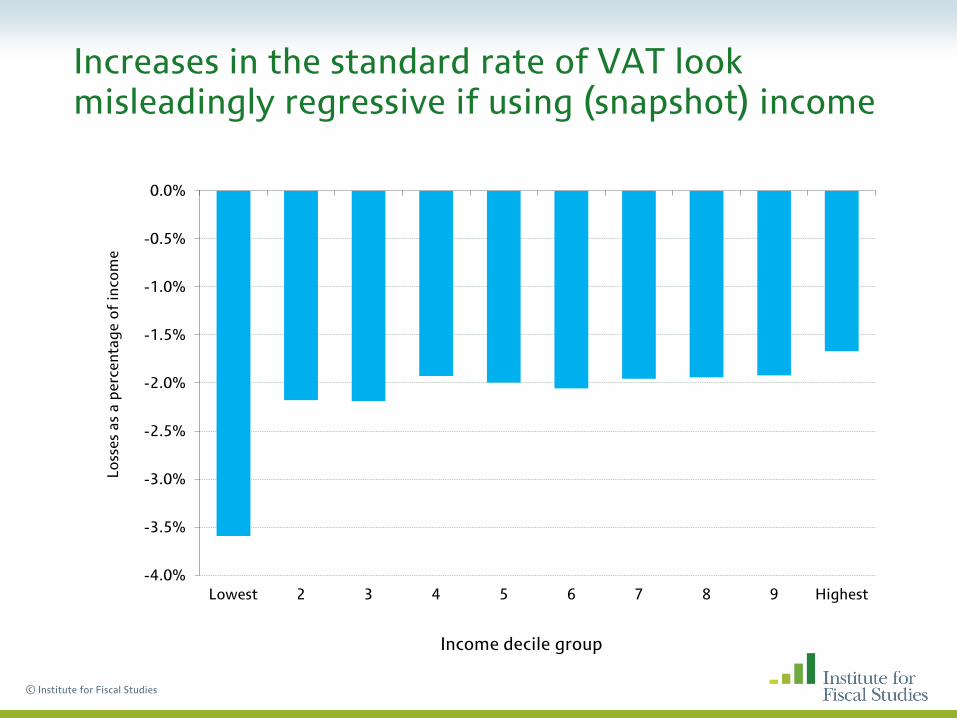

Increases in the standard rate of VAT look misleadingly regressive if using (snapshot) income

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

Lowest 2 3 4 5 6 7 8 9 Highest

Lo

sse

s a

s a

pe

rce

nta

ge

of

inco

me

Income decile group

© Institute for Fiscal Studies

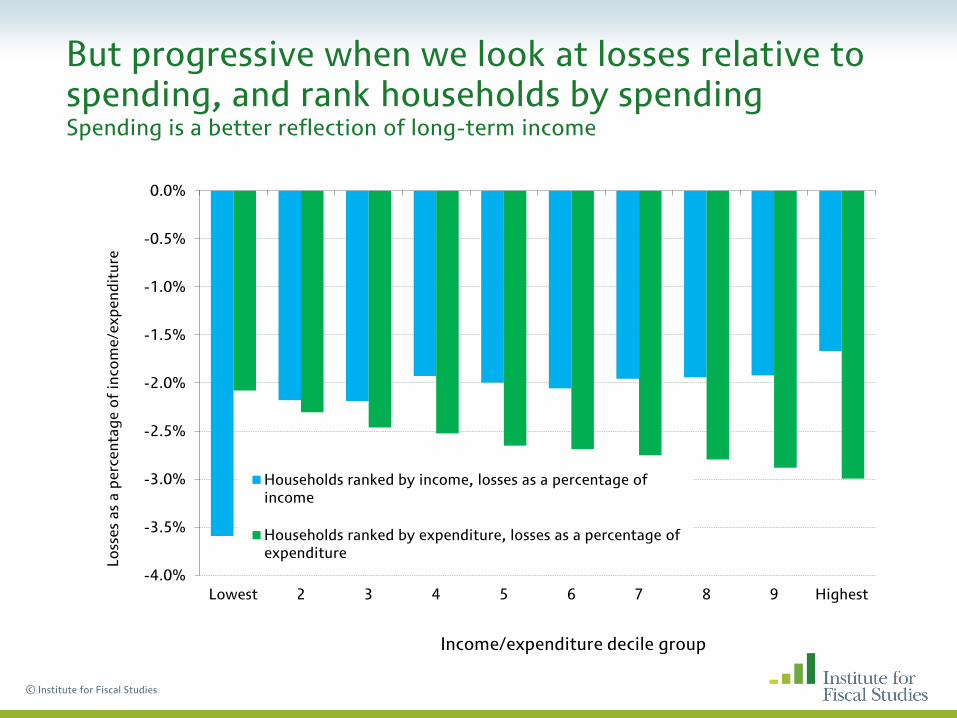

But progressive when we look at losses relative to spending, and rank households by spending Spending is a better reflection of long-term income

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

Lowest 2 3 4 5 6 7 8 9 Highest

Lo

sse

s a

s a

pe

rce

nta

ge

of

inco

me

/exp

en

dit

ure

Income/expenditure decile group

Households ranked by income, losses as a percentage of income

Households ranked by expenditure, losses as a percentage of expenditure

© Institute for Fiscal Studies

Tax policy and fairness / distribution General points

1. Consider effects of tax and welfare system as a whole

2. Take a long term (ideally lifetime) view of who gets what

– Can really change impression of policy impacts e.g. VAT, WTC

– Many more people (e.g.) have kids, are lone parents, or have health problems at some point in lifecycle than in a snapshot

– Of course short term needs do matter too - though more relevant for ‘safety net’ benefits than for taxes

© Institute for Fiscal Studies

Tax policy and fairness / distribution General points

1. Consider effects of tax and welfare system as a whole

2. Take a long term (ideally lifetime) view of who gets what

3. Use empirical evidence on how people respond to incentives

– e.g. labour supply of parents of school-age children more responsive than for those with younger kids: could increase employment overall by cutting Child Tax Credit for former and raising for latter

– Note again importance of lifecycle view –redistribution would largely be between periods of parenthood, not across people

– Sometimes evidence is less clear-cut: but that in itself can be good reason to proceed with caution...

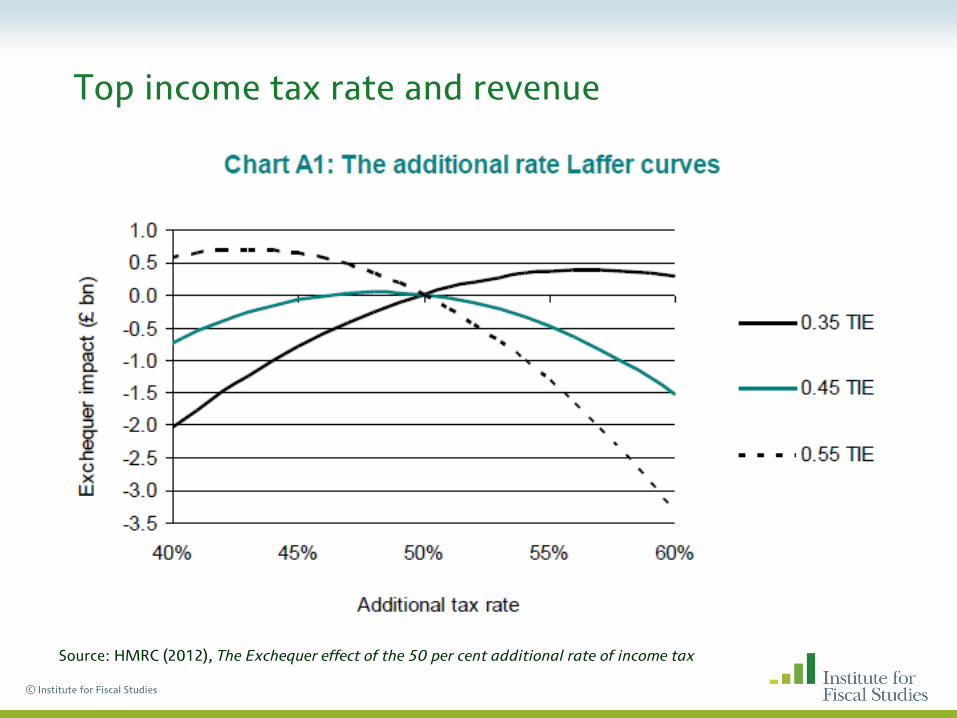

Top income tax rate and revenue

© Institute for Fiscal Studies

Source: HMRC (2012), The Exchequer effect of the 50 per cent additional rate of income tax

© Institute for Fiscal Studies

Direct tax: income tax and NI

• Increasing the IT personal allowance is not progressive and is a very expensive way of helping the lowest earning beneficiaries

– and increasingly so: 43% of adults now have incomes too low to pay income tax, and pensioners now benefit too

• Totemic significance of income tax and relative ability of NI to go ‘under the radar’ seems to lead to policy outcomes that are unintended and/or go against grain of govt policy

– e.g. earnings threshold for NI remained almost untouched while the income tax PA has been massively increased

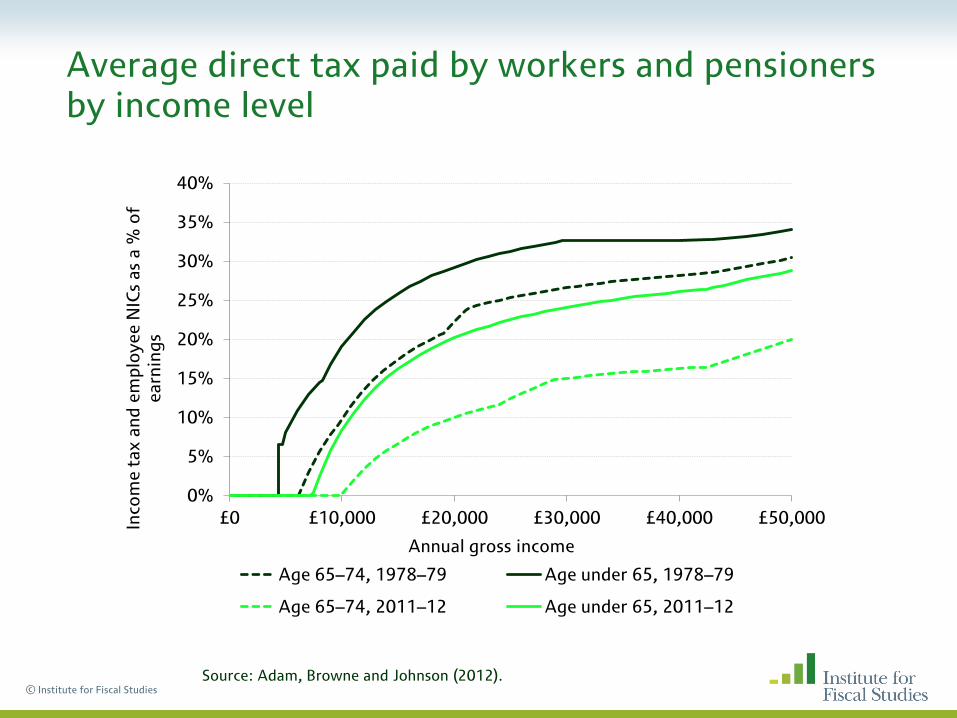

Average direct tax paid by workers and pensioners by income level

© Institute for Fiscal Studies

0%

5%

10%

15%

20%

25%

30%

35%

40%

£0 £10,000 £20,000 £30,000 £40,000 £50,000 Inco

me

tax a

nd

em

plo

ye

e N

ICs

as

a %

of

ea

rnin

gs

Annual gross income

Age 65–74, 1978–79 Age under 65, 1978–79

Age 65–74, 2011–12 Age under 65, 2011–12

Source: Adam, Browne and Johnson (2012).

© Institute for Fiscal Studies

Direct tax: income tax and NI

• Increasing the IT personal allowance is not progressive and is a very expensive way of helping the lowest earning beneficiaries

– and increasingly so: 43% of adults now have incomes too low to pay income tax, and pensioners now benefit too

• Totemic significance of income tax and relative ability of NI to go ‘under the radar’ seems to lead to policy outcomes that are unintended and/or go against grain of govt policy

– e.g. earnings threshold for NI remained untouched while the income tax PA has been massively increased

• (Big issues around top tax rates and tax relief on pension contributions, covered elsewhere)

Property tax

• Perhaps the worst-designed part of the tax system?

• From point of view of equity and fairness, obvious deficiencies in council tax:

– Still based on 1991 property values in England and Scotland

– Wide bands

– Regressive

© Institute for Fiscal Studies

© Institute for Fiscal Studies

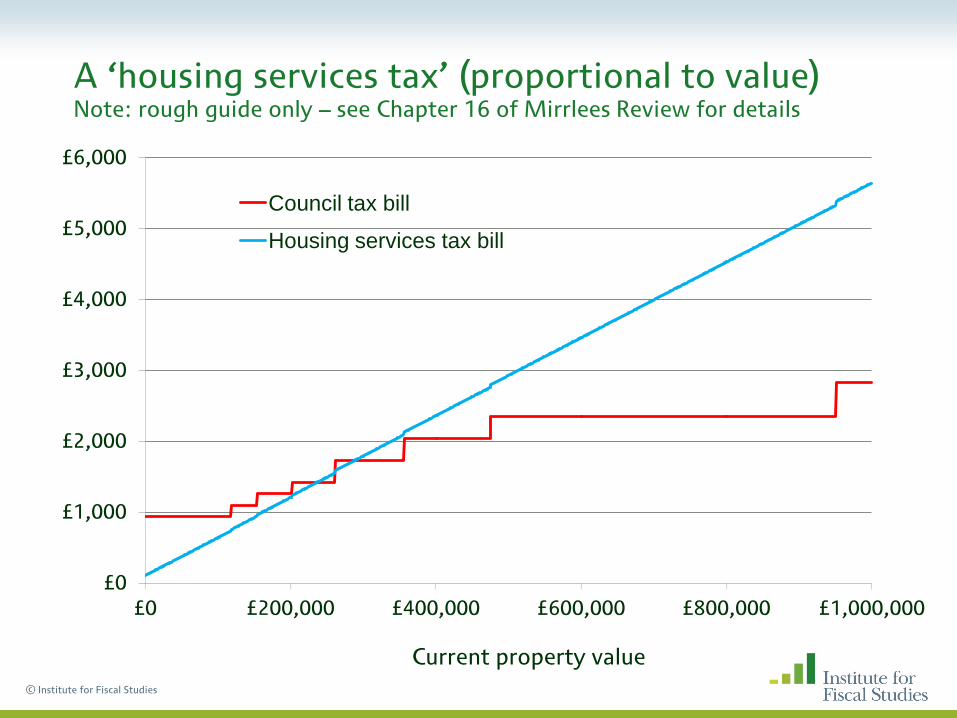

A ‘housing services tax’ (proportional to value) Note: rough guide only – see Chapter 16 of Mirrlees Review for details

£0

£1,000

£2,000

£3,000

£4,000

£5,000

£6,000

£0 £200,000 £400,000 £600,000 £800,000 £1,000,000

Current property value

Council tax bill

Housing services tax bill

Property tax

• Perhaps the worst-designed part of the tax system?

• From point of view of equity and fairness, obvious deficiencies in council tax:

– Still based on 1991 property values in England and Scotland

– Wide bands

– Regressive

• A sensibly reformed council tax would involve higher tax on expensive properties, which could replace revenue from stamp duty land tax...

• As a transaction tax, SDLT should not be part of tax system

– Why impose heavier tax on properties that change hands more often?

– Assets should be held by the people who value them most

– Reduced labour mobility and rates of downsizing are likely examples of damaging effects of SDLT

© Institute for Fiscal Studies

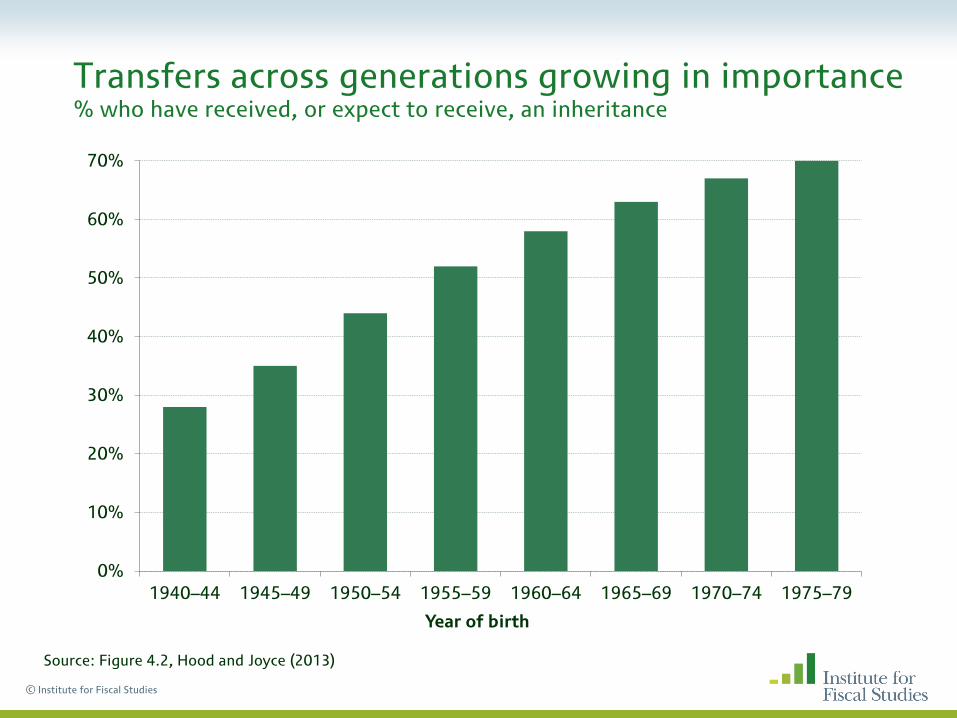

Transfers across generations growing in importance % who have received, or expect to receive, an inheritance

© Institute for Fiscal Studies

0%

10%

20%

30%

40%

50%

60%

70%

1940–44 1945–49 1950–54 1955–59 1960–64 1965–69 1970–74 1975–79

Year of birth

Source: Figure 4.2, Hood and Joyce (2013)

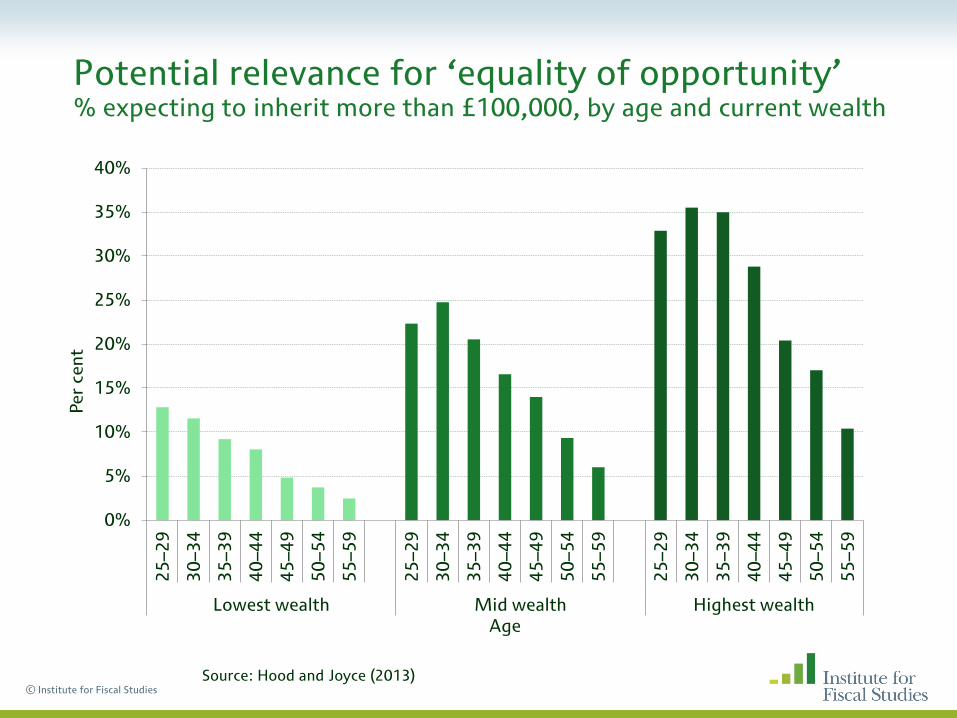

Potential relevance for ‘equality of opportunity’ % expecting to inherit more than £100,000, by age and current wealth

© Institute for Fiscal Studies

0%

5%

10%

15%

20%

25%

30%

35%

40% 2

5–

29

30

–3

4

35

–3

9

40

–4

4

45

–4

9

50

–5

4

55

–5

9

25

–2

9

30

–3

4

35

–3

9

40

–4

4

45

–4

9

50

–5

4

55

–5

9

25

–2

9

30

–3

4

35

–3

9

40

–4

4

45

–4

9

50

–5

4

55

–5

9

Lowest wealth Mid wealth Highest wealth

Pe

r ce

nt

Age

Source: Hood and Joyce (2013)

Taxing intergenerational transfers

• There are (principled) arguments over whether to tax intergenerational transfers

• But the way in which we do this can certainly be improved

• Lots of exemptions, e.g. for business assets, agricultural land, and any gifts made in at least seven years before death

– Inheritance tax favours “the healthy, wealthy and well-advised” (Kay and King, 1990)

– For some of the rich, it largely resembles a voluntary contribution

• Should certainly remove some avoidance opportunities

• More fundamentally, could either:

– Transform into a proper tax on lifetime receipts

– Abolish

© Institute for Fiscal Studies

Taxing the very richest

• Revenue heavily reliant on a small number of taxpayers

• 29% of income tax is paid by the 332,000 additional-rate taxpayers (0.6% of adults)

• 54% of CGT is paid by 5,000 individuals (<0.01%) realising gains >£1m

• 70% of inheritance tax is paid by 2,000 estates (0.4%) worth >£1m

• (...and these groups overlap to substantial degree)

• Must be conscious of how their behaviour responds to tax: stakes are high

• It matters not only how much you tax the rich, but how you tax them

© Institute for Fiscal Studies

Some relatively sensible ways to tax the well-off...

© Institute for Fiscal Studies

...More than we do ...Less than we do

• Remove IHT reliefs for agricultural and business assets and main homes

• Remove CGT entrepreneur’s relief and forgiveness at death

• Charge NICs on employer pension contributions and cut tax-free lump sum

• Increase (updated!) council tax at top end

• Merge income tax and CGT allowances

• Tax lifetime gifts as well as bequests

• Abolish withdrawal of personal allowance above £100,000

• Allow all to get tax relief on pension contributions at their marginal tax rate, with same annual allowance

• Reduce higher rates of SDLT (or abolish completely)

• Reduce or abolish IHT

• Give full IT & CGT allowance for amounts saved/invested

• Cancel abolition of higher-rate relief

for landlords’ mortgage interest

*But avoid*

• Increasing SDLT

• Further restricting pension tax relief

• Annual wealth tax

• Creating/increasing incentives to seek tax advantages

Note: important caveats not included!

© Institute for Fiscal Studies

Summary

• When assessing impacts on inequalities we should

– Consider system in the round

– Appreciate that people live lifecycles, not snapshots

• Never going to have agreement on what is fair and equitable

• But can achieve a given degree of equity in vastly different ways

– We should choose the least costly ways

– In many cases we have lots of evidence to guide us