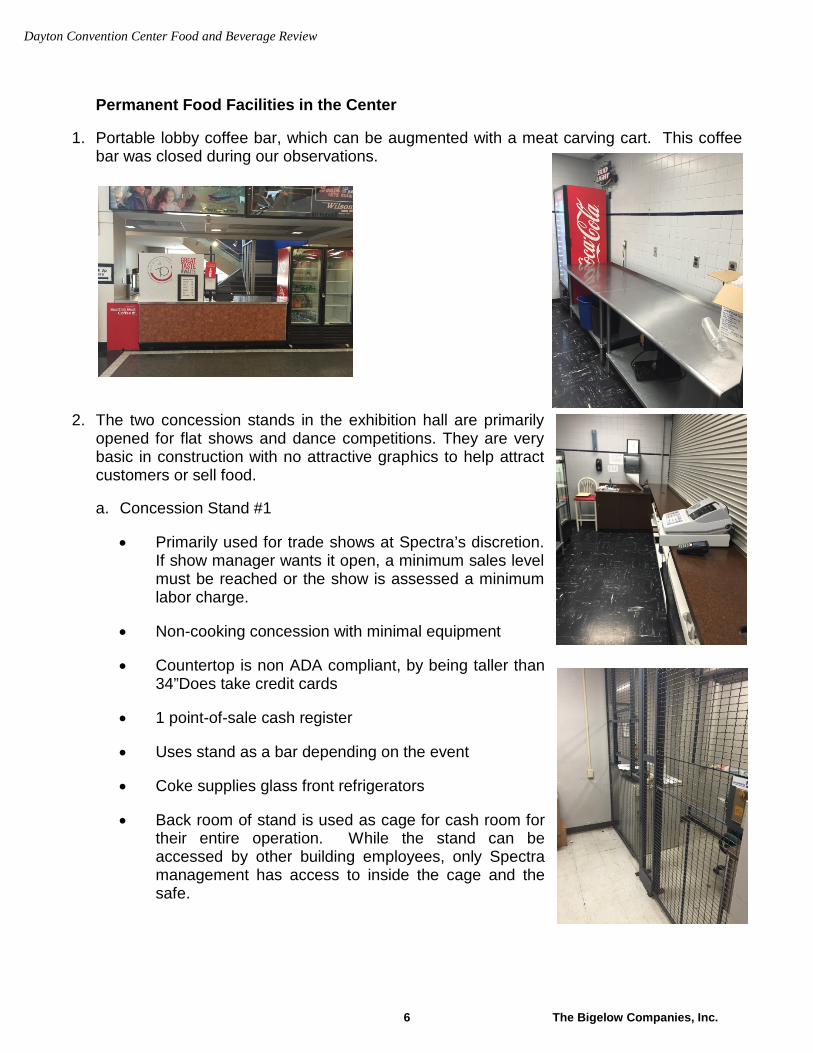

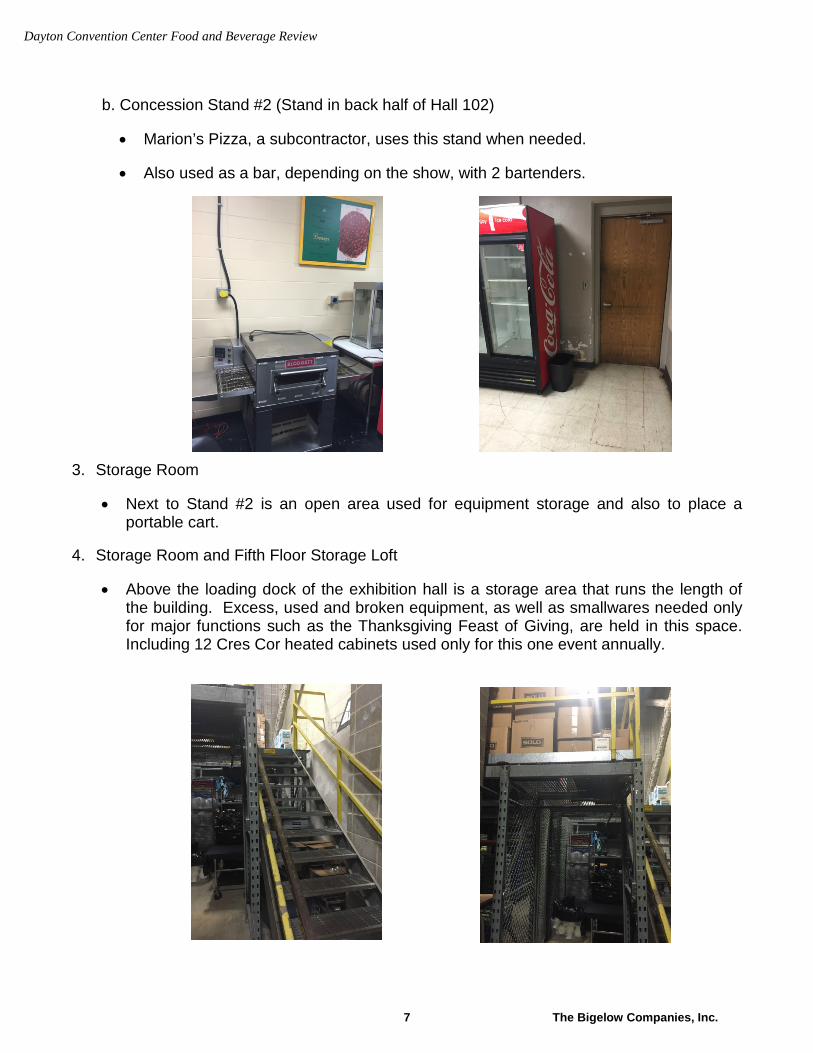

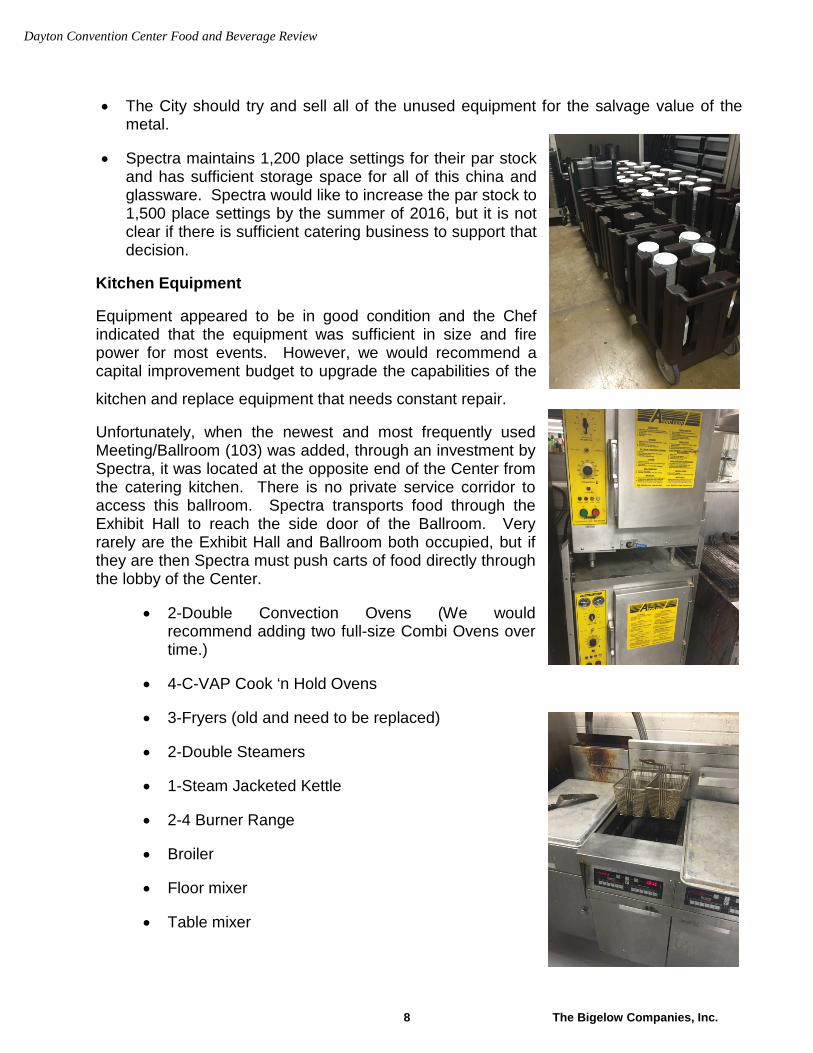

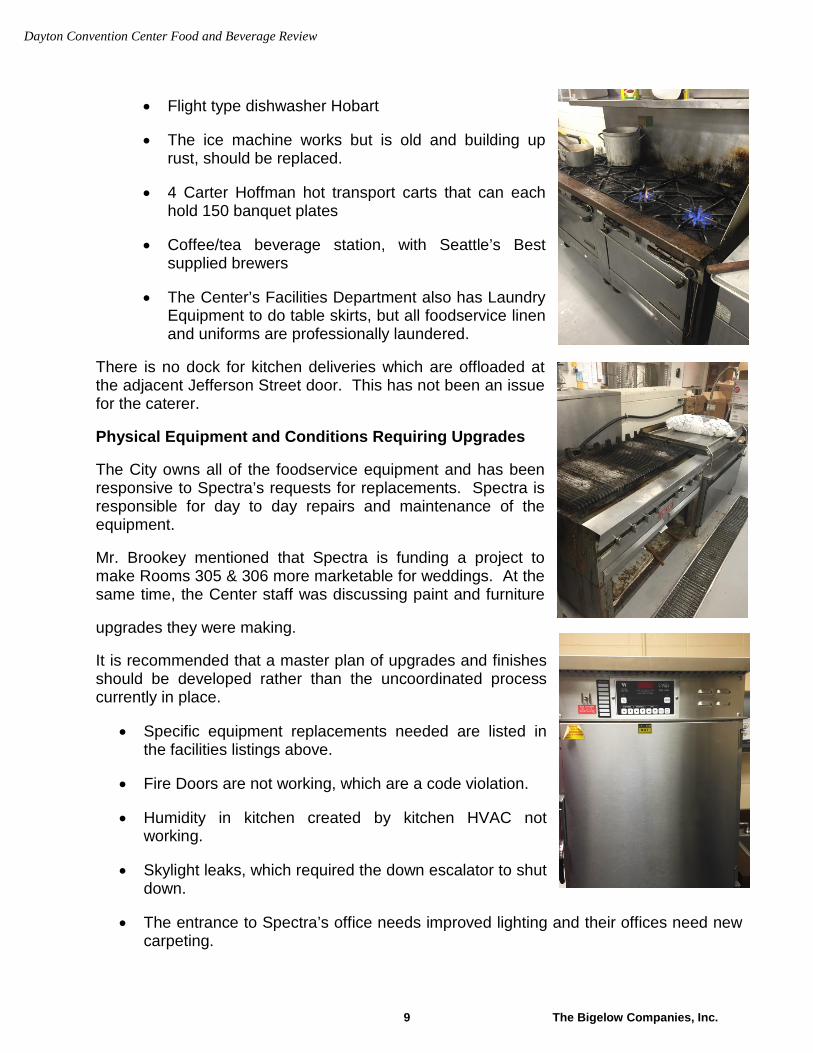

Embed Size (px)

Citation preview

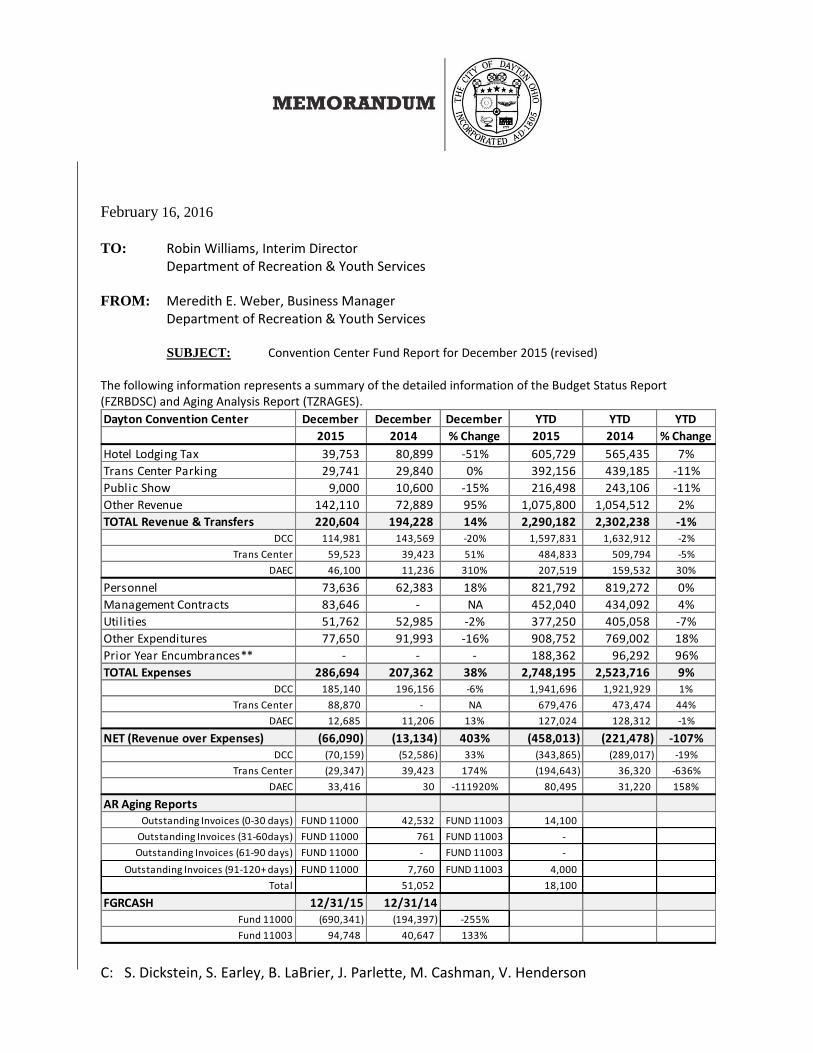

February 16, 2016

TO: Robin Williams, Interim Director Department of Recreation & Youth Services

FROM: Meredith E. Weber, Business Manager Department of Recreation & Youth Services

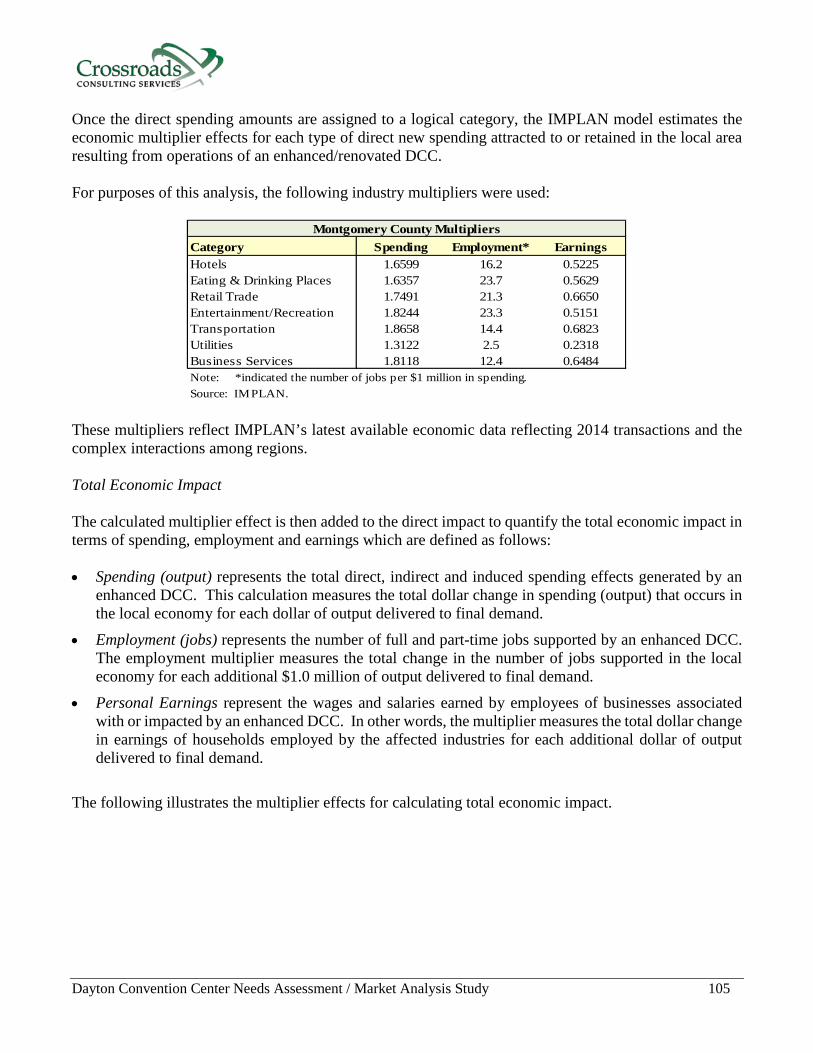

SUBJECT: Convention Center Fund Report for December 2015 (revised) The following information represents a summary of the detailed information of the Budget Status Report (FZRBDSC) and Aging Analysis Report (TZRAGES).

C: S. Dickstein, S. Earley, B. LaBrier, J. Parlette, M. Cashman, V. Henderson

Dayton Convention Center December December December YTD YTD YTD

2015 2014 % Change 2015 2014 % Change

Hotel Lodging Tax 39,753 80,899 -51% 605,729 565,435 7%

Trans Center Parking 29,741 29,840 0% 392,156 439,185 -11%

Public Show 9,000 10,600 -15% 216,498 243,106 -11%

Other Revenue 142,110 72,889 95% 1,075,800 1,054,512 2%

TOTAL Revenue & Transfers 220,604 194,228 14% 2,290,182 2,302,238 -1%DCC 114,981 143,569 -20% 1,597,831 1,632,912 -2%

Trans Center 59,523 39,423 51% 484,833 509,794 -5%

DAEC 46,100 11,236 310% 207,519 159,532 30%

Personnel 73,636 62,383 18% 821,792 819,272 0%

Management Contracts 83,646 - NA 452,040 434,092 4%

Utilities 51,762 52,985 -2% 377,250 405,058 -7%

Other Expenditures 77,650 91,993 -16% 908,752 769,002 18%

Prior Year Encumbrances** - - - 188,362 96,292 96%

TOTAL Expenses 286,694 207,362 38% 2,748,195 2,523,716 9%DCC 185,140 196,156 -6% 1,941,696 1,921,929 1%

Trans Center 88,870 - NA 679,476 473,474 44%

DAEC 12,685 11,206 13% 127,024 128,312 -1%

NET (Revenue over Expenses) (66,090) (13,134) 403% (458,013) (221,478) -107%DCC (70,159) (52,586) 33% (343,865) (289,017) -19%

Trans Center (29,347) 39,423 174% (194,643) 36,320 -636%

DAEC 33,416 30 -111920% 80,495 31,220 158%

AR Aging ReportsOutstanding Invoices (0-30 days) FUND 11000 42,532 FUND 11003 14,100

Outstanding Invoices (31-60days) FUND 11000 761 FUND 11003 -

Outstanding Invoices (61-90 days) FUND 11000 - FUND 11003 -

Outstanding Invoices (91-120+ days) FUND 11000 7,760 FUND 11003 4,000

Total 51,052 18,100

FGRCASH 12/31/15 12/31/14Fund 11000 (690,341) (194,397) -255%

Fund 11003 94,748 40,647 133%

5401 W. Kennedy Boulevard ∙ Suite 755 ∙ Tampa, Florida 33609 ∙ Phone 813.281.1222 ∙ Fax 813.315.6040

Needs Assessment / Market Analysis Study

for the Dayton Convention Center

Presented to:

City of Dayton

Dayton/Montgomery County Convention & Visitors Bureau

Presented by:

Final Report – December 2015

5401 W. Kennedy Boulevard ∙ Suite 755 ∙ Tampa, Florida 33609 ∙ Phone 813.281.1222 ∙ Fax 813.315.6040

December 31, 2015 Ms. Jacquie Powell, President & CEO Dayton/Montgomery County Convention & Visitors Bureau 1 Chamber Plaza, Suite A Dayton, OH 45402-2400 Dear Ms. Powell: Crossroads Consulting Services LLC (Crossroads), in association with Convergence Design and the Bigelow Companies, Inc., has completed its needs assessment/market analysis study for the Dayton Convention Center. This report summarizes our research and analysis. The information contained in the report is based on estimates, assumptions, and information developed from market research; knowledge of the convention/meeting and sports industries; input from potential demand generators; as well as data provided by management at the Dayton Convention Center and the Dayton/Montgomery County Convention & Visitors Bureau. We have utilized sources that are deemed to be reliable but cannot guarantee their accuracy. All information provided to us by others was not audited or verified and was assumed to be correct. Moreover, estimates and analysis are based on trends and assumptions and, therefore, there will usually be differences between the projected and actual results because events and circumstances frequently do not occur as expected, and those differences may be material. We have no obligation, unless subsequently engaged, to update this report or revise the information contained therein to reflect events and transactions occurring after the date of this report. In accordance with the terms of our engagement letter, the accompanying report is restricted to internal use by the City of Dayton and Dayton/Montgomery County Convention & Visitors Bureau and may not be relied upon by any third party for any purpose including financing. Notwithstanding these limitations, it is understood that this document may be subject to public information laws and, as such, can be made available to the public upon request. Although you have authorized reports to be sent electronically for your convenience, only the final hard copy report should be viewed as our work product. We have enjoyed our relationship with the City of Dayton and Dayton/Montgomery County Convention & Visitors Bureau and look forward to providing you with continued services in the future. Sincerely, Crossroads Consulting Services LLC

Dayton Convention Center Needs Assessment / Market Analysis Study 1

Table of Contents

1 Introduction and Executive Summary 1 2 General Market Overview 11 3 Key Industry Trends 20 4 Historical Facility Operations 27 5 General Management Practices Assessment 47 6 Physical Facility Assessment 57 7 Competitive Facility Assessment 71 8 Needs Assessment 85 9 Economic Analysis 94

10 Funding Analysis 113

11 Limiting Conditions and Assumptions 120

12 Appendix 122

Dayton Convention Center Needs Assessment / Market Analysis Study 2

Introduction

Opened in 1973, the Dayton Convention Center (DCC) is owned and operated by the City of Dayton. The facility currently offers 68,400 square feet of exhibit space; 20,000 square feet of ballroom space; 12,400 square feet of meeting space; and a 672-seat theater. The facility is located in downtown and connected to the Crowne Plaza hotel which offers 289 sleeping rooms as well as a 6,300 square-foot ballroom and 5,800 square feet of meeting space. Downtown Dayton’s Oregon District is a mixed-use urban center offering residential, entertainment, dining and shopping establishments within two blocks of the DCC. In July 2013, the DCC became a component of the City of Dayton Department of Recreation and Youth Services. Efforts are ongoing to revitalize downtown Dayton by attracting new residents and businesses. The bulk of development has occurred along the Great Miami River, the northern border of downtown. The Oregon District continues to experience revitalization. Meanwhile, the area immediately surrounding the DCC includes several vacant buildings and limited visitor amenities. Competitive destinations including Akron, Cincinnati, Columbus, Fort Wayne and Sharonville are continuing to invest in their convention facilities as well as supporting visitor infrastructure proximate to these venues. These improvements, along with newer facilities such as the Cleveland Convention Center and Kalahari Hotel & Conference Center in Sandusky have changed the competitive landscape for the DCC. Given this backdrop, the Dayton/Montgomery County Convention & Visitors Bureau (Dayton CVB), on behalf of the City of Dayton, retained the project team of Crossroads Consulting, Convergence Design, and The Bigelow Companies, Inc. to assess the strengths and challenges of the existing DCC from a physical and operational perspective. Based on this assessment, the CVB and the City of Dayton want to better understand the benefits, opportunities and challenges posed by the potential renovation/expansion of the DCC or construction of a new convention center. From a macro level, our work plan consisted of the following primary elements:

Situational Overview

•Market Overview

•Management Practices Assessment

•Physical Facility Assessment

•Competitive Facility Assessment

Recommended Action Steps/ Implementation Strategy

•Operational Recommendations

•Prioritized Physical Needs Assessment by Building Area, Relative Cost and Implementation Timeline

•Cost Estimate

Renovation/Enhancement Economic Analysis

•Impact to Event Activity

•Impact to Financial Operations

•Impact to Economic/Fiscal Benefits

•Potential Funding Strategies

Dayton Convention Center Needs Assessment / Market Analysis Study 3

Specific research tasks conducted for this analysis include, but are not limited to, the following:

• Conducted interviews with representatives of the City of Dayton, DCC, the Dayton CVB, and external organizations that interact with the DCC including the Downtown Dayton Partnership, Dayton Development Coalition, Greater Dayton Regional Transit Authority, Dayton Area Chamber of Commerce, Oregon District, Dayton International Airport, hoteliers, facility users and other stakeholders.

• Profiled existing market conditions in terms of demographic/economic statistics, area employment, accessibility, hotel supply, area attractions, area facilities and local planning efforts.

• Analyzed key areas of DCC operations including governance, mission statement, booking policy, sales and marketing efforts, organizational structure, staffing levels, event activity, financial operations and capital planning in the context of industry best practices.

• Obtained input from past and potential users regarding the strengths and challenges of the existing DCC as well as the opportunities and threats from a competitive market standpoint.

• Attended an event to gauge consumer/customer impressions and assess operational issues including food and beverage operations.

• Recommended operational changes to enhance the DCC’s operating efficiency.

• Evaluated the DCC’s existing condition from physical, mechanical, cosmetic, and technological perspectives.

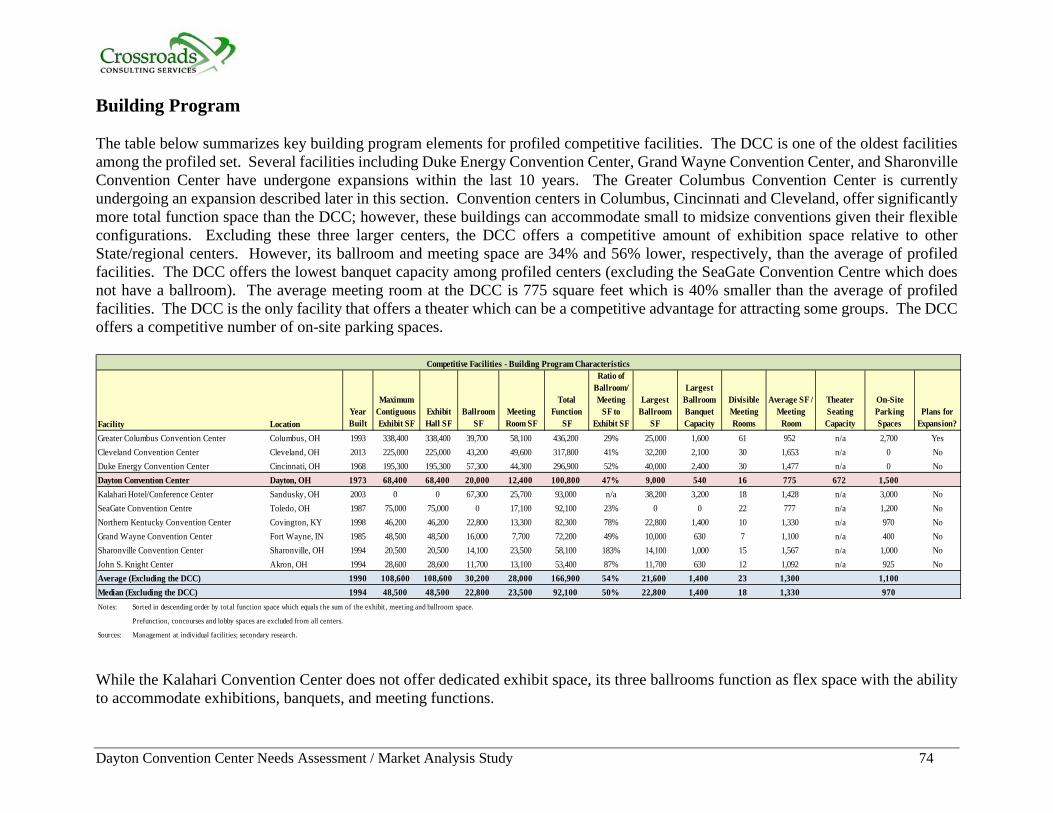

• Compared key building program elements at the DCC and destination attributes of Dayton to competitive venues and markets to provide context for recommended improvements.

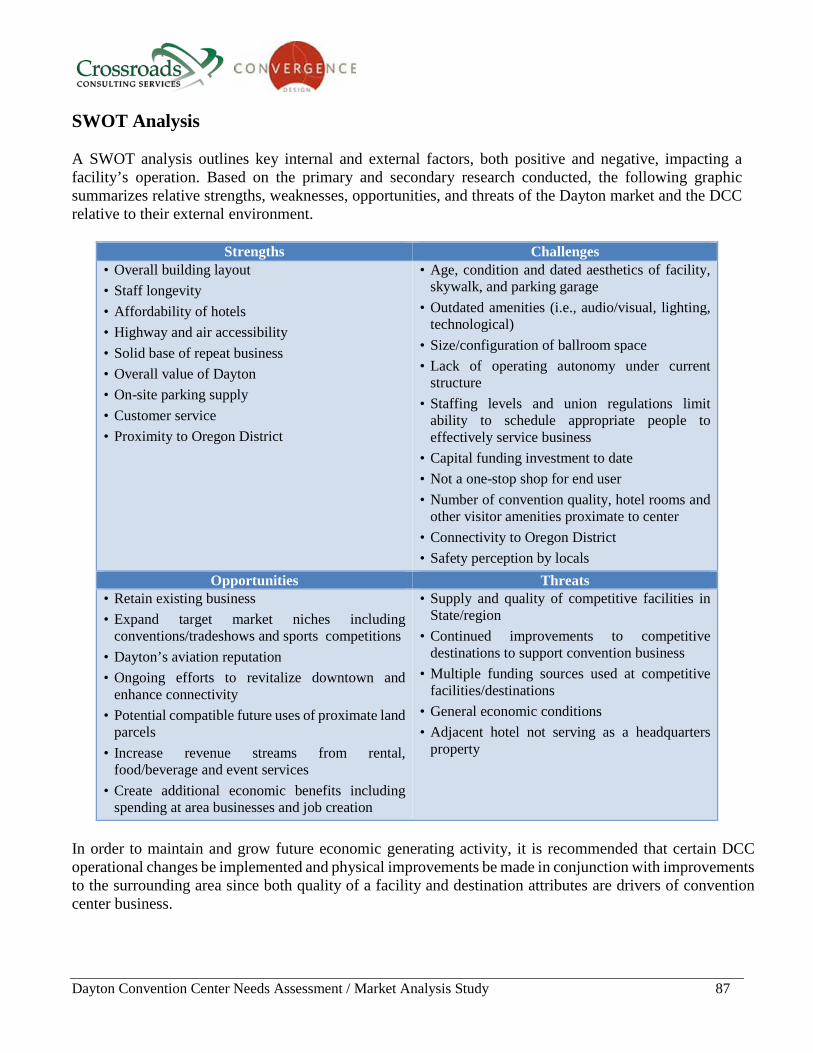

• Developed a SWOT analysis outlining strengths, weaknesses, opportunities and threats of the DCC within the context of its competitive environment.

• Prepared a prioritized, three-tiered statement of needs that addresses key issues identified in the situational overview.

• Summarized estimated project costs of the recommended renovations/enhancements and their associated return in terms of event activity, financial performance and economic/fiscal benefits.

• Identified potential funding strategies.

The remainder of this report summarizes the key findings and conclusions from our research and analysis.

Dayton Convention Center Needs Assessment / Market Analysis Study 4

Executive Summary

The project team of Crossroads Consulting, Convergence Design, and The Bigelow Companies, Inc. was retained to evaluate options for enhancements/renovations to the DCC in order to maximize its marketability, competitiveness and economic impact to the community. It is our understanding that the driving forces of any potential DCC enhancements/renovations are to maintain the financial investment and value of the existing asset, enhance downtown investments made by both the public and private sector, improve marketability that results in an increase of out-of-town group business, accommodate diverse community usage, minimize the financial operating subsidy, and maximize economic and fiscal impacts to the community.

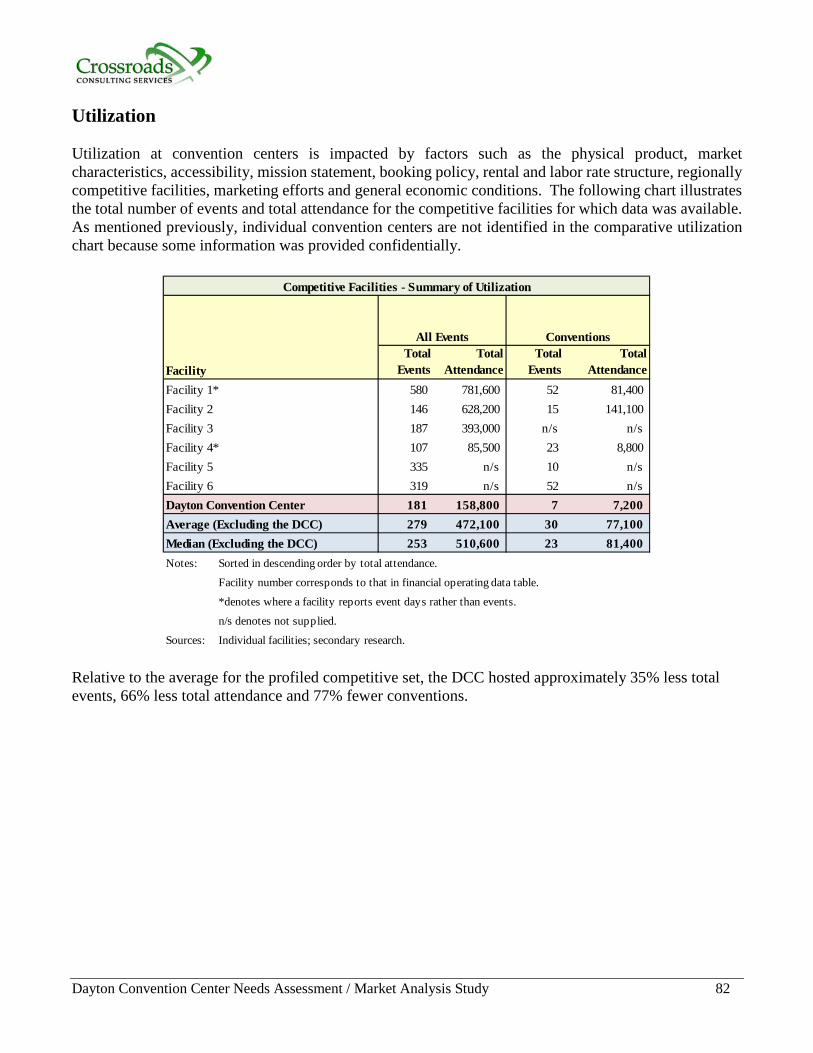

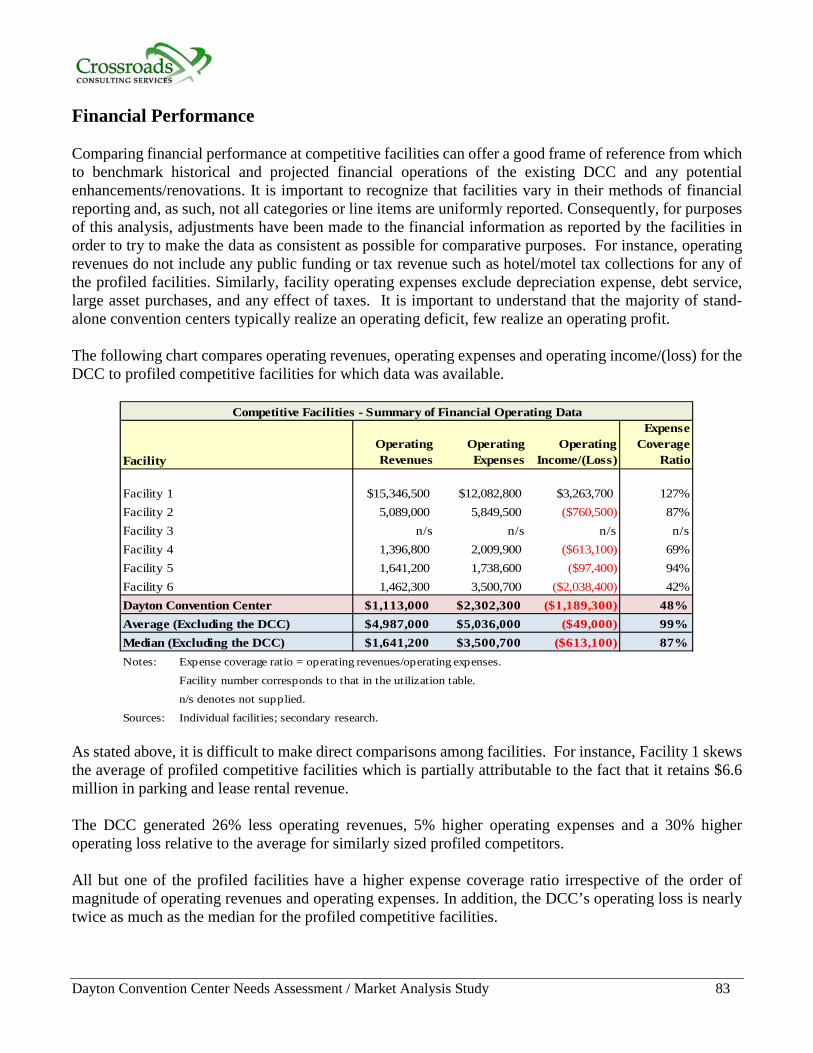

Competitive Market Overview The DCC and the City of Dayton have a number of strengths relative to attracting convention/meeting business that draws attendees from outside the local area and creates economic benefits. The facility’s layout is functional for a variety of event types including conventions, tradeshows, consumer shows, competitive sporting events, banquets, and meetings. The DCC offers a competitive supply of exhibit and meeting space and is the only facility in the State that offers a theater which provides a competitive advantage for group business that requires an auditorium setting. The DCC’s largest ballroom is constrained by its size, configuration, dated finishes, and lack of modern amenities relative to its competitive set. The DCC’s biggest external constraint is the supply of convention quality hotel rooms within walking distance. Historically, professional and trade association meeting planners have considered Dayton one of the four primary convention/tradeshow destinations in Ohio. However, the competitive landscape has changed in the past decade resulting in a loss of economic generating event activity at the DCC. Other regional competitive markets including Akron, Cincinnati, Cleveland, Columbus, and Sharonville in Ohio as well as Covington, Kentucky and Fort Wayne, Indiana have and continue to invest in facility and destination improvements to enhance their convention centers’ marketability. While some of these cities such as Cincinnati, Cleveland and Columbus offer significantly larger convention centers than the DCC, they often compete for the same business given their facilities’ flexibility to accommodate multiple, smaller groups. In addition, the past decade saw significant growth in larger meeting hotels competing for group business. Properties such as the Kalahari Hotel/Conference Center in Sandusky have been developed with group business in mind. These types of properties offer competitive advantages including offering hotel rooms on-site, controlling all the potential revenue streams such as lodging, room rental, and food/beverage service as well as offering a one-stop shop to meeting planners. These and other changes to Dayton’s competitive environment, as well as the broader convention/meeting industry, have led to more of a buyers’ market. Groups now demand a seamless booking process, high levels of customer service, and value for their business. Although customers were generally positive regarding both the DCC and Dayton, facility and destination issues are taking a toll on the DCC’s ability to book long-time, repeat users as well as new business. Groups such as the Order of the Eastern Star have chosen to leave Dayton given the state of the current building and alternative venue options in the region.

Dayton Convention Center Needs Assessment / Market Analysis Study 5

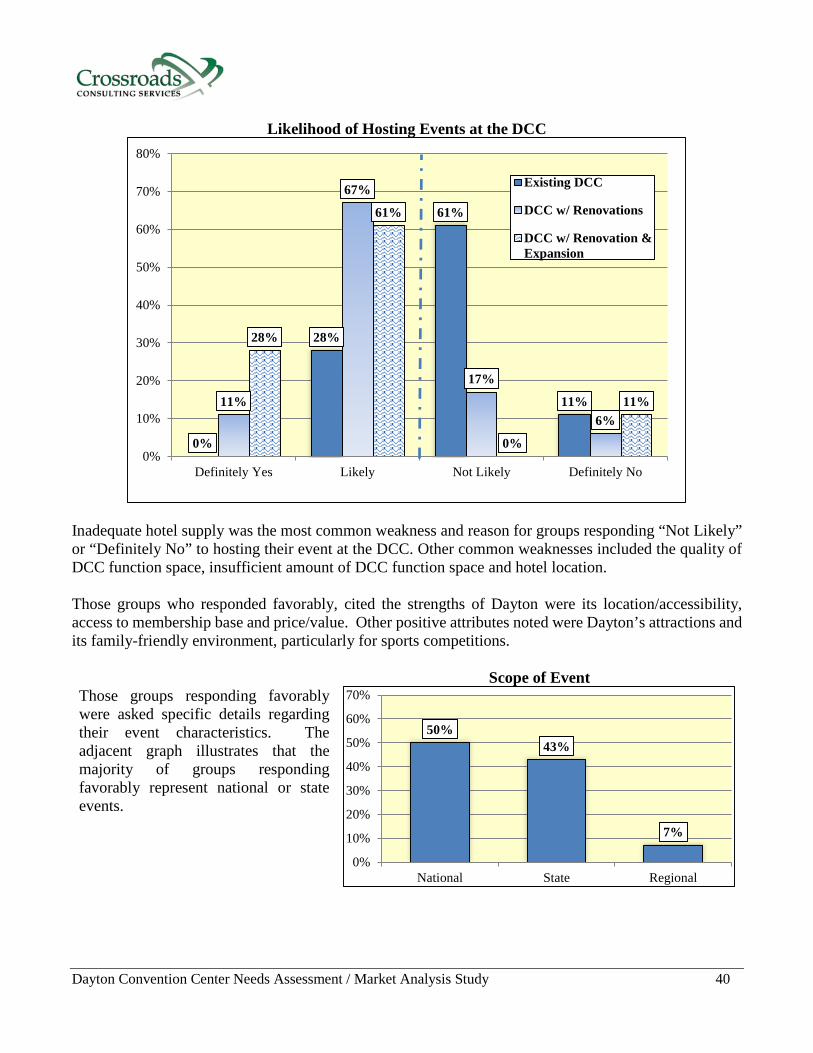

As a point of our survey effort, meeting planners were asked if they would consider meeting at the DCC under three scenarios: remains the same, is renovated/upgraded, or is renovated/upgraded and expanded. Only 28% of meeting planners responded “Definitely Yes” or “Likely” with the existing facility whereas 78% responded favorably with renovations/upgrades and 89% responded favorably with renovations/upgrades and expansion. Inadequate hotel supply was the most common weakness and reason for groups responding “Not Likely” or “Definitely No” to hosting their event at the DCC. Other common weaknesses included the quality of DCC function space, insufficient amount of DCC function space and hotel location. Other operational challenges, such as the limited number of full-time staff and a lack of operating autonomy, also hinder the DCC’s ability to effectively compete for group business. Unlike many other public facilities such as parks and libraries, convention centers operate in a constantly evolving industry where customers have multiple options from which to choose. Remaining status quo will likely result in a continued decline in convention group business and resulting economic/fiscal benefits generated by DCC event activity. The changing competitive environment as well as direct input received from past and potential DCC users suggests market demand for a renovated/enhanced DCC that offers improved aesthetics, greater space functionality, and modern amenities. This desire to return to Dayton or book new group business is driven, in part, by its strengths including location/accessibility, access to membership base and price/value. Event organizers for sports-related competitions also consider Dayton to be a family-friendly environment. Research indicates that conventions/tradeshows and sports competitions are primary market niches that present future growth opportunities. These event types should be considered a booking priority since they have the ability to produce room nights that generate positive economic impact to the area which is consistent with DCC’s mission statement. From a short-term booking perspective (e.g., inside 12 months), facility management should strive to increase the number of banquets/food functions. While these events primarily attract local attendees, they have the ability to positively impact the facility’s financial operations as they tend to be profitable.

Summary of Recommendations A review of historical operations, attributes of competitive facilities and destinations, and industry best practices as well as a comprehensive review of the existing DCC yielded recommended changes to specific operating strategies, program elements and supporting infrastructure that can better meet the expectations of users which will be imperative to the facility’s long-term success. These recommended changes should result in better event functionality, enhanced revenue generation and operating efficiency, as well as additional economic/fiscal impacts for the area. Key Operational Recommendations Although the City of Dayton owns the DCC, Montgomery County also benefits financially from out-of-town visitor spending resulting from DCC operations. Relative to ownership and governance, one option for consideration is forming an authority that has representation from both the City of Dayton and Montgomery County in order to enhance involvement from both jurisdictions. Such a change would also align ownership with a broader set of potential funding sources for ongoing operations and capital improvements.

Dayton Convention Center Needs Assessment / Market Analysis Study 6

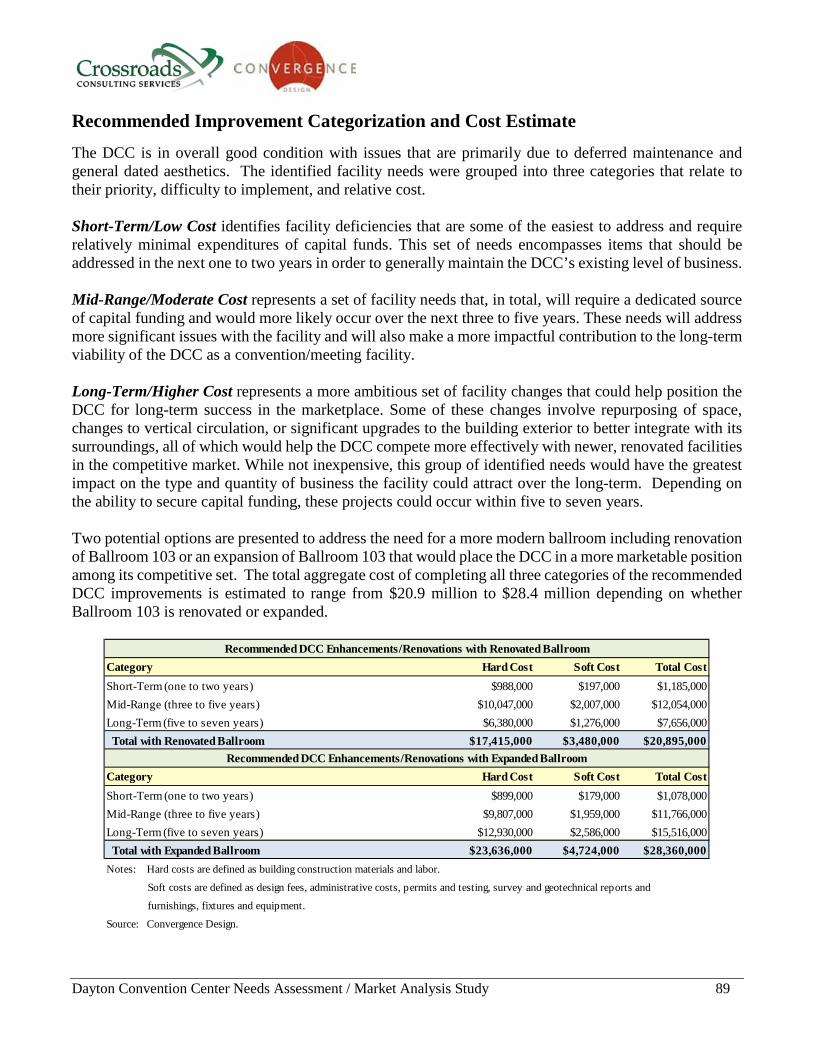

Competitive convention centers are owned and operated in a manner that provides them with greater operating autonomy than the current DCC structure as a City of Dayton department including the ability to more cost effectively service event activity. It is strongly recommended that the City of Dayton consider outsourcing management of the DCC to a third party, either a professional management company or the Dayton CVB, in order to provide greater operating autonomy and flexibility with regard to staffing, sales, contracting, and event management. Other operational recommendations include reviewing and modifying the DCC’s mission statement, operating objectives and booking policy to reflect the improved building, current competitive environment, and general industry trends. Booking parameters in terms of timing and responsibilities (e.g., facility management, Dayton CVB) should be clearly articulated along with desired outcomes. Improving marketing efforts and effectiveness with increased full-time staffing, providing incentives for DCC sales staff and enhancing joint efforts with the Dayton CVB, Crowne Plaza, and Marriott at the University of Dayton are also recommended. Recommendations related to food/beverage service include increasing DCC staff to generate short-term bookings and drive sales as well as establishing an annual capital plan to upgrade retail (concession) spaces and graphics and replacing older kitchen equipment. In order to safeguard the past and future investments in any physical improvements to the DCC, the City should develop a formal maintenance and capital improvement process/plan with a dedicated funding source. Key DCC Program Recommendations Based on factors including, but not limited to, the analysis of historical DCC operations, the competitive facility assessment and the existing facility assessment, a needs assessment was prepared. The identified facility needs were grouped into three categories, relating to their priority, difficulty to implement, and relative cost. The DCC is in overall good condition with issues that are primarily due to deferred maintenance and general dated aesthetics. Physical improvement recommendations outlined in the body of the report are prioritized as follows: Short-Term/Low Cost identifies facility deficiencies that are some of the easiest to address and require relatively minimal expenditures of capital funds. This set of needs encompasses items that should be addressed in the next one to two years in order to generally maintain the DCC’s existing level of business. Examples include improving/expanding restrooms, replacing skywalk carpet/ceiling, and upgrading elevators. Mid-Range/Moderate Cost represents a set of facility needs that, in total, will require a dedicated source of capital funding and would more likely occur over the next three to five years. These needs will address more significant issues with the facility and will also make a more impactful contribution to the long-term viability of the DCC as a convention/meeting facility. Examples include replacing telescopic seating, renovating the skywalk to the parking garage to create a positive arrival experience, adding a third passenger elevator, replacing north roof segments and skylight, and repurposing theater dressing rooms as locker rooms.

Dayton Convention Center Needs Assessment / Market Analysis Study 7

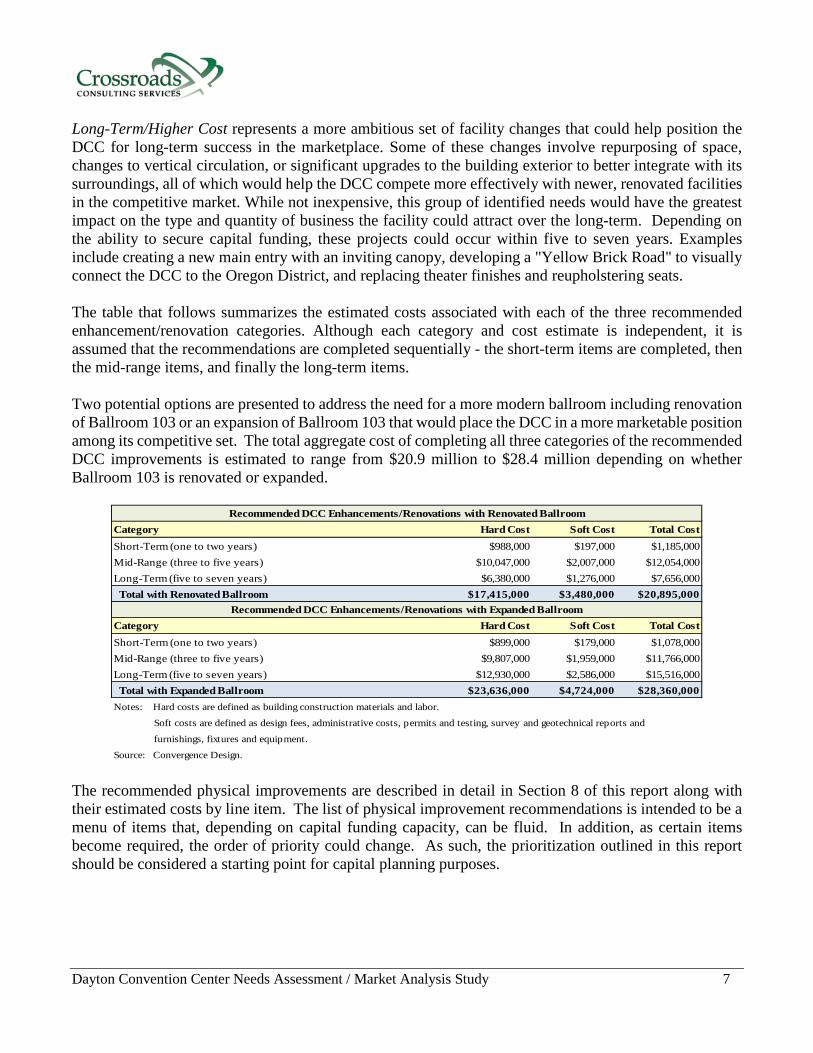

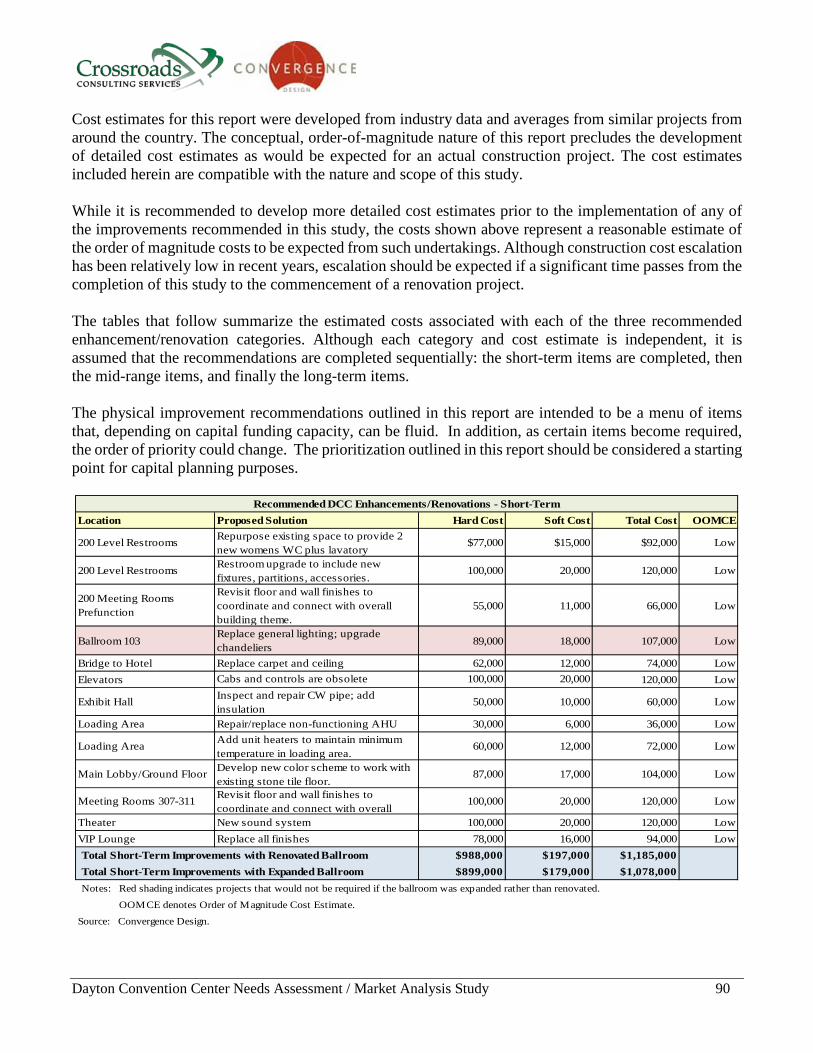

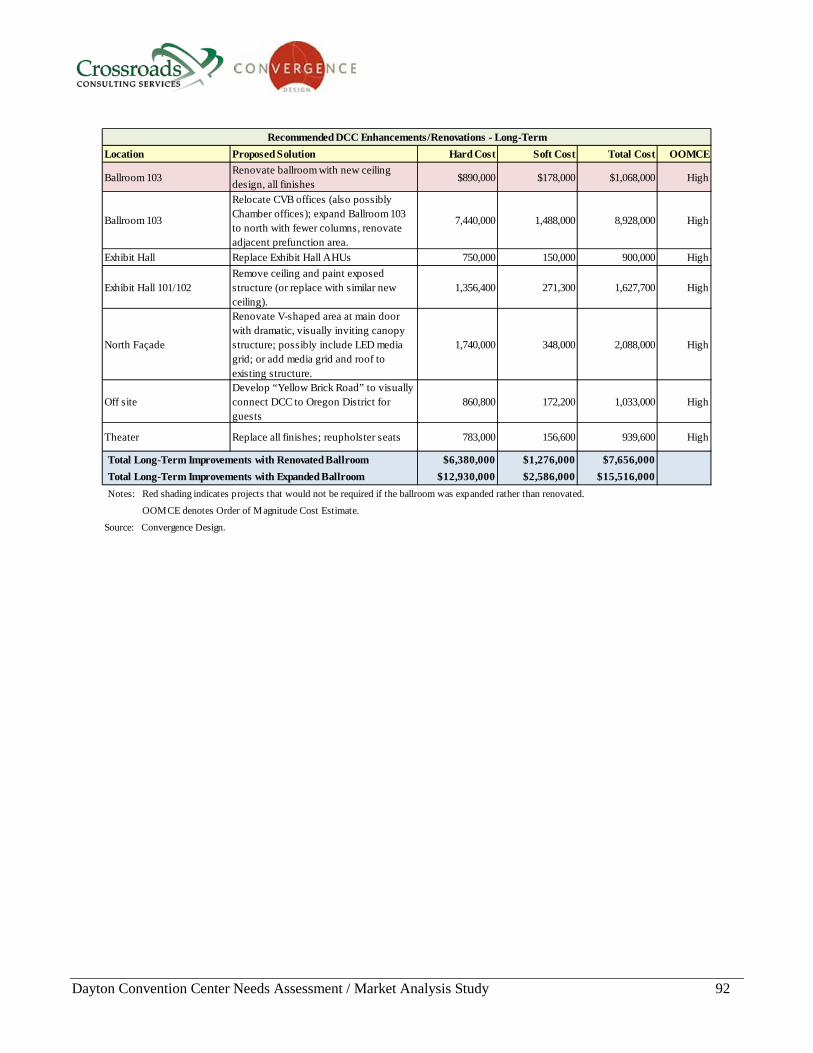

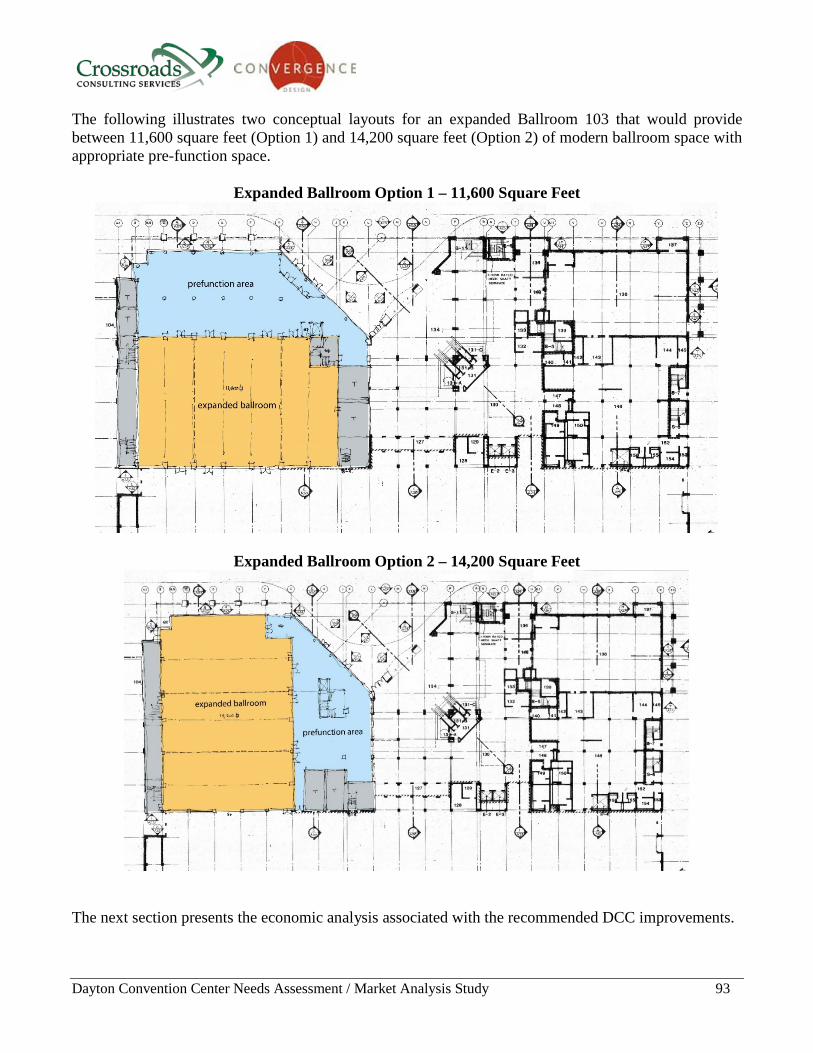

Long-Term/Higher Cost represents a more ambitious set of facility changes that could help position the DCC for long-term success in the marketplace. Some of these changes involve repurposing of space, changes to vertical circulation, or significant upgrades to the building exterior to better integrate with its surroundings, all of which would help the DCC compete more effectively with newer, renovated facilities in the competitive market. While not inexpensive, this group of identified needs would have the greatest impact on the type and quantity of business the facility could attract over the long-term. Depending on the ability to secure capital funding, these projects could occur within five to seven years. Examples include creating a new main entry with an inviting canopy, developing a "Yellow Brick Road" to visually connect the DCC to the Oregon District, and replacing theater finishes and reupholstering seats. The table that follows summarizes the estimated costs associated with each of the three recommended enhancement/renovation categories. Although each category and cost estimate is independent, it is assumed that the recommendations are completed sequentially - the short-term items are completed, then the mid-range items, and finally the long-term items. Two potential options are presented to address the need for a more modern ballroom including renovation of Ballroom 103 or an expansion of Ballroom 103 that would place the DCC in a more marketable position among its competitive set. The total aggregate cost of completing all three categories of the recommended DCC improvements is estimated to range from $20.9 million to $28.4 million depending on whether Ballroom 103 is renovated or expanded.

Category Hard Cost Soft Cost Total CostShort-Term (one to two years) $988,000 $197,000 $1,185,000Mid-Range (three to five years) $10,047,000 $2,007,000 $12,054,000Long-Term (five to seven years) $6,380,000 $1,276,000 $7,656,000 Total with Renovated Ballroom $17,415,000 $3,480,000 $20,895,000

Category Hard Cost Soft Cost Total CostShort-Term (one to two years) $899,000 $179,000 $1,078,000Mid-Range (three to five years) $9,807,000 $1,959,000 $11,766,000Long-Term (five to seven years) $12,930,000 $2,586,000 $15,516,000 Total with Expanded Ballroom $23,636,000 $4,724,000 $28,360,000Notes: Hard costs are defined as building construction materials and labor.

Soft costs are defined as design fees, administrative costs, permits and testing, survey and geotechnical reports and

furnishings, fixtures and equipment.

Source: Convergence Design.

Recommended DCC Enhancements/Renovations with Renovated Ballroom

Recommended DCC Enhancements/Renovations with Expanded Ballroom

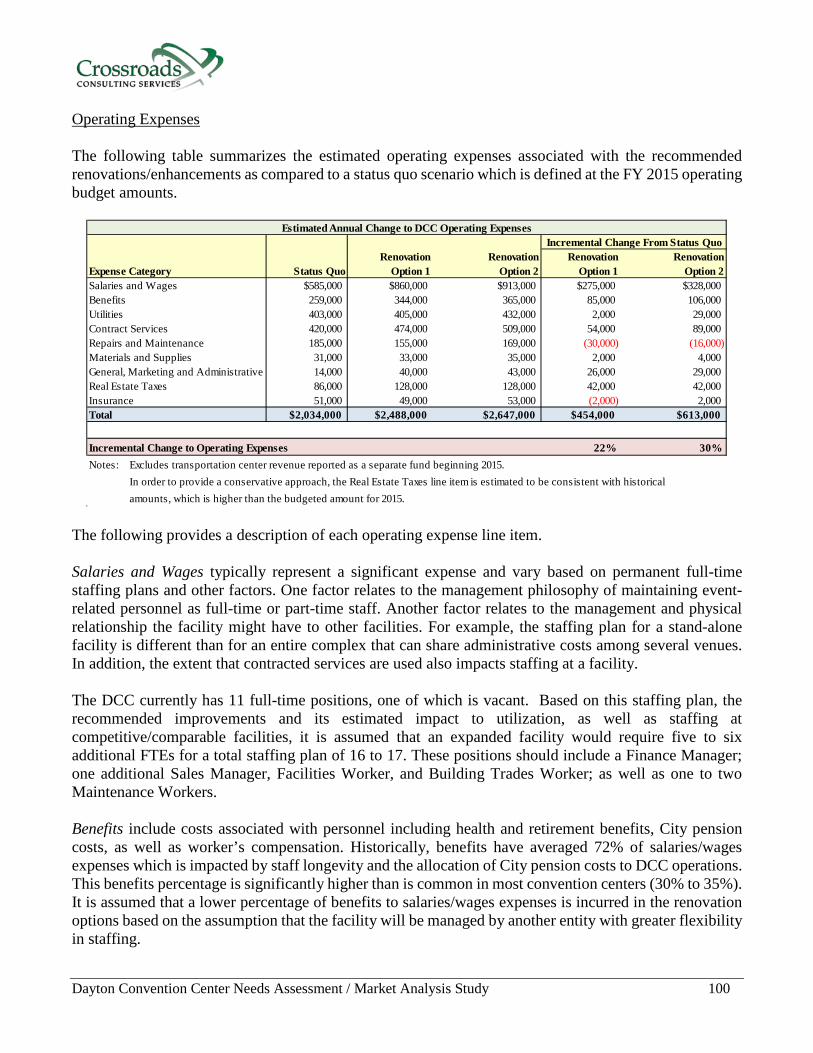

The recommended physical improvements are described in detail in Section 8 of this report along with their estimated costs by line item. The list of physical improvement recommendations is intended to be a menu of items that, depending on capital funding capacity, can be fluid. In addition, as certain items become required, the order of priority could change. As such, the prioritization outlined in this report should be considered a starting point for capital planning purposes.

Dayton Convention Center Needs Assessment / Market Analysis Study 8

Key Supporting Infrastructure Recommendations As mentioned previously, competitive destinations including Cincinnati, Cleveland, Columbus and Sharonville have made, or are currently making, improvements to their visitor amenities surrounding their respective convention centers. These include new hotel developments, streetscape improvements, and the creation of a vibrant convention center district to capture visitor spending. It is recommended that the City of Dayton actively advocate, and possibly provide incentives, for private investment in the area surrounding the DCC including additional convention quality hotels, restaurants, and retail establishments. Efforts should also be made to enhance connectivity between the DCC and Oregon District that is more pedestrian friendly/inviting to attendees. While these external improvements may be outside the direct control of the City of Dayton, it should take an active role working with other stakeholders such as the Downtown Dayton Partnership, the Dayton Development Coalition, the Oregon District and the private sector to garner support for such developments.

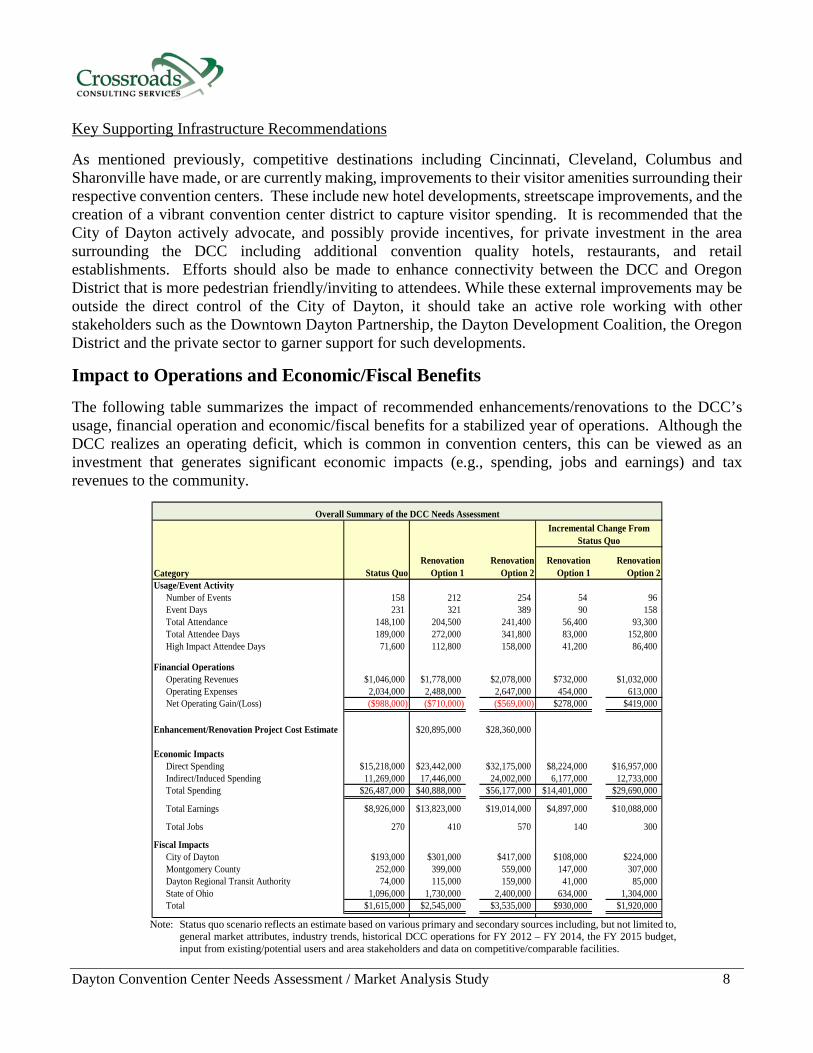

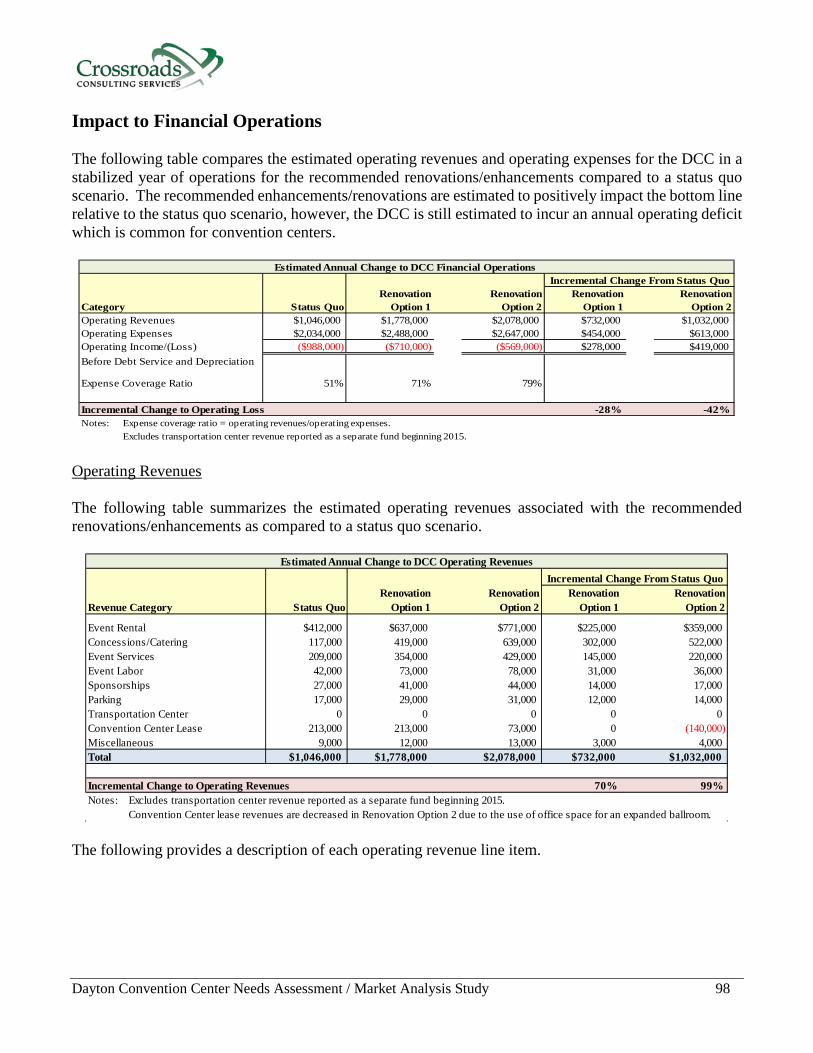

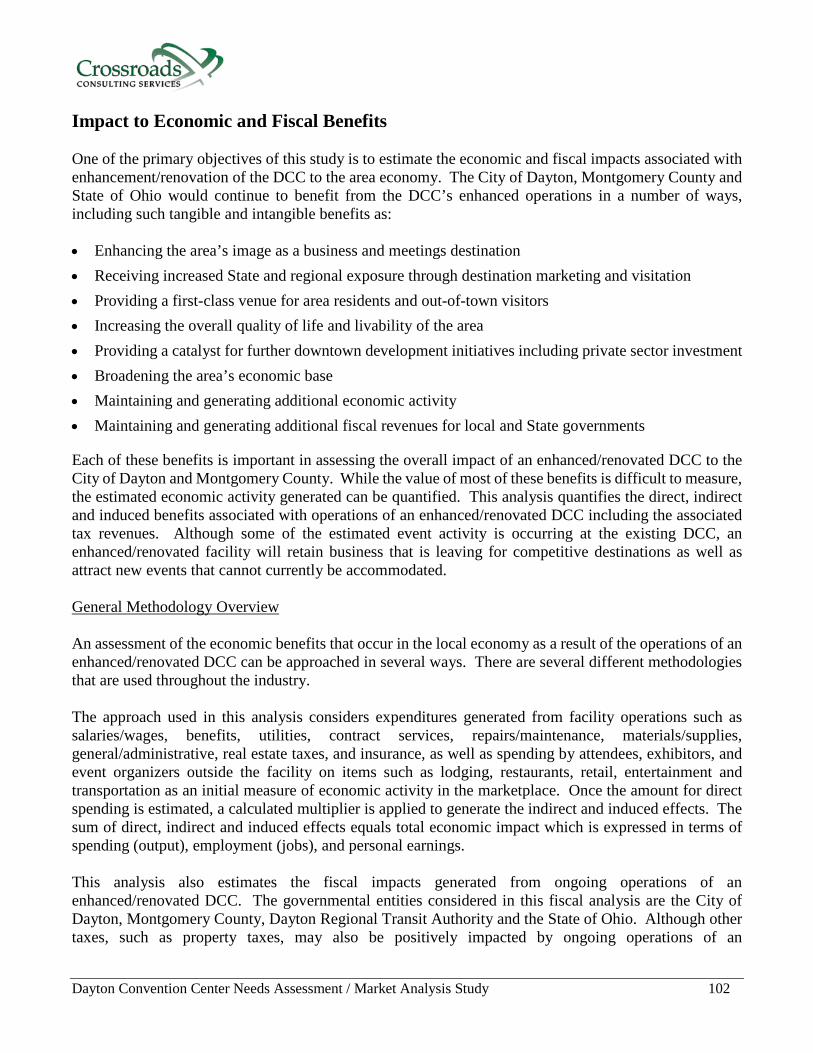

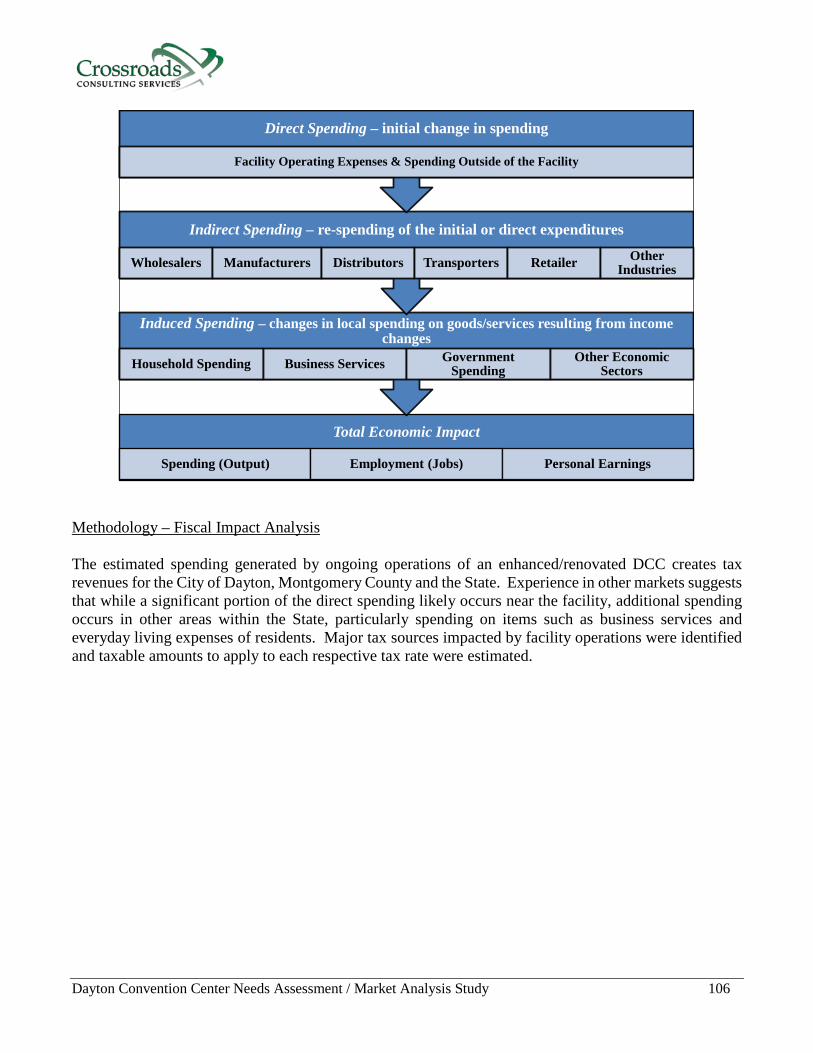

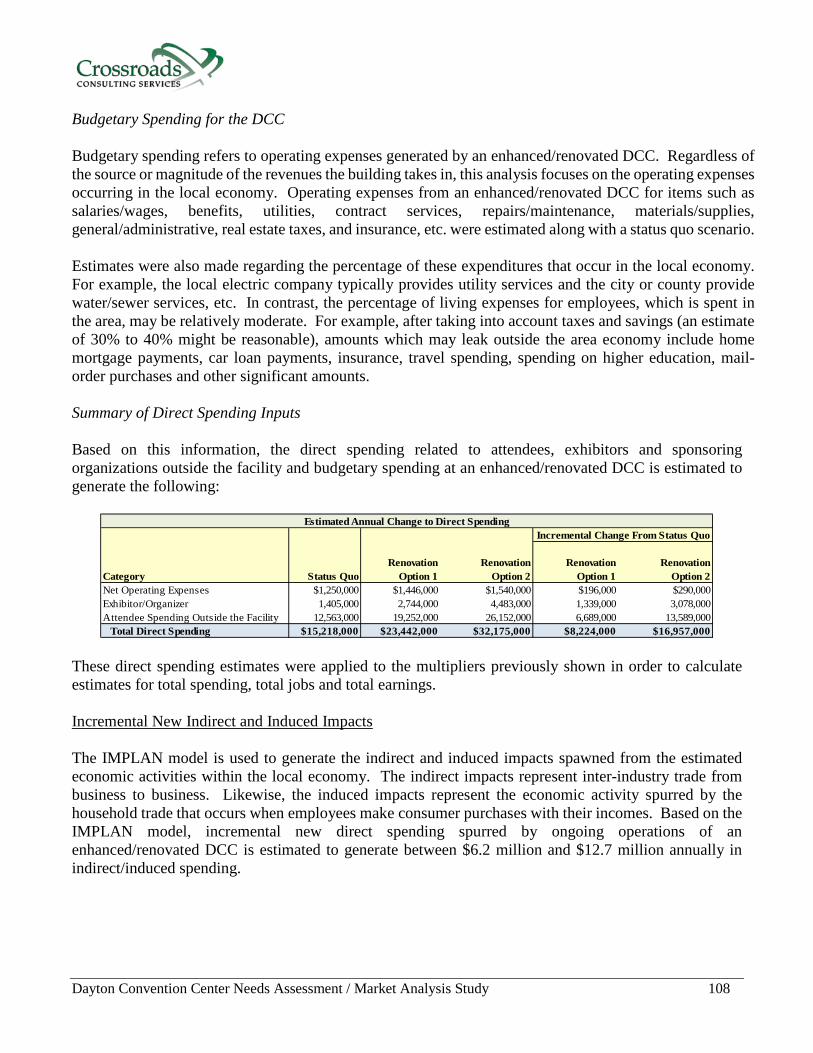

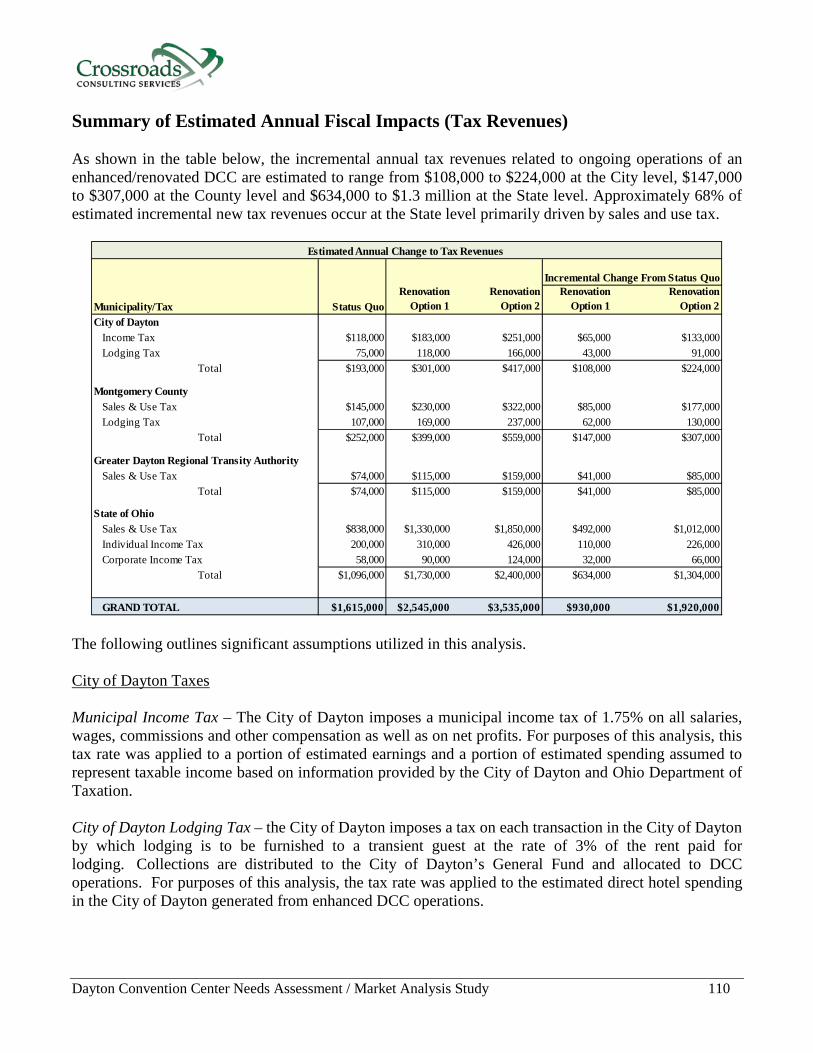

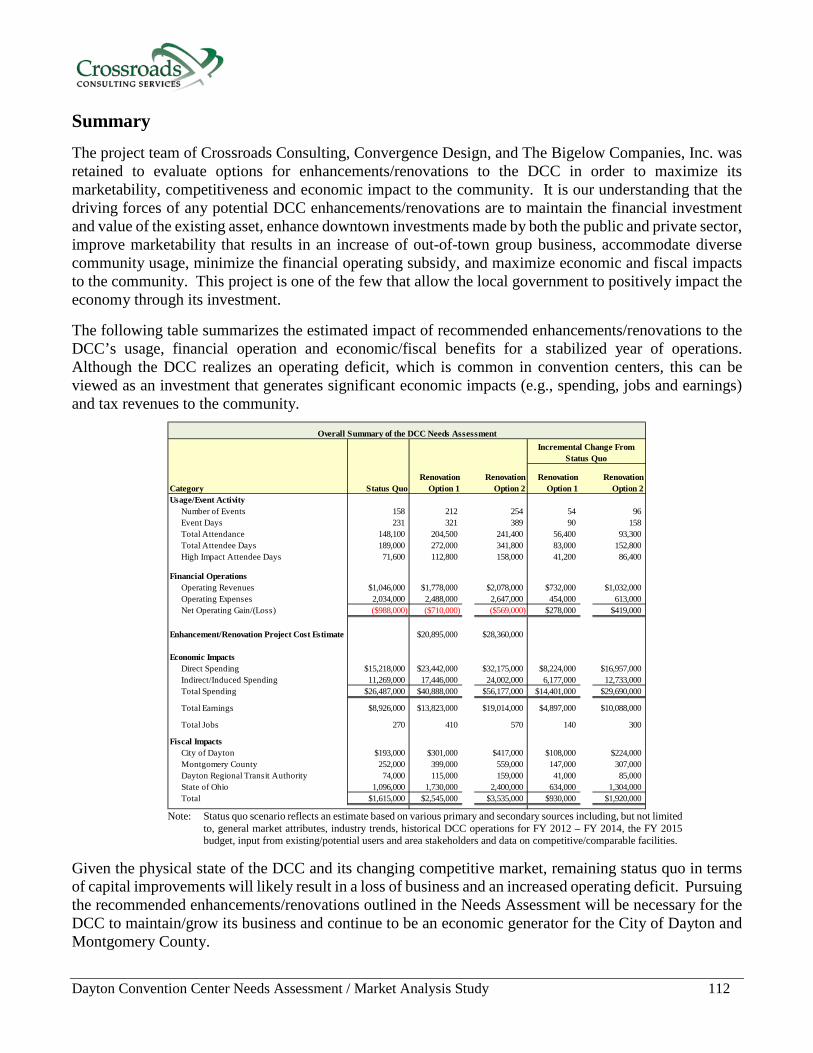

Impact to Operations and Economic/Fiscal Benefits The following table summarizes the impact of recommended enhancements/renovations to the DCC’s usage, financial operation and economic/fiscal benefits for a stabilized year of operations. Although the DCC realizes an operating deficit, which is common in convention centers, this can be viewed as an investment that generates significant economic impacts (e.g., spending, jobs and earnings) and tax revenues to the community.

Category Status QuoRenovation

Option 1Renovation

Option 2Renovation

Option 1Renovation

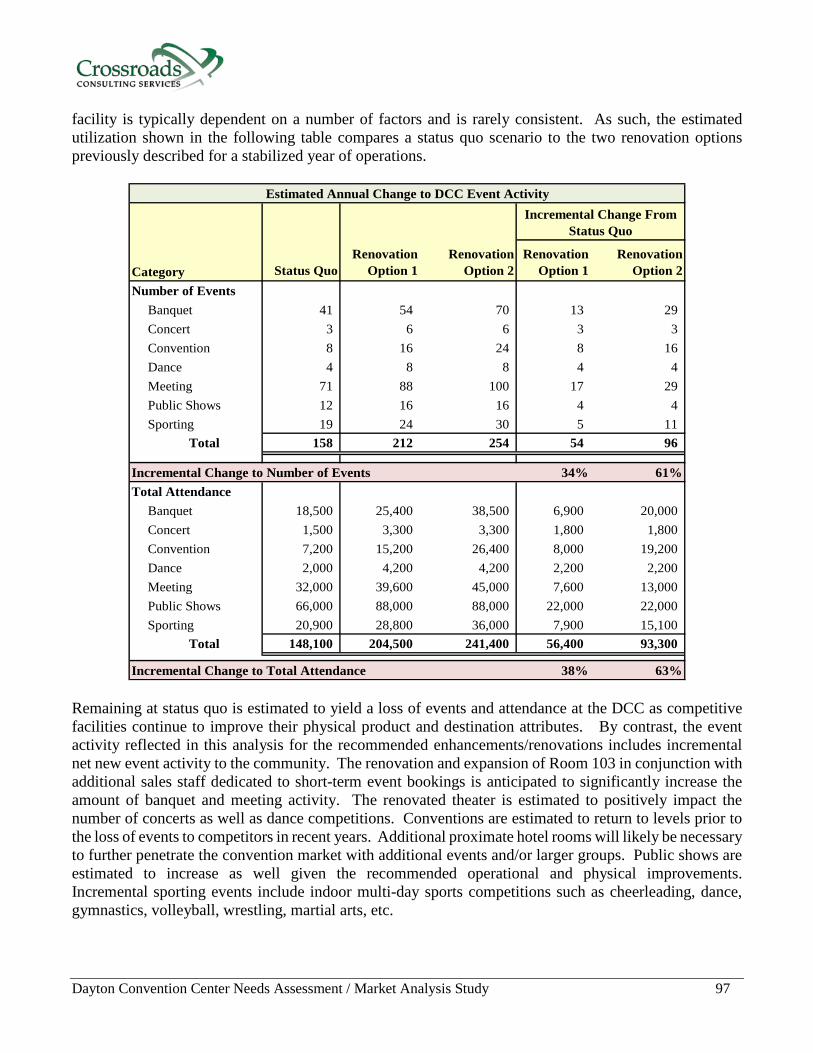

Option 2Usage/Event Activity

Number of Events 158 212 254 54 96Event Days 231 321 389 90 158Total Attendance 148,100 204,500 241,400 56,400 93,300Total Attendee Days 189,000 272,000 341,800 83,000 152,800High Impact Attendee Days 71,600 112,800 158,000 41,200 86,400

Financial OperationsOperating Revenues $1,046,000 $1,778,000 $2,078,000 $732,000 $1,032,000Operating Expenses 2,034,000 2,488,000 2,647,000 454,000 613,000Net Operating Gain/(Loss) ($988,000) ($710,000) ($569,000) $278,000 $419,000

Enhancement/Renovation Project Cost Estimate $20,895,000 $28,360,000

Economic Impacts Direct Spending $15,218,000 $23,442,000 $32,175,000 $8,224,000 $16,957,000Indirect/Induced Spending 11,269,000 17,446,000 24,002,000 6,177,000 12,733,000Total Spending $26,487,000 $40,888,000 $56,177,000 $14,401,000 $29,690,000

Total Earnings $8,926,000 $13,823,000 $19,014,000 $4,897,000 $10,088,000

Total Jobs 270 410 570 140 300

Fiscal Impacts City of Dayton $193,000 $301,000 $417,000 $108,000 $224,000Montgomery County 252,000 399,000 559,000 147,000 307,000Dayton Regional Transit Authority 74,000 115,000 159,000 41,000 85,000State of Ohio 1,096,000 1,730,000 2,400,000 634,000 1,304,000Total $1,615,000 $2,545,000 $3,535,000 $930,000 $1,920,000

Overall Summary of the DCC Needs AssessmentIncremental Change From

Status Quo

Note: Status quo scenario reflects an estimate based on various primary and secondary sources including, but not limited to,

general market attributes, industry trends, historical DCC operations for FY 2012 – FY 2014, the FY 2015 budget, input from existing/potential users and area stakeholders and data on competitive/comparable facilities.

Dayton Convention Center Needs Assessment / Market Analysis Study 9

Given the physical state of the DCC and its changing competitive market, remaining status quo in terms of capital improvements will likely result in a loss of business and an increased operating deficit. For purposes of this analysis, the status quo scenario assumes that no major capital improvements are made to the DCC and that the facility continues to be operated as a division within the City of Dayton’s Recreation and Youth Services Department. Renovation Option 1 assumes that all the recommended operational and physical improvements are made and that Ballroom 103 is renovated rather than expanded. Renovation Option 2 assumes all recommended operational and physical improvements are made and that Ballroom 103 is expanded. In addition, Renovation Option 2 assumes that additional proximate, convention quality hotels are developed that can service larger conventions. Pursuing the recommended enhancements/renovations outlined in this report will be necessary for the DCC to maintain/grow its business and continue to be a significant economic generator for the City of Dayton and Montgomery County.

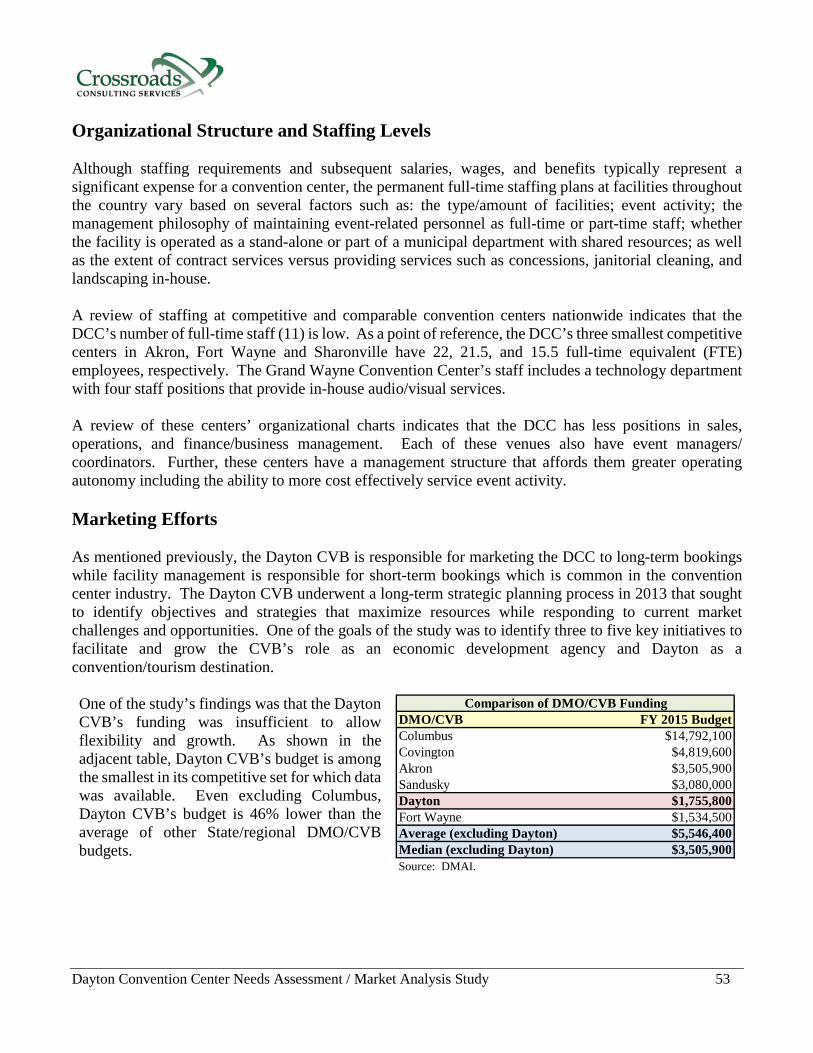

Potential Funding Sources Improving the DCC from a physical perspective alone will not allow Dayton to effectively compete in the long-term for convention/meeting business that draws out-of-town visitors. Rather, a combined effort that addresses the building’s physical needs and operational challenges, modernizes its amenities, and enhances supporting elements of the surrounding location (i.e., streetscape improvements; additional hotel, restaurant, retail and entertainment establishments) will place Dayton in a more competitive position. In addition, a strategy that increases sales and marketing efforts will need to be implemented which will require more funding both at the DCC for short-term bookings and at the Dayton CVB for long-term bookings. Currently, there are virtually no dedicated marketing funds in the DCC’s operating budget and the Dayton CVB’s budget is among the smallest in its competitive set. These combined internal and external improvements will serve to retain existing DCC-related visitors, expand its target markets, and capture more spending and resulting economic and fiscal impacts generated by those visitors. Montgomery County used lodging tax revenues to fund the DCC’s debt service until 2013 when the debt was retired. Convention centers in Cincinnati, Cleveland, Columbus and Sharonville have been built, renovated, and/or expanded with the financial support of their respective counties. Each of these counties dedicate a portion of their hotel/motel tax collections to debt service and/or ongoing operations and capital improvements to the convention center located in their primary municipality recognizing the economic value of these investments. Based on input from City of Dayton and Montgomery County officials, one potential public funding source for future DCC improvements could be an increase in the County lodging tax. Based on annual collections over the past three years, a one-point increase could potentially generate approximately $900,000 annually. One benefit of increasing the lodging tax is that this cost is borne by visitors, not area residents, and the DCC should be considered an investment in Dayton’s economy. Also, an increased lodging tax rate should not negatively impact Dayton’s competitive position since, even with a modest increase, the City of Dayton would still have one of the lowest total tax rates on hotels among competitive destinations.

Dayton Convention Center Needs Assessment / Market Analysis Study 10

Other potential public funding sources include a Tax Increment Financing District and/or a Tourism Improvement District where funds generated within an established district can be dedicated to physical improvements as well as enhanced marketing efforts. The DCC is not currently in a defined taxing district but potential exists to create one and should be considered in the overall financing plan. Remaining status quo will have a detrimental impact on the City of Dayton as well as hoteliers, restaurateurs, and other area businesses if DCC event activity continues to decline. Any investment requires a substantial commitment but one that would result in a direct, long-term return. Significant public and private investments have been made in the DCC and downtown Dayton in the past. An ongoing effort to continue to invest in the DCC and to improve the area’s visitor amenities will better position the community to effectively compete for convention/meeting activity that can support its long-term objectives including revitalizing downtown, generating economic benefits, and providing space for local event activity. Potential Next Steps A facility assessment/economic analysis is an initial step in any planning process. Renovating/enhancing the DCC will require detailed proactive and strategic planning to maximize operational opportunities and mitigate potential physical programmatic issues. Potential next steps include: • Exploring potential changes to ownership and operating structure.

• Identifying potential financing strategy and related timeline.

• Securing funding to conduct more detailed site and architectural planning studies that could include, but not be limited to, developing a more detailed spatial program and further refining the preferred renovation option construction cost estimates.

• Addressing other renovation/enhancement related issues such minimizing disruption to the existing DCC and assessing the impact to future bookings.

• Developing a strategic plan for future land uses of surrounding parcels to accommodate long-term development of supporting amenities such as another convention quality hotel or potential expansion of the Crowne Plaza’s room supply.

Because the information presented in the executive summary is extracted from the more detailed report, it is important for the reader to review the report in its entirety in order to gain a better understanding of the research, methodology and assumptions used.

Dayton Convention Center Needs Assessment / Market Analysis Study 11

Table of Contents

1 Introduction and Executive Summary 1 2 General Market Overview 11 3 Key Industry Trends 20 4 Historical Facility Operations 27 5 General Management Practices Assessment 47 6 Physical Facility Assessment 57 7 Competitive Facility Assessment 71 8 Needs Assessment 85 9 Economic Analysis 94

10 Funding Analysis 113

11 Limiting Conditions and Assumptions 120

12 Appendix 122

Dayton Convention Center Needs Assessment / Market Analysis Study 12

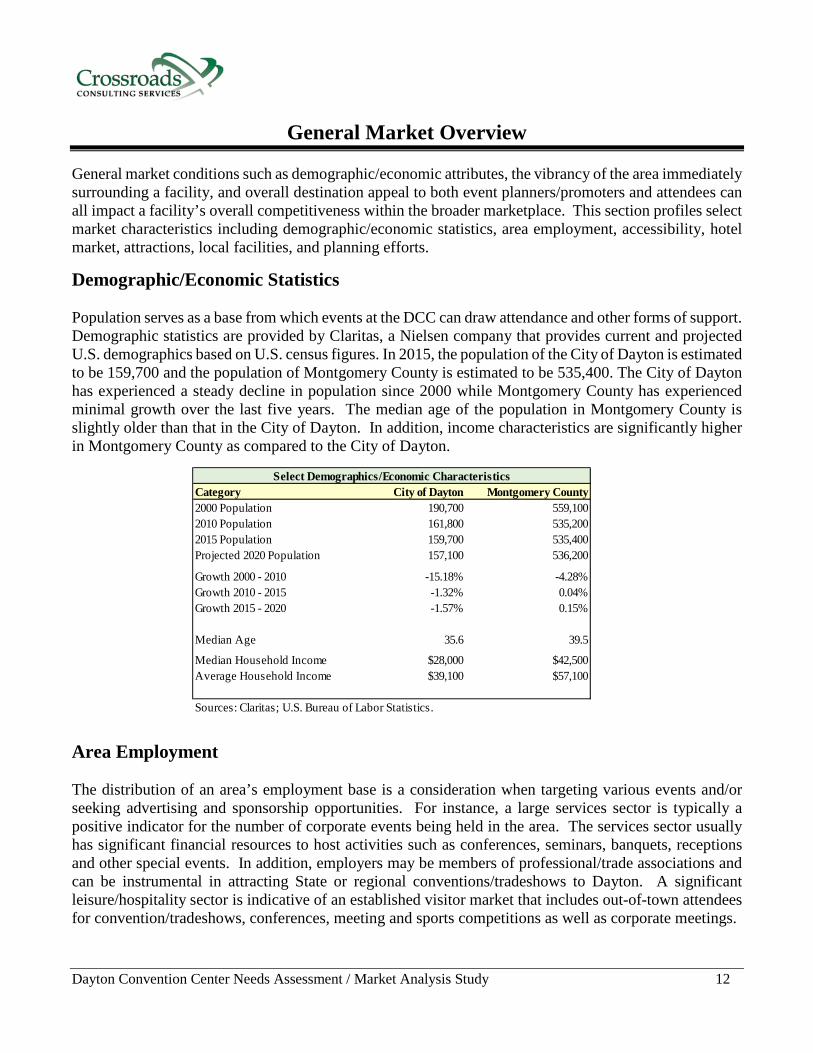

General Market Overview

General market conditions such as demographic/economic attributes, the vibrancy of the area immediately surrounding a facility, and overall destination appeal to both event planners/promoters and attendees can all impact a facility’s overall competitiveness within the broader marketplace. This section profiles select market characteristics including demographic/economic statistics, area employment, accessibility, hotel market, attractions, local facilities, and planning efforts.

Demographic/Economic Statistics Population serves as a base from which events at the DCC can draw attendance and other forms of support. Demographic statistics are provided by Claritas, a Nielsen company that provides current and projected U.S. demographics based on U.S. census figures. In 2015, the population of the City of Dayton is estimated to be 159,700 and the population of Montgomery County is estimated to be 535,400. The City of Dayton has experienced a steady decline in population since 2000 while Montgomery County has experienced minimal growth over the last five years. The median age of the population in Montgomery County is slightly older than that in the City of Dayton. In addition, income characteristics are significantly higher in Montgomery County as compared to the City of Dayton.

Category City of Dayton Montgomery County2000 Population 190,700 559,1002010 Population 161,800 535,2002015 Population 159,700 535,400Projected 2020 Population 157,100 536,200

Growth 2000 - 2010 -15.18% -4.28%Growth 2010 - 2015 -1.32% 0.04%Growth 2015 - 2020 -1.57% 0.15%

Median Age 35.6 39.5

Median Household Income $28,000 $42,500Average Household Income $39,100 $57,100

Sources: Claritas; U.S. Bureau of Labor Statistics.

Select Demographics/Economic Characteristics

Area Employment The distribution of an area’s employment base is a consideration when targeting various events and/or seeking advertising and sponsorship opportunities. For instance, a large services sector is typically a positive indicator for the number of corporate events being held in the area. The services sector usually has significant financial resources to host activities such as conferences, seminars, banquets, receptions and other special events. In addition, employers may be members of professional/trade associations and can be instrumental in attracting State or regional conventions/tradeshows to Dayton. A significant leisure/hospitality sector is indicative of an established visitor market that includes out-of-town attendees for convention/tradeshows, conferences, meeting and sports competitions as well as corporate meetings.

Dayton Convention Center Needs Assessment / Market Analysis Study 13

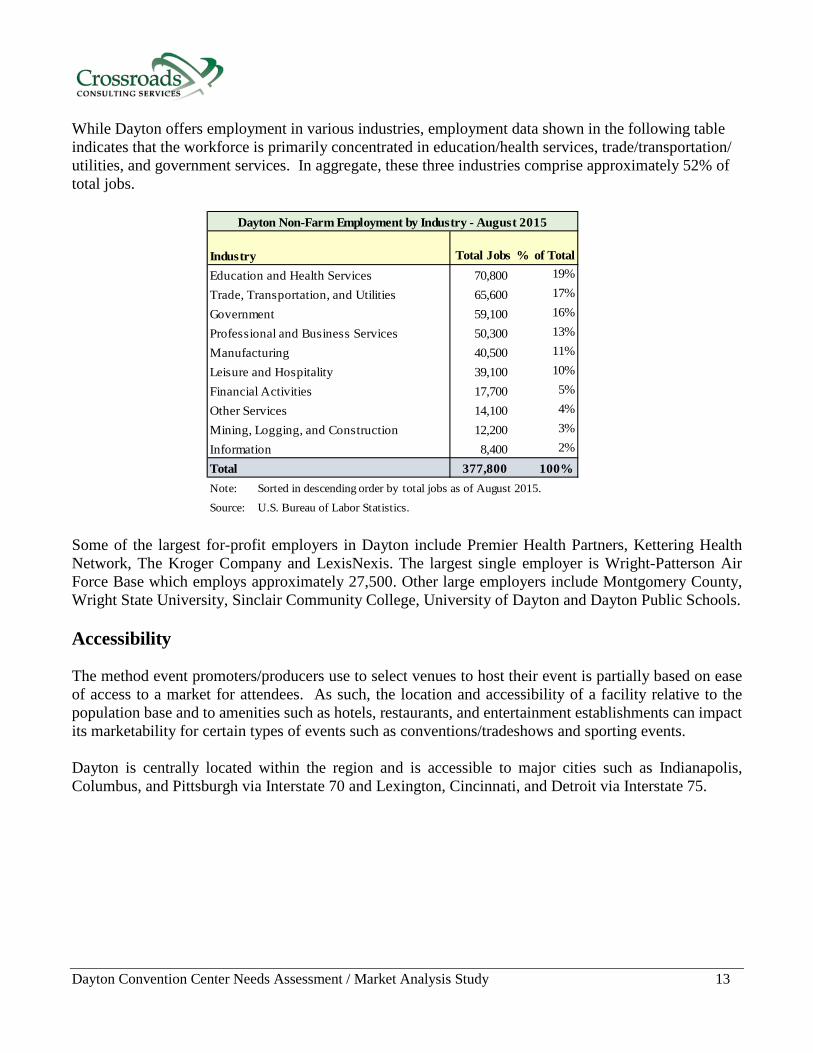

While Dayton offers employment in various industries, employment data shown in the following table indicates that the workforce is primarily concentrated in education/health services, trade/transportation/ utilities, and government services. In aggregate, these three industries comprise approximately 52% of total jobs.

Industry Total Jobs % of TotalEducation and Health Services 70,800 19%

Trade, Transportation, and Utilities 65,600 17%

Government 59,100 16%

Professional and Business Services 50,300 13%

Manufacturing 40,500 11%

Leisure and Hospitality 39,100 10%

Financial Activities 17,700 5%

Other Services 14,100 4%

Mining, Logging, and Construction 12,200 3%

Information 8,400 2%

Total 377,800 100%Note: Sorted in descending order by total jobs as of August 2015.

Source: U.S. Bureau of Labor Statistics.

Dayton Non-Farm Employment by Industry - August 2015

Some of the largest for-profit employers in Dayton include Premier Health Partners, Kettering Health Network, The Kroger Company and LexisNexis. The largest single employer is Wright-Patterson Air Force Base which employs approximately 27,500. Other large employers include Montgomery County, Wright State University, Sinclair Community College, University of Dayton and Dayton Public Schools. Accessibility The method event promoters/producers use to select venues to host their event is partially based on ease of access to a market for attendees. As such, the location and accessibility of a facility relative to the population base and to amenities such as hotels, restaurants, and entertainment establishments can impact its marketability for certain types of events such as conventions/tradeshows and sporting events. Dayton is centrally located within the region and is accessible to major cities such as Indianapolis, Columbus, and Pittsburgh via Interstate 70 and Lexington, Cincinnati, and Detroit via Interstate 75.

Dayton Convention Center Needs Assessment / Market Analysis Study 14

Vehicular Access

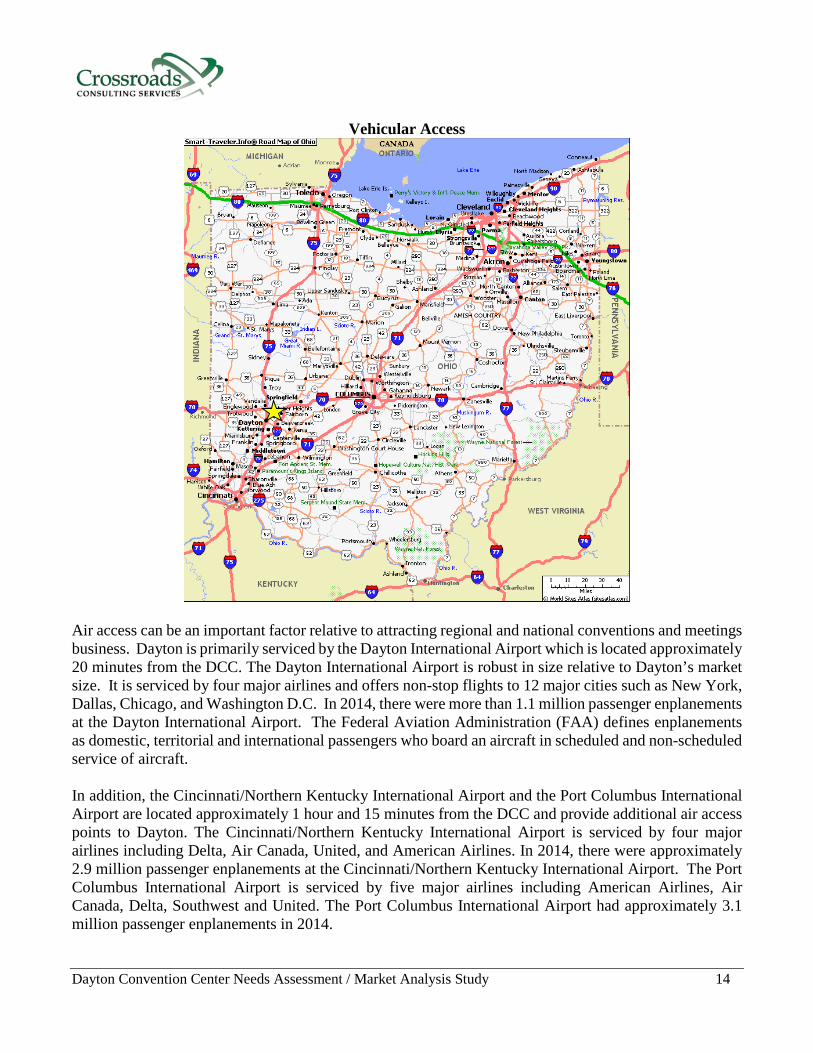

Air access can be an important factor relative to attracting regional and national conventions and meetings business. Dayton is primarily serviced by the Dayton International Airport which is located approximately 20 minutes from the DCC. The Dayton International Airport is robust in size relative to Dayton’s market size. It is serviced by four major airlines and offers non-stop flights to 12 major cities such as New York, Dallas, Chicago, and Washington D.C. In 2014, there were more than 1.1 million passenger enplanements at the Dayton International Airport. The Federal Aviation Administration (FAA) defines enplanements as domestic, territorial and international passengers who board an aircraft in scheduled and non-scheduled service of aircraft. In addition, the Cincinnati/Northern Kentucky International Airport and the Port Columbus International Airport are located approximately 1 hour and 15 minutes from the DCC and provide additional air access points to Dayton. The Cincinnati/Northern Kentucky International Airport is serviced by four major airlines including Delta, Air Canada, United, and American Airlines. In 2014, there were approximately 2.9 million passenger enplanements at the Cincinnati/Northern Kentucky International Airport. The Port Columbus International Airport is serviced by five major airlines including American Airlines, Air Canada, Delta, Southwest and United. The Port Columbus International Airport had approximately 3.1 million passenger enplanements in 2014.

Dayton Convention Center Needs Assessment / Market Analysis Study 15

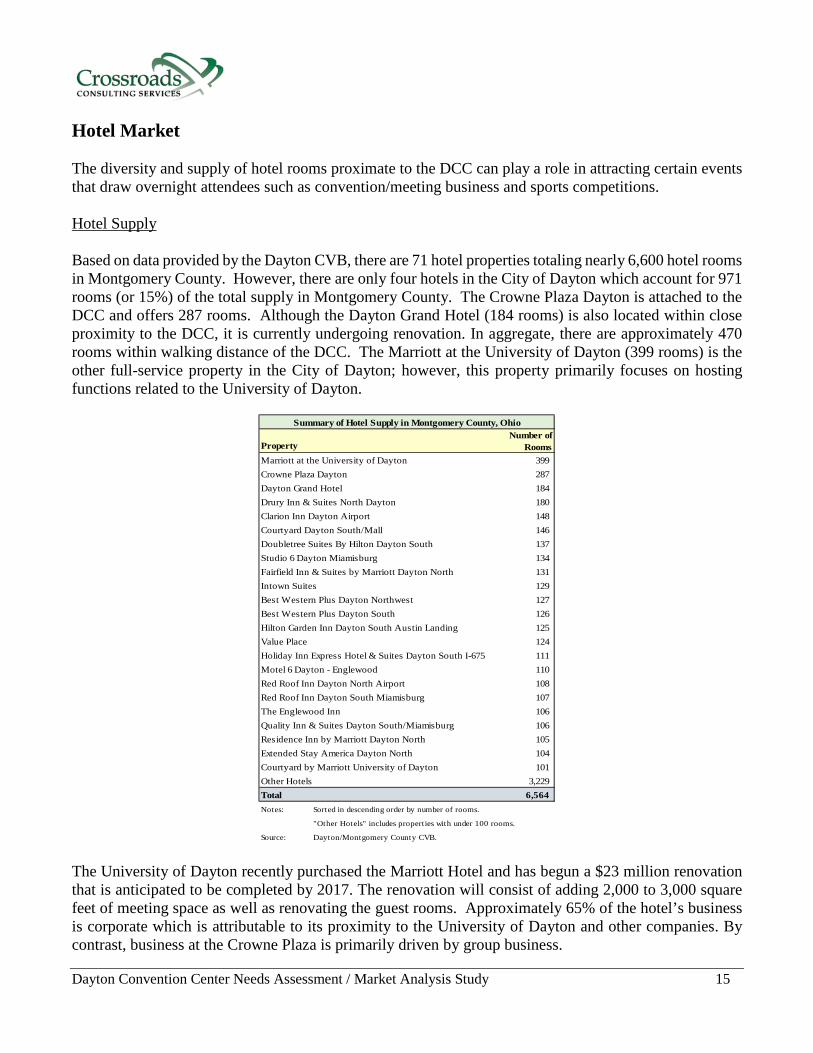

Hotel Market The diversity and supply of hotel rooms proximate to the DCC can play a role in attracting certain events that draw overnight attendees such as convention/meeting business and sports competitions. Hotel Supply Based on data provided by the Dayton CVB, there are 71 hotel properties totaling nearly 6,600 hotel rooms in Montgomery County. However, there are only four hotels in the City of Dayton which account for 971 rooms (or 15%) of the total supply in Montgomery County. The Crowne Plaza Dayton is attached to the DCC and offers 287 rooms. Although the Dayton Grand Hotel (184 rooms) is also located within close proximity to the DCC, it is currently undergoing renovation. In aggregate, there are approximately 470 rooms within walking distance of the DCC. The Marriott at the University of Dayton (399 rooms) is the other full-service property in the City of Dayton; however, this property primarily focuses on hosting functions related to the University of Dayton.

PropertyNumber of

RoomsMarriott at the University of Dayton 399 Crowne Plaza Dayton 287 Dayton Grand Hotel 184 Drury Inn & Suites North Dayton 180 Clarion Inn Dayton Airport 148 Courtyard Dayton South/Mall 146 Doubletree Suites By Hilton Dayton South 137 Studio 6 Dayton Miamisburg 134 Fairfield Inn & Suites by Marriott Dayton North 131 Intown Suites 129 Best Western Plus Dayton Northwest 127 Best Western Plus Dayton South 126 Hilton Garden Inn Dayton South Austin Landing 125 Value Place 124 Holiday Inn Express Hotel & Suites Dayton South I-675 111 Motel 6 Dayton - Englewood 110 Red Roof Inn Dayton North Airport 108 Red Roof Inn Dayton South Miamisburg 107 The Englewood Inn 106 Quality Inn & Suites Dayton South/Miamisburg 106 Residence Inn by Marriott Dayton North 105 Extended Stay America Dayton North 104 Courtyard by Marriott University of Dayton 101 Other Hotels 3,229 Total 6,564 Notes: Sorted in descending order by number of rooms.

"Other Hotels" includes properties with under 100 rooms.

Source: Dayton/Montgomery County CVB.

Summary of Hotel Supply in Montgomery County, Ohio

The University of Dayton recently purchased the Marriott Hotel and has begun a $23 million renovation that is anticipated to be completed by 2017. The renovation will consist of adding 2,000 to 3,000 square feet of meeting space as well as renovating the guest rooms. Approximately 65% of the hotel’s business is corporate which is attributable to its proximity to the University of Dayton and other companies. By contrast, business at the Crowne Plaza is primarily driven by group business.

Dayton Convention Center Needs Assessment / Market Analysis Study 16

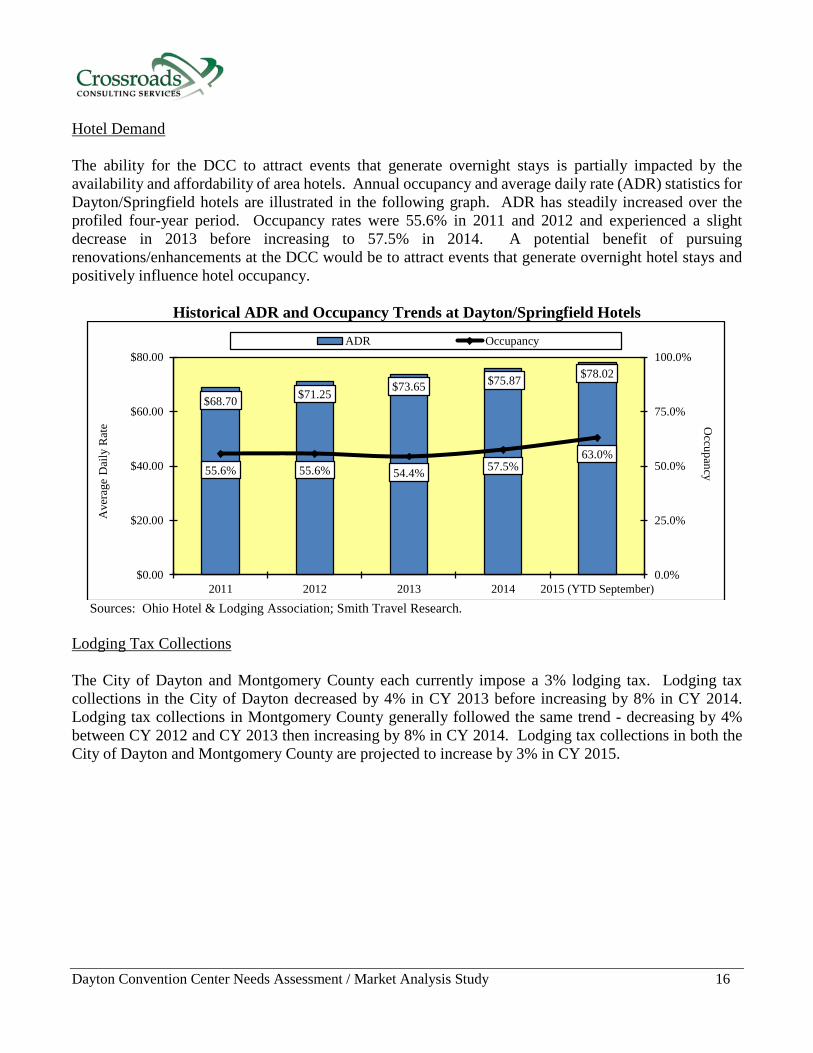

Hotel Demand The ability for the DCC to attract events that generate overnight stays is partially impacted by the availability and affordability of area hotels. Annual occupancy and average daily rate (ADR) statistics for Dayton/Springfield hotels are illustrated in the following graph. ADR has steadily increased over the profiled four-year period. Occupancy rates were 55.6% in 2011 and 2012 and experienced a slight decrease in 2013 before increasing to 57.5% in 2014. A potential benefit of pursuing renovations/enhancements at the DCC would be to attract events that generate overnight hotel stays and positively influence hotel occupancy.

Historical ADR and Occupancy Trends at Dayton/Springfield Hotels

Sources: Ohio Hotel & Lodging Association; Smith Travel Research.

Lodging Tax Collections The City of Dayton and Montgomery County each currently impose a 3% lodging tax. Lodging tax collections in the City of Dayton decreased by 4% in CY 2013 before increasing by 8% in CY 2014. Lodging tax collections in Montgomery County generally followed the same trend - decreasing by 4% between CY 2012 and CY 2013 then increasing by 8% in CY 2014. Lodging tax collections in both the City of Dayton and Montgomery County are projected to increase by 3% in CY 2015.

$68.70 $71.25 $73.65 $75.87 $78.02

55.6% 55.6% 54.4% 57.5%63.0%

0.0%

25.0%

50.0%

75.0%

100.0%

$0.00

$20.00

$40.00

$60.00

$80.00

2011 2012 2013 2014 2015 (YTD September)

Occupancy

Ave

rage

Dai

ly R

ate

ADR Occupancy

Dayton Convention Center Needs Assessment / Market Analysis Study 17

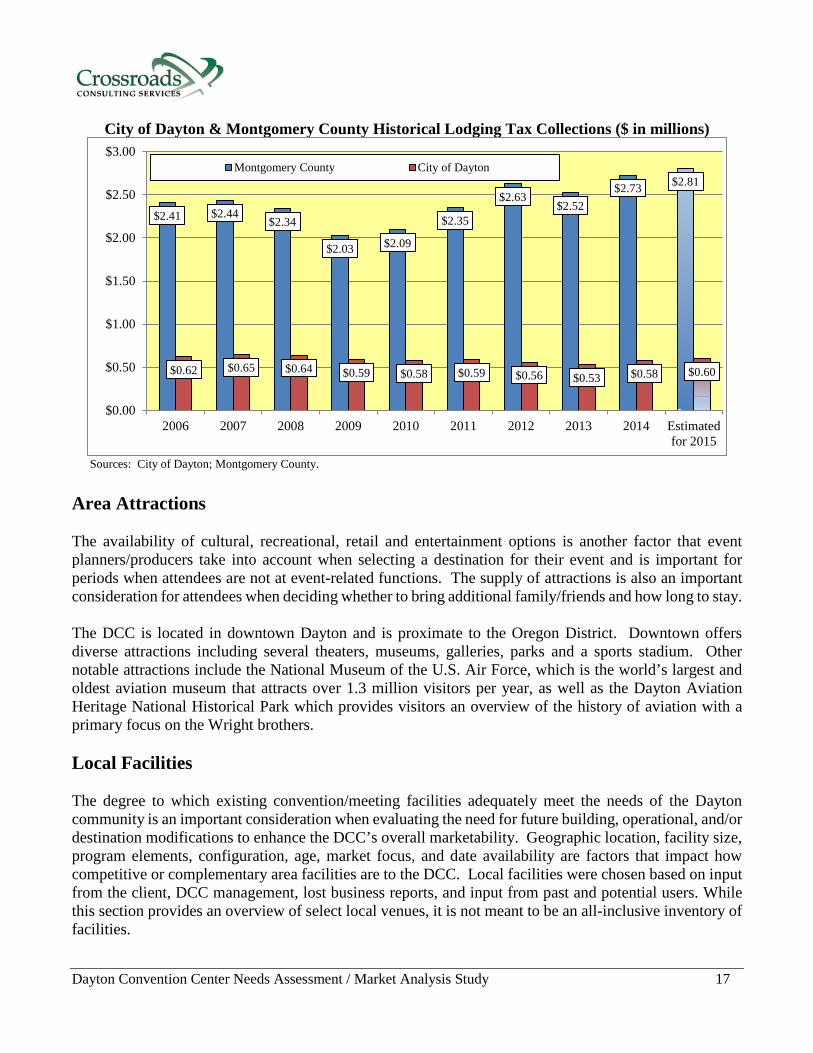

City of Dayton & Montgomery County Historical Lodging Tax Collections ($ in millions)

Sources: City of Dayton; Montgomery County.

Area Attractions The availability of cultural, recreational, retail and entertainment options is another factor that event planners/producers take into account when selecting a destination for their event and is important for periods when attendees are not at event-related functions. The supply of attractions is also an important consideration for attendees when deciding whether to bring additional family/friends and how long to stay. The DCC is located in downtown Dayton and is proximate to the Oregon District. Downtown offers diverse attractions including several theaters, museums, galleries, parks and a sports stadium. Other notable attractions include the National Museum of the U.S. Air Force, which is the world’s largest and oldest aviation museum that attracts over 1.3 million visitors per year, as well as the Dayton Aviation Heritage National Historical Park which provides visitors an overview of the history of aviation with a primary focus on the Wright brothers. Local Facilities The degree to which existing convention/meeting facilities adequately meet the needs of the Dayton community is an important consideration when evaluating the need for future building, operational, and/or destination modifications to enhance the DCC’s overall marketability. Geographic location, facility size, program elements, configuration, age, market focus, and date availability are factors that impact how competitive or complementary area facilities are to the DCC. Local facilities were chosen based on input from the client, DCC management, lost business reports, and input from past and potential users. While this section provides an overview of select local venues, it is not meant to be an all-inclusive inventory of facilities.

$2.41 $2.44$2.34

$2.03 $2.09

$2.35

$2.63$2.52

$2.73 $2.81

$0.62 $0.65 $0.64 $0.59 $0.58 $0.59 $0.56 $0.53 $0.58 $0.60

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 Estimatedfor 2015

Montgomery County City of Dayton

Dayton Convention Center Needs Assessment / Market Analysis Study 18

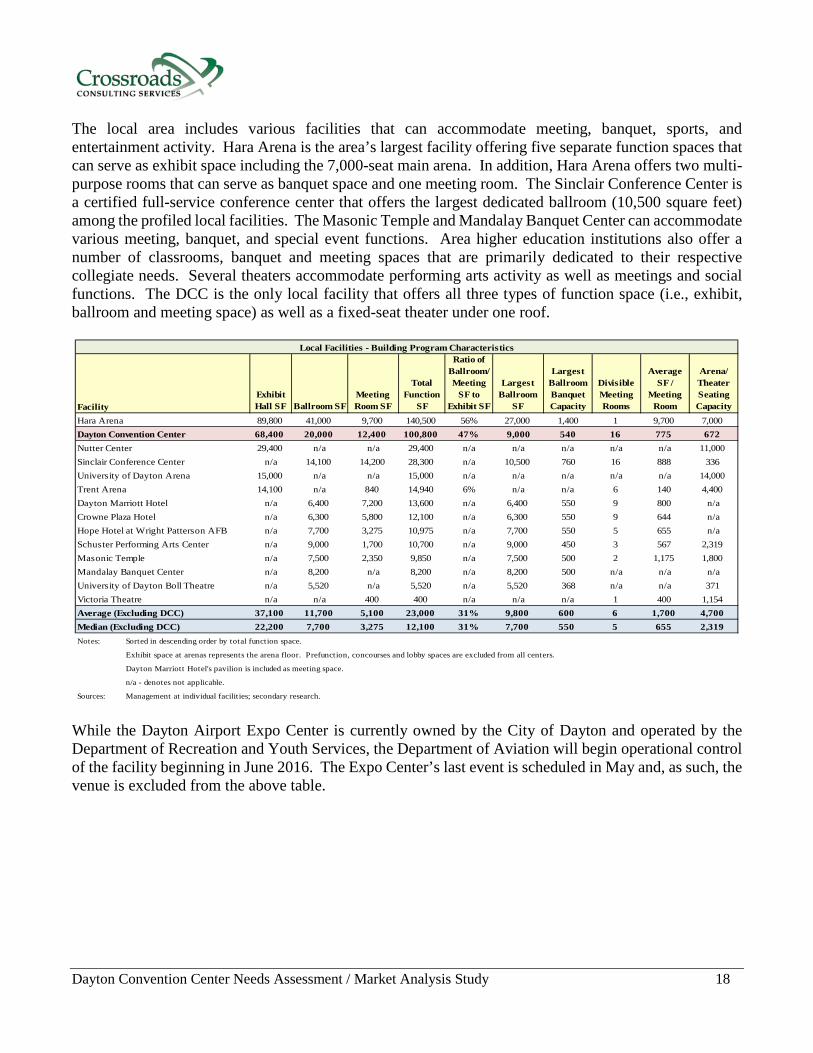

The local area includes various facilities that can accommodate meeting, banquet, sports, and entertainment activity. Hara Arena is the area’s largest facility offering five separate function spaces that can serve as exhibit space including the 7,000-seat main arena. In addition, Hara Arena offers two multi-purpose rooms that can serve as banquet space and one meeting room. The Sinclair Conference Center is a certified full-service conference center that offers the largest dedicated ballroom (10,500 square feet) among the profiled local facilities. The Masonic Temple and Mandalay Banquet Center can accommodate various meeting, banquet, and special event functions. Area higher education institutions also offer a number of classrooms, banquet and meeting spaces that are primarily dedicated to their respective collegiate needs. Several theaters accommodate performing arts activity as well as meetings and social functions. The DCC is the only local facility that offers all three types of function space (i.e., exhibit, ballroom and meeting space) as well as a fixed-seat theater under one roof.

FacilityExhibit Hall SF Ballroom SF

Meeting Room SF

Total Function

SF

Ratio of Ballroom/ Meeting

SF to Exhibit SF

Largest Ballroom

SF

Largest Ballroom Banquet Capacity

Divisible Meeting Rooms

Average SF /

Meeting Room

Arena/ Theater Seating Capacity

Hara Arena 89,800 41,000 9,700 140,500 56% 27,000 1,400 1 9,700 7,000Dayton Convention Center 68,400 20,000 12,400 100,800 47% 9,000 540 16 775 672Nutter Center 29,400 n/a n/a 29,400 n/a n/a n/a n/a n/a 11,000Sinclair Conference Center n/a 14,100 14,200 28,300 n/a 10,500 760 16 888 336University of Dayton Arena 15,000 n/a n/a 15,000 n/a n/a n/a n/a n/a 14,000Trent Arena 14,100 n/a 840 14,940 6% n/a n/a 6 140 4,400Dayton Marriott Hotel n/a 6,400 7,200 13,600 n/a 6,400 550 9 800 n/aCrowne Plaza Hotel n/a 6,300 5,800 12,100 n/a 6,300 550 9 644 n/aHope Hotel at Wright Patterson AFB n/a 7,700 3,275 10,975 n/a 7,700 550 5 655 n/aSchuster Performing Arts Center n/a 9,000 1,700 10,700 n/a 9,000 450 3 567 2,319Masonic Temple n/a 7,500 2,350 9,850 n/a 7,500 500 2 1,175 1,800Mandalay Banquet Center n/a 8,200 n/a 8,200 n/a 8,200 500 n/a n/a n/aUniversity of Dayton Boll Theatre n/a 5,520 n/a 5,520 n/a 5,520 368 n/a n/a 371Victoria Theatre n/a n/a 400 400 n/a n/a n/a 1 400 1,154Average (Excluding DCC) 37,100 11,700 5,100 23,000 31% 9,800 600 6 1,700 4,700Median (Excluding DCC) 22,200 7,700 3,275 12,100 31% 7,700 550 5 655 2,319Notes: Sorted in descending order by total function space.

Exhibit space at arenas represents the arena floor. Prefunction, concourses and lobby spaces are excluded from all centers.

Dayton Marriott Hotel's pavilion is included as meeting space.

n/a - denotes not applicable.

Sources: Management at individual facilit ies; secondary research.

Local Facilities - Building Program Characteristics

While the Dayton Airport Expo Center is currently owned by the City of Dayton and operated by the Department of Recreation and Youth Services, the Department of Aviation will begin operational control of the facility beginning in June 2016. The Expo Center’s last event is scheduled in May and, as such, the venue is excluded from the above table.

Dayton Convention Center Needs Assessment / Market Analysis Study 19

Planning Efforts Groups such as the Downtown Dayton Partnership are continually striving to position downtown Dayton as a vibrant, pedestrian-friendly, urban environment. Public and private developments can positively impact DCC operations in a variety of ways including, creating a more dynamic destination through enhanced visitor amenities as well as by establishing new or enhanced industry connections to the City Dayton. Several of the ongoing efforts occurring in the City of Dayton are summarized below. City of Dayton Greater Downtown Plan The City of Dayton Greater Downtown Plan aims to capitalize on downtown’s strength by utilizing the underutilized or not utilized spaces downtown; creating interconnectivity downtown through the development of a bus loop as well as a bike share transportation system; and continuing to encourage the development of small businesses by providing a network for small business owners. These plans are expected to increase the marketability of the City of Dayton as a community-friendly, unique, and vibrant urban environment. Oregon District One of the major developments in the Oregon District is the shuttle service. The free Oregon District Shuttle provides a convenient way to explore the various shops, restaurants, bars, and other businesses in the Oregon District. The shuttle runs on a hop on and off method with various stops throughout the Oregon District and operates Fridays and Saturdays from 5pm to 1am with shuttles arriving every 15 minutes. Miami Valley Regional Planning Commission Throughout 2015, the Miami Valley Regional Planning Commission is partnering with Montgomery County to implement their Open Space Planning. Open Space Planning is centered on improving outdoor spaces, entertainment, and personal well-being. The initiative also aims to provide environmental services such as flood control, providing natural habitats for wildlife, and improving overall water and air quality. Summary Market characteristics such as population base, accessibility and hotel supply as well as destination attributes such as attractions, restaurants and retail establishments impact a facility’s ability to attract non-local events and capture visitor spending that generates economic and fiscal impacts. The DCC’s downtown setting as well as Dayton’s central location, accessibility, attractions, and affordability offer a marketable destination for a variety of group business including conventions, competitive sports, banquets, meetings, and consumer shows.

Dayton Convention Center Needs Assessment / Market Analysis Study 20

Table of Contents

1 Introduction and Executive Summary 1 2 General Market Overview 11 3 Key Industry Trends 20 4 Historical Facility Operations 27 5 General Management Practices Assessment 47 6 Physical Facility Assessment 57 7 Competitive Facility Assessment 71 8 Needs Assessment 85 9 Economic Analysis 94

10 Funding Analysis 113

11 Limiting Conditions and Assumptions 120

12 Appendix 122

Dayton Convention Center Needs Assessment / Market Analysis Study 21

Key Industry Trends

Potential demand associated with any public assembly facility is somewhat dependent on the attributes of the industry(s) as a whole as well as specific target market segments. This analysis is based on information provided by secondary sources including, but not limited to, Center for Exhibition Industry Research (CEIR), Meeting Professionals International (MPI), Trade Show Executive, International Association of Conference Centers (IACC), Destination Marketing Association International (DMAI), Pollstar, IBISWorld, and the Sports and Fitness Industry Association. This section outlines key trends in the convention/meeting and competitive sports industries that may impact future operations of the DCC. Convention/Meetings Business The following summarizes key trends in the convention/meetings industry:

• The convention/meetings market has experienced tremendous growth in the supply of space over the past two decades.

• This growth coupled with an economic downturn created a gap in the supply of space and demand for space that led to a more competitive buyer’s market. – Numerous facilities can now accommodate meeting planners’ needs strictly in terms of the amount

of space required. – Hotels and larger convention centers are vying for more moderately sized group business.

• Hotels with exhibit and/or ballroom/meeting space can have an advantage over stand-alone meeting facilities because they control all major components of an event (i.e., function space, lodging and food/beverage) under one roof. Since the hotel is the primary beneficiary of all revenue streams, it can negotiate packages as it sees fit in any or all areas to attract business. – Some privately operated hotels offer entertainment (i.e., a headliner act for a banquet) as part of

their overall package to entice meeting planners. Some of these properties, such as those adjacent to casinos, are situated in suburban locations, remote from other businesses that might attract some of the attendee spending away from the hotel’s internal revenue generators.

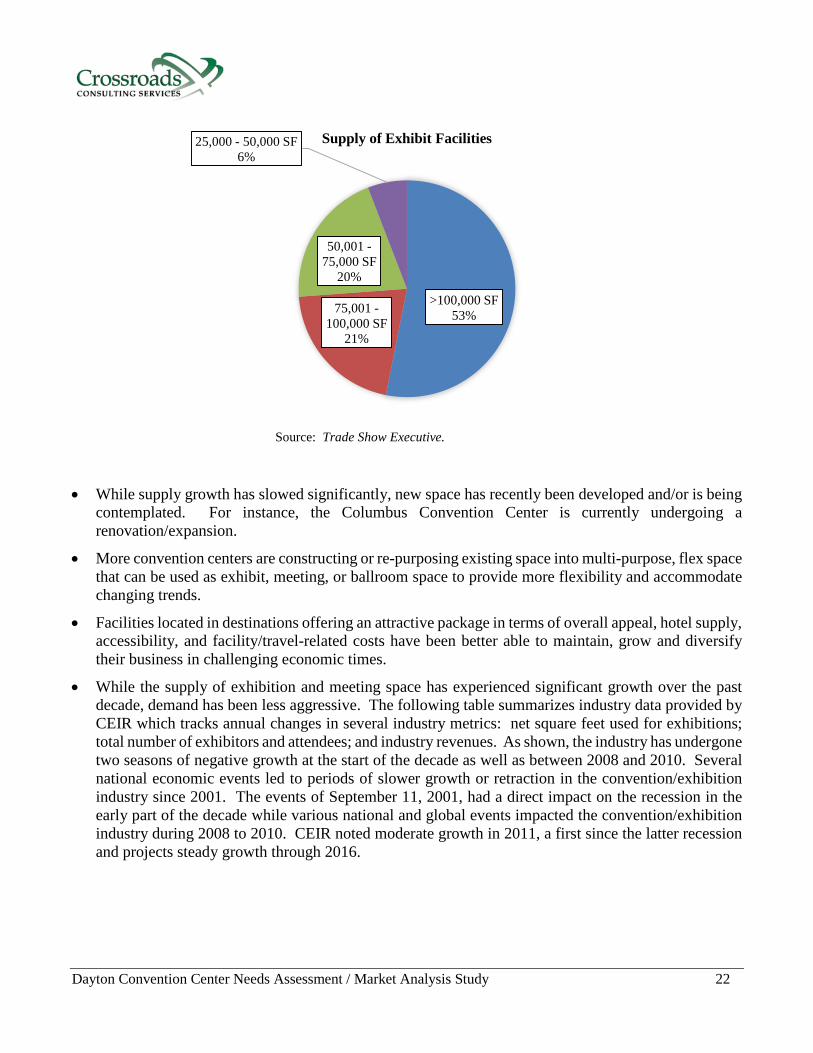

• The pie chart that follows represents the supply of exhibit facilities within the U.S. based on information from Trade Show Executive. Of the 250+ facilities located in the U.S., 53% offer greater than 100,000 square feet while only 6% offer between 25,000 and 50,000 square feet.

Dayton Convention Center Needs Assessment / Market Analysis Study 22

Source: Trade Show Executive. • While supply growth has slowed significantly, new space has recently been developed and/or is being

contemplated. For instance, the Columbus Convention Center is currently undergoing a renovation/expansion.

• More convention centers are constructing or re-purposing existing space into multi-purpose, flex space that can be used as exhibit, meeting, or ballroom space to provide more flexibility and accommodate changing trends.

• Facilities located in destinations offering an attractive package in terms of overall appeal, hotel supply, accessibility, and facility/travel-related costs have been better able to maintain, grow and diversify their business in challenging economic times.

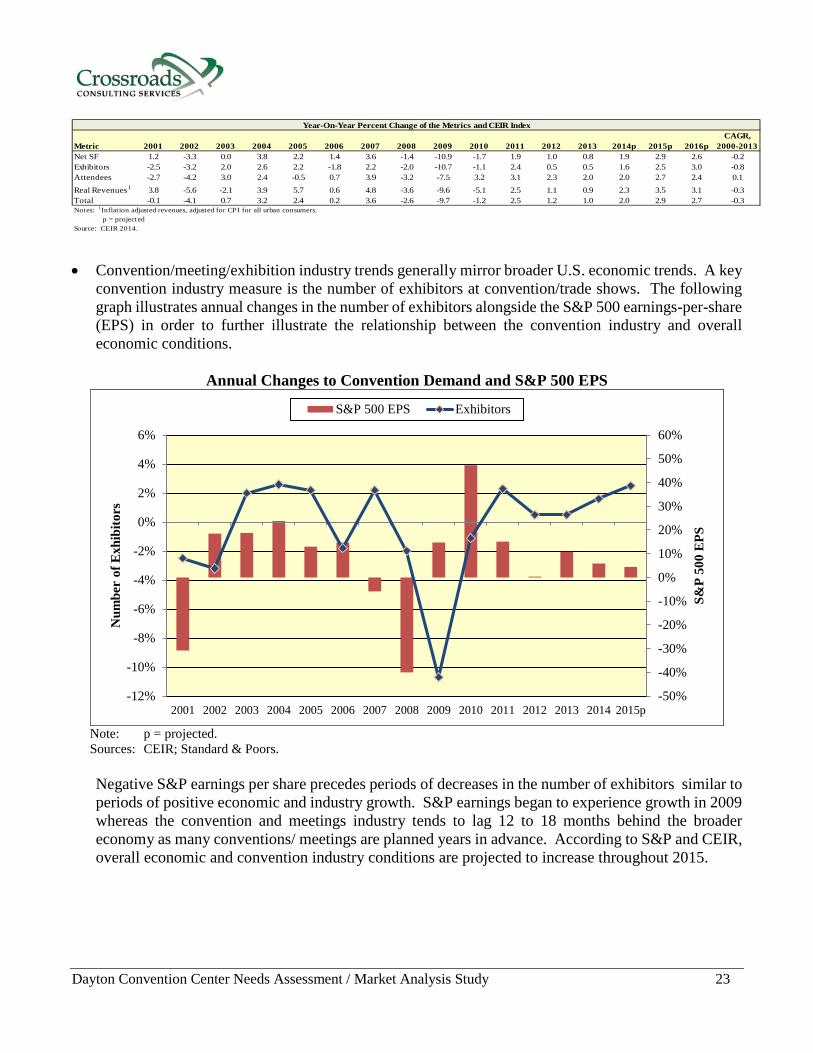

• While the supply of exhibition and meeting space has experienced significant growth over the past decade, demand has been less aggressive. The following table summarizes industry data provided by CEIR which tracks annual changes in several industry metrics: net square feet used for exhibitions; total number of exhibitors and attendees; and industry revenues. As shown, the industry has undergone two seasons of negative growth at the start of the decade as well as between 2008 and 2010. Several national economic events led to periods of slower growth or retraction in the convention/exhibition industry since 2001. The events of September 11, 2001, had a direct impact on the recession in the early part of the decade while various national and global events impacted the convention/exhibition industry during 2008 to 2010. CEIR noted moderate growth in 2011, a first since the latter recession and projects steady growth through 2016.

>100,000 SF53%75,001 -

100,000 SF21%

50,001 -75,000 SF

20%

25,000 - 50,000 SF6%

Supply of Exhibit Facilities

Dayton Convention Center Needs Assessment / Market Analysis Study 23

Metric 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014p 2015p 2016pCAGR,

2000-2013Net SF 1.2 -3.3 0.0 3.8 2.2 1.4 3.6 -1.4 -10.9 -1.7 1.9 1.0 0.8 1.9 2.9 2.6 -0.2Exhibitors -2.5 -3.2 2.0 2.6 2.2 -1.8 2.2 -2.0 -10.7 -1.1 2.4 0.5 0.5 1.6 2.5 3.0 -0.8Attendees -2.7 -4.2 3.0 2.4 -0.5 0.7 3.9 -3.2 -7.5 3.2 3.1 2.3 2.0 2.0 2.7 2.4 0.1Real Revenues1 3.8 -5.6 -2.1 3.9 5.7 0.6 4.8 -3.6 -9.6 -5.1 2.5 1.1 0.9 2.3 3.5 3.1 -0.3Total -0.1 -4.1 0.7 3.2 2.4 0.2 3.6 -2.6 -9.7 -1.2 2.5 1.2 1.0 2.0 2.9 2.7 -0.3Notes: 1Inflation adjusted revenues, adjusted for CPI for all urban consumers. p = projectedSource: CEIR 2014.

Year-On-Year Percent Change of the Metrics and CEIR Index

• Convention/meeting/exhibition industry trends generally mirror broader U.S. economic trends. A key

convention industry measure is the number of exhibitors at convention/trade shows. The following graph illustrates annual changes in the number of exhibitors alongside the S&P 500 earnings-per-share (EPS) in order to further illustrate the relationship between the convention industry and overall economic conditions.

Annual Changes to Convention Demand and S&P 500 EPS

Note: p = projected. Sources: CEIR; Standard & Poors.

Negative S&P earnings per share precedes periods of decreases in the number of exhibitors similar to periods of positive economic and industry growth. S&P earnings began to experience growth in 2009 whereas the convention and meetings industry tends to lag 12 to 18 months behind the broader economy as many conventions/ meetings are planned years in advance. According to S&P and CEIR, overall economic and convention industry conditions are projected to increase throughout 2015.

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015pS&

P 50

0 E

PS

Num

ber

of E

xhib

itors

S&P 500 EPS Exhibitors

Dayton Convention Center Needs Assessment / Market Analysis Study 24

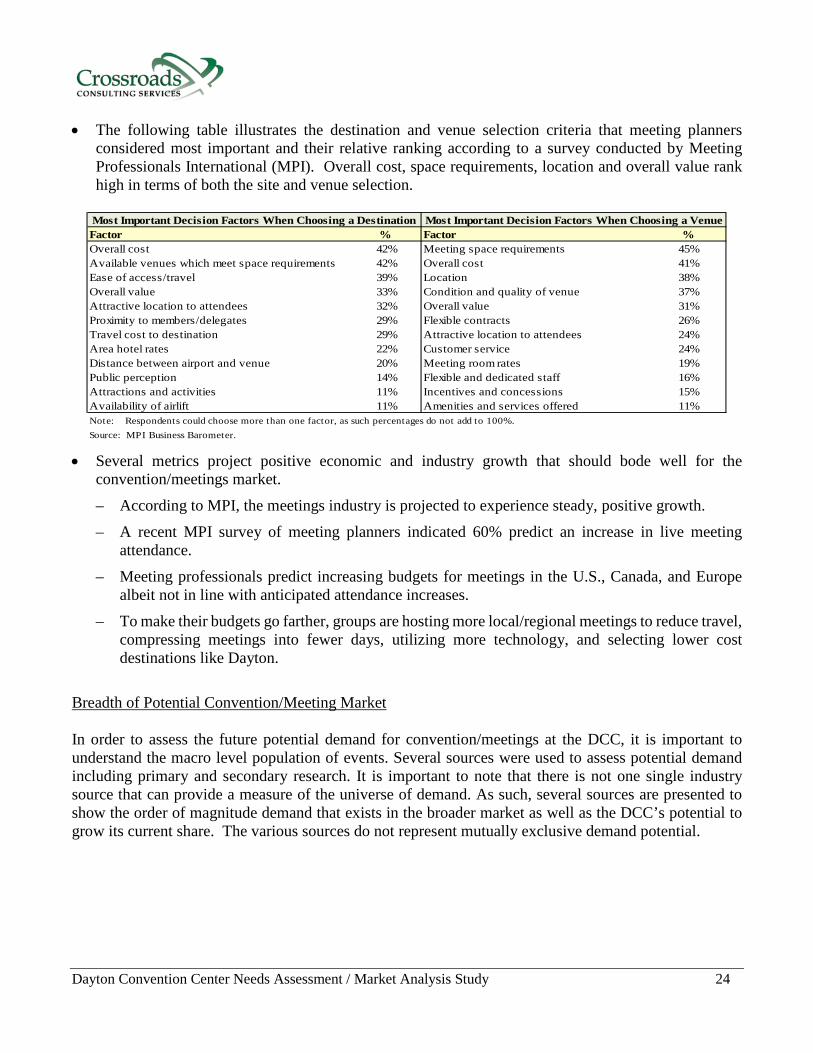

• The following table illustrates the destination and venue selection criteria that meeting planners considered most important and their relative ranking according to a survey conducted by Meeting Professionals International (MPI). Overall cost, space requirements, location and overall value rank high in terms of both the site and venue selection.

Factor % Factor %Overall cost 42% Meeting space requirements 45%Available venues which meet space requirements 42% Overall cost 41%Ease of access/travel 39% Location 38%Overall value 33% Condition and quality of venue 37%Attractive location to attendees 32% Overall value 31%Proximity to members/delegates 29% Flexible contracts 26%Travel cost to destination 29% Attractive location to attendees 24%Area hotel rates 22% Customer service 24%Distance between airport and venue 20% Meeting room rates 19%Public perception 14% Flexible and dedicated staff 16%Attractions and activities 11% Incentives and concessions 15%Availability of airlift 11% Amenities and services offered 11%Note: Respondents could choose more than one factor, as such percentages do not add to 100%.Source: MPI Business Barometer.

Most Important Decision Factors When Choosing a Destination Most Important Decision Factors When Choosing a Venue

• Several metrics project positive economic and industry growth that should bode well for the

convention/meetings market. – According to MPI, the meetings industry is projected to experience steady, positive growth. – A recent MPI survey of meeting planners indicated 60% predict an increase in live meeting

attendance. – Meeting professionals predict increasing budgets for meetings in the U.S., Canada, and Europe

albeit not in line with anticipated attendance increases. – To make their budgets go farther, groups are hosting more local/regional meetings to reduce travel,

compressing meetings into fewer days, utilizing more technology, and selecting lower cost destinations like Dayton.

Breadth of Potential Convention/Meeting Market In order to assess the future potential demand for convention/meetings at the DCC, it is important to understand the macro level population of events. Several sources were used to assess potential demand including primary and secondary research. It is important to note that there is not one single industry source that can provide a measure of the universe of demand. As such, several sources are presented to show the order of magnitude demand that exists in the broader market as well as the DCC’s potential to grow its current share. The various sources do not represent mutually exclusive demand potential.

Dayton Convention Center Needs Assessment / Market Analysis Study 25

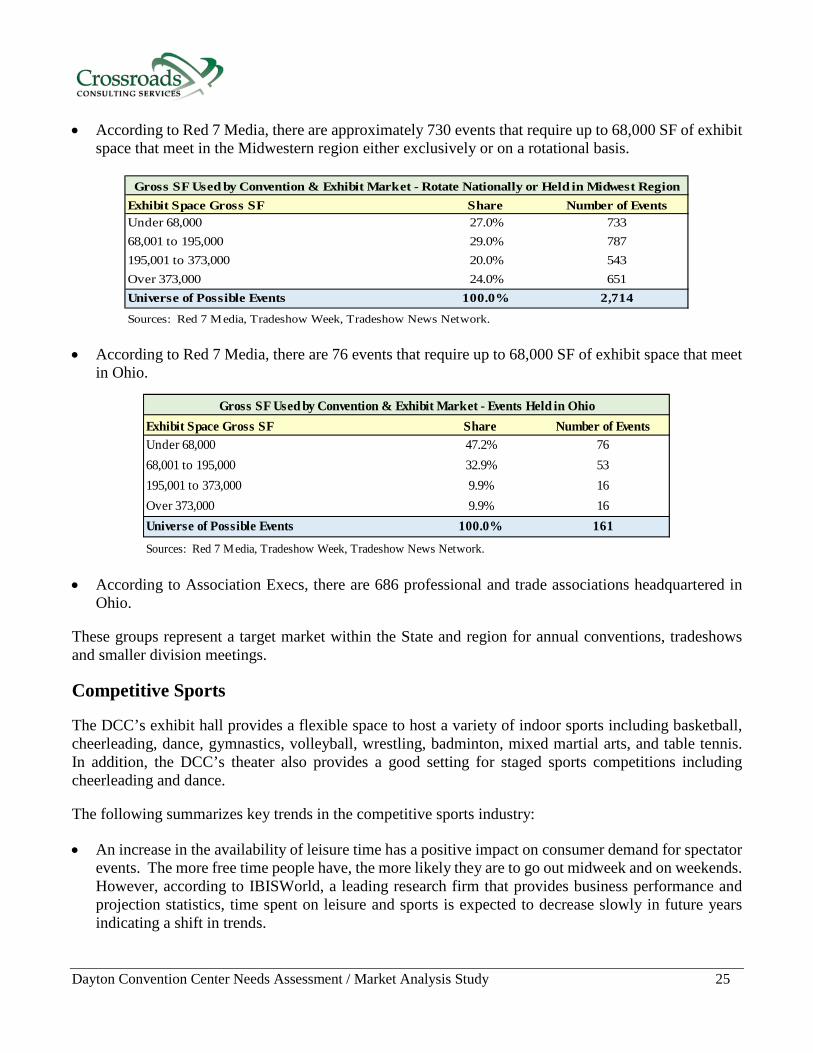

• According to Red 7 Media, there are approximately 730 events that require up to 68,000 SF of exhibit space that meet in the Midwestern region either exclusively or on a rotational basis.

Exhibit Space Gross SF Share Number of EventsUnder 68,000 27.0% 733 68,001 to 195,000 29.0% 787 195,001 to 373,000 20.0% 543 Over 373,000 24.0% 651 Universe of Possible Events 100.0% 2,714

Sources: Red 7 Media, Tradeshow Week, Tradeshow News Network.

Gross SF Used by Convention & Exhibit Market - Rotate Nationally or Held in Midwest Region

• According to Red 7 Media, there are 76 events that require up to 68,000 SF of exhibit space that meet

in Ohio.

Exhibit Space Gross SF Share Number of EventsUnder 68,000 47.2% 76 68,001 to 195,000 32.9% 53 195,001 to 373,000 9.9% 16 Over 373,000 9.9% 16 Universe of Possible Events 100.0% 161

Sources: Red 7 Media, Tradeshow Week, Tradeshow News Network.

Gross SF Used by Convention & Exhibit Market - Events Held in Ohio

• According to Association Execs, there are 686 professional and trade associations headquartered in Ohio.

These groups represent a target market within the State and region for annual conventions, tradeshows and smaller division meetings. Competitive Sports The DCC’s exhibit hall provides a flexible space to host a variety of indoor sports including basketball, cheerleading, dance, gymnastics, volleyball, wrestling, badminton, mixed martial arts, and table tennis. In addition, the DCC’s theater also provides a good setting for staged sports competitions including cheerleading and dance. The following summarizes key trends in the competitive sports industry:

• An increase in the availability of leisure time has a positive impact on consumer demand for spectator events. The more free time people have, the more likely they are to go out midweek and on weekends. However, according to IBISWorld, a leading research firm that provides business performance and projection statistics, time spent on leisure and sports is expected to decrease slowly in future years indicating a shift in trends.

Dayton Convention Center Needs Assessment / Market Analysis Study 26

• More communities are realizing the value of sports tourism as an economic generator.

• The competitive youth and adult amateur sports industry has continued to be a significant market opportunity with multiple sports/age groups/demand segments.

• Based on a survey of households conducted by the Sports and Fitness Industry Association in conjunction with the Physical Activity Council, there are an estimated 68.7 million indoor sport participants representing a significant demand segment for competitive level tournaments that could be held in the DCC.

• Demand is less impacted by economic fluctuations as participants and family/friends are willing to travel significant distances for their preferred sport.

• More communities are developing specialized indoor and/or outdoor complexes to accommodate multiple games/competitions due to their value as a tourism generator.

• It is important for destinations to have a strong volunteer base and elite level leagues to support and promote tournament activity that generates overnight stays.

Summary The convention/meetings market has experienced tremendous growth in the supply of space creating a gap in supply and demand which has led to a more competitive buyer’s market. Numerous facilities can accommodate meeting planners’ needs strictly in terms of the amount of space required including larger convention centers that are vying for more moderately sized events as well as hotels that are aggressively marketing their function space to small and mid-sized events. Smaller convention centers such as the DCC must compete on the overall package – price, value, quality customer service, and destination attributes. Facilities located in destinations offering an attractive package in terms of overall appeal, hotel supply, accessibility, and facility/travel-related costs have been better able to maintain, grow and diversify their business in challenging economic times. Communities are increasingly seeing the value of hosting competitive sporting events given their ability to attract overnight visitors and associated spending on lodging, transportation, restaurants, retail, and entertainment establishments. Convention centers are well-suited to host a variety of indoor sporting events given the flexibility of their exhibit halls. The DCC’s theater is a competitive advantage for sports competitions that require a stage. Destinations that offer good highway accessibility, a family-friendly environment and hotels at a variety of price points are preferred by sporting event organizers. Most event attendees are willing to drive between the host facility and their hotels within five to ten miles which makes Dayton appealing to these groups given the location of its hotel supply in relation to the DCC.

Dayton Convention Center Needs Assessment / Market Analysis Study 27

Table of Contents

1 Introduction and Executive Summary 1 2 General Market Overview 11 3 Key Industry Trends 20 4 Historical Facility Operations 27 5 General Management Practices Assessment 47 6 Physical Facility Assessment 57 7 Competitive Facility Assessment 71 8 Needs Assessment 85 9 Economic Analysis 94

10 Funding Analysis 113

11 Limiting Conditions and Assumptions 120

12 Appendix 122

Dayton Convention Center Needs Assessment / Market Analysis Study 28

Historical Facility Operations

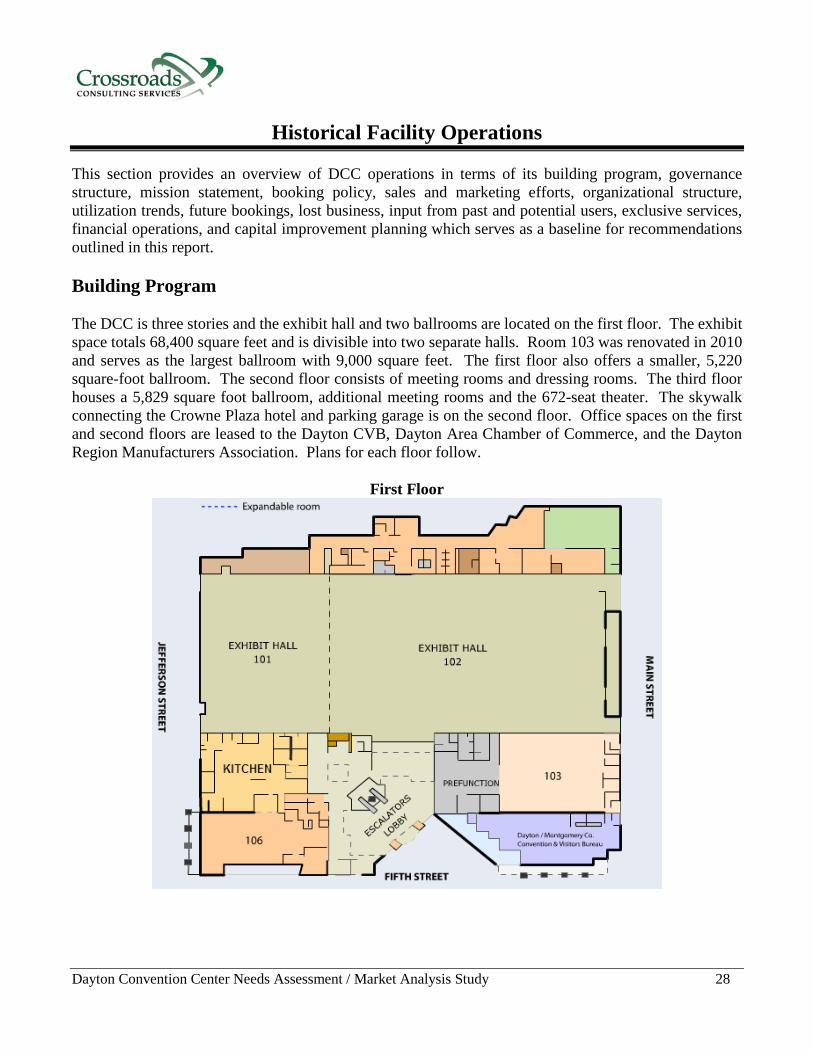

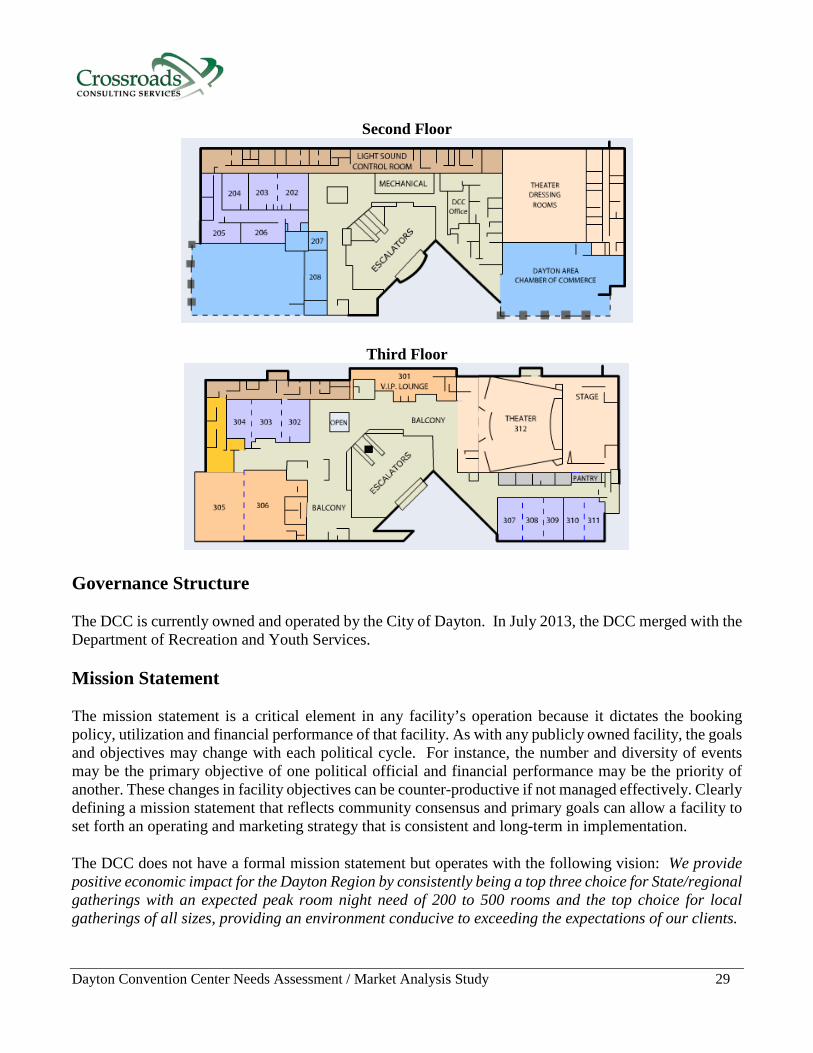

This section provides an overview of DCC operations in terms of its building program, governance structure, mission statement, booking policy, sales and marketing efforts, organizational structure, utilization trends, future bookings, lost business, input from past and potential users, exclusive services, financial operations, and capital improvement planning which serves as a baseline for recommendations outlined in this report. Building Program The DCC is three stories and the exhibit hall and two ballrooms are located on the first floor. The exhibit space totals 68,400 square feet and is divisible into two separate halls. Room 103 was renovated in 2010 and serves as the largest ballroom with 9,000 square feet. The first floor also offers a smaller, 5,220 square-foot ballroom. The second floor consists of meeting rooms and dressing rooms. The third floor houses a 5,829 square foot ballroom, additional meeting rooms and the 672-seat theater. The skywalk connecting the Crowne Plaza hotel and parking garage is on the second floor. Office spaces on the first and second floors are leased to the Dayton CVB, Dayton Area Chamber of Commerce, and the Dayton Region Manufacturers Association. Plans for each floor follow.

First Floor

Dayton Convention Center Needs Assessment / Market Analysis Study 29

Second Floor

Third Floor

Governance Structure The DCC is currently owned and operated by the City of Dayton. In July 2013, the DCC merged with the Department of Recreation and Youth Services. Mission Statement The mission statement is a critical element in any facility’s operation because it dictates the booking policy, utilization and financial performance of that facility. As with any publicly owned facility, the goals and objectives may change with each political cycle. For instance, the number and diversity of events may be the primary objective of one political official and financial performance may be the priority of another. These changes in facility objectives can be counter-productive if not managed effectively. Clearly defining a mission statement that reflects community consensus and primary goals can allow a facility to set forth an operating and marketing strategy that is consistent and long-term in implementation. The DCC does not have a formal mission statement but operates with the following vision: We provide positive economic impact for the Dayton Region by consistently being a top three choice for State/regional gatherings with an expected peak room night need of 200 to 500 rooms and the top choice for local gatherings of all sizes, providing an environment conducive to exceeding the expectations of our clients.

Dayton Convention Center Needs Assessment / Market Analysis Study 30

Booking Policy For any facility to be successful it is important for the booking policy to appropriately support and implement the mission statement through its prioritization of events. A well-defined mission statement and booking policy can help reduce the potential for perceived differences in the facility’s role by various stakeholders. The DCC does not have a formal booking policy. Given the recent decline in winning bids for future convention business, staff has begun booking business on a first-come basis. DCC staff controls the facility’s event calendar and CVB sales staff does not have access to view the calendar. Sales and Marketing Efforts Typically, convention centers are marketed by the facility itself, the local CVB, and sometimes jointly with headquarters hotel properties. Currently, the City of Dayton does not dedicate funds for marketing the DCC. The Dayton CVB receives 70% of Montgomery County’s hotel tax collections annually and serves as the destination marketing organization for the City of Dayton and Montgomery County. The current policy/ agreement with the Dayton CVB protects space needed to book conventions 18 months in advance. The Dayton CVB primarily focuses its efforts on the following target markets: competitive sports; social, military reunion, educational, religious groups; hobby; aviation; and State/regional associations. According to facility management, past and potential DCC convention business can generally be classified into three categories with the corresponding percentage of business noted below: • Yearly, bi-annual, or three- to six-year rotation events such as state associations that include Dayton

in their rotation throughout the State of Ohio (45%)

• One-time events that are not on a rotation or do not visit the same city twice (45%)

• Those that rotate a minimum of every 10 years (10%) The City of Dayton established a discount policy that includes no space rental charges for new conventions/meetings with a minimum of 200 room nights and $10,000 to $15,000 in food/beverage sales for events booked during 2015. This policy was recently extended for events booking in 2016. The Dayton CVB provides subsidies for qualifying first-time DCC users that can be applied to a local Montgomery County vendor including facility rent, food/beverage, and/or transportation services. Event contracts in excess of $10,000 require the City of Dayton’s legal department approval for use of the DCC. Contracts below this threshold can be approved by the Department of Recreation and Youth Services Director. Separate contracts are required for space rental, audio/visual services, food/beverage, and hotel rooms, making the booking process onerous for users.

Dayton Convention Center Needs Assessment / Market Analysis Study 31

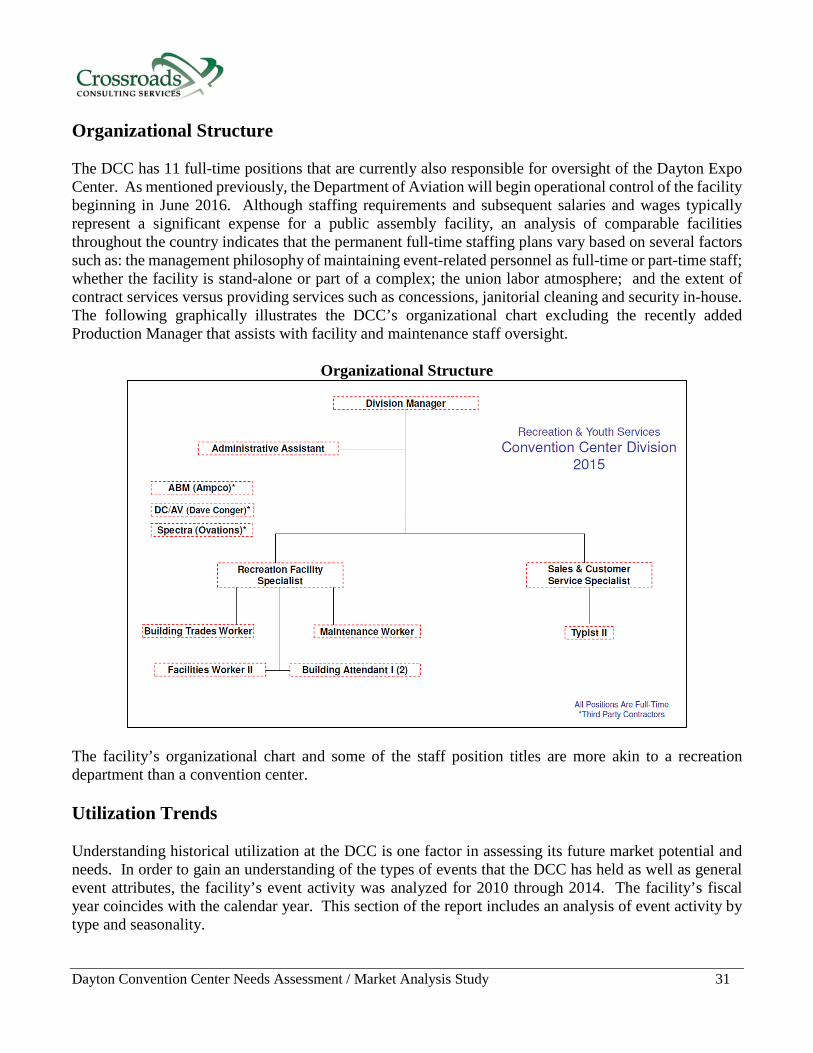

Organizational Structure The DCC has 11 full-time positions that are currently also responsible for oversight of the Dayton Expo Center. As mentioned previously, the Department of Aviation will begin operational control of the facility beginning in June 2016. Although staffing requirements and subsequent salaries and wages typically represent a significant expense for a public assembly facility, an analysis of comparable facilities throughout the country indicates that the permanent full-time staffing plans vary based on several factors such as: the management philosophy of maintaining event-related personnel as full-time or part-time staff; whether the facility is stand-alone or part of a complex; the union labor atmosphere; and the extent of contract services versus providing services such as concessions, janitorial cleaning and security in-house. The following graphically illustrates the DCC’s organizational chart excluding the recently added Production Manager that assists with facility and maintenance staff oversight.

Organizational Structure

The facility’s organizational chart and some of the staff position titles are more akin to a recreation department than a convention center. Utilization Trends Understanding historical utilization at the DCC is one factor in assessing its future market potential and needs. In order to gain an understanding of the types of events that the DCC has held as well as general event attributes, the facility’s event activity was analyzed for 2010 through 2014. The facility’s fiscal year coincides with the calendar year. This section of the report includes an analysis of event activity by type and seasonality.

Dayton Convention Center Needs Assessment / Market Analysis Study 32

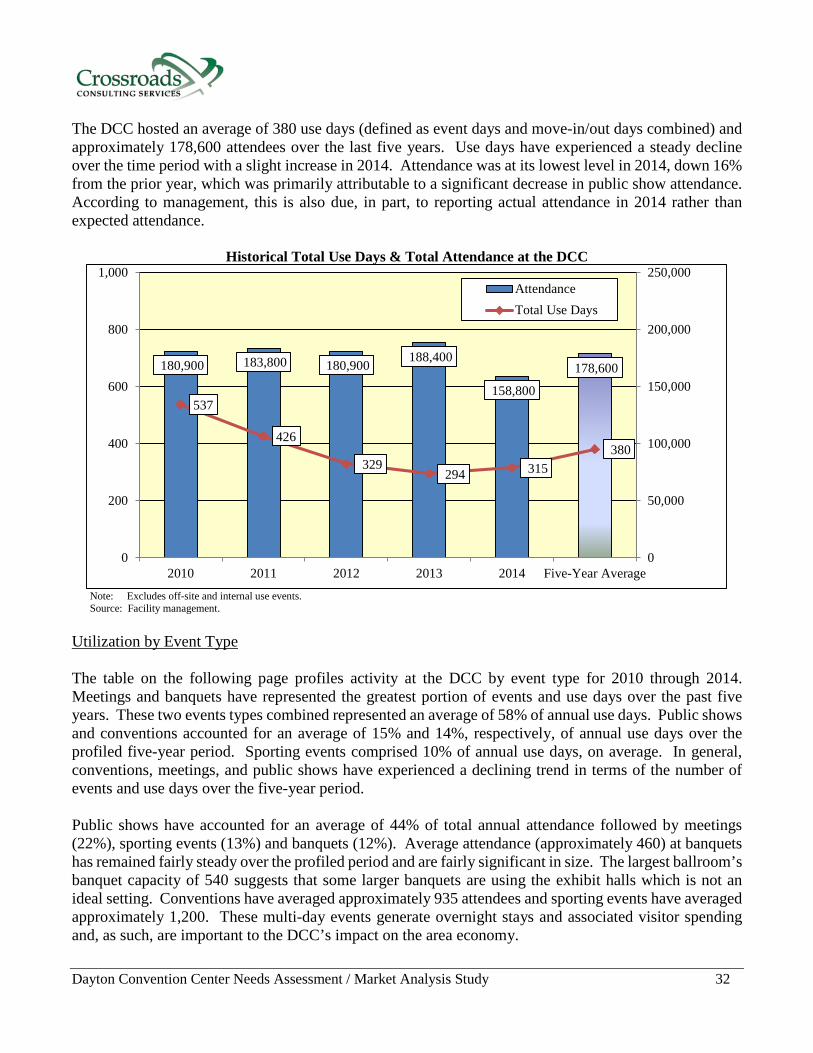

The DCC hosted an average of 380 use days (defined as event days and move-in/out days combined) and approximately 178,600 attendees over the last five years. Use days have experienced a steady decline over the time period with a slight increase in 2014. Attendance was at its lowest level in 2014, down 16% from the prior year, which was primarily attributable to a significant decrease in public show attendance. According to management, this is also due, in part, to reporting actual attendance in 2014 rather than expected attendance.

Historical Total Use Days & Total Attendance at the DCC

Note: Excludes off-site and internal use events. Source: Facility management.

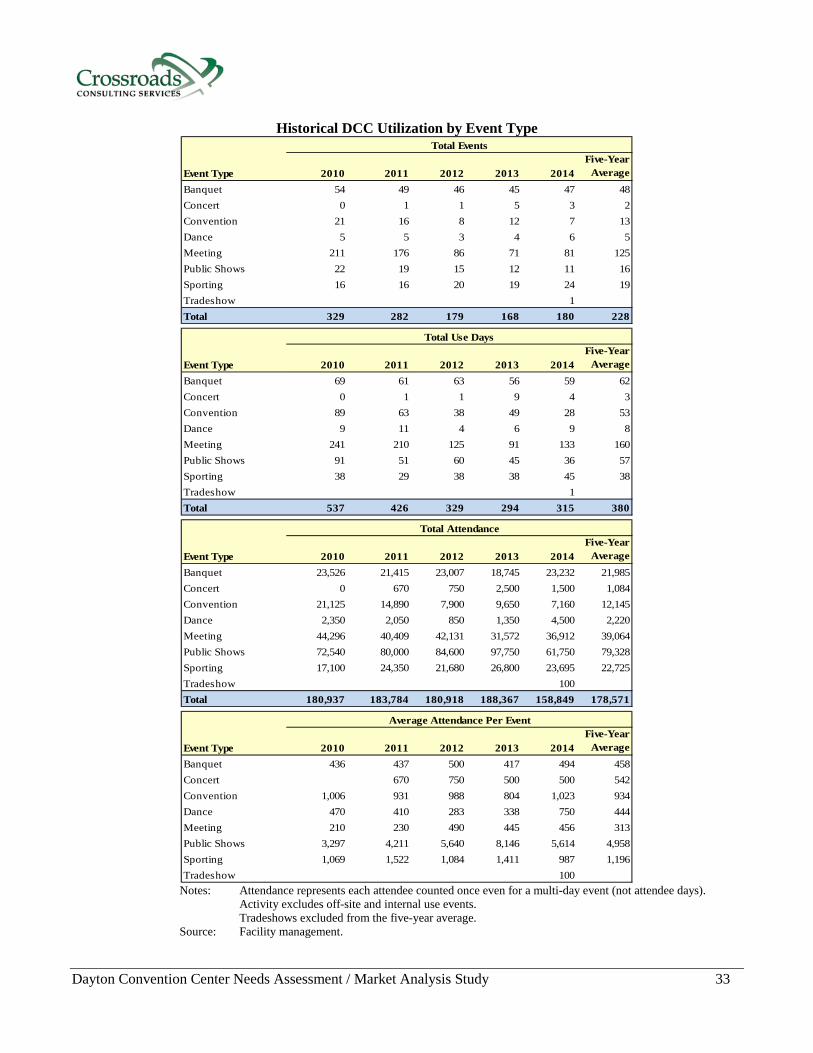

Utilization by Event Type The table on the following page profiles activity at the DCC by event type for 2010 through 2014. Meetings and banquets have represented the greatest portion of events and use days over the past five years. These two events types combined represented an average of 58% of annual use days. Public shows and conventions accounted for an average of 15% and 14%, respectively, of annual use days over the profiled five-year period. Sporting events comprised 10% of annual use days, on average. In general, conventions, meetings, and public shows have experienced a declining trend in terms of the number of events and use days over the five-year period. Public shows have accounted for an average of 44% of total annual attendance followed by meetings (22%), sporting events (13%) and banquets (12%). Average attendance (approximately 460) at banquets has remained fairly steady over the profiled period and are fairly significant in size. The largest ballroom’s banquet capacity of 540 suggests that some larger banquets are using the exhibit halls which is not an ideal setting. Conventions have averaged approximately 935 attendees and sporting events have averaged approximately 1,200. These multi-day events generate overnight stays and associated visitor spending and, as such, are important to the DCC’s impact on the area economy.

180,900 183,800 180,900 188,400

158,800

178,600

537

426

329 294 315

380

0

50,000

100,000

150,000

200,000

250,000

0

200

400

600

800

1,000

2010 2011 2012 2013 2014 Five-Year Average

AttendanceTotal Use Days

Dayton Convention Center Needs Assessment / Market Analysis Study 33

Historical DCC Utilization by Event Type

Event Type 2010 2011 2012 2013 2014Five-Year

AverageBanquet 54 49 46 45 47 48Concert 0 1 1 5 3 2Convention 21 16 8 12 7 13Dance 5 5 3 4 6 5Meeting 211 176 86 71 81 125Public Shows 22 19 15 12 11 16Sporting 16 16 20 19 24 19Tradeshow 1Total 329 282 179 168 180 228

Event Type 2010 2011 2012 2013 2014Five-Year