Embed Size (px)

Citation preview

Stuff to Help Connect Study Material D2L Practice Quizzes Read your textbook Solutions to selected

homework questions in D2L

1

Analyzing and Recording

Transactions

More of

C H A P T E R 2

2

Learning Objectives

1. Explain the accounting cycle. (LO1)

2. Describe an account, its use, and its relationship to the ledger. (LO2)

3. Define debits and credits and explain their role in double-entry accounting. (LO3)

4. Describe a chart of accounts and its relationship to the ledger. (LO4)

3-3

5. Analyze the impact of transactions on

accounts. (LO5)6. Record transactions in a journal and

post entries to a ledger. (LO6)7. Prepare and explain the use of a trial

balance. (LO7)

Learning Objectives

3-4

The normal balance of an account refers to the debit or credit side where increases are recorded.

A) True

B) False5

Example #1:

The owner, V. Klimb, invests $10,000 in the business.

Accounts affected

Increase/ Decrease

Debit/Credit

Cash Increase Debit

V.Klimb, capital Increase Credit

Analyzing Transactions

1 2 3

3-6LO 5

Example #1:

The owner invests $10,000 in the business. Debit Cash for $10,000 Credit V.Klimb, Capital for $10,000

Cash10,000

V.Klimb, Capital10,000

Analyzing Transactions

3-7LO 5

Entries are originally recorded in the General Journal. This process is called “journalizing”.

The General Journal

3-8LO 6

GENERAL JOURNAL Page 1

Date Account Titles and Explanation PR Debit Credit 2014 Jan. 1 Cash 10 000 V.Klimb, Capital 10 000 Investment by owner

GENERAL JOURNAL Page 1

Date Account Titles and Explanation PR Debit Credit 2014 Jan. 1 Cash 10 000 V.Klimb, Capital 10 000 Investment by owner

Elements of a Journal Entry

9

1. Date of transaction/event2. Name of accounts affected3. Amount of each change4. A brief description

12 3

4

Note “debits” are listed first

Example #2:

The company purchases supplies by paying $2,500 cash.

Accounts affected

Increase/ Decrease

Debit/Credit

Analyzing Transactions

1 2 3

3-10LO 5

Example #2:

The company purchases supplies by paying $2,500 cash.

Accounts affected

Increase/ Decrease

Debit/Credit

Supplies Increase Debit

Cash Decrease Credit

Analyzing Transactions

1 2 3

3-11LO 5

Analyzing TransactionsExample #2:

The company purchases supplies by paying $2,500 cash.

Supplies2,500

Cash2,500

3-12LO 5

GENERAL JOURNAL Page 1

Date Account Titles and Explanation PR Debit Credit 2014 Jan. 1 Supplies 2 500 Cash 2 500 Purchased store supplies for cash

Focussed Workout

QS 2-9

Ex 2-6 (pt 1)

14

• A record (or list) containing all accounts used by a business.

• May be computerized or maintained manually.

• Each company has its own unique set of accounts.

The Ledger

3-15LO 2 Typically numbered

18

Ledger Account

19

GENERAL LEDGER

ACCOUNT NAME ACCOUNT NO. 101

DATE EXPLANATION PR DEBIT CREDIT BALANCE

The “T” has not really gone away

• General Journal information is transferred to the General Ledger.

• Account balances are updated.• This process is called “posting”.

Posting Journal Entries

3-20LO 6

GENERAL JOURNAL Page 1

Date Account Titles and Explanation PR Debit Credit Jan. 1 Cash 101 1 0 000 Virgil Klimb, Capital 301 10 000 Investment by owner

GENERAL LEDGER

Cash ACCOUNT NO. 101

DATE EXPLANATION PR DEBIT CREDIT BALANCE

Jan. 1 G1 10 0 0 0 10 0 0 0

Virgil Klimb, Capital ACCOUNT NO. 301

DATE EXPLANATION PR DEBIT CREDIT BALANCE

Jan . 1 G1 10 0 0 0 10 0 0 0

General journal information is transferred (posted) to the general ledger

General journal information is transferred (posted) to the general ledger

Steps:

1. Identify the accounts.

2. Enter date

3. Enter amount

4. Calculate new account balance

5. Enter posting references (where to/from)

Steps:

1. Identify the accounts.

2. Enter date

3. Enter amount

4. Calculate new account balance

5. Enter posting references (where to/from)

2 1 3

4

5

5

Posting

LO 621

Test Run

23

QS 2-10, 2-11

Ex 2-6 (pt 2)

The Accounting Cycle

LO 13-24

Prepare post-closingtrial balance

Journalize

Close

Prepareunadjusted trial balance

Post

Analyzetransactions

Prepare adjusted

trial balance

Prepare statements

Adjust

2

3

4

6

8

19

7

5

Ch 1-2

Ch 2

Ch 2

Ch 2

Ch 3

Ch 4

Ch 4

Ch 1-4

Ch 3

• A list of accounts and their balances at a point in time.

• Used to determine if total debits equals total credits.

• May also be used to prepare financial statements.

Trial Balance

3-25LO 7

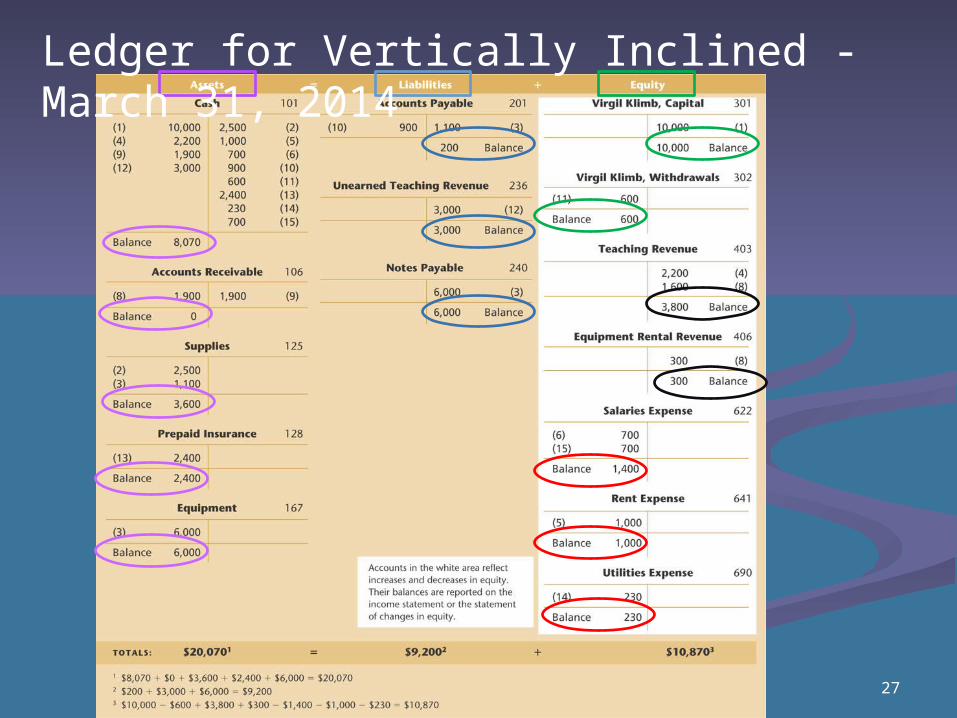

Just One Account from the General Ledger (GL)

26

27

Ledger for Vertically Inclined - March 31, 2014

28

Practice!EX 2-12,13

QS 2-12

29

What if it Doesn’t Balance? Add debit column and credit column,

again Check for the difference

Divisible by 9? Amounts copied correctly Amounts in the right columns Recheck posting Recheck original journal entries

30

See page 84

Income Statement

31

2,400

Statement of Changes in Equity

32

2,400

11,800

Balance Sheet

33

11,800

Comprehensive Practice

Problem 2-6A

34

Solution available on D2L

• What is journalizing?• What is posting?• What is the purpose of

a trial balance?• What goes on each

statement?

Review

3-36

Chapter 2 – Major HurdleHow are you doing?

3-37