Embed Size (px)

Citation preview

1

CHAPTER - I

STOCK PRICE VOLATILITY AND INDIAN CAPITAL MARKETS

1.1 Introduction

Economic status of a country is greatly reflected by the introduction of new economic

policy in the middle of the year 1991. The Indian Capital Market has witnessed a tremendous

growth. There was an explosion of investor interest during the nineties and an equity cult

emerged in the country. To experience sustained growth statutory legislations have helped the

capital market. Foreign Exchange Regulations Act is one such legislation in this direction. An

important recent development has been the entry of Foreign Institutional Investors as

participants in the primary and secondary markets for industrial securities. In the past several

years, investments in developing countries have increased remarkably. Among the

developing countries, India has received considerable capital inflows in recent years. The

liberalization policy of the Government of India has now started yielding results and the

country is poised for a big leap in the industrial and economic growth. The economy of the

country is mainly based on the development of the corporate sectors. Funds may be raised

through securities market for financing corporate growth. The Indian capital market has

witnessed radical changes, especially during the last decade. Having discarded the age old

practices like open outcry trading system, physical form of shares and new settlement

procedure, and others, the markets are now operating with world class practices and products.

The reforms in the capital markets have helped to improve efficiency in many aspects

namely, the dissemination of information, transparency in operations, prohibiting unfair trade

practices.

The stock market is one of the most important sources for companies to raise money.

This allows businesses to be publicly traded, or raise additional financial capital for

expansion by selling shares of ownership of the company in a public market. The liquidity

that an exchange affords the investors gives them the ability to quickly and easily sell

securities. This is an attractive feature of investing in stocks, compared to other less liquid

investments such as real estate. Some companies actively increase liquidity by trading in their

own shares. History has shown that the price of shares and other assets is an important part of

the dynamics of economic activity, and can influence or be an indicator of social mood. An

economy where the stock market is on the rise is considered to be an up-and-coming

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

2

economy. In fact, the stock market is often considered the primary indicator of a country's

economic strength and development. Stock prices are changed every day by the market.

Buyers and sellers cause prices to change as they decide how valuable each stock is.

Basically, share prices change because of supply and demand. If more people want to buy a

stock than sell it-the price moves up. Conversely, if more people want to sell a stock, there

would be more supply than demand - the price would start to fall. Volatility in the stock Price

is an integral part of stock market with the alternating bull and bear phases. In the bullish

market, the share prices soar high and in the bearish market, share prices fall down and these

ups and downs, determine the return and volatility of the stock market. Volatility is a

symptom of a highly liquid stock market. Pricing of securities, depends on volatility of each

asset. An increase in stock market volatility brings a large stock price change of advances or

declines. Investors interpret a raise in stock market volatility as an increase in the risk of

equity investment and consequently, they shift their funds to less risky assets. The issues of

price volatility have become increasingly important in recent times to the Indian investors,

regulators, brokers, policy makers, dealers and researchers. Share prices also affect the wealth

of households and their consumption.

1.1.1 Volatility

Volatility is a statistical measure of the dispersion of returns for a given security or

market index. It is generally measured either by using the standard deviation or variance

between returns from that same security or market index. Commonly, the higher the

volatility, the riskier is the security. In terms of option’s pricing, volatility is a variable in

option-pricing formula showing the extent to which the return of the underlying asset will

fluctuate between now and the option’s expiration. Volatility, expressed as a percentage

coefficient within option-pricing formula, arises from daily trading activities. How volatility

is measured, will affect the value of the coefficient used. The concept of volatility refers to a

variable degree of unpredictable change over time. To most investors, risk represents the

variability of an asset’s price. It is typically expressed as the standard deviation of the change

in value of an asset over a given period, typically one year. Volatility, therefore, reflects the

risk taken by someone with exposure to said variable or asset. The more volatile the price of

an asset, the riskier the asset will be. Volatility is much more than the standard deviation of

an asset’s price over time. It is a critical input in valuing options and other derivative

instruments. As such, measures of volatility - historical and prospective - impact the

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

3

valuation and return of a wide range of financial instruments, from interest rates to futures. It

also acts as a barometer of investor sentiment: while high levels of volatility indicate investor

nervousness, low volatility signals a stronger appetite for risk. As a concept, volatility is

simple and intuitive. It measures the variability or dispersion about a central tendency. In

other words, it measures how for the current price of an asset deviates from its average past

values. The study of volatility becomes more important due to the growing linkages of

national markets in currency; commodity and stock with rest of the world markets and

existence of common players have given volatility a new property- that of its speedy

transmissibility across markets.

To many, among the general public, the term volatility, is simply synonymous with

risk: in their view high volatility is to be deplored, because it means that security values are

not dependable and the capital markets are not functioning as well as they should. By

volatility, public seems to mean days when large market movements, particularly down

moves, occur. These precipitous market wide price drops cannot always traced to a specific

news event. Nor should this lack of smoking gun be seen as in any way anomalous in market

for assets like common stock, whose value depends on subjective judgment about cash flow

and resale prices in highly uncertain future. The public takes a more deterministic view of

stock prices; if the market crashes, there must be a specific reason. Asset return variability

can be summarized by statistical distributions. Typically, the normal distribution is used to

characterize a series of returns. The distribution is centred at the mean and its width is

determined by the standard deviation. Return series may not be normally distributed and

often tends to exhibit excess kurtosis, so that extreme values are more likely than the normal

distribution would suggest. Such fat tailed distributions are common with financial

parameters. Skewness is also common, especially with equity returns, where big down moves

are typically more likely than comparable big up moves.

1.1.2 Nature of Stock Market Volatility in Emerging Markets

Emerging markets found to have four distinguishing features: average returns were

higher, correlations with developed markets returns were low, returns were more predictable

and volatility is higher. They argued that Modeling volatility is difficult in emerging markets,

especially in segmented markets. In fully integrated markets, volatility is strongly influenced

by world factors, whereas in segmented markets, it is strongly influenced by local factors.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

4

More open economies had lower volatility and political risk to a large extent explained the

cross sectional variation in volatility. Finally, they found significant decline in volatility in

emerging markets following capital market liberalization. Bekaert et al. (1998) argued that

emerging markets returns are highly non- normally distributed and exhibit positive skewness

in it.

Generally, the security prices reflect the performance of a company. Both economic

and non-economic factors invariably affect stock return behaviour. Cootner (1964) says that

the prices of securities are typically very sensitive, responsive to all events, both real and

imagined. Again a major factor responsible for stock return fluctuations is speculative

purchase and sale by Foreign Institutional Investors. Indian financial institutions also play a

major role in equity market leading to stock return fluctuations. Many theories have come up

which have empirically verified the investors’ behaviour at the international as well as at the

Indian context. In the present study, it is attempted to test the volatility behaviour, taking 37

companies as the sample size.

Volatility, in simple words, is the variation in the price of financial assets during a

period of time. It is the amount by which the price of a financial asset such as share of a

company has fluctuated or is expected to fluctuate during a period. Thus, it is clear that

volatility measures variability or dispersion. In other words, it measures the deviation from its

average past price. Greater the deviation, the greater is the volatility. Volatility is the measure

of risk and can be used to measure the market risk of an individual asset or an entire portfolio.

Volatility of the financial markets remains a concern for investors, policy makers and

regulators. The concern about volatility stems from the fact that price of an asset under

volatile conditions no longer plays its role as a ‘signal’ about the true value of a firm, a

concept that is core paradigm of the informational efficiency of markets. Volatility is closely

associated with the notion of risk. Risk and uncertainty play critical role in economics. Many

economic models assume that the variance, as a measure of risk and uncertainty, is constant

over time. However, many empirical studies investigating behaviour of returns and volatility

have shown that variance is not constant over time. Most stock returns data are characterized

by a feature called volatility clustering where large volatility tend to be followed by large

volatility and small volatility tend to be followed by small volatility. Thus, volatility can be

predicted as it is determined by the immediate past. In order to model volatility, it is necessary

to formulate an appropriate model not only for variance but also for mean of the data. Engle

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

5

(1982), developed autoregressive conditional heteroscedastic (ARCH) model to capture time

varying variance that has proven to be very useful for Modeling the variance of stock returns

data. The seminal work on ARCH process by Engle (1982) to model volatility and its

generalized from (GARCH) by Bollerslev (1986), has paved a new way of Modeling of

volatility. Much of the empirical work after this has used these models and their various

extensions to incorporate other aspects such as negative asymmetry that is commonly found in

stock return data. This study concentrates on these basic GARCH and asymmetric GARCH

models and evaluates their applicability to some recent Indian stock market data during the

period of the US sub-prime crisis.

Table - 1.1

Volatility* of Major Indices in India

Year/Index BSE

Sensex BSE-100 BSE-500

CNX

Nifty

CNX Nifty

Junior CNX 500

2000-01 2.2 2.4 2.4 2.0 2.8 2.3

2001-02 1.5 1.6 1.6 1.4 1.6 1.6

2002-03 1.0 1.0 1.0 1.0 1.2 1.0

2003-04 1.4 1.5 1.5 1.4 1.6 1.5

2004-05 1.5 1.5 1.6 1.6 1.8 1.7

2005-06 1.0 1.0 1.0 1.0 1.1 1.0

2006-07 1.8 1.8 1.7 1.8 2.1 1.7

2007-08 1.9 2.0 2.0 2.0 2.4 2.0

2008-09 2.8 2.7 2.6 2.7 2.8 2.5

2009-10 1.9 1.8 1.8 1.9 2.0 1.8

2010-11 1.1 1.1 1.1 1.1 1.1 1.0

2011-12 1.3 1.3 1.2 1.3 1.3 1.2

Source: BSE & NSE * Volatility is calculated as the standard deviation of the natural log of returns in indices for

the respective period.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

6

1.1.3 Forecasting Efficiency of Implied Volatility

The forecasting efficiency of implied volatility is the contemporary phenomenon in

Indian option market. Market expectations are reflected in the option prices about the

distribution of the future value of underlying assets. Under a rational expectations

assumption, the market uses all the information available to form its expectations about future

volatility. Therefore, the market option price displays the market’s true volatility estimate.

Furthermore, the implied volatility is the best possible forecast in case market is efficient.

That is, implied volatility subsumed all necessary information generated by other explanatory

variables to explain future realized volatility. In forecasting volatility, two approaches are

followed. One is the historical variance of the future return and the second is to elicit market

expectations about the future volatility from observed option prices.

Under the assumption that option pricing model correctly represents investors’

behaviour, in deriving the implied volatility from observed option prices and other observable

variables. When the market is informationally efficient, the implied volatility should reflect

the information contained in historical volatility. Hence, forecasts based on historical

volatility should not outperform forecasts based on implied volatilities.

1.1.4 Conceptual Framework of Volatility

The emergence of globalization, leads to stock market booms and the volume of

transactions multiplies its previous quantum, which put the investors, technical analysts,

economists and academicians on high alert for deep studies and understanding the behaviour

of stock market minutely. The stock market development in a nation represents the optimistic

behaviour of investors over there, and the economic development of the nation. With the

liberalization, more and more countries provided access to investors in their markets; one day

number of opportunities comes up for investment in their domestic and foreign markets.

Development of stock markets provides investors with lucrative opportunities to

invest in diversified portfolios across the world. Global investment decisions are taken,

depending upon several aspects, but the knowledge of volatility of market, is a vital aspect

for making smart decisions to get maximum return with minimum risk.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

7

Globalization enables the investors to make better portfolios in global markets.

Volatility remains high in a single nations portfolio when comparison to international

portfolios in global markets due to economic and political environments, industrial and

business growth rates and inflationary conditions.

To measure the extent of risk involved in an investment, one has to check for the

extent of volatility. It could be said that volatility is the most basic statistical measure of risk.

It can be used to measure the market risk of a single instrument or an entire portfolio of

instruments. The volatility of an asset indicates the variability of its returns. In day to day

practice, volatility is calculated for all sorts of random financial variables such as stock

prices, interest rates, exchange rates, the market value of a portfolio, etc. Stock market

volatility means different things to different people. Most academic studies have defined

volatility in term of statistical measure of the variability of the stock price changes. These

measures are useful because they correspond to standard measure of risk in theories of

portfolio selection and asset pricing. Many investors seem more apt to define volatility as

episode of extreme or rapid price movements within certain days - even if these incidents do

not noticeably affect measure of volatility calculated over longer time periods. Volatility is

defined in term of statistical measure of the variability of percentage price changes or rate of

return. The most commonly used statistical measure of the volatility is the standard deviation

or variance of return. The standard deviation measure the dispersion of return or the degree to

which they vary from period to period, the period being a month, day and even hour or

minute. Thus volatility can be calculated for month to month returns, day to day returns and

even minute to minute returns.

1.1.5 Volatility and Liquidity

Much research has been devoted to modeling and forecasting the volatility of

financial returns, and yet few theoretical models explain how volatility comes to exist in the

first place. Roll (1984) shows that volatility is affected by market microstructure. Glosten and

Milgrom (1985) shows that at least one source of volatility can be explained by the liquidity

provision process. When market makers infer the possibility of adverse selection, they adjust

their trading ranges, which in turn increase the band of price oscillation.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

8

1.1.6 Volatility and Direction

Volatility is immune to the directional change which measures merely their dispersion

when calculating standard deviation (or variance) and all differences are squared, so that

negative and positive differences are combined into one quantity. Two instruments with

different volatilities may have the same expected return, but the instrument with higher

volatility will have larger swings in values over a given period of time.

1.1.7 Volatility over time

It is common knowledge that types of assets experience periods of high and low

volatility. That is, during some period prices go up and down quickly, while during other

times they might not seem to move at all. Periods when prices fall quickly (a crash) are often

followed by prices going down even more, or going up by an unusual amount. Also, a time

when prices rise quickly (a bubble) may often be followed by prices going up even more, or

going down by an unusual amount. The converse behaviour, the 'doldrums' can last for a long

time as well. Most typically, extreme movements do not appear 'out of nowhere'; they're

presaged by larger movements than usual. This is termed autoregressive conditional

heteroskedasticity. Of course, whether such large movements have the same direction, or the

opposite, is more difficult to say. And an increase in volatility does not always presage a

further increase - the volatility may simply go back down again.

1.1.8 Volatility for Investors

Investors care about volatility for five reasons which are mentioned as follows:

1. The wider the swings in an investment's price the harder emotionally it is not to

worry.

2. When certain cash flows from selling a security are needed at a specific future date,

higher volatility means a greater chance of a shortfall.

3. Higher volatility of returns while saving for retirement results in a wider distribution

of possible final portfolio values.

4. Higher volatility of return when retired gives withdrawals a larger permanent impact

on the portfolio's value.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

9

5. Price volatility presents opportunities to buy assets cheaply and sell when overpriced.

In today's markets, it is also possible to trade volatility directly, through the use of

derivative securities such as options and variance swaps.

1.1.9 Benefits of Volatility

Volatility is often viewed as a negative phenomenon as it represents uncertainty and

risk. However, volatility can be good if it is peak and buys on the lows, one can make money,

with greater money coming with greater volatility. The possibility for money to be made via

volatile market is how short term market players like day traders hope to make money, and is

in contrast to the long term investment view of buy and hold. The dispersion (volatility) may

be in any direction; it benefits the one and harms the other out of the buyer and the seller.

Now it is the intelligence of the investor that how investor keeps themself as the beneficiary

out of the act of buying or selling. The importance of volatility is as follows:

� The importance of volatility in financial markets is much more than a measure of

investor’s sentiment. Volatility is important because it dramatically affects banks and

hedge funds' Value-at-Risk (VaR). VaR estimates the maximum a bank or hedge fund

can expect to lose over a specific time period at a given confidence interval. VaR is

the primary tool of risk management. Low volatility leads to low VaR, and high

volatility leads to high VaR. Banks and hedge funds' leverage ratios are generally tied

to VaR - the lower an institution's VaR, the more it can lever up. More importantly for

right now, the higher an institution's VaR, the less leverage it can use.

� The importance of volatility is that, it has the single biggest effect of the amount of

extrinsic value in an option's price. When volatility goes up (increases), the extrinsic

value of both the calls and the puts increase. This makes all the option prices more

expensive. When volatility goes down (decreases), the extrinsic value of both the calls

and the puts decrease. This makes all of the option prices less expensive.

� Mobilizing funds from savers and regulating it up to investors is one of the key

functions of financial markets and institutions of an economy. Some volatility in the

prices of financial assets is a normal part of the process of allocating investible funds

among competing users. However, excessive or extreme volatility of stock returns,

interest rates or exchange rates may be detrimental because such volatility may impair

the smooth functioning of the financial system and adversely affect the economic

performance of economy.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

10

� Volatility has become a matter of concern because when the asset prices fluctuate

sharply over time periods as short as one day, investors may find it difficult to accept

that the explanation for changes lies in information about fundamental economic

factors, and hence, they may associate pure speculation and irrationality with the

market. This can lead to general erosion of investor confidence and flow of capital

away from equity markets.

� The rise in volatility will tend to raise the risks faced by market makers, leading them

to charge correspondingly more for the liquidity they provide.

� Volatility is perceived as an indicator of market inefficiency and a potential threat to

the very integrity of the market mechanism.

The wide spread concern in the market place has underlined the importance of being

able to measure and predict stock market volatility to market participants.

1.1.10 Causes of Volatility

A high frequency of crisis is closely associated with higher macroeconomic volatility

and is just another aspect of higher macro-financial risks and vulnerabilities. In addition to

output forgone during these crises, which entails major welfare losses, there is significant

evidence than such crises have lasting effects on growth because of irreversible losses of

physical, organizational, and human capital. Stock prices are established in the marketplace,

but what exactly causes them to behave the way they do? Here are several factors that

influence their movements.

1) Latest Information on Stock Prices

Information is a crucial factor in the movement of stock prices as it is what the market

uses to put a value on a stock at a certain price level. These are usually based on all data that

the public has been made aware of. As the information is updated, the market adjusts the

prices up or down depending on the way the market interprets that the information will affect

the company's future earnings ability.

2) Inflation and Stock Prices

Inflation is another influential factor that affects the motion of stock prices. History

indicates that there had been a strong inverse correlation between low inflation and

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

11

valuations. This is because low inflation propels high multiples and high inflation drives low

multiples.

3) Economic Strength of Market and Peers

Company stocks have the propensity to track with the market, as well as with their

sector or industry contemporaries. A lot of leading investment firms put significant

importance on overall market and sector movements as major factors involved in the

movement of prices. An example would be when a negative outlook for one stock affects

other similar ones due to mere association with each other, dragging the demand for the

whole sector along the way.

4) Psychological Issues on Stock Prices

These prices are also greatly influenced by human behaviour. Greed is one trait that

can cause stock prices to increase more than it should. New information can elicit a frantic

market, may cause an increase in prices, and may make investors disregard rational valuation,

preferring instead to buy the stock to ensure they are not left behind. Fear can cause

significant decreases in stock prices when investors rush for the exit in an effort to avoid

losses. This factor is probably the most important factor in determining the volatility of the

market at any given time.

5) Supply and Demand

Stocks that trade smaller volumes of shares do not have the liquidity of the more

popular stocks. So, prices for these smaller ones are prone to fluctuations because of supply

and demand. When a large shareholder wants to sell a large quantity of shares into a market

with weak liquidity, that shareholder can considerably move share price.

6) Uncertainty

The movement of stock prices is also affected by a vague future. Prices do tend to

bounce around a bit due to market apprehension and the unpredictable future. Because of the

ambiguity of a company's future, volatility in stock prices is possible even without new

information.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

12

7) Trading Volume

Trading in any financial asset is induced by the arrival of new information. As the

information is unobserved, price changes or/and trading activity can be used as proxy of

information. Trading volume is supposed to reflect information about aggregate changes in

the expectations of the market participants. Understanding the informational role of trading

volume and its relationship with price changes may help in devising short-term price forecast,

trading and hedging strategies and regulations. The issues like whether positive price changes

(volatility) is associated with higher volume as compared to negative price changes, whether

trading volume is leading the price change or price change is driving the trading volume in a

financial asset, are important from both theoretical as well as practical point of view. The

higher the volume, the narrower are the spreads, as a result, there is less slippage, and less

volatility.

8) Business condition

It is widely said that stock volatility increase during economic recession because

during recession, there is excess capacity and unemployment. Fixed cost for the economy

would have the effect of increasing the volatility of stock returns during period of low

demand. Therefore business conditions are the main cause of high and low volatility.

9) The Media

The media including newspaper, magazine, and news channels are the main source of

information which provides the financial news, views and advice of experts to the public.

These information and advice may influence the decision of investors and fund managers

which could lead to herd-type behaviour and stock price fluctuation. Media comment may

influence the timing of prices changes with or without influencing longer term movements.

10) Market Industry Concentration

Modern portfolio theory predicts a significant relationship between market industry

concentration and market volatility. High industry concentration in a market means less

diversification. Therefore, high industry concentration would lead to high market volatility.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

13

11) The Average Education Level of Investors

Investors typically exhibit a strong “home bias”. Given the existence of these bias,

local investors collective behaviour could be decisive in shaping stock market movements in

a country. Thus, the collective characteristics of investors that may influence their behaviour

should not be neglected, when one examines stock market fluctuations. We choose the

average education level of investors, which itself is represented by the school life expectancy

in a country, as a proxy for the collective characteristics of all investors in a market. Since

better-educated people may have better cognitive and analytical capability and thus behave

more rationally, therefore it is expected that the average education level of investors is

negatively related to market volatility.

12) International Integration

Increased integration has resulted in the removal of controls on the international

movement of capital by the government. The stocks of leading companies are now quoted on

foreign stock markets. Movements of one country stock prices are affected by the movement

of stock prices on overseas markets. Even the stock prices of one country are influenced by

the international events of their global counterparts, statement made by the US president,

international development and financial crises.

13) Computerized Trading

The remarkable advances in information technology have made it much easier for

large number of people to learn about and react to information very quickly. They have also

made it possible for financial markets to provide liquidity to investors around the world.

Since new information spread more quickly, the rate at which price change in response to

information would also accelerate.

14) The Relative Size of the Equity Market

The relative size of the equity market in a country is defined as:

CAP

GDPX 100

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

14

Where CAP is the total market capitalization of all listed firms in a market and GDP

is the Gross Domestic Production (GDP). Harvey (1995) argues that, in a larger market, noise

trading is probably offset more completely by one another and thus is less influential.

Therefore, market size would be related to market volatility. The larger the market size, the

more stable the market could be.

15) The Number of Listed Firms

On the one hand, the total number of listed firms may be positively related to market

industry concentration. It might be the case that the more firms listed, the more diversified

the market. On the other hand, it could also be true that the more firms listed, the larger the

relative market size. In either case, the number of listed firms could be negatively related to

market volatility.

16) Other Factor

One of the major reasons of volatility in stock market may be due to change in the

macroeconomic policies, regarding different variables like interest rate, money supply,

industrial production, foreign institutional investment, national income, exchange rate etc. If

there is any change in these variables then stock price will adjust accordingly. Other factor

which may influence volatility is attitude of the investor regarding risk.

1.1.11 Measurement of Volatility

Volatility is measured by variance or the standard deviation of stock returns around

their average value. When measuring the volatility, stock returns are taken rather than stock

prices because mean must be stable at the different time period while measuring the

dispersion around an average value. Another reason behind using return is that absolute price

changes are dependent on the price level. In order to symmetrically treat the up moves and

down moves, returns are calculated as the logarithmic difference of closing prices at the

beginning and end of one measurement period. In order to compare the volatilities over

different periods and over different countries, volatility is expressed as an annualized

percentage. To annualize the volatility, the number of trading days in a year must be used.

Also, volatility scales with the square root of time. So annualisation factor would be square

root of the number of trading days in a year.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

15

1.1.12 Modeling of Volatility

Modeling and forecasting of volatility of asset returns is important in various

applications related to financial markets such as valuation of derivatives, risk management,

etc. Extensive research has been done world over in Modeling volatility for estimation and

forecasting. There are broadly four possible approaches for estimating and forecasting

volatility. These are:

Traditional Volatility Estimators: These estimators assume that ‘true’ volatility is

unconditional and constant. The estimation is based on either squared returns or standard

deviation of returns over a period.

Extreme Value Volatility Estimators: These estimators are similar to traditional estimators

except that these also incorporate high and low prices observed unlike traditional estimators

which are based on closing prices of the asset.

Conditional Volatility Models: These models (ARCH/GARCH type models) take into

account the time-varying nature of volatility. There have been quite a few extensions of the

basic conditional volatility models to incorporate ‘observed’ characteristics of asset/ stock

returns.

Implied Volatility: In case of options, most of the parameters relevant for their valuation can

be directly observed or estimated, except volatility. Volatility is, therefore, backed out from

the observed option values and is used as volatility forecast.

Uncertainty plays an important role in economic theory. Many economic models

assume that the variance, as a measure of uncertainty, is constant through time. However,

empirical evidence rejects this assumption. Financial time series, such as stock returns or

exchange rates exhibit so called volatility clustering. This means that the large changes in

these series tend to be followed by large changes and small changes by small changes. The

technical term given to this behaviour is autoregressive conditional heteroskedasticity

(ARCH). As variance (or standard deviation) is often used as a risk measure in risk

management systems, accurate modeling and forecasting of the variance has received a lot of

attention in the investment community for the last two decades. In a seminal paper, Engle

(1982), for the first time, proposed to model time varying conditional variance with the

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

16

ARCH process that uses past disturbances to model the variances of the series and allows the

variance of the error term to vary over time. Bollerslev (1986) generalized the ARCH process

by allowing the conditional variance to be a function of prior period’s squared errors as well

as its past conditional variances. Following the introduction of models of ARCH by Engle

(1982) and their generalization by Bollerslev (1986), there have been numerous refinements

of the approach to modeling conditional volatility to better capture the stylized characteristics

of the data. Empirically, the family of GARCH (Generalized ARCH) models has been very

successful in describing the financial data. Of these models, the GARCH (1, 1) is often

considered by most investigators to be an excellent model for estimating conditional volatility

for a wide range of financial data.

Though, in most of the cases, the ARCH and the GARCH models are apparently

successful in estimating and forecasting the volatility of the financial time series data, they

cannot capture some of the important features of the data. The most interesting feature not

addressed by these models is the ‘leverage effect’ where the conditional variance tends to

respond asymmetrically to positive and negative shocks in errors. To solve this problem,

many nonlinear extensions of the GARCH model have been proposed. Nelson (1991)

proposed an exponential GARCH (EGARCH) model based on a logarithmic expression of

the conditional variability in the variable under analysis. Later, a number of modifications

were derived from this method. One of them is the Threshold ARCH (TARCH) method

which was introduced by Zakoian (1994). The model developed by Glosten, Jagannathan and

Runkle (GJR, 1993) has been considered the best in estimating the impact of positive and

negative shocks on volatility (Engle and Victor, 1993).

1.2 An Overview of Indian Capital Markets

1.2.1 Introduction

This chapter gives brief account of capital market developments in India under

various heads like Indian Capital Market before 1990s, Indian Capital Market after 1990s,

Primary Market Developments, Secondary Market Developments, SEBI registered market

intermediaries, Mutual Funds, Derivatives, Foreign Institutional Investments, Screen based

Trading System, Depositories, Clearing, Processing and Settlement system, Risk

Management System, Margin Trading Facility, Regulatory Frame work for investor

protection, Security Regulations in force, Security guidelines in force, Grievances Redressal

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

17

Mechanism, Investor Education, Recent initiatives and Indian capital markets future road

map. Capital market is the backbone of any country’s economy. It is an engine for economic

growth, providing an efficient means of resource mobilisation and allocation. The literature is

full of theoretical and empirical evidence that have established robust, statistically significant

two-way relationship between the developments in the securities market and economic

growth. Levine and Zervos (1991) argue that well developed stock markets may be able to

offer financial services of different kind that may provide a different kind of impetus to the

economic development1. In India, Agarwall’s (1999), study clearly supports the Levine and

Zervos’s argument and proves that the two main parameters of capital market development

namely, size and liquidity, are found statistically significant to explain the economic activity.

The Indian capital market is one of the oldest capital markets in the world. It dates

back to the 18th century when the securities of the East India Company were traded in

Mumbai and Kolkata. However, the orderly growth of the capital market began with the

setting up of The Stock Exchange of Bombay in July 1875 and Ahmedabad Stock Exchange

in 1984. Eventually 19 other Stock Exchanges sprang up in various parts of the country. In

this chapter an attempt has been made by the researcher to review the Capital Market

Developments.

1.2.2 Indian Capital Market – Before 1990s

India’s Capital Market was dormant till the mid – 1980s. The long term financing

needs of the corporate sector were met by the Development Financial Institutions (DFIs)

namely IDBI, IFCI, ICICI as well as by other investment institutions like LIC, UTI, GIC etc.

Working capital needs were met by the Commercial Banks through an elaborate network of

bank branches spread all over the country. Capital Market activities were limited mainly due

to the easy availability of loans from banks and financial institutions and administered

structure of interest rates. However, three important legislations namely Capital Issues

(Control) Act 1947: Securities Contracts (Regulation) Act, 1956; and Companies Act, 1956

were enacted to provide suitable legal framework for the development of capital market in

India. The pricing of the primary issues was decided by the Office of the Controller of

Capital Issues. A few stock exchanges, dominated by Bombay Stock Exchange (BSE)

provided the trading platforms for the secondary market transactions under an open outcry

system.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

21

In a deregulated regime, the market determines the price of the public issues, i.e.,

either by the issuer through fixed price or by the investors through book-building process. A

fair system of proportionate allotment of shares has been put in place. The share of retail

investors in the allotment of book-built issues has been increased to 35 per cent.

Discretionary allotment to the Qualified Institutional Buyers (QIBs) has been withdrawn.

Companies are allowed to issue ADRs/ GDRs and also raise funds through external

commercial borrowing. The ADR / GDR’s have two–way functionality. The Foreign

Institutional Investors have been allowed to invest in primary issues within the sectoral limits

set by the Government.

1.2.5 Secondary Market Developments

The securities issued in the Primary Market are traded in the Secondary Market.

Exchanges in India offer screen based on electronic trading. The trading system is connected

using the VSAT technology from around 201 cities. There are 8,652 trading members

registered with SEBI at the end of March 2009. Market capitalization as per cent to GDP in

India reached nearly 58 per cent in 2008–09 and still further on a fluctuating trend.

The rate of growth in market capitalisation and turnover over the period indicates that

more companies have started using the trading platform of the Stock Exchanges. Although

there are 22 stock exchanges, NSE and BSE together account for more than 99 per cent of the

total turnover. Enormous amount of developments have taken place in the secondary market

during the last one decade. The selected indicators given in Table-1.3 clearly indicate this.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

22

Table - 1.3

Performance of Secondary Markets from 2000 to 2012 – Selected Indicators

(Rs. in Million)

Year

Capital Market Segment of Stock Exchanges

No.

of Brokers

No. of

Listed

Companies

CNX

Nifty

S&P

Sensex

Market

Capitalisation

Market

Capitalisation

Ratio (%)

Turnover

Turnover

Ratio (%)

2000-01 9069 9877 1078.05 3739 740640 34.1 10233820 178.3

2001-02 9192 9871 1528.45 5001 11926300 84.7 20670310 173.3

2002-03 9782 9954 1148.20 3604 7688630 54.5 28809900 374.7

2003-04 9687 9644 1129.55 3469 7492480 36.4 8958180 119.6

2004-05 9519 9413 978.20 3048 6319212 28.5 9689098 153.3

2005-06 9368 8240 1771.90 5590 13187953 52.3 16204977 122.9

2006-07 9128 8645 2035.65 6492 16984280 119.1 16668963 98.1

2007-08 9519 9413 978.20 3048 6319212 28.5 9689098 153.3

2008-09 9335 9020 3402.55 11280 30221900 85.5 23901030 79.09

2009-10 9443 9431 3821.55 13072 35488081 86.0 29014715 81.76

2010-11 9487 6551 4734.50 15644 51497010 109.3 51308160 99.63

2011-12 9628 6856 3020.95 9708 30929738 58.1 38520970 124.54

Sources: SEBI Hand Book 2013

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

23

Table - 1.4

Monthly and Annual Averages of CNX Nifty from 2001 to 2012

(Base: November 3, 1995 = 1000)

Year/

Month Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Annual

2000-01 1469.03 1312.65 1451.74 1445.26 1350.94 1371.27 1201.60 1240.59 1291.43 1316.96 1371.91 1214.47 1336.49

2001-02 1116.41 1159.44 1107.15 1077.98 1069.01 949.43 953.92 1031.62 1075.87 1087.20 1138.17 1159.33 1077.13

2002-03 1120.74 1079.80 1065.90 1034.70 977.60 987.12 955.12 992.26 1074.25 1073.48 1055.84 1016.38 1036.10

2003-04 965.08 963.20 1068.59 1150.01 1261.13 1369.03 1506.10 1580.02 1740.06 1906.00 1848.67 1779.63 1428.13

2004-05 1848.45 1640.20 1506.12 1568.08 1615.30 1691.96 1794.98 1873.94 2021.94 1977.83 2067.39 2096.23 1805.26

2005-06 1987.10 2002.28 2134.29 2236.70 2357.56 2511.70 2486.78 2574.66 2772.61 2892.68 3019.48 3235.78 2513.40

2006-07 3494.06 3437.41 2914.91 3092.11 3305.58 3492.13 3649.43 3868.61 3910.18 4037.06 4083.74 3731.13 3572.44

2007-08 3947.28 4184.39 4222.17 4474.18 4301.36 4659.92 5456.62 5748.58 5963.57 5756.35 5201.56 4769.50 4896.60

2008-09 4901.91 5028.66 4463.79 4124.60 4417.12 4206.69 3210.22 2834.79 2895.80 2854.36 2819.21 2802.27 3731.03

2009-10 3359.83 3957.96 4436.37 4343.10 4571.11 4859.31 4994.11 4953.54 5099.74 5156.22 4839.57 5178.15 4657.77

2010-11 5294.76 5052.97 5187.78 5359.75 5457.24 5811.48 6096.11 6055.33 5971.32 5782.71 5400.92 5538.42 5583.54

2011-12 5839.09 5492.20 5472.64 5596.59 5076.74 5015.58 5060.02 5004.28 4782.36 4920.02 5409.09 5242.74 5248.74

Source: NSE

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

24

Table - 1.5

Annual Average of Share Price Indices and Market Capitalization from

2000 to 2012

Year Sensex CNX Nifty

Market Capitalization

( Rs. in Crores )

BSE NSE

2000-01 4270 1335 571553 657847

2001-02 3332 1077 612224 636861

2002-03 3206 1037 572198 537133

2003-04 4492 1428 1201207 1120976

2004-05 5741 1805 1698428 1585585

2005-06 8280 2513 3022191 2813201

2006-07 12277 3572 3545041 3367350

2007-08 16569 4897 5138014 4858122

2008-09 12366 3731 3086075 2896194

2009-10 15585 4658 6165619 6009173

2010-11 18605 5584 6839084 6702616

2011-12 17423 5243 6214941 6096518

Source: BSE, NSE

1.2.6 SEBI Registered Market Intermediaries

Various institutions / intermediaries associated with primary as well as secondary

markets such as merchant bankers, registrars to issues, portfolio managers, underwriters,

bankers to issues, stock exchanges, brokers and sub-brokers, share transfer agents,

depositories, FIIs, custodians, credit rating agencies, venture capital funds, collective

investment schemes including mutual funds have to register with SEBI and operate within the

guidelines issued from time to time. SEBI also promotes self-regulatory organizations. SEBI

registered market intermediaries from 2001 which are listed below in Table-1.6.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

25

Table -1.6

SEBI Registered Market Intermediaries from 2001 to 2012

Market Intermediates 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Stock Exchanges

(Cash Market) 23 23 23 23 22 22 21 19 19 19 19 20

Stock Exchanges

(Derivatives Market) 2 2 2 2 2 2 2 2 2 2 2 2

Stock Exchanges

(Currency Derivatives) - - - - - - - - 3 4 4 4

Brokers

(Cash Segment) 9782 9687 9519 9368 9128 9335 9384 8517 8652 8804 9235 9307

Corporate Brokers

(Cash Segment) 3808 3862 3835 3746 3733 3961 4101 3955 4079 4197 4593 4672

Sub Brokers

(Cash Segment) 9957 12208 13291 12815 13684 23479 27540 43874 62471 75378 83952 77165

Brokers

(Derivative) 519 705 795 829 994 1120 1258 1442 1587 1899 2301 2337

Foreign Institutional

Investors 527 490 502 540 685 882 997 1319 1635 1713 1722 1765

Custodians 14 12 11 11 11 11 11 15 16 17 19 19

Depositories 2 2 2 2 2 2 2 2 2 2 2 2

Depository Participants 335 380 438 431 477 526 593 654 714 758 805 823

Merchant Bankers 233 145 124 123 128 130 152 155 134 164 192 200

Bankers to an issue 69 68 67 55 59 60 47 50 51 48 55 56

Underwriters 57 54 43 47 59 57 45 35 19 5 3 3

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

26

Market Intermediates 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Debenture Trustees 37 40 35 34 35 32 30 28 30 30 29 32

Credit Rating Agencies 4 4 4 4 4 4 4 5 5 5 6 5

Venture Capital Funds 35 34 43 45 50 80 90 106 132 158 184 207

Foreign Venture Capital

Investors 1 2 6 9 14 39 78 97 129 143 153 175

Registrars to an Issue &

Share Transfer Agents 186 161 143 78 83 83 82 76 71 74 73 74

Portfolio Managers 39 47 54 60 84 132 158 205 232 243 267 250

Mutual Funds 39 38 38 37 39 38 40 40 44 47 51 49

Collective Investment

Schemes 0 0 0 0 0 0 0 0 1 1 1 1

Approved

Intermediaries(Stock

Lending Schemes)

8 10 4 3 3 3 3 2 3 2 2 2

Source: SEBI Hand Book 2013

As on 31st March 2012, there were 20 Stock Exchanges, 9307 Brokers (Cash Segment) and 77,165 Sub-brokers, over 9,000 Listed

Companies, 2 Depositories, 823 Depository Participants, 200 Merchant Bankers, 3 Underwriters, 5 Credit Rating Agencies and 1765 Foreign

Institutional Investors in India.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

29

��� ���� #�# ���� ���������� #��� ��� ��������� +"� ���-� � ����� ���$� �#���� ��� ���-�

�#�����,’=� ��$�� ����� ���������� �+������������������� �������%������$� � �����

��������:�������������� �+����������������������3 �"��������������� �����

1.2.9 Foreign Institutional Investments

���� 1����%� ��� ����� �������� �1����� ����� �������� �� ����� �� ����� �� ���6�

�������#�������� ������������������"������ ����� �������� ��#�����#��� �����# +����

��� ��������+�����3 �����������������������������������3 ��������������������������-���

���������+���� ����+"����������������������+������� ��������������������1�����

����%������������%����������������������������+���������+���

Table - 1.8�

Foreign Investment Inflows in India from 2000 to 2012

Year

A. Direct Investment B. Portfolio Investment Total (A +B)

(Rs.

Crores )

(Us $

Millions)

(Rs.

Crores )

(US $

Millions)

(Rs.

Crores )

(US $

Millions)

6888&8�� �8�5�� 6;�6� &65 � &��� �8�8�� 6;8��

688�&86� ����� 6�55� ����6� �86�� 66;58� 5����

6886&8�� ��;8�� ;86�� �6�8�� 6 �8� ��8�5� � ���

688�&8;� 6�6�5� ���8� ����� 686�� ��� ;� ��5��

688;&85� 6;�� � 58�5� ; ��� � �� 6��85� �8�;�

6885&8�� ����8� ;�66� 566 �� ��� � 6���� �5����

688�&8 � 6 ���� �85�� ;��5;� ���5� ��8;6� �5����

688 &8�� ��� ;� ����� 55�8 � �6;�6� �;���� 6�;5��

688�&8�� �8��� � 66�6�� �� ��� 88�� ��58�8� 6��6��

688�&�8� ���6 �� �;��6� �8� ;�� 6 6 �� 6;�8� � ������

68�8&��� ���;��� �5���� &������ &���55� � ���� 6�����

68��&�6� ���5;�� ;��;6� �5�8� � � �� ��5�8�� ��8��� Source: RBl Bulletin

1����%� ������� ������� +��� +"� ������ ������� ��� #�������� �������

��� �����4������5��8��)����������’�>���8���7�������������st�7�����68�6��1���������

+���+ ������������������� ��������������������������"�"��������#�����������������

��"�����������������������������-��#���6888&8��?�68��&�6�������������+���+����@�

�

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

30

Table - 1.9

Trends in FII Investment from 2001 to 2012

Year

Gross

Purchases

(Rs. in

Crores )

Gross

Sales

(Rs. in

Crores )

Net

Investment

(Rs. in

Crores )

Net

Investment

(US $ Mns)

Cumulative

Net

Investment

(US $ Mns)

6888&8�� ;85�� �;���� ����� 6��8� ��5���

688�&86� 588 �� ;��8�� � ��� ����� �5� ��

6886&8�� ; 8�6� ;;� 6� 6���� 5��� �5����

688�&8;� �;;�55� ��8��� ;5 �;� �8885� 65�;6�

688;&85� 6��5�� � �8 �� ;5��8� �8�56� ��6���

6885&8�� �;�� �� �8558�� ;�;� � ����� ;5�5 �

688�&8 � 56858�� ;����5� �8�;�� ��6�� 56; �

688 &8�� �;�8��� ������� ��� �� ��;;6� ������

688�&8�� ��;5 �� ��8���� &;5���� &��� � 5�8�6�

688�&�8� �;�;��� 8� �� �;6�5�� �8656� ������

68�8&��� ��65��� �;��5�� �;�;��� �666�� �6�55��

68��&�6� �6�6�5� �6 5�6� �� 65� ���6�� �;8;�6�Source: SEBI

����� � ���������������+"�1�������������������’�>��������7��������������

���7�����68�8��� ���������������� �’� >���;8�;�6�7������+"����������7�����68�6��,��

�������+"�1��������� ������� %��"��’�>��8�(������������������������������ ����

"�����������������%��������"�������� +������:����7���������68�8����� �+������

1������%�����������’=(��������������������� �������������������5�+"����������7�����

68���� :+� � ;�� #��� ��� ��� ���� 1���� ���%���� ����� ��� �’:�� ��������� +"� ��� �0���������������

����#���������

2 ��%� ��� ���� ��� ��� ����� "������ ��� 1���� ����� ��������� ����� ��� �� #���������

��������� ’��%� ������������� � ��������� ���� ��+��� �-� ������� ��������

��� �������������������� ��%�%����#�������� ��������+�� ��������� ����"�%��� �������

���%��#���������������+"����1�������������

�

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

31

1.2.10 Screen Based Trading System

���� ������ +����� ����%� �"���� ��� �� ������$� ��������� � ��� ��� ����� ��#����

���$�������,’=����� ������������&+���������%��������� ���#������������+"������

���$� �-���%���� ���� �����&+����� ����%� ��+���� ��� #�����#��� ���� ������ ����������

��"�� ����������&��������������������� ���#����������8�888����������#����������

;88������������������+��������������#����#�����+�%%�������%�����$����"��� �"����

��� ������� ���� ������ �����%� ��� ���� �����"� �� #����A� ����#�����"�� ���� �����&+�����

����%� ��� ���#���� ��� #�������� �3 ��� ������� �� ���� �������� �����#������ ��� �����

%��%��#���������������’����&+���������%� ������%������"� ��#��������#�� �����3 ���"�

���������$���

1.2.11 Depositories

2�#���������:������������ ������������$�������#��� ����� ��� ��"��������B��

��#���� ���$��� ���������� ��� ��#��������� ����"�� )�� ��� 2�#�����"� ’�������� .������

�)2’.�����,������’�� ������2�#�����"�.�������,’2.���������� #��)2’.����,’2.�

�����+���� ������ �����������������/���������� ������������-��������#������������

�������$����#����/�����) ����"���������������������#��������"�������� %��+��$&

��"� ������ ����� ���� ������ ��"� ��#������ ��� �#����� ��� ���"� ��� ��� ��"� ��� ���

��������"�����:+� ������#�����������������(’=�����88�#�����������������,’=����

����� �� ��+��� ���8� ���� � ����"� ������ ��� %�� �������"�� ������ ��� #����+��� ��"� � �� ��

����������/�����������#�+"���������#����������

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

32

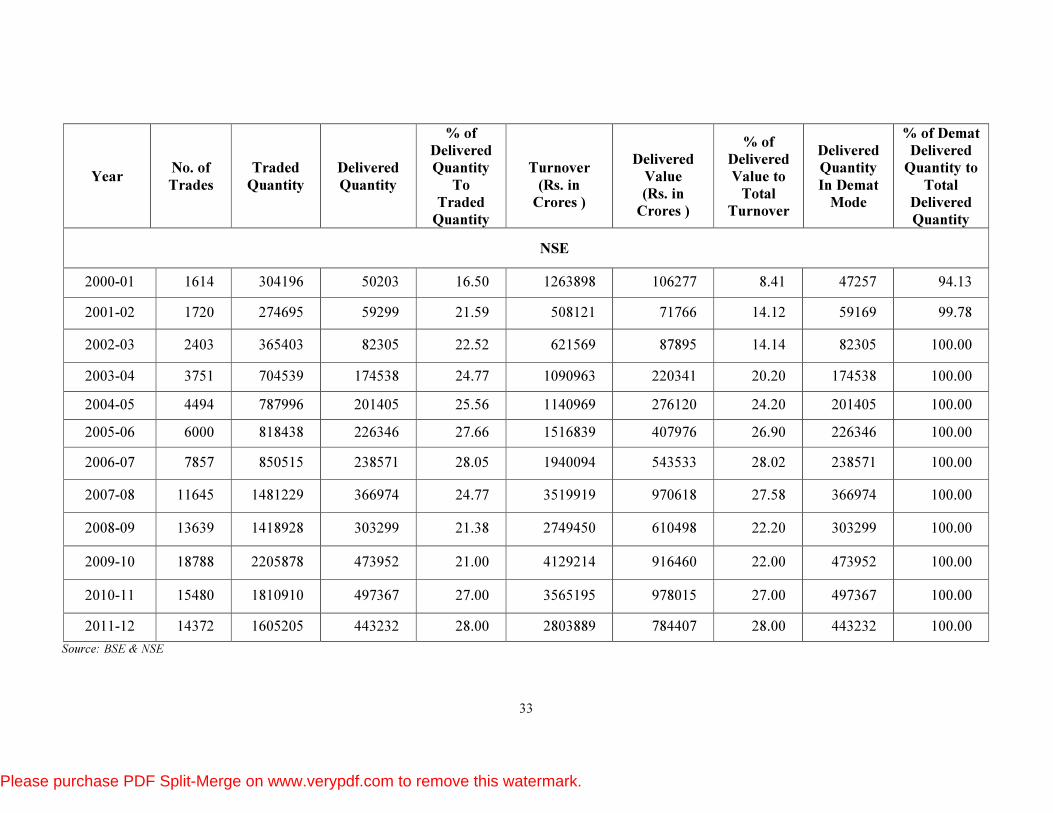

Table - 1.10

Settlement Statistics for Cash Segment of BSE and NSE from 2000 to 2012

Year No. of

Trades

Traded

Quantity

Delivered

Quantity

% of

Delivered

Quantity

To

Traded

Quantity

Turnover

(Rs. in

Crores )

Delivered

Value

(Rs. in

Crores )

% of

Delivered

Value to

Total

Turnover

Delivered

Quantity

In Demat

Mode

% of Demat

Delivered

Quantity to

Total

Delivered

Quantity

BSE

2000-01 1428 258511 86684 33.53 1000032 1666941 16.69 - -

2001-02 1277 182196 57668 31.65 307292 59980 19.52 - -

2002-03 1413 221401 69893 31.57 314073 48741 15.52 - -

2003-04 2005 385806 133240 34.54 503053 107153 21.30 132941 99.78

2004-05 2374 477171 187519 39.30 518716 140056 27.00 187347 99.91

2005-06 2643 664467 300653 45.25 816074 271227 33.24 300497 99.95

2006-07 3462 560780 229685 40.96 956185 297660 31.13 229573 99.95

2007-08 5303 986009 361628 36.68 1578855 476196 30.16 361542 99.98

2008-09 5408 739601 196630 26.59 1100074 230332 20.94 196096 99.73

2009-10 6056 1136513 363578 32.00 1378809 311364 23.00 363500 100.00

2010-11 5285 990776 376890 38.00 1105027 302126 27.00 374277 99.00

2011-12 3944 654137 255999 39.00 667498 181560 27.00 255990 100.00

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

33

Year No. of

Trades

Traded

Quantity

Delivered

Quantity

% of

Delivered

Quantity

To

Traded

Quantity

Turnover

(Rs. in

Crores )

Delivered

Value

(Rs. in

Crores )

% of

Delivered

Value to

Total

Turnover

Delivered

Quantity

In Demat

Mode

% of Demat

Delivered

Quantity to

Total

Delivered

Quantity

NSE

2000-01 1614 304196 50203 16.50 1263898 106277 8.41 47257 94.13

2001-02 1720 274695 59299 21.59 508121 71766 14.12 59169 99.78

2002-03 2403 365403 82305 22.52 621569 87895 14.14 82305 100.00

2003-04 3751 704539 174538 24.77 1090963 220341 20.20 174538 100.00

2004-05 4494 787996 201405 25.56 1140969 276120 24.20 201405 100.00

2005-06 6000 818438 226346 27.66 1516839 407976 26.90 226346 100.00

2006-07 7857 850515 238571 28.05 1940094 543533 28.02 238571 100.00

2007-08 11645 1481229 366974 24.77 3519919 970618 27.58 366974 100.00

2008-09 13639 1418928 303299 21.38 2749450 610498 22.20 303299 100.00

2009-10 18788 2205878 473952 21.00 4129214 916460 22.00 473952 100.00

2010-11 15480 1810910 497367 27.00 3565195 978015 27.00 497367 100.00

2011-12 14372 1605205 443232 28.00 2803889 784407 28.00 443232 100.00

Source: BSE & NSE

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

34

1.2.12 Clearing, Processing and Settlement System

The setting of the Clearing Houses / Clearing Corporations (CCs) has been a critical

institutional arrangement to improve the market microstructure of the Indian stock market.

NSE has a dedicated subsidiary namely, National Securities Clearing Corporation Limited

(NSCCL) which performs the role of a central counterparty. The CCs provide full innovation

with multilateral netting. Trade and Settlement Guarantee Funds have been set up to

guarantee settlement in case of default by brokers. There is also a system of security lending

and borrowing to obviate settlement risk. As CCs provide guaranteed settlement; there is no

counterparty risk in India. Moreover, India is one of the few countries of the world to

implement full- fledged Straight Through Processing (STP). The STP has been made

mandatory for all institutional trades.

Another notable achievement has been the short ending of the settlement cycle and

adoption of the rolling settlement. The settlement cycle was as high as 14 days for specified

scripts and 30 days for others. The settlement risk was very high as many things can happen

between the transaction and the settlement. Initially, the settlement cycle was reduced to a

week. Thereafter the settlement vehicle was further reduced to T+3 from April 2002 and to

T+2 from April 2003. Efforts are being made to reduce the settlement cycle further to T+1

basis. India’s settlement cycle is one of the best in the world.

1.2.13 Risk Management System

SEBI has put in place a comprehensive risk management system. The major features

of the dynamic risk management system include, interlaid, capital adequacy norms, trading

and exposure limits, margin requirement based or mark to market and VaR based margins,

market-wide circuit filters, on-line position monitoring and automatic disablement of broker’s

terminals. Indian capital market remained insulated against the South-East Asian meltdown in

the late 1990s. The 17th May 2004, crash of the stock market in India was short-lived due to

comprehensive risk management system. The T+2 trading cycle, settlement guarantee funds,

guaranteed settlement by CCs together with risk management system have significantly

reduced the risk perception of the Indian stock market.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

35

1.2.14 Margin Trading Facility

SEBI has allowed the member brokers to provide margin trading facility to their

clients in the cash segment since 1st April 2004. Securities with mean impact cost of less than

or equal to one and traded at least 80 per cent of the days during the previous 18 months

would be eligible for margin trading. Only corporate brokers with net-worth of at least Rs. 3

Crores would be eligible to offer this facility after obtaining prior permission from the

exchanges.

1.2.15 Regulatory Framework for Investor Protection

Investors are the major stakeholders in the securities market. It is mandatory for SEBI

to protect the interests of the investors. As a matter of fact, protection of investors’ interest is

pursued by the securities market regulators throughout the world. Although the objective is

more or less the same for most of the regulators, the means to achieve it varies from one

jurisdiction to another. In India, one of the major achievements has been to shift from merit-

based regime to disclosure-based regime. SEBI issued Disclosure and Investor Protection

(DIP) Guidelines in 2000 and amended the same from time to time keeping in view the

investors’ interest. The disclosure norms in India are considered as one of the best in the

world. Listed companies have to comply with the disclosure norms on an initial as well as on

a continuous basis. The major objectives of the disclosure norms have been to ensure

transparency and provide adequate protection to the investors.

Pricing of the public issues has been deregulated, since the early 1990s. In a

deregulated regime, disclosures play a crucial role for the investors to take informed

decisions about their investment. Nevertheless, many companies, which flooded the primary

market in the early 1990s, have vanished. Hence, the disclosure norms have been tightened

from time to time. Disclosure ought to be done on the stock exchange in addition to filing of

regular returns to stock exchange where it is listed, as well as to the Registrar of Companies.

Any price sensitive information about the company disclosed elsewhere attracts penal action.

Moreover, unfair trade practices, including insider trading, is prohibited in India, in

order to provide a level playing field to all investors. If any person indulges in fraudulent and

unfair practices, he shall be liable to a maximum penalty of Rs. 25 Crores or three times the

amount of profits made out of such practices, whichever is higher.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

36

There is a system of proportional allotment of public issues in India. In case of fixed

price public issues, 50 per cent shares are being allotted to the retail investors. In case of

book-built issues, the share of allotment for the retail investors has been raised from 25 per

cent to 35 per cent. Keeping in view the possible misuse, the discretionary allotment to the

Qualified Institutional Buyers (QIBs) has been withdrawn. In a move towards providing a

level playing field, QIBs have been asked to deposit 10 per cent of the bid amount.

SEBI has given in-principle approval for the introduction of IPO grading at the option

of the issuer. IPO grading would be done by credit rating agencies registered with SEBI. The

grading is intended to be an independent and unbiased opinion of the concerned agency. It

would be a onetime exercise and would focus on assisting the investor, particularly the retail

investors, for taking informed investment decision, SEBI will not certify the assessment made

by the rating agency. An issuer, who has opted for IPO grading, has to disclose all grading in

the offer document. Cost of IPO grading can be met by stock exchanges or out of the corpus

maintained for Investor Education and Protection Funds.

It has been recognised the world over that investors’ protection can be strengthened

by adhering to high corporate governance standards. Corporate governance standards

prescribed in India are based on international best practices. Following recommendations of

the expert committees, SEBI prescribed several governance standards to be achieved by the

companies by 31st December 2005, under the revised Clause 49 of the Listing Agreement

with the stock exchanges. Violation of this would now attract penalty under the Listing

Agreement. Corporate governance needs to be seen not as compliance, but as a way of life. In

this context, the quality of compliance assumes significance. High corporate governance

standards are not only desirable within the economy, but also helpful for companies accessing

the international capital market. SEBI gives utmost importance to the corporate governance

including mandatory induction of independent directors.

The governance standards of the stock exchanges are also being improved through the

process called Corporatisation and Demutualisation (C & D) of stock exchanges. The stock

exchanges, world over, have been generally formed as mutual organisations. The ownership,

trading rights and management are often vested with the same set of persons. This leads to

conflicting interest between ownership and management. In order to segregate the

management function from the ownership and trading rights, there is a need for

demutualisation of stock exchanges. Moreover, stock exchanges should function as body

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

39

same on plain paper. Investors who visit the SEBI offices or access the investor helpline are

guided regarding the appropriate authority to lodge their complaints which are outside the

jurisdiction of SEBI. An account of receipt and redressal of investor grievances by SEBI is

highlighted in Table below:

��������

�� �������������������������������������� ����������������������

������������ ����� ������ ������� ������������� � � �������

���������������!"��# ���$��%��

&����� � � ������ # ���$��%��&����� � � ������

1991-92 18794 18794 4061 4061 21.6

1992-93 110317 129111 22946 27007 20.9

1993-94 584662 713773 339517 366524 51.4

1994-95 516080 1229853 351842 718366 58.4

1995-96 376478 1606331 315652 1034018 64.4

1996-97 217394 1823725 431865 1465883 80.4

1997-98 511507 2335232 676555 2142438 91.7

1998-99 99132 2434364 127227 2269665 93.2

1999-00 98605 2532969 146553 2416218 95.4

2000-01 96913 2629882 85583 2501801 95.1

2001-02 81600 2711482 70326 2572129 94.9

2002-03 37434 2748916 38972 2611101 95.0

2003-04 36744 2785660 21531 2632632 94.5

2004-05 54435 2840095 53361 2685993 94.6

2005-06 40485 2880580 37067 2723060 94.5

2006-07 26473 2907053 17899 2740959 94.3

2007-08 54933 2961980 31676 2772577 93.6

2008-09 57580 3019560 75989 2848566 94.3

2009-10 32335 2706895 42742 2546302 94.1

2010-11 56670 2763565 66552 2612854 94.5

2011-12 46548 2810113 53841 2666695 94.9

Sources: SEBI Hand Book 2013

During the period 1991-92 to 2011-12, the SEBI received 28,10,113 grievances from

the investors of which a total of 26,66,695 grievances were redressed by the respective

entities, indicating a redressal rate of 94.9 per cent.

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

44

����������

:��������,-�,���.�����������������’st�#� ����������

;��,��� ;.����� ������.�,���� ;� ���9��� ���.�

1 ACC ACC Ltd. Cement & Cement Products

2 AMBUJACEM Ambuja Cements Ltd. Cement & Cement Products

3 ASIANPAINTS Asian Paints Ltd. Paints

4 AXISBANK Axis Bank Ltd. Banks

5 BAJAJ-AUTO Bajaj Auto Ltd. Automobiles

6 BANKBARODA Bank of Baroda Banks

7 BHEL Bharat Heavy Electricals Ltd. Electrical Equipment

8 BPCL Bharat Petroleum Corporation Ltd. Refineries

9 BHARTIARTL Bharti Airtel Ltd. Telecommunication

10 CAIRN Cairn India Ltd. Oil Exploration / Production

11 CIPLA Cipla Ltd. Pharmaceuticals

12 COALINDIA Coal India Ltd. Mining

13 DLF DLF Ltd. Construction

14 DRREDDY Dr. Reddy's Laboratories Ltd. Pharmaceuticals

15 GAIL GAIL (India) Ltd. Gas

16 GRASIM Grasim Industries Ltd. Cement & Cement Products

17 HCLTECH HCL Tech Numberlogies Ltd. Computers - Software

18 HDFCBANK HDFC Bank Ltd. Banks

19 HEROMOTOCO Hero Motor Corporation Ltd. Automobiles

20 HINDALCO Hindalco Industries Ltd. Aluminium

21 HINDUNILVR Hindustan Unilever Ltd. Diversified

22 HDFC Housing Development Finance

Corporation Ltd. Finance - Housing

23 ITC ITC Ltd. Cigarettes

24 ICICIBANK ICICI Bank Ltd. Banks

25 IDFC IDFC Ltd. Financial Institution

26 INDUSINDBK IndusInd Bank Ltd. Banks

27 INFY Infosys Ltd. Computers - Software

28 JPASSOCIAT Jaiprakash Associates Ltd. Construction

29 JINDALSTEL Jindal Steel & Power Ltd. Steel and Steel Products

30 KOTAKBANK Kotak Mahindra Bank Ltd. Banks

31 LT Larsen & Toubro Ltd. Engineering

32 LUPIN Lupin Ltd. Pharmaceuticals

33 M&M Mahindra & Mahindra Ltd. Automobiles - 4 Wheelers

34 MARUTI Maruti Suzuki India Ltd. Automobiles - 4 Wheelers

35 NMDC NMDC Ltd. Mining

36 NTPC NTPC Ltd. Power

37 ONGC Oil & Natural Gas Corporation Ltd. Oil Exploration / Production

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

45

38 POWERGRID Power Grid Corporation of India

Ltd. Power

39 PNB Punjab National Bank Ltd. Banks

40 RANBAXY Ranbaxy Laboratories Ltd. Pharmaceuticals

41 RELIANCE Reliance Industries Ltd. Refineries

42 RELINFRA Reliance Infrastructure Ltd. Power

43 SESAGOA Sesa Goa Ltd. Mining

44 SBIN State Bank of India Ltd. Banks

45 SUNPHARMA Sun Pharmaceutical Industries Ltd. Pharmaceuticals

46 TCS Tata Consultancy Services Ltd. Computers - Software

47 TATAMOTORS Tata Motors Ltd. Automobiles - 4 Wheelers

48 TATAPOWER Tata Power Co. Ltd. Power

49 TATASTEEL Tata Steel Ltd. Steel and Steel Products

50 WIPRO Wipro Tech Numberlogies Ltd. Computers - Software

Sources: NSE

1.3.2 Profile of Select CNX NIFTY Companies

� ����:�������

ACC Limited (ACC) is engaged in manufacture of cement. The Company is also

engaged in the manufacture of ready mixed concrete. During the year ended December 31,

2011, the Company produced 2,01,954 metric tons of Portland Slag Cement (PSC). During

49

In 2012 consolidated revenues increased by 30% to Rs. 96.7 Billion, Net income US $ 300

Million, Diluted Earnings Per Share (EPS) increased to Rs. 83.8 Crores.

� ���:!�������:�������

It is the largest state-owned natural gas processing and distribution company

headquartered in New Delhi, India. It has six segments: Transmission services of natural gas

and Liquefied Petroleum Gas (LPG), Natural gas trading, petrochemicals, LPG and Liquid

hydrocarbons, GAILTEL and Others. The company possessing a well developed and efficient

infrastructure was established as a wholly owned company of the Government of India in

August, 1984 with 100% equity held by the Government of India. The various activities of

the Company range from Gas marketing and distribution through trunk and regional systems,

to retailing of Natural Gas to Gas processing for production and marketing of LPG, liquid

hydrocarbons and Petrochemicals. The equity pattern in the Company has also changed and

the Government today holds about 67% of the equity in the Company. In 2001, GAIL

commissioned worlds longest and India's first Cross Country LPG Transmission Pipeline

from Jamnagar to Loni. It is actively scouting for foreign blocks both exploratory or

discovery. In 2012 its revenue was US $ 7.27 Billion and Net income was US $ 654 Million.

� ���������� �������:�������

Grasim Industries Limited is a company of Aditya Birla Group. The Company is engaged

primarily in two businesses: Viscose Staple Fibre (VSF) and Cement. It also produces caustic

soda and allied chemicals and rayon grade pulp, which are used in the manufacture of VSF.

The manufacturing plants of the Company are located in India, Middle East, Sri Lanka,

Canada, Bangladesh and China. It operates in three segments: fibre and pulp, chemicals and

others. Fibre and Pulp segment includes viscose staple fibre and rayon grade pulp. Chemicals

segment includes caustic soda and allied chemicals. Others include mainly textiles. Textile

segment includes yarn. During the fiscal year ended 31st March 2012, it acquired 33.33%

interest in Aditya Group Sweden. In August 2011, it acquired Aditya Birla Power Ventures

Ltd.

� =�:��� %�, ������$����:�������(=�:)

It is an Indian provider of Information Technology (IT) services and consulting company

headquartered in Noida, Uttar Pradesh, India. It is primarily engaged in providing a range of

Please purchase PDF Split-Merge on www.verypdf.com to remove this watermark.

50

outsourcing services, business process outsourcing and infrastructure services. In November

10th, 1999 the company announced its public issue 1,42,00,000 equity shares of Rs. 4/- each .

The issue includes a Book Built Portion of 1,27,80,000 equity shares and Fixed Price Portion

of 14,20,000 equity shares. HCL Technologies is fourth largest IT Company in India and is

ranked 48 in the global list of IT services providers. HCL Technologies is one of the two

businesses – both of them separately listed in India – falling under the corporate umbrella of

HCL Enterprise with combined annual 2011 revenues of US$ 6 Billion. HCL Enterprise was

founded in 1976 and is one of India's original IT garage start ups. They have decided to vast

their features in Information Technology all over the world. During the last 20 years, HCL

has expanded its service portfolio in IT applications (custom applications for industry

solutions and package implementation), IT infrastructure management, and business process

outsourcing, while maintaining and extending in product engineering.

� =#1��:�������

Housing Development Finance Corporation Limited (HDFC Ltd.) was established in

1977 is a pioneer and leader in housing finance in India. It has assisted more than 4.4 Mllion

customers to own a home of their own, through cumulative housing loan approvals of over

Rs. 5.66 Trillion and disbursements of over Rs. 4.56 Trillion as on March 31, 2013. HDFC

has a wide network of 333 Offices. HDFC's specialist team of over 1,833 (as on 31st March,

2013) trained and experienced professionals follows a 'single-window concept' for providing