Embed Size (px)

Citation preview

Stationary Markovian Processes Stationary Markovian Processes with Long-Range correlations and with Long-Range correlations and

Ergodicity breakingErgodicity breakingSalvatore MiccichèSalvatore Miccichè

with

Fabrizio Lillo, Rosario N. MantegnaFabrizio Lillo, Rosario N. Mantegna

http://lagash.dft.unipa.ithttp://lagash.dft.unipa.it

Observatory of Complex Observatory of Complex SystemsSystems

Università degli Studi di Palermo, Dipartimento di Fisica e Tecnologie RelativeUniversità degli Studi di Palermo, Dipartimento di Fisica e Tecnologie Relative

INFORMAL WORKSHOP onFokker-Planck equations, algebraic correlations, long range correlations, and related Fokker-Planck equations, algebraic correlations, long range correlations, and related

questionsquestionsENS - Lyon, 29-30 March 2005

Stationary Markovian Processes with Long-Range correlations and Ergodicity Stationary Markovian Processes with Long-Range correlations and Ergodicity breakingbreaking

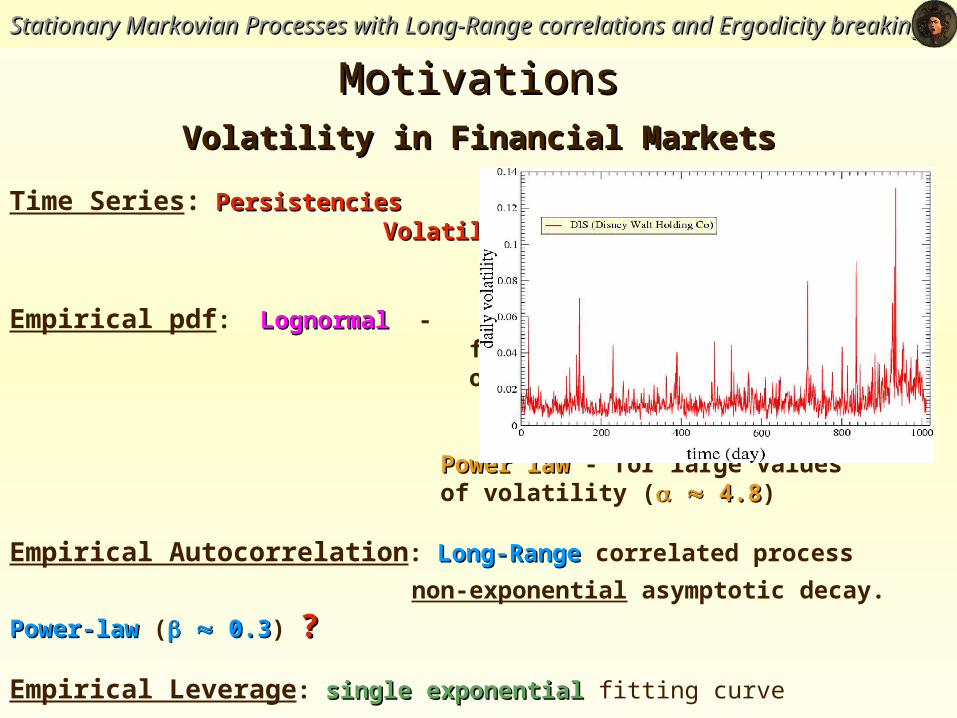

Volatility in Financial MarketsVolatility in Financial Markets

Time Series: PersistenciesPersistencies Volatility ClusteringVolatility Clustering

Empirical pdf: LognormalLognormal - for intermediate values of volatility

Power lawPower law - for large values of volatility ( 4.8 4.8)

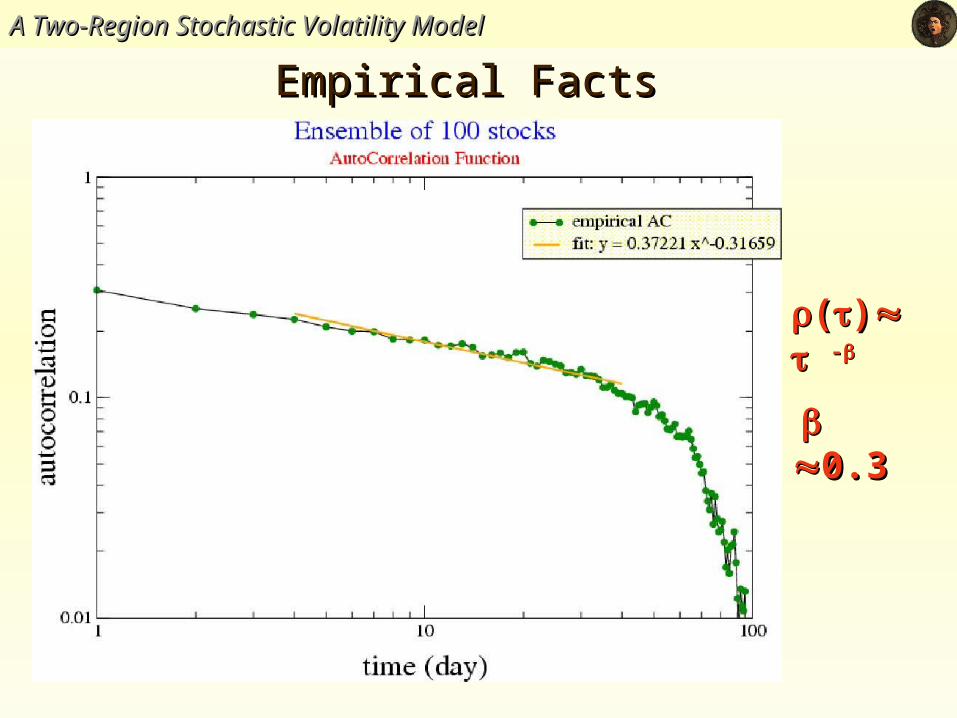

Empirical Autocorrelation: Long-RangeLong-Range correlated process

non-exponential asymptotic decay. Power-lawPower-law ( 0.3 0.3) ??

Empirical Leverage: single exponentialsingle exponential fitting curve

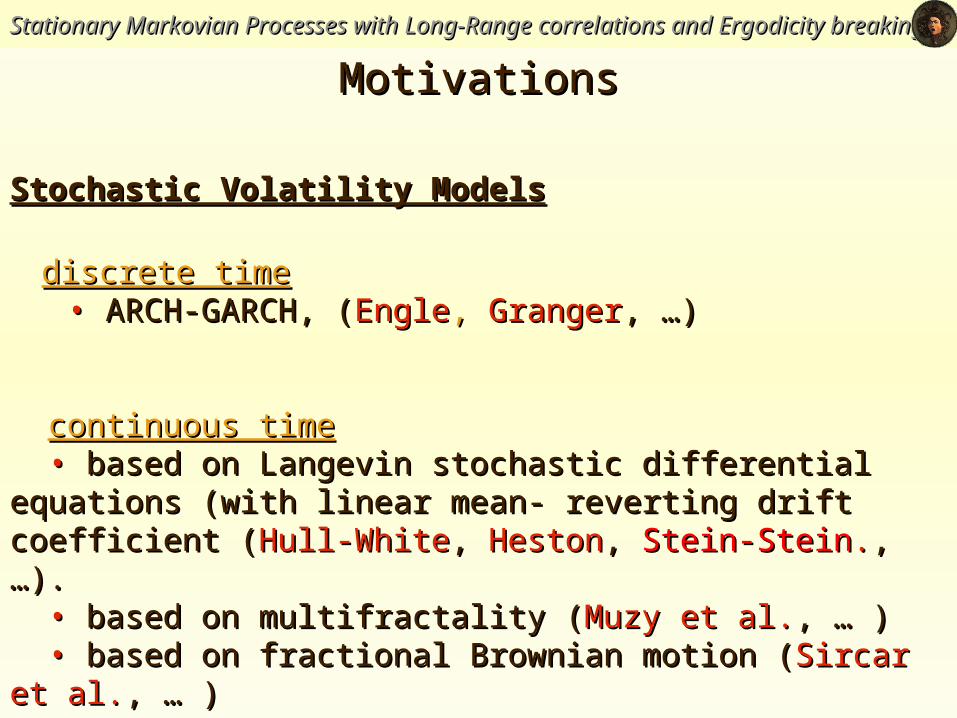

MotivationsMotivations

Stationary Markovian Processes with Long-Range correlations and Ergodicity Stationary Markovian Processes with Long-Range correlations and Ergodicity breakingbreaking

MotivationsMotivations

Stochastic Volatility ModelsStochastic Volatility Models

discrete timediscrete time •• ARCH-GARCH, (ARCH-GARCH, (EngleEngle, , GrangerGranger, …), …)

continuous timecontinuous time • • based on Langevin stochastic differential equations (with linear mean- based on Langevin stochastic differential equations (with linear mean- reverting drift coefficient (reverting drift coefficient (Hull-WhiteHull-White, , HestonHeston, , Stein-SteinStein-Stein.., …)., …). •• based on multifractality (based on multifractality (Muzy et al.Muzy et al., … ), … ) •• based on fractional Brownian motion (based on fractional Brownian motion (Sircar et al.Sircar et al., … ), … ) • • ……

Stationary Markovian Processes with Long-Range correlations and Ergodicity Stationary Markovian Processes with Long-Range correlations and Ergodicity breakingbreaking

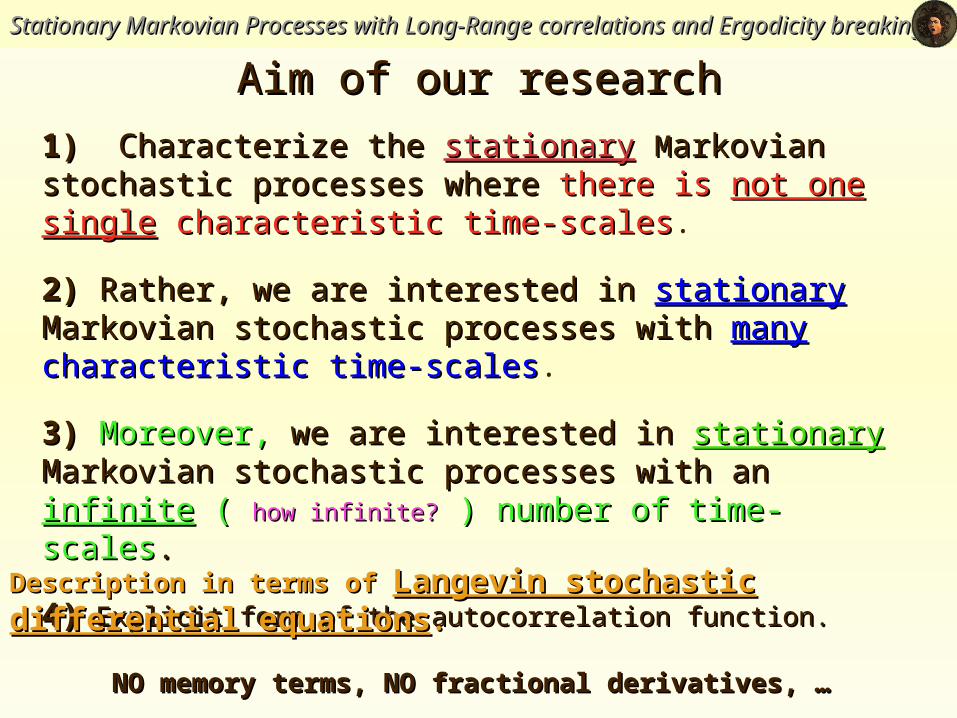

1) 1) Characterize the Characterize the stationarystationary MMarkovian stochastic arkovian stochastic processes whereprocesses where there is there is not one singlenot one single characteristic time-scalescharacteristic time-scales.

2) 2) Rather, we are interested in Rather, we are interested in stationarystationary Markovian Markovian stochastic processes withstochastic processes with manymany characteristic time- characteristic time-scalesscales.

3) 3) Moreover, Moreover, we are interested in we are interested in stationarystationary Markovian Markovian stochastic processes with anstochastic processes with an infiniteinfinite ( ( how infinite?how infinite? ) ) number of time-scalesnumber of time-scales..

4)4) Explicit form of the autocorrelation function.Explicit form of the autocorrelation function.

Aim of our researchAim of our research

Description in terms of Description in terms of Langevin stochastic differential Langevin stochastic differential equationsequations..

NO memory terms, NO fractional derivatives, … NO memory terms, NO fractional derivatives, …

Stationary Markovian Processes with Long-Range correlations and Ergodicity Stationary Markovian Processes with Long-Range correlations and Ergodicity breakingbreaking

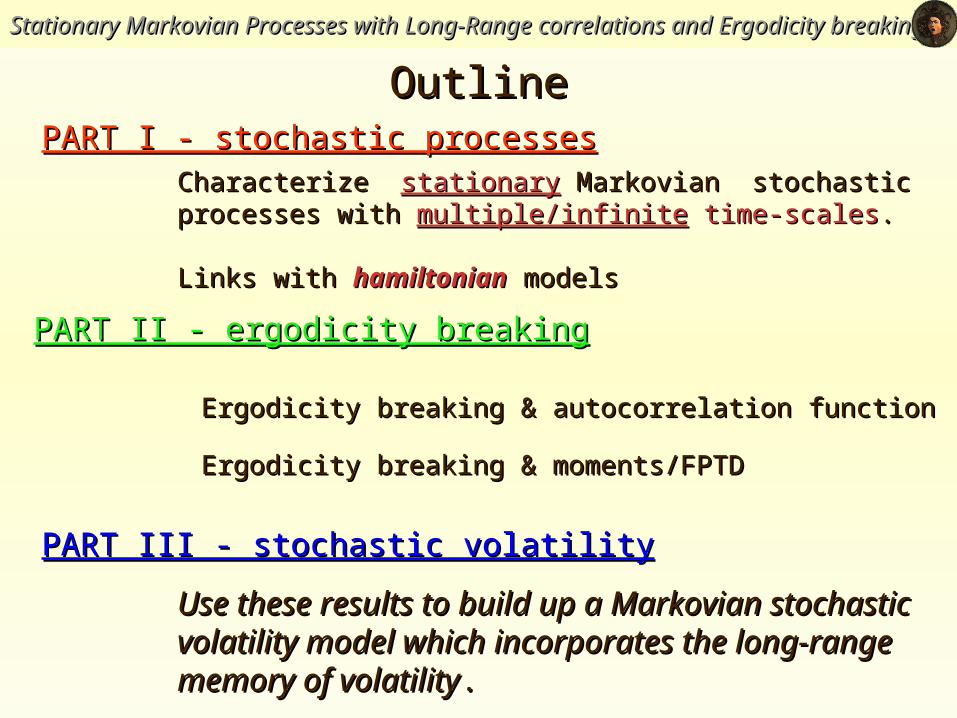

PART I - stochastic processesPART I - stochastic processes

PART III - stochastic volatilityPART III - stochastic volatility

OutlineOutline

CharacterizeCharacterize stationarystationary Markovian stochastic Markovian stochastic processes with processes with multiple/infinitemultiple/infinite time-scales time-scales..

Use these results to build up a Markovian Use these results to build up a Markovian stochastic volatility model which incorporates stochastic volatility model which incorporates the long-range memory of volatilitythe long-range memory of volatility..

PART II - ergodicity breakingPART II - ergodicity breaking

Ergodicity breaking & autocorrelation functionErgodicity breaking & autocorrelation function

Ergodicity breaking & moments/FPTDErgodicity breaking & moments/FPTD

Links with Links with hamiltonianhamiltonian models models

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

Part IPart I

Stationary Markovian Stochastic Processes Stationary Markovian Stochastic Processes with Multiple Time-Scaleswith Multiple Time-Scales

ReferencesReferences[1] [1] A. Schenzle, H. BrandA. Schenzle, H. Brand, Phys. Rev. A, , Phys. Rev. A, 20(4), 20(4), 1628, (1979) , (1979) [2][2] M. Suzuki, K. Kaneko, F. Sasagawa M. Suzuki, K. Kaneko, F. Sasagawa, Prog. Theor. Phys., , Prog. Theor. Phys., 65(3), 65(3), 828, (1981), (1981)[3][3] J. Farago J. Farago, Europhys. Lett., , Europhys. Lett., 52(4), 52(4), 379, (2000) , (2000) [4][4] F. Lillo, S. Miccichè, R. N. Mantegna F. Lillo, S. Miccichè, R. N. Mantegna, cond-mat, , cond-mat, 02034420203442, (2002), (2002)

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

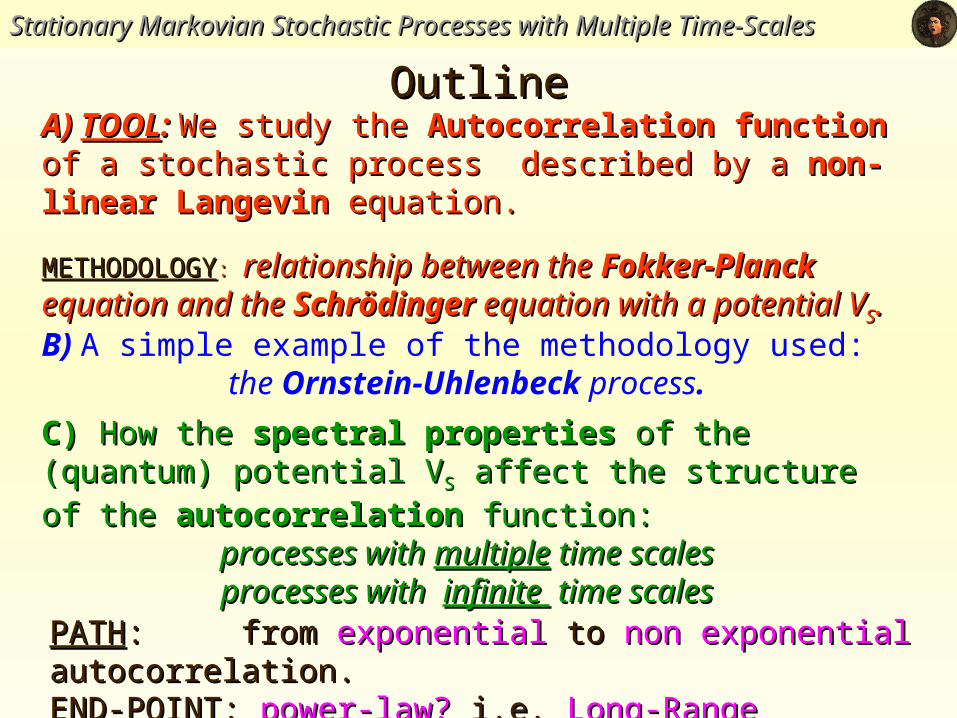

A) A) TOOLTOOL: : We study the We study the Autocorrelation functionAutocorrelation function of of a stochastic process described by a a stochastic process described by a non-linear non-linear LangevinLangevin equation. equation.

METHODOLOGYMETHODOLOGY: : relationship between the relationship between the Fokker-PlanckFokker-Planck equation and the equation and the SchrödingerSchrödinger equation with a equation with a potential Vpotential VSS.. B) A simple example of the methodology used:

the Ornstein-Uhlenbeck process.

C) C) How the How the spectral propertiesspectral properties of the (quantum) potential V of the (quantum) potential VSS

affect the structure of the affect the structure of the autocorrelationautocorrelation function: function:processes with processes with multiplemultiple time scales time scalesprocesses with processes with infinite infinite time scales time scales

OutlineOutline

PATHPATH: : from from exponentialexponential to to non exponential non exponential autocorrelation.autocorrelation.END-POINTEND-POINT:: power-law? power-law? i.e.i.e. Long-Range CorrelatedLong-Range Correlated processes processes ??

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

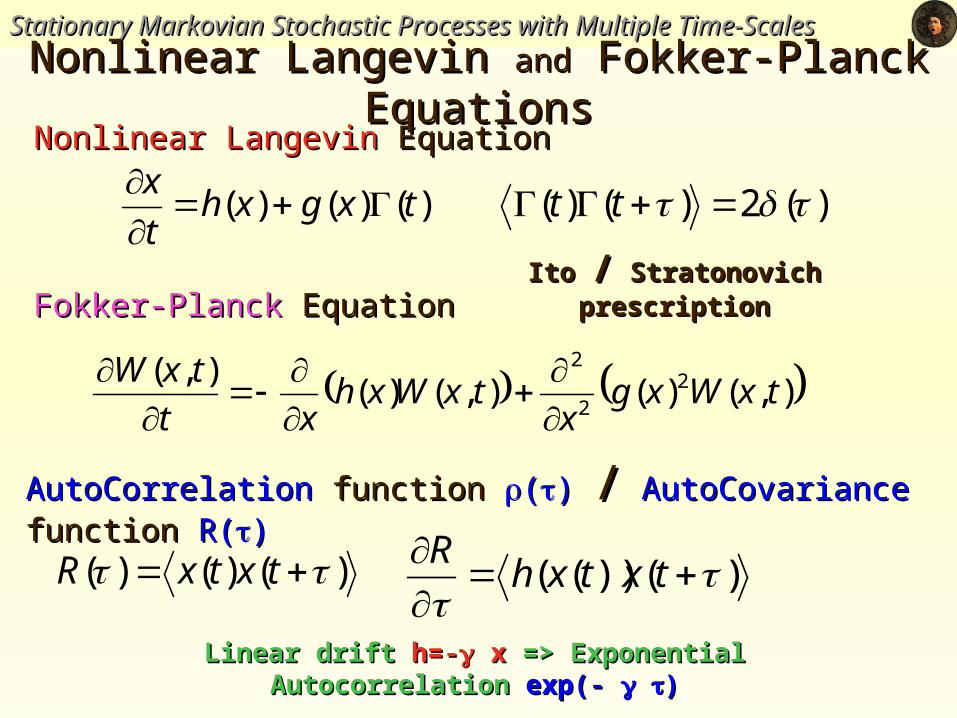

Nonlinear LangevinNonlinear Langevin Equation Equation

Fokker-Planck Fokker-Planck EquationEquation

AutoCorrelationAutoCorrelation function function (()) // AutoCovarianceAutoCovariance function function R(R())

Nonlinear Langevin Nonlinear Langevin andand Fokker-Planck Fokker-Planck EquationsEquations

)()()( txgxht

x

)(2)()( tt

),()(),()(),( 2

2

2

txWxgx

txWxhxt

txW

Linear drift Linear drift h=-h=- x x => Exponential Autocorrelation => Exponential Autocorrelation exp(- exp(- ))

)()()( txtxR )())((

txtxhR

Ito Ito // Stratonovich prescription Stratonovich prescription

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

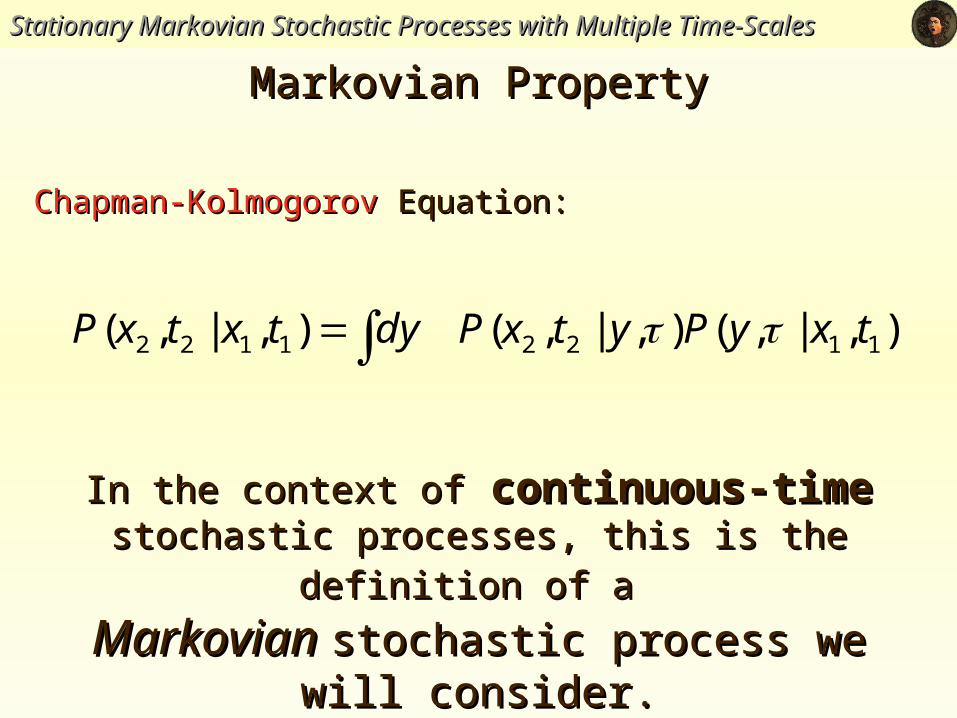

Chapman-Kolmogorov Chapman-Kolmogorov Equation:Equation:

Markovian PropertyMarkovian Property

),|,(),|,(),|,( 11221122 txyPytxPdytxtxP

In the context ofIn the context of continuous-timecontinuous-time stochastic stochastic

processes, this is the definition of aprocesses, this is the definition of a Markovian Markovian stochastic process we will consider.stochastic process we will consider.

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

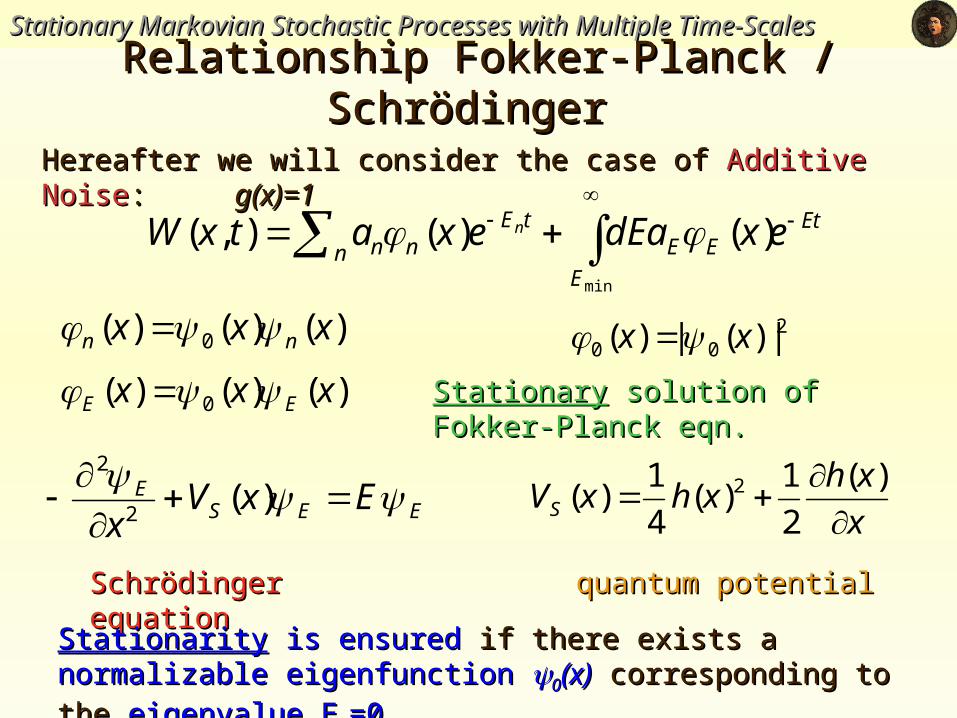

Relationship Fokker-Planck / Schrödinger Relationship Fokker-Planck / Schrödinger

Et

E

EEn

tEnn exdEaexatxW n

min

)()(),(

Hereafter we will consider the case of Hereafter we will consider the case of Additive NoiseAdditive Noise: : g(x)=1g(x)=1

)()()( 0 xxx nn

)()()( 0 xxx EE

EESE ExV

x

)(2

2

x

xhxhxVS

)(

2

1)(

4

1)( 2

200 |)(|)( xx

StationaryStationary solution of Fokker-Planck eqn. solution of Fokker-Planck eqn.

Schrödinger equationSchrödinger equation quantum potentialquantum potential

StationarityStationarity is ensured is ensured if there exists aif there exists a normalizable eigenfunction normalizable eigenfunction 00(x)(x)

corresponding to thecorresponding to the eigenvalue E eigenvalue E00=0.=0.

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

Relationship Fokker-Planck / Schrödinger Relationship Fokker-Planck / Schrödinger

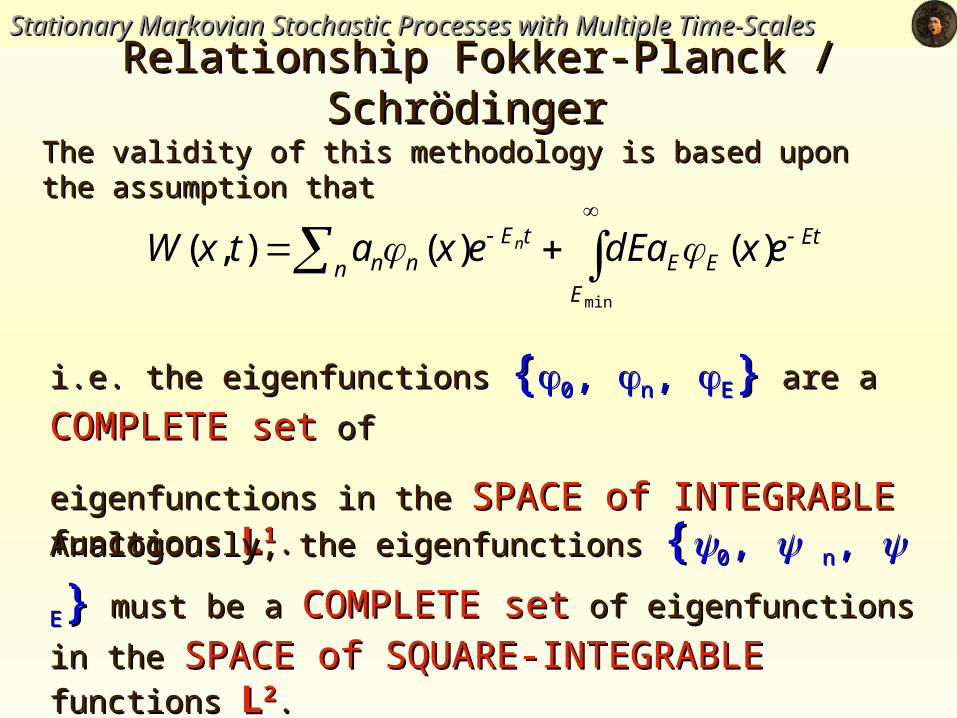

The validity of this methodology is based upon the assumption thatThe validity of this methodology is based upon the assumption that

i.e. the eigenfunctions i.e. the eigenfunctions {{00, , nn, , EE}} are a are a COMPLETECOMPLETE setset of of

eigenfunctions in the eigenfunctions in the SPACE of INTEGRABLESPACE of INTEGRABLE functions functions LL11..

Analogously, the eigenfunctions Analogously, the eigenfunctions {{00, , nn, , EE}} must be a must be a

COMPLETECOMPLETE setset of eigenfunctions in the of eigenfunctions in the SPACE of SPACE of SQUARE-INTEGRABLESQUARE-INTEGRABLE functions functions LL22..

Et

E

EEn

tEnn exdEaexatxW n

min

)()(),(

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

Relationship Fokker-Planck / Schrödinger Relationship Fokker-Planck / Schrödinger

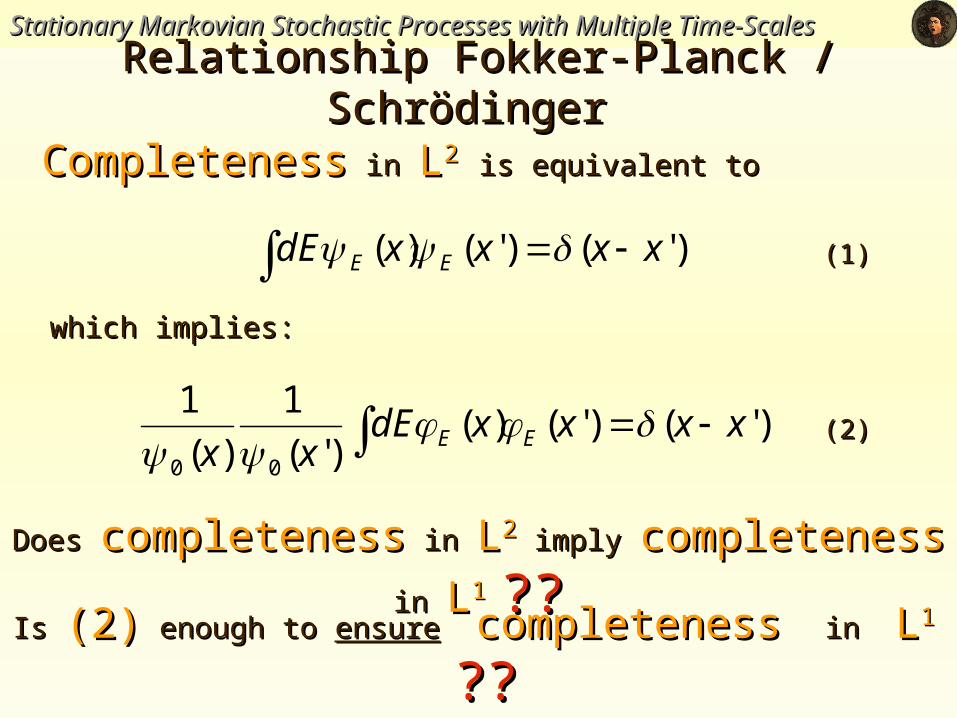

CompletenessCompleteness in in LL22 is equivalent to is equivalent to

)'()'()( xxxxdE EE

Is Is (2)(2) enough to enough to ensureensure completeness completeness in in LL11 ????

)'()'()()'(

1

)(

1

00

xxxxdExx EE

Does Does completenesscompleteness in in LL22 imply imply completenesscompleteness in in LL1 1 ????

(1)(1)

(2)(2)

which implies: which implies:

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

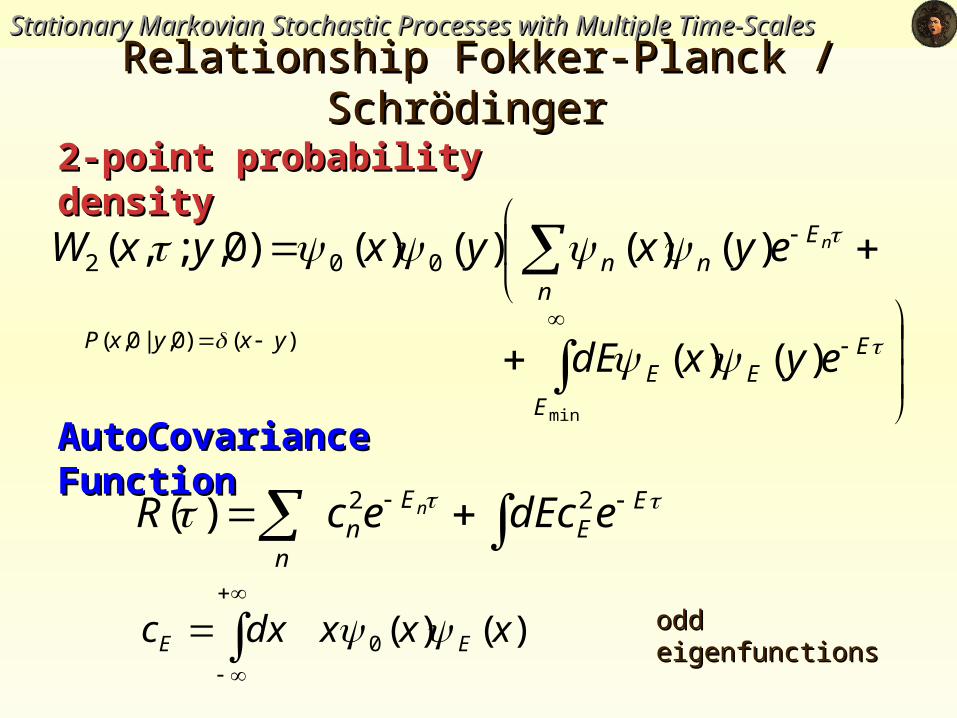

AutoCovariance FunctionAutoCovariance Function

Relationship Fokker-Planck / Schrödinger Relationship Fokker-Planck / Schrödinger

nE

nn

n eyxyxyxW )()()()()0,;,( 002

2-point probability density2-point probability density

)()(0 xxxdxc EE

EE

En

n

ecdEecR n 22)(

EEE

E

eyxdE )()(min

odd eigenfunctionsodd eigenfunctions

)()0,|0,( yxyxP

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

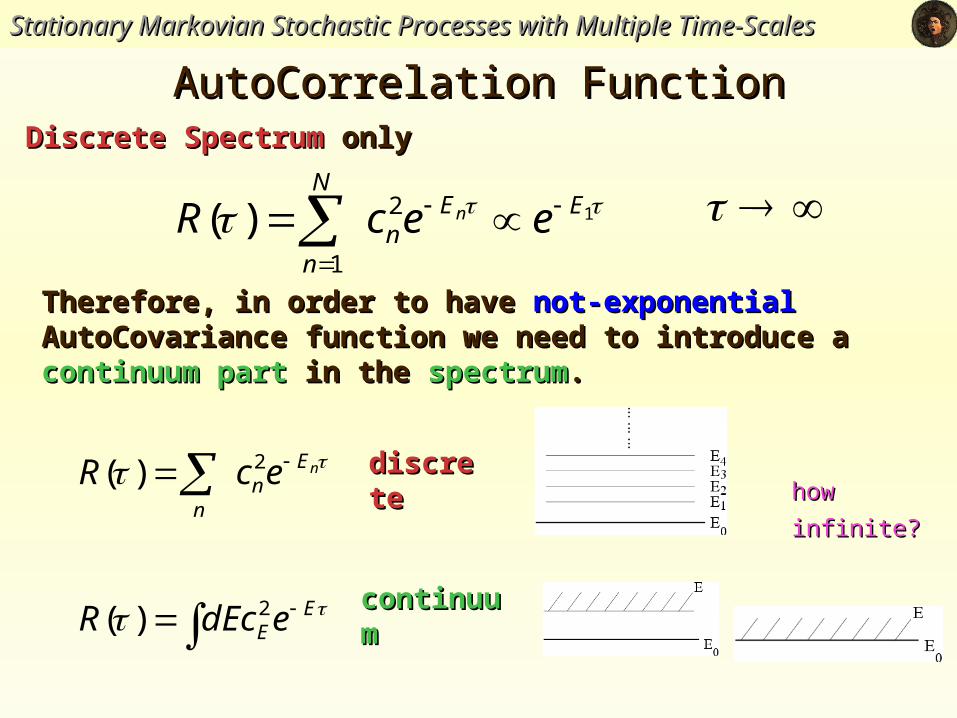

AutoCorrelation FunctionAutoCorrelation FunctionDiscrete SpectrumDiscrete Spectrum only only

Therefore, in order to have Therefore, in order to have not-exponentialnot-exponential AutoCovariance function AutoCovariance function we need to introduce a we need to introduce a continuum partcontinuum part in the in the spectrumspectrum..

12

1

)( EEn

N

n

eecR n

nEn

n

ecR 2)(

EEecdER 2)(

discretediscrete

continuumcontinuum

how how

infinite?infinite?

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

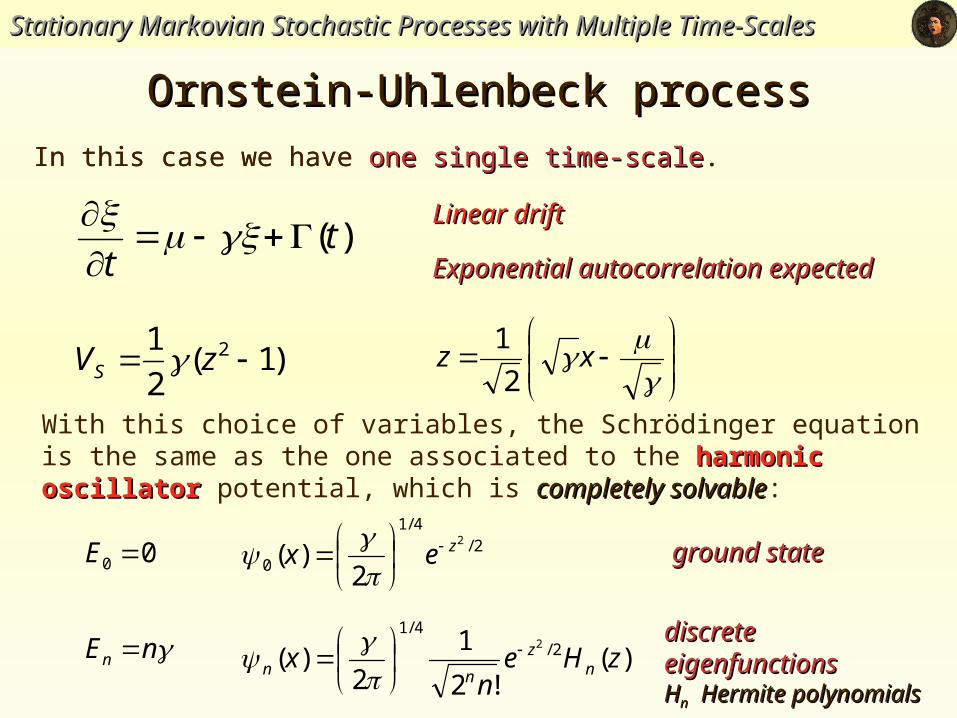

Ornstein-Uhlenbeck processOrnstein-Uhlenbeck process

Linear driftLinear drift

Exponential autocorrelation expectedExponential autocorrelation expected

In this case we have one single time-scale.

)(tt

)1(2

1 2 zVS

xz

2

1

In this case we have one single time-scaleone single time-scale.

With this choice of variables, the Schrödinger equation is the same as the one associated to the harmonic oscillatorharmonic oscillator potential, which is completely solvablecompletely solvable:

2/4/1

0

2

2)( zex

)(!2

1

2)( 2/

4/12

zHen

x nz

nn

00 E

nEn

ground stateground state

discrete eigenfunctionsdiscrete eigenfunctionsHHnn Hermite polynomials Hermite polynomials

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

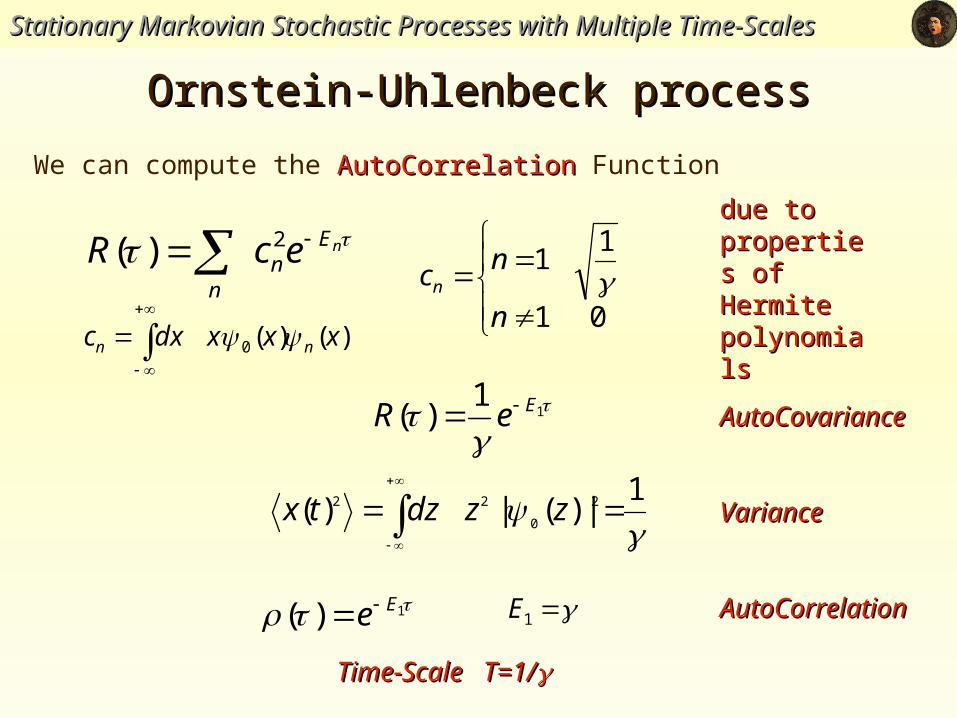

Ornstein-Uhlenbeck processOrnstein-Uhlenbeck process

01

11

n

ncn

We can compute the AutoCorrelationAutoCorrelation Function

AutoCovarianceAutoCovariance

nEn

n

ecR 2)(

1

1)( EeR

due to due to properties of properties of Hermite Hermite polynomialspolynomials

1

|)(|)( 2

0

22

zzdztx VarianceVariance

1)( Ee AutoCorrelationAutoCorrelation

)()(0 xxxdxc nn

1E

Time-Scale T=1/Time-Scale T=1/

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

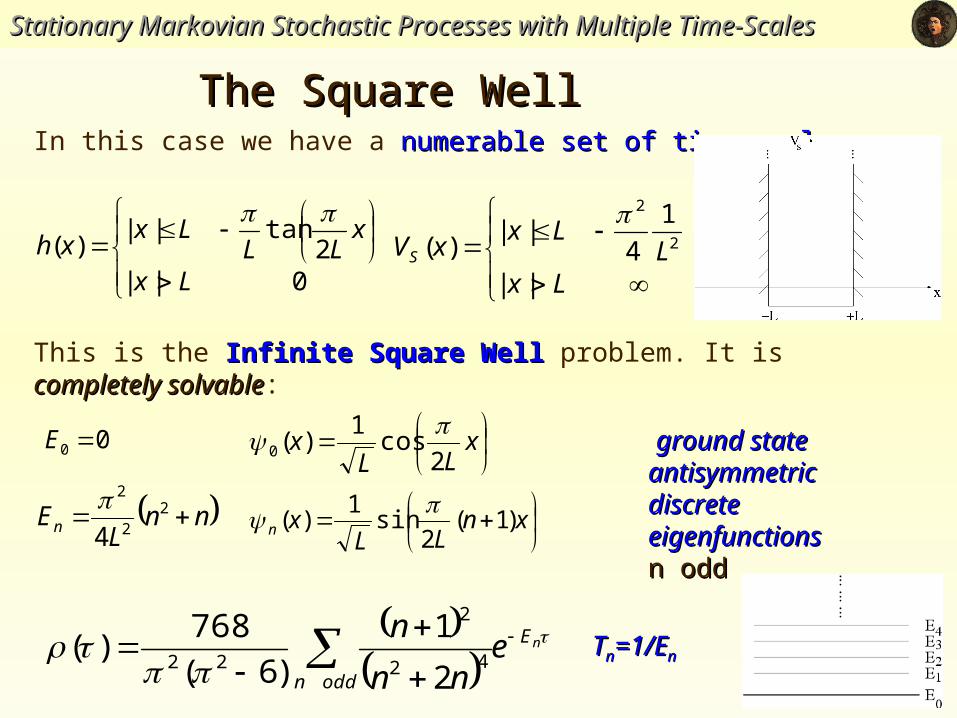

The Square Well The Square Well

0||

2tan||

)(Lx

xLL

Lxxh

In this case we have a numerable set of time-scalesnumerable set of time-scales.

Lx

LLx

xVS

||

1

4||

)( 2

2

x

LLx

2cos

1)(0

xn

LLxn )1(

2sin

1)(

00 E

nnL

En 22

2

4

ground stateground state

antisymmetricantisymmetricdiscrete eigenfunctionsdiscrete eigenfunctionsn oddn odd

nE

oddn

enn

n

42

2

222

1

)6(

768)(

This is the Infinite Square Well Infinite Square Well problem. It is completely solvablecompletely solvable:

TTnn=1/E=1/Enn

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

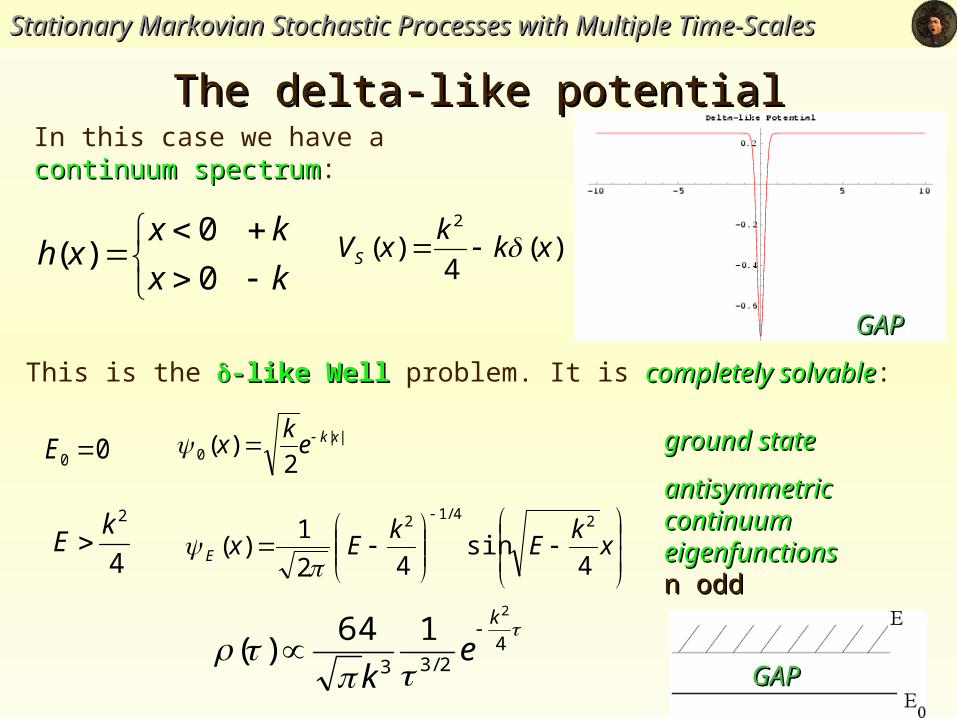

The delta-like potentialThe delta-like potentialIn this case we have a continuum spectrumcontinuum spectrum:

kx

kxxh

0

0)( )(

4)(

2

xkk

xVS

||0 2

)( xkek

x

xk

Ek

ExE 4sin

42

1)(

24/12

00 E

4

2kE

ground stateground state

antisymmetricantisymmetriccontinuum eigenfunctionscontinuum eigenfunctionsn oddn odd

4

2/33

2

164)(

k

ek

This is the -like Well-like Well problem. It is completely solvablecompletely solvable:

GAPGAP

GAPGAP

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

The delta-like potentialThe delta-like potential

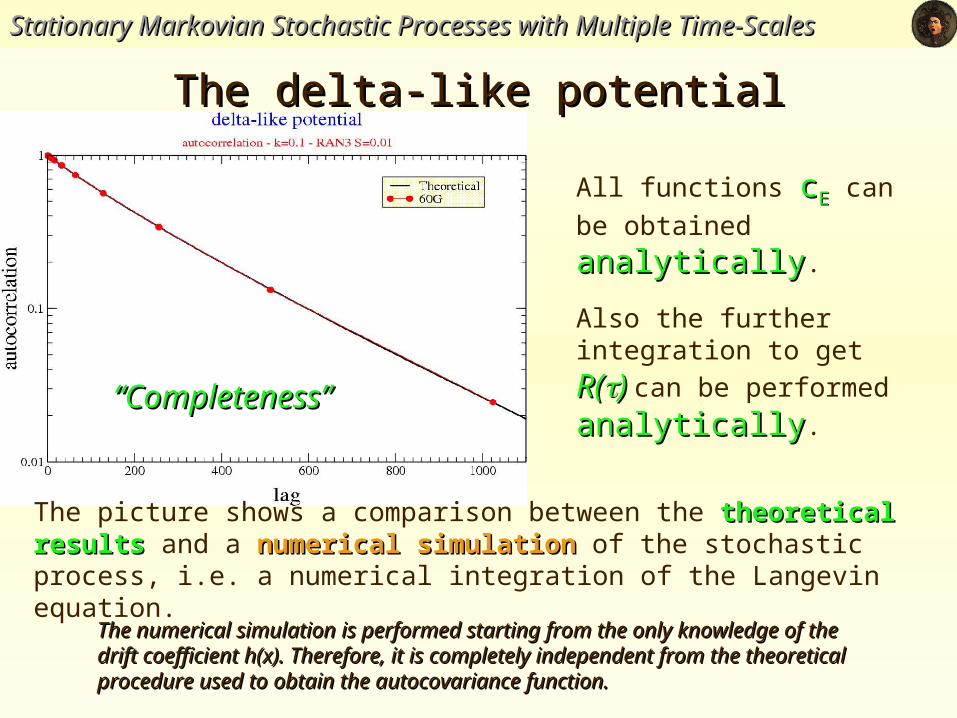

All functions ccEE can be

obtained analyticallyanalytically.

Also the further integration to

get R(R()) can be performed

analyticallyanalytically.

The picture shows a comparison between the theoretical resultstheoretical results and a numerical numerical simulationsimulation of the stochastic process, i.e. a numerical integration of the Langevin equation.

The numerical simulation is performed starting from the only knowledge of the drift The numerical simulation is performed starting from the only knowledge of the drift coefficient h(x). Therefore, it is completely independent from the theoretical procedure coefficient h(x). Therefore, it is completely independent from the theoretical procedure used to obtain the autocovariance function.used to obtain the autocovariance function.

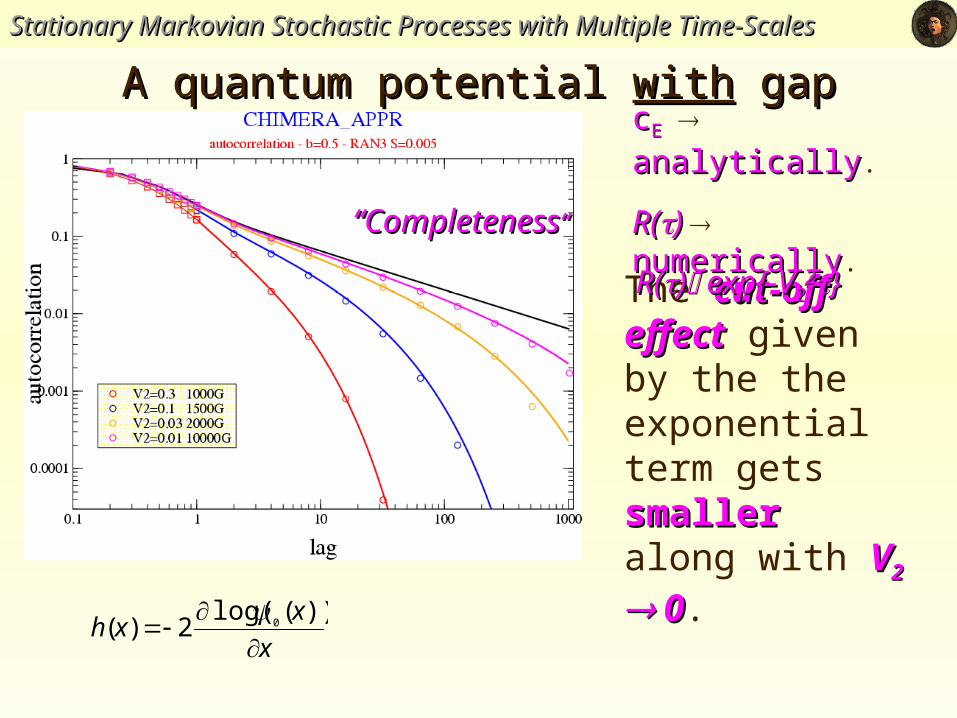

““Completeness”Completeness”

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

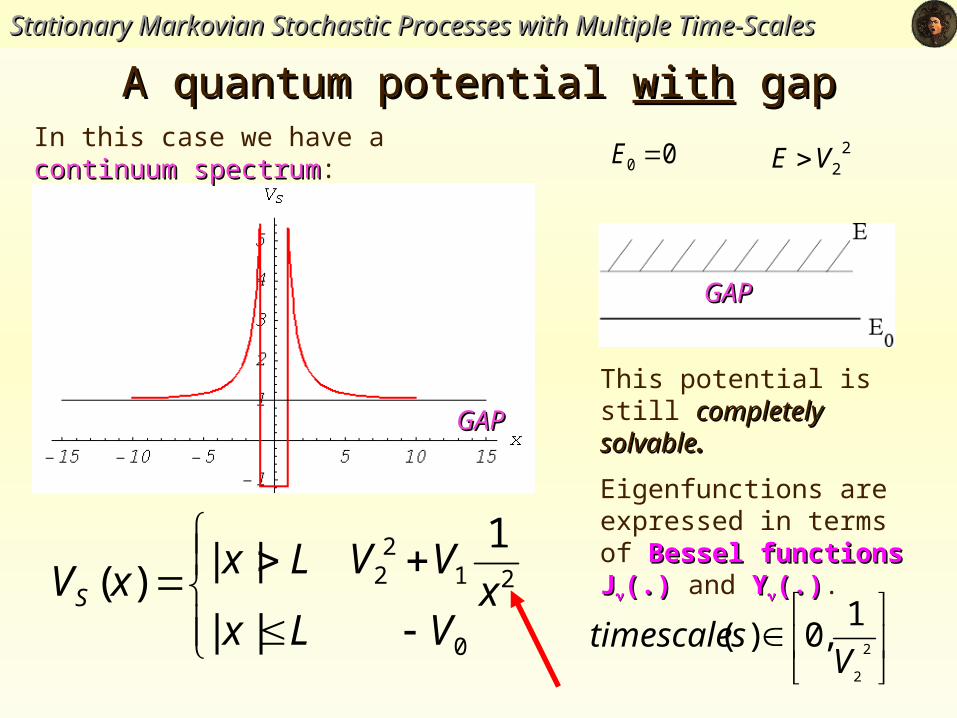

A quantum potential A quantum potential withwith gap gap

0

212

2

||

1||)(

VLxx

VVLxxVS

In this case we have a continuum spectrumcontinuum spectrum:

This potential is still completely solvablecompletely solvable..

Eigenfunctions are expressed in terms of Bessel functions Bessel functions JJ(.)(.) and YY(.)(.).

GAPGAP

GAPGAP

00 E

2

2

1,0)(V

stimescale

22VE

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

A quantum potential A quantum potential withwith gap gap

ccEE analyticallyanalytically.

R(R()) numericallynumerically.

The cut-off effectcut-off effect given by the the exponential term gets smallersmaller along with VV2 2 0 0.

R(R()) exp{-V exp{-V2222}}

““CompletenessCompleteness““

x

xxh

))(log(

2)( 0

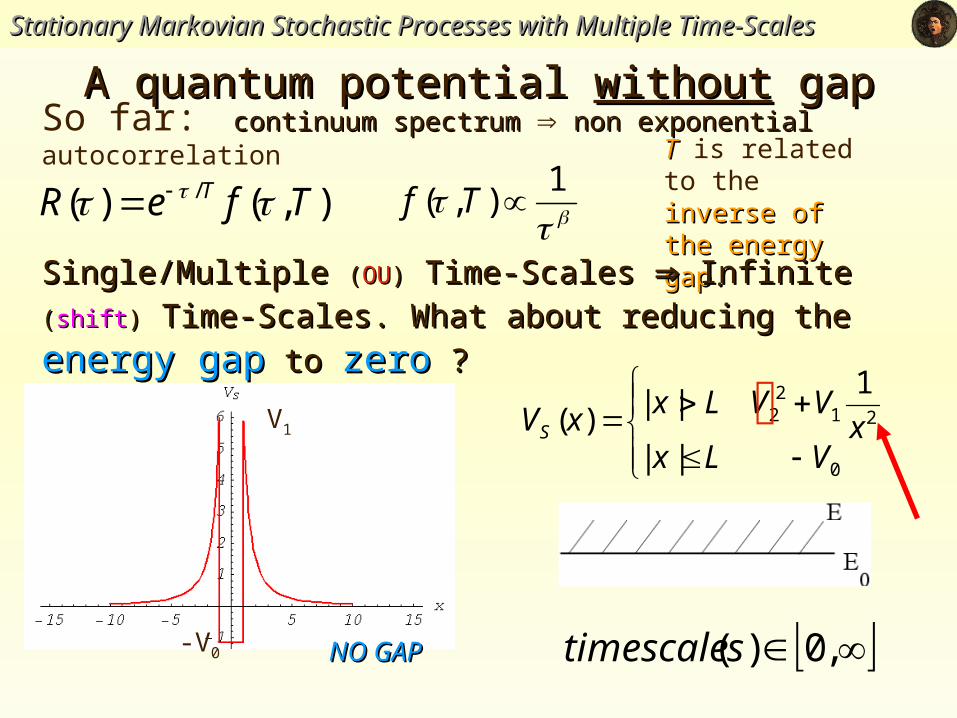

So far: continuum spectrumcontinuum spectrum non exponentialnon exponential autocorrelation

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

A quantum potential A quantum potential withoutwithout gap gap

1

),( TfTT is related to the inverse of the inverse of the energy gapenergy gap..

),()( / TfeR T

Single/MultipleSingle/Multiple ((OUOU)) Time-ScalesTime-Scales InfiniteInfinite ((shiftshift)) Time-Scales. What Time-Scales. What

about reducing theabout reducing the energy gapenergy gap to to zerozero ? ?

0

212

2

||

1||)(

VLxx

VVLxxVS

NO GAPNO GAP

V1

-V0 ,0)(stimescale

Eigenfunctions x>L

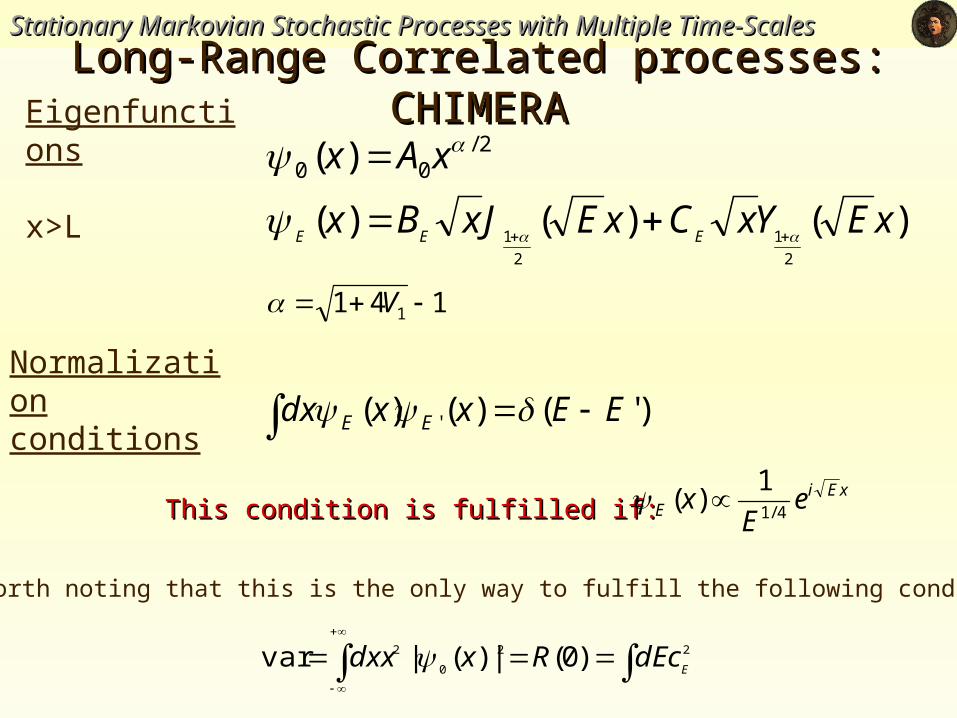

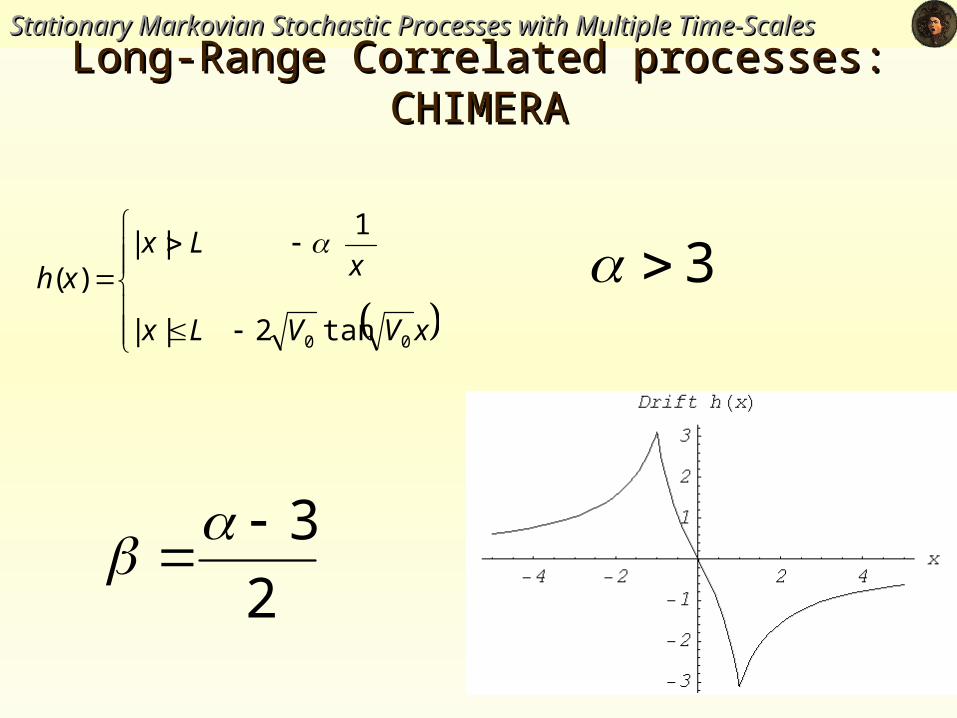

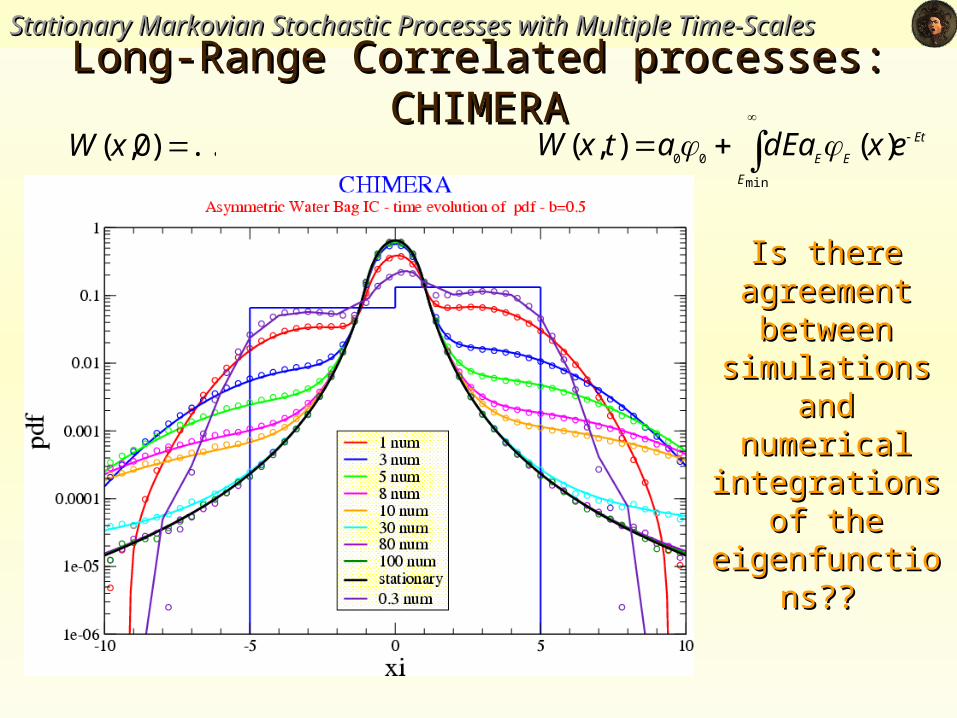

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesLong-Range Correlated processes: Long-Range Correlated processes:

CHIMERACHIMERA2/

00 )( xAx

)()()(2

1

2

1xEYxCxEJxBx

EEE

)'()()( ' EExxdx EE

This condition is fulfilled if:This condition is fulfilled if:xEi

E eE

x4/1

1)(

It is worth noting that this is the only way to fulfill the following condition:

22

0

2 )0(|)(|varE

cdERxdxx

Normalizationconditions

141 1 V

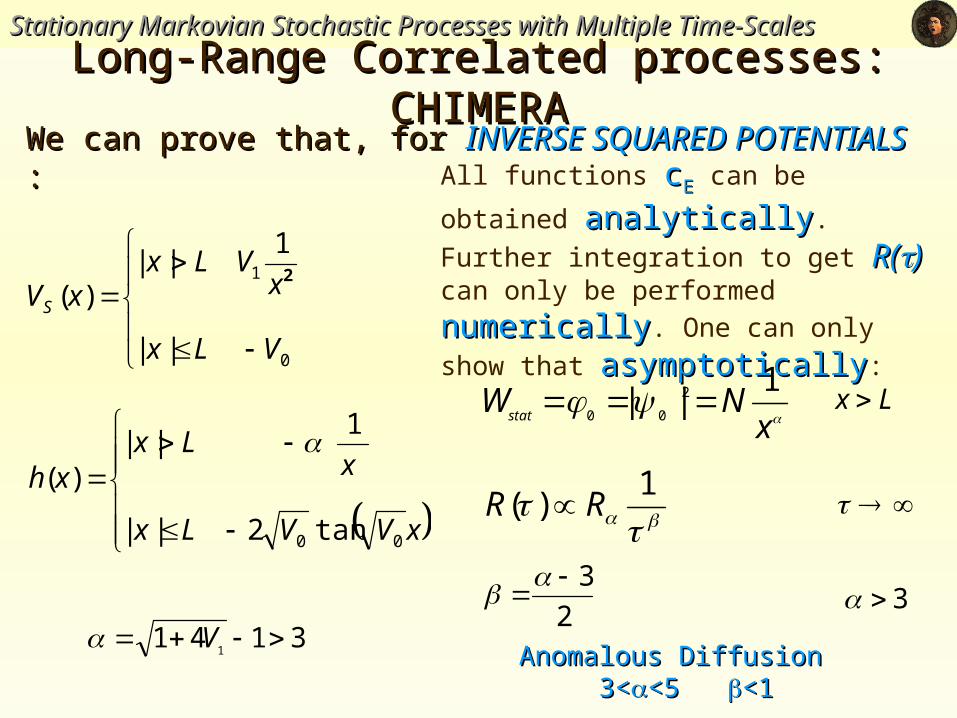

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesLong-Range Correlated processes: Long-Range Correlated processes:

CHIMERACHIMERA

0

1

||

1||

)(

VLx

xVLx

xVS

2

We can prove that, for We can prove that, for INVERSE SQUARED POTENTIALS INVERSE SQUARED POTENTIALS ::

xVVLx

xLx

xh

00 tan2||

1||

)(

All functions ccEE can be obtained

analyticallyanalytically. Further integration to get

R(R()) can only be performed numericallynumerically.

One can only show that asymptoticallyasymptotically:

31411

V

1

)( RR

2

3

xNW

stat

1|| 2

00

3

Lx

Anomalous Diffusion 3<Anomalous Diffusion 3<<5 <5 <1<1

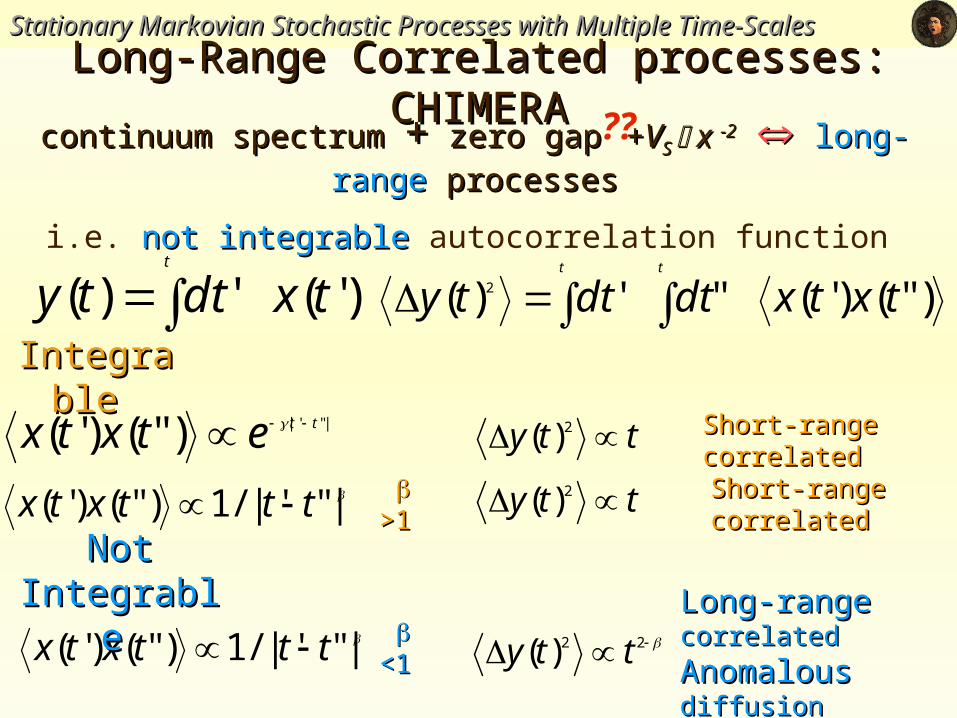

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesLong-Range Correlated processes: Long-Range Correlated processes:

CHIMERACHIMERA

xVVLx

xLx

xh

00 tan2||

1||

)( 3

2

3

continuum spectrum continuum spectrum ++ zero gap zero gap ++VVS S x x -2-2 long-rangelong-range processes processes

i.e. not integrablenot integrable autocorrelation function

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesLong-Range Correlated processes: Long-Range Correlated processes:

CHIMERACHIMERA

t

txdtty )'(')( t t

txtxdtdtty )"()'("')( 2

|"'|)"()'( ttetxtx

|"'|/1)"()'( tttxtx

|"'|/1)"()'( tttxtx

tty 2)(

tty 2)(

22)( tty

>1>1

<1<1

Short-range correlatedShort-range correlated

Short-range correlatedShort-range correlated

Long-rangeLong-range correlated correlated

AnomalousAnomalous diffusion diffusion

??

Not IntegrableNot Integrable

Integrable Integrable

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesLong-Range Correlated processes: Long-Range Correlated processes:

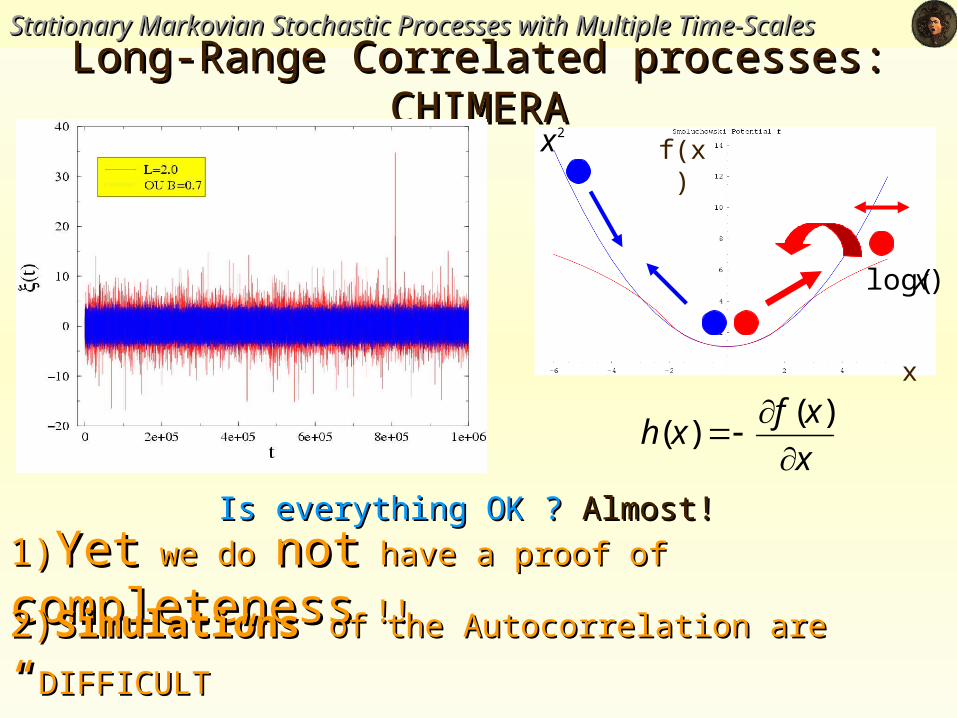

CHIMERACHIMERA

x

xfxh

)(

)(

Is everything OK ? Is everything OK ? Almost!Almost!

1)1)YetYet we do we do notnot have a proof of have a proof of

completenesscompleteness !! !!

2)2)SimulationsSimulations of the Autocorrelation areof the Autocorrelation are “ “DIFFICULTDIFFICULT””

x

f(x)

)log(x

2x

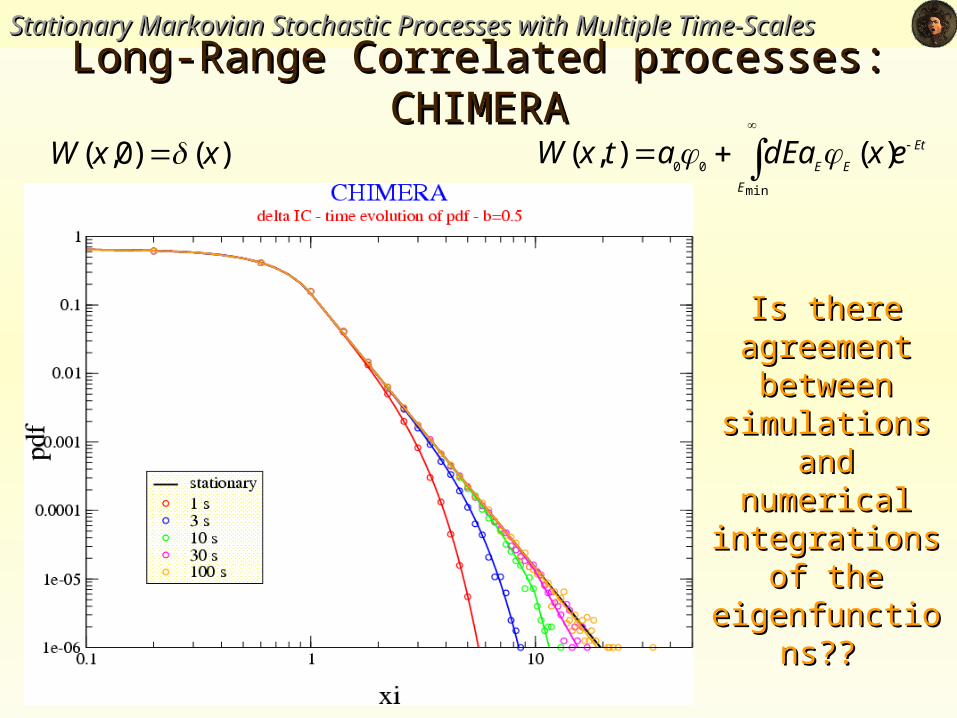

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesLong-Range Correlated processes: Long-Range Correlated processes:

CHIMERACHIMERA

Is there Is there agreement agreement between between

simulations simulations and numerical and numerical integrations of integrations of

the the eigenfunctionseigenfunctions

????

Et

E

EEexdEaatxW

min

00)(),( )()0,( xxW

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesLong-Range Correlated processes: Long-Range Correlated processes:

CHIMERACHIMERA

Is there Is there agreement agreement between between

simulations simulations and numerical and numerical integrations of integrations of

the the eigenfunctionseigenfunctions

????

Et

E

EEexdEaatxW

min

00)(),( ...)0,( xW

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

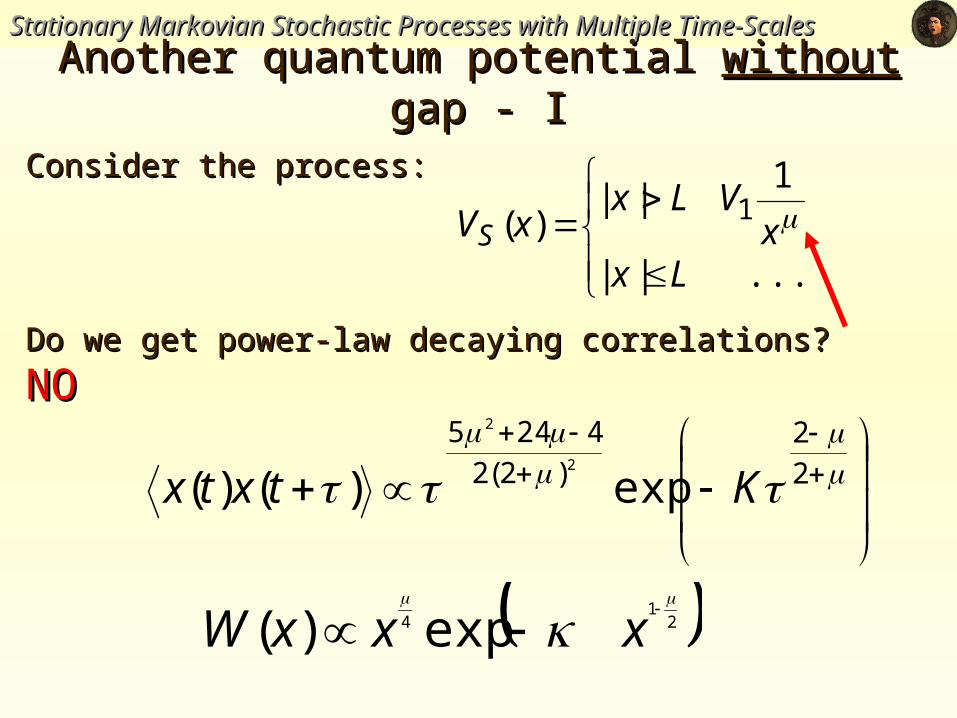

Another quantum potential Another quantum potential withoutwithout gap - I gap - I

Consider the process:Consider the process:

....||

1||

)( 1

Lxx

VLxxVS

Do we get power-law decaying correlations? Do we get power-law decaying correlations? NONO

2

2)2(2

4245

exp)()(2

2

Ktxtx

21

4 exp)(

xxxW

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

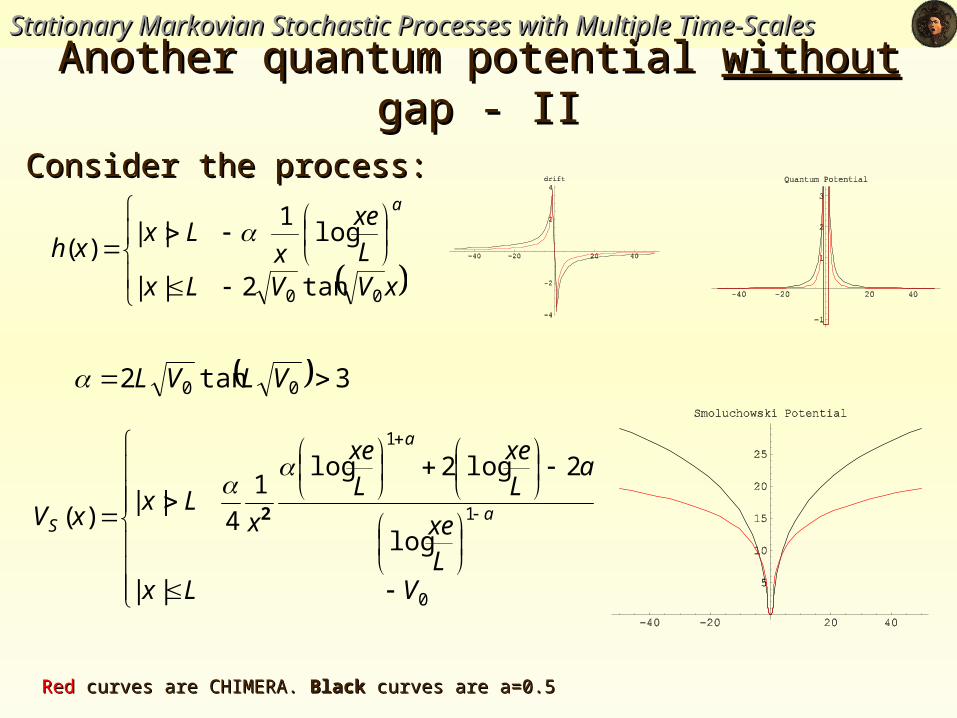

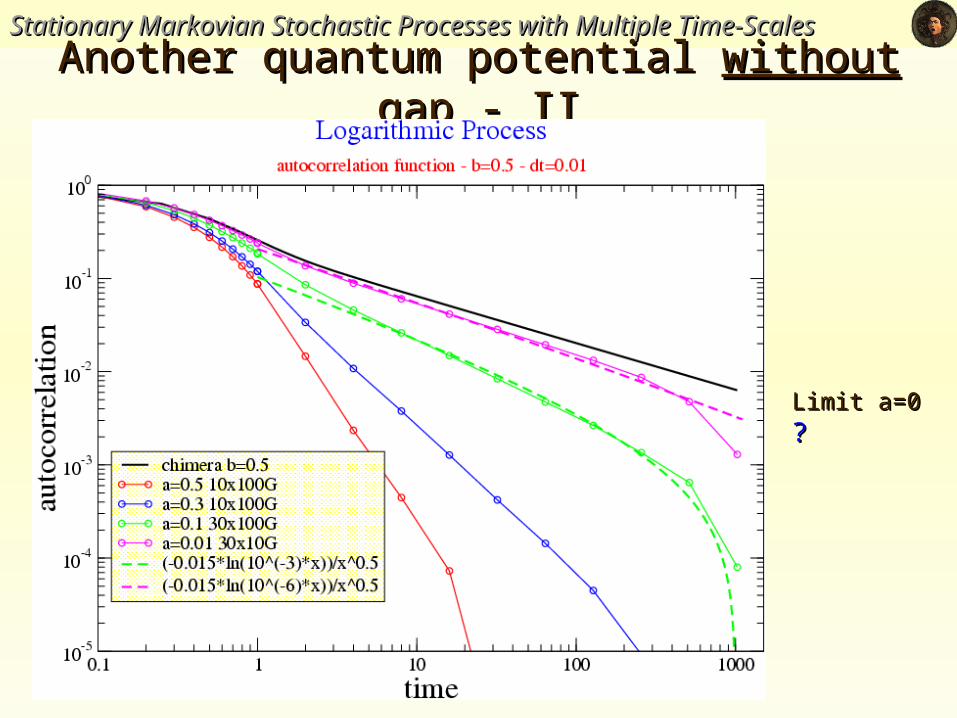

Another quantum potential Another quantum potential withoutwithout gap - II gap - II

Consider the process:Consider the process:

xVVLxL

xe

xLx

xh

a

00 tan2||

log1

||)(

3tan2 00 VLVL

0

1

1

||

log

2log2log1

4||

)(

VLxLxe

aLxe

Lxe

xLx

xV a

a

S

2

RedRed curves are CHIMERA. curves are CHIMERA. BlackBlack curves are a=0.5 curves are a=0.5

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

Another quantum potential Another quantum potential withoutwithout gap - II gap - II

Limit a=0Limit a=0 ? ?

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

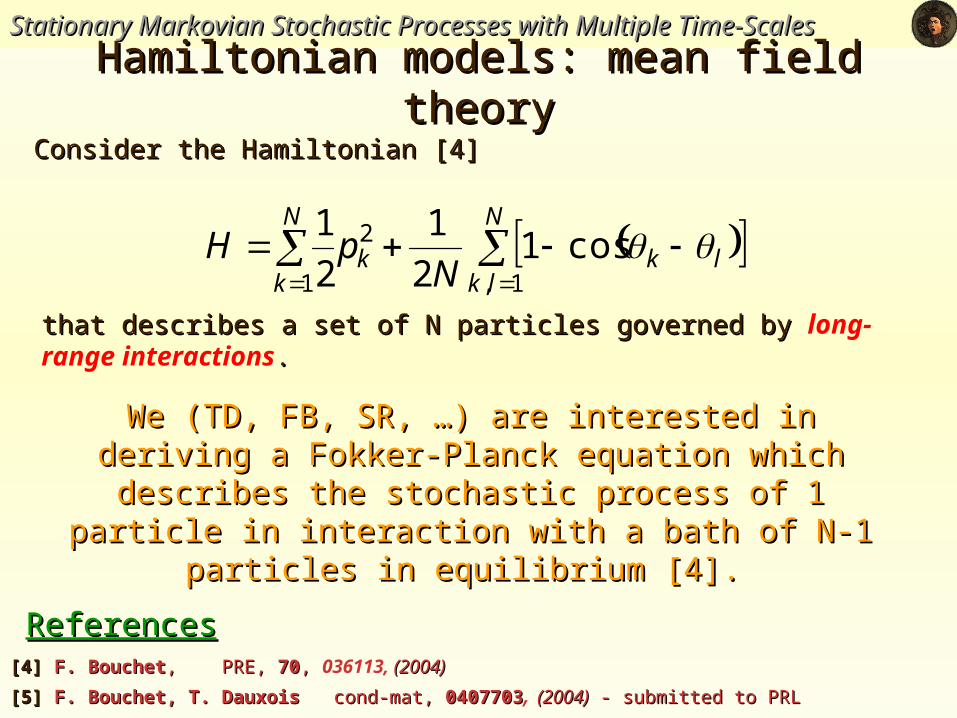

Hamiltonian models: mean field theoryHamiltonian models: mean field theory

We (TD, FB, SR, …) are interested in deriving a We (TD, FB, SR, …) are interested in deriving a Fokker-Planck equation which describes the Fokker-Planck equation which describes the

stochastic process of 1 particle in interaction with a stochastic process of 1 particle in interaction with a bath of N-1 particles in equilibrium [4].bath of N-1 particles in equilibrium [4].

Consider the Hamiltonian [4]Consider the Hamiltonian [4]

that describes a set of N particles governed by that describes a set of N particles governed by long-range interactions..

ReferencesReferences[4][4] F. Bouchet F. Bouchet, PRE, , PRE, 7070, , 036113, (2004)(2004)

[5][5] F. Bouchet, T. Dauxois F. Bouchet, T. Dauxois cond-mat, cond-mat, 04077030407703, (2004)(2004) - submitted to PRL - submitted to PRL

N

lklkk

N

k NpH

1,

2

1cos1

2

1

2

1

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

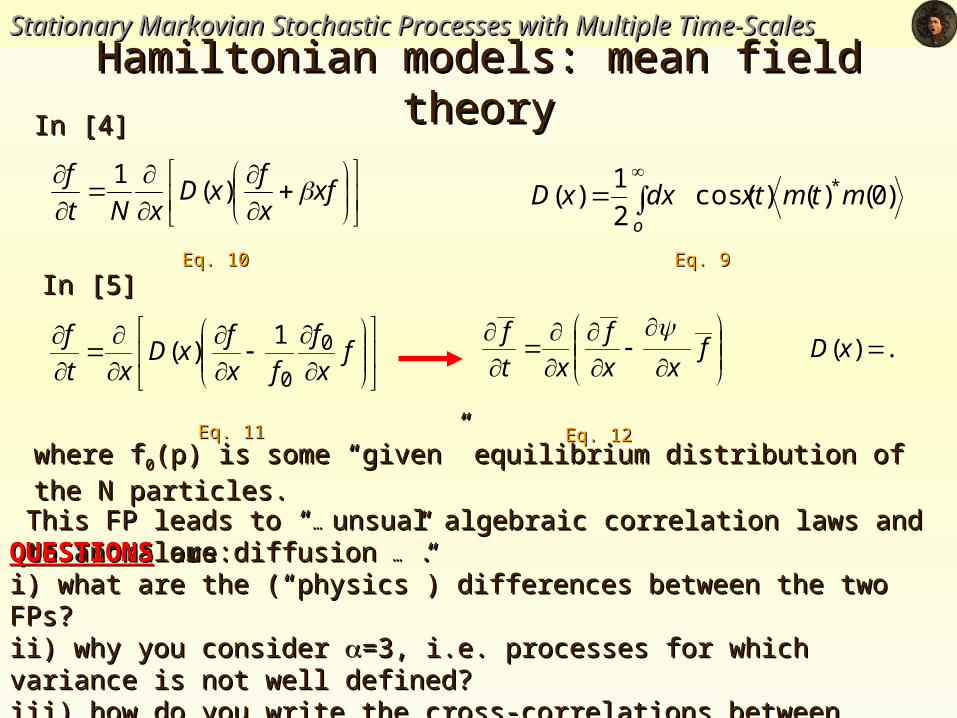

Hamiltonian models: mean field theoryHamiltonian models: mean field theoryIn [4]In [4]

In [5]In [5]Eq. 10Eq. 10

This FP leads to “This FP leads to “… … unsual algebraic correlation laws and to anomalous diffusion unsual algebraic correlation laws and to anomalous diffusion ……”.”.

where fwhere f00(p) is some “given” equilibrium distribution of the N particles.(p) is some “given” equilibrium distribution of the N particles.

QUESTIONSQUESTIONS are: are:i) what are the (“physics”) differences between the two FPs?i) what are the (“physics”) differences between the two FPs?ii) why you consider ii) why you consider =3, i.e. processes for which variance is not well defined?=3, i.e. processes for which variance is not well defined?iii) how do you write the cross-correlations between particles ?iii) how do you write the cross-correlations between particles ?

xfx

fxD

xNt

f )(1

Eq. 11Eq. 11 Eq. 12Eq. 12

Eq. 9Eq. 9

)0()()cos(2

1)( *mtmxtdxxD

o

fx

f

fx

fxD

xt

f 0

0

1)(

fxx

f

xt

f ...)( xD

ConclusionsConclusionsStationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

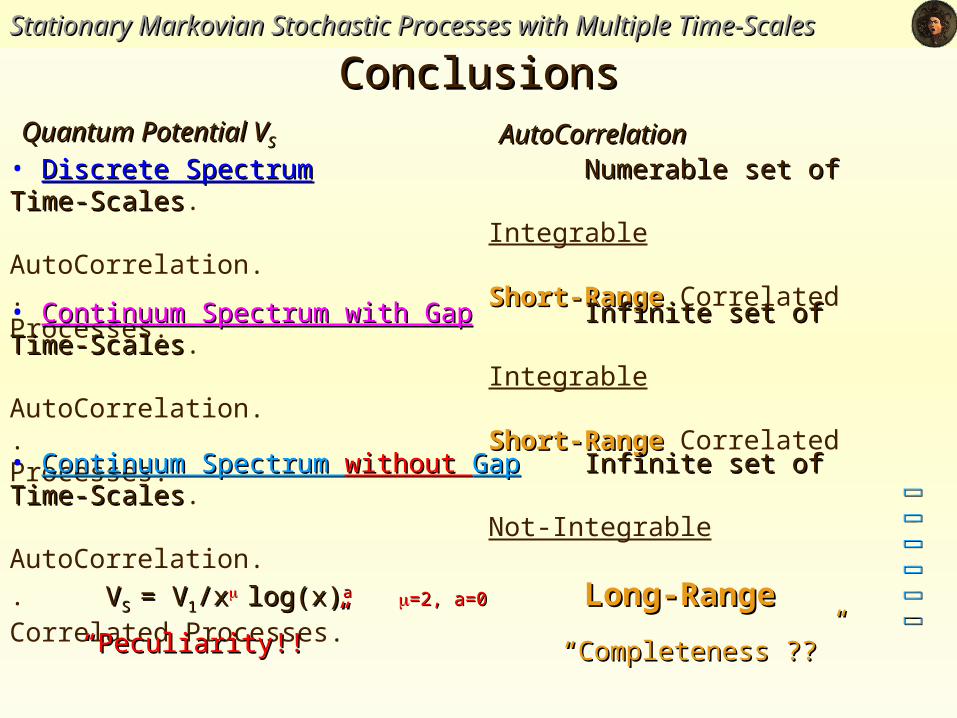

• Discrete SpectrumDiscrete Spectrum Numerable set of Time-ScalesNumerable set of Time-Scales. Integrable AutoCorrelation.. Short-RangeShort-Range Correlated Processes.

• Continuum Spectrum with GapContinuum Spectrum with Gap Infinite set of Time-ScalesInfinite set of Time-Scales. Integrable AutoCorrelation.. Short-RangeShort-Range Correlated Processes.

• Continuum Spectrum Continuum Spectrum without without GapGap Infinite set of Time-ScalesInfinite set of Time-Scales. Not-Integrable AutoCorrelation.

. VVS S = V= V11/x/x log(x)log(x)aa =2, a=0=2, a=0 Long-RangeLong-Range Correlated Processes.

““Completeness ??”Completeness ??”

Quantum Potential VQuantum Potential VSS AutoCorrelationAutoCorrelation

““Peculiarity!! ”Peculiarity!! ”

Ergodicity breakingErgodicity breaking

Part IIPart II

Ergodicity BreakingErgodicity Breaking

ReferencesReferences[1] [1] E. LutzE. Lutz, PRL, , PRL, 9393, , 190602, , (2004)(2004)[2][2] S. Miccichè, F. Lillo, R. N. Mantegna S. Miccichè, F. Lillo, R. N. Mantegna, in preparation, in preparation[3] [3] J.-P. BouchaudJ.-P. Bouchaud, J. Phys. I France, , J. Phys. I France, 22, , 1705, , (1992)(1992)[4][4] G. Bel, E. Barkai G. Bel, E. Barkai, cond-mat/0502154, cond-mat/0502154

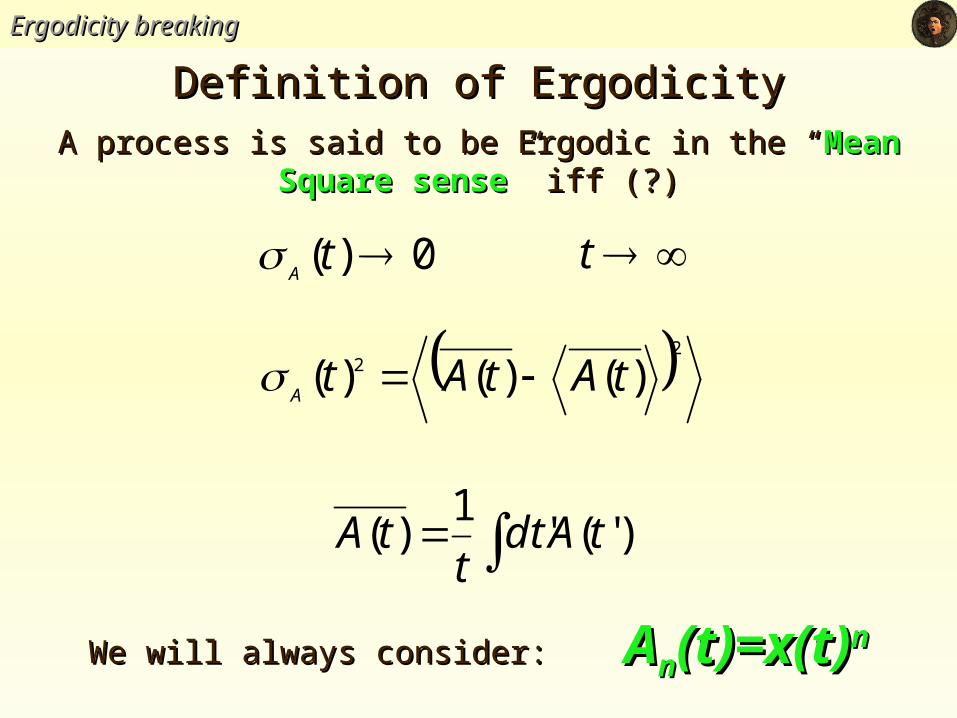

Ergodicity breakingErgodicity breaking

A process is said to be Ergodic in the “A process is said to be Ergodic in the “Mean Square Mean Square sensesense” iff (?)” iff (?)

22 )()()( tAtAtA

0)( tA

t

)'('1

)( tAdtt

tA

Definition of ErgodicityDefinition of Ergodicity

We will always consider: We will always consider: AAnn(t)=x(t)(t)=x(t)nn

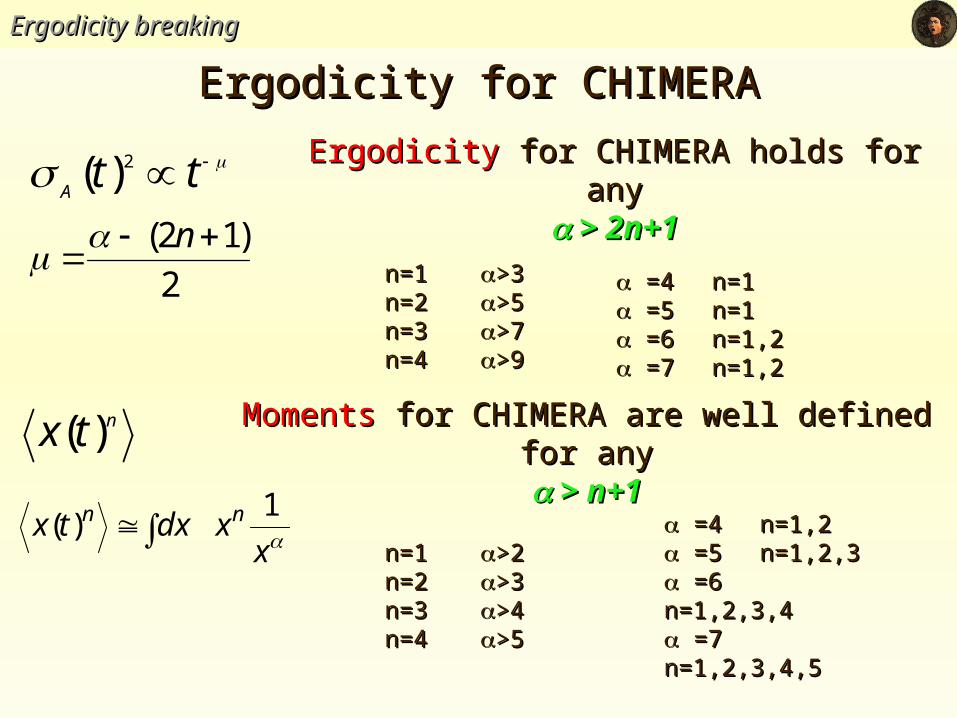

Ergodicity breakingErgodicity breaking

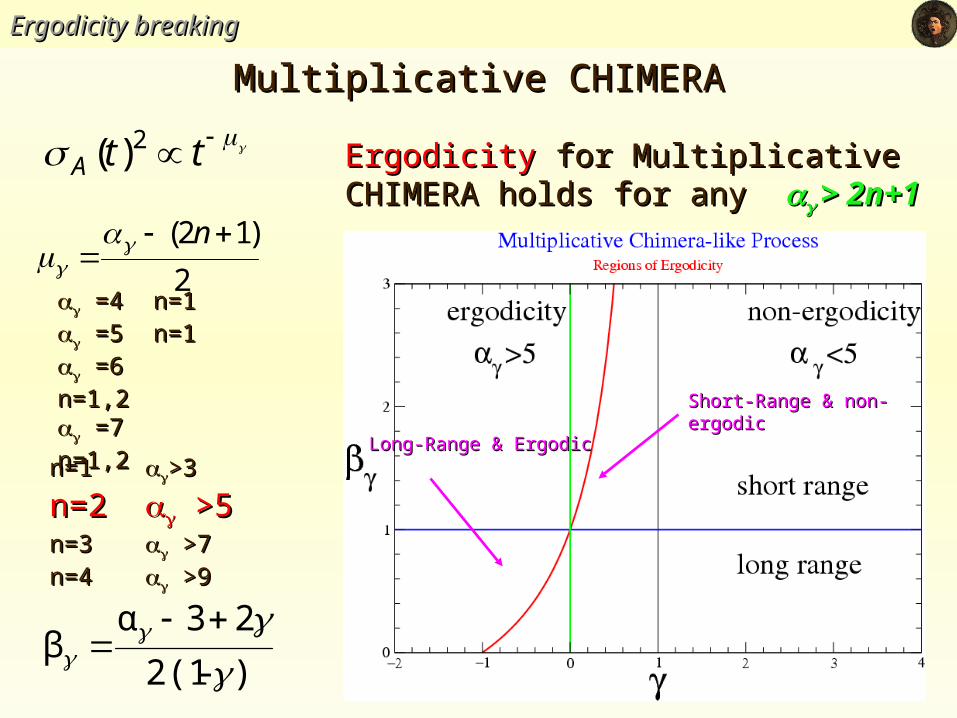

Ergodicity for CHIMERAErgodicity for CHIMERA

ttA

2)(

2

)12(

n

ErgodicityErgodicity for CHIMERA holds for any for CHIMERA holds for any > 2n+1 > 2n+1

n=1n=1 >3>3n=2n=2 >5>5n=3n=3 >7>7n=4n=4 >9>9

ntx )( MomentsMoments for CHIMERA are well defined for for CHIMERA are well defined for anyany

> n+1 > n+1

n=1n=1 >2>2n=2n=2 >3>3n=3n=3 >4>4n=4n=4 >5>5

=4=4 n=1,2n=1,2 =5 =5 n=1,2,3n=1,2,3 =6 =6 n=1,2,3,4n=1,2,3,4 =7 =7n=1,2,3,4,5n=1,2,3,4,5

=4=4 n=1n=1 =5 =5 n=1n=1 =6 =6 n=1,2n=1,2 =7 =7 n=1,2n=1,2

xxdxtx nn 1

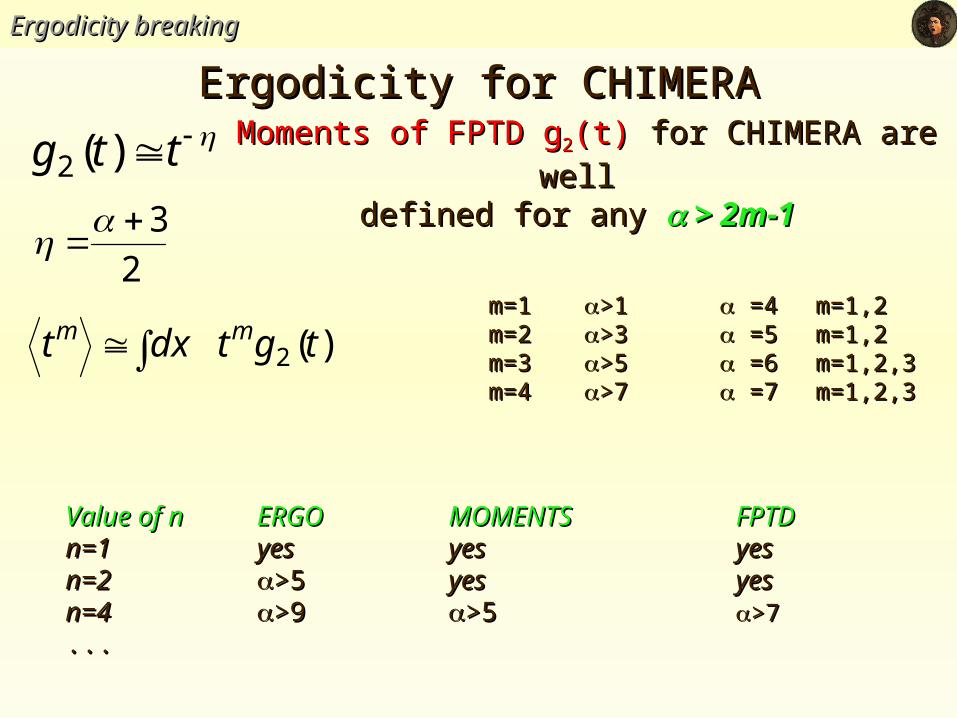

)(

Ergodicity breakingErgodicity breaking

ttg )(2 Moments of FPTD gMoments of FPTD g22(t)(t) for CHIMERA are well for CHIMERA are well defined for any defined for any > 2m-1 > 2m-1

=4=4 m=1,2m=1,2 =5 =5 m=1,2m=1,2 =6 =6m=1,2,3m=1,2,3 =7 =7m=1,2,3m=1,2,3

Value of nValue of n ERGOERGO MOMENTSMOMENTS FPTDFPTDn=1n=1 yesyes yesyes yesyesn=2n=2 >5>5 yes yes yesyes n=4n=4 >9>9 >5>5 >7>7 ......

Ergodicity for CHIMERAErgodicity for CHIMERA

m=1m=1 >1>1m=2m=2 >3>3m=3m=3 >5>5m=4m=4 >7>7

)(2 tgtdxt mm

2

3

Ergodicity breakingErgodicity breaking

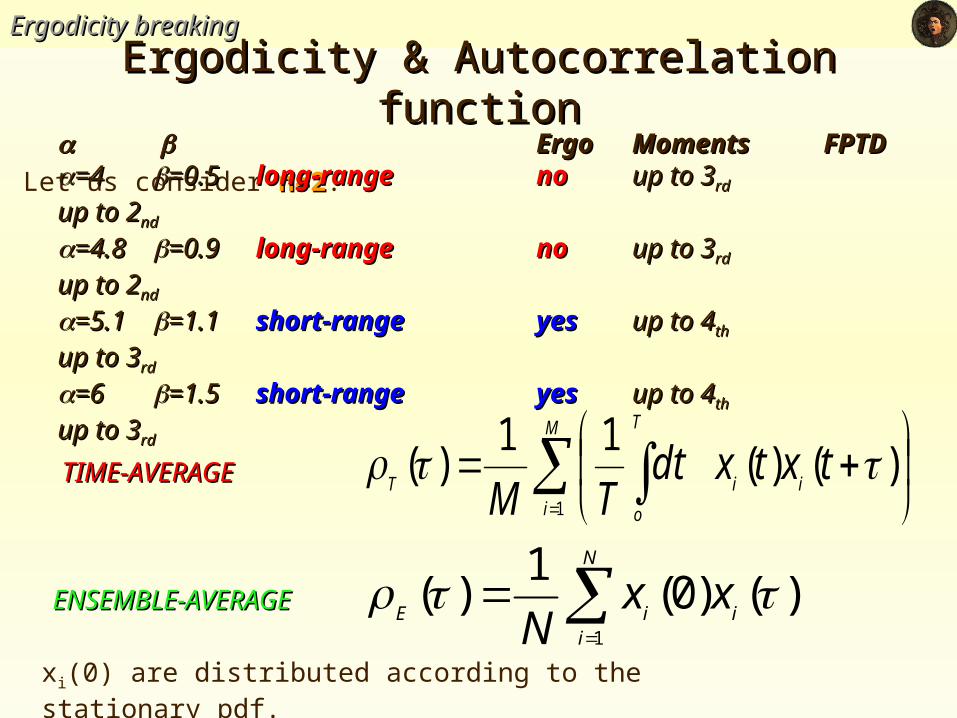

Let us consider n=2n=2:

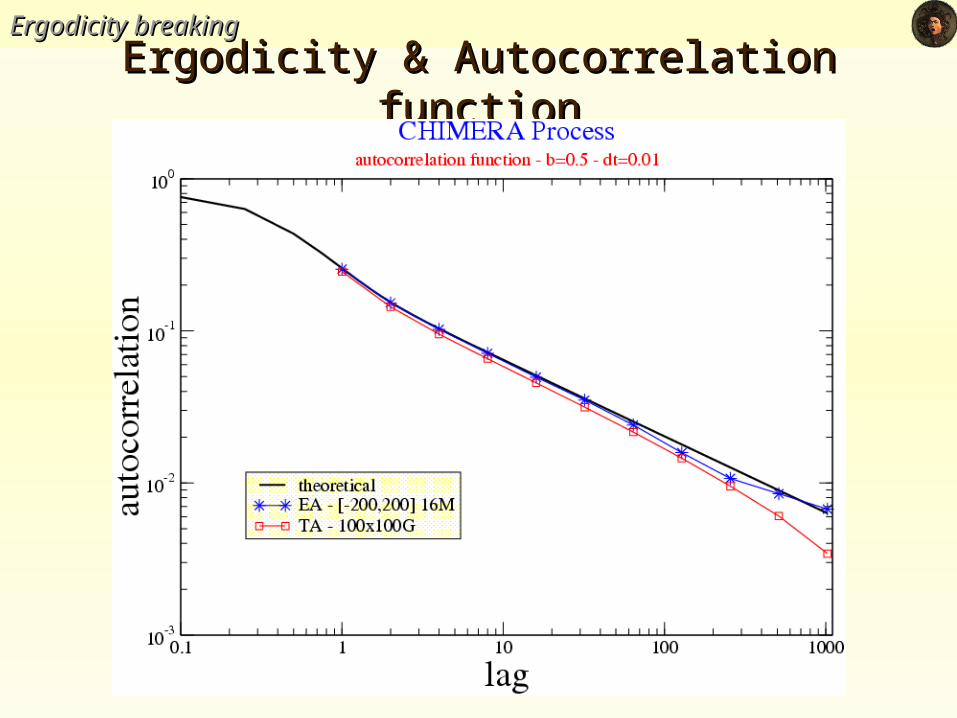

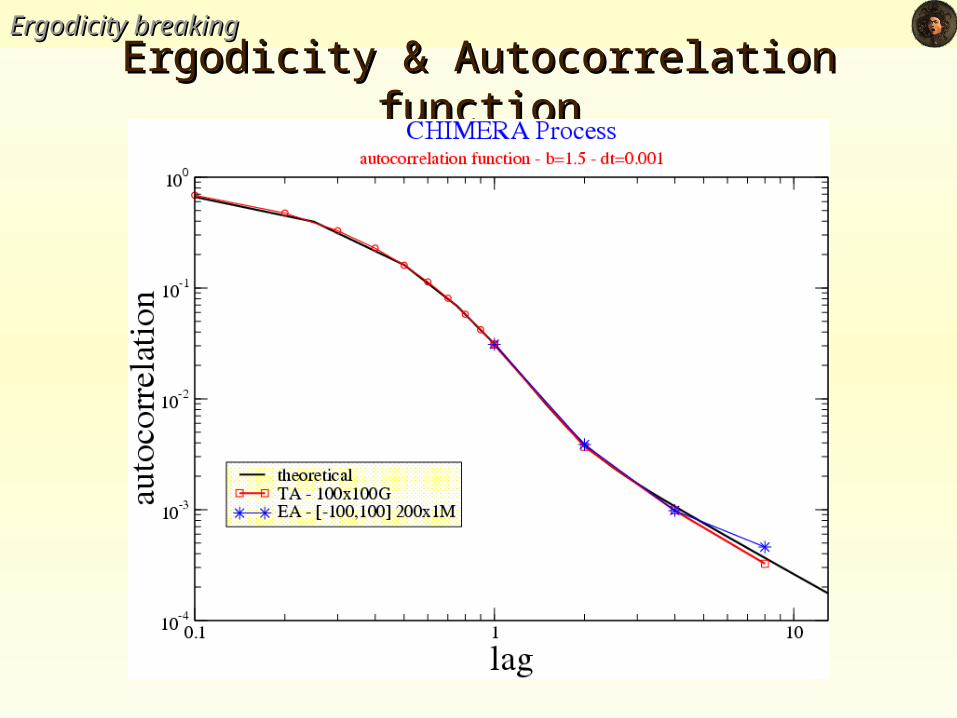

Ergodicity & Autocorrelation functionErgodicity & Autocorrelation function

ErgoErgo MomentsMoments FPTDFPTD=4=4 =0.5=0.5 long-rangelong-range nono up to 3up to 3rd rd up to 2up to 2ndnd

=4.8=4.8 =0.9=0.9 long-rangelong-range nono up to 3up to 3rd rd up to 2up to 2ndnd

=5.1=5.1 =1.1=1.1 short-rangeshort-range yesyes up to 4up to 4thth up to up to 33rdrd

=6=6 =1.5=1.5 short-rangeshort-range yesyes up to 4up to 4th th up to 3up to 3rdrd

TIME-AVERAGETIME-AVERAGE

ENSEMBLE-ENSEMBLE-AVERAGEAVERAGE

N

iiiE

xxN 1

)()0(1

)(

M

i

T

o

iiTtxtxdt

TM 1

)()(11

)(

xi(0) are distributed according to the stationary pdf.

Ergodicity breakingErgodicity breaking

Ergodicity & Autocorrelation functionErgodicity & Autocorrelation function

Ergodicity breakingErgodicity breaking

Ergodicity & Autocorrelation functionErgodicity & Autocorrelation function

Ergodicity breakingErgodicity breaking

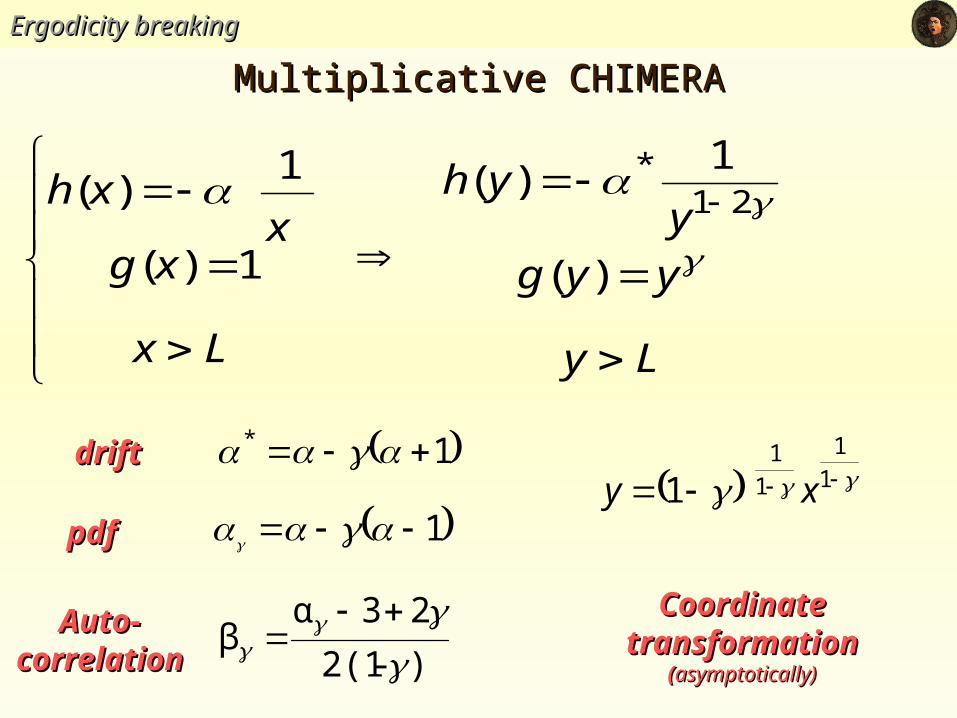

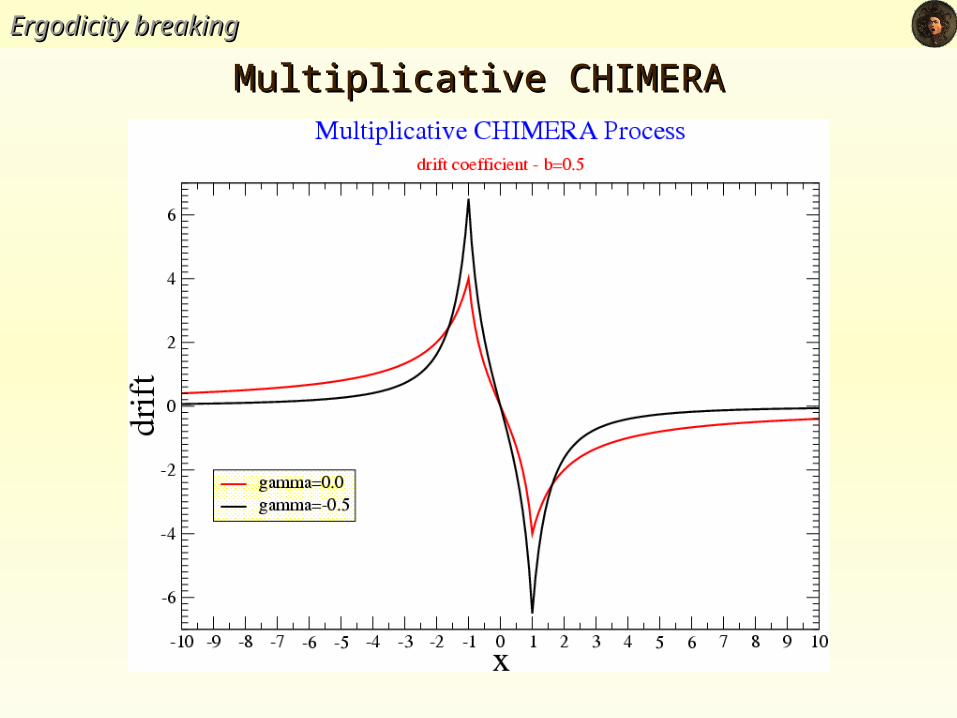

Multiplicative CHIMERAMultiplicative CHIMERA

)-2(1

23αβ

Ly

yyg

yyh

Lx

xgx

xh

)(

1)(

1)(

1)( 21

*

1 pdfpdf

Auto-Auto-correlatiocorrelatio

nn

driftdrift 1*

CoordinateCoordinatetransformationtransformation

((asymptotically)asymptotically)

1

1

1

1

1 xy

Ergodicity breakingErgodicity breaking

Multiplicative CHIMERAMultiplicative CHIMERA

Ergodicity breakingErgodicity breaking

Multiplicative CHIMERAMultiplicative CHIMERA

ttA2)(

2

)12(

n

ErgodicityErgodicity for Multiplicative CHIMERA for Multiplicative CHIMERA holds for any holds for any > 2n+1> 2n+1

n=1n=1 >3>3

n=2n=2 >5 >5n=3n=3 >7 >7n=4n=4 >9 >9

=4=4 n=1n=1 =5 =5 n=1n=1 =6 =6n=1,2n=1,2 =7 =7n=1,2n=1,2

)-2(1

23αβ

Short-Range & non-Short-Range & non-ergodicergodic

Long-Range & ErgodicLong-Range & Ergodic

Ergodicity breakingErgodicity breaking

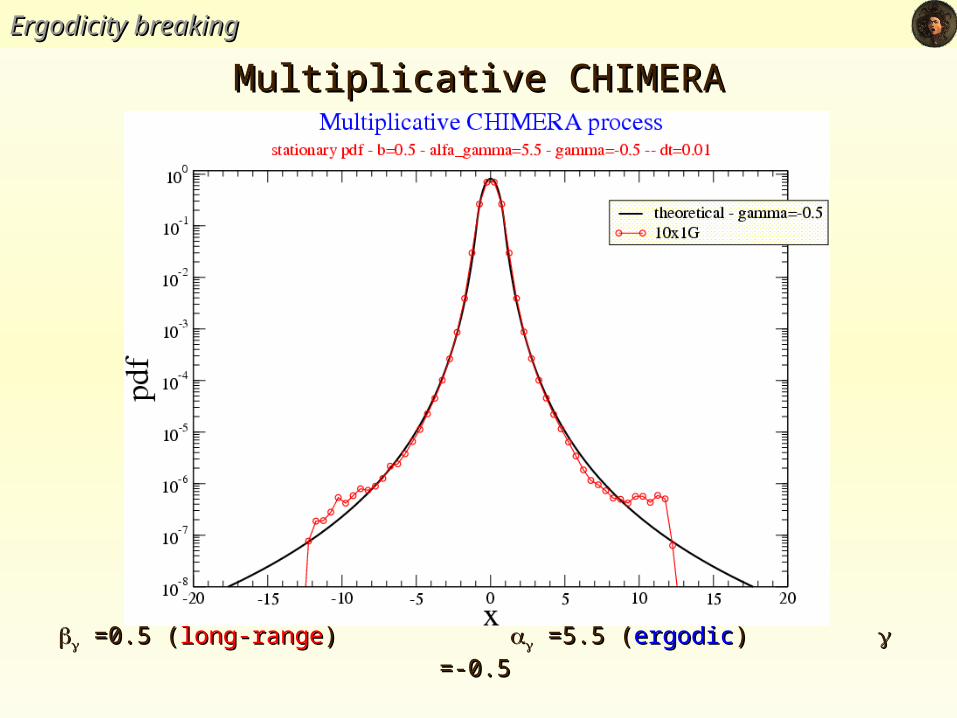

Multiplicative CHIMERAMultiplicative CHIMERA

=0.5 (=0.5 (long-rangelong-range) ) =5.5 ( =5.5 (ergodicergodic) ) =-0.5 =-0.5

Ergodicity breakingErgodicity breaking

Multiplicative CHIMERAMultiplicative CHIMERA

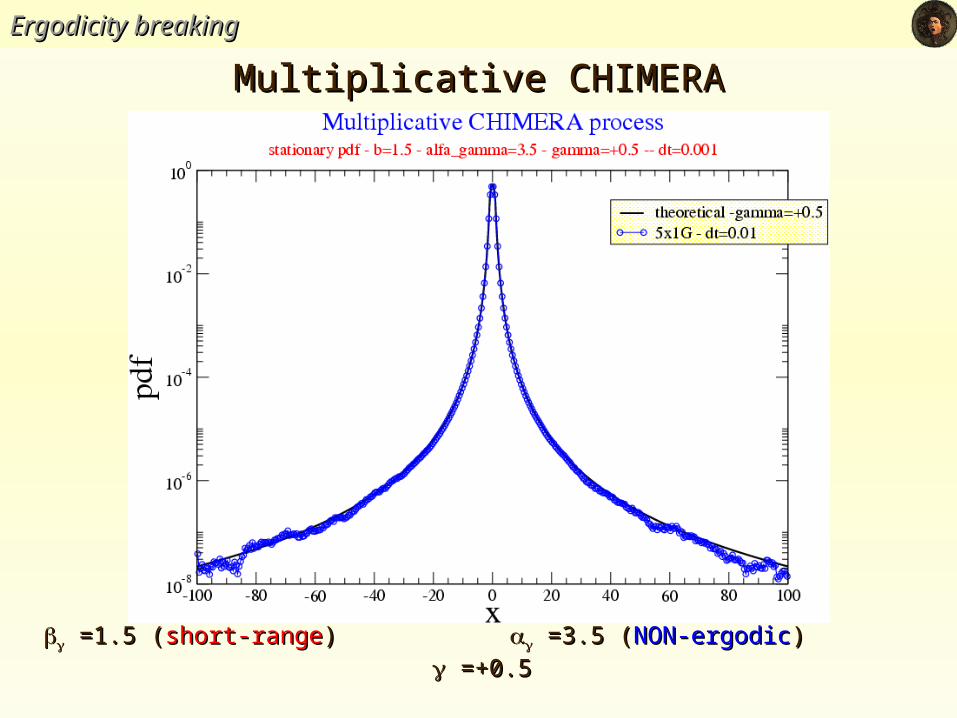

=1.5 (=1.5 (short-rangeshort-range) ) =3.5 ( =3.5 (NON-ergodicNON-ergodic) ) =+0.5 =+0.5

Tentative ConclusionsTentative ConclusionsErgodicity breakingErgodicity breaking

Ergodicity Short-Range CorrelationNon-Ergodicity Long-Range CorrelationIs true only true for Stationary Markovian processes with additive

noise

1)1)

For Stationary Markovian processes with multiplicative noise one For Stationary Markovian processes with multiplicative noise one might have:might have:2)2)

Non-Ergodicity & Short-Range Non-Ergodicity & Short-Range CorrelationCorrelation

Ergodicity Ergodicity Long-Range Correlation Long-Range Correlation

MOMENTS of pdfMOMENTS of pdf are diverging ? are diverging ?or

MOMENTS of FPTDMOMENTS of FPTD are diverging - Sojourn times [3]? are diverging - Sojourn times [3]?

3)3) QUESTIONQUESTION is: what is the intimateintimate source of Ergodicity Breaking ?

In In CHIMERACHIMERA-like processes these features are both present. -like processes these features are both present. What about other (non markovian ? ) processes [4]?What about other (non markovian ? ) processes [4]?

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

Part IIIPart III

EconoEcono PhysicsPhysics

from from -PHYSICS-PHYSICS to to ECONO-ECONO- (?) (?)

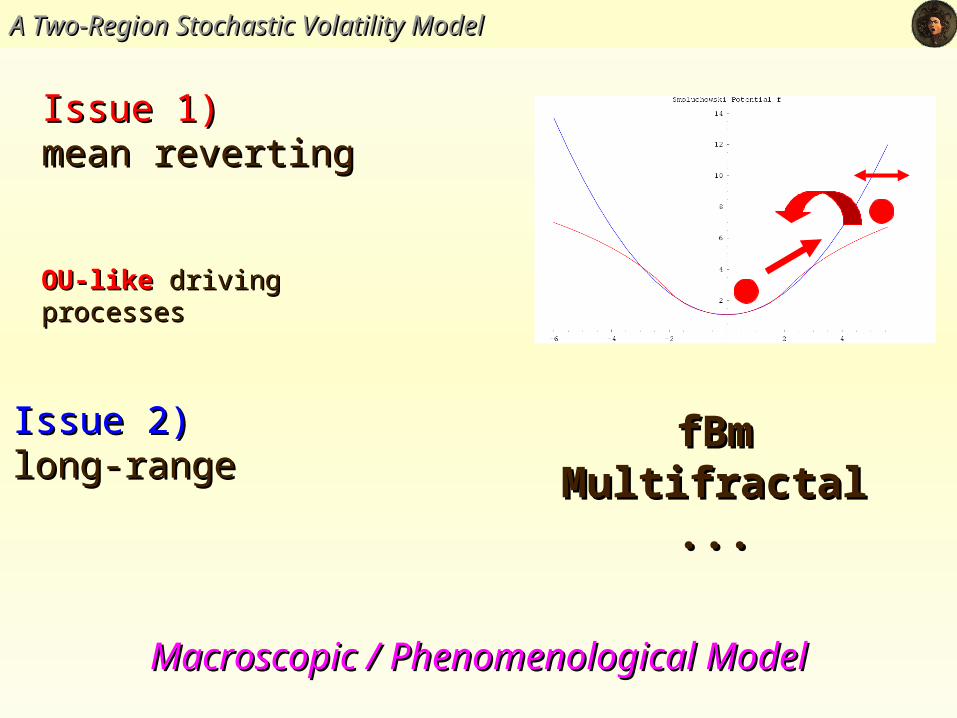

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

Issue 1)Issue 1) mean revertingmean reverting

OU-likeOU-like driving processes driving processes

Issue 2)Issue 2) long-rangelong-range

fBmfBmMultifractalMultifractal

......

Macroscopic / Phenomenological ModelMacroscopic / Phenomenological Model

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

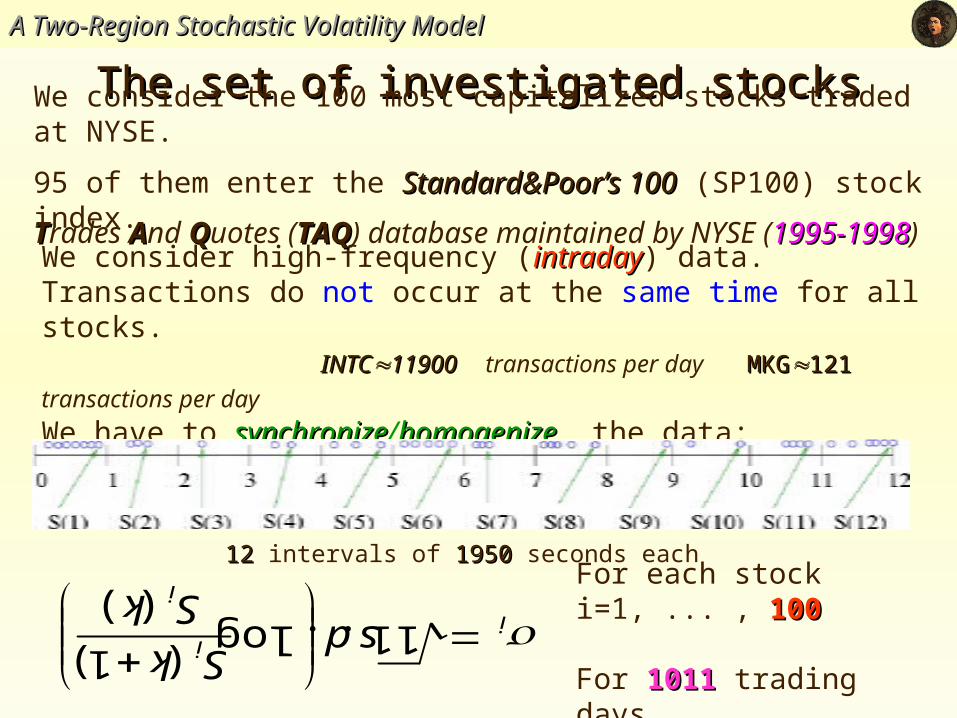

The set of investigated stocksThe set of investigated stocksWe consider the 100 most capitalized stocks traded at NYSE.

95 of them enter the Standard&Poor’s 100Standard&Poor’s 100 (SP100) stock index.

We consider high-frequency (intradayintraday) data. Transactions do not occur at the same time for all stocks. INTCINTC1190011900 transactions per day MKGMKG121 121 transactions per day We have to synchronizesynchronize/homogenizehomogenize the data:

) (

)1 (log . . 11

k S

k Sds

i

ii For each stock i=1, ... , 100100

For 10111011 trading days

1212 intervals of 19501950 seconds each

TTrades AAnd QQuotes (TAQTAQ) database maintained by NYSE (1995-19981995-1998)

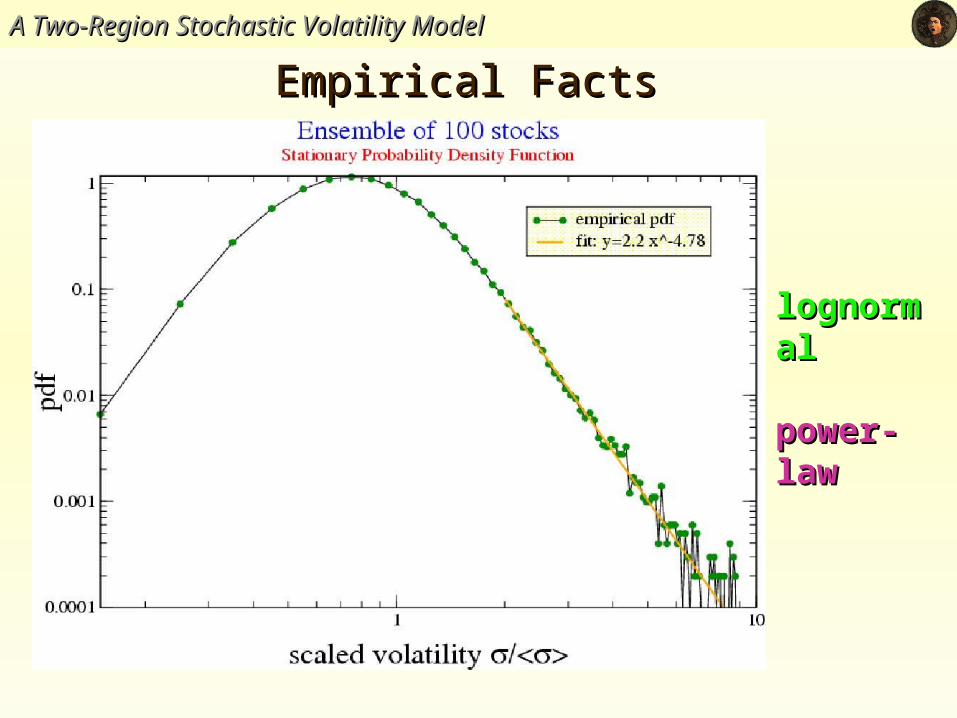

Empirical FactsEmpirical Facts A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

lognormallognormal

power-lawpower-law

Empirical Facts Empirical Facts A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

(()) --

0.30.3

Empirical Facts Empirical Facts A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

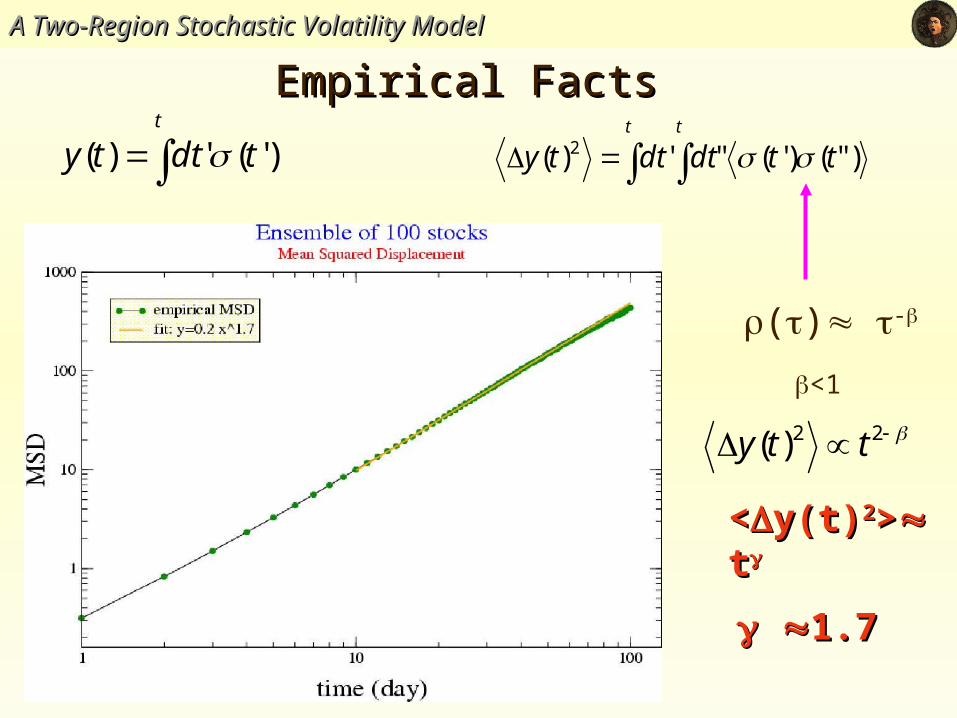

<<y(t)y(t)22>> t t

1.71.7

() -

<1

t

tdtty )'(')( t t

ttdtdtty )"()'("')( 2

22)( tty

Empirical Facts Empirical Facts A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

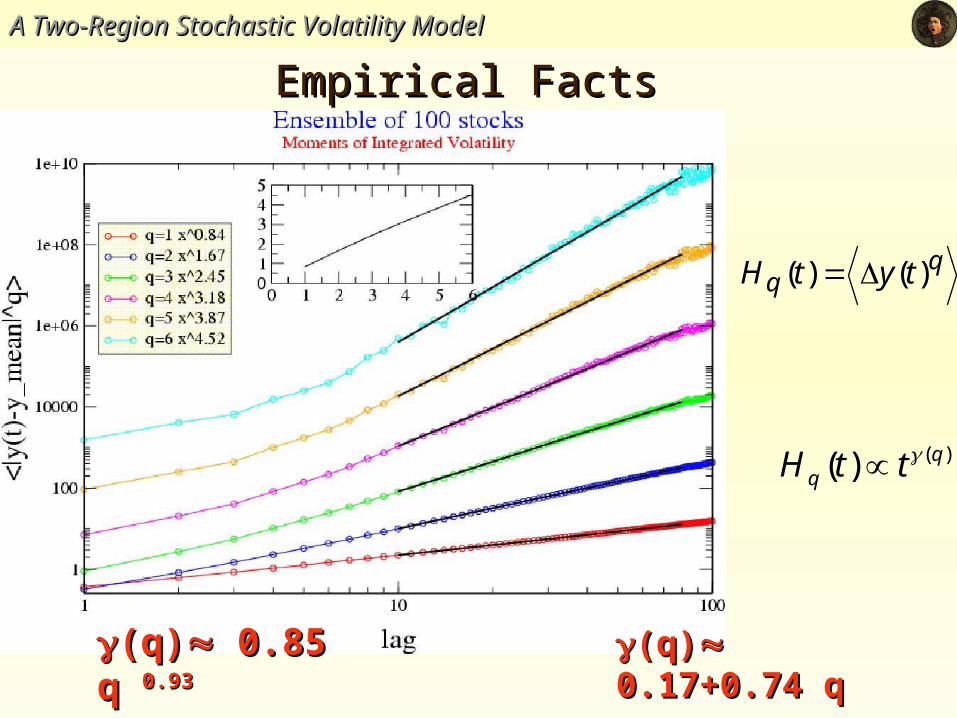

qq tytH )()(

)()( qq ttH

(q)(q) 0.17+0.74 0.17+0.74 qq

(q)(q) 0.85 q 0.85 q 0.930.93

Empirical Facts Empirical Facts A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

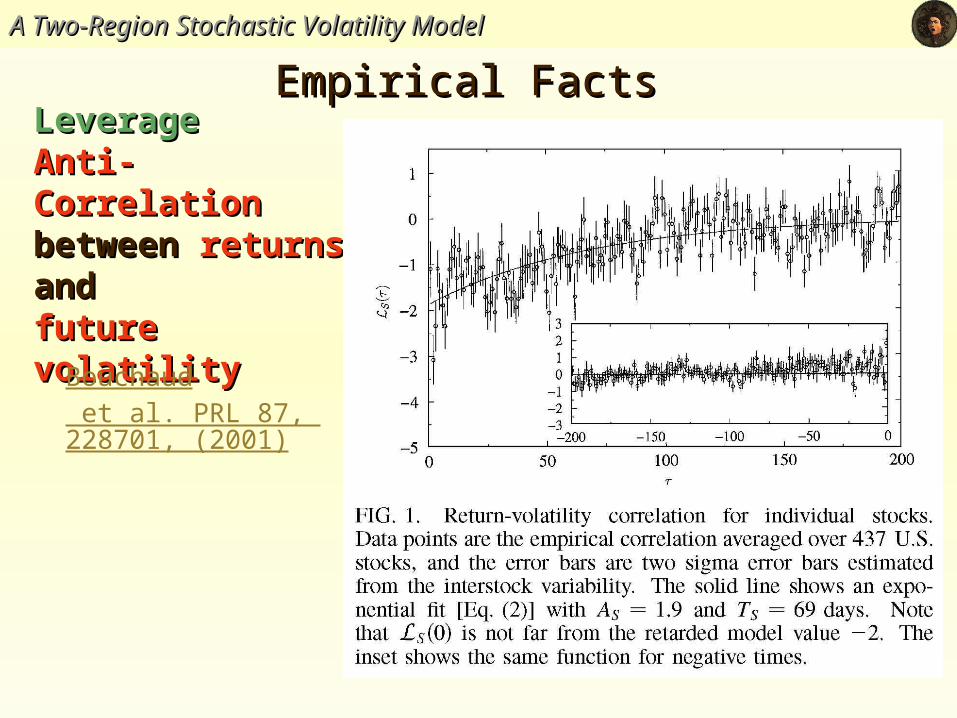

LeverageLeverage Anti-Correlation Anti-Correlation between between returnsreturns and and future volatility future volatility

Bouchaud et al. PRL 87, 228701, (2001)

Models of Stochastic VolatilityModels of Stochastic VolatilityA Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

What are the appropriate

i) Drift coefficient h(Drift coefficient h())

ii) Diffusion coefficient g(Diffusion coefficient g())

able to reproduce the previous empirical stylized facts ?

We are looking for models of stochastic volatility:

dS/S = dt + d z

d = h() dt + g() d z.

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

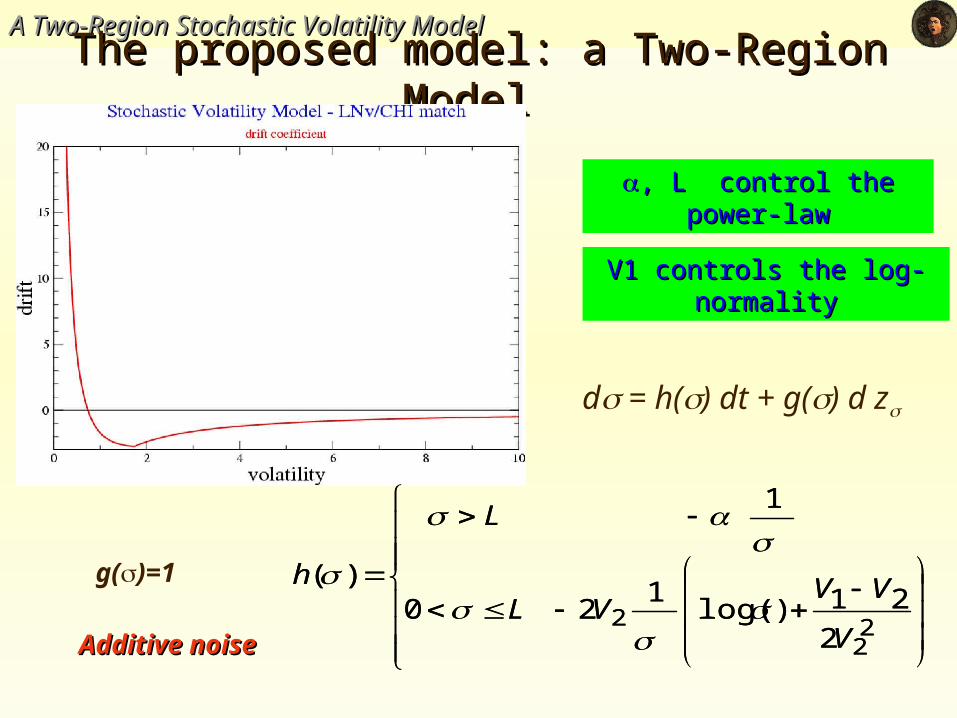

The proposed model: a Two-Region Model The proposed model: a Two-Region Model

22

22

21)log(1

20

1

)(

V

VVVL

L

h

g()=1

Additive noiseAdditive noise

, L control the power-, L control the power-lawlaw

V1 controls the log-V1 controls the log-normalitynormality

22

22

21)log(1

20

1

)(

V

VVVL

L

h

d = h() dt + g() d z

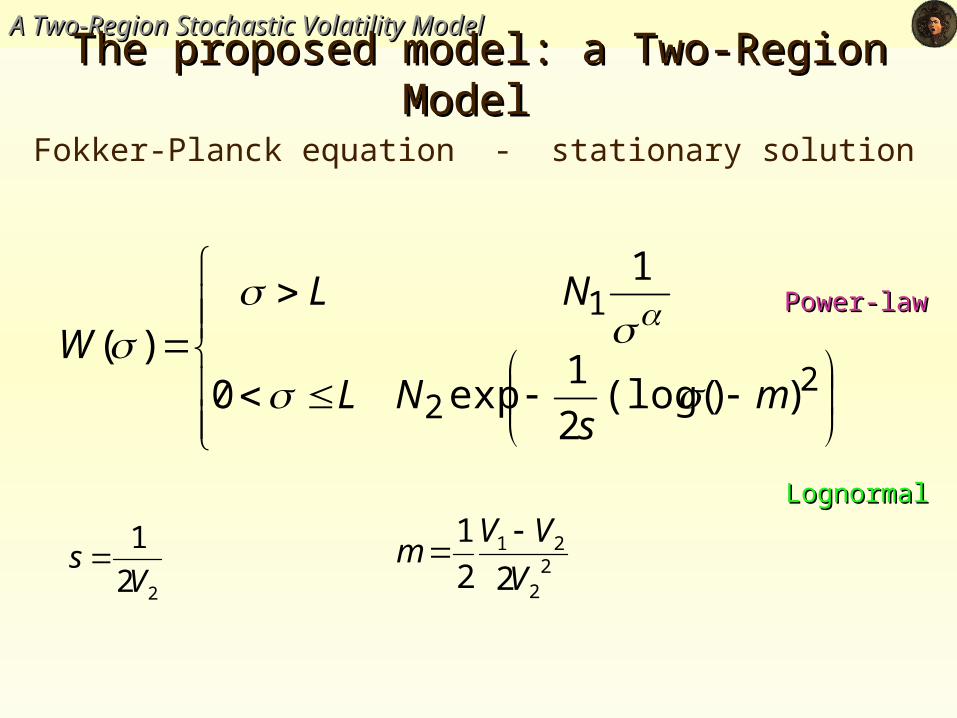

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

The proposed model: a Two-Region Model The proposed model: a Two-Region Model

22

1

))(log(2

1exp0

1

)(m

sNL

NLW

22

21

22

1

V

VVm

22

1

Vs

LognormalLognormal

Power-lawPower-law

Fokker-Planck equation - stationary solution

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

The proposed model: a Two-Region Model The proposed model: a Two-Region Model

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

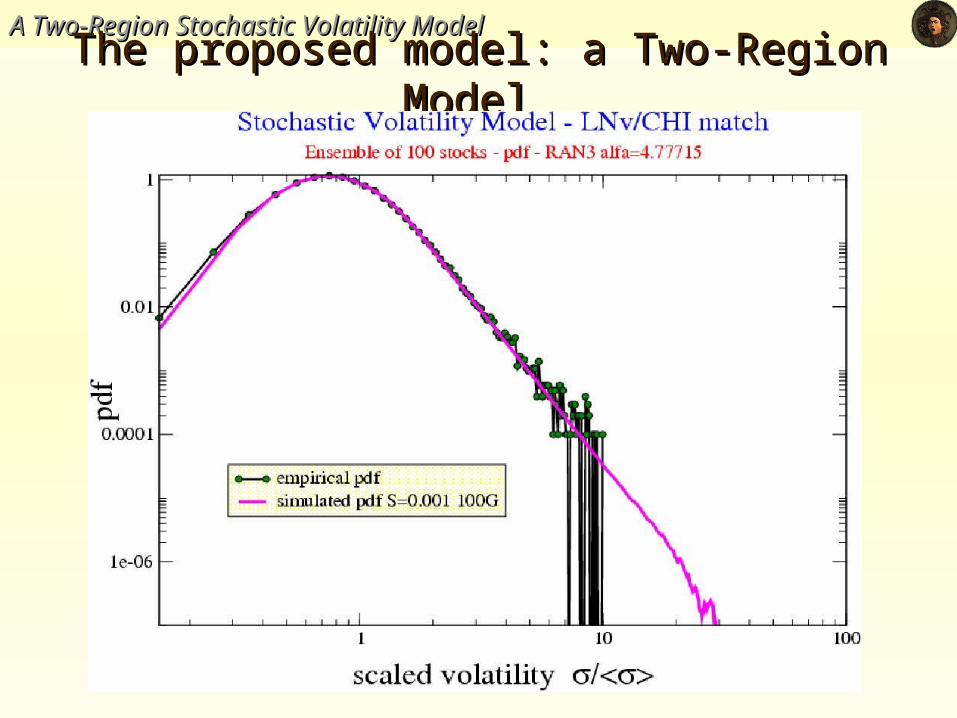

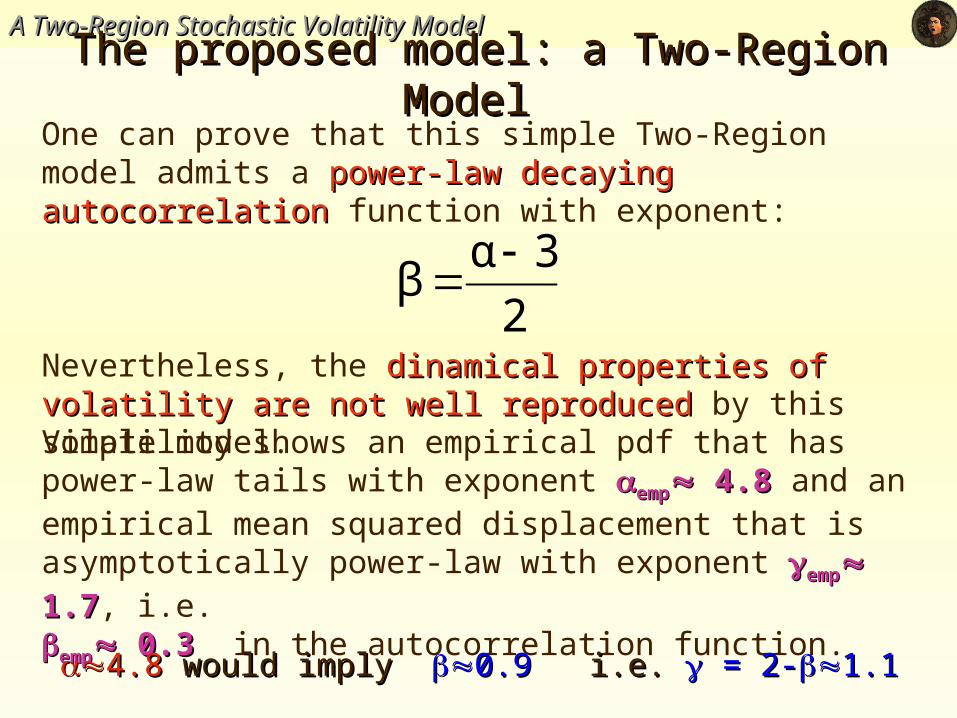

Nevertheless, the dinamical properties of volatility are not well dinamical properties of volatility are not well reproducedreproduced by this simple model.

The proposed model: a Two-Region Model The proposed model: a Two-Region Model

Volatility shows an empirical pdf that has power-law tails with exponent empemp 4.8 4.8 and an empirical mean squared displacement that is asymptotically power-law with exponent empemp 1.7 1.7, i.e.

empemp 0.3 0.3 in the autocorrelation function.

One can prove that this simple Two-Region model admits a power-power-law decaying autocorrelationlaw decaying autocorrelation function with exponent:

2

3αβ

4.8 4.8 would imply would imply 0.9 0.9 i.e.i.e. = 2- = 2-1.11.1

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

The proposed model: a Two-Region Model The proposed model: a Two-Region Model

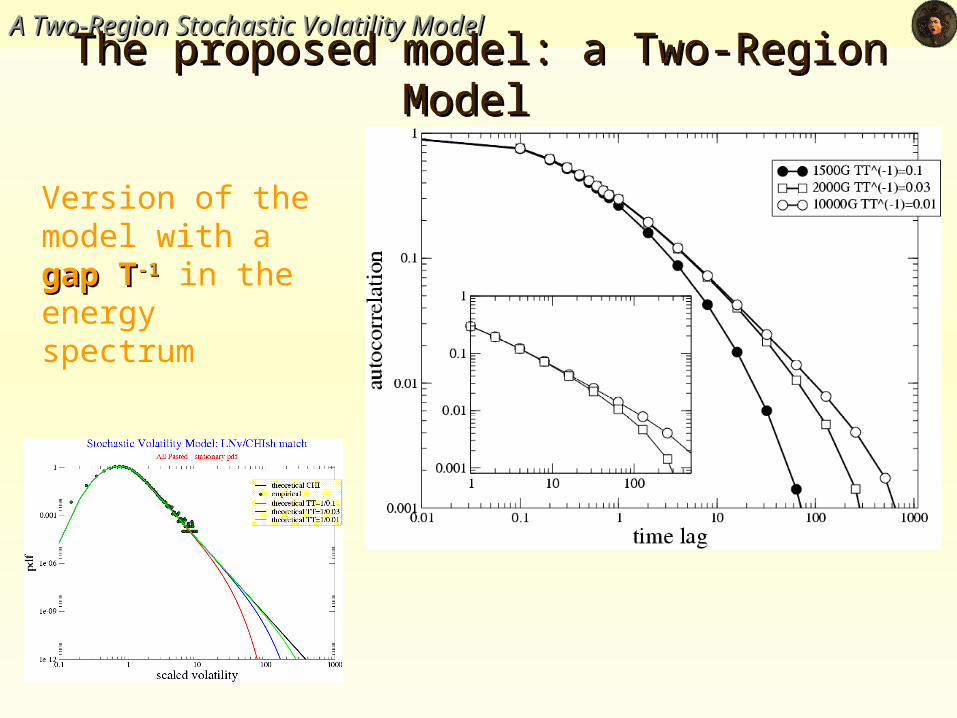

Version of the model with a gapgap TT-1-1 in the energy spectrum

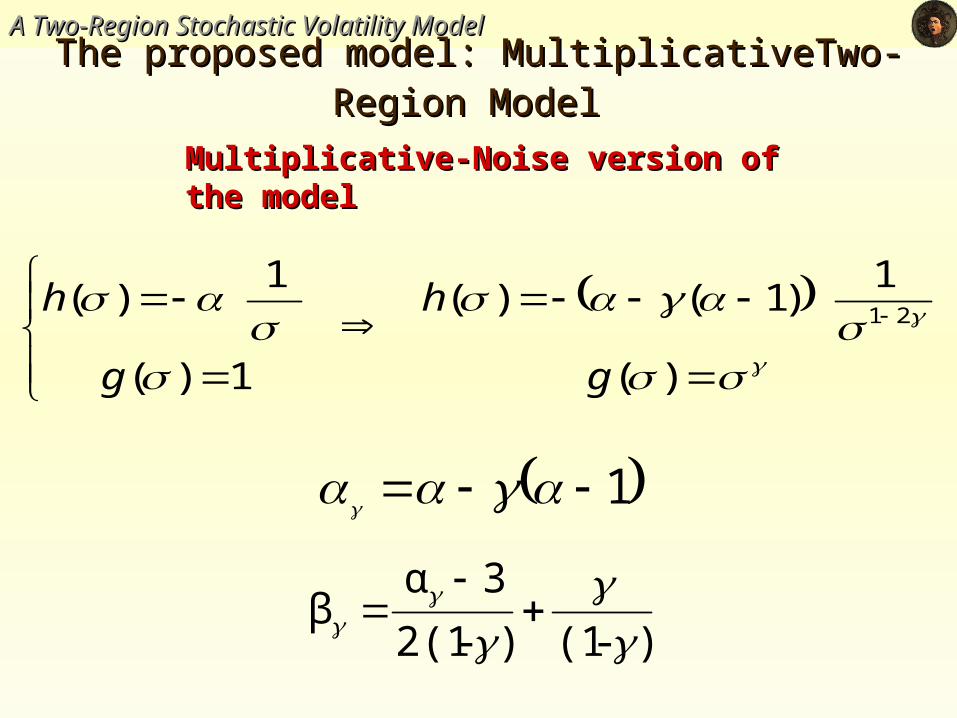

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility ModelThe proposed model: MultiplicativeTwo-Region The proposed model: MultiplicativeTwo-Region

ModelModel

Multiplicative-Noise version of the modelMultiplicative-Noise version of the model

)-(1)-2(1

3αβ

)(

1)1()(

1)(

1)(

21

g

h

g

h

1

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

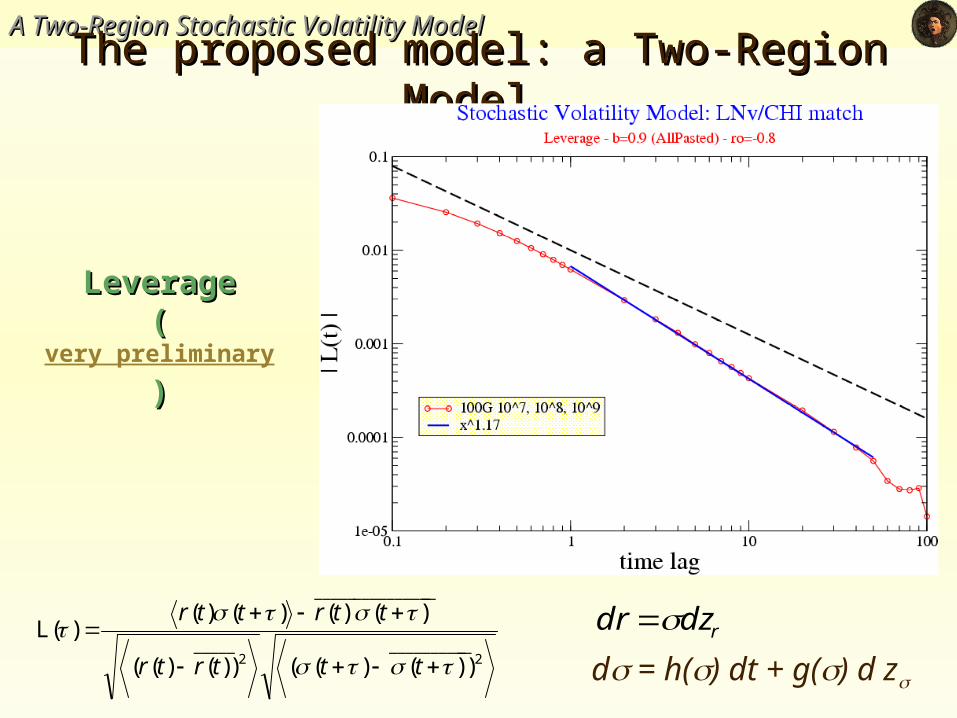

The proposed model: a Two-Region Model The proposed model: a Two-Region Model

LeverageLeverage((very preliminary))

2___________

2_____

________________

))()(())()((

)()()()()(L

tttrtr

ttrttrrdzdr

d = h() dt + g() d z

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

ConclusionsConclusions

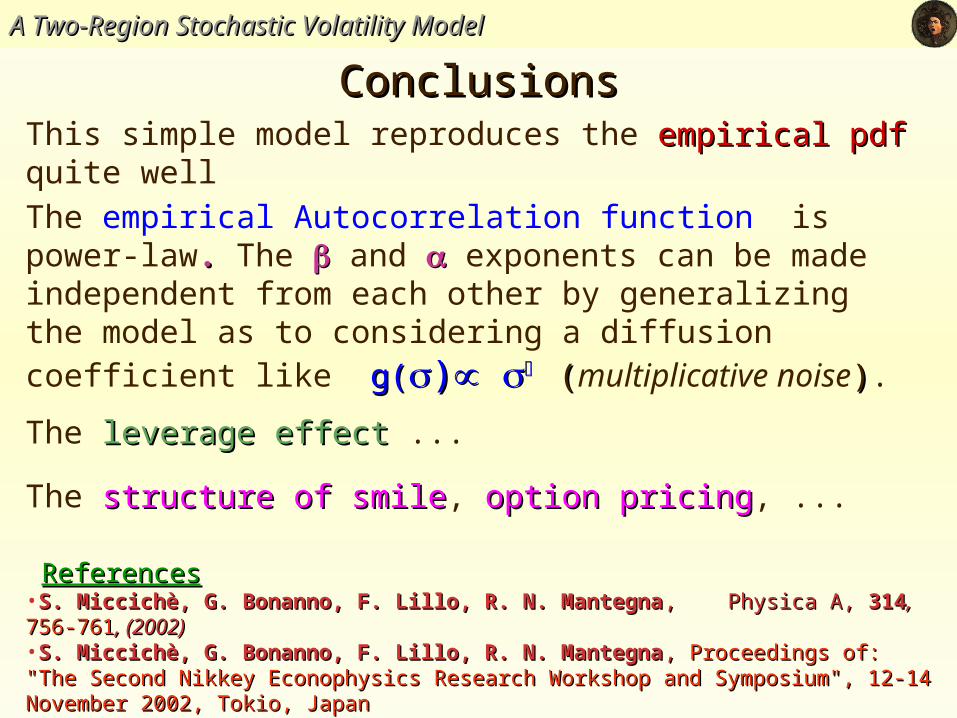

ReferencesReferences•S. Miccichè, G. Bonanno, F. Lillo, R. N. MantegnaS. Miccichè, G. Bonanno, F. Lillo, R. N. Mantegna , Physica A, , Physica A, 314314, , 756-761756-761, (2002), (2002)•S. Miccichè, G. Bonanno, F. Lillo, R. N. MantegnaS. Miccichè, G. Bonanno, F. Lillo, R. N. Mantegna , , Proceedings of: "The Second Nikkey Proceedings of: "The Second Nikkey Econophysics Research Workshop and Symposium", 12-14 November 2002, Tokio, Japan Econophysics Research Workshop and Symposium", 12-14 November 2002, Tokio, Japan Springer Verlag, Tokio, edited by H. Takayasu Springer Verlag, Tokio, edited by H. Takayasu

This simple model reproduces the empirical pdfempirical pdf quite well

The empirical Autocorrelation function is power-law. . The and exponents can be made independent from each other by generalizing the model as to considering a diffusion coefficient like g(g())

((multiplicative noise)).

The leverage effectleverage effect ...

The structure of smilestructure of smile, option pricingoption pricing, ...

A Two-Region Stochastic Volatility ModelA Two-Region Stochastic Volatility Model

Additional SlidesAdditional Slides

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

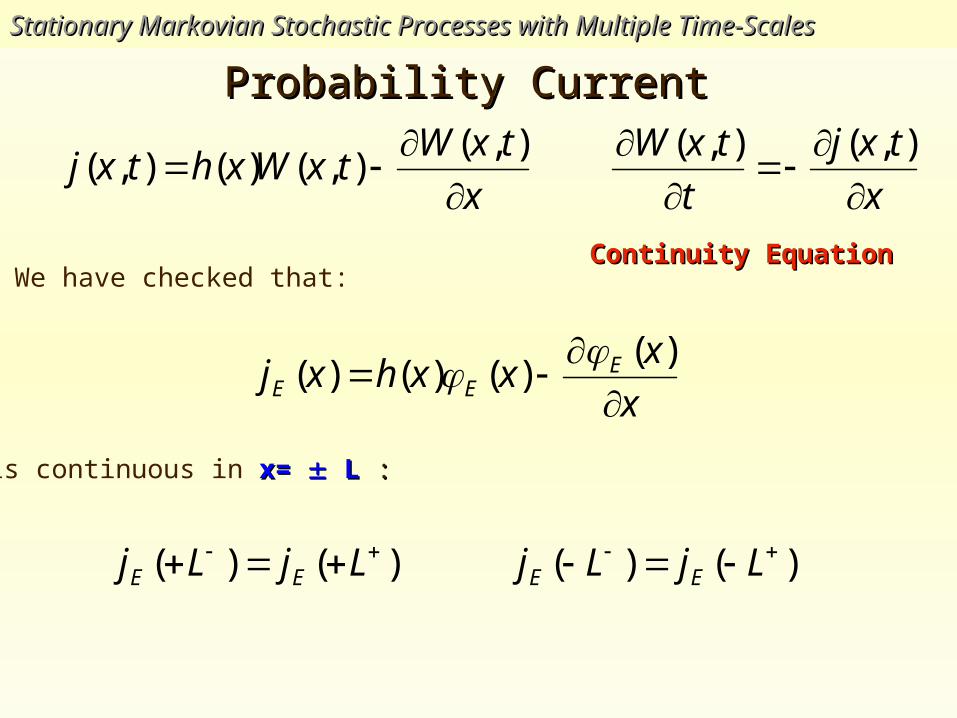

Probability Current Probability Current

x

txWtxWxhtxj

),(

),()(),(

We have checked that:

x

xxxhxj E

EE

)(

)()()(

is continuous in x= x= L L ::

)()( LjLj EE )()( LjLj EE

x

txj

t

txW

),(),(

Continuity EquationContinuity Equation

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

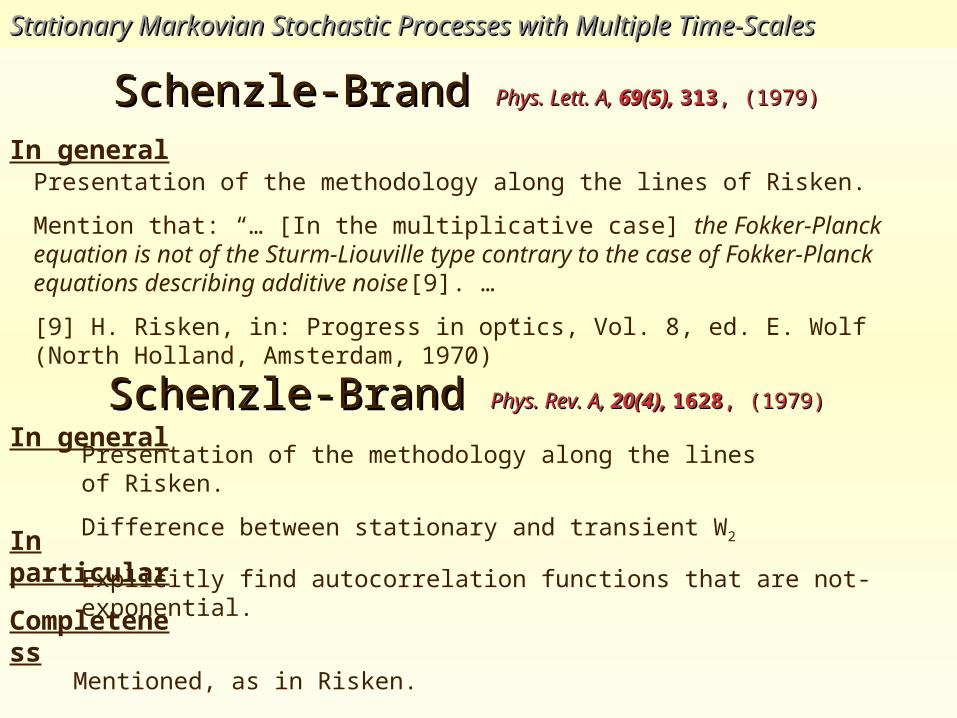

Schenzle-Brand Schenzle-Brand Phys. Rev. A, Phys. Rev. A, 20(4), 20(4), 16281628, (1979), (1979)

Completeness

In particular

Presentation of the methodology along the lines of Risken.

Difference between stationary and transient W2

Explicitly find autocorrelation functions that are not-exponential.

In general

Mentioned, as in Risken.

Schenzle-Brand Schenzle-Brand Phys. Lett. A, Phys. Lett. A, 69(5), 69(5), 313313, (1979), (1979)

Presentation of the methodology along the lines of Risken.

Mention that: “… [In the multiplicative case] the Fokker-Planck equation is not of the Sturm-Liouville type contrary to the case of Fokker-Planck equations describing additive noise[9]. …

[9] H. Risken, in: Progress in optics, Vol. 8, ed. E. Wolf (North Holland, Amsterdam, 1970)”

In general

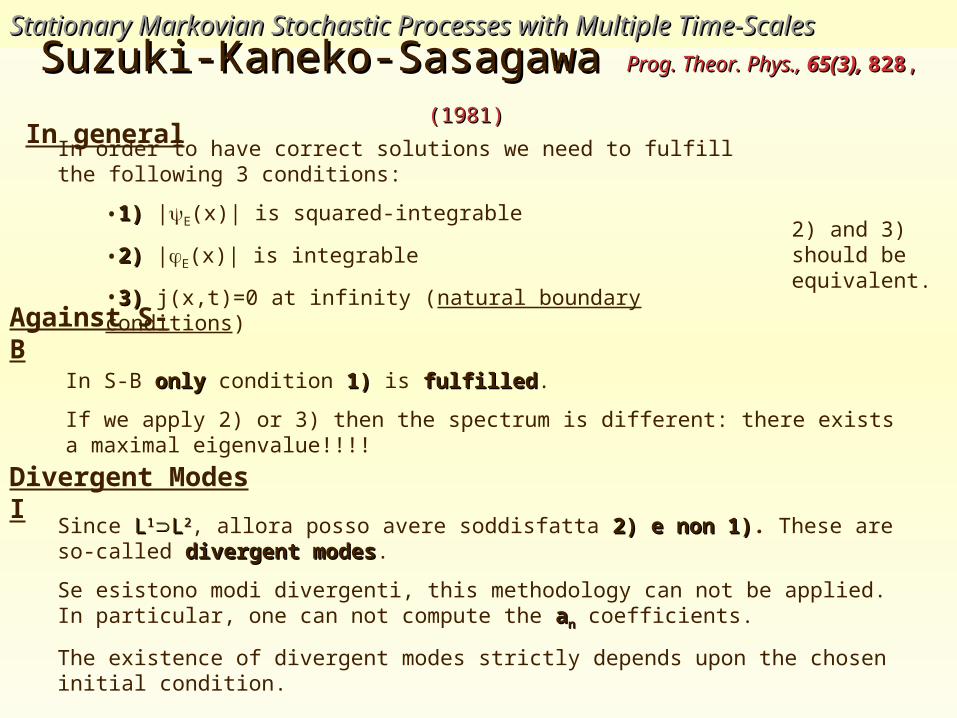

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesSuzuki-Kaneko-Sasagawa Suzuki-Kaneko-Sasagawa Prog. Theor. Phys., Prog. Theor. Phys., 65(3), 65(3), 828828, ,

(1981)(1981) In general

Against S-B

Divergent Modes I

In order to have correct solutions we need to fulfill the following 3 conditions:

•1)1) |E(x)| is squared-integrable

•2)2) |E(x)| is integrable

•3)3) j(x,t)=0 at infinity (natural boundary conditions)

In S-B onlyonly condition 1)1) is fulfilledfulfilled.

If we apply 2) or 3) then the spectrum is different: there exists a maximal eigenvalue!!!!

2) and 3) should be equivalent.

Since LL11LL22, allora posso avere soddisfatta 2) e non 1)2) e non 1). These are so-called divergent modesdivergent modes.

Se esistono modi divergenti, this methodology can not be applied. In particular, one can not compute the aann coefficients.

The existence of divergent modes strictly depends upon the chosen initial condition.

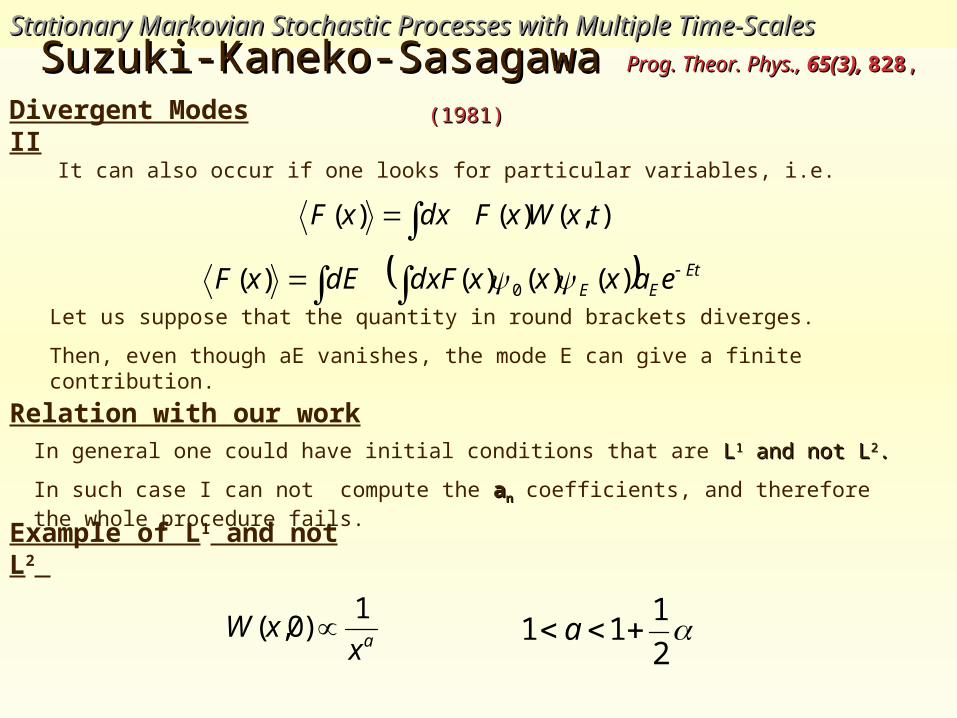

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-ScalesSuzuki-Kaneko-Sasagawa Suzuki-Kaneko-Sasagawa Prog. Theor. Phys., Prog. Theor. Phys., 65(3), 65(3), 828828, ,

(1981)(1981)

Relation with our work

In general one could have initial conditions that are LL11 and not L and not L22..

In such case I can not compute the aann coefficients, and therefore the whole procedure fails.

Divergent Modes II

It can also occur if one looks for particular variables, i.e.

),()()( txWxFdxxF

EtEE eaxxxdxFdExF )()()()( 0

Let us suppose that the quantity in round brackets diverges.

Then, even though aE vanishes, the mode E can give a finite contribution.

Example of L1 and not L2

axxW

1)0,(

2

111 a

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

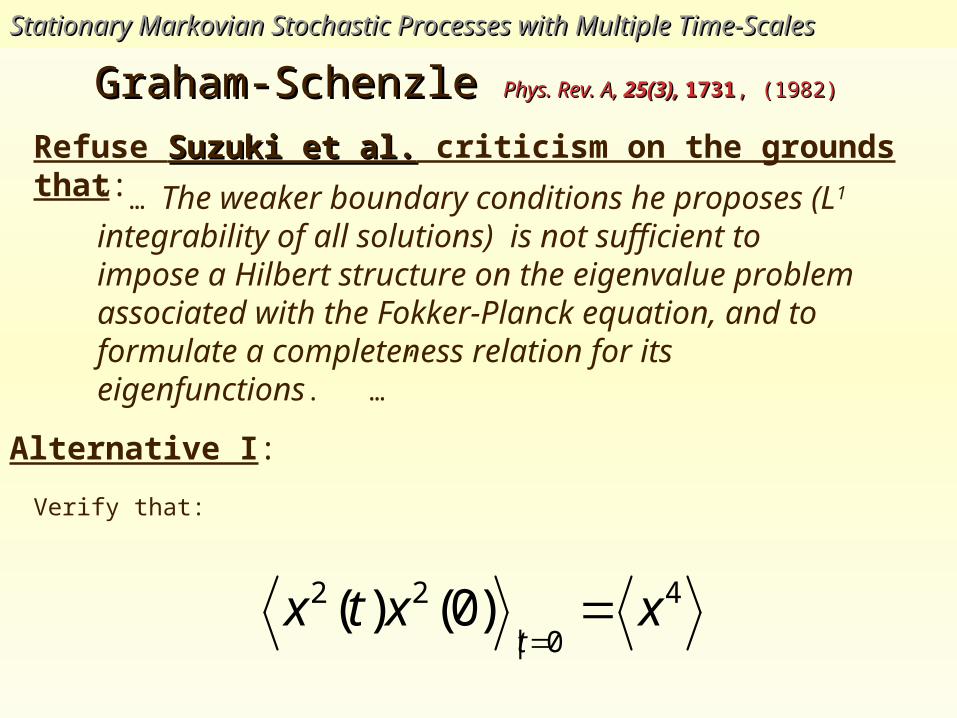

Graham-Schenzle Graham-Schenzle Phys. Rev. A, Phys. Rev. A, 25(3), 25(3), 17311731, (1982), (1982)

“ … The weaker boundary conditions he proposes (L1 integrability of all solutions) is not sufficient to impose a Hilbert structure on the eigenvalue problem associated with the Fokker-Planck equation, and to formulate a completeness relation for its eigenfunctions. …”

Verify that:

4

0|

22 )0()( xxtxt

Refuse Suzuki et al.Suzuki et al. criticism on the grounds that:

Alternative I:

Stationary Markovian Stochastic Processes with Multiple Time-ScalesStationary Markovian Stochastic Processes with Multiple Time-Scales

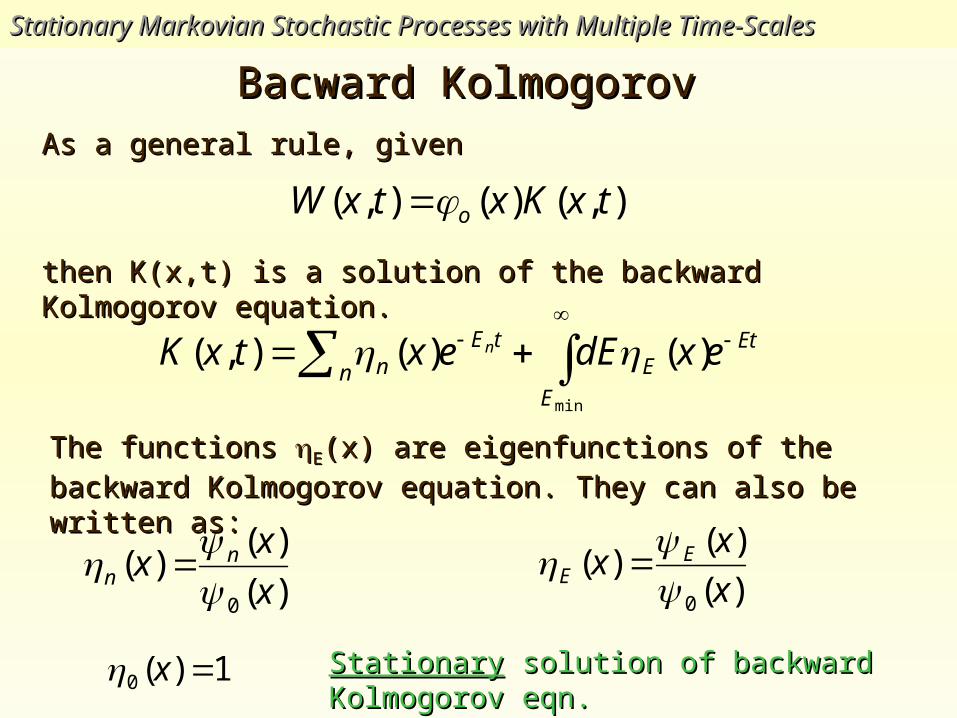

Bacward Kolmogorov Bacward Kolmogorov

),()(),( txKxtxW oAs a general rule, givenAs a general rule, given

)(

)()(

0 x

xx n

n

)(

)()(

0 x

xx E

E

1)(0 x StationaryStationary solution of backward Kolmogorov eqn. solution of backward Kolmogorov eqn.

then K(x,t) is a solution of the backward Kolmogorov equation.then K(x,t) is a solution of the backward Kolmogorov equation.

Et

E

En

tEn exdEextxK n

min

)()(),(

The functions The functions EE(x) are eigenfunctions of the backward Kolmogorov (x) are eigenfunctions of the backward Kolmogorov

equation. They can also be written as:equation. They can also be written as:

![N. Mantegna arXiv:1107.3942v1 [q-fin.TR] 20 Jul 2011 of](https://img.pdfslide.us/doc/110x75/625414675af99c695a7ba41d/n-mantegna-arxiv11073942v1-q-fintr-20-jul-2011-of-.jpg)