Embed Size (px)

Citation preview

1 Reinsurance Market Outlook

Contents

Executive Summary: Risk Transfer Market Responds Well Following Losses 1

Global Reinsurer Capital: Alternative Capital Surge Continues 2

Traditional capital 3

Alternative capital 5

Quiet Start for Catastrophe Losses; Convective Storms Lead the Way 6

2017 Hurricane Losses Continue to Evolve as More Claims are Processed 8

Forecasters: 2018 Atlantic Hurricane Season May Be Quieter 9

Florida Insurance Market Endures Despite Hurricane Irma Losses 11

Florida Hurricane Catastrophe Fund 11

Florida Citizens 12

Contact Information 14

Aon Benfield 1

Executive Summary: Risk Transfer Market Responds Well Following Losses Peak zone Florida risk continues to dominate June and July treaty reinsurance renewals with strong trading also in United States nationwide and Australian property catastrophe risk. Despite catastrophe loss from Hurricane Irma causing nearly USD10 billion in damage in 2017, the risk transfer market continued to show a strong appetite for renewals in each of these regions, even on loss-affected accounts.

First quarter showed significant growth again in alternative market capital with a USD6 billion increase, or 7 percent through first quarter 2018, ending the period at USD95 billion. Overall, total reinsurance capital increased 1 percent, with traditional capital ending the quarter flat compared to year end 2017.

Appetites for mid-year renewals were also assisted by low catastrophe loss activity through the first half of 2018. Insured catastrophe losses sustained have reached just over half of the 10-year average at USD21 billion compared to USD35 billion.

As we approach the peak months of the Atlantic hurricane season, our analysis of the Florida market shows strong claims paying capacity in the Florida Hurricane Catastrophe Fund (FHCF) as a result of a high fund balance and continued risk transfer. Florida Citizens policies in force remain at one of its lowest levels and premium to PHS is its lowest in more than a decade. In addition, Florida-driven insurers are in a much stronger position with capital more than doubled in the last six years.

Of note, the three main hurricane season prognosticators (National Oceanic and Atmospheric Administration (NOAA), Colorado State University (CSU) and Tropical Storm Risk (TSR)) have all forecast either near normal or slightly below normal hurricane activity.

2 Reinsurance Market Outlook

Global Reinsurer Capital: Alternative Capital Surge Continues Aon Benfield estimates that global reinsurer capital stood at USD610 billion at March 31, 2018, an increase of 1 percent relative to the end of 2017. This calculation is a broad measure of the capital available for insurers to trade risk with. Traditional capital was flat at USD515 billion, while alternative capital rose by 7 percent, or USD6 billion, to USD95 billion, now representing 16 percent of the total.

Exhibit 1: Change in global reinsurer capital

Sources: Company financial statements, Aon Benfield Analytics, Aon Securities Inc.

17 22 19 22 24 28 44 50 64 72 81 89 95

385 410340

400

470 455505

540575 565

595 605 610

6%-17% 18%

18%-3% 11%

7%6% -2% 5% 2% 1%

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Q12018

USD

(bill

ions

)

Traditional capital Alternative capital Global reinsurer capital

Aon Benfield 3

Traditional capital Across the 18 Aon Benfield Aggregate (ABA) companies reporting first quarter results, total equity fell by 1 percent to USD190 billion. Solid earnings in the period were out-weighed by the payment of final dividends and the impact of rising interest rates on bond valuations.

Exhibit 2: Change in ABA* total equity

Sources: Company financial statements / Aon Benfield Analytics *Companies included: Alleghany, Arch, Argo, Aspen, AXIS, Everest Re, Fairfax, Hannover Re, Lancashire, MAPFRE, Markel, Munich Re, Partner Re, Ren Re, SCOR, Swiss Re, Validus and XL Catlin.

120 136

112

140 144 147

169 172 181 178 185

191 190

13% -18% 25%

3%2%

15%2% 5% -2% 4% 4% -1%

-

20

40

60

80

100

120

140

160

180

200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Q12018

USD

(bi

llion

s)

4 Reinsurance Market Outlook

The first half of 2018 has been relatively benign in terms of major losses. The average first quarter combined ratio across the 18 reporting ABA companies was 89.8 percent. The ordinary investment yield declined marginally to 2.5 percent, with total returns impacted by unrealized losses on bonds. The annualized return on equity averaged 7.8 percent. Valuations have ticked-up, influenced by the two significant M&A deals involving Validus and XL Catlin.

Exhibit 3: Reinsurance sector performance*

Source: Aon Benfield Analytics *Companies included: Alleghany, Arch, Argo, Aspen, AXIS, Everest Re, Fairfax, Hannover Re, Lancashire, MAPFRE, Markel, Munich Re, Partner Re, Ren Re, SCOR, Swiss Re, Validus and XL Catlin.

0%

1%

2%

3%

4%

5%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q2018

Ordinary investment return

0.6

0.7

0.8

0.9

1.0

1.1

1.2

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q2018

Valuation - price to book

0%2%4%6%8%

10%12%14%

2008 2010 2012 2014 2016 1Q 2018

Return on equity

50%60%70%80%90%

100%110%120%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q2018

Combined ratio

Aon Benfield 5

Alternative capital Most of the capital lost or trapped has since been replaced. Many investors previously enjoyed excellent returns and losses in 2017 generally fell within published risk tolerance ranges. In addition, the prospect of improved returns in the classes and territories most affected has attracted new participants.

Exhibit 4: Alternative capital deployment

Source: Aon Securities Inc. Catastrophe bond issuance from new and repeat sponsors remained at strong levels in the first half of 2018, albeit somewhat down on the record volumes seen last year, as shown in Exhibit 5. In many cases, pricing has been below guidance ranges, resulting in upsizing of the limits ultimately transacted.

Exhibit 5: Property catastrophe bond issuance

Source: Aon Securities Inc.

0102030405060708090

100

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q2018

Lim

it (U

SD b

illio

ns)

Catastrophe bonds Sidecar ILW Collateralized re

500 716 575 300 1,015 1,343520 1,210 1,494 2,215 2,170

3,5803,955

1,794810

2,300 592

2,095 3,303

4,4922,702 800

6,378 4,0291,356

320

411

232674

5291,441

250

650

925

780

2,048

1,600

2,0181,990

1,888

1,8772,075

1,4251,850

1,353

7,859

2,8303,396

4,8504,271

5,855

7,1418,027

6,2715,790

10,681

7,609

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USD

mill

ions

Q1 Q2 Q3 Q4

6 Reinsurance Market Outlook

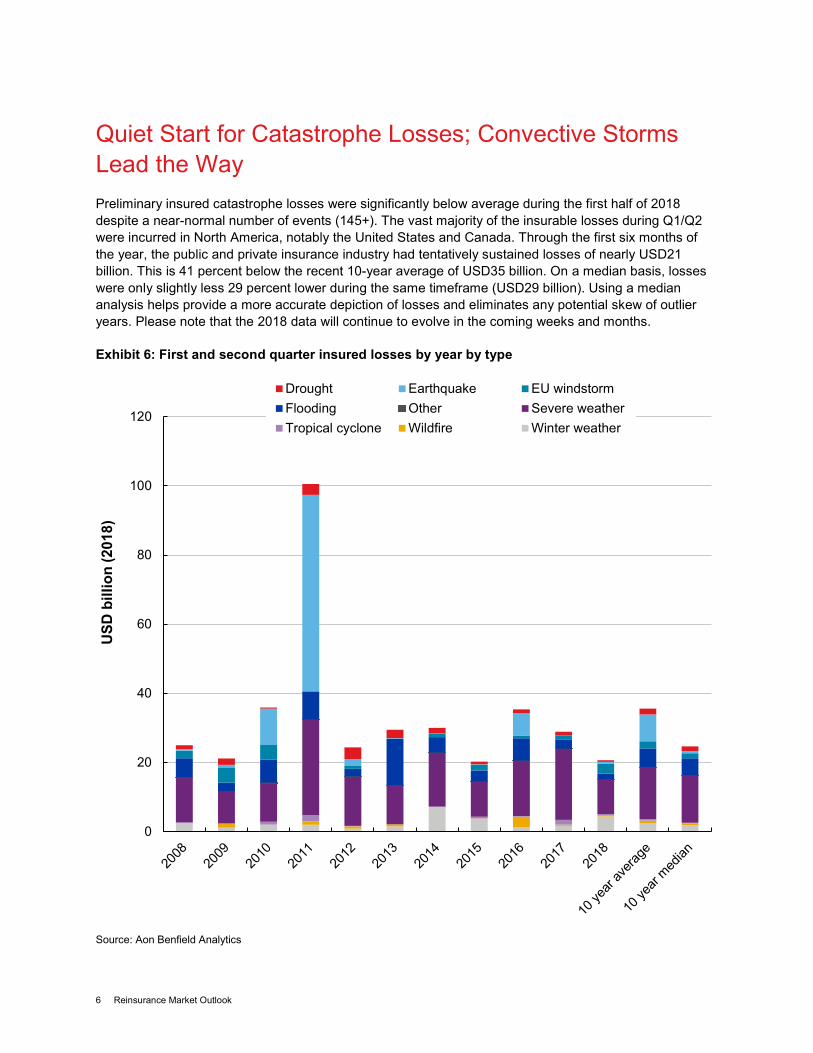

Quiet Start for Catastrophe Losses; Convective Storms Lead the Way Preliminary insured catastrophe losses were significantly below average during the first half of 2018 despite a near-normal number of events (145+). The vast majority of the insurable losses during Q1/Q2 were incurred in North America, notably the United States and Canada. Through the first six months of the year, the public and private insurance industry had tentatively sustained losses of nearly USD21 billion. This is 41 percent below the recent 10-year average of USD35 billion. On a median basis, losses were only slightly less 29 percent lower during the same timeframe (USD29 billion). Using a median analysis helps provide a more accurate depiction of losses and eliminates any potential skew of outlier years. Please note that the 2018 data will continue to evolve in the coming weeks and months.

Exhibit 6: First and second quarter insured losses by year by type

Source: Aon Benfield Analytics

0

20

40

60

80

100

120

USD

bill

ion

(201

8)

Drought Earthquake EU windstormFlooding Other Severe weatherTropical cyclone Wildfire Winter weather

Aon Benfield 7

The first half of the year was highlighted by no fewer than four individual catastrophe events which caused more than USD1.0 billion in insurable losses. Preliminary data showed that three of the four events occurred inside the United States. Two of the three US events resulted from severe convective storms (losses driven by tornadoes, hail or straight-line winds) and the other was a powerful early March winter storm and subsequent cold snap. The combined cost of the three billion-dollar US insured events is tentatively estimated at USD3.75 billion. The other event that cost insurers at least USD1.0 billion was Windstorm Friederike, which swept through Europe in January. At USD1.9 billion, it was the costliest insured event in Q1/Q2 and the costliest European Windstorm since Xynthia in 2010 (USD4.2 billion).

Slightly less than two-thirds insured losses (61 percent) were sustained in the United States; or approximately USD12.6 billion. Most of the losses were attributed to the severe convective storm peril as several major hailstorm events pelted densely populated areas across the Rockies, Plains, and Midwest. A major early March winter storm led to considerable damage throughout the Eastern US. No fewer than seven events in the United States caused at least USD500 million in insurable losses; all of which were SCS or winter storm-related. The two non-US events passing the half-billion threshold were both European windstorms: Windstorm Friederike and a one-two combination of windstorms Eleanor and Carmen.

Beyond the US, the highest percentage of insured losses occurred in EMEA (26 percent), Americas (6 percent), and APAC (6 percent).

Exhibit 7: 2018 year-to-date insured losses compared to recent annual averages by region

Source: Aon Benfield Analytics

As previously noted, the largest portion of the USD21 billion in global insured losses was attributed to the severe convective storm peril. The more than USD10 billion in losses accounted for nearly 50 percent of the overall Q1/Q2 total. The two other perils that accounted for more than 10 percent of the first-half total included winter weather (21 percent) and European windstorm (14 percent). The only additional peril above five percent was flooding (8 percent).

Should current trends from the first half of the year continue, 2018 is on pace to be below normal for the entire year. As always, it is imperative to remind that it only takes one catastrophic natural disaster event to entirely change the trajectory of a year for the insurance industry. The peak months for catastrophe losses are often found in July, August and September – which nearly coincides with the most active months for Atlantic hurricanes. This was especially true in 2017. For the most up-to-date global catastrophe loss data for 2017, and other historical loss information, please visit Aon Benfield’s Catastrophe Insight website: www.aonbenfield.com/catastropheinsight

22.4

1.03.1 2.4

12.6

1.2

5.6

1.2

19.0

2.24.7

9.2

18.0

0.8

4.92.9

0

5

10

15

20

25

United States Americas EMEA APAC

USD

biil

lion

(201

8)

2017 2018 10 year average 10 year median

8 Reinsurance Market Outlook

2017 Hurricane Losses Continue to Evolve as More Claims are Processed It has now been 10 calendar months since the end of a very busy period in the Atlantic Ocean that saw Hurricanes Harvey, Irma, and Maria make landfall across the mainland United States and the Caribbean Islands in a matter of weeks. In the months that followed, various insured loss estimates released by catastrophe model vendors, insurance industry groups, and other private sector companies to quantify the cost of the storms for the re/insurance industry. As time has progressed, more and more claims have continued to be filed and/or settled by public and private insurers which has allowed a more accurate depiction of the cost of these events to develop. However, using historical major hurricane events as a guide, the evolution of claims data is expected to potentially take years until fully settling.

A real-time example of this loss evolution is Hurricane Irma in Florida. Based on data from the Florida Office of Insurance Regulation (OIR), the value of claims payouts as of June 2018 had risen to nearly USD10 billion. This was a more than 10 percent increase in payouts since the last update in April 2018. As seen in the graphic below, there has been a steady incremental increase in the volume of claims payouts since September 2017. The OIR states that 91 percent of filed claims are now closed, including 92 percent of residential claims, though 31 percent of commercial claims remain open. These payouts are often some of the larger ones to occur, which would partially explain the robust bump from April to June.

Exhibit 8: Hurricane Irma private insurance payments in the state of Florida

Data Source: Florida Office of Insurance Regulation; Graphic: Aon Benfield Analytics

The payouts from the OIR include data from nearly all private insurers in the state of Florida. Updated aggregate data releases are expected again on July 27 and September 14.

In the case of Hurricane Maria, uncertainty remains given the continuation of business interruption losses across several sections of the island. The vast majority of claims payouts in Puerto Rico were tied to the commercial side and insurers remain vigilant in trying to expedite the claims process.

The prolonged settling of the claims process for major catastrophe events is not only directly tied to the private market. This is also a common occurrence for public or government-run insurance programs, such as the National Flood Insurance Program (NFIP) in the United States.

2.0 3.1 3.9 4.66.3 6.6 7.2 8.0 8.6 9.7

0

2

4

6

8

10

12

USD

bill

ion

(201

8)

Aon Benfield 9

In the case of Hurricanes Katrina, Ike, Sandy and others, a monthly review of NFIP paid claims and the amount of paid claims shows that even several years after an event occurrence, there are still claims being processed. There are various reasons for these delays, including replacement costs, appraisals, and judicial processes surrounding policy coverages, that can cause challenges in finalizing event payments.

This is additionally expected with Hurricane Harvey. Data from the NFIP as of February 2018 indicated that nearly USD8.7 billion in NFIP payouts had been made in relation to Harvey, with the majority of payments coming from the greater Houston, Texas metropolitan region. More than 75,000 claims have been paid, with an average payout listed at USD114,638. On a nominal basis, this makes Harvey costliest event on record on a “payment-per-claim” basis – even more than the USD97,475 for Katrina and USD65,997 for Sandy prior to an adjustment to today’s dollars.

Exhibit 9: Costliest NFIP events (inflation adjusted)

Data as of February 28, 2018 2018 USD inflation-adjustment using US Consumer Pricing Index Source: FEMA and Aon Benfield Analytics

The final NFIP total for Harvey is anticipated to be much higher than the current total. The Federal Emergency Management Agency (FEMA) extended the deadline for submitting a Proof of Loss claim from the standard 60-day window to a full year (365 days). This alone will ensure that it will be more than a calendar year after Harvey’s landfall until a more robust/final insurance view of resultant claims payments due to flood-related damage can begin.

Forecasters: 2018 Atlantic Hurricane Season May Be Quieter The three main hurricane season prognosticators (National Oceanic and Atmospheric Administration (NOAA), Colorado State University (CSU) and Tropical Storm Risk (TSR)) have all forecast either near normal or slightly below normal hurricane activity for the Atlantic Hurricane Season. Each agency cites uncertainty surrounding a possible transition from current ENSO-neutral conditions to El Niño conditions in the Central and Eastern Pacific Ocean once entering the peak development months of August, September, and October. Should an El Niño occur, this could lead to less conducive atmospheric and oceanic conditions in the main development region of the Atlantic Ocean for cyclogenesis.

20.3

9.2 8.7

3.0 2.5 2.1 1.5 1.5 1.0 0.90

5

10

15

20

25

HurricaneKatrina

HurricaneSandy

HurricaneHarvey

HurricaneIke

LouisianaFlood

(August2016)

HurricaneIvan

TropicalStormAllison

HurricaneIrene

HurricaneIrma

LouisianaFlood

(May 1995)

USD

bill

ion

10 Reinsurance Market Outlook

However, beyond any prospective arrival of El Niño, sea surface temperatures across the tropical Atlantic Ocean have been significantly cooler than normal in recent months. Deterrent mid and upper-level winds in the form of wind shear throughout the Atlantic and Caribbean Sea are also currently at elevated levels which may make conditions less conducive for tropical development.

As always, it only takes one landfalling storm to entirely alter the perception of a season from a financial loss perspective – regardless of how meteorologically active or inactive a year may be.

Exhibit 10: Hurricane Forecasts for 2018 Season

Named storms Hurricanes Major hurricanes TSR (May 2018) 1950-2017 Average 11 6 3 2018 9 4 1 CSU (June 2018) 1981-2010 Median 12.0 6.5 2.0 2018 14 6 2 NOAA (May 2018) 1981-2010 Average 12 6 3 2018 10-16 5-9 1-4

Sources: Tropical Storm Risk (TSR), Colorado State University (CSU), NOAA

Aon Benfield 11

Florida Insurance Market Endures Despite Hurricane Irma Losses Despite Hurricane Irma losses of nearly USD10 billion in 2017, Florida remains in one of its strongest positions heading into the 2018 hurricane season. Both the private market and FHCF / Florida Citizens have increased capital and continued to transfer risk to the reinsurance market.

Florida Hurricane Catastrophe Fund With an estimated USD2 billion in losses that led to a slight reduction in the fund balance, the FHCF remains well positioned to cover claims paying requirements for the 2018/2019 season at nearly the highest level of fund balance since its inception. Funds totaling the statutory limit for this season of USD17.0 billion are comprised of USD14.1 billion projected fund balance, USD1.0 billion in risk transfer and USD1.9 billion of the USD2.2 billion in existing pre-event liquidity.

Exhibit 11: Total claims paying capacity

Source: Florida Hurricane Catastrophe Fund website In addition to the funds available for the 2018 season, approximately USD8.2 billion is estimated to be available as post-event borrowing capacity for a subsequent season according to Raymond James summary from May 2018.

-

5

10

15

20

25

30

Projected fund balance Pre-event debt

Risk transfer Estimated borrowing capacity needed

12 Reinsurance Market Outlook

Florida Citizens As of April 2018, policies in force remain at a fifteen-year low of 440,000, only 30 percent of the peak position held in 2011. Throughout the last 6 years alone, nearly 1.5 million policies have been depopulated from Florida Citizens and despite significantly less policies in the portfolio, assumed policies in 2017 still reached 34,000, or 7.5 as a percent of the prior year policy count.

Exhibit 12: Historical policy count, TIV and depopulations

Source: Florida Citizens Website While Florida Citizens paid approximately USD1.8 billion in Hurricane Irma losses, Premium to PHS remains significantly better balanced than in prior years at a 0.14 to 1 ratio.

Exhibit 13: Historical premium to PHS

Source: Florida Citizens Website Citizens also secured risk transfer for the 2018 season with a total of USD1.42 billion transferred through both traditional reinsurance (of which USD660 million remains in place from prior years) and catastrophe bonds of USD300 million.

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

0%5%

10%15%20%25%30%35%40%45%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Assumed policies as % of PY Assumed TIV as a % of PY Policy Count TIV

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Premiums PHS

Aon Benfield 13

Private Market More than 75 percent of Citizens market share has been returned to the private market for homeowners in Florida since 2011. While we have seen a meaningful drop in participation by top nationwide insurers, the Florida driven companies, like those with more than 80 percent of premium in Florida homeowner residential premiums, have increased market share from nearly 36 percent in 2011 to 47 percent in 2017. What’s key here is while that group increased market share by nearly 50 percent in the period, it increased PHS by over 150 percent, significantly improving the financial position of the private market in Florida exposure to catastrophes. In addition, other insurers (typically more diversified larger insurers) now make up nearly 40 percent of the market share, up from 30 percent.

Exhibit 14: Florida residential market share change

Source: S&P

2011 2017

14 Reinsurance Market Outlook

Contact Information Tracy Hatlestad Global Chief Operating Officer of Analytics Aon Benfield +65 6512 0244 [email protected] Greg Heerde Head of Analytics & Inpoint, Americas Aon Benfield +1 312 381 5364 [email protected] Kelly Superczynski Head of Analytics, EMEA Aon Benfield +44 0(20) 7086 2175 [email protected]

Peter Cheesman Head of Analytics, APAC Aon Benfield +61 2 9650 0462 [email protected] Mike Van Slooten Head of Market Analysis, International Aon Benfield +44 0(20) 7522 8106 [email protected] Marie Teissier Market Analysis, International Aon Benfield +44 0(20) 7522 3951 [email protected]

Aon Benfield 1

© Aon Benfield 2018. | All rights reserved. This document is is provided for the purpose of providing general information and intended for general information purposes only and should not be construed as advice or opinions on any specific facts or circumstances. The comments in this summary are based upon Aon Benfield’s preliminary analysis of publicly available information as well as aggregated insight collected by Aon Benfield. The content of this document is made available on an “as is” basis, without warranty of any kind. Aon Benfield disclaims any legal liability to any person or organization for loss or damage caused by or resulting from any reliance placed on that content. Aon Benfield reserves all rights to the content of this document. This document is not intended to serve as legal accounting or actuarial advice or guidance. © Aon Securities Inc. 2018 | All Rights Reserved Aon Securities Inc. is providing this document and all of its contents (collectively, the “Document”) for general informational and discussion purposes only, and this Document does not create any obligations on the part of Aon Securities Inc., Aon Securities Limited or their affiliated companies (collectively, “Aon”). This Document is intended only for the designated recipient to whom it was originally delivered and any other recipient to whose delivery Aon consents (each, a “Recipient”). This Document is not intended and should not be construed as advice, opinions or statements with respect to any specific facts, situations or circumstances, and Recipients should not take any actions or refrain from taking any actions, make any decisions (including any business or investment decisions), or place any reliance on this Document (including without limitation on any forward-looking statements). This Document is provided for the purpose of providing general information and is not intended, nor shall it be construed as (1) an offer to sell or a solicitation of an offer to buy reinsurance, (2) an offer, solicitation, confirmation or any other basis to engage or effect in any transaction or contract (in respect of reinsurance, a security, financial product or otherwise), or (3) a statement of fact, advice or opinion by Aon or its directors, officers, employees, and representatives (collectively, the “Representatives”). Any projections or forward-looking statements contained or referred to in this Document are subject to various assumptions, conditions, risks and uncertainties (which may be known or unknown and which are inherently unpredictable) and any change to such items may have a material impact on the information set forth in this Document. Actual results may differ substantially from those indicated or assumed in this Document. No representation, warranty or guarantee is made that any transaction can be effected at the values provided or assumed in this Document (or any values similar thereto) or that any transaction would result in the structures or outcomes provided or assumed in this Document (or any structures or outcomes

2 Reinsurance Market Outlook

similar thereto). Aon makes no representation or warranty, whether express or implied, that the products or services described in this Document are suitable or appropriate for any cedent, sponsor, issuer, investor, counterparty or participant, or in any location or jurisdiction. The information in this document is based on or compiled from sources that are believed to be reliable, but Aon has made no attempts to verify or investigate any such information or sources. Aon undertakes no obligation to review, update or revise this Document based on changes, new developments or otherwise, nor any obligation to correct any errors or inaccuracies in this Document. This Document is made available on an “as is” basis, and Aon makes no representation or warranty of any kind (whether express or implied), including without limitation in respect of the accuracy, completeness, timeliness, or sufficiency of the Document. Aon does not provide and this Document does not constitute any form of legal, accounting, taxation, regulatory, or actuarial advice. Recipients should consult their own professional advisors to undertake an independent review of any legal, accounting, taxation, regulatory, or actuarial implications of acribed in or related to this Document. Aon and its Representatives may have independent business relationships with, and may have been or in the future will be compensated for services provided to, companies mentioned in this Document.