Embed Size (px)

Citation preview

Reducing Undeclared Work in Hungary- the role of Tax policy

and administration

byWilli Leibfritz

Undeclared work in HungaryWhat is the problem and how big is it?What are the reasons? High taxes or ineffective

enforcement or both?• Tax level and tax mix• Labour tax burden and labour market outcomes• Measuring cost-efficiency and effectiveness of tax

administration Policies to reduce undeclared work: a „carrot and

stick“ approach

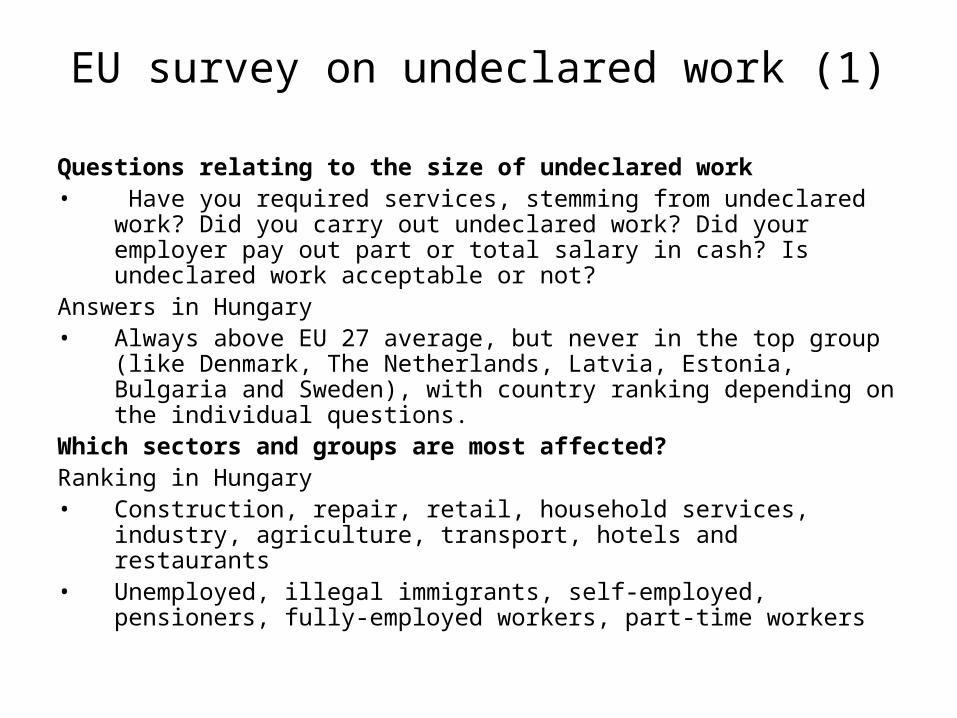

EU survey on undeclared work (1)

Questions relating to the size of undeclared work• Have you required services, stemming from undeclared work? Did you

carry out undeclared work? Did your employer pay out part or total salary in cash? Is undeclared work acceptable or not?

Answers in Hungary• Always above EU 27 average, but never in the top group (like Denmark,

The Netherlands, Latvia, Estonia, Bulgaria and Sweden), with country ranking depending on the individual questions.

Which sectors and groups are most affected?Ranking in Hungary• Construction, repair, retail, household services, industry, agriculture,

transport, hotels and restaurants • Unemployed, illegal immigrants, self-employed, pensioners, fully-

employed workers, part-time workers

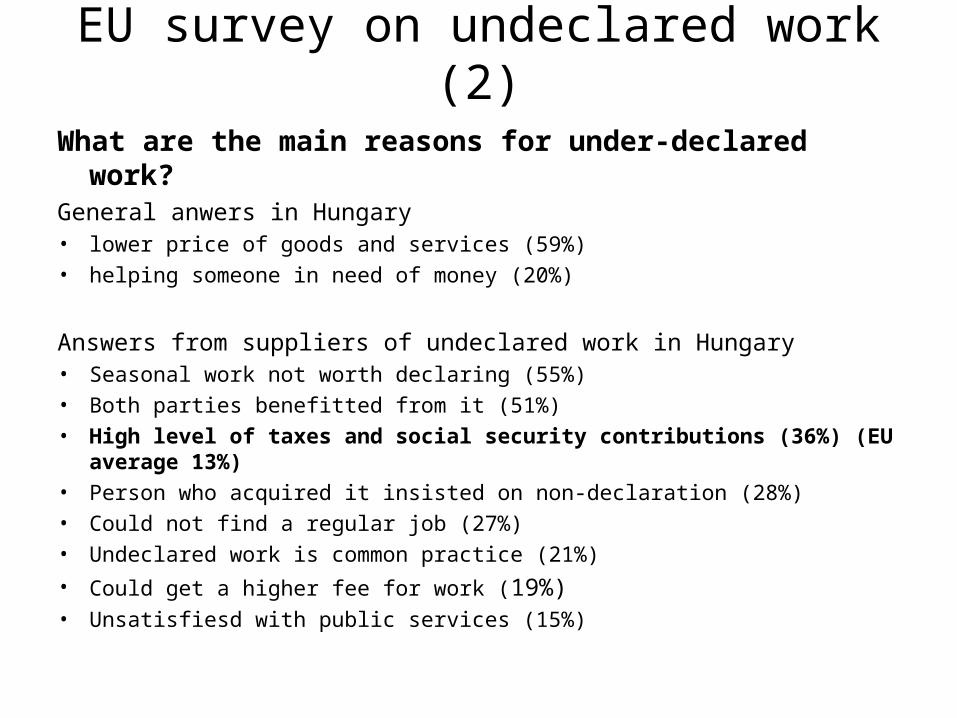

EU survey on undeclared work (2)

What are the main reasons for under-declared work?General anwers in Hungary• lower price of goods and services (59%)• helping someone in need of money (20%)

Answers from suppliers of undeclared work in Hungary• Seasonal work not worth declaring (55%)• Both parties benefitted from it (51%)• High level of taxes and social security contributions (36%) (EU average 13%)• Person who acquired it insisted on non-declaration (28%)• Could not find a regular job (27%)• Undeclared work is common practice (21%)• Could get a higher fee for work (19%)• Unsatisfiesd with public services (15%)

Size of informal economy and fiscal costs• EUROSTAT (2000) 12% (Poland and Slovakia 15%, Czech

Republic 7%)

• Estimates by others (Lacko, Todt, Semjén): 17-18% in 2006, down from one third in 1993

• World Bank/EBRD survey: Hungarian firms did, on average, not declare 10-15% of their sales,

10-15% of firms bribed tax collectors (somewhat lower than in Poland and Slovakia but higher than in Czech Republic, Slovenia, Estonia, Latvia, Lithuania)

• 30% revenue gap in social security contributions

• Effective VAT rate is only 46% of standard rate

Assessing the tax system

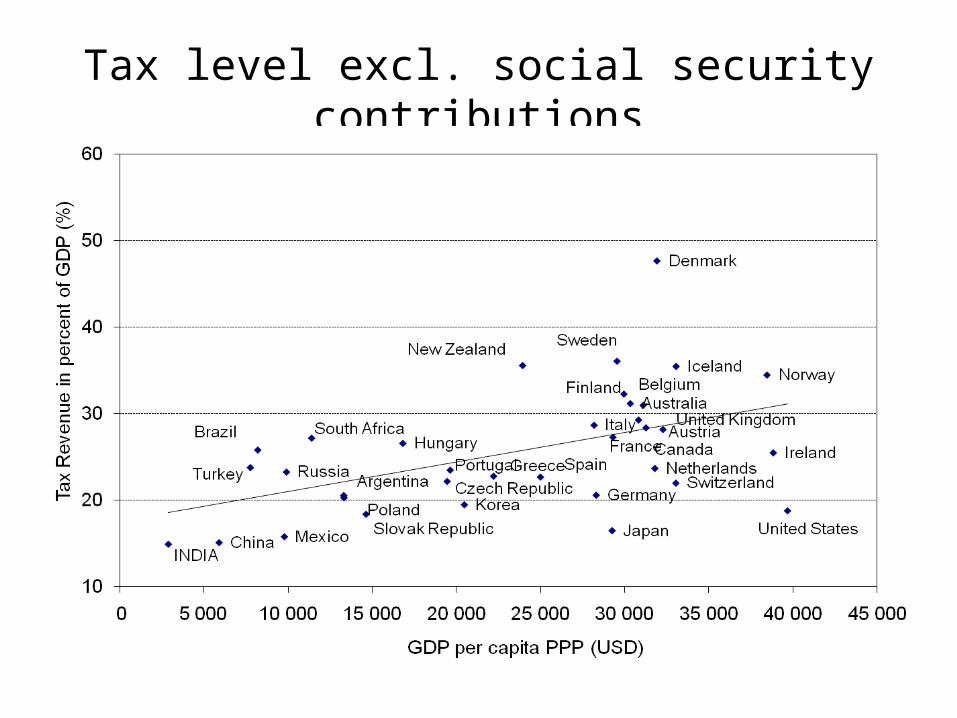

• The overall tax level, as measured by tax revenues as % of GDP, is relatively high, despite pervasive tax evasion

• The tax mix is dominated by taxes on labour and consumption while capital taxation is relatively low

• The implicit tax rates on labour and consumption are well above EU average (tax revenues as % of theoretical tax base from National Accounts)

Tax level in international comparisonTax revenues incl. social security contributions as % of GDP

Tax level excl. social security contributions

Taxes on labour as % of GDP

Averages 1995-2004

0

5

10

15

20

25

30

35

SE DK BE FI AT DE FR SI EU-25

HU NL IT EE CZ LU ES PL LV SK LT PT UK EL IE CY MT

% G

DP

Employed paid by employers Employed paid by employees Non-employed

Taxes on consumption as % of GDPAverages 1995-2004

0

2

4

6

8

10

12

14

16

DK HU SI FI EL SE AT EE PL UK IE LT FR PT SK LV LU EU-25

NL BE CY MT CZ IT DE ES

% G

DP

Taxes on capital as % of GDP

Averages 1995-2004

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

LU IT UK BE EL FR NL CY ES EU-25

PT MT IE FI PL AT CZ DK SE DE SK HU LV SI EE LT

% G

DP

Income of corporations Income of households Income of self-employed Stock (wealth) of capital

Average implicit tax rates on consumption and labour in Hungary and the EU-27

36

37

38

39

40

41

42

43

44

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

19.0

20.5

22.0

23.5

25.0

26.5

28.0

29.5

31.0

Labour income, HU (left axis) Labour income, EU27 (left axis)

Consumption, HU (right axis) Consumption, EU27 (right axis)

Labour tax burden

• Average and marginal labour tax wedges are high in international comparison and in absolute terms

• The withdrawal of income dependent benefits increases the marginal effective tax rate (METR) further and increases incentives to under-declare wages and to work in the informal sector

Average labour tax wedge

0,0 10,0 20,0 30,0 40,0 50,0 60,0

Belgium

Germany

Hungary

France

Austria

Sweden

Italy

Netherlands

Finland

Poland

Turkey

Czech Republic

Denmark

Greece

Spain

Slovak Republic

OECD average

Norway

Luxembourg

Portugal

United Kingdom

Canada

Switzerland

United States

Japan

Iceland

Australia

Ireland

New Zealand

Korea

Mexico

Income tax

Employee SSC

Employer SSC

.

Marginal effective tax rates incl. withdrawal of income dependent benefits

0

20

40

60

80

100

120

Mar

gina

l eff

ecti

ve ta

x ra

te (

%)

0

10000

20000

30000

40000

No.

of

hous

ehol

ds

0 1000000 2000000 3000000Gross wage

No. of households Marginal effective tax rate (%)

Marginal effective tax rate incl. all payroll taxes

-4.000.000

-3.000.000

-2.000.000

-1.000.000

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

7.000.000

30 40 50 60 70 80 90 100

110

120

130

140

150

160

170

180

190

200

210

220

% of AW

nat

ion

al c

urr

ency

per

yea

r

-25%

0%

25%

50%

75%

100%

125%

mar

gin

al/a

vera

ge

rate

s

income tax central income tax local employee SSCemployer SSC payroll taxes gross earningsfamily benefits net earnings total labour costnet personal marginal tax rate marginal tax wedge net personal average tax rateaverage tax wedge average income tax rate

Elements of the tax system which also create incentives for tax evasion

• The large gap between tax rates on labour and profits contributes to under-declaring wages

• Self-policing nature of VAT should, in principle, help to combat evasion. It is also a means of taxing (indirectly) those who escape direct taxation

• Simplified tax treatment, such as EVA, has positive and negative effects on evasion, with the net effect being (probably) negative

Net income as % of total wage costs

Annual income (HUF) 2 Mio 4 Mio 10 Mio EVA 64.5 76.7 83.9

EKHO 61.7 65.8 60.8

Dependent employment 46.9 40.8 38.9

Effects of taxes on the labour market and undeclared work • The effect of labour taxes on wage costs and employment

depend on the flexibility of wages

• Minimum wage sets a floor to the gross wage so that employer contributions have to be born by firms and raise wage costs

• The combination of high labour taxes and high minimum wages reduces job opportunities for lower-skilled workers in the formal sector and creates incentives to under-declare earnings

• The higher the minimum wage, the bigger the incentive to just declare the minimum wage

Labour tax wedge and employment in international comparison

Aggregate tax wedge at the country level

Source : Bassanini and Duval (2006); OECD Economic Outlook No 81, OECD Taxing Wages database.

Aus

Aut

Bel

Can

Cze

Deu

Dnk

Esp

Fin

Fra

Gbr

Grc

Hun

Irl

IslIta

Jpn

Lux

Nld Nor

Pol

Prt

Svk

Swe

Usa

1200

1300

1400

1500

1600

1700

1800

1900

2000

2100

0 .3 0.4 0 .5 0 .6 0 .7

Annual hours worked per person in employment

(Taxes and social contributions + indirect taxes) / GDP

Tax policies to reduce undeclared work (1)Designing a strategy

How to overcome the dilemma of the need to reduce

labour taxes without putting fiscal consolidation at risk?

„Carrot and stick“ approach: Reduce labour taxes, increase some other taxes and strengthen enforcement

Set a revenue target and promise that any additional revenue from improved enforcement will be used for tax cuts in the next year

Tax policies to reduce undeclared work (2)

Changing the tax mix

• reduce employer contributions to social

security• increase dividend tax• raise VAT• introduce real estate tax

Tax policies to reduce undeclared work (3)

• Simplifying the tax system (reduce loopholes and exemptions, eliminate minor taxes)

Tax policies to reduce undeclared work (4)

• Targeting specific sectors (retail sector, construction etc.)

Social and labour market policies to reduce undeclared work

• Strengthen the link between social security contributions and benefits

• Reduce undeclared work of unemployment benefit recipients

- by better monitoring - by allowing them to work officially within limits

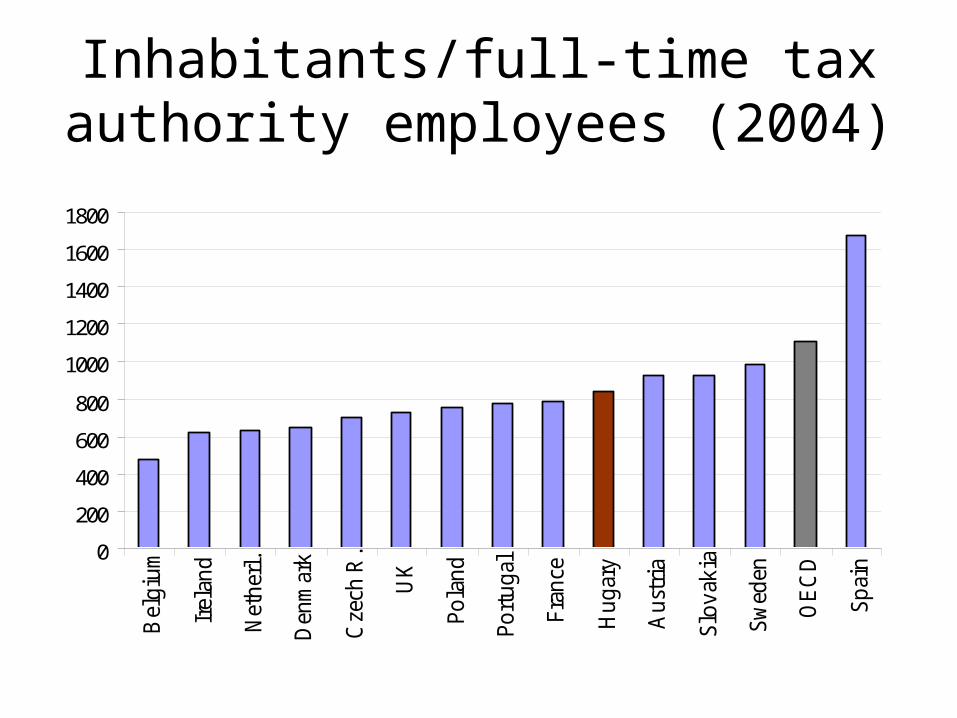

Some (tentative) considerations about improving tax collection (1)

Are tax authorities under-staffed?

Tax authority administration costs/net revenue (2004) %

0

0.5

1

1.5

2

2.5

Swed

en

Aus

tria

Den

mar

k

Spai

n

Irel

and

Bel

gium

OE

CD

Hug

ary

UK

Pola

nd

Fran

ce

Slov

akia

Port

ugal

Net

herl

.

Cze

ch R

.

Inhabitants/full-time tax authority employees (2004)

0

200

400

600

800

1000

1200

1400

1600

1800

Bel

giu

m

Irel

and

Net

her

l.

Den

mar

k

Cze

ch R

.

UK

Po

lan

d

Po

rtu

gal

Fra

nce

Hu

gar

y

Au

stri

a

Slo

vak

ia

Sw

eden

OE

CD

Sp

ain

Some (tentative) considerations about improving tax collection

• Should the various institutions (APEH, Customs and Finance Guard HCFG, local tax administrations) be merged into one agency?

• Should tax authorities be more independent (e.g. from political influences, setting performance-based pay to boosting motivation of staff)?

• Is the organisational structure of APEH by functions (registration, accounting, information processing, audit, collection) too rigid and should it be supplemented by a taxpayer- type organisation (large business, SMEs, self-employed, employees etc.)?

• How could auditing be improved? (Joint auditing of all taxes, Risk analysis)

The End