Embed Size (px)

Citation preview

Real EstateReal Estate Principles and Practices Principles and Practices

Chapter 11Chapter 11

FinancingFinancing

© 2014 OnCourse Learning

© 2014 OnCourse Learning

Key TermsKey Terms

Adjustable rate mortgage

Amortization

Balloon payment

Blanket mortgage

Deed of trust

Discount points

Equity

Escrow agreement

Estoppel certificate

Foreclosure

General liens

Hypothecation

Interest

Involuntary lien

Lien

Lien theory

Moratorium

© 2014 OnCourse Learning

Key TermsKey Terms

Mortgage

Mortgagee

Mortgagor

Open-end mortgage

PITI

Short-sale

Specific liens

Straight loan

Tax lien

Title theory

Voluntary lien

© 2014 OnCourse Learning

OverviewOverview

Interest rates

Clauses found in notes & mortgages

Foreclosure procedures

General & specific liens

© 2014 OnCourse Learning

Interest RatesInterest Rates

Interest: rent for the use of money

Factors:Risk

Business outlook

Alternative

investments

Future inflation

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

AKA: Straight loanStraight loan

Interest only

Amount borrowed paid on final due date

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

Equal payments include principal and interest

Reduce unpaid balance

Amortization: Amortization: liquidation of financial obligation

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

Periodic payments with a remaining balance due at end of term

Balloon payment: Balloon payment: used to shorten term of loan

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

Interest only: principal is not reduced

“Option Arm”Interest only OROR

15, 20, or 30 year amortized payment

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

1/12th taxes and insurance added to PITI

EquityEquity Difference between value and

loan amount

UsuryUsury Interest in excess of the amountInterest in excess of the amount

allowed – illegalallowed – illegal

MoratoriumMoratorium

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

Increase the lenders yield

1 point equals 1% of loan amount1 point equals 1% of loan amount

General Rule: 1 point lowers the rate 1/8th of 1%

Origination fee: charged by lender for originating and processing the loan

1% of loan amount

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

Ratio of loan amount to sales price

The greater the LTV the greater the risk

Value is sales price or appraised value whichever is lower

© 2014 OnCourse Learning

Mortgage Payment MethodsMortgage Payment Methods

Backed by a mortgage

Note details the terms

Prepayment penalty

© 2014 OnCourse Learning

The MortgageThe Mortgage

Mortgage: Mortgage: pledges the property as collateral for the debt

Hypothecation: Hypothecation: pledge property without giving up possession

Mortgagee: Mortgagee: lender

Mortgagor: Mortgagor: borrower

Negotiable instrument: Negotiable instrument: can be bought or sold

© 2014 OnCourse Learning

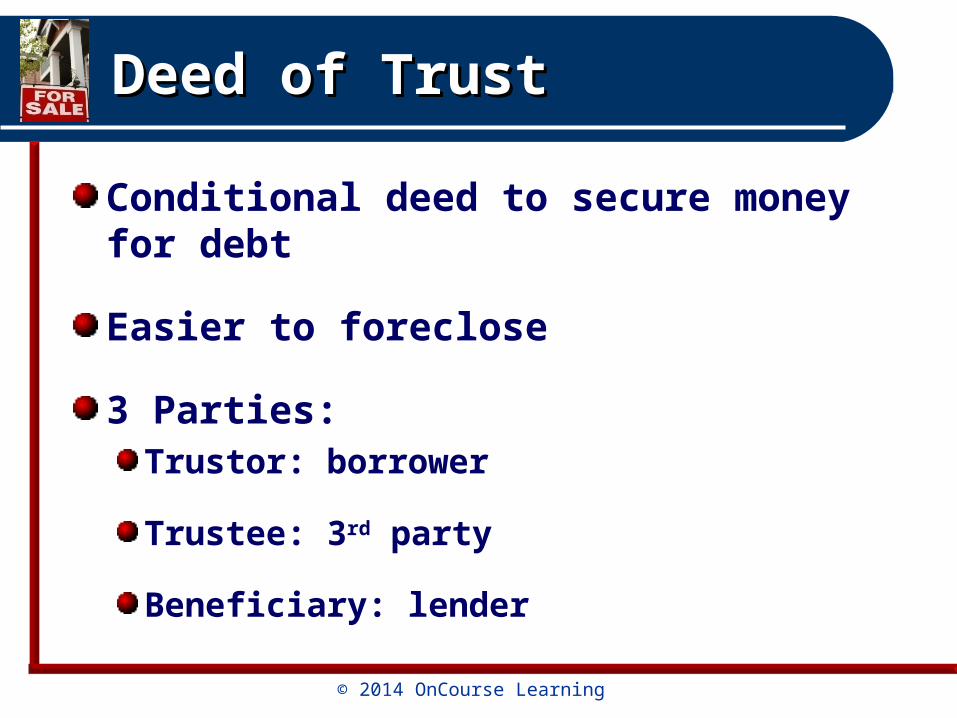

Deed of TrustDeed of Trust

Conditional deed to secure money for debt

Easier to foreclose

3 Parties:Trustor: borrower

Trustee: 3rd party

Beneficiary: lender

© 2014 OnCourse Learning

Other Mortgage Clauses and Other Mortgage Clauses and ConditionsConditions

Mortgage lien is second second in priorityin priority

Interest rate is usually higher due to higher risk

© 2014 OnCourse Learning

Other Mortgage Clauses and Other Mortgage Clauses and ConditionsConditions

Penalty if loan is paid off early

Not allowed on FHA and VA loans

© 2014 OnCourse Learning

Other Mortgage Clauses and Other Mortgage Clauses and ConditionsConditions

Buyer is obligated to pay the loan

Original owner secondarily liable

Release of liability

“Subject to existing loan”

FHA and VA loans

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

Require a larger down payment than FHA and VA

Lenders want a higher LTV

Lending no more than 80% of value

Requires PMI

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

Mortgagor may extend the amount of the loan

Terms may change

Common use: construction loans

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

Includes both real and personal property

Common uses:New homes

Farm and tractor

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

Single mortgage that covers more than one piece of property

Often used by developers

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

Seller financing: seller takes back a note

1st or 2nd lien

Investment for seller who does not need the equity

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

Pledges owner’s equity as collateral

Second priority

Greater risk – higher rate

Specified period Demand full payment at

end of period

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

For specified periods of time and demand full payment at the end of those periods

Often used by builders

© 2014 OnCourse Learning

Types of MortgagesTypes of Mortgages

2 or more mortgages consolidated into 1 payment

Lender wraps new loan around an existing assumable loan

Existing loan may not have a due-on-sale clause

© 2014 OnCourse Learning

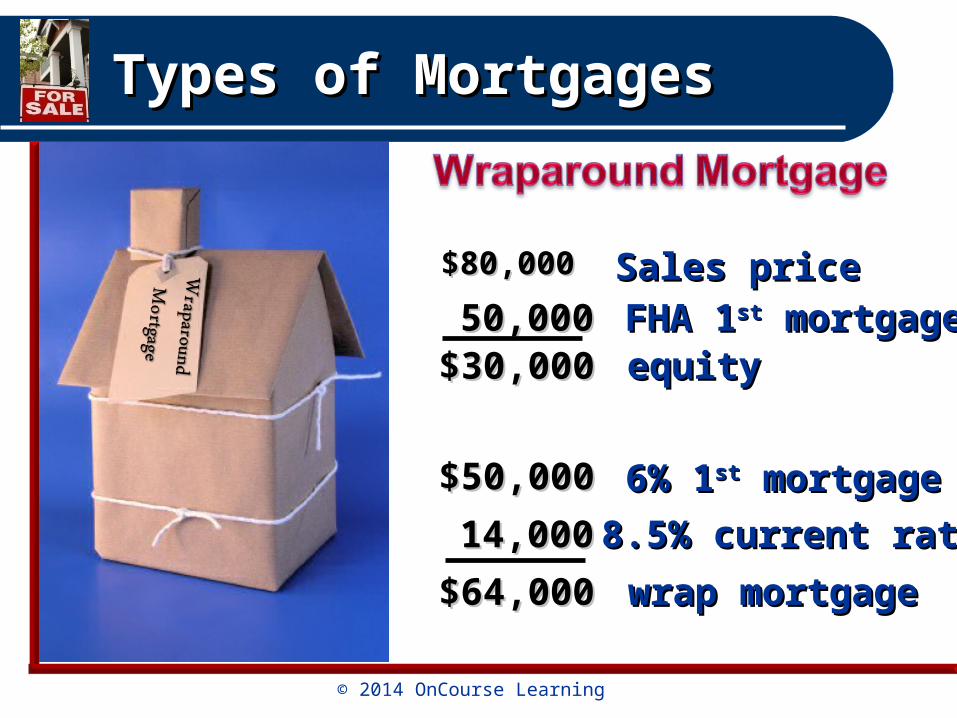

Types of MortgagesTypes of Mortgages

$80,000$80,000

50,00050,000$30,000$30,000

Sales priceSales price

FHA 1FHA 1stst mortgage mortgageequityequity

$50,000$50,000

14,00014,000

$64,000$64,000

6% 16% 1stst mortgage mortgage

8.5% current rate8.5% current rate

wrap mortgagewrap mortgage

© 2014 OnCourse Learning

Alternate Mortgage PlansAlternate Mortgage Plans

Allows a change in the rate up or down

Index: cost of funds (one-year T-bill)

Margin: 2 – 3%, allows for reasonable profit

Adjustment period: time rates can change

Adjustable Rate Mortgages (ARMs)Adjustable Rate Mortgages (ARMs)

Cap rates Periodic Aggregate

© 2014 OnCourse Learning

Alternate Mortgage PlansAlternate Mortgage Plans

For homeowners 62 years or older

Converts the equity in their homes into cash

Owner may receive lump sum, monthly payments, or a line of credit

Loan is repaid upon sale or death

Reverse Annuity Mortgages (RAMs)Reverse Annuity Mortgages (RAMs)

© 2014 OnCourse Learning

Alternate Mortgage PlansAlternate Mortgage Plans

Borrow shares appreciation in return for lower rate

Payable when:

Property is sold

Loan is paid off

Ten years have passed

Sold prior to 10 years - % appreciation is due

Available for commercial properties

© 2014 OnCourse Learning

Alternate Mortgage PlansAlternate Mortgage Plans

Reduces the rate for the first 2 - 3 years

Seller prepays the interest

Placed in a saving account for the buyer

Rate reduced: 1st year – 3% 2nd year – 2% 3rd year – 1%

Qualifies at 1st year rate with 90% LTV

© 2014 OnCourse Learning

Alternate Mortgage PlansAlternate Mortgage Plans

Line of credit or fixed amountNot to exceed 80% LTV

Interest paid on amount borrowed

Home Equity Line of CreditSimilar to credit card

Access funds as needed

© 2014 OnCourse Learning

Instruments Relative to Instruments Relative to FinancingFinancing

Estoppel certificate: Estoppel certificate: acknowledges the debt owed to new mortgagee

Certificates of no defenseCertificates of no defense

Declaration of no set offDeclaration of no set off

Satisfaction Piece: Satisfaction Piece: acknowledges full payment

© 2014 OnCourse Learning

Instruments Relative to Instruments Relative to FinancingFinancing

Pledge: Pledge: money kept on deposit as security for the debt

Frozen asset

Escrow agreement: used to carry out terms of an agreement

Escrow agent: third partyEscrow agent: third party

© 2014 OnCourse Learning

Instruments Relative to Instruments Relative to FinancingFinancing

Short salesShort sales

Judicial foreclosureJudicial foreclosure

Nonjudicial foreclosureNonjudicial foreclosure

Strict foreclosure

© 2014 OnCourse Learning

Real Estate Mortgage Real Estate Mortgage TheoriesTheories

Defeasance clause: upon payment property reverts to mortgagor

Gives right of redemption

Deed of Trust as security instrument

© 2014 OnCourse Learning

Real Estate Mortgage Real Estate Mortgage TheoriesTheories

Borrower retains legal rights

Beneficiary has equitable rights

Mortgage as security instrument

© 2014 OnCourse Learning

Real Estate Mortgage Real Estate Mortgage TheoriesTheories

Lender does not wait for foreclosure for possession

Title is not turned over until redemption period expires

Deficiency judgment

© 2014 OnCourse Learning

LiensLiens

The mortgageThe mortgage: pledges property as collateral

Property Taxes: hProperty Taxes: have priority over all other liensProperty sold to successful bidder who receives a tax certificate

Tax deed or treasurer’s deed is issued after redemption period

Special assessments: Special assessments: pay for improvementsAssessed per front foot for sidewalks, paved roads

Assessed equally for sewer

Mechanics Liens: Mechanics Liens: suppliers of labor or materials may lien for nonpayment

Filed within a specified time after completion

Action must be taken within a specified time

Attachment Attachment against personal property is a writ of attachment writ of attachmentPrevents owner form leaving state with merchandise

Sheriff can seize property to satisfy the debt

© 2014 OnCourse Learning

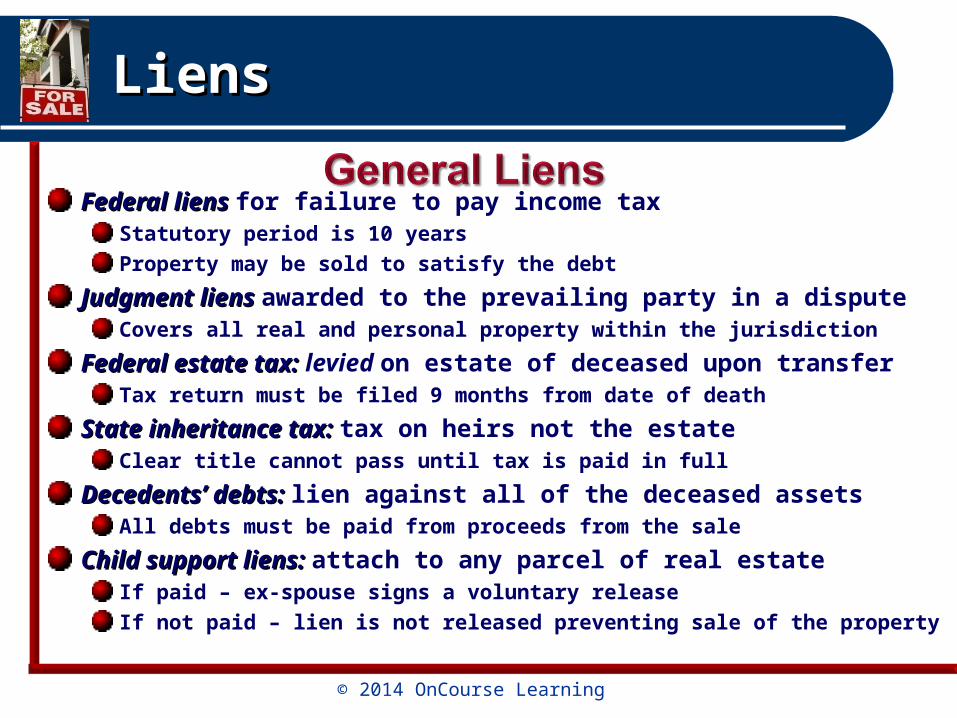

LiensLiens

Federal liens Federal liens for failure to pay income taxStatutory period is 10 years

Property may be sold to satisfy the debt

Judgment liens Judgment liens awarded to the prevailing party in a disputeCovers all real and personal property within the jurisdiction

Federal estate tax: Federal estate tax: levied on estate of deceased upon transferTax return must be filed 9 months from date of death

State inheritance tax: State inheritance tax: tax on heirs not the estateClear title cannot pass until tax is paid in full

Decedents’ debts: Decedents’ debts: lien against all of the deceased assetsAll debts must be paid from proceeds from the sale

Child support liens: Child support liens: attach to any parcel of real estateIf paid – ex-spouse signs a voluntary release

If not paid – lien is not released preventing sale of the property