Embed Size (px)

Citation preview

Real Estate CyclesGlenn R. Mueller, Ph.D.

ProfessorUniversity of Denver

Franklin L. Burns School of Real Estate & Construction Management

&

Real Estate Investment StrategistDividend Capital Research

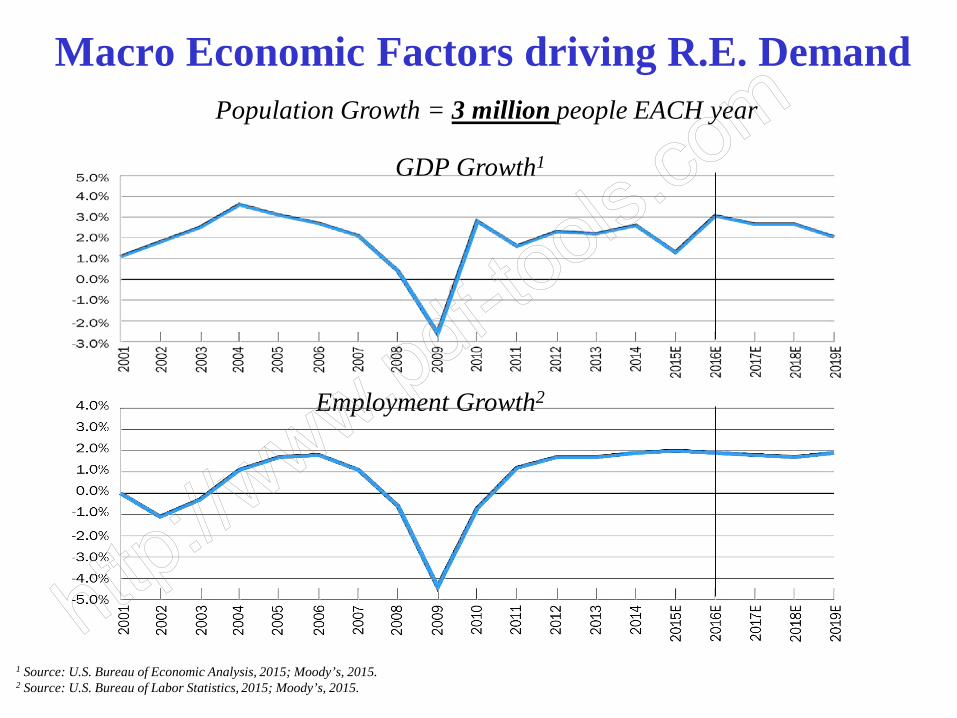

Macro Economic Factors driving R.E. DemandPopulation Growth = 3 million people EACH year

1 Source: U.S. Bureau of Economic Analysis, 2015; Moody’s, 2015.2 Source: U.S. Bureau of Labor Statistics, 2015; Moody’s, 2015.

Employment Growth2

GDP Growth1

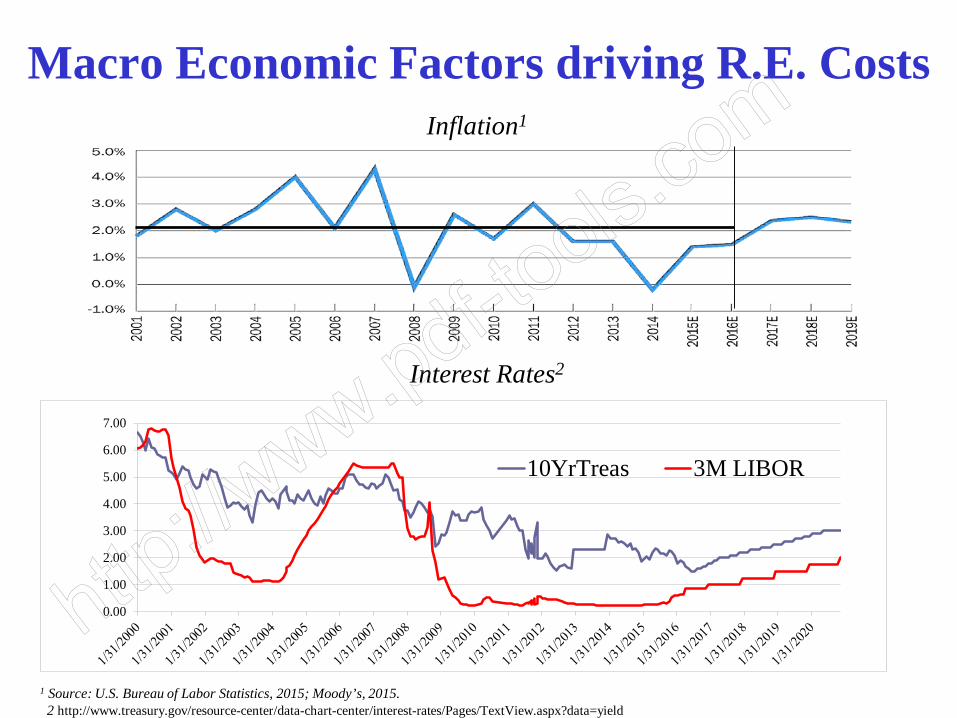

Macro Economic Factors driving R.E. Costs

1 Source: U.S. Bureau of Labor Statistics, 2015; Moody’s, 2015. 2 http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=yield

Inflation1

Interest Rates2

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

10YrTreas 3M LIBOR

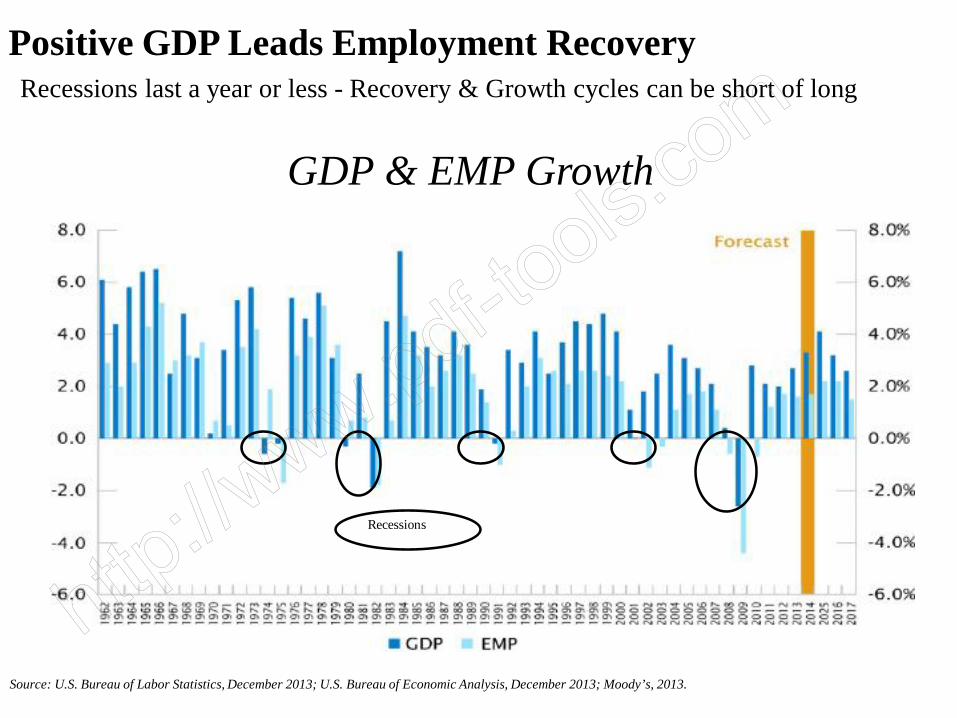

Recessions last a year or less - Recovery & Growth cycles can be short of long Positive GDP Leads Employment Recovery

Source: U.S. Bureau of Labor Statistics, December 2013; U.S. Bureau of Economic Analysis, December 2013; Moody’s, 2013.

GDP & EMP Growth

Recessions

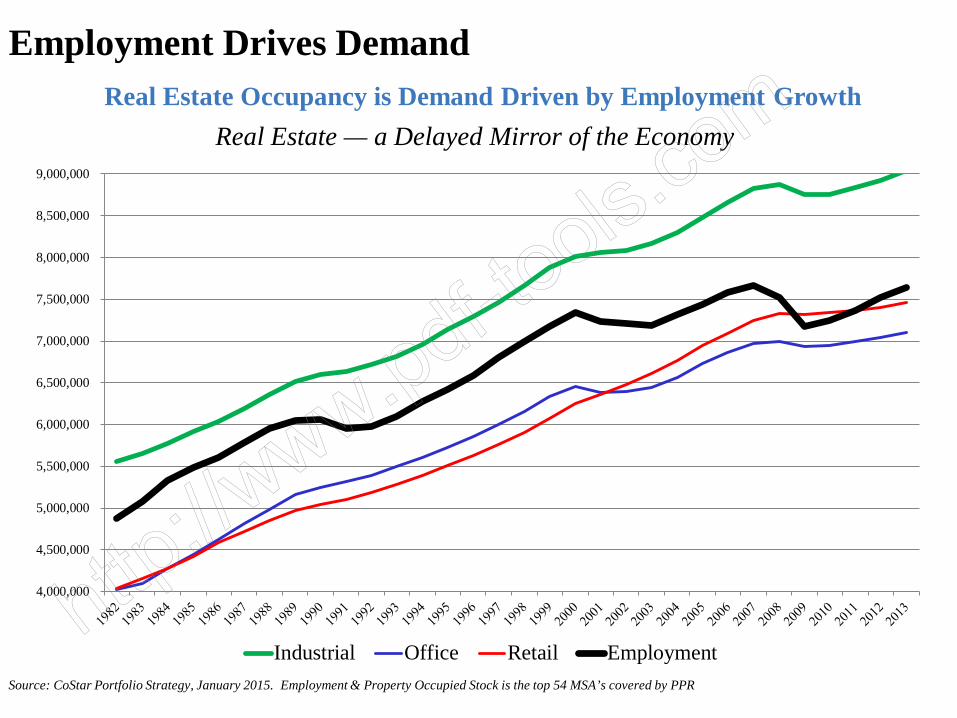

Real Estate Occupancy is Demand Driven by Employment Growth

4,000,000

4,500,000

5,000,000

5,500,000

6,000,000

6,500,000

7,000,000

7,500,000

8,000,000

8,500,000

9,000,000

Industrial Office Retail Employment

Employment Drives Demand

Real Estate — a Delayed Mirror of the Economy

Source: CoStar Portfolio Strategy, January 2015. Employment & Property Occupied Stock is the top 54 MSA’s covered by PPR

US Commercial Real Estate CycleFollows US Economic Cycles

3 Key Metrics:• Occupancies

• Rents• Property Prices

Source: Glenn Mueller, PhD

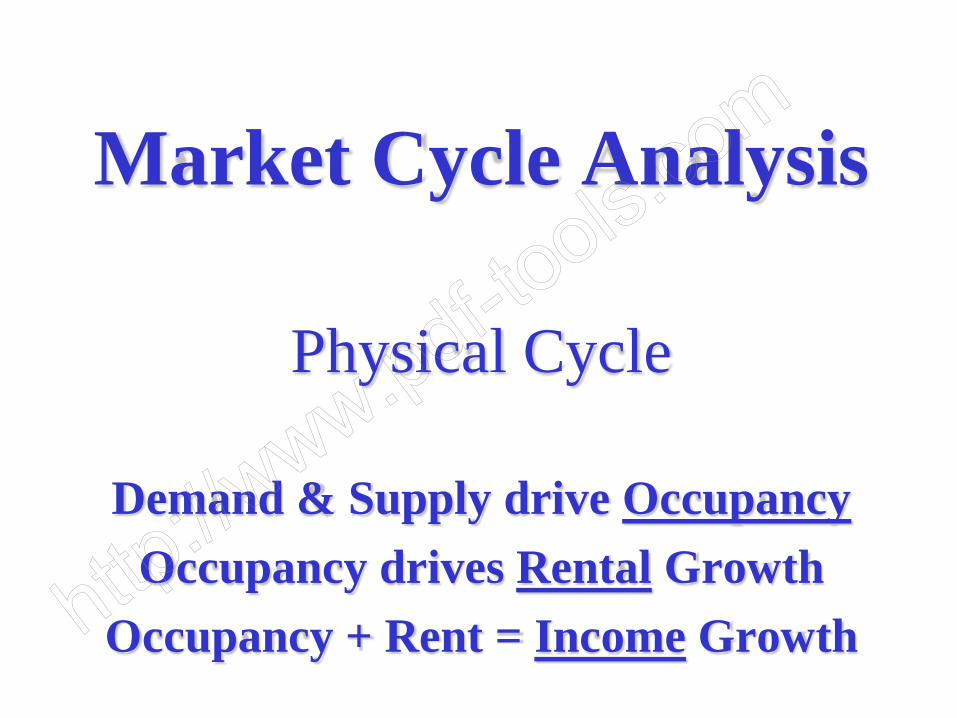

Market Cycle Analysis

Physical Cycle

Demand & Supply drive OccupancyOccupancy drives Rental Growth

Occupancy + Rent = Income Growth

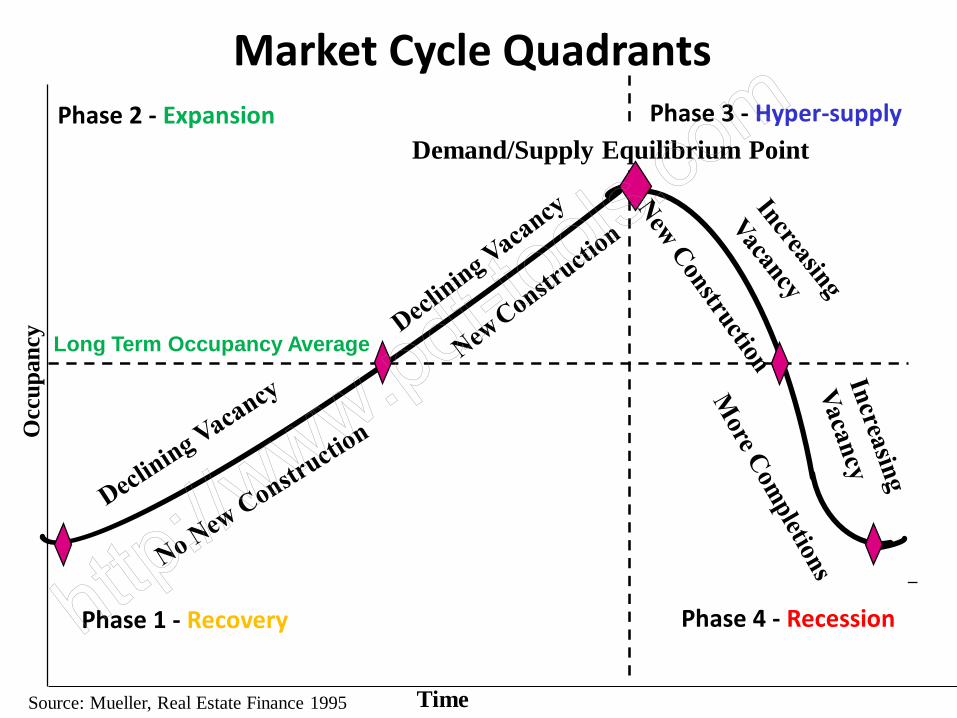

Source: Mueller, Real Estate Finance 1995

Market Cycle Quadrants

Phase 1 - Recovery

Phase 2 - Expansion

Phase 4 - Recession

Demand/Supply Equilibrium Point

Long Term Occupancy Average

Occ

upan

cy

Time

Phase 3 - Hyper-supply

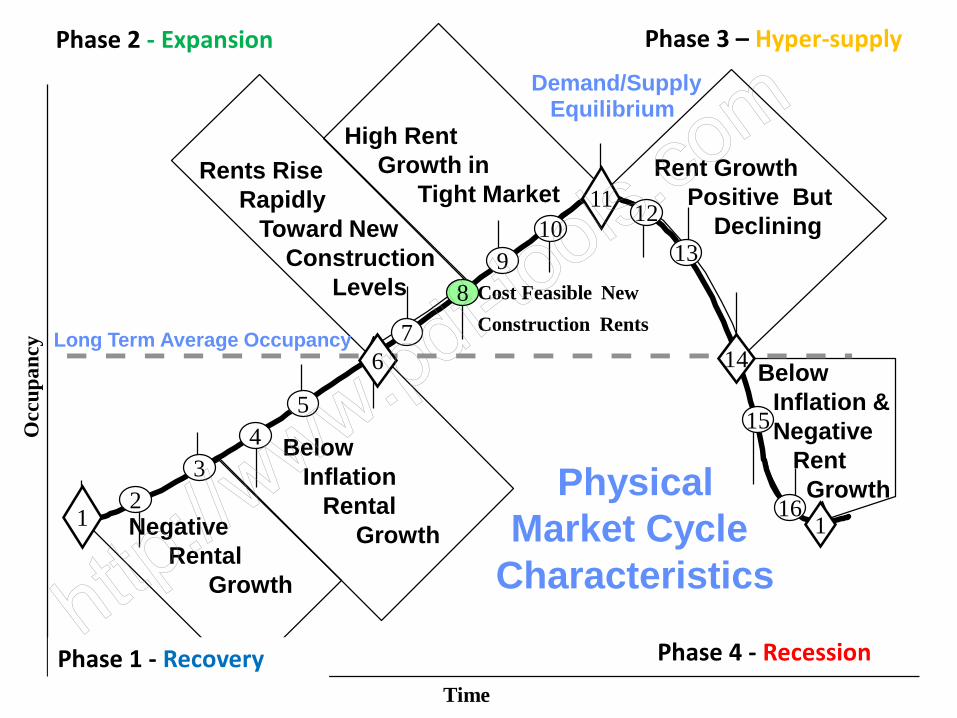

PhysicalMarket Cycle

CharacteristicsNegative

RentalGrowth

BelowInflation

RentalGrowth

Rents Rise Rapidly

Toward New Construction

Levels

High RentGrowth in

Tight Market

Demand/SupplyEquilibrium

Rent GrowthPositive But

Declining

-Below Inflation &Negative

RentGrowth

Cost Feasible NewConstruction Rents

Long Term Average Occupancy

Occ

upan

cy

Time

1467

8

1012

13

1

15

16

54

32

11

9

1

Phase 1 - Recovery

Phase 2 - Expansion

Phase 4 - Recession

Phase 3 – Hyper-supply

2

54

3

89

7

10

16

15

13

1

6

11

14

1

12

0.3%

2.7%

-3.0%

-1.5%

1.7%

4.0%

6.4%

11.0%

12.5%

10.5%

6.7%

-1.0%1.6%

3.3%

6.1%

10.0%

30 year Historic National Office Rental Growth

30 Year Cycle - Periods 1968-1997

Long Term Average Occupancy

Occ

upan

cy

Time

Phase 1 - Recovery

Phase 2 - Expansion

Phase 4 - Recession

Phase 3 – Hyper-supply

Source: Mueller, Real Estate Finance 1998

2

54

3

89

7

10

16

15

13

1

6

11

14

1

12

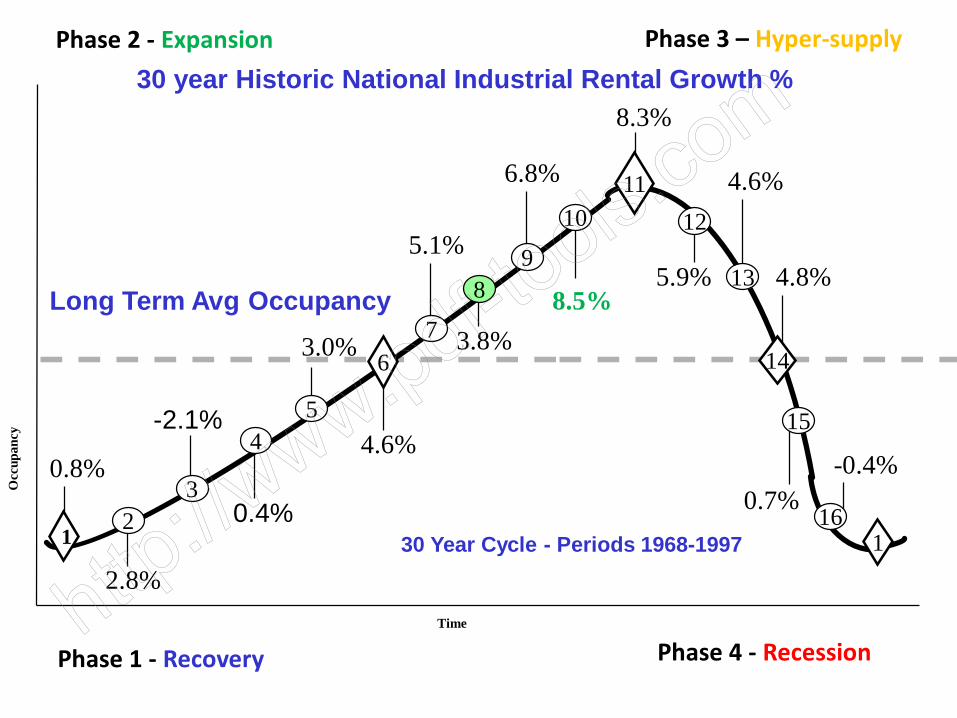

-2.1%

30 year Historic National Industrial Rental Growth %

0.4%0.8%

2.8%

3.0%

4.6%

5.1%

8.3%

8.5%

6.8%

3.8%

-0.4%0.7%

4.8%

4.6%

5.9%

30 Year Cycle - Periods 1968-1997

Long Term Avg Occupancy

Occ

upan

cy

Time

Phase 1 - Recovery

Phase 2 - Expansion

Phase 4 - Recession

Phase 3 – Hyper-supply

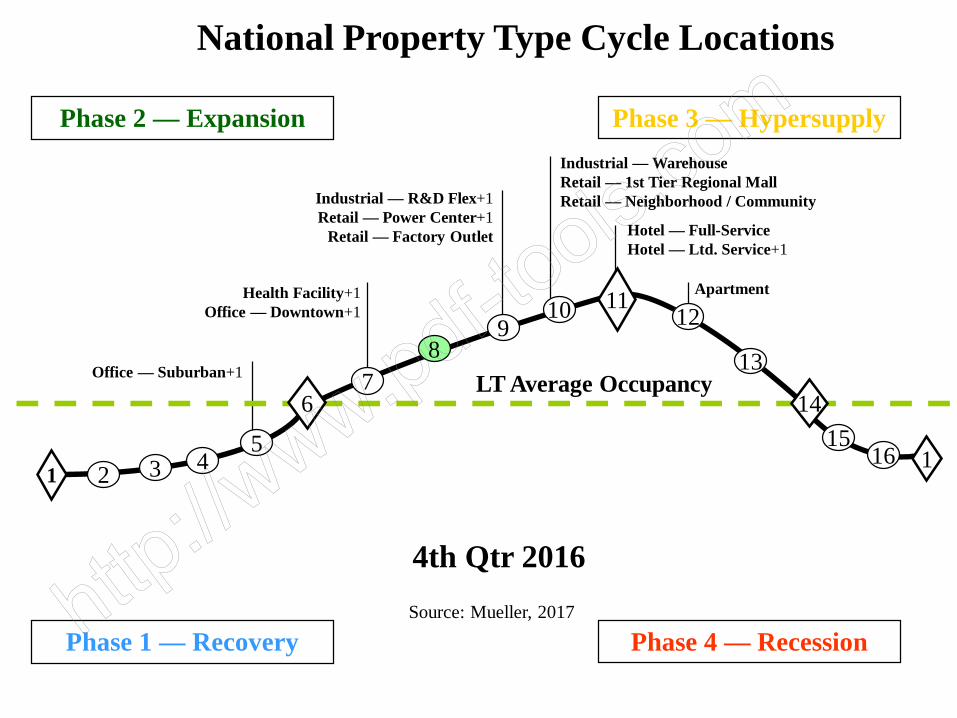

National Property Type Cycle Locations

4th Qtr 2016

LT Average Occupancy

Source: Mueller, 2017

Phase 2 — Expansion

Phase 1 — Recovery

Phase 3 — Hypersupply

Phase 4 — Recession

11

1467

89

10 12

13

1165421

15

Health Facility+1Office — Downtown+1

Office — Suburban+1

3

Industrial — WarehouseRetail — 1st Tier Regional MallRetail — Neighborhood / Community

Apartment

Hotel — Full-ServiceHotel — Ltd. Service+1

Industrial — R&D Flex+1Retail — Power Center+1

Retail — Factory Outlet

Houston

LT Average Occupancy

Source: Mueller, 2017

11

146

89

10 12

115

1654321

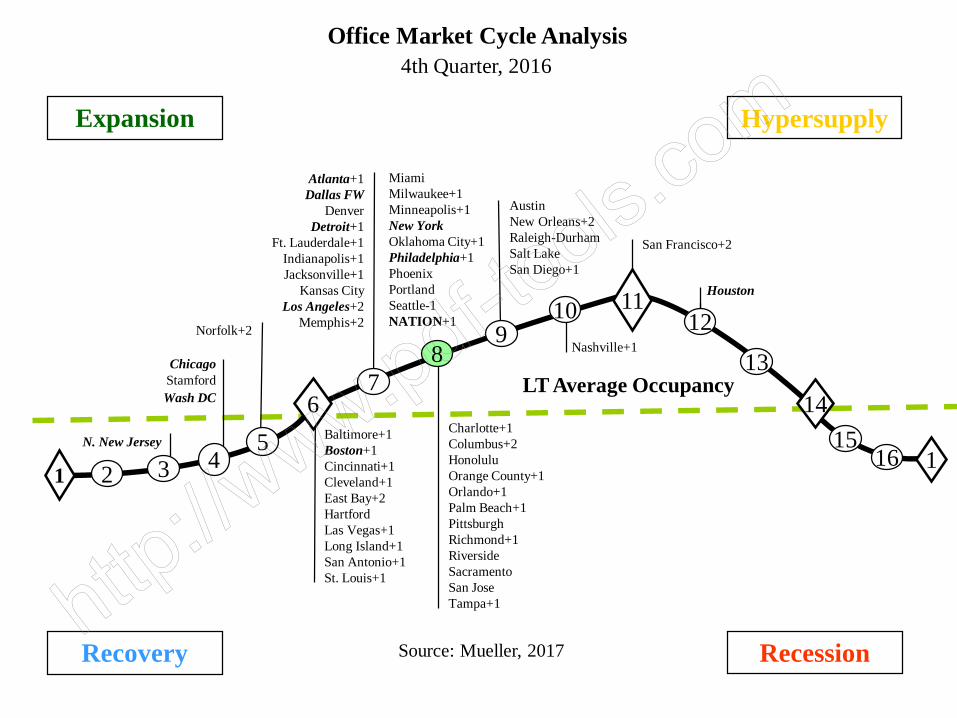

Office Market Cycle Analysis4th Quarter, 2016

713

N. New Jersey

Atlanta+1Dallas FW

DenverDetroit+1

Ft. Lauderdale+1Indianapolis+1Jacksonville+1

Kansas CityLos Angeles+2

Memphis+2

Charlotte+1Columbus+2HonoluluOrange County+1Orlando+1Palm Beach+1PittsburghRichmond+1RiversideSacramentoSan JoseTampa+1

AustinNew Orleans+2 Raleigh-DurhamSalt LakeSan Diego+1

Baltimore+1Boston+1Cincinnati+1Cleveland+1East Bay+2HartfordLas Vegas+1Long Island+1San Antonio+1St. Louis+1

ChicagoStamfordWash DC

Recovery Recession

Expansion Hypersupply

San Francisco+2

Nashville+1Norfolk+2

MiamiMilwaukee+1Minneapolis+1New YorkOklahoma City+1Philadelphia+1PhoenixPortlandSeattle-1NATION+1

BostonColumbus

Ft. LauderdaleIndianapolis

Las VegasLong Island+1

Source: Mueller, 2017

1467

8

10 12

13

115

1654321

LT Average Occupancy

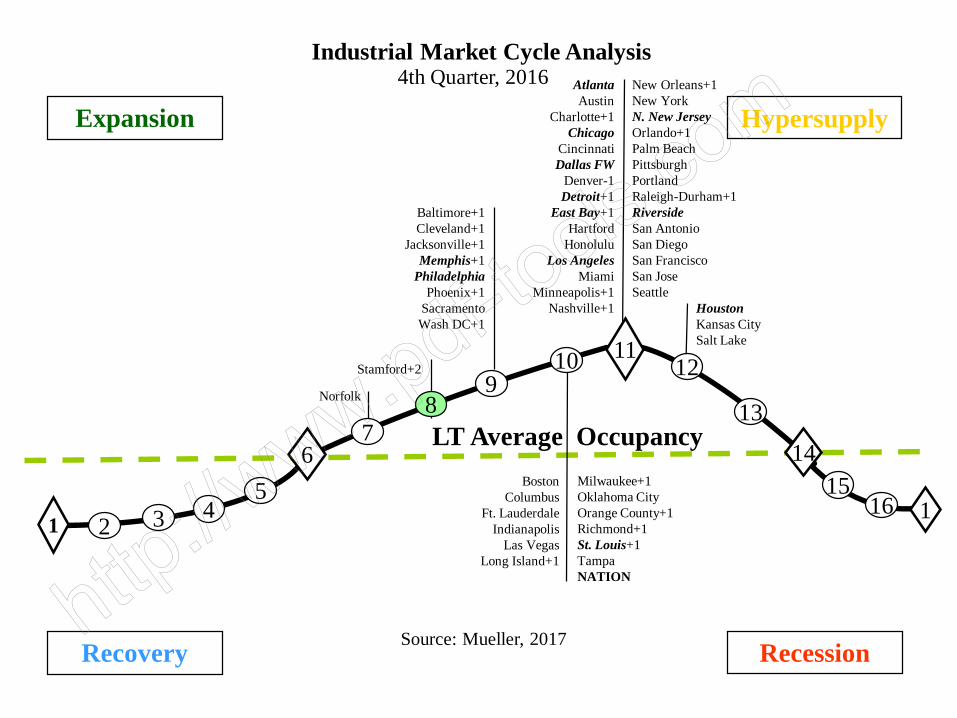

Industrial Market Cycle Analysis

11Stamford+2

Baltimore+1Cleveland+1

Jacksonville+1Memphis+1

PhiladelphiaPhoenix+1

SacramentoWash DC+1

AtlantaAustin

Charlotte+1Chicago

CincinnatiDallas FW

Denver-1Detroit+1

East Bay+1Hartford

HonoluluLos Angeles

MiamiMinneapolis+1

Nashville+1

9

4th Quarter, 2016

Norfolk

HoustonKansas CitySalt Lake

Milwaukee+1Oklahoma CityOrange County+1 Richmond+1St. Louis+1TampaNATION

New Orleans+1New YorkN. New JerseyOrlando+1Palm BeachPittsburghPortlandRaleigh-Durham+1RiversideSan AntonioSan DiegoSan FranciscoSan JoseSeattle

Recovery Recession

Expansion Hypersupply

Source: Mueller, 2017

11

1467

89

10 12

115

1654

21

LT Average Occupancy

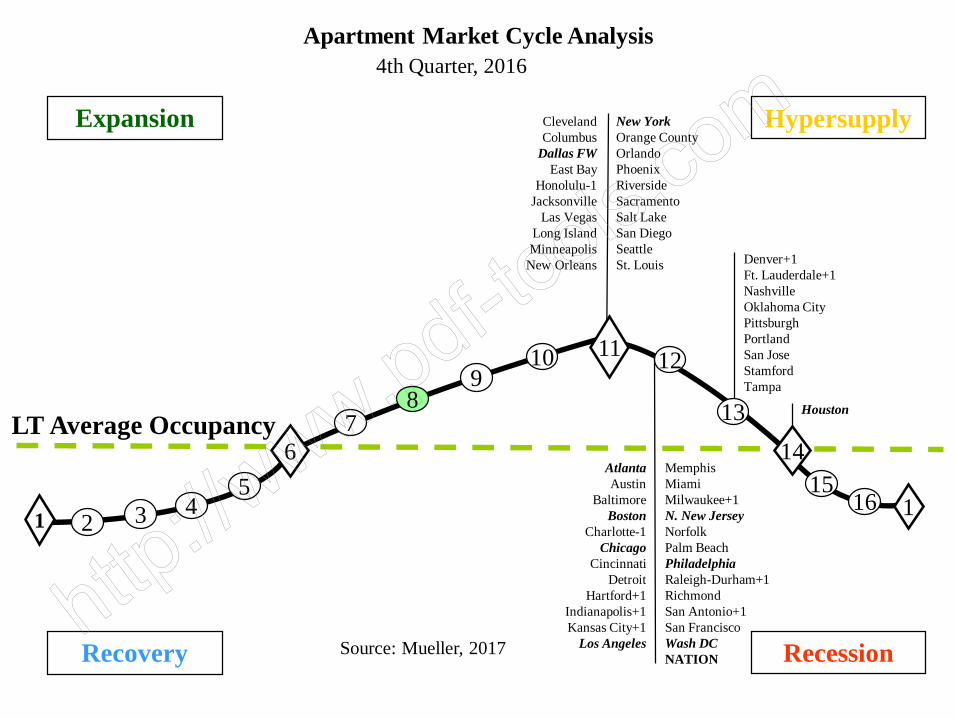

Apartment Market Cycle Analysis

13

ClevelandColumbus

Dallas FWEast Bay

Honolulu-1Jacksonville

Las VegasLong IslandMinneapolis

New Orleans

3

AtlantaAustin

BaltimoreBoston

Charlotte-1Chicago

CincinnatiDetroit

Hartford+1Indianapolis+1Kansas City+1

Los Angeles

New YorkOrange CountyOrlandoPhoenixRiversideSacramentoSalt LakeSan DiegoSeattleSt. Louis

4th Quarter, 2016

Denver+1Ft. Lauderdale+1NashvilleOklahoma CityPittsburghPortlandSan JoseStamfordTampa

MemphisMiamiMilwaukee+1N. New JerseyNorfolkPalm BeachPhiladelphiaRaleigh-Durham+1RichmondSan Antonio+1San FranciscoWash DCNATIONRecovery Recession

Expansion Hypersupply

Houston

Source: Mueller, 2017

11

1467

89 12

13

115

165

4321

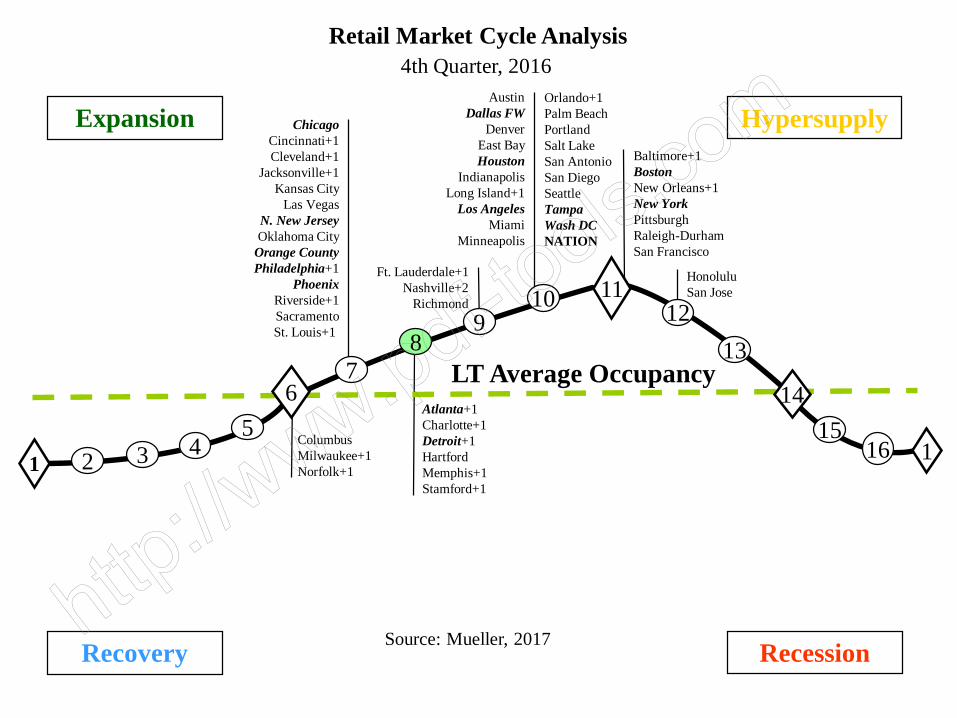

Retail Market Cycle Analysis

10

LT Average OccupancyAtlanta+1Charlotte+1Detroit+1HartfordMemphis+1Stamford+1

ChicagoCincinnati+1Cleveland+1

Jacksonville+1Kansas City

Las VegasN. New JerseyOklahoma City

Orange CountyPhiladelphia+1

PhoenixRiverside+1SacramentoSt. Louis+1

AustinDallas FW

DenverEast BayHouston

IndianapolisLong Island+1

Los AngelesMiami

Minneapolis

Baltimore+1BostonNew Orleans+1New YorkPittsburghRaleigh-DurhamSan Francisco

ColumbusMilwaukee+1Norfolk+1

Ft. Lauderdale+1Nashville+2

Richmond

4th Quarter, 2016

HonoluluSan Jose

Orlando+1 Palm BeachPortlandSalt Lake San AntonioSan DiegoSeattleTampaWash DCNATION

Recovery Recession

Expansion Hypersupply

Source: Mueller, 2017

1467

89 12

13

115

1654321

1110

LT Average Occupancy

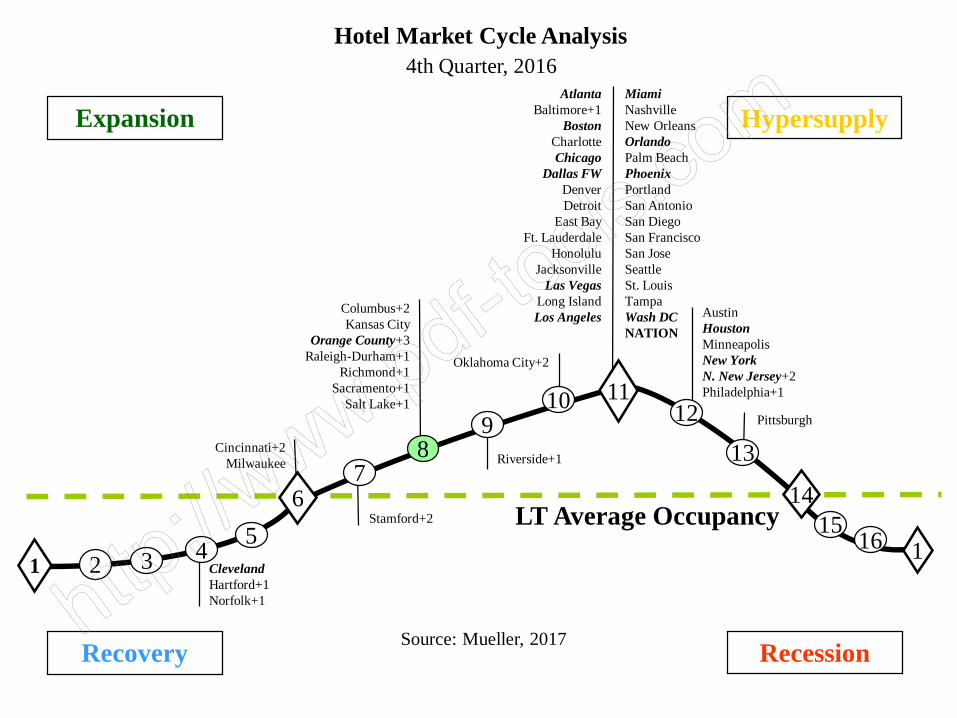

Hotel Market Cycle Analysis

Cincinnati+2Milwaukee

AtlantaBaltimore+1

BostonCharlotteChicago

Dallas FWDenverDetroit

East BayFt. Lauderdale

HonoluluJacksonville

Las VegasLong IslandLos Angeles Austin

HoustonMinneapolisNew YorkN. New Jersey+2Philadelphia+1

4th Quarter, 2016

Columbus+2Kansas City

Orange County+3Raleigh-Durham+1

Richmond+1Sacramento+1

Salt Lake+1Pittsburgh

MiamiNashvilleNew OrleansOrlandoPalm BeachPhoenixPortlandSan AntonioSan DiegoSan FranciscoSan JoseSeattleSt. LouisTampaWash DCNATION

ClevelandHartford+1Norfolk+1

Recovery Recession

Expansion Hypersupply

Oklahoma City+2

Riverside+1

Stamford+2

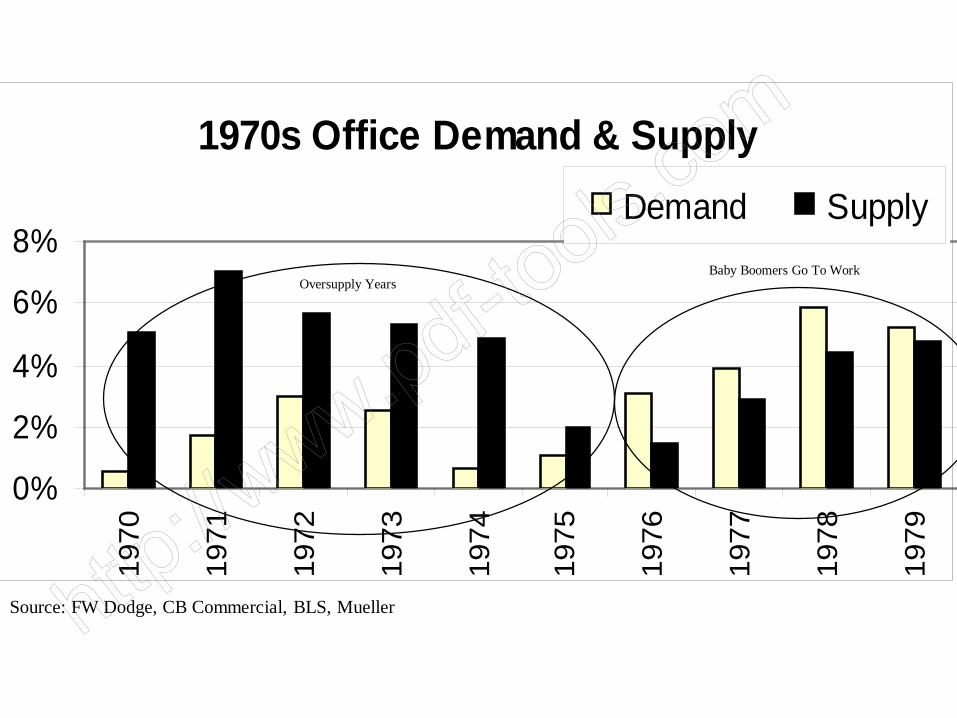

1970s Cycle•Factors Driving The First Half Cycle (5 Year)

•Strong Demand from the 1960s that stopped

•Recession 1974

•Capital Flow - Mortgage REITs produced oversupply

•Factors Driving The Second Half Cycle (5 Year)•Baby Boom Generation Goes to Work = Demand

•Capital Flow Shut Down = no supply = Lenders Recover

•Markets tighten and reach peak occupancy 1979 (5% vacancy)

1970s Office Demand & Supply

0%

2%

4%

6%

8%

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

Demand Supply

Source: FW Dodge, CB Commercial, BLS, Mueller

Oversupply YearsBaby Boomers Go To Work

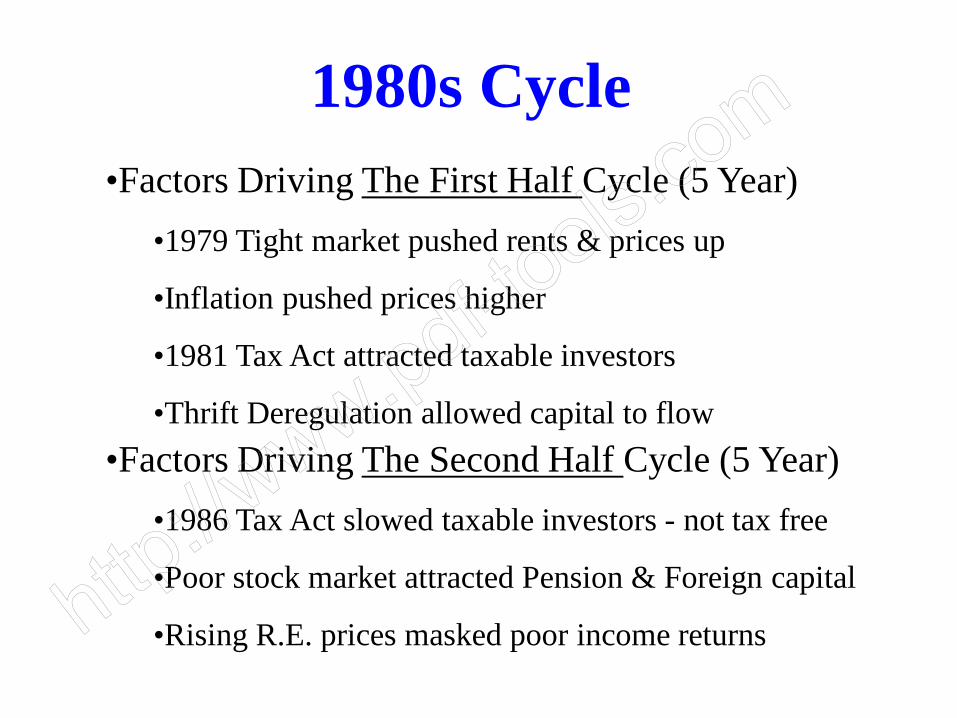

1980s Cycle•Factors Driving The First Half Cycle (5 Year)

•1979 Tight market pushed rents & prices up

•Inflation pushed prices higher

•1981 Tax Act attracted taxable investors

•Thrift Deregulation allowed capital to flow•Factors Driving The Second Half Cycle (5 Year)

•1986 Tax Act slowed taxable investors - not tax free

•Poor stock market attracted Pension & Foreign capital

•Rising R.E. prices masked poor income returns

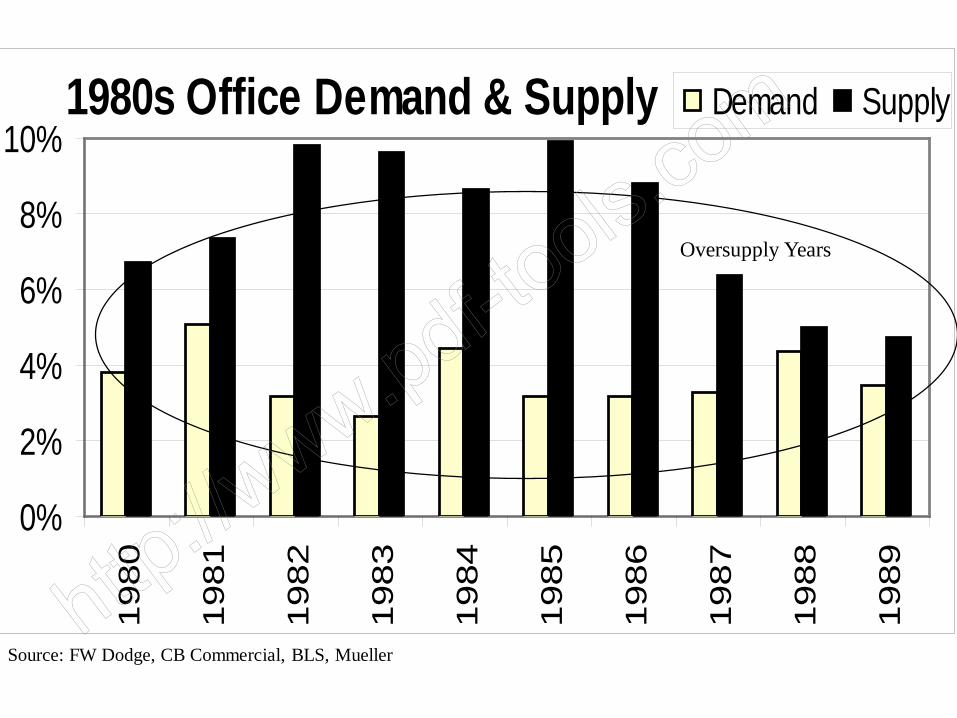

1980s Office Demand & Supply

0%

2%

4%

6%

8%

10%1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

Demand Supply

Source: FW Dodge, CB Commercial, BLS, Mueller

Oversupply Years

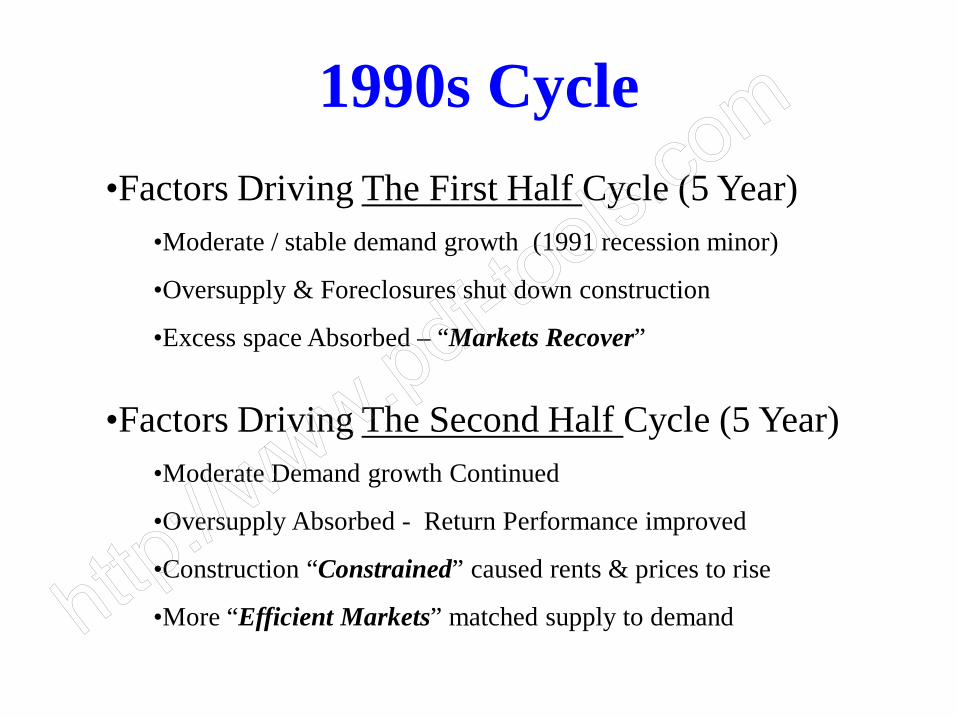

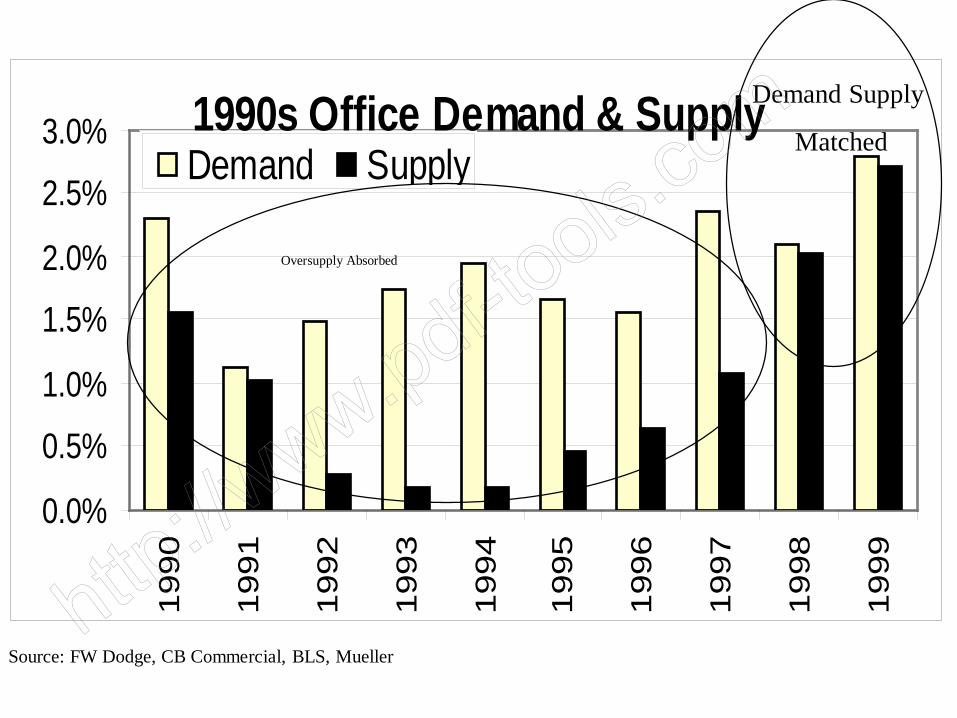

1990s Cycle•Factors Driving The First Half Cycle (5 Year)

•Moderate / stable demand growth (1991 recession minor)

•Oversupply & Foreclosures shut down construction

•Excess space Absorbed – “Markets Recover”

•Factors Driving The Second Half Cycle (5 Year)•Moderate Demand growth Continued

•Oversupply Absorbed - Return Performance improved

•Construction “Constrained” caused rents & prices to rise

•More “Efficient Markets” matched supply to demand

1990s Office Demand & Supply

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%19

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

Demand Supply

Source: FW Dodge, CB Commercial, BLS, Mueller

Oversupply Absorbed

Demand Supply

Matched

2000s Cycle•“Globalization” – stable but slower U.S. economic growth

•Technology vs manufacturing economy

•Market Data available

•Feedback loop = demand / supply balance

•Millennial Generation started entering workforce

•Public Markets (R.E. Capital markets more efficient)

•Supply Constraints (labor, steel & concrete costs, infrastructure)

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

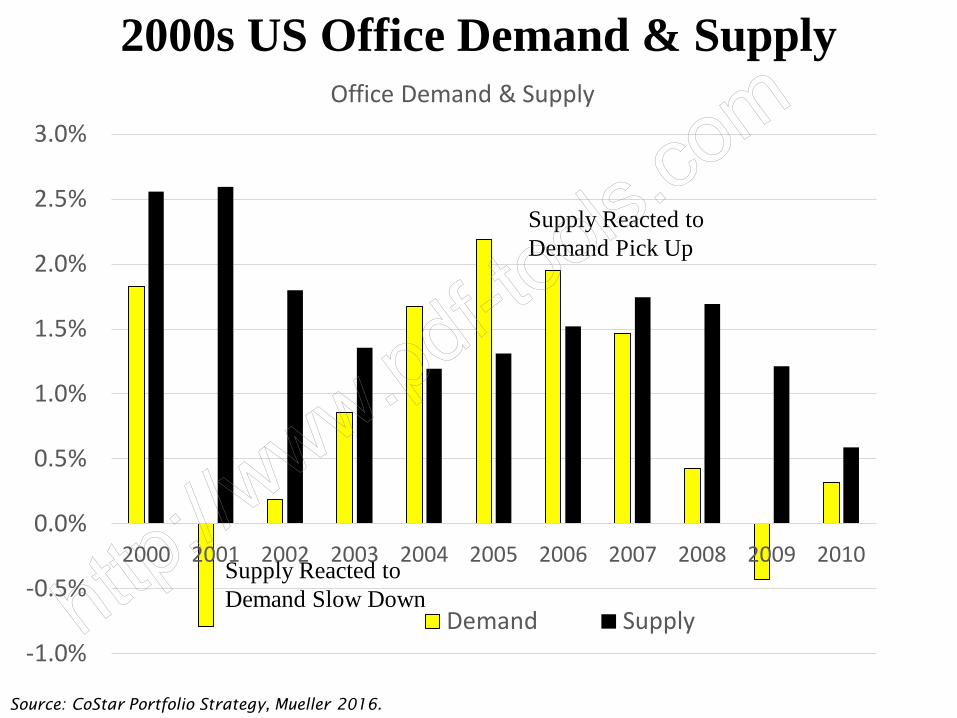

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Office Demand & Supply

Demand Supply

Supply Reacted to Demand Slow Down

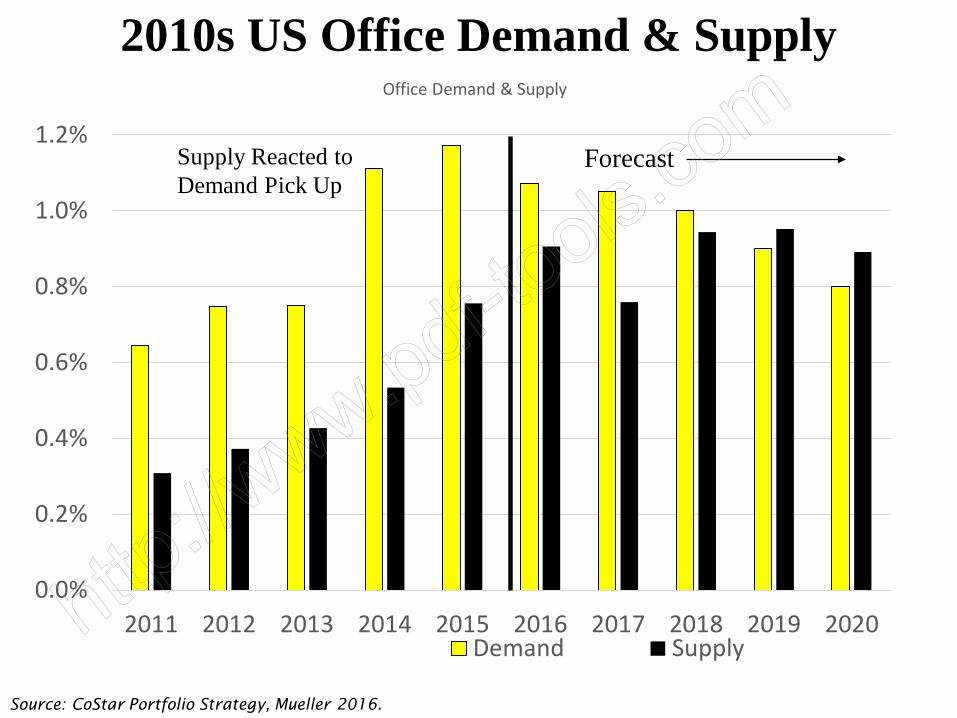

2000s US Office Demand & Supply

Supply Reacted to Demand Pick Up

Source: CoStar Portfolio Strategy, Mueller 2016.

2010s Cycle• Slow Economic Growth – 2% GDP the norm ?

• Economic Cycle Longer ?

•Low Interest Rate Environment – 2% 10/Year Treasury average?

•Millennial Generation workforce

•Millennial Generation consumer

•Technology

•Baby Boomers retiring

•Sustainability

•Employment Growth drives commercial demand

Source: Costar Portfolio Strategy, January 2015

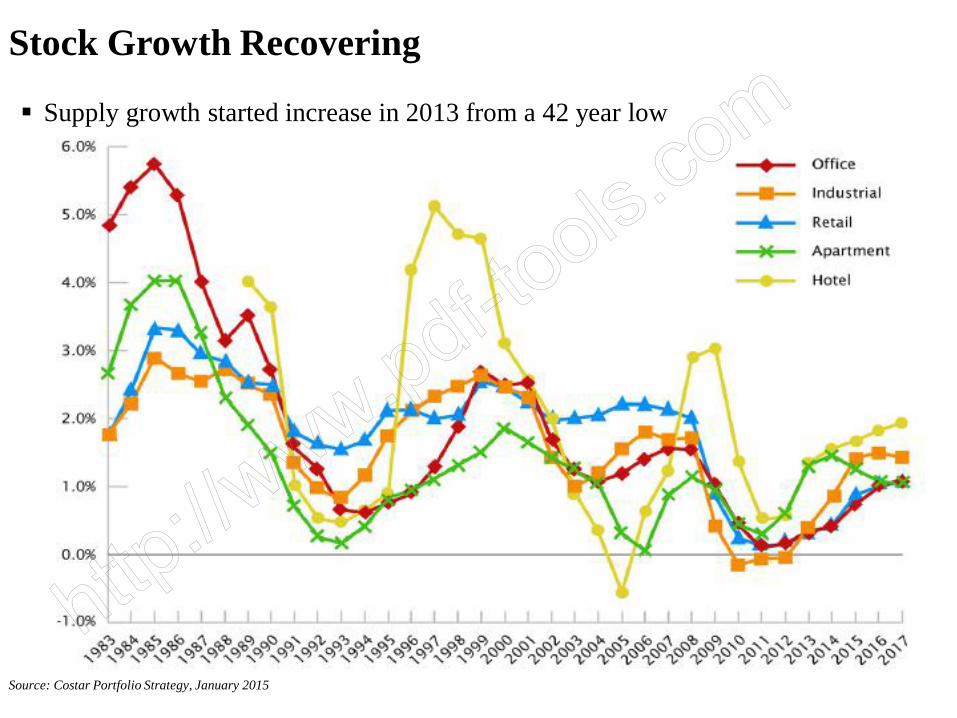

Stock Growth Recovering

Supply growth started increase in 2013 from a 42 year low

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Office Demand & Supply

Demand Supply

2010s US Office Demand & Supply

Supply Reacted to Demand Pick Up

Source: CoStar Portfolio Strategy, Mueller 2016.

Forecast

Rec

essi

on

Rec

essi

on

Rec

essi

on

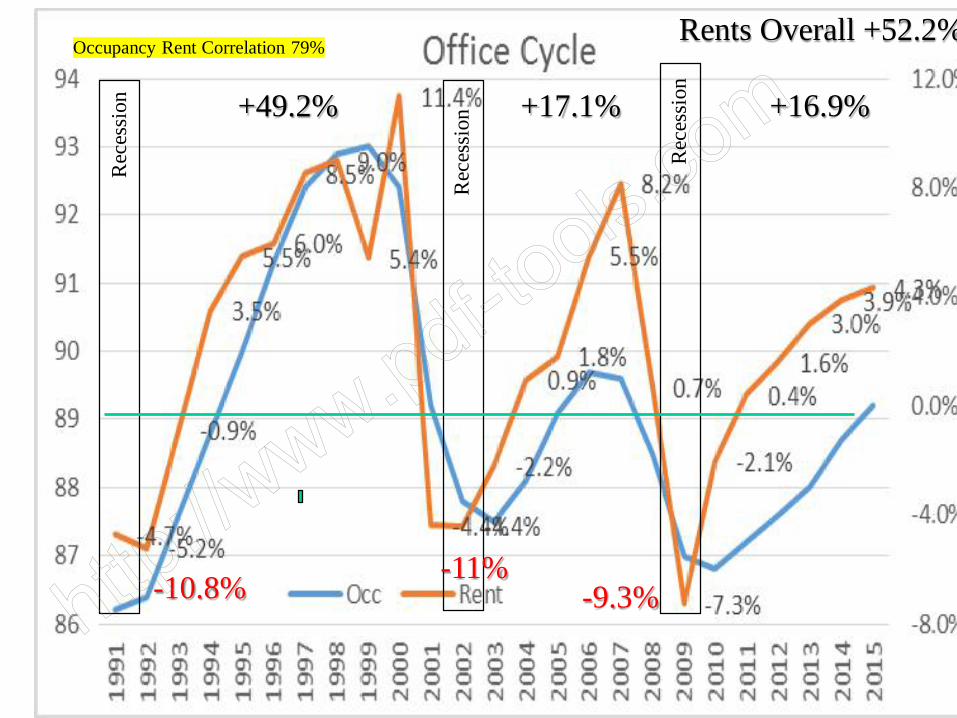

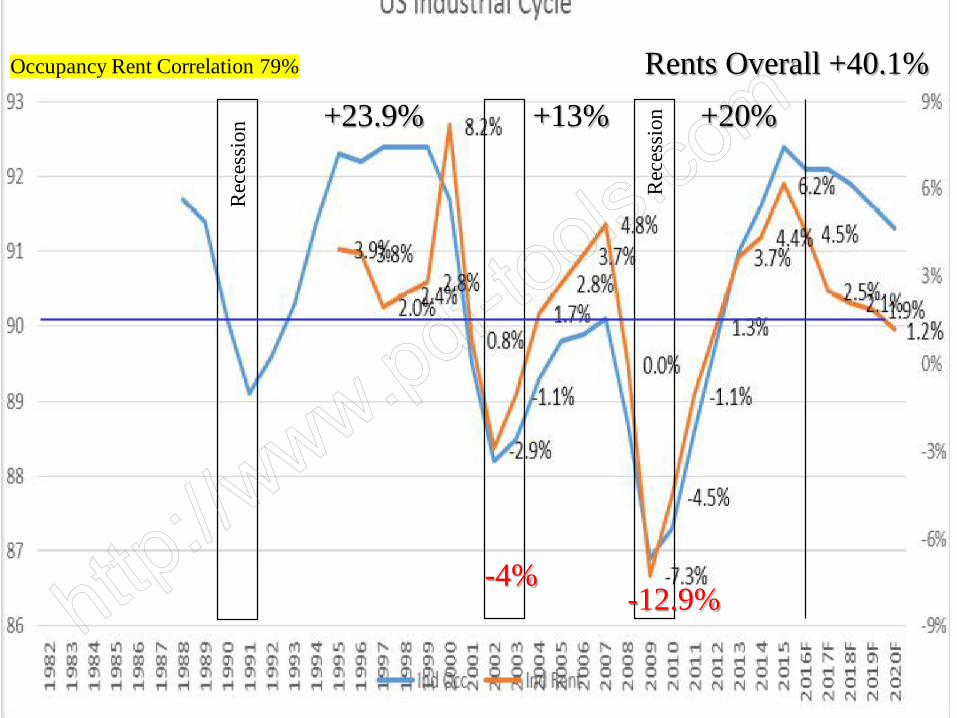

Occupancy Rent Correlation 79%

-10.8% -11%-9.3%

+16.9%+17.1%+49.2%

Rents Overall +52.2%

Source: Mueller, 2017

11

1467

89

10 12

13

115

164321

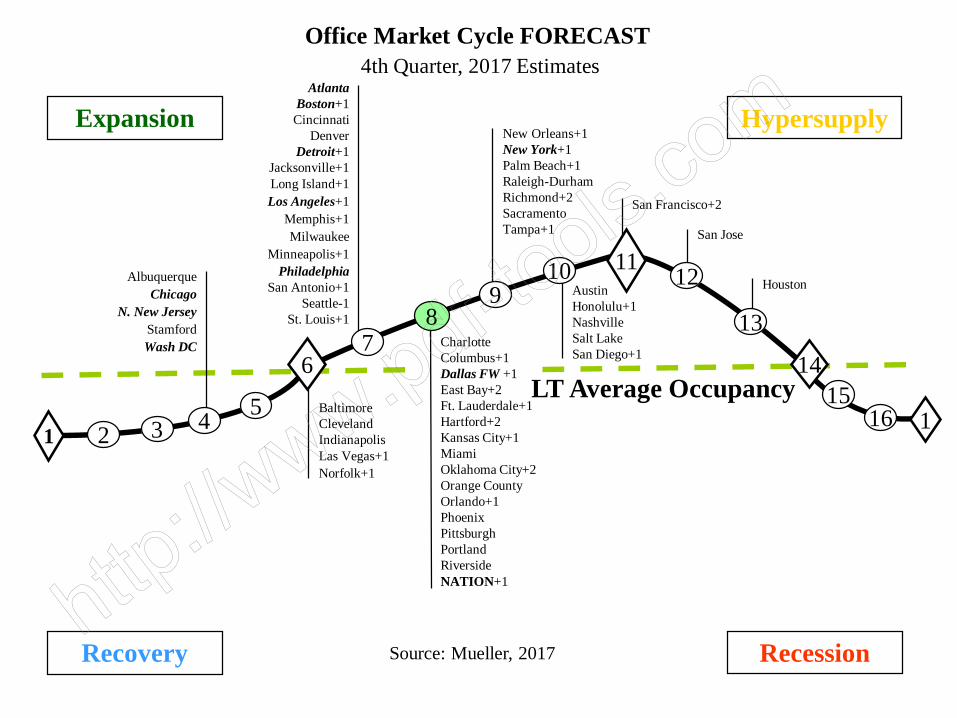

4th Quarter, 2017 Estimates

LT Average Occupancy

Office Market Cycle FORECAST

Houston

CharlotteColumbus+1Dallas FW +1East Bay+2 Ft. Lauderdale+1Hartford+2 Kansas City+1MiamiOklahoma City+2Orange CountyOrlando+1Phoenix PittsburghPortlandRiversideNATION+1

BaltimoreClevelandIndianapolisLas Vegas+1Norfolk+1

5

AustinHonolulu+1NashvilleSalt LakeSan Diego+1

New Orleans+1New York+1Palm Beach+1Raleigh-DurhamRichmond+2SacramentoTampa+1 San Jose

AlbuquerqueChicago

N. New JerseyStamfordWash DC

AtlantaBoston+1Cincinnati

DenverDetroit+1

Jacksonville+1Long Island+1Los Angeles+1

Memphis+1Milwaukee

Minneapolis+1Philadelphia

San Antonio+1Seattle-1

St. Louis+1

Recovery Recession

Expansion Hypersupply

San Francisco+2

Rec

essi

on

Rec

essi

on

Occupancy Rent Correlation 79%

-4%-12.9%

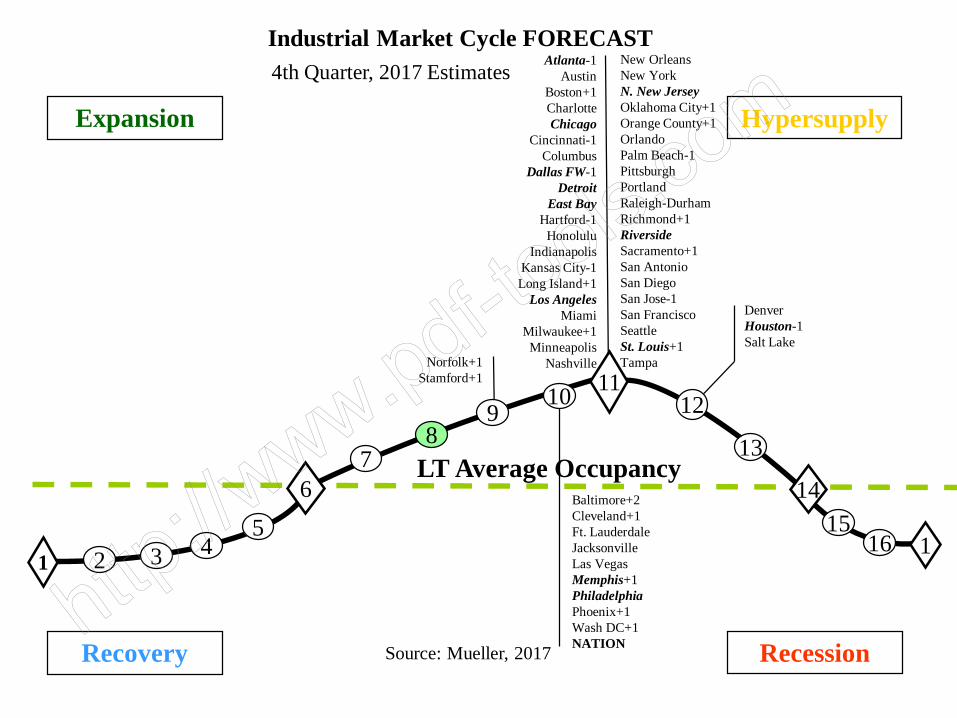

+20%+13%+23.9%Rents Overall +40.1%

Source: Mueller, 2017

11

14

89

10 12

13

115

16531

LT Average Occupancy

Industrial Market Cycle FORECAST

42

76 Baltimore+2

Cleveland+1Ft. LauderdaleJacksonvilleLas VegasMemphis+1PhiladelphiaPhoenix+1Wash DC+1 NATION

Atlanta-1Austin

Boston+1CharlotteChicago

Cincinnati-1Columbus

Dallas FW-1Detroit

East BayHartford-1

HonoluluIndianapolis

Kansas City-1Long Island+1

Los AngelesMiami

Milwaukee+1Minneapolis

Nashville

DenverHouston-1Salt Lake

4th Quarter, 2017 Estimates

Norfolk+1Stamford+1

New OrleansNew YorkN. New JerseyOklahoma City+1Orange County+1OrlandoPalm Beach-1PittsburghPortlandRaleigh-DurhamRichmond+1RiversideSacramento+1San AntonioSan DiegoSan Jose-1San FranciscoSeattleSt. Louis+1Tampa

Recovery Recession

Expansion Hypersupply

Rec

essi

on

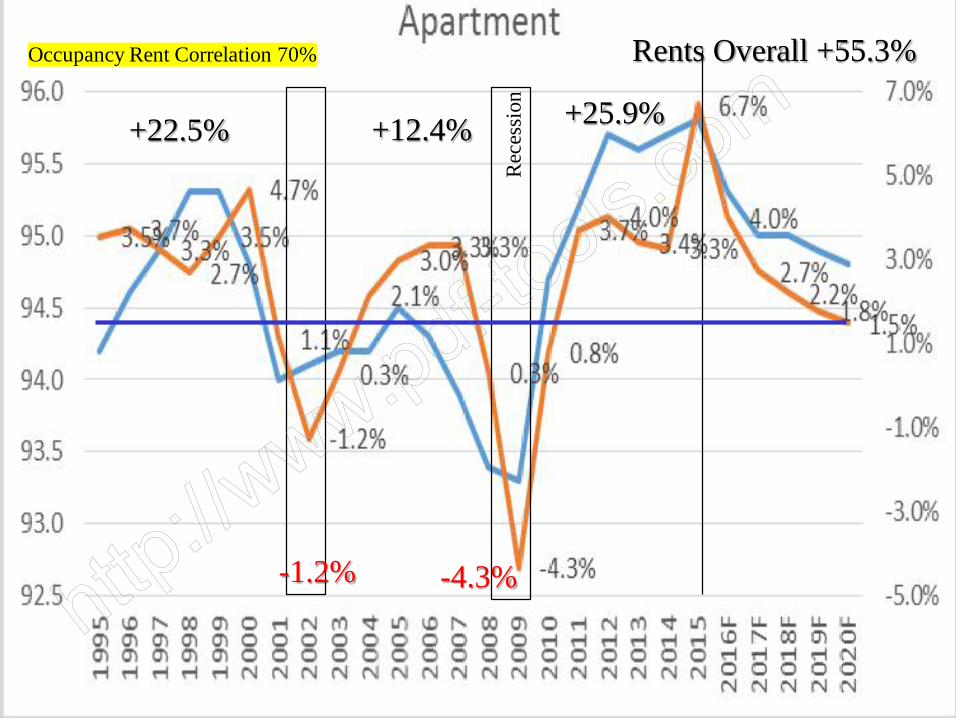

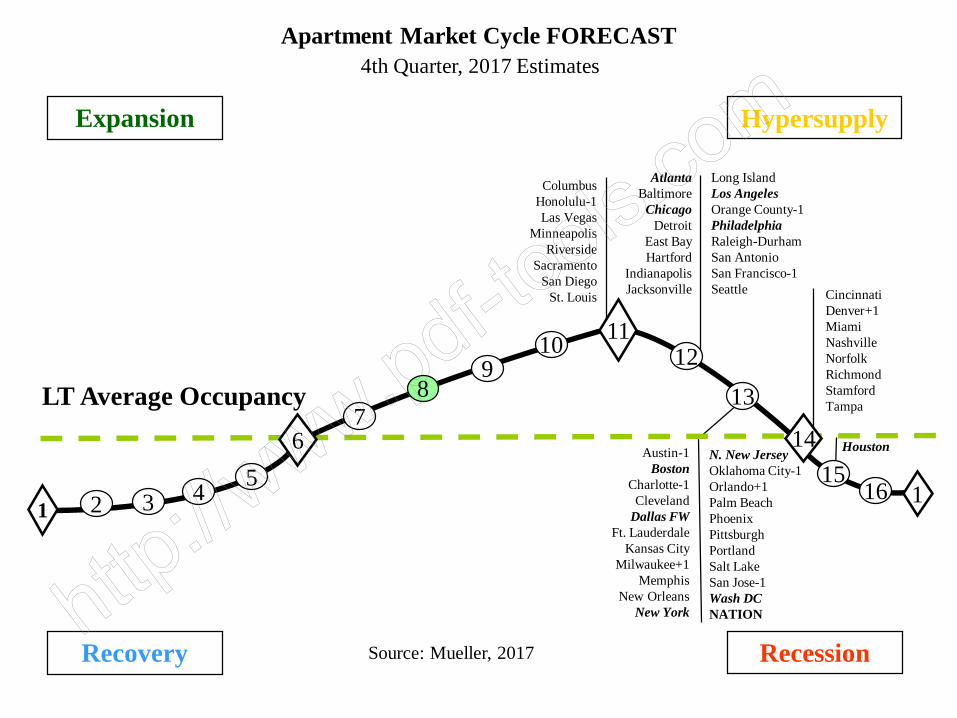

Occupancy Rent Correlation 70%

-1.2% -4.3%

+25.9%+12.4%+22.5%

Rents Overall +55.3%

Source: Mueller, 2017

11

146

89

10 12

115

164321

LT Average Occupancy

Apartment Market Cycle FORECAST

5

7

CincinnatiDenver+1MiamiNashvilleNorfolkRichmondStamfordTampa

Austin-1Boston

Charlotte-1Cleveland

Dallas FWFt. Lauderdale

Kansas CityMilwaukee+1

MemphisNew Orleans

New York

ColumbusHonolulu-1Las Vegas

MinneapolisRiverside

SacramentoSan Diego

St. Louis

13

4th Quarter, 2017 Estimates

N. New JerseyOklahoma City-1Orlando+1Palm BeachPhoenixPittsburghPortlandSalt LakeSan Jose-1Wash DCNATION

AtlantaBaltimore

ChicagoDetroit

East BayHartford

IndianapolisJacksonville

Houston

Long Island Los AngelesOrange County-1PhiladelphiaRaleigh-DurhamSan AntonioSan Francisco-1Seattle

Recovery Recession

Expansion Hypersupply

Rec

essi

on

Rec

essi

on

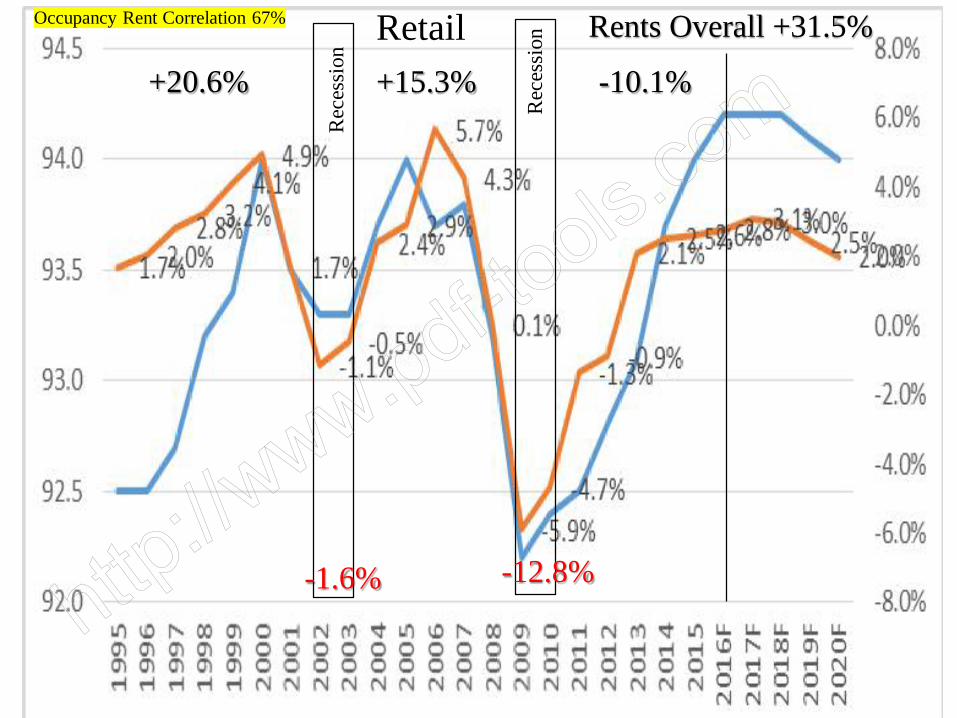

Occupancy Rent Correlation 67%

-1.6% -12.8%

-10.1%+15.3%+20.6%

Rents Overall +31.5%Retail

Source: Mueller, 2017

11

147

910 12

13

115

164321

LT Average

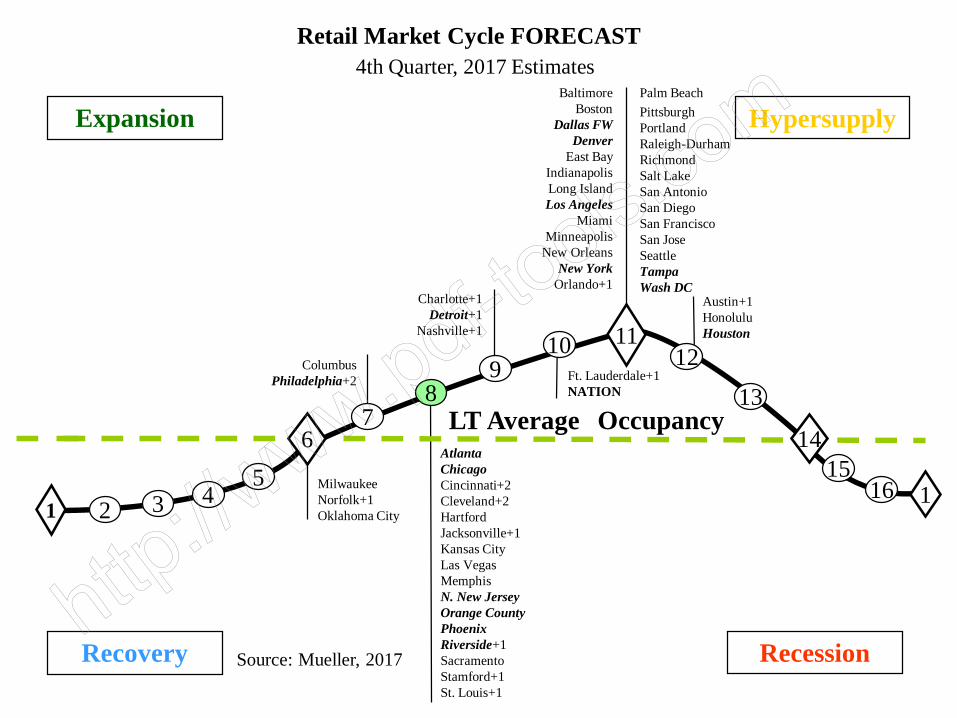

Retail Market Cycle FORECAST

6Occupancy

MilwaukeeNorfolk+1Oklahoma City

ColumbusPhiladelphia+2

AtlantaChicagoCincinnati+2Cleveland+2HartfordJacksonville+1Kansas CityLas Vegas MemphisN. New JerseyOrange CountyPhoenixRiverside+1SacramentoStamford+1St. Louis+1

Ft. Lauderdale+1NATION

5

8

Palm BeachPittsburghPortlandRaleigh-DurhamRichmondSalt LakeSan AntonioSan DiegoSan FranciscoSan JoseSeattleTampaWash DC

4th Quarter, 2017 Estimates

Austin+1HonoluluHouston

Recovery Recession

Expansion Hypersupply

Charlotte+1Detroit+1

Nashville+1

BaltimoreBoston

Dallas FWDenver

East BayIndianapolisLong IslandLos Angeles

MiamiMinneapolis

New OrleansNew York

Orlando+1

Rec

essi

on

Rec

essi

on

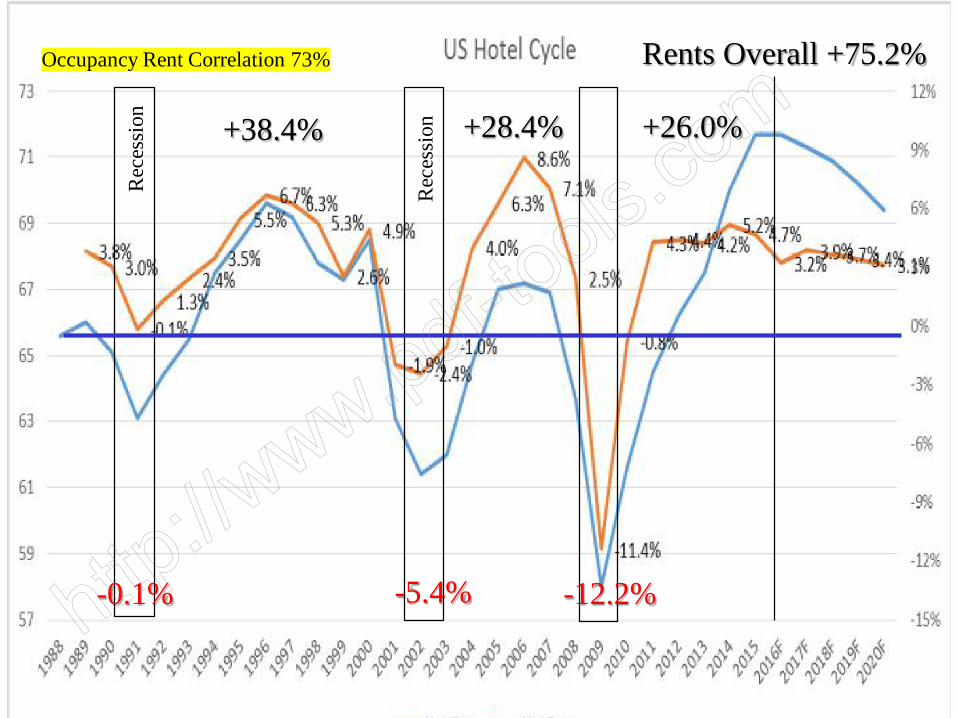

Occupancy Rent Correlation 73%

-0.1% -5.4%

+26.0%+28.4%+38.4%

Rents Overall +75.2%

-12.2%

Cleveland+1HartfordNorfolk+1

LT Average Occupancy

Source: Mueller, 2017

11

1467

8 910 12

13

115

1654321

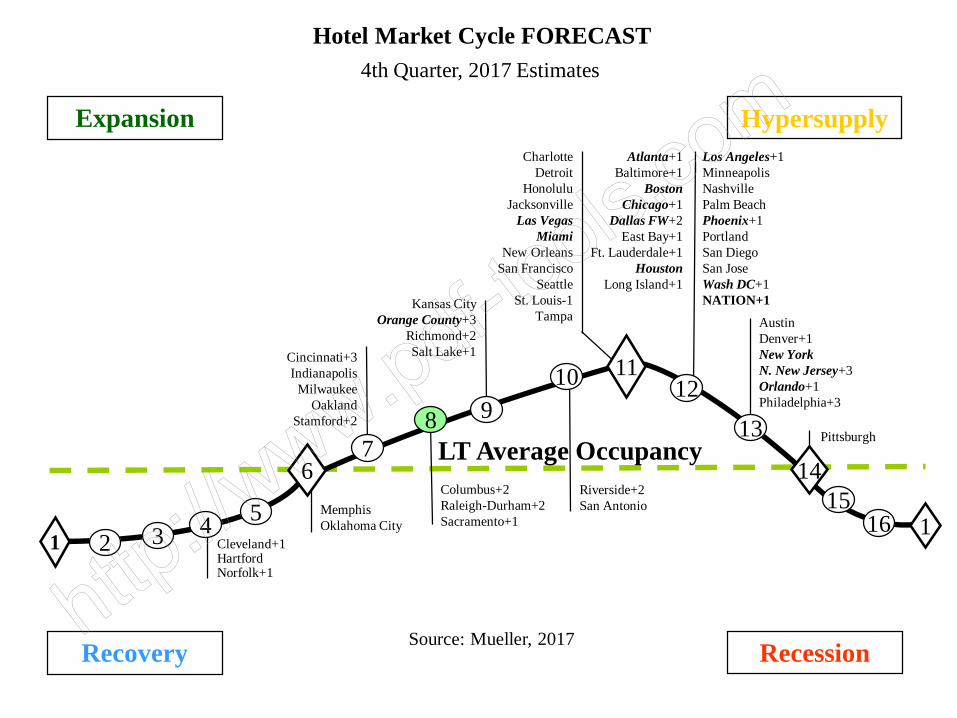

Hotel Market Cycle FORECAST

MemphisOklahoma City

Cincinnati+3Indianapolis

MilwaukeeOakland

Stamford+2

Los Angeles+1MinneapolisNashvillePalm BeachPhoenix+1PortlandSan DiegoSan JoseWash DC+1NATION+1

Riverside+2San Antonio

CharlotteDetroit

HonoluluJacksonville

Las VegasMiami

New OrleansSan Francisco

SeattleSt. Louis-1

Tampa

4th Quarter, 2017 Estimates

AustinDenver+1New YorkN. New Jersey+3Orlando+1 Philadelphia+3

Columbus+2Raleigh-Durham+2Sacramento+1

Pittsburgh

Recovery Recession

Expansion Hypersupply

Kansas CityOrange County+3

Richmond+2Salt Lake+1

Atlanta+1Baltimore+1

BostonChicago+1

Dallas FW+2East Bay+1

Ft. Lauderdale+1Houston

Long Island+1

Financial Cycle

$Capital$ Flows affect Prices

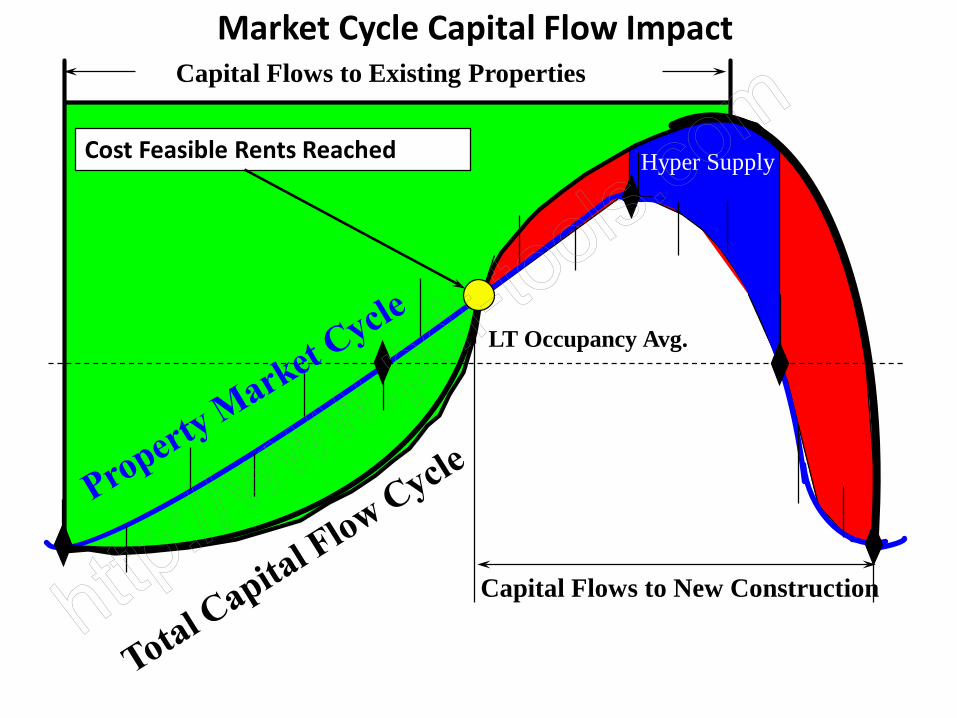

Hyper Supply

LT Occupancy Avg.

Market Cycle Capital Flow ImpactCapital Flows to Existing Properties

Capital Flows to New Construction

Cost Feasible Rents Reached

Source: Bonds = SIFMA, January 2015; Equities = World Federation of Exchanges for Equities, January 2015; U.S. Real Estate = Moody’s Real CPPI, January 2015. Commercial real estate are subject to real estate risks associated with operating and leasing properties. Additional risks include changes in economic conditions, interest rates, property values, and supply and demand, as well as possible environmental liabilities, zoning issues and natural disasters.

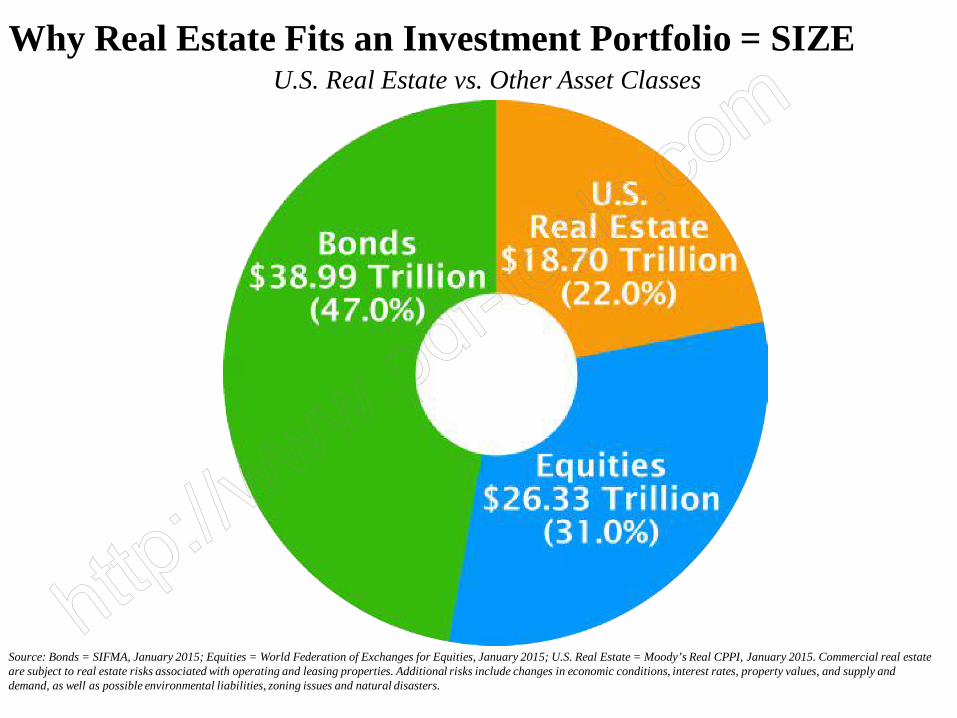

U.S. Real Estate vs. Other Asset ClassesWhy Real Estate Fits an Investment Portfolio = SIZE

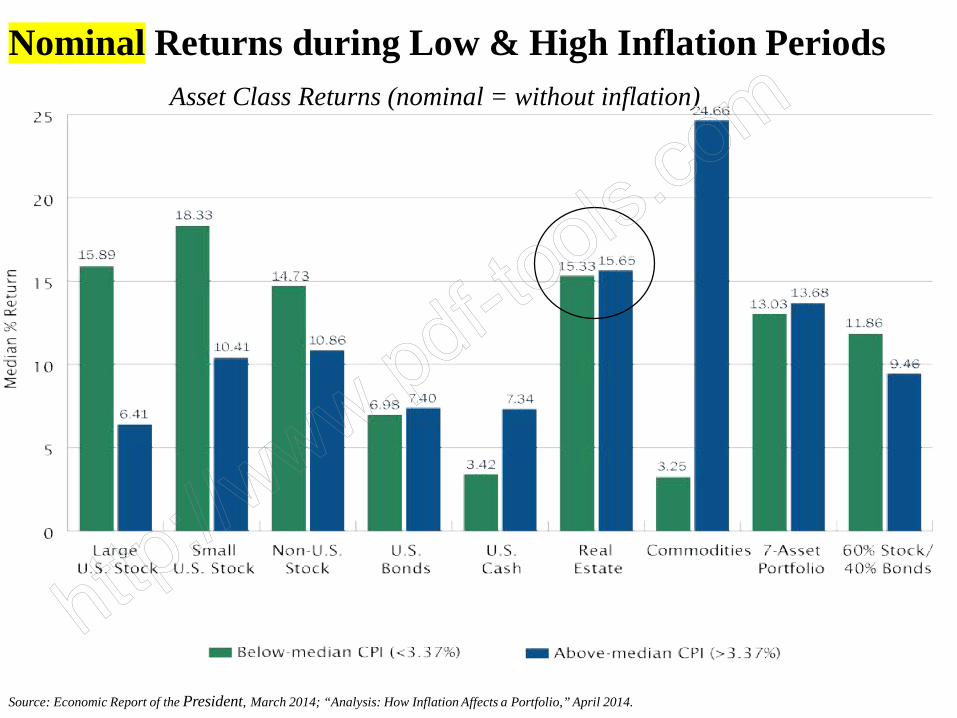

Nominal Returns during Low & High Inflation Periods

Source: Economic Report of the President, March 2014; “Analysis: How Inflation Affects a Portfolio,” April 2014.

Asset Class Returns (nominal = without inflation)

Real Returns during Low & High Inflation Periods

Source: Economic Report of the President, March 2014; “Analysis: How Inflation Affects a Portfolio,” April 2014.

REAL Asset Class Returns (inflation-adjusted)

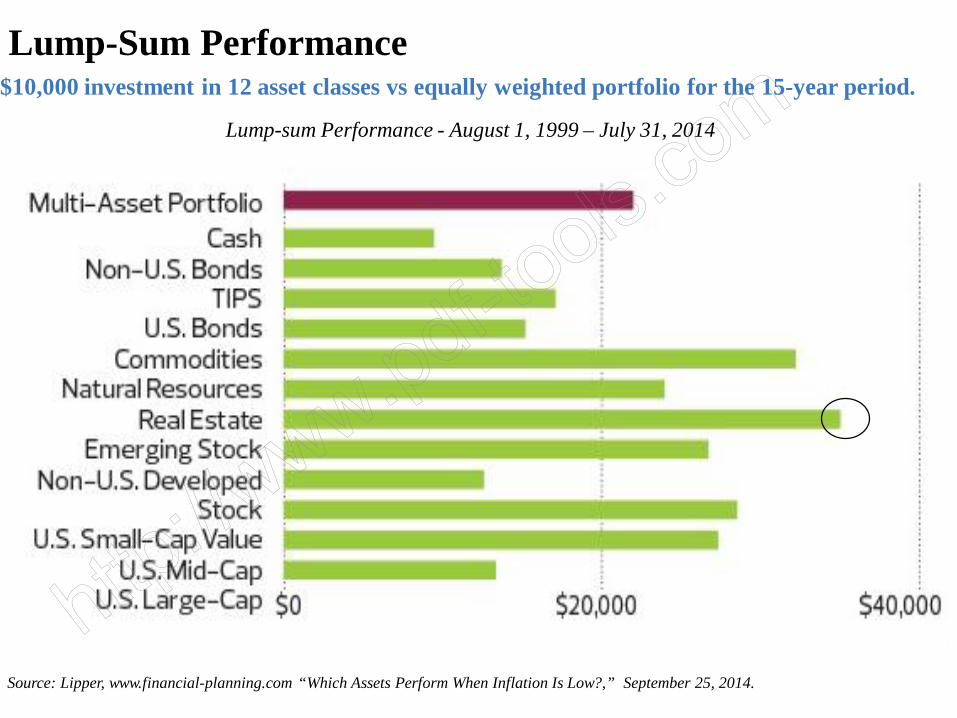

Lump-Sum Performance

Source: Lipper, www.financial-planning.com “Which Assets Perform When Inflation Is Low?,” September 25, 2014.

Lump-sum Performance - August 1, 1999 – July 31, 2014

$10,000 investment in 12 asset classes vs equally weighted portfolio for the 15-year period.

1.00

3.00

5.00

7.00

9.00

11.00

13.00

15.00

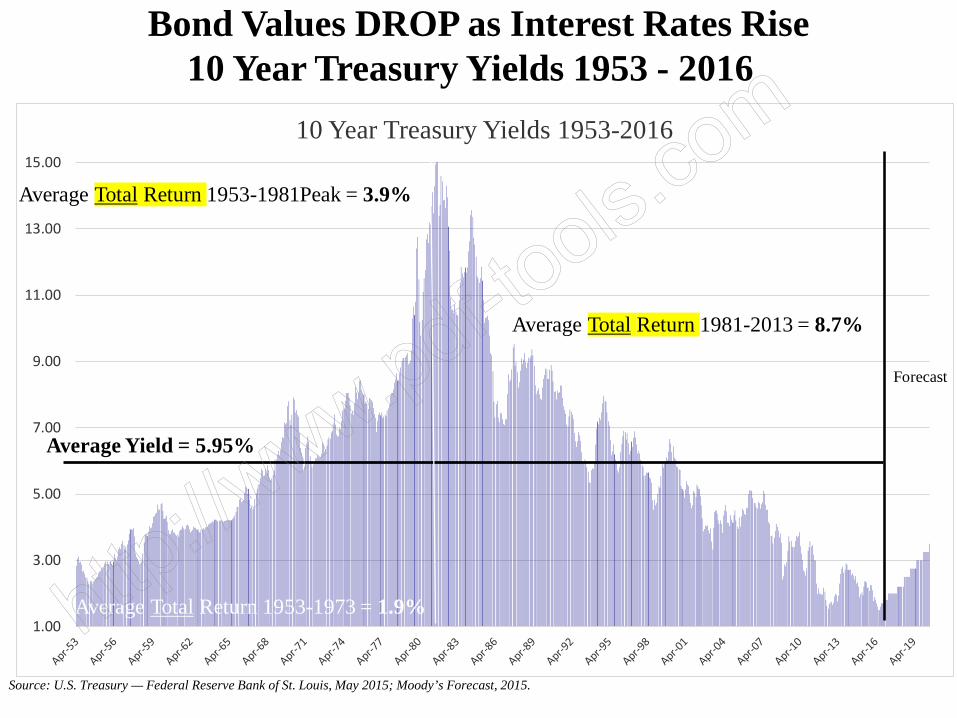

10 Year Treasury Yields 1953-2016

Source: U.S. Treasury — Federal Reserve Bank of St. Louis, May 2015; Moody’s Forecast, 2015.

Average Total Return 1981-2013 = 8.7%

Average Total Return 1953-1973 = 1.9%

Average Total Return 1953-1981Peak = 3.9%

Average Yield = 5.95%

Forecast

Bond Values DROP as Interest Rates Rise10 Year Treasury Yields 1953 - 2016e

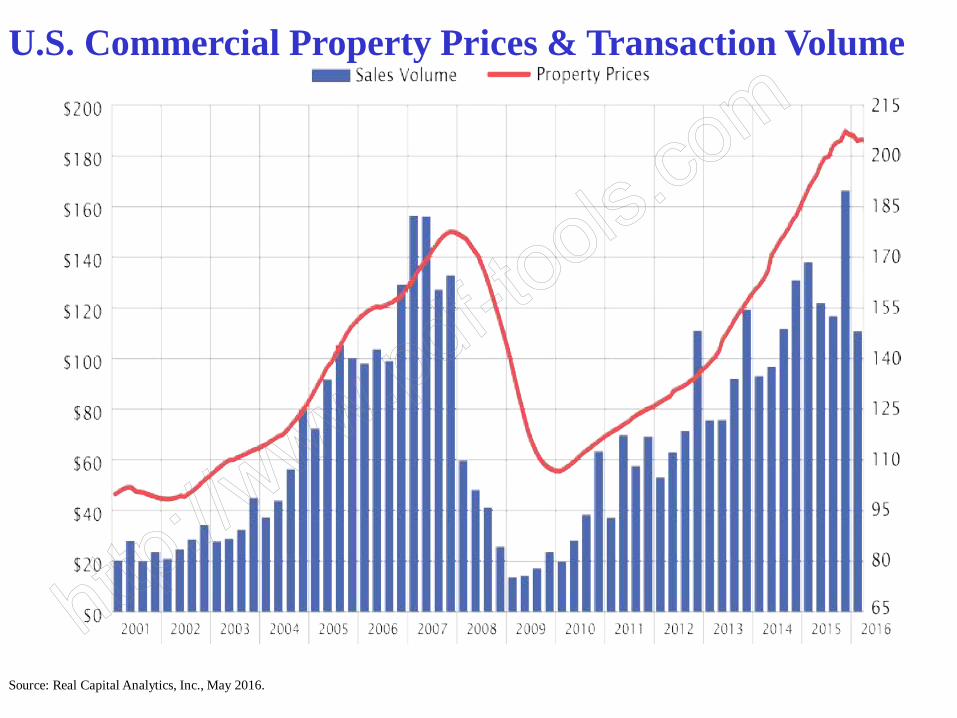

U.S. Commercial Property Prices & Transaction Volume

Source: Real Capital Analytics, Inc., May 2016.

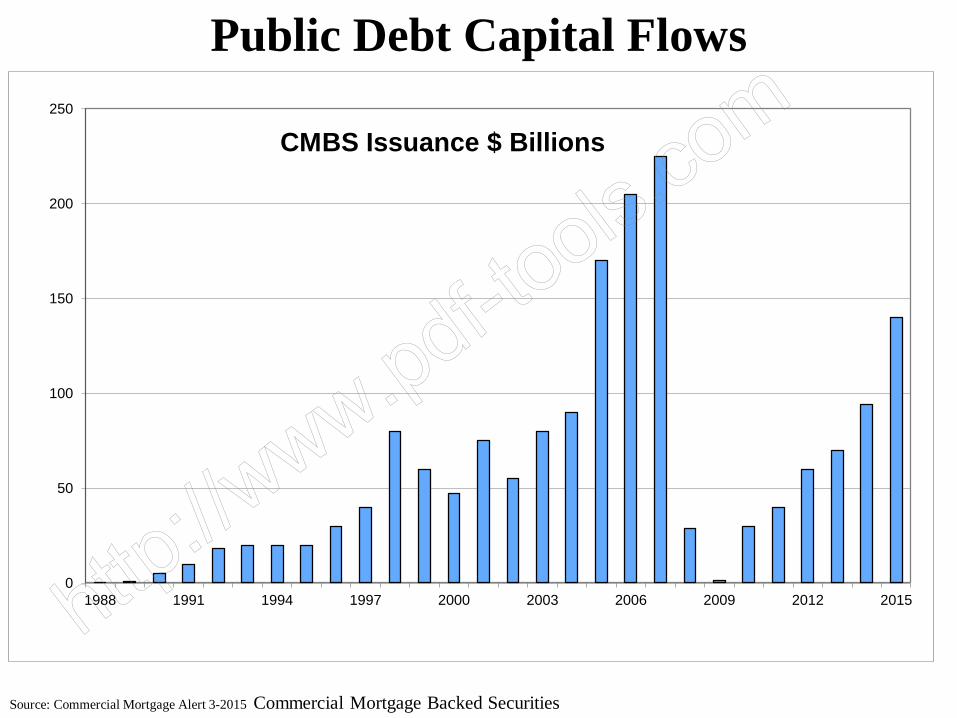

Source: Commercial Mortgage Alert 3-2015 Commercial Mortgage Backed Securities

Public Debt Capital Flows

0

50

100

150

200

250

1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

CMBS Issuance $ Billions

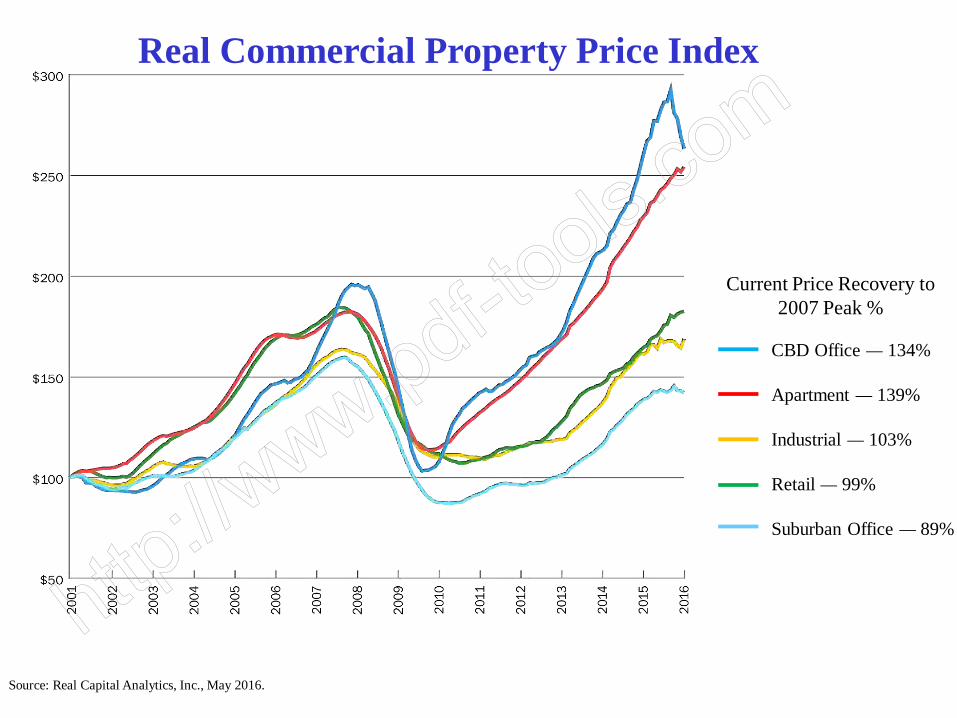

Real Commercial Property Price Index

Source: Real Capital Analytics, Inc., May 2016.

Current Price Recovery to 2007 Peak %

CBD Office — 134%

Apartment — 139%

Industrial — 103%

Retail — 99%

Suburban Office — 89%

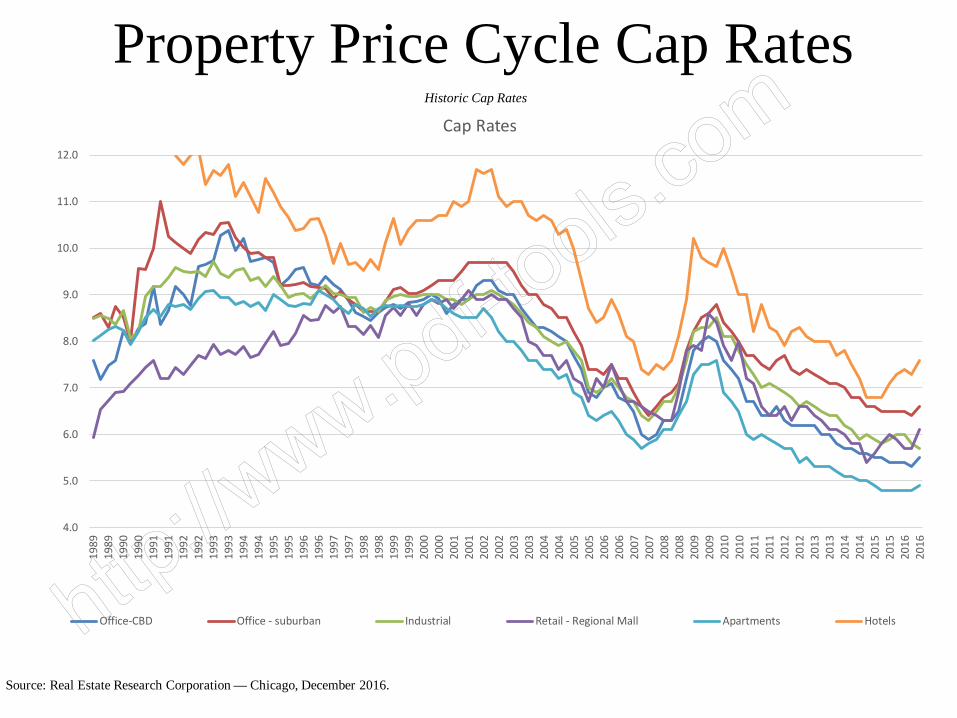

Property Price Cycle Cap RatesHistoric Cap Rates

Source: Real Estate Research Corporation — Chicago, December 2016.

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

1989

1989

1990

1990

1991

1991

1992

1992

1993

1993

1994

1994

1995

1995

1996

1996

1997

1997

1998

1998

1999

1999

2000

2000

2001

2001

2002

2002

2003

2003

2004

2004

2005

2005

2006

2006

2007

2007

2008

2008

2009

2009

2010

2010

2011

2011

2012

2012

2013

2013

2014

2014

2015

2015

2016

2016

Cap Rates

Office-CBD Office - suburban Industrial Retail - Regional Mall Apartments Hotels

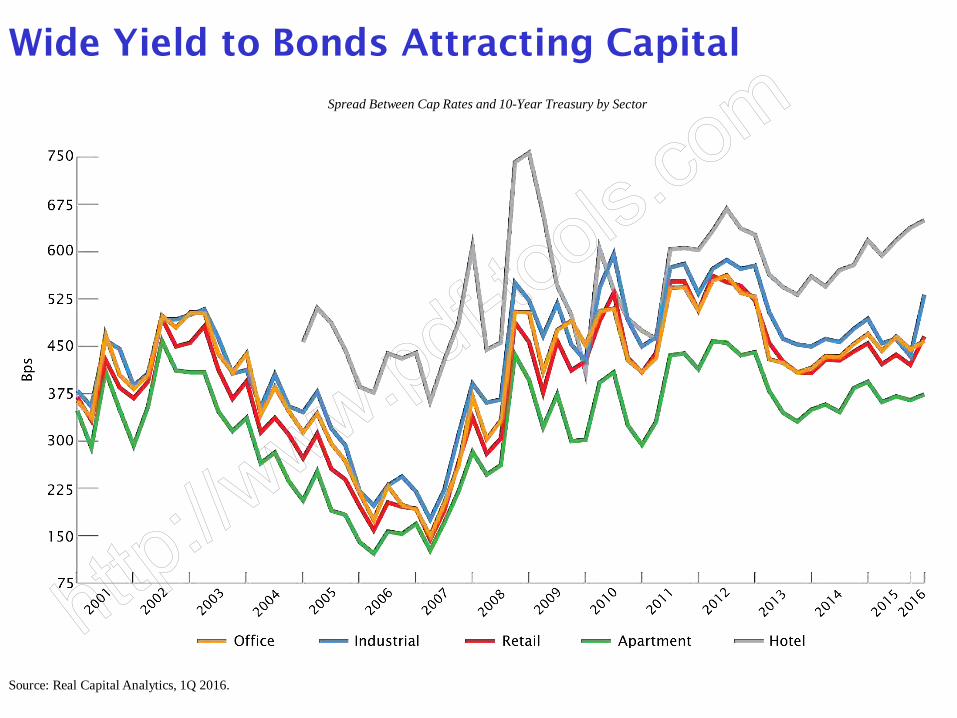

Wide Yield to Bonds Attracting CapitalSpread Between Cap Rates and 10-Year Treasury by Sector

Source: Real Capital Analytics, 1Q 2016.

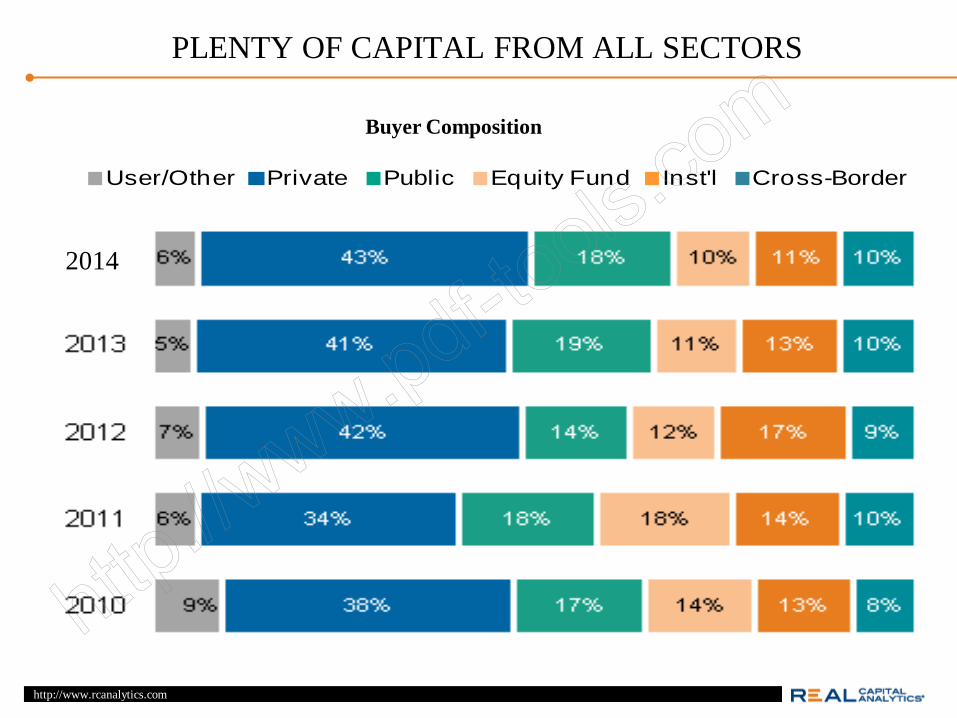

PLENTY OF CAPITAL FROM ALL SECTORS

Buyer Composition

User/Other Private Public Equity Fund Inst'l Cross-Border

http://www.rcanalytics.com

2014

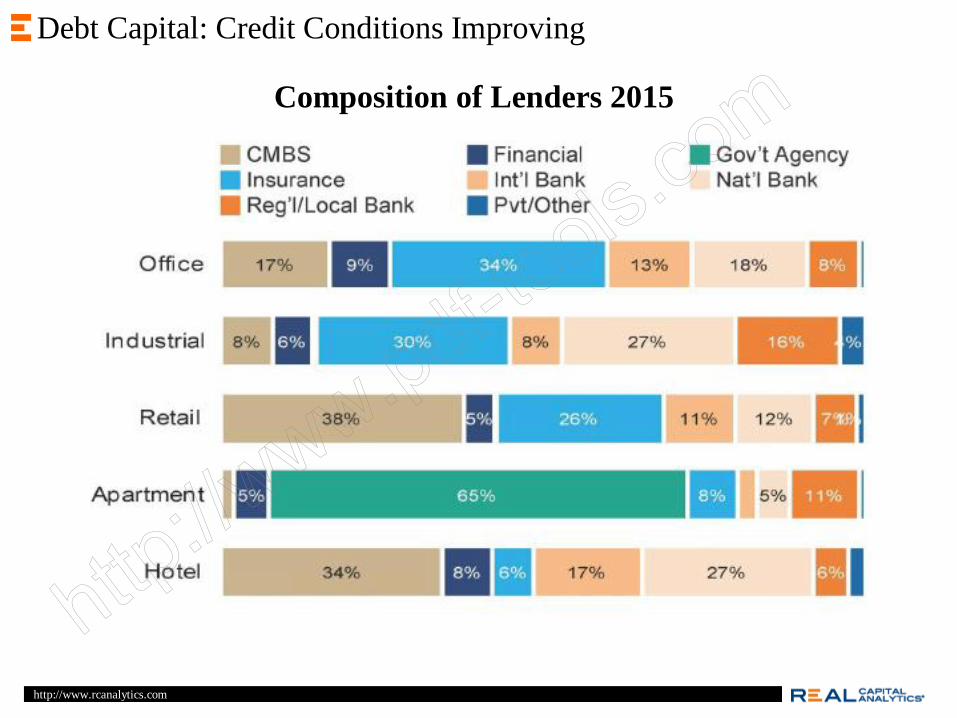

Composition of Lenders 2015

http://www.rcanalytics.com

Debt Capital: Credit Conditions Improving

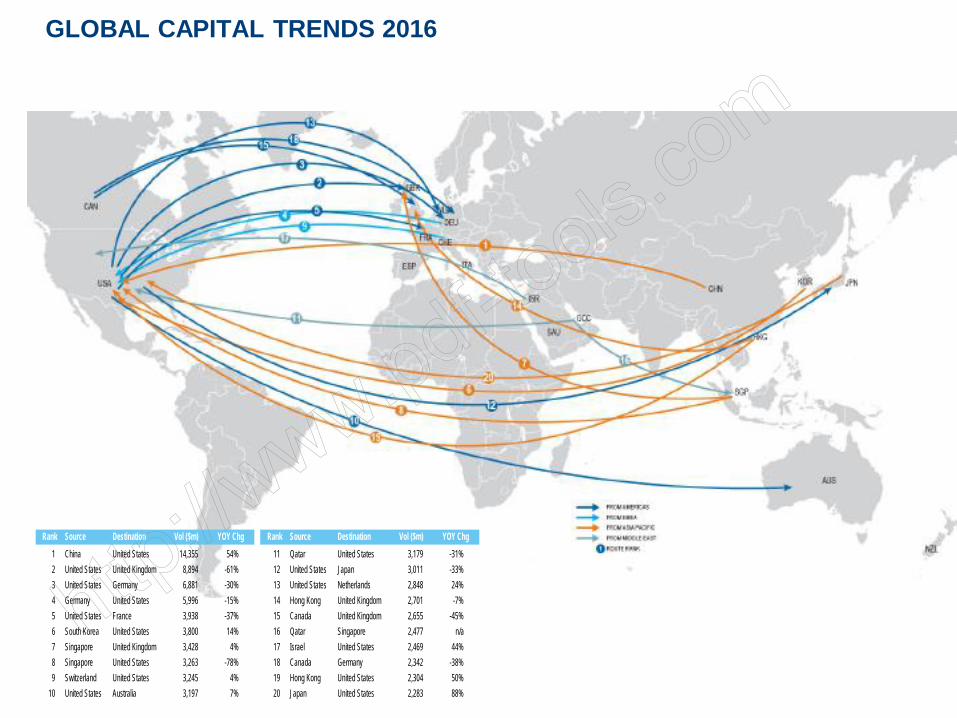

GLOBAL CAPITAL TRENDS 2016

Rank Source Destination Vol ($m) YOY Chg Rank Source Destination Vol ($m) YOY Chg1 China United States 14,355 54% 11 Qatar United States 3,179 -31%2 United States United Kingdom 8,894 -61% 12 United States Japan 3,011 -33%3 United States Germany 6,881 -30% 13 United States Netherlands 2,848 24%4 Germany United States 5,996 -15% 14 Hong Kong United Kingdom 2,701 -7%5 United States France 3,938 -37% 15 Canada United Kingdom 2,655 -45%6 South Korea United States 3,800 14% 16 Qatar Singapore 2,477 n/a7 Singapore United Kingdom 3,428 4% 17 Israel United States 2,469 44%8 Singapore United States 3,263 -78% 18 Canada Germany 2,342 -38%9 Switzerland United States 3,245 4% 19 Hong Kong United States 2,304 50%

10 United States Australia 3,197 7% 20 Japan United States 2,283 88%

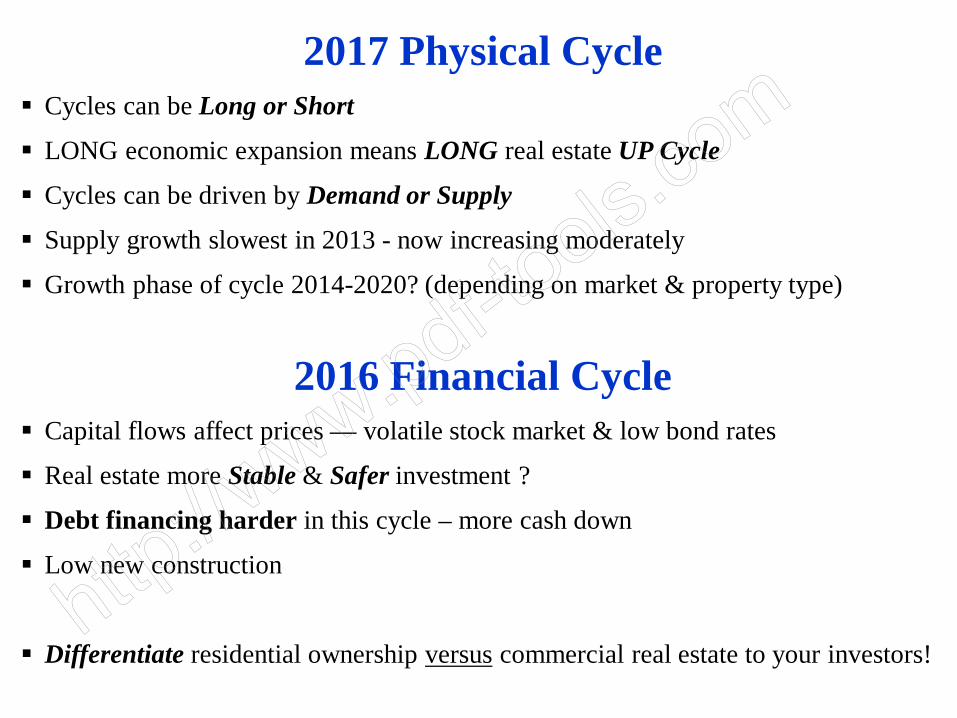

2008 Physical and Financial Cycle2017 Physical Cycle Cycles can be Long or Short

LONG economic expansion means LONG real estate UP Cycle

Cycles can be driven by Demand or Supply

Supply growth slowest in 2013 - now increasing moderately

Growth phase of cycle 2014-2020? (depending on market & property type)

2016 Financial Cycle Capital flows affect prices — volatile stock market & low bond rates

Real estate more Stable & Safer investment ?

Debt financing harder in this cycle – more cash down

Low new construction

Differentiate residential ownership versus commercial real estate to your investors!

QUESTIONS?

Topics Covered

Economic Fundamentals5 key Macro Economic Drivers of Real Estate PerformanceEconomic Base Analysis

Real Estate Physical Cycle FundamentalsDemand for Real Estate Supply of Real EstateOccupancy CyclesRent Cycles

Real Estate Financial Cycle FundamentalsInterest RatesCapital FlowsBuyersReal Estate PricesCap Rates

![Monetary Policy and Real Estate Prices: A Disaggregated ... · PDF fileReal Estate Prices: A Disaggregated Analysis for Switzerland ... Dupor [2005] analyzes in ... A Disaggregated](https://img.pdfslide.us/doc/110x75/5a79a5d87f8b9ae1468d0da8/monetary-policy-and-real-estate-prices-a-disaggregated-estate-prices-a-disaggregated.jpg)