Embed Size (px)

Citation preview

1

1

REAL ESTATE PROJECTS –

INTRODUCTION TO INCOME TAX

By

H Padamchand KhinchaB.Com, LLB, FCA

Chartered Accountant, Bangalore

&

Chythanya K.KB.Com, FCA, LLB

Advocate, Bangalore

2

Real estate projects

Some legislations having a bearing:

Stamp Act

Transfer of Property Act

Indian Easements Act

Income Tax Act

Accounting standards

FEMA – FDI Guidelines

Subject demands multi disciplinary approach

2

3

Discussion centres around

Characterization of asset

Characterization of income

Timing of income

Computation of income

4

Business income v. Capital Gains

If charged as long term capital gains, concessional rate of tax under section 112 would apply

Further, deduction under section 54, 54EC and 54F would be available

If charged as short term capital gains, normal rate of tax would apply and no incentives are available

If charged as business income, normal rate of tax would apply and provisions of sections 54, 54EC, 54F and section 112 are not applicable

However, section 50C and section 2(47) don’t apply

3

5

Business income v. Capital Gains

Tests for determination - Source

Draft Instructions of CBDT (2006)153 Taxman-St 9

CBDT Instruction No.1827 dated 31.08.1989

G.Venkata Swami Naidu & Co. v CIT (1959) 35 ITR 594

H. Mohammad & Co. v. CIT (1977) 177 ITR 637 Guj

Sarder Indra Singh & Sons v. CIT (1953) 24 ITR 415 SC

Karam Chand Thapar & Bros.V. CIT (1971) 83 ITR 899

CIT v. Rewashanker A Kothari (2006) 283 ITR 338 Guj

6

Tests for determination – Courts Whether initial acquisition was with intention of dealing in

the item, or with a view to finding an investment

Does transaction, since inception, appear to be impressedwith character of a Commercial transaction entered into with aview to earn profit

Why, how & for what purpose sale was effectedsubsequently

How assessee dealt with subject-matter of transactionduring the time the asset was with the assessee

Has it been treated as stock-in-trade, or has it been shown inthe books of account and balance sheet as an investment.This inquiry, though relevant, is not conclusive

4

7

Tests for determination – Courts• How assessee himself has returned income from such

activities and how Department has dealt with same in thecourse of preceding and succeeding assessments

This factor, though not conclusive, affords good & cogentevidence to judge the nature of transaction and is relevantto be considered in absence of any satisfactory explanation

• Whether partnership deed or MA authorizes such anactivity

• The most important test, is the volume, frequency,continuity and regularity of transactions of purchase andsale of the goods concerned

Where there is repetition and continuity, coupled with themagnitude of the transaction, an inference can be drawnthat the activity is in the nature of business

8

Single transaction – does it

constitute a business

• Yes as per

- CIT Vs S P Balasubramaniam 250 ITR 127 (Mad)

- CIT Vs Sutlet Cotton Mills Supply Agency Ltd 100 ITR

706 (SC)

• Not necessarily as per

- Indian Hume Pipe Co Ltd Vs CIT 195 ITR 386 (Bom)

- CIT Vs Shashikumar Agarwal 195 ITR 767 (All)

5

9

Conversion of capital asset into stock

in trade

• Such conversion is deemed as transfer–Sec 2(47)(iv)

• FMV on the date of conversion shall be deemed to befull value consideration for the purpose of section 48

• However, capital gains will be charged to tax in theprevious year in which such converted capital asset issold or otherwise transferred

• The time limit for investment under section 54EC etc ishowever with reference to date of deemed transfer andnot the date of actual sale. This position is mitigated byCircular No.791 of 2.6.2000

10

Conversion of capital asset into

stock in trade

• FMV on conversion will be cost to business as per CITv. Bai Shirinbai K. Kooka [1962] 46 ITR 86

• Need for such conversion

- To overcome provisions of section 50C

- To possibly claim certain expenses particularly when theasset is held for not more than 36 months

- To claim the set off of past unabsorbed business loss

6

11

Conversion of stock in trade into

capital asset

• Need for such change??

- To make use of brought forward capital loss

- To avail the concessional rate of tax applicable

to long term capital asset

• Practice is not recognised expressly in the Act

• Permissible if the circumstances justify

• Risk of courts treating the above as a

colourable device

12

Conversion of stock in trade into

capital asset

• No tax upon such conversion in the absence ofdeeming provision - CIT v.Sir Kika Bhai Premchand[1953] 24 ITR 506 [SC]

7

13

Conversion of stock in trade into

capital asset• Upon sale, chargeable to tax as capital gains as

nature of capital asset should be determined on thedate of transfer and not on the date of acquisition asper Nachiappan [M] v. CIT [1998] 230 ITR 98 Mad.

• For computing capital gains – actual cost should betaken and not the converted costs as per

- Ranchhodbhai Bhaijibhai Patel vs. CIT (1971) 81 ITR446 [Guj.]

- CIT vs. M. Ramaiah Reddy (1986) 158 ITR 611 (Kar)

- CIT vs. Vishwanath (1993) 201 ITR 920 (All)

- Keshavji Karsondas vs. CIT (1994) 207 ITR 737 (Bby)

14

Capital asset – short term or

long term

Normal case :

Short term : Period of holding </= 36 months

Long term : Period of holding > 36 months

Special case : Circumstances listed in

section 49(1)

8

15

Tax rates

Short term capital gains : Will be part of

common hotch pot and normal slab rate

will apply

Long term capital gains : Normal case –

20% flat

Business income : Will be part of

common hotch pot and normal slab rate

will apply

16

Joint Development

The Partners :

– Developer

– Co developer

– Land owner

9

17

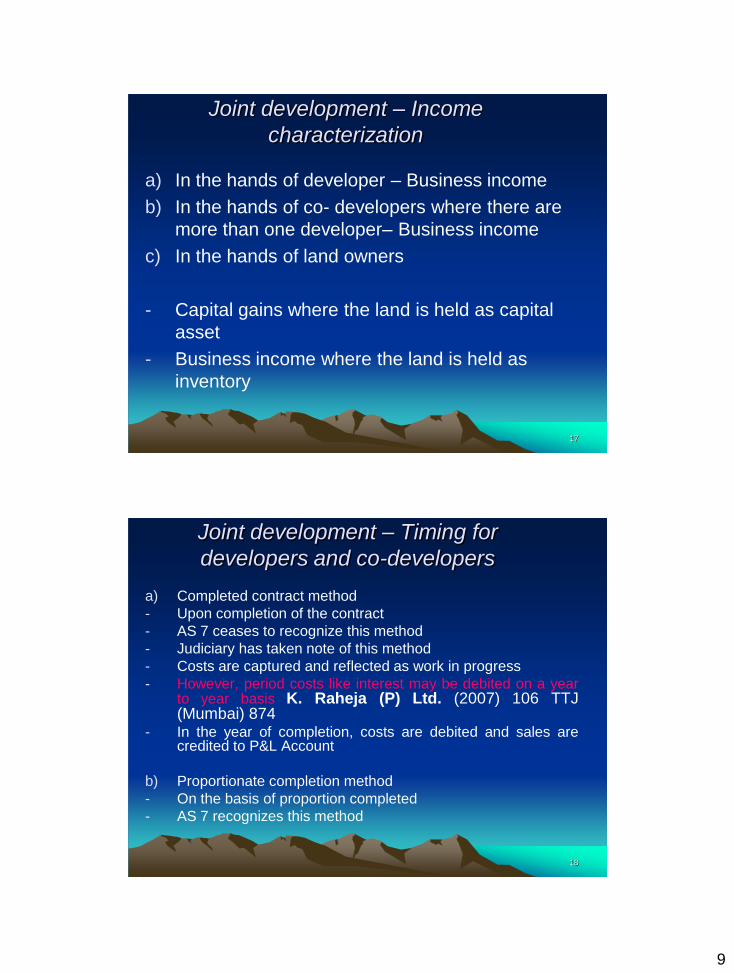

Joint development – Income

characterization

a) In the hands of developer – Business income

b) In the hands of co- developers where there are

more than one developer– Business income

c) In the hands of land owners

- Capital gains where the land is held as capital

asset

- Business income where the land is held as

inventory

18

Joint development – Timing for

developers and co-developers

a) Completed contract method

- Upon completion of the contract

- AS 7 ceases to recognize this method

- Judiciary has taken note of this method

- Costs are captured and reflected as work in progress

- However, period costs like interest may be debited on a yearto year basis K. Raheja (P) Ltd. (2007) 106 TTJ(Mumbai) 874

- In the year of completion, costs are debited and sales arecredited to P&L Account

b) Proportionate completion method

- On the basis of proportion completed

- AS 7 recognizes this method

10

19

Joint development – Timing for Land owner

a) Where held as a capital asset

- In the year of transfer

- Method of accounting is not relevant

- Transfer is as per section 2(47)

- Applicability of section 53A of TP Act

b) Where held as a business asset

- In the year of sale

- Method of accounting, cash/accrual, will decide the year of tax

- Extended meaning of transfer as per section 2(47) is not applicable

20

Joint Development – Issues for discussion

Whether joint development word is appropriate? Does it create an AOP

Amendment to section 53A of Transfer of Property Act -Relevance

Whether possession to developer tantamounts to a transfer under section 2(47)

Whether role of developer to be legally segregated into a contractor and a seller?

If transfer is completed on possession, whether charge could fail in view of impossibility of computation of gains

Feasibility of converting capital asset into stock in trade

11

21

Contribution of land into firm

Contribution at cost / indexed cost

Contribution to be oral (and by intent) to a mitigate stamp duty incidence

After contribution, terms of partnership as orally agreed may be recorded

Revaluation of land thereafter

Changes in partners / their ratio to achieve desired objective

Stamp duty implications to be separately monitored

22

Issues

Whether revaluation can be effected immediately after contribution

Whether revaluation is a taxable event

Whether settlement of retiring partner paying him in excess of capital contribution is a taxable event

12

23

Conversion of firm into Company

Firm converted into Company under Part IX of Companies Act

Company to allot shares

Provisions of 47(xiii) to be complied with as a back-up plan

24

Issues for discussion

Whether the Company can adopt the “stepped up” cost for computing gains on subsequent sale

Whether capital of partner before conversion but after revaluation could be split into capital and loan

Whether shares could be allotted only to the extent of capital, leaving the loan free for withdrawal

13

25

Tax incentives

a) Infrastructure – sec 80IA(4)(i)

b) Industrial parks – sec 80IA(4)(iii)

c) Housing projects – sec 80IB(10)

d) SEZ development – sec 80IAB

e) WB’s aided housing project – sec 80HHBA

26

IT BENEFITS to SEZ - SUMMARY

PERSON SECTION INCOME

Developer & Co-developer

80 IAB , 115 O Development Income

SEZ Authority 80 IAB, 115 O ..Do..

Infrastructure cap Fund/Company or Co-op society

10 (23G) Dividend, Interest and Long term capital gains

Entrepreneur 10 AA / 54 GA Business Income

Off shore banking unit (OBU)

80 LA, 197 A (1D) Interest

NR /NOR 10 (15) (viii) Interest On Deposit

IFSC 80 LA Interest

Non Resident 26(1)(f) of SEZ Act Security Transaction

Investor In Shares 115 (O) (6), 10(34) Dividend Income

14

27

Issues

Completed contract method no longer being a recognised method as per AS, can proportionate completion method be imposed by the AO?

Where a project runs for several years and assessee has adopted project completion method and same was accepted by department, can AO impose percentage completion method for later years? No as per Bakshi Vikram P Ltd (2007) 158 TAXMAN ITAT (61) NEW DELHI & Vishal Infrastructure Ltd (2007) 104 ITD 537 Hyd.

28

IssuesCan the AO disturb the book profits for thepurpose of section 115JB on the basis ofqualified accounts where completed contractmethod was adopted?

Is treating land as capital asset andconstruction as inventory and therebyaffording different treatment permissible?See Chandrika Tower’s in 275 ITR 173 (MP)

Taxation of retention money – Timing?

Adjustment of security deposit in case of pastcontract against current bill – Allowability?

15

29

Issues – 44AD

Is sub contractor covered? Yes as per Manohar Ram Chandra Patil v. UOI 133 Taxman 792 (Ori.)

Is an interior decorator covered? No as per Sanjay Kataria (2004) TAXMAN ITAT 141 63 (Delhi)

Is addition u/s 69 etc permissible where section 44AD is applied? Yes as per Devisingh Solanki [2006] 99 TTJ [Jp] 890

30

Issues – 44AD

Belated filing of audit report may entail penalty but there is no denial of benefit of section 44AD as per LEYLAND AUTOMOBILES (2007) 105 ITD 73 (COCHIN)

When taxed under this section, income from sale of scrap etc should not be taxed again as per MOHD. ASLAM [2006] 150 TAXMAN – ITAT 20 [JODH.] [2005] 94 TTJ [Jd] 282

FDR interest income does not qualify to be assessed under this section as per ALLIED CONSTRUCTION (2007) 105 ITD 1 (DELHI) (SB)

Presumed income is not book profit for the purpose of sec 40b as per Parul Toys (2007) 105 ITD 81(HYD.)

16

31