Embed Size (px)

Citation preview

CompanyPresentation

March 2021

Disclaimer

2

Important noticeThis presentation (the “Presentation”) has been prepared by HeliosTowers plc (the “Company”) for information purposes only. As arecipient of this Presentation, you: (i) will be deemed to haveagreed to the obligations and restrictions set out below; and (ii)represent and warrant that you are duly authorised to receive thisPresentation.The distribution of this document in certain jurisdictions may berestricted by law and persons into whose possession thisPresentation comes should inform themselves about, and observe,any such restrictions. References in this notice to the“Presentation” shall be deemed to include any other materials orinformation given or distributed to you by or on behalf of theCompany in connection with this Presentation, whether before,during or after this Presentation and whether given or distributedorally, in writing or otherwise.No investment adviceThis Presentation does not constitute or form part of, and shouldnot be construed as, an offer, invitation or inducement orrecommendation to purchase or subscribe for any securities in theCompany or any of its affiliates or subsidiaries (together the“Group”) in any jurisdiction nor should it or any part of it form thebasis of, or be relied on in connection with, any contract topurchase or subscribe for any securities of the Company or anymember of its group or with any other contract or commitmentwhatsoever.Further, it should not be treated as giving investment, legal,accounting, regulatory, taxation or other advice and recipientsshould each make their own evaluation of the Company and ofthe relevance and adequacy of the information containedherein.No warrantyNo representations or warranties, express or implied are given in,or in respect of, this Presentation. To the fullest extent permitted bylaw, in no circumstances will the Company, or any of its respectivesubsidiaries, shareholders, affiliates, representatives, partners,directors, officers, employees, advisers or agents be responsible orliable for any direct, indirect or consequential loss, loss of profit,damages or costs arising from the use of this Presentation, itscontents, its omissions, reliance on the information containedwithin it, or on opinions communicated in relation thereto orotherwise arising in connection therewith. The informationcontained in this Presentation has not been independentlyverified.

Third party sourcesCertain statistical and other information about the Company, itsaffiliates, the industry and the market where the Group operatesincluded in this Presentation is sourced from publicly availablethird party sources. Third-party industry publications, studies andsurveys generally state that the data therein have been obtainedfrom sources believed to be reliable, but that there is noguarantee of the fairness, quality, accuracy, relevance,completeness or sufficiency of such data. As such it presents theviews of those third parties, but may not necessarily correspond tothe views held by the Company or its Representatives and theCompany expressly disclaims any responsibility for, or liability inrespect of, such information.Such research and estimates, and their underlying methodologyand assumptions, have not been verified by any independentsource for accuracy or completeness and are subject to changewithout notice. Accordingly, undue reliance should not be placedon any of the industry or market data contained in thisPresentation.Forward-looking statementsThis Presentation contains illustrative returns, projections, estimatesand beliefs and similar information (together, “Forward LookingStatements”). The Forward Looking Statements can be identifiedby the use of forward looking terminology, including the terms“believes”, “estimates”, “anticipates”, “expects”, “intends”,“plans”, “may”, “will” or “should” or, in each case, their negativeor other variations or comparable terminology.The Forward Looking Statements are subject to inherentuncertainties and qualifications and are based on numerousassumptions, in each case whether or not identified in thePresentation. The Forward Looking Statements are provided forillustrative purposes only and are not intended to serve as, andmust not be relied upon by any investor as a guarantee, anassurance, a prediction or a definitive statement of fact orprobability.Nothing in this Presentation should be construed as a profitforecast. Actual events and circumstances are difficult orimpossible to predict and will differ from assumptions. Manyactual events and circumstances are beyond the control of theCompany. Some important factors that could cause actualresults to differ materially from those in any Forward LookingStatements could include changes in domestic and foreignbusiness, market, financial, political and legal conditions. Therecan be no assurance that any particular Forward LookingStatements will be realised, and the performance of the Companymay be materially and adversely different from the ForwardLooking Statements. The Forward Looking Statements speak only

as of the date of this Presentation. The Company expresslydisclaims any obligation or undertaking to release any updates orrevisions to any Forward Looking Statements to reflect any changein the Company’s expectations with regard thereto or anychanges in events, conditions or circumstances on which anyForward Looking Statements are based. Accordingly, no relianceshould be placed upon the Forward Looking Statements.Other important remarksThe Presentation contains financial information regarding theGroup. Such financial information may not have been audited,reviewed or verified by any independent accounting firm. Inparticular, the preliminary results for FY 2020 in this presentationhave not been audited or reviewed. The Group’s audited resultscould vary from the preliminary results presented herein.The inclusion of such financial information in the Presentationshould not be regarded as a representation or warranty by theGroup or any Representatives as to the accuracy orcompleteness of such information’s portrayal of the financialposition or results of operations of the Group. In addition, thisPresentation contains certain unaudited pro forma and asadjusted financial information. The Group’s auditors have notperformed any procedures with respect to such unaudited proforma and as adjusted financial information for the purpose ofinclusion herein and accordingly, they have not expressed anopinion or provided any form of assurance with respect thereto. Inaddition, although we believe the unaudited financial informationto be reasonable, our actual results may vary from the informationcontained herein and such variations could be material. As such,you should not place undue reliance on the inclusion of suchunaudited financial information and it should not be regarded asan indication that it will be an accurate prediction of futureevents.Furthermore, certain financial data included in the Presentationconsists of “non-IFRS financial measures”, which may not becomparable to similarly-titled measures as presented by othercompanies, nor should they be considered as an alternative tothe historical financial results or other indicators of the Group’scash flow based on IFRS. You are cautioned not to place unduereliance on any non-IFRS financial measures and ratios includedherein.

Agenda

• Investment thesis

1) A Leading Independent Tower Company

2) Structurally Attractive Markets

3) Highly Visible Revenue Stream with FX and Cost Inflation Protection

4) Experienced Management Team and Board of Directors

• FY 2020 update

3

1

3

2

4

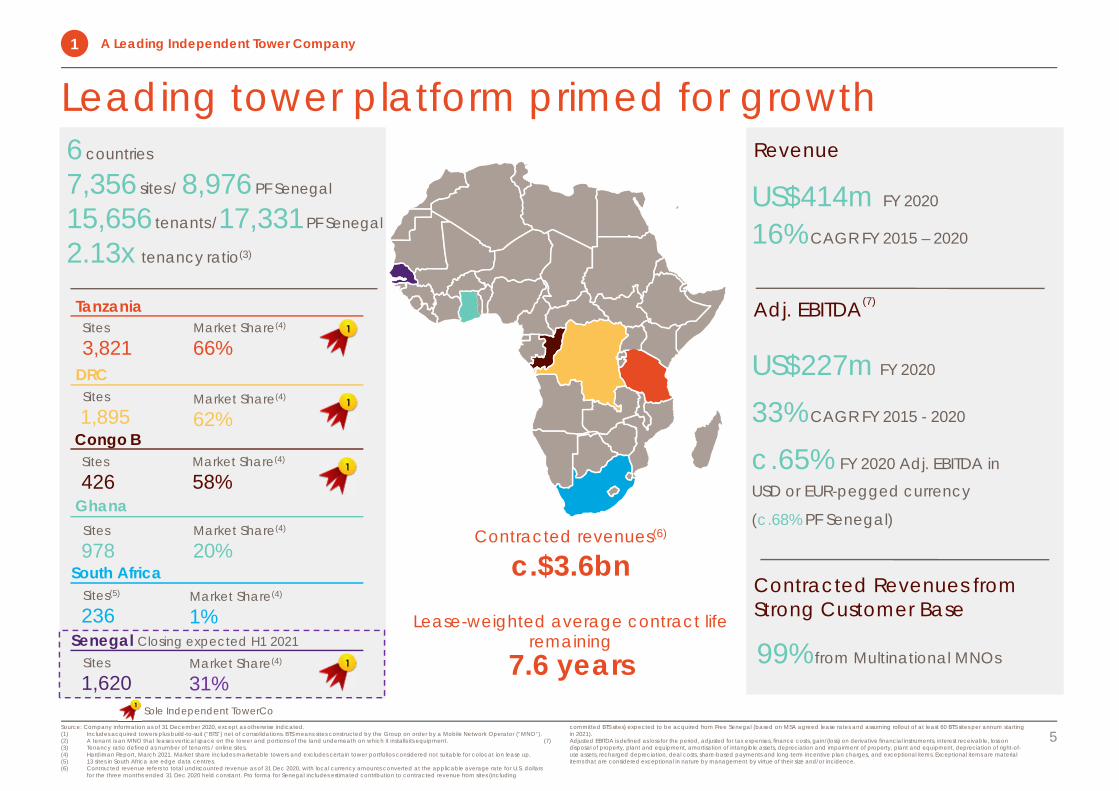

A Leading Independent Tower Company

1

6 countries

7,356 sites/ 8,976 PF Senegal

15,656tenants/17,331PF Senegal

2.13x tenancy ratio(3)

Senegal Closing expected H1 2021

Leading tower platform primed for growth

5

Sole Independent TowerCo

TanzaniaSites

3,821DRCSites

1,895Congo BSites

426

Sites

978

Ghana

Market Share(4)

66%

Market Share(4)

62%

Market Share(4)

58%

Market Share(4)

20%Contracted revenues(6)

c.$3.6bn

Lease-weighted average contract life remaining

7.6 years

South Africa

US$414m FY 2020

16% CAGR FY 2015 – 2020

99% from Multinational MNOs

US$227m FY 2020

33% CAGR FY 2015 - 2020

c.65% FY 2020 Adj. EBITDA in

USD or EUR-pegged currency

(c.68% PF Senegal)

Revenue

Contracted Revenues from Strong Customer Base

(7)Adj. EBITDA

Source: Company information as of 31 December 2020, except as otherwise indicated.(1) Includes acquired towers plus build-to-suit (“BTS”) net of consolidations. BTS means sites constructed by the Group on order by a Mobile Network Operator (“MNO”).(2) A tenant is an MNO that leases vertical space on the tower and portions of the land underneath on which it installs its equipment.(3) Tenancy ratio defined as number of tenants / online sites.(4) Hardiman Report, March 2021. Market share includes marketable towers and excludes certain tower portfolios considered not suitable for colocat ion lease up.(5) 13 sites in South Africa are edge data centres.(6) Contracted revenue refers to total undiscounted revenue as of 31 Dec 2020, with local currency amounts converted at the applicable average rate for U.S. dollars

for the three months ended 31 Dec 2020 held constant. Pro forma for Senegal includes estimated contribution to contracted revenue from sites (including

committed BTS sites) expected to be acquired from Free Senegal (based on MSA agreed lease rates and assuming rollout of at least 60 BTS sites per annum starting in 2021).

(7) Adjusted EBITDA is defined as loss for the period, adjusted for tax expenses, finance costs, gain/(loss) on derivative financial instruments, interest receivable, loss on disposal of property, plant and equipment, amortisation of intangible assets, depreciation and impairment of property, plant and equipment, depreciation of right-of-use assets, recharged depreciation, deal costs, share-based payments and long-term incentive plan charges, and exceptional items. Exceptional items are material items that are considered exceptional in nature by management by virtue of their size and/or incidence.

A Leading Independent Tower Company1

Sites(5)

236

Sites

1,620

Market Share(4)

1%

Market Share(4)

31%

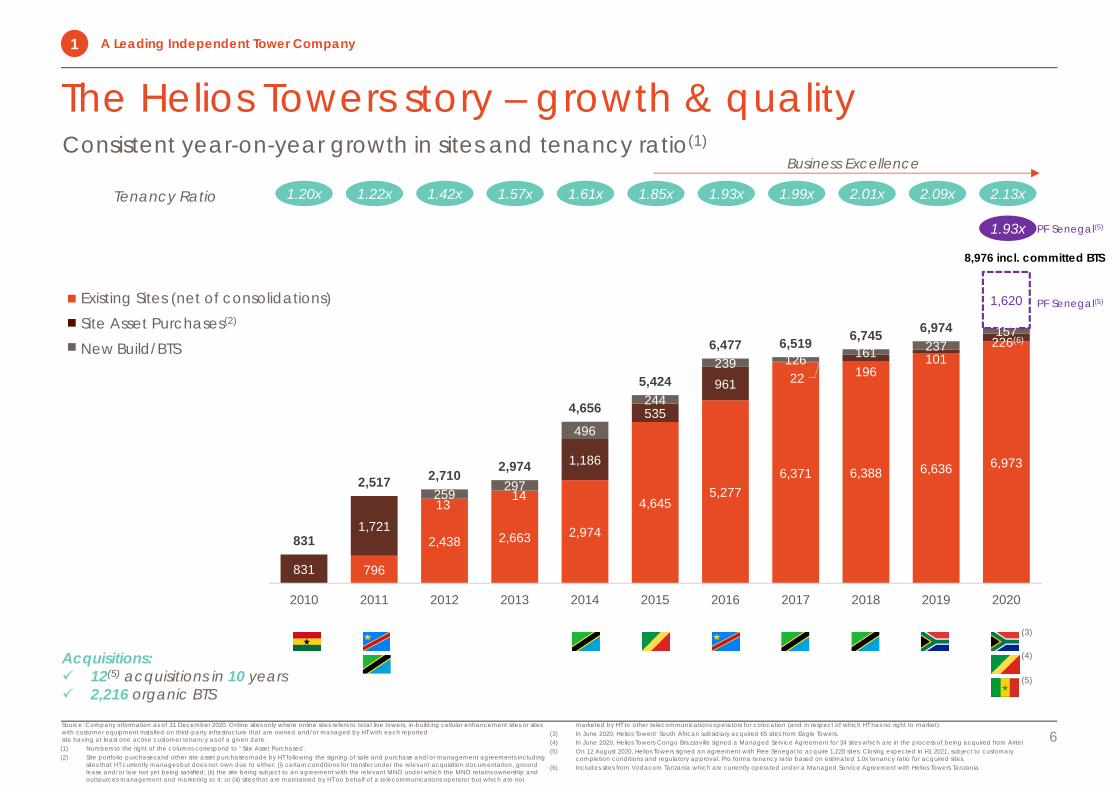

-796

2,438 2,663 2,974

4,6455,277

6,371 6,388 6,636 6,973

831

1,72113

14

1,186

535

961 22 196101

226(6)

259 297

496

244

239 126 161 237157

1,620

831

2,517 2,710 2,974

4,656

5,424

6,477 6,519 6,745 6,974

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Company information as of 31 December 2020. Online sites only where online sites refers to total live towers, in-building cellular enhancement sites or sites with customer equipment installed on third-party infrastructure that are owned and/or managed by HT with each reported site having at least one active customer tenancy as of a given date.(1) Numbers to the right of the columns correspond to “Site Asset Purchases”.(2) Site portfolio purchases and other site asset purchases made by HT following the signing of sale and purchase and/or management agreements including

sites that HT currently manages but does not own due to either: (i) certain conditions for transfer under the relevant acquisition documentation, ground lease and/or law not yet being satisfied; (ii) the site being subject to an agreement with the relevant MNO under which the MNO retains ownership and outsources management and marketing to it; or (iii) sites that are maintained by HT on behalf of a telecommunications operator but which are not

marketed by HT to other telecommunications operators for colocation (and in respect of which HT has no right to market).(3) In June 2020, Helios Towers’ South African subsidiary acquired 65 sites from Eagle Towers.(4) In June 2020, Helios Towers Congo Brazzaville signed a Managed Service Agreement for 34 sites which are in the process of being acquired from Airtel(5) On 12 August 2020, Helios Towers signed an agreement with Free Senegal to acquire 1,220 sites. Closing expected in H1 2021, subject to customary

completion conditions and regulatory approval. Pro forma tenancy ratio based on estimated 1.0x tenancy ratio for acquired sites.(6) Includes sites from Vodacom Tanzania which are currently operated under a Managed Service Agreement with Helios Towers Tanzania.

Existing Sites (net of consolidations)Site Asset Purchases(2)

New Build/BTS

Consistent year-on-year growth in sites and tenancy ratio(1)

6

Acquisitions: 12(5) acquisitions in 10 years 2,216 organic BTS

Tenancy Ratio

Business Excellence

A Leading Independent Tower Company1

1.20x 1.22x 1.42x 1.57x 1.61x 1.93x 1.99x1.85x 2.01x 2.09x 2.13x

1.93x

(3)

(4)

(5)

PF Senegal(5)

PF Senegal(5)

8,976 incl. committed BTS

The Helios Towers story – growth & quality

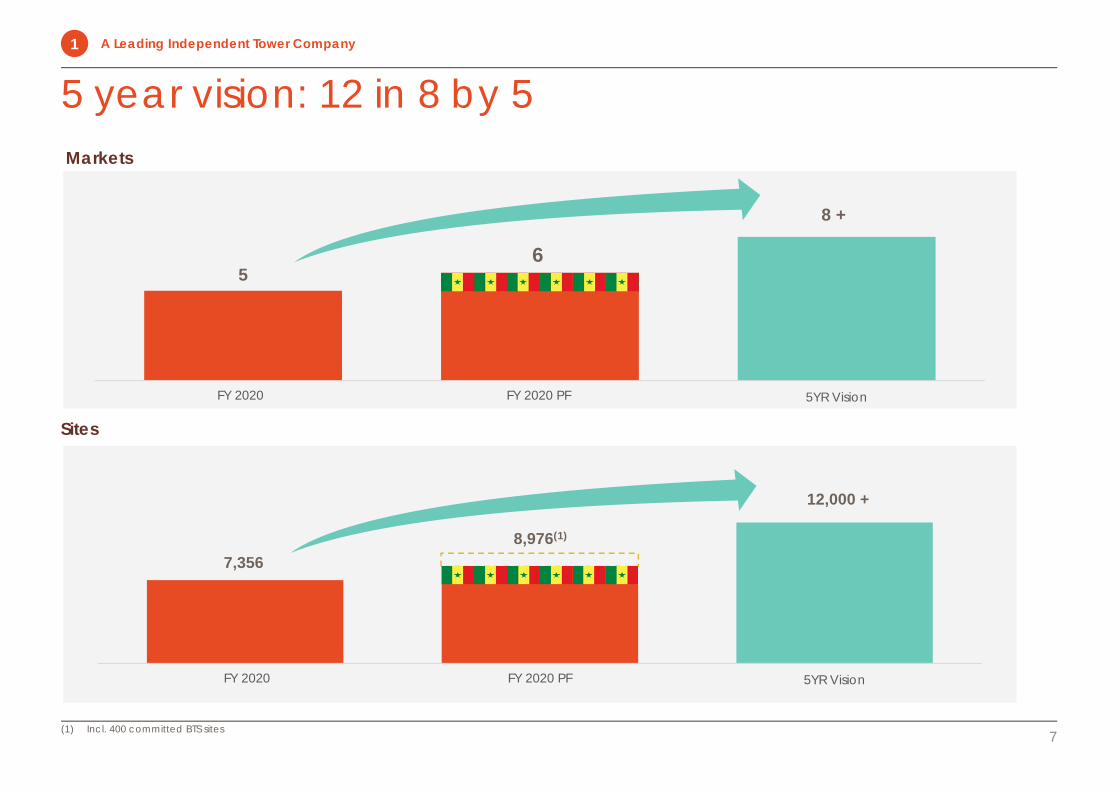

5 year vision: 12 in 8 by 5

7

5

8 +

Q2 20 Q2 20 PF 5YR Vision

Sites

Markets

6

7,3568,976(1)

12,000 +

Q2 20 Q2 20 PF 5YR Vision

(1) Incl. 400 committed BTS sites

A Leading Independent Tower Company1

FY 2020 PF

FY 2020 PFFY 2020

FY 2020

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19 Q4 19 Q1 20 Q2 20 Q3 20 Q4 20

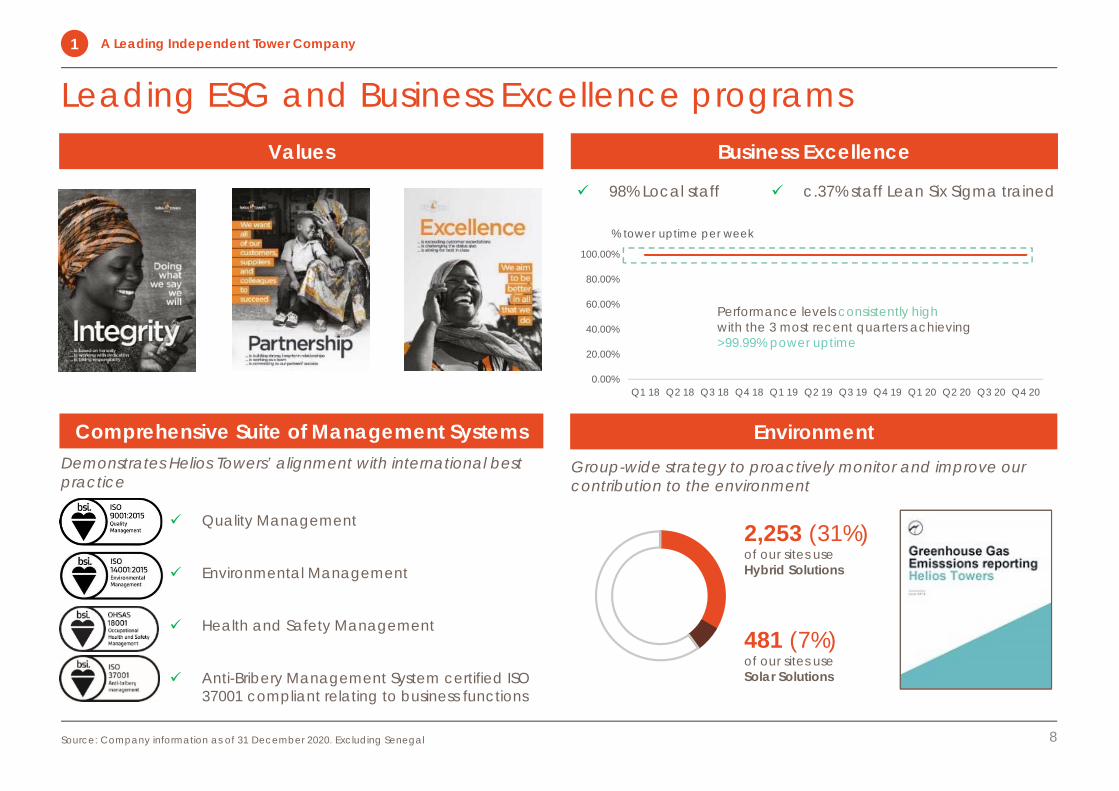

Leading ESG and Business Excellence programs

8Source: Company information as of 31 December 2020. Excluding Senegal

Business Excellence

Comprehensive Suite of Management Systems

Values

Demonstrates Helios Towers’ alignment with international best practice

EnvironmentGroup-wide strategy to proactively monitor and improve our contribution to the environment

Quality Management

Environmental Management

Health and Safety Management

Anti-Bribery Management System certified ISO 37001 compliant relating to business functions

A Leading Independent Tower Company1

98% Local staff

% tower uptime per week

Performance levels consistently highwith the 3 most recent quarters achieving >99.99% power uptime

c.37% staff Lean Six Sigma trained

2,253 (31%)of our sites use Hybrid Solutions

481 (7%)of our sites use Solar Solutions

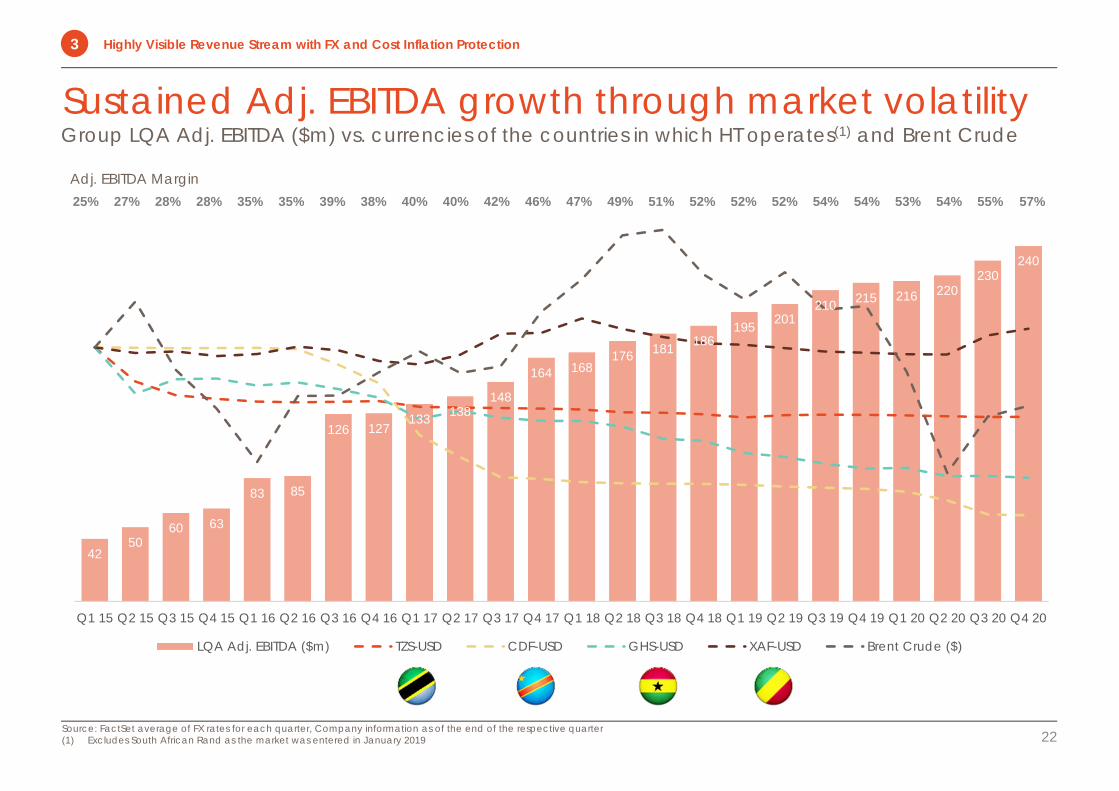

42 50 60 63 83 85

126 127 133 138 148 164 168 176 181 186 195 201 210 215 216 220 230 240

25%27% 28% 28%

35% 35%39% 38% 40% 40%

42%46% 47%

49% 51% 52% 52% 52%54% 54% 53% 54% 55% 57%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

(40)

10

60

110

160

210

260

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19 Q4 19 Q1 20 Q2 20 Q3 20 Q4 20

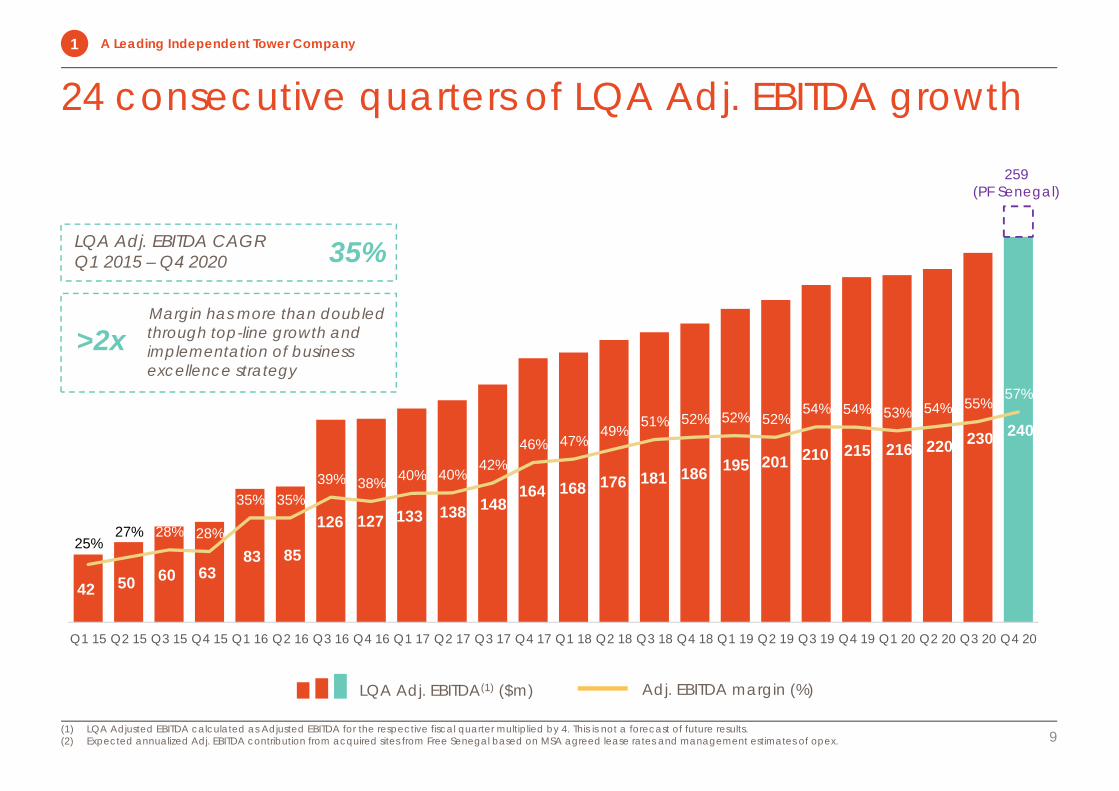

24 consecutive quarters of LQA Adj. EBITDA growth

9(1) LQA Adjusted EBITDA calculated as Adjusted EBITDA for the respective fiscal quarter multiplied by 4. This is not a forecast of future results.(2) Expected annualized Adj. EBITDA contribution from acquired sites from Free Senegal based on MSA agreed lease rates and management estimates of opex.

A Leading Independent Tower Company1

LQA Adj. EBITDA CAGR Q1 2015 – Q4 2020 35%

Margin has more than doubled through top-line growth and implementation of business excellence strategy

>2x

Adj. EBITDA margin (%)LQA Adj. EBITDA(1) ($m)

259 (PF Senegal)

Structurally Attractive Markets for Organic and Inorganic Growth

2

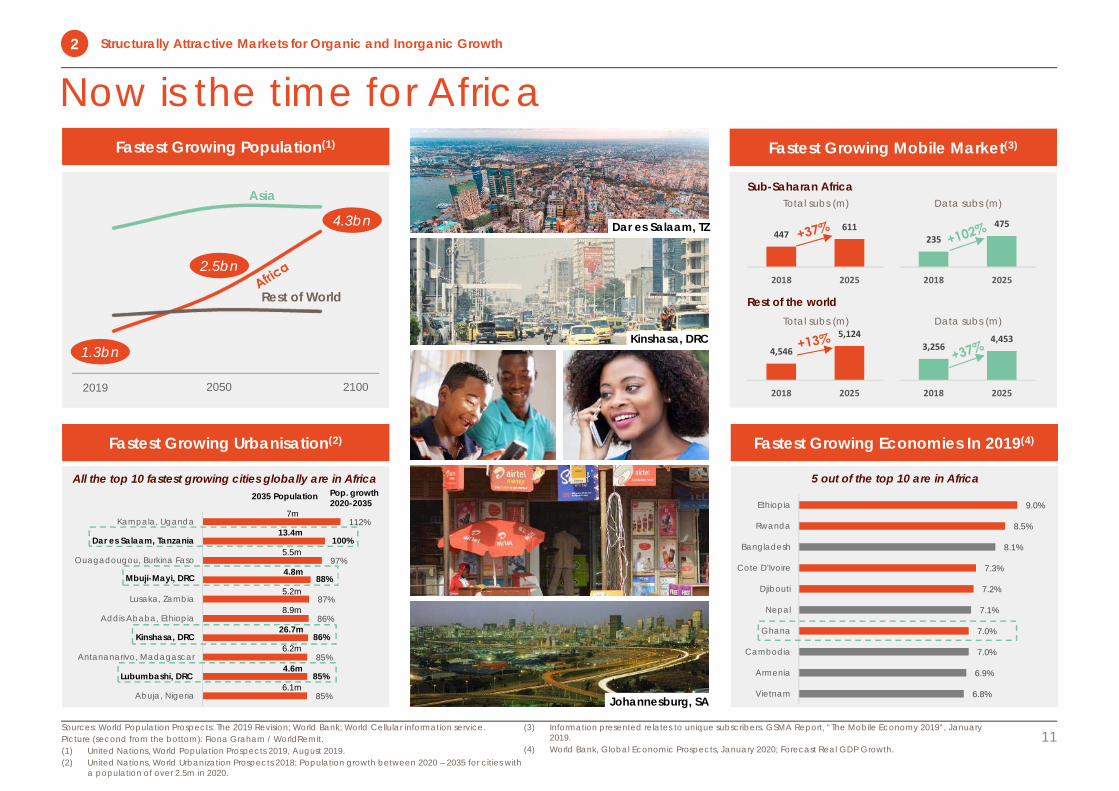

Now is the time for Africa

11Sources: World Population Prospects: The 2019 Revision; World Bank; World Cellular information service.Picture (second from the bottom): Fiona Graham / WorldRemit.(1) United Nations, World Population Prospects 2019, August 2019.(2) United Nations, World Urbanization Prospects 2018; Population growth between 2020 – 2035 for cities with

a population of over 2.5m in 2020.

(3) Information presented relates to unique subscribers. GSMA Report, “The Mobile Economy 2019”, January 2019.

(4) World Bank, Global Economic Prospects, January 2020; Forecast Real GDP Growth.

5 out of the top 10 are in Africa

4.3bn

1.3bn

Fastest Growing Population(1)

Rest of World

4,546

5,124

2018 2025

3,2564,453

2018 2025

Fastest Growing Urbanisation(2) Fastest Growing Economies In 2019(4)

Fastest Growing Mobile Market(3)

2.5bn

Sub-Saharan Africa

Rest of the world

2019 2050 2100

Total subs (m) Data subs (m)

Kinshasa, DRC

Dar es Salaam, TZ

Johannesburg, SA

9.0%

8.5%

8.1%

7.3%

7.2%

7.1%

7.0%

7.0%

6.9%

6.8%

Ethiopia

Rwanda

Bangladesh

Cote D'Ivoire

Djibouti

Nepal

Ghana

Cambodia

Armenia

Vietnam

All the top 10 fastest growing cities globally are in AfricaPop. growth 2020-2035

2035 Population

85%

85%

85%

86%

86%

87%

88%

97%

100%

112%

Abuja, Nigeria

Lubumbashi, DRC

Antananarivo, Madagascar

Kinshasa, DRC

Addis Ababa, Ethiopia

Lusaka, Zambia

Mbuji-Mayi, DRC

Ouagadougou, Burkina Faso

Dar es Salaam, Tanzania

Kampala, Uganda13.4m

5.5m

4.8m

5.2m

8.9m

26.7m

6.2m

4.6m

6.1m

7m

Dar es Salaam, Tanzania

Mbuji-Mayi, DRC

Kinshasa, DRC

Lubumbashi, DRC

100%

88%

86%

85%

13.4m

4.8m

26.7m

4.6m

447611

2018 2025

Total subs (m)

235

475

2018 2025

Data subs (m)Asia

Structurally Attractive Markets for Organic and Inorganic Growth2

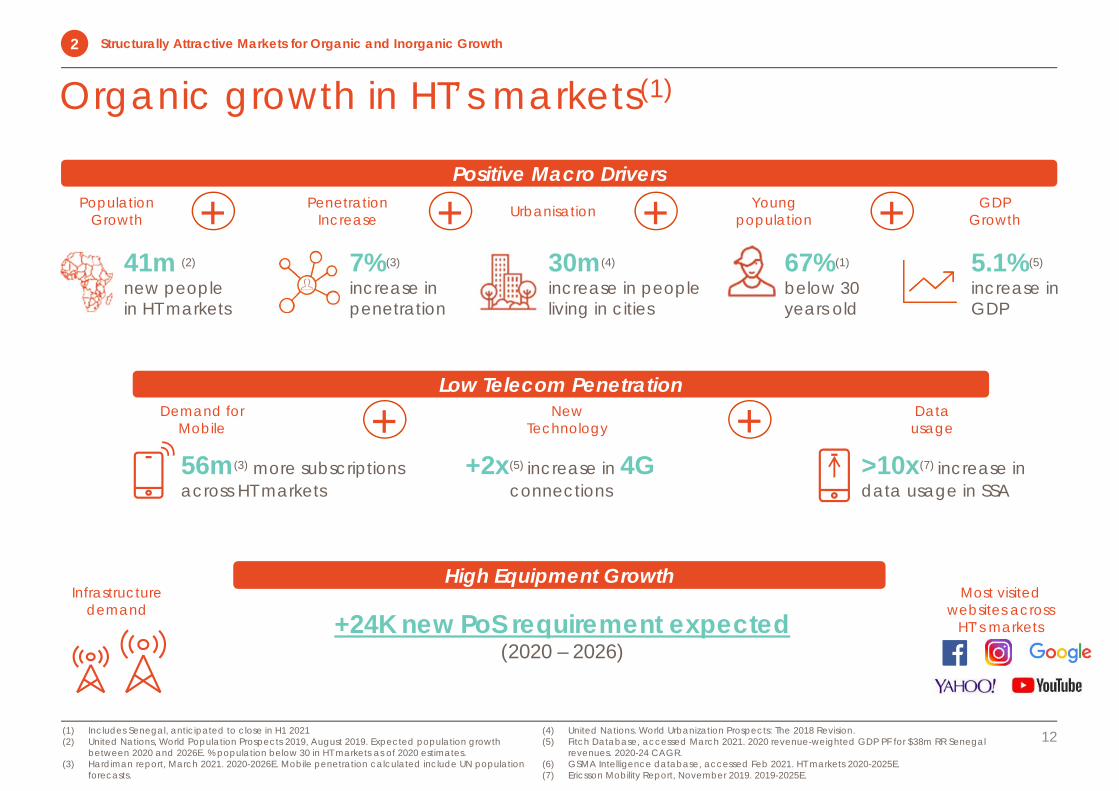

Organic growth in HT’s markets(1)

Infrastructure demand

(1) Includes Senegal, anticipated to close in H1 2021 (2) United Nations, World Population Prospects 2019, August 2019. Expected population growth

between 2020 and 2026E. % population below 30 in HT markets as of 2020 estimates.(3) Hardiman report, March 2021. 2020-2026E. Mobile penetration calculated include UN population

forecasts.

(4) United Nations. World Urbanization Prospects: The 2018 Revision.(5) Fitch Database, accessed March 2021. 2020 revenue-weighted GDP PF for $38m RR Senegal

revenues. 2020-24 CAGR. (6) GSMA Intelligence database, accessed Feb 2021. HT markets 2020-2025E.(7) Ericsson Mobility Report, November 2019. 2019-2025E.

41m (2)

new people in HT markets

Population Growth

7%(3)

increase in penetration

Penetration Increase Urbanisation

30m(4)

increase in people living in cities

Young population

67%(1)

below 30 years old

GDP Growth

5.1%(5)

increase in GDP

+Positive Macro Drivers

+ + +

High Equipment Growth

+24K new PoS requirement expected(2020 – 2026)

56m(3) more subscriptions across HT markets

Demand for Mobile

+2x(5) increase in 4Gconnections

Data usage

>10x(7) increase in data usage in SSA

+Low Telecom Penetration

+ New Technology

Most visited websites across

HT’s markets

12

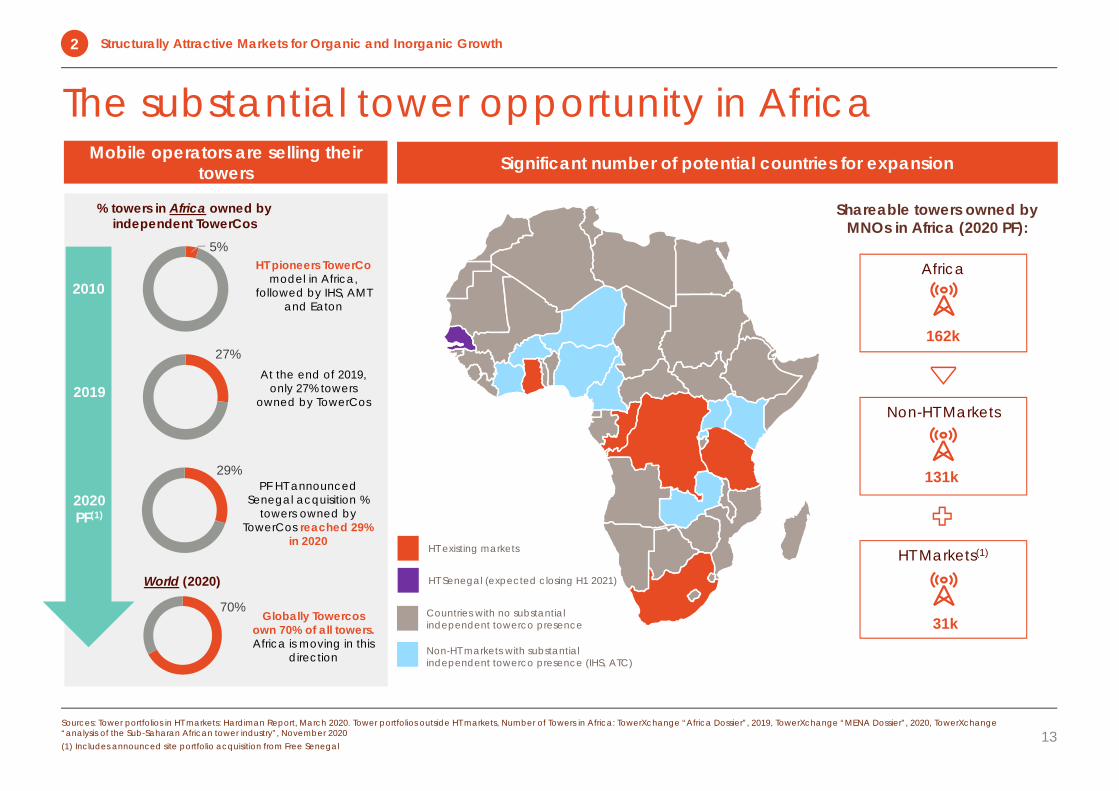

Structurally Attractive Markets for Organic and Inorganic Growth2

The substantial tower opportunity in AfricaMobile operators are selling their

towers

70%

World (2020)

% towers in Africa owned by independent TowerCos

Shareable towers owned by MNOs in Africa (2020 PF):

HT Markets(1)

31k

Non-HT Markets

131k

Non-HT markets with substantial independent towerco presence (IHS, ATC)

Countries with no substantial independent towerco presence

Significant number of potential countries for expansion

Africa

162k

Sources: Tower portfolios in HT markets: Hardiman Report, March 2020. Tower portfolios outside HT markets, Number of Towers in Africa: TowerXchange “Africa Dossier”, 2019, TowerXchange “MENA Dossier”, 2020, TowerXchange“analysis of the Sub-Saharan African tower industry”, November 2020(1) Includes announced site portfolio acquisition from Free Senegal

HT existing markets

HT Senegal (expected closing H1 2021)

2010

2019

HT pioneers TowerComodel in Africa,

followed by IHS, AMT and Eaton

Globally Towercos own 70% of all towers.Africa is moving in this

direction

29%

2020PF(1)

PF HT announced Senegal acquisition %

towers owned by TowerCos reached 29%

in 2020

27%

5%

At the end of 2019, only 27% towers

owned by TowerCos

13

Structurally Attractive Markets for Organic and Inorganic Growth2

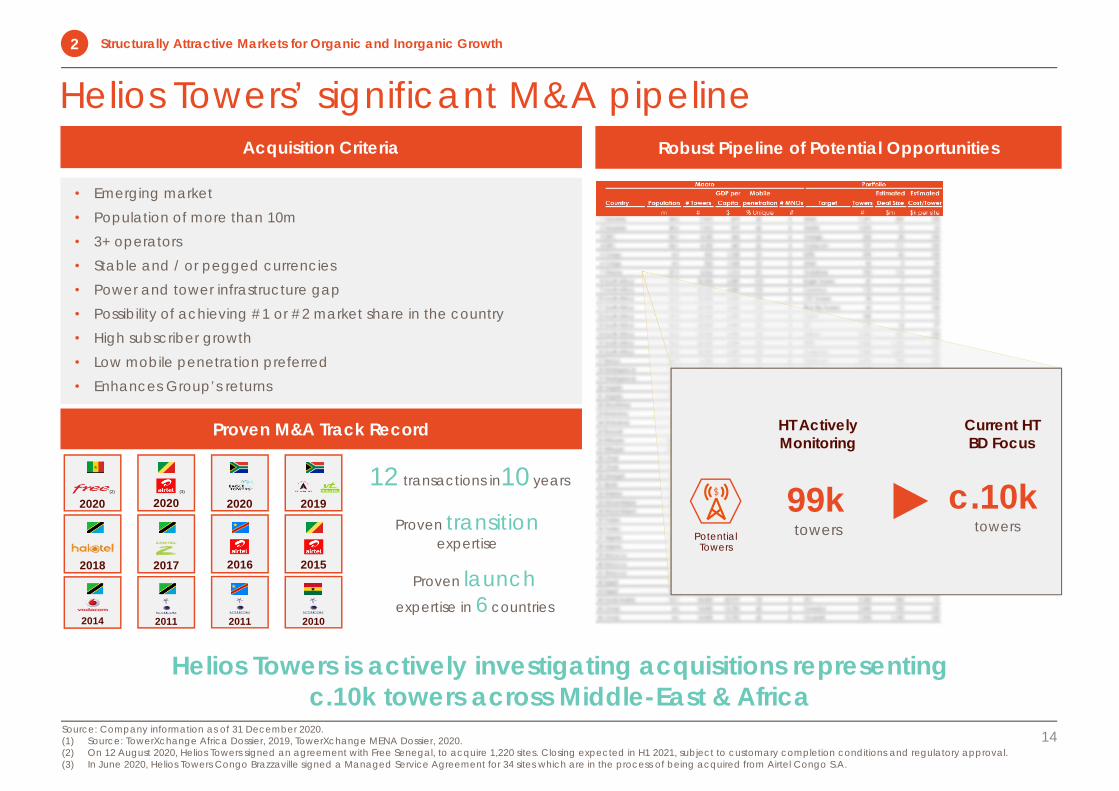

Helios Towers’ significant M&A pipeline

14Source: Company information as of 31 December 2020.(1) Source: TowerXchange Africa Dossier, 2019, TowerXchange MENA Dossier, 2020.(2) On 12 August 2020, Helios Towers signed an agreement with Free Senegal, to acquire 1,220 sites. Closing expected in H1 2021, subject to customary completion conditions and regulatory approval.(3) In June 2020, Helios Towers Congo Brazzaville signed a Managed Service Agreement for 34 sites which are in the process of being acquired from Airtel Congo S.A.

Acquisition Criteria Robust Pipeline of Potential Opportunities

Proven M&A Track Record

• Emerging market• Population of more than 10m• 3+ operators• Stable and / or pegged currencies• Power and tower infrastructure gap• Possibility of achieving #1 or #2 market share in the country• High subscriber growth• Low mobile penetration preferred• Enhances Group’s returns

2019

2018 2017 20152016

2014 2011

12 transactions in10 years

Proven transitionexpertise

Proven launchexpertise in 6 countries

HT Actively Monitoring

Current HT BD Focus

99ktowers

c.10ktowers

Potential Towers

2020

2011 2010

20202020(2) (3)

Structurally Attractive Markets for Organic and Inorganic Growth2

Helios Towers is actively investigating acquisitions representing c.10k towers across Middle-East & Africa

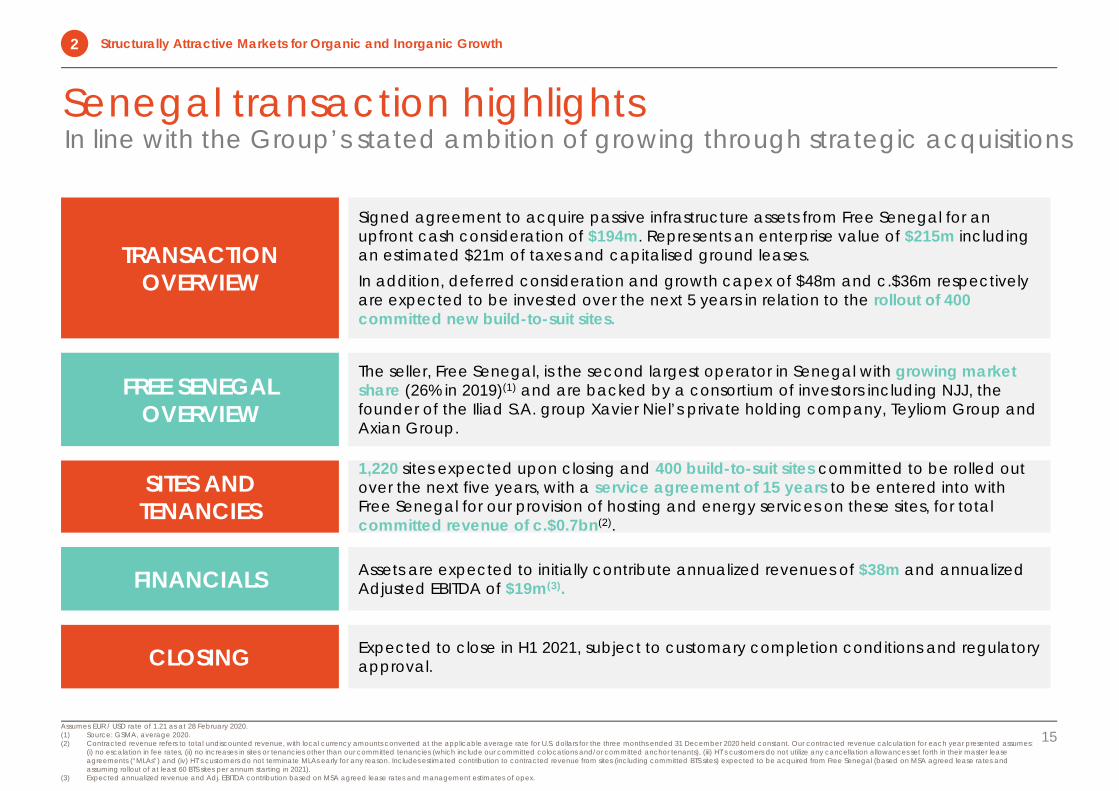

In line with the Group’s stated ambition of growing through strategic acquisitionsSenegal transaction highlights

15Assumes EUR / USD rate of 1.21 as at 28 February 2020.(1) Source: GSMA, average 2020.(2) Contracted revenue refers to total undiscounted revenue, with local currency amounts converted at the applicable average rate for U.S. dollars for the three months ended 31 December 2020 held constant. Our contracted revenue calculation for each year presented assumes:

(i) no escalation in fee rates, (ii) no increases in sites or tenancies other than our committed tenancies (which include our committed colocations and/or committed anchor tenants), (iii) HT’s customers do not utilize any cancellation allowances set forth in their master lease agreements (“MLAs”) and (iv) HT’s customers do not terminate MLAs early for any reason. Includes estimated contribution to contracted revenue from sites (including committed BTS sites) expected to be acquired from Free Senegal (based on MSA agreed lease rates and assuming rollout of at least 60 BTS sites per annum starting in 2021).

(3) Expected annualized revenue and Adj. EBITDA contribution based on MSA agreed lease rates and management estimates of opex.

TRANSACTION OVERVIEW

Signed agreement to acquire passive infrastructure assets from Free Senegal for an upfront cash consideration of $194m. Represents an enterprise value of $215m including an estimated $21m of taxes and capitalised ground leases.In addition, deferred consideration and growth capex of $48m and c.$36m respectively are expected to be invested over the next 5 years in relation to the rollout of 400 committed new build-to-suit sites.

SITES AND TENANCIES

1,220 sites expected upon closing and 400 build-to-suit sites committed to be rolled out over the next five years, with a service agreement of 15 years to be entered into with Free Senegal for our provision of hosting and energy services on these sites, for totalcommitted revenue of c.$0.7bn(2).

FINANCIALS Assets are expected to initially contribute annualized revenues of $38m and annualized Adjusted EBITDA of $19m(3).

CLOSING Expected to close in H1 2021, subject to customary completion conditions and regulatory approval.

FREE SENEGALOVERVIEW

The seller, Free Senegal, is the second largest operator in Senegal with growing market share (26% in 2019)(1) and are backed by a consortium of investors including NJJ, the founder of the Iliad S.A. group Xavier Niel’s private holding company, Teyliom Group and Axian Group.

Structurally Attractive Markets for Organic and Inorganic Growth2

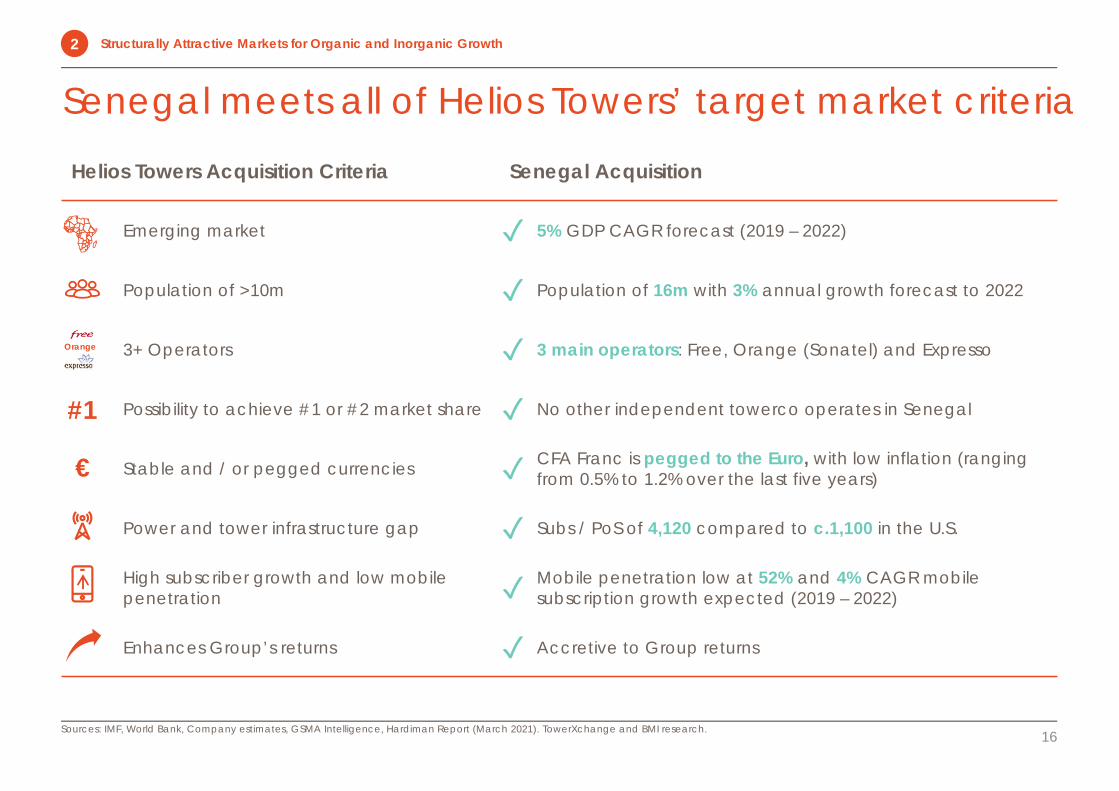

Helios Towers Acquisition Criteria Senegal Acquisition

Emerging market ✓ 5% GDP CAGR forecast (2019 – 2022)

Population of >10m ✓ Population of 16m with 3% annual growth forecast to 2022

3+ Operators ✓ 3 main operators: Free, Orange (Sonatel) and Expresso

Possibility to achieve #1 or #2 market share ✓ No other independent towerco operates in Senegal

Stable and / or pegged currencies ✓ CFA Franc is pegged to the Euro, with low inflation (ranging from 0.5% to 1.2% over the last five years)

Power and tower infrastructure gap ✓ Subs / PoS of 4,120 compared to c.1,100 in the U.S.

High subscriber growth and low mobile penetration ✓ Mobile penetration low at 52% and 4% CAGR mobile

subscription growth expected (2019 – 2022)

Enhances Group’s returns ✓ Accretive to Group returns

Senegal meets all of Helios Towers’ target market criteria

16Sources: IMF, World Bank, Company estimates, GSMA Intelligence, Hardiman Report (March 2021). TowerXchange and BMI research.

€

#1

Orange

Structurally Attractive Markets for Organic and Inorganic Growth2

Highly Visible Revenue Stream with FX and Cost Inflation Protection

3

Illustrative Cumulative Build-To-Suit Site Free Cash Flow(1)

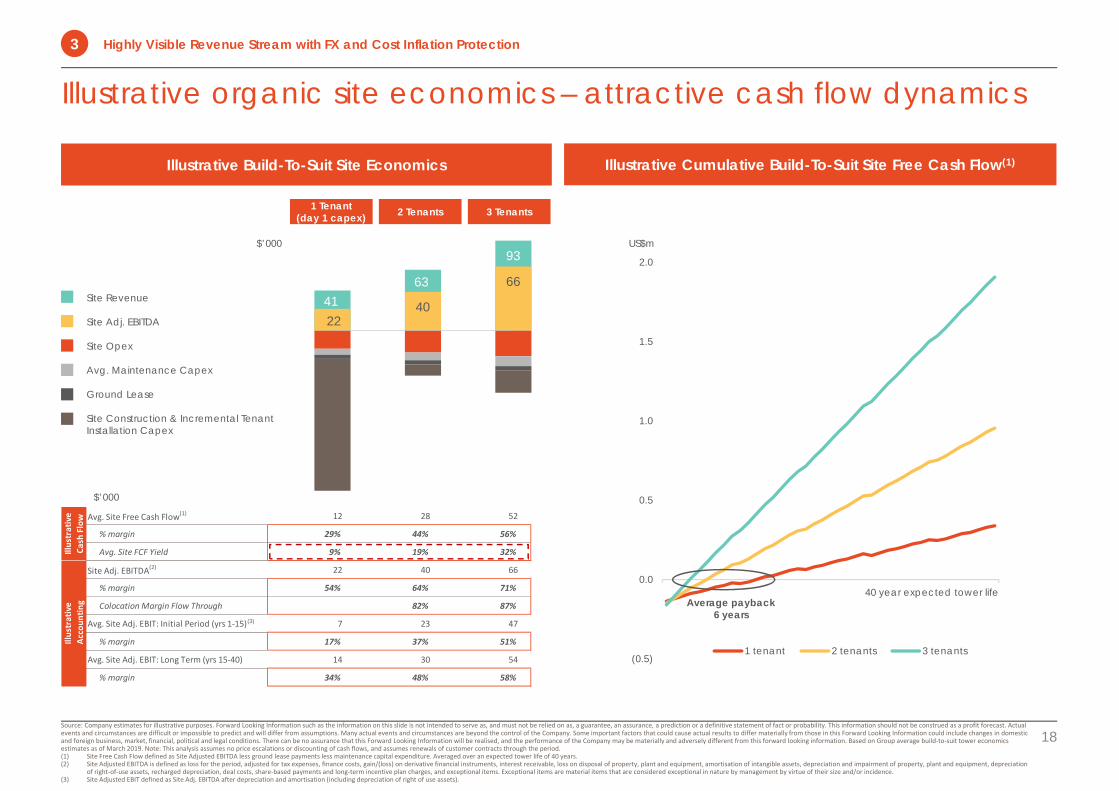

Illustrative organic site economics – attractive cash flow dynamics

18

Illustrative Build-To-Suit Site Economics

Source: Company estimates for illustrative purposes. Forward Looking Information such as the information on this slide is not intended to serve as, and must not be relied on as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. This information should not be construed as a profit forecast. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of the Company. Some important factors that could cause actual results to differ materially from those in this Forward Looking Information could include changes in domestic and foreign business, market, financial, political and legal conditions. There can be no assurance that this Forward Looking Information will be realised, and the performance of the Company may be materially and adversely different from this forward looking information. Based on Group average build‐to‐suit tower economics estimates as of March 2019. Note: This analysis assumes no price escalations or discounting of cash flows, and assumes renewals of customer contracts through the period.(1) Site Free Cash Flow defined as Site Adjusted EBITDA less ground lease payments less maintenance capital expenditure. Averaged over an expected tower life of 40 years.(2) Site Adjusted EBITDA is defined as loss for the period, adjusted for tax expenses, finance costs, gain/(loss) on derivative financial instruments, interest receivable, loss on disposal of property, plant and equipment, amortisation of intangible assets, depreciation and impairment of property, plant and equipment, depreciation

of right‐of‐use assets, recharged depreciation, deal costs, share‐based payments and long‐term incentive plan charges, and exceptional items. Exceptional items are material items that are considered exceptional in nature by management by virtue of their size and/or incidence.(3) Site Adjusted EBIT defined as Site Adj. EBITDA after depreciation and amortisation (including depreciation of right of use assets).

(0.5)

0.0

0.5

1.0

1.5

2.0

40 year expected tower life

1 tenant 2 tenants 3 tenants

Average payback6 years

$’000 US$m

1 Tenant(day 1 capex) 2 Tenants 3 Tenants

Site Revenue

Site Adj. EBITDA

Site Opex

Avg. Maintenance Capex

Ground Lease

Site Construction & Incremental Tenant Installation Capex

4163

93

2240

66

$’000

Avg. Site Free Cash Flow(1) 12 28 52

% margin 29% 44% 56%

Avg. Site FCF Yield 9% 19% 32%

Site Adj. EBITDA(2) 22 40 66

% margin 54% 64% 71%

Colocation Margin Flow Through 82% 87%

Avg. Site Adj. EBIT: Initial Period (yrs 1‐15) 7 23 47

% margin 17% 37% 51%

Avg. Site Adj. EBIT: Long Term (yrs 15‐40) 14 30 54

% margin 34% 48% 58%

Illustrative

Cash Flow

Illustrative

Accou

nting

(3)

Highly Visible Revenue Stream with FX and Cost Inflation Protection3

20%

17%

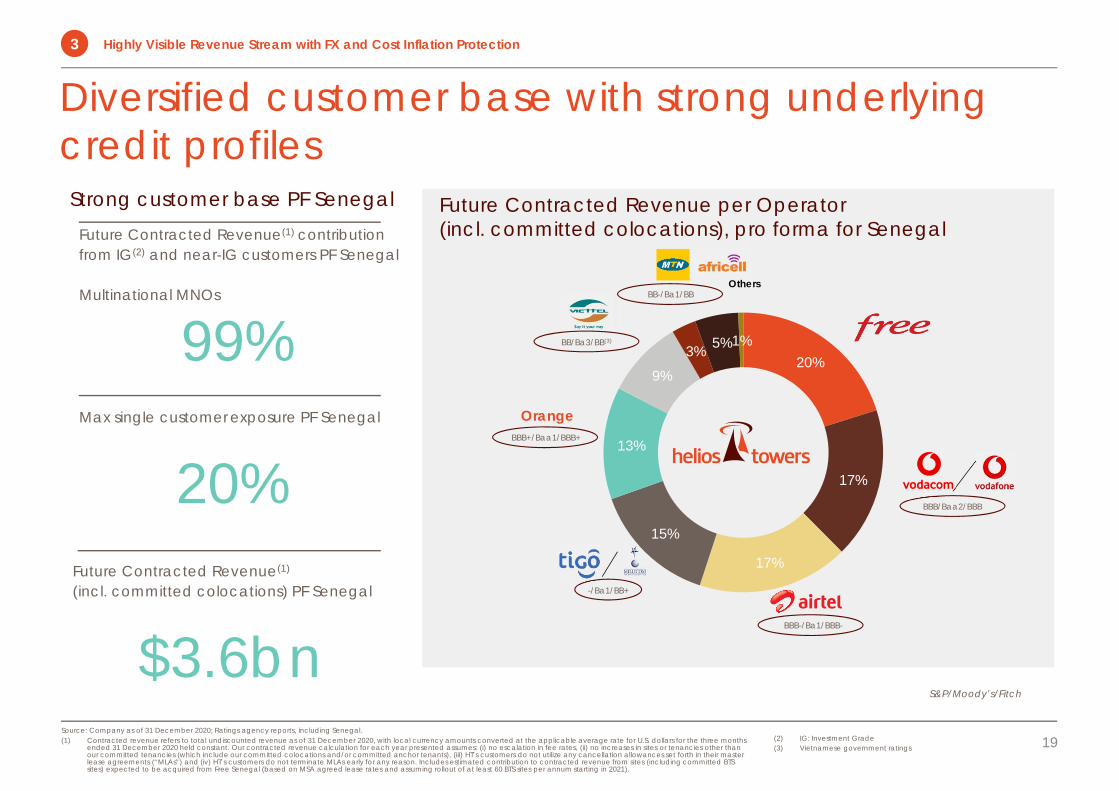

17%

15%

13%

9% 3% 5% 1%

Strong customer base PF SenegalFuture Contracted Revenue(1) contributionfrom IG(2) and near-IG customers PF Senegal

Multinational MNOs

99%Max single customer exposure PF Senegal

20%

Future Contracted Revenue per Operator(incl. committed colocations), pro forma for Senegal

Others

BBB-/Ba1/BBB-

S&P/Moody’s/Fitch

BB-/Ba1/BB

-/Ba1/BB+

Future Contracted Revenue(1)

(incl. committed colocations) PF Senegal

$3.6bn

BB/Ba3/BB(3)

19

Diversified customer base with strong underlying credit profiles

(2) IG: Investment Grade (3) Vietnamese government ratings

Source: Company as of 31 December 2020; Ratings agency reports, including Senegal.(1) Contracted revenue refers to total undiscounted revenue as of 31 December 2020, with local currency amounts converted at the applicable average rate for U.S. dollars for the three months

ended 31 December 2020 held constant. Our contracted revenue calculation for each year presented assumes: (i) no escalation in fee rates, (ii) no increases in sites or tenancies other than our committed tenancies (which include our committed colocations and/or committed anchor tenants), (iii) HT’s customers do not utilize any cancellation allowances set forth in their master lease agreements (“MLAs”) and (iv) HT’s customers do not terminate MLAs early for any reason. Includes estimated contribution to contracted revenue from sites (including committed BTS sites) expected to be acquired from Free Senegal (based on MSA agreed lease rates and assuming rollout of at least 60 BTS sites per annum starting in 2021).

Highly Visible Revenue Stream with FX and Cost Inflation Protection3

BBB+/Baa1/BBB+

Orange

BBB/Baa2/BBB

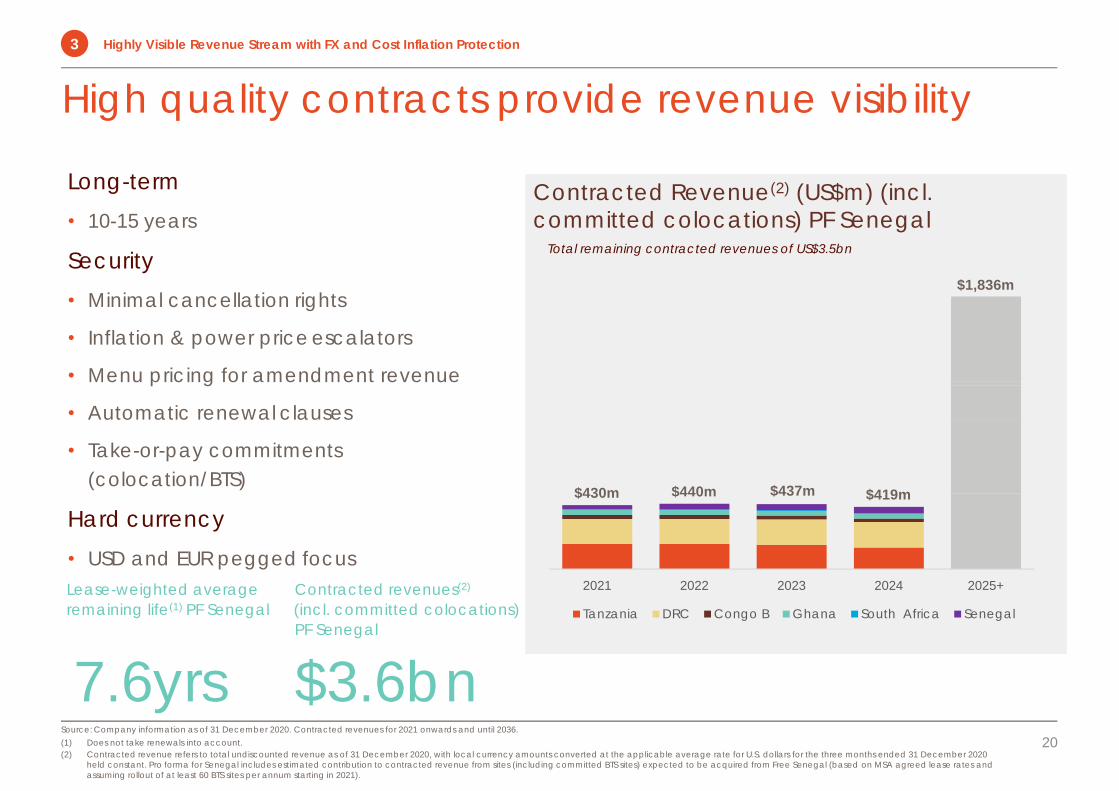

Long-term• 10-15 years

Security• Minimal cancellation rights

• Inflation & power priceescalators

• Menu pricing for amendment revenue

• Automatic renewal clauses

• Take-or-pay commitments (colocation/BTS)

Hard currency• USD and EUR pegged focus

High quality contracts provide revenue visibility

Lease-weighted average Contracted revenues(2)

remaining life(1) PF Senegal (incl. committed colocations) PF Senegal

7.6yrs $3.6bn

Contracted Revenue(2) (US$m) (incl. committed colocations) PF Senegal

Total remaining contracted revenues of US$3.5bn

Source: Company information as of 31 December 2020. Contracted revenues for 2021 onwards and until 2036.(1) Does not take renewals into account.(2) Contracted revenue refers to total undiscounted revenue as of 31 December 2020, with local currency amounts converted at the applicable average rate for U.S. dollars for the three months ended 31 December 2020

held constant. Pro forma for Senegal includes estimated contribution to contracted revenue from sites (including committed BTS sites) expected to be acquired from Free Senegal (based on MSA agreed lease rates and assuming rollout of at least 60 BTS sites per annum starting in 2021).

20

Highly Visible Revenue Stream with FX and Cost Inflation Protection3

$430m $440m $437m $419m

$1,836m

2021 2022 2023 2024 2025+

Tanzania DRC Congo B Ghana South Africa Senegal

10.0 9.0 9.0 9.0 9.020.0 18.0 14.4 19.8 19.8

70.0 63.0 63.0 63.0 70.6

100.0 90.0 86.4 91.8 99.4

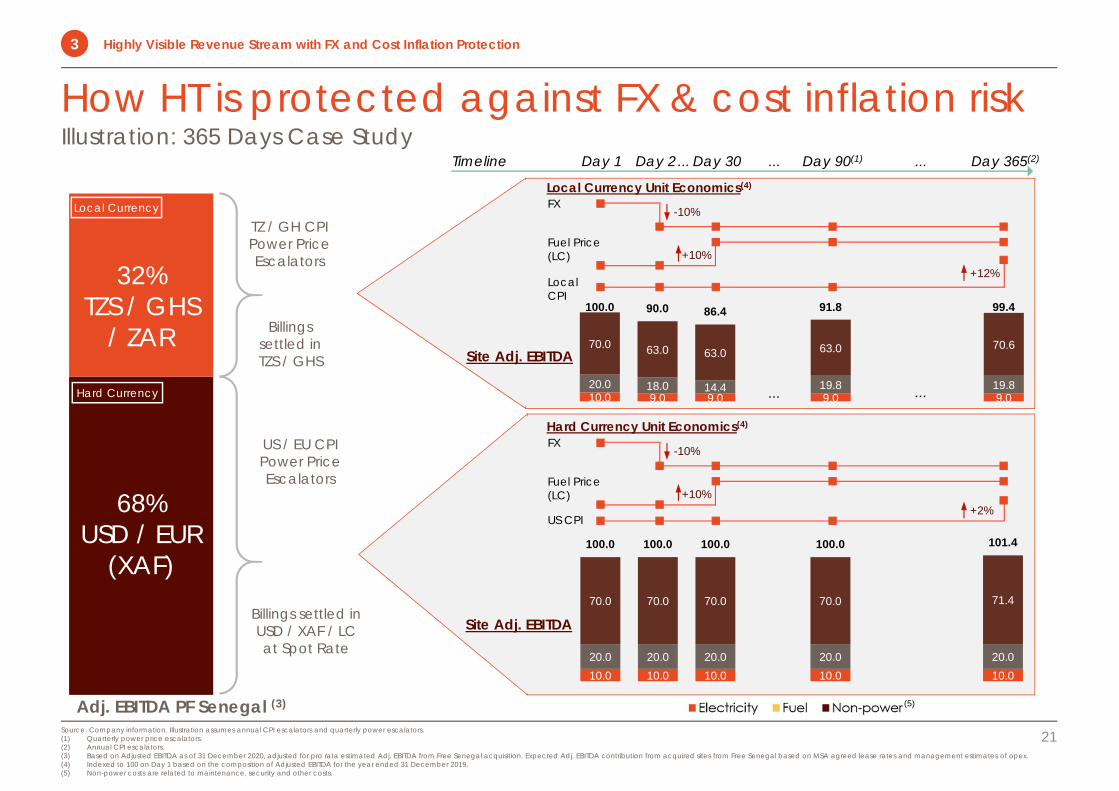

How HT is protected against FX & cost inflation riskIllustration: 365 Days Case Study

21

Adj. EBITDA PF Senegal (3)

32% TZS / GHS

/ ZAR

68% USD / EUR

(XAF)

US / EU CPI Power Price Escalators

Billings settled in USD / XAF / LC at Spot Rate

TZ / GH CPI Power Price Escalators

Billings settled in TZS / GHS

Day 1 Day 2 Day 30 Day 90(1) Day 365(2)

Local Currency Unit Economics(4)

Site Adj. EBITDA

Hard Currency Unit Economics(4)

Local Currency

Hard Currency

FX

Fuel Price (LC)

Local CPI

-10%

+10%+12%

Site Adj. EBITDA

Timeline ... ......

... ...

FX

Fuel Price (LC)

US CPI

-10%

+10%+2%

10.0 10.0 10.0 10.0 10.020.0 20.0 20.0 20.0 20.0

70.0 70.0 70.0 70.0 71.4

100.0 100.0 100.0 100.0 101.4

(5)

Source: Company information. Illustration assumes annual CPI escalators and quarterly power escalators.(1) Quarterly power price escalators.(2) Annual CPI escalators. (3) Based on Adjusted EBITDA as of 31 December 2020, adjusted for pro rata estimated Adj. EBITDA from Free Senegal acquisition. Expected Adj. EBITDA contribution from acquired sites from Free Senegal based on MSA agreed lease rates and management estimates of opex.(4) Indexed to 100 on Day 1 based on the composition of Adjusted EBITDA for the year ended 31 December 2019. (5) Non-power costs are related to maintenance, security and other costs.

Highly Visible Revenue Stream with FX and Cost Inflation Protection3

4250

60 63

83 85

126 127133 138

148

164 168176 181 186

195 201210 215 216 220

230240

0

50

100

150

200

250

300

20%

40%

60%

80%

100%

120%

140%

160%

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19 Q4 19 Q1 20 Q2 20 Q3 20 Q4 20

LQA Adj. EBITDA ($m) TZS-USD CDF-USD GHS-USD XAF-USD Brent Crude ($)

Sustained Adj. EBITDA growth through market volatility Group LQA Adj. EBITDA ($m) vs. currencies of the countries in which HT operates(1) and Brent Crude

22Source: FactSet average of FX rates for each quarter, Company information as of the end of the respective quarter(1) Excludes South African Rand as the market was entered in January 2019

Adj. EBITDA Margin35% 35% 39% 38% 40% 40% 42% 49%46% 51%25% 27% 28% 28% 52% 52% 52%47% 54% 54% 53% 54% 55%

Highly Visible Revenue Stream with FX and Cost Inflation Protection3

57%

Experienced Management Team and Board of Directors

4

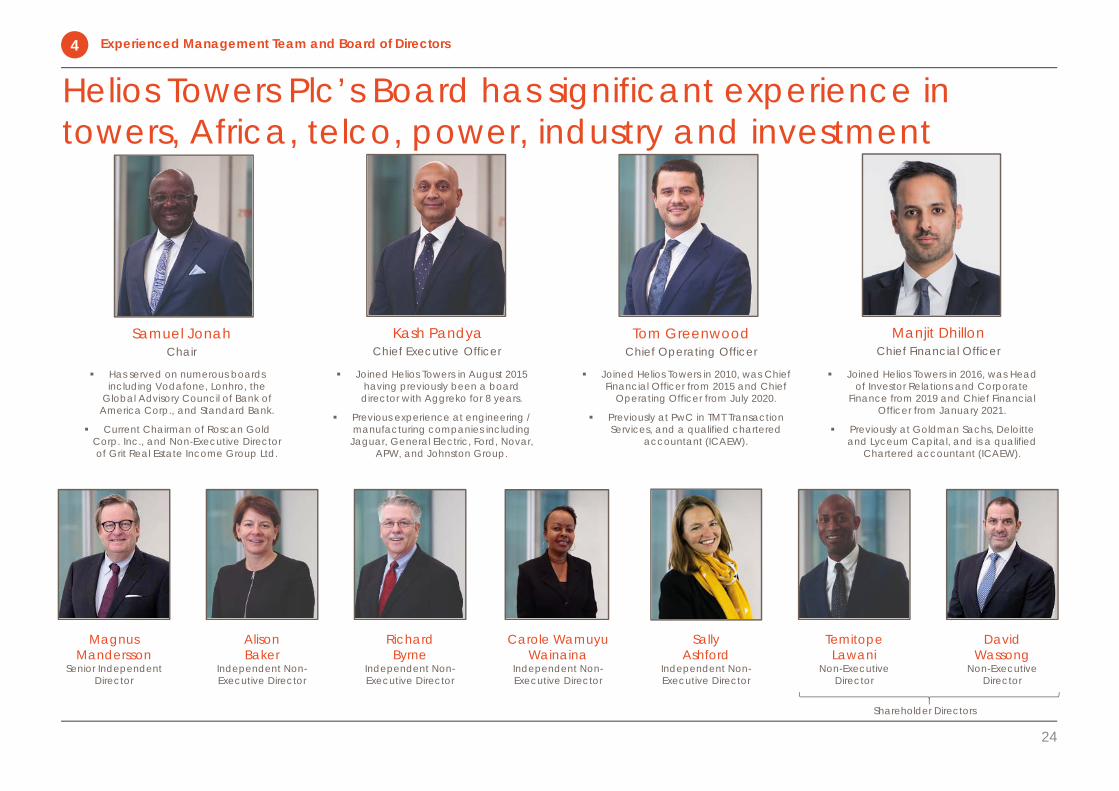

Helios Towers Plc’s Board has significant experience in towers, Africa, telco, power, industry and investment

24

Samuel JonahChair

Kash PandyaChief Executive Officer

Tom GreenwoodChief Operating Officer

Magnus Mandersson

Senior Independent Director

Alison Baker

Independent Non-Executive Director

Richard Byrne

Independent Non-Executive Director

Carole Wamuyu Wainaina

Independent Non-Executive Director

Sally Ashford

Independent Non-Executive Director

Temitope Lawani

Non-Executive Director

David Wassong

Non-Executive Director

Has served on numerous boards including Vodafone, Lonhro, the

Global Advisory Council of Bank of America Corp., and Standard Bank.

Current Chairman of Roscan Gold Corp. Inc., and Non-Executive Director of Grit Real Estate Income Group Ltd.

Joined Helios Towers in August 2015 having previously been a board

director with Aggreko for 8 years.

Previous experience at engineering / manufacturing companies including

Jaguar, General Electric, Ford, Novar, APW, and Johnston Group.

Joined Helios Towers in 2010, was Chief Financial Officer from 2015 and Chief

Operating Officer from July 2020.

Previously at PwC in TMT Transaction Services, and a qualified chartered

accountant (ICAEW).

Shareholder Directors

Manjit DhillonChief Financial Officer

Joined Helios Towers in 2016, was Head of Investor Relations and Corporate

Finance from 2019 and Chief Financial Officer from January 2021.

Previously at Goldman Sachs, Deloitte and Lyceum Capital, and is a qualified

Chartered accountant (ICAEW).

Experienced Management Team and Board of Directors4

Sainesh VallabhCEO Southern Africa• Joined 2020• Previously at

Vodacom• SA citizen

Philippe Loridon(1)

CEO East & West Africa• Joined 2011• Previously at

Hutchison Telecom and BeMobile

Experienced management team

25

Ramsey KoolaMD HT Tanzania• Joined 2015• 20+ years of

mobile commsexperience

• Tanzanian citizen

Colard NkoleMD HT Congo B• Joined 2011• Appointed MD of

HTCB early 2020• Prior roles at

Celtel/Airtel• DRC citizen

Jeffrey SchumacherDirector of Commercial• Joined 2011• Previously at Soros

Fund Management

Localised and Regional

ManagementTeams

Supplemented by Strong

Group Executive

Team

Léon-Paul O. Manya(1)

Group Technical Advisor: New Markets• Joined 2011• Prior roles at Tigo and

Dimension Data• DRC citizen

+100 Years Experience of Towers and Power in Emerging Markets(1) Philippe and Léon-Paul are also part of the HT executive team.

Nick SummersDirector of Sustainability & Organisational Development• Joined 2010• Previously at

Vodafone

Tom GreenwoodChief Operating Officer• Joined 2010• Previously at PwC

Roy CursleyDirector ofTechnology• Joined 2015• Previously at

Aggreko

Kash PandyaChief Executive Officer• Joined 2015• Previously at

Aggreko

Paul BarrettGeneral Counsel and Company Secretary• Joined 2020• Previously at RAC

Motoring Services and Home Retail Group plc

Fritz DzekloMD HT Ghana• Joined 2012• Previously at

Vodafone Ghana• Ghanaian citizen

Colin GastonDirector of Special Projects• Joined 2015• Previously at

Aggreko and Schlumberger

Experienced Management Team and Board of Directors4

Manjit DhillonChief Financial Officer• Joined 2016• Previously at Lyceum

Capital, Deloitte and Goldman Sachs

Neil ConquestDirector of Delivery• Joined 2015• Previously at

Aggreko

Marlene Kiniffo-ZounonCEO Central Africa• Joined 2020• Previously at

LafargeHolcim and BlackBerry

• Beninese national

Marinus GieselbachMD Helios TowersSouth Africa• Joined 2019• Previously at Vulatel• SA citizen

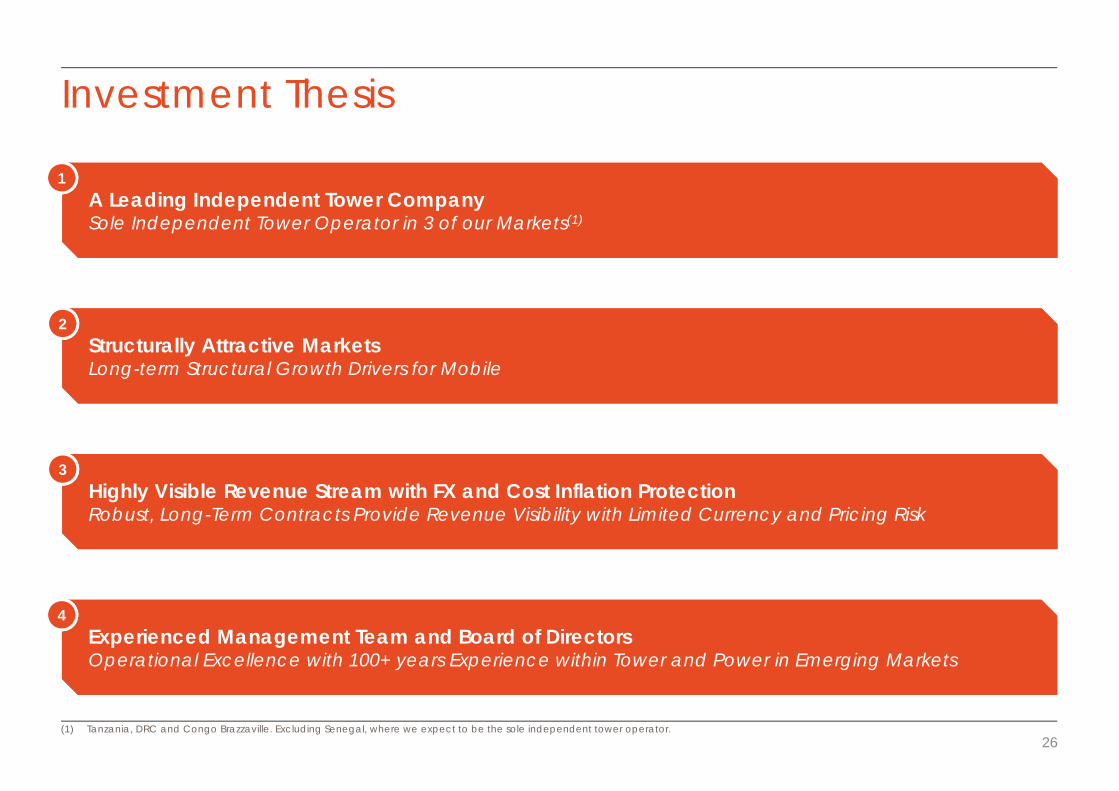

Investment Thesis

A Leading Independent Tower CompanySole Independent Tower Operator in 3 of our Markets(1)A Leading Independent Tower CompanySole Independent Tower Operator in 3 of our Markets(1)

1

Highly Visible Revenue Stream with FX and Cost Inflation ProtectionRobust, Long-Term Contracts Provide Revenue Visibility with Limited Currency and Pricing RiskHighly Visible Revenue Stream with FX and Cost Inflation ProtectionRobust, Long-Term Contracts Provide Revenue Visibility with Limited Currency and Pricing Risk

3

Structurally Attractive MarketsLong-term Structural Growth Drivers for MobileStructurally Attractive MarketsLong-term Structural Growth Drivers for Mobile

2

26

Experienced Management Team and Board of DirectorsOperational Excellence with 100+ years Experience within Tower and Power in Emerging MarketsExperienced Management Team and Board of DirectorsOperational Excellence with 100+ years Experience within Tower and Power in Emerging Markets

4

(1) Tanzania, DRC and Congo Brazzaville. Excluding Senegal, where we expect to be the sole independent tower operator.

FY 2020 Update

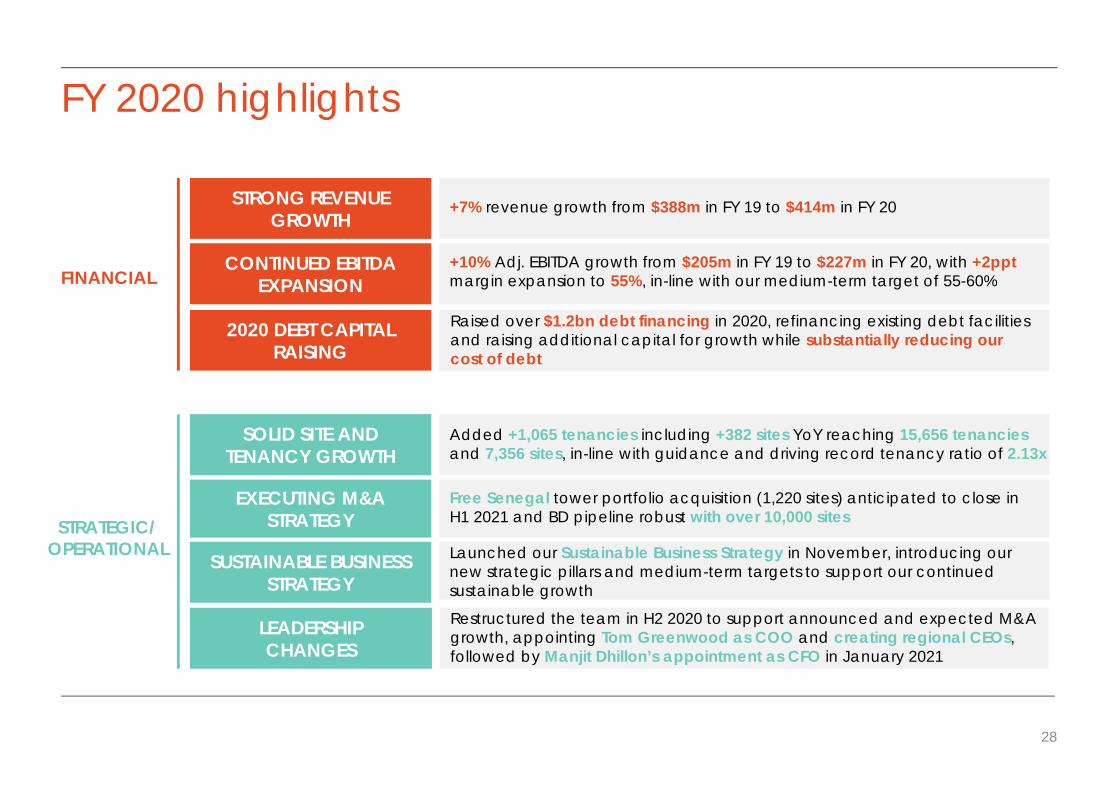

FY 2020 highlights

+10% Adj. EBITDA growth from $205m in FY 19 to $227m in FY 20, with +2pptmargin expansion to 55%, in-line with our medium-term target of 55-60%

CONTINUED EBITDA EXPANSIONFINANCIAL

STRONG REVENUE GROWTH

+7% revenue growth from $388m in FY 19 to $414m in FY 20

STRATEGIC/OPERATIONAL Launched our Sustainable Business Strategy in November, introducing our

new strategic pillars and medium-term targets to support our continued sustainable growth

SUSTAINABLE BUSINESS STRATEGY

Restructured the team in H2 2020 to support announced and expected M&A growth, appointing Tom Greenwood as COO and creating regional CEOs, followed by Manjit Dhillon’s appointment as CFO in January 2021

LEADERSHIPCHANGES

Raised over $1.2bn debt financing in 2020, refinancing existing debt facilities and raising additional capital for growth while substantially reducing our cost of debt

2020 DEBT CAPITAL RAISING

Added +1,065 tenancies including +382 sites YoY reaching 15,656 tenancies and 7,356 sites, in-line with guidance and driving record tenancy ratio of 2.13x

SOLID SITE AND TENANCY GROWTH

Free Senegal tower portfolio acquisition (1,220 sites) anticipated to close in H1 2021 and BD pipeline robust with over 10,000 sites

EXECUTING M&ASTRATEGY

28

105

146

178

205227

37%

42%

50%53%

55%

2016 2017 2018 2019 2020

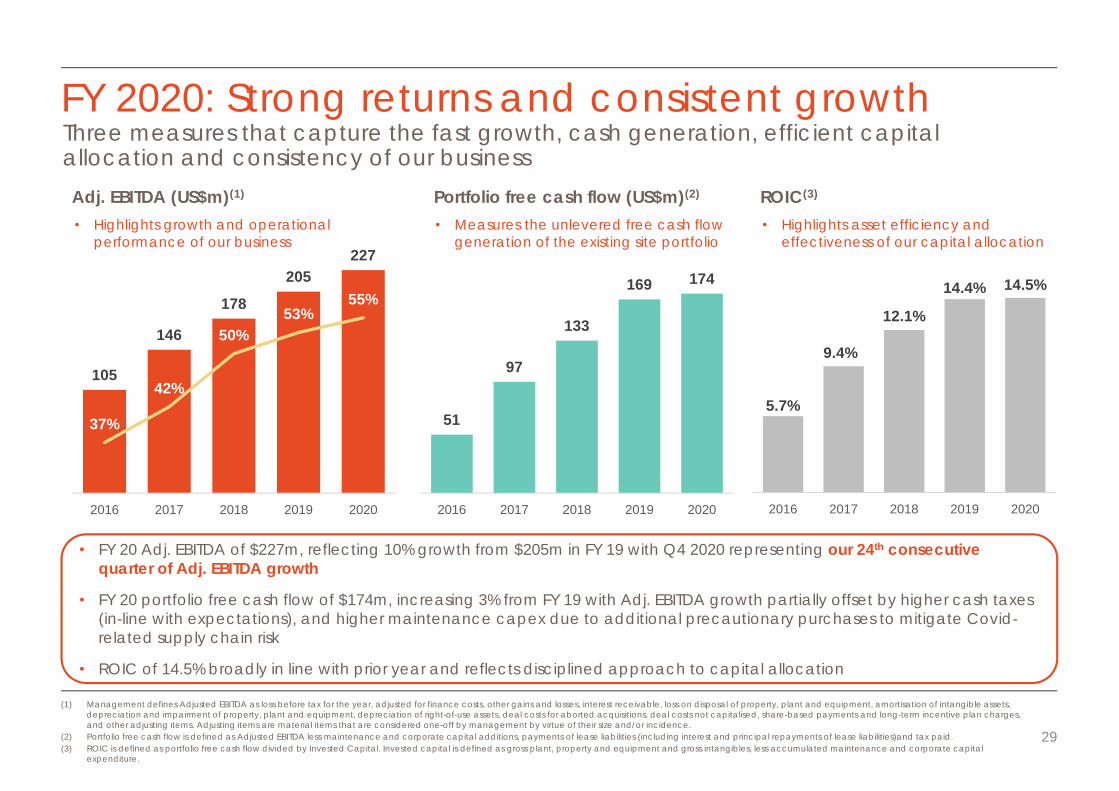

FY 2020: Strong returns and consistent growth

• FY 20 Adj. EBITDA of $227m, reflecting 10% growth from $205m in FY 19 with Q4 2020 representing our 24th consecutive quarter of Adj. EBITDA growth

• FY 20 portfolio free cash flow of $174m, increasing 3% from FY 19 with Adj. EBITDA growth partially offset by higher cash taxes (in-line with expectations), and higher maintenance capex due to additional precautionary purchases to mitigate Covid-related supply chain risk

• ROIC of 14.5% broadly in line with prior year and reflects disciplined approach to capital allocation

Adj. EBITDA (US$m)(1) Portfolio free cash flow (US$m)(2) ROIC(3)

• Highlights growth and operational performance of our business

• Measures the unlevered free cash flow generation of the existing site portfolio

• Highlights asset efficiency and effectiveness of our capital allocation

Three measures that capture the fast growth, cash generation, efficient capital allocation and consistency of our business

51

97

133

169 174

2016 2017 2018 2019 2020

(1) Management defines Adjusted EBITDA as loss before tax for the year, adjusted for finance costs, other gains and losses, interest receivable, loss on disposal of property, plant and equipment, amortisation of intangible assets, depreciation and impairment of property, plant and equipment, depreciation of right-of-use assets, deal costs for aborted acquisitions, deal costs not capitalised, share-based payments and long-term incentive plan charges, and other adjusting items. Adjusting items are material items that are considered one-off by management by virtue of their size and/or incidence.

(2) Portfolio free cash flow is defined as Adjusted EBITDA less maintenance and corporate capital additions, payments of lease liabilities (including interest and principal repayments of lease liabilities)and tax paid.(3) ROIC is defined as portfolio free cash flow divided by Invested Capital. Invested capital is defined as gross plant, property and equipment and gross intangibles, less accumulated maintenance and corporate capital

expenditure.

29

5.7%

9.4%

12.1%

14.4% 14.5%

2016 2017 2018 2019 2020

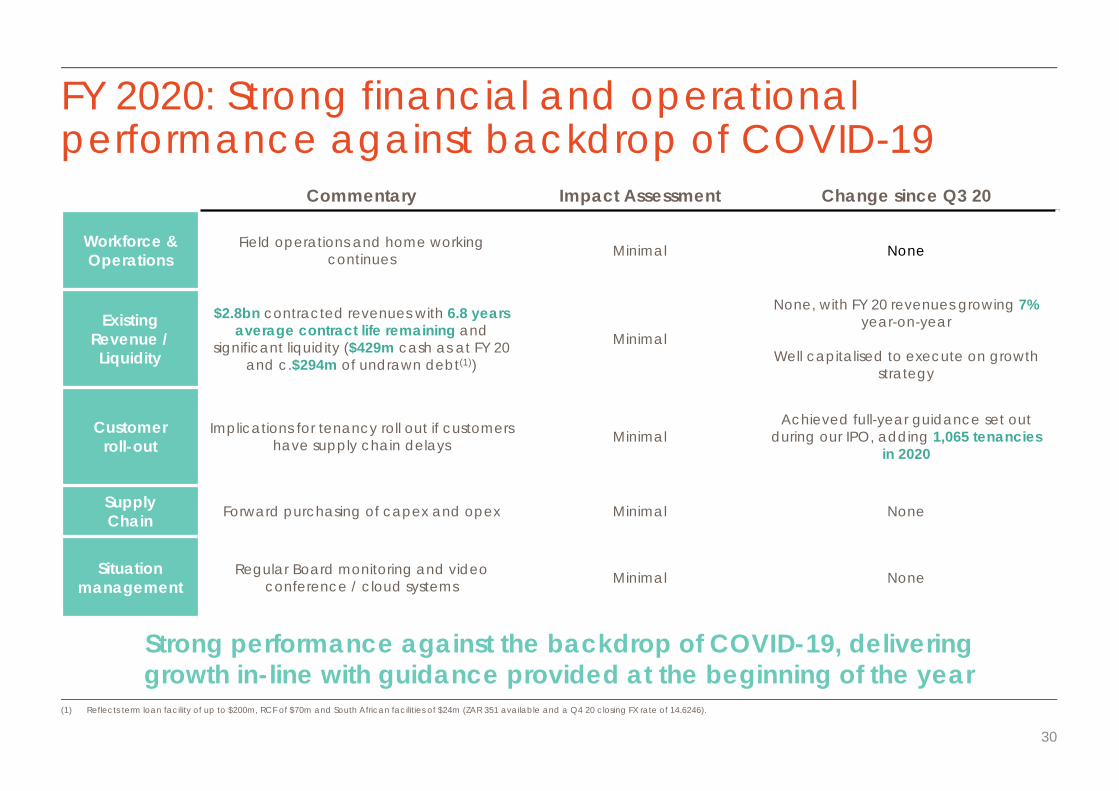

FY 2020: Strong financial and operational performance against backdrop of COVID-19

Commentary Impact Assessment Change since Q3 20

Workforce & Operations

Field operations and home working continues Minimal None

Existing Revenue / Liquidity

$2.8bn contracted revenues with 6.8 years average contract life remaining and

significant liquidity ($429m cash as at FY 20 and c.$294m of undrawn debt(1))

Minimal

None, with FY 20 revenues growing 7% year-on-year

Well capitalised to execute on growth strategy

Customer roll-out

Implications for tenancy roll out if customers have supply chain delays Minimal

Achieved full-year guidance set out during our IPO, adding 1,065 tenancies

in 2020

Supply Chain Forward purchasing of capex and opex Minimal None

Situation management

Regular Board monitoring and video conference / cloud systems Minimal None

(1) Reflects term loan facility of up to $200m, RCF of $70m and South African facilities of $24m (ZAR 351 available and a Q4 20 closing FX rate of 14.6246).

Strong performance against the backdrop of COVID-19, deliveringgrowth in-line with guidance provided at the beginning of the year

30

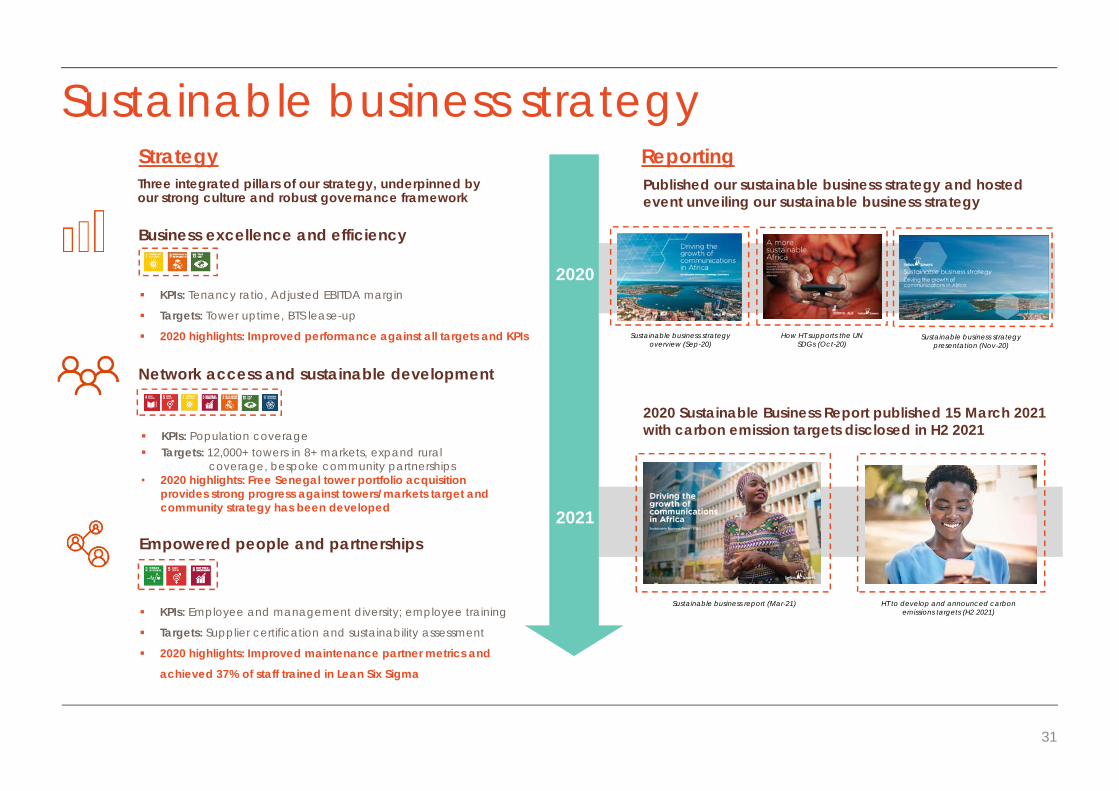

Sustainable business strategy

31

Strategy

Business excellence and efficiency

Network access and sustainable development

Empowered people and partnerships

2020

2021

Reporting Published our sustainable business strategy and hosted event unveiling our sustainable business strategy

2020 Sustainable Business Report published 15 March 2021with carbon emission targets disclosed in H2 2021

KPIs: Tenancy ratio, Adjusted EBITDA margin

Targets: Tower uptime, BTS lease-up

2020 highlights: Improved performance against all targets and KPIs

KPIs: Population coverage Targets: 12,000+ towers in 8+ markets, expand rural

coverage, bespoke community partnerships• 2020 highlights: Free Senegal tower portfolio acquisition

provides strong progress against towers/markets target and community strategy has been developed

KPIs: Employee and management diversity; employee training

Targets: Supplier certification and sustainability assessment

2020 highlights: Improved maintenance partner metrics and

achieved 37% of staff trained in Lean Six Sigma

Three integrated pillars of our strategy, underpinned by our strong culture and robust governance framework

Sustainable business strategy presentation (Nov-20)

Sustainable business strategy overview (Sep-20)

How HT supports the UNSDGs (Oct-20)

Sustainable business report (Mar-21) HT to develop and announced carbon emissions targets (H2 2021)

Guidance and outlook

32

Guidance

Exist

ing

five

mar

kets

Tenancies • Guidance unchanged, targeting 1-1.5k per year over the medium term• Of which 50% BTS gradually reducing to 25% BTS over the medium term

Lease rateper tenancy

• Decrease of c.3% in 2021 driven by power price movements• USD inflationary growth from 2022 onwards, in-line with prior guidance

Opexper site

• Decrease of c.3% in 2021 driven by lower power opex• Flat opex per site from 2022 onwards, in-line with prior guidance

SG&A • USD inflationary growth + c.$3m growth investment in 2021• USD inflationary growth from 2022 onwards, in-line with prior guidance

Capex• Targeting $110 – 140m capex in 2021, of which $20 - $25m non-discretionary capex• Medium term driven by c.$125k per new BTS and $10k per colocation tenant and non-discretionary capex

growing with site count, in-line with prior outlook

New

mar

kets

Senegalconsiderations

• 1,220 sites deliver initial annualised revenues of $38m and Adjusted EBITDA of $19m• $215m capex reflecting acquisition and expansion in 2021• Anticipated closing H1 2021, with 400 committed BTS to be rolled over the next five years

Medium term tenancy roll-out expectations for existing markets unchanged, with further growth anticipated through Senegal acquisition