Embed Size (px)

Citation preview

Managing UDAAP Risks in

Payments: What Have We

Learned to Expect from the

Regulators?

BAI Payments Connect

March 12, 2013

Cliff Stanford, Alston & Bird, LLP

Lyn Farrell, Treliant Risk Advisors, LLC

Disclaimer

• Nothing in this presentation is or is intended to be

legal advice.

• Please consult with your own legal counsel for

guidance specific to your organization or

situation.

2

Are legal changes driving payments innovation?

• There is a positive correlation between legal/regulatory changes and

payments product innovation across all payments channels

• More often than not, payments regulation is reactive – payments

innovation is driving legal change

• Expect accelerating regulatory reaction to perceived unfair, deceptive

or abusive practices (overdraft fees, prepaid card fees, binding

arbitration, etc.)

• Expect more, not less, unintended consequences

• Be careful (and thoughtful) – it’s a compliance jungle out there

3

4

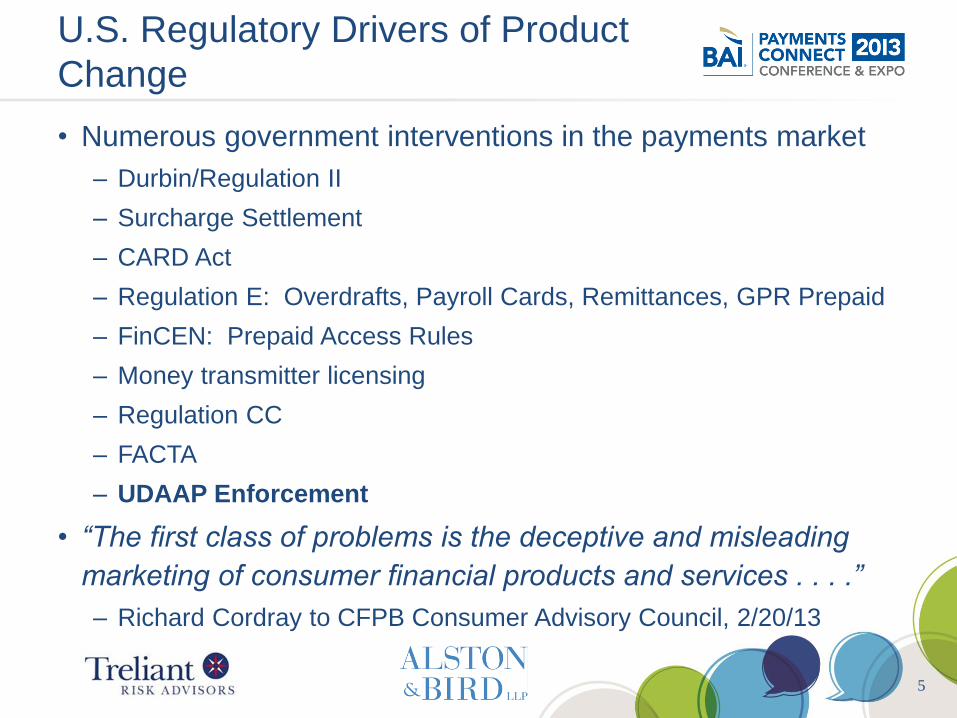

U.S. Regulatory Drivers of Product

Change

• Numerous government interventions in the payments market

– Durbin/Regulation II

– Surcharge Settlement

– CARD Act

– Regulation E: Overdrafts, Payroll Cards, Remittances, GPR Prepaid

– FinCEN: Prepaid Access Rules

– Money transmitter licensing

– Regulation CC

– FACTA

– UDAAP Enforcement

• “The first class of problems is the deceptive and misleading

marketing of consumer financial products and services . . . .”

– Richard Cordray to CFPB Consumer Advisory Council, 2/20/13

5

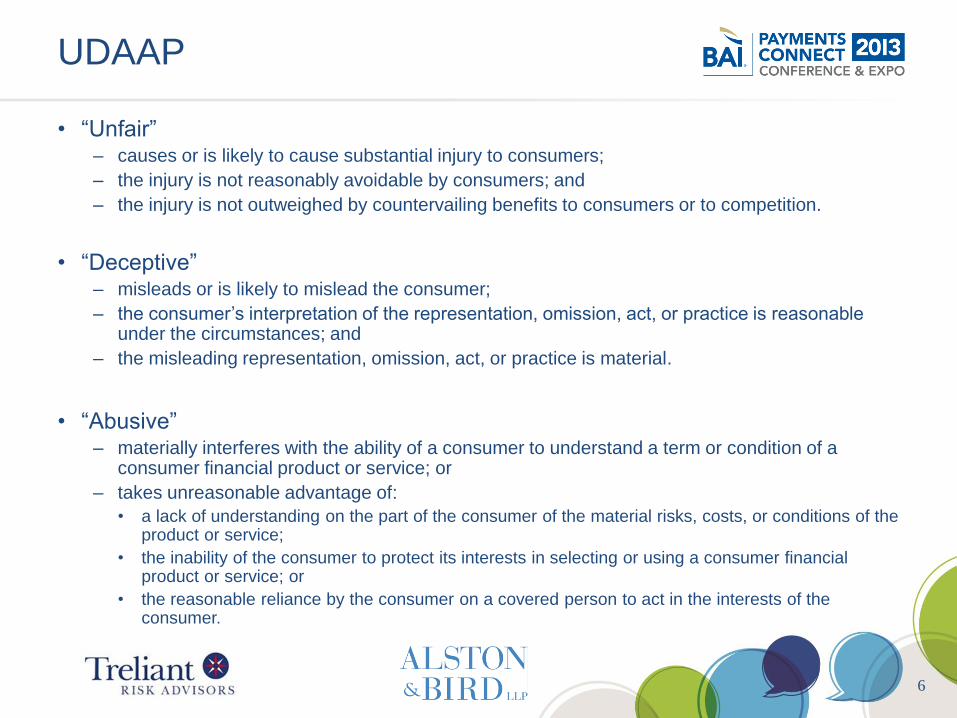

UDAAP

• “Unfair” – causes or is likely to cause substantial injury to consumers;

– the injury is not reasonably avoidable by consumers; and

– the injury is not outweighed by countervailing benefits to consumers or to competition.

• “Deceptive” – misleads or is likely to mislead the consumer;

– the consumer’s interpretation of the representation, omission, act, or practice is reasonable under the circumstances; and

– the misleading representation, omission, act, or practice is material.

• “Abusive”

– materially interferes with the ability of a consumer to understand a term or condition of a consumer financial product or service; or

– takes unreasonable advantage of:

• a lack of understanding on the part of the consumer of the material risks, costs, or conditions of the product or service;

• the inability of the consumer to protect its interests in selecting or using a consumer financial product or service; or

• the reasonable reliance by the consumer on a covered person to act in the interests of the consumer.

6

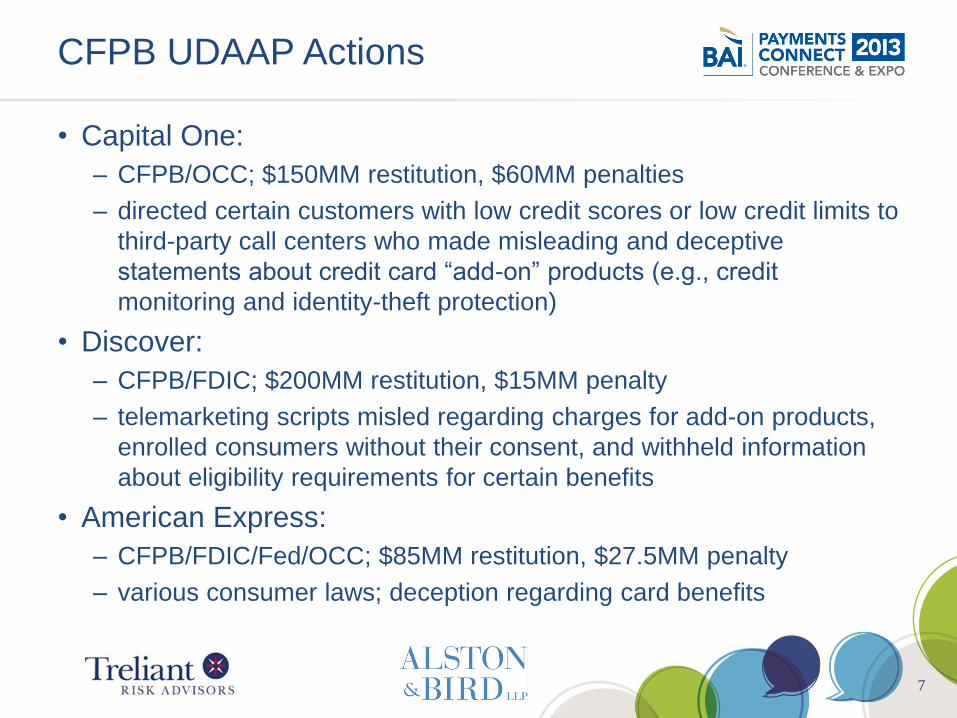

CFPB UDAAP Actions

• Capital One:

– CFPB/OCC; $150MM restitution, $60MM penalties

– directed certain customers with low credit scores or low credit limits to

third-party call centers who made misleading and deceptive

statements about credit card “add-on” products (e.g., credit

monitoring and identity-theft protection)

• Discover:

– CFPB/FDIC; $200MM restitution, $15MM penalty

– telemarketing scripts misled regarding charges for add-on products,

enrolled consumers without their consent, and withheld information

about eligibility requirements for certain benefits

• American Express:

– CFPB/FDIC/Fed/OCC; $85MM restitution, $27.5MM penalty

– various consumer laws; deception regarding card benefits

7

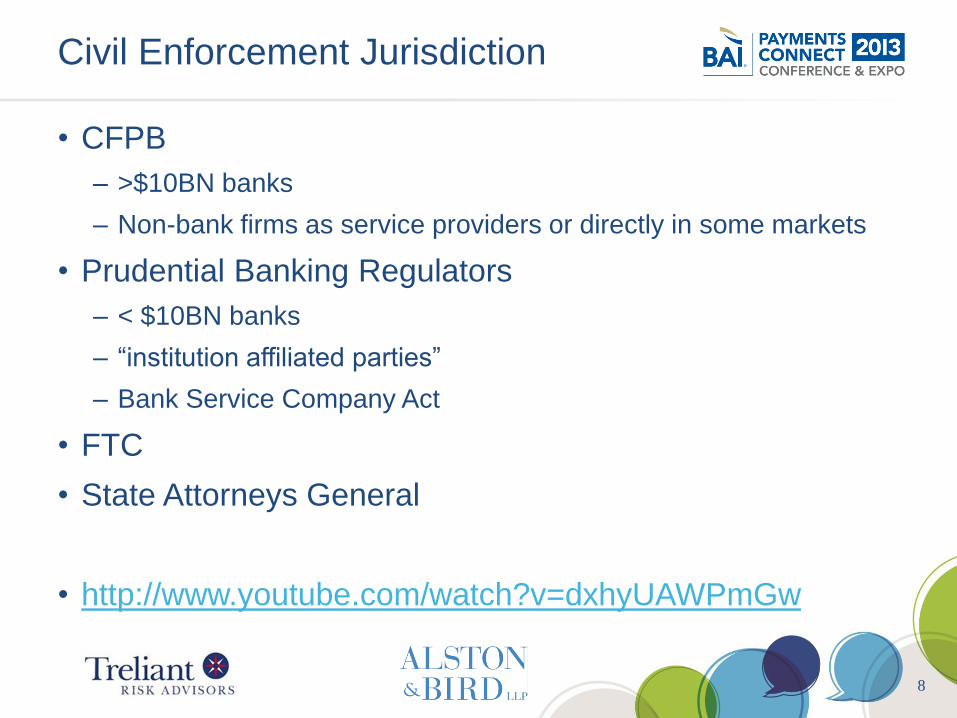

Civil Enforcement Jurisdiction

• CFPB

– >$10BN banks

– Non-bank firms as service providers or directly in some markets

• Prudential Banking Regulators

– < $10BN banks

– “institution affiliated parties”

– Bank Service Company Act

• FTC

• State Attorneys General

• http://www.youtube.com/watch?v=dxhyUAWPmGw

8

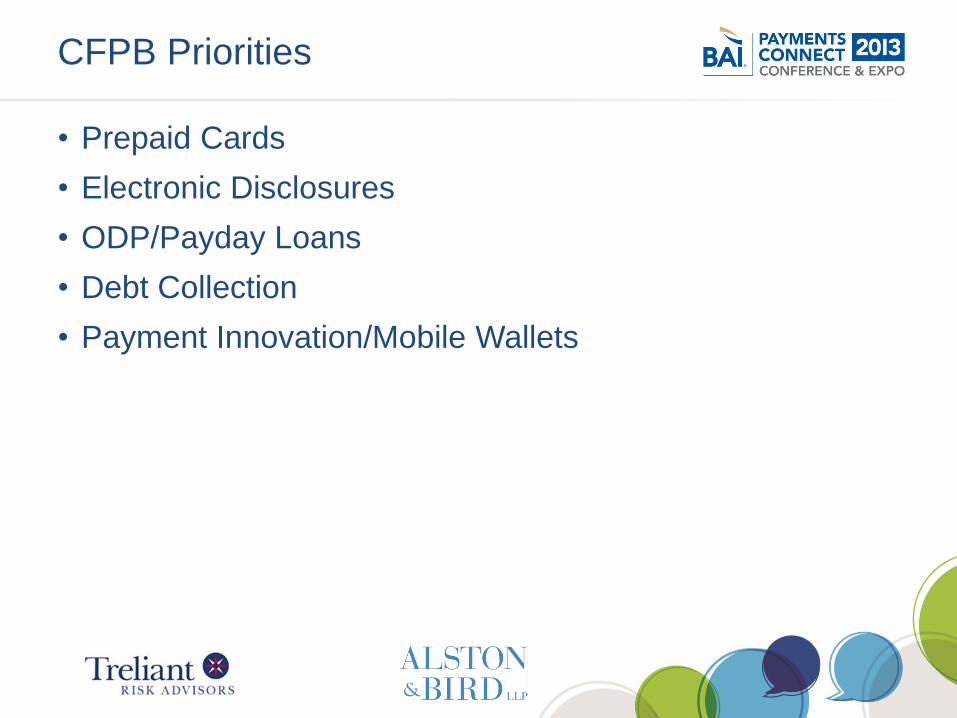

CFPB Priorities

• Prepaid Cards

• Electronic Disclosures

• ODP/Payday Loans

• Debt Collection

• Payment Innovation/Mobile Wallets

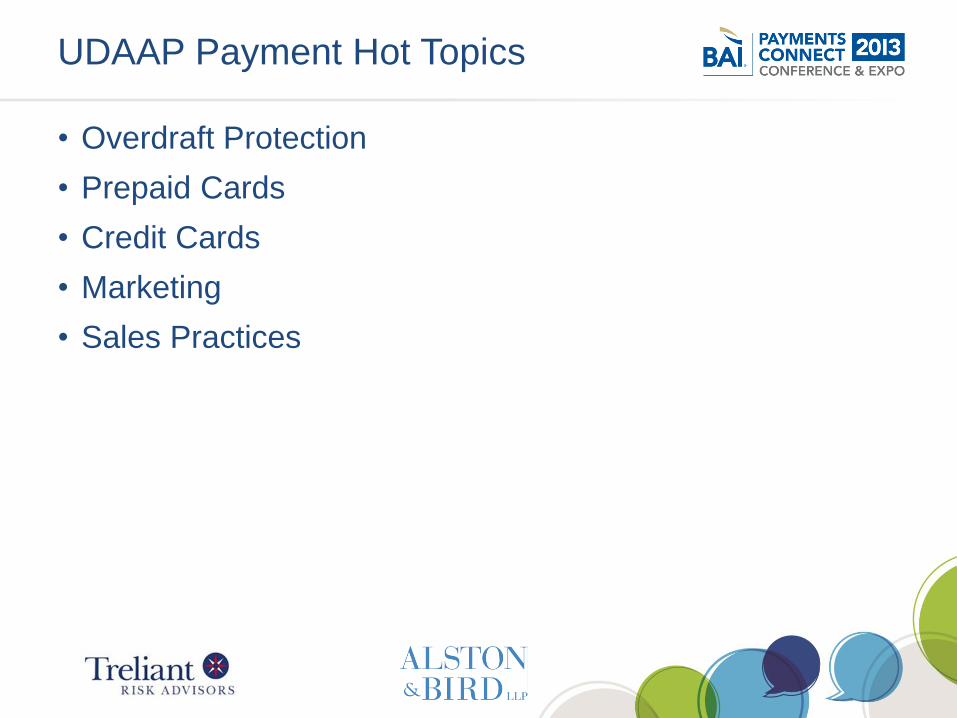

UDAAP Payment Hot Topics

• Overdraft Protection

• Prepaid Cards

• Credit Cards

• Marketing

• Sales Practices

Example #1

• Non-enforcement action examination finding

• Restitution required

• Approximately $25 million

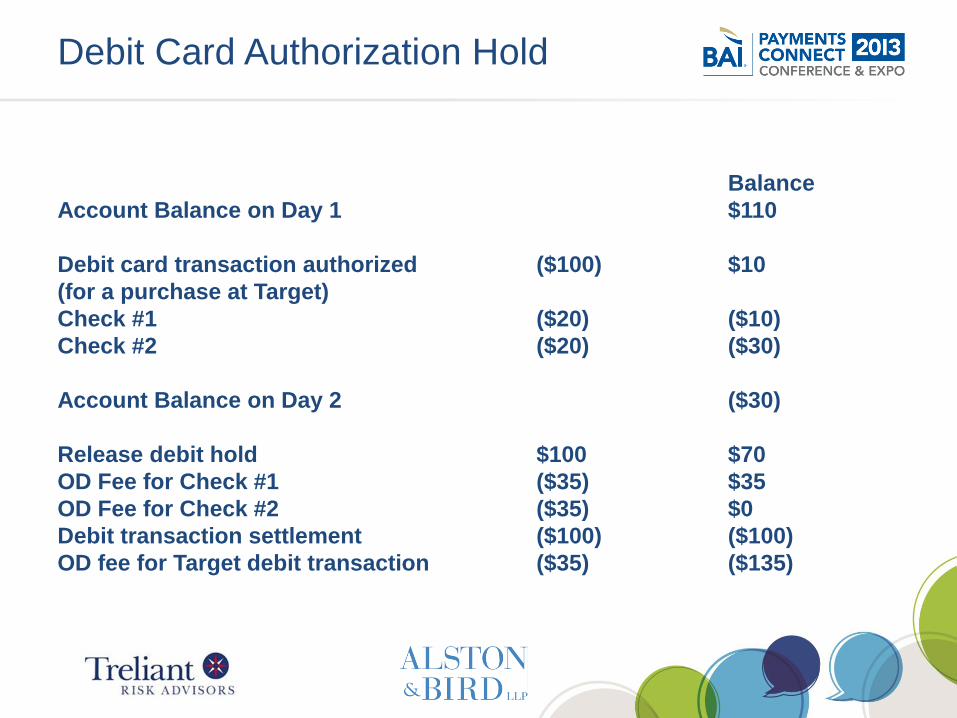

Debit Card Authorization Hold

Balance

Account Balance on Day 1 $110

Debit card transaction authorized ($100) $10

(for a purchase at Target)

Check #1 ($20) ($10)

Check #2 ($20) ($30)

Account Balance on Day 2 ($30)

Release debit hold $100 $70

OD Fee for Check #1 ($35) $35

OD Fee for Check #2 ($35) $0

Debit transaction settlement ($100) ($100)

OD fee for Target debit transaction ($35) ($135)

Example #2

FDIC Enforcement Action against

Higher One, Inc.

The Bancorp Bank

Multiple NSF fees on prepaid cards marketed to college

students

Four Pillars for Product Fairness

• Value

• Predictability

• Understanding

• Appropriateness

These principles should be applied to the bank’s products,

services and practices. They should also be applied to third

party vendor activities and products.

Value

The consumer receives value that is

reasonably related to the cost of the product

or service.

Predictability

The consumer can predict how the product

or service will perform.

Understanding

The consumer understands the terms and

conditions of the product or service

(particularly any limitations or exclusions).

Appropriateness

The bank provides products that are

appropriate for their customers and their

customers can rely on the bank to show

them the most appropriate product.

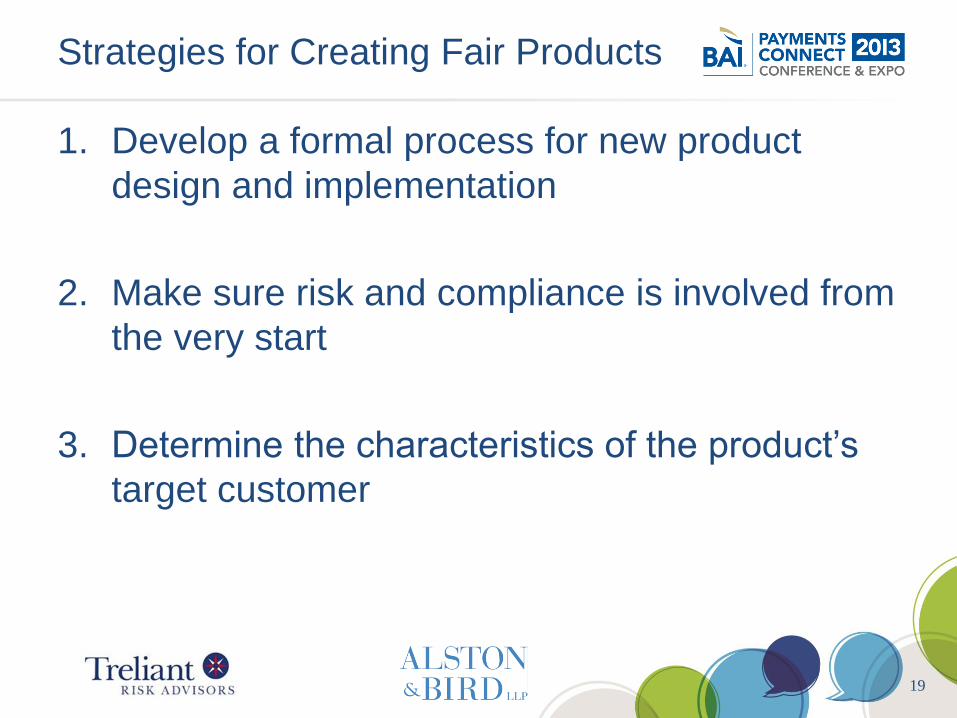

Strategies for Creating Fair Products

1. Develop a formal process for new product

design and implementation

2. Make sure risk and compliance is involved from

the very start

3. Determine the characteristics of the product’s

target customer

19

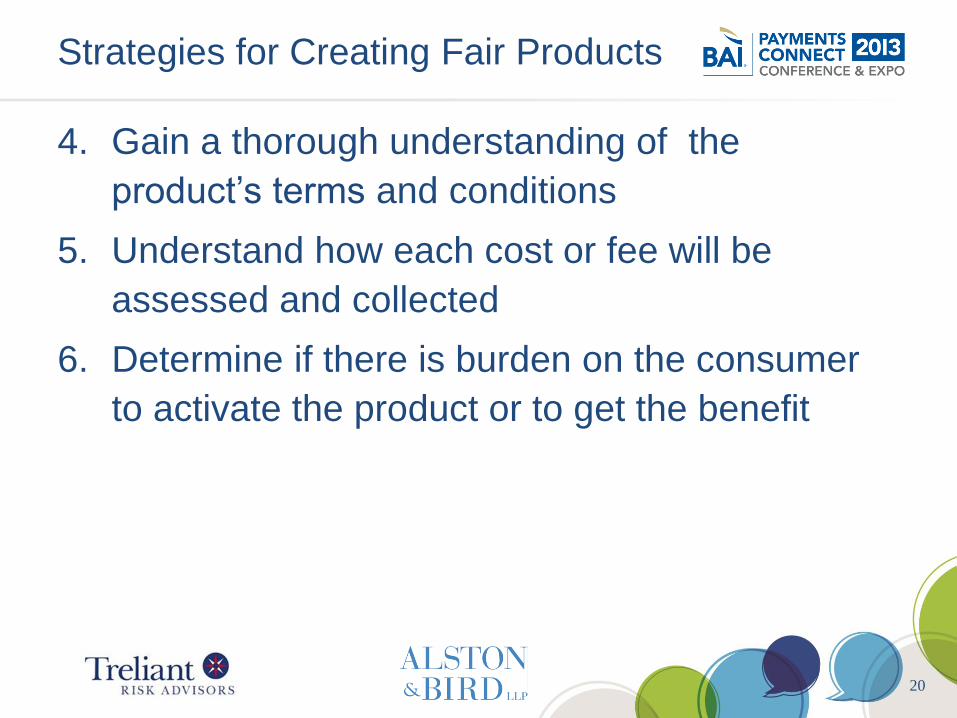

Strategies for Creating Fair Products

4. Gain a thorough understanding of the

product’s terms and conditions

5. Understand how each cost or fee will be

assessed and collected

6. Determine if there is burden on the consumer

to activate the product or to get the benefit

20

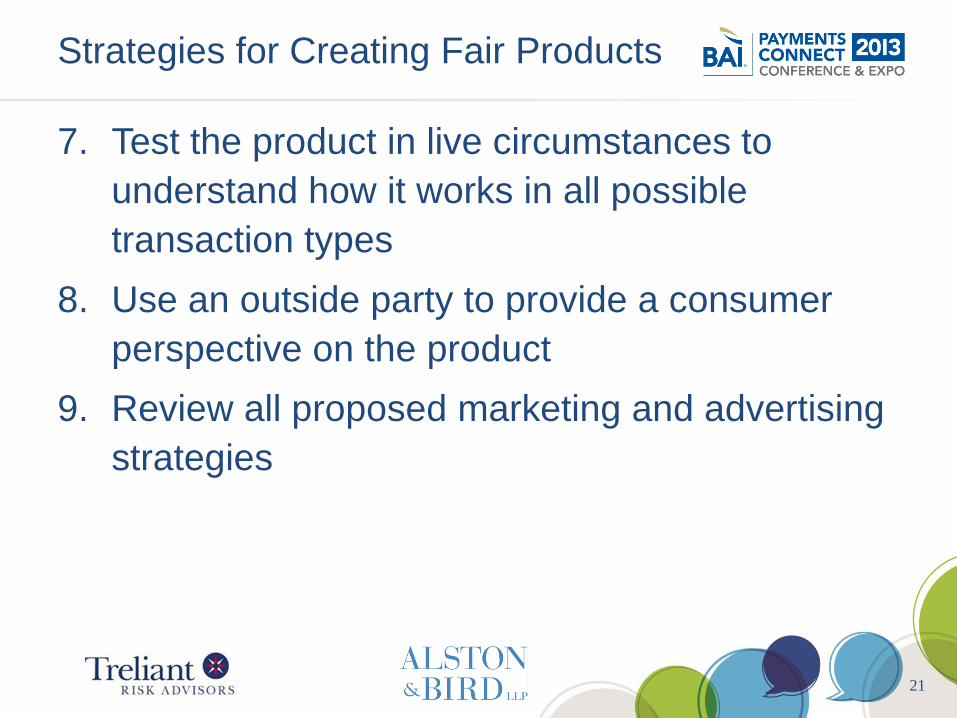

Strategies for Creating Fair Products

7. Test the product in live circumstances to

understand how it works in all possible

transaction types

8. Use an outside party to provide a consumer

perspective on the product

9. Review all proposed marketing and advertising

strategies

21

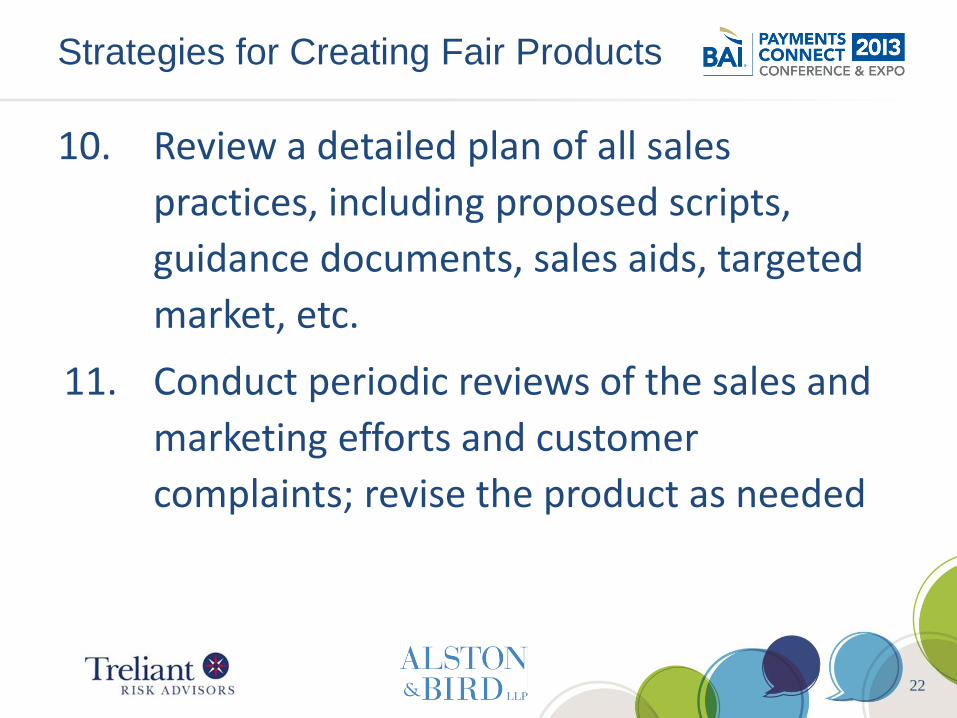

Strategies for Creating Fair Products

10. Review a detailed plan of all sales

practices, including proposed scripts,

guidance documents, sales aids, targeted

market, etc.

11. Conduct periodic reviews of the sales and

marketing efforts and customer

complaints; revise the product as needed

22

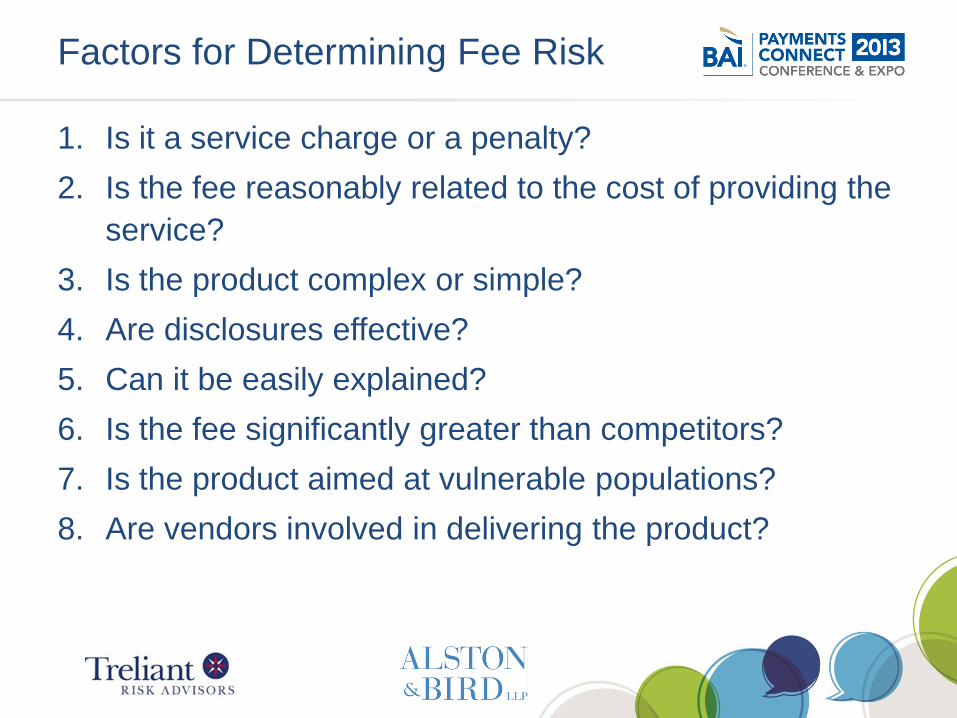

Factors for Determining Fee Risk

1. Is it a service charge or a penalty?

2. Is the fee reasonably related to the cost of providing the

service?

3. Is the product complex or simple?

4. Are disclosures effective?

5. Can it be easily explained?

6. Is the fee significantly greater than competitors?

7. Is the product aimed at vulnerable populations?

8. Are vendors involved in delivering the product?

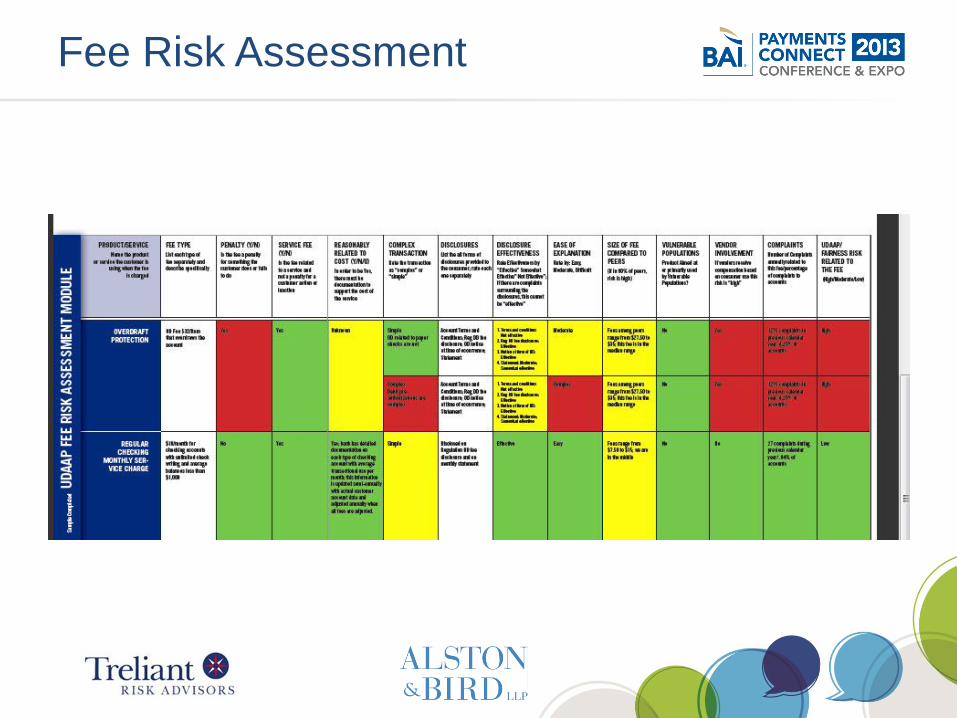

Fee Risk Assessment

Recommendations

• Make sure your disclosures and agreements (including

authorizations) comply with current laws

• Consider the current legal landscape and the costs/benefits of

conforming “gray area” products to the most nearly applicable law

• Consider legal developments on the horizon and ensure product and

legal agreement flexibility to accommodate anticipated and

unanticipated changes

• The future may hold more, not less, legal uncertainty, particularly as

the pace of payments product innovation accelerates – make sure

your compliance decisions are informed and consistent with your

organization’s risk tolerances

25

26

Lyn Farrell, CRCM, CAMS

Treliant Risk Advisors, LLC

713-204-9500

Cliff Stanford

Alston & Bird LLP

404-881-7833