Embed Size (px)

Citation preview

PRELIMINARY RESULTS FOR THE 52 WEEKS

ENDED 26 JUNE 2021

OVERVIEW

• The foundations of the business are strong and the fundamental drivers remain solid

• Key success factors:

• Resilient people and culture

• Three legged strategy brings balance

• Excellent licensee relationships

• Adaptability and agility of senior team

• Retail opportunities with outside space

• Cost and cash control has been meticulous

• Trade has been encouraging since the restart. We are likely to face further supply chain

and other challenges

2

KEY GOVERNANCE CHANGES IN 2021

• Adoption of QCA code

• Independent Directors

• Expanded Directors disclosures

• Enhanced Governance sections in the Annual Report

• Transition to IFRS

• Appointment of new auditors: BDO from Deloitte

• Appointment of Senior Independent Director

• Establishment of Operations Committee

3

BOARD CHANGES

4

Richard Oldfield Appointed Chairman

Hilary Riva Appointed Senior Independent Director

Mark Rider Appointed Chief Financial Officer

Nigel Bunting

Kevin Georgel Appointed Non Executive Director

• Will become Commercial Director at the end of the Financial year • Currently recruiting for Director of Retail Pub Operations

NET ASSETS AND DIVIDEND PER SHARE

• No dividend will be declared for 2021

• NAV Per Share has fallen as a result of IFRS transition and accumulated losses due to Covid

• The company carried out a valuation of licensed assets as at end June 2021 which shows a

surplus over book value of £35.9m, +13%

5 * Net assets at the reporting date divided by the number of shares in issue being 14,857,500 50p shares

*

CHIEF FINANCIAL OFFICER MARK RIDER

6

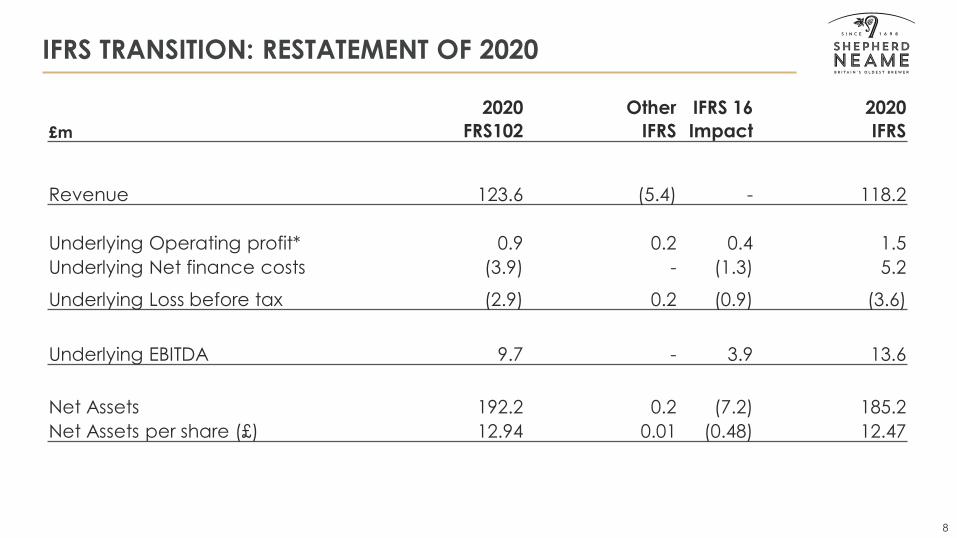

TRANSITION TO IFRS

• Adoption of International Financial Reporting Standards as adopted by the European

Union with a date of transition 29 June 2019

• Results for the 52 weeks to 27 June 2020 restated under IFRS

• IFRS regarded as the accepted accounting standards for publically listed companies and

allows easier comparison of performance to peer companies

• FRS102 broadly aligned to IFRS but key impacts result from IFRS16 where leases now

capitalised on balance sheet with corresponding level of debt

7

29 June 2019

Date of transition

27 June 2020

Previous Results restated under IFRS

26 June 2021

First Results under IFRS

IFRS TRANSITION: RESTATEMENT OF 2020

8

2020 Other IFRS 16 2020

£m FRS102 IFRS Impact IFRS

Revenue 123.6 (5.4) - 118.2

Underlying Operating profit* 0.9 0.2 0.4 1.5

Underlying Net finance costs (3.9) - (1.3) 5.2

Underlying Loss before tax (2.9) 0.2 (0.9) (3.6)

Underlying EBITDA 9.7 - 3.9 13.6

Net Assets 192.2 0.2 (7.2) 185.2

Net Assets per share (£) 12.94 0.01 (0.48) 12.47

2020 AND 2021 KEY METRICS

9

2021 2020

Underlying results £m £m

Revenue 86.9 118.2

Operating (loss)/profit (4.2) 1.5

Finance costs Pre IFRS 16 (4.5) (3.9)

Total net finance costs (5.8) (5.2)

Profit before tax (10.1) (3.6)

Tax rate (%) 18.6 12.3

Loss per share (pence) (55.5) (21.7)

Full year dividend per share (pence) Nil Nil

Reconciliation to statutory profit

Total items excluded from underlying results (6.4) (17.3)

Statutory loss before tax (16.4) (21.0)

CONTINUOUS FOCUS ON CASH FLOW AND DEBT

10

• Tight cost control and focus on

cash

• Decrease in HMRC liabilities that

were delayed in the prior year

• Bank and Private Placement debt

increased due to closure periods

• Lease liabilities increased due to

modifications agreed with

landlords

84.5 90.8

11.0 2.4

55.9 58.3

0.0

20.0

40.0

60.0

80.0

100.0

June 2020 June 2021

Net Debt (£m)

Bank and Private placement debt

Liabilities deferred as agreed with HMRC

IFRS16 lease debt

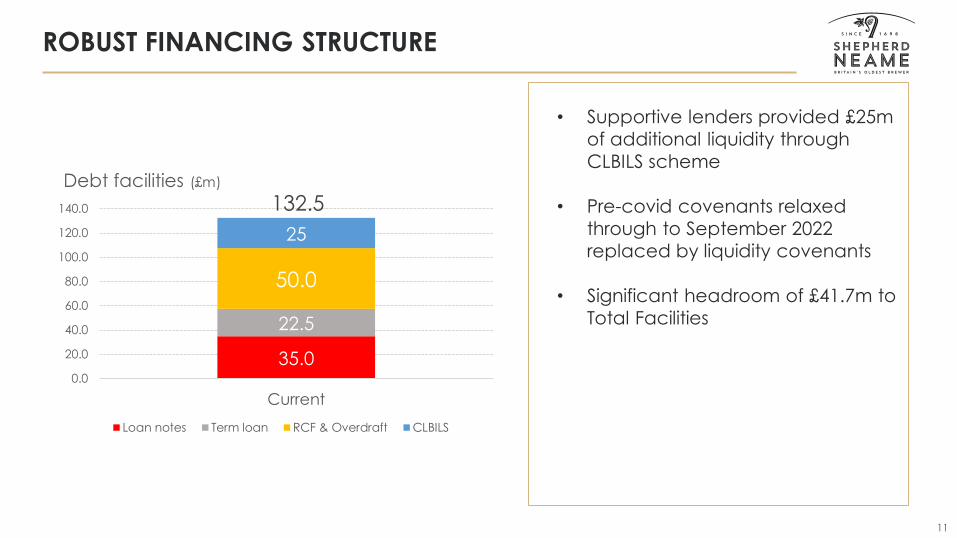

ROBUST FINANCING STRUCTURE

11

• Supportive lenders provided £25m

of additional liquidity through

CLBILS scheme

• Pre-covid covenants relaxed

through to September 2022

replaced by liquidity covenants

• Significant headroom of £41.7m to

Total Facilities

35.0

22.5

50.0

25

132.5

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Current

Debt facilities (£m)

Loan notes Term loan RCF & Overdraft CLBILS

CHIEF EXECUTIVE JONATHAN NEAME

12

OVERVIEW

• Demand for the great British pub experience is as strong

as ever

• We achieved record grocery sales during period of

restrictions. Export sales remain strong

• The company weathered lockdown through tight cash

management and £15m government support

• Sales have grown progressively over the summer and

autumn

• The return to work in September has driven higher than

anticipated sales in the City of London

• The supply chain and inflation outlook is challenging in

the short term

13

The Rose in June, Margate

OUR STRATEGIC GOALS

RECRUIT NEW CUSTOMERS

DELIGHT THEM WITH GREAT

EXPERIENCES

BUILD A GREAT TEAM

OF DEDICATED

PEOPLE

CREATE PASSIONATE ADVOCATES

FOR OUR BEER AND PUBS

OUR STRATEGIC

GOALS

14

Be trusted to do the right thing for our communities

THE FUNDAMENTAL DRIVERS FOR OUR BUSINESS REMAIN

STRONG

15

Tenanted Pubs Managed Pubs Brewing and Brands

Segment

characteristics

• Typically freehold,

operated by

independent licensees

• Revenue derived from

sale of drinks and rent

• Managed directly by SN

employees

• Retail revenue from sale

of drinks, food and

accommodation

• Manufacturer and

wholesaler of portfolio of

drinks to on and off trade

Financial

characteristics

• Stable levels of growth

• Capex to maintain high

standards

• Highly cash generative

• Higher levels of growth

but greater capital

intensity to transform

offer

• Largest division by

turnover

• Lowest margin but least

capital intensive

• Cash generative

Value to the

business

• Bedrock of cash

generation

• Principal area of

investment and of

growth

• National brand presence

• Distinctive portfolio is USP

for pub estate

• Significant local housing and infrastructure development

• Local population expected to rise by 20% by 2031

EMERGING TRENDS

16

• Experience led socialising

• Al fresco Hospitality

• Booming Suburbs

• City Centres Return to Strength

• Hybrid working

• Mid-week flourish

• Premium Experiences offer growth potential

The Britannia, Guildford

Truly at Pub in the Park

THE GREAT RE-OPENING: CONSUMER CONFIDENCE RETURNS

17

The East Kent, Whitstable

Betsy Trotwood, London

12 April – 16 May

% 2019 sales1

17 May – 26 June

% 2019 sales1

Retail Pubs (Open Days)

62% 97%

Tenanted Pubs (Volume)

77% 91%

Total Beer (Volume)

+8.4%

• Two thirds of all pubs opened on 12 April 2021 to

utilise their outside space

• 15 pubs remained closed in London until the end of

August 2021

1. The periods referred to are the comparative month(s) during the financial year 52 weeks to 29

June 2019.

THE ROAD TO NORMALITY: RETAIL PUBS

18 Albion Taverna, Faversham

Same outlet like-

for-like

18 Weeks to 30 October 2021

% 2019 sales1 vs 20202

Retail Pubs (like-for-like sales)

91% +37.0%

Reopening of the City of London

• Food and accommodation sales have been strong

since the restart. Occupancy is at 81% as a result of

staycations

• Drinks sales were behind 2019 in the summer but

have recovered in the Autumn as the return to

offices has driven a faster recovery than expected in

London

• On 1 November we exchanged on the sale of two

hotels that no longer fit our profile for £5.75m

1. The periods referred to are the comparative month(s) during the financial year 52 weeks to 27 June 2020.

2. The periods referred to are the comparative month(s) during the financial year 52 weeks to 26 June 2021.

THE ROAD TO NORMALITY: RETAIL FOOD, DRINK AND

ACCOMMODATION

19

Same outlet like-

for-like

18 Weeks to

30 October 2021

% 2019

sales1 vs 20202

Retail Food 106% +22.2%

Same outlet like-

for-like

18 Weeks to

30 October 2021

% 2019

sales1 vs 20202

Retail Drinks 76% +49.1%

Same outlet like-

for-like

18 Weeks to

30 October 2021

% 2019

sales1 vs 20202

Retail

Accommodation 129% +44.0%

1. The periods referred to are the comparative month(s) during the financial year 52 weeks to 27 June 2020.

2. The periods referred to are the comparative month(s) during the financial year 52 weeks to 26 June 2021.

THE ROAD TO NORMALITY: TENANTED PUBS

20

Same outlet like-

for-like

13 Weeks to 25 September 2021

% 2019 sales1 vs 20202

Tenanted Pubs

net income 93% +26.2%

• Excellent support for our licensees throughout

pandemic, has strengthened reputation and

relationships

• Full rent restored by August 2021. Licensee turnover

low

• Supply chain disruption in August/September is now

easing

The Earl Grey, Northfleet

The Rose in June, Margate 1. The periods referred to are the comparative month(s) during the financial year 52 weeks to 27 June 2020.

2. The periods referred to are the comparative month(s) during the financial year 52 weeks to 26 June 2021.

OUR PUB PROFILE: 2021

21

2019 Acquisitions Net transfers Disposals 2021

Tenanted 239 - (1) (3) 235

Managed 70 1 (4) (2) 65

Investment

Properties 13 - 5 (8) 10

Total 322 1 - (13) 310

• 100% of the estate is in the south east • 85% of pub estate is freehold • Revaluation of Pub estate at June 2021 showed surplus overbook value of £35.9m +13%

• Over the past 10 years 78 pubs and a number of investment properties have been

disposed of for total proceeds of £47.4m. 36 pubs have been acquired at a cost of

£66.2m

WE HAVE INVESTED £3.9M CAPITAL EXPENDITURE IN

ESSENTIAL PROJECTS

22

Completed the

acquisition on

the Ebbsfleet

site, The Chalk

Yard.

The Juggs, Lewes The Imperial, Southborough

Yeast Propagation Plant

Inward investment will

increase in 2022 and

return to pre

pandemic levels in

2023

THE ROAD TO NORMALITY: BREWING AND BRANDS

23

18 Weeks to 30 October 2021

% 2019 sales1 vs 20202

Total Beer (Volume)

106% +9.6%

18 weeks to 30 October 2021

% 2019 sales1 vs 20202

Total Own Beer (Volume)

93% +1.6%

Drive brands

Exploiting New Opportunities

1. The periods referred to are the comparative month(s) during the financial year 52 weeks to 27 June 2020.

2. The periods referred to are the comparative month(s) during the financial year 52 weeks to 26 June 2021.

BUILDING BETTER BRANDS FOR THE FUTURE

24

Southampton Boat Show

Live and Unlocked

Broadstairs Folk Week

Gone Wild

We have supported

more events and

music festivals this

summer than ever

before

BUILDING ON LOCAL PARTNERSHIPS

25

We are delighted to

have been the official

beer provider of The

Open Golf and the

sponsor of the

victorious Kent Cricket

T20 side

SKILLS SHORTAGES AND SUPPLY CHAIN CHALLENGES

• Skills shortages exist in many sectors. We have

relaunched our Chef and Front of House Apprentice

programme

• Inflation in the hospitality sector is running at c14%.

Key drivers are:

• Logistics and Supply Chain

• Energy and energy related products

• Employment costs

• Prices are likely to rise in pubs mitigated in part by

extended rates relief for independent pubs and by

alcohol duty changes

26

Apprentice Brandon Raines shortlisted for Purple Umbrella Award

Apprentice Jodie Butcher won Purple Umbrella Award

GOVERNMENT POLICY

• Coronavirus job retention scheme ended on 30 September

• VAT increased from 5% to 12.5% on 1 October, and moves to 20% on March 2022

• Pubs will continue to receive 66% business rates relief until 1 April 2022 and then our

tenanted pubs will receive 50% relief through to March 2023

• Industry continues to seek business rate reform

• Alcohol duties to be realigned from 2023 with the following impacts:

• Simplification of alcohol banding

• Preferential rate of duty for beers under 3.4%abv and higher rate of duty for beers

above 8.5%abv

• 5% lower duty differential for draught beer

• Additional benefits for cider and English wine producers

27

THE YEAR AHEAD

• Demand trends remain strong but ongoing caution about

further restrictions

• Supply chain and inflation will continue to be challenging

into 2022

• Board focused on tight cash management and net debt

reduction

• Plan to return to prior levels of investment and restore the

dividend as soon as circumstances allow

• Board following recovery plan is:

• 2021 – Stabilise

• 2022 – Reduce debt. Prepare for growth

• 2023 – The new normal

28

Albion Taverna, Faversham

QUESTIONS

29