Embed Size (px)

Citation preview

Potential MBTA Fare Increaseand Service Changes in 2012:Scenario 3 Impact AnalysisA report produced for the Massachusetts Bay Transportation Authority by the Central Transportation Planning Staff

Potential MBTA Fare Increase and Service Changes in 2012: Scenario 3 Impact Analysis

Project ManagerRobert Guptill

Project PrincipalElizabeth Moore

Data AnalystsGrace King Robert Guptill

Graphics Robert Guptill

Cover DesignKim Noonan

The preparation of this document was funded by the Massachusetts Bay Transportation Authority.

Produced for the Massachusetts BayTransportation Authority by the Central Transportation Planning Staff CTPS is directed by the Boston Region Metropolitan Planning Organization. The MPO is composed of state and regional agencies and authorities, and local governments.

March 28, 2012

To request additional copies of this document orcopies in an accessible format, contact:

Central Transportation Planning Staff State Transportation Building Ten Park Plaza, Suite 2150 Boston, Massachusetts 02116

(617) 973-7100 (617) 973-8855 (fax) (617) 973-7089 (TTY)

[email protected] www.bostonmpo.org

SOUTH-BOROUGH

HUDSON

MARLBOROUGH

SHERBORN

NATICK

SUDBURYWALTHA

WELLESLEY

WATERTOW

NEWTON

WOBURN

STON

EHA

WAKE-FIELD

HOPKINTON

NEEDHAM

DOVER

FOXBOROUGH

MILLIS

HOLLISTONMEDFIELD

NORFOLK

WALPOLMILFORD

MEDWAY

FRANKLIN

DUXBURY

CANTON

SHARON

NORWOOD

HINGHAM

HANOVER

MILTON

NORWELL

QUINCY

READING

MEDFORD

PEABODY

SWAMPSCOTT

REVEREMALDEN

EVERETT

MELROSENAHANT

LYNN

SALEM MARBLEHEAD

ROCKPOR

IPSWICH

WENHAM

MIDDLE-TON

DANVERS

TOPS-

MANCHESTERBEVERLY

ESSEX GLOUCESTER

CONCORD

CARLISLE

LINCOLN

BEDFORD

STOWBOLTON

LITTLE-TON

ACTON

SOMERVILLE

CAMBRIDGE

BRO

OKL

INE

STOUGH-

BEL

LIN

GH

AM

WRENTHAM

WESTW

OOD

WAY

LAN

D

ASHLAND

FRAMIN

GH

AM

BOX-BOR-

OUGH

MAY-NARD

BELMO

NTWESTO

N

DEDHAM

LEXINGTON

ARLINGTO

WINCHESTE

R

BUR-LINGTON

WILMING-TON LYN

NFIELD

COHASSET

HOL-BROOK

BRAINTREE

RAND

OLPH RO

CKLA

ND

WEY

-MO

UTH

PEMBROKE

SCITUATE

MARSHFIELD

HULLBOSTON

WINTHROP

SAU

GU

S

CHELSEA

HAMILTON

NORTHREADING

CTPS 3/28/2012 iii

ABSTRACT This analysis estimates various impacts of a potential scenario for MBTA pricing and service aimed at reducing a projected budget deficit. The proposed scenario raises most of its projected revenue through a fare increase; it also includes service changes that eliminate some of the MBTA’s least cost-effective services. The ridership, revenue, air quality, and environmental justice impacts of these measures are estimated. Two different modeling methodologies are used to produce these projections. The two models are complementary; in addition, producing two sets of estimates provides a range of possible impacts.

iv 3/28/2012 Boston Region MPO

Acknowledgments We wish to thank Charles Planck, Melissa Dullea, and Greg Strangeways of the MBTA for their participation in the analysis of various fare increase and service change scenarios.

CTPS 3/28/2012 v

CONTENTS List of Exhibits vii

EXECUTIVE SUMMARY ix

1 INTRODUCTION 1

2 DESCRIPTION OF PROPOSED FARE INCREASE/SERVICE CHANGE SCENARIO 3

2.1 Fare Structure Changes 3 2.2 Service Changes 5 2.2.1 Bus 5 2.2.2 Rapid Transit, Commuter Rail, Ferry, and THE RIDE 7 2.2.3 Summary of Service Changes 9 2.3 Fare Increase: Single-Ride Fares, Pass Prices, and Parking Rates 13

3 METHODS USED TO ESTIMATE RIDERSHIP AND REVENUE 19 3.1 CTPS Spreadsheet Model Approach 19 3.1.1 Modeling of Existing Ridership and Revenue 19 3.1.2 Estimation of Ridership Changes Resulting from a Fare Increase 21 3.2 Boston Region MPO Travel Demand Model Set Approach 22 3.3 Differences between the Two Estimation Methodologies 24

4 RIDERSHIP AND REVENUE IMPACTS 25 4.1 Overview of Results and Methodology 25 4.2 Spreadsheet Model Estimates 25 4.2.1 Projections 25 4.2.2 Sensitivity Analysis 26 4.2.3 Total Revenue Estimate 27 4.3 Regional Travel Demand Model Set Estimates 27

CONTENTS

vi 3/28/2012 Boston Region MPO

4.3.1 Projections 27 4.3.2 Total Revenue Estimate 28 4.4 Comparison of Model Results: Ranges of Projected Impacts 29

5 AIR QUALITY IMPACTS 33 5.1 Background 33 5.2 Estimated Air Quality Impacts 34

6 ENVIRONMENTAL JUSTICE IMPACTS 37 6.1 Definition of Environmental Justice Communities 37 6.2 Equity Determination 37 6.2.1 Transit Equity Metrics 38 6.2.2 Highway Congestion and Air Quality Equity Metrics 39 6.2.3 Accessibility Equity Metrics 40 6.2.4 Summary of Equity Impacts 40

7 CONCLUSIONS 43

APPENDIX: SPREADSHEET MODEL METHODOLOGY A.1 Apportionment of Existing Ridership A-1 A.2 Price Elasticity Estimation A-1 A.3 Price Elasticity A-3 A.4 Diversion Factors A-4 A.5 Examples of Ridership and Revenue Calculations A-5

CTPS 3/28/2012 vii

EXHIBITS

Figure

2-1 Scenario 3 Weekday Bus, Rapid Transit, and Ferry Service Changes 10 2-2 Scenario 3 Saturday Bus, Rapid Transit, and Ferry Service Changes 11 2-3 Scenario 3 Sunday Bus, Rapid Transit, and Ferry Service Changes 12 2-4 Percentages of Riders Affected and Unaffected by the Proposed

Scenario 3 Service Changes 13

Table E-1 Range of Revenue and Ridership Projections for the Proposed Fare

Increase and Service Changes x 2-1 MBTA-Operated Bus Routes with Average Net Cost per Passenger

(Subsidy) Greater than 3.5 Times the Systemwide Average, by Day of Week 5

2-2 Percentage of Service Affected 13 2-3 Key Single-Ride Fares: Existing and Proposed 14 2-4 Pass Prices: Existing and Proposed 15 2-5 Park-and-Ride Facility Rates: Existing and Proposed 16 2-6 Weighted Average Percentage Change in Average Fares, by Modal

Category, for Unlinked Trips 17 3-1 Price Elasticity Ranges Used in the Spreadsheet Model 22 4-1 Spreadsheet Model Estimates of Annual Ridership and Fare Revenue

Impacts 26 4-2 Spreadsheet Model Ranges of Estimates of Annual Ridership and Fare

Revenue Impacts Using Low and High Ranges of Elasticities 27 4-3 Spreadsheet Model Estimates of Total Revenue Change: Combined

Fare Revenue Gains and Saved Operating Costs 27 4-4 Travel Demand Model Set Estimates of Annual Ridership and Fare

Revenue Impacts 28

EXHIBITS

viii 3/28/2012 Boston Region MPO

4-5 Travel Demand Model Set Estimates of Total Revenue Change: Combined Fare Revenue Gains and Saved Operating Costs 28

4-6 Range of Ridership Projections 30 4-7 Range of Fare Revenue Projections 30 4-8 Range of Projections for Total Revenue: Combined Fare Revenue

Gains and Saved Operating Costs 31 5-1 Projected Average Weekday Changes in Selected Pollutants

(Regionwide) 35 6-1 Existing and Projected Measures of Transit Equity Metrics 41 6-2 Existing and Projected Measures of Highway Congestion and Air

Quality Equity Metrics 41 6-3 Existing and Projected Measures of Accessibility Equity Metrics 42 A-1 AFC Fare Categories A-1 A-2 AFC Modal Categories A-2 A-3 Single-Ride and Pass Elasticities by Fare Type and Mode A-3

KEYWORDS ridership revenue air quality environmental justice fare increase service reduction

CTPS 3/28/2012 ix

EXECUTIVE SUMMARY The Massachusetts Bay Transportation Authority (MBTA) faced a projected $185 million operating budget deficit for fiscal year (FY) 2013 (July 1, 2012–June 30, 2013). A series of one-time financial and administrative actions were taken to reduce the projected deficit to $161 million. This report identifies a combination of new fare revenues and operating cost savings through targeted service reductions to address the remaining $161 million projected deficit. The MBTA will continue to advance the operational and administrative efficiencies undertaken since the implementation of forward funding in 2000 and transportation reform in 2009, but it has limited means by which to raise revenue sufficiently to close this operating budget deficit. The primary means are raising fares, reducing service, or a combination of both. The MBTA has developed three potential scenarios, each of which employs the combination approach in different ways. Scenarios 1 and 2, described in a separate report, raise enough revenue to close the FY 2013 budget gap.

Scenario 3, described in the present report, raises fares and reduces service less than Scenarios 1 and 2 and consequently does not close the entire FY 2013 budget gap. It is projected to result in an increase in revenue of $88.3 million to $91.6 million. This scenario, which was developed after the MBTA had received significant public input in response to Scenarios 1 and 2, is now feasible, as the Massachusetts Department of Transportation (MassDOT) has identified additional funding sources that will meet the remainder of the MBTA’s FY 2013 budget deficit.

Scenario 3 raises the majority of its projected revenue through a fare increase, with the remainder of its revenue obtained by reducing service. This report documents the projection of the impacts of this scenario on ridership, revenue, air quality, and environmental justice communities.

The Central Transportation Planning Staff (CTPS) to the Boston Region Metropolitan Planning Organization (MPO), using a spreadsheet model, assisted the MBTA in determining the fare levels for each mode and fare category that would be needed in the context of Scenario 3 to reach the revenue targets the MBTA had established. It then used several analysis techniques to estimate and evaluate the impacts of the scenario’s proposed fare increase and

EXECUTIVE SUMMARY

x 3/28/2012 Boston Region MPO

service reductions. Both the spreadsheet model and the Boston Region MPO’s regional travel demand model set were used to estimate the projected ridership loss associated with the scenario and the net revenue change that would result from the lower ridership and higher fares. By employing both techniques, CTPS produced a range of estimates of potential impacts on ridership and revenue. The travel demand model set was also used to predict the effects of the fare increase on regional air quality and environmental justice.

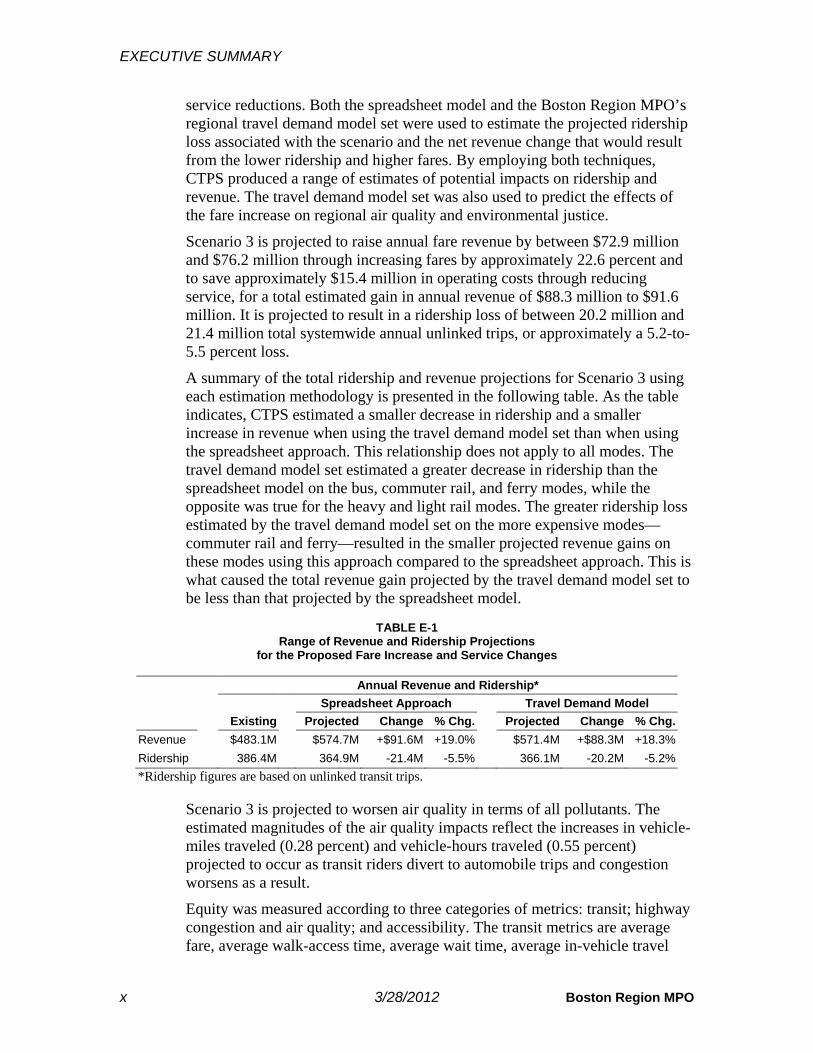

Scenario 3 is projected to raise annual fare revenue by between $72.9 million and $76.2 million through increasing fares by approximately 22.6 percent and to save approximately $15.4 million in operating costs through reducing service, for a total estimated gain in annual revenue of $88.3 million to $91.6 million. It is projected to result in a ridership loss of between 20.2 million and 21.4 million total systemwide annual unlinked trips, or approximately a 5.2-to-5.5 percent loss.

A summary of the total ridership and revenue projections for Scenario 3 using each estimation methodology is presented in the following table. As the table indicates, CTPS estimated a smaller decrease in ridership and a smaller increase in revenue when using the travel demand model set than when using the spreadsheet approach. This relationship does not apply to all modes. The travel demand model set estimated a greater decrease in ridership than the spreadsheet model on the bus, commuter rail, and ferry modes, while the opposite was true for the heavy and light rail modes. The greater ridership loss estimated by the travel demand model set on the more expensive modes—commuter rail and ferry—resulted in the smaller projected revenue gains on these modes using this approach compared to the spreadsheet approach. This is what caused the total revenue gain projected by the travel demand model set to be less than that projected by the spreadsheet model.

TABLE E-1

Range of Revenue and Ridership Projections for the Proposed Fare Increase and Service Changes

Annual Revenue and Ridership* Spreadsheet Approach Travel Demand Model Existing Projected Change % Chg. Projected Change % Chg. Revenue $483.1M $574.7M +$91.6M +19.0% $571.4M +$88.3M +18.3% Ridership 386.4M 364.9M -21.4M -5.5% 366.1M -20.2M -5.2% *Ridership figures are based on unlinked transit trips.

Scenario 3 is projected to worsen air quality in terms of all pollutants. The estimated magnitudes of the air quality impacts reflect the increases in vehicle-miles traveled (0.28 percent) and vehicle-hours traveled (0.55 percent) projected to occur as transit riders divert to automobile trips and congestion worsens as a result.

Equity was measured according to three categories of metrics: transit; highway congestion and air quality; and accessibility. The transit metrics are average fare, average walk-access time, average wait time, average in-vehicle travel

EXECUTIVE SUMMARY

CTPS 3/28/2012 xi

time, number of transfers, and total transit trips. Scenario 3 has a smaller increase in the average fare and a smaller estimated loss in transit riders for environmental justice (EJ) communities than non-EJ communities. There is no measurable difference between EJ and non-EJ communities in the change in average walk-access, wait, or in-vehicle-travel times or in the change in the number of transfers. As for local highway congestion and air pollution, the increases in Scenario 3 are worse for EJ communities than non-EJ communities (the existing levels of congestion and air pollution are also worse in EJ communities than non-EJ communities). Finally, the differences between the changes for EJ communities and those for non-EJ communities in the accessibility of jobs, healthcare, and educational opportunities are so small that they are not statistically significant, indicating that there would be no perceptible difference.

CTPS 3/28/2012 1

Introduction

The Massachusetts Bay Transportation Authority (MBTA) currently faces serious financial problems. Its fiscal year (FY) 2013 (July 1, 2012–June 30, 2013) operating budget deficit was projected to total $185 million. A series of one-time financial and administrative actions were taken to reduce the projected deficit to $161 million. Given continued increases in operating expenses, projected decreases in revenue, and growing debt service costs for capital investments, the Authority will face continuous and growing deficits in future years.

The primary methods that the MBTA has at its disposal for reducing deficits are raising fares to increase revenue and reducing service to decrease operating expenses, though the MBTA can raise revenue through other, less significant means. The MBTA recently explored the impacts of various combinations of potential fare-increase and service-reduction levels and decided to model two scenarios with different combinations. The amount of the fare increase and service reductions proposed by the MBTA for each of those scenarios was determined by the objective of closing the projected FY 2013 budget deficit. These two scenarios and their projected impacts are described in a separate report. A third scenario has now been explored because the Massachusetts Department of Transportation (MassDOT) has identified additional funding sources that will help the MBTA to close its FY 2013 budget gap. This report models this new third scenario, which was developed by the MBTA after receiving significant input from the public regarding Scenarios 1 and 2.

The first step in the analysis process was for the Central Transportation Planning Staff (CTPS) to the Boston Region Metropolitan Planning Organization (MPO), in consultation with the MBTA, to determine the fare level for each mode and fare category that would be needed to reach the MBTA’s revenue targets given the estimated ridership loss due to the scenario’s proposed service reductions. This was accomplished through an iterative process in which CTPS utilized a spreadsheet model that was specifically developed to analyze the degree to which ridership and revenue would change if fares were raised by any given amount. CTPS also produced alternative estimates of the impact on both ridership and revenue using the Boston Region MPO’s regional travel demand model set. A comparison of the

INTRODUCTION

2 3/28/2012 Boston Region MPO

projections of each model provides a range of estimated impacts on ridership and revenue. The impacts on air quality and environmental justice were projected using the travel demand model set.

This report first presents detailed descriptions of the proposed scenario. It then explains the estimation methods used by CTPS in its analysis and presents the projected impacts of the proposed scenario on ridership, revenue, air quality, and environmental justice communities. A brief summary of findings concludes the report.

CTPS 3/28/2012 3

Description of Proposed Fare Increase/Service Change Scenario

This chapter describes first the scenario’s fare structure, then its service changes, and finally its fare increases.

2.1 FARE STRUCTURE CHANGES Significant time and effort were expended, as part of developing the last fare increase plan, implemented in 2007, to simplify the fare structure and to modify it in ways that encourage riders to use certain fare media. Zoned local bus routes were collapsed into a single local bus category. Fare zones and exit fares were eliminated on the rapid transit system. The number of express bus zones was reduced. The transfer price between bus and rapid transit was reduced for CharlieCard users. CharlieTicket fares were priced at a higher rate than CharlieCard fares. The Subway Pass was eliminated and the LinkPass was introduced for use on both local bus routes and rapid transit routes at a reduced price compared to the similar pass type that existed prior to the fare increase, the Combo Pass. While the proposed Scenario 3 for FY 2013 raises prices, eliminates services, and changes the fare structure, the suggested changes do not conflict with or alter the structural changes or goals of the previous restructuring.

One recommendation for fare structure changes in Scenario 3 concerns the single-ride discounts for seniors and students for local bus and rapid transit. In the current fare structure, the senior fare and student fare (regardless of whether a CharlieCard or CharlieTicket is used) are set at approximately 33 percent and 50 percent, respectively, of the CharlieCard single-ride adult fare. In Scenario 3, these ratios are set at approximately 40 percent for both seniors and students, and the CharlieTicket single-ride adult fare, rather than the CharlieCard fare, is used as the base rate. This change is in keeping with the MBTA’s enabling legislation (MGL 161A, Section 5(e)) that links student and senior discounts to the “adult cash fare,” which is equivalent to the CharlieTicket adult fare.

Another change in the fare structure is proposed for THE RIDE. The current fare structure charges a flat fare for any trip within THE RIDE’s service area. THE RIDE currently serves riders living in any part of the towns to which the MBTA provides fixed-route local bus or rapid transit service as well as riders

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

4 3/28/2012 Boston Region MPO

living in some nearby towns that do not have any fixed-route service. In Scenario 3, THE RIDE’s base fare increases to twice the CharlieTicket local bus adult fare, and a premium fare is charged for (a) trips to or from any area outside of the service area mandated by the Americans with Disabilities Act (ADA) (0.75-mile buffer from any local bus route or rapid transit station), (b) trips before or after the service hours mandated by the ADA, and (c) same-day and will-call1 trips (which are outside the scope of the ADA).

Several other changes are also proposed. Tokens (used for MBTA fares prior to 2007 and still accepted in fare vending machines) are no longer accepted; this reduces administrative costs. A 7-Day Student Pass is introduced to accompany the existing 5-Day Student Pass. Both Student Passes will have all-day validity, eliminating the existing 11:00 PM limit on use of the Student Pass. As with the 5-Day Student Pass, the 7-Day Student Pass is valid on local bus, rapid transit, inner and outer express bus, and commuter rail in zones up to Zone 2.

Scenario 3 also changes the structure of multi-ride tickets. The 12-ride ticket on commuter rail is replaced by a 10-ride ticket, and the 60-ride ticket on the ferry is eliminated. Therefore, commuter rail and ferry will have the same multi-ride ticket structure: a 10-ride adult ticket and a 10-ride reduced-fare ticket. On neither commuter rail nor ferry do the multi-ride tickets receive a multi-ride discount. The “Group Fare” on commuter rail is also eliminated, because of its limited usage and the cost of providing a separate product. The “Family Fare” on commuter rail remains, but its use is limited to off-peak trains. Finally, the duration of the validity of single- and multi-ride tickets is reduced from 180 days to 14 days and 30 days, respectively. Note that a round-trip ticket is considered to be two single-ride tickets, each with the single-ride duration of validity.

A surcharge is currently charged for commuter rail tickets that are sold onboard the trains. This policy is to charge a $2.00 surcharge during the peak time periods and a $1.00 surcharge during the off-peak time periods. Scenario 3 sets fares for single-ride tickets that are sold onboard the trains. The fare for such a ticket equals the price for the same zonal ticket if sold before boarding the train plus $3.00. There is no differentiation between peak and off-peak time periods. The $3.00 is added per ticket, not per transaction. In other words, the price of multiple onboard tickets bought by a single person would equal the number of tickets multiplied by the total single-ride onboard ticket price; that is, $3.00 would be added to the single-ride pre-sold fare for each ticket. For example, for two tickets with a pre-sold single-ride fare of $5.00 each, the total onboard cost would be $16.00.

1 Will-call trips are a type of same-day trip in which, although the passenger selects a time range for pick-up before the day of the trip, the passenger only specifies the exact pick-up time on the day of the trip.

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

CTPS 3/28/2012 5

2.2 SERVICE CHANGES

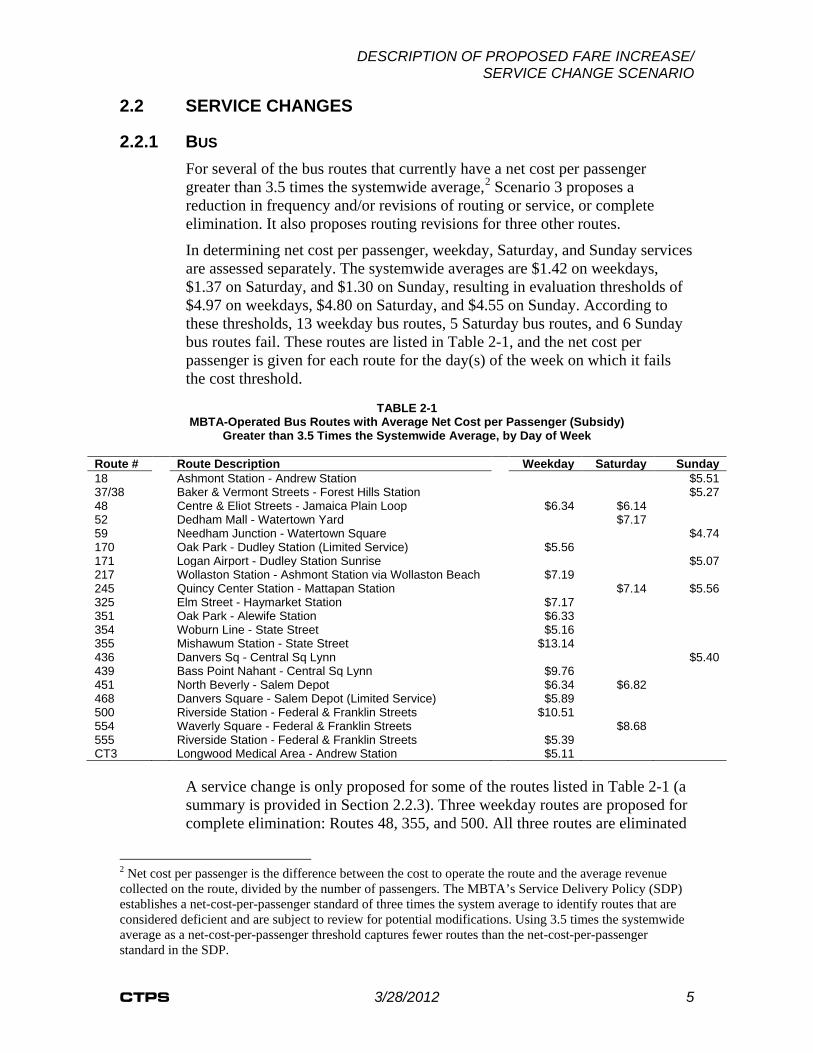

2.2.1 BUS For several of the bus routes that currently have a net cost per passenger greater than 3.5 times the systemwide average,2 Scenario 3 proposes a reduction in frequency and/or revisions of routing or service, or complete elimination. It also proposes routing revisions for three other routes.

In determining net cost per passenger, weekday, Saturday, and Sunday services are assessed separately. The systemwide averages are $1.42 on weekdays, $1.37 on Saturday, and $1.30 on Sunday, resulting in evaluation thresholds of $4.97 on weekdays, $4.80 on Saturday, and $4.55 on Sunday. According to these thresholds, 13 weekday bus routes, 5 Saturday bus routes, and 6 Sunday bus routes fail. These routes are listed in Table 2-1, and the net cost per passenger is given for each route for the day(s) of the week on which it fails the cost threshold.

TABLE 2-1

MBTA-Operated Bus Routes with Average Net Cost per Passenger (Subsidy) Greater than 3.5 Times the Systemwide Average, by Day of Week

Route # Route Description Weekday Saturday Sunday 18 Ashmont Station - Andrew Station $5.51 37/38 Baker & Vermont Streets - Forest Hills Station $5.27 48 Centre & Eliot Streets - Jamaica Plain Loop $6.34 $6.14 52 Dedham Mall - Watertown Yard $7.17 59 Needham Junction - Watertown Square $4.74 170 Oak Park - Dudley Station (Limited Service) $5.56 171 Logan Airport - Dudley Station Sunrise $5.07 217 Wollaston Station - Ashmont Station via Wollaston Beach $7.19 245 Quincy Center Station - Mattapan Station $7.14 $5.56 325 Elm Street - Haymarket Station $7.17 351 Oak Park - Alewife Station $6.33 354 Woburn Line - State Street $5.16 355 Mishawum Station - State Street $13.14 436 Danvers Sq - Central Sq Lynn $5.40 439 Bass Point Nahant - Central Sq Lynn $9.76 451 North Beverly - Salem Depot $6.34 $6.82 468 Danvers Square - Salem Depot (Limited Service) $5.89 500 Riverside Station - Federal & Franklin Streets $10.51 554 Waverly Square - Federal & Franklin Streets $8.68 555 Riverside Station - Federal & Franklin Streets $5.39 CT3 Longwood Medical Area - Andrew Station $5.11

A service change is only proposed for some of the routes listed in Table 2-1 (a summary is provided in Section 2.2.3). Three weekday routes are proposed for complete elimination: Routes 48, 355, and 500. All three routes are eliminated

2 Net cost per passenger is the difference between the cost to operate the route and the average revenue collected on the route, divided by the number of passengers. The MBTA’s Service Delivery Policy (SDP) establishes a net-cost-per-passenger standard of three times the system average to identify routes that are considered deficient and are subject to review for potential modifications. Using 3.5 times the systemwide average as a net-cost-per-passenger threshold captures fewer routes than the net-cost-per-passenger standard in the SDP.

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

6 3/28/2012 Boston Region MPO

because of their high net cost per passenger and low ridership, and the fact that other transit services are nearby.3 These eliminations would likely require many of these passengers to walk a greater distance to access other transit services or to transfer between services at a greater rate. As an alternative for passengers using one of the four daily reverse-commute trips on Route 355, it is recommended that the inbound commuter rail train on the Lowell Line that passes through Mishawum Station around 3:36 PM stop at the station. As for weekend service, five routes on Saturday (Routes 48, 52, 245, 451, and 554) and four routes on Sunday (Routes 18, 37/38, 245, and 436) are recommended for elimination. Collectively, the eliminations proposed on these selected routes affect approximately 65,000 annual weekday unlinked trips, 40,000 annual Saturday unlinked trips, and 28,000 annual Sunday unlinked trips, for a total of 133,000 annual trips, or 0.12 percent of all annual MBTA bus unlinked trips.

Route revisions are proposed for three of the routes listed in Table 2-1: Routes 217, 439, and 555. For Route 217, the route segment serving Wollaston Beach is recommended for elimination. However, several school trips are combined with Route 217, which extends service on these trips to Ashmont Station. For Route 439, the recommendations are the elimination of service between Vinnin Square and Central Square, Lynn, and the extension of service beyond Central Square, Lynn, to Wonderland Station for 1.5 round-trips out of each day’s trips. Route 555 is merged into the schedule of Route 553 and the route terminus moved from Riverside Station to Central Square, Waltham. This variation of Route 553 would still serve Copley Square. Finally, it is also recommended that weekday Haymarket services on Routes 441, 442, and 455 terminate at Wonderland Station, replicating the weekend routing; while these routes do not have a net cost per passenger greater than 3.5 times the systemwide average, the revision of these routes would save nearly $0.5 million in annual operating costs. Passengers on these routes would need to transfer to the Blue Line, but the fare on these bus routes would be lowered from the current Inner Express fare to a Local Bus fare. Passengers still wanting a one-seat ride to and from downtown Boston could use Routes 448, 449, and 459.

In addition to the route revisions described above, Scenario 3 recommends the elimination of midday-only weekday service for Routes 354 and 451. This proposal maintains peak-period weekday service on these routes. When the unlinked trips on these two routes are added to the unlinked trips of riders affected by the routing revisions (on Routes 217, 439, 441, 442, 455, and 555), the annual weekday total is approximately 297,000, or 0.28 percent of all annual MBTA bus unlinked trips.

Changes to the frequency of service are recommended for five routes listed in Table 2-1. Weekday peak service is maintained for Route 52, but midday frequency is reduced from 45 minutes to 90 minutes. The total number of trips

3 Parts of Route 48 are also served by the Orange Line and Routes 22, 29, 41, and 44; Route 355 passengers can use commuter rail; Route 500 passengers can use the Green Line D Branch.

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

CTPS 3/28/2012 7

on Route 217 is reduced from 11 to 4.5 round-trips. Frequency on Route 351 is reduced from 30 minutes to 45 minutes. The total number of trips on Route 439 is reduced from 9 to 5 round-trips, with 1.5 round-trips serving the route’s extension to Wonderland Station. Weekday peak service is maintained for Route CT3, but midday frequency is reduced from 30 minutes to 60 minutes. Collectively, the frequency reductions proposed on these selected routes affect approximately 69,000 annual weekday unlinked trips, or 0.06 percent of all annual MBTA bus unlinked trips. On Saturday, the only frequency reduction is proposed for Route 465, from 70 minutes to 120 minutes. With the proposed elimination of Route 451 service and the fact that buses are currently shared between Routes 451 and 465, the reduction in Route 465 frequency would avoid having Route 465 buses sit idle between trips. This proposal affects approximately 17,000 annual Saturday unlinked trips.

For private bus routes (routes that are part of the Private Carrier Bus Program or the Suburban Bus Program, under which bus service is funded by the MBTA but operated by a private contractor), two changes are recommended. First, the private-carrier route serving Medford (Route 710) is recommended for elimination, since a portion of this route would still be served by MBTA Route 134. Second, a reduction of 50 percent is recommended for the subsidy provided to all Suburban Bus Program recipients. While it is unknown how this reduction in subsidies might affect recipients’ decisions regarding whether to modify or to not operate service, this policy could potentially affect all passengers currently riding these routes. The sum of annual unlinked trips on Route 710 and all Suburban Bus Program routes is approximately 169,000 on weekdays and 4,000 on Saturdays, for a total of 173,000 annual trips, or 23.5 percent of all annual unlinked trips on routes subsidized through the Private Carrier Bus and Suburban Bus Programs. This total is 0.16 percent of annual unlinked trips on all bus routes (both MBTA and private bus routes).

Figure 2-1 presents a map of weekday service that shows MBTA and private bus routes and the service changes proposed in Scenario 3. Figures 2-2 and 2-3 do the same for Saturday and Sunday services, respectively. The figures also present estimates of the numbers of unlinked trips that would be affected by the proposed service changes.

2.2.2 RAPID TRANSIT, COMMUTER RAIL, FERRY, AND THE RIDE Two changes are proposed in Scenario 3 for rapid transit. First, the elimination of weekend service on the Green Line E Branch between Brigham Circle and Heath Street is recommended. An average of 7.3 passengers per trip use this segment of the Green Line on Saturday, and on Sunday this average is 5.1 passengers per trip. It is assumed that these passengers could use Route 39, which duplicates service on much of the Green Line, including between Brigham Circle and Heath Street. The second proposed change affects the Mattapan High-Speed Line on Saturday between 6:00 AM and 10:00 AM and between 8:00 PM and 1:00 AM, and on Sunday all day. It is recommended that the frequency be reduced from every 11–13 minutes to every 23–26 minutes

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

8 3/28/2012 Boston Region MPO

(this is the frequency that is estimated to result from the elimination of one of the two trains serving the line during these time periods while maintaining coordination with every other Red Line train at Ashmont Station). Ridership during these time periods currently averages between eight and nine passengers per trip. The combined existing annual unlinked trips on the Green Line E Branch between Brigham Circle and Heath Street and on the Mattapan High-Speed Line during the defined time periods is 116,000 on Saturday and 89,000 on Sunday, for a total of 205,000 annual trips, or 0.31 percent of all annual unlinked trips on light rail.

Of the ferry routes, the F1 service between Hingham and Rowes Wharf and the F2H service between Quincy, Hull, Logan Airport, and Long Wharf currently operate only on weekdays, and the F2 service between Quincy, Logan Airport, and Long Wharf and the F4 Inner Harbor Ferry service currently operate on weekdays, Saturdays, and Sundays. It is recommended in Scenario 3 that weekend F2 service be eliminated, but no service changes are proposed for the other ferry services. It is assumed that weekend F2 riders could use the Red Line. Existing Saturday ridership on the F2 service is approximately 42,000 annual trips; existing Sunday ridership is approximately 29,000. The combined weekend ridership total is 71,000, or 5.5 percent of all annual trips on ferry routes.

The elimination of weekend service is recommended for the commuter rail lines with the lowest weekend ridership totals. These are the Greenbush Line and the Plymouth/Kingston Line on Saturday and Sunday, and the Needham Line on Saturday (the Needham Line already does not operate on Sunday). Together, these lines serve approximately 179,000 annual trips on Saturday and 113,000 annual trips on Sunday. The combined weekend ridership total is 292,000, or 0.79 percent of all annual trips on commuter rail.

Finally, while no service reductions per se are proposed for THE RIDE, the increase in fares and the institution of a premium-fare zone are estimated to reduce the demand for service in Scenario 3, saving the MBTA the cost of serving the trips no longer made. Based on an analysis of a sample day of RIDE trips in which the trip pick-up and drop-off locations are linked,4 it was estimated that 11.7 percent of existing RIDE trips would fall into the premium-

4 Linking the trip pick-up and drop-off locations permits an analysis of not only how many trips are located outside the required ADA buffer, but also how many trips cross the border of this buffer into the premium-fare zone, for which the ADA permits a premium fare to be charged. According to the sample day, 1.1 percent of RIDE trips had both a pick-up and drop-off location outside the ADA buffer and 10.7 percent had one pick-up or drop-off location inside the buffer and the corresponding drop-off or pick-up location outside the buffer. An analysis of an annual total of all RIDE pick-up and drop-off locations that are not linked indicated that 6.4 percent of locations were outside the ADA buffer. If one assumes, from the sample day, that approximately 10 percent of all premium fares have both the pick-up and drop-off locations outside the ADA buffer (1.1 percent divided by 10.7 percent), then approximately 90 percent of the 6.4 percent of premium-fare locations in the annual total, or 5.7 percent, could be assumed to have either a corresponding pick-up or drop-off location within the ADA buffer. The sum of 6.4 percent and 5.7 percent, which represents the percentage of locations associated with trips charged at the premium fare, is 12.1 percent, which is close to the 11.7 percent estimated using the sample day. Based on this comparison of the annual and the sample-day trips, sufficient confidence was felt in the percentage from the sample day.

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

CTPS 3/28/2012 9

fare category.

Figure 2-1 presents a map of weekday service that shows rapid transit and ferry routes and the service changes proposed in Scenario 3. Figures 2-2 and 2-3 do the same for Saturday and Sunday services, respectively. The figures also present estimates of the numbers of unlinked trips that would be affected by the proposed service changes.

2.2.3 SUMMARY OF SERVICE CHANGES In summary, Scenario 3 includes the following service changes:

• Bus o Eliminate the following routes: Weekday: 48, 355, and 500.

Saturday: 48, 52, 245, 451, and 554. Sunday: 18, 37/38, 245, and 436.

o Revise the routing: Weekday: 217, 439, 441, 442, 455, and 555 o Eliminate midday service: Weekday: 354 and 451 o Reduce the frequency: Weekday: 52, 217, 351, 439, and CT3

• Rapid Transit o Eliminate weekend service on the Green Line E Branch between

Brigham Circle and Heath Street o Reduce frequency on the Mattapan High-Speed Line on

Saturday from 6:00 AM to 10:00 AM and from 8:00 PM to 1:00 AM, and all day Sunday

• Commuter Rail: Eliminate the following service: o Saturday: Needham Line, Plymouth/Kingston Line, and

Greenbush Line o Sunday: Plymouth/Kingston Line and Greenbush Line

• Ferry: Eliminate weekend service on Quincy Ferry (Route F2) • Private Bus: Eliminate Private Carrier Bus Program in Medford (Route

710) and reduce subsidies by 50 percent to Suburban Bus Program in all locations (Bedford, Beverly, Boston [Mission Hill], Burlington, Dedham, and Lexington)

Figures 2-1, 2-2, and 2-3 all show the numbers of riders while Figure 2-4 shows the relative percentages of riders on each mode that are affected by the proposed service changes (eliminations, revisions, and frequency reductions) in Scenario 3. Table 2-2 summarizes four measures of service that are affected by the proposed scenario. The four measures are unlinked trips (the number of trips riders take on each transit vehicle), passenger miles (the total number of miles traveled on those unlinked trips), vehicle revenue hours (the total number of hours all transit vehicles are in service), and vehicle revenue miles (the total number of miles traveled by those transit vehicles in service). The table also presents the number of MBTA jobs that are estimated to be lost and the number of MBTA buses that could be removed from service. Scenario 3 generally reduces bus and commuter rail service on routes traversing longer distances, which is why the percentages of passenger miles, vehicle revenue hours, and vehicle revenue miles affected are greater than the percentage of unlinked trips.

BOSTON

HINGHAM

CANTON

QUINCY

LYNN

NORWELL

NEWTON

WALPOLE

BILLERICA

MILTON

PEABODY

SCITUATE

SHARON

BEVERLY

WEYMOUTH

DOVER

LEXINGTON

WOBURN

WALTHAM

SAUGUS

HANOVER MARSHFIELD

NEEDHAM

BRAINTREE

DEDHAM

SALEM

WILMINGTON

BEDFORD

READING

DANVERS

NORWOOD

STOUGHTON

WESTON

LYNNFIELD

RANDOLPH

WESTWOOD

COHASSET

BURLINGTON

AVON ABINGTON

REVERE

WAKEFIELD

MEDFORD

HOLBROOK

WELLESLEY

MALDEN

NORTH READING

MELROSE

BELMONT

WINCHESTER

ARLINGTONEVERETT

MANCHESTER

WATERTOWN

ROCKLAND

LINCOLN

MEDFIELD

STONEHAM

CAMBRIDGE

BROOKLINE

HULL

SOMERVILLE

MARBLEHEAD

BROCKTON

MIDDLETON

CHELSEA

SWAMPSCOTT

TEWKSBURY

WINTHROP

NAHANT

PEMBROKE

GLOUCESTERWENHAM

NORFOLK

CONCORD

LegendBus: Maintained ServiceRapid Transit: Maintained ServiceFerry: Maintained ServiceReduced-Frequency ServiceMidday-Only Eliminated ServiceEliminated ServiceSuburban Bus Program Service

FIGURE 2-1Scenario 3 Weekday Bus, Rapid Transit, andFerry Service Changes

CTPS - 3/28/20120 2 41 Miles

Route Eliminations (65,000 annual trips):- Eliminate routes: 48, 355, and 500Route Revisions (297,000 annual trips):- Route 217: Eliminate Wollaston Beach section- Route 354: Eliminate midday service- Route 439: Eliminate service between Central Square (Lynn) and Vinnin Square; extend service to Wonderland- Route 441: Eliminate service between Wonderland and Haymarket- Route 442: Eliminate service between Wonderland and Haymarket- Route 451: Eliminate midday service- Route 455: Eliminate service between Brown Circle and Haymarket and terminate at Wonderland- Route 555: Change terminus from Riverside to Central Square (Waltham)Reduce Frequency (69,000 annual trips):- Route 52: From 45 to 90 minutes in midday- Route 217: From 11 to 4.5 round-trips- Route 351: From 30 to 45 minutes- Route 439: From 9 to 5 round-trips; 1.5 round-trips to serve Wonderland- Route CT3: From 30 to 60 minutes in middayEliminate Private Carrier Bus Program in Medford (Route 710) and reduce Suburban Bus Program subsidies by 50% in all locations (Bedford, Boston[Mission Hill], Beverly, Burlington, Dedham, andLexington) (169,000 annual trips)

BOSTON

REVEREMEDFORD

MALDEN

CAMBRIDGE

BROOKLINE

ARLINGTON

EVERETT

SOMERVILLE

QUINCY

BELMONT CHELSEA

WATERTOWN

WINCHESTER

NEWTON

WINTHROP

SAUGUSMELROSE

MILTON

±

BOSTON

HINGHAM

CANTON

QUINCY

LYNN

NORWELL

NEWTON

WALPOLE

BILLERICA

MILTON

PEABODY

SCITUATE

SHARON

WEYMOUTH

BEVERLY

DOVER

LEXINGTON

WOBURN

WALTHAM

HANOVER

SAUGUS

MARSHFIELD

NEEDHAM

BRAINTREE

DEDHAM

SALEM

WILMINGTON

BEDFORD

READING

DANVERS

STOUGHTON

NORWOOD

LYNNFIELD

WESTON

RANDOLPH

WESTWOOD

COHASSET

BURLINGTON

AVON ABINGTON

REVERE

WAKEFIELD

MEDFORD

HOLBROOK

MALDEN

WELLESLEY

NORTH READING

MELROSE

BELMONT

WINCHESTER

ARLINGTONEVERETT

MANCHESTER

WATERTOWN

BROCKTON

ROCKLAND

LINCOLN

MEDFIELD

STONEHAM

CAMBRIDGE

BROOKLINE

HULL

SOMERVILLE

MARBLEHEAD

CHELSEA

MIDDLETON

SWAMPSCOTT

TEWKSBURY

WINTHROP

NAHANT

PEMBROKE

GLOUCESTERWENHAM

NORFOLK

CONCORD

FIGURE 2-2Scenario 3 Saturday Bus, Rapid Transit, andFerry Service Changes

CTPS - 3/28/20120 2 41 Miles

Route Eliminations (82,000 annual trips):- Eliminate routes: 48, 52, 245, 451, 554 and Quincy ferry (Route F2)Route Revisions (107,000 annual trips):- Green Line E Branch: Eliminate service between Brigham Circle and Heath StreetReduce Frequency (27,000 annual trips):- Route 465: From 70 to 120 minutes- Mattapan High-Speed Line: From 11-13 to 23-26 minutes, 6:00 to 10:00 AM and 8:00 PM to 1:00 AMEliminate Private Carrier Bus Program in Medford (Route 710) and reduce Suburban Bus Programsubsidies by 50% in both locations (Boston [Mission Hill]and Beverly) (4,000 annual trips)

BOSTON

REVEREMEDFORD

MALDEN

CAMBRIDGE

BROOKLINE

ARLINGTON

EVERETT

SOMERVILLEBELMONT CHELSEA

WATERTOWN

WINCHESTER

QUINCY

WINTHROP

SAUGUSMELROSE

LegendBus: Maintained ServiceRapid Transit: Maintained ServiceFerry: Maintained ServiceReduced-Frequency ServiceEliminated ServiceSuburban Bus Program Service±

BOSTON

HINGHAM

CANTON

QUINCY

LYNN

NORWELL

NEWTON

WALPOLE

BILLERICA

MILTON

PEABODY

SCITUATE

SHARON

WEYMOUTH

BEVERLY

LEXINGTON

DOVER

WOBURN

HANOVER

WALTHAM

SAUGUS

MARSHFIELD

NEEDHAM

BRAINTREE

DEDHAM

SALEM

WILMINGTON

BEDFORD

READING

DANVERS

STOUGHTON

NORWOOD

LYNNFIELD

RANDOLPH

WESTWOOD

COHASSET

BURLINGTON

WESTON

ABINGTONAVON

REVERE

WAKEFIELD

MEDFORD

HOLBROOK

MALDEN

WELLESLEY

NORTH READING

MELROSE

BELMONT

WINCHESTER

ARLINGTONEVERETT

MANCHESTER

BROCKTON

WATERTOWN

ROCKLAND

LINCOLN

STONEHAM

CAMBRIDGE

MEDFIELD

BROOKLINE

HULL

SOMERVILLE

MARBLEHEAD

CHELSEA

MIDDLETON

SWAMPSCOTT

TEWKSBURY

WINTHROP

PEMBROKE

NAHANT

GLOUCESTERWENHAM

NORFOLK

CONCORD

FIGURE 2-3Scenario 3 Sunday Bus, Rapid Transit, andFerry Service Changes

CTPS - 3/28/20120 2 41 Miles

Route Eliminations (57,000 annual trips):- Eliminate routes: 18, 37/38, 245, 436 and Quincy ferry F2Route Revisions (68,000 annual trips):- Green Line E Branch: Eliminate service between Brigham Circle and Heath StReduce Frequency (21,000 annual trips):- Mattapan High-Speed Line: From 11-13 to 23-26 minutes all day

BOSTON

REVEREMEDFORD

MALDEN

CAMBRIDGE

BROOKLINE

ARLINGTON

EVERETT

SOMERVILLEBELMONT CHELSEA

WATERTOWN

WINCHESTER

NEWTON

QUINCY

WINTHROP

SAUGUSMELROSE

MILTON

±

LegendBus: Maintained ServiceRapid Transit: Maintained ServiceFerry: Maintained ServiceReduced-Frequency ServiceEliminated Service

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

CTPS 3/28/2012 13

TABLE 2-2 Percentage of Service Affected

Measure Number Percent Unlinked Trips 1,212,242 0.3% Passenger Miles 8,692,607 0.5% Vehicle Revenue Hours 60,677 1.2% Vehicle Revenue Miles 1,076,494 1.4% MBTA Jobs Lost 15 Buses Removed 3

2.3 FARE INCREASE: SINGLE-RIDE FARES, PASS PRICES, AND PARKING RATES Table 2-3 presents the key existing and proposed single-ride fares for each fare category, along with the percentage change in price from the existing to the proposed price. Table 2-4 presents the existing and proposed pass prices for each pass category, along with the percentage change in price from the existing to the proposed price. Table 2-5 presents the existing and proposed parking rates for each parking facility, along with the percentage change in price from the existing to the proposed price.

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

14 3/28/2012 Boston Region MPO

TABLE 2-3 Key Single-Ride Fares: Existing and Proposed

Fare Category Existing Proposed % Chg. $ Chg. CharlieCard Adult Local Bus $1.25 $1.50 20.0% $0.25 Rapid Transit $1.70 $2.00 17.6% $0.30 Bus + RT* $1.70 $2.00 17.6% $0.30 Inner Express $2.80 $3.50 25.0% $0.70 Outer Express $4.00 $5.00 25.0% $1.00 Senior Local Bus $0.40 $0.75 87.5% $0.35 Rapid Transit $0.60 $1.00 66.7% $0.40 Bus + RT* $0.60 $1.00 66.7% $0.40 Student Local Bus $0.60 $0.75 25.0% $0.15 Rapid Transit $0.85 $1.00 17.6% $0.15 Bus + RT* $0.85 $1.00 17.6% $0.15 CharlieTicket Adult Local Bus $1.50 $2.00 33.3% $0.50 Rapid Transit $2.00 $2.50 25.0% $0.50 Bus + RT* $3.50 $4.50 28.6% $1.00 Inner Express $3.50 $4.50 28.6% $1.00 Outer Express $5.00 $6.50 30.0% $1.50 Commuter Rail** Zone 1A $1.70 $2.00 17.6% $0.30 Zone 1 $4.25 $5.50 29.4% $1.25 Zone 2 $4.75 $6.00 26.3% $1.25 Zone 3 $5.25 $6.75 28.6% $1.50 Zone 4 $5.75 $7.25 26.1% $1.50 Zone 5 $6.25 $8.00 28.0% $1.75 Zone 6 $6.75 $8.75 29.6% $2.00 Zone 7 $7.25 $9.25 27.6% $2.00 Zone 8 $7.75 $10.00 29.0% $2.25 Zone 9 $8.25 $10.50 27.3% $2.25 Zone 10*** N/A $11.00 N/A N/A InterZone 1 $2.00 $2.50 37.5% $0.50 InterZone 2 $2.25 $3.00 33.3% $0.75 InterZone 3 $2.50 $3.25 30.0% $0.75 InterZone 4 $2.75 $3.50 36.4% $0.75 InterZone 5 $3.00 $4.00 41.7% $1.00 InterZone 6 $3.50 $4.50 35.7% $1.00 InterZone 7 $4.00 $5.00 31.3% $1.00 InterZone 8 $4.50 $5.50 27.8% $1.00 InterZone 9*** N/A $6.00 N/A N/A InterZone 10*** N/A $6.50 N/A N/A Ferry F1 $6.00 $8.00 33.3% $2.00 F2: Boston $6.00 $8.00 33.3% $2.00 F2: X-Harbor $10.00 $13.00 30.0% $3.00 F2: Logan $12.00 $16.00 33.3% $4.00 Inner Harbor $1.70 $3.00 76.5% $1.30 THE RIDE ADA Territory $2.00 $4.00 100.0% $2.00 Premium Territory*** N/A $5.00 N/A N/A

* “Bus + RT” indicates the linked-trip price of a trip on both local bus and rapid transit. ** Multi-ride and onboard ticket prices are described in Section 2.1, Fare Structure Changes. *** This fare category does not currently exist; therefore, both the existing price and percent

change are marked as “N/A.”

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

CTPS 3/28/2012 15

TABLE 2-4 Pass Prices: Existing and Proposed

Pass Category Existing Proposed % Chg. $ Chg. Local Bus $40.00 $48.00 20.0% $8.00 LinkPass $59.00 $70.00 18.6% $11.00 Senior/TAP $20.00 $28.00 40.0% $8.00 Student 5-Day $20.00 $25.00 25.0% $5.00 Student 7-Day* N/A $28.00 N/A N/A 1-Day $9.00 $11.00 22.2% $2.00 7-Day $15.00 $18.00 20.0% $3.00 Inner Express $89.00 $110.00 23.6% $21.00 Outer Express $129.00 $160.00 24.0% $31.00 Commuter Rail Zone 1A $59.00 $70.00 18.6% $11.00 Zone 1 $135.00 $173.00 28.1% $38.00 Zone 2 $151.00 $189.00 25.2% $38.00 Zone 3 $163.00 $212.00 30.1% $49.00 Zone 4 $186.00 $228.00 22.6% $42.00 Zone 5 $210.00 $252.00 20.0% $42.00 Zone 6 $223.00 $275.00 23.3% $52.00 Zone 7 $235.00 $291.00 23.8% $56.00 Zone 8 $250.00 $314.00 25.6% $64.00 Zone 9 $265.00 $329.00 24.2% $64.00 Zone 10* N/A $345.00 N/A N/A InterZone 1 $65.00 $82.00 26.2% $17.00 InterZone 2 $77.00 $100.00 29.9% $23.00 InterZone 3 $89.00 $109.00 22.5% $20.00 InterZone 4 $101.00 $118.00 16.8% $17.00 InterZone 5 $113.00 $134.00 18.6% $21.00 InterZone 6 $125.00 $151.00 20.8% $26.00 InterZone 7 $137.00 $167.00 21.9% $30.00 InterZone 8 $149.00 $184.00 23.5% $35.00 InterZone 9* N/A $201.00 N/A N/A InterZone 10* N/A $218.00 N/A N/A Commuter Boat $198.00 $262.00 32.3% $64.00

* This fare category does not currently exist; therefore, both the existing price and percent change are marked as “N/A.”

The overall price increase across all modes and fare/pass categories is approximately 22.6 percent. This systemwide average is based on the weighted averages that were calculated by multiplying the percentage change in price for each fare/pass category by the existing ridership in that category and dividing by total existing modal ridership. Table 2-6 presents these weighted average percentage increases by modal category. Note that the percentage changes in price can differ between modes that are similarly priced (such as local bus and the Silver Line–Washington Street, or subway and surface light rail) because of differences in how the riders on these modes pay for their trips.

In Scenario 3, the percentage change in prices (Table 2-6) is relatively consistent across modal categories except for ferry and THE RIDE. The latter faces a significant price increase with the introduction of the premium fare and the change in how the base fare is defined. The large price increase for ferry is driven by the percentage changes in the prices for the F1 and F4 services. Commuter rail receives the next-greatest percentage price increase; this is meant to compensate for the fact that no increase in commuter rail park-and-ride facility rates, except for the Route 128 facility, is proposed.

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

16 3/28/2012 Boston Region MPO

TABLE 2-5 Park-and-Ride Facility Rates: Existing and Proposed

Park-and-Ride Facility

Existing Proposed % Chg. $ Chg.

Alewife $7.00 $7.00 0.0% $0.00 Beachmont $5.00 $5.00 0.0% $0.00 Braintree $7.00 $7.00 0.0% $0.00 Chestnut Hill $5.50 $6.00 9.1% $0.50 Eliot $5.50 $6.00 9.1% $0.50 Forest Hills $6.00 $6.00 0.0% $0.00 Lechmere $5.50 $6.00 9.1% $0.50 Malden $5.50 $6.00 9.1% $0.50 Mattapan* $4.50 $4.00 -11.1% -$0.50 Milton* $5.00 $4.00 -20.0% $1.00 North Quincy $5.00 $5.00 0.0% $0.00 Oak Grove $5.50 $6.00 9.1% $0.50 Orient Heights $5.00 $5.00 0.0% $0.00 Quincy Adams $7.00 $7.00 0.0% $0.00 Quincy Center $7.00 $7.00 0.0% $0.00 Riverside $5.75 $6.00 4.3% $0.25 Suffolk Downs $5.00 $5.00 0.0% $0.00 Sullivan $5.50 $6.00 9.1% $0.50 Waban $5.50 $6.00 9.1% $0.50 Wellington $5.50 $6.00 9.1% $0.50 Wollaston $5.00 $5.00 0.0% $0.00 Woodland $6.00 $6.00 0.0% $0.00 Wonderland $5.00 $5.00 0.0% $0.00 Express Bus** $5.00 $5.00 0.0% $0.00 Commuter Rail** $4.00 $4.00 0.0% $0.00 Route 128*** $5.00 $7.00 40.0% $2.00 Ferry** $3.00 $4.00 33.3% $1.00

* The Mattapan and Milton facilities currently have a $3.00 parking rate, as they are part of the “Competitive Lots Program,” which investigates lowering the parking rate at underutilized facilities. The existing rates listed in the table are those that were in place before the program. This program is intended to terminate on July 1, 2012, and the rates are programmed to increase to those listed as proposed.

** Park-and-ride daily facility rates are the same for all facilities serving these modes except for the Route 128 facility. The Fore River Shipyard Ferry Terminal in Quincy also has overnight and weekly rates that are currently set at $6.00 and $36.00, respectively. These proposed rates will increase to $8.00 and $48.00, respectively.

*** The park-and-ride rate at the Route 128 facility is currently set at $5.00 for the first 14 hours and $12.00 for each day thereafter. The post-14 hour rate will increase to $14.00 per day.

The percentage change in prices (Table 2-6) for parking is less than the percentage changes in single-ride fares and pass prices. This is because parking rate increases are proposed only for those facilities that are at or above 100 percent utilization. This includes several subway and surface light rail parking facilities and the Route 128 facility. The zero percent changes for the facilities with less than 100 percent utilization bring down the percentage changes in the parking price for subway, surface light rail, and commuter rail as well as for the overall parking category. Note that the average “fares” (in this case, the parking rates) for park-and-ride facility modal categories, as in all the other modal categories, reflect the unlinked-trip price rather than the linked-trip price.

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

CTPS 3/28/2012 17

The largest proposed percentage increases in price (Table 2-6) within a modal category are generally for CharlieTicket and onboard cash fares. These increases are greater than the more modest increases in the CharlieCard fares, due to the greater price increases assessed to CharlieTicket and onboard cash fares for the local bus, express bus, and rapid transit modes. The increase in CharlieTicket and onboard cash fares is most apparent when comparing those fare categories with the CharlieCard with respect to the price for transfers between local bus and rapid transit service. With a CharlieCard, a “step-up” transfer between those modes would make the total price for a linked trip $2.00. The “step-up” transfer benefit is not available on CharlieTickets, however, resulting in a total proposed linked-trip price of $4.50 using CharlieTickets or onboard cash.

TABLE 2-6 Weighted Average Percentage Change in Average Fares,

by Modal Category, for Unlinked Trips

Modal Category % Change Bus 23.9% Local Bus 23.5% Inner Express 27.7% Outer Express 26.4% Rapid Transit 19.7% Subway 19.6% SL Washington 24.7% SL Waterfront 20.5% Surface Light Rail 20.0% Commuter Rail 29.2% Zone 1A 19.4% Zone 1 30.0% Zone 2 26.1% Zone 3 30.5% Zone 4 23.9% Zone 5 22.9% Zone 6 25.9% Zone 7 25.4% Zone 8 27.4% Zone 9 26.9% InterZone 25.3% Onboard 73.1% Ferry 43.1% F1 42.4% F2: Boston 34.6% F2: X-Harbor 30.3% F2: Logan 33.4% Inner Harbor 69.8% THE RIDE 100.0% ADA Territory 94.9% Premium Territory 140.0% Parking 1.2% Express Bus 0.0% Subway 1.1% Surface Light Rail 3.6% Commuter Rail 0.3% Ferry 33.3% Total System 22.6%

DESCRIPTION OF PROPOSED FARE INCREASE/ SERVICE CHANGE SCENARIO

18 3/28/2012 Boston Region MPO

The percentage increase in pass prices is generally less than that in the respective single-ride fares. Pass prices increase by various amounts in order to maintain or revise certain cash-fare equivalents (based on the lowest-priced respective single-ride fare), which are the number of single-ride trips equivalent to the total pass price. The difference between the lowest and highest cash-fare-equivalent values of the various commuter rail passes is reduced. The cash-fare equivalents of commuter rail passes currently range from 31.05 to 33.60 trips per pass; under the proposed fare increase in Scenario 3, the cash-fare equivalent would range from 31.33 to 31.50 trips per pass. For local bus, express bus, and rapid transit passes, the cash-fare equivalent would decrease or remain virtually the same.

CTPS 3/28/2012 19

Methods Used to Estimate Ridership and Revenue

Two separate approaches were used in this analysis to project the impact of the proposed fare increase and service reductions on MBTA ridership and revenue. One approach utilized a set of spreadsheets created by CTPS in consultation with the MBTA specifically for the purpose of such calculations. The second approach consisted of applying the Boston Region MPO’s regional travel demand model set to estimate demand for each MBTA mode using the existing and proposed fare levels.

The travel demand model set was also employed as a complement to the spreadsheet model in the 2007 Pre–Fare Increase Impacts Analysis, with the two models together providing an indication of the potential range of impacts on ridership and revenue. In addition, unlike the spreadsheet model, the travel demand model set can also be used to conduct the air quality and environmental justice impact analyses.

3.1 CTPS SPREADSHEET MODEL APPROACH The spreadsheet model was used to estimate the revenue and ridership impacts of the fare increase component of the proposed scenario. This model reflects the many fare-payment categories of the MBTA pricing system and applies price elasticities to analyze various changes across these categories. The accuracy of this methodology was proven to be satisfactory through the 2007 Post–Fare Increase Impacts Analysis, which included an analysis of its effectiveness in predicting the impacts of the proposed 2007 fare increase.

3.1.1 MODELING OF EXISTING RIDERSHIP AND REVENUE Inputs to the spreadsheet model included existing ridership in the form of unlinked trips by mode, by fare-payment method, and by fare-media type. An unlinked trip is an individual trip on any one transit vehicle; any trip using multiple vehicles—so-called “linked” trips—is counted as multiple unlinked trips.

Existing ridership5 (to which the spreadsheet model applies price elasticity figures – see Section 3.1.2) for the local bus, express bus, and rapid transit

5 Existing ridership is that for fiscal year 2011 (July 1, 2010–June 30, 2011).

METHODS USED TO ESTIMATE RIDERSHIP AND REVENUE

20 3/28/2012 Boston Region MPO

networks was provided in the form of automated fare-collection (AFC) data. Data were provided by month, with subtotals of transactions (unlinked trips) by the various possible combinations of product type (single-ride fare or pass) and stock (smart card, magnetic-stripe ticket, etc.). AFC data were also provided at the modal level at which each transaction occurs. More detailed information on AFC fare types, modes, and media can be found in the appendix.

Because AFC equipment has not yet been deployed on commuter rail and commuter boat, the number of trips on these modes was estimated using sales figures. Single-ride trips on commuter rail and ferry were set equal to the number of single-ride fares sold, while pass trips on these modes were estimated by dividing the number of pass sales by the estimated average number of trips made using the respective pass type, calculated as part of the 2007 Post–Fare Increase Impacts Analysis. Dividing the number of pass sales by the estimated number of trips per pass resulted in an estimate of the total number of pass trips for each pass type.

Other data used were estimates of the number of trips currently made using THE RIDE and the number of cars currently parked at transit stations. These data were provided to CTPS directly by the MBTA.

Because the spreadsheet model cannot estimate the ridership impacts of eliminating or revising service, estimates of the ridership changes that would be associated with service changes without a fare increase were first calculated separately in order to adjust the existing ridership numbers to reflect a post-service-change situation. The spreadsheet model then estimated the ridership and revenue impacts of a fare increase using the revised existing ridership as the baseline. The MBTA estimated the ridership loss associated with the service changes and provided those estimates to CTPS.

Revenue for single-ride trips was calculated in the spreadsheet model by multiplying the number of trips in each fare/modal category by that category’s price. Revenue for pass trips was calculated for each pass type by multiplying the number of pass sales by the pass price. Pass revenue was then distributed between modal categories based on each category’s ridership and weighted by each category’s single-ride fare.

The calculation of the change in ferry fare revenue collected by the MBTA presents a special challenge. Currently, the MBTA pays a subsidy to all contracted ferry operators, who collect and keep all fare revenue. Therefore, the MBTA does not currently receive any revenue whatsoever from ferry operations. However, under a new contract that will take effect at the start of FY 2013, the MBTA will receive the revenue from fare collection. Given this accounting change, the increase in ferry fare revenue specifically collected by the MBTA will consist of 100 percent of the existing revenue as well as whatever additional amount is collected because of the fare increase. However, this analysis assumed a net ferry revenue change consisting only of the additional fare revenue resulting from the fare increase.

METHODS USED TO ESTIMATE RIDERSHIP AND REVENUE

CTPS 3/28/2012 21

3.1.2 ESTIMATION OF RIDERSHIP CHANGES RESULTING FROM A FARE INCREASE Fares are one of many factors that influence the level of ridership on transit services. Price elasticity is the measure of either the expected or observed rate of change in ridership relative to a change in fares if all other factors remain constant. On a traditional demand curve that describes the relationship between price, on the y-axis, and demand, on the x-axis, elasticities are equivalent to the slope along that curve. As such, price elasticities are generally expected to be negative, meaning that a price increase will lead to a decrease in demand (with a price decrease having the opposite effect). The larger the negative value of the price elasticity (the greater its distance from zero), the greater the projected impact on demand. Larger (more negative) price elasticities are said to be relatively “elastic,” while smaller negative values, closer to zero, are said to be relatively “inelastic.” Thus, if the price elasticity of the demand for transit were relatively elastic, a given fare increase would cause a greater loss of ridership than if demand were relatively inelastic. An example of the application of price elasticities is demonstrated in the appendix.

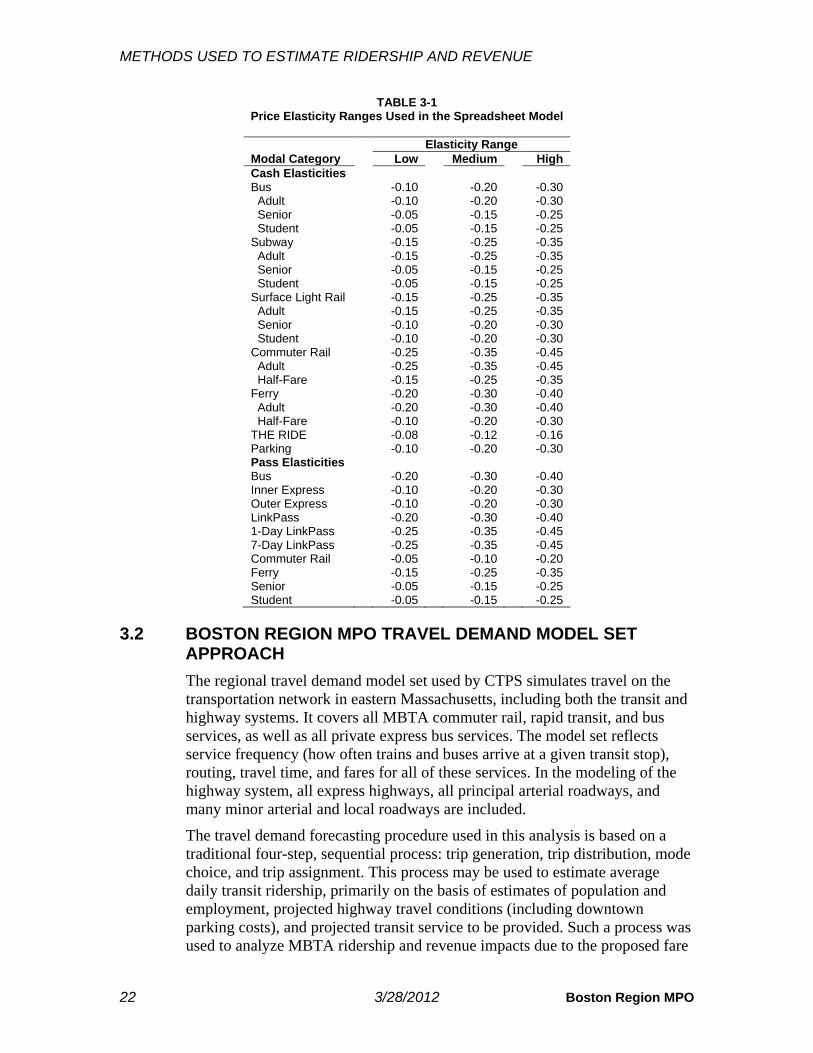

The spreadsheet model permits the use of various ranges of elasticities to estimate different possible ridership impacts of price increases. Performing calculations in the spreadsheet model with the same prices but with a range of higher and lower elasticities provides a range of estimates. In the present analysis, the model was generally set to use the middle range of elasticities, as these represent the best estimate of where the elasticities should be set based on past experiences. However, estimates were also made using more inelastic and elastic elasticities, as a sensitivity analysis of the model’s projections of the ridership losses and revenue gains. Table 3-1 presents the three elasticity ranges used in the spreadsheet model for this study’s analysis. For a description of how these elasticity values were determined, see the appendix.

An additional complexity of the spreadsheet model that provides increased accuracy is its use of ridership diversion factors. These factors reflect estimates of the likelihood of a switch in demand from one MBTA product type or mode to another as a result of a change in the relative prices. The diversion factors essentially work to redistribute demand between the two product types or modes after the respective price elasticities have been applied. The appendix provides examples of the application of diversion factors and the methodology for combining the use of price elasticities and diversion factors. These examples reflect the methodology used in the present analysis. While diversion factors estimate the diversion of riders between MBTA product types and modes based on their price, the spreadsheet model can only estimate the total loss of riders from the MBTA transit system, not the diversion of riders to specific non-MBTA modes such as driving or walking.

METHODS USED TO ESTIMATE RIDERSHIP AND REVENUE

22 3/28/2012 Boston Region MPO

TABLE 3-1 Price Elasticity Ranges Used in the Spreadsheet Model

Elasticity Range Modal Category Low Medium High Cash Elasticities Bus -0.10 -0.20 -0.30 Adult -0.10 -0.20 -0.30 Senior -0.05 -0.15 -0.25 Student -0.05 -0.15 -0.25 Subway -0.15 -0.25 -0.35 Adult -0.15 -0.25 -0.35 Senior -0.05 -0.15 -0.25 Student -0.05 -0.15 -0.25 Surface Light Rail -0.15 -0.25 -0.35 Adult -0.15 -0.25 -0.35 Senior -0.10 -0.20 -0.30 Student -0.10 -0.20 -0.30 Commuter Rail -0.25 -0.35 -0.45 Adult -0.25 -0.35 -0.45 Half-Fare -0.15 -0.25 -0.35 Ferry -0.20 -0.30 -0.40 Adult -0.20 -0.30 -0.40 Half-Fare -0.10 -0.20 -0.30 THE RIDE -0.08 -0.12 -0.16 Parking -0.10 -0.20 -0.30 Pass Elasticities Bus -0.20 -0.30 -0.40 Inner Express -0.10 -0.20 -0.30 Outer Express -0.10 -0.20 -0.30 LinkPass -0.20 -0.30 -0.40 1-Day LinkPass -0.25 -0.35 -0.45 7-Day LinkPass -0.25 -0.35 -0.45 Commuter Rail -0.05 -0.10 -0.20 Ferry -0.15 -0.25 -0.35 Senior -0.05 -0.15 -0.25 Student -0.05 -0.15 -0.25

3.2 BOSTON REGION MPO TRAVEL DEMAND MODEL SET APPROACH The regional travel demand model set used by CTPS simulates travel on the transportation network in eastern Massachusetts, including both the transit and highway systems. It covers all MBTA commuter rail, rapid transit, and bus services, as well as all private express bus services. The model set reflects service frequency (how often trains and buses arrive at a given transit stop), routing, travel time, and fares for all of these services. In the modeling of the highway system, all express highways, all principal arterial roadways, and many minor arterial and local roadways are included.

The travel demand forecasting procedure used in this analysis is based on a traditional four-step, sequential process: trip generation, trip distribution, mode choice, and trip assignment. This process may be used to estimate average daily transit ridership, primarily on the basis of estimates of population and employment, projected highway travel conditions (including downtown parking costs), and projected transit service to be provided. Such a process was used to analyze MBTA ridership and revenue impacts due to the proposed fare

METHODS USED TO ESTIMATE RIDERSHIP AND REVENUE

CTPS 3/28/2012 23

increase and service reductions.

The eastern Massachusetts geographic area represented in the model set is divided into several hundred areas known as transportation analysis zones (TAZs). The model set employs sophisticated and complex techniques in each of the four steps of the process. These steps can be very briefly summarized as follows.

Trip Generation: This step estimates the number of trips produced in and attracted to each TAZ. This is done using estimates of the population, employment, and other socioeconomic and household characteristics of each zone.

Trip Distribution: This step links the trip ends estimated in the trip generation step to form zonal trip interchanges (movements between pairs of zones). The output of this step is a trip table, which is a matrix containing the number of trips occurring in every origin-zone-to-destination-zone combination.

Mode Choice: This step allocates the person trips estimated in the trip distribution step to the two primary competing modes, automobile and transit, and to walking and biking. This allocation is based on the desirability or utility of each choice a traveler can opt for, based on the attributes of that choice and the characteristics of the individual. The resulting output of this step includes the percentage of trips that use automobiles and the percentage that use transit for all trips that have been generated.

Trip Assignment: This final step assigns the transit trips to the various transit modes, such as subway, commuter rail, local bus, or express bus. This is done by assigning each trip to one of several possible transit paths from one zone to another; each of these assignments is based on minimizing the generalized “cost” (including not only the transit fare, but also in-vehicle travel time, number of transfers, etc.). These paths may involve just one mode, such as express bus or commuter rail, or multiple modes, such as a local bus and a transfer to the subway. The trip assignment step also assigns the highway trips to the highway network. Thus, the traffic volumes on the highways and the ridership on the transit lines can be obtained from the outputs of this step.

Population and employment data are key inputs to the demand forecasting process; those used in this study were obtained from the Metropolitan Area Planning Council (MAPC). The highway travel times used in the analysis are those used in recent CTPS transit and highway studies. Downtown parking costs were obtained from recent CTPS studies. The travel demand model set assumes that, in general, people wish to minimize transfers. It also assumes that they may wish to minimize travel time, even if doing so costs more.

Note that the travel demand model set does not possess the capability of modeling THE RIDE, given the nature of paratransit service. As a result, the ridership and revenue impacts on THE RIDE that are included with the travel demand model set results are taken from the spreadsheet model results.

Existing revenue was estimated by multiplying the trips estimated by the model

METHODS USED TO ESTIMATE RIDERSHIP AND REVENUE

24 3/28/2012 Boston Region MPO

set for each mode by the average fare for that mode. The average fares were based on calculations in the spreadsheet model. The revenue impact was estimated by taking the ratio from the spreadsheet model of each mode’s change in revenue divided by the change in unlinked trips and applying this to the travel demand model set’s estimate of the change in that mode’s unlinked trips.

3.3 DIFFERENCES BETWEEN THE TWO ESTIMATION METHODOLOGIES There are several differences between the two methodologies. The spreadsheet model is primarily used to estimate the impacts of a fare change (though the estimated ridership impacts of service changes can be added to the model as an adjustment to existing ridership, so that the spreadsheet model’s projections will reflect the impacts of a simultaneous change in fare and service). On the other hand, the travel demand model set can forecast both impacts caused by fare changes and those caused by service changes.

The chief strengths of the spreadsheet model are that it accounts for every distinct type of fare that can be paid for an MBTA transit mode and that it assigns the fare to the correct number of passengers who are in that fare-payment/modal category. In comparison, the travel demand model set does not permit analysis of fares at this detailed level, but assumes for each more-generalized modal category an average fare for all fare types. However, unlike the travel demand model set, the spreadsheet model cannot predict how many riders who leave the system due to a fare increase are switching to modes other than transit (driving alone, carpooling, bicycling, or walking). The travel demand model set also provides the outputs necessary for conducting the air quality and environmental justice impact analyses.

There is another key difference between the two approaches in how they estimate ridership changes. The use of elasticities in the spreadsheet model has a relatively simple premise: the greater the percent change in price, the greater the percent change in demand. In the travel demand model set, while a greater percent change in fares will undoubtedly trigger a greater decline in transit ridership, it is not so much the percent change in transit fares that is important for determining the overall ridership change. Rather, it is the comparison of the resulting transit fares to the comparable cost of making the same trip via a different mode. For example, if the price of transit increases relative to the cost of driving, the travel demand model set will show transit diversions to driving.

CTPS 3/28/2012 25

Ridership and Revenue Impacts

4.1 OVERVIEW OF RESULTS AND METHODOLOGY Scenario 3 is projected to result in a gain in annual revenue of between $88.3 million using the travel demand model set and $91.6 million using the spreadsheet model. The corresponding estimated annual ridership losses are 20.2 million and 21.4 million unlinked trips.

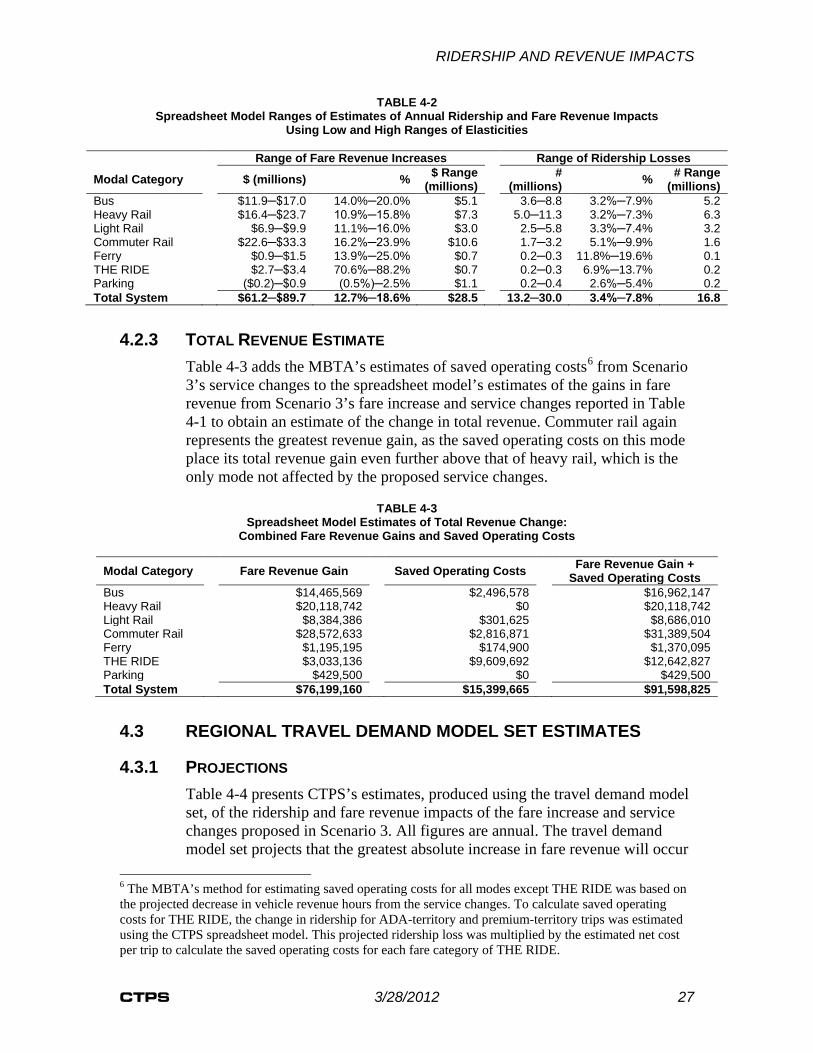

The 2007 Post–Fare Increase Impacts Analysis shows the projections from the spreadsheet model, which uses elasticities to project ridership and revenue changes based on a detailed analysis by mode and fare category, to be close to the actual changes in ridership and revenue that occurred after that fare increase was implemented. In addition, through the 2007 Post–Fare Increase Impacts Analysis, CTPS was able to adjust the elasticities in the spreadsheet model to even better reflect the changes that occurred. This presumably improved the capability of the spreadsheet model to accurately project the ridership and revenue impacts of other fare increases. However, this marks the first time that CTPS has modeled the combined impacts of both a fare increase and service changes. The travel demand model set is capable of incorporating both a fare increase and service changes into its projections, whereas in the case of the spreadsheet model, the ridership losses associated with service changes must be made independently and then added to the model. Therefore, it was appropriate to use both models in combination as well as to conduct a sensitivity analysis of the spreadsheet model using different elasticity values to help to define a range of probable outcomes of the changes in fares and service.

4.2 SPREADSHEET MODEL ESTIMATES

4.2.1 PROJECTIONS Table 4-1 presents CTPS’s estimates of the ridership and fare revenue impacts of the Scenario 3 fare increase and service changes produced using the spreadsheet model and its medium range of elasticities. The existing ridership and fare revenue numbers, also presented, represent existing conditions before any adjustments are made to account for the estimated ridership lost due to the service reductions in this scenario. All figures are annual.

RIDERSHIP AND REVENUE IMPACTS

26 3/28/2012 Boston Region MPO

The total projected fare revenue increase from Scenario 3 comes to $76.2 million, or a 15.8 percent increase. The total projected ridership loss is estimated at 21.4 million annual unlinked trips, or a 5.5 percent decrease. The greatest absolute fare revenue increase is projected for the commuter rail category ($28.6 million). This is due partly to the fact that commuter rail not only has one of the highest existing average fares, but also faces one of the greater percentage increases in price of all modes. Heavy rail (Blue, Orange, and Red Lines) has the second-greatest projected absolute revenue increase ($20.1 million), followed by the bus category ($14.5 million). Ferry is projected to have the greatest percentage decrease in ridership (15.7 percent), while the absolute number of lost riders is projected to be greatest for heavy rail (8.1 million unlinked trips).

TABLE 4-1 Spreadsheet Model Estimates of Annual Ridership and Fare Revenue Impacts

Existing Fare Revenue Change Ridership Change

Modal Category Fare Revenue Ridership $ % # % Bus $84,943,464 111,903,868 $14,465,569 17.0% -6,168,961 -5.5% Heavy Rail $150,316,826 153,439,900 $20,118,742 13.4% -8,067,167 -5.3% Light Rail $61,940,368 77,659,524 $8,384,386 13.5% -4,143,170 -5.3% Commuter Rail $139,408,504 32,808,010 $28,572,633 20.5% -2,346,821 -7.2% Ferry $6,123,737 1,309,167 $1,195,195 19.5% -204,992 -15.7% THE RIDE $3,820,407 2,359,966 $3,033,136 79.4% -242,634 -10.3% Parking $36,501,063 6,889,609 $429,500 1.1% -263,279 -3.8% Total System $483,054,370 386,370,044 $76,199,160 15.8% -21,437,023 -5.5%

4.2.2 SENSITIVITY ANALYSIS The results reported in Table 4-1 were produced using the medium range of elasticities. Table 4-2 presents a sensitivity analysis of the spreadsheet model, showing the range of Scenario 3’s estimated ridership and fare revenue impacts from the fare increase and service changes using the lower and higher ranges of elasticities presented in Table 3-1. In the ranges of ridership-loss estimates in the table, the greater losses are those resulting from the higher range of elasticities, while in the ranges of fare-revenue-increase estimates, the greater increases are those resulting from the lower range of elasticities.

The use of the higher range of elasticities results in much greater estimates of ridership losses: 30.0 million unlinked trips, compared to 13.2 million using the lower range of elasticities; using the medium range of elasticities results in a loss of 21.4 million unlinked trips. As a result, the projected revenue gain from the fare increase estimated using the higher range of elasticities is approximately $15.0 million less than that estimated using the medium range of elasticities ($61.2 million versus $76.2 million) and $28.5 million less than that estimated using the lower range of elasticities.

RIDERSHIP AND REVENUE IMPACTS

CTPS 3/28/2012 27

TABLE 4-2 Spreadsheet Model Ranges of Estimates of Annual Ridership and Fare Revenue Impacts

Using Low and High Ranges of Elasticities

Range of Fare Revenue Increases Range of Ridership Losses

Modal Category $ (millions) % $ Range (millions) #

(millions) % # Range (millions)