Embed Size (px)

Citation preview

HANK WATKINS Sean Murphy

PRESIDENT, LLOYD’S North AMERICA PRESIDENT, LLOYD’S CANADA

May 2013

Market Presentation North America

> www.lloyds.com/marketpresentations

> www.lloyds.com/countryprofiles

© Lloyd’s

Co

nt

en

t

LLOYD’S CANADA

LLOYD’S AMERICA • Hank Watkins

President, Lloyd’s North America

• Sean Murphy

President, Lloyd’s Canada

1

2

2

© Lloyd’s

Lloyd’s CANADA

• Canadian Economy Overview

• (Re)Insurance Market

• Lloyd’s Business Profile

• Operations

• Events

1

3

© Lloyd’s

Canada is a country where nothing

seems ever to happen. ….Clean…..

Dull….

Carol Shield

© Lloyd’s

ECONOMY

• Canadian economy projected to remain sub-par for a second consecutive year.

• Most major commodity prices suffered setbacks in 2012

• Canada economic fortunes are tied to the US – comprise for 75% of total exports

• Western provinces will grow faster than the national average, with the exception of

Newfoundland.

Lloyd’s > Canadian Economic Outlook Gross Domestic Product (GDP) (nominal GDP levels in billion US$; Real GDP change)

© Lloyd’s

Market data: The ‘Big Four’ Canadian Provinces

ON BC AB QC

2012 Premium

($000)

$488 $427 $321 $279

Market Share% 2% 6% 4% 4%

GDP%

13/14 real

1.4/2.5 1.6/2.6 2.5/3.3 1.4/2.3

GDP - nominal $ 655 bn $ 218 bn $ 295 bn $ 345 bn

Population

(2012)

14 m 5 m 4 m 8 m

Sources: RBC Economic Research – Provincial Outlook

TD Economics – Provincial Forecast

Insurance Market > Overview

© Lloyd’s

2013 Forecast Lead Provinces – Real GDP Growth

NF SK AB MB

2012 Premium

($1000)

$20 $38 $321 $43

Market Share % 3% 2% 4% 5%

GDP % 13/14

real

3.4/1.1 2.3/3.2 2.5/3.3 1.6/2.4

GDP nominal $33.6 bn $ 74.7 bn $295 bn $55 bn

Population 513 k 1 m 3.8 m 1.2 m

Economic Drivers Oil

Gas

Mining

Oil

Gas

Mining

Oil

Gas

Agriculture

Manufacturing

Mining

Sources: RBC Economic Research – Provincial Outlook

TD Economics – Provincial Forecast

Insurance Market > Overview

© Lloyd’s

Insurance Market > Overview

INSURANCE

New entrant activity:

Starr and Ironshore

Recent push by the Ontario government to reduce personal lines auto

premiums by 15%.

Rates in property and casualty remain generally flat

EQ hardening in BC and some parts of Quebec

reinsurance

Written Premiums dropped by 1%

9% improvement in combined LR

Little CAT activity in 2012

Source: Economy: Market Intelligence based on IHS Global Insight and other economic reports; May 2012; Insurance and Reinsurance: based on local intelligence from Lloyd’s Canada.

2

8

© Lloyd’s Source: Market Intelligence calculations based on P&C Canada 2012 Market Share Report - MSA Research Inc. www.msaresearch.com

* Please note: This figure does not include Reinsurance premiums.

insurance Market > Market Share

Total 2012

Canada Market

$49.9bn

2012 Direct Premiums by Class of Business in CAD m

Total 2012

Lloyd’s Canada

$1.7bn

Personal Lines business dominates the Canadian insurance market. Lloyd’s is not a

serious player in this segment.

1

© Lloyd’s

Top Five Canadian Catastrophes of 2012

Source: As published in the Top Canadian Insurance Brokers’ “The Claims Issue”

When What and Where Insured Loss

August 12 Hailstorm Calgary Alberta

$ 520 million

May 26 - 29 Series of Heavy Storms, Tornadoes Ontario and Quebec

$ 245 million

October 29 - 31 Remnants of Super-storm Sandy Ontario and Quebec

$ 100 million

July 11 - 12 Thunderstorm Edmonton, Alberta

$ 100 million

July 22 - 23 Wind and Rainstorms Hamilton / Ottawa corridor

$ 85 million

Insurance Market > Overview 1

© Lloyd’s

Lloyd’s > Provincial Share Lloyd’s Canadian Premium Written By Province

Ontario 33%

BC 22%

Alberta 16%

Quebec 15%

Other 14%

BC

CH – 91

OMC - 40

QC

CH – 61

OMC - 51

AB

CH – 31

OMC - 35

ON

CH – 116

OMC - 86

0

10

20

30

40

50

60

2009 2010 2011 2012 2013

Coverholders

Open Market Correspondents

Distribution

• Lloyd’s Coverholders - 333

• Open Market Correspondents - 251

New CH and OMC applications processed

Ontario,

47%

BC,

17%

Alberta,

16%

Quebec,

16%

Others,

4%

Canadian Market Premium Written by Province

© Lloyd’s

Positive industry result – 96% combined loss ratio

Double digit ROE – 11%. 3% top line growth.

Exclusive C/L insurer experience a 4.7% decrease

in direct premium

Avg 90% combined loss ratio for exclusive

C/L insurers.

insurance Market > Market Size

2009-2012 Loss Ratios for Total Market:

in % KEY FEATURES

2009-2012 Direct Premiums for Total Market:

in billion CAD

Source: Market Intelligence calculation based on: MSA Market Share Report Property & Casualty, Canada 2013

2

12

43.9 46.4

48.6 49.9

1.5 1.7 1.9 1.7 0

10

20

30

40

50

2009 2010 2011 2012

Market Lloyd's

71.1 70.7 70.5 64.6

51.7

62.7 62.1

50.8

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012

Market Lloyd's

Total

Premium

$2.1bn

Direct Written

Premium, $1.7bn

Reinsurance,

$0.3bn

2012 Total Lloyd’s Canadian Premiums

in billion CAD

© Lloyd’s

insurance Market > Competitor Ranking

2012 Market Leaders in CAD m

Excluding Auto & Personal Property

2012

Loss

Ratio

50%

51%

60%

55%

33%

55%

88%

50%

35%

Source: Market Intelligence calculation based on: MSA Market Share Report Property & Casualty, Canada 2013

1

Lloyd’s Underwriters has lost it’s number 1 status

13

956

879

871

757

644

584

560

497

Lloyd’s

Intact

Aviva

Royal & Sun All.

Chartis

Zurich

Genworth

Co-operators

Economical Mutual

Northbridge

61%

1,615

1,714

© Lloyd’s

Major lines of business breakdown 2012 * (in million CAD)

Source: Market Intelligence calculations based on P&C Canada 2013 Market Share Report - MSA Research Inc. www.msaresearch.com

* Please note: This figure does not include Reinsurance premiums. (this needs to be checked)

DWP 11

DWP 10

Loss Ratio

2012*

50%

58%

45%

46%

50%

DWP 12

Marine

Aviation

Personal

Property

Other

Commercial

Property

Liability

Premiums

2012*

827

595

110

110

62

Lloyd’s > Classes of business 2

Lloyd’s Underwriters DWP decreased by 7% - underwriting profitability

increased

14

40

-20%

© Lloyd’s

insurance Market > Liability 2009-2012 Premiums for Liability:

in million CAD

2012 Top 5 Companies in Liability:

prems in CAD / loss ratios in %

Lloyd’s 827.5m 58

Intact 569.3m 39

Aviva 352.4m 69

Chartis 341.5m 43

Zurich 304.8m 39

Premiums Loss Ratio

Source: Market Intelligence calculation based on: MSA Market Share Report Property & Casualty, Canada 2013

1

KEY CHARACTERISTICS

Commercial liability continues to attract capacity due

to its relative profitability

Pricing for Professional Liability and D+O will continue

to be under pressure due to surplus capacity

Cyber liability is relatively new and there appears to

be much capacity but at lower limits.

OUTLOOK

15

4,908 5,041 5,204 5,161

671 723 855 827

0

1000

2000

3000

4000

5000

6000

2009 2010 2011 2012

Market Lloyd's

© Lloyd’s

Private new dwelling construction has slowed down in

most parts of Canada. There is many insurers

competing for fewer projects.

Smaller mining operations are seeing flat to small price

reductions to the availability of capacity mostly from

local domestics

insurance Market > Commercial Property

2012 Top 5 Companies in Com. Property:

prems in CAD / loss ratios in %

2009-2012 DWP for Commercial Property:

in million CAD KEY CHARACTERISTICS

OUTLOOK 2012/2013

Intact 946.7m 63

Lloyd’s 595.3m

50

Aviva 504.3m 61

Royal & Sun

Alliance 420.0m 62

Zurich 382.6m 74

Premiums Loss Ratio

Source: Market Intelligence calculation based on: MSA Market Share Report Property & Casualty, Canada 2013

1

16

5,617 5,958

6,262 6,455

646 555 634 595

0

1000

2000

3000

4000

5000

6000

7000

2009 2010 2011 2012

Market Lloyd's

© Lloyd’s

Lloyd’s > Distribution

Source: Market Intelligence calculation based on: Xchanging data

2012 Top 10 Brokers by Premiums

CA

D m

illio

ns

2

The largest 10 London brokers accounted for 61% of business into Lloyd’s

17

0

50

100

150

200

250

300

BR1 BR2 BR3 BR4 BR5 BR6 BR7 BR8 BR9 BR10

Accident & Health Aviation Casualty Casualty Treaty Energy

Marine Overseas Motor Property (D&F) Property Treaty

© Lloyd’s

● OSFI Revised B-9 Guideline

● OSFI newly introduced draft ORSA Guideline

● Renewed Lloyd’s OSFI Prudential agreement

● OSFI Corporate Governance Guideline

insurance Market > Regulatory changes 2

18

© Lloyd’s

Operational Activity

19

Year Direct Reinsurance

2012 22,424 851

2013 9053 518

Bound contracts through ASPS from

January 2012 up to end April 2013 Lineage Growth in Premium 2007-2012

Lineage 2010 2011 2012

Training Sessions 44 71 72

In 2013, Lloyd’s Canada have made provisions for 15 webinar sessions. The main scope behind these

sessions is to provide sufficient knowledge for effective and efficient use of the main features of Lineage to

our stakeholders

© Lloyd’s

Lloyd’s > Raising Your Profile

Raising Awareness Associations

3

2013 Sponsorships

Photo courtesy of Canadian Insurance Top Broker – Copyright 2013

© Lloyd’s

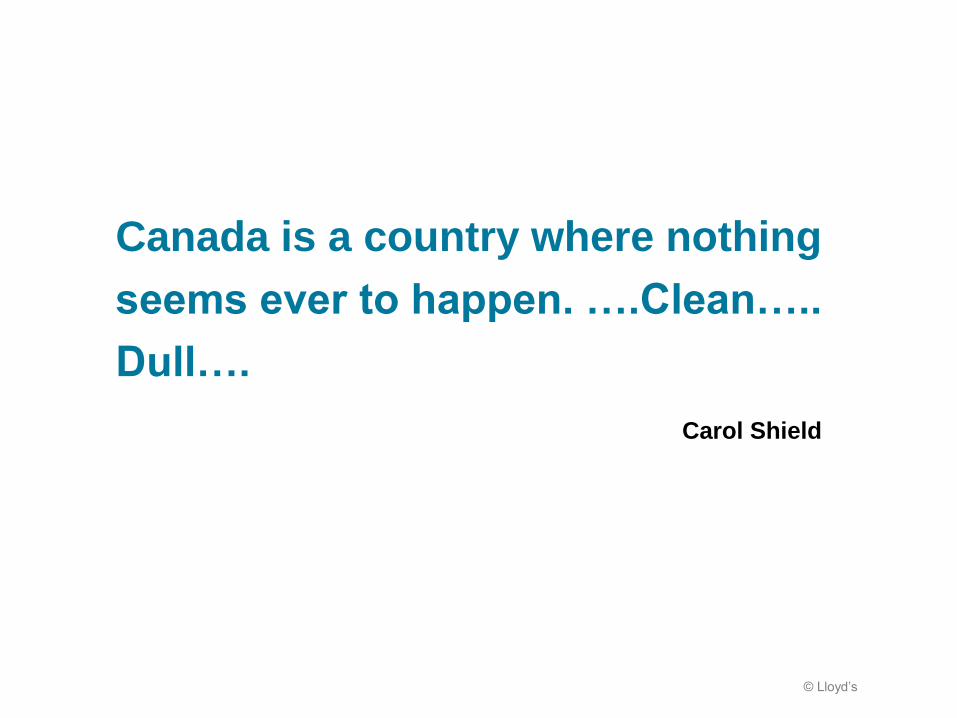

The Team

Sean Murphy, Angela Blackwood, Diana Dimech, Debbie Hnatiw

Toronto

Toronto

4 staff

Montreal

4 staff + 37

Seconded

TELUS

employees

• Relationship management with various industry bodies and

external stakeholders

• Regulatory strategy & management

• Lloyd’s promotion and market development support

• Operational oversight: Lloyd’s Canada & Lloyd’s Underwriters

• Operational hub

• AIF Signing Process

• Attorney in Fact office

• Lineage operations management &

IT enhancements

• Lineage customer relationships &

training

• Website content updates

• Financial/ tax reporting

• Compliance

• Management of

coverholder systems

• Call centre management

Essential to Lloyd’s in

Canada

Lucie Payette, Mary Arabian, Frank Flood, Andre Farant

Montreal

© Lloyd’s 22 22