Embed Size (px)

Citation preview

October 2013

Nido Petroleum Limited

Investor Update

Phil Byrne, Managing Director

2

Disclaimer and Competent Person Consent

This presentation contains forward looking statements concerning the financial condition, results of operations and business of Nido Petroleum Limited (‘the Company’). All statements other than statements of historical fact are, or may be deemed to be, forward looking statements. Forward looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause the actual results, performance or events to differ materially from those expressed or implied in these statements. These risks and uncertainties include, but are not limited to: price fluctuations, actual demand, currency fluctuations, drilling and production results, commercialisation, development progress, operating results, reserve estimates, environmental risks, physical risks, legislative, fiscal and regulatory developments, economic and financial market conditions in various countries, approvals and cost estimates, political risks including the risk of expropriation and renegotiation of the terms of contracts with government entities, delays or advancements in the approval of projects and delays in the reimbursement of shared costs. All references to dollars, cents or $ in this presentation are to Australian currency, unless otherwise stated.

Peer Group Comparisons

Any reference to ASX peer group includes the following companies: Tap Oil, MEO Ltd, Carnarvon Petroleum Ltd, Otto Energy Ltd, Rialto Ltd, Pan Pacific Petroleum Ltd, Cue Energy Resources Ltd, Pancontinental Oil & Gas Ltd, Neon Energy Ltd and Nexus Energy Ltd.

Reserves Information and Competent Person Consent

The reserves information contained in this presentation concerning the West Linapacan A field is a summary of the report filed by the Company on the ASX on 4 September 2013. Mr Stephen Lane, B.Sc. (Hons.) Geology, Technical Director, Gaffney Cline & Associates who is a member of the Society of Petroleum Engineers and has at least five years’ experience in the sector consented in writing to the inclusion of this information in the form and context in which it appears in this presentation.

The reserves information concerning the Galoc oil field contained in this presentation has been reviewed by Mr David Lim, BSc. (Hons), MSc. Director, Odin Reservoir Consultants Pty Ltd. Mr Lim is a Petroleum Reservoir Engineer and a member of the Society of Petroleum Engineers and has over five years’ experience in the sector. Mr Lim consented in writing to the inclusion of the information concerning the Galoc oil field in the form and context in which it appears in this presentation.

3

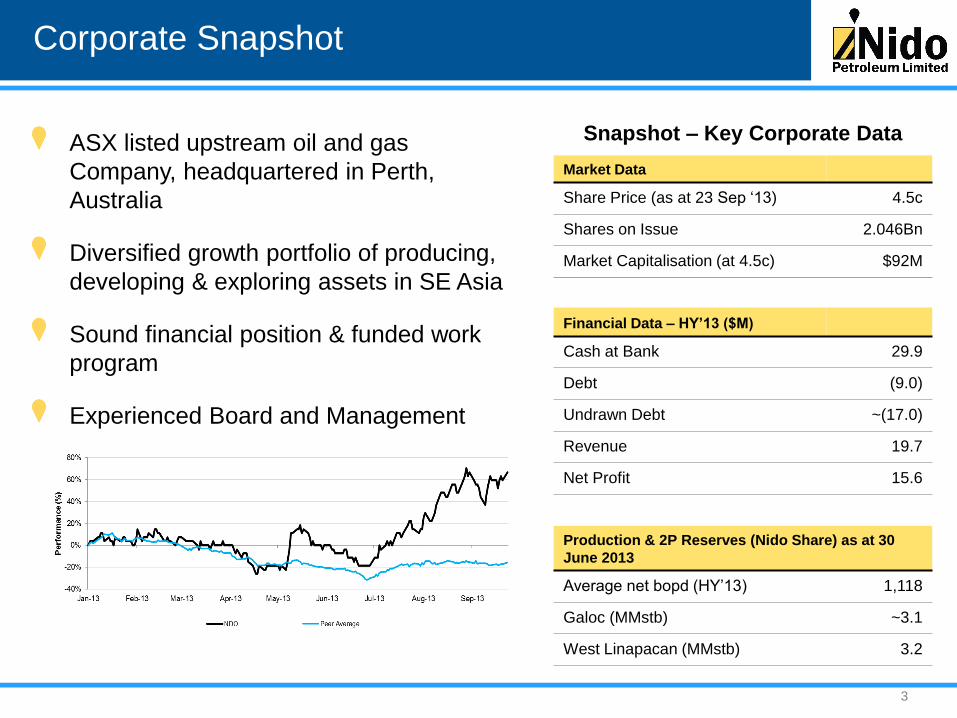

Corporate Snapshot

Snapshot – Key Corporate Data

Market Data

Share Price (as at 23 Sep ‘13) 4.5c

Shares on Issue 2.046Bn

Market Capitalisation (at 4.5c) $92M

Financial Data – HY’13 ($M)

Cash at Bank 29.9

Debt (9.0)

Undrawn Debt ~(17.0)

Revenue 19.7

Net Profit 15.6

Production & 2P Reserves (Nido Share) as at 30

June 2013

Average net bopd (HY’13) 1,118

Galoc (MMstb) ~3.1

West Linapacan (MMstb) 3.2

ASX listed upstream oil and gas

Company, headquartered in Perth,

Australia

Diversified growth portfolio of producing,

developing & exploring assets in SE Asia

Sound financial position & funded work

program

Experienced Board and Management

4

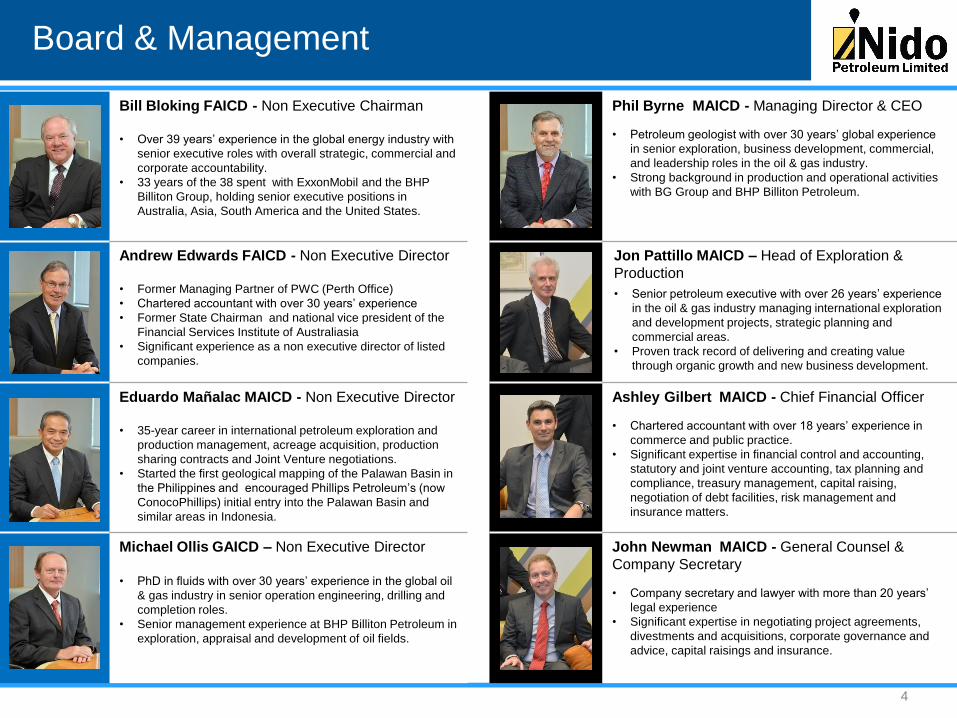

Board & Management

Bill Bloking FAICD - Non Executive Chairman

• Over 39 years’ experience in the global energy industry with

senior executive roles with overall strategic, commercial and

corporate accountability.

• 33 years of the 38 spent with ExxonMobil and the BHP

Billiton Group, holding senior executive positions in

Australia, Asia, South America and the United States.

Phil Byrne MAICD - Managing Director & CEO

• Petroleum geologist with over 30 years’ global experience

in senior exploration, business development, commercial,

and leadership roles in the oil & gas industry.

• Strong background in production and operational activities

with BG Group and BHP Billiton Petroleum.

Andrew Edwards FAICD - Non Executive Director

• Former Managing Partner of PWC (Perth Office)

• Chartered accountant with over 30 years’ experience

• Former State Chairman and national vice president of the

Financial Services Institute of Australiasia

• Significant experience as a non executive director of listed

companies.

Jon Pattillo MAICD – Head of Exploration &

Production

• Senior petroleum executive with over 26 years’ experience

in the oil & gas industry managing international exploration

and development projects, strategic planning and

commercial areas.

• Proven track record of delivering and creating value

through organic growth and new business development.

Eduardo Mañalac MAICD - Non Executive Director

• 35-year career in international petroleum exploration and

production management, acreage acquisition, production

sharing contracts and Joint Venture negotiations.

• Started the first geological mapping of the Palawan Basin in

the Philippines and encouraged Phillips Petroleum’s (now

ConocoPhillips) initial entry into the Palawan Basin and

similar areas in Indonesia.

Ashley Gilbert MAICD - Chief Financial Officer

• Chartered accountant with over 18 years’ experience in

commerce and public practice.

• Significant expertise in financial control and accounting,

statutory and joint venture accounting, tax planning and

compliance, treasury management, capital raising,

negotiation of debt facilities, risk management and

insurance matters.

Michael Ollis GAICD – Non Executive Director

• PhD in fluids with over 30 years’ experience in the global oil

& gas industry in senior operation engineering, drilling and

completion roles.

• Senior management experience at BHP Billiton Petroleum in

exploration, appraisal and development of oil fields.

John Newman MAICD - General Counsel &

Company Secretary

• Company secretary and lawyer with more than 20 years’

legal experience

• Significant expertise in negotiating project agreements,

divestments and acquisitions, corporate governance and

advice, capital raisings and insurance.

5

Company Strategy

To build a high quality balanced portfolio of producing,

development and exploration assets in Asia

To focus on reserves and production growth in the

near term

To provide a high quality exploration drilling program

which is fundable from cash resources and has the

potential to have a material impact

To forge partnerships with value adding partners

6

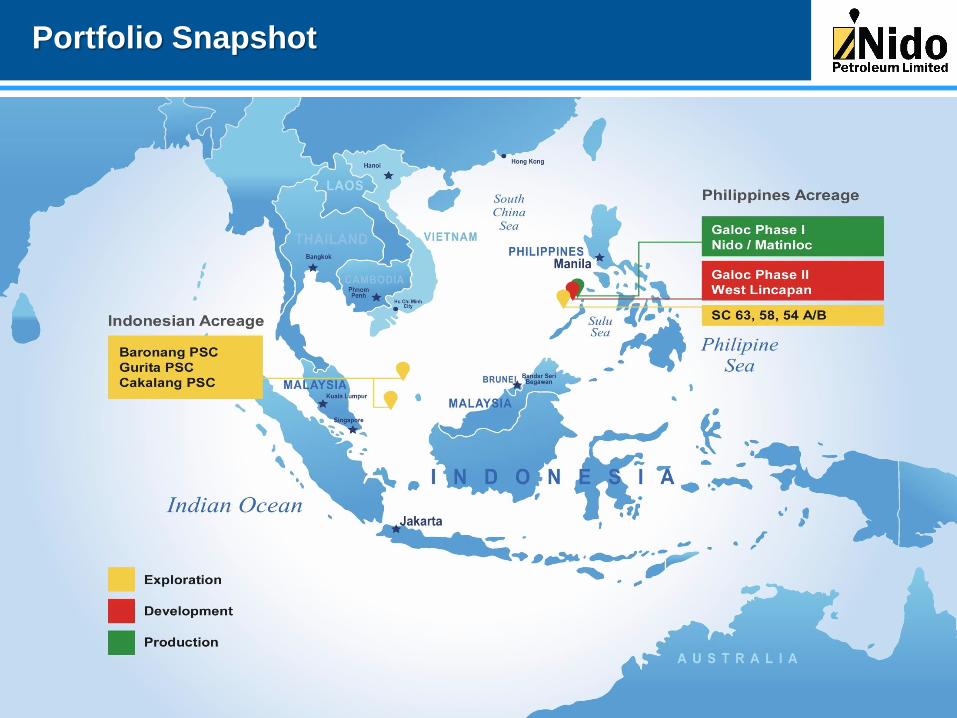

Portfolio Snapshot

7

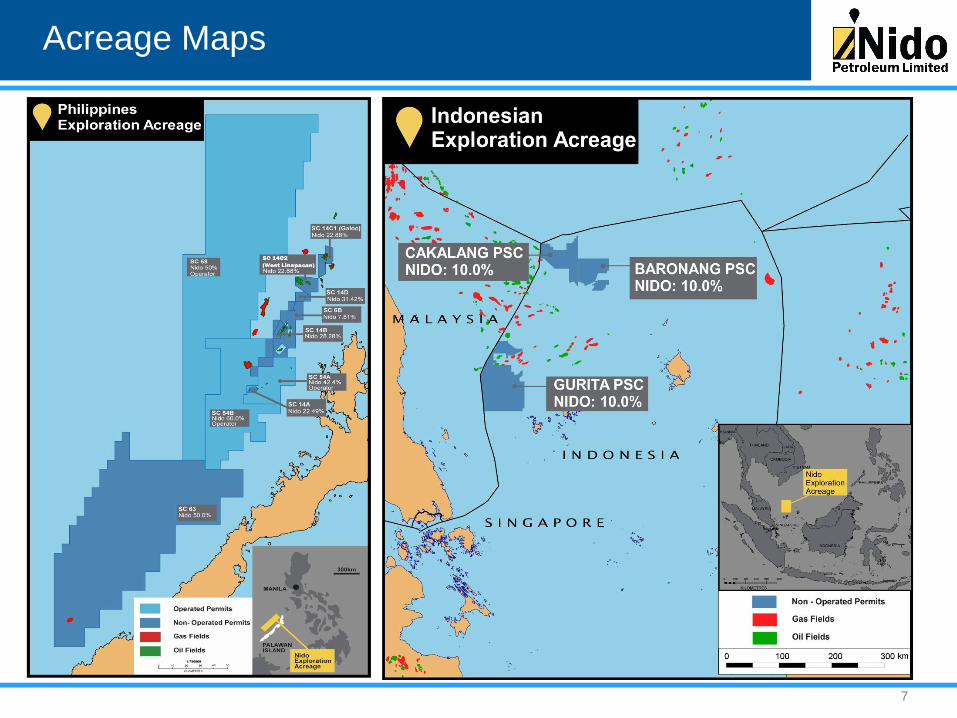

Acreage Maps

8

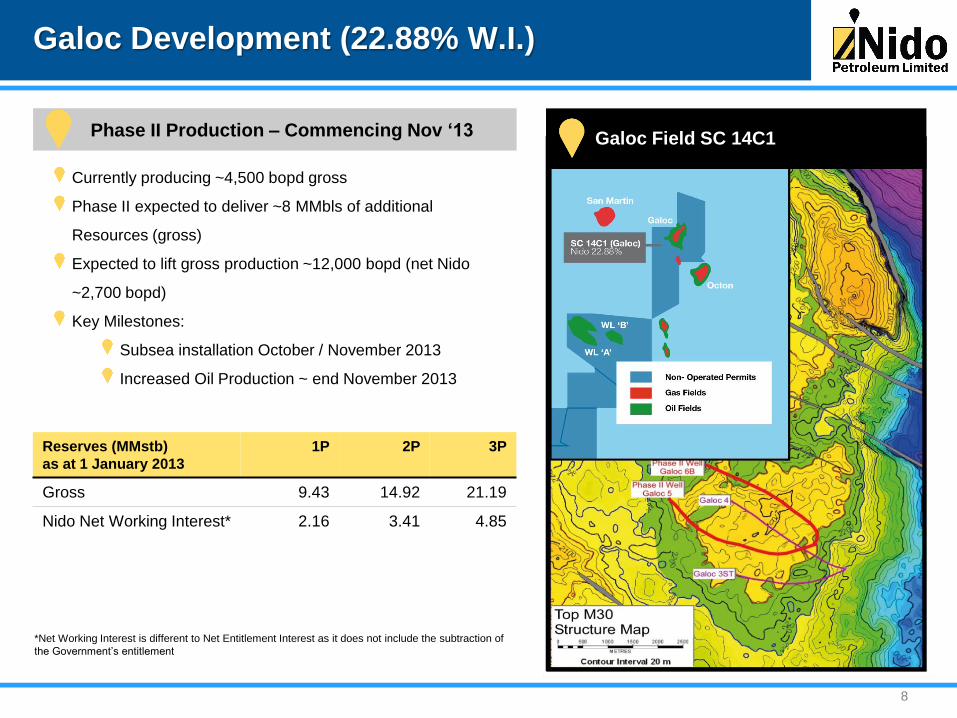

Galoc Development (22.88% W.I.)

Phase II Production – Commencing Nov ‘13

Currently producing ~4,500 bopd gross

Phase II expected to deliver ~8 MMbls of additional

Resources (gross)

Expected to lift gross production ~12,000 bopd (net Nido

~2,700 bopd)

Key Milestones:

Subsea installation October / November 2013

Increased Oil Production ~ end November 2013

Galoc Field SC 14C1

Reserves (MMstb)

as at 1 January 2013

1P 2P 3P

Gross 9.43 14.92 21.19

Nido Net Working Interest* 2.16 3.41 4.85

*Net Working Interest is different to Net Entitlement Interest as it does not include the subtraction of

the Government’s entitlement

9

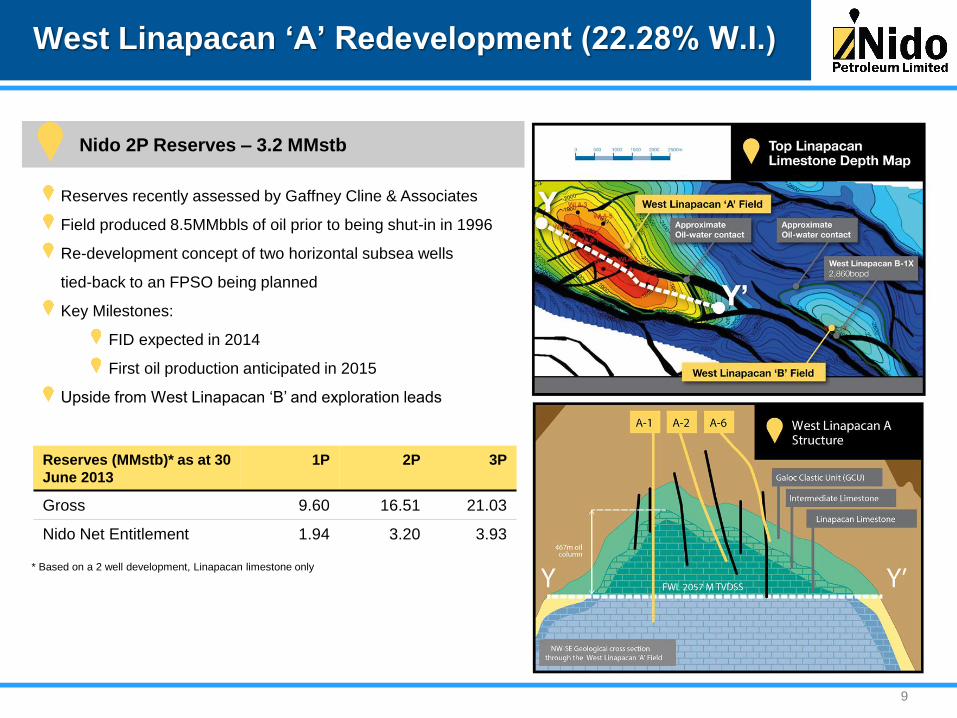

West Linapacan ‘A’ Redevelopment (22.28% W.I.)

Nido 2P Reserves – 3.2 MMstb

Reserves recently assessed by Gaffney Cline & Associates

Field produced 8.5MMbbls of oil prior to being shut-in in 1996

Re-development concept of two horizontal subsea wells

tied-back to an FPSO being planned

Key Milestones:

FID expected in 2014

First oil production anticipated in 2015

Upside from West Linapacan ‘B’ and exploration leads

Reserves (MMstb)* as at 30

June 2013

1P 2P 3P

Gross 9.60 16.51 21.03

Nido Net Entitlement 1.94 3.20 3.93

* Based on a 2 well development, Linapacan limestone only

10

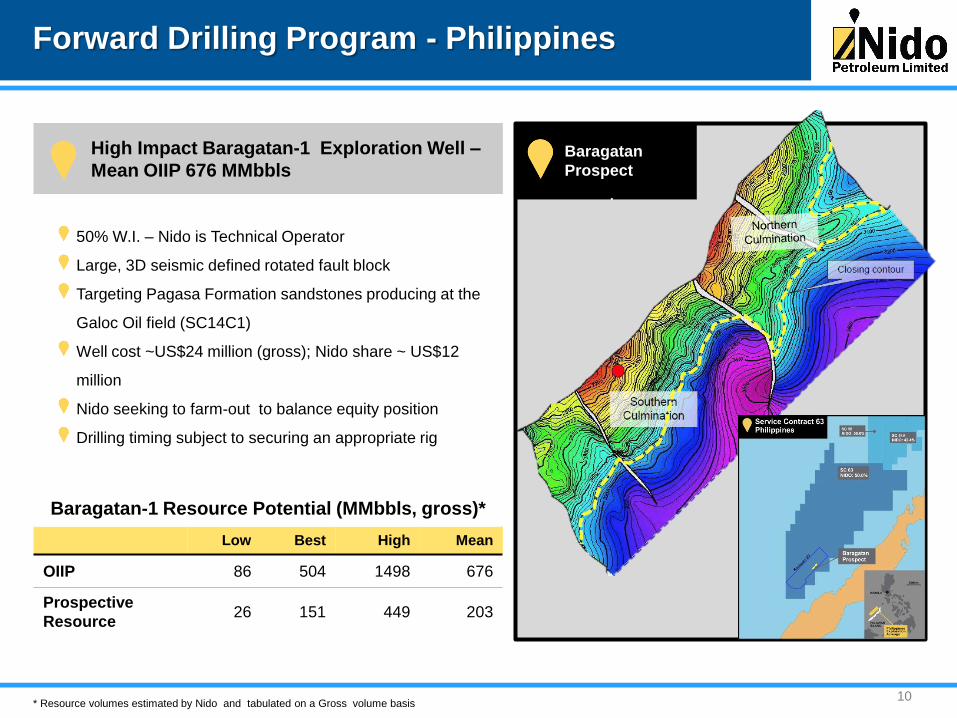

Forward Drilling Program - Philippines

High Impact Baragatan-1 Exploration Well –

Mean OIIP 676 MMbbls

50% W.I. – Nido is Technical Operator

Large, 3D seismic defined rotated fault block

Targeting Pagasa Formation sandstones producing at the

Galoc Oil field (SC14C1)

Well cost ~US$24 million (gross); Nido share ~ US$12

million

Nido seeking to farm-out to balance equity position

Drilling timing subject to securing an appropriate rig

* Resource volumes estimated by Nido and tabulated on a Gross volume basis

Baragatan-1 Resource Potential (MMbbls, gross)*

Low Best High Mean

OIIP 86 504 1498 676

Prospective

Resource 26 151 449 203

Baragatan

Prospect

11

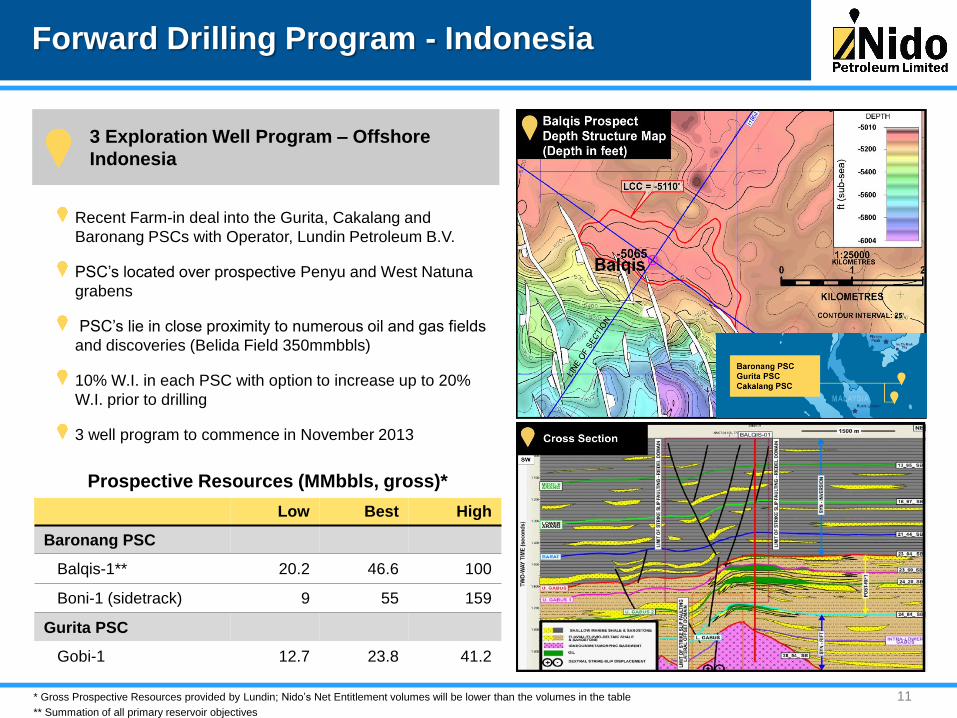

Forward Drilling Program - Indonesia

3 Exploration Well Program – Offshore

Indonesia

Recent Farm-in deal into the Gurita, Cakalang and

Baronang PSCs with Operator, Lundin Petroleum B.V.

PSC’s located over prospective Penyu and West Natuna

grabens

PSC’s lie in close proximity to numerous oil and gas fields

and discoveries (Belida Field 350mmbbls)

10% W.I. in each PSC with option to increase up to 20%

W.I. prior to drilling

3 well program to commence in November 2013

* Gross Prospective Resources provided by Lundin; Nido’s Net Entitlement volumes will be lower than the volumes in the table

** Summation of all primary reservoir objectives

Prospective Resources (MMbbls, gross)*

Low Best High

Baronang PSC

Balqis-1** 20.2 46.6 100

Boni-1 (sidetrack) 9 55 159

Gurita PSC

Gobi-1 12.7 23.8 41.2

12

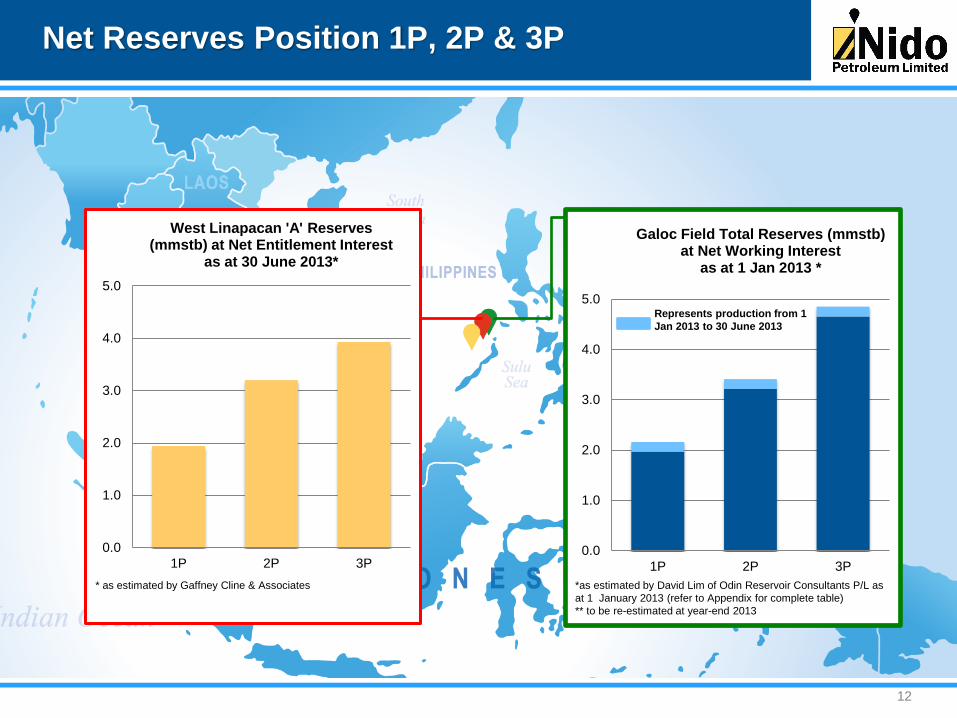

Net Reserves Position 1P, 2P & 3P

0.0

1.0

2.0

3.0

4.0

5.0

1P 2P 3P

West Linapacan 'A' Reserves (mmstb) at Net Entitlement Interest

as at 30 June 2013*

* as estimated by Gaffney Cline & Associates

0.0

1.0

2.0

3.0

4.0

5.0

1P 2P 3P

Galoc Field Total Reserves (mmstb) at Net Working Interest

as at 1 Jan 2013 *

Represents production from 1

Jan 2013 to 30 June 2013

*as estimated by David Lim of Odin Reservoir Consultants P/L as

at 1 January 2013 (refer to Appendix for complete table)

** to be re-estimated at year-end 2013

13

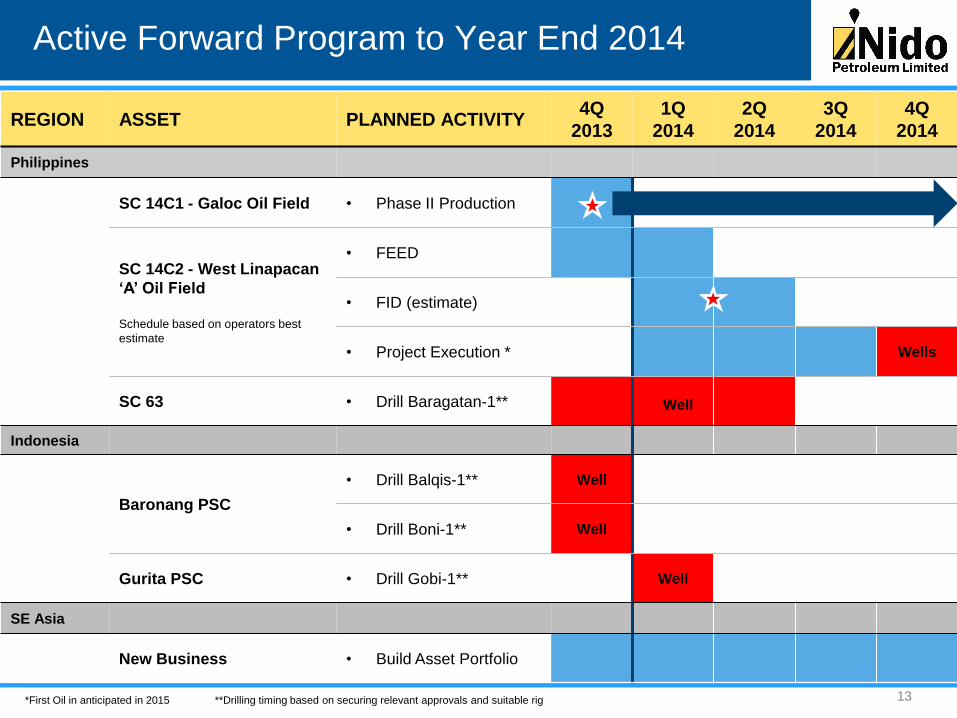

Active Forward Program to Year End 2014

REGION ASSET PLANNED ACTIVITY 4Q

2013

1Q

2014

2Q

2014

3Q

2014

4Q

2014

Philippines

SC 14C1 - Galoc Oil Field • Phase II Production

SC 14C2 - West Linapacan

‘A’ Oil Field

Schedule based on operators best

estimate

• FEED

• FID (estimate)

• Project Execution * Wells

SC 63 • Drill Baragatan-1**

Indonesia

Baronang PSC

• Drill Balqis-1** Well

• Drill Boni-1** Well

Gurita PSC • Drill Gobi-1** Well

SE Asia

New Business • Build Asset Portfolio

*First Oil in anticipated in 2015 **Drilling timing based on securing relevant approvals and suitable rig

Well

14

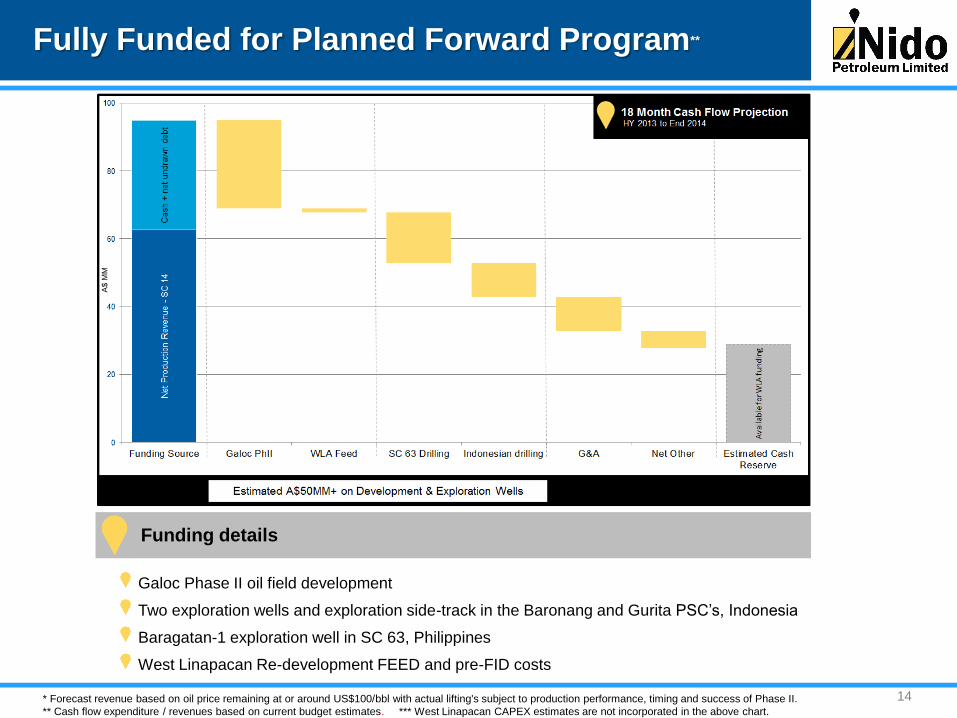

Fully Funded for Planned Forward Program**

* Forecast revenue based on oil price remaining at or around US$100/bbl with actual lifting's subject to production performance, timing and success of Phase II.

** Cash flow expenditure / revenues based on current budget estimates. *** West Linapacan CAPEX estimates are not incorporated in the above chart.

A$

MM

Funding details

Galoc Phase II oil field development

Two exploration wells and exploration side-track in the Baronang and Gurita PSC’s, Indonesia

Baragatan-1 exploration well in SC 63, Philippines

West Linapacan Re-development FEED and pre-FID costs

15

Fully funded work program for approved activity in 2013 and 2014

Base production set to almost triple by end of November 2013

(~1000 bopd to ~2700 bopd)

Recent significant reserves upgrade (2P reserves from ~3MMstb

to ~6 MMstb bbls net)

Active exploration program with 4 wells over the next 12 months

targeting a combined prospective resource of ~88 MMbbls net to

Nido

West Linapacan A reserves base paves the way for a second field

development with expected cash flow stream in 2015

Investment Proposition

Current share price underpinned by Galoc production,

with little recognition for West Linapacan A

development or near term exploration drilling potential

16

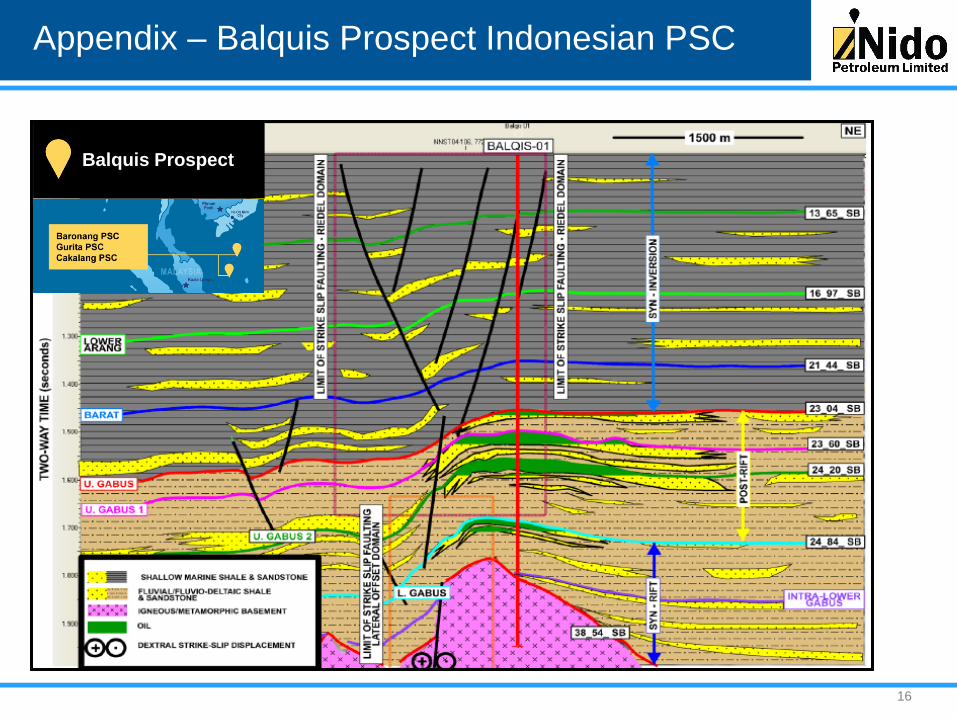

Appendix – Balquis Prospect Indonesian PSC

Balquis Prospect