Embed Size (px)

Citation preview

annual repor t2010

For

per

sona

l use

onl

y

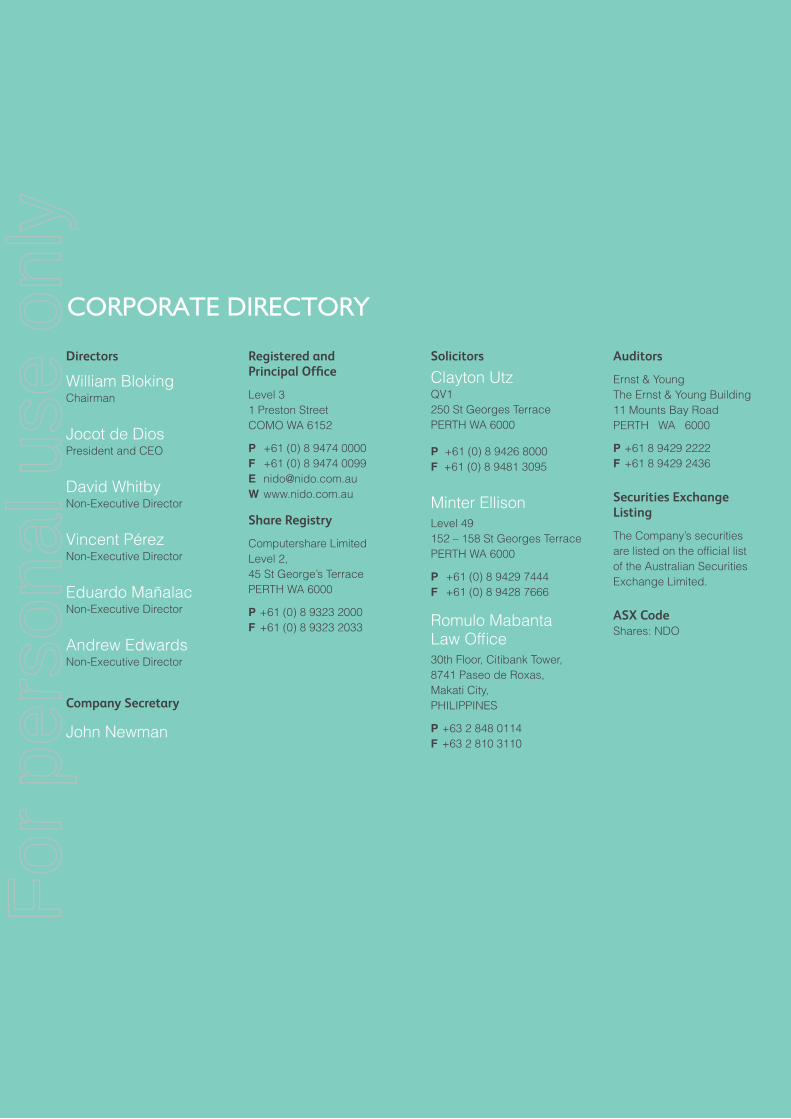

CORPORATE DIRECTORY

Directors

William Bloking Chairman

Jocot de Dios President and CEO

David Whitby Non-Executive Director

Vincent Pérez Non-Executive Director

Eduardo Mañalac Non-Executive Director

Andrew Edwards Non-Executive Director

Company Secretary

John Newman

Registered and Principal Office

Level 3 1 Preston Street COMO WA 6152

P +61 (0) 8 9474 0000 F +61 (0) 8 9474 0099 E [email protected] W www.nido.com.au

Share Registry

Computershare Limited Level 2, 45 St George’s Terrace PERTH WA 6000

P +61 (0) 8 9323 2000 F +61 (0) 8 9323 2033

Solicitors

Clayton Utz QV1 250 St Georges Terrace PERTH WA 6000

P +61 (0) 8 9426 8000 F +61 (0) 8 9481 3095

Minter EllisonLevel 49 152 – 158 St Georges Terrace PERTH WA 6000

P +61 (0) 8 9429 7444 F +61 (0) 8 9428 7666

Romulo Mabanta Law Office 30th Floor, Citibank Tower, 8741 Paseo de Roxas, Makati City, PHILIPPINES

P +63 2 848 0114 F +63 2 810 3110

Auditors

Ernst & Young The Ernst & Young Building 11 Mounts Bay Road PERTH WA 6000

P +61 8 9429 2222 F +61 8 9429 2436

Securities Exchange Listing

The Company’s securities are listed on the official list of the Australian Securities Exchange Limited.

ASX Code Shares: NDO

For

per

sona

l use

onl

y

2010 Summary 2

Chairman’s Letter 3

Chief Executive Offi cer’s Report 4

Operations Review 6

Petroleum Permit Interest Schedule 17

Directors’ Report 18

Auditor’s Independence Declaration 38

Corporate Governance Statement 39

Directors’ Declaration 47

Statement of Comprehensive Income 48

Balance Sheet 49

Statement Cash Flows 50

Statement of Changes In Equity 51

Notes to the Financial Statements 52

Independent Auditor’s Report 99

Additional Information 101

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 2

2010 SUMMARY

Production

❯ A total of 2.6 MMstb (gross) were produced from the Galoc oil

fi eld in 2010 corresponding to an average uptime of 84%.

❯ A total of 0.3 MMstb (gross) were produced from the Tindalo oil

fi eld Extended Well Test in 2010.

❯ Revenue from crude oil sales increased by 25.7% from

the previous year, to $60.1 million.

Development

❯ In March 2010 Nido farmed out 7.6% of its interest in SC 54A to

TG World (BVI) Corporation, ahead of the commencement of the

Tindalo oil fi eld Extended Well Test.

❯ Nido reprocessed 140 sq. km. of 3D seismic data within

SC 54A covering the Nido 1x1 and Yakal discoveries and the

Pungapong and Nandino prospects.

❯ First oil was achieved on 30 May 2010 at the Tindalo oil fi eld,

some fi ve months after achieving Final Investment Decision in

December 2009.

❯ The Tindalo oil fi eld Extended Well Test commenced on

6 June 2010.

❯ The Extended Well Test failed to produce oil at economic

rates due to excessive water production and the SC 54A Joint

Venture decided to abandon the well in December 2010 with

completion of abandonment occurring in the fi rst quarter of

2011.

Exploration

❯ The Company announced at its 21 May 2010 AGM a fi ve well

exploration program.

❯ In October 2010, Shell Philippines Exploration B.V. farmed into

SC 54B to earn a 45% Participating Interest in the block.

❯ A deepwater multi-beam and sea-bed coring program was

completed in SC 58 between March and April 2010. Results

indicate widespread micro-seepage of mature hydrocarbons

across the most prospective part of the block.

❯ Reprocessing of the Talusi 2D seismic in SC 58 was completed

during 2010 improving the subsurface imaging of the source

grabens in the deepwater.

❯ In SC 63, Pre Stack Depth Migration processing of the Kawayan

3D seismic was completed in July 2010.

❯ The SC 54 Sub-Phase 5 relinquishment of 25% due in August

2010 was successfully deferred to the end of Sub-Phase 6 in

August 2011.

❯ The Joint Philippine Basin Study conducted between Nido and

a SE Asian National Oil Company was completed in the fi rst half

of 2010.

Health, Safety, Security and Environment (HSSE)

❯ Excellent 2010 HSSE performance across all assets and

activities.

❯ Zero fatalities and zero Lost Time Injuries.

❯ Total Recordable Injury Frequency Rate (TRIFR) for 2010 was

2.05 compared to the National Offshore Petroleum Safety

Authority (NOPSA) benchmark of 7.87 as at 30 June 2010.

Corporate and Financial

❯ Cash on hand at year end of $24.2 million.

❯ Gross profi t from continuing operations of $7.5 million.

❯ Successfully completed a private share placement and Share

Purchase Plan, raising a total of $28.0 million (net).

❯ Debt reduced by US$10.0 million during the year, with debt

outstanding at year end of US$9.2 million (US$3.1 million as of

the date of this Annual Financial Report).

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 3

Dear Shareholder,

I am pleased to present my second Report to you as Chairman of Nido Petroleum Limited (Nido).

2010 was a very challenging year for our

Company – with highly mixed results.

The failure of the Extended Well Test at

Tindalo to produce oil at economic rates,

despite the investment of a signifi cant

amount of time, money, and effort, was a

major disappointment and the Company

recognises that we fell well short of

shareholders’ – and our own - expectations.

We are currently undertaking a thorough,

independent review of the Tindalo

development project in order to identify and

capture any lessons to be learned for future

development activities.

Notwithstanding the disappointing results at

Tindalo, we were pleased to have delivered

the project on schedule, on budget, and

with an excellent HSSE record. Moreover,

given our successful equity raising and

farmout activities during the year, coupled

with the continuing production at Galoc,

the Tindalo disappointment will not deter

Nido from pursuing its strategic exploration

objectives.

On a more positive note, the Galoc asset

performed very well, with 8 off-take cargoes

totaling 2.6 million barrels of oil (gross)

and a signifi cant increase in facility uptime

from 64 percent in 2009 to 84 percent in

2010. The Galoc Joint Venture is currently

considering further development options

which have the potential to signifi cantly

increase the life of the fi eld, and we are thus

optimistic about its future.

During the year, we farmed out 27 percent

of our 60 percent Participating Interest in

Service Contract 54B to Shell Philippines

Exploration B.V., thus enabling the

SC 54B Joint Venture to drill the Gindara

prospect commencing in May 2011. This

was a major strategic achievement for

the Company, with the Gindara prospect

marking the beginning of Nido’s “big hit”,

5-Well exploration campaign.

Whilst the current plan has the Aboabo

prospect in SC 63 as the likely second

well in our 5-Well campaign, the recently

completed Kawayan 3D Seismic Survey

within SC 63 has identifi ed a number of

exciting new leads and prospects which,

after further interpretation, could alter the

drilling sequence in that block and/or in the

overall program.

Nido also completed the geochemical

analysis of the deepwater sea-bed cores

acquired in SC 58 during the year. The

results provide evidence of an active source

system within the block, and the work

brings into focus the huge upside potential

of the large Balyena, Butanding and Dorado

prospects.

We also made signifi cant strides in the

reduction of our external debt. Through

share conversions as well as principal and

interest payments under the Convertible

Note with Merrill Lynch, external debt has

been reduced from US$19.2 million at the

beginning of 2010 to US$3.1 million as at

the date of this Annual Financial Report.

We look to the future with continued

enthusiasm and optimism. Nido’s

exploration portfolio contains more than

90 prospects and leads, with potential oil in

place (gross, mean, unrisked) of more than

11 billion barrels of oil equivalent. We have

spent more than $70 million on exploration

activities, including the acquisition of 2D

and 3D seismic over all areas of interest in

SC 54A and B, SC 63, and SC 58, as

well as sea-bed cores over the key areas

of interest in SC 58, in order to move key

prospects to a “drill-ready” status. This

work was an essential precursor to the

drilling of a strategic, statistically signifi cant

program that will test the key play types

across the basin and provide additional

technical data to further de-risk the portfolio.

The campaign will commence in 6 to 8

weeks with the drilling of Gindara, followed

by subsequent wells in SC 63, SC 58 and

SC 54A.

I would like to express my sincere thanks

to my fellow Directors, our Leadership

Team and our staff for their commitment

and dedication during the year, particularly

given some of the diffi cult decisions that

were required to be made concerning the

abandonment of Tindalo and the decision

to preserve our cash reserves for our

exploration drilling rather than pursuing a

development at Yakal. I would also like

to thank you, our shareholders, for your

support.

We eagerly await the commencement of

our drilling campaign. With the continued

support of our shareholders, our employees

and our Board, we can look forward to

2011 with excitement and enthusiasm

as we pursue the creation of signifi cant

shareholder value through the discovery

and development of new hydrocarbon

resources.

Yours faithfully,

William Bloking FAICD

Chairman

CHAIRMAN’S LETTERF

or p

erso

nal u

se o

nly

NIDO PETROLEUM ANNUAL REPORT 2010 4

CHIEF EXECUTIVE OFFICER’S REPORT

Dear Shareholder,

At the beginning of 2010, we were optimistic about the prospects of the coming year and looked forward to achieving first oil at Tindalo and strategically farming out working interests from our acreage to enable us to commence our “big hit” exploration program.

While we succeeded in achieving fi rst oil at Tindalo within fi ve months

from fi nal investment decision early water incursion proved to be

insurmountable and as the year ended the SC 54A Joint Venture

decided to plug and abandon the well.

We were, however, more fortunate with our farmout activities as

Shell Philippines Exploration B.V. entered into a farm-in transaction

involving the SC 54B block and a signifi cant carry for the drilling

of the Gindara prospect, one of Nido’s larger prospects. The

drilling of Gindara represents the start of the Company’s “big-hit”

exploration program that will see us drill the major prospects within

our portfolio.

Against the backdrop of these two key activities, work continued

on the rest of our acreage as we sought to mature other drilling

prospects. We also continued with the prudent monitoring and

management of spending even as credit and capital markets

began to open up.

Importantly, we achieved an excellent safety record during 2010,

in a year where the Company operated its fi rst offshore production

facility at Tindalo. We accumulated 977,788 man-hours during

the year with zero fatalities, zero Lost Time Injuries and a Total

Recordable Injury Frequency Rate (TRIFR) of 2.05. This TRIFR

rate compares well with the Australian National Offshore Petroleum

Safety Authority (NOPSA) current industry rate of 7.87 as at

30 June 2010.

With the drilling of Gindara on the horizon, we ended the year with renewed purpose and vigour to make 2011 better.

Exploration ActivityOur subsurface work for SC 54B’s Gindara prospect continued

and as Nido has been asked to continue as operator for the drilling

campaign, we have expanded our drilling and operations teams.

In SC 58, we completed a sea-bed coring survey which was

initiated to prove an active oil source within the block. Positive

results from geochemical studies of the cores indicate micro-

seepage concentrated in the central portion of the contract area.

These results highlight the very prospective nature of SC 58,

particularly around our key drilling prospects. The forward program

for this year involves further geological and geophysical work to

feed into drill planning.

Processing was completed on the Kawayan 3D seismic in

SC 63 showing a marked increase in imaging over the previous 2D

seismic. Structural studies and interpretation of this 3D seismic

have identifi ed a number of new Prospects and Leads. Further

work in 2011 is aimed at progressing Aboabo and other prospects

towards drilling.

As we completed the Shell Philippines Exploration B.V. farmout

near the end of 2010, we resumed farm-in activities for our other

blocks. Given the oil price environment and the continued level of

activity in the Philippine upstream sector, we are seeing continued

interest in exploration activity.

Development & Appraisal ActivityWhile Nido achieved fi rst oil at Tindalo in May 2010, early water

breakthrough on the third day of the Extended Well Test set the

pattern for what would ultimately be a disappointing project.

Despite signifi cant attempts to address the water infl ux, which

included the drilling of a short radius sidetrack well and a workover

of the sidetrack, the problem persisted. Given the uneconomic oil

production rates, the SC 54A Joint Venture decided in December

to plug and abandon the well and subsequently demobilise the rig.

Nido, as operator of the block has commissioned a thorough review of the project with a view to applying the lessons learned to other potential shallow water opportunities within our acreage.

Production ActivityAs we experienced disappointment with Tindalo, Galoc’s performance impressed. In 2010, Galoc produced a total of 2.6 MMstb of crude oil (604,208 stb net to Nido) with an average uptime of 84%. The crude cargoes continued to be marketed and sold throughout Southeast Asia, attracting repeat buyers in an increasingly improving price environment.

In the last twelve months, the Galoc Joint Venture continued to

review development options for the fi eld. This work has resulted in

a more robust understanding of the Galoc North Prospect as well

as the identifi cation of a new exploration target in the SC 14C1

block. This will add to the menu of options to be considered by the

SC 14C1 Joint Venture in 2011.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 5

CHIEF EXECUTIVE OFFICER’S REPORT

Corporate DevelopmentsNido continued to monitor its general and administrative

expenditures to stay in line with our commitment to run our

corporate operations more prudently and economically. When

Tindalo did not provide us with the expected second revenue

stream we conducted a private placement followed by a Share

Purchase Plan that generated the Company $28.0 million (net).

During the year we worked closely with Merrill Lynch to

successfully restructure our Convertible Note repayments in order

to manage our cash fl ow. Through a combination of principal

repayments and Merrill Lynch’s conversion of Notes, debt was

reduced by US$10 million to US$9.2 million by year end.

While we had hoped that 2010 would be better, this has only strengthened our resolve to continue with our “big hit” exploration program and our search for additional near term revenue streams from within our portfolio to complement Galoc production.

The fi rst part of 2011 will see the Company investing heavily not

only in preparations for Gindara, but also in maturing the identifi ed

prospects in SC 63 and SC 58. We have committed ourselves to

drilling an exploration program, and not just one well. While Gindara

sits as one of our leading prospects in the inventory today, there

are more that Nido intends to drill within the NW Palawan Basin.

The current production asset and other shallow water opportunities

will be evaluated and pursued to enable us to fund this program.

With your continued support we will meet with success.

Yours faithfully,

J.V. Emmanuel Araullo de Dios MAICD

President and Chief Executive Offi cer

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 6

OPERATIONS REVIEW

PRODUCTION AND DEVELOPMENT

2010 PRODUCTION SUMMARY

Field

Gross Oil Production Net Production to Nido

Year Total

Average Daily

Year Total

Average Daily

Stb Bopd Stb Bopd

Galoc 2,640,826 7,235 604,208 1,655

Nido & Matinloc 156,131 428 39,137 107

Tindalo 268,851 737 113,993 312

Total 3,065,808 8,400 757,338 2,074

Galoc – SC 14 Block C1, North West Palawan Basin, Philippines

The Company’s wholly owned subsidiaries, Nido Production

(Galoc) Pty Ltd and Nido Petroleum Philippines Pty Ltd, hold a

combined 22.879% interest in Service Contract SC 14C1 which

contains the Galoc oil fi eld development.

Production ActivitiesOperationally, 2010 was a better year for the Galoc oil fi eld with

an average uptime of 84% compared to the 64% average uptime

registered in 2009. The improved uptime allowed the fi eld to

produce at a rate of 7,235 bopd (gross average for the year).

The Galoc oil fi eld produced about 2.6 MMstb gross (604,208

stb net to Nido) during the year with a cumulative production from

start-up to year end of 6.2 MMstb. A total of eight cargoes were

sold to buyers in Korea and Japan.

Facility Repairs and EnhancementsIn the fourth quarter of 2010 the FPSO contractor tested a Torpedo

Buoy enhancement to the Mooring and Riser system. Unfortunately,

during rough weather it separated on 25 October 2010 and a

31 day shutdown ensued. The Operator resumed production on

25 November 2010 and the system has been restored to its

pre-trial condition.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 7

OPERATIONS REVIEW

Galoc – SC 14 Block C1, North West Palawan Basin, Philippines - continued

Further DevelopmentPotential Phase 2 options for the development of the Galoc oil

fi eld were investigated throughout 2010. Reprocessed Pre Stack

Depth Migration Galoc 3D seismic data was integrated with

previous 3D mapping and in this context new Top Nido depth

maps were generated by the Operator and Nido. Various potential

development scenarios involving one to two horizontal wells with

possible pilot holes were being considered by the Joint Venture

during the year, but no decisions on the optimal development

scenario had been made by the end of 2010.

A biostratigraphic review of key fi eld wells was also completed by

Nido on behalf of the SC 14C1 Joint Venture to better constrain

the vertical and lateral position of the G-3 and G-4 wells within

the Galoc Clastic Unit (GCU) stratigraphic sequences and provide

an improved realisation of the 3D-based structural model over

the western fl ank of the fi eld. It is anticipated that this work will

culminate in a revised view of the existing and future potential of

the Galoc development and will be critical in determining the scope

and value of Phase 2 development activities.

An independent subsurface review was also completed by Nido on

the Galoc North structure which lies immediately north of the Galoc

oil fi eld. Preliminary seismic interpretation indicates that a common

oil-water contact could exist between the Galoc fi eld and the Galoc

North structure which would signifi cantly upgrade Galoc North as a

potential low risk drilling target. Drilling of the Galoc North prospect

could potentially be combined with Phase 2 development activity.

Reserves Nido commissioned Gaffney Cline & Associates (GCA)

independently of the Galoc Joint Venture in the fi rst quarter of

2010 to update the Reserves estimates of the Galoc oil fi eld as at

31st December, 2009 from its pre-production estimates following

receipt of additional data from down-hole pressure measurements

in the two producing wells together with production data through to

the end of 2009.

Reserves estimates as at 31st December, 2009 outlined below

for the Galoc oil fi eld represent GCA’s estimates and are not

necessarily those of the SC 14C1 Joint Venture partners.

Nido has advised GCA that production performance of the Galoc

fi eld during 2010 has been consistent with the expectations for the

fi eld that were assumed for the 31st December, 2009 Reserves

estimate and has therefore applied the 2010 recorded production

volumes from the fi eld to update the Reserves position for the fi eld

at 31st December, 2010.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 8

OPERATIONS REVIEW

Galoc – SC 14 Block C1, North West Palawan Basin, Philippines - continued

The Reserves position for the Galoc oil fi eld is shown below:

Reserves

Category

STOIIP Recovery

Factor

Estimated

Ultimate

Recovery

at

31 Dec

2009

Production

Oct

2008 to

Dec 2009

Reserves(1)

at

31 Dec

2009

Production

Jan to

Dec

2010

Reserves(3)

at

31 Dec

2010

MMstb % MMstb MMstb MMstb MMstb MMstb

Proved

(1P)(2)89 11.7 10.4 3.6 6.8 2.6 4.2

Proved +

Probable

(2P)(2)

121 15.1 18.3 3.6 14.7 2.6 12.1

Proved +

Probable +

Possible

(3P)(2)

178 15.1 26.9 3.6 23.4 2.6 20.8

(1) In accordance with ASX Listing Rule 5.11, the Company confi rms that the hydrocarbon

reserves information above, was reviewed and signed off by Mr David S. Ahye, B. Eng.,

Principal Advisor, Gaffney Cline & Associates, who is a member of the Society of Petroleum

Engineers and has at least 5 years’ experience in the sector. Mr Ahye is not an employee of

the Company and consented in writing to the inclusion above of the hydrocarbon reserves

information in the form and context in which it appears.

(2) Please refer to the Glossary for defi nitions.

(3) Nido updated Reserves estimate based on 2010 fi eld production performance results.

Internal studies are underway to update the Galoc reserve

estimates as well as to determine options for further development

of the fi eld which have not yet been incorporated into the Reserves

estimates.

Nido and Matinloc – SC 14 Blocks A & B, North West Palawan Basin, Philippines

Nido’s wholly owned subsidiary, Nido Production (Galoc) Pty

Ltd, holds a 22.486% working interest in the Nido oil fi eld and a

28.283% working interest in the Matinloc oil fi eld. Both the Nido

and Matinloc oil fi elds are in late-life, cyclical production.

During 2010, both fi elds produced a combined total of 156,131

stb, averaging 428 bopd (approximately 107 bopd net to Nido).

Revenue from crude oil sales relating to the Nido and Matinloc

fi elds totalled $2.2 million for the year (2009: $1.5 million).

Tindalo and SC 54 BLOCK A – SC 54A, North West Palawan Basin, Philippines

The Company’s wholly owned subsidiary, Nido Petroleum

Philippines Pty Ltd, holds a 42.4% working interest in the SC 54A

block.

Development and Production ActivitiesFirst oil from the Tindalo project fl owed to surface on 30 May 2010.

Approximately 44 metres of the Nido limestone reservoir was

perforated and stimulated with acid achieving a maximum oil fl ow

rate of 18,689 bopd of 27°API oil with choke size 136/64th and a

fl owing tubing head pressure of 59 psig. Following a short-term drill

stem test, an Extended Well Test commenced on 6 June 2010.

Not long after the start of the Extended Well Test, the well saw

formation water breakthrough which displaced oil production. A

short radius sidetrack drilling program and subsequent sidetrack

workover failed to eliminate water production or reduce it

suffi ciently to permit economic oil production. The SC 54A Joint

Venture subsequently decided to abandon the Tindalo-1ST1 well

in December. Abandonment was completed in January 2011 and

the Joint Venture demobilised the project equipment (including the

Aquamarine Driller rig and Tove Knutsen FSO) from the Service

Contract area.

During the drill stem test and the Extended Well Test the Tindalo

fi eld produced a total of 268,851 stb* (gross). One cargo of

194,336 bbl* @ 60˚F was sold in September 2010 and another

cargo of 73,420 bbl* @ 60˚F was sold in the fi rst quarter of 2011.

* Please note that the difference in the cumulative volume of the cargoes compared with

the volume produced in the fi eld is due to the different units of measurement used.

Farmout to TG WorldOn 11 March 2010, Nido Petroleum Philippines Pty Ltd farmed-out

7.6% of its interest in SC 54A to TG World (BVI) Corporation (TG

World) a subsidiary of Canadian junior oil and gas company, TG

World Energy Corporation. Consideration from the transaction,

which includes contingent payments based on production

milestones, will total a maximum of US$6.8 million.

Seismic Reprocessing and Other StudiesNido has reprocessed 3D seismic data covering an area of

140 sq. km. within the central portion of the contract area which

includes the Tindalo fi eld and the Nido 1X1 and Yakal discoveries,

as well as the Pungapong and Nandino prospects along with

numerous smaller leads.

Following a thorough review of the Tindalo project including a

consideration of the lessons learned the SC 54A Joint Venture

intends to review the existing discoveries along with the prospects

and leads with a view to evaluating further development options in

this block.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 9

OPERATIONS REVIEW

West Linapacan – SC 14 Block C2, North West Palawan Basin, Philippines

The Company’s wholly owned subsidiary, Nido Production (Galoc)

Pty Ltd, holds a 22.279% working interest in the West Linapacan

block.

West Linapacan A was discovered in the early 1990’s and,

following the drilling and completion of three vertical subsea wells,

an FPSO-type development was employed to produce from the

fi eld from 1992 through to early 1996. The fi eld generated a peak

production rate of over 18,000 bopd. The fi eld has now been shut

in for over 12 years and it is believed that it will have returned to

close to its pre-production state. This presents the West Linapacan

Joint Venture with the opportunity to redevelop the fi eld, possibly

in conjunction with a development of the nearby unproduced West

Linapacan B oil discovery.

Throughout 2010 the block Operator, Pitkin Petroleum, continued

its development studies over the West Linapacan area. This

included the reprocessing of the 3D seismic data set and

interpretation and integration with the fi elds’ production history.

Detailed stratigraphic and structural mapping of the reservoir

utilising the 3D seismic inversion volume was undertaken and

the Operator is planning to update the potential reserves and

conceptual development plan following this detailed reservoir

mapping.

EXPLORATION

At the Company’s Annual General Meeting held on 21 May 2010,

the Board of Directors announced plans to initiate a fi ve well

drilling exploration program across its NW Palawan exploration

acreage commencing in 2011. The planned drilling candidates

in this program are designed to deliver a number of key strategic

objectives:

• Maximise the chances of making a signifi cant commercial

discovery by drilling a set of wells comprising a balanced mix of

low to high risk/reward prospects.

• Test a number of key play types across the basin which

would provide additional subsurface data to further de-risk the

exploration portfolio.

• Meet future Service Contract work program obligations.

• Secure tenure over the Company’s exploration acreage.

The fi ve well program will test two distinct geological provinces:

(i) the NW Palawan geological province (SC 54B/SC 58) where

the primary target is the proven Nido Limestone play in both

shallow and deepwater environments; and (ii) the Sabah geological

province (SC 63) which represents the extension of the prolifi c

offshore fold-thrust belt of Brunei and Sabah where the primary

reservoirs are the Miocene-aged clastics and a new potential

reservoir objective in the deeper pre-Nido section.

The current drilling candidates for the fi ve well program are:

Gindara (mid water depth, SC 54B), Balyena (deepwater,

SC 58), Aboabo area and Kalapato (shallow water, SC 63) and

Lawaan (shallow water, SC 54A). The timing of these wells will be

infl uenced by a number of factors including Joint Venture approvals

and rig availability.

Following the Shell Philippines Exploration B.V. farm-in to SC 54B,

the Gindara prospect will be the fi rst well to be drilled in 2011.

PuertoPrincesa

Lawaan

Kalapato

Gindara

Balyena

Aboabo

120°

0'0"

E

10°0'0"N

0 50 10025

km

Prospects

Gas Fields

Oil Fields

NIDO Operated Permits

Non Operated PermitsSC 58

SC 63

SC 54A

SC 54B

SC 14C-1

SC 14C-2

SC 6B

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 10

OPERATIONS REVIEW

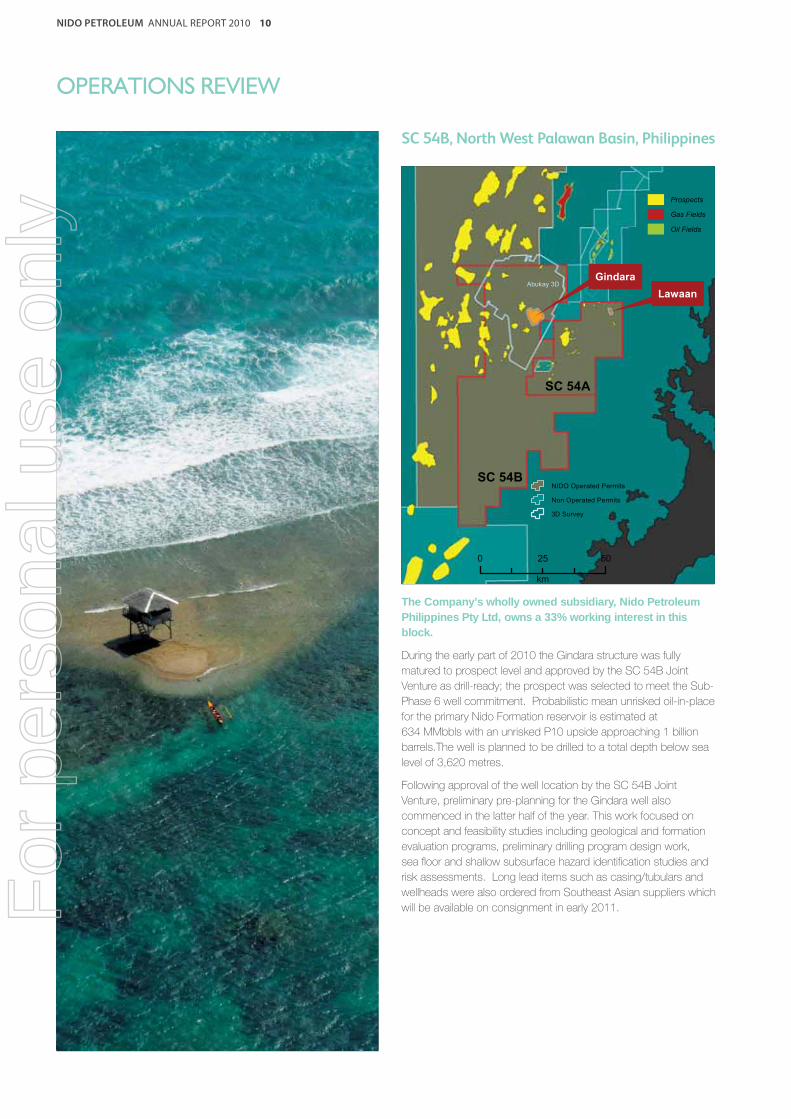

SC 54B, North West Palawan Basin, Philippines

LawaanGindara

0 5025

km

Prospects

Gas Fields

Oil Fields

NIDO Operated Permits

Non Operated Permits

3D Survey

Abukay 3D

SC 54A

SC 54B

The Company’s wholly owned subsidiary, Nido Petroleum Philippines Pty Ltd, owns a 33% working interest in this block.

During the early part of 2010 the Gindara structure was fully

matured to prospect level and approved by the SC 54B Joint

Venture as drill-ready; the prospect was selected to meet the Sub-

Phase 6 well commitment. Probabilistic mean unrisked oil-in-place

for the primary Nido Formation reservoir is estimated at

634 MMbbls with an unrisked P10 upside approaching 1 billion

barrels.The well is planned to be drilled to a total depth below sea

level of 3,620 metres.

Following approval of the well location by the SC 54B Joint

Venture, preliminary pre-planning for the Gindara well also

commenced in the latter half of the year. This work focused on

concept and feasibility studies including geological and formation

evaluation programs, preliminary drilling program design work,

sea fl oor and shallow subsurface hazard identifi cation studies and

risk assessments. Long lead items such as casing/tubulars and

wellheads were also ordered from Southeast Asian suppliers which

will be available on consignment in early 2011. For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 11

OPERATIONS REVIEW

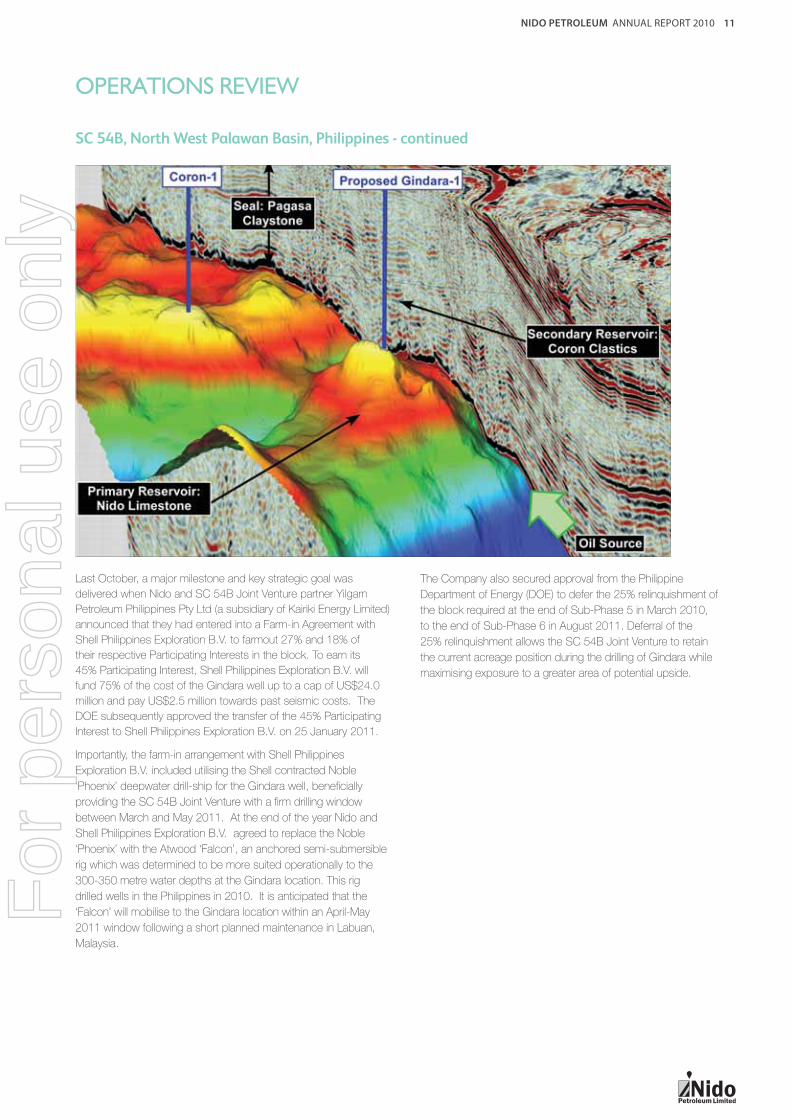

Last October, a major milestone and key strategic goal was

delivered when Nido and SC 54B Joint Venture partner Yilgarn

Petroleum Philippines Pty Ltd (a subsidiary of Kairiki Energy Limited)

announced that they had entered into a Farm-in Agreement with

Shell Philippines Exploration B.V. to farmout 27% and 18% of

their respective Participating Interests in the block. To earn its

45% Participating Interest, Shell Philippines Exploration B.V. will

fund 75% of the cost of the Gindara well up to a cap of US$24.0

million and pay US$2.5 million towards past seismic costs. The

DOE subsequently approved the transfer of the 45% Participating

Interest to Shell Philippines Exploration B.V. on 25 January 2011.

Importantly, the farm-in arrangement with Shell Philippines

Exploration B.V. included utilising the Shell contracted Noble

‘Phoenix’ deepwater drill-ship for the Gindara well, benefi cially

providing the SC 54B Joint Venture with a fi rm drilling window

between March and May 2011. At the end of the year Nido and

Shell Philippines Exploration B.V. agreed to replace the Noble

‘Phoenix’ with the Atwood ‘Falcon’, an anchored semi-submersible

rig which was determined to be more suited operationally to the

300-350 metre water depths at the Gindara location. This rig

drilled wells in the Philippines in 2010. It is anticipated that the

‘Falcon’ will mobilise to the Gindara location within an April-May

2011 window following a short planned maintenance in Labuan,

Malaysia.

The Company also secured approval from the Philippine

Department of Energy (DOE) to defer the 25% relinquishment of

the block required at the end of Sub-Phase 5 in March 2010,

to the end of Sub-Phase 6 in August 2011. Deferral of the

25% relinquishment allows the SC 54B Joint Venture to retain

the current acreage position during the drilling of Gindara while

maximising exposure to a greater area of potential upside.

SC 54B, North West Palawan Basin, Philippines - continued

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 12

OPERATIONS REVIEW

SC 58, North West Palawan Basin, Philippines

Dorado

Butanding

Balyena

0 5025

km

Prospects

Gas Fields

Oil Fields

Non Operated Permits

NIDO Operated Permits

SC 58

SC 63

SC 54A

SC 54B

Abukay 3D

The Company’s wholly owned subsidiary, Nido Petroleum Philippines Pty Ltd, holds a 50% working interest in the SC 58 block. The working interest is dependent upon the completion of the Company’s obligations (which includes payment of 100% of the costs of drilling an exploration well in Sub-Phase 3) under its Farm-in Agreement with PNOC Exploration Corporation dated 17 July 2006.

Exploration activity in SC 58 during 2010 focused on the multi-

beam and deepwater sea-bed coring program implemented

between March and April 2010. One of a number of key

subsurface uncertainties or risks in deepwater SC 58 is the direct

evidence of the presence of an active charge system. 2D and

3D seismic mapping had confi rmed the presence of a number of

NE-SW trending graben systems interpreted to contain potential

source rocks similar to those recognised as being present and

thermally mature in the Malampaya graben immediately to the east

of SC 58.

However, as no wells have been drilled in SC 58 there is no

calibration point to de-risk this key petroleum system element.

By geochemically analysing carefully located sea-bed cores it

is possible to detect seepage of hydrocarbons at the sea fl oor.

These can provide direct evidence that a working source and

charge system is present in the subsurface. Furthermore the

seeped oils can be compared to oils collected from fi elds providing

a geochemical ‘fi nger-print’ that similar hydrocarbons are being

generated in the area.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 13

OPERATIONS REVIEW

SC 58, North West Palawan Basin, Philippines - continued

The multi-beam survey acquired by Fugro Survey Pte Ltd

commenced in March 2010 and acquired approximately 1,500 sq.

km. of data producing a highly detailed topographic map of the sea

fl oor over the central sector of the block which contains a number

of large prospects including Balyena, Balyena East, Butanding and

Dorado. The map was integrated with seismic data and areas of

potential sea fl oor seepage identifi ed.

A total of 180 drop cores were collected from the high-graded areas

and analysed geochemically using Gas Chromatography and Gas

Chromatography Mass Spectrometry.

The results were very encouraging:

• The majority of core data indicates widespread micro-

seepage of liquid hydrocarbons across SC 58 based on Gas

Chromatography (GC) results.

• Gas Chromatography – Mass Spectrometry (GC-MS) analysis of

14 selected core samples for biomarker ‘fi ngerprinting’ confi rmed

the liquid hydrocarbons show similar thermal maturities and

biomarker affi nities with known NW Palawan source rocks and

oils recovered from fi elds in the inboard parts of the NW Palawan

basin (Malampaya/Galoc/Nido/Tindalo fi elds).

• The central area of the sea-bed coring survey showed the

strongest evidence for light hydrocarbon micro-seepage

corresponding with the location of the large Butanding, Balyena,

Balyena East and Dorado Prospects.

The Company believes that the results of the sea-bed coring

program have signifi cantly reduced the charge risk in deepwater

SC 58 and upgraded the prospectivity of the Prospects and Leads

portfolio identifi ed from the existing 2D and 3D seismic data.

In tandem with the sea-bed coring work, the Company also

reprocessed a portion of the Talusi 2D seismic survey in order to

aid core locations by providing better imaging of the deep graben

systems. This work commenced in March and was completed

in September 2010 and has been integrated into the subsurface

providing important data on thermal modelling of the deepwater

grabens, in particular the timing of hydrocarbon generation into the

main prospects.

During the latter half of the year, exploration activity focused on

the detailed integration of the sea-bed coring results into the re-

assessment of the Prospects and Leads portfolio and remaining

subsurface risks. This work was ongoing at the end of the year with

subsurface studies starting to focus on the need to further de-risk

reservoir uncertainty using seismic inversion and amplitude versus

offset (AVO) seismic analyses.

The fi ve well exploration program includes the drilling of an SC 58

deepwater well for which the Company has secured long lead

drilling items (casing/tubulars). It is anticipated that the fi rst drilling

candidate will be Balyena with the other large deepwater prospects

- Butanding and Dorado to follow. The fi nal drilling decision will be

made following completion of the remaining de-risking work planned

for 2011.

Subsequent to the end of the 2010 Financial Year, the Company,

with the agreement of the DOE, deferred the SC 58 Sub-Phase 3

well commitment by 12 months from January 2012 to January 2013

so as to enable the Company to complete the remaining

de-risking work. The Company has also sought to defer the election

to drill under the Farm-in Agreement with PNOC-EC (the election is

currently required to be made prior to the end of April 2011) by a

period of 12 months. Discussions with PNOC-EC concerning this

request were ongoing as at the date of this Annual Financial Report.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 14

OPERATIONS REVIEW

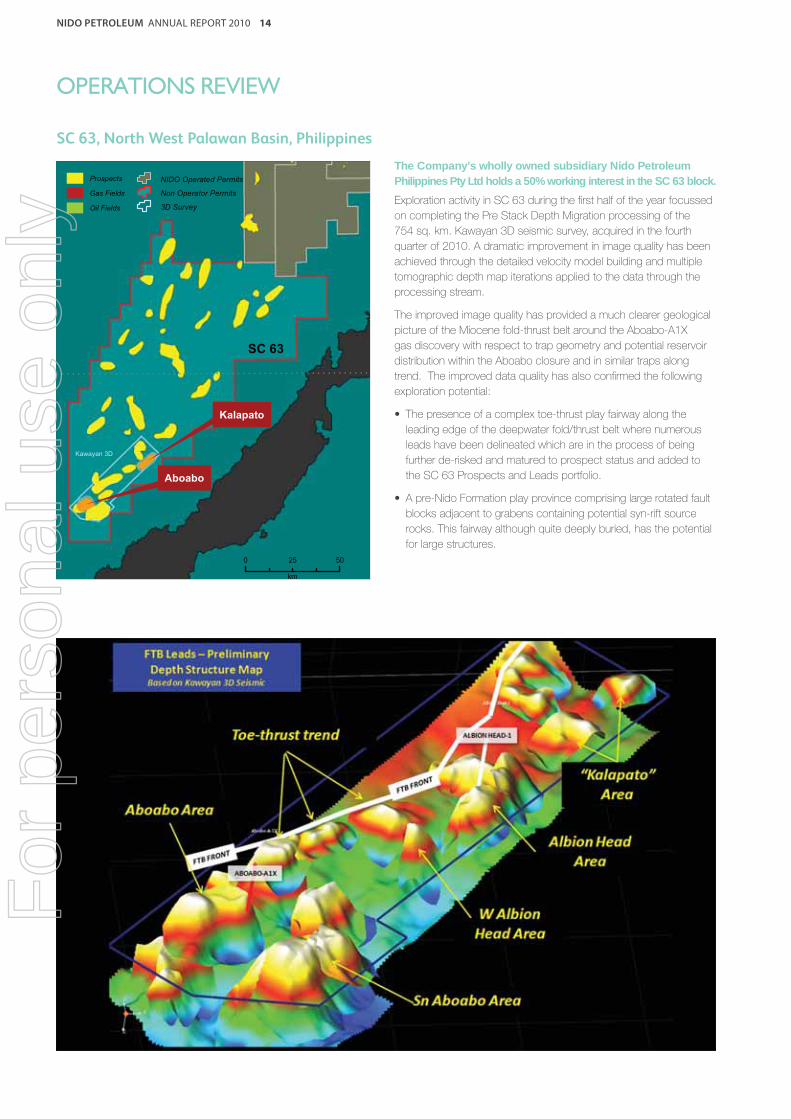

SC 63, North West Palawan Basin, Philippines

Kalapato

Aboabo

0 5025

km

Prospects

Gas Fields

Oil Fields

NIDO Operated Permits

Non Operator Permits

3D Survey

SC 63

Kawayan 3D

The Company’s wholly owned subsidiary Nido Petroleum Philippines Pty Ltd holds a 50% working interest in the SC 63 block.

Exploration activity in SC 63 during the fi rst half of the year focussed

on completing the Pre Stack Depth Migration processing of the

754 sq. km. Kawayan 3D seismic survey, acquired in the fourth

quarter of 2010. A dramatic improvement in image quality has been

achieved through the detailed velocity model building and multiple

tomographic depth map iterations applied to the data through the

processing stream.

The improved image quality has provided a much clearer geological

picture of the Miocene fold-thrust belt around the Aboabo-A1X

gas discovery with respect to trap geometry and potential reservoir

distribution within the Aboabo closure and in similar traps along

trend. The improved data quality has also confi rmed the following

exploration potential:

• The presence of a complex toe-thrust play fairway along the

leading edge of the deepwater fold/thrust belt where numerous

leads have been delineated which are in the process of being

further de-risked and matured to prospect status and added to

the SC 63 Prospects and Leads portfolio.

• A pre-Nido Formation play province comprising large rotated fault

blocks adjacent to grabens containing potential syn-rift source

rocks. This fairway although quite deeply buried, has the potential

for large structures.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 15

OPERATIONS REVIEW

SC 63, North West Palawan Basin, Philippines - continued

During the second half of the year, the SC 63 Joint Venture secured

the services of UK based structural geology specialists to assist with

the preliminary structural framework interpretation using 3D structural

balancing software. The result of this work which was completed

in November has assisted in de-risking the play and trap geometry

uncertainty for many of the leads identifi ed from the 3D seismic

interpretation, especially around the Aboabo A-1X well and the toe-

thrust play fairway.

Detailed seismic interpretation was continuing at the end of the

year with a target of delivering a fully risk/ranked Prospect and Lead

inventory in the third quarter of 2011. Once this work has been

completed the SC 63 Joint Venture will select the drilling candidate

or candidates to meet the Sub-Phase 2b well commitment, which

is required to be drilled before November 2012. Current favoured

drilling candidates are an Aboabo-2 well (re-test of the Aboabo A1-X

gas discovery, Phillips 1981) and the large Kalapato lead which

are currently included in the Company’s fi ve well exploration drilling

program.

Philippine Basin Study

The Joint Philippine Basin Study between Nido and a SE Asian

National Oil Company (NOC) was completed in the fi rst half of 2010.

The study reviewed the petroleum potential of all onshore and

offshore basins known to exist within the Philippines providing a

technical and commercial ranking of these basins for possible future

exploration focus and a basis for high-grading blocks released by

the DOE in future acreage gazettal rounds.

The project was conducted by a joint team from both companies

located in Nido’s Manila offi ce. The joint study may precipitate Nido

and the SE Asian NOC forming a more formal relationship to bid on

blocks gazetted by the Philippine DOE in the future.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 16

OPERATIONS REVIEW

HEALTH, SAFETY, SECURITY AND ENVIRONMENT (HSSE)

In 2009, Nido implemented a comprehensive HSSE Management

System comprising 16 Standards and associated Systems in order

to provide the Company with a systematic, verifi able and continually

improving approach to HSSE across its operations and organisation.

To support the oversight of HSSE across the organisation Nido

appointed an HSSE Manager during the year and established a

monthly HSSE meeting to monitor HSSE performance against

Company key performance indicators and address HSSE issues

and incidents which arise during activities.

HSSE performance over 2010 was excellent considering Nido

became an offshore operator for the fi rst time at the Tindalo fi eld.

The Company accumulated 977,788 man-hours during the year

with zero fatalities, zero Lost Time Injuries and a Total Recordable

Injury Frequency Rate of 2.05 which compares well with the

Australian National Offshore Petroleum Safety Authority (NOPSA)

current industry rate of 7.87 as at 30 June 2010.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 17

PETROLEUM PERMIT INTEREST SCHEDULE

Philippines Nido Approx Net

Interest Area

Permit Basin (%) (sq. km.) Operator

SC 14 Block A North West Palawan 22.49 5 Philodrill (1)

SC 14 Block B North West Palawan 28.28 44 Philodrill (1)

SC 14 Block C-1 (2) North West Palawan 22.88 40 GPC (3)

SC 14 Block C-2 (4) North West Palawan 22.28 37 Philodrill (1)

SC 14 Block D North West Palawan 31.42 55 Philodrill (1)

SC 6B North West Palawan 7.81 43 Philodrill (1)

SC 54A North West Palawan 42.40(5) 441 Nido

SC 54B North West Palawan 60.00(6) 1,897 Nido

SC 58 North West Palawan 50.00(7) 6,743 Nido (8)

SC 63 North West Palawan 50.00 5,336 PNOC (9)

Total 14,641

Data as at 31 December 2010:

(1) The Philodrill Corporation

(2) Galoc Block

(3) Galoc Production Company WLL

(4) West Linapacan Block

(5) In March 2010 Nido Petroleum Philippines Pty Ltd farmed down a 7.6% working interest in SC 54A to TG World (BVI) Corporation,

a subsidiary of TG World Energy Corporation

(6) Nido’s interest reduced to 33% on 25 January 2011. Refer to Note 32(1) in the Notes to Financial Statements

(7) Subject to Nido completing its obligations under its Farm-in Agreement with PNOC Exploration Corporation

(8) SC 58 operatorship reverts to PNOC Exploration Corporation upon completion of Nido’s farm-in obligations

(9) PNOC Exploration Corporation

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 18

DIRECTORS’ REPORT

The Directors of Nido Petroleum Limited are pleased to present the Annual Financial Report for the year ended 31 December 2010.

Directors

The names and details of the Company’s Directors in office during the financial year and until the date of this Report are as follows. Directors were in office for the entire period unless otherwise stated.

William Bloking FAICD

B.E Science (University of South Carolina)

(Summa cum Laude)

Chairman (Appointed 15 May 2009,

previously Non-Executive Director Appointed

6 February 2008)

Member and Chair, Remuneration and

Nomination Committee (Appointed

8 September 2008)

Member, Audit & Risk Management

Committee (Appointed 6 September 2010)

Bill has over 35 years’ experience in the energy

sector with ExxonMobil and the BHP Billiton

Group, holding senior executive positions

in Australia, Asia, South America and the

United States. Until his retirement in January

2007, Bill was President of Australia/Asia

Gas at BHP Billiton Petroleum, where he had

overall strategic, commercial and corporate

accountability for BHP Billiton’s international

LNG business and its domestic gas business

in Australia. Prior to joining BHP, he had spent

24 years with ExxonMobil holding a variety

of senior executive positions including Chief

Operating Offi cer of Esso Eastern Products

Trading Company, Supply Operations Manager

for the Far East and Western Hemisphere and

General Manager of Natural Gas in Indonesia.

Bill is currently Executive Chairman and

President of KAL Energy, Inc. (Appointed

26 June 2007), Chairman of Transerv Energy

Limited (Appointed 15 March 2011) and

he is a Non-Executive Director of the John

Holland Group (Appointed 1 January 2007),

Miclyn Express Offshore Limited (Appointed

19 February 2010), the Lions Eye Institute

(Appointed 1 October 2003), and the West

Australian Symphony Orchestra (Appointed

19 August 2005). He is also a Fellow of the

Australian Institute of Company Directors,

a Governor of the American Chamber of

Commerce in Australia and an Adjunct

Professor at Murdoch University.

Bill was formerly Chairman of Cool Energy Ltd

(Appointed 10 January 2007, Resigned

6 March 2009), the National Offshore

Petroleum Safety Authority (Appointed

1 March 2008, Resigned 25 August 2009),

Norwest Energy NL (Appointed 12 February

2007, Resigned 30 June 2009), and Cullen

Wines (Australia) Pty Ltd (Appointed

27 May 2006, retired 21 November 2009).

J.V. Emmanuel (Jocot) Araullo de Dios

MAICD

B.Sc in BA (Uni. of the Philippines), LL.B

(Ateneo de Manila University), LL.M (Harvard

Law School)

President and Chief Executive Offi cer

(Appointed 6 February 2008)

Jocot has over 15 years of experience

in commercial and fi nancial transactions,

including within the international energy sector.

Jocot was Managing Director at Merritt

Advisory Partners Inc., an energy advisory fi rm

focusing on energy projects and transactions

within Asia. Jocot also served as Chairman of

the Board of publicly listed PNOC Exploration

Corporation (the oil and gas arm of the

Philippine National Oil Company, Appointed

3 November 2004, Resigned 30 August 2005)

and held the position of Undersecretary of the

Philippine Department of Energy for three years

where he led the preparation of the Philippine

Energy Plan, supervised the country’s

downstream oil sector and participated in the

restructuring of the Philippine power sector.

He continues to hold the position of President

of Nido Petroleum Philippines Pty Ltd of which

he was Appointed in 2008.

Jocot has represented the Philippines in

various international organisations including the

APEC Energy Working Group. In 2005, Jocot

received the prestigious Secretary’s Award

of Recognition for Distinguished Government

Service. Jocot is currently a Non-Executive

Director of the Boards of Phoenix Petroleum

Philippines Inc., a publicly-listed downstream

oil company in the Philippines (Appointed

1 April 2007), and Davies Energy Services,

Inc., an energy services company (Appointed

10 March 2006). Jocot is a member of the

Australian Institute of Company Directors.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 19

DIRECTORS’ REPORT

David Whitby MAICD

B.E. Mechanical (Royal Military College,

Canada)

Non-Executive Director (Appointed

15 May 2009)

Chairman, Non-Independent (Appointed

6 February 2008 – Resigned 15 May 2009)

Managing Director (Appointed 21 July 2004

- Resigned 6 February 2008)

Member, Remuneration and Nomination

Committee (Appointed 21 January 2010)

David’s prior work experience includes

appointments as Project Director of the

West Java Gas Project with Conoco-Phillips

in Jakarta, Vice President of Corporate

Development for Gulf Indonesia, Jakarta,

President of Gulf (Australia) Resources Ltd in

Perth and Vice President of Heavy Oil for Husky

Oil in Canada. Prior to entering the oil industry,

David was an offi cer in the Canadian Armed

Forces military engineering branch.

David is the Non-Executive Chairman of Xstate

Resources Limited (Appointed 13 February 2011).

David was formerly a Director of Cool Energy

Pty Ltd (Appointed 11 June 2007, Resigned

9 February 2009). He is a member of the

Australian Institute of Company Directors.

Vincent S Pérez

B.Bus. Econs (Uni. of the Philippines),

MBA (Wharton School, Uni. of Pennsylvania)

Non-Executive Director, Independent

(Appointed 5 April 2006)

Member Audit and Risk Management

Committee (Appointed 2 November 2006 –

Resigned 6 September 2010)

Member Remuneration and Nomination

Committee (Appointed 8 September 2008 –

Resigned 21 January 2010)

Vince has over 17 years of experience in debt

restructuring, capital markets and private equity

in emerging markets, including appointments in

Pittsburgh, London, New York and Singapore

with Mellon Bank and Lazard Frères. In early

2001, he served as Philippine Undersecretary

for Industry at the Department of Trade

and Industry and Managing Head of this

Department’s Board of Investments. He then

served as Philippine Energy Secretary from

June 2001 to March 2005.

Vince has held Board positions on several

listed companies including the Philippine

National Bank (Appointed 24 May 2005,

Resigned 30 May 2006), PNOC Energy

Development Corporation (Appointed

14 June 2007, Resigned 31 July 2010),

Del Monte Pacifi c Limited (Appointed

2 August 1999, Resigned 21 March 2001),

and SM Investments Corporation (Appointed

15 July 2005). Vince is currently Chairman of

WWF Philippines and a member of the Board

of Trustees of WWF International and the

Board of Advisors of the Center for Business

and the Environment at Yale University, Coca

Cola Philippines, and Pictet Clean Energy

Fund. He is the Chairman of Merritt Partners

Pte Ltd and Merritt Advisory Partners Inc.,

and is Chief Executive Offi cer of Alternergy

Philippine Holdings Corporation and Alternergy

Philippines Investments Corporation.

Eduardo V. Mañalac AAICD

B.S. Geology, Post Graduate Petroleum Geology (Uni. of the Philippines) Non-Executive Director, Independent (Appointed 20 February 2009) Member, Audit and Risk Management Committee (Appointed 20 February 2009) Member, Remuneration and Nomination Committee (Appointed 20 February 2009)

Ed has had a 35-year career in international petroleum exploration and production management, acreage acquisition, production sharing contracts and Joint Venture negotiations. During his early career he joined a national oil company and started the fi rst geological mapping of the Palawan Basin in the Philippines.

For 28 of those 35 years he enjoyed a career with Phillips Petroleum (now Conoco Phillips) in many parts of the world, most recently in China, and encouraged Phillips’ initial entry into the Palawan Basin and similar areas in Indonesia. From 2003 to 2004, Ed was Undersecretary of the Department of Energy in the Philippines, where he introduced the fi rst public bidding round for exploration acreage targeting the Palawan Basin. From 2004 to 2006 he was President and CEO of the Philippine National Oil Company (Appointed 20 August 2004, Resigned 31 October 2006) and its subsidiary PNOC Exploration Corporation (Appointed 24 September 2004, Resigned 31 October 2006), and was Chairman of PNOC Energy Development Corporation (Appointed 13 September 2004, Resigned 31 October 2006). Ed was a Non-Executive Director of Wellex Industries (Appointed 7 January 2008, Resigned 1 April 2010) a publicly listed energy, mining and exploration company in the Philippines of which he was Chairman up to January 2009.

He brings to the Board a wealth of understanding in exploration and operations and a deep knowledge of the Palawan Basin and markets and acreage in the region.

He is the President of TransEnergy International Limited (Appointed 28 November 2006), an energy resources consultancy company in the Philippines, where he has been the principal consultant since December 2006. More recently, in November 2009, Eduardo was Appointed Non-Executive Director of Basic Energy Corporation (Appointed 1 October 2009), another listed energy company in the Philippines. He is a member of the Australian Institute of Company Directors.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 20

DIRECTORS’ REPORT

Andrew Edwards GAICD

B.Com (University of Western Australia) Non-Executive Director, Independent (Appointed 11 December 2009) Member and Chair, Audit and Risk Management Committee (Appointed 11 December 2009)

Andrew is a former managing partner of PriceWaterhouseCoopers, Perth Offi ce (PWC), past National Vice President of the (then) Securities Institute of Australia (now the Financial Services Institute of Australasia) and past President of the Western Australian division of that Institute, past State Chairman of the Institute of Chartered Accountants local Education Committee and a past member of its National Education Committee.

Andrew is a current Board member of Mermaid Marine Australia Limited (Appointed 18 December 2009), Mermaid Marine Vessel Operations Pty Ltd (Appointed 1 February 2010), Mermaid Marine Supply Base Pty Ltd (Appointed 1 February 2010), Mermaid Marine Charters Pty Ltd (Appointed 1 February 2010), Sungrid Limited (Appointed 30 April 2010), MACA Limited (Appointed

1 October 2010), and Activ Foundation Inc (Appointed 27 October 2008). He is a member of the Australian Institute of Company Directors.

Alternate Director

Joanne Williams

B.E. (Chem) (University of Adelaide) (Appointed 6 February 2008. Resigned 6 April 2010.)

Joanne, who is also the Company’s Deputy Managing Director, was appointed an Alternate Director for both Mr David Whitby and Mr Vince Pérez on 6 February 2008 and Resigned on 6 April 2010.

Joanne has 15 years of experience in the upstream oil and gas industry where she has held positions in the areas of offshore production operations and management, reservoir engineering, hands-on FPSO operations, fi eld appraisal and development planning, project management, mergers and acquisitions, corporate and business development.

Joanne has extensive expertise in identifying and realising marginal fi eld opportunities as well as optimisation and extension of late life fi eld production. Joanne’s experience includes positions with upstream and gas operating companies including Woodside Petroleum, Newfi eld Exploration, Crusader Resources, Clyde Resources and Gulf Australia. Joanne was a winner of the 2007 40 Under 40 Award and fi nalist in the Telstra Business Women of the Year awards in 2007.

Ms Williams has not attended any meetings in her capacity as Alternate Director for either Mr Whitby or Mr Pérez for the period ending 31 December 2010.

Company Secretary

John Newman MAICD

BEc,LLB (Monash University)

(Appointed 4 November 2009)

John is a lawyer with over 15 years of

experience, nine of which have been in the

energy and resources sector. John manages

the Company group’s legal, compliance and

company secretarial affairs. John’s previous

experience includes positions with the Timor

Sea Designated Authority, Cridlands Lawyers

and the Northern Land Council. Prior to

working in a resources context John was

the principal solicitor with the Refugee and

Immigration Legal Centre in Melbourne.

John is currently a member of the Law Society

of Western Australia, Australian Institute of

Company Directors (AICD), the Resources

and Energy Law Association (AMPLA),

the Association of International Petroleum

Negotiators (AIPN) and an affi liate of Chartered

Secretaries Australia (CSA).

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 21

DIRECTORS’ REPORT

Directors’ and Committee Meetings

The following Table details the number of Directors’ and Committee

meetings held during the fi nancial year and the number of meetings

attended by each Director.

Board of Directors Meetings 2010

Directors Held(1) Attended

W Bloking 6 6

J de Dios 6 6

D Whitby 6 6

V Pérez 6 6

E Mañalac 6 6

A Edwards 6 6

J Williams (as Alternate) 0(2) 0

Audit & Risk Management Committee Meetings 2010

Directors Held(1) Attended

V Pérez 2(3) 2

W Bloking 1(3) 1

E Mañalac 3 3

A Edwards 3 3

Remuneration & Nomination Committee Meetings 2010

Directors Held(1) Attended

W Bloking 2 2

E Mañalac 2 2

D Whitby 2 2

(1) Number of meetings held during term of offi ce.

(2) Joanne Williams Resigned as Alternate Director of D Whitby and V Pérez as at 6 April 2010.

(3) V Pérez Resigned as a member of the Audit & Risk Management Committee and was

replaced by W Bloking on 6 September 2010.

Directors’ Interests in Securities of the Company

As at the date of this Report, the interests of the Directors in the shares, options and Performance Rights of Nido Petroleum Limited were:

Options Over Ordinary Shares

Director OrdinaryShares

Expiry Date: 12 May 2011

Exercisable at 35 cents

Expiry Date: 12 May 2011

Exercisable at 40 cents

Expiry Date: 12 May 2011

Exercisable at 45 cents

Expiry Date: 12 May 2011

Exercisable at 50 cents

Performance Rights

W Bloking 1,320,000 3,000,000 2,000,000 - - -

J de Dios 1,120,000 - 3,000,000 2,000,000 2,000,000 1,047,535

D Whitby 11,893,524 - - - - -

V Pérez 1,000,000 - - - - -

A Edwards 470,000 - - - - -

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 22

DIRECTORS’ REPORT

Principal Activities

The principal activities of the consolidated entity during the fi nancial

year, which occurred primarily in the Philippines, included:

• Exploration for oil and gas;

• Development of its oil and gas assets; and

• Production and sale of oil.

There were no signifi cant changes in the nature of the principal

activities during the year.

Operating and Financial Review

A full review of operations of the consolidated entity during the

year ended 31 December 2010 is included in the section entitled

“Operations Review” preceding this Directors’ Report.

Summary of Financial Performance

A summary of key fi nancial indicators for the Company, with prior

year comparison, is set out in the following table:

Consolidated Consolidated

2010 2009

$’000 $’000

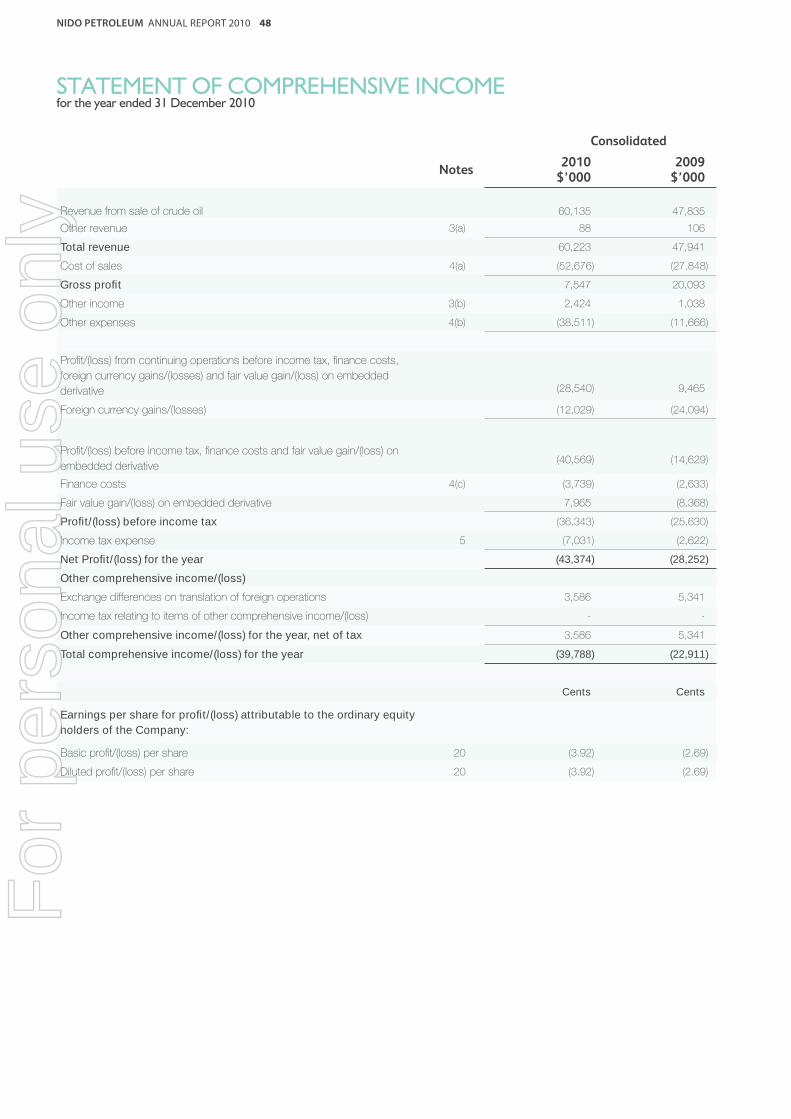

Revenue from sale of crude oil 60,135 47,835

Gross profi t 7,547 20,093

Net loss before tax and fi nance costs

(40,569) (14,629)

Net loss for the year after tax (43,374) (28,252)

Basic loss per share (cents) from continuing operations

(3.92) (2.69)

Net cash from operating activities

3,195 9,599

Net cash from/(used in) investing activities

(16,814) 282

Net cash from/(used in) fi nancing activities

21,655 (3,030)

The profi t/(loss) from continuing operations before income tax,

fi nance costs, foreign currency gains/(losses) and fair value gain/

(loss) on embedded derivative of the Group for the year ended

31 December 2010 was a loss of $28,540,000 (2009: profi t of

$9,465,000).

The net loss of the Group for the year ended 31 December 2010

of $43.4 million (2009: loss $28.3 million), was impacted by the

following signifi cant items:

• Oil revenue totalled $60.1 million, of which revenue from the

Galoc oil fi eld for the year was $51.1 million (2009:

$46.6 million), revenue from the Tindalo oil fi eld for the year was

$6.8 million, and revenue from the Nido and Matinloc oil fi elds

for the year was $2.2 million (2009: $1.2 million).

• Cost of sales for the year increased by $24.9 million to

$52.7 million (2009: $27.8 million). This increase is due primarily

to costs relating to the Extended Well Test at the Tindalo oil fi eld

during 2010.

• Other income of $2.4 million (2009: $ 1.0 million) relates

primarily to a net gain on the farmout of SC 54A working interest

($1.9 million) and insurance proceeds relating to Galoc oil fi eld

activities ($0.5 million).

• Total fi nance costs for the year of $3.7 million (2009:

$2.6 million) relate predominantly to the Merrill Lynch Convertible

Note interest.

• Fair value gain of $8.0 million (2009: loss of $8.4 million) on

embedded derivative relates to the non-cash fair value gain

movement in relation to the Convertible Note call option.

• An increase in other expenses in 2010 to $38.5 million (2009:

$11.7 million), is due primarily to the impairment of the Tindalo oil

fi eld in Service Contract 54A in the amount of $29.7 million as a

result of abandoning the fi eld in December 2010 offset by:

° A decrease in employee benefi ts expense (net of share based

payments expense) of $0.4 million to $5.5 million (2009:

$5.9 million);

° A decrease in share based payments to $0.1 million (2009:

$1.0 million); and

° A 31% reduction in offi ce and other expenses in 2010 to

$2.3 million (2009: $3.3 million) which was due to the

Company’s ongoing focus on lowering administrative costs.

• Net foreign currency loss of $12.0 million (2009: loss of

$24.1 million) was due to the strengthening of the Australian

dollar which had a negative impact on net US dollar balances

predominately from AUD denominated parent company loans

to subsidiaries (with USD functional currencies), offset by the

impact of the USD Convertible Note debt in the parent company

(with AUD functional currency).

Financing Activities

The Company’s fi nancing costs primarily represent costs of the

Convertible Note which appear in the Income Statement and in the

Notes to the Financial Statements. For the year ended

31 December 2010, fi nance costs relating to the Convertible

Note totaled $3.7 million (2009: $2.6 million). The fair value gain

in relation to the Convertible Note call option embedded derivative

totalled a non-cash fair value movement of $8.0 million (2009: loss

of $8.4 million).

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 23

DIRECTORS’ REPORT

Operating and Financial Review - continued

The fair value of the call option represents the value of the option

to the holder to convert the Convertible Note into fully paid shares

in the Company. The fair value has been determined using a

Black Scholes model, taking into account factors such as share

price volatility, expected life, exercise price and current share

price. As the Company’s share price changes, the value of the

call option will change, resulting in a change to the liability reported

in the Balance Sheet and an income or expense in the Income

Statement. As at 31 December 2010, the value of the call option

was $1.8 million (2009: $9.8 million) which has reduced primarily

due to a reduction in remaining Notes that are, as at 31 December

2010, convertible into a maximum of 57,571,544 shares (2009:

114,307,091). Refer to Note 17.

The underlying debt repayable to Merrill Lynch of US$9.2 million

plus interest will not change, assuming that the Convertible

Notes are not redeemed or converted, subject to the Terms and

Conditions detailed in the Notes to the Financial Statements.

Summary of Financial Position

The Company’s cash reserves at the end of 2010 totalled $24.2

million compared to $17.1 million on 31 December 2009. The

increase in cash was due primarily to net proceeds from oil

production of $22.7 million; proceeds (after selling costs) received

from farming out 7.6% out of Nido’s interest in SC 54A of $5.6

million; and proceeds of $28.0 million (net of capital raising costs)

resulting from the issuance of capital, offset by $16.5 million in

development expenditure and security bonds relating primarily

to Tindalo oil fi eld capital expenditure; repayment of principal

and interest relating to the Convertible Note of $9.0 million (not

including the impact of conversions); exploration expenditure of

$5.7 million predominantly relating to the SC 58 sea-bed coring

program and the SC 63 Kawayan 3D seismic acquisition; income

tax paid in the amount of $7.1 million; and overheads and other

expenditures of $10.3 million.

Production Activities

In 2010, Nido achieved the following key production milestones:

• 2.6 MMstb (gross) were produced from the Galoc fi eld.

• Production uptime at Galoc averaged 84% during the year.

• 0.3 MMstb were produced during the Tindalo oil fi eld Extended

Well Test.

• Revenue from crude oil sales increased by 25.7% to $60.1 million.

Exploration & Evaluation Activities

In 2010, Nido undertook the following key exploration activities:

• The Company’s Board of Directors announced a fi ve well

exploration program at the 21 May 2010 AGM.

• In October 2010, Shell Philippines Exploration B.V. farmed-in

to SC 54B to earn a 45% Participating Interest in the block by

providing a signifi cant carry of costs for the drilling of the Gindara

exploration well in 2011.

• The deepwater multi-beam and sea-bed coring program was

completed in SC 58 between March and April 2010. Results

indicate widespread micro-seepage of mature hydrocarbons

across the most prospective part of the block and adjacent to

key prospects.

• Reprocessing of the Talusi 2D seismic in SC 58 was also

completed during the year which improved subsurface imaging

of the source grabens in the deepwater.

• In SC 63, Pre Stack Depth Migration processing of the Kawayan

3D seismic was completed in July 2010.

• The SC 54 Sub-Phase 5 (25%) relinquishment due in August

2010 was successfully deferred to the end of Sub-Phase 6 in

August 2011.

Development Activities

In 2010, Nido undertook the following key development activities:

• In March 2010 Nido farmed out 7.6% of its interest in SC 54A to

TG World (BVI) Corporation, ahead of the commencement of the

Tindalo oil fi eld Extended Well Test.

• First oil achieved on 30 May 2010 at the Tindalo oil fi eld, some

fi ve months after achieving Final Investment Decision.

• Extended Well Test commenced on 6 June 2010 at Tindalo.

• The Extended Well Test failed to produce oil at economic

rates due to excessive water production and the SC 54A Joint

Venture decided to abandon the well in December 2010 with

completion of abandonment occurring in the fi rst quarter of

2011.

Corporate Activities

SC 54B – Shell Philippines Exploration B.V. Farm-in During the year Nido announced it had farmed out 27% of its

Participating Interest in SC 54B to Shell Philippines Exploration

B.V.. The farmout was coordinated jointly with SC 54B partner

Yilgarn Petroleum Philippines Pty Ltd which also contributed 18%

of its Participating Interest to Shell Philippines Exploration B.V..

To earn its 45% Participating Interest, Shell Philippines Exploration

B.V. will carry 75% of the Gindara well cost up to a cap of

US$24.0 million and has agreed to pay US$2.5 million of past

seismic costs. Following approval by the Philippine DOE of

the Shell Philippines Exploration B.V. farm-in in January 2011,

Participating Interests in the block are:

• Nido Petroleum Philippines Ltd 33%

• Yilgarn Petroleum Philippines Pty Ltd 22%

• Shell Philippines Exploration B.V. 45%.

Nido will remain operator of the block through to the completion of

drilling activities on the Gindara well after which Shell Philippines

Exploration B.V. has the option to assume operatorship from Nido.

Successful Completion of Share Placement, Raising $19.9 millionOn 28 October 2010, Nido completed a successful placement

of 159,000,000 ordinary fully paid shares to sophisticated and

professional investors at $0.125 per share to raise total proceeds

of $19.9 million (before costs).

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 24

DIRECTORS’ REPORT

Operating and Financial Review - continued

Successful Completion of Share Purchase Plan, Raising $9.3 millionOn 3 December 2010 Nido successfully completed a Share

Purchase Plan and raised gross proceeds of $9.3 million. On

8 December 2010, 74,080,000 new ordinary shares were allotted

at an issue price of $0.125 per share.

Proceeds from the Placement and Share Purchase Plan are

intended to be used towards securing Nido’s future exploration

program and for general working capital and partial debt reduction.

Dividends

No dividends were paid or declared by the consolidated entity

during the fi nancial year.

Corporate Structure

The Company is limited by shares and is incorporated and

domiciled in Australia.

Signifi cant Changes in the State of Affairs

Signifi cant changes in the state of affairs of the Company during

the fi nancial year are detailed in the fi nancial and activities review in

this Report.

Likely Developments and Expected Results

The Company will continue to maximise revenues from its

interest in the Galoc oil fi eld and consider the merits of a Phase 2

development together with its Joint Venture Partners. In addition,

the Company will continue to assess potential opportunities

for appraisal and development within SC 54A to add a second

revenue stream, which would enable the Company to accelerate

the drilling of its expansive deepwater portfolio of assets over the

longer term through a multi-well exploration drilling program.

The Company continues to pursue strategic opportunities with

respect to its assets and is in discussions with a number of

potential partners including oil majors concerning possible farmout

transactions.

For

per

sona

l use

onl

y

NIDO PETROLEUM ANNUAL REPORT 2010 25

DIRECTORS’ REPORT

Corporate Social Responsibility

Nido is committed to enhancing shareholder value by conducting

international oil and gas exploration, development and production

in a manner that, through its Corporate Social Responsibility

Programs, shares part of the benefi ts of this activity with the

communities in which it operates.

Nido has adopted a two pronged approach to its Corporate

Social Responsibility Programs. This involves the Nido Petroleum

Foundation, Inc. (Nido Foundation) in the Philippines and the

Company’s Charitable Donations Committee, which actively

encourages and supports staff as they work in a range of

community organisations in Australia and the Philippines.

In 2010, Nido provided funds to the Social Services Programs of

the Holy Trinity Parish in Quezon City, Philippines which caters to

the needs of the urban poor and marginalised members of the

community. The program includes medical/dental outreach clinics,

livelihood opportunities, out of school youth education, skills

training program and adult literacy education classes.

Nido also supported the fund raising campaign of the Association

of Filipinos for the Advancement of Geosciences, Inc (AFAG)

where the proceeds were used to purchase equipment for a small

university geology department.

Staff Involvement

During 2010 the Company supported staff involvement with

the Breast Cancer Foundation of Western Australia, Channel 7

Telethon, Ronald MacDonald charities and the Salvation Army.

Nido also proudly supported the Mission Australia Christmas Lunch

for the third year in a row.

Further details on the Company’s Corporate Social Responsibility

activities can be accessed from the Company’s website.

For

per

sona

l use

onl

y

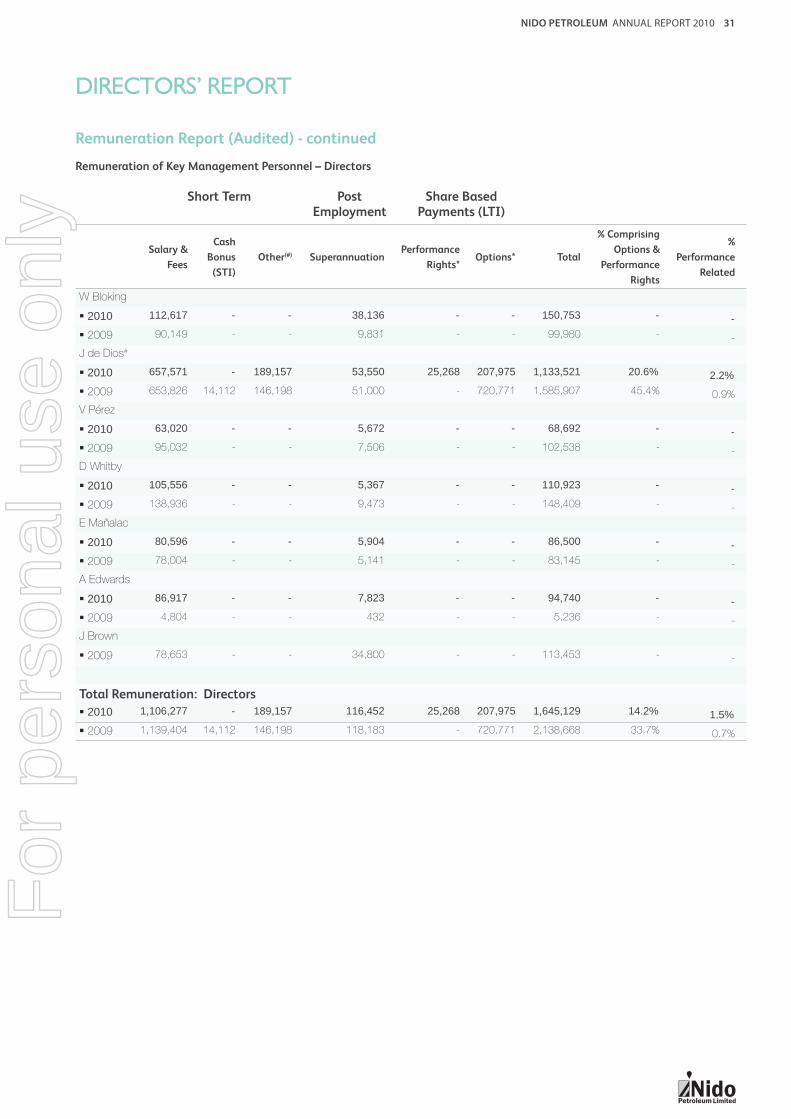

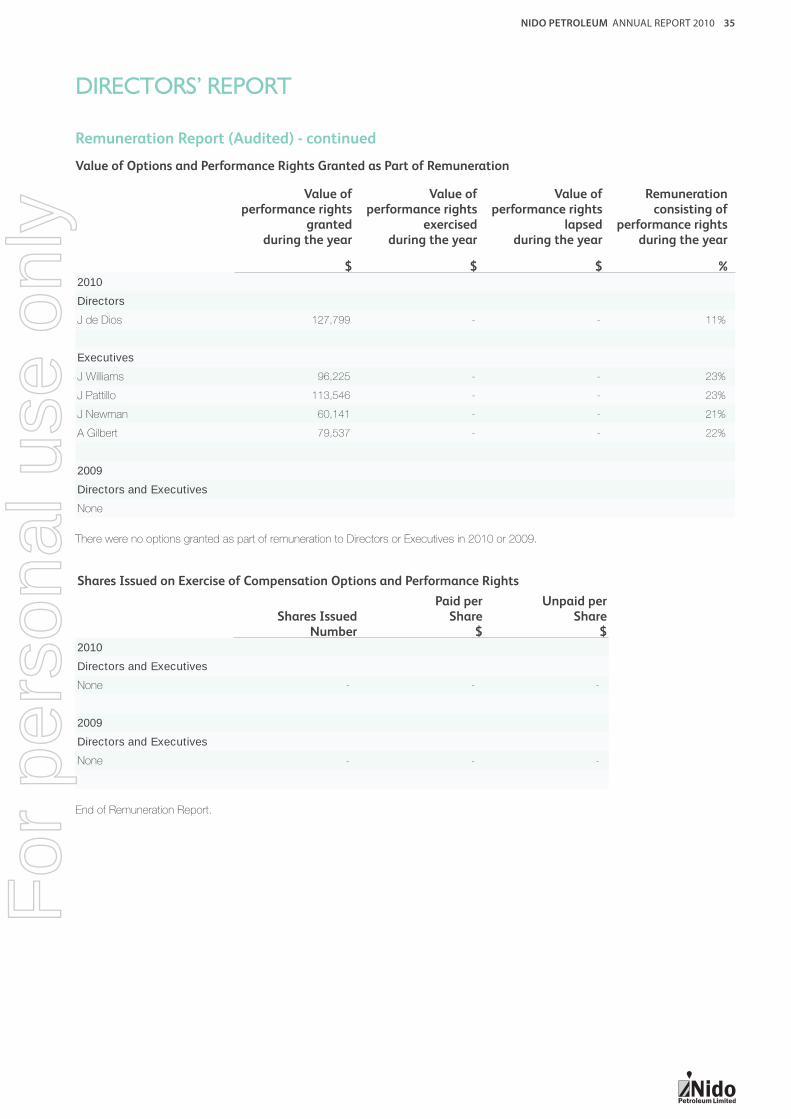

NIDO PETROLEUM ANNUAL REPORT 2010 26