Embed Size (px)

Citation preview

The New Client Acquisition Process

BUILDINGSUSTAINABLE RESULTS

1

The How-To Section

The New Client Acquisition Process

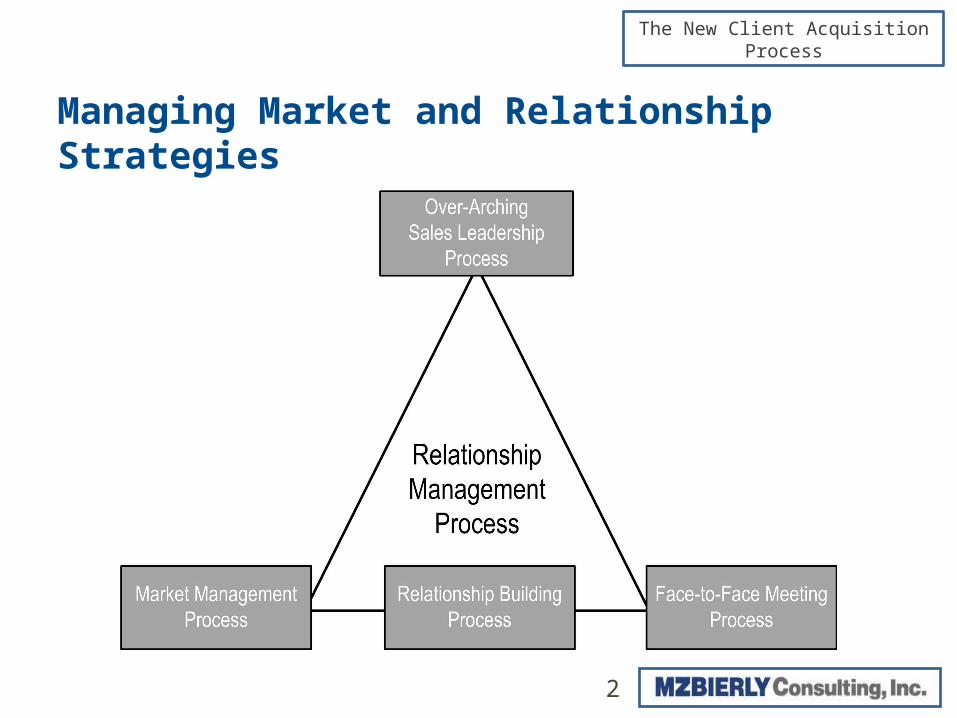

Managing Market and Relationship Strategies

2

The New Client Acquisition Process

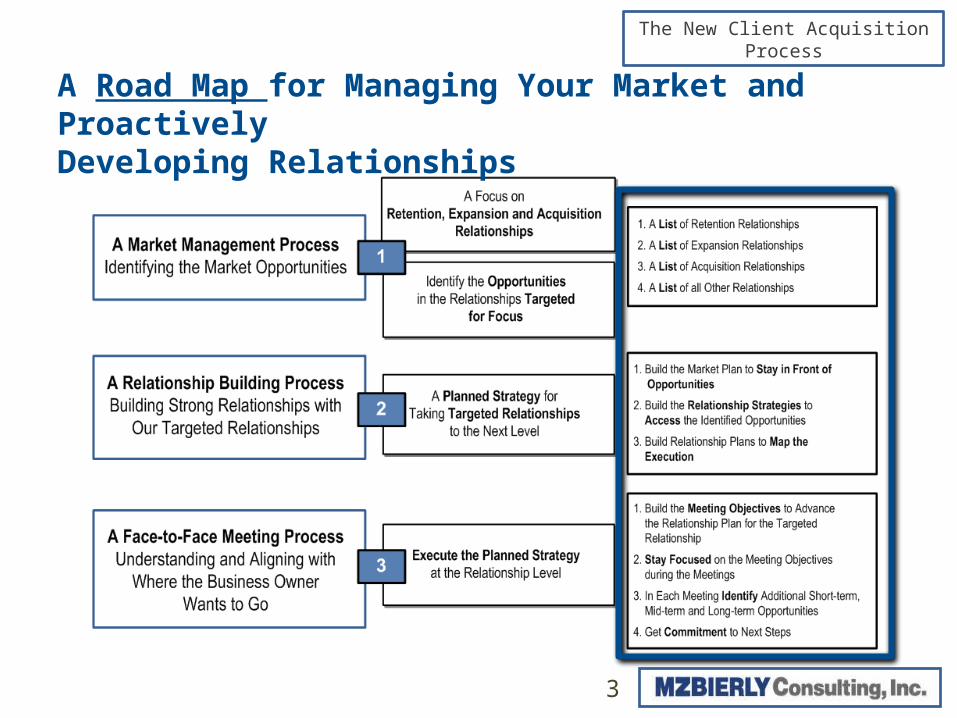

A Road Map for Managing Your Market and ProactivelyDeveloping Relationships

3

The New Client Acquisition Process

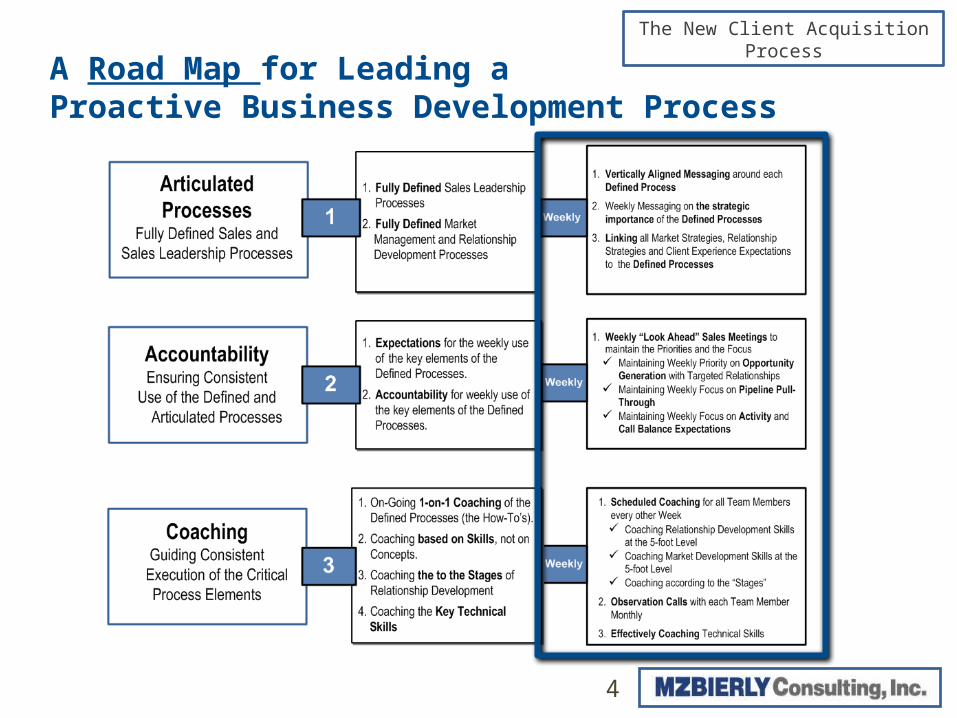

A Road Map for Leading a Proactive Business Development Process

4

The New Client Acquisition Process

DEFINE THE MARKET AND BUILD A FOCUS

The How-To Section: An Articulated Process

5

The New Client Acquisition Process

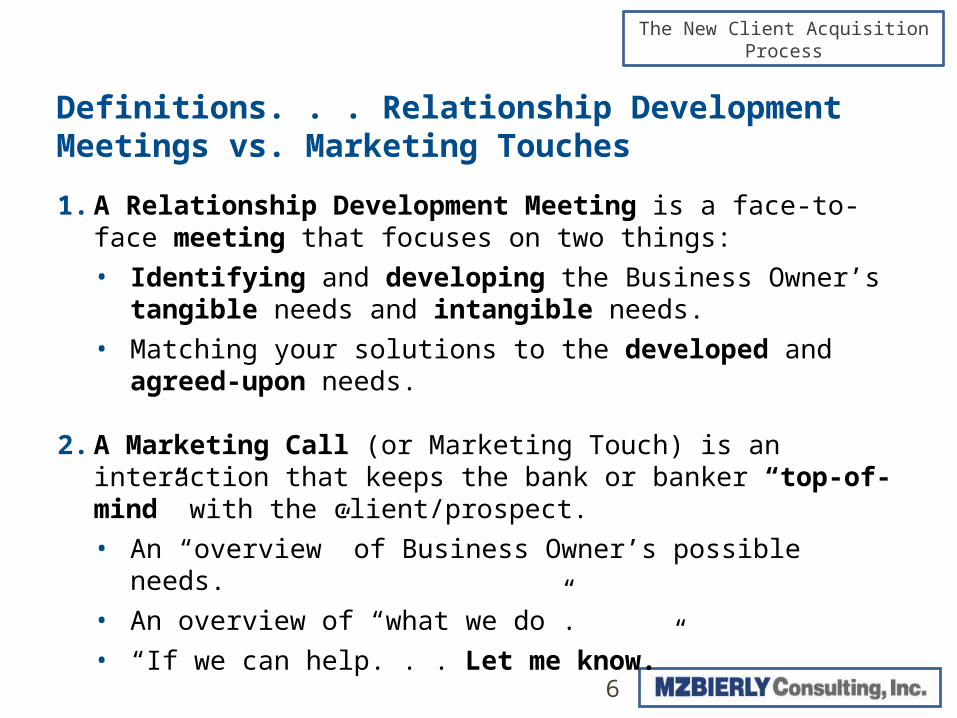

1. A Relationship Development Meeting is a face-to-face meeting that focuses on two things:

• Identifying and developing the Business Owner’s tangible needs and intangible needs.

• Matching your solutions to the developed and agreed-upon needs.

2. A Marketing Call (or Marketing Touch) is an interaction that keeps the bank or banker “top-of-mind” with the client/prospect.

• An “overview” of Business Owner’s possible needs.

• An overview of “what we do”.

• “If we can help. . . Let me know.”

Definitions. . . Relationship Development Meetings vs. Marketing Touches

6

The New Client Acquisition Process

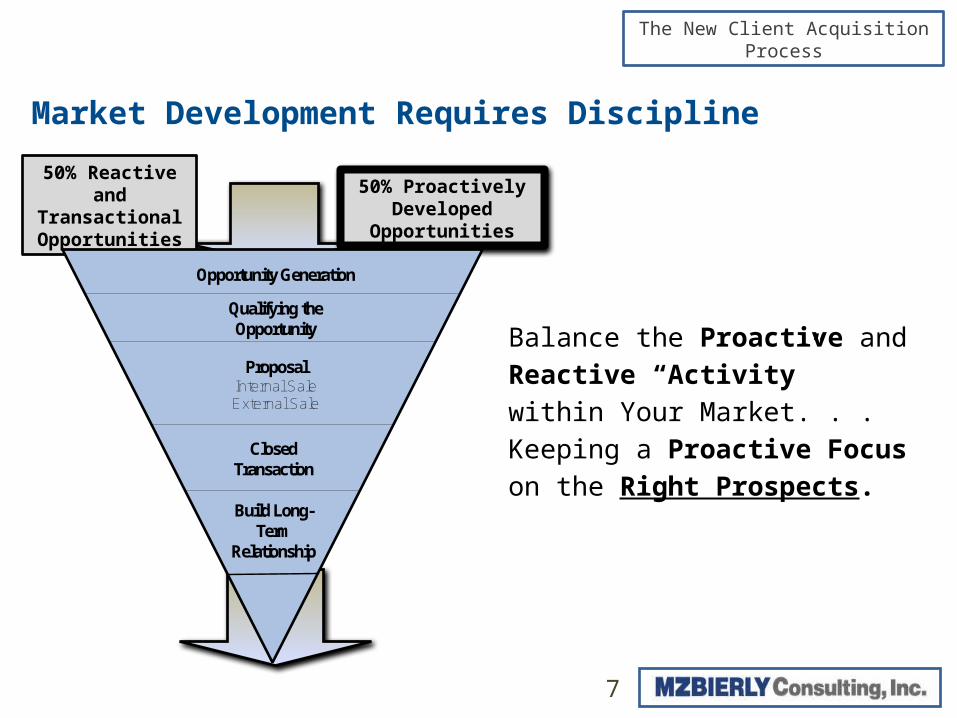

Opportunity Generation

Qualifying the Opportunity

ProposalInternal SaleExternal Sale

Closed Transaction

Build Long-Term

Relationship

7

50% Proactively Developed Opportunities

50% Reactive and Transactional Opportunities

Balance the Proactive and

Reactive “Activity” within Your

Market. . . Keeping a Proactive

Focus on the Right Prospects.

Market Development Requires Discipline

The New Client Acquisition Process

Segment the Client Base

1. Retention Relationships

2. Expansion Relationships

3. Acquisition Relationships

4. Other Clients

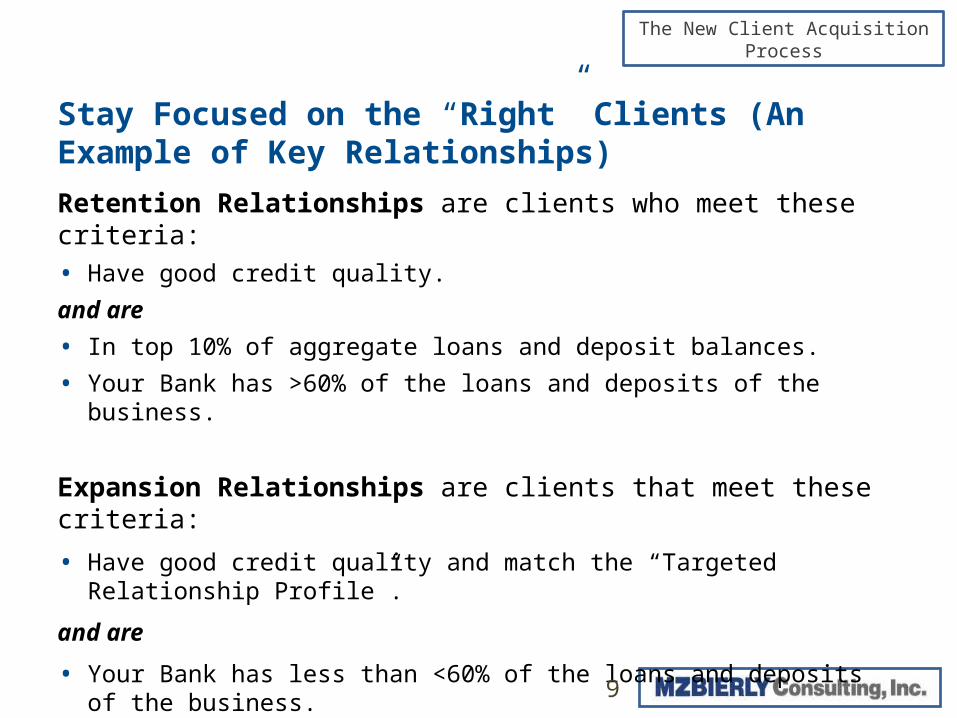

Stay Focused on the “Right” Clients (An Example of Key Relationships)

8

The New Client Acquisition Process

Retention Relationships are clients who meet these criteria:

• Have good credit quality.

and are

• In top 10% of aggregate loans and deposit balances.

• Your Bank has >60% of the loans and deposits of the business.

Expansion Relationships are clients that meet these criteria:

• Have good credit quality and match the “Targeted Relationship Profile”.

and are

• Your Bank has less than <60% of the loans and deposits of the business.

and have

• Significant cross-sell/up-sell opportunities in next 18 months.

Stay Focused on the “Right” Clients (An Example of Key Relationships)

9

The New Client Acquisition Process

High Appeal Industries Limited Appeal Industries

Manufacturers Real Estate Investment

Wholesalers Low-End Retail

Distributors Restaurants Architect, Engineering and Business Service

Firms Mini-Warehouses/Carwashes

Law Practices Landscaping

Accounting Firms Service or Gas Stations

Insurance Brokers or Firms Used Car Dealerships

Large General Contractors Real Estate Investment

Medical, Dental and Health Practices Low-End Retail

Ag-Related Businesses Restaurants

Stay Focused on the Right Businesses

10

Defining the “Industries” you want to Focus on

The New Client Acquisition Process

Business Characteristics

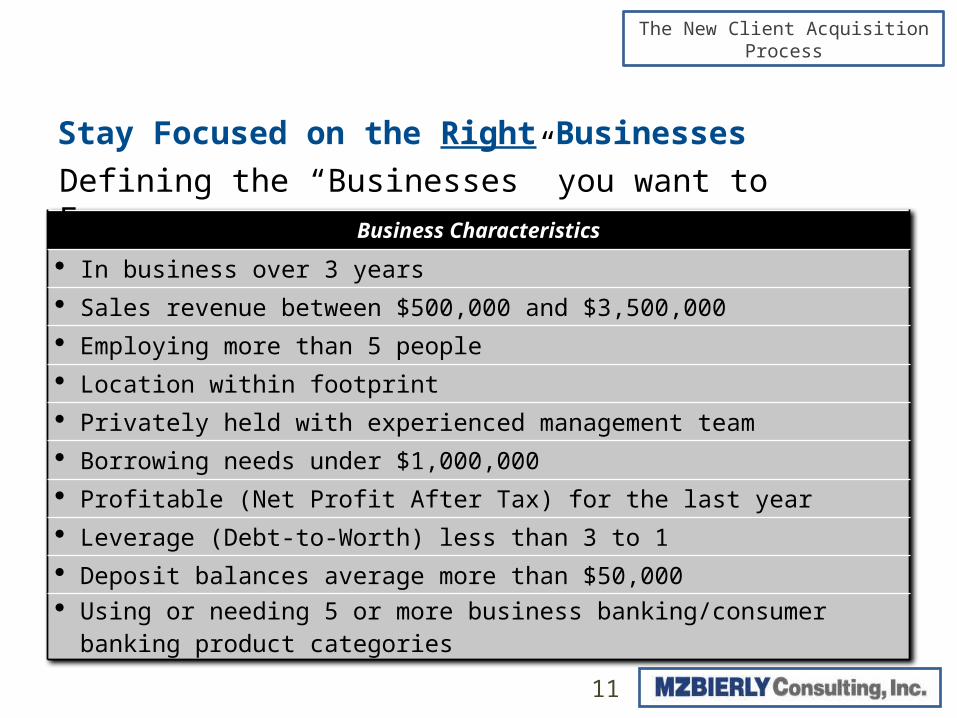

In business over 3 years

Sales revenue between $500,000 and $3,500,000

Employing more than 5 people

Location within footprint

Privately held with experienced management team

Borrowing needs under $1,000,000

Profitable (Net Profit After Tax) for the last year

Leverage (Debt-to-Worth) less than 3 to 1

Deposit balances average more than $50,000

Using or needing 5 or more business banking/consumer banking product categories

Stay Focused on the Right Businesses

11

Defining the “Businesses” you want to Focus on

The New Client Acquisition Process

Business Characteristics

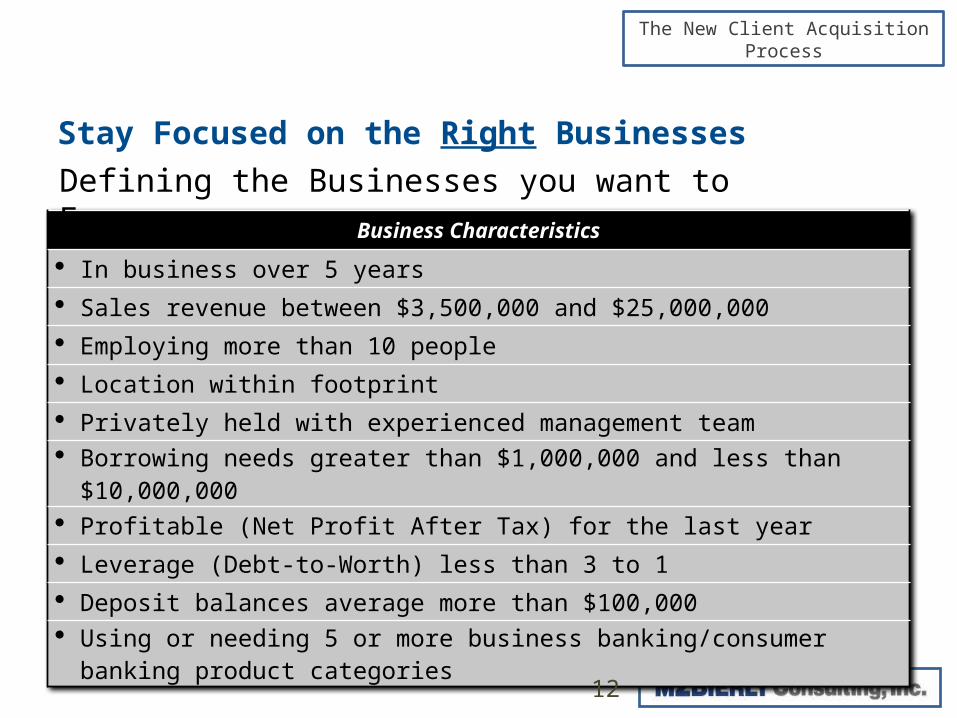

In business over 5 years

Sales revenue between $3,500,000 and $25,000,000

Employing more than 10 people

Location within footprint

Privately held with experienced management team

Borrowing needs greater than $1,000,000 and less than $10,000,000

Profitable (Net Profit After Tax) for the last year

Leverage (Debt-to-Worth) less than 3 to 1

Deposit balances average more than $100,000

Using or needing 5 or more business banking/consumer banking product categories

Stay Focused on the Right Businesses

12

Defining the Businesses you want to Focus on

The New Client Acquisition Process

13

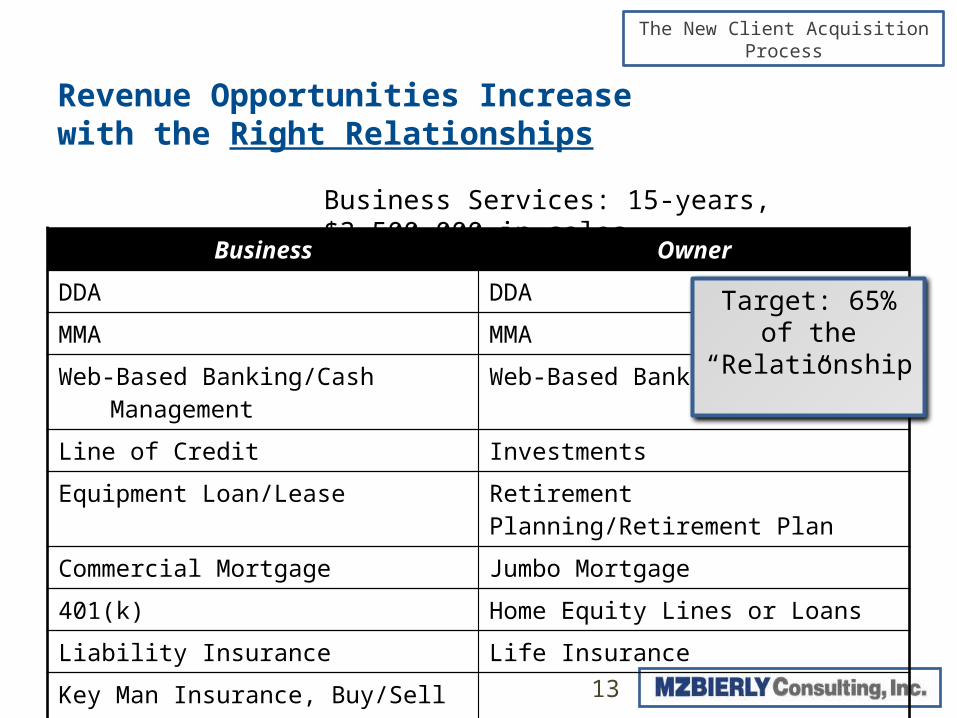

Business Owner

DDA DDA

MMA MMA

Web-Based Banking/Cash Management Web-Based Banking

Line of Credit Investments

Equipment Loan/Lease Retirement Planning/Retirement Plan

Commercial Mortgage Jumbo Mortgage

401(k) Home Equity Lines or Loans

Liability Insurance Life Insurance

Key Man Insurance, Buy/Sell Agreement

Total: 9 Total: 8

Business Services: 15-years, $3,500,000 in sales

Revenue Opportunities Increasewith the Right Relationships

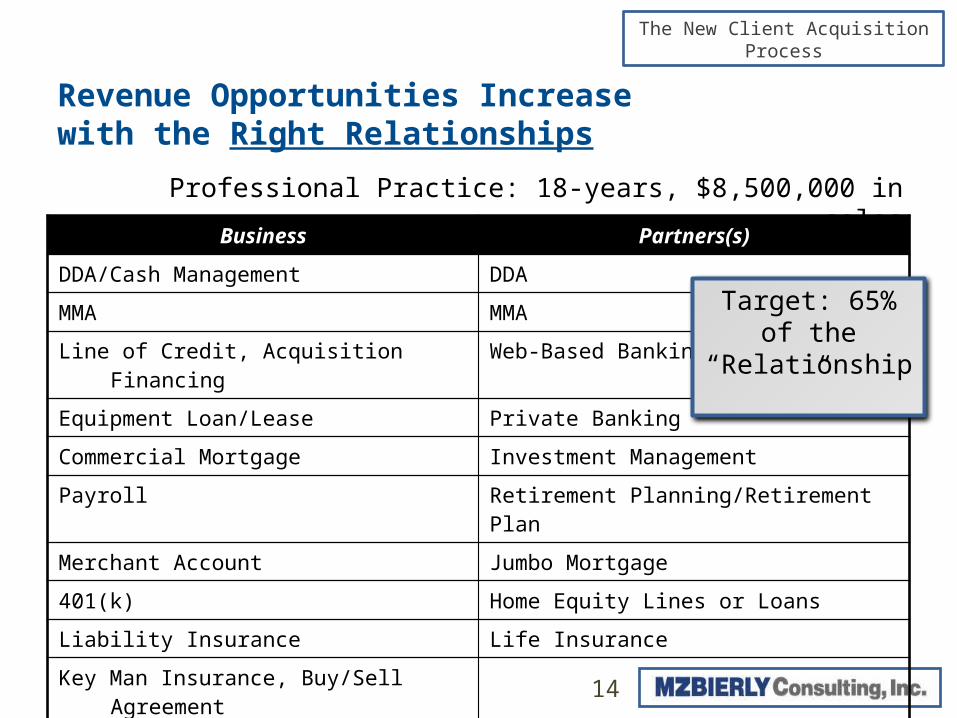

Target: 65% of the “Relationship”

The New Client Acquisition Process

14

Business Partners(s)

DDA/Cash Management DDAMMA MMALine of Credit, Acquisition Financing Web-Based BankingEquipment Loan/Lease Private BankingCommercial Mortgage Investment ManagementPayroll Retirement Planning/Retirement PlanMerchant Account Jumbo Mortgage401(k) Home Equity Lines or LoansLiability Insurance Life Insurance

Key Man Insurance, Buy/Sell AgreementTotal: 10 Total: 9

Revenue Opportunities Increasewith the Right Relationships

Professional Practice: 18-years, $8,500,000 in sales

Target: 65% of the “Relationship”

The New Client Acquisition Process

15

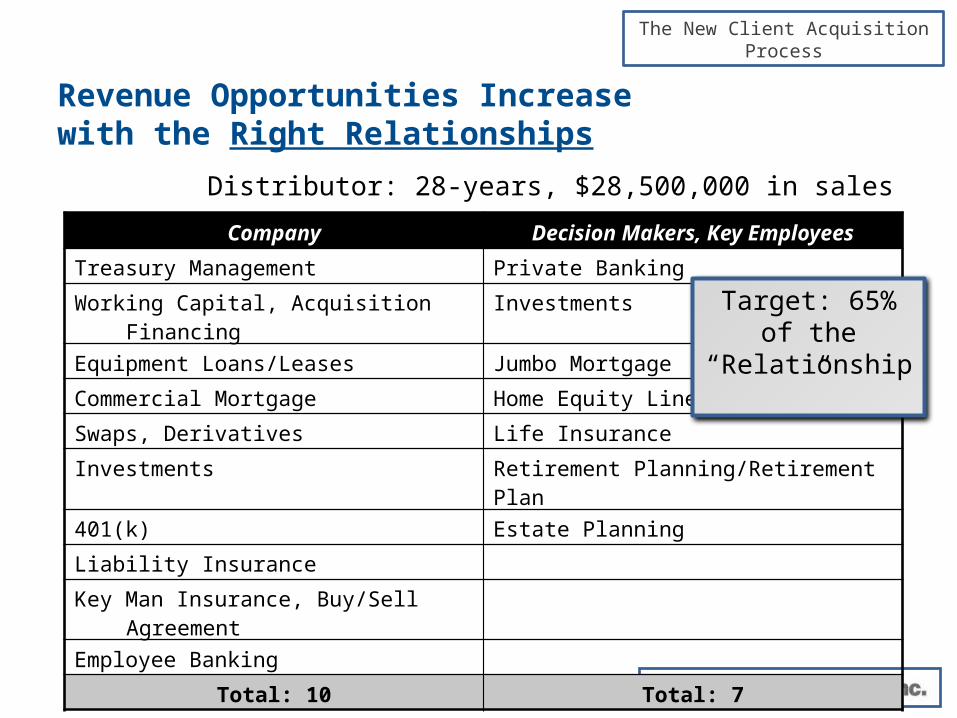

Distributor: 28-years, $28,500,000 in sales

Company Decision Makers, Key Employees

Treasury Management Private Banking

Working Capital, Acquisition Financing Investments

Equipment Loans/Leases Jumbo Mortgage

Commercial Mortgage Home Equity Lines or Loans

Swaps, Derivatives Life Insurance

Investments Retirement Planning/Retirement Plan

401(k) Estate Planning

Liability Insurance

Key Man Insurance, Buy/Sell Agreement

Employee Banking

Total: 10 Total: 7

Target: 65% of the “Relationship”

Revenue Opportunities Increasewith the Right Relationships

The New Client Acquisition Process

CHANGE THE CONVERSATION

16

The How-To Section: An Articulated Process

The New Client Acquisition Process

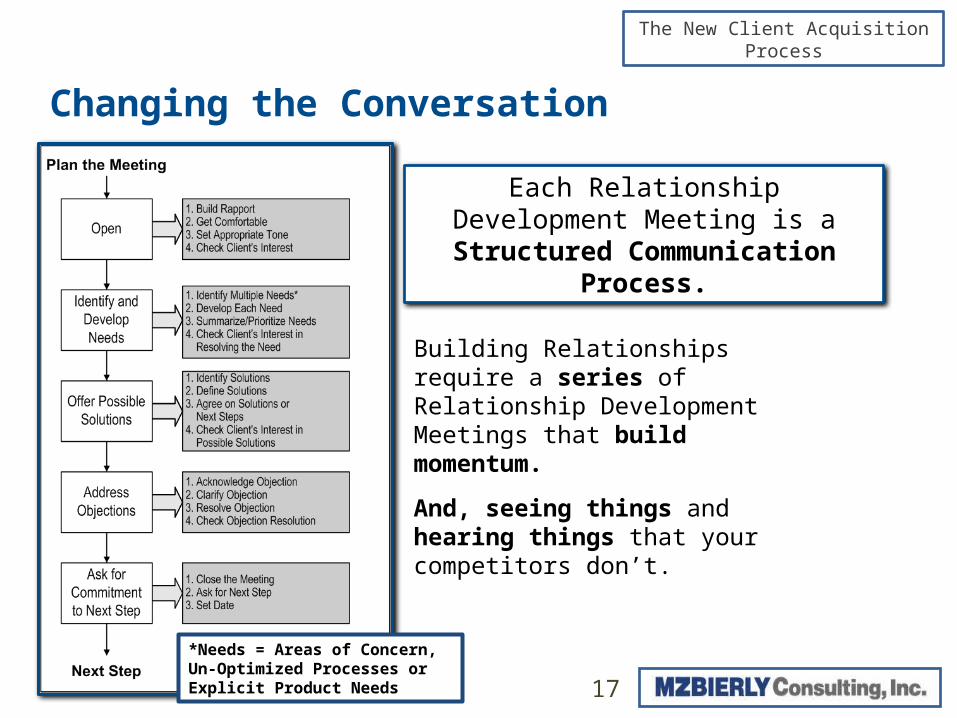

Building Relationships require a series of Relationship Development Meetings that build momentum.

And, seeing things and hearing things that your competitors don’t.

Changing the Conversation

17

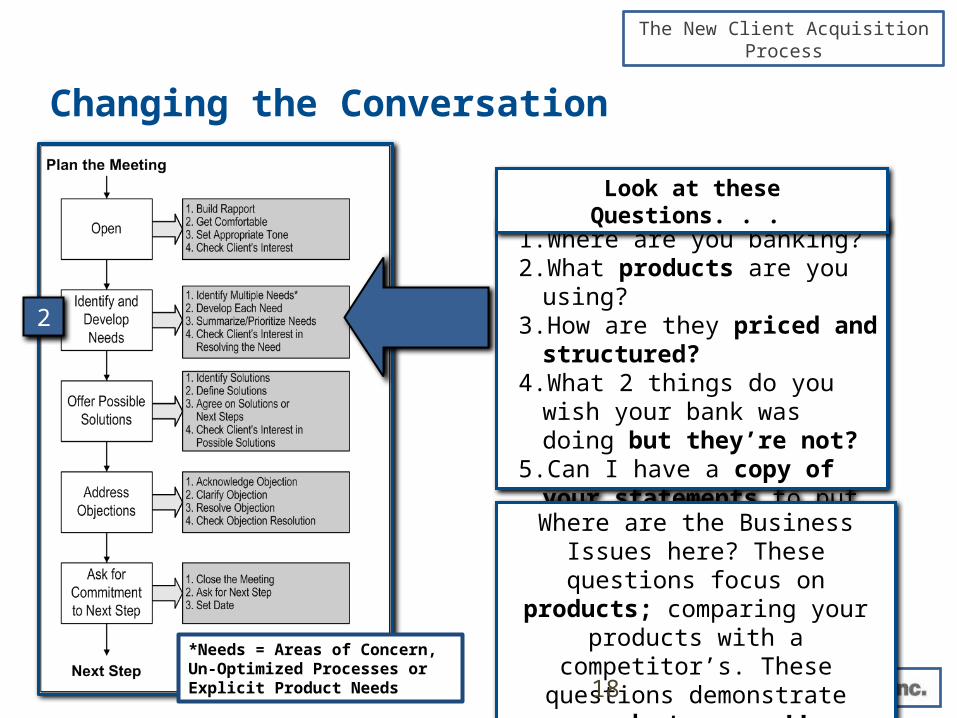

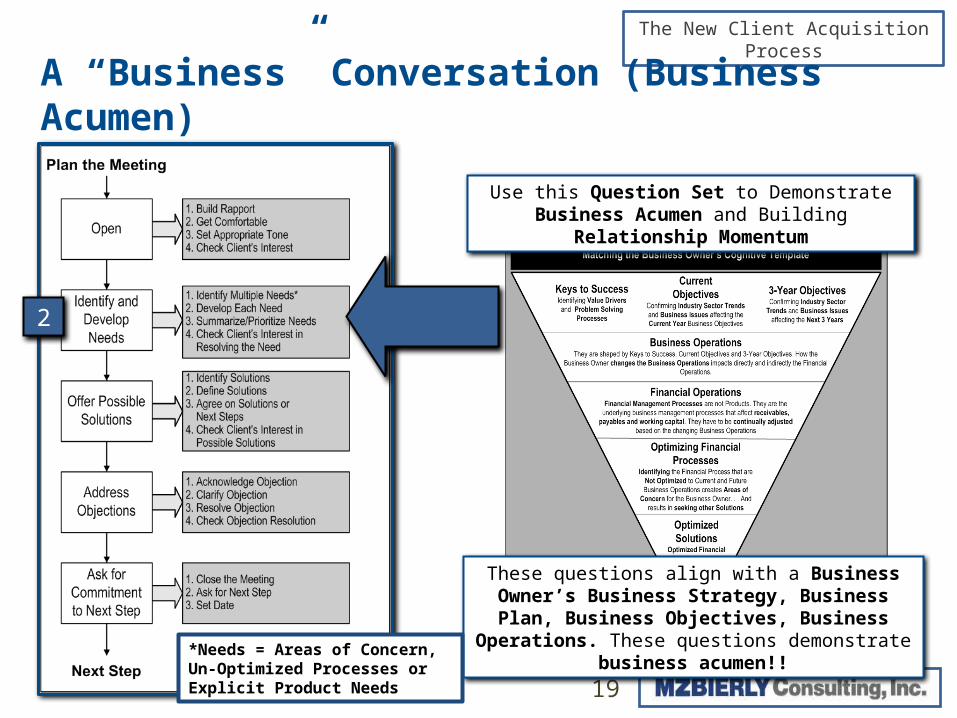

Each Relationship Development Meeting is a Structured

Communication Process.

*Needs = Areas of Concern, Un-Optimized Processes or Explicit Product Needs

The New Client Acquisition Process

1. Where are you banking?2. What products are you using?3. How are they priced and structured?4. What 2 things do you wish your bank

was doing but they’re not?5. Can I have a copy of your

statements to put together an offer of how we would handle your banking relationship?

Where are the Business Issues here? These questions focus on products;

comparing your products with a competitor’s. These questions demonstrate

product acumen!!

Look at these Questions. . .

2

Changing the Conversation

18

*Needs = Areas of Concern, Un-Optimized Processes or Explicit Product Needs

The New Client Acquisition Process

A “Business” Conversation (Business Acumen)

19

These questions align with a Business Owner’s Business Strategy, Business Plan, Business

Objectives, Business Operations. These questions demonstrate business acumen!!

Use this Question Set to Demonstrate Business Acumen and Building

Relationship Momentum

2

*Needs = Areas of Concern, Un-Optimized Processes or Explicit Product Needs

The New Client Acquisition Process

20

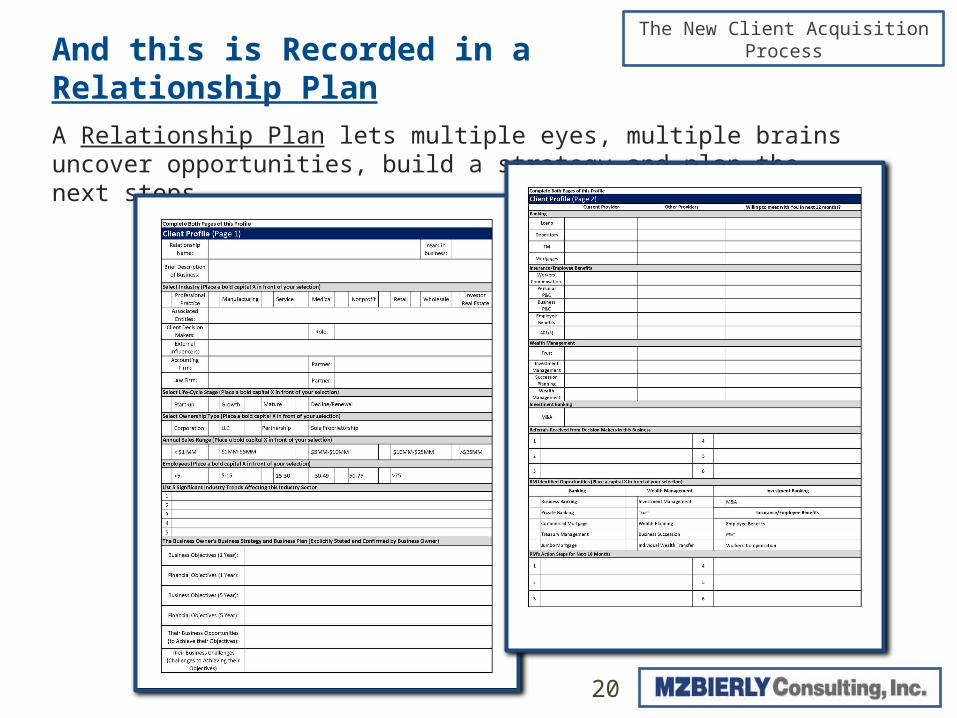

And this is Recorded in aRelationship Plan

A Relationship Plan lets multiple eyes, multiple brains uncover opportunities, build a strategy and plan the next steps.

The New Client Acquisition Process

ACQUIRINGNEW RELATIONSHIPS

21

The How-To Section: An Articulated Process

The New Client Acquisition Process

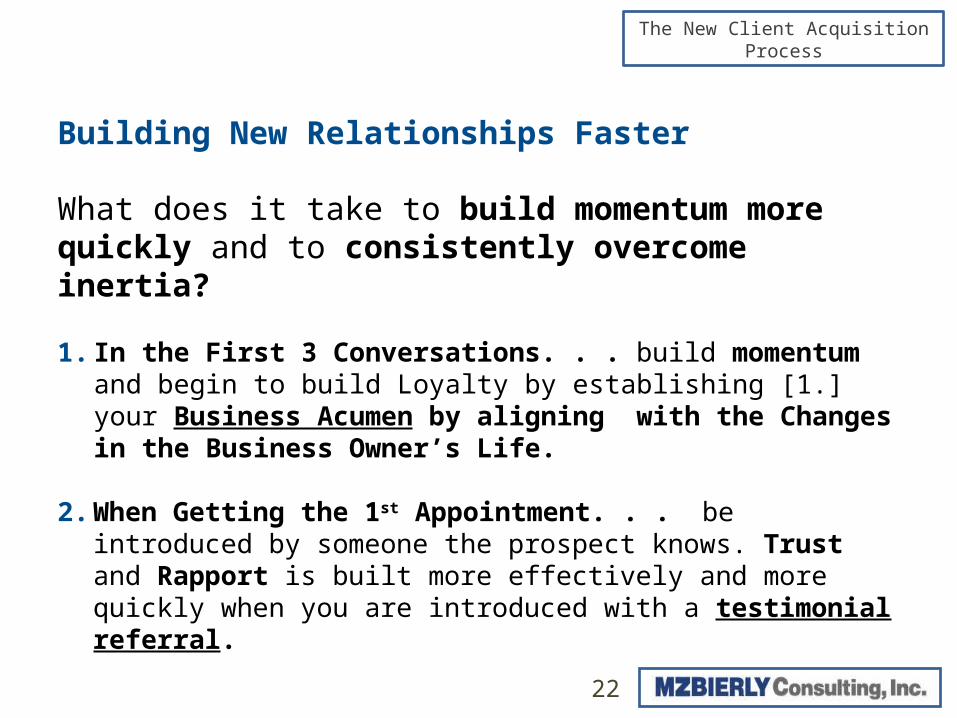

What does it take to build momentum more quickly and to consistently overcome inertia?

1. In the First 3 Conversations. . . build momentum and begin to build Loyalty by establishing [1.] your Business Acumen by aligning with the Changes in the Business Owner’s Life.

2. When Getting the 1st Appointment. . . be introduced by someone the prospect knows. Trust and Rapport is built more effectively and more quickly when you are introduced with a testimonial referral.

Building New Relationships Faster

22

The New Client Acquisition Process

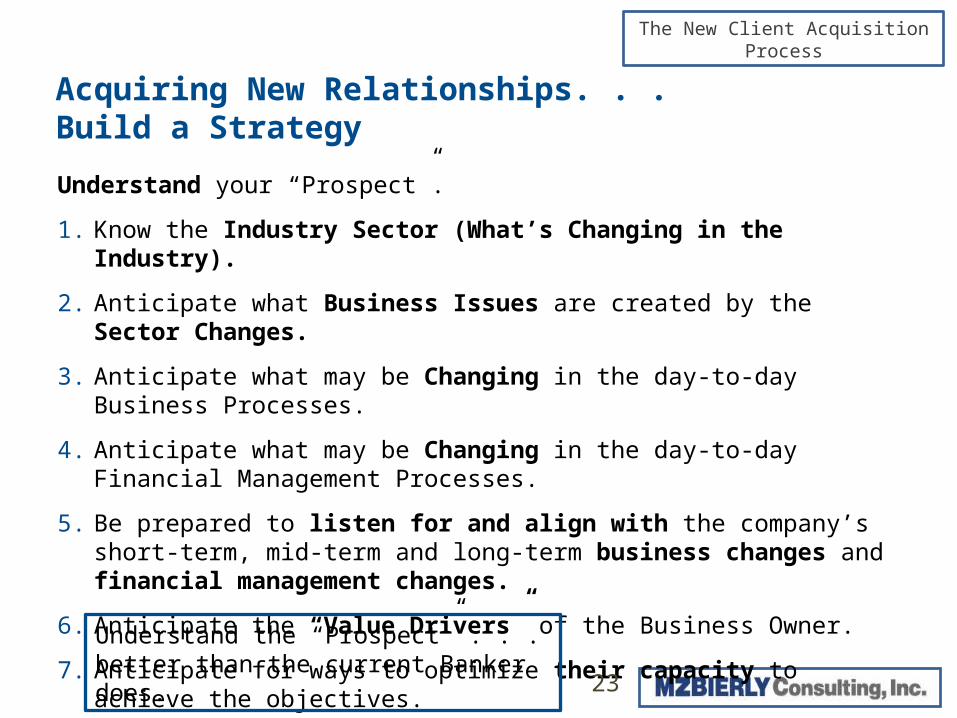

Understand your “Prospect”.

1. Know the Industry Sector (What’s Changing in the Industry).

2. Anticipate what Business Issues are created by the Sector Changes.

3. Anticipate what may be Changing in the day-to-day Business Processes.

4. Anticipate what may be Changing in the day-to-day Financial Management Processes.

5. Be prepared to listen for and align with the company’s short-term, mid-term and long-term business changes and financial management changes.

6. Anticipate the “Value Drivers” of the Business Owner.

7. Anticipate for ways to optimize their capacity to achieve the objectives.

Acquiring New Relationships. . .Build a Strategy

23

Understand the “Prospect” . . . better than the current Banker does.

The New Client Acquisition Process

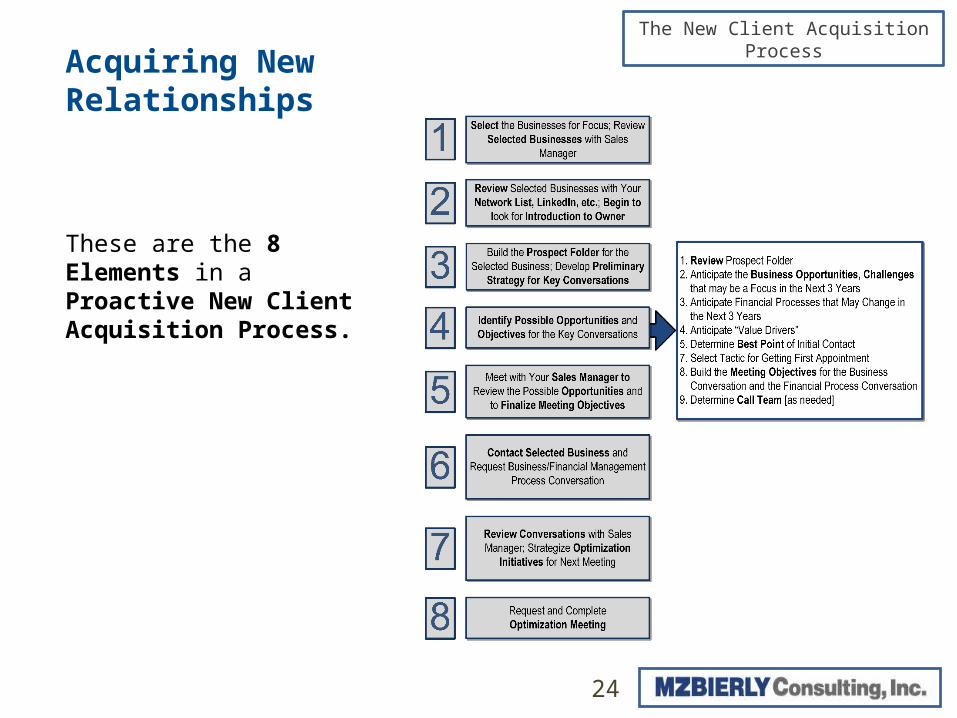

Acquiring New Relationships

24

These are the 8 Elements in a Proactive New Client Acquisition Process.

The New Client Acquisition Process

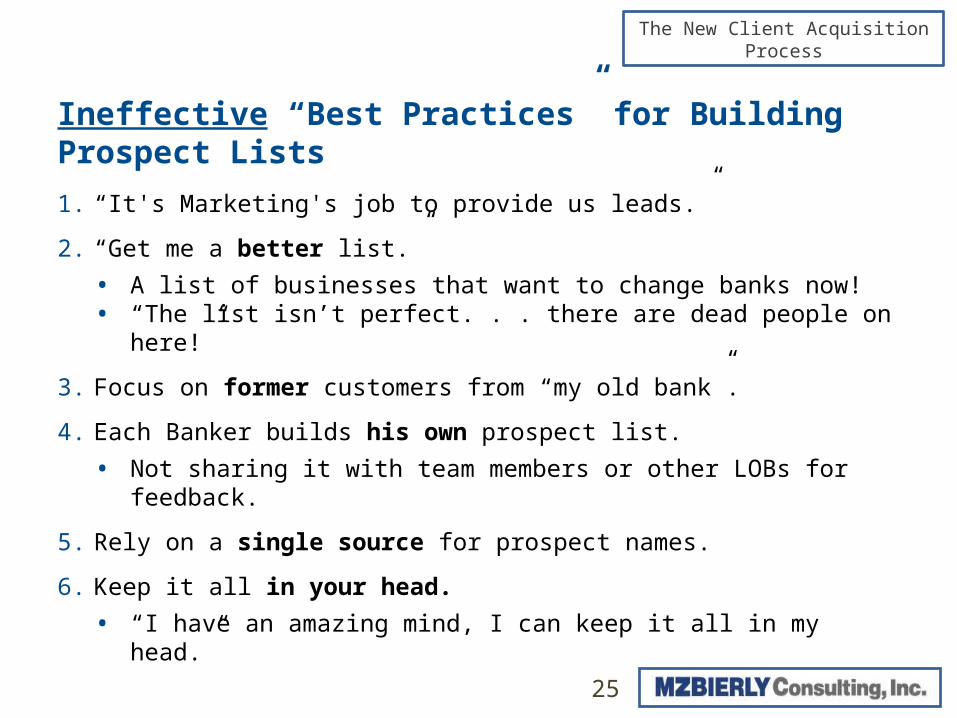

1. “It's Marketing's job to provide us leads.”

2. “Get me a better list.”

• A list of businesses that want to change banks now!• “The list isn’t perfect. . . there are dead people on here!”

3. Focus on former customers from “my old bank”.

4. Each Banker builds his own prospect list.

• Not sharing it with team members or other LOBs for feedback.

5. Rely on a single source for prospect names.

6. Keep it all in your head.

• “I have an amazing mind, I can keep it all in my head.”

Ineffective “Best Practices” for Building Prospect Lists

25

The New Client Acquisition Process

1. D&B Strategic Marketing Database, Hoovers Lead Builder, Data.com

2. ReferenceUSA

3. Local Industrial Development Authority (electronic version)

4. UCC Filings (there are compilation services)

5. Local Business Publication directories (not always a good choice, too visible)

6. Guidestar.org (a great source for 501C3s)

7. Trade Association Memberships or Websites (a few examples)• American Society of Association Executives (www.asaenet.org/find/)• American Dental Association directory (www.ada.org)• American Institute of Architects directory (www.AIA.org)• State and local trade association listings

Using Multiple Sources for Your Prospect List

26

The New Client Acquisition Process

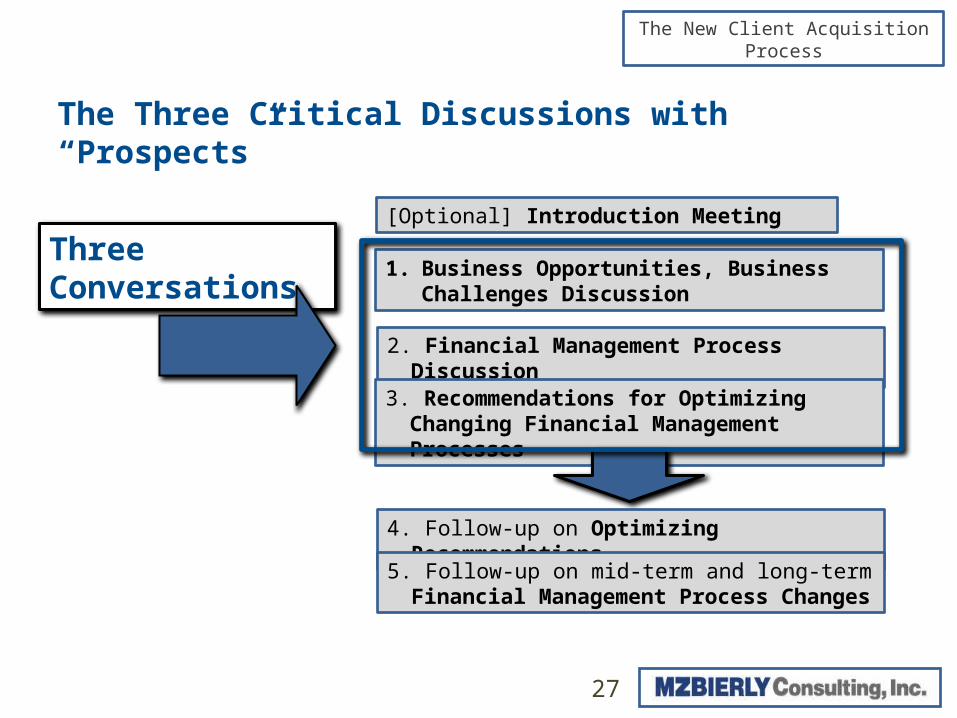

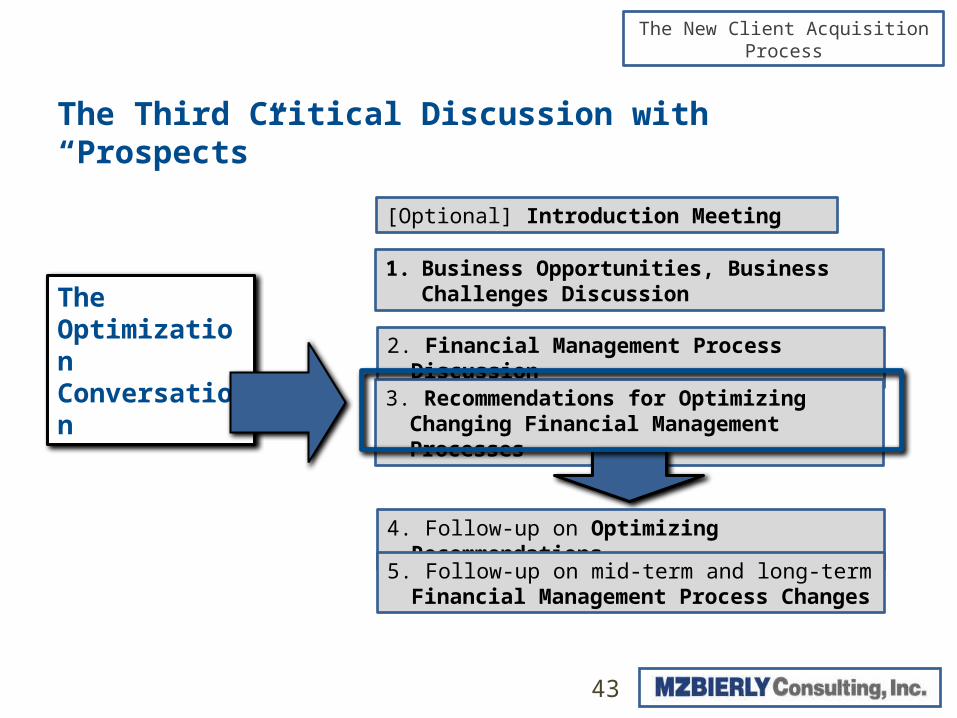

The Three Critical Discussions with “Prospects”

27

Three Conversations[Optional] Introduction Meeting

1. Business Opportunities, Business Challenges Discussion

2. Financial Management Process Discussion

3. Recommendations for Optimizing Changing Financial Management Processes

4. Follow-up on Optimizing Recommendations

5. Follow-up on mid-term and long-term Financial Management Process Changes

The New Client Acquisition Process

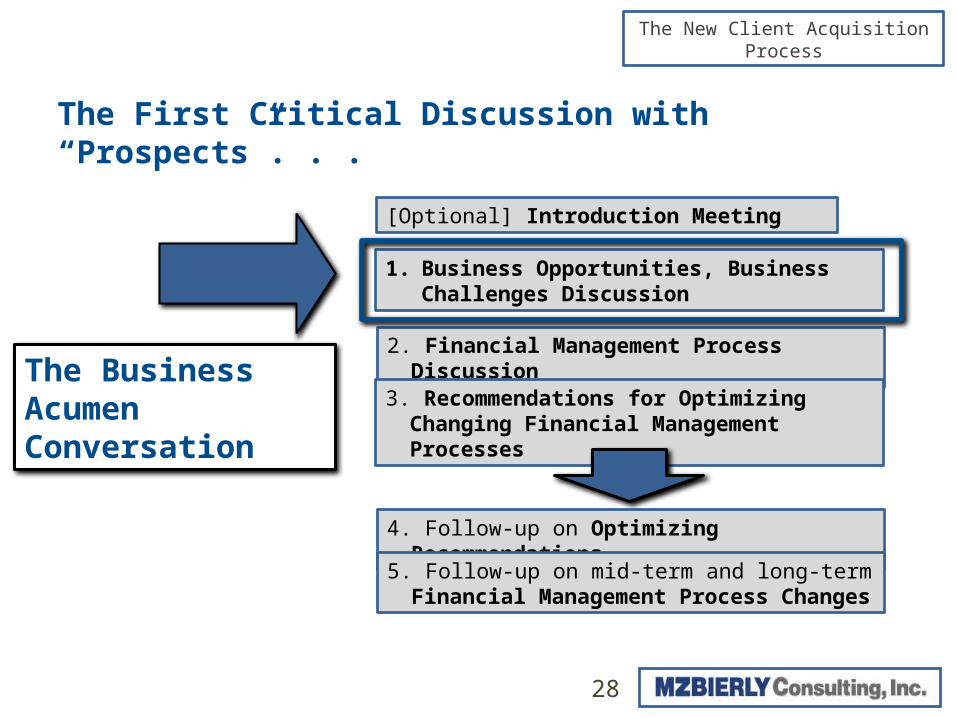

The First Critical Discussion with “Prospects”. . .

28

The Business Acumen Conversation

[Optional] Introduction Meeting

1. Business Opportunities, Business Challenges Discussion

2. Financial Management Process Discussion

3. Recommendations for Optimizing Changing Financial Management Processes

4. Follow-up on Optimizing Recommendations

5. Follow-up on mid-term and long-term Financial Management Process Changes

The New Client Acquisition Process

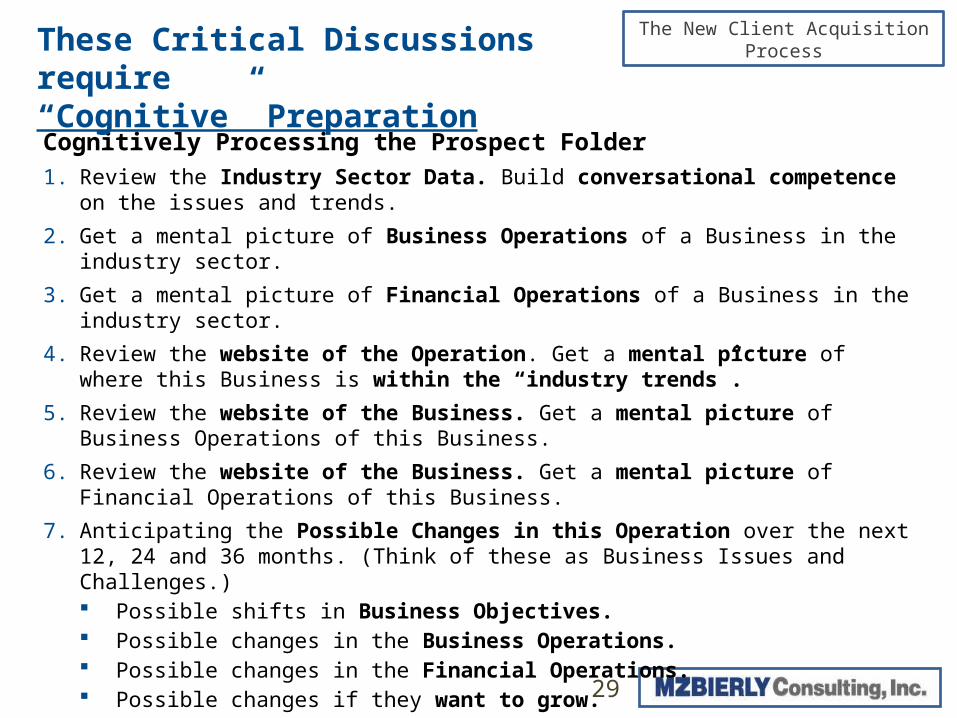

Cognitively Processing the Prospect Folder

1. Review the Industry Sector Data. Build conversational competence on the issues and trends.

2. Get a mental picture of Business Operations of a Business in the industry sector.

3. Get a mental picture of Financial Operations of a Business in the industry sector.

4. Review the website of the Operation. Get a mental picture of where this Business is within the “industry trends”.

5. Review the website of the Business. Get a mental picture of Business Operations of this Business.

6. Review the website of the Business. Get a mental picture of Financial Operations of this Business.

7. Anticipating the Possible Changes in this Operation over the next 12, 24 and 36 months. (Think of these as Business Issues and Challenges.) Possible shifts in Business Objectives. Possible changes in the Business Operations. Possible changes in the Financial Operations. Possible changes if they want to grow. Possible changes if they don’t want to grow.

These Critical Discussions require“Cognitive” Preparation

29

The New Client Acquisition Process

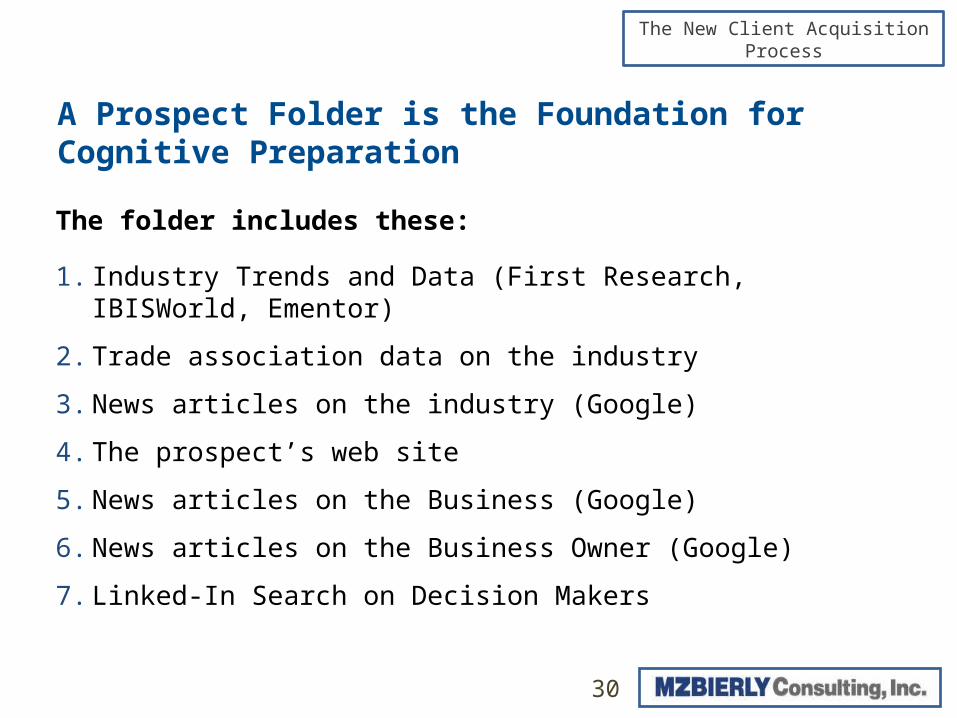

The folder includes these:

1. Industry Trends and Data (First Research, IBISWorld, Ementor)

2. Trade association data on the industry

3. News articles on the industry (Google)

4. The prospect’s web site

5. News articles on the Business (Google)

6. News articles on the Business Owner (Google)

7. Linked-In Search on Decision Makers

A Prospect Folder is the Foundation forCognitive Preparation

30

The New Client Acquisition Process

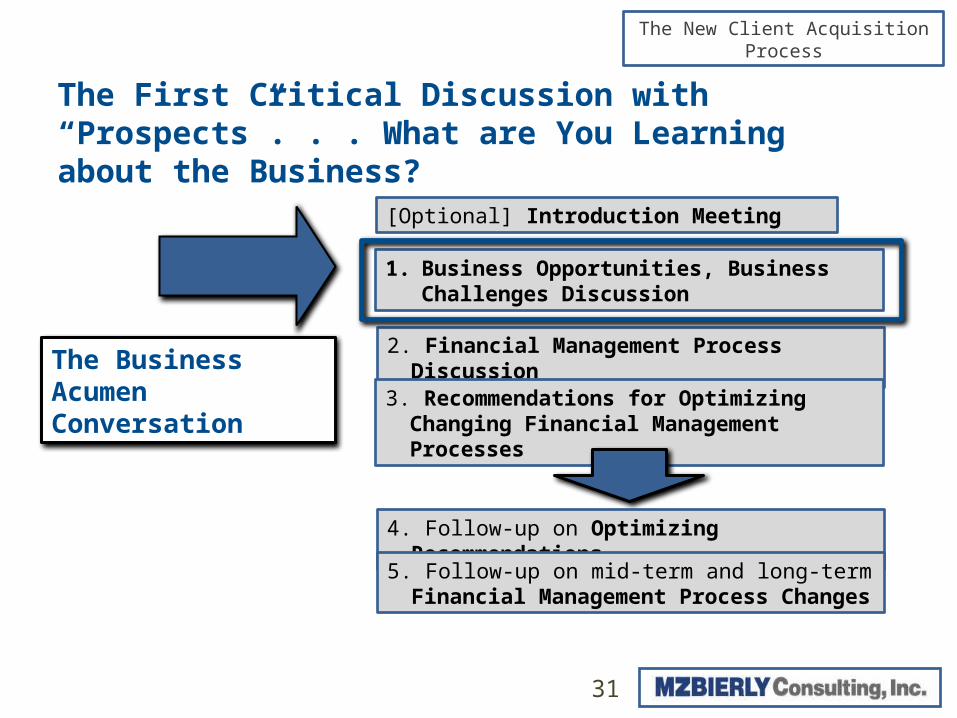

The First Critical Discussion with “Prospects”. . . What are You Learning about the Business?

31

The Business Acumen Conversation

[Optional] Introduction Meeting

1. Business Opportunities, Business Challenges Discussion

2. Financial Management Process Discussion

3. Recommendations for Optimizing Changing Financial Management Processes

4. Follow-up on Optimizing Recommendations

5. Follow-up on mid-term and long-term Financial Management Process Changes

The New Client Acquisition Process

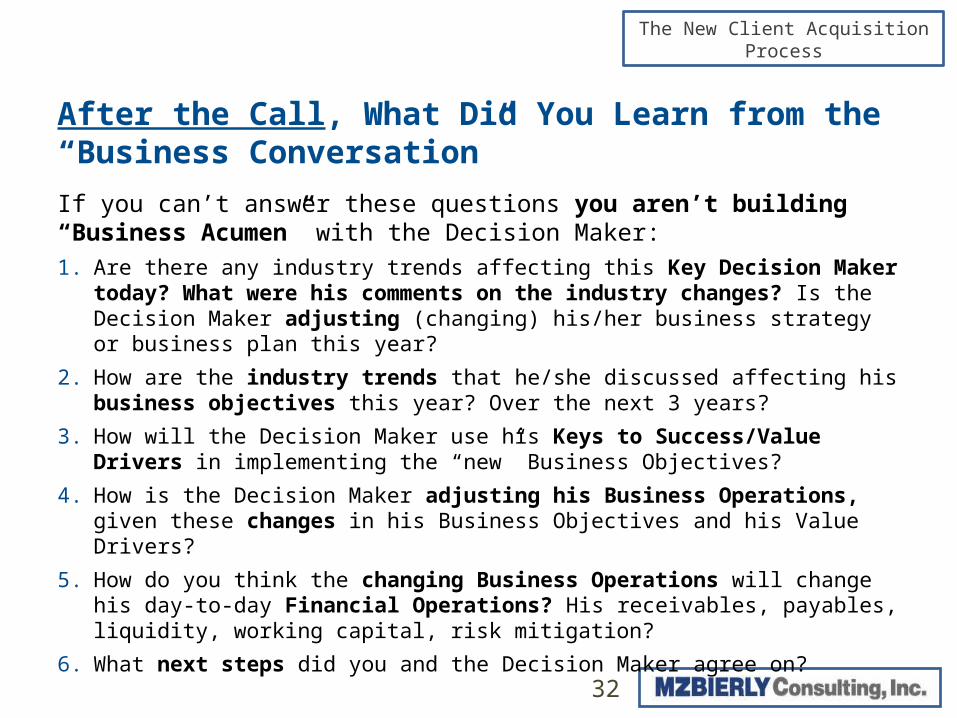

If you can’t answer these questions you aren’t building “Business Acumen” with the Decision Maker:

1. Are there any industry trends affecting this Key Decision Maker today? What were his comments on the industry changes? Is the Decision Maker adjusting (changing) his/her business strategy or business plan this year?

2. How are the industry trends that he/she discussed affecting his business objectives this year? Over the next 3 years?

3. How will the Decision Maker use his Keys to Success/Value Drivers in implementing the “new” Business Objectives?

4. How is the Decision Maker adjusting his Business Operations, given these changes in his Business Objectives and his Value Drivers?

5. How do you think the changing Business Operations will change his day-to-day Financial Operations? His receivables, payables, liquidity, working capital, risk mitigation?

6. What next steps did you and the Decision Maker agree on?

After the Call, What Did You Learn from the “Business Conversation”

32

The New Client Acquisition Process

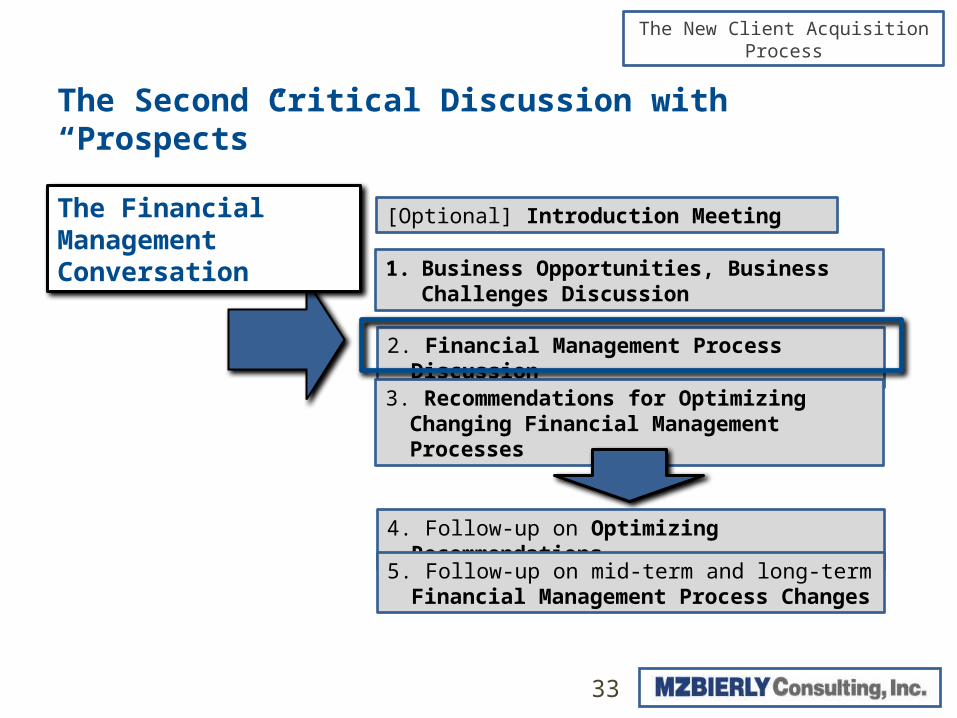

The Second Critical Discussion with “Prospects”

33

The Financial Management Conversation

[Optional] Introduction Meeting

1. Business Opportunities, Business Challenges Discussion

2. Financial Management Process Discussion

3. Recommendations for Optimizing Changing Financial Management Processes

4. Follow-up on Optimizing Recommendations

5. Follow-up on mid-term and long-term Financial Management Process Changes

The New Client Acquisition Process

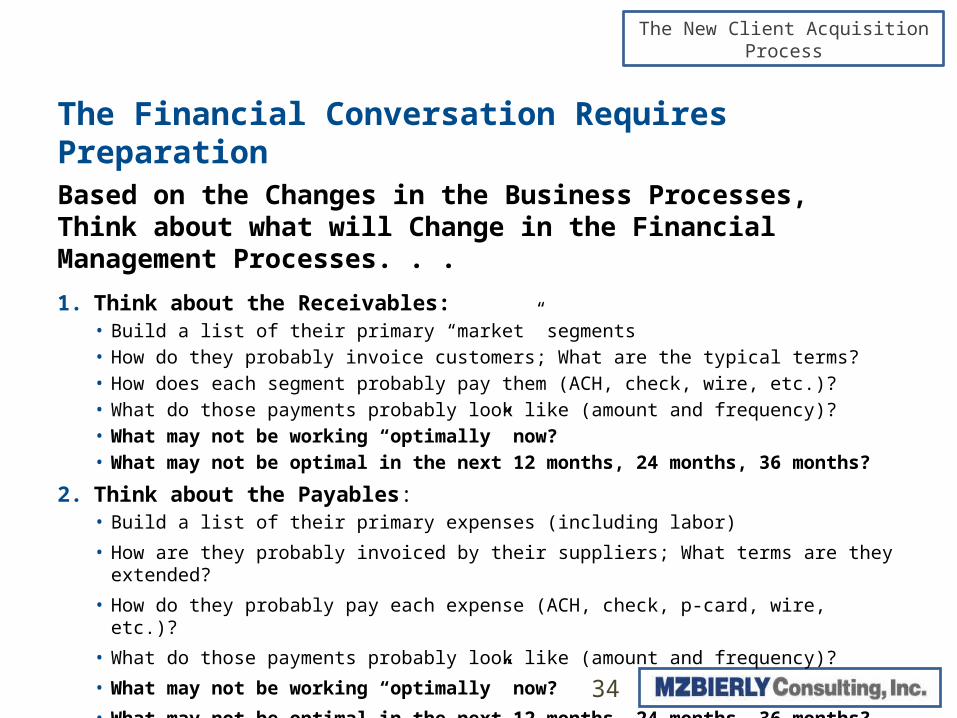

Based on the Changes in the Business Processes, Think about what will Change in the Financial Management Processes. . .

1. Think about the Receivables:• Build a list of their primary “market” segments• How do they probably invoice customers; What are the typical terms?• How does each segment probably pay them (ACH, check, wire, etc.)?• What do those payments probably look like (amount and frequency)?• What may not be working “optimally” now?• What may not be optimal in the next 12 months, 24 months, 36 months?

2. Think about the Payables:• Build a list of their primary expenses (including labor)

• How are they probably invoiced by their suppliers; What terms are they extended?

• How do they probably pay each expense (ACH, check, p-card, wire, etc.)?

• What do those payments probably look like (amount and frequency)?

• What may not be working “optimally” now?

• What may not be optimal in the next 12 months, 24 months, 36 months?

The Financial Conversation Requires Preparation

34

The New Client Acquisition Process

3. Think about how they manage liquidity/working capital?

• From the time they receive a payment until they make a payment, how does the cash flow through the business (the accounts they use, etc.)?

• How do they know their cash position every morning?

• What do they do when they have too little cash?

• What do they do when they have too much cash?

• How do they manage CAP EX needs?

• How do the Owners take money out of the business? Where does it go? (Another bank?)

• What may not be working “optimally” now?

• What may not be optimal in the next 12 months, 24 months, 36 months?

The Financial Conversation Requires Preparation

35

The New Client Acquisition Process

36

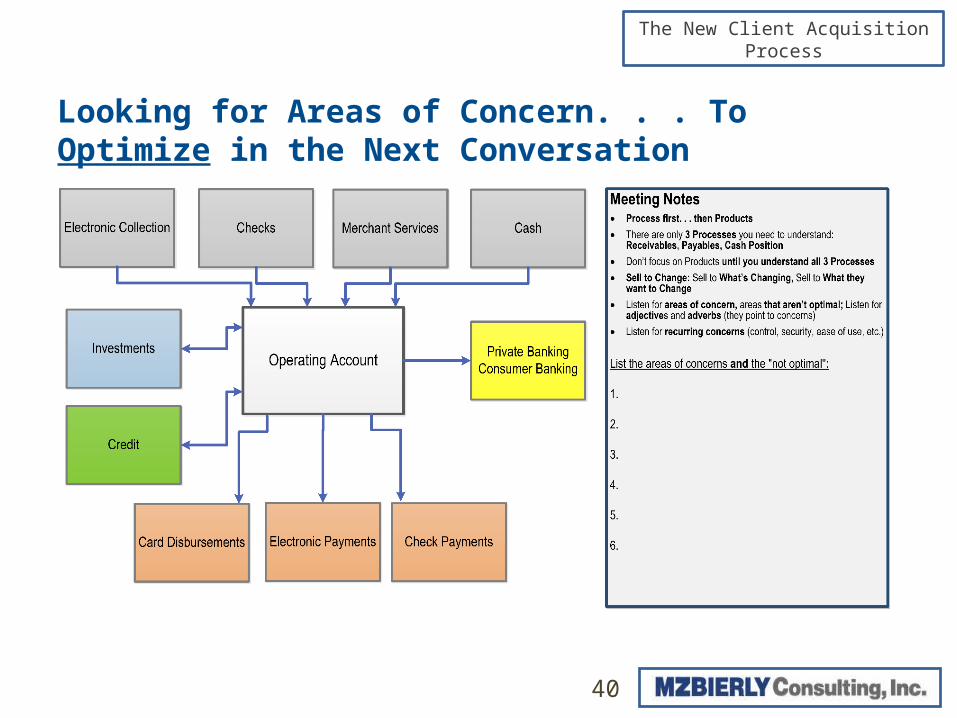

Looking for Areas of Concern. . . To Optimize in the Next Conversation

The New Client Acquisition Process

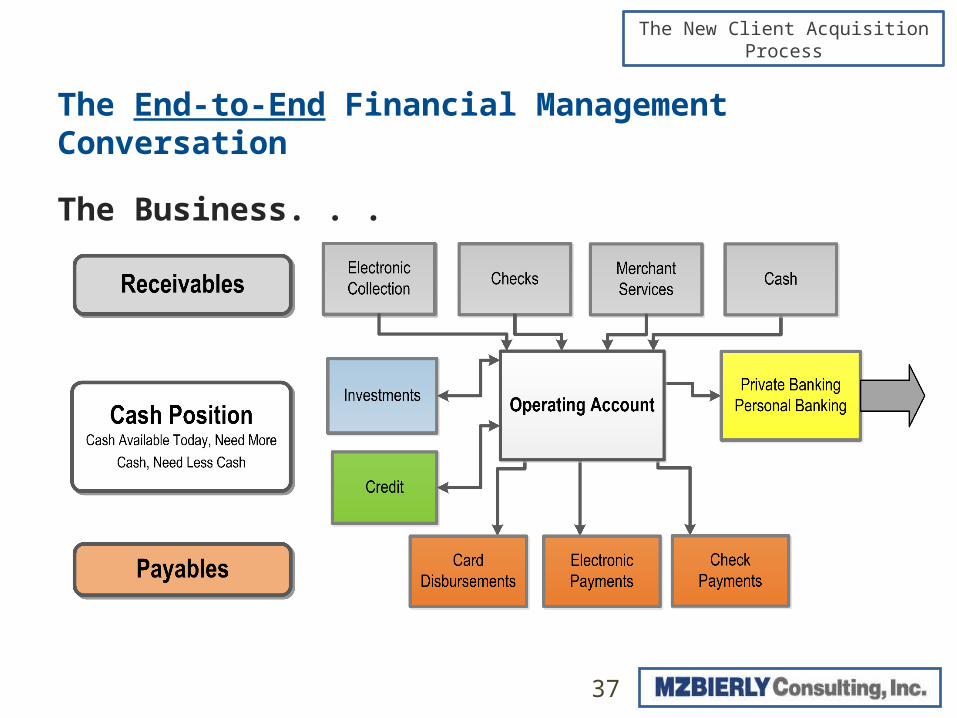

The End-to-End Financial Management Conversation

37

The Business. . .

The New Client Acquisition Process

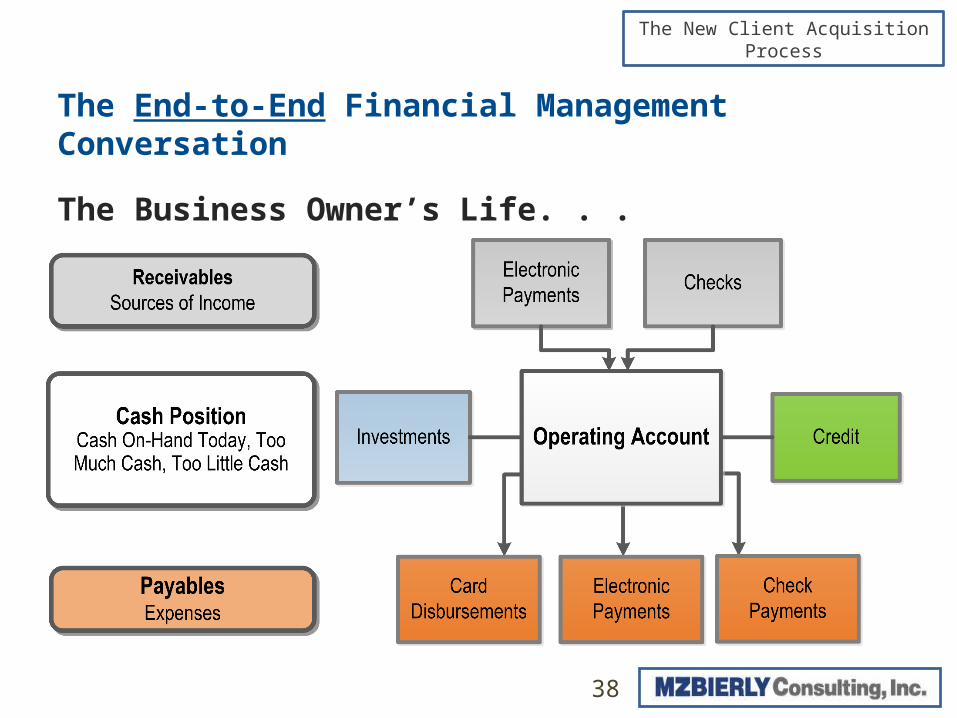

The End-to-End Financial Management Conversation

38

The Business Owner’s Life. . .

The New Client Acquisition Process

39

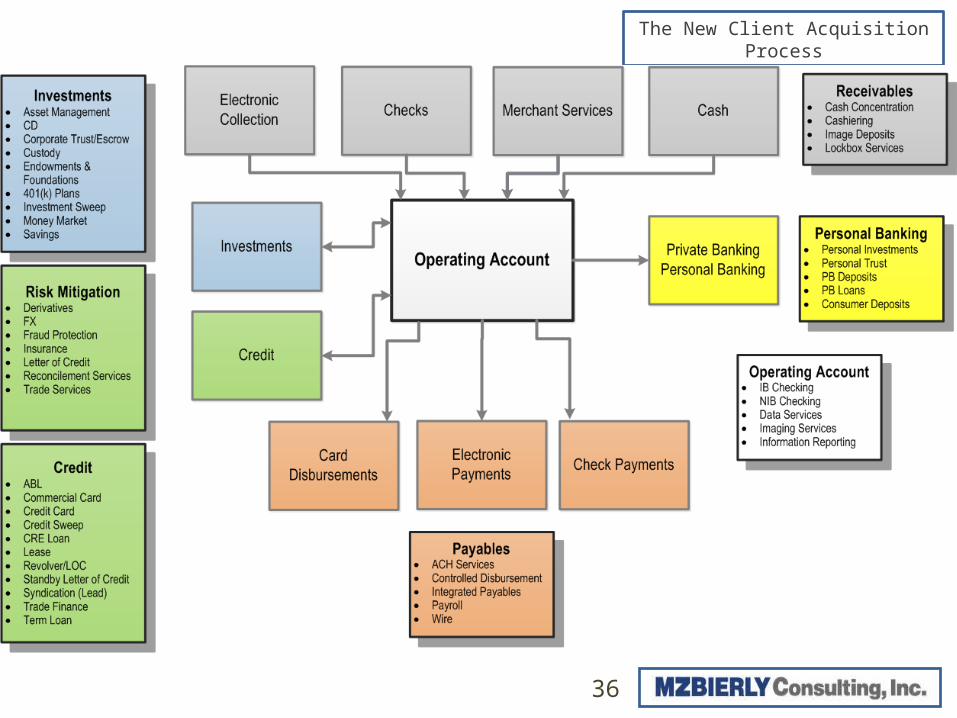

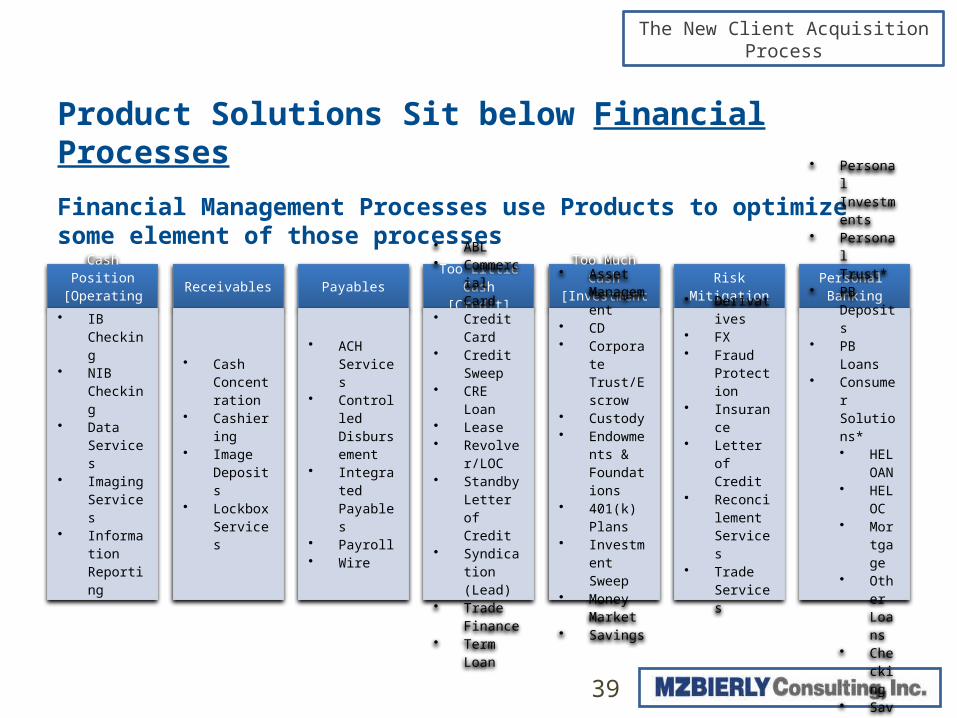

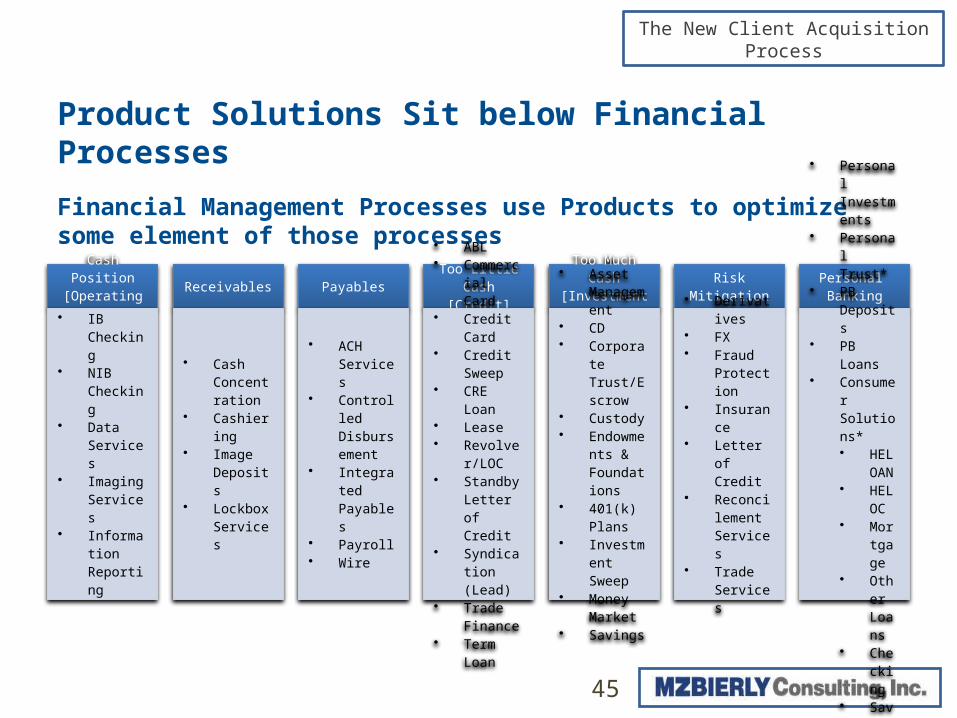

Product Solutions Sit below Financial Processes

Financial Management Processes use Products to optimize some element of those processes

Cash Position [Operating Account]

• IB Checking• NIB

Checking• Data

Services• Imaging

Services• Information

Reporting

Receivables

• Cash Concentration

• Cashiering• Image

Deposits• Lockbox

Services

Payables

• ACH Services

• Controlled Disbursement

• Integrated Payables

• Payroll • Wire

Too Little Cash[Credit]

• ABL• Commercial

Card• Credit Card• Credit

Sweep• CRE Loan• Lease• Revolver/

LOC• Standby

Letter of Credit

• Syndication (Lead)

• Trade Finance

• Term Loan

Too Much Cash[Investments]

• Asset Management

• CD• Corporate

Trust/Escrow

• Custody• Endowment

s & Foundations

• 401(k) Plans

• Investment Sweep

• Money Market

• Savings

RiskMitigation

• Derivatives• FX• Fraud

Protection• Insurance• Letter of

Credit• Reconcilem

ent Services• Trade

Services

Personal Banking

• Personal Investments

• Personal Trust*

• PB Deposits• PB Loans• Consumer

Solutions*• HELO

AN• HELO

C• Mortg

age• Other

Loans• Chec

king• Savin

gs

The New Client Acquisition Process

40

Looking for Areas of Concern. . . To Optimize in the Next Conversation

The New Client Acquisition Process

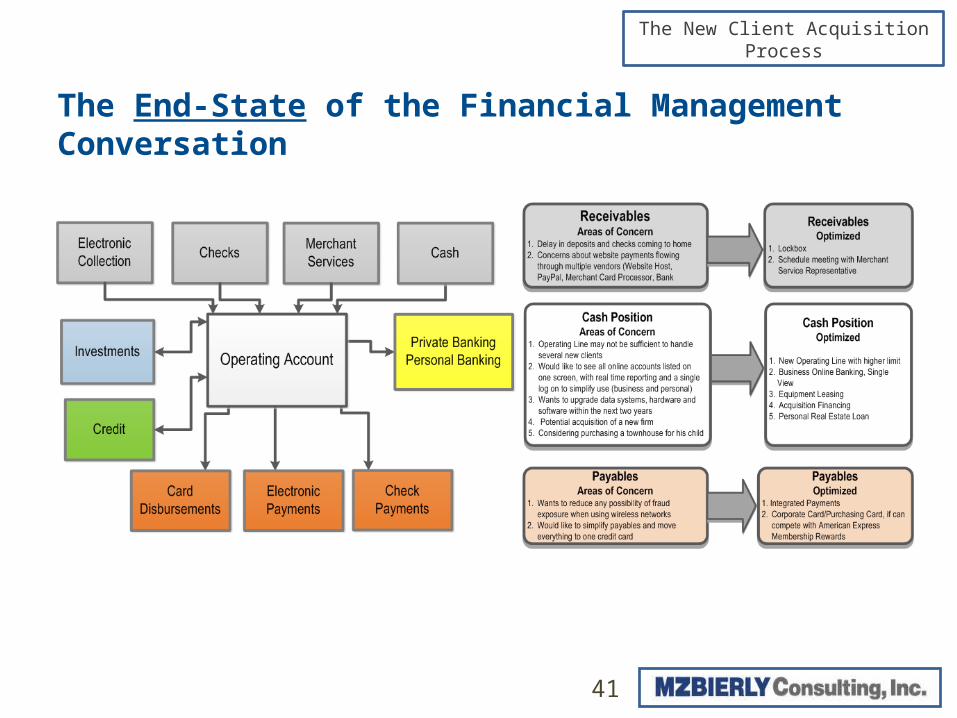

The End-State of the Financial Management Conversation

41

The New Client Acquisition Process

If you can answer these questions in detail you completed successfully the Financial Conversation.

1. Describe the process the Owner uses to manage his invoicing and receivables process. Starting with the largest customer segment down to the smallest.

2. Describe the process the Owner uses to manage his expenses and payables process. Starting with his largest expenses and down to his smallest.

3. Describe the process he uses to manage his cash position on a day-to-day basis.

4. Describe what he does when he has too much cash.

5. Describe what he does when he has too little cash.

6. Describe what he does to take money out of the business, say for a shareholder distribution.

7. What were the recurring themes that you heard, for example, convenience, security?

8. What were the un-optimized areas that you uncovered and confirmed with Owner?

9. Did you get agreement to a next meeting to present “Optimized Ideas”?

After the Call, What Did You Learn from the “Financial Management Conversation”

42

The New Client Acquisition Process

The Third Critical Discussion with “Prospects”

43

The Optimization Conversation

[Optional] Introduction Meeting

1. Business Opportunities, Business Challenges Discussion

2. Financial Management Process Discussion

3. Recommendations for Optimizing Changing Financial Management Processes

4. Follow-up on Optimizing Recommendations

5. Follow-up on mid-term and long-term Financial Management Process Changes

The New Client Acquisition Process

1. Using the Financial Management Map you reviewed with the Decision Maker, update the Map with the not-optimized processes you agreed on.

2. Determine if and how you can add value to this business’s current cash cycle (review with your Business Partners too).

3. Create an Optimized Map that you will present to the Decision Maker. Include the following:

• The product/service name (next to the appropriate box).

• “Flow lines” that show how it will “hook” together.

• An estimate of the costs/fees on a monthly basis for the optimized elements.

4. Create a statement that shows how your total solution matches the “intangible needs” of the Decision Maker.

Preparing for the “Optimized Solutions” Conversation

44

The New Client Acquisition Process

45

Product Solutions Sit below Financial Processes

Financial Management Processes use Products to optimize some element of those processes

Cash Position [Operating Account]

• IB Checking• NIB

Checking• Data

Services• Imaging

Services• Information

Reporting

Receivables

• Cash Concentration

• Cashiering• Image

Deposits• Lockbox

Services

Payables

• ACH Services

• Controlled Disbursement

• Integrated Payables

• Payroll • Wire

Too Little Cash[Credit]

• ABL• Commercial

Card• Credit Card• Credit

Sweep• CRE Loan• Lease• Revolver/

LOC• Standby

Letter of Credit

• Syndication (Lead)

• Trade Finance

• Term Loan

Too Much Cash[Investments]

• Asset Management

• CD• Corporate

Trust/Escrow

• Custody• Endowment

s & Foundations

• 401(k) Plans

• Investment Sweep

• Money Market

• Savings

RiskMitigation

• Derivatives• FX• Fraud

Protection• Insurance• Letter of

Credit• Reconcilem

ent Services• Trade

Services

Personal Banking

• Personal Investments

• Personal Trust*

• PB Deposits• PB Loans• Consumer

Solutions*• HELO

AN• HELO

C• Mortg

age• Other

Loans• Chec

king• Savin

gs

The New Client Acquisition Process

46

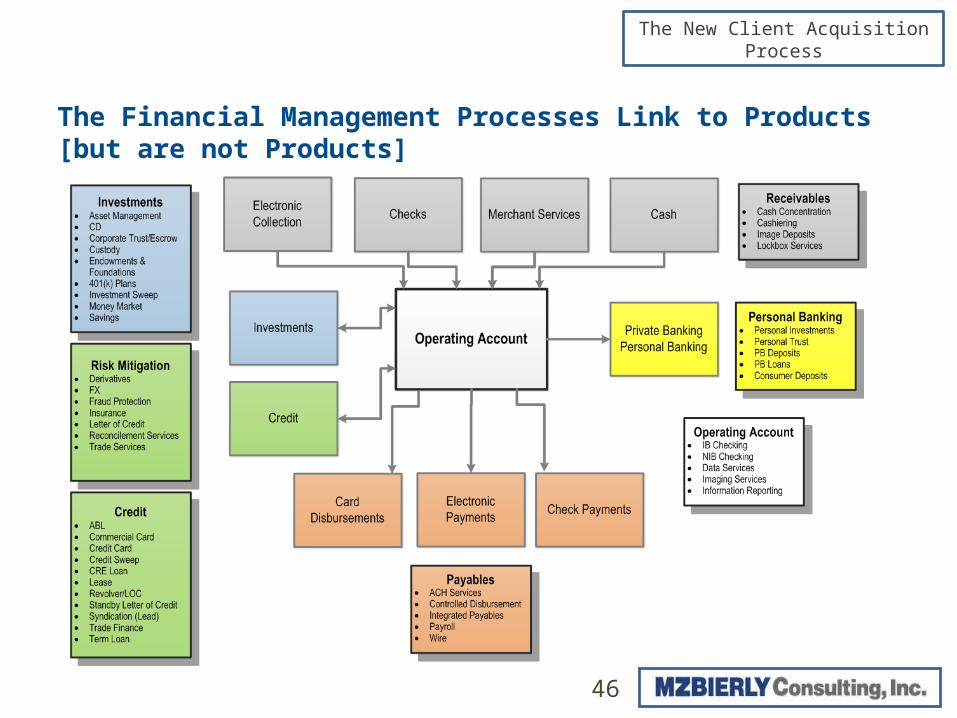

The Financial Management Processes Link to Products [but are not Products]

The New Client Acquisition Process

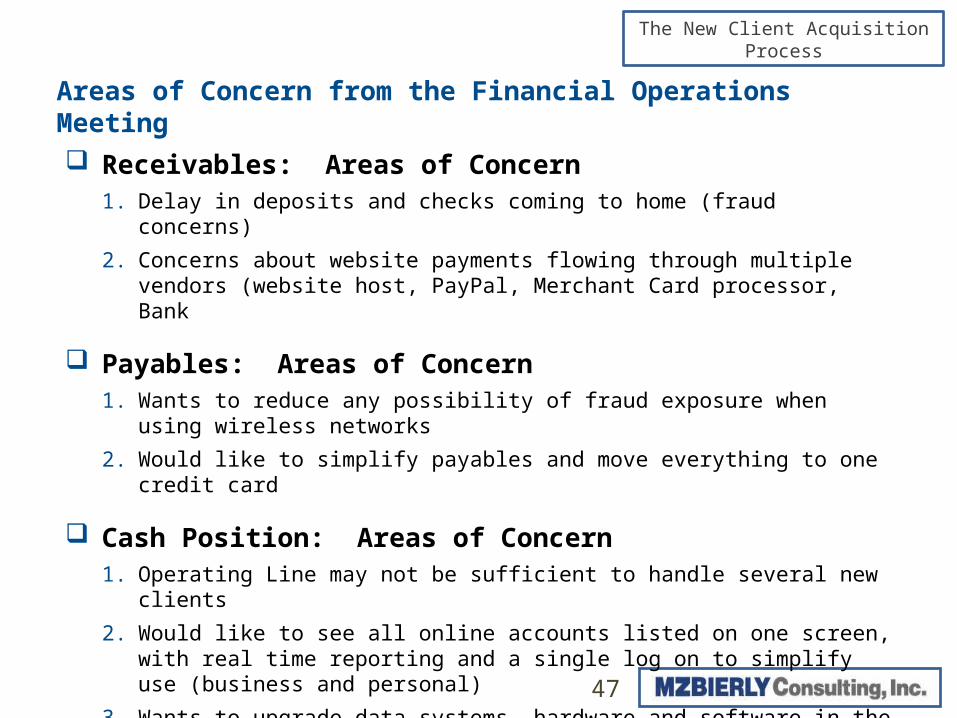

Receivables: Areas of Concern1. Delay in deposits and checks coming to home (fraud concerns)

2. Concerns about website payments flowing through multiple vendors (website host, PayPal, Merchant Card processor, Bank

Payables: Areas of Concern1. Wants to reduce any possibility of fraud exposure when using wireless networks

2. Would like to simplify payables and move everything to one credit card

Cash Position: Areas of Concern1. Operating Line may not be sufficient to handle several new clients

2. Would like to see all online accounts listed on one screen, with real time reporting and a single log on to simplify use (business and personal)

3. Wants to upgrade data systems, hardware and software in the next two years

4. Potential acquisition of a new firm

5. Considering purchasing a townhouse for his son in next 6 months

Areas of Concern from the Financial Operations Meeting

47

The New Client Acquisition Process

48

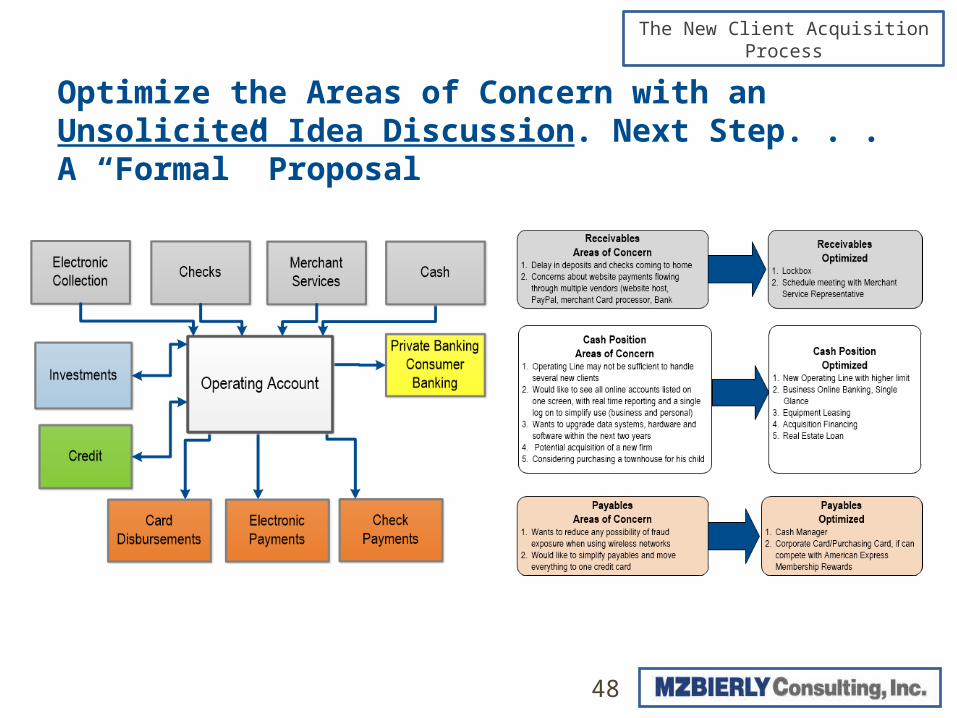

Optimize the Areas of Concern with an Unsolicited Idea Discussion. Next Step. . . A “Formal” Proposal

![Wayfair Client Letter FINAL DRAFT 2018 June 27 v1[1]kinseycp/files/Wayfair-Client-Letter.pdf · Microsoft Word - Wayfair Client Letter FINAL DRAFT 2018 June 27 v1[1].docx Created](https://img.pdfslide.us/doc/110x75/603e41c66c5c67229e001f06/wayfair-client-letter-final-draft-2018-june-27-v11-kinseycpfileswayfair-client-letterpdf.jpg)

![[hal-00911765, v1] Les big data et la relation client](https://img.pdfslide.us/doc/110x75/617e76ae35207920726b691e/hal-00911765-v1-les-big-data-et-la-relation-client.jpg)