Embed Size (px)

Citation preview

Date: 28-11-2017

NCML Commodity Market Monitor

HOME

NCoMM

NCML COMMODITY MARKET MONITOR

Cotton | Sugar | Soybean | RM Seed | Castor seed | Turmeric | Jeera

OUTLOOK

OTHER DATA Sowing progress | Advance estimates | Kharif and rabi MSP

WEEKLY ONLINE QUIZ

Click on the link above to participate

Participate in our weekly quiz and get a chance to win Amazon gift coupons. Winners will be announced in next report and rewarded.

Date: 28-11-2017

NCML Commodity Market Monitor

s

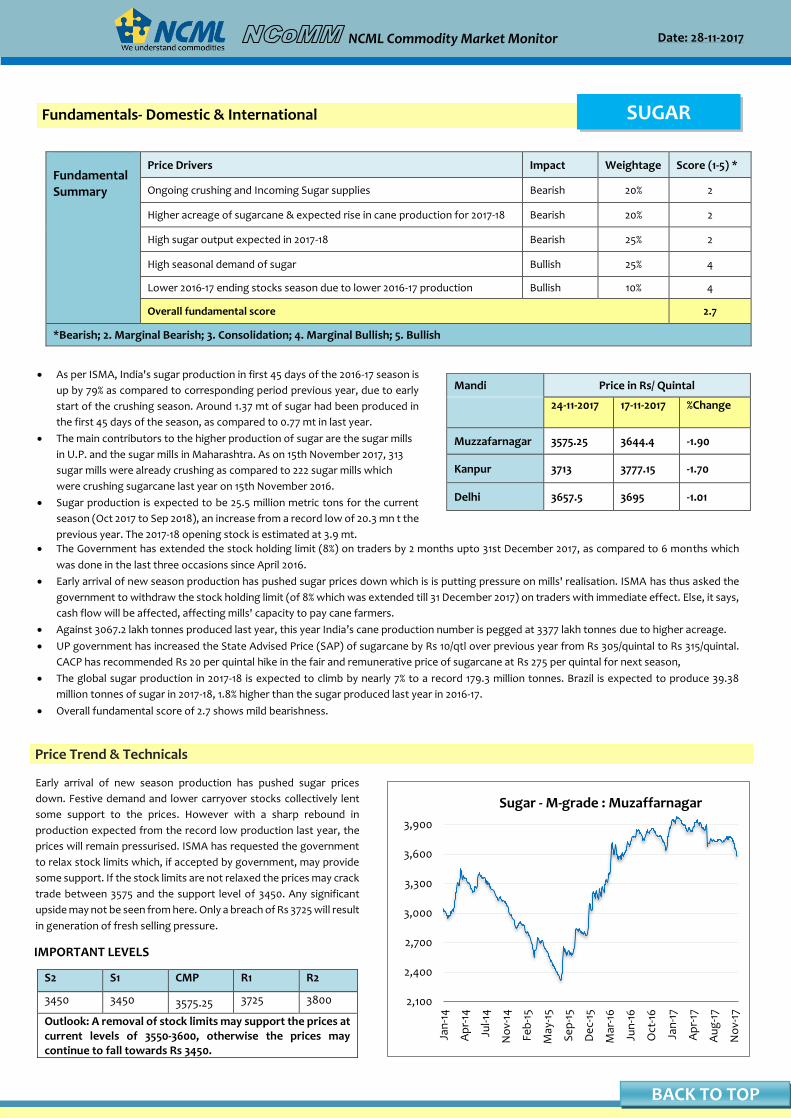

Price Trend & Technicals

Early arrival of new season production has pushed sugar prices

down. Festive demand and lower carryover stocks collectively lent

some support to the prices. However with a sharp rebound in

production expected from the record low production last year, the

prices will remain pressurised. ISMA has requested the government

to relax stock limits which, if accepted by government, may provide

some support. If the stock limits are not relaxed the prices may crack

trade between 3575 and the support level of 3450. Any significant

upside may not be seen from here. Only a breach of Rs 3725 will result

in generation of fresh selling pressure.

IMPORTANT LEVELS

• As per ISMA, India's sugar production in first 45 days of the 2016-17 season is

up by 79% as compared to corresponding period previous year, due to early

start of the crushing season. Around 1.37 mt of sugar had been produced in

the first 45 days of the season, as compared to 0.77 mt in last year.

• The main contributors to the higher production of sugar are the sugar mills

in U.P. and the sugar mills in Maharashtra. As on 15th November 2017, 313

sugar mills were already crushing as compared to 222 sugar mills which

were crushing sugarcane last year on 15th November 2016.

• Sugar production is expected to be 25.5 million metric tons for the current

season (Oct 2017 to Sep 2018), an increase from a record low of 20.3 mn t the

previous year. The 2017-18 opening stock is estimated at 3.9 mt.

•

Mandi Price in Rs/ Quintal

24-11-2017 17-11-2017 %Change

Muzzafarnagar 3575.25 3644.4 -1.90

Kanpur 3713 3777.15 -1.70

Delhi 3657.5 3695 -1.01

• The Government has extended the stock holding limit (8%) on traders by 2 months upto 31st December 2017, as compared to 6 months which

was done in the last three occasions since April 2016.

• Early arrival of new season production has pushed sugar prices down which is is putting pressure on mills' realisation. ISMA has thus asked the

government to withdraw the stock holding limit (of 8% which was extended till 31 December 2017) on traders with immediate effect. Else, it says,

cash flow will be affected, affecting mills' capacity to pay cane farmers.

• Against 3067.2 lakh tonnes produced last year, this year India’s cane production number is pegged at 3377 lakh tonnes due to higher acreage.

• UP government has increased the State Advised Price (SAP) of sugarcane by Rs 10/qtl over previous year from Rs 305/quintal to Rs 315/quintal.

CACP has recommended Rs 20 per quintal hike in the fair and remunerative price of sugarcane at Rs 275 per quintal for next season,

• The global sugar production in 2017-18 is expected to climb by nearly 7% to a record 179.3 million tonnes. Brazil is expected to produce 39.38

million tonnes of sugar in 2017-18, 1.8% higher than the sugar produced last year in 2016-17.

• Overall fundamental score of 2.7 shows mild bearishness.

BACK TO TOP

S2 S1 CMP R1 R2

3450 3450 3575.25 3725 3800

Outlook: A removal of stock limits may support the prices at current levels of 3550-3600, otherwise the prices may continue to fall towards Rs 3450.

2,100

2,400

2,700

3,000

3,300

3,600

3,900

Jan

-14

Ap

r-14

Jul-1

4

No

v-14

Feb

-15

May

-15

Se

p-1

5

De

c-15

Mar

-16

Jun

-16

Oct

-16

Jan

-17

Ap

r-17

Au

g-1

7

No

v-17

Sugar - M-grade : Muzaffarnagar

Fundamental Summary

Price Drivers Impact Weightage Score (1-5) *

Ongoing crushing and Incoming Sugar supplies Bearish 20% 2

Higher acreage of sugarcane & expected rise in cane production for 2017-18 Bearish 20% 2

High sugar output expected in 2017-18 Bearish 25% 2

High seasonal demand of sugar Bullish 25% 4

Lower 2016-17 ending stocks season due to lower 2016-17 production Bullish 10% 4

Overall fundamental score 2.7

*Bearish; 2. Marginal Bearish; 3. Consolidation; 4. Marginal Bullish; 5. Bullish

Fundamentals- Domestic & International

Mandi Price in Rs/ Quintal

02-06-2017 26-05-2017 %Change

Muzzafarnagar 3915 3892.5 0.58

Kolhapur 3837 3847.5 -0.27

Delhi 3932.55 3920 0.32

Fundamentals- Domestic & International

SUGAR

Date: 28-11-2017

NCML Commodity Market Monitor

Fundamentals- Domestic & International

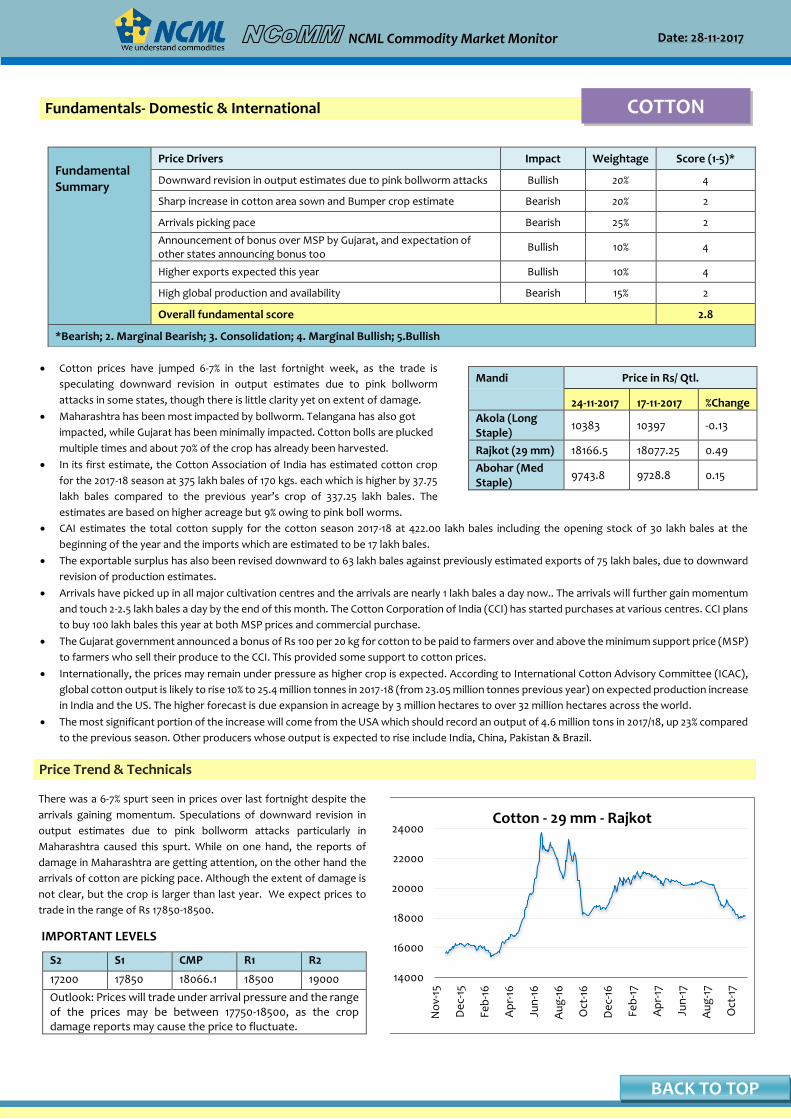

Price Trend & Technicals

14000

16000

18000

20000

22000

24000

No

v-15

De

c-15

Feb

-16

Ap

r-16

Jun

-16

Au

g-1

6

Oct

-16

De

c-16

Feb

-17

Ap

r-17

Jun

-17

Au

g-1

7

Oct

-17

Cotton - 29 mm - Rajkot

COTTON

There was a 6-7% spurt seen in prices over last fortnight despite the

arrivals gaining momentum. Speculations of downward revision in

output estimates due to pink bollworm attacks particularly in

Maharashtra caused this spurt. While on one hand, the reports of

damage in Maharashtra are getting attention, on the other hand the

arrivals of cotton are picking pace. Although the extent of damage is

not clear, but the crop is larger than last year. We expect prices to

trade in the range of Rs 17850-18500.

IMPORTANT LEVELS

S2 S1 CMP R1 R2

17200 17850 18066.1 18500 19000

Outlook: Prices will trade under arrival pressure and the range of the prices may be between 17750-18500, as the crop damage reports may cause the price to fluctuate.

• CAI estimates the total cotton supply for the cotton season 2017-18 at 422.00 lakh bales including the opening stock of 30 lakh bales at the

beginning of the year and the imports which are estimated to be 17 lakh bales.

• The exportable surplus has also been revised downward to 63 lakh bales against previously estimated exports of 75 lakh bales, due to downward

revision of production estimates.

• Arrivals have picked up in all major cultivation centres and the arrivals are nearly 1 lakh bales a day now.. The arrivals will further gain momentum

and touch 2-2.5 lakh bales a day by the end of this month. The Cotton Corporation of India (CCI) has started purchases at various centres. CCI plans

to buy 100 lakh bales this year at both MSP prices and commercial purchase.

• The Gujarat government announced a bonus of Rs 100 per 20 kg for cotton to be paid to farmers over and above the minimum support price (MSP)

to farmers who sell their produce to the CCI. This provided some support to cotton prices.

• Internationally, the prices may remain under pressure as higher crop is expected. According to International Cotton Advisory Committee (ICAC),

global cotton output is likely to rise 10% to 25.4 million tonnes in 2017-18 (from 23.05 million tonnes previous year) on expected production increase

in India and the US. The higher forecast is due expansion in acreage by 3 million hectares to over 32 million hectares across the world.

• The most significant portion of the increase will come from the USA which should record an output of 4.6 million tons in 2017/18, up 23% compared

to the previous season. Other producers whose output is expected to rise include India, China, Pakistan & Brazil.

Fundamental Summary

Price Drivers Impact Weightage Score (1-5)*

Downward revision in output estimates due to pink bollworm attacks Bullish 20% 4

Sharp increase in cotton area sown and Bumper crop estimate Bearish 20% 2

Arrivals picking pace Bearish 25% 2

Announcement of bonus over MSP by Gujarat, and expectation of other states announcing bonus too

Bullish 10% 4

Higher exports expected this year Bullish 10% 4

High global production and availability Bearish 15% 2

Overall fundamental score 2.8

*Bearish; 2. Marginal Bearish; 3. Consolidation; 4. Marginal Bullish; 5.Bullish

• Cotton prices have jumped 6-7% in the last fortnight week, as the trade is

speculating downward revision in output estimates due to pink bollworm

attacks in some states, though there is little clarity yet on extent of damage.

• Maharashtra has been most impacted by bollworm. Telangana has also got

impacted, while Gujarat has been minimally impacted. Cotton bolls are plucked

multiple times and about 70% of the crop has already been harvested.

• In its first estimate, the Cotton Association of India has estimated cotton crop

for the 2017-18 season at 375 lakh bales of 170 kgs. each which is higher by 37.75

lakh bales compared to the previous year’s crop of 337.25 lakh bales. The

estimates are based on higher acreage but 9% owing to pink boll worms.

BACK TO TOP

Mandi Price in Rs/ Qtl.

24-11-2017 17-11-2017 %Change

Akola (Long Staple)

10383 10397 -0.13

Rajkot (29 mm) 18166.5 18077.25 0.49

Abohar (Med Staple)

9743.8 9728.8 0.15

Date: 28-11-2017

NCML Commodity Market Monitor

Price Trend & Technicals

2700

2930

3160

3390

3620

3850

4080

4310

Feb

-15

May

-15

Au

g-1

5

De

c-15

Mar

-16

Jul-1

6

Oct

-16

Jan

-17

May

-17

Au

g-1

7

No

v-17

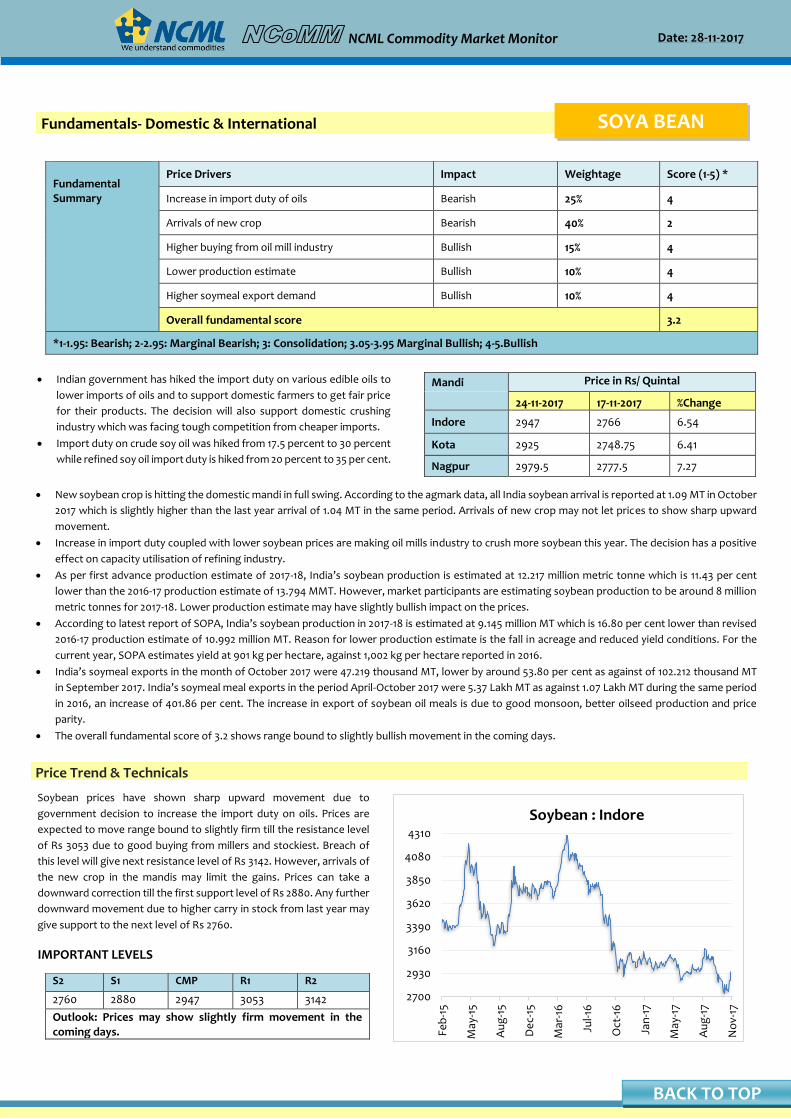

Soybean : IndoreSoybean prices have shown sharp upward movement due to

government decision to increase the import duty on oils. Prices are

expected to move range bound to slightly firm till the resistance level

of Rs 3053 due to good buying from millers and stockiest. Breach of

this level will give next resistance level of Rs 3142. However, arrivals of

the new crop in the mandis may limit the gains. Prices can take a

downward correction till the first support level of Rs 2880. Any further

downward movement due to higher carry in stock from last year may

give support to the next level of Rs 2760.

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2760 2880 2947 3053 3142

Outlook: Prices may show slightly firm movement in the coming days.

• Indian government has hiked the import duty on various edible oils to

lower imports of oils and to support domestic farmers to get fair price

for their products. The decision will also support domestic crushing

industry which was facing tough competition from cheaper imports.

• Import duty on crude soy oil was hiked from 17.5 percent to 30 percent

while refined soy oil import duty is hiked from 20 percent to 35 per cent.

Mandi Price in Rs/ Quintal

24-11-2017 17-11-2017 %Change

Indore 2947 2766 6.54

Kota 2925 2748.75 6.41

Nagpur 2979.5 2777.5 7.27

• New soybean crop is hitting the domestic mandi in full swing. According to the agmark data, all India soybean arrival is reported at 1.09 MT in October

2017 which is slightly higher than the last year arrival of 1.04 MT in the same period. Arrivals of new crop may not let prices to show sharp upward

movement.

• Increase in import duty coupled with lower soybean prices are making oil mills industry to crush more soybean this year. The decision has a positive

effect on capacity utilisation of refining industry.

• As per first advance production estimate of 2017-18, India’s soybean production is estimated at 12.217 million metric tonne which is 11.43 per cent

lower than the 2016-17 production estimate of 13.794 MMT. However, market participants are estimating soybean production to be around 8 million

metric tonnes for 2017-18. Lower production estimate may have slightly bullish impact on the prices.

• According to latest report of SOPA, India’s soybean production in 2017-18 is estimated at 9.145 million MT which is 16.80 per cent lower than revised

2016-17 production estimate of 10.992 million MT. Reason for lower production estimate is the fall in acreage and reduced yield conditions. For the

current year, SOPA estimates yield at 901 kg per hectare, against 1,002 kg per hectare reported in 2016.

• India’s soymeal exports in the month of October 2017 were 47.219 thousand MT, lower by around 53.80 per cent as against of 102.212 thousand MT

in September 2017. India’s soymeal meal exports in the period April-October 2017 were 5.37 Lakh MT as against 1.07 Lakh MT during the same period

in 2016, an increase of 401.86 per cent. The increase in export of soybean oil meals is due to good monsoon, better oilseed production and price

parity.

• The overall fundamental score of 3.2 shows range bound to slightly bullish movement in the coming days.

Fundamental Summary

Price Drivers Impact Weightage Score (1-5) *

Increase in import duty of oils Bearish 25% 4

Arrivals of new crop Bearish 40% 2

Higher buying from oil mill industry Bullish 15% 4

Lower production estimate Bullish 10% 4

Higher soymeal export demand Bullish 10% 4

Overall fundamental score 3.2

*1-1.95: Bearish; 2-2.95: Marginal Bearish; 3: Consolidation; 3.05-3.95 Marginal Bullish; 4-5.Bullish

Fundamentals- Domestic & International SOYA BEAN

BACK TO TOP

Date: 28-11-2017

NCML Commodity Market Monitor

Price Trend &Technicals

3,500

3,750

4,000

4,250

4,500

4,750

5,000

5,250

Jun

-15

Au

g-1

5

Oct

-15

De

c-15

Feb

-16

May

-16

Jul-1

6

Se

p-1

6

No

v-16

Jan

-17

Ap

r-17

Jun

-17

Au

g-1

7

Oct

-17

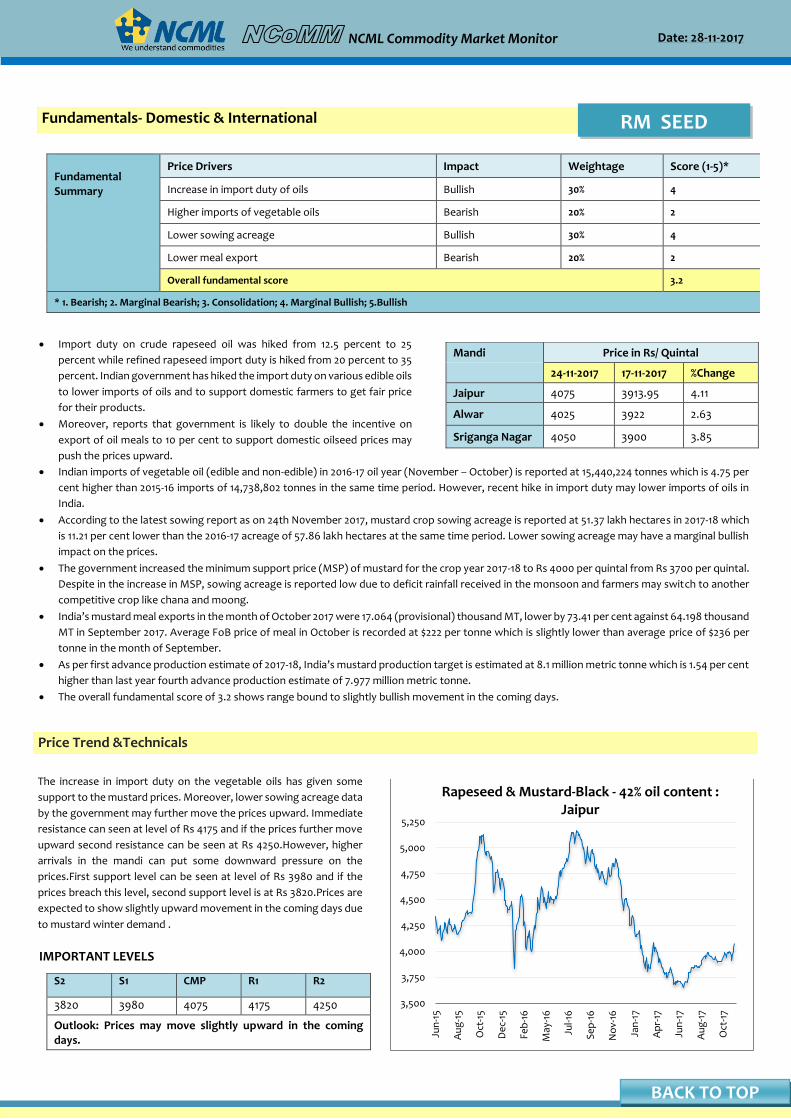

Rapeseed & Mustard-Black - 42% oil content : Jaipur

The increase in import duty on the vegetable oils has given some

support to the mustard prices. Moreover, lower sowing acreage data

by the government may further move the prices upward. Immediate

resistance can seen at level of Rs 4175 and if the prices further move

upward second resistance can be seen at Rs 4250.However, higher

arrivals in the mandi can put some downward pressure on the

prices.First support level can be seen at level of Rs 3980 and if the

prices breach this level, second support level is at Rs 3820.Prices are

expected to show slightly upward movement in the coming days due

to mustard winter demand .

IMPORTANT LEVELS

S2 S1 CMP R1 R2

3820 3980 4075 4175 4250

Outlook: Prices may move slightly upward in the coming days.

• Import duty on crude rapeseed oil was hiked from 12.5 percent to 25

percent while refined rapeseed import duty is hiked from 20 percent to 35

percent. Indian government has hiked the import duty on various edible oils

to lower imports of oils and to support domestic farmers to get fair price

for their products.

• Moreover, reports that government is likely to double the incentive on

export of oil meals to 10 per cent to support domestic oilseed prices may

push the prices upward.

•

Mandi Price in Rs/ Quintal

24-11-2017 17-11-2017 %Change

Jaipur 4075 3913.95 4.11

Alwar 4025 3922 2.63

Sriganga Nagar 4050 3900 3.85

• Indian imports of vegetable oil (edible and non-edible) in 2016-17 oil year (November – October) is reported at 15,440,224 tonnes which is 4.75 per

cent higher than 2015-16 imports of 14,738,802 tonnes in the same time period. However, recent hike in import duty may lower imports of oils in

India.

• According to the latest sowing report as on 24th N0vember 2017, mustard crop sowing acreage is reported at 51.37 lakh hectares in 2017-18 which

is 11.21 per cent lower than the 2016-17 acreage of 57.86 lakh hectares at the same time period. Lower sowing acreage may have a marginal bullish

impact on the prices.

• The government increased the minimum support price (MSP) of mustard for the crop year 2017-18 to Rs 4000 per quintal from Rs 3700 per quintal.

Despite in the increase in MSP, sowing acreage is reported low due to deficit rainfall received in the monsoon and farmers may switch to another

competitive crop like chana and moong.

• India’s mustard meal exports in the month of October 2017 were 17.064 (provisional) thousand MT, lower by 73.41 per cent against 64.198 thousand

MT in September 2017. Average FoB price of meal in October is recorded at $222 per tonne which is slightly lower than average price of $236 per

tonne in the month of September.

• As per first advance production estimate of 2017-18, India’s mustard production target is estimated at 8.1 million metric tonne which is 1.54 per cent

higher than last year fourth advance production estimate of 7.977 million metric tonne.

• The overall fundamental score of 3.2 shows range bound to slightly bullish movement in the coming days.

•

Fundamental Summary

Price Drivers Impact Weightage Score (1-5)*

Increase in import duty of oils Bullish 30% 4

Higher imports of vegetable oils Bearish 20% 2

Lower sowing acreage Bullish 30% 4

Lower meal export Bearish 20% 2

Overall fundamental score 3.2

* 1. Bearish; 2. Marginal Bearish; 3. Consolidation; 4. Marginal Bullish; 5.Bullish

Fundamentals- Domestic & International RM SEED

BACK TO TOP

Date: 28-11-2017

NCML Commodity Market Monitor

Fundamentals- Domestic & International

Price Trend &Technicals

2800

3050

3300

3550

3800

4050

4300

4550

4800

Jan

-15

Ap

r-15

Jul-1

5

Oct

-15

Jan

-16

Mar

-16

Jun

-16

Se

p-1

6

De

c-16

Mar

-17

May

-17

Au

g-1

7

No

v-17

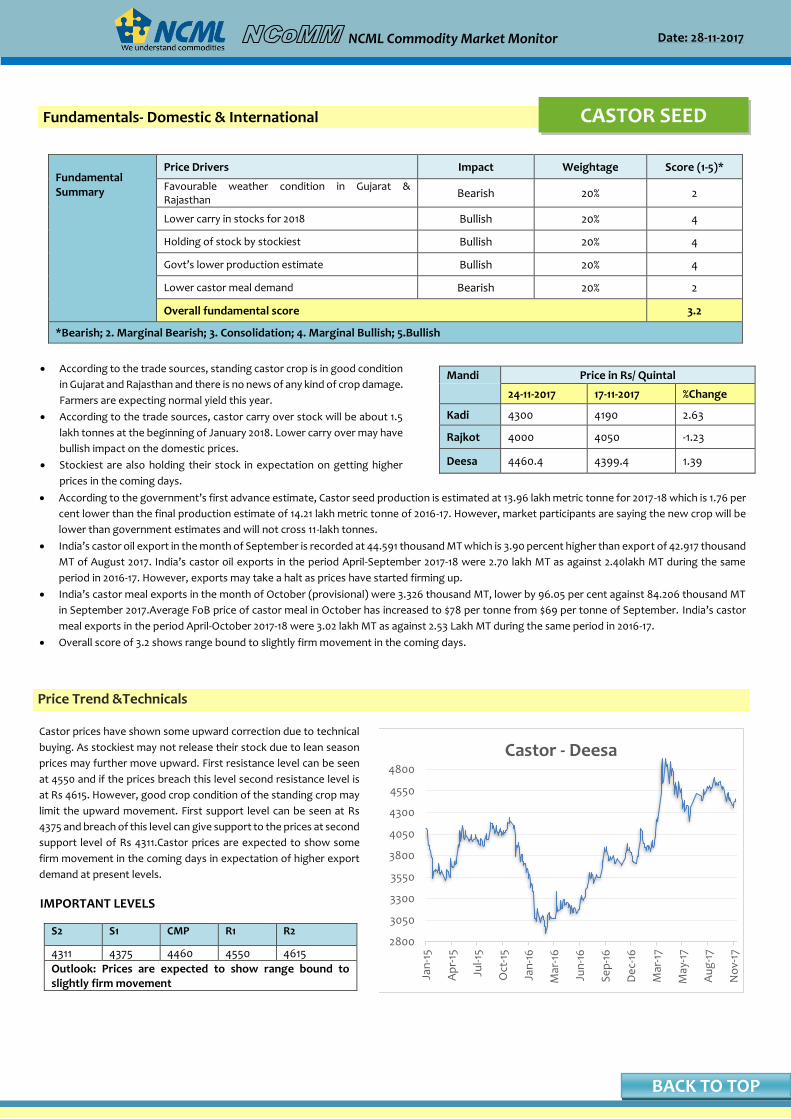

Castor - Deesa

CASTOR SEED

Castor prices have shown some upward correction due to technical

buying. As stockiest may not release their stock due to lean season

prices may further move upward. First resistance level can be seen

at 4550 and if the prices breach this level second resistance level is

at Rs 4615. However, good crop condition of the standing crop may

limit the upward movement. First support level can be seen at Rs

4375 and breach of this level can give support to the prices at second

support level of Rs 4311.Castor prices are expected to show some

firm movement in the coming days in expectation of higher export

demand at present levels.

IMPORTANT LEVELS

S2 S1 CMP R1 R2

4311 4375 4460 4550 4615

Outlook: Prices are expected to show range bound to slightly firm movement

• According to the trade sources, standing castor crop is in good condition

in Gujarat and Rajasthan and there is no news of any kind of crop damage.

Farmers are expecting normal yield this year.

• According to the trade sources, castor carry over stock will be about 1.5

lakh tonnes at the beginning of January 2018. Lower carry over may have

bullish impact on the domestic prices.

• Stockiest are also holding their stock in expectation on getting higher

prices in the coming days.

Mandi Price in Rs/ Quintal

24-11-2017 17-11-2017 %Change

Kadi 4300 4190 2.63

Rajkot 4000 4050 -1.23

Deesa 4460.4 4399.4 1.39

• According to the government’s first advance estimate, Castor seed production is estimated at 13.96 lakh metric tonne for 2017-18 which is 1.76 per

cent lower than the final production estimate of 14.21 lakh metric tonne of 2016-17. However, market participants are saying the new crop will be

lower than government estimates and will not cross 11-lakh tonnes.

• India’s castor oil export in the month of September is recorded at 44.591 thousand MT which is 3.90 percent higher than export of 42.917 thousand

MT of August 2017. India’s castor oil exports in the period April-September 2017-18 were 2.70 lakh MT as against 2.40lakh MT during the same

period in 2016-17. However, exports may take a halt as prices have started firming up.

• India’s castor meal exports in the month of October (provisional) were 3.326 thousand MT, lower by 96.05 per cent against 84.206 thousand MT

in September 2017.Average FoB price of castor meal in October has increased to $78 per tonne from $69 per tonne of September. India’s castor

meal exports in the period April-October 2017-18 were 3.02 lakh MT as against 2.53 Lakh MT during the same period in 2016-17.

• Overall score of 3.2 shows range bound to slightly firm movement in the coming days.

Fundamental Summary

Price Drivers Impact Weightage Score (1-5)*

Favourable weather condition in Gujarat & Rajasthan

Bearish 20% 2

Lower carry in stocks for 2018 Bullish 20% 4

Holding of stock by stockiest Bullish 20% 4

Govt’s lower production estimate Bullish 20% 4

Lower castor meal demand Bearish 20% 2

Overall fundamental score 3.2

*Bearish; 2. Marginal Bearish; 3. Consolidation; 4. Marginal Bullish; 5.Bullish

BACK TO TOP

Date: 28-11-2017

NCML Commodity Market Monitor

x

Price Trend &Technicals

16,500.00

17,000.00

17,500.00

18,000.00

18,500.00

19,000.00

19,500.00

20,000.00

20,500.00

21,000.00

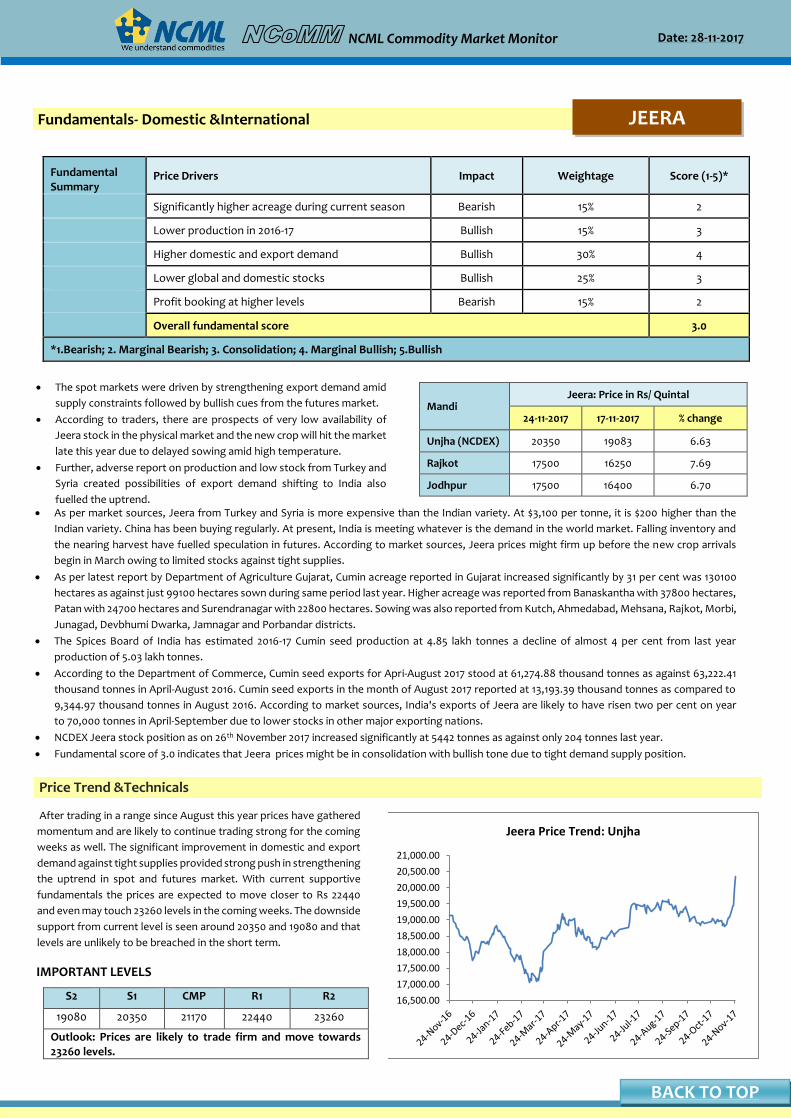

Jeera Price Trend: Unjha After trading in a range since August this year prices have gathered

momentum and are likely to continue trading strong for the coming

weeks as well. The significant improvement in domestic and export

demand against tight supplies provided strong push in strengthening

the uptrend in spot and futures market. With current supportive

fundamentals the prices are expected to move closer to Rs 22440

and even may touch 23260 levels in the coming weeks. The downside

support from current level is seen around 20350 and 19080 and that

levels are unlikely to be breached in the short term.

IMPORTANT LEVELS

S2 S1 CMP R1 R2

19080 20350 21170 22440 23260

Outlook: Prices are likely to trade firm and move towards 23260 levels.

• The spot markets were driven by strengthening export demand amid

supply constraints followed by bullish cues from the futures market.

• According to traders, there are prospects of very low availability of

Jeera stock in the physical market and the new crop will hit the market

late this year due to delayed sowing amid high temperature.

• Further, adverse report on production and low stock from Turkey and

Syria created possibilities of export demand shifting to India also

fuelled the uptrend.

Mandi Jeera: Price in Rs/ Quintal

24-11-2017 17-11-2017 % change

Unjha (NCDEX) 20350 19083 6.63

Rajkot 17500 16250 7.69

Jodhpur 17500 16400 6.70

• As per market sources, Jeera from Turkey and Syria is more expensive than the Indian variety. At $3,100 per tonne, it is $200 higher than the

Indian variety. China has been buying regularly. At present, India is meeting whatever is the demand in the world market. Falling inventory and

the nearing harvest have fuelled speculation in futures. According to market sources, Jeera prices might firm up before the new crop arrivals

begin in March owing to limited stocks against tight supplies.

• As per latest report by Department of Agriculture Gujarat, Cumin acreage reported in Gujarat increased significantly by 31 per cent was 130100

hectares as against just 99100 hectares sown during same period last year. Higher acreage was reported from Banaskantha with 37800 hectares,

Patan with 24700 hectares and Surendranagar with 22800 hectares. Sowing was also reported from Kutch, Ahmedabad, Mehsana, Rajkot, Morbi,

Junagad, Devbhumi Dwarka, Jamnagar and Porbandar districts.

• The Spices Board of India has estimated 2016-17 Cumin seed production at 4.85 lakh tonnes a decline of almost 4 per cent from last year

production of 5.03 lakh tonnes.

• According to the Department of Commerce, Cumin seed exports for Apri-August 2017 stood at 61,274.88 thousand tonnes as against 63,222.41

thousand tonnes in April-August 2016. Cumin seed exports in the month of August 2017 reported at 13,193.39 thousand tonnes as compared to

9,344.97 thousand tonnes in August 2016. According to market sources, India's exports of Jeera are likely to have risen two per cent on year

to 70,000 tonnes in April-September due to lower stocks in other major exporting nations.

• NCDEX Jeera stock position as on 26th November 2017 increased significantly at 5442 tonnes as against only 204 tonnes last year.

• Fundamental score of 3.0 indicates that Jeera prices might be in consolidation with bullish tone due to tight demand supply position.

Fundamental Summary

Price Drivers Impact Weightage Score (1-5)*

Significantly higher acreage during current season Bearish 15% 2

Lower production in 2016-17 Bullish 15% 3

Higher domestic and export demand Bullish 30% 4

Lower global and domestic stocks Bullish 25% 3

Profit booking at higher levels Bearish 15% 2

Overall fundamental score 3.0

*1.Bearish; 2. Marginal Bearish; 3. Consolidation; 4. Marginal Bullish; 5.Bullish

Fundamentals- Domestic &International JEERA

BACK TO TOP

Date: 28-11-2017

NCML Commodity Market Monitor

Price Trend &Technicals

4,500.00

5,000.00

5,500.00

6,000.00

6,500.00

7,000.00

7,500.00

8,000.00

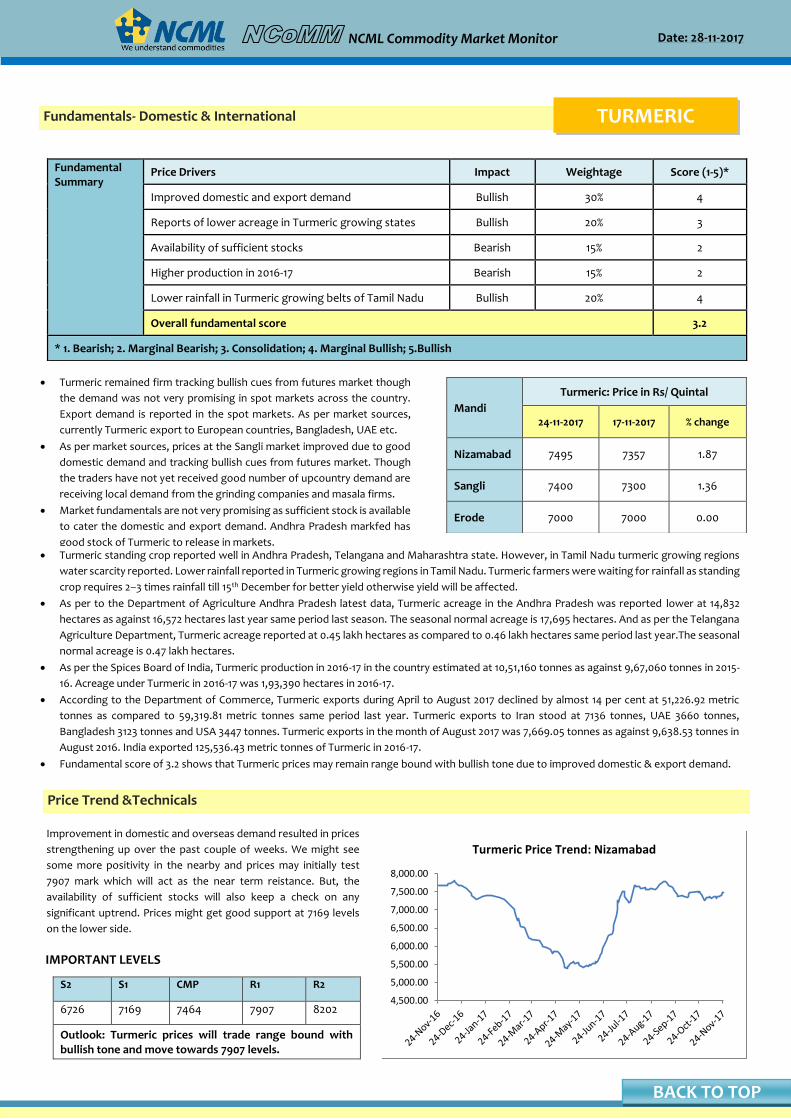

Turmeric Price Trend: NizamabadImprovement in domestic and overseas demand resulted in prices

strengthening up over the past couple of weeks. We might see

some more positivity in the nearby and prices may initially test

7907 mark which will act as the near term reistance. But, the

availability of sufficient stocks will also keep a check on any

significant uptrend. Prices might get good support at 7169 levels

on the lower side.

IMPORTANT LEVELS

S2 S1 CMP R1 R2

6726 7169 7464 7907 8202

Outlook: Turmeric prices will trade range bound with bullish tone and move towards 7907 levels.

Fundamentals- Domestic & International TURMERIC

• Turmeric remained firm tracking bullish cues from futures market though

the demand was not very promising in spot markets across the country.

Export demand is reported in the spot markets. As per market sources,

currently Turmeric export to European countries, Bangladesh, UAE etc.

• As per market sources, prices at the Sangli market improved due to good

domestic demand and tracking bullish cues from futures market. Though

the traders have not yet received good number of upcountry demand are

receiving local demand from the grinding companies and masala firms.

• Market fundamentals are not very promising as sufficient stock is available

to cater the domestic and export demand. Andhra Pradesh markfed has

good stock of Turmeric to release in markets.

Mandi

Turmeric: Price in Rs/ Quintal

24-11-2017 17-11-2017 % change

Nizamabad 7495 7357 1.87

Sangli 7400 7300 1.36

Erode 7000 7000 0.00

• Turmeric standing crop reported well in Andhra Pradesh, Telangana and Maharashtra state. However, in Tamil Nadu turmeric growing regions

water scarcity reported. Lower rainfall reported in Turmeric growing regions in Tamil Nadu. Turmeric farmers were waiting for rainfall as standing

crop requires 2–3 times rainfall till 15th December for better yield otherwise yield will be affected.

• As per to the Department of Agriculture Andhra Pradesh latest data, Turmeric acreage in the Andhra Pradesh was reported lower at 14,832

hectares as against 16,572 hectares last year same period last season. The seasonal normal acreage is 17,695 hectares. And as per the Telangana

Agriculture Department, Turmeric acreage reported at 0.45 lakh hectares as compared to 0.46 lakh hectares same period last year.The seasonal

normal acreage is 0.47 lakh hectares.

• As per the Spices Board of India, Turmeric production in 2016-17 in the country estimated at 10,51,160 tonnes as against 9,67,060 tonnes in 2015-

16. Acreage under Turmeric in 2016-17 was 1,93,390 hectares in 2016-17.

• According to the Department of Commerce, Turmeric exports during April to August 2017 declined by almost 14 per cent at 51,226.92 metric

tonnes as compared to 59,319.81 metric tonnes same period last year. Turmeric exports to Iran stood at 7136 tonnes, UAE 3660 tonnes,

Bangladesh 3123 tonnes and USA 3447 tonnes. Turmeric exports in the month of August 2017 was 7,669.05 tonnes as against 9,638.53 tonnes in

August 2016. India exported 125,536.43 metric tonnes of Turmeric in 2016-17.

• Fundamental score of 3.2 shows that Turmeric prices may remain range bound with bullish tone due to improved domestic & export demand.

Fundamental Summary

Price Drivers Impact Weightage Score (1-5)*

Improved domestic and export demand Bullish 30% 4

Reports of lower acreage in Turmeric growing states Bullish 20% 3

Availability of sufficient stocks Bearish 15% 2

Higher production in 2016-17 Bearish 15% 2

Lower rainfall in Turmeric growing belts of Tamil Nadu Bullish 20% 4

Overall fundamental score 3.2

* 1. Bearish; 2. Marginal Bearish; 3. Consolidation; 4. Marginal Bullish; 5.Bullish

BACK TO TOP

Date: 28-11-2017

NCML Commodity Market Monitor

• Govt may scrap sugar stock limit to arrest price fall News Link

• India cotton exports to drop as pink bollworms eat crop News Link

• Sugar production till November 15 up by 79%: ISMA News Link

• Government to dispose of 5 lakh tons of pulses buffer stock by March News Link

• Farmers to reap Rs. 80 cr gain from oil palm duty hike News Link

• ISMA seeks easing of stock limit as sugar output rises News Link

• Commerce Ministry to address pepper growers’ woes on imports, prices News Link

• Cotton Seed Oilcake recovers from a vital long-term low News Link

• Maharashtra govt to sell tur dal at subsidised rates News Link

• Sugar prices down; mills want stock limits to be lifted News Link

• Rice prices climb on improved overseas demand, fresh crop supply caps gains News Link

• Farmers to reap Rs. 80 cr gain from oil palm duty hike News Link

• Pink bollworm tears into the very fibre of Maharashtra’s cotton growers News Link

• US crop deterioration helps wheat prices, but corn declines News Link

News corner

OFFICIAL PRODUCTION ESTIMATES

First advance estimates 2017-18 &

previous years’ estimates :

First Advance Estimates 2017-18

Link for commodity-wise and

market-wise prices and arrivals:

http://agmarknet.gov.in/PriceAndArrivals/

CommodityWiseDailyReport2.aspx

MSP in Rs /Qtl- Kharif 2017-18

Commodity 2016-17 2017-18

Paddy Common 1470 1550

paddy grade A 1510 1590

Jowar Hybrid 1625 1700

Jowar Maldandi 1650 1725

Bajra 1330 1425

Ragi 1725 1900

Maize 1365 1425

Tur 5050 5450*

Moong 5225 5575*

Urad 5000 5400*

Groundnut 4220 4450*

Sunflower seed 3950 4100 #

Soyabean black 2775 3050

Sesamum 5000 5300 #

Nigerseed 3825 4050 #

Cotton(Medium Staple) 3680 4020

Cotton(Long Staple) 4160 4320

MSP in Rs /Qtl- Rabi 2017-18

Commodity 2016-17 2017-18

Wheat 1625 1735

Barley 1325 1410

Gram 4000* 4400

Masur (Lentil) 3950* 4250

Rapeseed/Mustard 3700* 4000

Safflower 3700* 4100

Wheat 1625 1735

*includes bonus of Rs 200 per quintal

# includes bonus of Rs 100 per quintal

BACK TO TOP

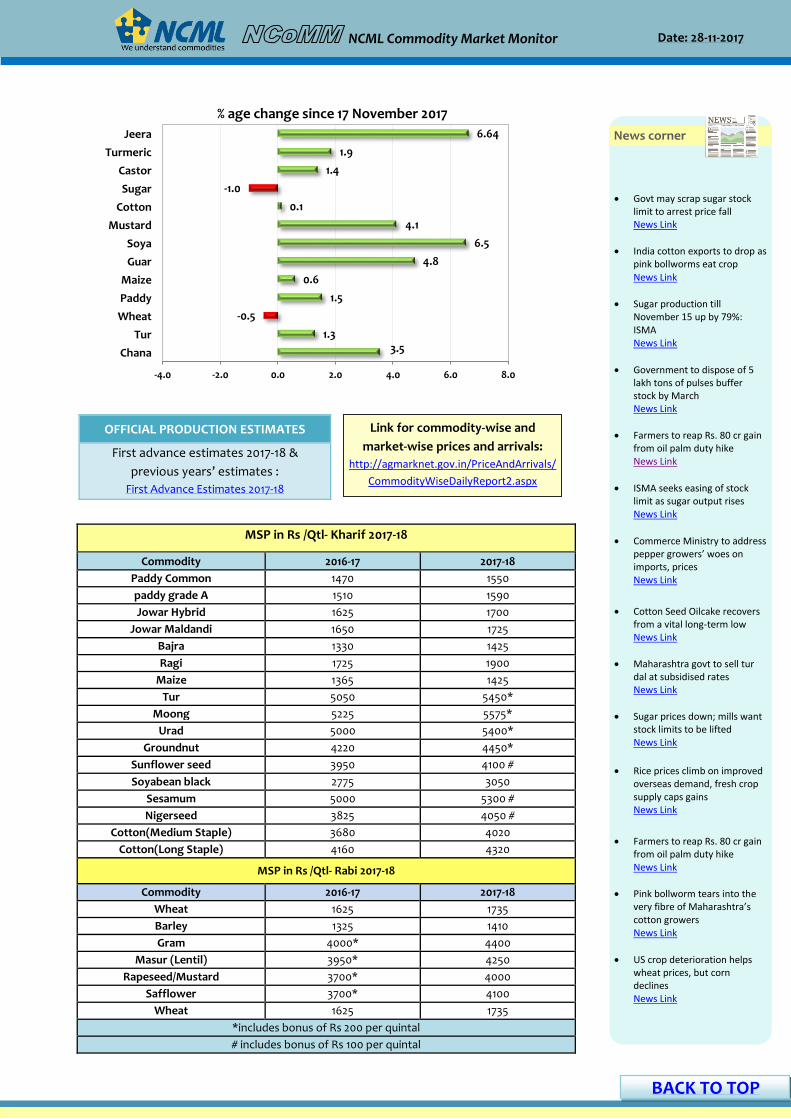

.

3.51.3

-0.5

1.5

0.6

4.8

6.5

4.1

0.1

-1.0

1.4

1.9

6.64

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0

Chana

Tur

Wheat

Paddy

Maize

Guar

Soya

Mustard

Cotton

Sugar

Castor

Turmeric

Jeera

% age change since 17 November 2017

Date: 28-11-2017

NCML Commodity Market Monitor

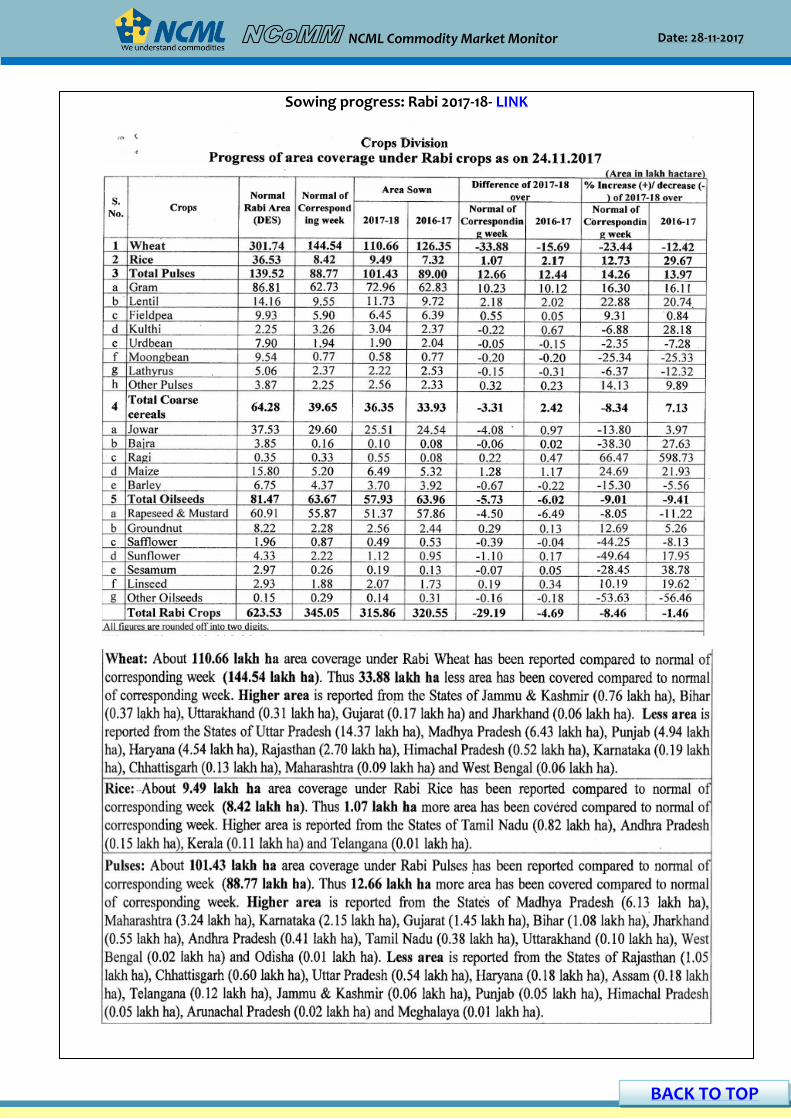

Sowing progress: Rabi 2017-18- LINK

BACK TO TOP

Date: 28-11-2017

NCML Commodity Market Monitor

Answers of NCoMM report dated 21 November 2017:

1. 1.5 Lakh MT

2. 2.53 Lakh Tonnes

3. Black Sea Region

The following people gave correct answers:

Anilkumar Parvathaneni Mayank Mishra Dr. Raina Jain S.NARENDRA Vidhi Bhasin Akshay Thoravashe Bhawani Singh Naruka Rohit Dhyani Mohdathar Anand Swaminathan Akshay Riteshkumar Sahu Dhillukaushik rahuldhyani Prashant Sharma Maheshwari Shveta Harveen Kaur Deepak Acharya Mohd Sumranuddin Faizan Ahmed Shyam Sunder Chandolu Ankit Gupta Ajay Singh VIJAYPAL Singh Tushar Patil Akbar Inamdar Himanshu Bhardwaj

Manoj kumar sah Himanshu Chourasia Aparna Modi Abhay Modi Abhishek Parihar Karan Arora Sunita Katyal Sunny saharan SRINIVAS REDDY BOYAPALLI Deepa Priyanshu Chourasia Yashvardhan Aggarwal Bichhanda Kumar sahoo Adarsh Verma K.Priyanka Rajeswarareddy.s Manoj Kumar Karan Banga Venkanna Katikella Dr. Ravi Pratap Singh Sangwan Sanjay Singh Supriya Vineet Poonia deepak saini Ranjit Singh SUSHIL SWAMI sandeep Kumar

Manish kumar rohilla anjali ANURAG KUSHWAHA Nikhil Kumar Gautam Vashistha Pravendra Singh Amit Sahu Aaftab khan Yadbir Singh Shiv Singh Dhaked Ankita Sharma Babloo Kumar sushil Sharma Gaurav Kumar Mathur lalit Sharma kulvinder singh Prachi Agarwal Chetana Madhukar Iswalkar Devaraj L Maheshkumar Ramaswamy Som Dutt Sharma amit gangadhar Aparna Mothe Sunny Kumar

LUCKY WINNER :

Lalit Kumar

Date: 28-11-2017

NCML Commodity Market Monitor

Advisory Team

Basant Vaid Head: TCIG [email protected]

Sreedhar Nandam Vice President: SCM [email protected]

Research Team

Suresh Solanki Assistant Manager: TCIG [email protected]

Kamna Malhotra Economist: TCIG [email protected]

Akash Jaiswal Research Analyst: TCIG [email protected]

Ansh Aggarwal Senior Officer: Trade Support [email protected]

For any research queries, contact us at [email protected]

STOCK

Stock limits of States/UTs

Disclaimer:

This consultancy report has been prepared by National Collateral Management Services Limited (NCML) for the sole benefit of the addressee.

Neither the report nor any part of the report shall be provided to third parties without the written consent of NCML. Any third party in possession

of the report may not rely on its conclusions without the written consent of NCML. NCML has exercised reasonable care and skill in preparation

of this consultancy report but has not independently verified information provided by others. No other warranty, express or implied, is made in

relation to this report. Therefore, NCML assumes no liability for any loss resulting from errors, omissions or misrepresentations made by others.

Any recommendations, opinions and findings stated in this report are based on circumstances and facts as they existed at the time of preparation

of this report. Any change in circumstances and facts on which this report is based may adversely affect any recommendations, opinions or

findings contained in this report.

© National Collateral Management Services Limited (NCML) 2017