Embed Size (px)

Citation preview

Natural Gas Facts & Figures

3. LNG

3. LNGSources : Total LNG group, PGCD special report

Trade movementsTerminals for import, terminals for exports Liquefaction, regazeificationShips

LNG by road, fluvial

49

On-board regasification offers low cost and convenient option to supply gas to new and existing markets

LNG: More flexibility through new technology

50Source: Skaugen

Gas source

Small scale LNGoffers opportunities to produce otherwise stranded gas and reduce gas

flaring

LNG: More flexibility through new technology

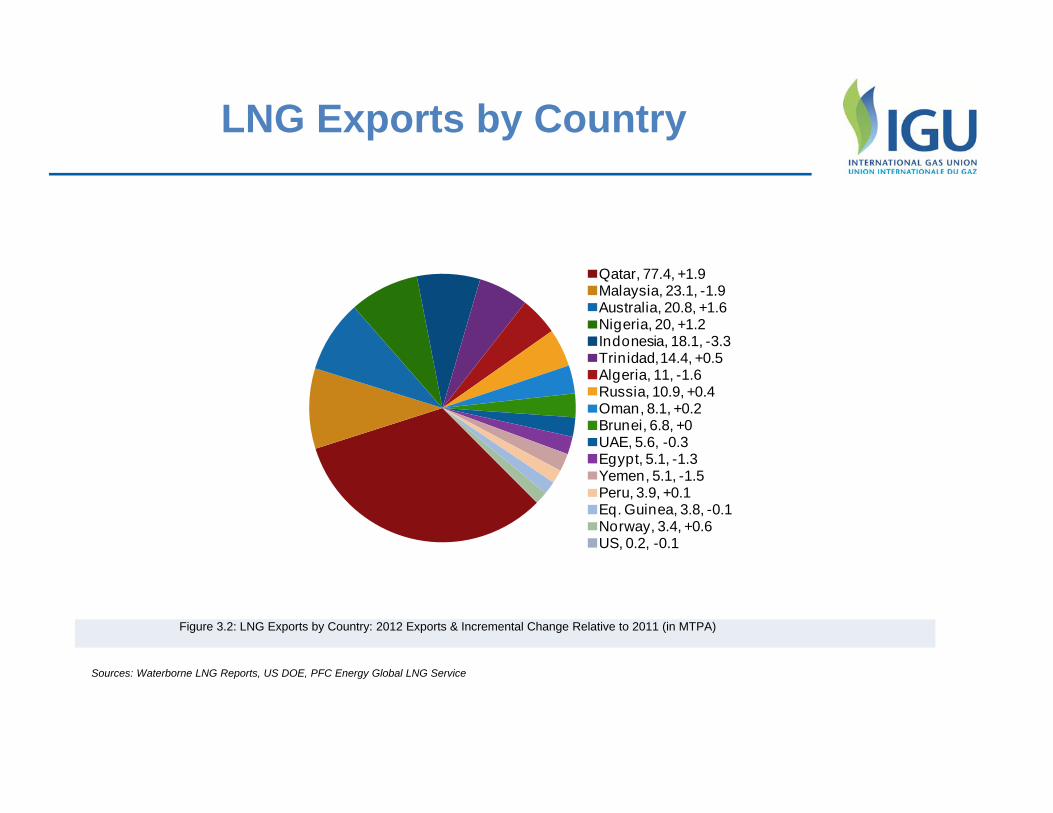

LNG Exports by Country

Qatar, 77.4, +1.9Malaysia, 23.1, -1.9Australia, 20.8, +1.6Nigeria, 20, +1.2Indonesia, 18.1, -3.3Trinidad, 14.4, +0.5Algeria, 11, -1.6Russia, 10.9, +0.4Oman, 8.1, +0.2Brunei, 6.8, +0UAE, 5.6, -0.3Egypt, 5.1, -1.3Yemen, 5.1, -1.5Peru, 3.9, +0.1Eq. Guinea, 3.8, -0.1Norway, 3.4, +0.6US, 0.2, -0.1

Figure 3.2: LNG Exports by Country: 2012 Exports & Incremental Change Relative to 2011 (in MTPA)

Sources: Waterborne LNG Reports, US DOE, PFC Energy Global LNG Service

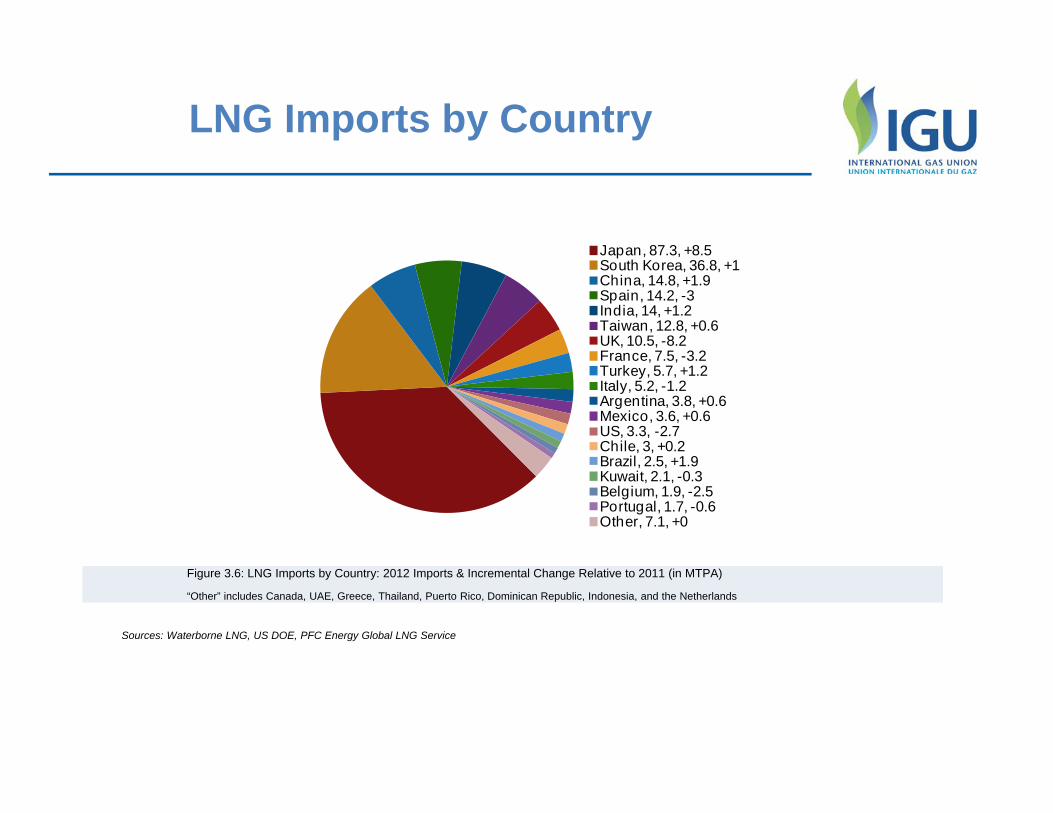

LNG Imports by Country

Japan, 87.3, +8.5South Korea, 36.8, +1China, 14.8, +1.9Spain, 14.2, -3India, 14, +1.2Taiwan, 12.8, +0.6UK, 10.5, -8.2France, 7.5, -3.2Turkey, 5.7, +1.2Italy, 5.2, -1.2Argentina, 3.8, +0.6Mexico, 3.6, +0.6US, 3.3, -2.7Chile, 3, +0.2Brazil, 2.5, +1.9Kuwait, 2.1, -0.3Belgium, 1.9, -2.5Portugal, 1.7, -0.6Other, 7.1, +0

Figure 3.6: LNG Imports by Country: 2012 Imports & Incremental Change Relative to 2011 (in MTPA)

“Other” includes Canada, UAE, Greece, Thailand, Puerto Rico, Dominican Republic, Indonesia, and the Netherlands

Sources: Waterborne LNG, US DOE, PFC Energy Global LNG Service

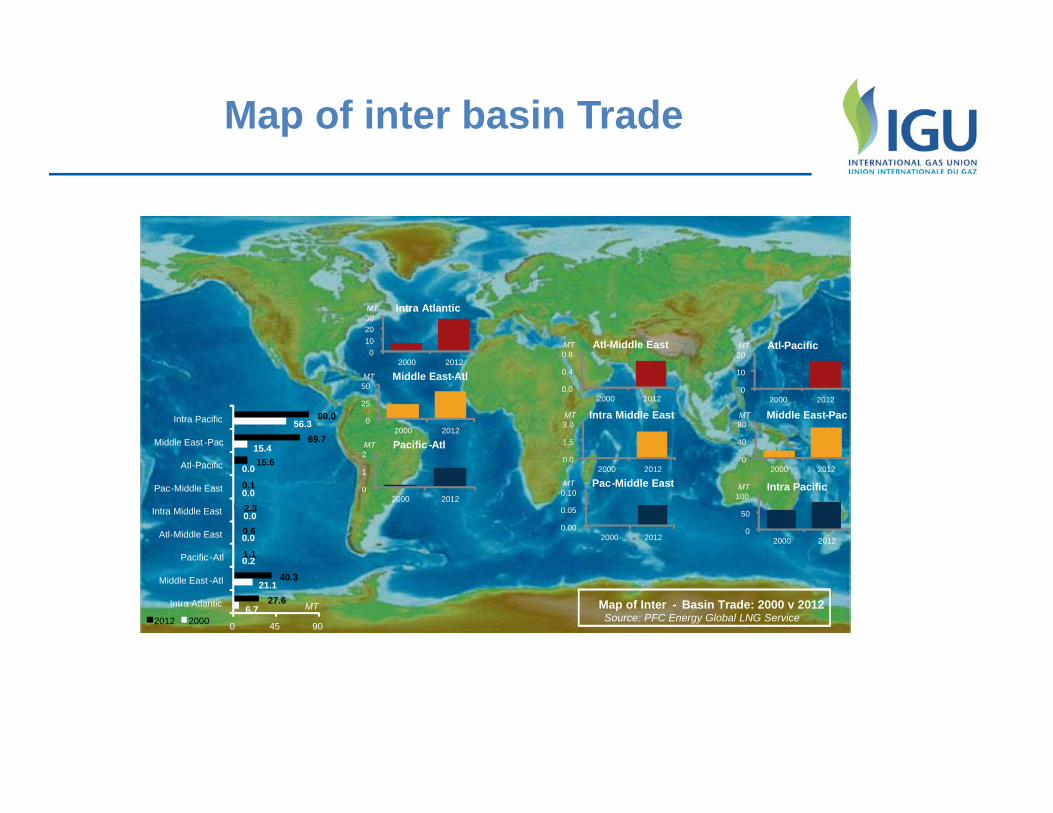

Map of inter basin Trade

6.7

21.1

0.2

0.0

0.0

0.0

0.0

15.4

56.3

27.6

40.3

1.1

0.6

2.3

0.1

15.6

69.7

80.0

0 45 90

Intra Atlantic

Middle East -Atl

Pacific -Atl

Atl-Middle East

Intra Middle East

Pac-Middle East

Atl-Pacific

Middle East -Pac

Intra Pacific

MT2012 2000

0 10 20 30

2000 2012

MT Intra Atlantic

0.0

0.4

0.8

2000 2012

MT Atl-Middle East

0

10

20

2000 2012

MT Atl-Pacific

0

25

50

2000 2012

MT Middle East-Atl

0.0

1.5

3.0

2000 2012

MT Intra Middle East

0

40

80

2000 2012

MT Middle East-Pac

0

1

2

2000 2012

MT Pacific -Atl

0.00

0.05

0.10

2000 2012

MT Pac-Middle East

0

50

100

2000 2012

MT Intra Pacific

Map of Inter - Basin Trade: 2000 v 2012Source: PFC Energy Global LNG Service

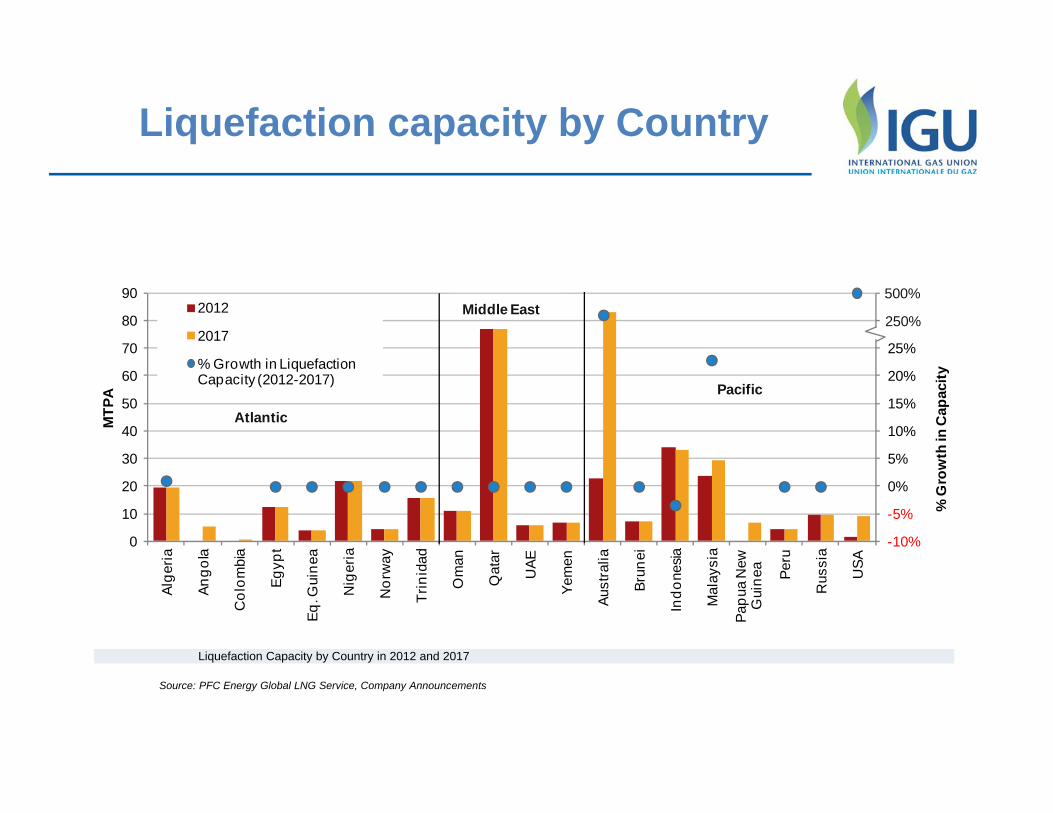

Liquefaction capacity by Country

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

10

20

30

40

50

60

70

80

90

Alge

ria

Ango

la

Col

ombi

a

Egyp

t

Eq. G

uine

a

Nig

eria

Nor

way

Trin

idad

Om

an

Qat

ar

UAE

Yem

en

Aust

ralia

Brun

ei

Indo

nesia

Mal

aysi

a

Papu

a N

ew

Gui

nea

Peru

Rus

sia

USA

% G

row

th in

Cap

acity

MTP

A

2012

2017

% Growth in Liquefaction Capacity (2012-2017)

Middle East

Pacific

Atlantic

250%

500%

Liquefaction Capacity by Country in 2012 and 2017

Source: PFC Energy Global LNG Service, Company Announcements

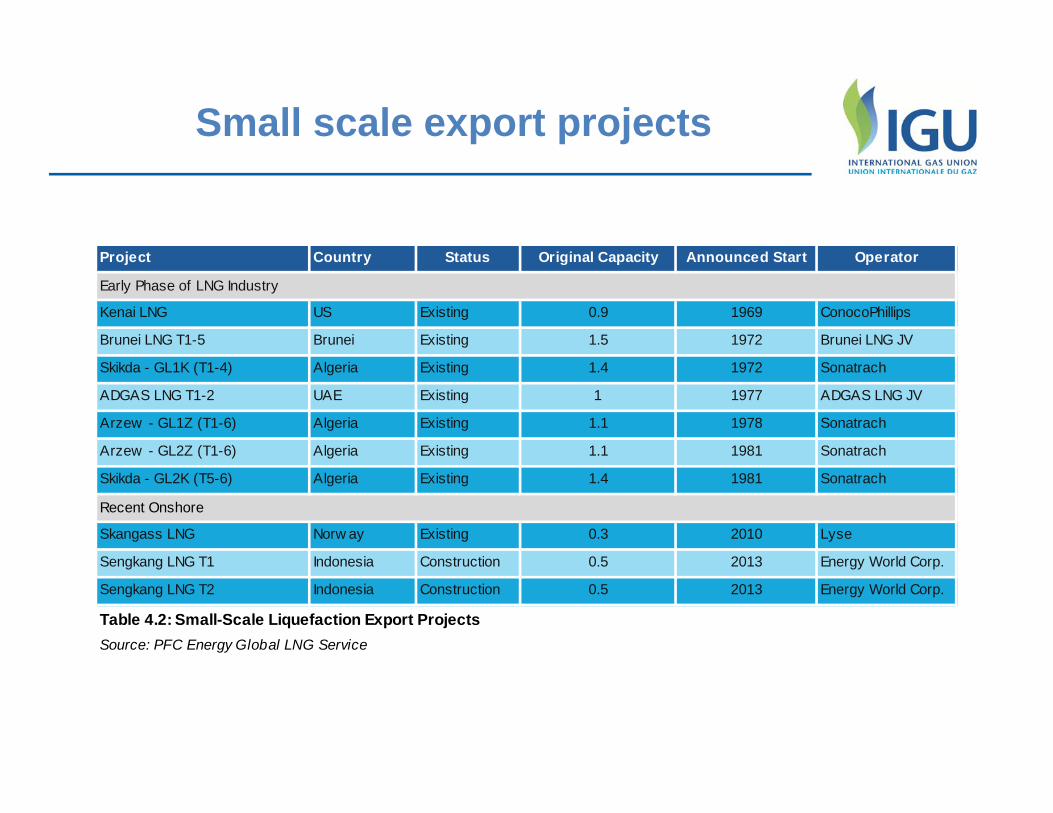

Small scale export projects

Project Country Status Original Capacity Announced Start Operator

Kenai LNG US Existing 0.9 1969 ConocoPhillips

Brunei LNG T1-5 Brunei Existing 1.5 1972 Brunei LNG JV

Skikda - GL1K (T1-4) Algeria Existing 1.4 1972 Sonatrach

ADGAS LNG T1-2 UAE Existing 1 1977 ADGAS LNG JV

Arzew - GL1Z (T1-6) Algeria Existing 1.1 1978 Sonatrach

Arzew - GL2Z (T1-6) Algeria Existing 1.1 1981 Sonatrach

Skikda - GL2K (T5-6) Algeria Existing 1.4 1981 Sonatrach

Skangass LNG Norw ay Existing 0.3 2010 Lyse

Sengkang LNG T1 Indonesia Construction 0.5 2013 Energy World Corp.

Sengkang LNG T2 Indonesia Construction 0.5 2013 Energy World Corp.

Early Phase of LNG Industry

Recent Onshore

Table 4.2: Small-Scale Liquefaction Export ProjectsSource: PFC Energy Global LNG Service

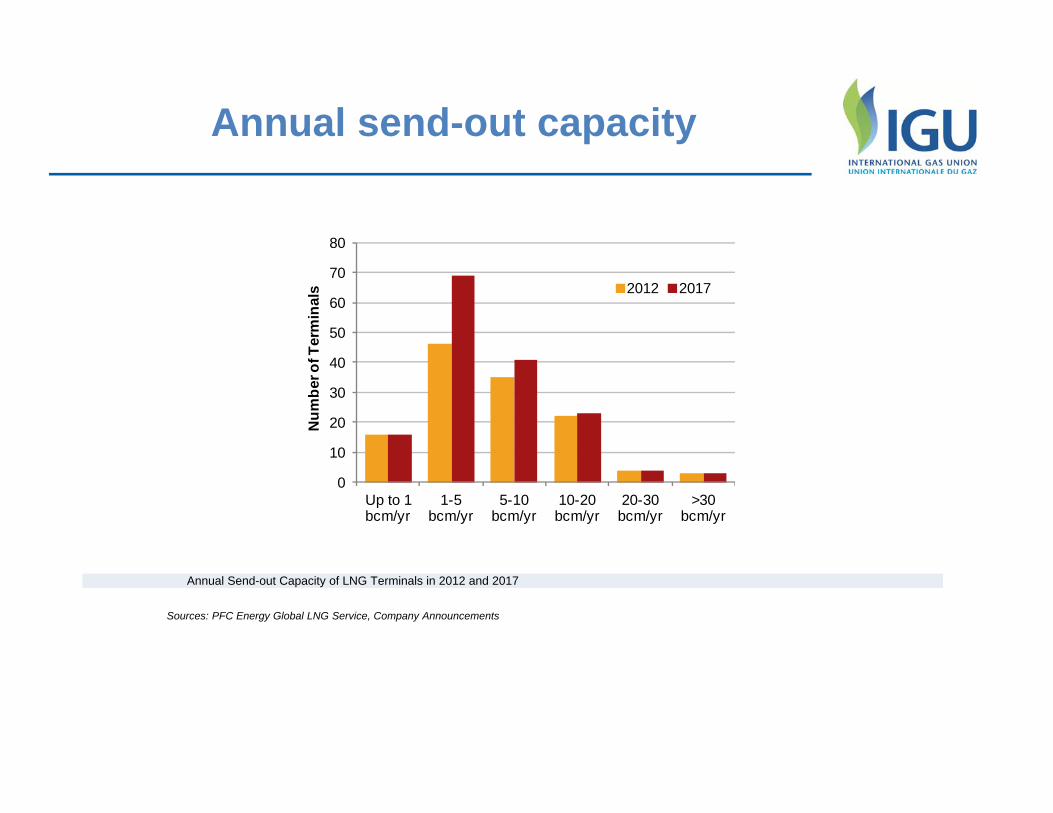

Annual send-out capacity

0

10

20

30

40

50

60

70

80

Up to 1 bcm/yr

1-5 bcm/yr

5-10 bcm/yr

10-20 bcm/yr

20-30 bcm/yr

>30 bcm/yr

Num

ber o

f Ter

min

als 2012 2017

Annual Send-out Capacity of LNG Terminals in 2012 and 2017

Sources: PFC Energy Global LNG Service, Company Announcements

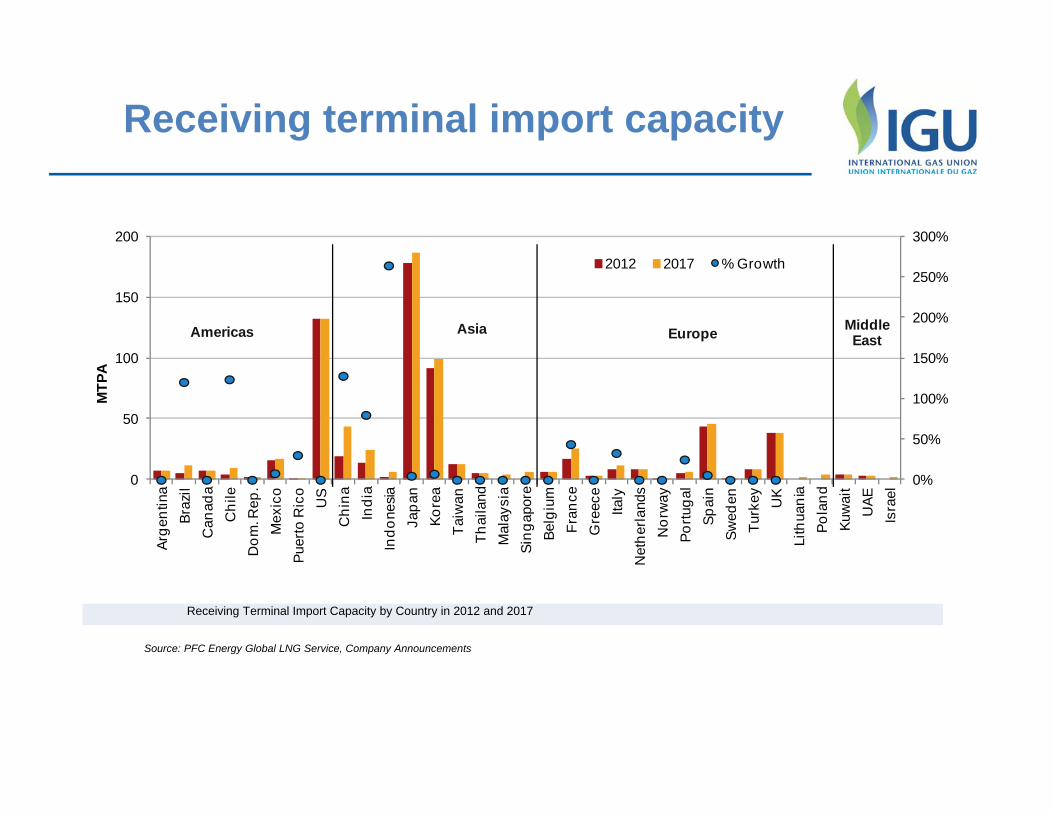

Receiving terminal import capacity

0%

50%

100%

150%

200%

250%

300%

0

50

100

150

200

Arge

ntin

aBr

azil

Can

ada

Chi

leD

om. R

ep.

Mex

ico

Puer

to R

ico

US

Chi

naIn

dia

Indo

nesia

Japa

nKo

rea

Taiw

anTh

aila

ndM

alay

sia

Sing

apor

eBe

lgiu

mFr

ance

Gre

ece

Italy

Net

herla

nds

Nor

way

Portu

gal

Spai

nSw

eden

Turk

ey UK

Lith

uani

aPo

land

Kuw

ait

UAE

Isra

el

MTP

A

2012 2017 % Growth

Americas Asia Europe Middle East

Receiving Terminal Import Capacity by Country in 2012 and 2017

Source: PFC Energy Global LNG Service, Company Announcements

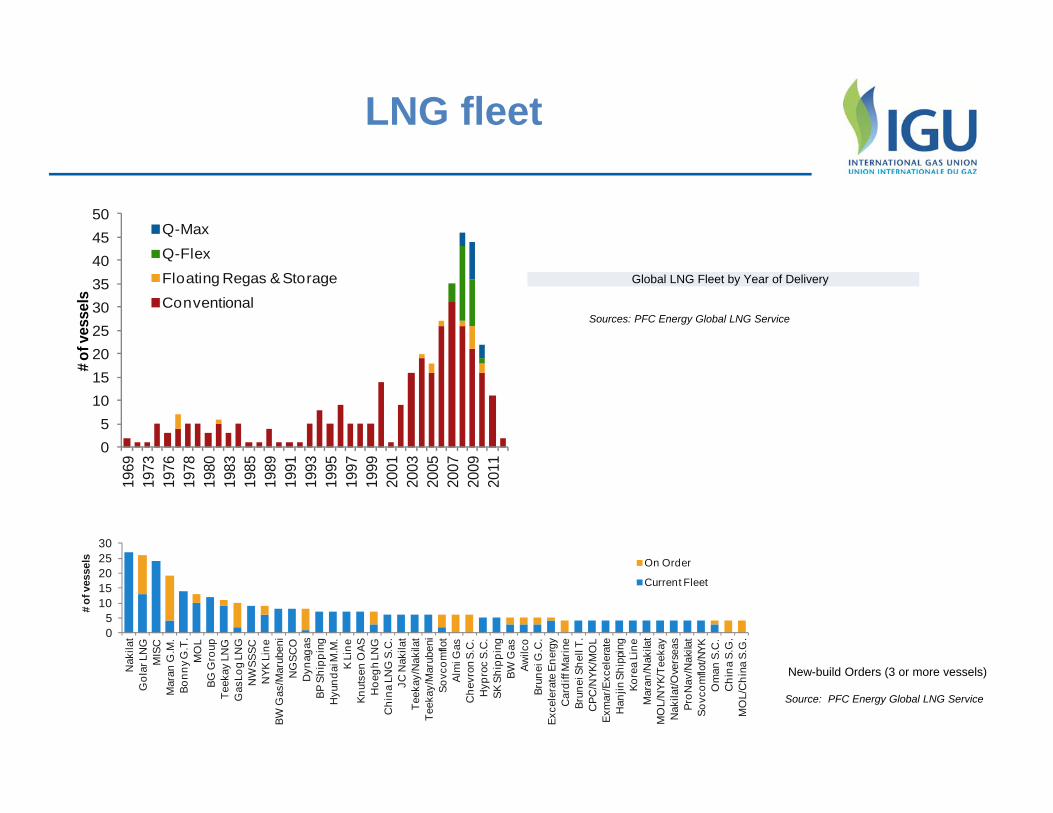

LNG fleet

05

101520253035404550

1969

1973

1976

1978

1980

1983

1985

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Q-Max

Q-Flex

Floating Regas & Storage

Conventional

#of v

esse

ls

Global LNG Fleet by Year of Delivery

Sources: PFC Energy Global LNG Service

05

1015202530

Nak

ilat

Gol

ar L

NG

MIS

CM

aran

G.M

.Bo

nny G

.T.

MO

LBG

Gro

upTe

ekay

LN

GG

asLo

g LN

GN

WSS

SCN

YK L

ine

BW G

as/M

arub

eni

NG

SCO

Dyn

agas

BP S

hipp

ing

Hyu

ndai

M.M

.K

Line

Knut

sen

OAS

Hoe

gh L

NG

Chi

na L

NG

S.C

.JC

Nak

ilat

Teek

ay/N

akila

tTe

ekay

/Mar

uben

iSo

vcom

flot

Alm

i Gas

Che

vron

S.C

.H

ypro

c S.

C.

SK S

hipp

ing

BW G

asAw

ilco

Brun

ei G

.C.

Exce

lera

te E

nerg

yC

ardi

ff M

arin

eBr

unei

She

ll T.

CPC

/NYK

/MO

LEx

mar

/Exc

eler

ate

Han

jin S

hipp

ing

Kore

a Li

neM

aran

/Nak

ilat

MO

L/N

YK/T

eeka

yN

akila

t/Ove

rsea

sPr

oNav

/Nak

ilat

Sovc

omflo

t/NYK

Om

an S

.C.

Chi

na S

.G.

MO

L/C

hina

S.G

.

# of

ves

sels On Order

Current Fleet

Source: PFC Energy Global LNG Service

New-build Orders (3 or more vessels)

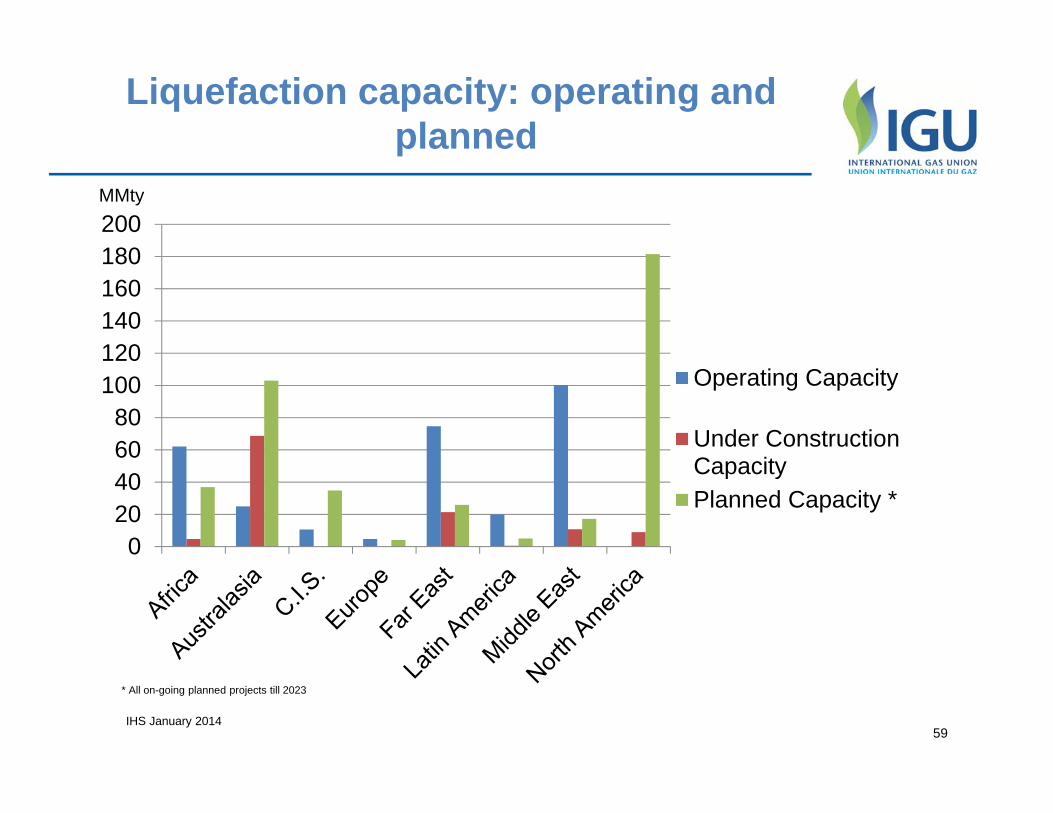

Liquefaction capacity: operating and planned

020406080

100120140160180200

Operating Capacity

Under ConstructionCapacityPlanned Capacity *

59IHS January 2014

MMty

* All on-going planned projects till 2023

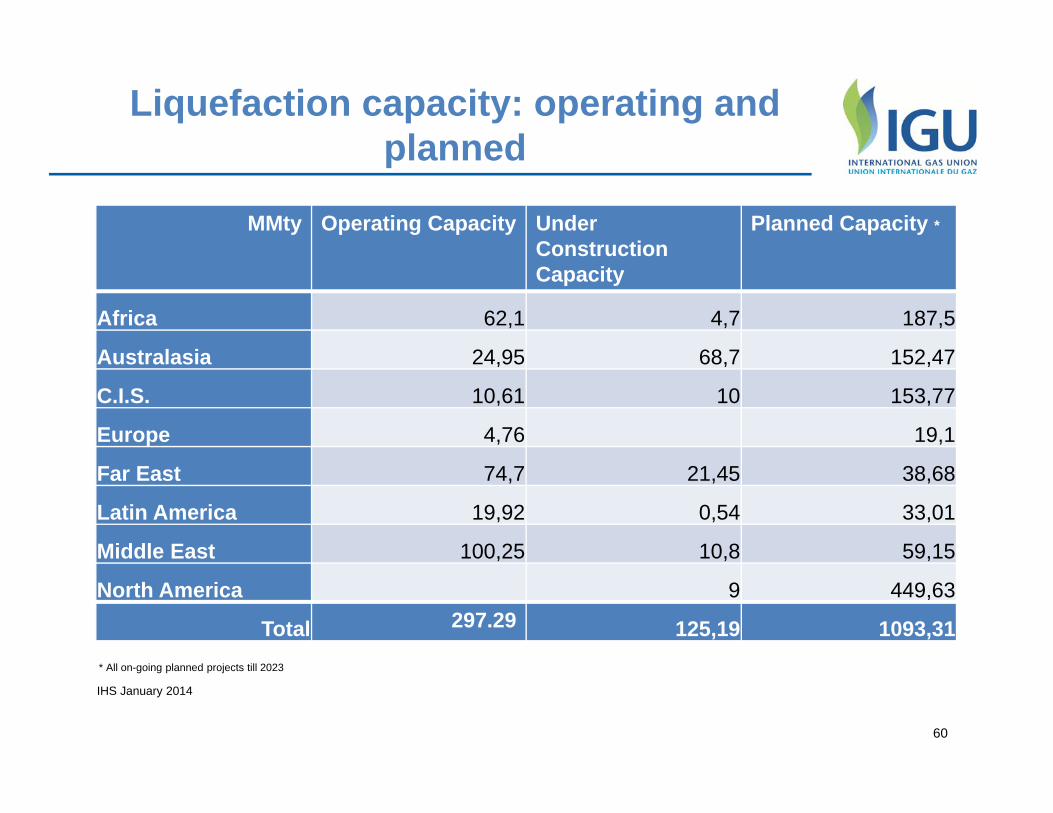

Liquefaction capacity: operating and planned

60

IHS January 2014

MMty Operating Capacity UnderConstructionCapacity

Planned Capacity *

Africa 62,1 4,7 187,5

Australasia 24,95 68,7 152,47

C.I.S. 10,61 10 153,77

Europe 4,76 19,1

Far East 74,7 21,45 38,68

Latin America 19,92 0,54 33,01

Middle East 100,25 10,8 59,15

North America 9 449,63

Total 297.29 125,19 1093,31* All on-going planned projects till 2023

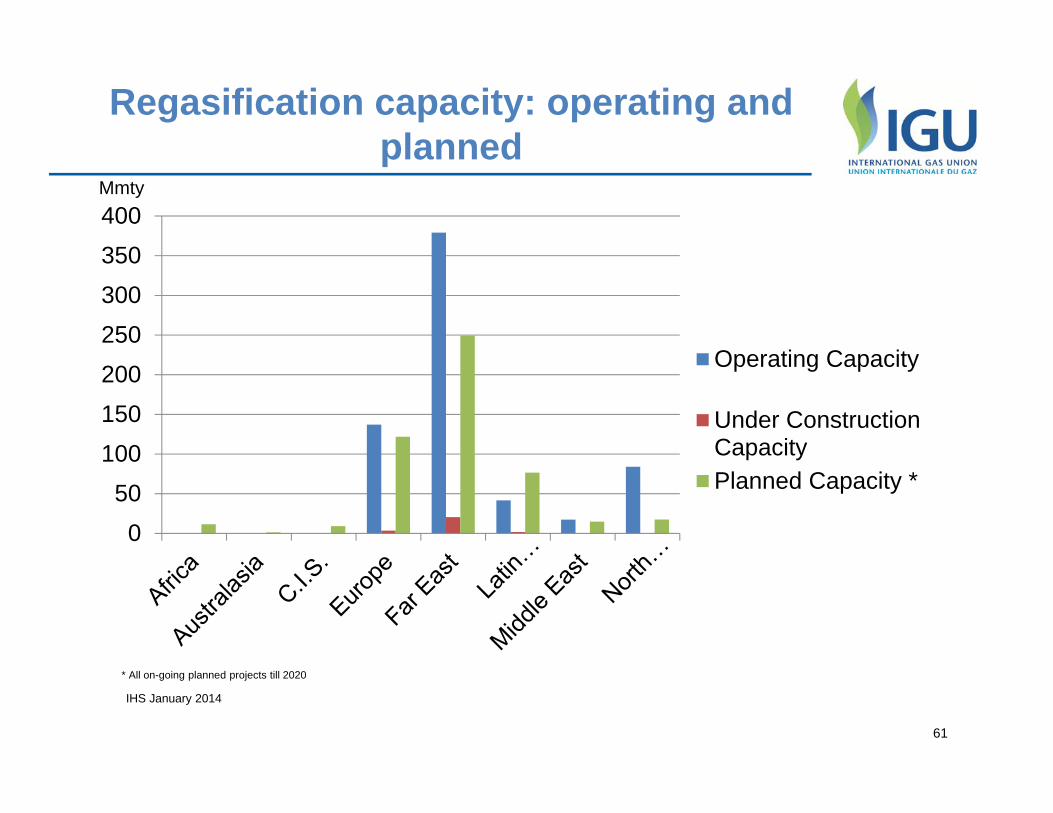

Regasification capacity: operating and planned

050

100150200250300350400

Operating Capacity

Under ConstructionCapacityPlanned Capacity *

61

IHS January 2014

Mmty

* All on-going planned projects till 2020

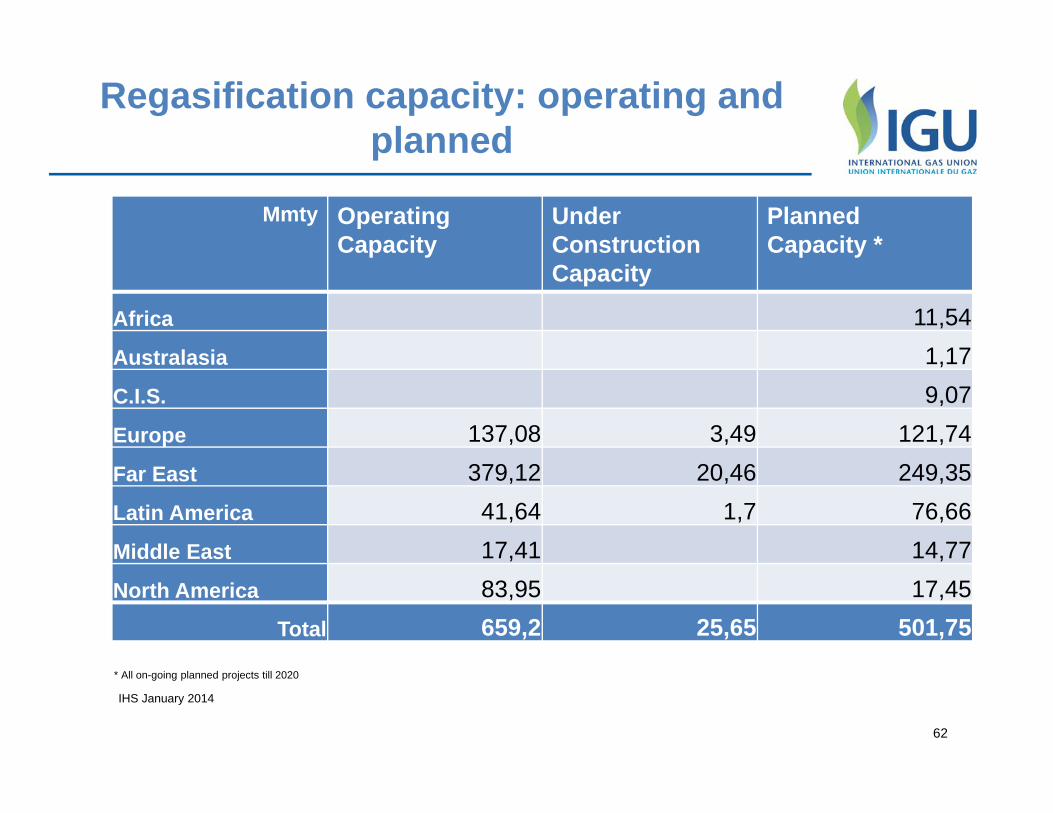

Regasification capacity: operating and planned

62

IHS January 2014

Mmty Operating Capacity

UnderConstruction Capacity

PlannedCapacity *

Africa 11,54Australasia 1,17C.I.S. 9,07Europe 137,08 3,49 121,74Far East 379,12 20,46 249,35Latin America 41,64 1,7 76,66Middle East 17,41 14,77North America 83,95 17,45

Total 659,2 25,65 501,75

* All on-going planned projects till 2020

63

Overland transport of LNG: By road trucks and railcars

LNG is transported by road truck in many countriesTrucked LNG has many small-scale uses:

Domestic and commercial piped gas supply from satellite re-gasification terminals located in places remote from pipelines

Small industrial users (electric power, engine tests, glass, paper)

Commercial users (trains, buses, ferries, institutions)

Supply to peak-shaving plants

Supply to pipeline network during repairs or maintenance