Embed Size (px)

Citation preview

Homebuyer Planning Kit

live – we commit to you

love - you are the heart of our success

be - we believe in making sure you’re ready

live it. love it. be it.

Accredited Business

Why Us

?

Direct Lender Complete Supervision Super Low Rates Save Money Real Pre-Approvals Save Time Experience Real Answers Streamline Process Easy & Efficient Modern Operation Convenience

Understanding Our Process

1 3 2

Learn Plan Close

During the

discovery period,

we get to learn

about you and your

goals.

We take the

discoveries and

create a plan: Rates,

Programs, Payments

and more.

After selecting a plan,

we finish processing

your loan and get you

ready to close.

Pre-Approval

Checklist

Two ID Cards

Drivers License

Social Security Card

Income Documents

Most Recent Paystubs

Last 2 Years of W2’s

Last 2 Years of Tax Returns

Proof of Funds 2 Most Recent Bank Statements

1

2

3

Additional Documents may be requested.

Lender

Attorney

Real Estate Agent

Home Inspector

Appraiser

You

Your Team

Key players work together to help accomplish

your goal of home ownership.

Get A Rate Online

Get a Quick and Easy mortgage rate with our online pricing engine.

Shop

Lender

s

Compar

e

Rates

Save

Money

Steps Kick Off Week 1 Week 2 Week 3 Week 4

Pre Approval

Find an Agent

Time To House Hunt

Place An Offer (Contract)

Find An Attorney

Attorney Review (3-5 Days)

Order Inspection

Home Loan Submission

Lender Orders Appraisal

Clear Underwriting Conditions

Mortgage Commitment

Title Ordered

Review & Sign Final

Disclosures

Clear To Close

Closing On Your Home

Move In

Timeframes listed are based on averages and are subject to change

Home Loan Process

Personal Profile

New Jersey State Licensed Mortgage Banker of Get A Rate Home loans, a

New Jersey Direct Lender Experience with Real Estate Transactions

Experience

Mortgage Banker since 2011 10+ years in sales and customer satisfaction Kean University Bachelors in Marketing

Languages English and Spanish

Products Conventional, Jumbo, FHA, VA, 203K, Construction, USDA, No Condo Questionnaire Foreign National, No PMI and more.

Office

1 U.S. 46 Suite 46

Elmwood Park, NJ 07407

201-393-0200 Ext 2019

Cell

973-900-0914

FAX

201-456-6080

WEB

Www.GetARate.com

“Over 200 Real Estate Agents refer their clients to Get A Rate”

Neftali Ricardo Hernandez Mortgage Banker

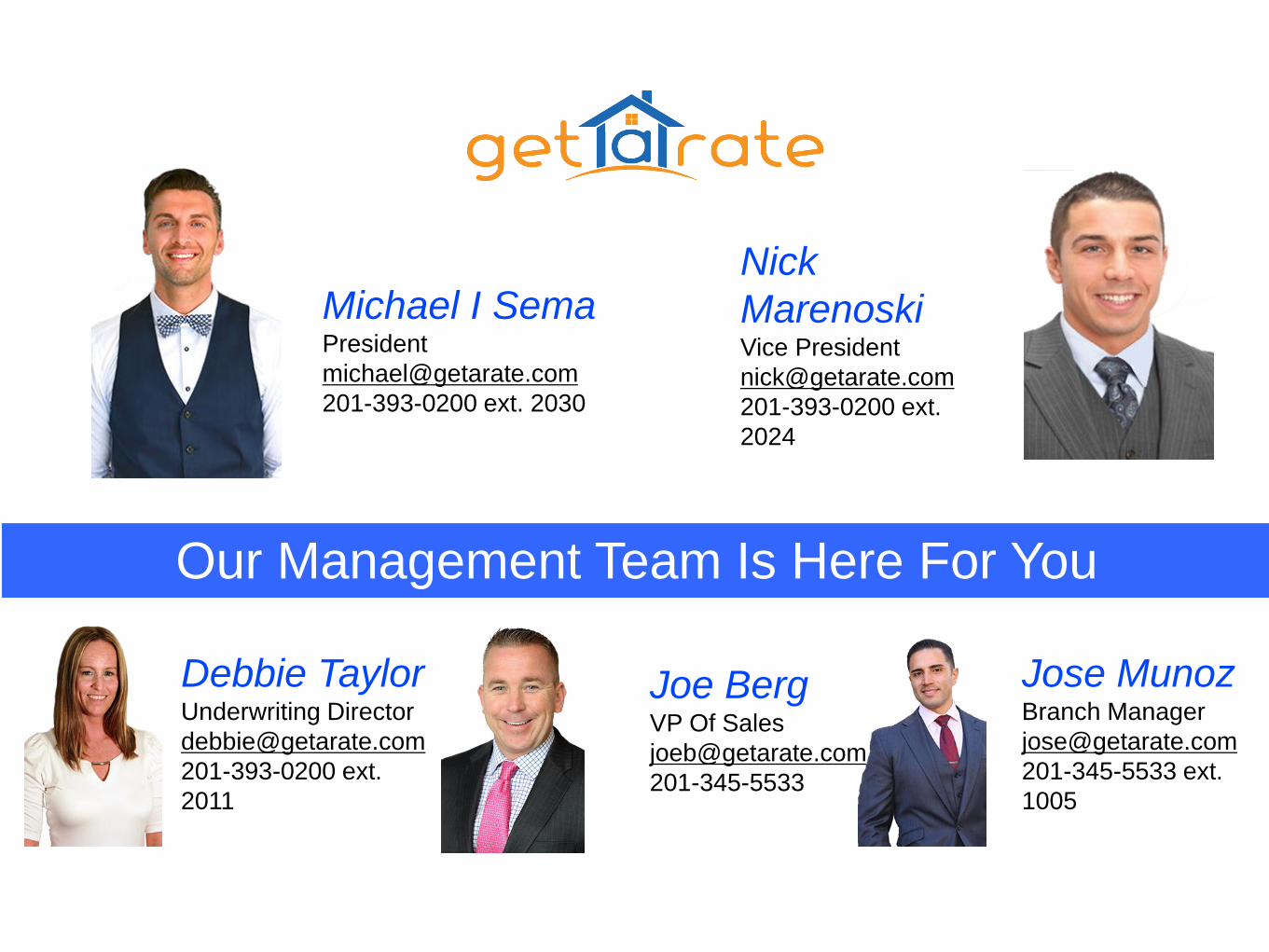

Michael I Sema President

201-393-0200 ext. 2030

Nick

Marenoski Vice President

201-393-0200 ext.

2024

Our Management Team Is Here For You

Debbie Taylor Underwriting Director

201-393-0200 ext.

2011

Joe Berg VP Of Sales

201-345-5533

Jose Munoz Branch Manager

201-345-5533 ext.

1005

Poor 619 Below

Fair 620-679

Average 680-719

Excellent 720-759

Elite 760 Plus

We Choose Your

Middle Credit Score

Do Make sure to factor in your

lifestyle.

Do some research on your own –

know the area you want to be in

and what home prices are at this

time.

Do create a checklist of must

haves and a wish list so that you

are only looking at homes that

meet your expectations.

Do think about the future.

Consider what you want today

and for the next 5 years.

Do relax. You are with the right

lender. You control a lot of the

timing. If documentation is

required, get it to your originator

as soon as possible.

Do Make sure to factor in your

lifestyle.

Do some research on your own –

know the area you want to be in

and what home prices are at this

time.

Do create a checklist of must

haves and a wish list so that you

are only looking at homes that

meet your expectations.

Do think about the future.

Consider what you want today and

for the next 5 years.

Do relax. You are with the right

lender. You control a lot of the

timing. If documentation is

required, get it to your originator as

soon as possible.

Do’s to Buying a Home

• Don’t use your credit card to buy

things for your home before you

close. (No excessive spending.)

• Don’t buy a vehicle. Even if you

are paying cash versus taking out

a loan.

• Don’t do either. Most home loans

close within 30-45 days. Wait

until you are in the home.

• Don’t quit your job.

• Don’t open new revolving credit

cards

• Don’t make out-of-the-ordinary

large deposits. If you must, be

prepared to provide a clear paper

trail from where and why.

•Don’t buy large items on your credit

cards. We can’t stress this enough.

•Don’t lie on your loan application.

•Don’t omit any information. (This can be

the same as lying!)

•Don’t co-sign on a loan for anyone no

matter how much you love them or how

many times they promise to pay it back.

•Don’t make sudden changes in your

spending habits or income.

•Don’t just get pre-qualified get pre-

approved.

Don’ts to Buying a Home

A

Adjustable-Rate Mortgage (ARM) - Loans with an

initial fixed rate period (usually 5,7 or 10 years. After the

fixed rate period, your interest rare may change once per

year- either up or down depending on market conditions.

ARM’s are almost always lower in rate than fixed loans

and can offer huge savings to first time home buyers

especially those who don’t plan on staying in their home

for more than 10 years.

Amortization - The paying off of a debt with a fixed

repayment schedule in regular installments over a period

of time.

Annual Percentage Rate (APR) - The total cost of a loan

which includes not only the interest rate, but all costs

associated with the loan, such as closing costs and fees.

Once this is determined, the APR is then amortized over

the life of the loan. In order to allow borrowers to compare

various loans and lenders, the APR is required to be

disclosed by the Federal Truth-in-Lending statues.

Application Fee - One time processing fee for a loan.

This fee may be applied towards various costs, including

the appraisal and credit report.

Appraisal - An estimate of the current market value of

the property. B

Buy down - The ability for the buyer to lower their initial

interest rate by providing money upfront or by paying

extra points up front at the closing of the loan. C

Closing - The time where buyer and seller exchange

money for title and sign closing papers to a new home.

This finalizes the agreements reached in the sales

agreement.

Closing Costs - Refers to the lender’s costs for closing

a loan, or all the costs associated with closing on a piece

of property as a buyer.

Conventional Mortgage - A loan that is underwritten,

following specific guidelines, by banks, savings and loans,

or other types of mortgage companies. Typically, this

refers to loans underwritten to the guidelines of Fannie

Mae or Freddie Mac.

Real Estate Terms

We Thought

You Should Know

P

PITI ( Principal-Interest-Taxes-and-Insurance)

Four pieces included in a monthly mortgage payment. Portion of

each payment applied to each of those elements.

Point - Each point equals one percent of your total loan amount.

The more points you pay, the lower the interest rate you get.

Private Mortgage Insurance (PMI) - Paid in monthly

installments by a borrower or upfront as part of the closing costs, this

insurance allows a lender to lend more than 80 percent of the value

of a property while protecting the lender on risk to the top 20 percent. L

Loan Origination Fee- Fee charged by a lender to cover

administrative costs of processing a loan. Loan-to-Value Ratio (LTV) - The money borrowed in a mortgage

transaction compared with the value of the property you wish to

purchase. (loan amount / home value) M

Mortgage - The document providing a lien on a home in exchange

for a lender’s financing. The lender secures this financed loan

through this mortgage, and has the ability to foreclose on this home

as well.

Mortgage Banker - An entity that lends its own funds to

borrowers while also bringing together lenders and borrowers.

Mortgage bankers may also collect monthly payments. R

Recording - Filing documents at various government agencies,

local, state, and federal to create a public record. S

Settlement Statement - Known as the HUD-1, this details the

transaction paid out and received by the buyer and seller at closing, T

Term - Typically 15 or 30 years, this is the life of the loan.

Title – The title is the actual document that gives evidence of

ownership of a property.

Title Insurance - Title insurance protects lenders against any title

dispute that may arise over a particular property. Home title

insurance is a required fee paid at closing.

D

Deed of Trust - The legal document that transfers property

from one owner to another.

Down Payment – The amount of your home’s purchase price

you pay upfront. E

Earnest Money - Upfront money provided by the borrower to

the seller as a show of good faith towards the purchase price of

a home.

Escrow Closing - A third party that acts as a neutral party and

receives documents for the exchange of the deed by the sellers

for the buyer’s money.

F

First Mortgage - Takes priority when there are other

voluntary liens present. G

Gift Letter - A letter, which details the amount of gift and

name of the giver, which indicates a gift of cash to the buyer of

a home. This can be provided by relatives, friends, non- profit

organizations, or government agencies depending on the

requirements of given lender and product.

Good Faith Estimate (GFE) – A written estimate of closing

costs that lenders are required to provide potential borrowers

within three days of an application submission. H

Hazard Insurance- Also known as homeowner’s insurance,

this covers the property from damages that may affect the

value. I

Interest- The fee a lender charges for permitting the borrower

to use their money for a specific length of time.

Interest Rate Cap- The max amount of percentage points that

ARMs may rise over a loans life. O

Origination Fee- A fee that is charged by a lender to cover

the administrative costs of processing a loan.

30 Year Fixed A 30 Year Fixed Mortgage offers the budget-conscious homeowner lower monthly payments. A fixed rate allows you to lock in a set principle and interest payment.

15 Year Fixed Another popular loan for homeowners who want to secure a lower mortgage rate and pay less interest over the life of the loan.

FHA Loan FHA loans help families with financial limitations become homeowners. The lower down payment makes it possible to buy a new home even with limited funds.

Adjustable Rate Loan Adjustable Rate Mortgage fluctuates based on current market trends at pre-determined times throughout the duration of the loan. These loans are ideal when buying a home when interest rates are high but are expected to drop in the future.

Jumbo Loans Jumbo loans were established for larger purchases. They come with specific limits and guidelines.

VA Loans Offer veteran buyers home loan options with no down payments or mortgage insurance.

HARP Is your home “underwater,” meaning that your outstanding balance on your existing NJ home mortgage currently exceeds the value of your home?

Reverse Mortgage Reverse mortgages are great for homeowners 62 and older who want to help supplement their income or take cash out for whatever need.

FHA Streamline If you already have an FHA loan and are looking to refinance, this is a great option for you AND you won’t need an appraisal!

Construction Loans Thinking of making structural repairs on your home or any other repairs – you may qualify for a Construction loan.

No PMI Mortgage No PMI Mortgages are a great option if you don’t have enough for a 20% down payment.

Loan Options

Act responsibly with the highest level

of ethical standards.

Educating our clients is a top priority.

Strive to make a positive difference in our community.

Locations

1 U.S. 46 Suite 101, Elmwood Park, NJ, 07407

201-393-0200

129 Washington Street Suite LL1, Hoboken, NJ, 07030

201-3450-4445

Email Us – [email protected]

www.getarate.com