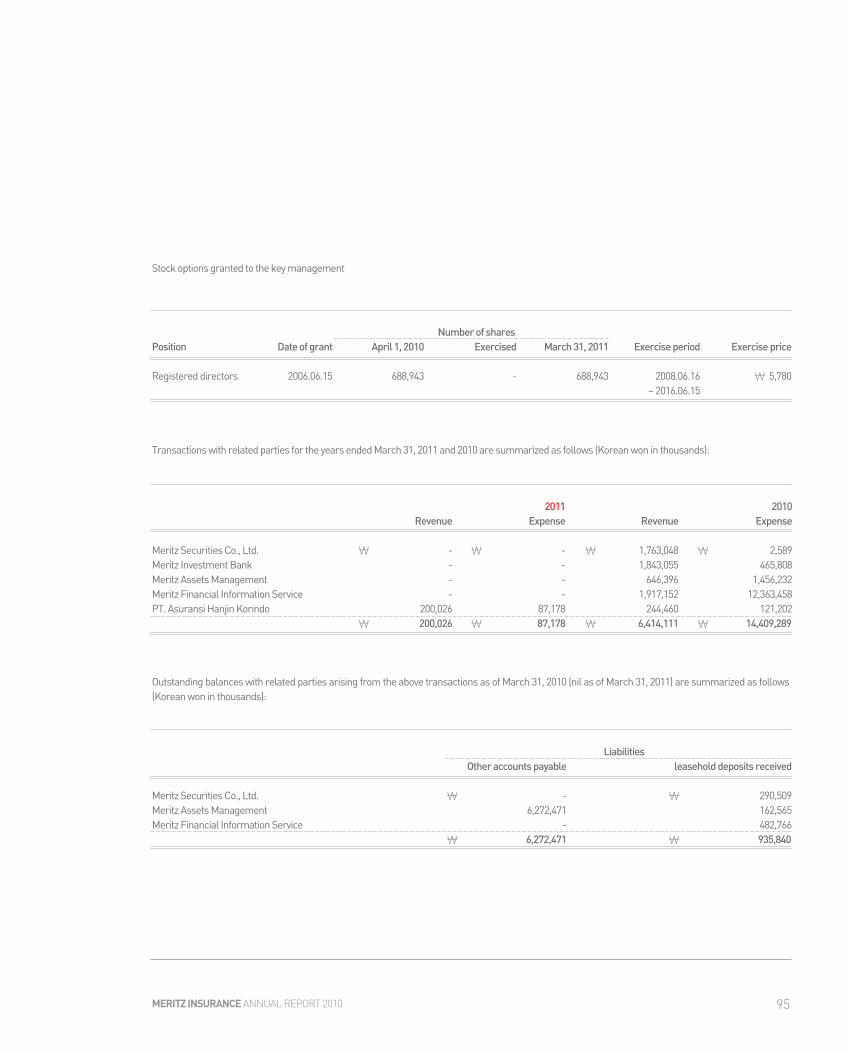

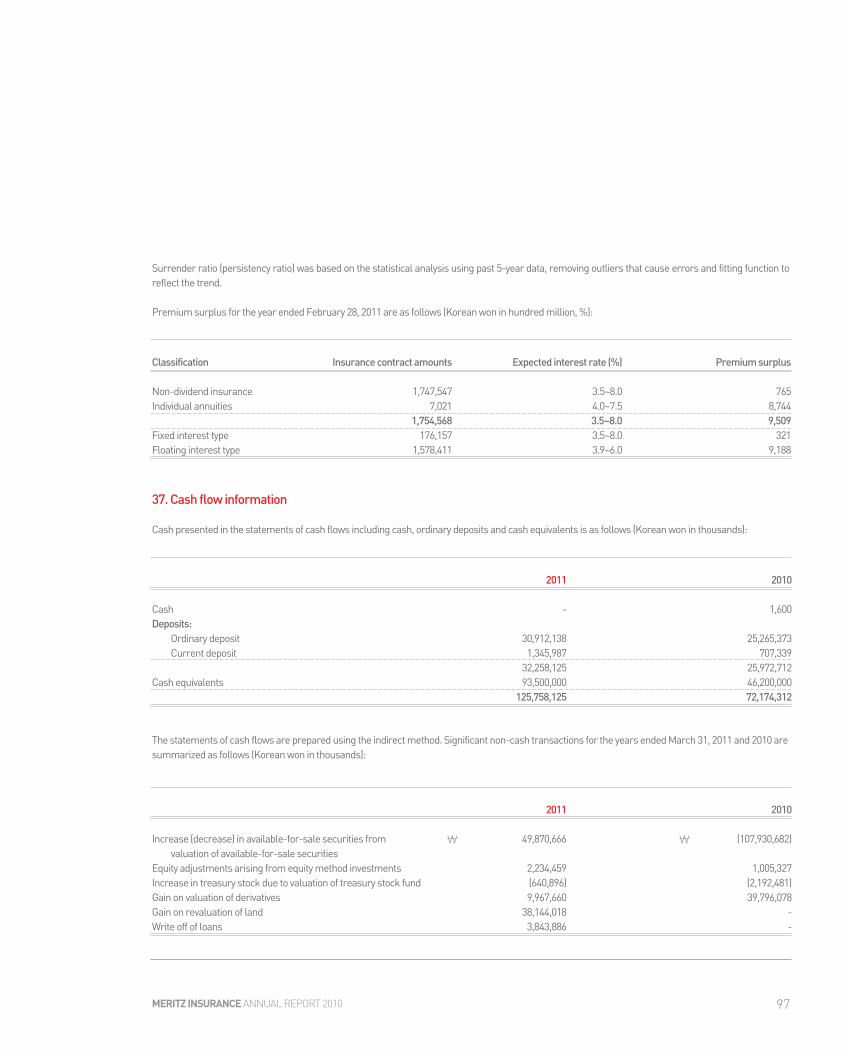

Embed Size (px)

Citation preview

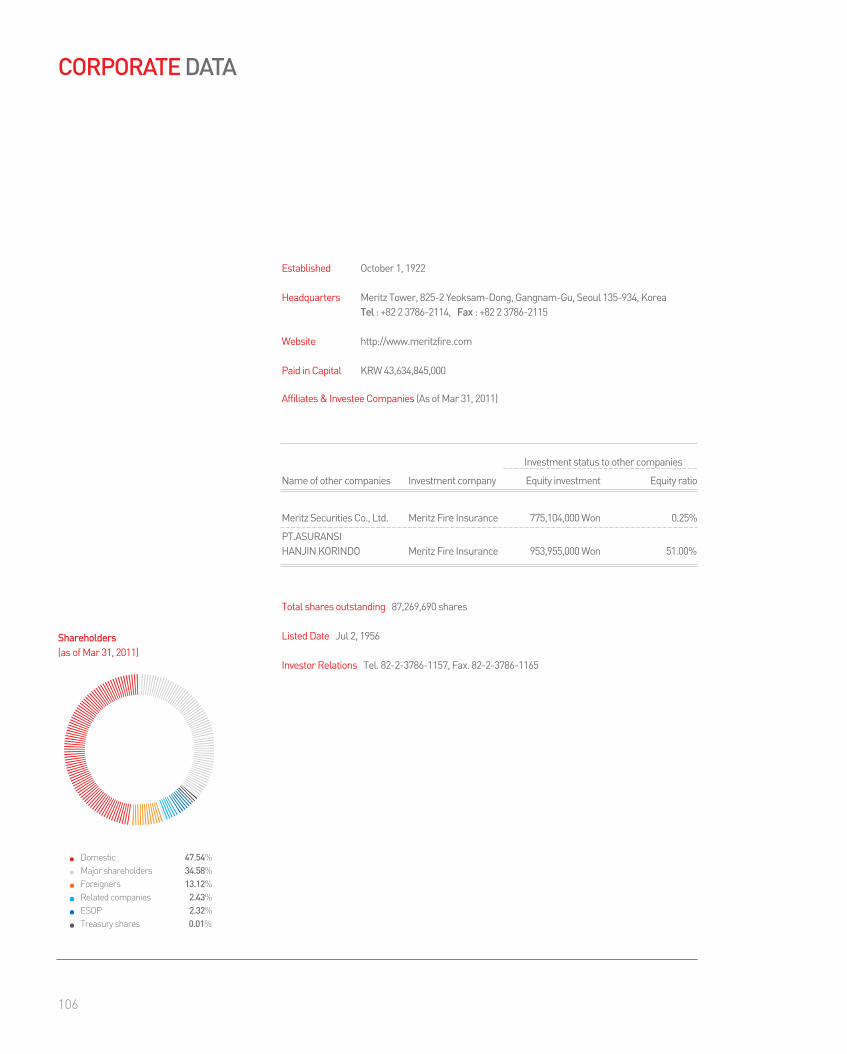

Meritz Tower, 825-2,Yeoksam-dong, Gangnam-gu, Seoul, KoreaTel . 82-2-3786-2114 Fax . 82-2-3786-2115

www.meritzfire.com

ANNUAL REPORT 2010MERITZ INSURANCE

CONTENTS

03 Company profile04 Financial Highlights06 A Message from the CEO08 2010 at a Glance12 Business Overview_Performance by Line15 Business Overview_Underwriting Management18 Business Overview_Investment Management20 Business Overview_Risk Management22 Management's Discussion & Analysis30 Independent Auditors' Report31 Financial Statements38 Notes to Non-consolidated Financial Statements100 Internal Control Over Financial Reporting Review Report101 Corporate History in Brief102 Accolades & Awards103 Board of Directors104 Organization105 Credit Ratings106 Corporate Data

Companyprofile

Meritz Insurance , the first non-life insurance company in Korea,celebrated its 88th anniversary in FY2010. It was a profit strengthtamping year in preparation for its 100th anniversary with a businessgrowth of KRW 7 trillion in total assets and 3.8 trillion Won in directwritten premiums in 2010. It was a result of the persistent promotion ofprofit oriented growth strategy distinguished from other insurers basedon the continuous trust and support of the customers.

FY2011 will be a year for new challenges and innovation for MeritzInsurance. We have taken first steps toward the new challenge bylaunching Meritz Financial Holdings on Mar 28, 2011, the first insuranceholding company in Korea. Meritz Insurance as the leading company of

Meritz Financial Holdings Group, and will contribute to thediversification of financial market in Korea and transparent governancestructure by developing of integrated financial products for themaximum synergy between the group companies and creation of thebest customer service in the insurance industry to maximize the valuesof customers and shareholders, who continuously support thecompany. The company will also make assurance of thorough efforts to be rebornas a 100 year-old innovative traditional company leading the trend andparadigm of the non-life insurance industry by drawing up thequantitative growth accompanied by quality and through optimal riskmanagement.

04

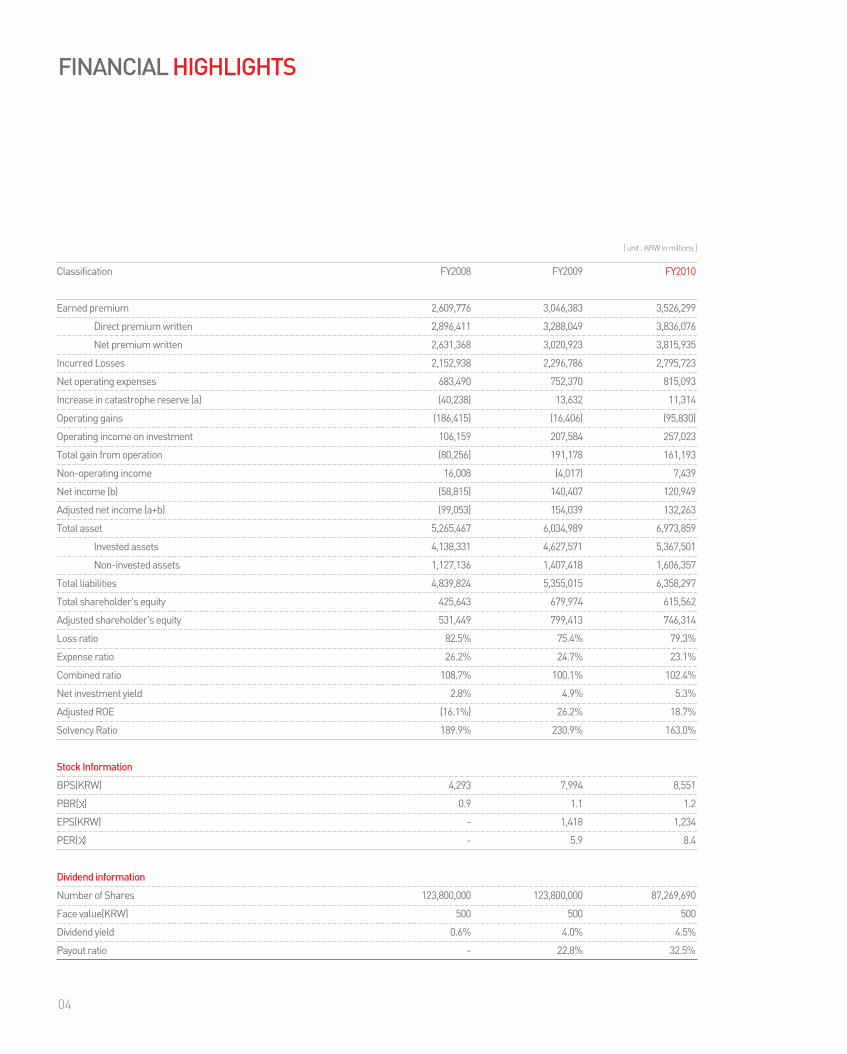

FINANCIAL HIGHLIGHTS

Classification FY2008 FY2009 FY2010

Earned premium 2,609,776 3,046,383 3,526,299

Direct premium written 2,896,411 3,288,049 3,836,076

Net premium written 2,631,368 3,020,923 3,815,935

Incurred Losses 2,152,938 2,296,786 2,795,723

Net operating expenses 683,490 752,370 815,093

Increase in catastrophe reserve (a) (40,238) 13,632 11,314

Operating gains (186,415) (16,406) (95,830)

Operating income on investment 106,159 207,584 257,023

Total gain from operation (80,256) 191,178 161,193

Non-operating income 16,008 (4,017) 7,439

Net income (b) (58,815) 140,407 120,949

Adjusted net income (a+b) (99,053) 154,039 132,263

Total asset 5,265,467 6,034,989 6,973,859

Invested assets 4,138,331 4,627,571 5,367,501

Non-invested assets 1,127,136 1,407,418 1,606,357

Total liabilities 4,839,824 5,355,015 6,358,297

Total shareholder's equity 425,643 679,974 615,562

Adjusted shareholder's equity 531,449 799,413 746,314

Loss ratio 82.5% 75.4% 79.3%

Expense ratio 26.2% 24.7% 23.1%

Combined ratio 108.7% 100.1% 102.4%

Net investment yield 2.8% 4.9% 5.3%

Adjusted ROE (16.1%) 26.2% 18.7%

Solvency Ratio 189.9% 230.9% 163.0%

Stock Information

BPS(KRW) 4,293 7,994 8,551

PBR( ) 0.9 1.1 1.2

EPS(KRW) - 1,418 1,234

PER( ) - 5.9 8.4

Dividend information

Number of Shares 123,800,000 123,800,000 87,269,690

Face value(KRW) 500 500 500

Dividend yield 0.6% 4.0% 4.5%

Payout ratio - 22.8% 32.5%

[ unit : KRW in millions ]

05MERITZ INSURANCE ANNUAL REPORT 2010

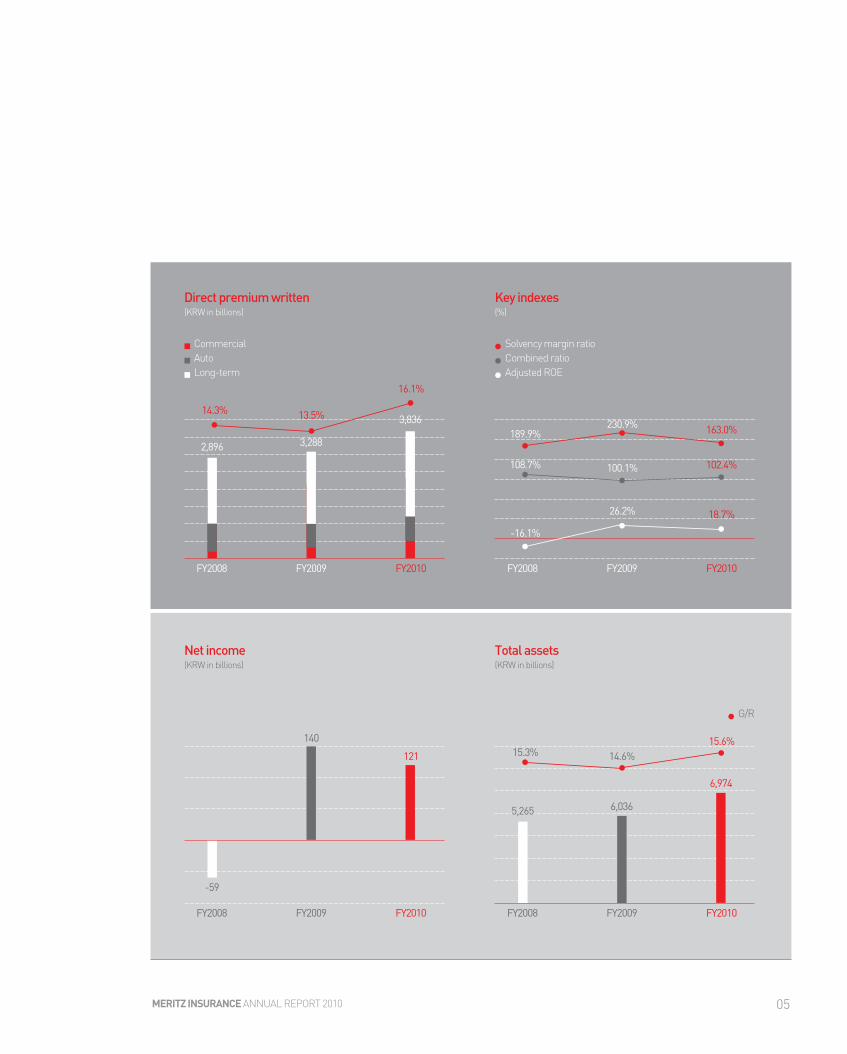

14.3% 13.5%

16.1%

2,896 3,288

3,836

Direct premium written(KRW in billions)

CommercialAutoLong-term

FY2008 FY2009 FY2010

15.3% 14.6%15.6%

6,036

6,974

Total assets(KRW in billions)

FY2008 FY2009 FY2010

189.9%230.9% 163.0%

108.7% 100.1% 102.4%

26.2%

Key indexes(%)

Solvency margin ratioCombined ratioAdjusted ROE

G/R

FY2008 FY2009 FY2010

18.7%

-59

140

121

Net income(KRW in billions)

FY2008 FY2009 FY2010

-16.1%

5,265

06

A MESSAGE FROM THE CEO

Meritz Insurance celebrated its 88th anniversary in FY2010. Since the 88th anniversary, we have paid tribute to the memory of thefirst non-life insurance company in Korea and unfolded variousactivities to become a better blue-chip company when we celebrateour 100th anniversary. We have commercialized the memorial productin the theme of ‘family’, as a representative example, and achievedsuccessful sales of that product through positive advertisement.

The direct written premium collected in the FY2010 amounted to KRW3,836.1 billion, which was a growth of 16.6% compared to that of theprevious year. It means the sales grew by 230% compared to theclosing date, on March 31, 2005, before promoting the 2nd founding,which was a 0.3%p improvement of the Market Share. The retentionpremium was increased by 250% in the same period, which showed a0.8%p improvement of the market share. The most profitable Long-term product made up 70% of the portfolio, which is the highestdevelopment in the non-life insurance industry rising by 26.0%pcompared to that of six years before. The portfolio of new long-terminsurance premium and protection premium per month improved bythe highest level in the insurance industry, which means that overallsales competitiveness has been drastically enhanced.

The net income of FY2010 was KRW 120.9 billion, which amounts to anaverage earning strength of KRW 10 billion per month. As a result,the net income M/S recorded 6.1%p up to 9.9% share compared tothat of six years before, the best improvement in the insuranceindustry. The combined ratio was 102.4%, which is an incredibleimprovement of 3.0%p compared to that of 6 years before, also mostof the indexes related to the company’s earnings, such as generalexpense ratio and ROE have significantly improved.

The numerical values of assets and financial soundness mustconsider the division of Meritz Insurance for the launching of afinancial holding company, which are not the same before and afterthe division. Please refer to the financial statement for the numericalvalues after the division. I will report with the numerical values beforethe division here for reporting purpose.

The total assets of the company before the division in FY2010 wereKRW7,223.3 billion (KRW6,973.9 billion after the division), which is anincrease of 19.7% compared to the previous year. At 270% higher thanthat of six years before, it is the highest growth in the insuranceindustry. The company’s weight has been secured with other investedassets and shareholder’s equity, which have been increased by 250%and 290% respectively.

The company’s solvency margin ratio in FY2010 was 256.0% beforethe division (163% after the division), which is the improvement by25.1%p compared to the prior year and by 76.9%p compared to that of6 years before, and it is much higher than the 233.9% of the 2nd-tieraverage solvency margin ratio.Meritz have passed a meaningful year with comparatively excellentmanagement performance in the overall outcome of sales amount,profits, and financial soundness last year. However, I can say that themost important accomplishment will be the launching of the financialholding company. I will go through the upcoming plans and meaningof the financial holding’s founding.

I am very pleased to report that our overall managementperformance has come to be much better than in the past,since most of the management strategies have beenachieved successfully in the ripe stage of last year, the 6thyear of the second founding.

The company has decided to transition into the ‘financial holdingscompany’system to achieve an advanced governance structure withvarious advantages. We advocate ‘honest and specialized financialcompany’to provide more diversified and superior financial servicesThe financial holdings company founding work had been promotedlegitimately with the application of preliminary approval for itsestablishment on August 5, 2010, which has been processed smoothly byacquisition of the preliminary approval on December 1, 2010, and itslicense on March 16, 2011.

Accordingly, the company has established a new holdings company on Mar25, 2011, with the division of KRW 328.3 billion in total assets, consisting ofKRW33.2 billion in cash and deposit, KRW 289.4 billion in treasury stock ofMeritz Insurance and subsidiaries stocks, and KRW 5.7 billion in brandtrademark rights, which launched as the Meritz Financial Holding Co., Ltd.officially on the 28th of March.

Meritz Insurance had changed its listing on April 11th, and the holdingscompany was re-listed on May 13th. Meritz Insurance acquired approval asa subsidiary of Meritz Financial Group on Jun 15, and its enrollment will becompleted by early August. Meritz Financial Holding Company will be themajor shareholder and a parent company of Meritz Insurance with a 34%share.

Meritz Insurance has founded the first insurance-oriented financialholdings company beyond being the first insurer in Korea. It will recoverthe weakened management indexes, and bring them over the level beforethe division within one year based on accumulated strategies andconfidence. Our financial holdings company will maximize the synergy andsharing of customer information through the collaboration with eachsubsidiary in the group. We will provide the complete mid/long term plansby collecting all the strong points of the non-bank financial holdingcompany that cannot be possessed by the bank-oriented financial holdingcompanies.

We entreat all the shareholders to anticipate the steady growth of Meritzand continue to extend to us the same exceptional attention and affectionthat you have always given.

Thank you!June 10, 2011

Meritz Fire & Marine Insurance Co., Ltd.

Myung Soo, Wohn / Vice-Chairman & CEO

07MERITZ INSURANCE ANNUAL REPORT 2010

NEW CEO

President Jin Kyu Song President Jin Kyu Song has been elected as the CEO in the general meeting of shareholders on June 10, 2011.

08

2010 AT A GLANCE

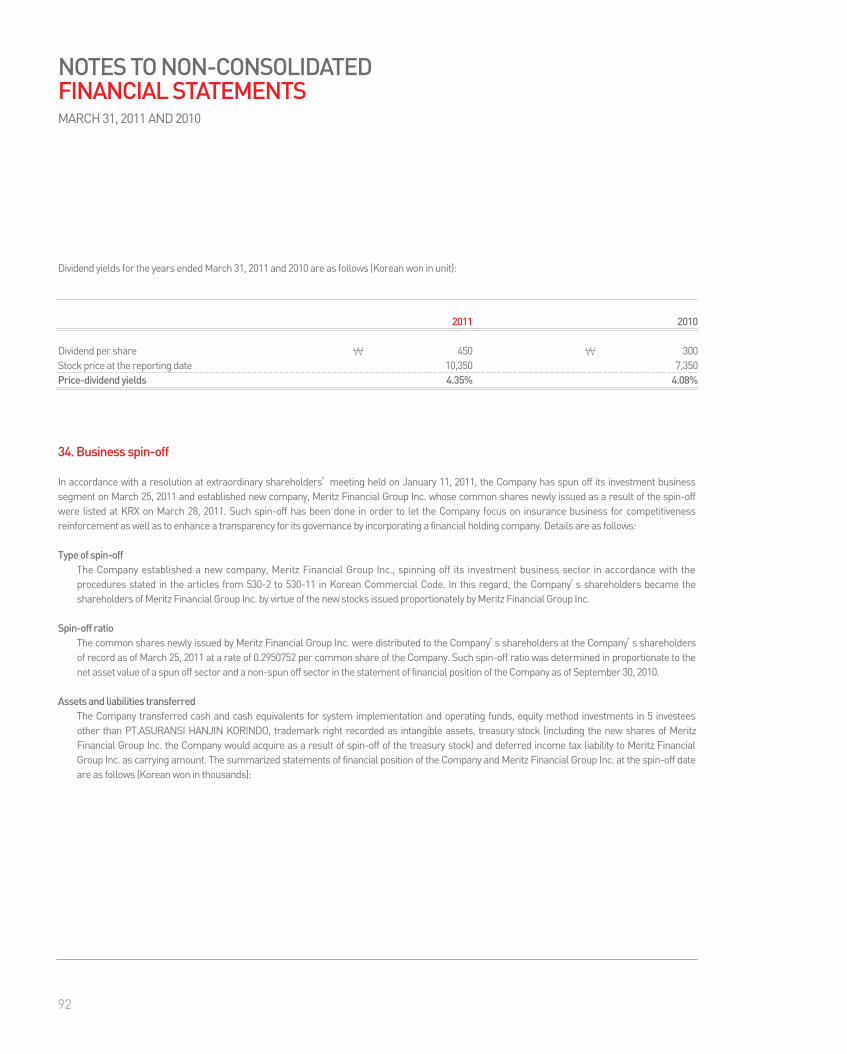

Meritz Insurance, the first non-life insurance company in Korea, established a financial holdingscompany on Mar 28, 2011. Meritz Financial Group is the first insurance financial holdings companylaunched in Korea, and it is comprised of Meritz Securities, Meritz Asset Management, MeritzFinancial Information Service, Ritz Partners, Meritz Business Service, as well as with MeritzFire&Marine Insurance in its center.

The reason behind the transition of Meritz Insurance into a holdings company is to accomplish thesynergy creation to secure stable market position and earnings, diversify the financial businesslines for the provision of comprehensive financial services, take preemptive measures against thedividing trend of production and sales of financial products, raise funds, and secure investmentcapacity, divide the risks and to set up independent management system of each subsidiary, securethe group control tower, and enhance the management efficiency through the concentration ofcore capabilities.

When Meritz F&M has fully transitioned into the holding company system, the group’s investmentcapacity will expand from KRW 160 billion to around KRW 350 billion to advance into new financialbusinesses. The company can devise the diversification of business lines by dominating non-financial companies followed by the deregulation of insurance holding company.

The company can gain strengthening of business specialties by allowing the management tomultitask and foment cost savings, together with the synergy effect by the sharing of customerinformation. It’s also an opportunity for integrated channels like the exclusive sales company togrow, inflow of exterior customers, and enhancement of management efficiency through theconcentration on core capabilities.

The establishment of the financial holdings company has been processed through the spin-offmethod by transferring parts of assets such as subsidiary stocks, treasury stocks, and cash assetspossessed by Meritz Insurance .

2010 Customer Service Award

In 2010, the company received its fourth consecutive “Grand Prize”at the 18th Customer ServiceAwards, which was organized by Korea Management Association Consultants (KMAC).

The Grand Prize is conferred to companies selected through the primary screening that haveachieved various customer satisfaction activities and recognized accomplishment through strictsite audit and assessment by the examiners consisted with the university professors.

The company received positive evaluations regarding its customer satisfaction activities by allexecutives and employees together to enhance the customer value. The Company’s persistentefforts for the ‘differentiated customer service’was done by securing the customer’s trust basedon the CEO’s enthusiasm and leadership towards the CS management.

This award confirms that exceptional customer service has been recognized by a reputablecustomer service institute. As such, it is necessary for Meritz employees to maintain a customer-service mindset in order to enhance the Company’s competitive edge. This award will support thecompany’s ceaseless efforts to maximize customer satisfaction.

MERITZ FIRE INSURANCE, THE FIRST NON-LIFE INSURER IN KOREAESTABLIESHED THE FIRST INSURANCE FINANCIAL HOLDING COMPANY

CUSTOMER SERVICE AWARD?

The Customer Service Award is the largest

awarding system in Korea related to the

customer satisfaction management, which is

organized by Korea Management

Associations Consultants (KMAC).

It evaluates the CS management system of

whole company such as establishment of

customer satisfaction management system

and infrastructure, CS activities and

techniques, employee assessment and

compensation system out of the 181

candidates of each industry in Korea.

09MERITZ INSURANCE ANNUAL REPORT 2010

Management of sharing

Meritz Insurance has selected the management of sharing as one of five core managementphilosophies. Since the company believes that an insurance enterprise is ultimately concerned withthe well-being of our society and customers and puts it into practice for the disadvantagedneighborhoods and local communities in need.The company carried out various sharing activities in 2010 such as supporting children/youth,constructing green environment, and active volunteering from every department.

Meritz Insurance sponsored an economic camp for young students in an effort to help themacquire a better understanding of financial and economic matters. Meritz helped to familiarizestudents with basic economic principles with activities like inviting children to financing field andeducating children of multicultural families about finance and economics.

The company supported the Meritz Arts Volunteer Corps and Lindenbaum Music Festival for theyouth. The Meritz Arts Volunteer Corps was selected among the high school and college studentswith great talent and passion for music. They were trained by professionals and performed at thesocial welfare facilitiesThe company provides scholarships to children whose parents have been lost or injured in trafficaccidents, to cheer up their dreams and to inspire vitality into their daily lives.

As a part of the green management, the company saved costs by lowering the building’stemperature and utilizing personal cups to fund green environment constitution projects such asmaking gardens and drawing wall paintings at children’s facilities. The company is also leading theeco-friendly living with environment preservation projects for the local community such as caringthe Seoul forest and Mt. Cheonggyesan.

In 2010, 4,550 Meritz employees and sales people engaged in volunteer activities at 85 welfareagencies to have warmhearted interaction with the underprivileged. The company supports a‘Beautiful Saturday event’where employees donate clothing and other items to support the needy

neighborhoods with the sales profit of donated goods. Also, the company provides medicaltreatment for children with pediatric cancer and heart diseases with the ‘sharing funds’constituted from voluntary donations from the executives and staff together with the matchinggrant donated from the company.

Meritz Insurance has come to known as a compassionate enterprise practicing the ‘lovingneighbor’through various sharing activities and supports. As a result, the company received thegratitude plaques from Korea Business Council for the Arts, Korea Scout Association, DongcheonNursing Home, Seoul Forest, and Briquettes Campaign Headquarters, as well as thecommendation of the Minister of Health & Welfare in the neighbor-aid category on the SocialWelfare Day organized by the Ministry of Health & Welfare and the Community Chest of Korea.

Meritz Insurance will not cease its efforts to promote ‘love’and ‘sharing’the most genuine valuesof the insurer to keep well-being of our community and customers.

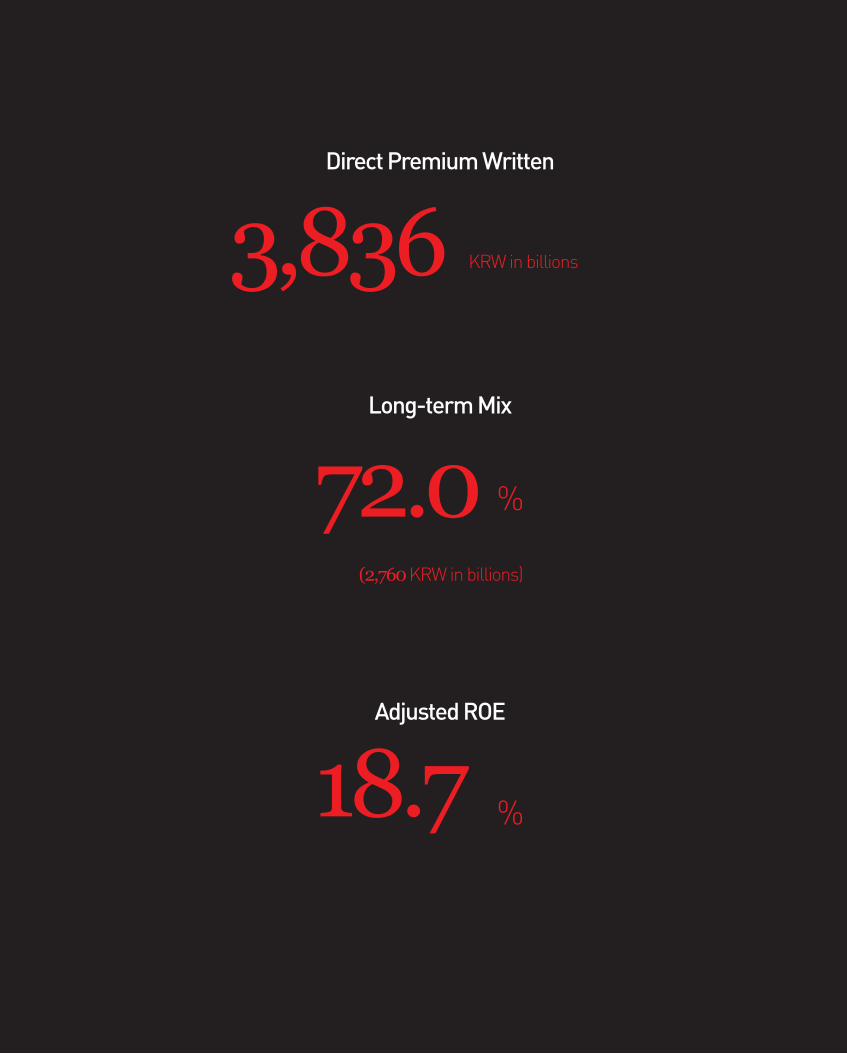

Business OverviewMeritz have passed a meaningful year with comparatively excellent management performances in the overall outcome of sales amount, profits and financial soundness.

3,836Direct Premium Written

KRW in billions

(2,760 KRW in billions)

72.0Long-term Mix

%

18.7Adjusted ROE

%

12

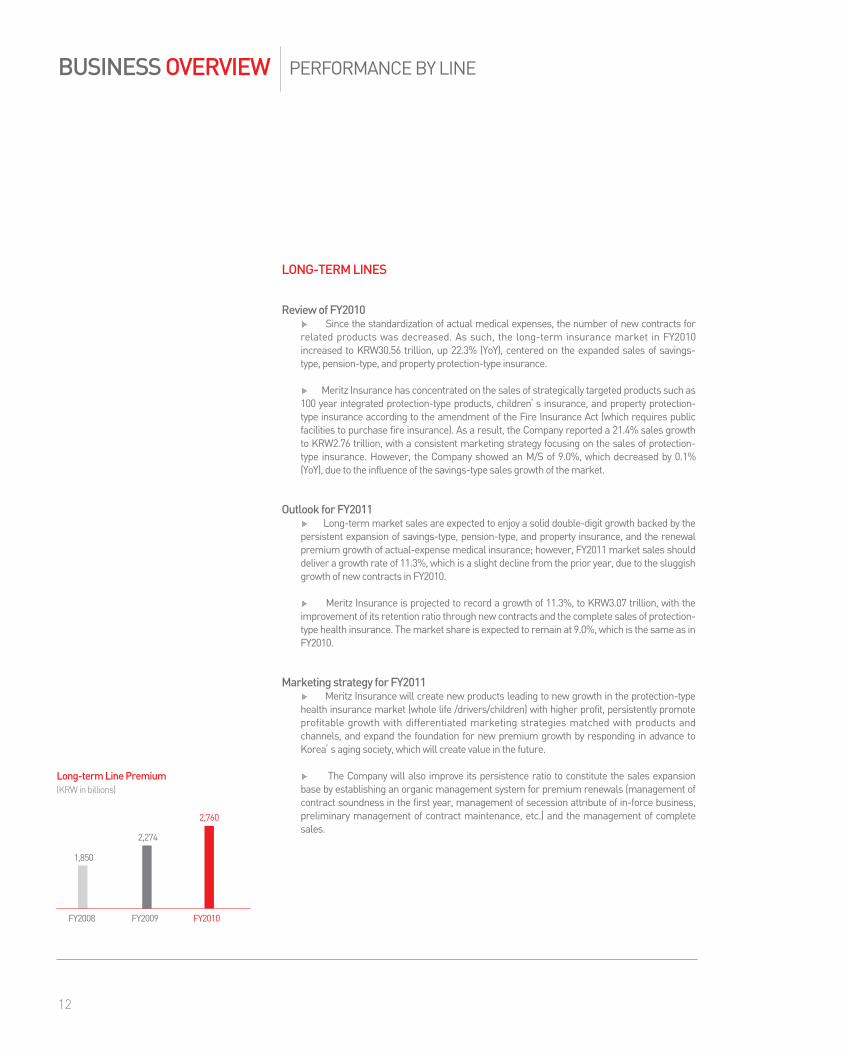

LONG-TERM LINES

Review of FY2010Since the standardization of actual medical expenses, the number of new contracts for

related products was decreased. As such, the long-term insurance market in FY2010increased to KRW30.56 trillion, up 22.3% (YoY), centered on the expanded sales of savings-type, pension-type, and property protection-type insurance.

Meritz Insurance has concentrated on the sales of strategically targeted products such as100 year integrated protection-type products, children’s insurance, and property protection-type insurance according to the amendment of the Fire Insurance Act (which requires publicfacilities to purchase fire insurance). As a result, the Company reported a 21.4% sales growthto KRW2.76 trillion, with a consistent marketing strategy focusing on the sales of protection-type insurance. However, the Company showed an M/S of 9.0%, which decreased by 0.1%(YoY), due to the influence of the savings-type sales growth of the market.

Outlook for FY2011Long-term market sales are expected to enjoy a solid double-digit growth backed by the

persistent expansion of savings-type, pension-type, and property insurance, and the renewalpremium growth of actual-expense medical insurance; however, FY2011 market sales shoulddeliver a growth rate of 11.3%, which is a slight decline from the prior year, due to the sluggishgrowth of new contracts in FY2010.

Meritz Insurance is projected to record a growth of 11.3%, to KRW3.07 trillion, with theimprovement of its retention ratio through new contracts and the complete sales of protection-type health insurance. The market share is expected to remain at 9.0%, which is the same as inFY2010.

Marketing strategy for FY2011Meritz Insurance will create new products leading to new growth in the protection-type

health insurance market (whole life /drivers/children) with higher profit, persistently promoteprofitable growth with differentiated marketing strategies matched with products andchannels, and expand the foundation for new premium growth by responding in advance toKorea’s aging society, which will create value in the future.

The Company will also improve its persistence ratio to constitute the sales expansionbase by establishing an organic management system for premium renewals (management ofcontract soundness in the first year, management of secession attribute of in-force business,preliminary management of contract maintenance, etc.) and the management of completesales.

Long-term Line Premium(KRW in billions)

FY2008 FY2009 FY2010

2,274

1,850

2,760

BUSINESS OVERVIEW PERFORMANCE BY LINE

13MERITZ INSURANCE ANNUAL REPORT 2010

AUTO LINES

Review of FY2010The auto insurance market in FY2010 recorded KRW11.75 trillion, up by 10.7%, influenced

by the increase of vehicle registrations thanks to greater sales of new automobiles as a resultof the economic recovery and the auto premium hike.

Direct written premium came in at KRW776.2 billion, up 12.2%, influenced by strategicadjustments of the premium rate and an expansion of online auto insurance sales. The marketshare increased by 0.1%, up to 6.3% in FY2010.

Outlook for FY2011The auto insurance market in FY2011 is expected to grow 5.6%, to KRW12.41 trillion, aided

by auto premium hikes and the regulation changes that occurred in FY2010 and by thepersistent increase of premium per vehicle due to the high-class trend of automobiles.

The Company’s auto insurance sales in FY2011 are projected to record a 10.4% growth toKRW856.8 billion, backed up with the expanded growth in the core base areas and theextended promotion of online auto insurance.

Marketing strategy for FY2011The Company’s FY2011 marketing strategy is the preemptive execution of 3S (Smart,

Speedy, and Specialized) focusing on solidifying its position as the 2nd ranking insurancecompany in Korea.The Company will promote growth, concentrating on the core base areas (all the capitalregions and a few metropolitan cities such as Busan, Daegu, and Ulsan), increasing the onlineauto insurance sales, and expanding the selective daily system sales.

Auto Line Premium(KRW in billions)

FY2008 FY2009 FY2010

692727

776

14

COMMERCIAL LINES

Review of FY2010In spite of the negative growth of fire and marine insurance products, the commercial

insurance market in FY2010 presented sales of KRW4.40 trillion, up 6.9%, concentrating onaccident, comprehensive, and other commercial insurances.

The Company showed a performance of KRW299.7 billion, down 6.9%, due to the baseeffect from the high growth of engineering insurance of last year and the reconstitution of theportfolio conforming to the profit oriented business strategy. The Company presented a 6.8%market share in FY2010.

Outlook for FY2011In spite of the projected negative growth for engineering and marine insurance due to the

slowdown of construction business and the appreciation of the Korean won, the commercialinsurance market of FY2011 is expected to grow 5.0%, to KRW4.62 trillion, thanks to expandednew demands for liability insurance and new types of commercial lines, the steady growthtrend of group accident and comprehensive insurance, and the continuous expansion ofoverseas business.

Meritz Insurance’s sales target in commercial lines is KRW269.0 billion, down 10.2% with5.9% of the market share (M/S 6.6% in the core profit market). The Company has removed the14% non-profit business from the existing sales amount according to the business remodelingstrategy concentrating on profit and based on risk management.

Marketing strategy for FY2011Meritz Insurance is planning to strengthen its profit-oriented sales portfolio by putting

resources into the core profit market. In addition, the Company will extend the profit scale andpromote the marketing strategy for securing the future profit creation power despite theshrinkage of the sales by ensuring competitiveness through the expansion of infrastructureand systematic R&D for the high grow new market to secure the future profit.Meritz Insurance will reallocate resources into profit-oriented sales, reform the assessmentand compensation system, and differentiate the customer service. Furthermore, the Companywill invest in expanding infrastructure for new market and strengthening the systematic R&Dand core capability for each value chain.

Commercial Line Premium(KRW in billions)

FY2008 FY2009 FY2010

322320 300

15MERITZ INSURANCE ANNUAL REPORT 2010

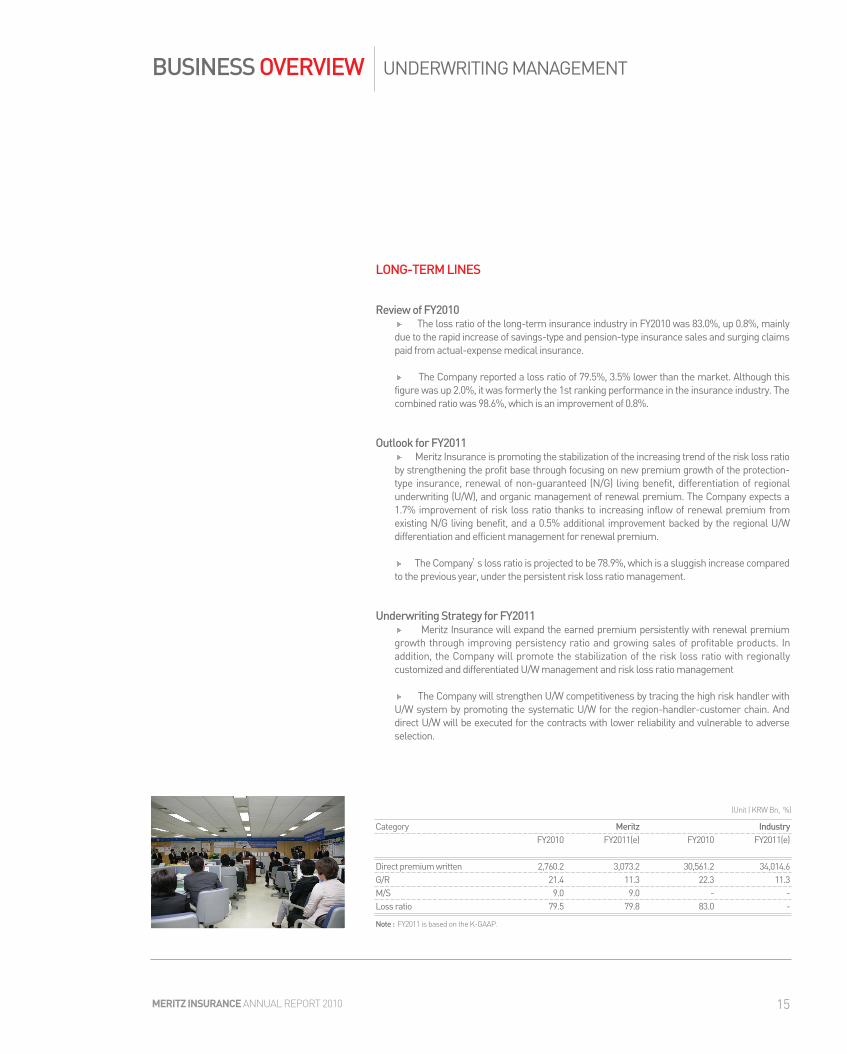

LONG-TERM LINES

Review of FY2010The loss ratio of the long-term insurance industry in FY2010 was 83.0%, up 0.8%, mainly

due to the rapid increase of savings-type and pension-type insurance sales and surging claimspaid from actual-expense medical insurance.

The Company reported a loss ratio of 79.5%, 3.5% lower than the market. Although thisfigure was up 2.0%, it was formerly the 1st ranking performance in the insurance industry. Thecombined ratio was 98.6%, which is an improvement of 0.8%.

Outlook for FY2011Meritz Insurance is promoting the stabilization of the increasing trend of the risk loss ratio

by strengthening the profit base through focusing on new premium growth of the protection-type insurance, renewal of non-guaranteed (N/G) living benefit, differentiation of regionalunderwriting (U/W), and organic management of renewal premium. The Company expects a1.7% improvement of risk loss ratio thanks to increasing inflow of renewal premium fromexisting N/G living benefit, and a 0.5% additional improvement backed by the regional U/Wdifferentiation and efficient management for renewal premium.

The Company’s loss ratio is projected to be 78.9%, which is a sluggish increase comparedto the previous year, under the persistent risk loss ratio management.

Underwriting Strategy for FY2011Meritz Insurance will expand the earned premium persistently with renewal premium

growth through improving persistency ratio and growing sales of profitable products. Inaddition, the Company will promote the stabilization of the risk loss ratio with regionallycustomized and differentiated U/W management and risk loss ratio management

The Company will strengthen U/W competitiveness by tracing the high risk handler withU/W system by promoting the systematic U/W for the region-handler-customer chain. Anddirect U/W will be executed for the contracts with lower reliability and vulnerable to adverseselection.

Category Meritz IndustryFY2010 FY2011(e) FY2010 FY2011(e)

Direct premium written 2,760.2 3,073.2 30,561.2 34,014.6G/R 21.4 11.3 22.3 11.3M/S 9.0 9.0 - -Loss ratio 79.5 79.8 83.0 -

Note : FY2011 is based on the K-GAAP.

(Unit | KRW Bn, %)

BUSINESS OVERVIEW UNDERWRITING MANAGEMENT

16

AUTO LINES

Review of FY2010The loss ratio of the auto insurance market in FY2010 was 79.6%, up 6.0%. The higher

auto loss ratio was attributed to the increase of vehicle traffics due to the economic recovery,increase of accident rate due to the adverse weather conditions in the winter season, andincrease of vehicle claims due to hike in ceiling for property damages.

The Company recorded a worsening of its loss ratio, by 4.8%, to 80.3%.

Outlook for FY2011The loss ratio of auto insurance market in FY2011 is estimated to be 77.6%, improved by

2.0%. It is based on the impact of premium increase and the regulation change of proportionaldeductible from fixed amount to variable rate (decreasing factor) and the impact of increasinginsurance premiums and accident rate (increasing factor).

The Company is targeting a 77% auto loss ratio in FY2011, and will accomplish thisthrough pricing strategy and through the differentiation and efficiency of underwriting.

Underwriting Strategy for FY2011The Company is concentrating on improving the efficiency/profitability and operating

expense efficiency through U/W guideline operation. Such a profit improvement strategy willbe promoted through the expansion of U/W guideline differentiation for each channel and thesupport for the sales of profitable products. The P/F improvement through the growth strategyfocusing on the core bases and the refinement of risk grade assessment system willcontribute to the stabilization of loss ratio. The Company’s auto insurance profit will bestabilized by seeking the ways to improve loss ratio through improvement of U/W process andexpansion of superior coverages.

Category Meritz IndustryFY2010 FY2011(e) FY2010 FY2011(e)

Direct premium written 776.2 856.8 11,750.7 12,406.8G/R 12.2 10.4 10.7 5.6M/S 6.3 6.6 - -L/R 80.3 77.0 79.6 77.6

Note : FY2011 is based on the K-GAAP.

(Unit | KRW Bn, %)

17MERITZ INSURANCE ANNUAL REPORT 2010

COMMERCIAL LINES

Review of FY2010Amidst a downward trend in the premium rates of primary products, along with

intensified price competition due to a growing number of insurers in the marketplace, theindustry's loss ratio for commercial lines in FY2010 declined by 8.4%, to 66.2%, or 2.9%, to60.7%, excluding RG charges. The growth of group accident insurance with the high loss ratioand natural disasters also affected a higher loss ratio.

In line with this, Meritz Insurance recorded 60.5%, slightly higher than the previous year.RG has been excluded based on the Company’s profit-oriented business strategy.

Outlook for FY2011Meritz Insurance is projected to record a 53.6% loss ratio in commercial lines, an

improvement of 6.9%, through business remodeling based on profit-oriented businessstrategy.

Underwriting Strategy for FY2011The Company has persistently promoted a solid U/W strategy since FY2009 with U/W

profit under the first priority. The Company will accomplish its transition into a thorough profitcenter by dividing the business type into profitability, risk, and U/W competitiveness, and byapplying differentiated U/W strategic stances for each division.

In order to achieve the strategic objectives,Consider the potential risk factors such as habitual sales and strengthen the reinsurance risk management by managing the accumulated reserves for each cat risktype.Plan to concentrate on the reinforcement of core capabilities such as innovation of the U/W process, improvement of the U/W system, development and promotion of humancapability improvement programs, and improvement of pricing capability.

Category Meritz IndustryFY2010 FY2011(e) FY2010 FY2011(e)

Direct premium written 299.7 269.0 4,395.7 4,615.5G/R (6.9) (10.2) 6.9 5.0M/S 6.8 5.9 - -L/R 69.7 58.1 66.2 55.0

(Unit | KRW Bn, %)

18

Review of FY2010

The invested assets of FY2010 were KRW5.37 trillion, up by 16%. The investment profit wasKRW257 billion with a 5.3% investment yield, up 0.4%.

By continuously promoting the improvement of asset portfolio to secure the stable investmentprofit since FY2009, the Company has expanded the portion of fixed income assets includingbonds and loans to 72.4%, up by 3.9% to KRW719.2 billion. As a result, the Company built upthe capability to generate the annual profit of KRW210 billion.

In terms of risk management, the Company is trying to minimize interest rate risk bymanaging the matching ratio of duration for liabilities (long-term/annuity account) over 80%.

Category FY2010 DurationAssets Liabilities Matching ratio

Long-term 4.01 5.03 80%Pension 5.12 5.09 101%Total of special accounts 4.21 5.04 84%

BUSINESS OVERVIEW INVESTMENT MANAGEMENT

19MERITZ INSURANCE ANNUAL REPORT 2010

Investment Environment of FY2011

The 2011 global financial market shows recovering processes at different speeds as isindicated in the contradictory polices - retrenchment policy of emerging countries and liquidityprovision of advanced countries through financial and monetary policy.

The stock market is faced with considerable volatility caused by the weakened economicmomentum of G2 countries (USA and China), concern about financial crisis in SouthernEuropean countries, such as Greece, and the termination of quantitative easing (QE2).However, it is projected that the G2 economy will return to recovery and the risk factors will beresolved in the second half. As such, it is expected to show a bull market in the annualviewpoint.

The interest rate may not show an increasing trend, considering the conditions of investors’buying power based on the weakened economy momentum, sluggish inflation rate, andabundant liquidity; however, it is expected that the interest rate will not drop down additionallyfrom current level considering the normalization of base rate and the current market interestrate at the level of financial crisis before. There may be ups and downs in the box zone in thefirst half, and is expected to be a gradually increasing trend as a result of the dissolution ofuncertainty.

Asset Management in FY2011

Meritz Insurance is projecting to achieve investment profits of KRW269.1 billion, based on a4.7% investment yield. Management will thus put forth its utmost efforts to acquire additionalfixed-income assets and restructure performance-based assets to broaden our profitability.

In terms of stocks, the Company will enhance the profitability through appropriate assetdistribution and market timing strategy, as it is expected that the stock market volatility will beenlarged in the rising trend of stock indexes.

For bond investment, the Company will focus on the management of stability and profitabilitywhile balancing aggressive operation and performing selective investment in blue-chipcompanies. The Company is planning to purchase overseas bonds and A.I. (AlternativeInvestments), focusing on products such as principal guaranteed products, yield-up products,and absolute profit pursuing products that exceed the bond yield within the limited market risk,while avoiding the pure index products of high volatility.

In case of loan assets, the Company will reinforce the preliminary screening of debtors withcredit and collateral analysis to secure the profitability and stability, and concentrate in theenhancement of asset soundness through positive and efficient post-management.

20

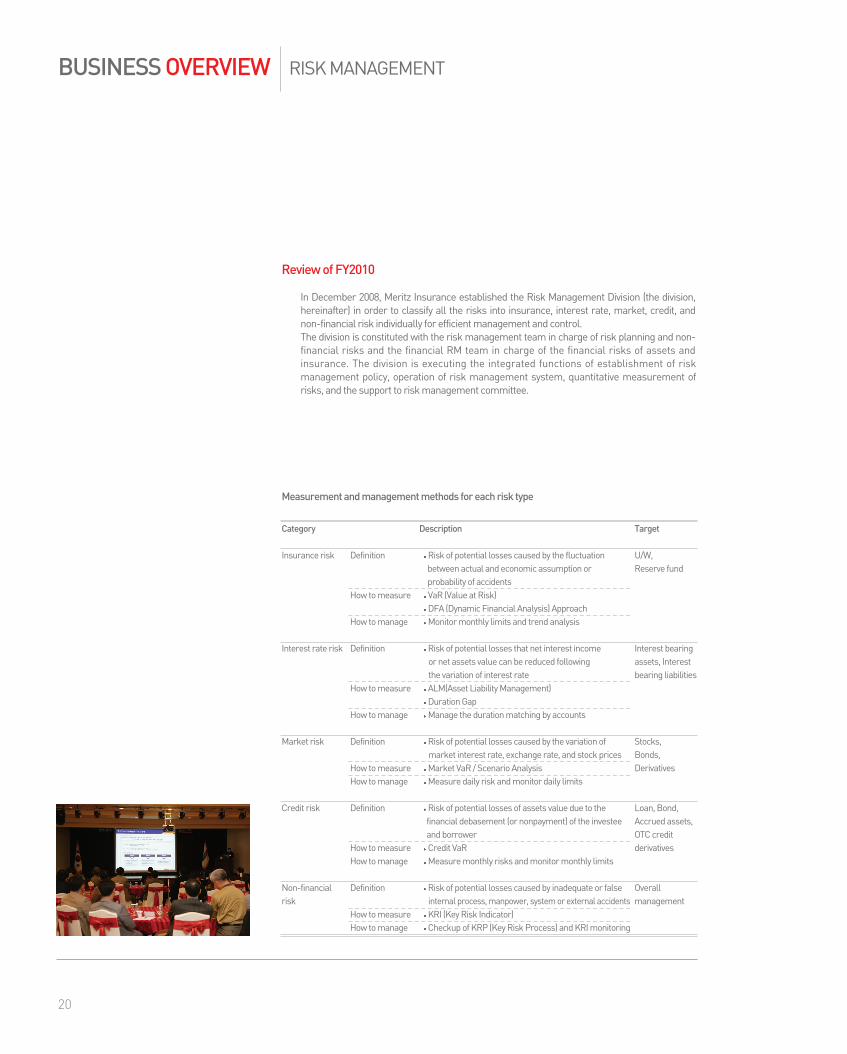

Review of FY2010

In December 2008, Meritz Insurance established the Risk Management Division (the division,hereinafter) in order to classify all the risks into insurance, interest rate, market, credit, andnon-financial risk individually for efficient management and control.The division is constituted with the risk management team in charge of risk planning and non-financial risks and the financial RM team in charge of the financial risks of assets andinsurance. The division is executing the integrated functions of establishment of riskmanagement policy, operation of risk management system, quantitative measurement ofrisks, and the support to risk management committee.

Category Description Target

Insurance risk Definition Risk of potential losses caused by the fluctuation U/W, between actual and economic assumption or Reserve fundprobability of accidents

How to measure VaR (Value at Risk)DFA (Dynamic Financial Analysis) Approach

How to manage Monitor monthly limits and trend analysis

Interest rate risk Definition Risk of potential losses that net interest income Interest bearingor net assets value can be reduced following assets, Interestthe variation of interest rate bearing liabilities

How to measure ALM(Asset Liability Management)Duration Gap

How to manage Manage the duration matching by accounts

Market risk Definition Risk of potential losses caused by the variation of Stocks, market interest rate, exchange rate, and stock prices Bonds,

How to measure Market VaR / Scenario Analysis DerivativesHow to manage Measure daily risk and monitor daily limits

Credit risk Definition Risk of potential losses of assets value due to the Loan, Bond,financial debasement (or nonpayment) of the investee Accrued assets,and borrower OTC credit

How to measure Credit VaR derivativesHow to manage Measure monthly risks and monitor monthly limits

Non-financial Definition Risk of potential losses caused by inadequate or false Overall risk internal process, manpower, system or external accidents management

How to measure KRI (Key Risk Indicator)How to manage Checkup of KRP (Key Risk Process) and KRI monitoring

Measurement and management methods for each risk type

BUSINESS OVERVIEW RISK MANAGEMENT

21MERITZ INSURANCE ANNUAL REPORT 2010

Risk Management Committee

The risk management committee is comprised of the CEO and two outside directors, who arethe financial experts, for its operation. The Committee held seven sessions in FY2010 todeliberate on and resolve critical bills. The matters for resolution were determination of risklimits and hurdle rates, strategic asset allocation (SAA), derivatives operation strategy, renewalof reinsurance treaty, assumed interest rate of long-term insurance and annuities, maximumallowance of minimum guaranteed interest rate, maximum interest rate allowance forpension insurance, risk management regulations, and amendment of reinsurancemanagement guidelines. The matters for reporting were annual plan of risk management,synthetic analysis of risk status, operation results of investment/loan monitoring board andLOB monitoring board, report of risk analysis and countermeasures, items related to thesupervision systems of RBC/RAAS, checkup of credit review, and inspection result of internalcontrol over the reinsurance.

The committee members have a very high perception on risk management, and they aresupporting the Company with keen interest for the advancement of risk management andsettlement of internal risk management culture.The committee has placed particular emphasis on the importance of risk management sincethe financial crisis, and is focusing on the macro-risk management of the whole Companythrough quarterly inspections of all the assets, detailed checkup of the contracts possessed,inspection of reinsurance operation status, and promotion of its improvement measures.

Risk Management Strategy for FY2011

In FY2011, Meritz Insurance intends to concentrate on risk management against the worst-case ‘killer’risks by establishing a preemptive countermeasure system for the overall risks.The Company will establish a risk analysis and response system against the worst situationsby upgrading the risk analysis system (Stress Test) and setting up BCP (Business ContinuityPlan) system, reinforce preventive risk management system through risk factor analysis ofnew investment assets or new insurance products, enhance RBC (Risk Based Capital) ratio,develop additional KRI (Key Risk Indicator) for the efficiency of operation risk management, andestablish risk management mind-set through practicing the RMG (Risk ManagementGuidance).

Strategy direction Establishment of a preemptive risk response system against risks

Strategy tasks 1. Establish risk analysis and responding system against the worst situation

2. Reinforce preventive risk management system for entrance control efficiency

3. Enhance its capital adequacy ratio

4. Enhance its efficiency of operation risk management

5. Settle down risk management culture by strengthening risk management ownership

22

OVERVIEW

BASIS OF PRESENTATION

Management’s discussion and analysis may contain forward-looking statements that are providedto assist in the understanding of anticipated future performance and business plans.

However, such expectations of future performance plans involve certain risk and uncertainty thatcan use actual results to differ materially from those expressed in the forward-looking statements,due to factors beyond the Company’s control. The term “Company,”used herein, without any otherqualifying description, refers to Meritz Fire & Marine Insurance Co., Ltd.

REVIEW OF FY2010

The Company achieved remarkable growth on total assets and direct premium written in FY2010,which is a result of the persistent promotion of profit driven strategy. Direct premium written,earned premium written and net premium written all have been grown up by double-digitincreases consecutively following previous year. It means that overall sales competitiveness hasbeen improved continuously.

Of particular note, capital decreased by 29.6% as a result of capital reduction arising fromlaunching of the financial holding company, which is the first insurance holding company in Koreaand brings combined financial products for the maximum synergy between the group companies.

MANAGEMENT’S DISCUSSION & ANALYSIS

23MERITZ INSURANCE ANNUAL REPORT 2010

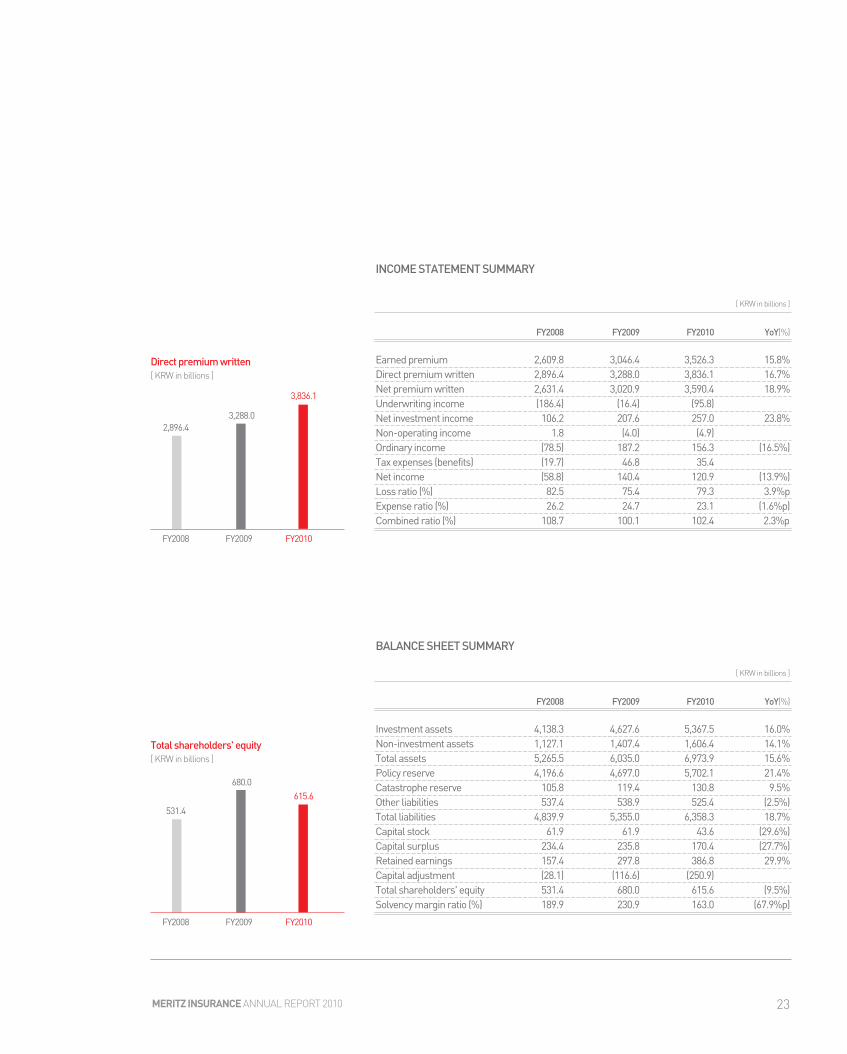

BALANCE SHEET SUMMARY

FY2008 FY2009 FY2010 YoY(%)

Earned premium 2,609.8 3,046.4 3,526.3 15.8%Direct premium written 2,896.4 3,288.0 3,836.1 16.7%Net premium written 2,631.4 3,020.9 3,590.4 18.9%Underwriting income (186.4) (16.4) (95.8)Net investment income 106.2 207.6 257.0 23.8%Non-operating income 1.8 (4.0) (4.9) Ordinary income (78.5) 187.2 156.3 (16.5%)Tax expenses (benefits) (19.7) 46.8 35.4 Net income (58.8) 140.4 120.9 (13.9%)Loss ratio (%) 82.5 75.4 79.3 3.9%pExpense ratio (%) 26.2 24.7 23.1 (1.6%p)Combined ratio (%) 108.7 100.1 102.4 2.3%p

[ KRW in billions ]

FY2008 FY2009 FY2010 YoY(%)

Investment assets 4,138.3 4,627.6 5,367.5 16.0%Non-investment assets 1,127.1 1,407.4 1,606.4 14.1%Total assets 5,265.5 6,035.0 6,973.9 15.6%Policy reserve 4,196.6 4,697.0 5,702.1 21.4%Catastrophe reserve 105.8 119.4 130.8 9.5%Other liabilities 537.4 538.9 525.4 (2.5%)Total liabilities 4,839.9 5,355.0 6,358.3 18.7%Capital stock 61.9 61.9 43.6 (29.6%)Capital surplus 234.4 235.8 170.4 (27.7%)Retained earnings 157.4 297.8 386.8 29.9%Capital adjustment (28.1) (116.6) (250.9)Total shareholders' equity 531.4 680.0 615.6 (9.5%)Solvency margin ratio (%) 189.9 230.9 163.0 (67.9%p)

[ KRW in billions ]

Direct premium written[ KRW in billions ]

FY2008 FY2009 FY2010

3,288.02,896.4

3,836.1

Total shareholders' equity[ KRW in billions ]

FY2008 FY2009 FY2010

680.0

531.4

615.6

INCOME STATEMENT SUMMARY

24

ANALYSIS OF RESULTS OF OPERATIONS

The results of operations of the company demonstrate that FY2010 was a good year. With overallsales competitiveness and profit strength, The results represent the true underlying performanceof the company and significant value for shareholders. In FY2010, direct premium written was up16.7% to KRW3,836.1 billion, primarily owing to observable growth of high margin long-terminsurance products, which are the Company’s prime growth engine

Compared to the FY2009, earned premiums rose 15.8% to KRW3526.3 billion, while net premiumwritten also recorded a notable growth of 18.9%, year on year.

FY2008 FY2009 FY2010 YoY(%)

Commercial lines 320.0 321.9 299.7 (6.9%)Auto lines 726.7 691.8 776.2 12.2%Long-term lines 1,849.6 2,274.4 2,760.2 21.4%Total 2,896.3 3,288.1 3,836.1 16.7%

[ KRW in billions ]

DIRECT PREMIUM WRITTEN BY LINE

FY2008 FY2009 FY2010 YoY(%)

Commercial lines 8.4 7.8 6.8 (1.0%p)Auto lines 7.0 6.2 6.6 0.4%pLong-term lines 9.2 9.1 9.0 (0.1%p)Combined market share 8.5 8.2 8.2 0.0%p

[ KRW in billions ]

MARKET SHARE BY LINE

Note : Long-term lines contain premiums paid at once

Commercial lines 9.8%Auto lines 21.0%Long-term lines 69.2%

Direct premium written by line[ % ]

FY 2009

Commercial lines 7.8%Auto lines 20.2%Long-term lines 72.0%

FY 2010

MANAGEMENT’S DISCUSSION & ANALYSIS

By line, direct premium written of long-term lines soared 21.4% in FY2010 compared to prior yearto KRW2,760.2 billion, which is a good profitability, mainly due to growth strategy with protection-type products and agency market expansion during the period.

The portfolio of long-term lines accounted for 72% from 69.2% of previous year contributed bettersales mix to result in the profit strength structure in FY2010. Auto lines also increased by 12.2% to KRW776.2 billion. However, commercial lines declined to6.9% to KRW299.7 billion.

25MERITZ INSURANCE ANNUAL REPORT 2010

In FY2010, earned premium rose 15.8% than that of previous year to KRW3,526.3 billion. Netpremium written was also up 18.9% to KRW3,590.4 billions.

Incurred losses rose 21.7% in FY2010 to KRW2,795.7 billion. Accordingly, loss ratio adverselyaffected by challenging market condition, increased by 3.9%p to 79.3% from 75.4% in FY2010.

Net operating expense rose 8.3% to KRW815.1 billion, year on year. However, expense ratiocontinuously improved down 1.6%p from 24.7% to 23.1% this year following FY2009.

Consequently, combined ratio up 2.3%p in FY2010 from 100.1% in FY2009 negatively influenced byloss ratio increase.

COMBINED RATIO

FY2008 FY2009 FY2010 YoY(%)

Earned premium 2,609.8 3,046.4 3,526.3 15.8%Incurred losses 2,152.9 2,296.8 2,795.7 21.7%

(1,971.3)Loss ratio (a) 82.5% 75.4% 79.3%Net operating expense 683.5 752.4 815.1 8.3%Expense ratio (b) 26.2% 24.7% 23.1% (1.6%p)Combined ratio (a+b) 108.7% 100.1% 102.4% 2.3%p

(101.7%)

[ KRW in billions ]

Loss ratio (a)[ % ]

FY2008 FY2009 FY2010

75.4%

82.5%

79.3%

Note : Figures in parenthesis exclude the effect the refund guarantee losses in 2008

26

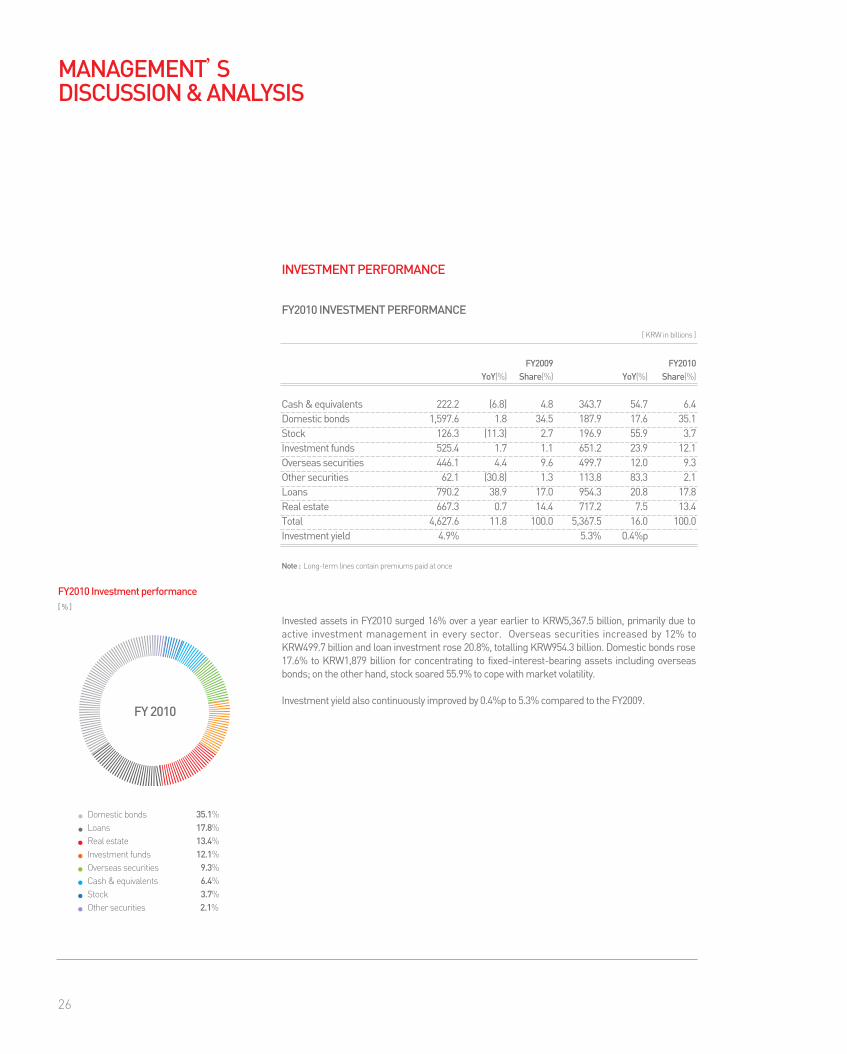

INVESTMENT PERFORMANCE

FY2010 INVESTMENT PERFORMANCE

MANAGEMENT’S DISCUSSION & ANALYSIS

FY2009 FY2010YoY(%) Share(%) YoY(%) Share(%)

Cash & equivalents 222.2 (6.8) 4.8 343.7 54.7 6.4Domestic bonds 1,597.6 1.8 34.5 187.9 17.6 35.1Stock 126.3 (11.3) 2.7 196.9 55.9 3.7Investment funds 525.4 1.7 1.1 651.2 23.9 12.1Overseas securities 446.1 4.4 9.6 499.7 12.0 9.3Other securities 62.1 (30.8) 1.3 113.8 83.3 2.1Loans 790.2 38.9 17.0 954.3 20.8 17.8Real estate 667.3 0.7 14.4 717.2 7.5 13.4Total 4,627.6 11.8 100.0 5,367.5 16.0 100.0Investment yield 4.9% 5.3% 0.4%p

[ KRW in billions ]

Note : Long-term lines contain premiums paid at once

Domestic bonds 35.1%Loans 17.8%Real estate 13.4%Investment funds 12.1%Overseas securities 9.3%Cash & equivalents 6.4%Stock 3.7%Other securities 2.1%

FY2010 Investment performance[ % ]

FY 2010

Invested assets in FY2010 surged 16% over a year earlier to KRW5,367.5 billion, primarily due toactive investment management in every sector. Overseas securities increased by 12% toKRW499.7 billion and loan investment rose 20.8%, totalling KRW954.3 billion. Domestic bonds rose17.6% to KRW1,879 billion for concentrating to fixed-interest-bearing assets including overseasbonds; on the other hand, stock soared 55.9% to cope with market volatility.

Investment yield also continuously improved by 0.4%p to 5.3% compared to the FY2009.

27MERITZ INSURANCE ANNUAL REPORT 2010

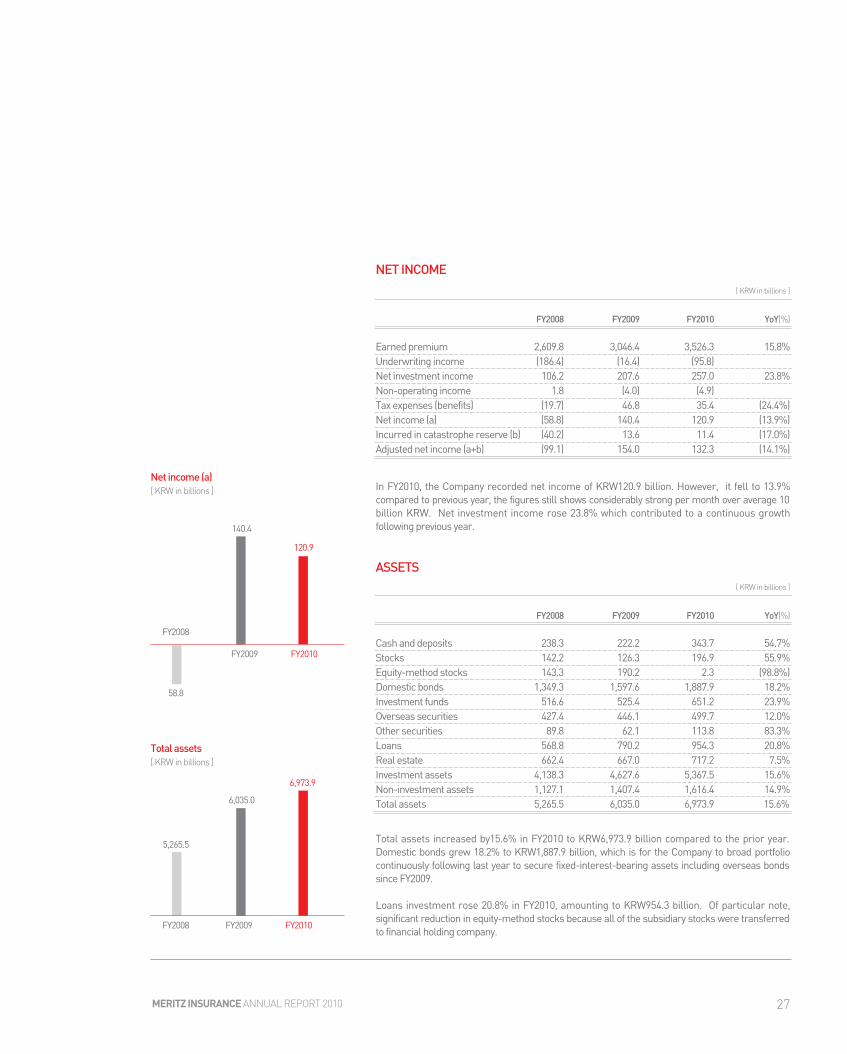

NET INCOME

FY2008 FY2009 FY2010 YoY(%)

Earned premium 2,609.8 3,046.4 3,526.3 15.8%Underwriting income (186.4) (16.4) (95.8)Net investment income 106.2 207.6 257.0 23.8%Non-operating income 1.8 (4.0) (4.9) Tax expenses (benefits) (19.7) 46.8 35.4 (24.4%)Net income (a) (58.8) 140.4 120.9 (13.9%)Incurred in catastrophe reserve (b) (40.2) 13.6 11.4 (17.0%)Adjusted net income (a+b) (99.1) 154.0 132.3 (14.1%)

[ KRW in billions ]

ASSETS

FY2008 FY2009 FY2010 YoY(%)

Cash and deposits 238.3 222.2 343.7 54.7%Stocks 142.2 126.3 196.9 55.9%Equity-method stocks 143.3 190.2 2.3 (98.8%)Domestic bonds 1,349.3 1,597.6 1,887.9 18.2%Investment funds 516.6 525.4 651.2 23.9%Overseas securities 427.4 446.1 499.7 12.0%Other securities 89.8 62.1 113.8 83.3%Loans 568.8 790.2 954.3 20.8%Real estate 662.4 667.0 717.2 7.5%Investment assets 4,138.3 4,627.6 5,367.5 15.6%Non-investment assets 1,127.1 1,407.4 1,616.4 14.9%Total assets 5,265.5 6,035.0 6,973.9 15.6%

[ KRW in billions ]

In FY2010, the Company recorded net income of KRW120.9 billion. However, it fell to 13.9%compared to previous year, the figures still shows considerably strong per month over average 10billion KRW. Net investment income rose 23.8% which contributed to a continuous growthfollowing previous year.

Net income (a)[ KRW in billions ]

FY2009 FY2010

FY2008

140.4

58.8

120.9

Total assets[ KRW in billions ]

FY2008 FY2009 FY2010

6,035.0

6,973.9

5,265.5 Total assets increased by15.6% in FY2010 to KRW6,973.9 billion compared to the prior year.Domestic bonds grew 18.2% to KRW1,887.9 billion, which is for the Company to broad portfoliocontinuously following last year to secure fixed-interest-bearing assets including overseas bondssince FY2009.

Loans investment rose 20.8% in FY2010, amounting to KRW954.3 billion. Of particular note,significant reduction in equity-method stocks because all of the subsidiary stocks were transferredto financial holding company.

28

MANAGEMENT’S DISCUSSION & ANALYSIS

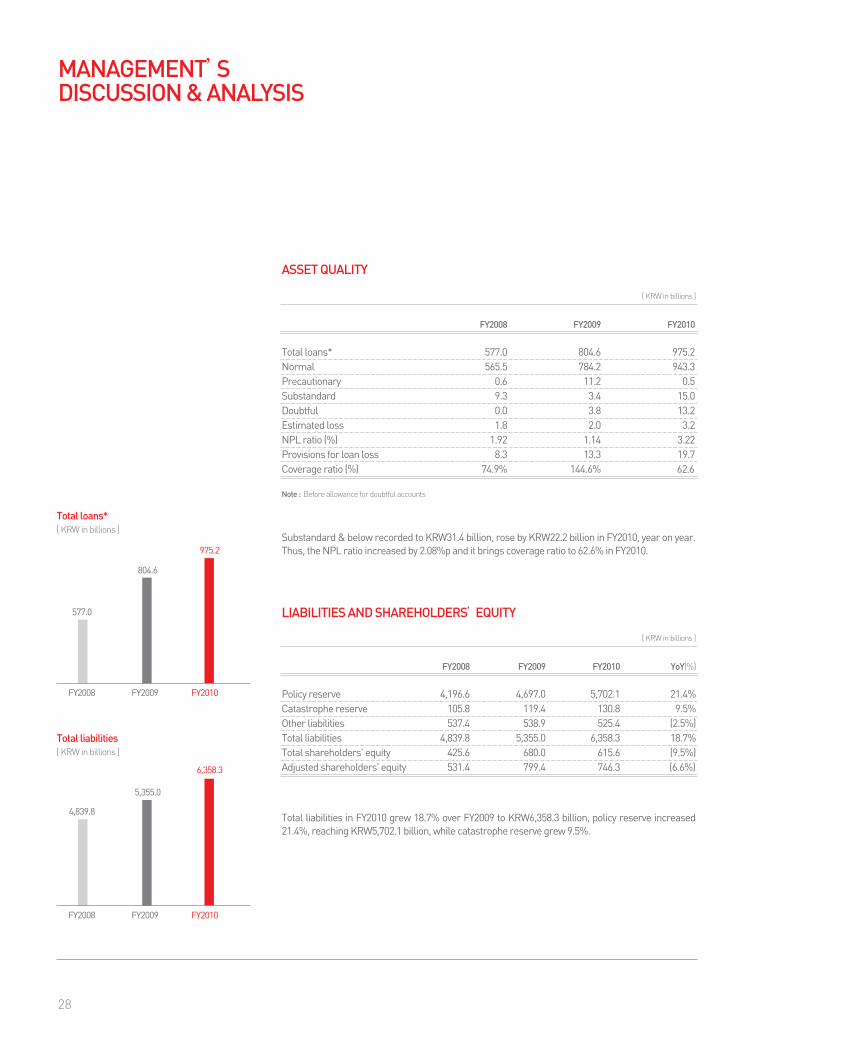

ASSET QUALITY

FY2008 FY2009 FY2010

Total loans* 577.0 804.6 975.2Normal 565.5 784.2 943.3Precautionary 0.6 11.2 0.5Substandard 9.3 3.4 15.0Doubtful 0.0 3.8 13.2Estimated loss 1.8 2.0 3.2NPL ratio (%) 1.92 1.14 3.22Provisions for loan loss 8.3 13.3 19.7Coverage ratio (%) 74.9% 144.6% 62.6

[ KRW in billions ]

LIABILITIES AND SHAREHOLDERS’EQUITY

FY2008 FY2009 FY2010 YoY(%)

Policy reserve 4,196.6 4,697.0 5,702.1 21.4%Catastrophe reserve 105.8 119.4 130.8 9.5%Other liabilities 537.4 538.9 525.4 (2.5%)Total liabilities 4,839.8 5,355.0 6,358.3 18.7%Total shareholders' equity 425.6 680.0 615.6 (9.5%)Adjusted shareholders' equity 531.4 799.4 746.3 (6.6%)

[ KRW in billions ]

Note : Before allowance for doubtful accounts

Total liabilities in FY2010 grew 18.7% over FY2009 to KRW6,358.3 billion, policy reserve increased21.4%, reaching KRW5,702.1 billion, while catastrophe reserve grew 9.5%.

Substandard & below recorded to KRW31.4 billion, rose by KRW22.2 billion in FY2010, year on year.Thus, the NPL ratio increased by 2.08%p and it brings coverage ratio to 62.6% in FY2010.

Total loans*[ KRW in billions ]

FY2008 FY2009 FY2010

804.6

975.2

577.0

Total liabilities[ KRW in billions ]

FY2008 FY2009 FY2010

5,355.0

4,839.8

6,358.3

29MERITZ INSURANCE ANNUAL REPORT 2010

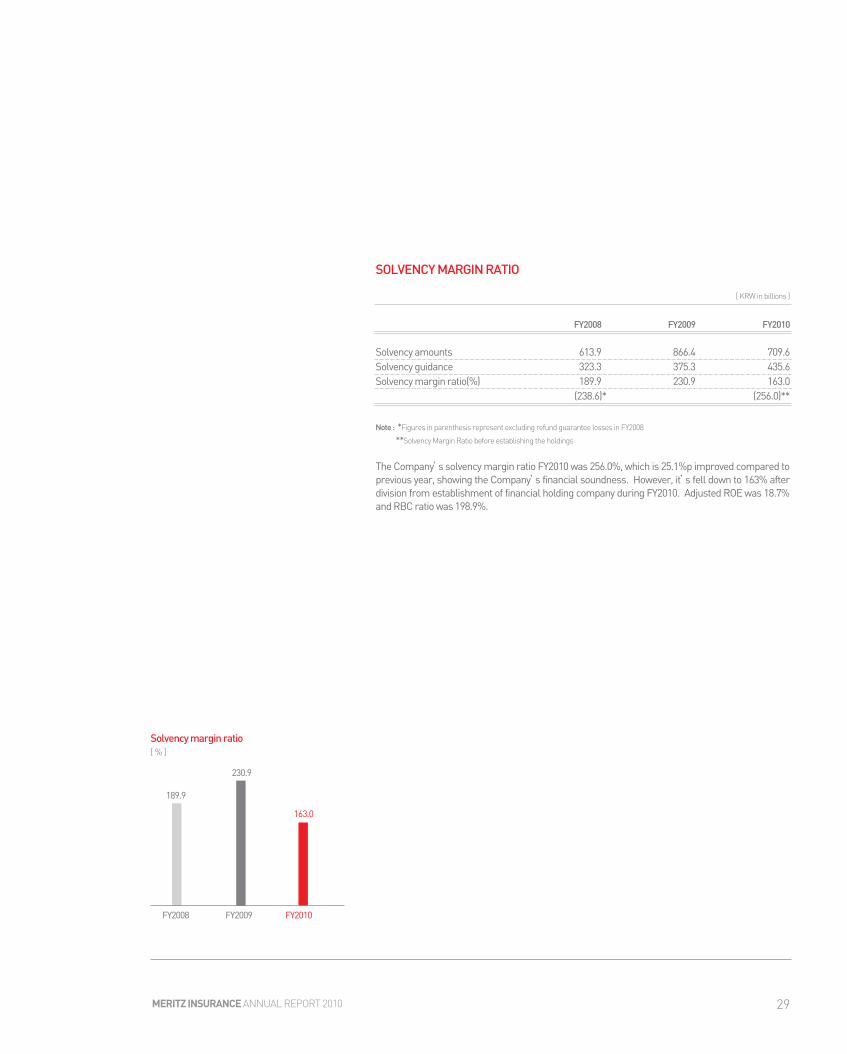

SOLVENCY MARGIN RATIO

FY2008 FY2009 FY2010

Solvency amounts 613.9 866.4 709.6Solvency guidance 323.3 375.3 435.6Solvency margin ratio(%) 189.9 230.9 163.0

(238.6)* (256.0)**

[ KRW in billions ]

Note : *Figures in parenthesis represent excluding refund guarantee losses in FY2008

**Solvency Margin Ratio before establishing the holdings

The Company’s solvency margin ratio FY2010 was 256.0%, which is 25.1%p improved compared toprevious year, showing the Company’s financial soundness. However, it’s fell down to 163% afterdivision from establishment of financial holding company during FY2010. Adjusted ROE was 18.7%and RBC ratio was 198.9%.

Solvency margin ratio[ % ]

FY2008 FY2009 FY2010

230.9

189.9

163.0

30

THE BOARD OF DIRECTORS AND STOCKHOLDERMERITZ FIRE & MARINE INSURANCE CO., LTD.

We have audited the accompanying non-consolidated statements of financial position of Meritz Fire & Marine Insurance Co., Ltd. (the “Company”) as ofMarch 31, 2011 and 2010, and the related non-consolidated statements of income, appropriations of retained earnings, changes in equity and cash flowsfor the years then ended. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion onthese financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the Republic of Korea.

Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of materialmisstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit alsoincludes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statementpresentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the non-consolidated financial statements referred to above present fairly, in all material respects, the non-consolidated financial positionof Meritz Fire & Marine Insurance Co., Ltd. as of March 31, 2011 and 2010, and the results of its financial performance, and its cash flows for the yearsthen ended, in conformity with accounting principles generally accepted in the Republic of Korea.

Accounting principles and auditing standards and their application in practice vary among countries. The accompanying non-consolidated financialstatements are not intended to present the financial position, results of financial performance, and cash flows in accordance with accounting principlesand practices generally accepted in countries other than the Republic of Korea. In addition, the procedures and practices utilized in the Republic of Koreato audit such financial statements may differ from those generally accepted and applied in other countries. Accordingly, this report and theaccompanying non-consolidated financial statements are for use by those who are knowledgeable about Korean accounting principles and auditingstandards and their application in practice.

April 28, 2011

INDEPENDENT AUDITORS’ REPORT

This audit report is effective as of April 28, 2011, the independent auditors’report date. Accordingly, certain material subsequent events or circumstances may have occurredduring the period from the auditors’report date to the time this audit report is used. Such events and circumstances could significantly affect the accompanying non-consolidated financial statements and may result in modifications to this report.

31MERITZ INSURANCE ANNUAL REPORT 2010

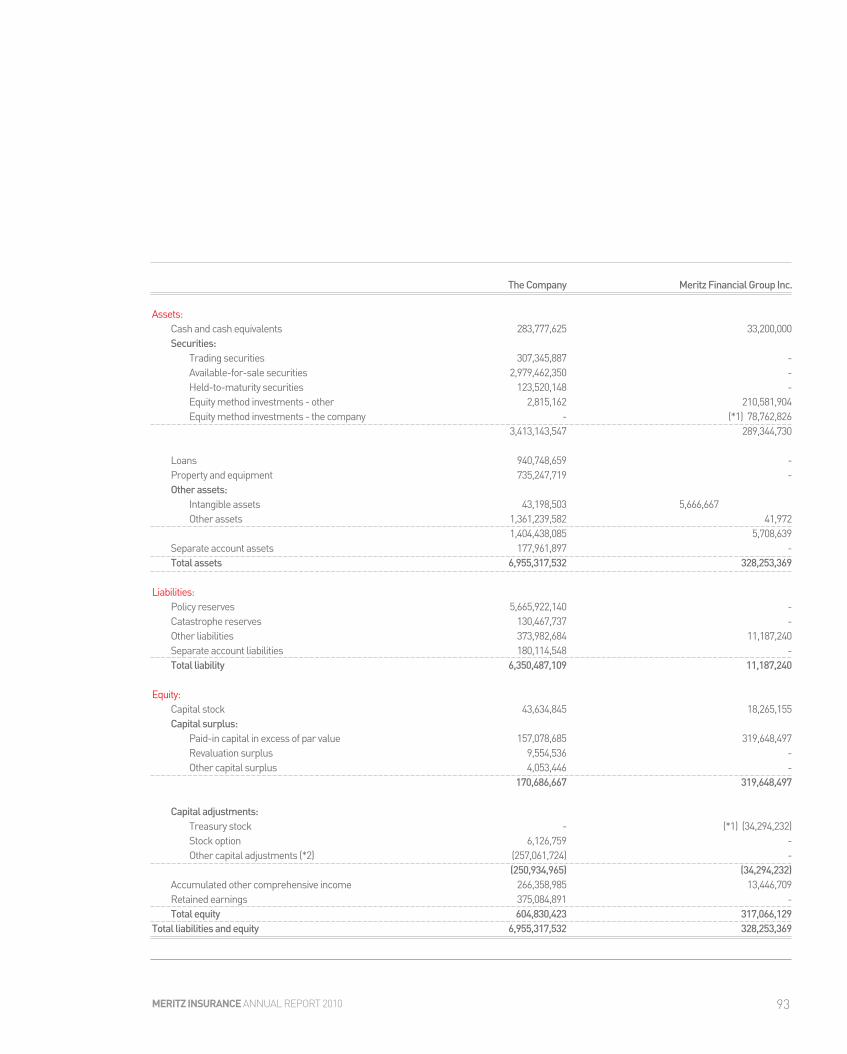

2011 2010

AssetsCash and cash equivalents (Notes 3, 9, 15, 27 and 37) ₩ 125,758,125 ₩ 72,174,312Deposits (Notes 9, 15 and 27) 217,921,858 49,999,460Trading securities (Notes 4, 15 and 27) 438,787,555 176,690,119Available-for-sale securities (Notes 4, 5, 15 and 27) 2,787,322,470 2,387,337,111 Held-to-maturity securities (Notes 4, 5, 6, 15 and 27) 123,355,704 193,567,089Equity method investments (Note 7) 2,815,162 190,238,600 Loans, less allowance for doubtful accounts of \20,893,639thousand in 2011 (\14,357,013 thousand in 2010) (Note 8) 954,307,285 790,244,245Property and equipment (Notes 9 and 22) 735,119,948 681,453,901Intangible assets (Note 10) 42,705,829 17,940,902Deferred acquisition costs (Note 14) 1,013,684,396 840,990,095Other assets, less allowance for doubtful accounts of12,130,925 thousand in 2011(\7,066,264 thousand in 2010)(Note 11) 355,537,615 323,934,654Separate account assets (Note 17) 176,542,850 210,418,544Total assets ₩ 6,973,858,797 ₩ 6,034,989,032

Liabilities and equityLiabilities:

Policy reserves (Notes 16 and 21) ₩ 5,702,119,201 ₩ 4,696,950,444Catastrophe reserves (Note 16) 130,752,257 119,438,218Insurance accounts payables (Notes 8, 15 and 18) 121,403,904 113,342,818Severance and retirement benefits (Note 19) 2,069,708 561,244Other liabilities (Note 20) 217,017,987 210,456,224Separate account liabilities (Note 17)Total liabilities 6,358,296,558 5,355,014,629

Equity: Capital stock (Notes 1 and 22) 43,634,845 61,900,000Capital surplus (Note 22) 170,432,783 235,797,493Capital adjustments (Note 22) (250,934,964) (116,585,558)Accumulated other comprehensive income (Notes 22 and 30) 265,675,762 201,087,426Retained earnings (Note 22) 386,753,813 297,775,042Total equity 615,562,239 679,974,403

Total liabilities and equity ₩ 6,973,858,797 ₩ 6,034,989,032

See accompanying notes.

NON-CONSOLIDATED STATEMENTS OFFINANCIAL POSITIONAS OF MARCH 31, 2011 AND 2010

(Korean won in thousands)

32

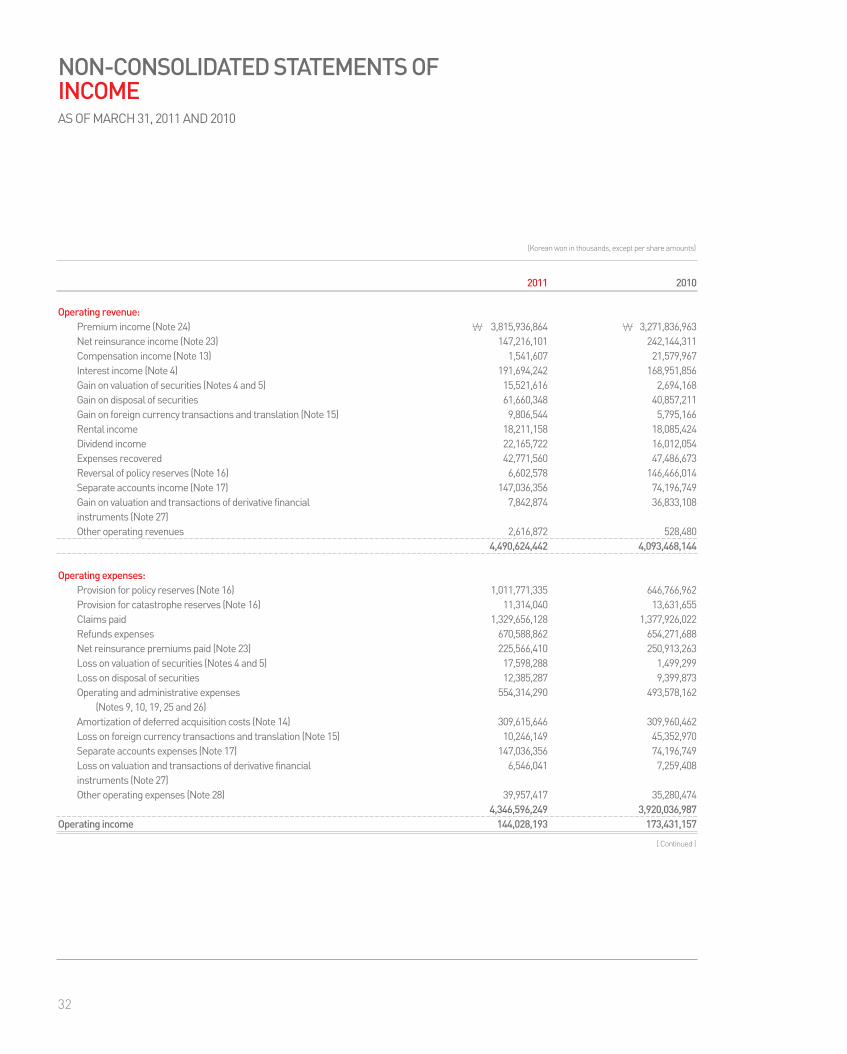

2011 2010

Operating revenue:Premium income (Note 24) ₩ 3,815,936,864 ₩ 3,271,836,963Net reinsurance income (Note 23) 147,216,101 242,144,311Compensation income (Note 13) 1,541,607 21,579,967Interest income (Note 4) 191,694,242 168,951,856Gain on valuation of securities (Notes 4 and 5) 15,521,616 2,694,168Gain on disposal of securities 61,660,348 40,857,211Gain on foreign currency transactions and translation (Note 15) 9,806,544 5,795,166Rental income 18,211,158 18,085,424 Dividend income 22,165,722 16,012,054Expenses recovered 42,771,560 47,486,673Reversal of policy reserves (Note 16) 6,602,578 146,466,014Separate accounts income (Note 17) 147,036,356 74,196,749Gain on valuation and transactions of derivative financial 7,842,874 36,833,108 instruments (Note 27)Other operating revenues 2,616,872 528,480

4,490,624,442 4,093,468,144

Operating expenses:Provision for policy reserves (Note 16) 1,011,771,335 646,766,962Provision for catastrophe reserves (Note 16) 11,314,040 13,631,655Claims paid 1,329,656,128 1,377,926,022Refunds expenses 670,588,862 654,271,688 Net reinsurance premiums paid (Note 23) 225,566,410 250,913,263Loss on valuation of securities (Notes 4 and 5) 17,598,288 1,499,299Loss on disposal of securities 12,385,287 9,399,873Operating and administrative expenses 554,314,290 493,578,162

(Notes 9, 10, 19, 25 and 26)Amortization of deferred acquisition costs (Note 14) 309,615,646 309,960,462Loss on foreign currency transactions and translation (Note 15) 10,246,149 45,352,970Separate accounts expenses (Note 17) 147,036,356 74,196,749Loss on valuation and transactions of derivative financial 6,546,041 7,259,408instruments (Note 27)Other operating expenses (Note 28) 39,957,417 35,280,474

4,346,596,249 3,920,036,987Operating income 144,028,193 173,431,157

(Korean won in thousands, except per share amounts)

NON-CONSOLIDATED STATEMENTS OFINCOMEAS OF MARCH 31, 2011 AND 2010

[ Continued ]

33MERITZ INSURANCE ANNUAL REPORT 2010

2011 2010

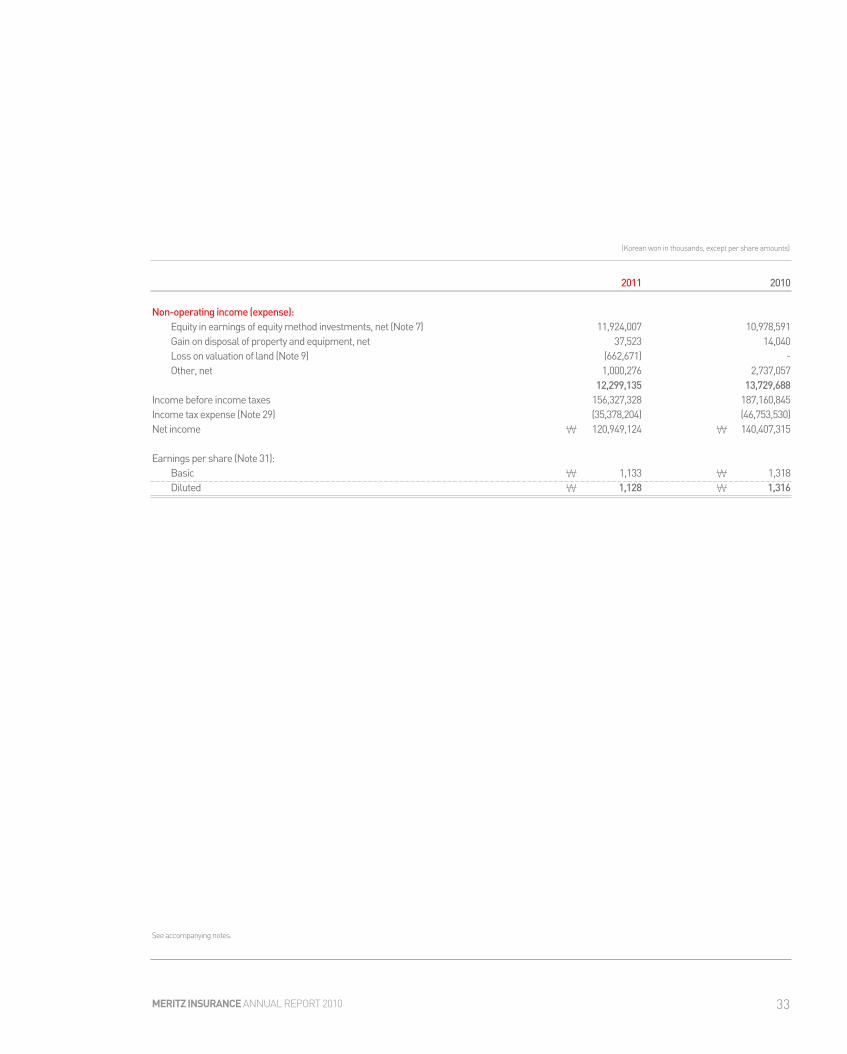

Non-operating income (expense):Equity in earnings of equity method investments, net (Note 7) 11,924,007 10,978,591Gain on disposal of property and equipment, net 37,523 14,040Loss on valuation of land (Note 9) (662,671) - Other, net 1,000,276 2,737,057

12,299,135 13,729,688Income before income taxes 156,327,328 187,160,845Income tax expense (Note 29) (35,378,204) (46,753,530)Net income ₩ 120,949,124 ₩ 140,407,315

Earnings per share (Note 31):Basic ₩ 1,133 ₩ 1,318Diluted ₩ 1,128 ₩ 1,316

See accompanying notes.

(Korean won in thousands, except per share amounts)

34

2011 2010

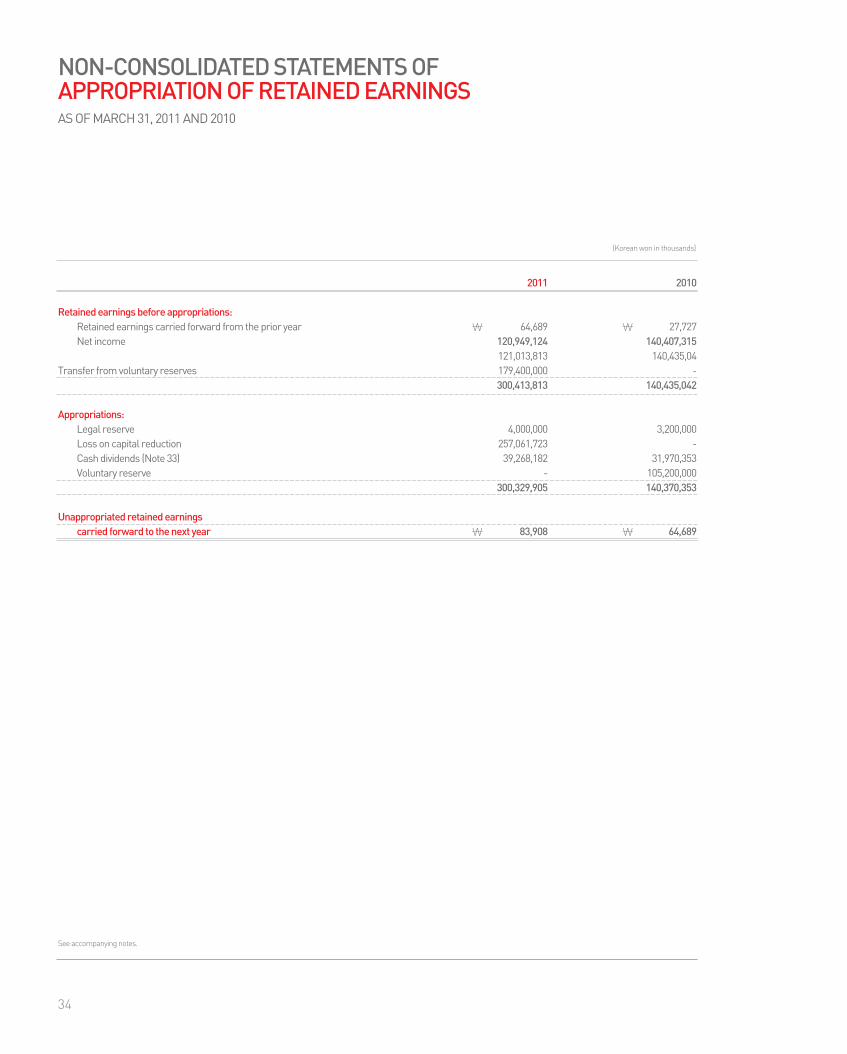

Retained earnings before appropriations:Retained earnings carried forward from the prior year ₩ 64,689 ₩ 27,727 Net income 120,949,124 140,407,315

121,013,813 140,435,04Transfer from voluntary reserves 179,400,000 -

300,413,813 140,435,042

Appropriations: Legal reserve 4,000,000 3,200,000Loss on capital reduction 257,061,723 - Cash dividends (Note 33) 39,268,182 31,970,353Voluntary reserve - 105,200,000

300,329,905 140,370,353

Unappropriated retained earningscarried forward to the next year ₩ 83,908 ₩ 64,689

See accompanying notes.

NON-CONSOLIDATED STATEMENTS OFAPPROPRIATION OF RETAINED EARNINGSAS OF MARCH 31, 2011 AND 2010

(Korean won in thousands)

35MERITZ INSURANCE ANNUAL REPORT 2010

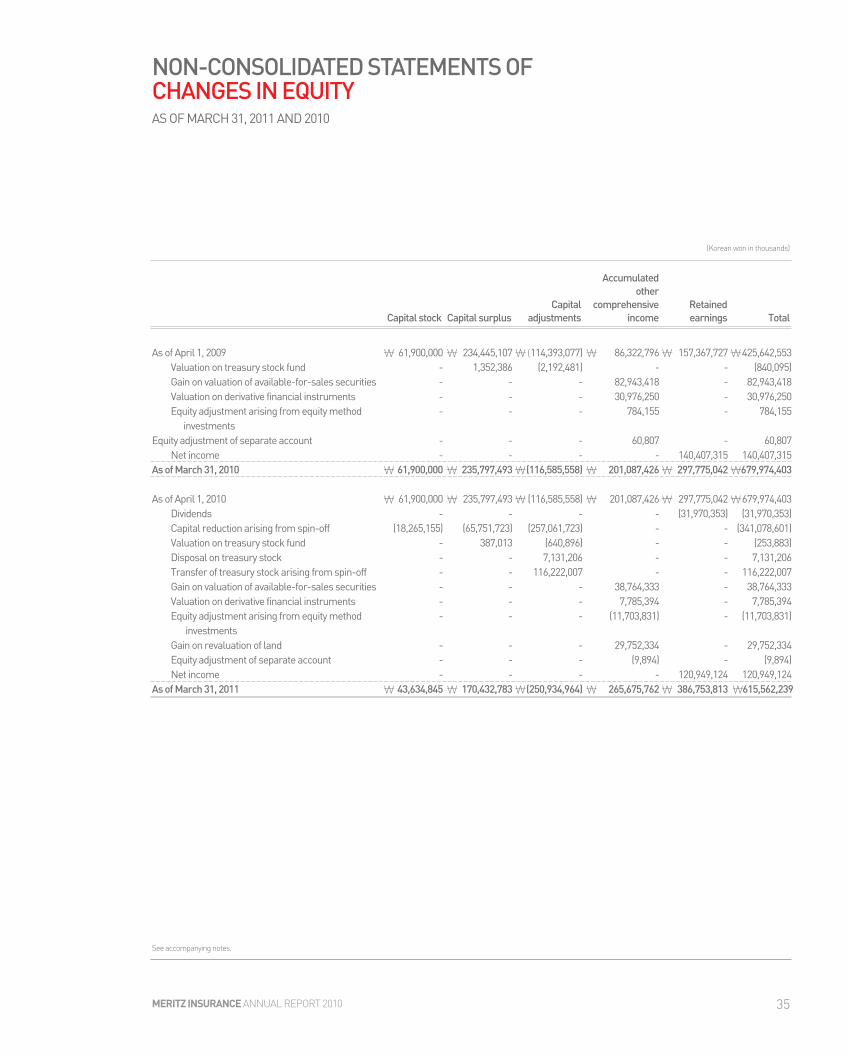

As of April 1, 2009 ₩ 61,900,000 ₩ 234,445,107 ₩(114,393,077) ₩ 86,322,796 ₩ 157,367,727 ₩425,642,553Valuation on treasury stock fund - 1,352,386 (2,192,481) - - (840,095)Gain on valuation of available-for-sales securities - - - 82,943,418 - 82,943,418Valuation on derivative financial instruments - - - 30,976,250 - 30,976,250 Equity adjustment arising from equity method - - - 784,155 - 784,155

investments Equity adjustment of separate account - - - 60,807 - 60,807

Net income - - - - 140,407,315 140,407,315As of March 31, 2010 ₩ 61,900,000 ₩ 235,797,493 ₩(116,585,558) ₩ 201,087,426 ₩ 297,775,042 ₩679,974,403

As of April 1, 2010 ₩ 61,900,000 ₩ 235,797,493 ₩ (116,585,558) ₩ 201,087,426 ₩ 297,775,042 ₩679,974,403Dividends - - - - (31,970,353) (31,970,353)Capital reduction arising from spin-off (18,265,155) (65,751,723) (257,061,723) - - (341,078,601)Valuation on treasury stock fund - 387,013 (640,896) - - (253,883)Disposal on treasury stock - - 7,131,206 - - 7,131,206Transfer of treasury stock arising from spin-off - - 116,222,007 - - 116,222,007Gain on valuation of available-for-sales securities - - - 38,764,333 - 38,764,333Valuation on derivative financial instruments - - - 7,785,394 - 7,785,394Equity adjustment arising from equity method - - - (11,703,831) - (11,703,831)

investmentsGain on revaluation of land - - - 29,752,334 - 29,752,334Equity adjustment of separate account - - - (9,894) - (9,894)Net income - - - - 120,949,124 120,949,124

As of March 31, 2011 ₩ 43,634,845 ₩ 170,432,783 ₩(250,934,964) ₩ 265,675,762 ₩ 386,753,813 ₩615,562,239

See accompanying notes.

NON-CONSOLIDATED STATEMENTS OFCHANGES IN EQUITYAS OF MARCH 31, 2011 AND 2010

(Korean won in thousands)

TotalRetainedearnings

Accumulated other

comprehensiveincome

CapitaladjustmentsCapital surplusCapital stock

36

2011 2010

Cash flows from operating activities:Net income ₩ 120,949,124 ₩ 140,407,315Adjustments to reconcile net income to net cash provided by

operating activities:Net provision for policy and catastrophe reserves 1,016,482,797 513,932,603Loss (gain) on valuation of securities, net 2,076,672 (1,194,869)Depreciation 18,765,346 17,889,190Amortization 6,031,983 3,669,817Provision for severance and retirement benefits 9,310,303 8,868,924 Provision for doubtful accounts, net 15,286,688 5,129,485Amortization of deferred acquisition costs 309,615,646 309,960,462Loss on foreign currency translation, net 3,833 25,695,336Gain on valuation of derivative financial instruments, net (4,675,951) (20,102,809)Equity in earnings of equity method investments, net (11,924,007) (10,978,591)Loss on revaluation of land 662,671 - Others, net (1,579,130) (21,594,010)Changes in operating assets and liabilities

Deposit (68,840,711) 18,320,555Trading securities (257,675,080) 73,172,145 Available-for-sale securities (355,060,092) (255,237,254)Held-to-maturity securities 69,975,385 44,575,224Dividend income from equity method investment - 2,896,492 Loans (174,285,067) (226,490,708)Deferred acquisition costs (482,309,946) (505,341,449)Separate account liabilities 3,952,628 (8,860,583)Insurance accounts payables 8,288,946 13,716,732Payment of severance and retirement benefits (1,511,035) (3,360,625)Separate account assets 580,994 1,823,294 Others, net (28,753,501) (39,845,113)Net cash provided by operating activities 195,368,496 87,051,563

(Korean won in thousands, except per share amounts)

NON-CONSOLIDATED STATEMENTS OFCASH FLOWSAS OF MARCH 31, 2011 AND 2010

[ Continued ]

37MERITZ INSURANCE ANNUAL REPORT 2010

2011 2010

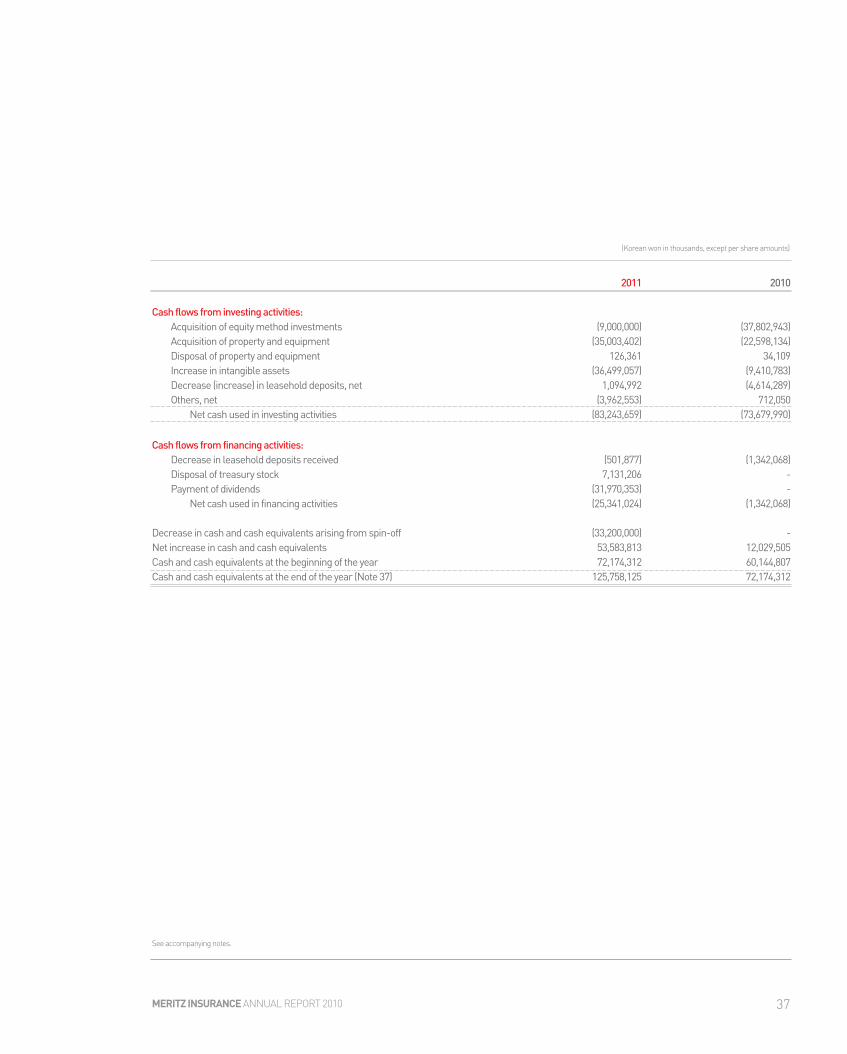

Cash flows from investing activities:Acquisition of equity method investments (9,000,000) (37,802,943)Acquisition of property and equipment (35,003,402) (22,598,134)Disposal of property and equipment 126,361 34,109 Increase in intangible assets (36,499,057) (9,410,783)Decrease (increase) in leasehold deposits, net 1,094,992 (4,614,289)Others, net (3,962,553) 712,050

Net cash used in investing activities (83,243,659) (73,679,990)

Cash flows from financing activities:Decrease in leasehold deposits received (501,877) (1,342,068)Disposal of treasury stock 7,131,206 - Payment of dividends (31,970,353) -

Net cash used in financing activities (25,341,024) (1,342,068)

Decrease in cash and cash equivalents arising from spin-off (33,200,000) -Net increase in cash and cash equivalents 53,583,813 12,029,505Cash and cash equivalents at the beginning of the year 72,174,312 60,144,807Cash and cash equivalents at the end of the year (Note 37) 125,758,125 72,174,312

See accompanying notes.

(Korean won in thousands, except per share amounts)

38

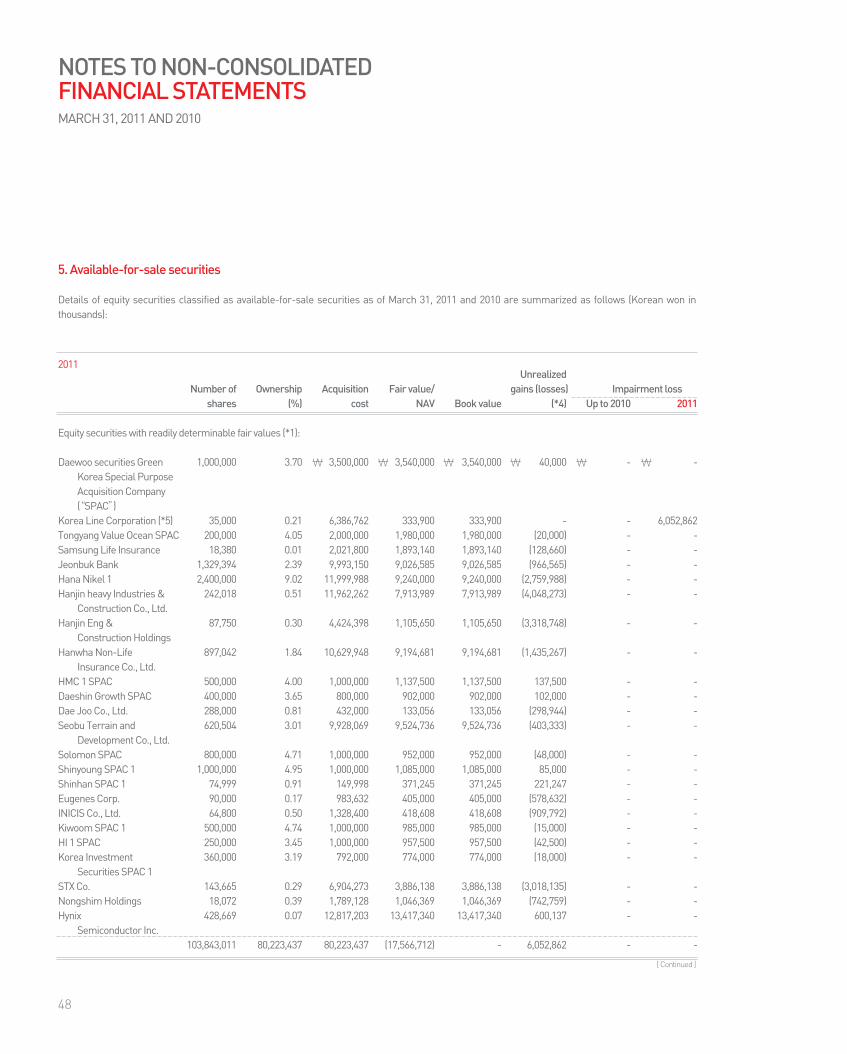

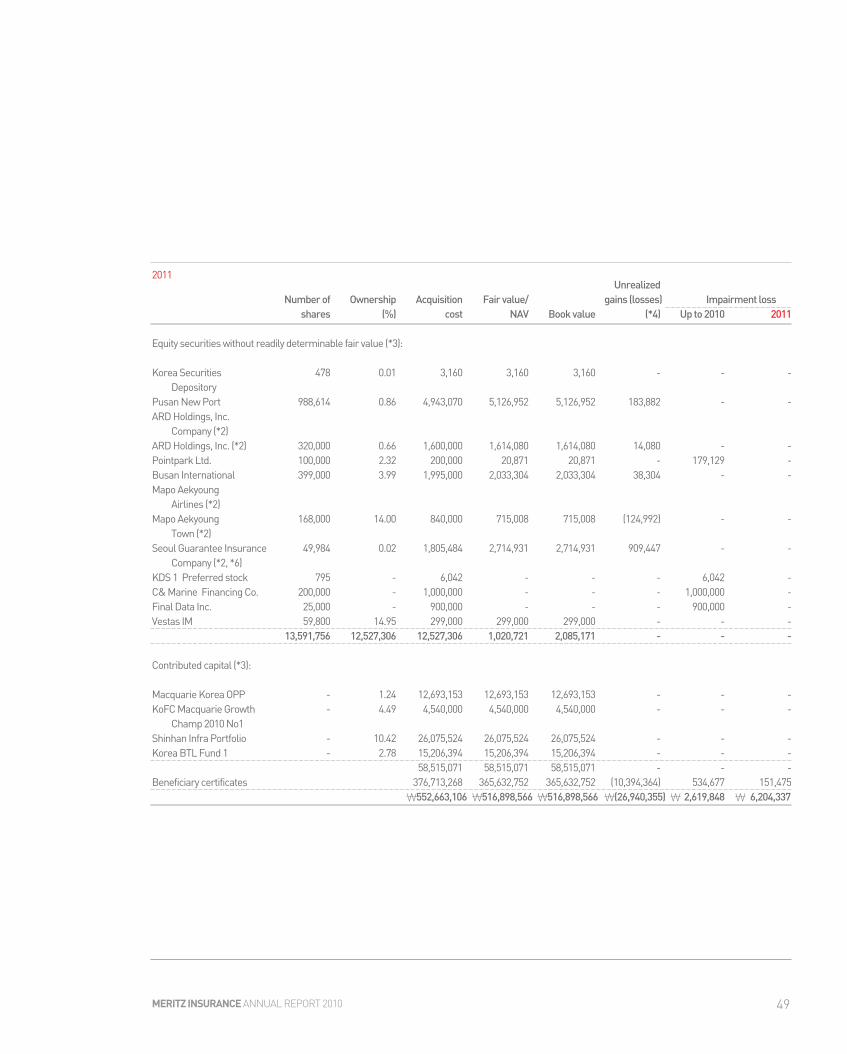

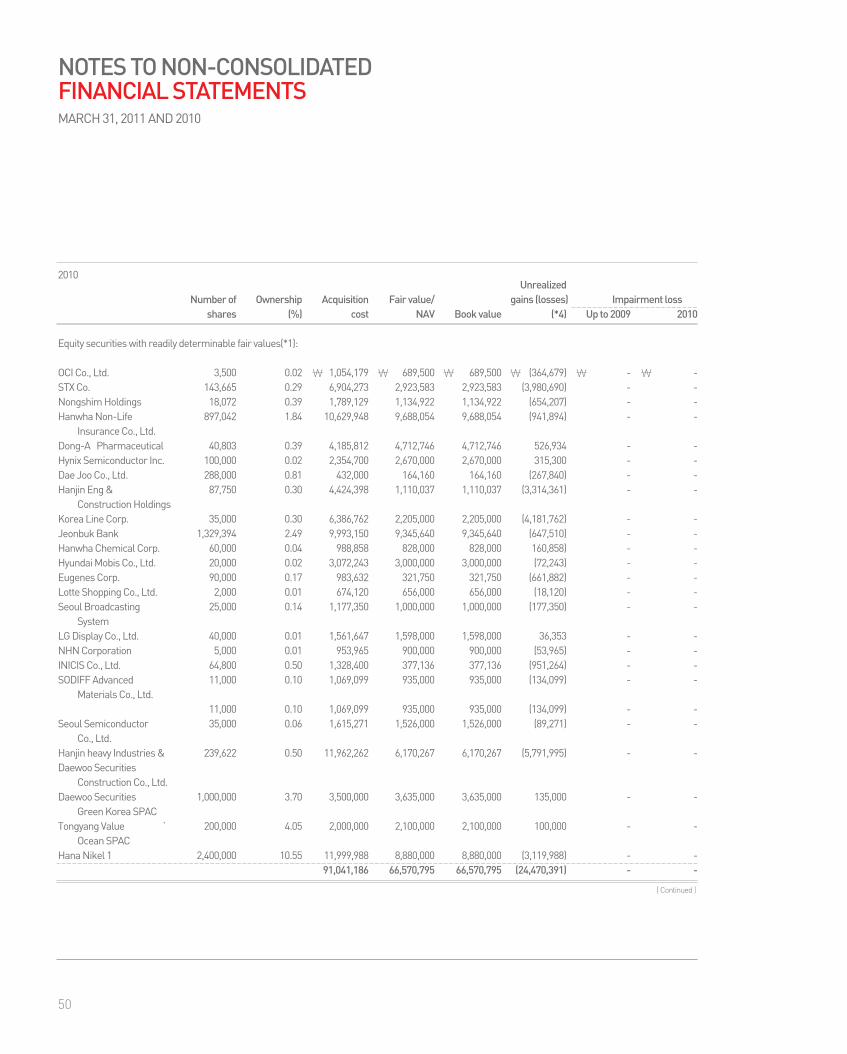

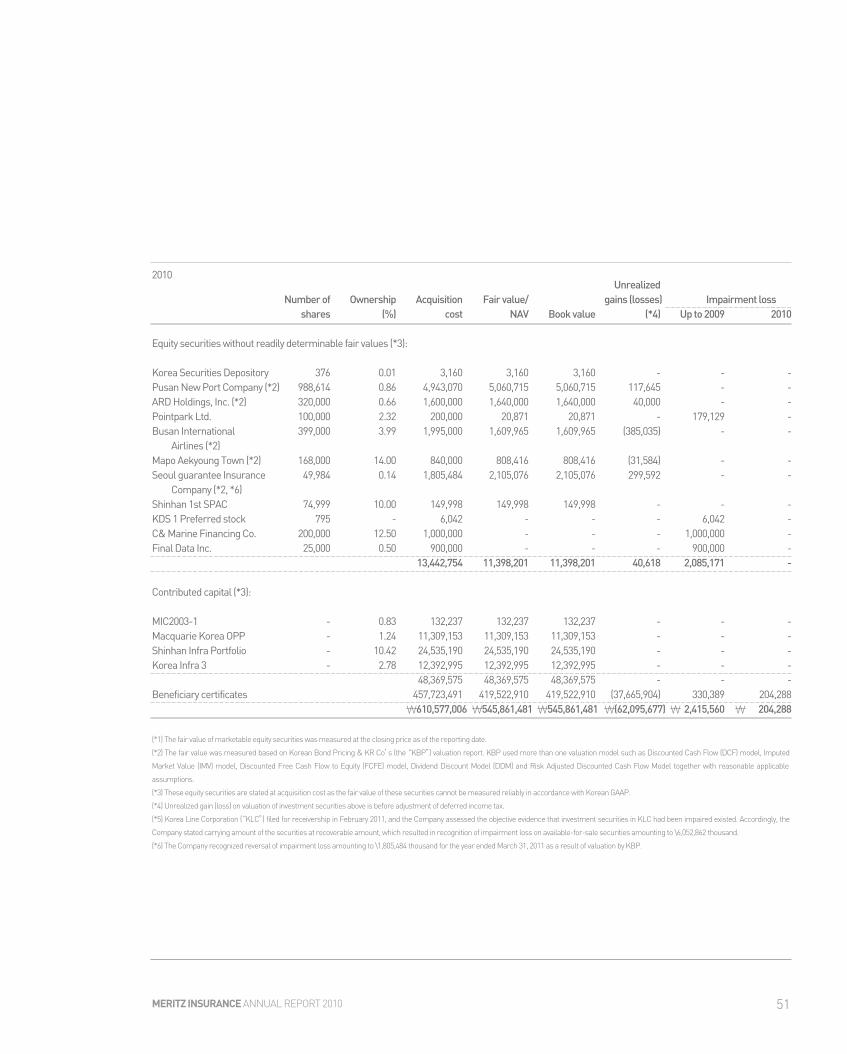

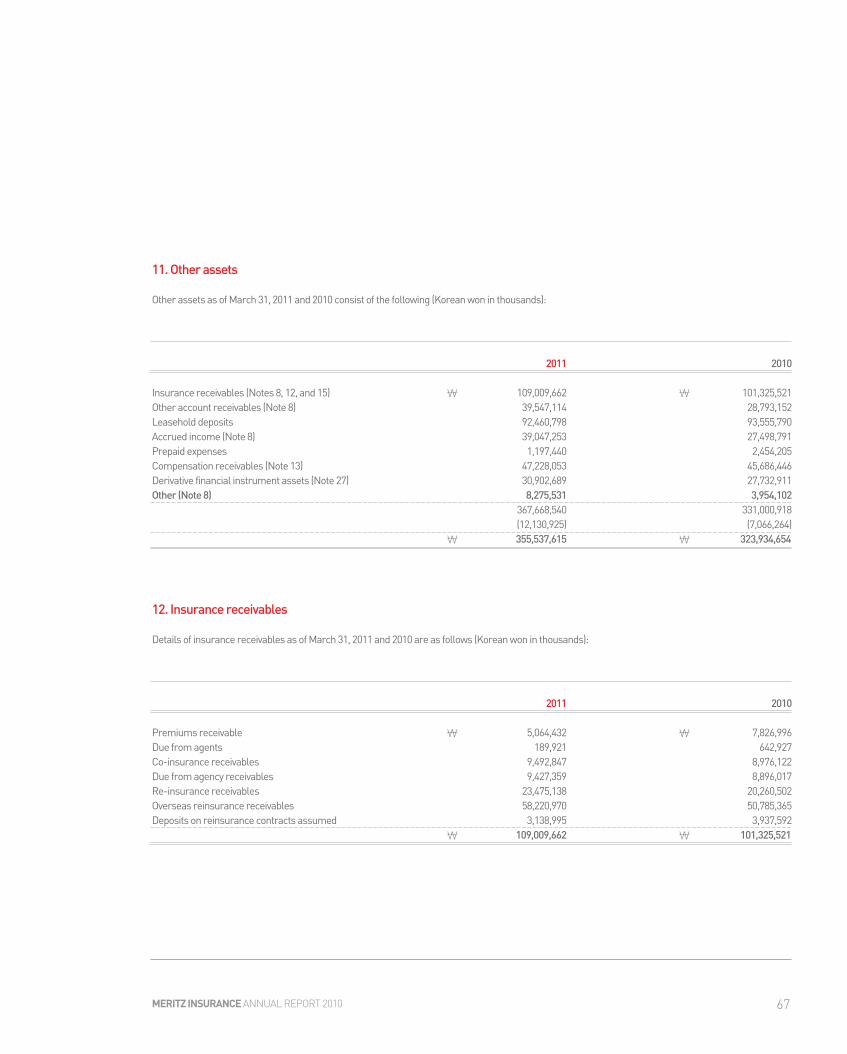

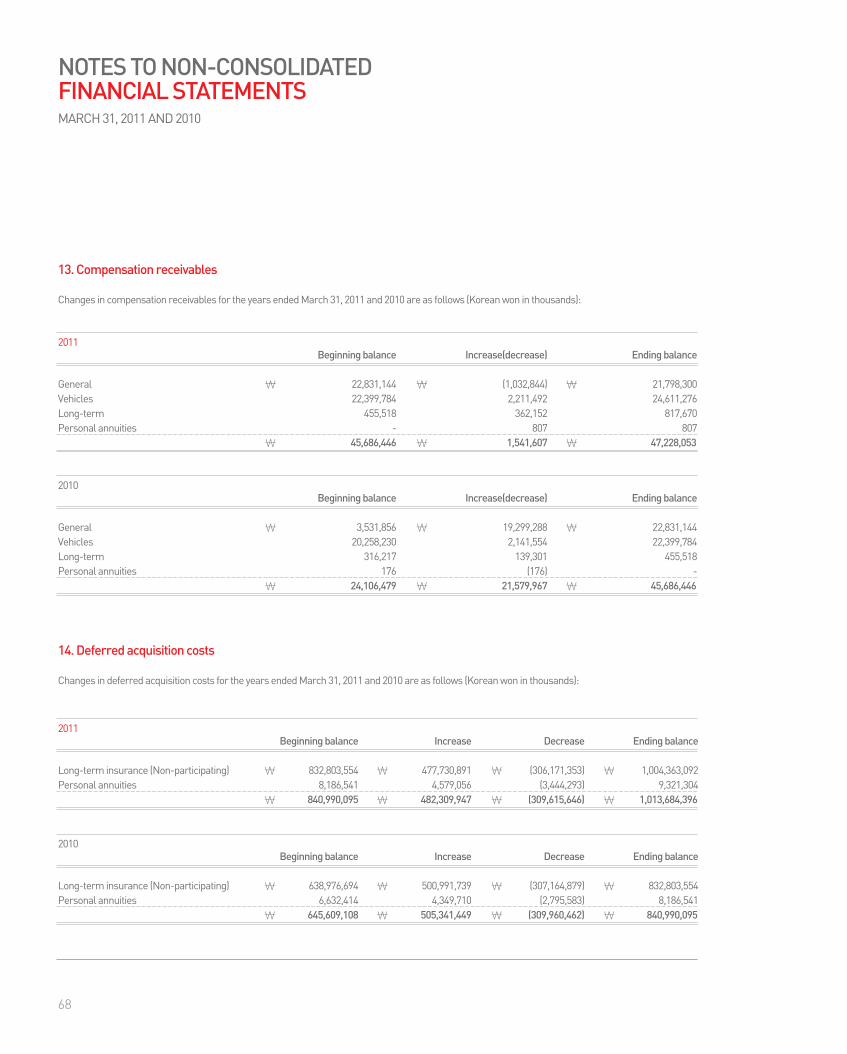

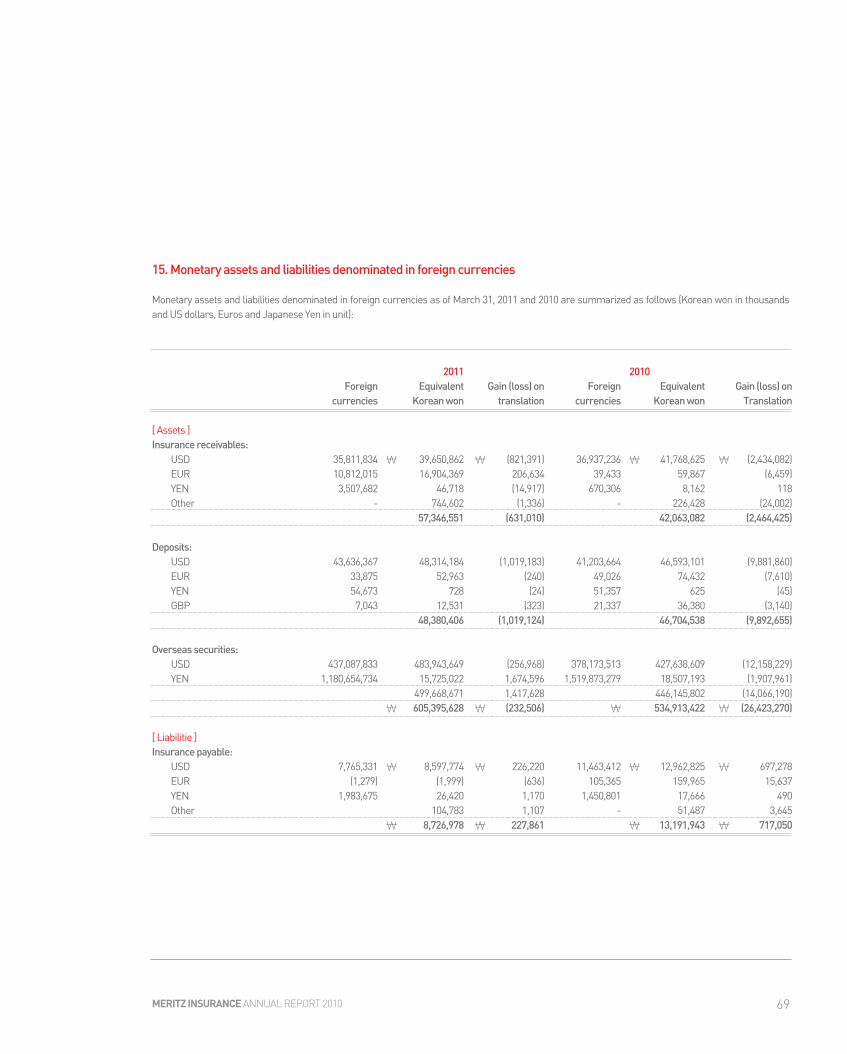

1. Company information

Meritz Fire & Marine Insurance Co., Ltd. (the “Company”) was incorporated in October 1922. The Company provides primarily property and casualtyinsurance products and related services. On October 1, 2005, the Company changed its name from Oriental Fire & Marine Insurance Co., Ltd. toMeritz Fire & Marine Insurance Co., Ltd.

The Company listed its common shares at the Korea Exchange (“KRX”) in July 1957 and the Company’s paid-in capital decreased by \18,265 millionas a result of capital reduction arising from spin-off on March 25, 2011 which was approved by an extra-ordinary shareholders’meeting held onJanuary 11, 2011. The Company completed the procedures for listing spun off common shares at KRX on April 11, 2011, and accordingly, as of March31, 2011, the Company has 87,269,690 common shares issued amounting to \43,635 million.

As of March 31, 2011, the stockholders of the Company and their shareholdings are as follows:

NOTES TO NON-CONSOLIDATEDFINANCIAL STATEMENTSMARCH 31, 2011 AND 2010

Stockholder Number of shares Percentage ofownership (%)

Nine individuals, including Cho Jeong-Ho 18,898,212 21.66Meritz Financial Group Inc. 11,364,520 13.02Employees’stock ownership association 1,349,010 1.54KB pure stocks 2 4,232,665 4.85Others 51,425,283 58.93

87,269,690 100.00

2. Summary of significant accounting policies

Basis of financial statement preparationThe Company maintains its official accounting records in Korean won and prepares statutory financial statements in the Korean language inconformity with accounting principles generally accepted in the Republic of Korea (“Korean GAAP”). Certain accounting principles applied by theCompany that conform with financial accounting standards and accounting principles in the Republic of Korea may not conform with generallyaccepted accounting principles in other countries. Accordingly, these non-consolidated financial statements are intended for use by those who areinformed about Korean accounting principles and practices. In the event of any differences in interpreting the non-consolidated financial statementsor the independent auditors’report thereon, the Korean version, which is used for regulatory reporting purposes, shall prevail. The accompanyingnon-consolidated financial statements have been condensed, restructured and translated into English (with certain expanded descriptions) from theKorean language financial statements.

The financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the Republic of Korea,including Statements of Korea Accounting Standards (“SKAS”) 1 to 24 (except for SKAS 14), and the significant accounting policies followed by theCompany in preparing the accompanying non-consolidated financial statements are summarized below.

39MERITZ INSURANCE ANNUAL REPORT 2010

Financial year The Company’s financial year is March 31. Reference in the accompanying non-consolidated financial statements for 2011 and 2010 represents theyears ended March 31, 2011 and 2010, respectively.

RevenuesRevenues from premium income are recognized at the time when such premium payments become due. However, in the case of insurancecontracts of which the first premium payment or single premium payment are uncollected as of the first day of the insured period due to a paymentextension allowed by the Company, the first premium payment or single premium payment is recognized as revenue in the period in which the firstday of insured period falls. If premium is received before the nominated collection due date, the Company records unearned insurance premiumbased on calendar period calculation.

Interest income on deposits, securities and loans, and other investments is recognized as income in the period when it is earned. Interest income ondefaulted, delinquent or restructured loans is recognized as income in the period when the payments are received.

Cash equivalentsHighly liquid deposits and marketable securities with original maturities of three months or less, and which have no significant risk of loss in value byinterest rate fluctuations, are considered as cash equivalents.

Investments in securitiesInvestments in securities within the scope of SKAS 8 Investments in Securities are classified as either trading, held-to-maturity or available-for-salesecurities, as appropriate, and are initially measured at cost, including incidental expenses.

Securities that are acquired and held principally for the purpose of selling them in the near term are classified as trading securities. Debt securitieswhich carry fixed or determinable payments and fixed maturity are classified as held-to-maturity if the Company has the positive intention and abilityto hold them to maturity. Securities that are not classified as either trading or held-to-maturity are classified as available-for-sale securities.

After initial measurement, available-for-sale securities are measured at fair value with unrealized gains or losses being recognized directly in equityas other comprehensive income. Likewise, trading securities are also measured at fair value after initial measurement, but with unrealized gains orlosses reported as part of net income. Held-to-maturity securities are measured at amortized cost after initial measurement. The cost is computedas the amount initially recognized minus principal repayments, plus or minus the cumulative amortization using the effective interest method of anydifference between the initially recognized amount and the maturity amount.

The fair value of trading and available-for-sale securities that are traded actively in the open market (marketable securities) is measured at theclosing price of those securities at the reporting date. Non-marketable equity securities are measured at cost subsequent to initial measurement iftheir fair values cannot be reliably estimated. Non-marketable debt securities are carried at a value using the present value of future cash flowsdiscounted using an appropriate interest rate which reflects the issuer’s credit rating announced by a public independent credit rating agency. If theapplication of such measurement method is not feasible, estimates of fair values may be made using a reasonable valuation model or quotedmarket prices of similar debt securities issued by entities conducting business in similar industries.

The Company recognizes an impairment loss on its investments in securities if there is objective evidence that the securities are impaired. Theimpairment loss is charged to the statement of income.

40

Equity method investmentsInvestments in entities over which the Company has control or significant influence are accounted for using the equity method.

Under the equity method of accounting, the Company’s initial investment in an investee is recorded at acquisition cost. Subsequently, the carryingamount of the investment is adjusted to reflect the Company’s share of income or loss of the investee in the statement of income and share ofchanges in equity that have been recognized directly in the equity of the investee in the related equity account of the Company in the statement offinancial position.

At the date of acquisition, the excess of the cost of the investment over the Company’s share of the net fair value of the investee’s identifiable assetsand liabilities is accounted for as goodwill which is amortized over its useful life within 20 years using the straight-line method. Conversely, negativegoodwill represents the excess of the Company’s share in the net fair value of the investee’s identifiable assets and liabilities over the cost of theinvestment. Negative goodwill is recorded to the extent of the fair value of acquired non-monetary assets and recognized as income using thestraight-line method over the remaining weighted-average useful life of those acquired non-monetary assets. The amount of negative goodwill inexcess of the fair value of acquired non-monetary assets is recognized as income immediately.

In translating the financial statements of foreign investees into Korean won, assets and liabilities are translated at the exchange rate at the reportingdate and income and expenses are translated at the average exchange rate for the reporting period. All resulting exchange differences arerecognized as foreign currency translation adjustments in other comprehensive income within equity.

Allowance for doubtful accountsThe allowance for doubtful accounts is provided in compliance with the Regulation of Insurance Supervision (“RIS”), which requires the application ofminimum loss ratios based on the degree of collectability of receivables, including loans. Receivables are classified as normal, precautionary,substandard, doubtful and estimated loss, and the related allowance is calculated at a minimum of 0.5% (0.75% for consumer loans), 2% (5% forconsumer loans), 20%, 50% and 100%, respectively, of the outstanding amount in each classification.

Property and equipmentProperty and equipment are stated at cost, less accumulated depreciation, except for certain assets in existence as of July 1, 1998 that wererevalued in accordance with the previous Korean Assets Revaluation Law and land and buildings that were revalued in accordance with the currentrevised SKAS 5 which are stated at fair value, less accumulated depreciation.

Maintenance and repairs are expensed in the year in which they are incurred. Expenditures which enhance the value or extend the useful life of therelated assets are capitalized.

Depreciation of property and equipment is provided using the declining balance method (buildings using the straight-line method) over the followingestimated useful lives:

NOTES TO NON-CONSOLIDATEDFINANCIAL STATEMENTSMARCH 31, 2011 AND 2010

Years

Buildings 40Vehicles 4Furniture and equipment 4

41MERITZ INSURANCE ANNUAL REPORT 2010

The Company has chosen the revaluation model as its accounting policy for its land. Accordingly, land is measured at fair value, less impairment lossesrecognized after the date of revaluation. Valuation is performed frequently enough to ensure that the fair value of a revalued land does not differmaterially from its carrying amount.

If a land’s carrying amount is increased as a result of a revaluation, the increase shall be credited directly to in the other comprehensive income.However, the increase shall be recognized in the statement of income to the extent that it reverses a revaluation decrease of the same land previouslyrecognized in the statement of income.

If a land’s carrying amount is decreased as a result of a revaluation, the decrease shall be recognized in the statement of income. However, the decreaseshall be debited directly to other comprehensive income to the extent of any credit balance existing in the revaluation surplus in respect of that land.

Intangible assetsIntangible assets of the Company consist of development cost and other intangible assets which are stated at cost, less accumulated amortization.Amortization is recognized as an expense based on the straight-line method over the estimated useful life of 5 years.

Impairment of assetsWhen the recoverable amount of an asset is less than its carrying amount due to obsolescence, physical damage or abrupt decline in the marketvalue of the asset, the decline in value, if material, is deducted from the carrying amount and recognized as an asset impairment loss in the currentyear.

If the value of impaired asset subsequently recovers and the recovery objectively relates to an event arising after the period when the impairmentloss was recorded, such recovery is credited in the current operations up to the previously recorded impairment loss.

Compensation receivablesInsurance benefits that are paid in advance to a policyholder in the event of a claim where the benefits paid can be recovered through the Companyexercising its recourse guarantee or compensation right, or disposal of insured assets acquired by the Company during the resolution process ofaccident claims, are accounted for as compensation receivables. Recoverable amounts out of the reserve for outstanding claims are deducteddirectly from policy reserves.

Compensation receivables are estimated by multiplying the average recovery ratio (ie, recoverable amount/net claims) for the last 3 years to the netclaims amount during the year.

42

Deferred acquisition costsThe expected cost of acquiring long-term insurance contracts entered into before April 1, 2004, except for those long-term contracts whose relatedactual acquisition costs exceeded the expected acquisition costs, were deferred and amortized using the straight-line method over the insurancecontract term, or 7 years, whichever is shorter. However, pursuant to the RIS and Accounting Standards for Insurance Companies, the Companycalculates the amortized deferred acquisition costs related to the insurance contracts during the reporting period, by deducting the differencebetween the policy reserves under the net level premium method and those under the surrender value method from the amounts computed byadding the unamortized acquisition costs at the prior year-end to acquisition costs incurred during the current year.

During the year ended March 31, 2005, the Company changed its accounting policy for deferred acquisition costs related to the long-term insurancecontracts which were entered into on or after April 1, 2004, pursuant to a revision of the RIS in 2004. According to the revised RIS, actual acquisitioncosts, or the expected deferred acquisition costs if the former exceeds the latter, are deferred and amortized using the straight-line method over theinsurance premium payment term, or over 7 years, whichever is shorter. However, if the unamortized deferred acquisition costs at the end of thereporting period exceed the difference between the policy reserves calculated using the net level premium method and surrender value method, thesurplus amount is fully expensed in the current period. No additional amount was amortized in 2011 and 2010.

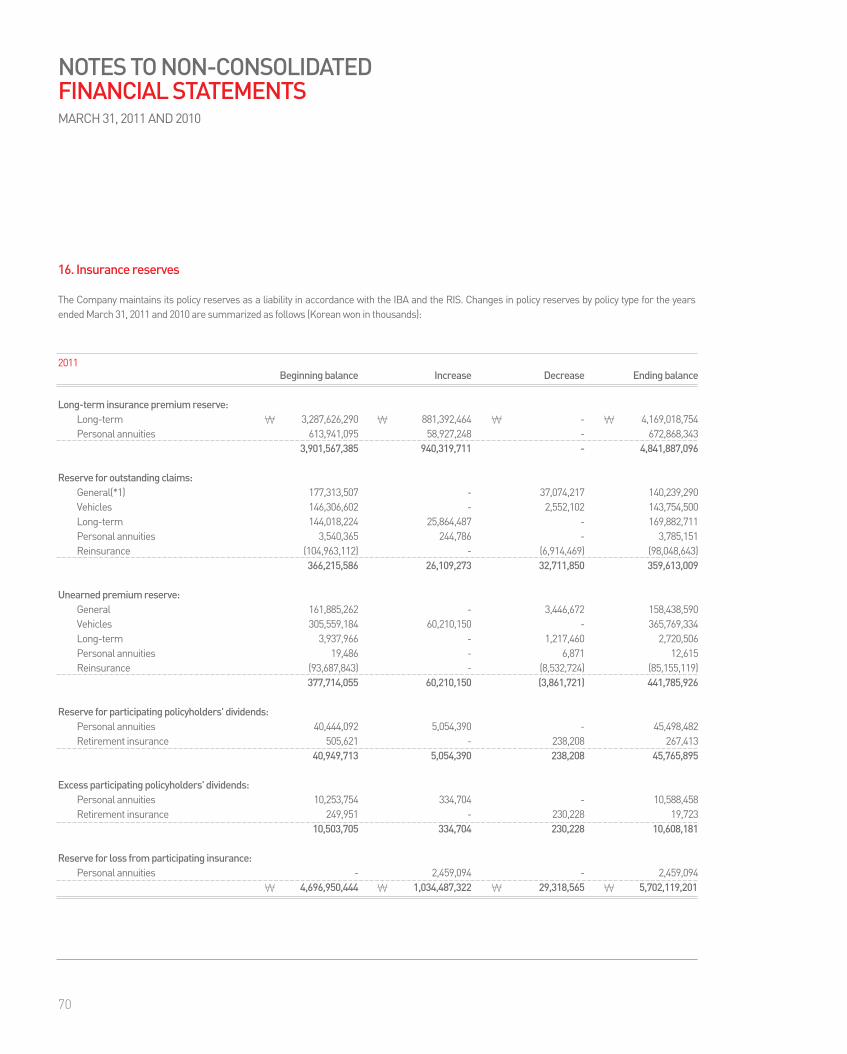

Policy reservesIn accordance with the Insurance Business Act (“IBA”) and the RIS, the Company is required to maintain policy reserves, and the details are asfollows:

1. Long-term insurance premium reservesThe Company maintains a reserve for the portion of premiums, which is refundable to policyholders upon maturity and cancellation of the policyunder long-term saving oriented insurance unless there has been a substantial claim for payment under the policy.

2. Reserve for outstanding claimsThe reserve for outstanding claims refers to a provision for claims received but not settled, or for claims not received, and therefore not yet settled,on the insurance policies where the events causing the payment of claims have occurred at the reporting date. The amount collectible fromexercising the compensation right or disposal of insured assets acquired by the Company is reported as a deduction from policy reserves.