Embed Size (px)

Citation preview

CHAPTER 6

Mergers and Acquisitions:Hot Topics & Current Transactions1

KAREN GILBREATH, ESQ.

Ernst & Young LLP

DIANA WOLLMAN, ESQ.

Sullivan & Cromwell

JOHN J. CLAIR, ESQ.

Latham & Watkins

JOSEPH M. DOLOBOFF, ESQ.

Ernst & Young National Office West

STACEY WARNIX, ESQ.

Ernst & Young LLP

DAVID KAHN, ESQ.

Latham & Watkins

1 The authors would like to thank Jennifer V. Stroffe of the Los Angeles officeof Latham & Watkins for her assistance in the preparation of these materials.

6–1

0001 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 1 1/1

SYNOPSIS

§ 6.01 Loss Disallowance Rules

[1] Introduction

[2] Former Loss Disallowance Rules

[a] General Loss Disallowance Rule

[b] General Deconsolidation Rule

[c] Overlap Between the Former Loss Disallowance andDeconsolidation Rules

[d] Reattribution of Subsidiary Losses to Parent

[e] Anti-stuffing Rules

[f] Extraordinary Gain Dispositions Factor

[g] Positive Investment Adjustments Factor

[h] Duplicated Losses Factor

[3] Rite Aid Invalidates the Loss Duplication Factor Under theFormer Rules

[a] Rite Aid Decision

[i] Background

[ii] Appellate Decision

[iii] Scope of Decision

[b] Notice 2002-18

[4] New Loss Disallowance Regulations

[a] Dispositions on or After March 7, 2002

[i] Reattribution of Subsidiary’s Losses and Anti-stuffing Rules

[ii] Netting

[b] Dispositions Prior to March 7, 2002

[i] Recalculation of Reattributed Losses

[ii] Apportionment of Applicable Limitations

[iii] Notification by Common Parent

[iv] Investment Adjustment for Losses Restored UponRetroactive Application of New Regulations

[5] Observations and Anticipated Developments

[a] Comprehensive LDR Regime

[b] Loss Duplication Regulations

[c] Refund Opportunity

[d] Pending Legislation

§ 6.02 Mergers with Disregarded Entities

[1] Former Proposed Regulations

6–261ST N.Y.U. INSTITUTE

0002 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 47

[a] No “A” Reorganization Treatment

[b] Rationale

[2] New Regulations

[a] “A” Reorganization Treatment for Certain Mergers

[b] New Terminology

[c] Requirements for Nontaxable Treatment as an “A”Reorganization

[d] Cross-Border and Foreign-to-Foreign Mergers

[e] Mergers Pursuant to Non-corporate Statutes

[3] Example — Merger of Target Corporation into DisregardedEntity in Exchange for Stock of Owner

[4] Observations and Anticipated Developments

[a] Private Letter Rulings

[b] Cross-Border and Foreign-to-Foreign Mergers

§ 6.03 Divisive Transactions

[1] Introduction

[2] Scope of Section 355(e)

[a] Former Proposed and Temporary Regulations

[b] New Proposed and Temporary Regulations

[i] Factors

[ii] Super Safe Harbor for Certain Post-distributionAcquisitions

[iii] Safe Harbors

[iv] Special Rules for Public Offerings and Auctions

[v] Similar Acquisitions

[vi] Options

[vii] Recent Private Letter Rulings

[3] Active Trade or Business Requirement

[a] Real Estate Investment Trusts (REITs)

[i] Revenue Ruling 2001-29

[ii] Recent Public Transaction

[b] Limited Liability Corporations (LLCs)

[i] Management of LLC Satisfies Active Trade inBusiness Requirement

[ii] Deemed Taxable Acquisition Fails Active Trade inBusiness Requirement

[4] Control Requirement

[a] Introduction

[b] Recapitalization to Acquire Control

[c] Post-spin Unwinding of Pre-spin Recapitalization

MERGERS & ACQUISITIONS — HOT TOPICS6–3

0003 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 81

[5] Business Purpose Requirement

[a] Key Employee Business Purpose

[6] Tracking Stock Dispositions

[a] Introduction

[b] Recent Private Letter Rulings

[c] Section 355(e) Consequences

[d] Other Section 355(e) Considerations

[7] Corporate Tax Consequences Associated with Post-distributionIssuances of Compensatory Stock

[a] Introduction

[b] Previous Guidance on Allocation of Post-distributionCompensation Deductions

[c] Current Service Position

[8] Anticipated Developments

§ 6.04 Step Transaction Doctrine in Triangular Reorganizations

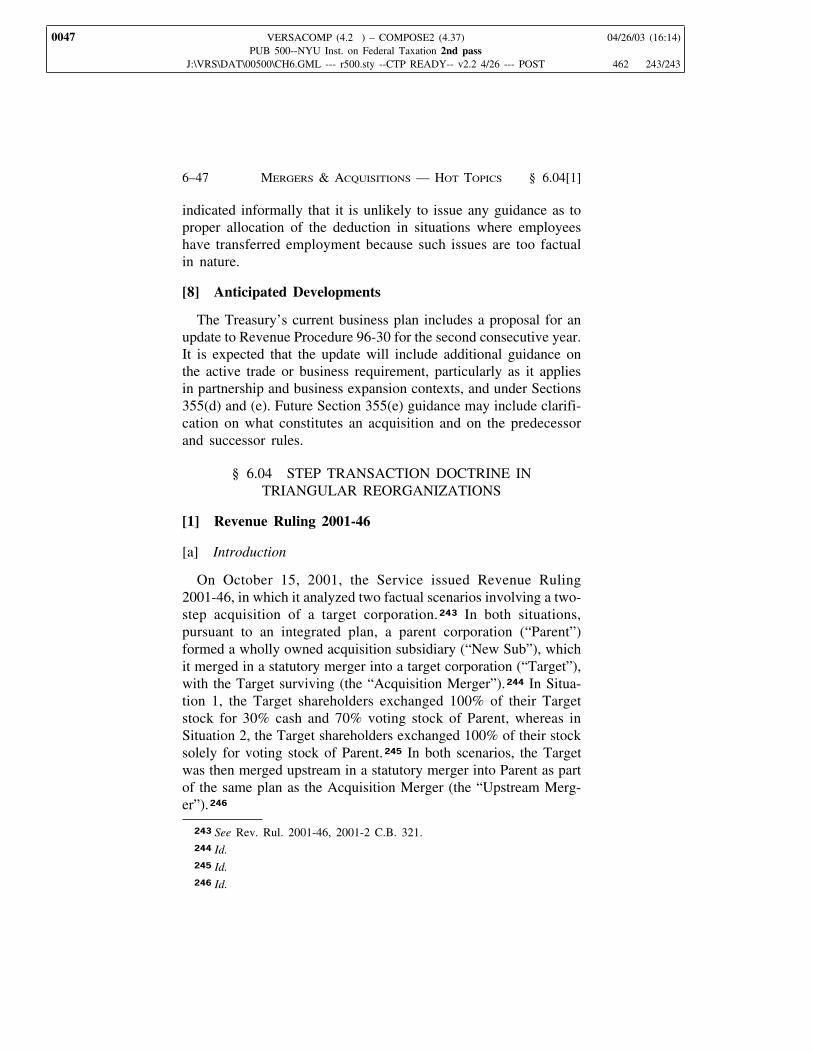

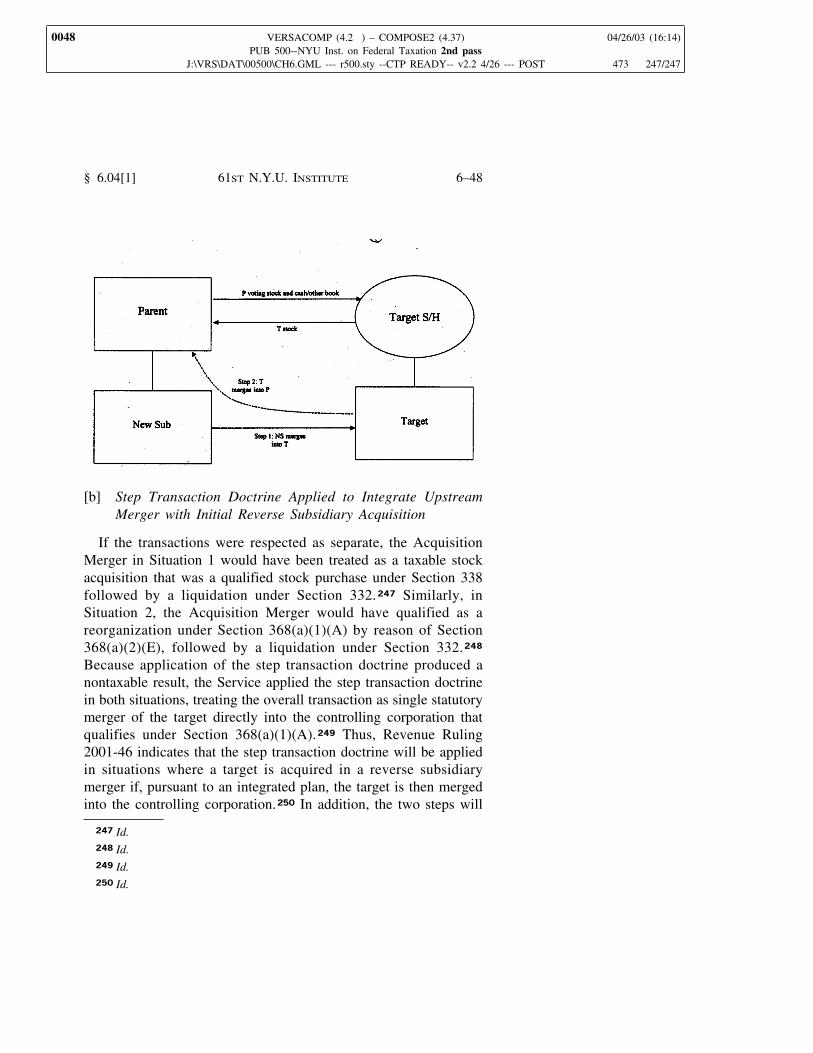

[1] Revenue Ruling 2001-46

[a] Introduction

[b] Step Transaction Doctrine Applied to Integrate UpstreamMerger with Initial Reverse Subsidiary Acquisition

[c] Modified Acquisition Structure

[i] Qualification Under Section 368(a)(2)(D)

[ii] Step Transaction Doctrine Applied to IntegrateSideways Merger with Initial Reverse SubsidiaryAcquisition

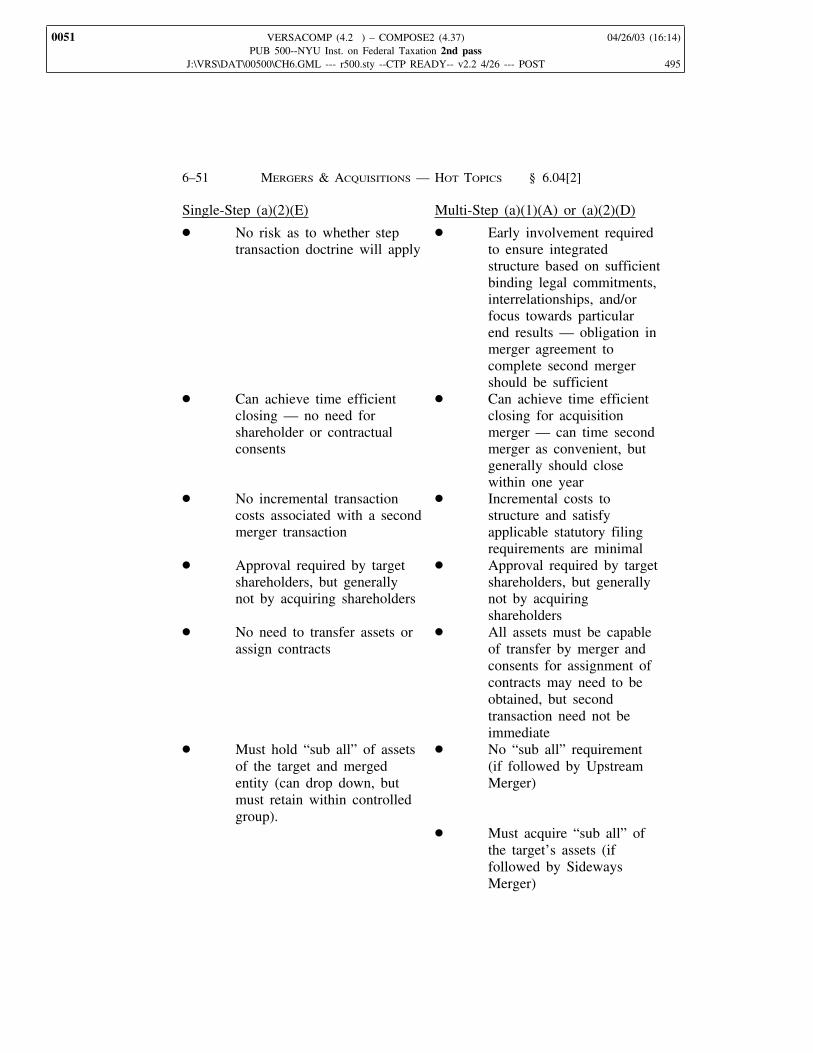

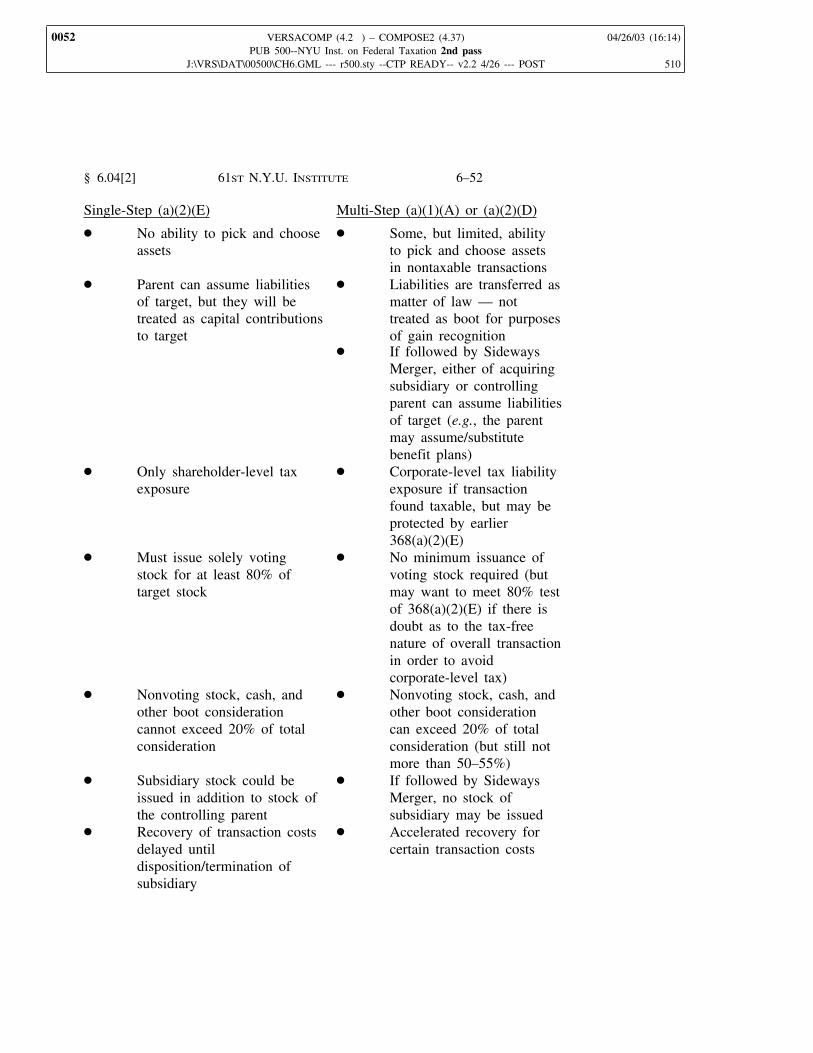

[2] Benefits of Multi-step Acquisition Structures

[3] Observations and Anticipated Developments

[a] Application of Step Transaction Doctrine Only in Nontax-able Contexts

[b] No Application of Step Transaction Doctrine Where InitialAcquisition is Reverse Subsidiary Merger

[c] Regulatory Guidance Under Section 338

§ 6.05 Circular 230

[1] Introduction

[2] Status of Tax Shelter Opinion Provisions of Circular 230

[3] Highlights of the July 2002 Final Regulations

[a] Sections 10.3 through 10.7 — Who May Represent aTaxpayer or Prepare a Tax Return

[b] Section 10.20(a) — Obligation to Furnish Information tothe Service Upon Request

[i] What is a “Matter Before the IRS”?

6–461ST N.Y.U. INSTITUTE

0004 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 116

[ii] What Records or Information Must be Submittedto the Service?

[iii] Section 10.20(b) — Obligation to Furnish Informa-tion Regarding an Alleged Violation of Circular 230to the Director of Practice

[c] Section 10.21 — Knowledge of a Client’s Omission

[i] Compromise Language Regarding Advice on“Consequences”

[d] Section 10.22 — Diligence as to Accuracy

[i] Presumption of Due Diligence for Papers Preparedby Persons Other Than the Practitioner

[e] Section 10.23 — Prompt Disposition of Matters PendingBefore the Service

[f] Section 10.24 — Assistance from or To Disbarred orSuspended Persons and Former Service Employees

[g] Section 10.26 — Notaries

[h] Section 10.27 — Fees

[i] Section 10.28 — Return of a Client’s Records

[i] Scope

[ii] Fee Disputes

[iii] Definition of “Records of the Client”

[j] Section 10.29 — Conflicting Interests

[i] Scope

[ii] Exception Where There is Informed WrittenConsent

[k] Section 10.34 — Standards for Advising with Respect toTax Return Positions and for Preparing or SigningReturns

[i] Good Faith Reliance Upon Information Provided Bya Client

[l] Sections 10.50 Through 10.82 — Sanctions for Violationsof Circular 230

§ 6.06 Proposed Tax Shelter Legislation

[1] Principle Features of the Proposed Legislation

[a] Coordination of Key Terms

[b] Definition of “Reportable Transactions”

[c] Definition of Listed Transactions

[d] Proposed Legislation to Prevent Expatriation Transac-tions and Earnings Stripping

[e] Proposed Legislation on Deferred Compensation

§ 6.07 Tax Implications of the Sarbanes-Oxley Act

[1] Limitation on Provision of Non-audit Services by Auditors

MERGERS & ACQUISITIONS — HOT TOPICS6–5

0005 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 147

[a] Effective Date

[2] Pre-approval of Non-audit Services by the Audit Committee

[a] Specificity of the Approval

[b] Delegation of Pre-approval Authority

[c] Advance Approvals

[d] De Minimis Exception

[3] Current Restrictions on Non-audit Services as Compared to theAct’s Limitations on the Provision of Non-audit Services

[4] Effect of the Act’s Non-audit Services Restrictions on Non-Registered Accounting Firms and Companies that Are Not SECRegistrants

[5] Under the Act, the CEO and CFO Must Personally Attest tothe Accuracy of the Company’s Financial Statements andPeriodic Reports with the SEC

[6] Companies May Not Avoid the Act by Expatriating

[7] Changes in Financial Statement Disclosures of Off-balanceSheet Transactions and the Use of Special Purpose Entities

[8] Fraudulently Influencing Accountants in Relation to the AuditReport

[9] Transfer of Employees from Accounting Firm to the PublicCompany

[10] Application of the Act to Non-U.S. Accounting Firms

[11] Will Corporate Tax Returns Have to be Signed by the CEO?

§ 6.01 LOSS DISALLOWANCE RULES

[1] Introduction

In March of 2002, the Internal Revenue Service (the “Service”)and Treasury Department (the “Treasury”) replaced the former lossdisallowance regulations2 with proposed and temporary regula-tions3 for transactions occurring on or after March 7, 2002.4 TheseRegulations were issued following the Federal Circuit’s decisionin Rite Aid Corporation and Subsidiary Corporations v. UnitedStates,5 which invalidated the duplicated loss factor of the priorregulations and threatened the continued viability of the remaining

2 See Treas. Reg. § 1.1502-20. 3 See Temp. Treas. Reg. § 1.1502-20T; Temp. Treas. Reg. § 1.337-2T. 4 Treas. Reg. § 1.1502-20T(i)(1). 5 255 F.3d 1357 (Fed. Cir. 2001).

6–661ST N.Y.U. INSTITUTE§ 6.01[1]

0006 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 176 2/2

factors.6 The following discussion summarizes the significantprovisions in the prior regulations and the anticipated changes tothe loss disallowance rules.

[2] Former Loss Disallowance Rules

The former loss disallowance regulations under Treasury Regula-tions Section 1.1502-20 limited the ability of a consolidated groupmember to recognize a loss on its disposition of stock or deconsoli-dation of a subsidiary member through loss disallowances7 orforced basis reductions.8 As stated in the preambles, the formerregulations were designed to reflect a balancing of concerns.9 Mostsignificantly, the former regulations did not prevent the reductionof gains, but instead, only operated to disallow loss.10 Accordingto the Service, these rules were intended to prevent the circumven-tion of the 1986 repeal of the General Utilities11 doctrine in theconsolidated return context.12

[a] General Loss Disallowance Rule

According to the former regulations, a corporation was generallynot permitted to take a deduction for any loss recognized upon adisposition on or after February 1, 1991 of stock in a subsidiarywhich, prior to such disposition, was a member of the corporation’sconsolidated group.13 Under the regulations, a disposition wasdefined as “any event in which gain or loss was recognized, inwhole or in part.”14 However, Treasury Regulations Section1.1502-20(c) limited the reach of the general disallowance byclarifying that the amount disallowed would be limited to the sumof three factors: (i) extraordinary gain dispositions, (ii) positive

6 Id. at 1360. 7 Treas. Reg. § 1.1502-20(a)(1). 8 Treas. Reg. § 1.1502-20(b)(1). 9 T.D. 8984, 2002-13 I.R.B. 668 (March 8, 2002). 10 Id. 11 General Utilities & Operating Co. v. Helvering, 295 U.S. 200 (1935); re-

pealed by Tax Reform Act 1986. 12 CO-93-90, 1990-2 C.B 696. 13 Treas. Reg. § 1.1502-20(h)(1). 14 Treas. Reg. § 1.1502-20(a)(2).

§ 6.01[2]MERGERS & ACQUISITIONS — HOT TOPICS6–7

0007 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 196 6/6

investment adjustments, and (iii) duplicated losses.15 As discussedin more detail below, the Service intended these factors to limitthe recognition of loss to only the “true economic loss” in asubsidiary’s stock.16 To benefit from this limitation, a corporationwas required to attach a statement meeting the requirements ofTreasury Regulations Section 1.1502-20(c)(3) to the consolidatedreturn for the year that encompassed the disposition.17

[b] General Deconsolidation Rule

Under the former regulations, if an event caused a subsidiary tobecome deconsolidated at a time when the consolidated member’sbasis in the share of such subsidiary exceeded the value of thesubsidiary’s stock, the basis in the subsidiary’s stock was requiredto be reduced to fair market value immediately before the deconsoli-dation, so that the loss would not be triggered.18 This rule wasintended to prevent a corporation from intentionally avoiding theloss disallowance rules by simply disaffiliating a subsidiary priorto the disposition of the subsidiary’s stock.19

Similar to the limitation upon a disposition of a subsidiarymember’s stock, Treasury Regulations Section 1.1502-20(c) cappedthe amount of the basis reduction upon a deconsolidation at anamount equal to the sum of the three factors. 20 In addition, in orderto benefit from this limitation, a corporation was required to filea statement meeting the requirements of Treasury RegulationsSection 1.1502-20(c)(3) with its consolidated return for the yearthat included the deconsolidation.21

[c] Overlap Between the Former Loss Disallowance and Decon-solidation Rules

Under the regulations, if an event gave rise to both a dispositionand a deconsolidation of the subsidiary’s stock, the disallowance

15 Treas. Reg. § 1.1502-20(c)(1)(i–iii). 16 Preamble to T.D. 8984, 2002-13 I.R.B. 668 (March 8, 2002). 17 Treas. Reg. § 1.1502-20(c)(3). 18 Treas. Reg. § 1.1502-20(b)(1). 19 Preamble to T.D. 8984, 2002-13 I.R.B. 668 (March 8, 2002). 20 See Treas. Reg. § 1.1502-20(c)(1)(i–iii). 21 Treas. Reg. § 1.1502-20(c)(3).

6–861ST N.Y.U. INSTITUTE§ 6.01[2]

0008 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 202 15/15

rules were to be applied first.22 Thereafter, to the extent necessaryto eliminate any remaining permissible loss, the basis in thesubsidiary’s stock would be reduced to fair market value.23

[d] Reattribution of Subsidiary Losses to Parent

The draconian effect of the disallowance under the formerregulations was somewhat mitigated by the ability of the consoli-dated group parent to reattribute to itself some, or all, of any netoperating loss or capital loss carryovers attributable to the subsid-iary or its lower tier subsidiaries for the parent’s future use uponthe disposition or deconsolidation of the subsidiary.24 However, inorder to be effective, this reattribution had to be made jointly byan irrevocable election by both the parent and the subsidiary.25

[e] Anti-stuffing Rules

The former regulations also contained an anti-stuffing rule thatrequired a basis reduction if an asset transfer was (i) made within2 years of a disposition or deconsolidation (or the making of anagreement, option, or other arrangement with respect thereto), and(ii) made with a view to avoid, directly or indirectly, the lossdisallowance or basis reduction rules upon the disposition ordeconsolidation or the recognition of unrealized gain.26 Adjust-ments to the amount of the reduction were made as necessary toremedy the perceived avoidance.27

[f] Extraordinary Gain Dispositions Factor

As noted above, under the former regulations, if a dispositionoccurred on or after November 19, 1990, the loss that resulted fromthe sale of stock in a member subsidiary was disallowed (or thebasis in the stock was reduced) by an amount equal to the incomeor gain from extraordinary gain dispositions, net of directly relatedexpenses (e.g. commissions, legal fees, and state income taxes).28

22 Treas. Reg. § 1.1502-20(b)(1). 23 Id. 24 Treas. Reg. § 1.1502-20(g)(1). 25 Treas. Reg. § 1.1502-20(g)(4)(i). 26 Treas. Reg. § 1.1502-20(e)(2)(i). 27 Treas. Reg. § 1.1502-20(e)(1). 28 Treas. Reg. § 1.1502-20(c).

§ 6.01[2]MERGERS & ACQUISITIONS — HOT TOPICS6–9

0009 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 209 22/22

If less than 100% of the shares were disposed of, the extraordinarygain amount was adjusted proportionately.29 However, extraordi-nary losses could not be offset against extraordinary gains to reducethe amount of the disallowance or basis adjustment.30

Extraordinary gain dispositions were actual or deemed disposi-tions of the following assets for a gain:

(1) capital assets;31

(2) depreciable property and real property used in a trade orbusiness;32

(3) inventory, if substantially all of the inventory was disposedof in one transaction or a series of related transactions;33

(4) certain categories of noncapital assets if substantially allsuch assets in a given category were disposed of in onetransaction or a series of related transactions;34

(5) assets sold in an applicable asset acquisition under Section1060(c);35 and

(6) certain other items arising from the disposition of an asset,such as cancellation of indebtedness or accounting methodchanges that gave rise to positive adjustments under Section481.36

[g] Positive Investment Adjustments Factor

As noted above, in calculating the amount of the disallowed lossor basis adjustment, the regulations also considered positive invest-ment adjustments.37 Positive investment adjustments were definedas any adjustments required to increase a member’s basis in its stockin a subsidiary under Treasury Regulations Section 1.1502-32.38

29 Treas. Reg. § 1.1502-20(c)(iii). 30 Treas. Reg. § 1.1502-20(c). 31 Treas. Reg. § 1.1502-20(c)(2)(i)(A)(1). 32 Treas. Reg. § 1.1502-20(c)(2)(i)(A)(2). 33 Treas. Reg. § 1.1502-20(c)(2)(i)(A)(3). 34 Id. 35 Treas. Reg. § 1.1502-20(c)(2)(i)(A)(4). 36 Treas. Reg. § 1.1502-20(c)(2)(i)(B–D). 37 See Treas. Reg. § 1.1502-20(c)(2)(ii). 38 Treas. Reg. § 1.1502-20(c)(1)(ii).

6–1061ST N.Y.U. INSTITUTE§ 6.01[2]

0010 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 218 29/29

The adjustments were considered to the extent they were reflecteddirectly or indirectly (from partnerships and other conduits) in thebasis of the share, immediately prior to the disposition or deconsoli-dation of the subsidiary.39 In an attempt to reflect what the Serviceperceived as the true economic loss in the stock, any amountsincluded in a loss carryover were taken into account in the yearthey arose, rather than in the year they were absorbed.40

Under a positive investment adjustment, limited netting wasallowed. Positive adjustments were generally allowed to offsetnegative adjustments (other than negative adjustments to reflectcorporate distributions) within the same tax year.41 Thus, theamount of the annual adjustment (if any) would equal the amountof positive earnings and profits before distributions for the year.However, net negative adjustments were not permitted to offset netpositive investment adjustments from prior years, unless the adjust-ments were for tax years ending on or before September 13, 1991.42

To the extent a loss was attributable to an extraordinary gain thatresulted in a positive investment adjustment, the amount wasdisallowed only once and was treated as an extraordinary gaindisposition.43 In other words, adjustments that related to extraordi-nary gain dispositions were eliminated from the total positiveinvestment adjustments.

[h] Duplicated Losses Factor

As noted above, the amount of the loss disallowance or basisadjustment was also based upon the amount of duplicated losses.The duplicated loss amount generally measured the net unrealizedloss inherent in the assets of the subsidiary, plus its loss carryoversimmediately following the disposition or deconsolidation.44 Morespecifically, it represented the sum of the total adjusted basis ofthe subsidiary’s assets, net operating or capital loss carryovers, plusdeferred deductions, less the value of the subsidiary’s stock and

39 Treas. Reg. § 1.1502-20(c)(1)(iii). 40 Id. 41 Id. 42 Treas. Reg. § 1.1502-20(c)(2)(v). 43 Treas. Reg. § 1.1502-20(c)(1)(ii). 44 Treas. Reg. § 1.1502-20(c)(2)(vi).

§ 6.01[2]MERGERS & ACQUISITIONS — HOT TOPICS6–11

0011 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 230 39/39

liabilities.45 The duplicated loss amount for a subsidiary includedits allocable portion of corresponding amounts for each of its lower-tiered subsidiaries.46

[3] Rite Aid Invalidates the Loss Duplication Factor Underthe Former Rules

[a] Rite Aid Decision

On July 6, 2001, the Court of Appeals for the Federal Circuitreversed the Court of Federal Claims in Rite Aid Corp., et al. v.United States, and held that the consolidated return loss disallow-ance rules were invalid as applied in that decision.47

[i] Background

In 1995, the Rite Aid Corporation claimed a loss on the sale ofstock in a subsidiary acquired in a multi-step stock purchase inwhich Rite Aid had made a Section 338 election.48 The Servicedisallowed the loss under the loss disallowance rules of TreasuryRegulations Section 1.1502-20.49 Rite Aid sued for a refund ongrounds that the loss disallowance rules were invalid, arguing thatthe issuance of regulations was beyond the Secretary’s regulatoryauthority.50 Rite Aid argued that the duplicated loss factor arbitrar-ily imposed a tax that wouldn’t otherwise be imposed on corpora-tions filing consolidated returns by denying a loss allowed underSection 165.51 Rite Aid also argued that the regulations did notfurther the stated purposes of Section 1502 — to clearly reflect theincome of the consolidated group and prevent tax avoidance.52

The trial court granted the government’s motion for summaryjudgment, finding that Treasury Regulations Section 1,1502-20 wasnot “arbitrary, capricious, or manifestly contrary to the statute.”53

45 Id. 46 Id. 47 255 F.3d 1357, 1360 (Fed. Cir. 2001). 48 Id. at 1358. 49 Id. 50 Id. 51 Id.at 1360. 52 Id. at 1359. 53 Id. at 1358.

6–1261ST N.Y.U. INSTITUTE§ 6.01[3]

0012 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 235 45/45

Thus, because the subsidiary’s duplicated loss factor exceeded RiteAid’s loss on the stock, the court disallowed Rite Aid’s entireclaimed loss.54

[ii] Appellate Decision

Like the lower court, the Circuit Court also applied the “arbitrary,capricious, or manifestly contrary to law” standard, noting that aregulation would be contrary to a statute if it were outside the scopeof delegated authority.55 The Circuit Court, however, reached adifferent conclusion than the trial court.56 After examining thelegislative history of Section 1502, the court concluded that thepurpose for the statute was to give the Secretary authority to identifyand correct instances of tax avoidance that were created by the filingof consolidated returns and that, in the absence of such avoidance,the Secretary was without authority to alter the application of othertax code provisions to consolidated groups.57 The court stated thata loss realized on the sale of a former subsidiary’s assets after theconsolidated group sells the subsidiary’s stock is not a problem thatresults from the filing of a consolidated income tax return.58 Thecourt determined that Rite Aid’s loss did not stem from the filingof a consolidated return and that the duplicated loss factor of theloss disallowance regulations, in particular, was manifestly contraryto the statute since it addressed situations that arise from the saleof stock regardless of whether a corporation files a separate orconsolidated return.59

Although the Service requested a rehearing by the FederalCircuit, the request was denied,60 and the Service ultimatelydecided not to file an appeal to the Supreme Court.

[iii] Scope of Decision

On January 31, 2002, the Service released Notice 2002-11, inwhich it indicated that it would no longer litigate the duplicated

54 Id. 55 Id. at 1359. 56 Id. at 1360. 57 Id. 58 Id. at 1360. 59 Id. 60 255 F.3d 1357, 1360 (Fed. Cir. 2001), rehearing denied, Oct. 3, 2001.

§ 6.01[3]MERGERS & ACQUISITIONS — HOT TOPICS6–13

0013 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 244 54/54

loss factor of the loss disallowance rules.61 The Service stated that,despite its continued position that the Federal Circuit’s decision inRite Aid was incorrect, the interests of sound tax administrationwould not be served by continuing to litigate the validity of theduplicated loss factor.62 The Service also announced that becauseof the interrelationships of the three loss disallowance factors, ithad decided to implement entirely new regulations.63 The Servicerevealed that the existing regulations would be replaced with interimregulations that require consolidated groups to determine theallowable loss on a sale or disposition of a subsidiary member’sstock under an amended version of Treasury Regulation Section1.337(d)-2.64 The Service also announced that it was undertakinga broader study of the regulations necessary to reflect the singleentity principles of the consolidated return rules.65

[b] Notice 2002-18

On March 7, 2002, in conjunction with its release of the newLDR regulations discussed below, the Service issued Notice2002-18. In the Notice, the Service announced the issuance of newproposed and temporary regulations under Sections 337 and 1502that set forth new rules governing a consolidated group’s allowableloss or basis reduction upon the disposition or deconsolidation ofa subsidiary’s stock.66 The Service pointed out that the new rulesdo not disallow stock losses that reflect net operating or built-inlosses.67

In the Notice, the Service nonetheless stated that the Service andTreasury intend to issue regulations to prevent a consolidated groupfrom duplicating tax benefits with respect to a single economic loss(i.e., where a deduction related to an asset would reflect the sameeconomic loss that gives rise to a stock loss).68 Interestingly, the

61 I.R.S. Notice 2002-11, 2002-7 I.R.B. 526. 62 Id. 63 Id. 64 Id. 65 Id. 66 I.R.S. Notice 2002-18, 2002-12 I.R.B. 644. 67 Id. 68 Id.

6–1461ST N.Y.U. INSTITUTE§ 6.01[3]

0014 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 251 61/61

Service and Treasury have not indicated that they will issueregulations allowing the reduction of gain, which could result inthe multiple taxation of a single economic gain.

The Notice was apparently issued in response to a transactionby Bank of America wherein it duplicated unrealized losses insecurities by transferring them to a subsidiary.69 At the May 10,2002, meeting of the Affiliated and Related Corporations Commit-tee of the ABA Section of Taxation (the “May ABA Tax Meeting”),a Treasury representative defended Notice 2002-18, indicating thatthe administration characterized the sweeping statements in Rite Aidas dicta.70 The representative also distinguished the Bank ofAmerica transaction at issue in the notice as involving duplicationof loss within a single affiliated group, whereas Rite Aid involvedthe disallowance of a single economic loss.71 Interestingly, therepresentative indicated that the Service would continue to pursuenot only duplicated losses within a single affiliated group, but alsoduplicated losses generated in a separate return context or insituations involving intermediaries such as partnerships or realestate investment trusts.72 It is not clear what authority exists tosupport the issuance of regulations beyond the consolidated groupcontext.

[4] New Loss Disallowance Regulations

On March 7, 2002, the Service and Treasury issued new proposedand temporary regulations under Sections 337(d) and 1502 of theCode.73 These complex regulations are intended to provide interimguidance while the IRS considers a revised permanent regulatoryregime for loss disallowance and basis allocations made upon aparent’s disposition or deconsolidation of a subsidiary.74 In addi-tion, on October 23, 2002, the IRS published proposed regulationsintended to address the concerns raised by the Service in Notice2002-18. As discussed below, however, considerable uncertainty

69 Id. 70 ABA Tax Meeting: Consolidated Return Issues and Rite Aid Discussed. Tax

Notes Today (May 10, 2002). 71 Id 72 Id 73 See I.R.S. Notice 2002-18, 2002-12 I.R.B. 644. 74 Id.

§ 6.01[4]MERGERS & ACQUISITIONS — HOT TOPICS6–15

0015 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 255 69/69

remains even after the promulgation of these proposed and tempo-rary regulations.

[a] Dispositions on or After March 7, 2002

All dispositions or deconsolidations arising on or after March 7,2002 are governed by the new regulations at Treasury RegulationsSection 1.337(d)-2T rather than the former regulations at Section1.1502-20.75 Under these new temporary regulations, a loss uponthe disposition or deconsolidation of a subsidiary member is onlypermitted if the group is able to establish that the stock loss is notattributable to the recognition of built-in gain on dispositions of thesubsidiary’s assets.76 Thus, the new regulations incorporate tracingprinciples in order to identify the extent to which a stock loss isattributable to the subsidiary’s recognition of excess asset value thatwas inherent in the parent’s stock basis.77 Unfortunately, however,the regulations do not provide a precise definition of recognizedbuilt-in gain and provide little guidance as to how a taxpayer shouldimplement the tracing regime. In fact, this tracing approach waspreviously considered and explicitly rejected by the Service in thiscontext because of administrative concerns.78 In addition, the newregulations eliminate the requirement under the prior Section 337regulations that a consolidated group must dispose of its entireequity interest in a subsidiary to unrelated persons in order torecognize a loss on the stock.79

[i] Reattribution of Subsidiary’s Losses and Anti-stuffingRules

Unlike Treasury Regulations Section 1.1502-20, the new regula-tions do not allow any of the subsidiary’s losses to be reattributedto the parent.80 The new regulations do, however, incorporate thesame anti-stuffing rules that were contained in the prior regula-tions.81

75 Temp. Treas. Reg. § 1.337(d)-2T(g). 76 Temp. Treas. Reg. § 1.337(d)-2T(c)(2). 77 Id.; Temp. Treas. Reg. § 1.337(d)-2T(b)(1). 78 Notice of Prop. Rule Making, 67 Fed. Reg. 11070 (Mar. 12, 2002). 79 Temp. Treas. Reg. § 1.337(d)-2T(c)(2). 80 Temp. Treas. Reg. § 1.337(d)-2T(a)(1). 81 Temp. Treas. Reg. § 1.337(d)-2T(e).

6–1661ST N.Y.U. INSTITUTE§ 6.01[4]

0016 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 259 75/75

[ii] Netting

The new regulations initially did not allow any form of netting.82

However, on May 30, 2002, the Service issued several clarificationsand amendments to the new regulations, including the adoption ofa netting rule comparable to the netting provisions in the priorregulations.83 The new netting provisions permit a loss recognizedby one member of a group to be offset against gain recognized bythe same or different member of its group, provided that the lossand gain are each recognized with respect to dispositions of stockof the same subsidiary, having the same material terms, that aredisposed of as part of the same plan or arrangement.84 Prior to thischange, a corporation could potentially have been required torecognize a stock gain, while at the same time, having its stockloss disallowed under the loss disallowance regulations.

[b] Dispositions Prior to March 7, 2002

For dispositions or deconsolidations occurring either prior toMarch 7, 2002, or pursuant to a binding contract in effect as ofMarch 7, 2002, a consolidated group is permitted to determine theamount of the allowable loss or basis reduction by applying theold rules at Section 1.1502-20 either in their entirety or by electingone of two alternatives: (i) application of the old regulations withoutregard to the duplicated loss factor (i.e., based upon the Rite-Aiddecision),85 or (ii) application of the new temporary regulations.86

[i] Recalculation of Reattributed Losses

The new regulations provide only limited guidance regardinghow to re-determine the allowable loss or basis reduction for priortax periods, or how to compute any reattribution elections and losscarryforwards if one of the alternative methods is elected. Althoughlimited reattribution is allowed, the recalculated amount will neverexceed the amount that would have been allowed under the priorLDR regime. If a corporation elects to apply the former loss

82 T.D. 8984, 2002-13 I.R.B. 668 (Mar. 7, 2002). 83 Temp. Treas. Reg. § 1.337(d)-2T(a)(4). 84 Id. 85 Temp. Treas. Reg. § 1.1502-20T(i)(2)(i). 86 Temp. Treas. Reg. § 1.1502-20T(i)(2)(ii).

§ 6.01[4]MERGERS & ACQUISITIONS — HOT TOPICS6–17

0017 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 266 82/82

disallowance rules without the duplicated loss factor and it timelyfiles an election to reattribute some or all of the subsidiary’s losses,the parent can preserve any reattributed losses that were absorbedin closed tax years. However, with respect to open tax years,reattribution will be permitted only to the extent that the loss isdisallowed under the extraordinary gain dispositions and positiveinvestment adjustments factors. On the other hand, if the taxpayerelects to apply the new regulations and a timely election is madeto reattribute some or all of the subsidiaries losses, although theparent may retain any reattributed losses that it absorbed in a closedyear, it will not be able to reattribute any losses that were absorbedin years that remain open. If the group elects to use one of thealternative methods listed, and such use reduces the amount oflosses subject to reattribution, the subsidiary or its consolidatedgroup is entitled to utilize these excess losses, subject to otherapplicable limitations on their use.

[ii] Apportionment of Applicable Limitations

Reattributed losses that are reduced and shifted back for use bythe subsidiary or a group of which it is a member, retain allapplicable limitations (e.g., Section 382 and SRLY).87 The newregulations allow the parent to make certain adjustments to thelimitations that must be apportioned between the parent and thesubsidiary or subsidiary group.88 The new regulations protect theacquirer by not requiring that a negative investment adjustmentreflect the expiration in closed tax years of any loss carryovers madeavailable to the subsidiary upon the retroactive application of oneof the alternative loss disallowance regimes.89 In addition, theregulations also authorize the acquiring group to elect to treat anyunexpired loss carryovers as having expired immediately before thesubsidiary became a member of the group, thereby enabling thegroup to avoid a negative basis adjustment upon the expiration ofsuch loss carryovers.90 However, in order to qualify, this electionmust be filed with the group’s tax return for the taxable year in

87 Temp. Treas. Reg. § 1.1502-20T(i)(3)(iii). 88 See Temp. Treas. Reg. § 1.1502-20T(i)(3)(iii)(C). 89 See Temp. Treas. Reg. § 1.1502-20T(i)(3)(iii). 90 Id.

6–1861ST N.Y.U. INSTITUTE§ 6.01[4]

0018 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 274 87/87

which the subsidiary receives notification of the recomputed lossallocations.91

[iii] Notification by Common Parent

The new regulations impose an obligation upon the parent tonotify the subsidiary and the common parent of the acquiring group,if any, of any recomputed reattribution amount and any adjustmentsto the apportionment of limitations to which the losses are subject.92

The practical implications of this obligation, however, remainsomewhat unclear.

[iv] Investment Adjustment for Losses Restored UponRetroactive Application of New Regulations

On May 30, 2002, the Service amended the new regulations toallow a positive investment adjustment for the amount of lossrestored as a result of an election to retroactively apply the newregulations to a closed tax year if the loss would either have beenabsorbed or expired in a closed year.93 This modification isintended to neutralize the negative investment adjustment thatwould have been required under Treasury Regulations Section1.1502-32.94

[5] Observations and Anticipated Developments

[a] Comprehensive LDR Regime

The Service and Treasury have indicated that the current regula-tions are simply a temporary measure until a comprehensive systemcan be identified, and that in finalizing the regulations, they willbe looking at all related issues.95 The preamble to the proposedand temporary regulations indicated that one approach beingconsidered was the denial of positive investment adjustments forgain recognized and income attributable to the disposition orconsumption of built-in gain assets held by a subsidiary prior to

91 Id. 92 Temp. Treas. Reg. § 1.1502-20T(i)(3)(iv). 93 T.D. 8998, 2002-26 I.R.B. 1 (May 30, 2002). 94 Id. 95 Id.

§ 6.01[5]MERGERS & ACQUISITIONS — HOT TOPICS6–19

0019 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 277 91/91

joining a consolidated group.96 The Service scheduled a publichearing on the new regulations for mid-July; however, because noone requested to speak, the hearing was cancelled.

[b] Loss Duplication Regulations

On October 23, 2002, the Service issued proposed loss duplica-tion regulations to implement Notice 2002-18.97 Under theseproposed regulations, a consolidated group would be preventedfrom duplicating losses by two rules: (i) a basis redeterminationrule and (ii) a loss suspension rule.98 The basis redetermination rulewould essentially require that the group’s basis in the stock of asubsidiary be redetermined prior to certain deconsolidations and/ordispositions if the group’s basis in such stock exceeds its value.Under the loss suspension rule, if, after application of the basisredetermination rule, a member of a consolidated group were torecognize loss on the disposition of the stock of another memberof the group that remains a member of the group, such loss wouldbe “suspended” to the extent of any “duplicated loss.” The proposedregulations define “duplicated loss” for this purpose as the excessof (1) the sum of the aggregate basis of the subsidiary member’sassets (excluding stock in other group subsidiaries), the subsidiary’slosses that are carried forward to its first taxable year after thedisposition, and the subsidiary’s deductions that have been recog-nized but otherwise deferred, over (2) the sum of the value of thestock of the subsidiary and it’s liabilities that have been taken intoaccount for tax purposes.99 The proposed regulations also includea basis reduction rule (intended to cover certain situations not withinthe scope of the loss suspension rule and anti-avoidance rules andcertain anti-abuse rules.)100 The loss duplication rules are effectivefor disposition of member stock on or after March 7, 2002. In orderto hold this effective date, however, the Service and Treasury mustissue temporary or final regulations by March 15, 2003.

96 Id. 97 67 F.R. 65060 98 Id. 99 Id. 100 Id.

6–2061ST N.Y.U. INSTITUTE§ 6.01[5]

0020 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 288 96/96

[c] Refund Opportunity

Because the new regulations do not incorporate the duplicatedloss or positive adjustment factors, the ability to elect to apply thenew regulations to prior dispositions and deconsolidations presentsa refund opportunity for many taxpayers. In order to elect into oneof the new regimes, a taxpayer must either file an amended returnprior to the due date for the consolidated tax return that encom-passes March 7, 2002, or attach an irrevocable election to itsoriginal return for such year.101 Additionally, in light of the RiteAid decision, it might even be argued that no LDR regime existsfor years prior to March 7, 2002.102 The fact that the Service hasdelineated a limited set of choices does not necessarily preventtaxpayers from taking the position that the prior LDR regime wascompletely invalidated by Rite Aid.

[d] Pending Legislation

Currently, both houses of Congress are considering bills thatwould undermine the Federal Circuit’s statements in Rite Aid thatthe ability of a formerly consolidated subsidiary to deduct a lossrealized on the sale of its assets after it has deconsolidated is nota problem that results from the filing of a consolidated income taxreturn.103 The proposed legislation would provide that the Service’sauthority to issue regulations under Section 1502 should be con-strued without regard to the interpretation of that authority in RiteAid and would confirm that the Treasury is authorized to issueconsolidated return regulations utilizing either a single or separateentity approach, or a combination thereof, to clearly reflect the taxliability of consolidated groups.104 In effect, if this legislation ispassed, it will limit the potential effect of Rite Aid on otherconsolidated return regulations and on the other factors of the priorLDR regulations.

101 Temp. Treas. Reg. § 1.1502-20T(i)(2). 102 See generally, Rite Aid, 255 F.3d 1357 (Fed. Cir. 2001). 103 See Affirmation of Consolidated Return Regulation Authority, H.R. 5095,

107th Cong. § 123 (2002); Affirmation of Consolidated Return RegulationAuthority, H.R. 7, 107th Cong. § 631 (2002).

104 Id.

§ 6.01[5]MERGERS & ACQUISITIONS — HOT TOPICS6–21

0021 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 292 101/101

§ 6.02 MERGERS WITH DISREGARDED ENTITIES

The Service has withdrawn earlier issued proposed regulationsthat would have precluded mergers between corporations anddisregarded entities from qualifying for tax-free treatment underIRS Code Section 368(a)(1)(A) (“A” reorganization).105 In theirplace, the Service has issued new proposed regulations which wouldpermit certain mergers including disregarded entities, to qualify asa tax-free “A” reorganization.106

[1] Former Proposed Regulations

[a] No “A” Reorganization Treatment

On November 14, 2001, the Service withdrew the proposedregulations at Treasury Regulations Section 1.368-2(b)(1) that wereissued on May 16, 2000.107 The prior regulations provided that eventhough it could potentially qualify under Sections 368(a)(1)(C), (D),or (F) or Section 351 if all other applicable requirements were met,neither a merger of a disregarded entity into a corporation nor amerger of a corporation into a disregarded entity would qualify asa tax-free statutory merger or consolidation under Section368(a)(1)(A).108 The Service indicated that compliance with acorporate law merger statute was not sufficient to qualify as an Areorganization.

[b] Rationale

Under the former proposed regulations, to qualify as a statutorymerger, a transaction was required to have, by operation of therelevant merger statute, involved both (i) an acquisition by theacquiring corporation of the assets of the merging corporation109

and (ii) the termination of the merging corporation’s existence.110

Thus, the Service took the position that a merger of a disregardedentity into a corporation, which under Federal tax law, is treated

105 See Notice of Prop. Rule Making, 65 Fed. Reg. 31115 (May 16, 2000).106 See Prop. Treas. Reg. § 1.368-2 (as amended in Nov. 14, 2001). 107 See Announcement 2001-121, 2001-2 CB 584. 108 See Notice of Prop. Rule Making, 65 Fed. Reg. 31115 (May 16, 2000).109 Id. 110 Id.

6–2261ST N.Y.U. INSTITUTE§ 6.02

0022 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 298 105/105

as if the owner of the disregarded entity had transferred the assetsheld in the disregarded entity to the acquiring corporation, wouldnot qualify under Section 368(a)(1)(A) because (i) not all of theowner’s assets would be transferred to the acquiring corporationand (ii) the owner would not cease to exist. The Service labeledthis type of transaction as a divisive transaction, and stated thatSection 355 was intended to be the sole means under which divisivetransactions may be afforded tax-free treatment.111 The Service hasretained this view in the new proposed regulations.

Furthermore, the Service determined that a merger of a corpora-tion into a disregarded entity, which under Federal tax law wouldbe treated as if the owner of the disregarded entity acquired all ofthe assets of the target corporation, did not conform closely enoughto a merger of the target corporation into the owner.112 Morespecifically, the Service objected on the grounds that (i) the ownerwould not be a party to the transaction and (ii) the combinationof the target corporation and owner’s assets and liabilities wouldnot be pursuant to a direct combination under state or Federalmerger law, but instead, merely a tax fiction.113

[2] New Regulations

[a] “A” Reorganization Treatment for Certain Mergers

Simultaneous to its withdrawal of the prior proposed regulations,the Service issued new proposed regulations on November 14, 2001,partially reversing its earlier position.114 The new regulations willbe effective when issued in final form.115 These regulationsreaffirm the Service’s earlier position that a merger of a disregardedentity into a corporation, is effectively a divisive transaction inwhich the owner of the disregarded entity continues to exist afterthe merger and retains its assets not held in the disregardedentity.116 However, under the new proposed regulations, some

111 Id. 112 Id. 113 Id. 114 See Announcement 2001-121, 2001-2 CB 584. 115 Prop. Treas. Reg. § 1.368-2(b)(1)(v) (as amended in Nov. 14, 2001). 116 Prop. Treas. Reg. § 1.368-2(b)(1)(ii) (as amended in Nov. 14, 2001).

§ 6.02[2]MERGERS & ACQUISITIONS — HOT TOPICS6–23

0023 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 308 111/111

mergers of corporations into disregarded entities will qualify fortax-free treatment under Section 368(a)(1)(A).117 To so qualify, thenew regulations require that the assets and liabilities of the targetbe transferred to a corporation and/or one or more disregardedentities whose assets are treated as owned by such corporation forFederal tax purposes.118 This modification eliminates the concernunder the prior proposed regulations that the target corporationwould not be directly combining its assets and liabilities with theassets and liabilities of the owner of the acquiring disregardedentity.

[b] New Terminology

The new proposed regulations introduced several key termswhich govern the determination of whether or not a merger orconsolidation will qualify as a statutory merger under Section368(a)(1)(A). A “combining entity” is a business entity that is acorporation and not disregarded for federal income tax purposes.119

A “disregarded entity” is a business entity that is disregarded asan entity separate from its owner for federal income tax purposes;it includes domestic single-member limited liability companies,qualified REIT subsidiaries, and qualified subchapter S subsidia-ries.120 A “combining unit” collectively refers to a single combiningentity and any disregarded entities of that combining entity.121

Every merger will involve at least two combining units, one knownas the “transferor unit” and the other as the “transferee unit.”122

[c] Requirements for Nontaxable Treatment as an “A”Reorganization

The new proposed regulations provide that a transaction canconstitute a tax-free statutory merger under Section 368(a)(1)(A)if two requisite events occur at the effective time. First, eachmember of one or more transferor units must transfer substantially

117 See Notice of Prop. Rule Making, 66 Fed. Reg. 57400 (as amended in Nov.15, 2000).

118 Id. 119 Prop. Treas. Reg. § 1.368-2(b)(1)(i)(B) (as amended, in Nov. 14, 2001).120 Prop. Treas. Reg. § 1.368-2(b)(1)(i)(A) (as amended in Nov. 14, 2001). 121 Prop. Treas. Reg. § 1.368-2(b)(1)(i)(C) (as amended in Nov. 14, 2001). 122 Prop. Treas. Reg. § 1.368-2(b)(1)(ii)(A) (as amended in Nov. 14, 2001).

6–2461ST N.Y.U. INSTITUTE§ 6.02[2]

0024 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 314 117/117

all of its assets and liabilities to one or more members of thetransferee unit, except to the extent that assets are distributed orliabilities are satisfied or discharged in the transaction.123 TheService explained in the preamble to the proposed regulations thatit did not intend that this requirement be interpreted in the samemanner as the “substantially all” requirement applicable to C, D,or triangular reorganizations.124 The Service did reiterate itsintention, however, that divisive transactions would not qualify asstatutory mergers under Section 368(a)(1)(A).125 Second, thecombining entity of each transferor unit must cease its separate legalexistence for all purposes.126

[d] Cross-Border and Foreign-to-Foreign Mergers

The new proposed regulations do not apply if either combiningentity (transferee or transferor), any disregarded entity of thetransferee group that acquires the assets or liabilities of the trans-feror combining entity, or any business entity through which thecombining entity of the transferee unit holds its interests in adisregarded entity, is foreign.127 Note that a transferor disregardedentity can be foreign, presumably because its owner must be adomestic corporation under these regulations.

[e] Mergers Pursuant to Non-corporate Statutes

As a final note, the new proposed regulations, consistent witha change made by the earlier proposed regulations, remove the word“corporation” from the requirement that a merger or consolidationmust be effected pursuant to the corporation laws of the relevantjurisdiction in order to qualify under Section 368(a)(1)(A).128 Thenew language conforms the regulation to the Service’s long-standing position that a merger or consolidation can qualify as an“A” reorganization even though it is undertaken under other lawsof a jurisdiction (e.g., pursuant to the National Banking Act).129

123 Prop. Treas. Reg. § 1.368-2(b)(1)(ii)(A) (as amended in Nov. 14, 2001).124 See Notice of Prop. Rule Making, 66 Fed. Reg. 57400. 125 Id. 126 Prop. Treas. Reg. § 1.368-2(b)(1)(ii)(B) (as amended in Nov. 14, 2001).127 Prop. Treas. Reg. § 1.368-2(b)(1)(iii)(as amended in Nov. 14, 2001). 128 See Notice of Prop. Rule Making, 66 Fed. Reg. 57400. 129 Id.

§ 6.02[2]MERGERS & ACQUISITIONS — HOT TOPICS6–25

0025 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 320 123/123

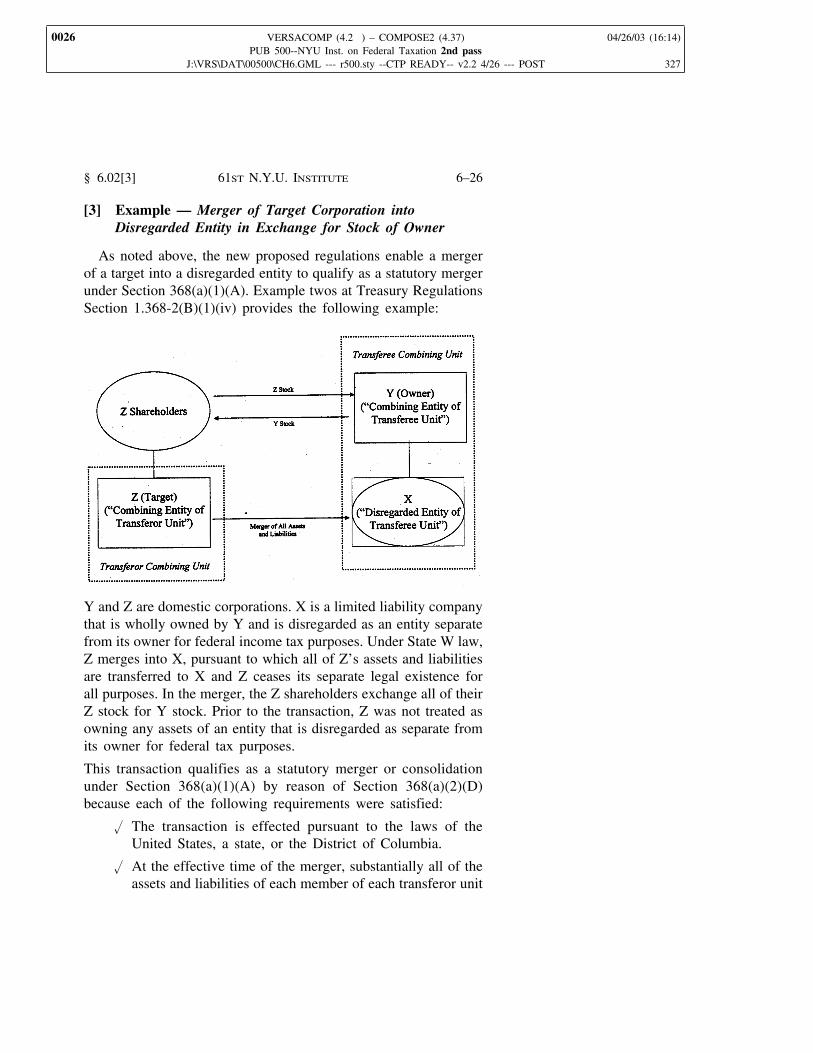

[3] Example — Merger of Target Corporation intoDisregarded Entity in Exchange for Stock of Owner

As noted above, the new proposed regulations enable a mergerof a target into a disregarded entity to qualify as a statutory mergerunder Section 368(a)(1)(A). Example twos at Treasury RegulationsSection 1.368-2(B)(1)(iv) provides the following example:

Y and Z are domestic corporations. X is a limited liability companythat is wholly owned by Y and is disregarded as an entity separatefrom its owner for federal income tax purposes. Under State W law,Z merges into X, pursuant to which all of Z’s assets and liabilitiesare transferred to X and Z ceases its separate legal existence forall purposes. In the merger, the Z shareholders exchange all of theirZ stock for Y stock. Prior to the transaction, Z was not treated asowning any assets of an entity that is disregarded as separate fromits owner for federal tax purposes.

This transaction qualifies as a statutory merger or consolidationunder Section 368(a)(1)(A) by reason of Section 368(a)(2)(D)because each of the following requirements were satisfied:

u The transaction is effected pursuant to the laws of theUnited States, a state, or the District of Columbia.

u At the effective time of the merger, substantially all of theassets and liabilities of each member of each transferor unit

6–2661ST N.Y.U. INSTITUTE§ 6.02[3]

0026 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 327

(in this case, Z) are transferred to one or more membersof the transferee unit (in this case, X) (except to the extentthat assets are distributed or liabilities are satisfied ordischarged in the transaction).

u At the effective time of the merger, the combining entityof each transferor unit (in this case, Z) must cease itsseparate legal existence for all purposes.

u The combining entity of the transferee unit and eachtransferor unit, each disregarded entity of the transfereeunit, and each business entity through which the combiningentity owns such disregarded entities (in this case, X, Y,and Z) are domestic.

Note once again that if the direction of this transaction were to bereversed (i.e., Z rather than X survives the merger), the transactionfalls outside of the proposed regulations.

[4] Observations and Anticipated Developments

[a] Private Letter Rulings

Since the new regulations will not be effective until publishedas final, it is difficult to determine whether a tax opinion can beissued on whether a transaction involving one or more disregardedentities qualifies under Section 368(a)(1)(A). This uncertainty hasgenerated questions as to whether the Service will entertain rulingson the issue. At the December 12, 2001 Corporate Tax Committeeluncheon of the Taxation Section of the D.C. Bar Association, anIRS representative stated that there was a strong possibility that theService would entertain private letter rulings on situations similarto the examples in the new proposed regulations. The merger ofa corporation into a disregarded entity likely presents a significantissue under Section 3.01 of Revenue Procedure 2001-3 sufficientfor the Service to rule on all aspects of the transaction relating toits qualification under Section 368(a)(1)(A). To date, the Servicehas issued one such private ruling, PLR 200236005.130 Interest-ingly, the Office of the Chief Counsel has issued a notice to theChief Counsel attorneys reminding them of the requirements tofollow legal positions established by published guidance or pro-posed regulations. This notice should give taxpayers comfort in

130 Priv. Ltr. Rul. 200236005 (May 23, 2002).

§ 6.02[4]MERGERS & ACQUISITIONS — HOT TOPICS6–27

0027 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 337 130/130

issuing opinions on disregarded entity mergers that are accom-plished consistent the proposed regulations.131

[b] Cross-Border and Foreign-to-Foreign Mergers

The Treasury’s current business plan contains an item calling forguidance on cross-border and foreign-to-foreign mergers for thethird consecutive year.

§ 6.03 DIVISIVE TRANSACTIONS

[1] Introduction

Over the past 18 months, the Service and Treasury have issuedextensive authority related to divisive transactions under Section355. These items have included regulatory guidance under Section355(e) regarding the meaning of a “plan or series of relatedtransactions”132 and several rulings on the various prerequisitesrequired for tax-free treatment, such as the active trade or business,control, and business purpose requirements.133 Further, the publicmarketplace has seen a growing reliance on Section 355 distribu-tions for the tax-free unwinding of tracking stock structures. Thesedevelopments, along with other anticipated developments, arediscussed in this section.

[2] Scope of Section 355(e)

Section 355(e) imposes restrictions on events occurring pursuantto a plan (or series of related transactions) that affect the sharehold-ers’ interests in the distributing or controlled corporations or anysuccessors thereto.134 In particular, Section 355(e) provides that thedistributing corporation will recognize gain on the distribution ofthe stock of the controlled corporation if the distribution is part ofa plan (or series of related transactions) pursuant to which one ormore persons acquire, directly or indirectly, stock representing a50% or greater interest in either the distributing corporation or

131 CC-2002-043. 132 See I.R.C. § 355(e). 133 See e.g., Rev. Rul. 2001-29, 2001-1 CB 1348; Rev. Rul. 2002-49, 2002-32

I.R.B. 288. 134 I.R.C. § 355(e)(3).

6–2861ST N.Y.U. INSTITUTE§ 6.03[1]

0028 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 346 131/131

controlled corporation.135 In addition, Section 355(e)(2)(B) estab-lishes a rebuttable presumption that acquisitions of stock within twoyears of a distribution are part of the distribution plan.136

[a] Former Proposed and Temporary Regulations

Since late 1999, the regulations under Section 355(e), regardingwhether a distribution and a stock acquisition would be treated aspart of a plan or series of related transactions, have been in aconstant state of flux. On August 24, 1999, proposed regulationswere issued, but they were subsequently withdrawn on December29, 2000.137 New proposed regulations were then issued on January2, 2001.138 On August 3, 2001, these regulations were adopted astemporary regulations in substantially identical form as the pro-posed regulations, except that the temporary regulations reservedon two of the proposed provisions.139 Specifically, the regulationsreserved upon the proposed suspension of the two-year presumptionperiod for any period in which there is a “substantial diminutionof risk of loss” within the meaning of Section 355(d)(6)(B) andon an example that illustrated application of the regulations regard-ing “similar acquisitions” in situations involving multiple acquisi-tions.140 In the preamble to the temporary regulations, the Serviceand Treasury stated that they would continue to analyze commentsreceived on the proposed regulations and that they would likelypromulgate additional guidance on their interpretation of a plan orseries of related transactions.141

[b] New Proposed and Temporary Regulations

On April 26, 2002, the Service and Treasury withdrew theexisting temporary regulations and issued a significantly revised setof temporary and proposed regulations concerning the scope ofSection 355(e).142 Generally, in comparison to the previous

135 See I.R.C. § 355(e)(2)(A)(ii). 136 I.R.C. § 355(e)(2)(B). 137 See Prop. Treas. Reg. 1.355-7 (Aug. 24, 1999). 138 See Prop. Treas. Reg. 1.355-7 (as amended in Jan. 2, 2001). 139 See Temp. Treas. Reg. § 1.355-7T (2001). 140 T.D. 8960, 2001-34 I.R.B. 176 (Aug. 3, 2001). 141 T.D. 8988, 2002-20 I.R.B. 929 (Apr. 29, 2002). 142 See Temp. Treas. Reg. § 1.355-7T (as amended in 2002).

§ 6.03[2]MERGERS & ACQUISITIONS — HOT TOPICS6–29

0029 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 357 135/135

regulations, the new regulations reduce the likelihood that a distri-bution and a stock acquisition will be treated as part of the sameplan or series of related transactions for purposes of Section355(e).143 The revised regulations are effective for distributionsafter April 26, 2002.144 However, taxpayers may apply the revisedregulations to distributions occurring after April 16, 1997, providedthe regulations are applied in their entirety.145

[i] Factors

Consistent with the approach taken in the prior temporaryregulations, the newly revised regulations adopt a facts and circum-stances-based approach and provide certain safe harbors.146 How-ever, whereas under the prior regulations, if an acquisition anddistribution arose within six months of one another, the existenceof a plan was rebuttably presumed, the new regulations eliminatethis presumption and provide a revised list of factors tending toshow whether a distribution and acquisition are part of the sameplan.147 These revisions reduce the likelihood that a post-distribution acquisition will be considered as part of a plan, althoughpublic offerings and pre-distribution acquisitions are subject tohigher scrutiny. As an example, in the case of a post-distributionacquisition that does not involve a public offering, the priorregulations treated discussions regarding the acquisition as tendingto show the existence of a common plan.148 The new regulations,on the other hand, focus only on whether there was an agreement,understanding, arrangement, or substantial negotiations within thetwo year period following the distribution.149 However, in the caseof acquisitions preceding a distribution and public offerings (regard-less of whether they occur before or after a distribution), the factthat the distributing or controlled corporation had discussionsregarding the latter transaction (or a similar acquisition) with anacquirer or investment banker within two years of the earlier

143 Id. 144 Temp. Treas. Reg. § 1.355-7T(k) (as amended in 2002). 145 Id. 146 See Temp. Treas. Reg. § 1.355-7T (as amended in 2002). 147 Temp. Treas. Reg. § 1.355-7T(b)(3) (as amended in 2002). 148 See Temp. Treas. Reg. § 1.355-7T(d)(2)(2001). 149 Temp. Treas. Reg. § 1.355-7T(b)(2) (as amended in 2002).

6–3061ST N.Y.U. INSTITUTE§ 6.03[2]

0030 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 363 143/143

transaction will tend to show that the distribution and acquisitionwere part of the same plan.150 Consistent with the earlier regula-tions, the revised regulations also consider the corporate businesspurpose(s) for the distribution, unexpected changes in market orbusiness conditions, a lack of discussions during the two-year periodregarding the latter transaction, and whether the distribution wouldhave occurred regardless of the acquisition or similar acquisition.151

The regulations generally do not specify the weight to be accordedeach factor.

[ii] Super Safe Harbor for Certain Post-distributionAcquisitions

The most significant change in the new temporary regulationsis that they contain a “super safe harbor.” Except in the case ofa stock acquisition that involves a public offering, under the newregulations, a distribution and a subsequent acquisition will not betreated as part of a plan unless there is an agreement, understanding,arrangement, or substantial negotiations regarding the acquisitionor a similar acquisition during the 2-year period that ends on thedate of the distribution.152 Only if there is an agreement, under-standing, etc., is it necessary to conduct a deeper factual inquiryinto whether or not a plan existed. 153 Because most taxpayers willlikely be interested in taking advantage of this super safe harbor,it is necessary to resolve such issues as what constitutes substantialnegotiations, similar acquisitions, and when pre-distribution negoti-ations or discussions have been terminated.

[iii] Safe Harbors

The regulations provide seven other safe harbors that treat certainacquisitions as not part of a plan or series of related transactionsfor purposes of Section 355(e).154 Safe Harbor I is applicable ifan acquisition occurs more than 6 months after a distribution and(i) the business purpose for the distribution was one other than to

150 Temp. Treas. Reg. § 1.355-7T(b)(3)(iii), (iv) (as amended in 2002). 151 Temp. Treas. Reg. § 1.355-7T(b)(3)(v) (as amended in 2002); Temp. Treas.

Reg. § 1.355-7T(b)(4) (as amended in 2002). 152 Temp. Treas. Reg. § 1.355-7T(b)(2) (as amended in 2002). 153 Id. 154 See Temp. Treas. Reg. § 1.355-7T(d)(as amended in 2002).

§ 6.03[2]MERGERS & ACQUISITIONS — HOT TOPICS6–31

0031 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 366 150/150

facilitate an acquisition of the acquired corporation,155 and (ii) therewas no agreement, understanding, arrangement, or substantialnegotiations regarding the acquisition during the 18-month periodbeginning one year before the distribution.156 Safe Harbor II appliesif an acquisition occurs more than 6 months after a distribution andduring the 18-month period beginning one year before the distribu-tion, (i) the business purpose for the distribution was one other thanto facilitate the acquisition of the acquired corporation or similaracquiring,157 (ii) there was no agreement, understanding, arrange-ment, or substantial negotiations regarding the acquisition or similaracquisition,158 and (iii) no more than 25% of the corporation’s stockwas acquired or subject to an agreement, understanding, arrange-ment, or substantial negotiations.159

Safe Harbors III and IV generally limit the length of time duringwhich an agreement, understanding, arrangement, or substantialnegotiations may be considered in determining whether an acquisi-tion and distribution are part of the same plan.160 For example, SafeHarbor III applies to acquisitions of the corporation’s stock occur-ring more than one year after a distribution, provided there was noagreement, understanding, or arrangement at the time of the distri-bution and no agreement, understanding, arrangement, or substantialnegotiations during the year following the acquisition.161 For stockacquisitions that occur more than two years prior to the distribution,Safe Harbor IV applies to the acquisition as long as there were noagreements, understanding, arrangements, or substantial negotia-tions concerning the distribution at the time of the acquisition orwithin 6 months thereafter.162

Other safe harbors relate to stock traded among public sharehold-ers, other than (i) 5% shareholders who actively participate inmanagement, 10% shareholders, underwriters, or affiliated members

155 Temp. Treas. Reg. § 1.355-7T(d)(1)(i)(as amended in 2002). 156 Temp. Treas. Reg. § 1.355-7T(d)(1)(ii)(as amended in 2002). 157 Temp. Treas. Reg. § 1.355-7T(d)(2)(i)(A)(as amended in 2002). 158 Temp. Treas. Reg. § 1.355-7T(d)(2)(i)(B)(as amended in 2002). 159 Temp. Treas. Reg. § 1.355-7T(d)(2)(i)(C)(as amended in 2002). 160 See Temp. Treas. Reg. § 1.355-7T(d)(3–4)(as amended in 2002). 161 Temp. Treas. Reg. § 1.355-7T(d)(3)(as amended in 2002). 162 Temp. Treas. Reg. § 1.355-7T(d)(4)(as amended in 2002).

6–3261ST N.Y.U. INSTITUTE§ 6.03[2]

0032 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 372 155/155

of the distributing or controlled corporation (Safe Harbor V),163

(ii) stock acquired pursuant to the exercise of options issued inexchange for services (Safe Harbor VI),164 and (iii) stock acquiredby qualified retirement plans (Safe Harbor VII).165 However, if thevoting power of publicly traded stock is decreased or otherwiseshifted upon or after a public acquisition, the public tradingexception will not apply to exempt the voting power associated withsuch stock upon its transfer.

[iv] Special Rules for Public Offerings and Auctions

The prior regulations tested public offerings and auctions underdifferent rules than generally applied to other acquisitions ofstock.166 While the new regulations continue to maintain specialrules for public offerings,167 the new regulations subject acquisi-tions involving a public auction to the same rules and presumptionsas apply to any acquisition other than a public offering.168

[v] Similar Acquisitions

The new regulations further reduce the likelihood that an acquisi-tion will be treated as part of the same plan as a distribution bylimiting the scope of the term “similar acquisition.”169 Under theprior regulations, even though the identity of the acquirer, the timingof the acquisition, or the terms of the acquisition differed betweenthe acquisitions, an acquisition may have been treated as identicalto an intended acquisition.170 The new regulations, however,generally treat an actual acquisition as similar to another acquisitiononly if the “actual acquisition effects a direct or indirect combina-tion of all or a significant portion of the same business operationsas the combination that would have been effected by such otherpotential acquisition.”171 An acquisition will not be treated as

163 Temp. Treas. Reg. § 1.355-7T(d)(5)(as amended in 2002). 164 Temp. Treas. Reg. § 1.355-7T(d)(6)(as amended in 2002). 165 Temp. Treas. Reg. § 1.355-7T(d)(7)(as amended in 2002). 166 See Temp. Treas. Reg. § 1.355-7T(d)(2)(2001). 167 See Temp. Treas. Reg. § 1.355-7T(b)(3)(ii)(as amended in 2002). 168 See Temp. Treas. Reg. § 1.355-7T(a)(as amended in 2002). 169 See Temp. Treas. Reg. § 1.355-7T(h)(8)(as amended in 2002). 170 See Temp. Treas. Reg. § 1.355-7T(b)(2)(2001). 171 Temp. Treas. Reg. § 1.355-7T(h)(8)(as amended in 2002).

§ 6.03[2]MERGERS & ACQUISITIONS — HOT TOPICS6–33

0033 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 374 163/163

substantially similar to another acquisition if the ultimate ownersof the acquired businesses operations are substantially differentfrom those of the other business.172

[vi] Options

As in the prior regulations, if an option is more likely than notto be exercised, it will be treated as an agreement, understanding,or arrangement to acquire stock on the earliest date that it waswritten, transferred, or modified to materially increase the likeli-hood of its exercise, provided that it was more likely than not tobe exercised on such date.173

[vii] Recent Private Letter Rulings

The Service ruled that a distributing corporation could divestitself of one of its two businesses which it had determined not longerfit with its strategic objectives, in a tax-free spin-off distributionunder Sections 355 and 368(a)(1)(D).174 Thereafter, immediatelyfollowing the distribution, the spun-off business (“Controlled”)would then be merged with and into an unrelated, publicly tradedacquiring company (“Acquiring”) in a transaction that would resultin Controlled shareholders receiving more than 50% of the outstand-ing Acquiring stock.175 The Private Letter Ruling contained thefollowing noteworthy rulings under Section 355(e).

Public Trading

Although Acquiring was publicly traded, as noted above, thepublic trading safe harbor will not apply if the voting powerassociated with the publicly traded stock is decreased or otherwiseshifted in connection with a public acquisition.176 As a result, thevoting power associated with such shifts is, for purposes of Section355(e), potentially counted when the underlying stock is ac-quired.177 In this case, Acquiring’s only class of common stock

172 Id. 173 Temp. Treas. Reg. § 1.355-7T(e) (as amended in 2002). 174 Priv. Ltr. Rul. 200234044 (Aug. 23, 2002). 175 Id. 176 Id. 177 Id.

6–3461ST N.Y.U. INSTITUTE§ 6.03[2]

0034 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 380 172/172

had been subject to a time-phased voting structure, wherein thevoting rights associated with each share were decreased upon atransfer or change in beneficial ownership and were restored to theoriginal amount only after ownership of the share was not changedfor a specified length of time.178 Because of the time-phased votingfeatures inherent in the Acquiring stock, Acquiring intended tomodify the voting structure of its stock in connection with theproposed merger to provide that each share would have equal andconstant voting rights for purposes of electing directors and all othermatters with the exception of certain specific matters delineated inAcquiring’s articles of incorporation.179 As a result, the time-phased voting feature of the stock remained in effect only withrespect to the specific matters granted in the articles of incorpora-tion, which included voting on plans related to:

(1) the dissolution or liquidation of Acquiring;

(2) the merger, share acquisition, or business combination ora significant lease, sale, or other disposition of assets ofAcquiring or its subsidiaries;

(3) amendments to the articles of incorporation or bylaws;

(4) matters related to a pre-existing “poison pill” plan and anystock option, compensation, and similar benefit plans,certain merger and share acquisition plans; and

(5) certain other matters generally reserved to shareholdersunder applicable laws.180

Significantly, the Service noted that Acquiring’s board of directorswould retain the types of powers traditionally reserved to a boardof directors in managing the company as they deemed fit.181

Accordingly, the Service ruled that shifts in voting power broughtabout by the time-phased voting features of the stock would notbe taken into account for purposes of Section 355(e).182 In soholding, the Service apparently reasoned, consistent with longstand-ing tax principles under Section 368, that the controlling factor inassessing the voting power of stock is the right to elect board

178 Id. 179 Id. 180 Id. 181 Id. 182 Id.

§ 6.03[2]MERGERS & ACQUISITIONS — HOT TOPICS6–35

0035 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 388 178/178

directors, as long as no material restrictions limit the ability of thedirectors to exercise the types of powers traditionally reserved tocorporate boards.183

Compensatory Issuances

Consistent with Safe Harbor VI of the revised regulationsdiscussed above, the Service ruled that post-distribution issuancesof Acquiring shares in connection with the performance of servicesby employees and directors of Acquiring in transactions underSection 83 would not be taken into account for purposes of Section355(e).184 The Service specifically indicated that this ruling wouldalso apply to acquisitions of Acquiring stock with respect to stockoptions granted to employees or directors before the distribution.185

Cash Issued for Fractional Shares

In connection with the proposed merger, Acquiring intended toaggregate for sale on the open market all fractional shares thatwould otherwise have been issuable to the Controlled shareholdersand to deliver the proceeds to the shareholders according to whowould have been entitled to the underlying shares.186 The Serviceruled that it viewed the fractional shares as having been transferredto the Controlled shareholders in the merger and then disposed ofby the shareholders in transactions that would not be counted forpurposes of Section 355(e).187

[3] Active Trade or Business Requirement

Sections 355(a)(1)(C) and 355(b) require that, immediately afterthe distribution, the distributing and controlled corporations musteach be engaged in the active conduct of a trade or business.188

Section 355(b)(2) provides, with certain limitations, that thisrequirement is satisfied only if the trade or business was activelyconducted throughout the five-year period ending on the date of

183 Id. 184 Id. 185 Id. 186 Id. 187 Id. 188 I.R.C. § 355(a)(1)(C); I.R.C. § 355(b).

6–3661ST N.Y.U. INSTITUTE§ 6.03[3]

0036 VERSACOMP (4.2 ) – COMPOSE2 (4.37) 04/26/03 (16:14) PUB 500--NYU Inst. on Federal Taxation 2nd pass

J:\VRS\DAT\00500\CH6.GML --- r500.sty --CTP READY-- v2.2 4/26 --- POST 396 183/183

distribution.189 Recent Revenue Rulings have provided guidanceon how this requirement applies to certain entities such as real estateinvestment trusts and limited liability companies, that have a specialstatus for Federal tax purposes.190

[a] Real Estate Investment Trusts (REITs)

[i] Revenue Ruling 2001-29