Embed Size (px)

Citation preview

MERGERS AND ACQUISITIONS- AN INTRODUCTION

Irfan Inamdar

CTM :CHAPTER 3

WHY ARE YOU HERE

• To learn the basics of mergers and acquisitions• To acquire knowledge about specialist M&A

firms• To know how to valuate a business• To learn how to control brand considerations

after a merger• To know the effects of mergers on management

2Irfan Inamdar

AGENDA• What is a M&A?• Differentiating M & A• Common Ways of Business Valuation• How Do We Get Finance?• Specialist M&A Advisory Firms• What Motives Lie Behind?• Effects on Management• Brand Building or Brand Destroying?• Factors of the Merger Movement• Merger Waves• Cross Border M & A• Major M&A’s

3Irfan Inamdar

WHAT IS A M&A?

• An aspect of corporate strategy, corporate finance and strategic management.

• Deals with buying, selling, combining of different companies that can– Aid– Finance– Help

a growing company in a given industry grow rapidly without having to create a new business entity.

4Irfan Inamdar

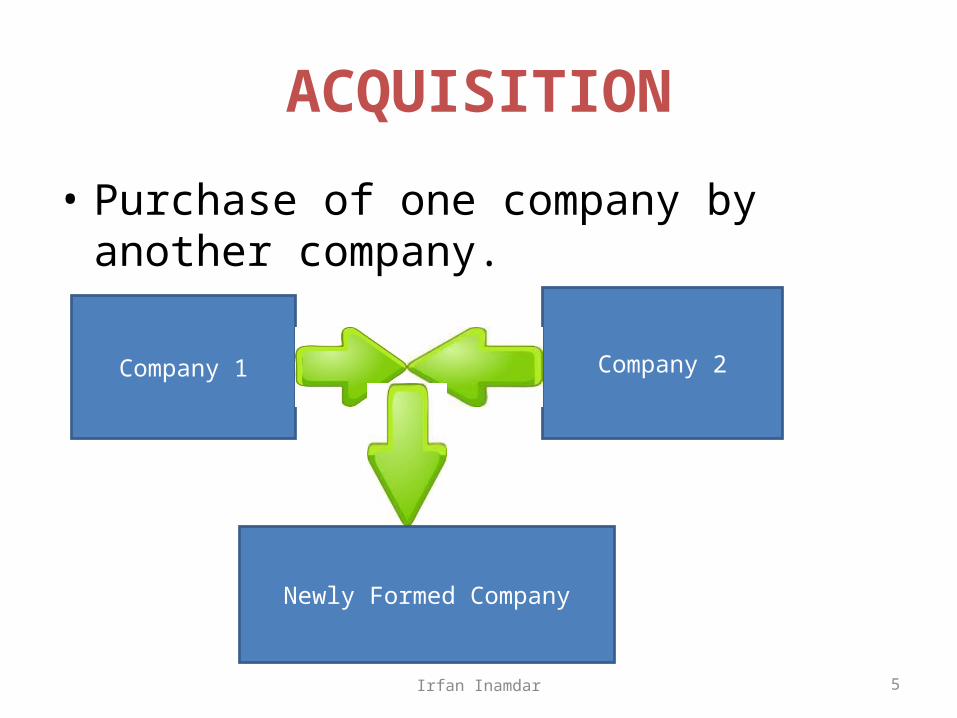

ACQUISITION

• Purchase of one company by another company.

Company 1 Company 2

Newly Formed Company

5Irfan Inamdar

TYPES OF ACQUISITIONS

• Depending upon– Acquiree or merging is or isn’t listed in public

markets.– How the communication is done and received by

the target.

6Irfan Inamdar

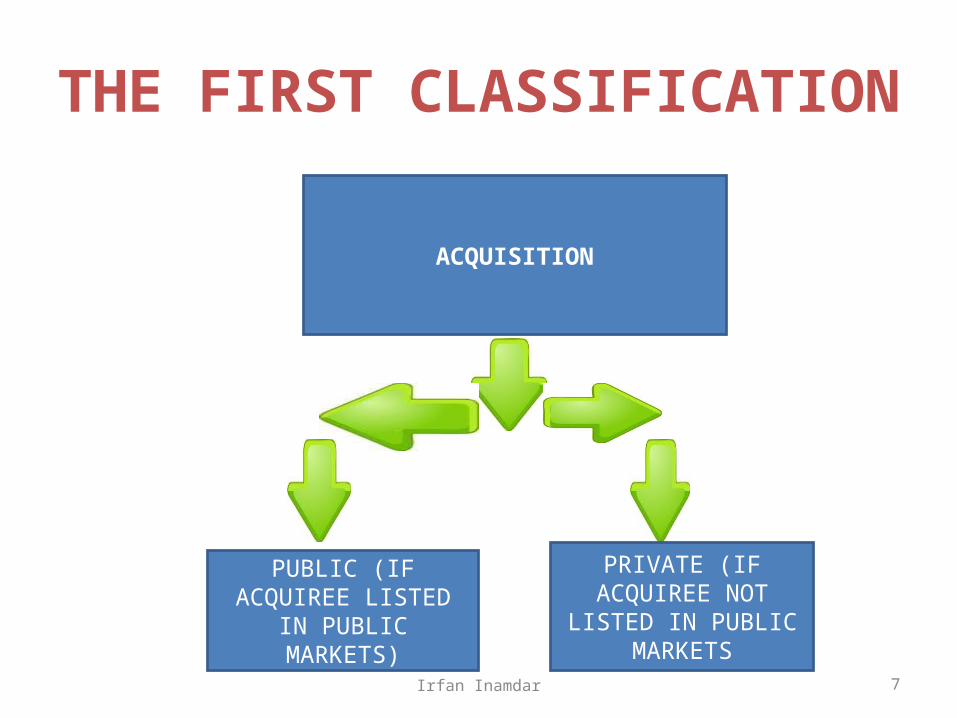

THE FIRST CLASSIFICATION

ACQUISITION

PUBLIC (IF ACQUIREE LISTED IN PUBLIC

MARKETS)

PRIVATE (IF ACQUIREE NOT LISTED IN PUBLIC

MARKETS

7Irfan Inamdar

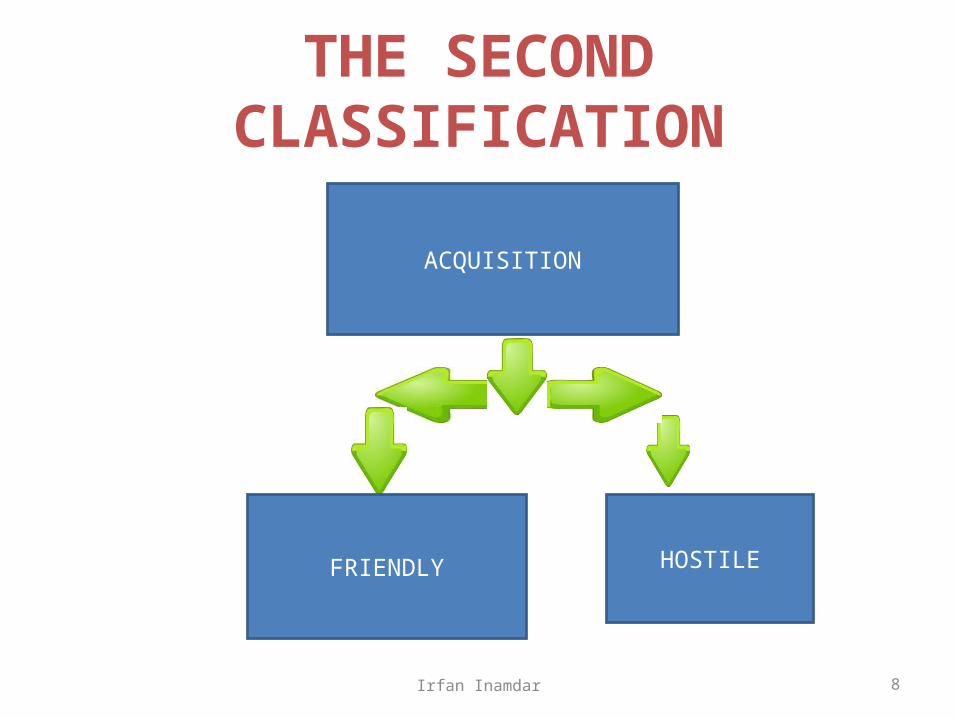

THE SECOND CLASSIFICATION

ACQUISITION

FRIENDLY HOSTILE

8Irfan Inamdar

CONFIDENTIALITY BUBBLE

• Quite normal for M&A deal communication to take place in a so called ‘confidentiality bubble’.

• Here information flows are restricted due to confidentiality agreements.

9Irfan Inamdar

FRIENDLY ACQUISITIONS

• Companies cooperate in negotiations.• Synonymous to merger of equals.

10Irfan Inamdar

HOSTILE ACQUISITIONS

• Takeover target unwilling to be purchased.• It can also be if the acquiree company has no

prior knowledge of offer.• Hostile takeovers do turn friendly in the end.

Most of the times.• For the above thing to happen, offer is usually

improved.

11Irfan Inamdar

REVERSE TAKEOVERS

• Acquisition usually refers to purchase of smaller firm by larger firm.

• Sometimes, smaller firm acquire management control of a larger / longer established company.

• Keep its name for combined entity.• Known as reverse takeover.

12Irfan Inamdar

REVERSE MERGER• Another type of acquisition.• Is a deal enabling a private company to become a

public company.• The deal enables private company by listing in a short

time period.• Occurs when a private company has strong prospects

and is eager to raise financing, buys a publicly listed shell company.

• Usually the public one is one with– No business– Limited assets

13Irfan Inamdar

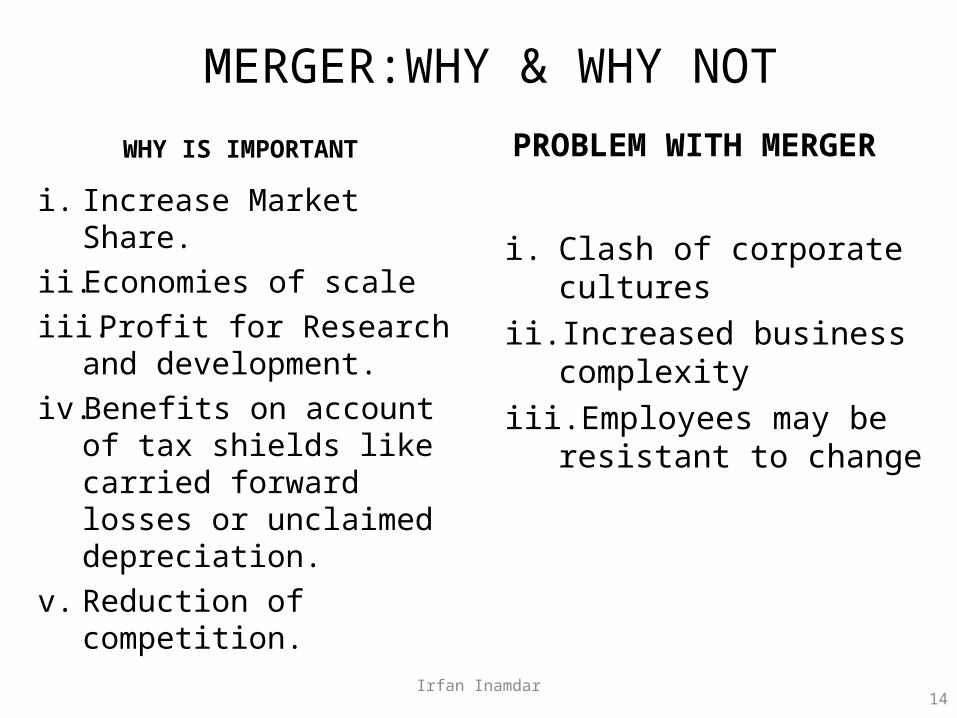

MERGER:WHY & WHY NOT

14

i. Increase Market Share.ii. Economies of scaleiii. Profit for Research and

development.iv. Benefits on account of

tax shields like carried forward losses or unclaimed depreciation.

v. Reduction of competition.

i. Clash of corporate culturesii. Increased business

complexityiii. Employees may be resistant

to change

WHY IS IMPORTANT PROBLEM WITH MERGER

Irfan Inamdar

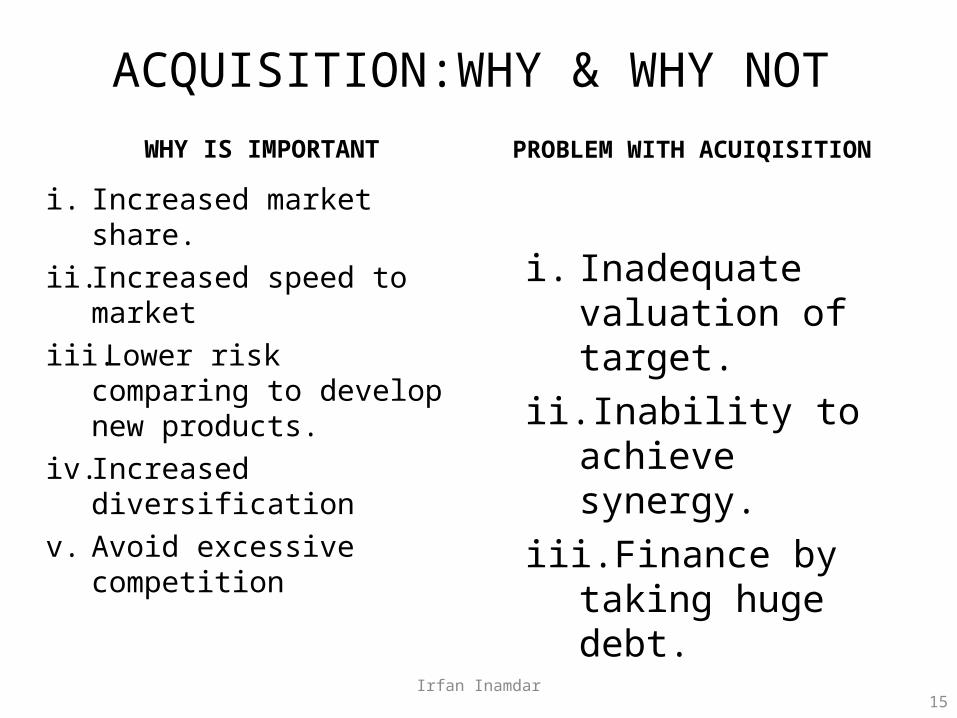

ACQUISITION:WHY & WHY NOT

15

i. Increased market share.ii. Increased speed to

marketiii. Lower risk comparing to

develop new products.iv. Increased diversificationv. Avoid excessive

competition

i. Inadequate valuation of target.

ii. Inability to achieve synergy.

iii. Finance by taking huge debt.

WHY IS IMPORTANT PROBLEM WITH ACUIQISITION

Irfan Inamdar

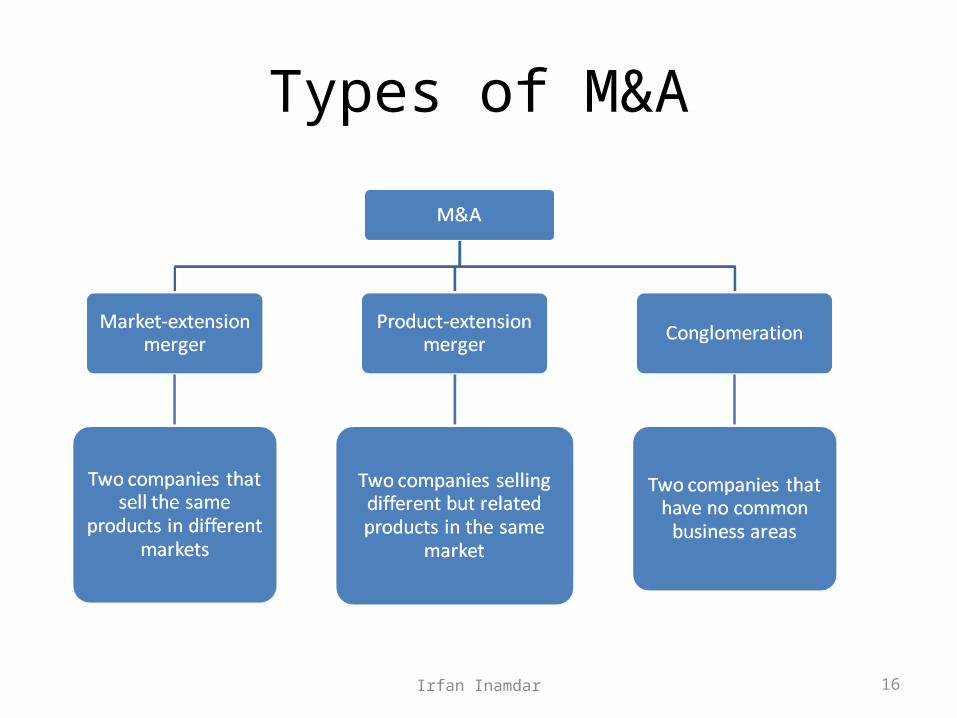

Types of M&A

16Irfan Inamdar

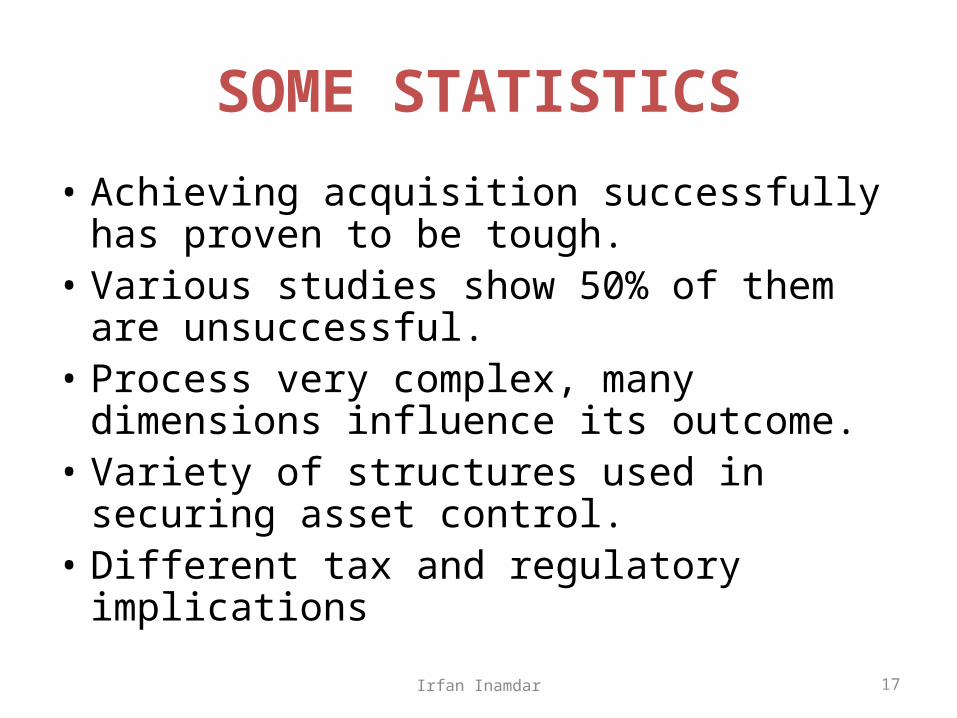

SOME STATISTICS

• Achieving acquisition successfully has proven to be tough.

• Various studies show 50% of them are unsuccessful.

• Process very complex, many dimensions influence its outcome.

• Variety of structures used in securing asset control.

• Different tax and regulatory implications

17Irfan Inamdar

THE ACQUISITION PROCESS• Buyer buys shares of target company• Ownership control conveys effective control over assets,

but since company is going concern, liabilities come as well.• Buyer buys assets of target company.• Cash target receives from sell-off is paid back to its

shareholders by– Dividend– Through liquidation

• If buyer buys out entire assets, then target company = empty shell.

• Buyer often cherry picks his assets

18Irfan Inamdar

SOME OTHER TERMS

• There are some other terms used as well like:– Demergers– Spin-off– Spin-out

• Sometimes used to indicate a situation where one company splits into two, generating a 2nd company separately listed on a stock exchange.

19Irfan Inamdar

DIFFERENTIATING MERGERS AND ACQUISITIONS

• Both terms are often used synonymously.• They mean slightly different things in reality.

20Irfan Inamdar

ACQUISITIONS FIRST

• When one company takes over another, clearly establishes as its new owner.

• Legal View: target ceases to exist.• Buyer swallows target• Buyer’s stock continues to be traded.

21Irfan Inamdar

MERGERS NEXT

• Happens when two firms agree to go forward as a single new company rather than remain separate.

• Often precisely termed as merger of equals.• Firms are often of same size.• Both companies stock surrendered• New company stock put into place instead.• Example: 1999 merger of Glaxo Wellcome and

SmithKline Beecham, both firms ceased to exist and a new firm GlaxoSmithKline was created.

22Irfan Inamdar

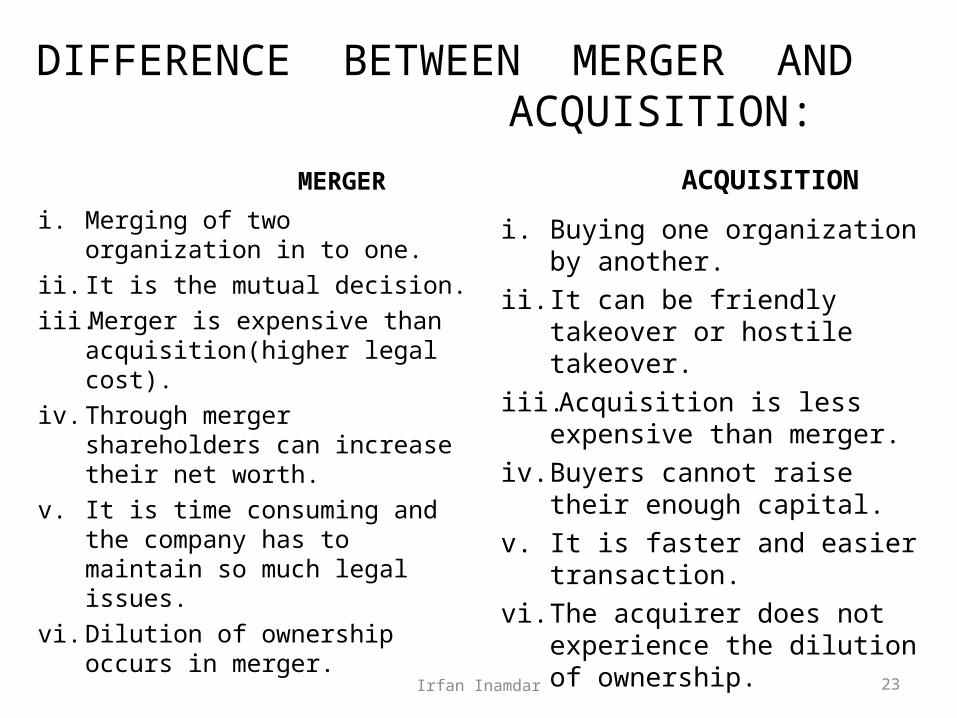

DIFFERENCE BETWEEN MERGER AND ACQUISITION:

i. Merging of two organization in to one.

ii. It is the mutual decision.iii. Merger is expensive than

acquisition(higher legal cost).iv. Through merger shareholders

can increase their net worth.v. It is time consuming and the

company has to maintain so much legal issues.

vi. Dilution of ownership occurs in merger.

i. Buying one organization by another.

ii. It can be friendly takeover or hostile takeover.

iii. Acquisition is less expensive than merger.

iv. Buyers cannot raise their enough capital.

v. It is faster and easier transaction.

vi. The acquirer does not experience the dilution of ownership.

MERGER ACQUISITION

23Irfan Inamdar

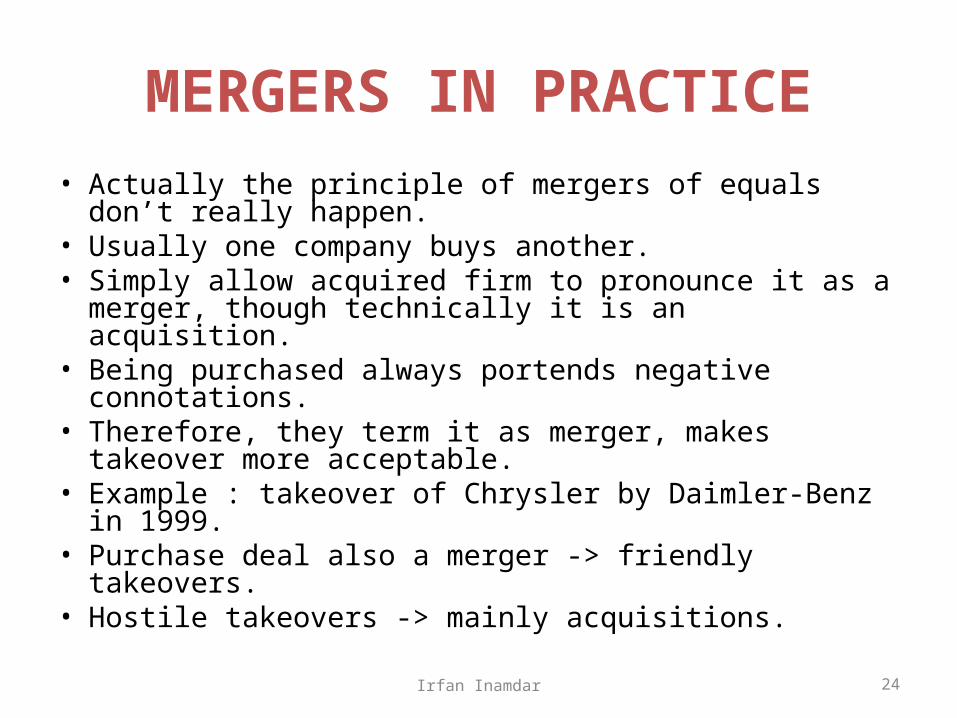

MERGERS IN PRACTICE• Actually the principle of mergers of equals don’t really

happen.• Usually one company buys another.• Simply allow acquired firm to pronounce it as a merger,

though technically it is an acquisition.• Being purchased always portends negative connotations.• Therefore, they term it as merger, makes takeover more

acceptable.• Example : takeover of Chrysler by Daimler-Benz in 1999.• Purchase deal also a merger -> friendly takeovers.• Hostile takeovers -> mainly acquisitions.

24Irfan Inamdar

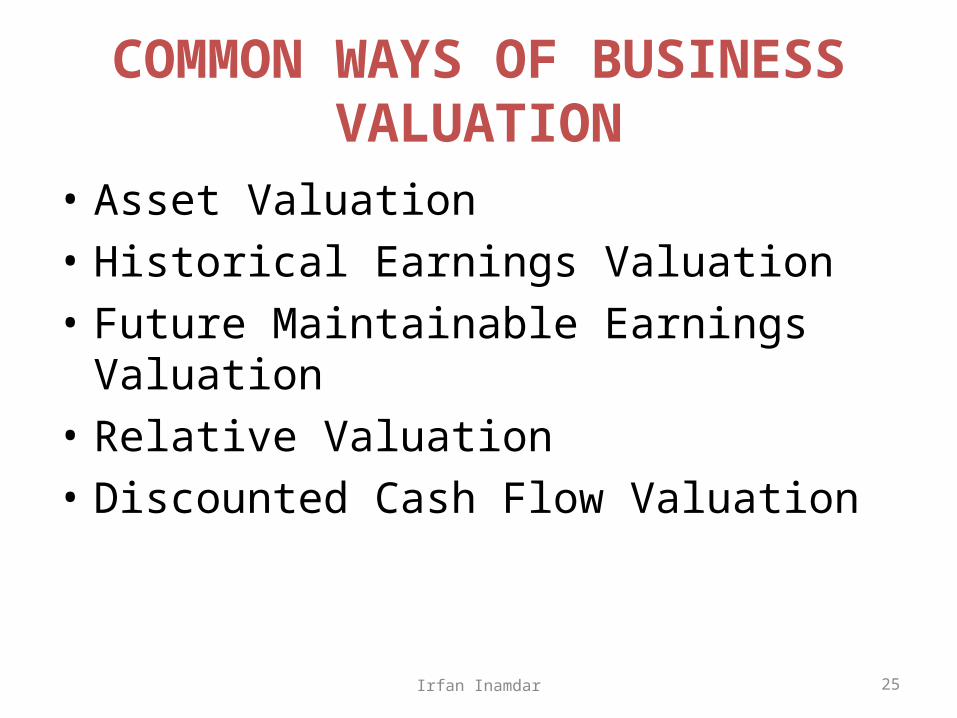

COMMON WAYS OF BUSINESS VALUATION

• Asset Valuation• Historical Earnings Valuation• Future Maintainable Earnings Valuation• Relative Valuation• Discounted Cash Flow Valuation

25Irfan Inamdar

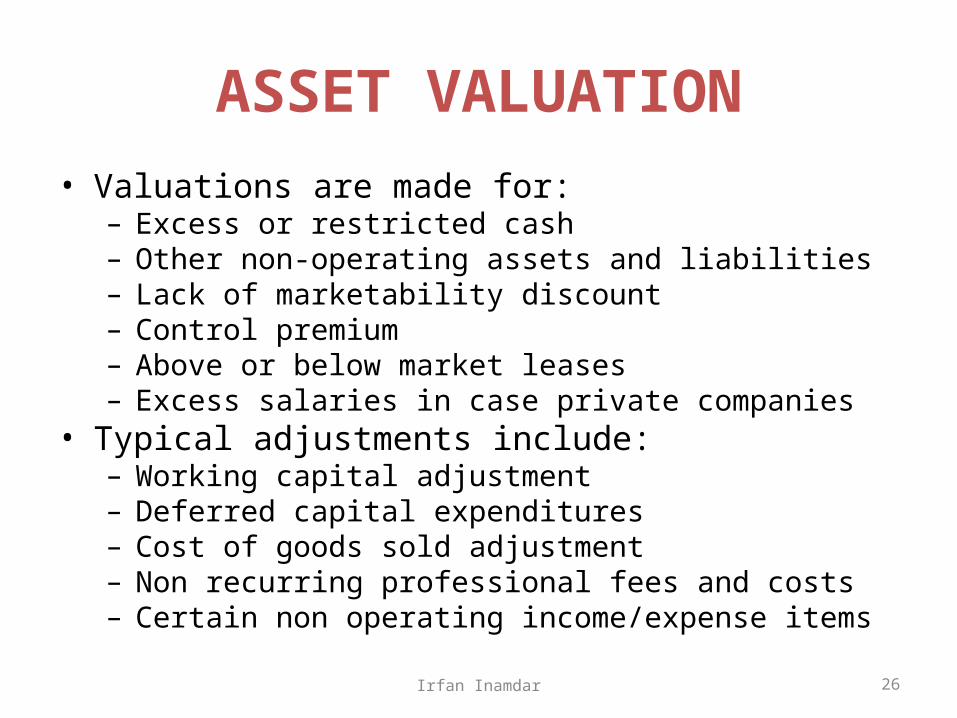

ASSET VALUATION• Valuations are made for:

– Excess or restricted cash– Other non-operating assets and liabilities– Lack of marketability discount– Control premium– Above or below market leases– Excess salaries in case private companies

• Typical adjustments include:– Working capital adjustment– Deferred capital expenditures– Cost of goods sold adjustment– Non recurring professional fees and costs– Certain non operating income/expense items

26Irfan Inamdar

VALUATION OF INTANGIBLE ASSETS

• Can be made for intangible assets like:– Patents– Copyrights– Software– Trade secrets– Customer relationships

• Uses either– Present value model– Estimating the costs to recreate it

• Process time consuming and costly• Often necessary for financial reporting and intellectual property

transactions.• Stock markets give only an indirect value.• Can be regarded as difference between its market capitalization and its

book value.

27Irfan Inamdar

VALUATION OF MINING PROJECTS

• Process of determining the value of a mining property.• Sometimes required for:– Initial Public Offers– Fairness opinions– Litigations– Mergers and acquisitions– Shareholder related matters

• Fair market value is standard value.• CIMVal Standards are recognized standards for mining

project valuations.

28Irfan Inamdar

HISTORICAL EARNINGS VALUATION

• Uses EPS (Earnings Per Share) values for valuation of stock.

• Figures can be used for forecasting performance by visiting free financial sites such as Yahoo Finance.

29Irfan Inamdar

RELATIVE VALUATION• Generic term that refers to the notion of comparing asset price to market

value of similar assets.• Presumably spot pricing anomalies on securities market.• Compare certain financial ratios such as:

– Price to book value– Price to earnings– EV/EBITDA– Mainly statistical and historical

• Compare national or industry stock performance to economic and market fundamentals like:– GDP growth– Interest rate– Inflation forecasts– Earnings growth– National equity index

30Irfan Inamdar

DISCOUNTED CASH FLOW METHOD

• Abbreviated as DCF• Uses concepts of time value of money• All future cash flows are estimated and discounted to give

their present values(PV’s).• Sum of all future values, is net present value (NPV).• Widely used in investment finance, real estate

development, corporate financial management• Most commonly used method is exponential discounting.• Other methods are:

– Hyperbolic discounting• Discount rate used is Weighted Average Cost of Capital

(WACC).

31Irfan Inamdar

HOW DO WE GET FINANCE?

• We can differentiate mergers and acquisitions by the way they are financed.

• Various methods of financing include:– Cash– Stock

32Irfan Inamdar

THINK STRATEGIC!!!!

• With pure cash deals, no doubt on real bid value.

• Contingency of share payment removed.,• Cash offer preempts competitors.

33Irfan Inamdar

TAXES

• Should be evaluated with counsel of – Competent tax advisors– Competent accounting advisors

34Irfan Inamdar

CASH V/S SHARES• With a share deal, buyer’s capital structure might

be affected and control of new company modified.

• If issuance of shares necessary, shareholders might prevent capital increase.

• Risk removed with cash transaction.• In cash deal, balance sheet of buyer will be

modified, liquidity ratios might decrease.• In stock transactions, lower profitability ratios

might show.

35Irfan Inamdar

THE CASH DEAL• If buyer pays cash, there are 3 main financing

options:– Cash on Hand: consumes financial slack. May

decrease debt rating. No major transaction costs,– Issue of debt: consumes financial slack. May decrease

debt rating. Increases cost of debt. Transaction costs include underwriting or closing costs of 1% to 3% of face value.

– Issue of stock: increases financial slack, may improve debt rating, reduce cost of debt, transaction costs include fees for preparation of proxy statement, an extraordinary shareholder meeting, registration.

36Irfan Inamdar

THE STOCK DEAL

• If buyer pays with stock:– Issue of Stock– Shares in Treasury: increases financial slack,

improve debt rating, reduce cost of debt, transaction costs include brokerage fees if shares repurchased in market otherwise no major costs.

37Irfan Inamdar

LETS GENERALIZE…

• Stock will create flexibility.• Transaction costs also to be considered but

tend to have greater impact.• Remember:

Buyers tend to offer stock when they believe their shares are overvalued and cash when undervalued.

38Irfan Inamdar

SPECIALIST M&A ADVISORY FIRMS

• Provided usually by– Full service investment banks

• Recently, specialized M&A firms have emerged.

• Sometimes referred to as Transition Companies.

• Assisting business referred to as companies in transition.

39Irfan Inamdar

CROSS SELLING

• A bank buying a stock broking firm• Manufacturer acquiring and selling

complementary products.

40Irfan Inamdar

TAXATION

• Profitable company can buy a loss maker to use target’s loss as their advantage by reducing their tax liability.

• But there are certain regulations to follow.

41Irfan Inamdar

GEOGRAPHICAL DIVERSIFICATION

• Designed to smooth company earnings• Smoothens stock price• Gives conservative investors more confidence• But does not always deliver value to

shareholders.

42Irfan Inamdar

RESOURCE TRANSFER

• Resources unevenly distributed across firms.• Can create value by– Overcoming information asymmetry– Combining scarce resources

43Irfan Inamdar

VERTICAL INTEGRATION

• Occurs when an upstream firm merges with a downstream firm.

• One reason is externality problem.• Common example is double marginalization

44Irfan Inamdar

EFFECTS ON MANAGEMENT

• M&A according to some studies destroy leadership continuity in target companies.

• Target companies lose 21% of their executives each year following an acquisition.

45Irfan Inamdar

BRAND CONSIDERATIONS• M&A’s often create brand problems.• 4 different approaches:

– Keep one name and discontinue other. Ex: United Airlines and Continental Airlines Merger.

– Keep one name and demote other: Caterpillar Inc. keeping Bucyrus International.

– Keep both names and use together: Pricewaterhouse Coopers.– Discard both legacy names and adopt new one:

• merger of Bell Atlantic and GTE which became Verizon Communications. This merger was successful.

• Merger of Yellow Freight and Roadway Corporation which became YRC Worldwide. This merger was partially successful, brand value lost.

• Factors range from political to tactical.• Ego as well as rational factors drive choice.• Rational factors : brand value, costs involved with changing brands.

46Irfan Inamdar

THE MERGER MOVEMENT

• Predominantly a US phenomenon.• Short run factors: desire to keep prices high,• Long run factors: reduction of transportation

and production costs.

47Irfan Inamdar

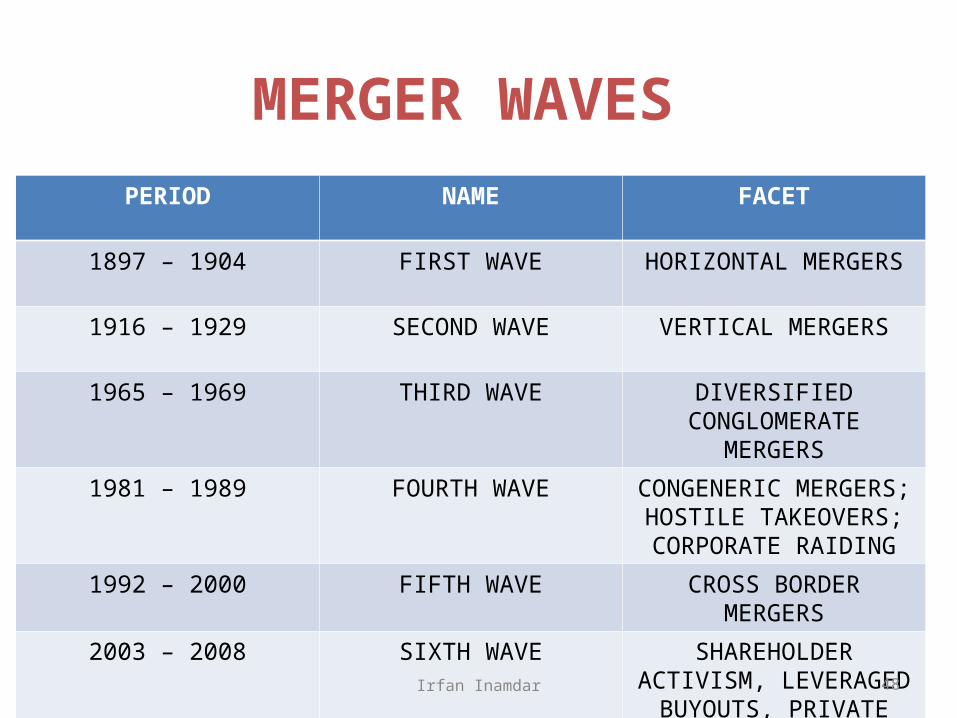

MERGER WAVESPERIOD NAME FACET

1897 – 1904 FIRST WAVE HORIZONTAL MERGERS

1916 – 1929 SECOND WAVE VERTICAL MERGERS

1965 – 1969 THIRD WAVE DIVERSIFIED CONGLOMERATE MERGERS

1981 – 1989 FOURTH WAVE CONGENERIC MERGERS; HOSTILE TAKEOVERS; CORPORATE RAIDING

1992 – 2000 FIFTH WAVE CROSS BORDER MERGERS

2003 – 2008 SIXTH WAVE SHAREHOLDER ACTIVISM, LEVERAGED BUYOUTS,

PRIVATE EQUITY 48Irfan Inamdar

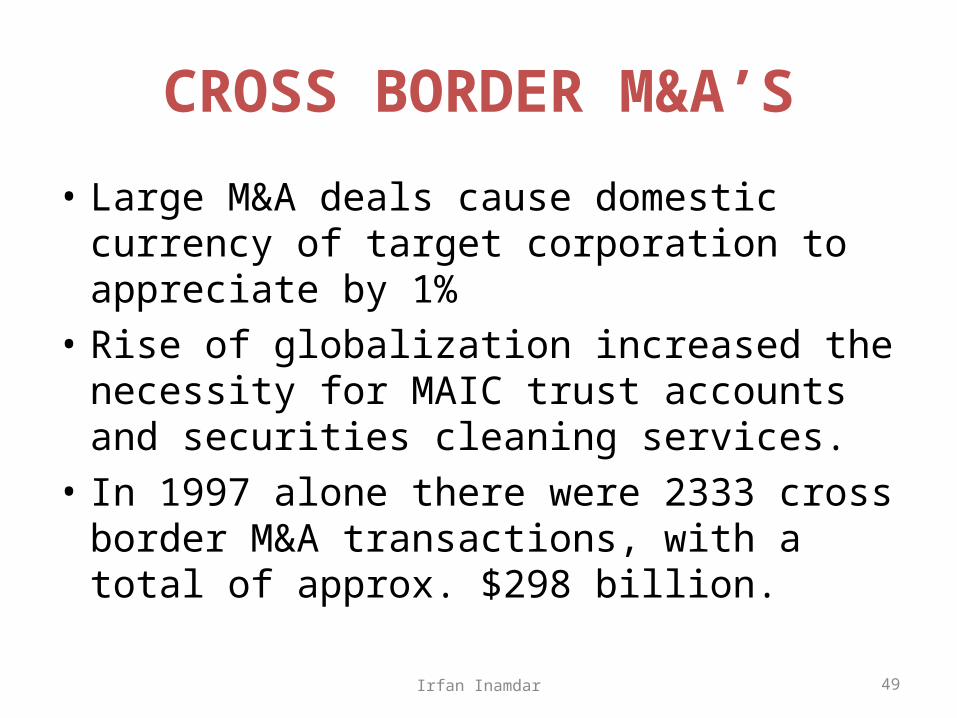

CROSS BORDER M&A’S

• Large M&A deals cause domestic currency of target corporation to appreciate by 1%

• Rise of globalization increased the necessity for MAIC trust accounts and securities cleaning services.

• In 1997 alone there were 2333 cross border M&A transactions, with a total of approx. $298 billion.

49Irfan Inamdar

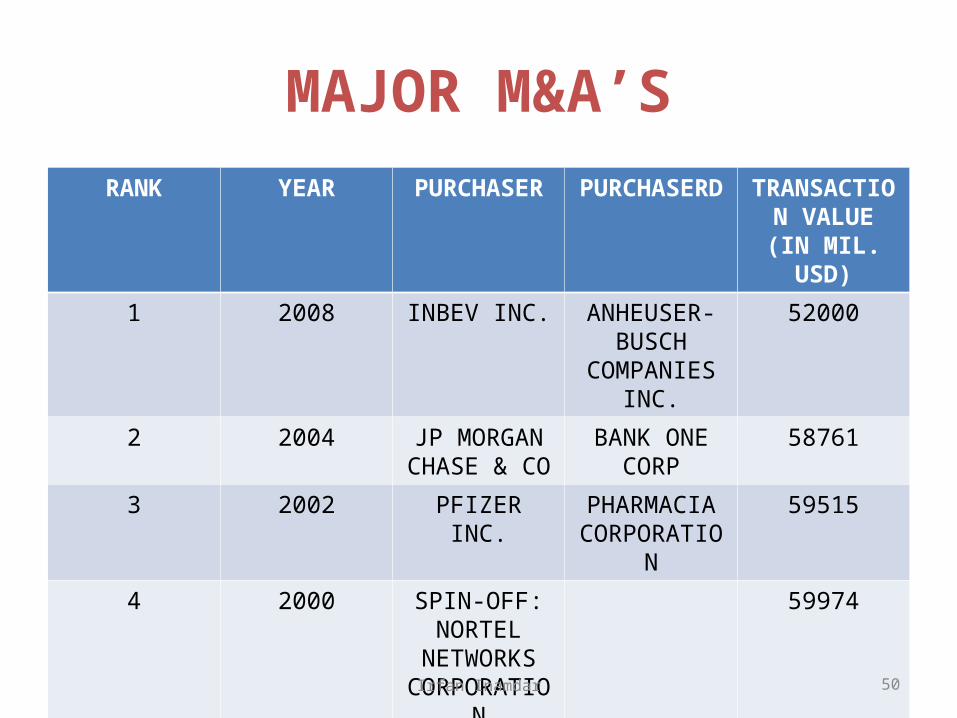

MAJOR M&A’SRANK YEAR PURCHASER PURCHASERD TRANSACTION

VALUE (IN MIL. USD)

1 2008 INBEV INC. ANHEUSER-BUSCH

COMPANIES INC.

52000

2 2004 JP MORGAN CHASE & CO

BANK ONE CORP

58761

3 2002 PFIZER INC. PHARMACIA CORPORATION

59515

4 2000 SPIN-OFF: NORTEL

NETWORKS CORPORATION

59974

5 2009 PFIZER INC. WYETH 6800050Irfan Inamdar

1. Tata Steel-Corus: $12.2 billion

• January 30, 2007

• Largest Indian take-over

• After the deal TATA’S

became the 5th largest

STEEL co.

• 100 % stake in CORUS

paying Rs 428/- per share

Image: B Mutharaman, Tata Steel MD; Ratan Tata, Tata chairman; J Leng, Corus chair; and P Varin, Corus CEO.

51Irfan Inamdar

2. Vodafone-Hutchison Essar: $11.1 billion

• TELECOM sector• 11th February 2007• 2nd largest takeover

deal• 67 % stake holding in

hutch

Image: The then CEO of Vodafone Arun Sarin visits Hutchison Telecommunications head office in Mumbai. 52Irfan Inamdar

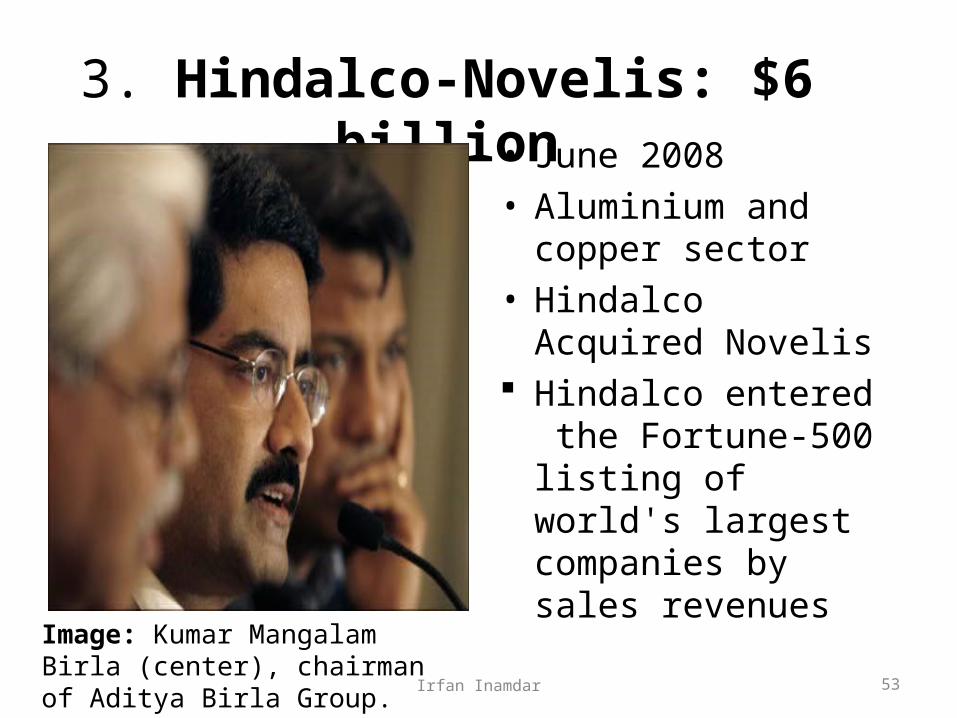

3. Hindalco-Novelis: $6 billion• June 2008• Aluminium and copper

sector• Hindalco Acquired

Novelis Hindalco entered the

Fortune-500 listing of world's largest companies by sales revenues

Image: Kumar Mangalam Birla (center), chairman of Aditya Birla Group.

53Irfan Inamdar

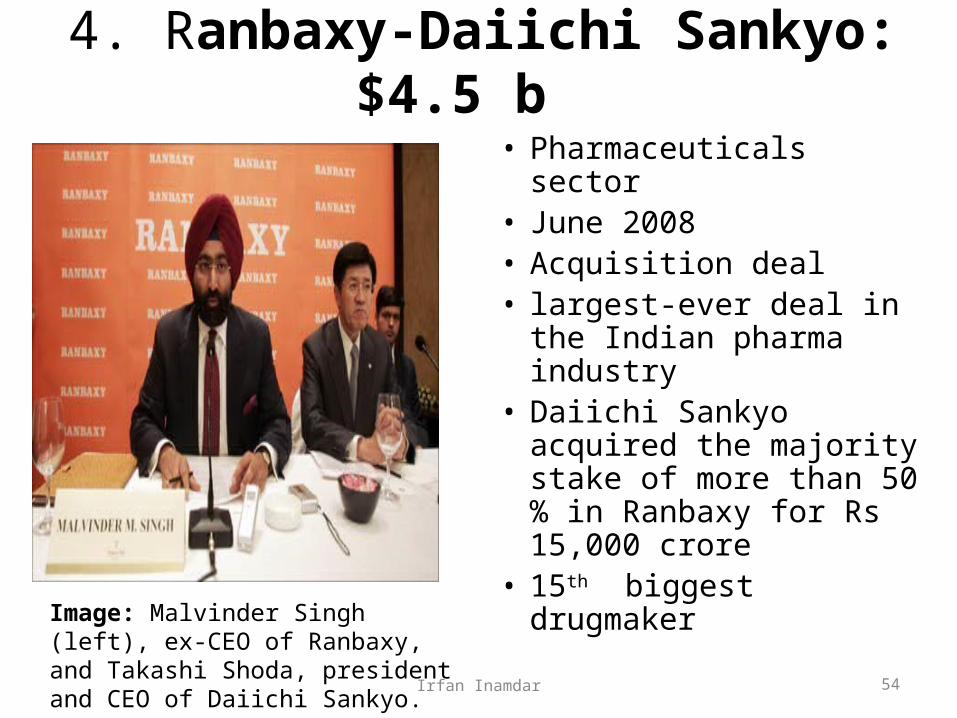

4. Ranbaxy-Daiichi Sankyo: $4.5 b

• Pharmaceuticals sector• June 2008• Acquisition deal• largest-ever deal in the

Indian pharma industry• Daiichi Sankyo acquired

the majority stake of more than 50 % in Ranbaxy for Rs 15,000 crore

• 15th biggest drugmakerImage: Malvinder Singh (left), ex-CEO of Ranbaxy, and Takashi Shoda, president and CEO of Daiichi Sankyo.

54Irfan Inamdar

5. ONGC-Imperial Energy:$2.8billion

• January 2009• Acquisition deal• Imperial energy is a

biggest chinese co.• ONGC paid 880 per

share to the shareholders of imperial energy

• ONGC wanted to tap the siberian market

Image: Imperial Oil CEO Bruce March. 55Irfan Inamdar

6. NTT DoCoMo-Tata Tele: $2.7 b

• November 2008 • Telecom sector• Acquisition deal • Japanese telecom giant

NTT DoCoMo acquired 26 per cent equity stake in Tata Teleservices for about Rs 13,070 cr.

Image: A man walks past a signboard of Japan's biggest mobile phone operator NTT Docomo Inc. in Tokyo. 56Irfan Inamdar

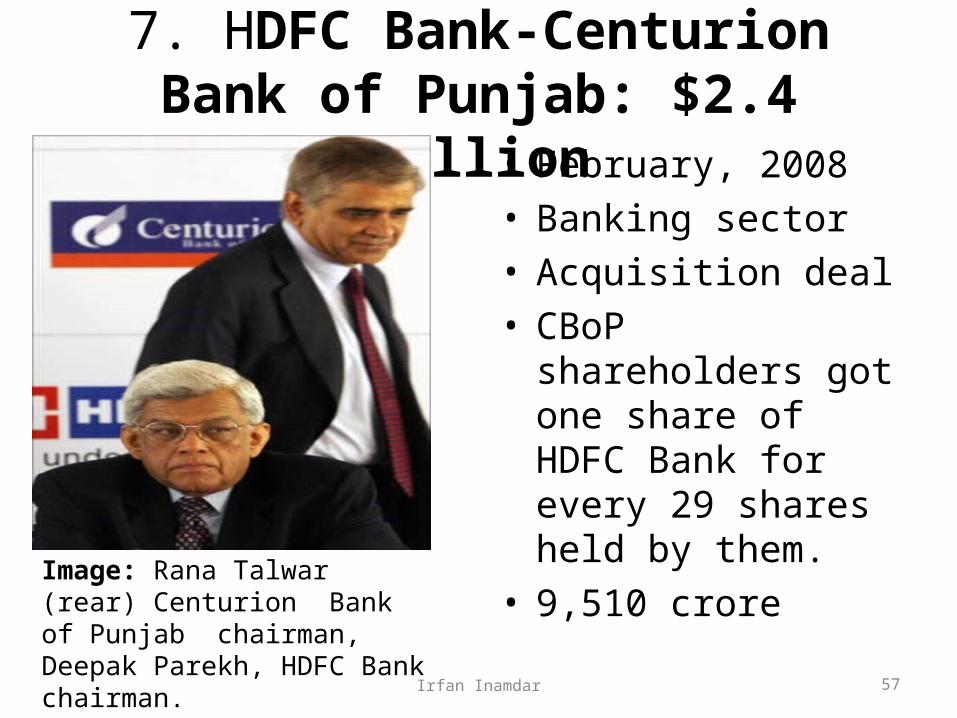

7. HDFC Bank-Centurion Bank of Punjab: $2.4 billion

• February, 2008• Banking sector• Acquisition deal• CBoP shareholders got

one share of HDFC Bank for every 29 shares held by them.

• 9,510 crore

Image: Rana Talwar (rear) Centurion Bank of Punjab chairman, Deepak Parekh, HDFC Bank chairman.

57Irfan Inamdar

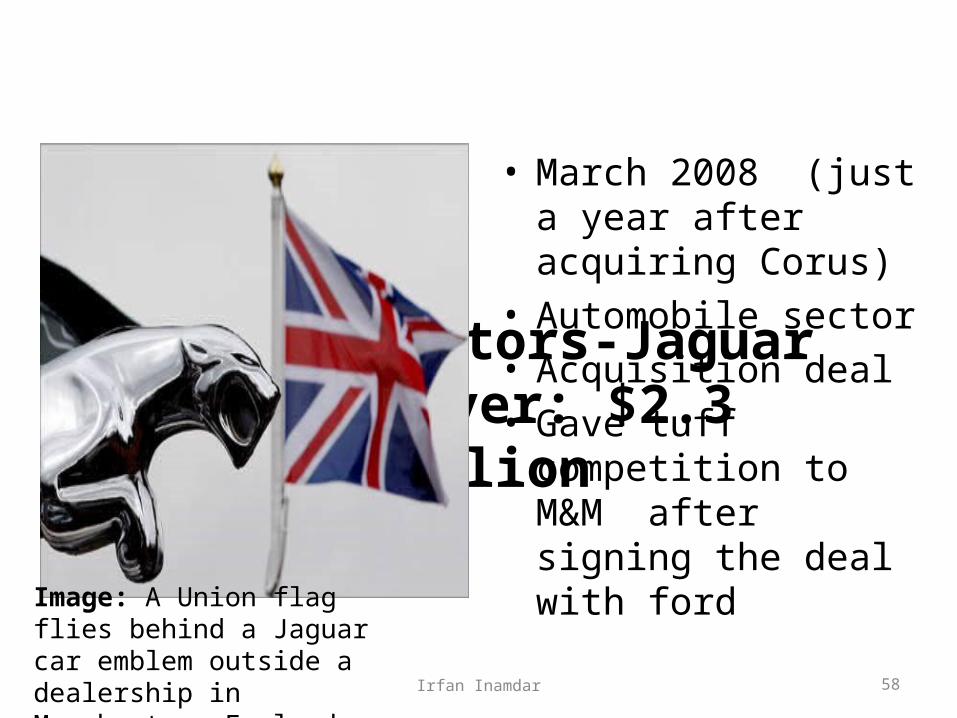

8. Tata Motors-Jaguar Land Rover: $2.3 billion

• March 2008 (just a year after acquiring Corus)

• Automobile sector• Acquisition deal• Gave tuff competition to

M&M after signing the deal with ford

Image: A Union flag flies behind a Jaguar car emblem outside a dealership in Manchester, England.

58Irfan Inamdar

9. Sterlite-Asarco: $1.8 billion• May 2008• Acquisition deal• Sector copper

Image: Vedanta Group chairman Anil Agarwal. 59Irfan Inamdar

10. Suzlon-RePower: $1.7 billion• May 2007 • Acquisition deal• Energy sector• Suzlon is now the

largest wind turbine maker in Asia

• 5th largest in the world.

Image: Tulsi Tanti, chairman & M.D of Suzlon Energy Ltd. 60Irfan Inamdar

11. RIL-RPL merger: $1.68 billion• March 2009• Merger deal• amalgamation of its

subsidiary Reliance Petroleum with the parent company Reliance industries ltd.

• Rs 8,500 crore• RIL-RPL merger swap

ratio was at 16:1Image: Reliance Industries' chairman Mukesh Ambani.

61Irfan Inamdar

Why India?

• Dynamic government policies• Corporate investments in industry• Economic stability• “Ready to experiment” attitude of Indian

industrialists

62Irfan Inamdar

Amongst BRIC Nations, India second most targeted country for Mergers & Acquisitions(2010):

63Irfan Inamdar

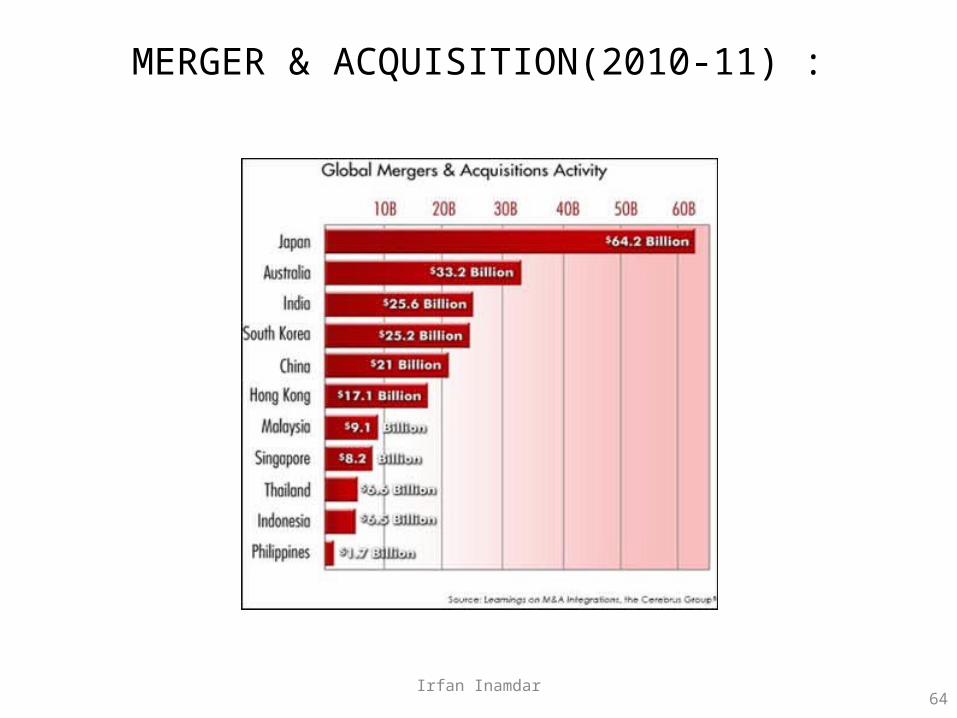

MERGER & ACQUISITION(2010-11) :

64Irfan Inamdar

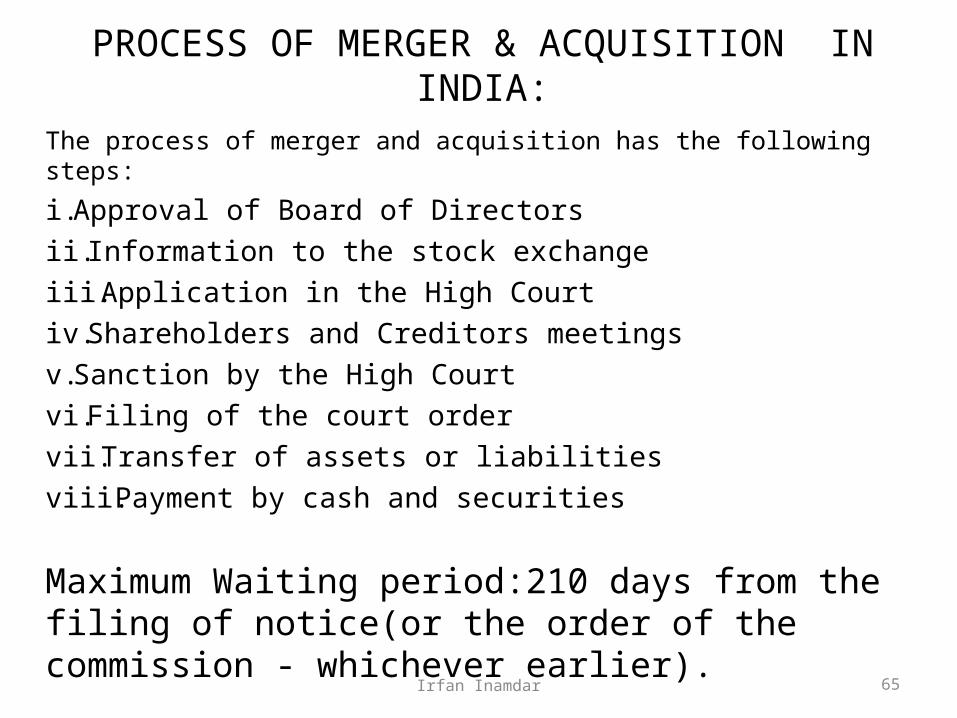

PROCESS OF MERGER & ACQUISITION IN INDIA:

The process of merger and acquisition has the following steps:

i.Approval of Board of Directorsii.Information to the stock exchangeiii.Application in the High Courtiv.Shareholders and Creditors meetingsv.Sanction by the High Courtvi.Filing of the court ordervii.Transfer of assets or liabilitiesviii.Payment by cash and securities

Maximum Waiting period:210 days from the filing of notice(or the order of the commission - whichever earlier). 65Irfan Inamdar

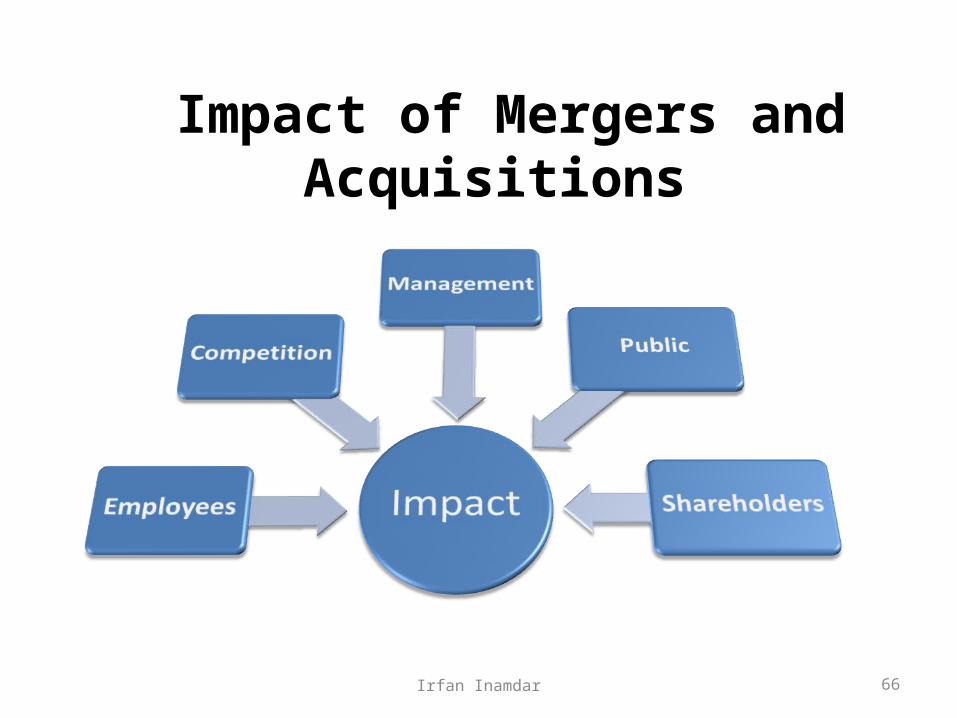

Impact of Mergers and Acquisitions

66Irfan Inamdar

Why Mergers and Acquisitions Fail?

• Cultural Difference

• Flawed Intention

• No guiding principles

• No ground rules

• No detailed investigating

• Poor stake holder outreach67Irfan Inamdar

How to Prevent the Failure

• Continuous communication – employees,

stakeholders, customers, suppliers and

government leaders.

• Transparency in managers operations

• Capacity to meet new culture higher

management professionals must be ready to greet

a new or modified culture.

• Talent management by the management68Irfan Inamdar

A CASE STUDY MERGER BETWEEN AIR INDIA AND

INDIAN AIRLINES

69

Irfan Inamdar

MERGER BETWEEN AIR INDIA AND INDIAN AIRLINES

• The government of India on 1 march 2007 approved the merger of Air India and Indian airlines.

• Consequent to the above a new company called National Aviation Company of India limited was incorporated under the companies act 1956 on 30 march 2007 with its registered office at New Delhi.

70

Irfan Inamdar

aim of the merger • Create the largest airline in India and comparable to other airlines in

Asia. • Provide an Integrated international/ domestic footprint which will

significantly enhance customer proposition and allow easy entry into one of the three global airline alliances, mostly Star Alliance with global consortium of 21 airlines.

• Enable optimal utilization of existing resources through improvement in load factors and yields on commonly serviced routes as well as deploy ‘freed up’ aircraft capacity on alternate routes.

• The merger had created a mega company with combined revenue of Rs 150 billion ($3.7billion) and an estimated fleet size of 150. It had a diverse mix of aircraft for short and long haul resulting in better fleet utilization.

• Provide an opportunity to fully leverage strong assets, capabilities and infrastructure.

• Provide an opportunity to leverage skilled and experienced manpower available with both the Transferor Companies to the optimum potential.

• Provide a larger and growth oriented company for the people and the same shall be in larger public interest. 71

Irfan Inamdar

aim of the merger • Potential to launch high growth & profitability businesses (Ground

Handling Services, Maintenance Repair and Overhaul etc.) • Provide maximum flexibility to achieve financial and capital

restructuring through revaluation of assets. • Economies of scale enabled routes rationalization and elimination of

route duplication. This resulted in a saving of Rs1.86 billion, ($0.04 billion) and the new airlines will be offering more competitive fares, flying seven different types of aircraft and thus being more versatile and utilizing assets like real estate, human resources and aircraft better. However the merger had also brought close to $10 billion (Rs 440 billion) of debt.

• The new entity was in a better position to bargain while buying fuel, spares and other materials. There were also major operational benefits.

• Traffic rights - The protectionism enjoyed by the national carriers with regard to the traffic right entitlements is likely to continue even after the merger. This will ensure that the merged Airlines will have enough scope for continued expansion, necessitated due to their combined fleet strength.

72

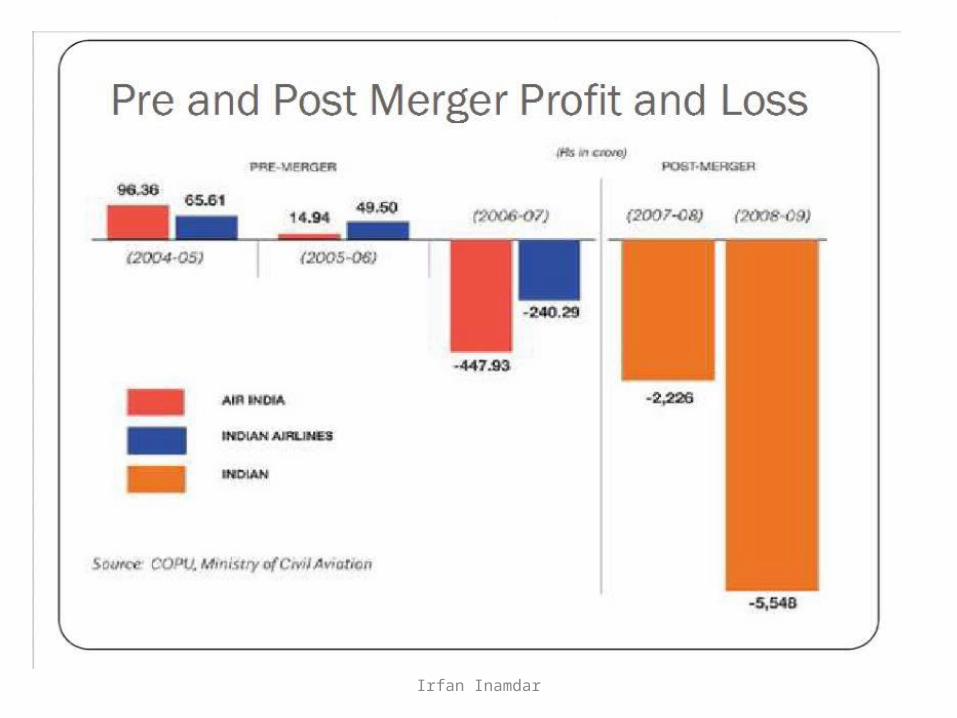

Irfan Inamdar

73

Irfan Inamdar

74

Irfan Inamdar

75

Irfan Inamdar

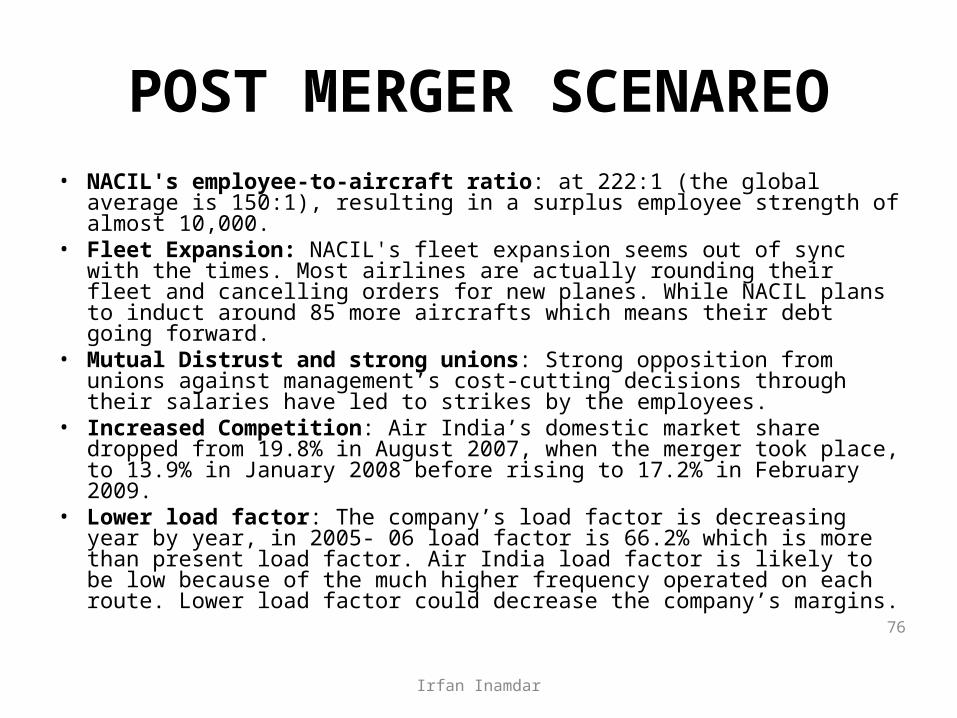

POST MERGER SCENAREO• NACIL's employee-to-aircraft ratio: at 222:1 (the global average is 150:1),

resulting in a surplus employee strength of almost 10,000.• Fleet Expansion: NACIL's fleet expansion seems out of sync with the

times. Most airlines are actually rounding their fleet and cancelling orders for new planes. While NACIL plans to induct around 85 more aircrafts which means their debt going forward.

• Mutual Distrust and strong unions: Strong opposition from unions against management’s cost-cutting decisions through their salaries have led to strikes by the employees.

• Increased Competition: Air India’s domestic market share dropped from 19.8% in August 2007, when the merger took place, to 13.9% in January 2008 before rising to 17.2% in February 2009.

• Lower load factor: The company’s load factor is decreasing year by year, in 2005- 06 load factor is 66.2% which is more than present load factor. Air India load factor is likely to be low because of the much higher frequency operated on each route. Lower load factor could decrease the company’s margins. 76

Irfan Inamdar

77

Irfan Inamdar

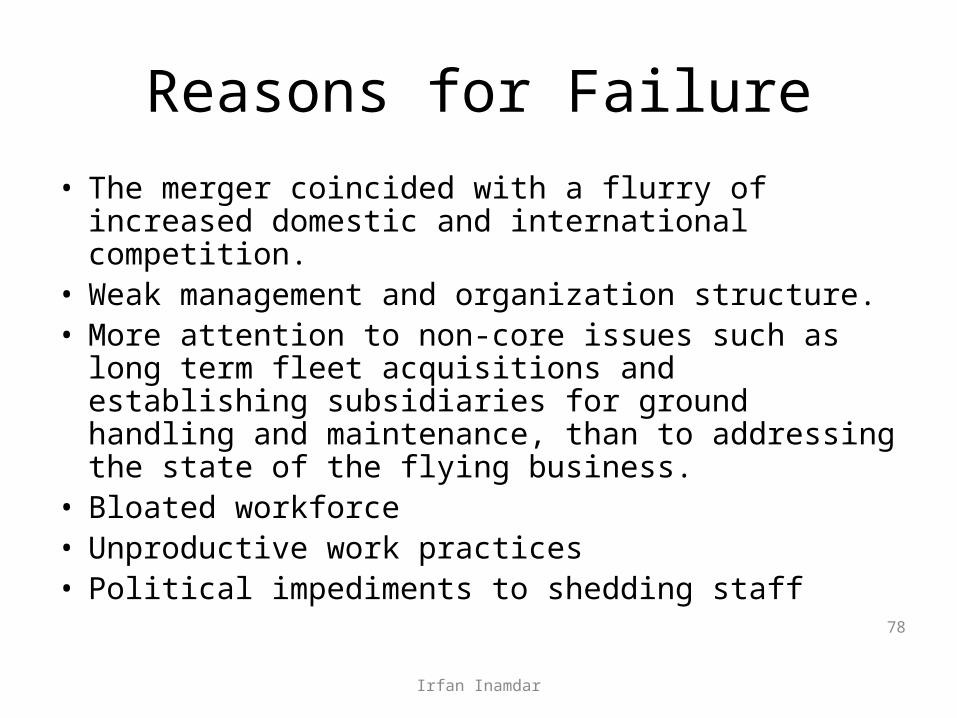

Reasons for Failure

• The merger coincided with a flurry of increased domestic and international competition.

• Weak management and organization structure. • More attention to non-core issues such as long term

fleet acquisitions and establishing subsidiaries for ground handling and maintenance, than to addressing the state of the flying business.

• Bloated workforce• Unproductive work practices • Political impediments to shedding staff

78

Irfan Inamdar

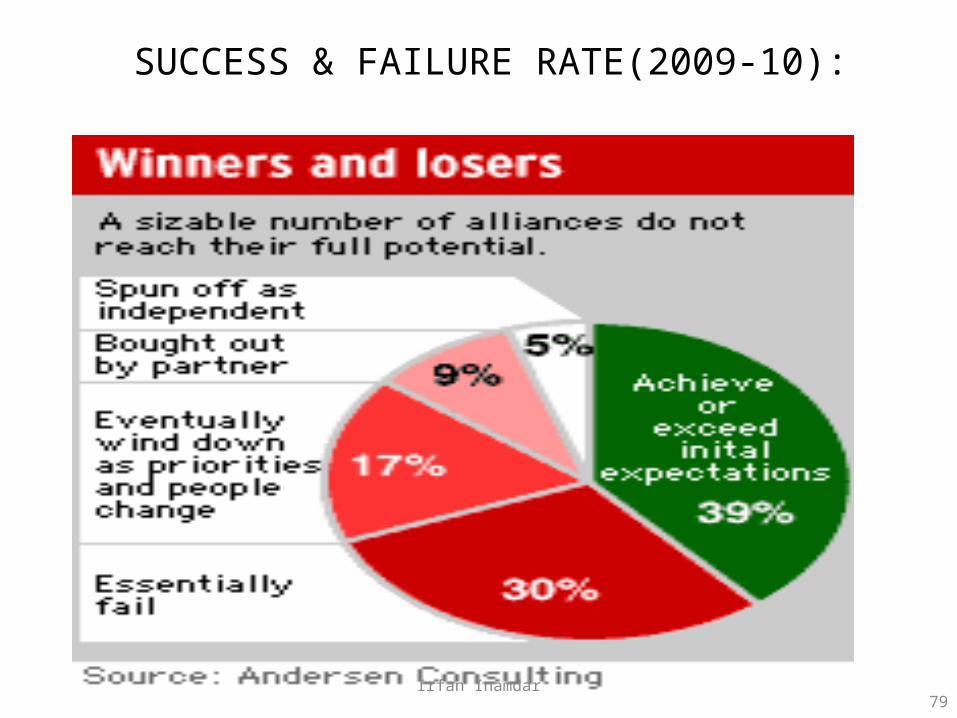

SUCCESS & FAILURE RATE(2009-10):

79Irfan Inamdar

EXPERIENCES IN M&A• Learn from mistakes of others• Define your objectives clearly• Complete strategy to achieve goal.• SWOT analysis for the merged business - a must• Conservative attitude necessary at evaluation

deskstrong arguments to support project• Pick holes in strategy to get the best• Will merged units be able to work at efficient /

ideal level?• Acquire expertise to interpret changes

80Irfan Inamdar

THANK YOU

81Irfan Inamdar