Embed Size (px)

Citation preview

Mergers and acquisitions Basics

Mergers and acquisitions BasicsAll You Need To Know

donald dePamphilis

Amsterdam • Boston • Heidelberg • LondonNew York • Oxford • Paris • San Diego

San Francisco • Singapore • Sydney • Tokyo

Academic Press is an imprint of Elsevier

Academic Press is an imprint of Elsevier30 Corporate Drive, Suite 400, Burlington, MA 01803, USAElsevier, The Boulevard, Langford Lane, Kidlington, Oxford, OX5 1GB, UK

Copyright © 2011 Elsevier Inc. All rights reserved

No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or any information storage and retrieval system, without permission in writing from the publisher. Details on how to seek permission, further information about the Publisher’s permissions policies and our arrangements with organizations such as the Copyright Clearance Center and the Copyright Licensing Agency, can be found at our website: www.elsevier.com/permissions.

This book and the individual contributions contained in it are protected under copyright by the Publisher (other than as may be noted herein).

NoticesKnowledge and best practice in this field are constantly changing. As new research and experience broaden our understanding, changes in research methods, professional practices, or medical treatment may become necessary.

Practitioners and researchers must always rely on their own experience and knowledge in evaluating and using any information, methods, compounds, or experiments described herein. In using such information or methods they should be mindful of their own safety and the safety of others, including parties for whom they have a professional responsibility.

To the fullest extent of the law, neither the Publisher nor the authors, contributors, or editors, assume any liability for any injury and/or damage to persons or property as a matter of products liability, negligence or otherwise, or from any use or operation of any methods, products, instructions, or ideas contained in the material herein.

Library of Congress Cataloging-in-Publication DataDePamphilis, Donald M. Mergers and acquisitions basics: all you need to know/Donald DePamphilis. p. cm. Includes bibliographical references. ISBN 978-0-12-374948-2 1. Consolidation and merger of corporations—United States—Management.

2. Corporate reorganizations—United States—Management. 3. Organizational change— United States—Management. I. Title. HG4028.M4D47 2011

658. 1620973—dc22 2010023983

British Library Cataloguing-in-Publication DataA catalogue record for this book is available from the British Library.

For information on all Academic Press publications visit our website at www.elsevierdirect.com

Printed in The United States of America

10 11 12 13 9 8 7 6 5 4 3 2 1

xiii

Why We Need to UNderstaNd the role of Mergers aNd acqUisitioNs iN today’s World

Mergers, acquisitions, business alliances, and corporate restructuring activi-ties are increasingly commonplace in both developed and emerging econ-omies. Given the frequency with which such activities occur, it is critical for business people and officials at all levels of government to have a basic understanding of why and how they take place and how they can affect economic growth. A lack of understanding of the role mergers and acqui-sitions (M&As) play in a modern economy can mean the failure to use such transactions as an effective means of implementing a business strat-egy. Moreover, ignorance can lead to overregulation of what are important means of disciplining incompetent managers and transferring ownership of operating assets to those who can utilize them most efficiently.

This book seeks to bring clarity to what is a complex, sometimes frus-trating, and ultimately exciting subject. It presents an integrated way to think about the myriad activities involved in mergers and acquisitions. Although various types of business alliances and aspects of corporate restructuring are addressed in brief, the primary focus is on M&As.

The Book’s Unique FeaturesThis book is unique among books of this type in several specific ways. First, it is aimed primarily at practitioners who need a quick overview of the sub-ject without getting bogged down in minutiae. Rather than provide inten-sive coverage of every aspect of mergers and acquisitions, as might be found in a comprehensive textbook, or “dumb down” the subject matter to provide only superficial—and perhaps inaccurate or misleading explanations—the text occupies a middle ground. No significant knowledge of finance, eco-nomics, or accounting is required, although a passing acquaintance with these disciplines is helpful. While reader-friendly, the text also draws on academic studies to substantiate key observations and conclusions that are empirically based. Details of these studies are often found in chapter footnotes.

Each chapter concludes with a section called “A Case in Point” that illustrates the chapter material with a real-world example. These sections include thought-provoking questions that encourage you, the reader, to apply the concepts explored in the chapter.

PreFace

Prefacexiv

Who Should read This BookThis book is aimed at buyers and sellers of businesses, financial analysts, chief executive officers, chief financial officers, operating managers, invest-ment bankers, and portfolio managers. Others who may have an interest include bank lending officers, venture capitalists, government regulators, human resource mangers, entrepreneurs, and board members. In addition, the book may be used as a companion or supplemental text for under-graduate and graduate students in courses on mergers and acquisitions, corporate restructuring, business strategy, management, governance, and entrepreneurship. Supplemented with newspaper and magazine articles, the book could serve as the primary text in an introductory course on mergers and acquisitions.

For a more rigorous and detailed discussion on mergers and acquisitions and other forms of corporate restructuring, the reader may wish to see the author’s textbook on the subject, Mergers, Acquisitions, and Other Restructuring Activities. The 5th edition (2009) is published by Academic Press. The reader also may be interested in the author’s Mergers and Acquisitions Basics: Negotiation and Deal Structuring, also published by Academic Press in 2010.

xv

I would like to express my sincere appreciation for the many resources of Academic Press/Butterworth-Heinemann/Elsevier in general and for the ongoing support provided by Karen Maloney, Managing Editor, and J. Scott Bentley, Executive Editor, as well as Scott M. Cooper, who helped streamline this manuscript for its primary audience. Finally, I would like to thank Alan Cherry, Ross Bengel, Patricia Douglas, Jim Healy, Charles Higgins, Michael Lovelady, John Mellen, Jon Saxon, David Offenberg, Chris Manning, and Maria Quijada for their many constructive comments.

Acknowledgments

�Mergers and Acquisitions Basics� ©�2011�Elsevier�Inc.ISBN:�����0�12��������2�� ��I: �ll ri���s reserve�.����0�12��������2�� ��I: �ll ri���s reserve�.�����I:� �ll�ri���s�reserve�.

CHAPTER

201110.1016/B����0�12��������2.00001��

Introduction to Mergers and Acquisitions

T�e�firs���eca�e�of���e�new�millennium��eral�e��an�era�of��lobal�me�a�mer�ers.� Like� ��e�mer�ers� an�� acquisi�ions� (M&�s)� frenzy� of� ��e� 1��0s�an��1��0s���several�fac�ors�fuele��ac�ivi�y���rou���mi��200�:�rea�ily�avail�able� cre�i���� �is�orically� low� in�eres�� ra�es��� risin�� equi�y� marke�s��� �ec�no�lo�ical� c�an�e��� �lobal� compe�i�ion��� an�� in�us�ry� consoli�a�ion.� In� �erms�of��ollar�volume���M&���ransac�ions�reac�e��a�recor�� level�worl�wi�e� in�200�.�Bu��ex�en�e���urbulence�in���e��lobal�cre�i��marke�s�soon�followe�.

T�e� specula�ive� �ousin�� bubble� in� ��e� Uni�e�� S�a�es� an�� elsew�ere���lar�ely� finance��by��eb����burs���urin�� ��e� secon���alf�of� ��e�year.�Banks���concerne��abou����e�value�of�many�of���eir�own�asse�s���became�excee�in�ly�selec�ive�an��lar�ely�wi���rew�from�financin����e��i��ly�levera�e���ransac��ions���a���a��become�commonplace���e�previous�year.�T�e�quali�y�of�asse�s��el��by�banks���rou��ou��Europe�an���sia�also�became�suspec����reflec�in����e��lobal�na�ure�of���e�cre�i��marke�s.��s�cre�i���rie��up���a�malaise�sprea��worl�wi�e�in���e�marke��for��i��ly�levera�e��M&���ransac�ions.

By�200����a�combina�ion�of�recor���i���oil�prices�an��a�re�uce��avail�abili�y�of�cre�i��sen��mos��of���e�worl�’s�economies�in�o�recession���re�uc�in���lobal�M&��ac�ivi�y�by�more� ��an�one���ir�� from�i�s�previous��i��.�T�is� �lobal� recession� �eepene�� �urin�� ��e� firs�� �alf� of� 200�—�espi�e� a��rama�ic��rop�in�ener�y�prices�an���i��ly�s�imula�ive�mone�ary�an��fiscal�policies—ex�en�in����e�slump�in�M&��ac�ivi�y.

In� recen�� years��� �overnmen�s� worl�wi�e� �ave� in�ervene�� a��ressively�in��lobal�cre�i��marke�s�(as�well�as�in�manufac�urin��an��o��er�sec�ors�of���e� economy)� in� an� effor�� �o� res�ore� business� an�� consumer� confi�ence���res�ore� cre�i��marke�� func�ionin���� an��offse�� �efla�ionary� pressures.�W�a��impac���ave�suc��ac�ions��a��on�mer�ers�an��acquisi�ions?�I��is��oo�early��o��ell���bu����e�implica�ions�may�be�si�nifican�.

M&�s�are�an�impor�an��means�of��ransferrin��resources��o�w�ere���ey�are�mos��nee�e��an��of�removin��un�erperformin��mana�ers.�Governmen���ecisions��o�save�some�firms�w�ile�allowin��o��ers��o�fail�are�likely��o��is�rup����is�process.�Suc���ecisions�are�of�en�base��on���e�no�ion���a��some�

1

Mergers and Acquisitions Basics�

firms� are� simply� �oo� bi�� �o� fail� because� of� ��eir� po�en�ial� impac�� on� ��e�economy—consi�er��IG� in� ��e� Uni�e�� S�a�es.� ���ers� are� clearly� mo�i�va�e��by�poli�ics.�Suc��ac�ions��isrup����e�smoo���func�ionin��of�marke�s���w�ic��rewar�s��oo���ecisions�an��penalizes�poor�ones.��llowin��a�business��o�believe� ��a�� i�� can� ac�ieve� a� size�“�oo�bi�� �o� fail”�may�crea�e�perverse�incen�ives.�Plus�����ere�is�very�li��le��is�orical�evi�ence���a���overnmen�s�are�be��er���an�marke�s�a���eci�in��w�o�s�oul��fail�an��w�o�s�oul��survive.

In� ��is� c�ap�er��� you� will� �ain� an� un�ers�an�in�� of� ��e� un�erlyin���ynamics�of�M&�s�in���e�con�ex��of�an�increasin�ly�in�erconnec�e��worl�.�T�e� c�ap�er� be�ins�wi��� a� �iscussion�of�M&�s� as� c�an�e� a�en�s� in� ��e�con�ex��of�corpora�e�res�ruc�urin�.�T�e�focus�is�on�M&�s�an��w�y���ey��appen��� wi��� brief� consi�era�ion� �iven� �o� al�erna�ive� ways� of� increasin��s�are�ol�er�value.�You�will�also�be�in�ro�uce���o�a�varie�y�of� le�al�s�ruc��ures�an��s�ra�e�ies���a��are�employe���o�res�ruc�ure�corpora�ions.

T�rou��ou����is�book���a�firm���a��a��emp�s��o�acquire�or�mer�e�wi���ano��er�company�is�calle��an�acquiring company���acquirer���or�bidder.�T�e�target company�or�target�is���e�firm�bein��solici�e��by���e�acquirin��com�pany.�Takeovers�or�buyouts�are��eneric��erms�for�a�c�an�e�in���e�con�rol�lin��owners�ip�in�eres��of�a�corpora�ion.

Wor�s� in�bold italics� are� ��e�ones�mos�� impor�an�� for�you� �o�un�er�s�an��fully;���ey�are�all�inclu�e��in�a��lossary�a����e�en��of���e�book.

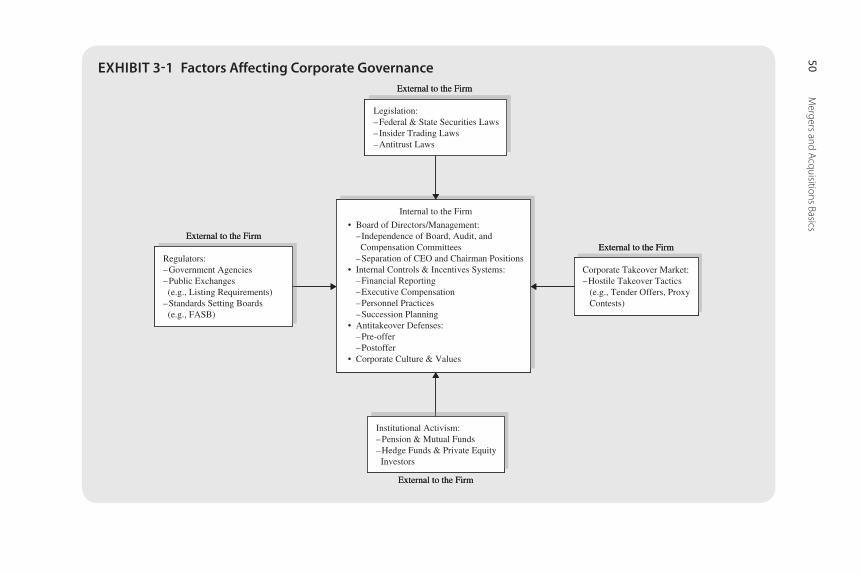

Mergers and acquisitions as change agents

Businesses�come�an���o�in�a�con�inuin��c�urn���per�aps�bes��illus�ra�e��by���e� ever�c�an�in�� composi�ion� of� ��e� so�calle�� For�une� 500—��e� 500�lar�es��U.S.�corpora�ions.��nly��0�of���e�firms�on���e�ori�inal�1�55�lis��of�500�are�on��o�ay’s�lis����an��some�2��000�firms��ave�appeare��on���e�lis��a��one��ime�or�ano��er.�Mos���ave��roppe��off���e�lis��ei��er���rou���mer�er���acquisi�ion��� bankrup�cy��� �ownsizin���� or� some� o��er� form� of� corpora�e�res�ruc�urin�.�Consi�er� a� few�examples:�C�rysler���Be��le�em�S�eel���Sco���Paper���Zeni�����Rubbermai����Warner�Lamber�.�T�e�popular�me�ia��en�s��o�use� ��e� �erm� corporate restructuring� �o� �escribe� ac�ions� �aken� �o� expan��or�con�rac��a� firm’s�basic�opera�ions�or� fun�amen�ally�c�an�e� i�s� asse��or�financial�s�ruc�ure.1

1� T�e�broa��array�of�ac�ivi�ies�fallin��un�er���is�ca�c�all��erm�runs���e��amu��from�reor�anizin��business�uni�s��o��akeovers�an��join��ven�ures��o��ives�i�ures�an��spin�offs�an��equi�y�carve�ou�s.�����e�aile���iscussion�of���ese�al�erna�ive�forms�of�res�ruc�urin��is�beyon����e�scope�of���is�book.��To�learn�more���see�Mergers, Acquisitions, and other Restructuring Activities�by��onal��M.��ePamp�ilis���now�in�i�s�fif���e�i�ion�an��available���rou����ca�emic�Press.

Introduction to Mergers and Acquisitions �

Why Mergers and acquisitions happen

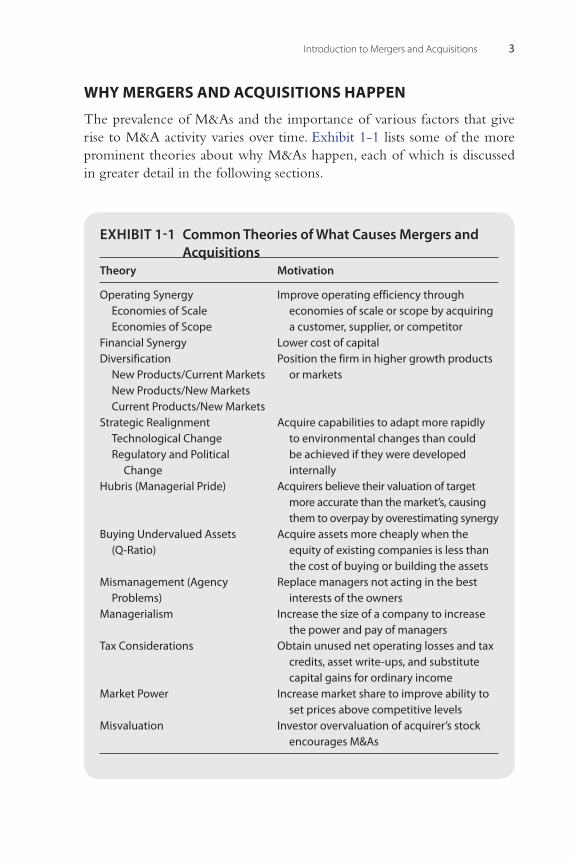

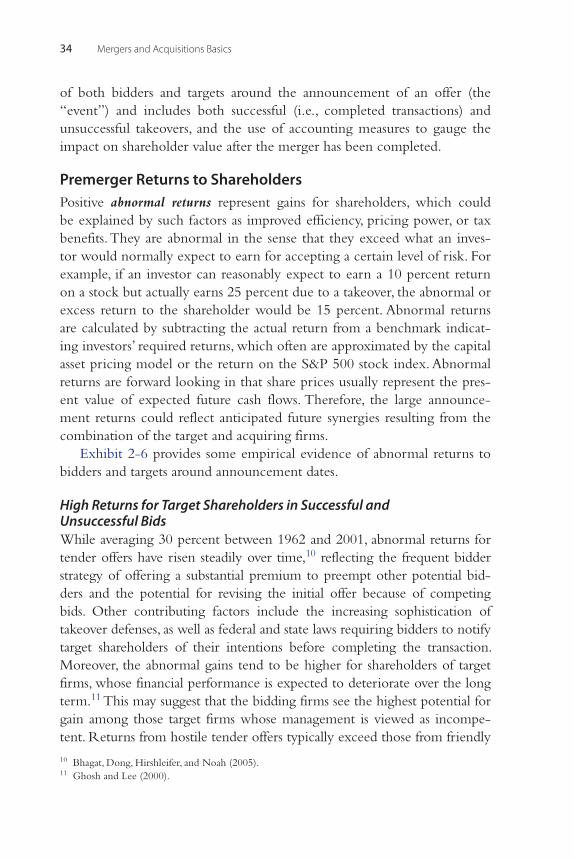

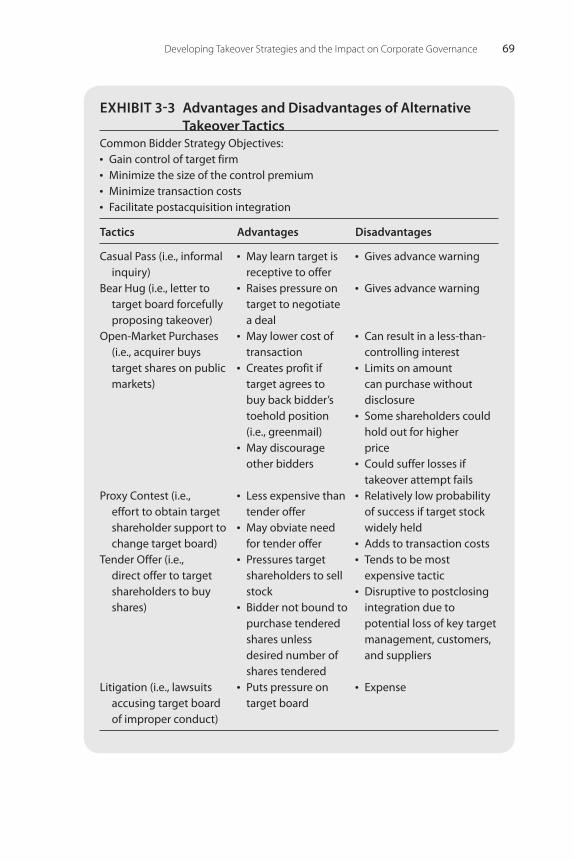

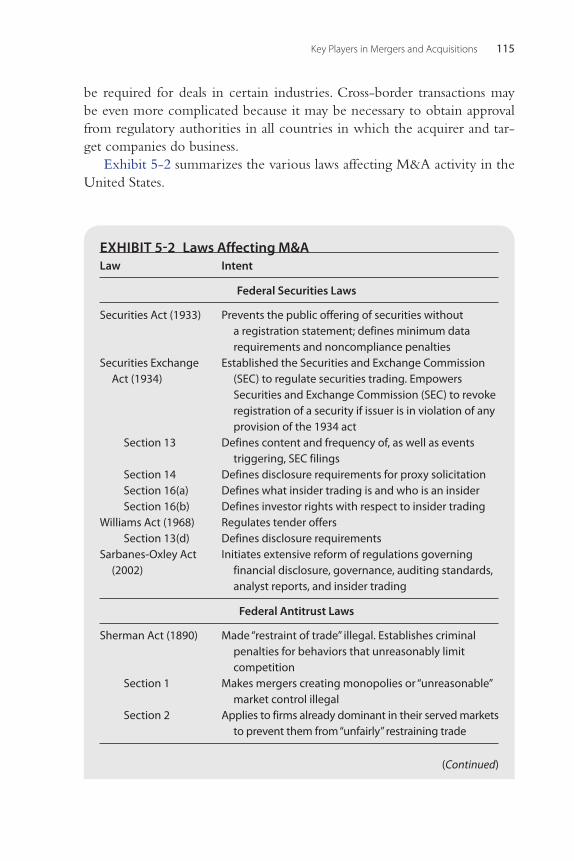

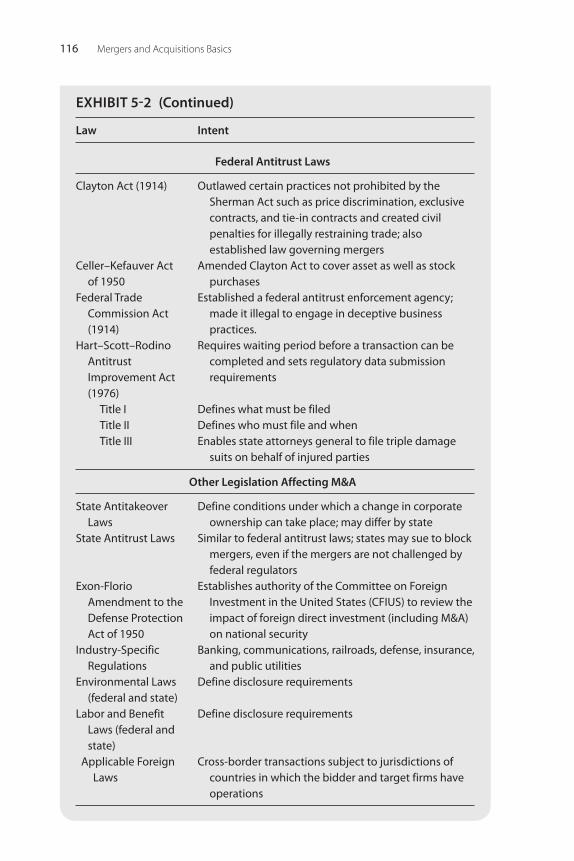

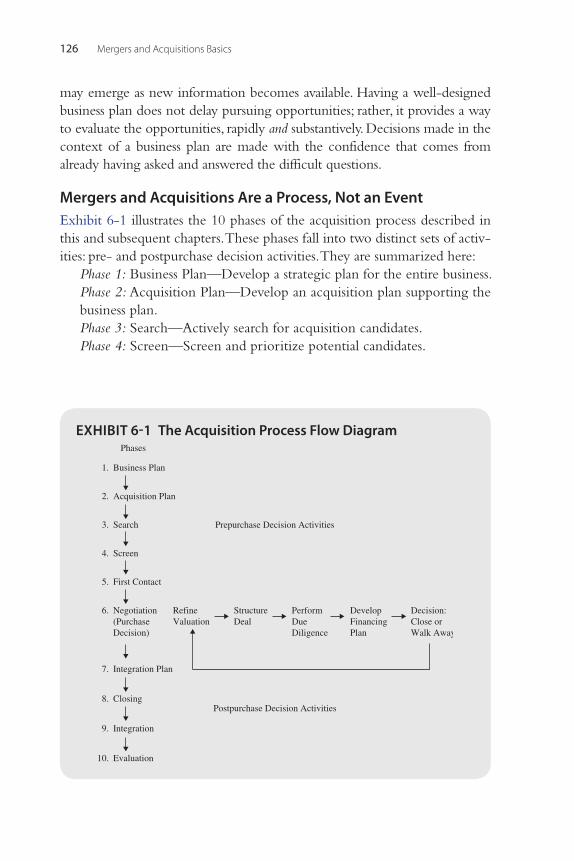

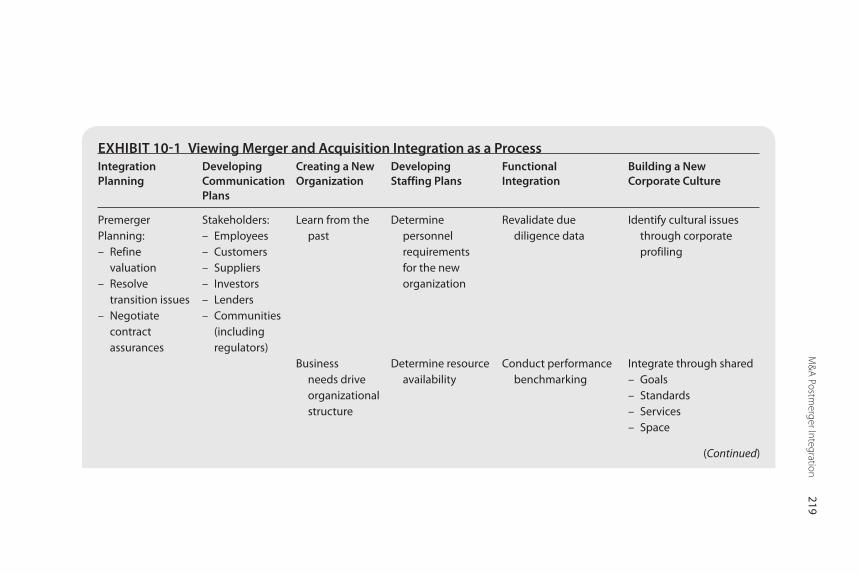

T�e�prevalence�of�M&�s�an����e�impor�ance�of�various�fac�ors���a���ive�rise��o�M&��ac�ivi�y�varies�over��ime.�Ex�ibi��1�1�lis�s�some�of���e�more�prominen����eories�abou��w�y�M&�s��appen���eac��of�w�ic��is��iscusse��in��rea�er��e�ail�in���e�followin��sec�ions.

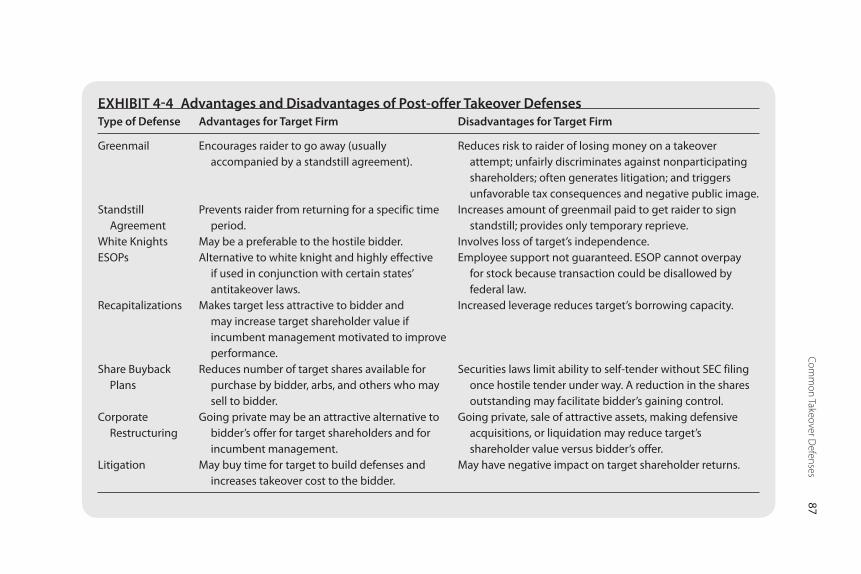

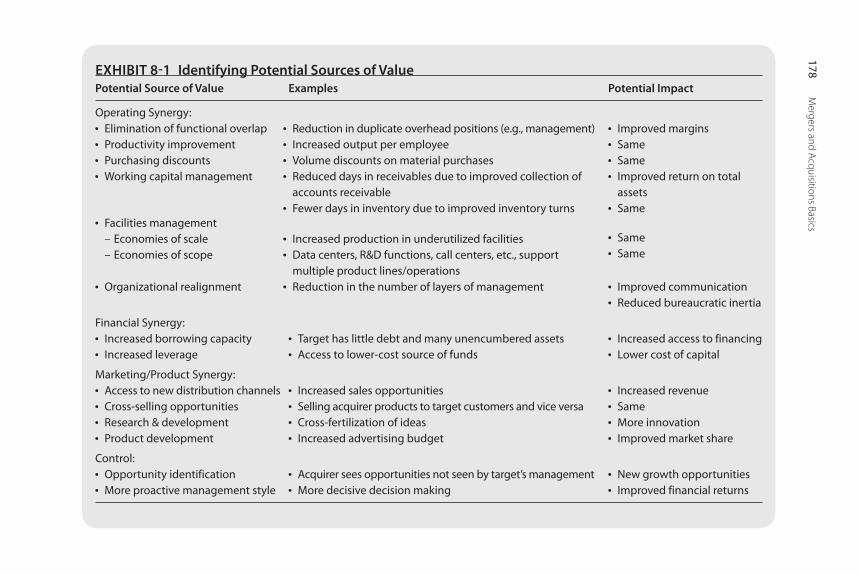

EXHIBIT 1-1 Common Theories of What Causes Mergers and Acquisitions

Theory Motivation

Operating SynergyEconomies of ScaleEconomies of Scope

Improve operating efficiency through economies of scale or scope by acquiring a customer, supplier, or competitor

Financial Synergy Lower cost of capitalDiversification

New Products/Current MarketsNew Products/New MarketsCurrent Products/New Markets

Position the firm in higher growth products or markets

Strategic RealignmentTechnological ChangeRegulatory and Political

Change

Acquire capabilities to adapt more rapidly to environmental changes than could be achieved if they were developed internally

Hubris (Managerial Pride) Acquirers believe their valuation of target more accurate than the market’s, causing them to overpay by overestimating synergy

Buying Undervalued Assets (Q-Ratio)

Acquire assets more cheaply when the equity of existing companies is less than the cost of buying or building the assets

Mismanagement (Agency Problems)

Replace managers not acting in the best interests of the owners

Managerialism Increase the size of a company to increase the power and pay of managers

Tax Considerations Obtain unused net operating losses and tax credits, asset write-ups, and substitute capital gains for ordinary income

Market Power Increase market share to improve ability to set prices above competitive levels

Misvaluation Investor overvaluation of acquirer’s stock encourages M&As

Mergers and Acquisitions Basics�

SynergySynergy�is���e�ra��er�simplis�ic�no�ion���a���wo�(or�more)�businesses�in�com�bina�ion�will�crea�e��rea�er�s�are�ol�er�value���an�if���ey�are�opera�e��sepa�ra�ely.�I��may�be�measure��as���e�incremen�al�cas��flow���a��can�be�realize����rou���combina�ion�in�excess�of�w�a��woul��be�realize��were���e�firms��o�remain�separa�e.�T�ere�are��wo�basic��ypes�of�syner�y:�opera�in��an��financial.

Operating Synergy (Economies of Scale and Scope)Operating synergy� comprises�bo��� economies�of� scale� an��economies�of�scope��� w�ic�� can� be� impor�an�� �e�erminan�s� of� s�are�ol�er� weal��� cre�a�ion.2�Gains�in�efficiency�can�come�from�ei��er�fac�or�an��from�improve��mana�erial�prac�ices.

Sprea�in��fixe��cos�s�over�increasin��pro�uc�ion�levels�realizes�economies of scale���wi��� scale��efine��by� suc�� fixe�� cos�s� as� �eprecia�ion�of� equip�men��an��amor�iza�ion�of�capi�alize��sof�ware;�normal�main�enance�spen��in�;� obli�a�ions� suc�� as� in�eres�� expense��� lease� paymen�s��� an�� lon���erm�union���cus�omer���an��ven�or�con�rac�s;�an�� �axes.�T�ese�cos�s�are� fixed� in���a����ey�canno��be�al�ere��in���e�s�or��run.�By�con�ras����variable�cos�s�are���ose� ��a�� c�an�e�wi��� ou�pu�� levels.�Consequen�ly��� for� a� �iven� scale� or�amoun��of� fixe�� expenses��� ��e��ollar� value�of� fixe�� expenses�per�uni��of�ou�pu��an��per��ollar�of�revenue��ecreases�as�ou�pu��an��sales�increase.

To�illus�ra�e���e�po�en�ial�profi��improvemen��from�economies�of�scale���le�’s� consi�er� an� au�omobile� plan�� ��a�� can� assemble� 10� cars� per� �our�an�� runs� aroun�� ��e� clock—w�ic�� means� ��e� plan�� pro�uces� 2�0� cars�per��ay.�T�e�plan�’s� fixe��expenses�per��ay�are�$1�million��� so� ��e�avera�e�fixe��cos��per�car�pro�uce��is�$���16��(i.e.���$1��000��000/2�0).�Now�ima�ine�an� improve�� assembly� line� ��a�� allows� ��e� plan�� �o� assemble� 20� cars� per��our���or���0�per��ay.�T�e�avera�e�fixe��cos��per�car�per��ay�falls��o�$2��0���(i.e.��� $1��000��000/��0).� If� variable� cos�s� (e.�.��� �irec�� labor)�per� car��o�no��increase��� an�� ��e� sellin��price�per�car� remains� ��e� same� for�eac��car��� ��e�profi�� improvemen��per�car��ue� �o� ��e��ecline� in�avera�e� fixe��cos�s�per�car�per��ay�is�$2��0���(i.e.���$���16��–�$2��0��).

�� firm�wi��� �i��� fixe�� cos�s� as� a� percen�a�e� of� �o�al� cos�s� will� �ave��rea�er� earnin�s� variabili�y� ��an�one�wi��� a� lower� ra�io�of� fixe�� �o� �o�al�cos�s.�Le�’s�consi�er��wo�firms�wi���annual�revenues�of�$1�billion�an��oper�a�in��profi�s�of�$50�million.�T�e�fixe��cos�s�a����e�firs��firm�represen��100�percen��of��o�al�cos�s���bu��a����e�secon��fixe��cos�s�are�only��alf�of�all�cos�s.�If�revenues�a��bo���firms�increase��by�$50�million�����e�firs��firm�woul��see�

2� �eLon��(200�);�Hous�on���James���an��Ryn�aer��(2001).

Introduction to Mergers and Acquisitions �

income�increase��o�$100�million���precisely�because�all�of�i�s�cos�s�are�fixe�.�Income�a����e�secon��firm�woul��rise�only��o�$�5�million���because��alf�of���e�$50�million�increase��revenue�woul���ave��o��o��o�pay�for�increase��variable�cos�s.

Usin��a�specific�se��of�skills�or�an�asse��curren�ly�employe���o�pro�uce�a� �iven� pro�uc�� or� service� �o� pro�uce� some��in�� else� realizes� economies of scope���w�ic��are�foun��mos��of�en�w�en�i��is�c�eaper��o�combine�mul��iple� pro�uc�� lines� in� one� firm� ��an� �o� pro�uce� ��em� in� separa�e� firms.�Proc�er�&�Gamble��� ��e�consumer�pro�uc�s��ian����uses� i�s��i��ly� re�ar�e��consumer�marke�in�� skills� �o� sell� a� full� ran�e� of� personal� care� as�well� as�p�armaceu�ical�pro�uc�s.�Hon�a�knows��ow��o�en�ance�in�ernal�combus��ion� en�ines��� so� in� a��i�ion� �o� cars��� ��e� firm��evelops�mo�orcycles��� lawn�mowers���an��snow�blowers.�Sequen��Tec�nolo�y�le�s�cus�omers�run�appli�ca�ions� on� UNIX� an�� NT� opera�in�� sys�ems� on� a� sin�le� compu�er� sys��em.�Ci�i�roup�uses���e�same�compu�er�cen�er��o�process�loan�applica�ions����eposi�s����rus��services���an��mu�ual�fun��accoun�s�for�i�s�bank’s�cus�omers.�Eac��is�an�example�of�economies�of�scope���w�ere�a�firm�is�applyin��a�spe�cific�se��of�skills�or�asse�s��o�pro�uce�or�sell�mul�iple�pro�uc�s�����us��enera��in��more�revenue.

Financial Synergy (Lowering the Cost of Capital)Financial synergy�refers��o���e�impac��of�mer�ers�an��acquisi�ions�on���e�cos��of�capi�al�of���e�acquirin��firm�or�newly�forme��firm�resul�in��from�a�mer�er�or�acquisi�ion.�T�e�cos��of�capi�al�is���e�minimum�re�urn�require��by�inves�ors�an��len�ers��o�in�uce���em��o�buy�a�firm’s�s�ock�or��o�len���o���e�firm.

In� ��eory��� ��e� cos�� of� capi�al� coul�� be� re�uce�� if� ��e� mer�e�� firms��ave�cas��flows���a���o�no��move�up�an���own�in��an�em�(i.e.���so�calle���co�insurance)��� realize� financial� economies� of� scale� from� lower� securi�ies�issuance�an���ransac�ions�cos�s���or�resul��in�a�be��er�ma�c�in��of�inves�men��oppor�uni�ies�wi���in�ernally��enera�e��fun�s.�Combinin��a�firm���a���as�excess�cas��flows�wi���one�w�ose�in�ernally��enera�e��cas��flow�is�insuf�ficien���o�fun��i�s�inves�men��oppor�uni�ies�may�also�resul��in�a�lower�cos��of�borrowin�.��� firm� in�a�ma�ure� in�us�ry�experiencin�� slowin���row���may�pro�uce�cas��flows�well�in�excess�of�available�inves�men��oppor�uni��ies.��no��er�firm�in�a��i����row���in�us�ry�may�no���ave�enou���cas���o�realize�i�s�inves�men��oppor�uni�ies.�Reflec�in����eir��ifferen���row���ra�es�an��risk�levels�����e�firm�in���e�ma�ure�in�us�ry�may��ave�a�lower�cos��of�capi�al���an���e�one�in���e��i����row���in�us�ry���an��combinin����e��wo�firms�coul��lower���e�avera�e�cos��of�capi�al�of���e�combine��firms.

Mergers and Acquisitions Basics�

DiversificationBuyin��firms�ou�si�e�a�company’s�curren��primary�lines�of�business�is�calle��diversification���an��is��ypically�jus�ifie��in�one�of��wo�ways.��iversifica�ion�may� crea�e� financial� syner�y� ��a�� re�uces� ��e� cos�� of� capi�al��� or� i�� may�allow�a�firm��o�s�if�� i�s�core�pro�uc�� lines�or�marke�s� in�o�ones���a���ave��i��er��row���prospec�s���even�ones���a��are�unrela�e���o���e�firm’s�curren��pro�uc�s�or�marke�s.�T�e�ex�en���o�w�ic���iversifica�ion�is�unrela�e���o�an�acquirer’s�curren��lines�of�business�can��ave�si�nifican��implica�ions�for��ow�effec�ive�mana�emen��is�in�opera�in����e�combine��firms.

Ex�ibi��1�2� is�a�pro�uc�–marke��ma�rix� ��a�� i�en�ifies�a� firm’s�primary��iversifica�ion�op�ions.��� firm� facin�� slower��row��� in� i�s� curren��marke�s�may�be�able��o�accelera�e��row�����rou���rela�e���iversifica�ion�by�sellin��i�s�curren��pro�uc�s� in�new�marke�s� ��a��are�somew�a��unfamiliar�an���� ��ere�fore���more�risky.�Suc��was� ��e�case�w�en�p�armaceu�ical��ian�� Jo�nson�&�Jo�nson�announce��i�s�ul�ima�ely�unsuccessful��akeover�a��emp��of�Gui�an��Corpora�ion� in� la�e� 200�.� J&J� was� seekin�� an� en�ry� poin�� for� i�s� me�ical��evices�business�in���e�fas���rowin��marke��for�implan�able��evices���in�w�ic��i�� �i��no�� ��en�par�icipa�e.��� firm�may� a��emp�� �o� ac�ieve��i��er� �row���ra�es� by� �evelopin��or� acquirin�� new�pro�uc�s�wi���w�ic�� i�� is� rela�ively�unfamiliar�an����en�sellin����em�in�familiar�an��less�risky�curren��marke�s.�Re�ailer�JCPenney’s�acquisi�ion�of���e�Ecker���ru�s�ore�c�ain�or�J&J’s�$16�billion�acquisi�ion�of�Pfizer’s�consumer��eal��care�pro�uc�s�line�in�2006�are��wo�examples�of� rela�e���iversifica�ion.� In�eac�� ins�ance��� ��e� firm�assume��a��i�ional�risk���bu��less�so���an�unrela�e���iversifica�ion�if�i���a���evelope��new�pro�uc�s� for� sale� in�new�marke�s.�T�ere� is�consi�erable�evi�ence� ��a��inves�ors��o�no��benefi��from�unrela�e���iversifica�ion.

Firms���a��opera�e�in�a�number�of�lar�ely�unrela�e��in�us�ries���suc��as�General�Elec�ric���are�calle��conglomerates.�T�e�s�are�prices�of�con�lomera�es��

EXHIBIT 1-2 Product–Market MatrixMarkets

ProductsCurrent New

Current Lower Growth/Lower Risk Higher Growth/Higher Risk (Related Diversification)

New Higher Growth/Higher Risk (Related Diversification)

Highest Growth/Highest Risk (Unrelated Diversification)

Introduction to Mergers and Acquisitions �

of�en� �ra�e� a�� a� �iscoun�—as� muc�� as� 10� �o� 15� percen��—compare�� �o�s�ares� of� focuse�� firms�or� �o� ��eir� value�were� ��ey� broken�up.�T�is� �is�coun��is�calle����e�conglomerate discount�or�diversification discount.�Inves�ors�of�en�perceive�companies��iversifie�� in�unrela�e��areas� (i.e.��� ��ose� in��if�feren�� s�an�ar�� in�us�rial� classifica�ions)� as� riskier� because� mana�emen���as� �ifficul�y� un�ers�an�in�� ��ese� companies� an�� of�en� fails� �o� provi�e�full� fun�in�� for� ��e�mos�� a��rac�ive� inves�men��oppor�uni�ies.��Moreover���ou�si�e� inves�ors� may� �ave� a� �ifficul�� �ime� un�ers�an�in�� �ow� �o� value���e� various� par�s� of� �i��ly� �iversifie�� businesses.5� Researc�ers� �iffer� on�w�e��er���e�con�lomera�e��iscoun��is�overs�a�e�.6

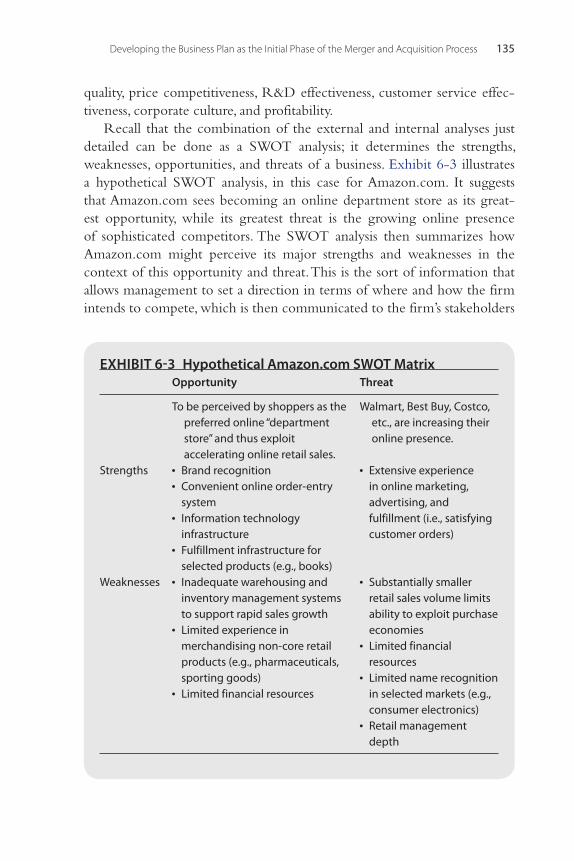

S�ill���al��ou�����e�evi�ence�su��es�s���a��firms�pursuin��a�more�focuse��corpora�e�s�ra�e�y�are�likely��o�perform�bes������ere�are�always�excep�ions.

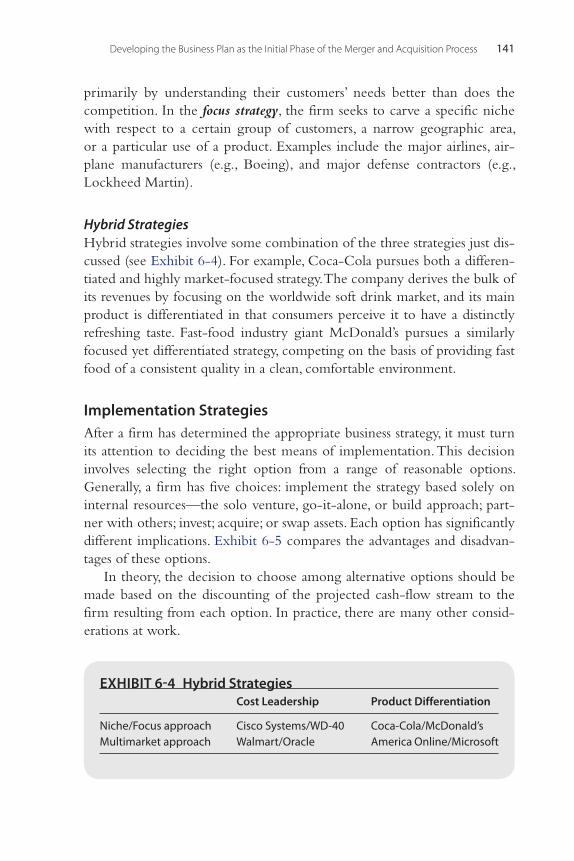

Strategic RealignmentT�e�strategic realignment���eory�su��es�s���a��firms�use�M&�s��o�make�rapi��a�jus�men�s��o�c�an�es�in���eir�ex�ernal�environmen�s.��l��ou���c�an�e�can�come�from�many��ifferen��sources�����is���eory�consi�ers�only�c�an�es�in���e�re�ula�ory�environmen��an���ec�nolo�ical�innova�ion—�wo�fac�ors���a����over���e�pas��20�years����ave�been�major�forces�in�crea�in��new�oppor�uni�ies�for��row�����an����rea�enin����or�makin��obsole�e���firms’�primary�lines�of�business.

Regulatory ChangeT�ose�in�us�ries���a���ave�been�subjec���o�si�nifican���ere�ula�ion�in�recen��years—financial� services��� �eal��� care��� u�ili�ies��� me�ia��� �elecommunica�ions���

�� Ber�er�an���fek�(1��5);�Lins�an��Servaes�(1���).�� Morck���S�leifer���an��Vis�ny�(1���).5� Bes��an��Ho��es�(200�).6� Some�ar�ue���a���iversifyin��firms�are�of�en�poor�performers�before���ey�become�con�lomera�es�

(Campa�an��Simi���2002;�Hylan����2001)���w�ereas�o��ers�conclu�e���a����e�con�lomera�e��iscoun��is�a�resul��of��ow���e�sample�s�u�ie��is�cons�ruc�e��(Gra�am���Lemmon���an��Wolf���2002;�Villalon�a���200�).�Several�su��es����a����e�con�lomera�e��iscoun��is�re�uce��w�en�firms�ei��er��ives��or�spin�off�businesses�in�an�effor���o�ac�ieve��rea�er�focus�on���e�core�business�por�folio�(�i��mar�an��S�iv�asani���200�;�S�in�an��S�ulz���1���).�S�ill�o��ers�fin��evi�ence���a����e�mos��successful�mer�ers�are���ose���a��focus�on��eals���a��promo�e���e�acquirer’s�core�business�(Har�in��an��Rovi����200�;�Me��inson�e��al.���200�).�Rela�e��acquisi�ions�may�even�be�more�likely��o�experience��i��er�financial�re�urns���an�unrela�e��acquisi�ions�(Sin���an��Mon��omery���200�).�T�is�s�oul��no��be�surprisin��in���a��rela�e��firms�are�more�likely��o�be�able��o�realize�cos��savin�s��ue��o�overlappin��func�ions�an��pro�uc��lines���an�are�unrela�e��firms.�T�ere�is�even�an�ar�umen����a���iversifie��firms�in��evelopin��coun�ries���w�ere�access��o�capi�al�marke�s�is�limi�e����may�sell�a��a�premium��o�more�focuse��firms�(Fauver���Hous�on���an��Narran�o���200�).�Un�er���ese�circums�ances���corpora�e��iversifica�ion�may�enable�more�efficien��inves�men��because��iversifie��firms�may�use�cas���enera�e��by�ma�ure�subsi�iaries��o�fun����ose�wi����i��er��row���po�en�ial.

Mergers and Acquisitions Basics�

�efense—�ave�been�a�� ��e�cen�er�of�M&��ac�ivi�y��because��ere�ula�ion�breaks��own�ar�ificial�barriers�an��s�imula�es�compe�i�ion.��urin����e�firs���alf� of� ��e� 1��0s��� for� ins�ance��� ��e� U.S.� �epar�men�� of� �efense� ac�ively�encoura�e�� consoli�a�ion� of� ��e� na�ion’s� major� �efense� con�rac�ors� �o�improve���eir�overall�opera�in��efficiency.

U�ili�ies�now�require��in�some�s�a�es��o�sell�power��o�compe�i�ors���a��can�resell���e�power�in���e�u�ili�y’s�own�marke�place�respon��wi���M&�s��o�ac�ieve��rea�er�opera�in��efficiency.�Commercial�banks���a���ave�move��beyon�� ��eir� �is�orical� role� of� accep�in�� �eposi�s� an�� �ran�in�� loans� are�mer�in�� wi��� securi�ies� firms� an�� insurance� companies� ��anks� �o� ��e�Financial�Services�Mo�erniza�ion��c��of�1������w�ic��repeale�� le�isla�ion��a�in��back��o���e�Grea���epression.�T�e�Ci�icorp–Travelers�mer�er�a�year�earlier�an�icipa�e����is�c�an�e���an��i�� is�probable���a����eir�represen�a�ives�were�lobbyin��for���e�new�le�isla�ion.�T�e�final�c�ap�er��as�ye���o�be�wri���en:� ��is� �ren�� �owar���u�e� financial� services� companies�may�ye�� be� s�y�mie��by�new�re�ula�ion�passe��in�2010�in�response��o�excessive�risk��akin�.

T�e��elecommunica�ions�in�us�ry�offers�a�s�rikin��illus�ra�ion.�His�orically���local� an�� lon���is�ance� p�one� companies� were� no�� allowe�� �o� compe�e�a�ains��eac��o��er���an��cable�companies�were�essen�ially�monopolies.�Since���e�Telecommunica�ions��c��of�1��6���local�an��lon���is�ance�companies�are�ac�ively�encoura�e���o�compe�e�in�eac��o��er’s�marke�s���an��cable�companies�are�offerin��bo���In�erne��access�an��local��elep�one�service.�W�en�a�fe�eral�appeals�cour��in�2002�s�ruck��own�a�Fe�eral�Communica�ions�Commission�re�ula�ion�pro�ibi�in��a�company�from�ownin��a�cable��elevision�sys�em�an��a�broa�cas��TV�s�a�ion�in���e�same�ci�y���an����rew�ou����e�rule���a��barre��a�company�from�ownin��TV�s�a�ions���a��reac��more���an��5�percen��of�U.S.��ouse�ol�s���i��encoura�e��new�combina�ions�amon����e�lar�es��me�ia�com�panies�or�purc�ases�of�smaller�broa�cas�ers.

Technological ChangeTec�nolo�ical�a�vances�crea�e�new�pro�uc�s�an�� in�us�ries.�T�e��evelop�men�� of� ��e� airplane� crea�e�� ��e� passen�er� airline��� avionics��� an�� sa�elli�e�in�us�ries.�T�e�emer�ence�of�sa�elli�e��elivery�of�cable�ne�works��o�re�ional�an��local�s�a�ions�i�ni�e��explosive��row���in���e�cable�in�us�ry.�To�ay���wi�����e�expansion�of�broa�ban���ec�nolo�y���we�are�wi�nessin����e�conver�ence�of�voice����a�a���an��vi�eo��ec�nolo�ies�on���e�In�erne�.�T�e�emer�ence�of��i�i�al�camera��ec�nolo�y��as�re�uce���rama�ically���e��eman��for�analo��

�� Mi�c�ell�an��Mul�erin�(1��6);�Mul�erin�an��Boone�(2000).

Introduction to Mergers and Acquisitions �

cameras� an�� film�an�� sen���ouse�ol��names� suc�� as�Ko�ak� an��Polaroi��scramblin���o�a�ap�.�T�e��row���of�sa�elli�e�ra�io�is�increasin��i�s�s�are�of���e�ra�io�a�ver�isin��marke��a����e�expense�of��ra�i�ional�ra�io�s�a�ions.

Smaller���more�nimble�players�ex�ibi��spee��an��crea�ivi�y�many�lar�er���more�bureaucra�ic�firms�canno��ac�ieve.�Wi���en�ineerin���alen��of�en�in�s�or��supply�an��pro�uc��life�cycles�s�or�enin������ese�lar�er�firms�may�no���ave� ��e� luxury�of� �ime�or� ��e� resources� �o� innova�e.�So��� ��ey�may� look��o�M&�s�as�a�fas��an��some�imes�less�expensive�way��o�acquire�new��ec��nolo�ies� an��proprie�ary�know��ow��o� fill� �aps� in� ��eir� curren��pro�uc��por�folios�or��o�en�er�en�irely�new�businesses.��cquirin���ec�nolo�ies�can�also� be� a� �efensive� weapon� �o� keep� impor�an�� new� �ec�nolo�ies� ou�� of���e��an�s�of�compe�i�ors.�In�2006���eBay�acquire��Skype�Tec�nolo�ies�����e�In�erne��p�one�provi�er��� for�$�.1�billion� in�cas���� s�ock���an��performance�paymen�s����opin����a����e�move�woul��boos���ra�in��on�i�s�online�auc�ion�si�e� an�� limi�� compe�i�ors’� access� �o� ��e� new� �ec�nolo�y.� By� Sep�ember�200����eBay��a���o�a�mi����a��i���a��been�unable��o�realize���e�benefi�s�of�ownin��Skype�an��was�sellin����e�business��o�a�priva�e�inves�or��roup�for�$2.�5�billion.

Hubris and the “Winner’s Curse”Mana�ers� some�imes�believe� ��a�� ��eir� own�valua�ion�of� a� �ar�e�� firm� is�superior��o���e�marke�’s�valua�ion.�T�us��� ��e�acquirin��company��en�s��o�overpay� for� ��e� �ar�e���� �avin�� been�overop�imis�ic�w�en� evalua�in�� syn�er�ies.�Compe�i�ion� amon��bi��ers� also� is� likely� �o� resul�� in� ��e�winner�overpayin��because�of�hubris���even�if�si�nifican��syner�ies�are�presen�.��In�an�auc�ion�environmen��wi���bi��ers�����e�ran�e�of�bi�s�for�a��ar�e��com�pany�is� likely��o�be�qui�e�wi�e���because�senior�mana�ers� �en���o�be�very�compe�i�ive� an�� some�imes� self�impor�an�.�T�eir� �esire� no�� �o� lose� can��rive���e�purc�ase�price�of�an�acquisi�ion�well�in�excess�of�i�s�ac�ual�eco�nomic�value�(i.e.���cas���enera�in��capabili�y).�T�e�winner�pays�more���an���e� company� is� wor��� an�� may� ul�ima�ely� feel� remorse� a�� �avin�� �one�so—�ence�w�a���as�come��o�be�calle����e�winner’s curse.

Buying Undervalued Assets (The Q-Ratio)T�e�q-ratio�is���e�ra�io�of���e�marke��value�of���e�acquirin��firm’s�s�ock��o���e�replacemen��cos��of�i�s�asse�s.�Firms�in�eres�e��in�expansion�can�c�oose��o�inves��in�new�plan�s�an��equipmen��or�ob�ain���e�asse�s�by�acquirin��a�

�� Roll�(1��6).

Mergers and Acquisitions Basics�0

company�wi���a�marke��value�less���an�w�a��i��woul��cos���o�replace���e�asse�s� (i.e.���q�ra�io��1).�T�is� ��eory�was�very�useful� in�explainin��M&��ac�ivi�y��urin����e�1��0s���w�en��i���infla�ion�an��in�eres��ra�es��epresse��s�ock�prices�well�below���e�book�value�of�many�firms.�Hi���infla�ion�also�cause�� ��e� replacemen�� cos�� of� asse�s� �o� be�muc���i��er� ��an� ��e� book�value�of� asse�s.�Book�value� refers� �o� ��e�value�of� asse�s� lis�e��on� a� firm’s�balance� s�ee�� an�� �enerally� reflec�s� ��e� �is�orical� cos�� of� acquirin�� suc��asse�s�ra��er���an���eir�curren��cos�.

W�en� �asoline� refiner�Valero� Ener�y� Corp.� acquire�� Premcor� Inc.�in� 2005��� ��e� $�� billion� �ransac�ion� crea�e�� ��e� lar�es�� refiner� in� Nor����merica.� I��woul���ave�cos�� an�es�ima�e���0�percen��more� for�Valero� �o�buil��a�new�refinery�wi���equivalen��capaci�y.�

Mismanagement (Agency Problems)Agency problems� arise� w�en� ��ere� is� a� �ifference� be�ween� ��e� in�eres�s�of�incumben��mana�ers�(i.e.�����ose�curren�ly�mana�in����e�firm)�an����e�firm’s�s�are�ol�ers.�T�is��appens�w�en�mana�emen��owns�a�small�frac�ion�of���e�ou�s�an�in��s�ares�of���e�firm.�T�ese�mana�ers���w�o�serve�as�a�en�s�of���e�s�are�ol�er���may�be�more�incline���o�focus�on���eir�own�job�secu�ri�y�an��lavis��lifes�yles���an�on�maximizin��s�are�ol�er�value.�W�en���e�s�ares�of�a�company�are�wi�ely��el������e�cos��of�suc��mismana�emen��is�sprea��across�a�lar�e�number�of�s�are�ol�ers���eac��of�w�om�bears�only�a�small�por�ion.�T�is�allows�for��olera�ion�of���e�mismana�emen��over�lon��perio�s.�Mer�ers�of�en��ake�place��o�correc��si�ua�ions�in�w�ic����ere�is�a�separa�ion�be�ween�w�a��mana�ers�an��owners� (s�are�ol�ers)�wan�.�Low�s�ock� prices� pu�� pressure� on� mana�ers� �o� �ake� ac�ions� �o� raise� ��e� s�are�price� or� become� ��e� �ar�e�� of� acquirers��� w�o� perceive� ��e� s�ock� �o� be�un�ervalue�10�an��w�o�are�usually�in�en��on�removin����e�un�erperform�in��mana�emen��of���e��ar�e��firm.

��ency� problems� also� con�ribu�e� �o� mana�emen��ini�ia�e�� buyou�s���par�icularly� w�en� mana�ers� an�� s�are�ol�ers� �isa�ree� over� �ow� excess�cas��flow�s�oul��be�use�.11�Mana�ers�may��ave�access��o�informa�ion�no��rea�ily� available� �o� s�are�ol�ers� an�� may� ��erefore� be� able� �o� convince�len�ers��o�provi�e�fun�s��o�buy�ou��s�are�ol�ers�an��concen�ra�e�owner�s�ip�in���e��an�s�of�mana�emen�.

����� Zellner�(2005).10� Fama�an��Jensen�(1���).11� Me�ran�an��Peris�iani�(2006).

Introduction to Mergers and Acquisitions ��

ManagerialismT�e� managerialism theory� for� acquisi�ions� asser�s� ��a�� mana�ers� make�acquisi�ions�for�selfis��reasons���w�e��er��o�a����o���eir�pres�i�e���buil����eir�sp�eres�of�influence���au�men����eir�compensa�ion���or�for�self�preserva�ion.12��Bu�� ascribin�� acquisi�ion� �o� ��e� mana�erialism� mo�ive� i�nores� ��e� pres�sure�mana�ers�of�lar�er�firms�are�un�er��o�sus�ain�earnin�s��row����o�sup�por����eir�firms’�s�are�price.��s���e�marke��value�of�a�firm�increases���senior�mana�ers� are� compelle�� �o� make� ever� lar�er� inves�men�� be�s� �o� sus�ain�increases�in�s�are�ol�er�value.�Small�acquisi�ions�simply��o�no���ave�suffi�cien��impac��on�earnin�s��row����o�jus�ify���e�effor��require���o�comple�e���em.� Consequen�ly��� even� ��ou��� ��e� resul�in�� acquisi�ions� may� �es�roy�value��� ��e�mo�ive� for�makin�� ��em�may�be�more� �o� suppor�� s�are�ol�er�in�eres�s���an��o�preserve�mana�emen��au�onomy.

Tax ConsiderationsTax�benefi�s���suc��as�loss�carry�forwar�s�an��inves�men���ax�cre�i�s���can�be�use�� �o�offse�� ��e� �axable� income�of� firms� ��a��combine� ��rou���M&�s.��cquirers�of�firms�wi���accumula�e��losses�may�use���em��o�offse��fu�ure�profi�s��enera�e��by���e�combine��firms.�Unuse���ax�cre�i�s��el��by��ar�e��firms�may�also�be�use���o�lower�fu�ure��ax�liabili�ies.����i�ional��ax�s�el��er�(i.e.����ax�savin�s)�is�crea�e���ue��o���e�purc�ase�me��o��of�accoun�in����w�ic�� requires� ��e� book� value� of� ��e� acquire�� asse�s� �o� be� revalue�� �o���eir� curren�� marke�� value� for� purposes� of� recor�in�� ��e� acquisi�ion� on���e�books�of���e�acquirin��firm.�T�e�resul�in���eprecia�ion�of���ese��ener�ally��i��er�asse��values�also�re�uces���e�amoun��of�fu�ure��axable�income��enera�e��by���e�combine��companies�as��eprecia�ion�expense�is��e�uc�e��from�revenue�in�calcula�in��a�firm’s��axable�income.

T�e��axable�na�ure�of���e��ransac�ion�of�en�plays�a�more�impor�an��role�in� �e�erminin�� w�e��er� a� mer�er� �akes� place� ��an� any� �ax� benefi�s� ��a��accrue��o���e�acquirin��company.�T�e�seller�may�view���e��ax�free�s�a�us�of� ��e� �ransac�ion�as� a�prerequisi�e� for� ��e��eal� �o� �ake�place.���properly�s�ruc�ure���ransac�ion�can�allow���e��ar�e��s�are�ol�ers��o��efer�any�capi��al��ain�resul�in��from���e��ransac�ion�un�il���ey�ac�ually�sell���e�acquirer’s�s�ock� receive�� in� exc�an�e� for� ��eir� s�ares.� If� ��e� �ransac�ion� is� no�� �ax�free��� ��e�seller� �ypically�will�wan��a��i��er�purc�ase�price� �o�compensa�e�for���e��ax�liabili�y�resul�in��from���e��ransac�ion.1�

12� Gro�on�e��al.�(200�);�Masulis���Wan����an��Xie�(200�).1�� �yers���Lefanowicz���an��Robinson�(200�).

Mergers and Acquisitions Basics��

Market PowerT�e� ��eory� of�market power� su��es�s� ��a�� firms�mer�e� �o� improve� ��eir�monopoly�power��o�se��pro�uc��prices�a��levels�no��sus�ainable�in�a�more�compe�i�ive� marke�.� However��� ��ere� is� li��le� evi�ence� ��a�� ��is� is� �rue����espi�e� �ow� of�en� ��e� popular� press� publis�es� i�� as� ��e� reason� mer�ers�s�oul�� no�� be� allowe�.� In� fac���� increase�� mer�er� ac�ivi�y� is� muc�� more�likely� �o� con�ribu�e� �o� improve�� opera�in�� efficiency� of� ��e� combine��firms���an��o�increase��marke��power���as�you�will�learn�la�er�in���is�c�ap�er.

MisvaluationT�e� presump�ion� ��a�� marke�s� are� efficien�� implies� ��a�� a� �ar�e�’s� s�are�price� reflec�s� accura�ely� all� informa�ion� abou�� ��e� firm� an�� ��erefore� i�s��rue�economic�value�(i.e.���po�en�ial�for��enera�in��cas�).�W�en�impor�an��informa�ion� is� no�� wi�ely� known� abou�� a� firm��� �owever��� inves�ors� may�over��or�un�ervalue���e�firm.�T�ere�is�subs�an�ial�evi�ence�of�a��isconnec�����owever:� over� �ime��� asse�� values� �o��� in�ee���� reflec�� ��eir� �rue� economic�value���bu��a��specific�momen�s���ey�may�no�.

Some�su��es����a��acquirers�can�perio�ically�profi��by�buyin��un�erval�ue���ar�e�s�for�cas��a��a�price�below���eir�ac�ual�value�or�by�usin��equi�y�(even� if� ��e� �ar�e�� is� overvalue�)��� so� lon�� as� ��e� �ar�e�� is� less�overvalue����an� ��e� bi��in�� firm’s� s�ock.1�� �vervalue�� s�ares� enable� ��e� acquirer��o�purc�ase� a� �ar�e�� firm� in� a� s�are�for�s�are� exc�an�e�by� issuin�� fewer�s�ares���w�ic�� re�uces� ��e� probabili�y� of� �ilu�in�� ��e� owners�ip� posi�ion�of�curren�� acquirer� s�are�ol�ers� in� ��e�newly�combine��company.�T�a�’s�impor�an�� because� �ilu�ion� represen�s� a� si�nifican�� cos�� �o� ��e� curren��s�are�ol�ers� of� ��e� acquirin�� firm;� ��eir� s�ares� represen�� claims� on� ��e�firm’s�earnin�s���cas��flows���asse�s���an��liabili�ies.

W�enever� a� firm� increases� i�s� s�ares� ou�s�an�in���� i�� re�uces� ��e� pro�por�iona�e�owners�ip�posi�ion�of�curren��s�are�ol�ers.��vervalue��s�ares��en���o�re�uce���is�cos�.�Consi�er�an�acquirer�w�o�offers���e��ar�e��firm�s�are�ol�ers� $10� for� eac�� s�are� ��ey� own.�T�e� acquirer’s� curren�� s�are�price�is�$10.�T�e�acquirer�woul���ave��o�issue�one�new�s�are�for�eac���ar��e��s�are�ou�s�an�in�.�If���e�acquirer’s�s�are�price�is�value��a��$20���only�0.5�new�s�ares�woul���ave��o�be�issue����an��so�for��.�Consequen�ly�����e�ini�ial��ilu�ion�of���e�owners�ip�posi�ion�of�curren��acquirer�s�are�ol�ers�in���e�new�firm�is�less���e��i��er���e�acquirer’s�s�are�price�compare���o���e�price�offere��for�eac��s�are�of��ar�e��s�ock�ou�s�an�in�.

1�� �n��an��C�en��(2006);��on��e��al.�(2006).

Introduction to Mergers and Acquisitions ��

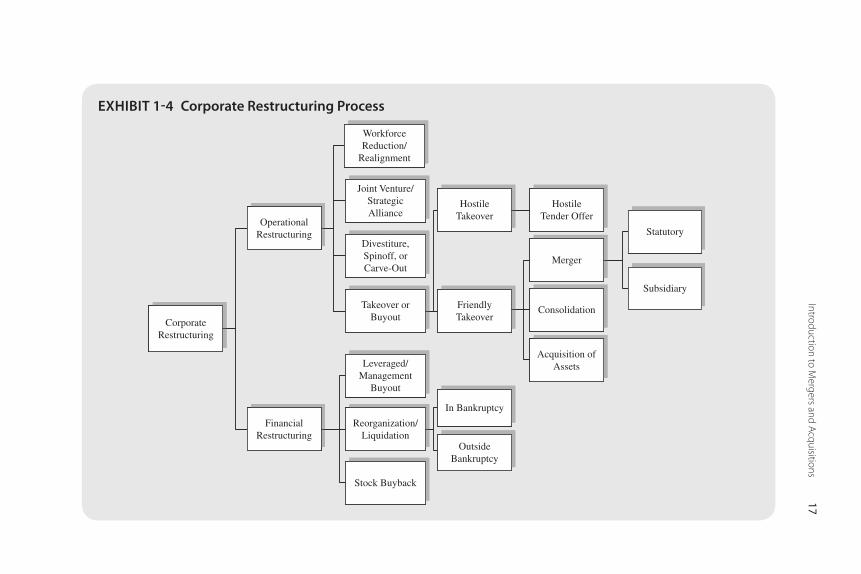

alternative ForMs oF corporate restructuring

Corpora�e�res�ruc�urin��ac�ivi�ies�are�of�en�broken�in�o��wo�specific�ca�e�o�ries.�Operational restructuring��ypically�refers��o���e�ou�ri����or�par�ial�sale�of�companies�or�pro�uc��lines�or��o��ownsizin��by�closin��unprofi�able�or�nons�ra�e�ic�facili�ies.�Financial restructuring��escribes�ac�ions�by�a�firm��o�c�an�e�i�s��o�al��eb��an��equi�y�s�ruc�ure���suc��as�s�are�repurc�ases�or�a���in���eb��ei��er��o�lower���e�corpora�ion’s�overall�cos��of�capi�al�or�as�par��of�an�an�i�akeover��efense�(�iscusse��in�more��e�ail�in�C�ap�er��).�T�e�rela�ive�propor�ions�of��eb��an��equi�y��el��by�a�firm�are���e�firm’s�capi�al�s�ruc�ure.

Mergers and ConsolidationsMer�ers� can� be� �escribe�� from� a� le�al� an�� an� economic� perspec�ive—a��is�inc�ion� impor�an�� �o� �iscussions� of� �eal� s�ruc�urin���� re�ula�ion��� an��s�ra�e�ic�plannin�.

A Legal PerspectiveT�e�le�al�s�ruc�ures�may��ake�on�many�forms��epen�in��on���e�na�ure�of�a��ransac�ion.���merger�is�a�combina�ion�of��wo�or�more�firms�in�w�ic��all�bu��one�cease��o�exis�� legally;���e�combine��or�aniza�ion�con�inues�un�er���e�ori�inal�name�of���e�survivin��firm.�In�a��ypical�mer�er���s�are�ol�ers�of� ��e� �ar�e�� firm—af�er� vo�in�� �o� approve� ��e� mer�er—exc�an�e� ��eir�s�ares�for���ose�of���e�acquirin��firm.�T�ose�no��vo�in��in�favor�(minori�y�s�are�ol�ers)�are�require���o�accep����e�mer�er�an��exc�an�e���eir�s�ares�for���ose�of���e�acquirer.

T�ere�are�several��ifferen���ypes�of�mer�ers.�If�a�mer�er�involves���e�sub�si�iary�of� a�paren�� firm�bu��no�� ��e�paren���� an�� ��e�paren�� is� ��e�primary�s�are�ol�er� in� ��e� subsi�iary��� ��e�mer�er� �oes�no�� require� approval� of� ��e�paren�’s� s�are�ol�ers� (a�� leas�� in� mos�� U.S.� s�a�es).� Suc�� a� mer�er� is� calle��a�s�or��form�mer�er.�T�e�principal�requiremen��is���a����e�paren�’s�owner�s�ip�excee�s���e�minimum���res�ol��se��by���e�s�a�e.�For�example����elaware�allows�a�paren��corpora�ion��o�mer�e�wi���a�subsi�iary�wi��ou��a�s�are�ol�er�vo�e�if���e�paren��owns�a��leas���0�percen��of���e�ou�s�an�in��vo�in��s�ares.

��statutory merger�is�one�in�w�ic����e�acquirin��company�assumes���e�asse�s� an�� liabili�ies� of� ��e� �ar�e�� in� accor�ance� wi��� ��e� s�a�u�es� of� ��e�s�a�e�in�w�ic����e�combine��companies�will�be�incorpora�e�.���subsidiary merger�involves���e��ar�e��becomin��a�subsi�iary�of���e�paren�.�To���e�pub�lic��� ��e� �ar�e�� firm�may�be�opera�e��un�er� i�s�bran��name���bu�� i��will�be�owne��an��con�rolle��by���e�acquirer.

Mergers and Acquisitions Basics��

�l��ou��� ��e� �erms� merger� an�� consolidation� of�en� are� use�� in�er�c�an�eably���a�statutory consolidation—w�ic��involves��wo�or�more�compa�nies�joinin���o�form�a�new�company—is��ec�nically�no��a�mer�er.��ll�le�al�en�i�ies���a��are�consoli�a�e��are��issolve���urin����e�forma�ion�of���e�new�company���w�ic��usually��as�a�new�name.�In�a�mer�er���ei��er���e�acquirer�or���e��ar�e��survives.�T�e�1����combina�ion�of��aimler�Benz�an��C�rysler��o�form��aimlerC�rysler� is�an�example�of�a�consoli�a�ion.�T�e�new�cor�pora�e� en�i�y� crea�e�� as� a� resul�� of� consoli�a�ion� or� ��e� survivin�� en�i�y�followin�� a�mer�er�usually� assumes�owners�ip�of� ��e� asse�s� an�� liabili�ies�of���e�mer�e��or�consoli�a�e��or�aniza�ions.�S�ock�ol�ers�in�consoli�a�e��companies��ypically�exc�an�e���eir�s�ares�for�s�ares�in���e�new�company.

��merger of equals�is�a�mer�er�framework�usually�applie��w�enever���e�mer�er�par�icipan�s�are�comparable�in�size���compe�i�ive�posi�ion���profi�abil�i�y���an��marke��capi�aliza�ion�(i.e.�����e��o�al�value�of�a�firm’s�s�ares)���an��so�i�� is� unclear�w�e��er� one� par�y� is� ce�in�� con�rol� �o� ano��er� an��w�ic��par�y� is� provi�in�� ��e��rea�es�� syner�y.� I�� is� �ypical� for� ��e�CE�s�of� ��e�mer�e��firms��o�become�co�equal�mana�ers�of���e�new�firm�an��for���e�new�firm’s�boar��of��irec�ors��o��ave�equal�represen�a�ion�from���e�boar�s�of���e�mer�e��firms.�Tar�e��firm�s�are�ol�ers�rarely�receive�any�si�nifican��premium� for� ��eir� s�ares� in� a�mer�er�of�equals.15� I�� is�qui�e�uncommon�for� ��e� owners�ip� spli�� �o� be� equally� �ivi�e�.16�T�e� 1���� forma�ion� of�Ci�i�roup�from�Ci�ibank�an��Travelers�is�an�example�of�a�mer�er�of�equals.

An Economic PerspectiveBusiness� combina�ions� may� also� be� �efine�� �epen�in�� on� w�e��er� ��e�mer�in��firms�are�in���e�same�or��ifferen��in�us�ries�an��on���eir�posi�ions�in���e�corpora�e�value�c�ain.1��T�ese��efini�ions�are�par�icularly�impor�an��for�an�i�rus��analysis.

��horizontal merger�occurs�be�ween��wo�firms�wi��in���e�same�in�us��ry;�Proc�er�&�Gamble�an��Gille��e�(2006)�in��ouse�ol��pro�uc�s����racle�an��PeopleSof�� (200�)� in� business� applica�ion� sof�ware��� oil� �ian�s� Exxon�an��Mobil� (1���)���SBC�Communica�ions�an���meri�ec�� (1���)� in� �ele�communica�ions���an��Na�ionsBank�an��Bank�merica�(1���)�in�commer�cial�bankin��are�all�examples.���conglomerate merger� is�one� in�w�ic����e�

1�� Por�er�(1��5).

15� Wulf�(200�)�su��es�e����a����e�CE�s�of��ar�e��firms�of�en�ne�o�ia�e��o�re�ain�a�si�nifican���e�ree�of�con�rol�in���e�mer�e��firm�for�bo�����eir�boar��an��mana�emen��in�exc�an�e�for�a�lower�premium�for���eir�s�are�ol�ers.

16� �ccor�in���o�Mallea�(200�)���only�1��percen���ave�a�50/50�spli�.

Introduction to Mergers and Acquisitions ��

acquirin��company�purc�ases�a�firm�in�a�lar�ely�unrela�e��in�us�ry���suc��as���e�mi��1��0s�acquisi�ion�by�U.S.�S�eel�of�Mara��on��il��o�form�USX.

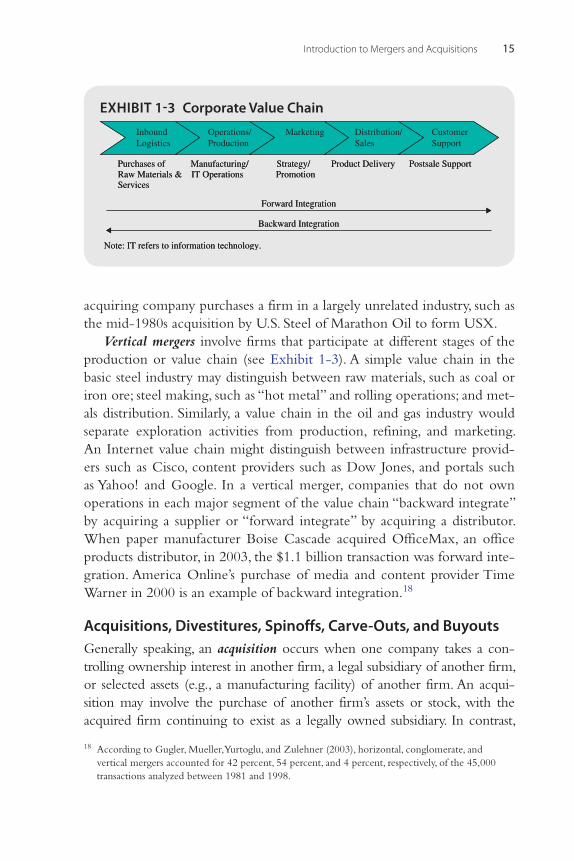

Vertical mergers�involve�firms���a��par�icipa�e�a���ifferen��s�a�es�of���e�pro�uc�ion�or�value�c�ain�(see�Ex�ibi��1��).���simple�value�c�ain� in� ��e�basic�s�eel�in�us�ry�may��is�in�uis��be�ween�raw�ma�erials���suc��as�coal�or�iron�ore;�s�eel�makin����suc��as�“�o��me�al”�an��rollin��opera�ions;�an��me��als��is�ribu�ion.�Similarly���a�value�c�ain�in���e�oil�an���as�in�us�ry�woul��separa�e� explora�ion� ac�ivi�ies� from� pro�uc�ion��� refinin���� an�� marke�in�.��n�In�erne��value�c�ain�mi�����is�in�uis��be�ween�infras�ruc�ure�provi��ers� suc��as�Cisco���con�en��provi�ers� suc��as��ow�Jones���an��por�als� suc��as�Ya�oo!� an��Goo�le.� In� a� ver�ical�mer�er��� companies� ��a�� �o�no�� own�opera�ions�in�eac��major�se�men��of���e�value�c�ain�“backwar��in�e�ra�e”�by�acquirin��a� supplier�or�“forwar�� in�e�ra�e”�by�acquirin��a��is�ribu�or.�W�en� paper�manufac�urer�Boise�Casca�e� acquire���fficeMax��� an� office�pro�uc�s��is�ribu�or���in�200������e�$1.1�billion��ransac�ion�was�forwar��in�e��ra�ion.��merica��nline’s�purc�ase�of�me�ia� an��con�en��provi�er�Time�Warner�in�2000�is�an�example�of�backwar��in�e�ra�ion.1�

Acquisitions, Divestitures, Spinoffs, Carve-Outs, and BuyoutsGenerally� speakin����an�acquisition�occurs�w�en�one�company� �akes�a�con��rollin��owners�ip�in�eres��in�ano��er�firm���a�le�al�subsi�iary�of�ano��er�firm���or� selec�e��asse�s� (e.�.��� a�manufac�urin�� facili�y)�of� ano��er� firm.��n�acqui�si�ion�may� involve� ��e� purc�ase� of� ano��er� firm’s� asse�s� or� s�ock���wi��� ��e�acquire�� firm�con�inuin�� �o�exis�� as�a� le�ally�owne�� subsi�iary.� In�con�ras�����

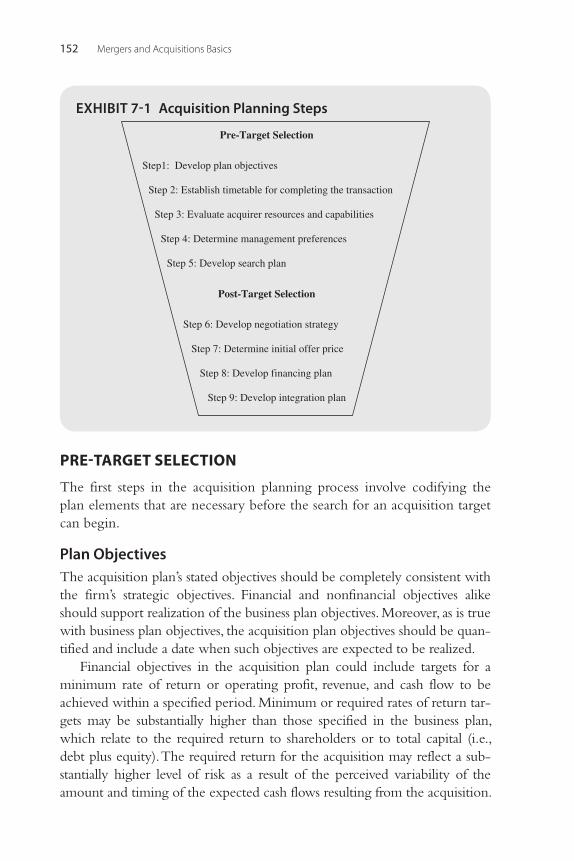

1�� �ccor�in���o�Gu�ler���Mueller���Yur�o�lu���an��Zule�ner�(200�)����orizon�al���con�lomera�e���an��ver�ical�mer�ers�accoun�e��for��2�percen����5��percen����an����percen����respec�ively���of���e��5��000��ransac�ions�analyze��be�ween�1��1�an��1���.

EXHIBIT 1-3 Corporate Value Chain

Purchases of Manufacturing/ Strategy/ Product Delivery Postsale SupportRaw Materials & IT Operations PromotionServices

Forward Integration

Backward Integration

Note: IT refers to information technology.

InboundLogistics

Operations/Production

Marketing Distribution/Sales

CustomerSupport

Purchases of Manufacturing/ Strategy/ Product Delivery Postsale SupportRaw Materials & IT Operations PromotionServices

Forward Integration

Backward Integration

Note: IT refers to information technology.

InboundLogistics

Operations/Production

Marketing Distribution/Sales

CustomerSupport

Mergers and Acquisitions Basics��

a�divestiture�is���e�sale�of�all�or�subs�an�ially�all�of�a�company�or�pro�uc��line��o�ano��er�par�y�for�cas��or�securi�ies.�In�a�spinoff���a�paren��crea�es�a�new�le�al�subsi�iary�an���is�ribu�es�s�ares�in���e�subsi�iary��o�i�s�curren��s�are�ol�ers�as�a� s�ock� �ivi�en�.��n� equity carve-out� �escribes� a� �ransac�ion� in�w�ic�� ��e�paren��firm�issues�a�por�ion�of�i�s�s�ock�or���a��of�a�subsi�iary��o���e�public.

�� leveraged buyout� (LB�)�or�highly leveraged transaction� involves� ��e�purc�ase�of�a�company�finance��primarily�by��eb�.��l��ou���LB�s��ypi�cally�involve�priva�ely�owne��firms�����e��erm�of�en�is�applie��w�en�a�firm�buys�back�i�s�s�ock�usin��primarily�borrowe��fun�s��o�conver��from�a�pub�licly��o�a�priva�ely�owne��company.

Ex�ibi��1���summarizes���e�various�forms�corpora�e�res�ruc�urin��may��ake.

Friendly versus hostile takeovers

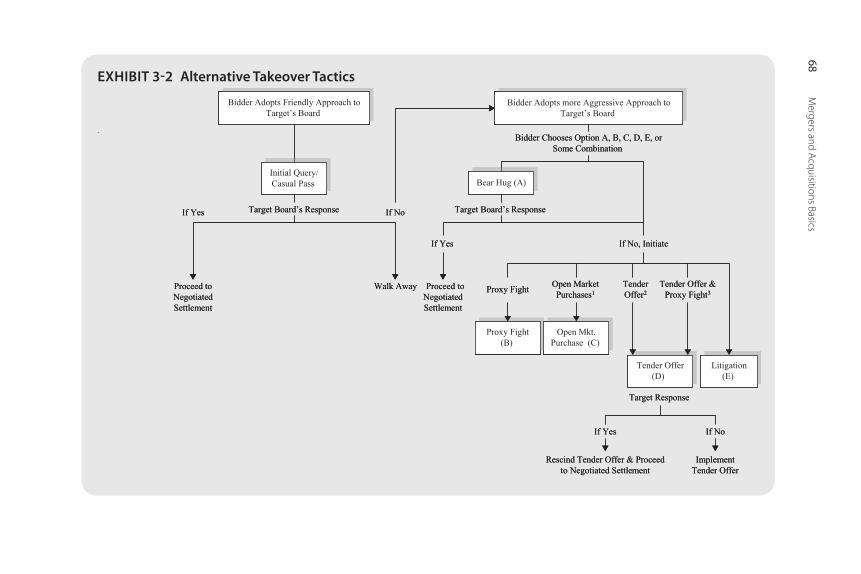

In�a�friendly takeover�of�con�rol�����e��ar�e�’s�boar��an��mana�emen��are�recep��ive� �o� ��e� i�ea� an�� recommen�� s�are�ol�er� approval.�To��ain� con�rol��� ��e�acquirin��company�usually�mus��offer�a�premium��o���e�curren��s�ock�price.�T�e�excess�of���e�offer�price�over���e��ar�e�’s�premer�er�s�are�price�is�calle��a�purchase premium�or�acquisition premium1��an��reflec�s���e�perceive��value�of�ob�ainin��a�con�rollin��in�eres��(i.e.�����e�abili�y��o��irec����e�ac�ivi�ies�of���e�firm)�in���e��ar�e������e�value�of�expec�e��syner�ies�(e.�.���cos��savin�s)�resul��in��from�combinin����e��wo�firms���an��any�overpaymen��for���e��ar�e��firm.��verpaymen��is���e�amoun��an�acquirer�pays�for�a��ar�e��firm�in�excess�of���e�presen��value�of�fu�ure�cas��flows���inclu�in��syner�y.�Presen��value�is�an�es�i�ma�e�of���e�curren��value�of�fu�ure�cas��flows����akin��in�o�accoun����e�mini�mum�financial�ra�es�of�re�urn�require��by�inves�ors�an��len�ers.�Cas��receive���o�ay��as�a��i��er�value���an�cas��receive��a��a�la�er��a�e�because�i��can�be�reinves�e��a��some�ra�e�of�in�eres����so�fu�ure�cas��flows�mus��be�re�uce��by�po�en�ial�accumula�e��in�eres��earnin�s��o�es�ima�e���eir�value��o�ay.

�nalys�s� of�en� a��emp�� �o� i�en�ify� ��e� amoun�� of� premium� pai�� for� a�con�rollin�� in�eres�� (i.e.��� control premium)� an�� ��e� amoun��of� incremen�al�

1�� U.S.�mer�er�premiums�avera�e��abou�����percen��be�ween�1����an��1����(�n�ra�e���Mi�c�ell���an��S�affor����2001).�Rossi�an��Volpin�(200�)��ocumen��an�avera�e�premium�of����percen���urin����e�1��0s�for�U.S.�mer�ers.�T�e�au��ors�also�fin��premiums�in����coun�ries�ran�in��from�10�percen��for�Brazil�an��Swi�zerlan���o�120�percen��for�Israel�an��In�onesia.�T�e�wi�e�ran�e�of�es�ima�es�may�reflec����e�value�a��ac�e���o���e�special�privile�es�associa�e��wi���con�rol�in�various�coun�ries.�For�example���insi�ers�in�Russian�oil�companies��ave�been�able��o�cap�ure�a�lar�e�frac�ion�of�profi�s�by�sellin��some�of���eir�oil�a��below�marke��prices��o�firms���ey�own.

Introduction to Mergers and Acquisitions

��

EXHIBIT 1-4 Corporate Restructuring Process

CorporateRestructuring

OperationalRestructuring

FinancialRestructuring

Divestiture,Spinoff, orCarve-Out

Takeover orBuyout

HostileTender Offer

Leveraged/Management

Buyout

Reorganization/Liquidation

Stock Buyback

Statutory

Subsidiary

HostileTakeover

FriendlyTakeover

Merger

Consolidation

Acquisition ofAssets

In Bankruptcy

OutsideBankruptcy

Joint Venture/StrategicAlliance

WorkforceReduction/

Realignment

CorporateRestructuring

OperationalRestructuring

FinancialRestructuring

Divestiture,Spinoff, orCarve-Out

Takeover orBuyout

HostileTender Offer

Leveraged/Management

Buyout

Reorganization/Liquidation

Stock Buyback

Statutory

Subsidiary

HostileTakeover

FriendlyTakeover

Merger

Consolidation

Acquisition ofAssets

In Bankruptcy

OutsideBankruptcy

Joint Venture/StrategicAlliance

WorkforceReduction/

Realignment

Mergers and Acquisitions Basics��

value�crea�e����a����e�acquirer�is�willin���o�s�are�wi�����e��ar�e�’s�s�are�ol��ers.��n�example�of�a�pure control premium�is�a�con�lomera�e�willin���o�pay�a�price�si�nifican�ly�above���e�prevailin��marke��price�for�a��ar�e��firm��o��ain�a�con�rollin��in�eres����even���ou���po�en�ial�opera�in��syner�ies�are�limi�e�.�In�suc��an�ins�ance�����e�acquirer�of�en�believes�i��will�recover���e�value�of���e�con�rol�premium�by�makin��be��er�mana�emen���ecisions�for���e��ar�e��firm.�I��is�impor�an���o�emp�asize���a��w�a��is�of�en�calle��a�con�rol�premium��in���e�popular�or��ra�e�press�is�ac�ually�a�purc�ase�or�acquisi�ion�premium���a��inclu�es�bo���a�premium�for�syner�y�an��a�premium�for�con�rol.

T�e�offer��o�buy�s�ares�in�ano��er�firm���usually�for�cas����securi�ies���or�bo�����is�calle��a�tender offer.��l��ou����en�er�offers�are�use��in�a�number�of� circums�ances��� ��ey� mos�� of�en� resul�� from� frien�ly� ne�o�ia�ions� (i.e.���ne�o�ia�e���en�er�offers)�be�ween���e�boar�s�of���e�acquirer�an����e��ar��e��firm.�T�ose���a��are�unwan�e��by���e��ar�e�’s�boar��are�referre���o�as�hostile tender offers. Self-tender offers�are�use��w�en�a�firm�seeks��o�repur�c�ase�i�s�own�s�ock.

�n� unfriendly takeover� or� hostile takeover� occurs� w�en� ��e� ini��ial� approac�� was� unsolici�e���� ��e� �ar�e�� was� no�� seekin�� a� mer�er��� ��e�approac��was�con�es�e��by���e��ar�e�’s�mana�emen����an��con�rol�c�an�e���an�s�(i.e.���usually�requirin����e�purc�ase�of�more���an��alf�of���e��ar�e�’s�vo�in��common�s�ock).�T�e�acquirer�may�a��emp���o�circumven��mana�e�men��by�offerin���o�buy�s�ares��irec�ly�from���e��ar�e�’s�s�are�ol�ers�(i.e.���a� �os�ile� �en�er� offer)� an�� by� buyin�� s�ares� in� a� public� s�ock� exc�an�e�(i.e.���an�open market purchase).

Frien�ly� �akeovers� are� of�en� consumma�e�� a�� a� lower� purc�ase� price���an��os�ile��ransac�ions.����os�ile��akeover�a��emp��may�a��rac��new�bi���ers�w�o�mi����no��o��erwise��ave�been�in�eres�e��in���e��ar�e�—calle��pu��in����e��ar�e��in play.�In���e�ensuin��auc�ion�����e�final�purc�ase�price�may�be�bi��up��o�a�poin��well�above���e�ini�ial�offer�price.��cquirers�pre�fer�frien�ly��akeovers�because���e�pos�mer�er�in�e�ra�ion�process�is�usually�more�expe�i�ious�w�en�bo���par�ies�are�coopera�in�� fully.�For� ��ese�rea�sons���mos���ransac�ions��en���o�be�frien�ly.

alternative Ways to increase shareholder value

��business alliance�refers��o�a�form�of�combina�ion�o��er���an�M&�.�Suc��alliances� inclu�e� join�� ven�ures��� s�ra�e�ic� alliances��� minori�y� inves�men�s���franc�ises���an��licenses.

�� joint venture� (JV)� is� a� coopera�ive� business� rela�ions�ip� forme�� by��wo� or� more� separa�e� par�ies� �o� ac�ieve� common� s�ra�e�ic� objec�ives.�

Introduction to Mergers and Acquisitions ��

W�ile���e�JV�is�of�en�an�in�epen�en��le�al�en�i�y�suc��as�a�corpora�ion�or�par�ners�ip�forme��for�a�specific�perio��an��for�a�specific�purpose���i��may��ake�any�or�aniza�ional�form��eeme��appropria�e�by���e�par�ies�involve�.�Eac�� JV� par�ner� con�inues� �o� exis�� as� a� separa�e� en�i�y.� JV� corpora�ions��ave���eir�own�mana�emen��repor�in���o�a�boar��of��irec�ors�comprisin��represen�a�ives�of���e�par�icipa�in��companies.

��strategic alliance��enerally�falls�s�or��of�crea�in��a�separa�e�le�al�en�i�y.���s�ra�e�ic�alliance�may�be�an�a�reemen���o�sell�eac��firm’s�pro�uc�s��o���e�o��er’s�cus�omers�or� �o�co��evelop�a� �ec�nolo�y���pro�uc����or�process.�T�e��erms�of�suc��an�a�reemen��may�be�le�ally�bin�in��or�lar�ely�informal.

��minority investment�requires�li��le�commi�men��of�mana�emen���ime�an��may�be��i��ly�liqui��if���e�inves�men��is�in�a�publicly��ra�e��company.���company�may�c�oose��o�assis��small�or�s�ar�up�companies�in���e��evel�opmen��of� pro�uc�s� or� �ec�nolo�ies� i�� fin�s�useful��� receivin�� represen�a��ion�on���e�boar��in�exc�an�e�for���e�inves�men�.�Suc��inves�men�s�may�also� be� oppor�unis�ic� in� ��a�� passive� inves�ors� �ake� a� lon���erm� posi�ion�in�a�firm�believe���o��ave�si�nifican��apprecia�ion�po�en�ial.�For�example���Warren�Buffe��’s�Berks�ire�Ha��away�firm�inves�e��$5�billion�in�Gol�man�Sac�s�in�200��by�acquirin��conver�ible�preferre��s�ock���a��pays�a�10�per�cen�� �ivi�en�.� Berks�ire� Ha��away� also� receive�� warran�s� �o� purc�ase��$5�billion�of�Gol�man�Sac�s�common�s�ock�a��$115�per�s�are.�T�is�exer�cise�price�is�less���an�one��alf�of���e�s�are�price�only�a�year�earlier.

�� license���w�ic��requires�no�ini�ial�capi�al���provi�es�a�convenien��way�for� a� company� �o� ex�en�� i�s� bran�s� �o� new� pro�uc�s� an�� new� marke�s.�T�e�company�simply�licenses�i�s�bran��names��o�o��ers.���company�may�also� �ain� access� �o� a� proprie�ary� �ec�nolo�y� ��rou��� ��e� licensin�� pro�cess.���franchise�is�a�specialize��form�of�a�license�a�reemen����a���ran�s�a�privile�e��o�a��ealer�from�a�manufac�urer�or�franc�ise�service�or�aniza�ion��o�sell���e�franc�iser’s�pro�uc�s�or�services�in�a��iven�area.�Suc��arran�e�men�s�can�be�exclusive�or�nonexclusive.�Un�er�a�franc�ise�a�reemen������e�franc�iser� may� offer� ��e� franc�isee� consul�a�ion��� promo�ional� assis�ance���financin����an��o��er�benefi�s�in�exc�an�e�for�a�s�are�of���e�franc�ise’s�rev�enue.� Franc�ises� represen�� a� low�cos�� way� for� ��e� franc�iser� �o� expan����because� ��e� franc�isee� usually� provi�es� ��e� nee�e�� capi�al.�T�e� success�of�franc�isin������ou������as�been�lar�ely�limi�e���o�in�us�ries�suc��as�fas��foo��services�an��re�ail�in�w�ic��a�successful�business�mo�el�can�be�easily�replica�e�.

T�e� major� a��rac�ion� of� ��ese� al�erna�ives� �o� ou�ri���� acquisi�ion� is���e�oppor�uni�y�for�eac��par�ner��o��ain�access��o���e�o��er’s�skills���pro��uc�s��� an�� marke�s� a�� a� lower� overall� cos�� in� �erms� of� mana�emen�� �ime�

Mergers and Acquisitions Basics�0

an��money.�Major��isa�van�a�es�inclu�e�limi�e��con�rol�����e�nee���o�s�are�profi�s���an����e�po�en�ial�loss�of��ra�e�secre�s�an��skills��o�compe�i�ors.

*�*�*

Mer�ers� an�� acquisi�ions� are� an� impor�an�� c�an�e� a�en�.� Businesses�are�cons�an�ly�c�urnin����an��only���e�mos��innova�ive�an��nimble�survive.�W�en�companies��o� fall� �o� ��e� compe�i�ion��� i�� is�of�en� ��rou���mer�er���acquisi�ion��� bankrup�cy��� �ownsizin���� or� some� o��er� form� of� corpora�e�res�ruc�urin�.�T�e�pace�a��w�ic��failin��businesses��isappear�of�en��epen�s�on� ��eir� size��� ��e� perceive��po�en�ial� impac�� ��ey��ave�on� ��e� economy���an�� �ow� cri�ical� ��ey� are� �o� na�ional� securi�y.� Lar�e� businesses�may� lin��er�for�an�ex�en�e��perio��as���eir�cre�i�ors�rene�o�ia�e�loans.�To�ay�����e�concep��of�“�oo�bi���o�fail”��as�le���o��u�e��overnmen��subsi�ies��o��yin��businesses��o�preven��w�a��may�be�inevi�able.

W�ile�M&�s�are�a�cri�ical�componen��in���e�business�s�ra�e�y�of�some�firms���i��is�impor�an���o�remember���a����ey�represen��only�one�of�several�ways�of�execu�in��business�plans.�T�ere�are�al�erna�ives��� from���e�various�forms�of�business�alliances� �o��oin�� i��on�your�own���rou���a� solo�ven��ure.�W�ic��me��o�� is�c�osen��epen�s�on�mana�emen�’s��esire� for�con��rol���willin�ness��o�accep��risk���an����e�ran�e�of�oppor�uni�ies�presen��a��a�par�icular�momen��in��ime.

A Case in Point: Mars Buys Wrigley in One Sweet DealWrigley Corporation, a U.S.-based leader in gum and confectionary products, had been losing market share since �00� to Cadbury Schweppes in the U.S. gum market. Mars Corporation, a privately owned candy company with annual glo-bal sales of $�� billion, sensed an opportunity to achieve sales, marketing, and distribution synergies by acquiring Wrigley. On April ��, �00�, Mars announced that it had reached an agreement to merge with Wrigley for $�� billion in cash.

The terms of the agreement were approved unanimously by the boards of both firms. Wrigley shareholders would receive $�0.00 in cash for each share of common stock outstanding. The purchase price represented a �� percent pre-mium to Wrigley’s closing share price of $��.�� on the announcement date. The merged firms would, in �00�, enjoy a ��.� percent share of the global confec-tionary market, annual revenue of $�� billion, and ��,000 employees worldwide.

When the deal was consummated in September �00�, it was a strategic blow to the efforts of Cadbury Schweppes to continue as the market leader in the global confectionary market with its gum and chocolate business. Prior to the announcement, Cadbury had a �0 percent worldwide market share.

Introduction to Mergers and Acquisitions ��

Wrigley became a separate standalone subsidiary of Mars, with $�.� billion in sales. The deal helps Wrigley augment its sales, marketing, and distribution capabilities. To provide more focus to the Mars brands and stimulate growth, Mars transferred its global nonchocolate confectionery sugar brands to Wrigley. Bill Wrigley, Jr., remains Executive Chairman of Wrigley, and the Wrigley man-agement team remains in place. The combined companies now have substan-tial brand recognition and product diversity in six growth categories: chocolate, nonchocolate confectionery, gum, food, drinks, and pet-care products. The resulting confectionery powerhouse also expects to achieve significant cost sav-ings by combining manufacturing operations and having a substantial presence in emerging markets.

Although mergers among competitors are not unusual, the deal’s highly leveraged financial structure is atypical of transactions of this type. Almost �0 percent of the purchase price was financed through borrowed funds, with the remainder financed largely by a third-party equity investor. Mars’ upfront exposure consisted of paying for closing costs from its cash balances in excess of its operating needs. JPMorgan Chase and Goldman Sachs provided the debt financing for the transaction, $�� billion and $�.� billion, respectively. Berkshire Hathaway, a nontraditional source of high-yield financing, put in an additional $�.� billion in subordinated debt. Typically, such financing would have been provided by investment banks or hedge funds and subsequently repackaged into securities and sold to long-term investors such as pension funds, insurance companies, and foreign investors, but the meltdown in the global credit markets in �00� forced investment banks and hedge funds to withdraw from the high-yield market in an effort to strengthen their balance sheets. Berkshire Hathaway completed the financing of the purchase price by providing $�.� billion in equity financing in exchange for a �.� percent ownership stake in Wrigley.

Things to Think About:�. Why did Wrigley’s share price not rise to the $�0 offer price following the

announcement of the merger? Why did competitor Cadbury’s shares gain �.� percent following the announcement?

�. Speculate as to how the Wrigley family may have been convinced to sell their firm.

�. How did factors external to both firms specifically influence their decision to merge?

�. Would you characterize this transaction as a friendly or hostile takeover? Why was this particular approach taken?

�. Of the motivations for business combinations outlined in this chapter, which do you think were most applicable in this case study?

Answers can be found at: www.elsevierdirect.com/companion.jsp?ISBN=���0���������

23Mergers and Acquisitions Basics� ©�2011�Elsevier�Inc.ISBN:�����0�12��������2�� ��I: �ll ri���s reserve�.����0�12��������2�� ��I: �ll ri���s reserve�.�����I:� �ll�ri���s�reserve�.

CHAPTER

201110.1016/B����0�12��������2.00002�0

What History Tells Us about M&A Performance

�l��ou�����ere�is�li��le�ques�ion���a����e�fu�ure�of�M&��ac�ivi�y�will�con��inue��o�evolve���reflec�in��new��lobal�compe�i�ion�an����e�c�an�in��re�u�la�ory� clima�e��� i��will� con�inue� �o� be� possible� �o� �raw�parallels�wi��� ��e�pas�.�T�ese�insi���s�s�oul���elp�us��o�un�ers�an���ow��o�a�ap����e�s�ruc��ure�an��financin��of�fu�ure�M&�s.

��ains����is�back�rop�����is�c�ap�er��iscusses�mer�er�ac�ivi�y�in��erms�of�cycles���or�waves���w�ic���en���o�mirror�c�an�es�in���e�business�cycle�as�well�as���e�re�ula�ory�environmen��an���ec�nolo�ical�innova�ion.�You�will�learn�w�y� ��ey�occur� an�� jus���ow� impor�an�� i�� is� �o�un�ers�an���ow�mer�er�waves� can�be� an�icipa�e�.�You� also�will� consi�er�w�e��er�M&�s��� �is�ori�cally����ave�pai��off� for� s�are�ol�ers���bon��ol�ers��� an�� socie�y.�Finally���you�will�explore�a�case���a��illus�ra�es��ow���e�marke��base��process�of�crea�ive��es�ruc�ion�paves���e�way�for�new�an��innova�ive�solu�ions��o�con�empo�rary�c�allen�es�an��i�en�ifies���e�impor�an��role�M&�s��ave�in���is�process.

Merger and acquisition Waves

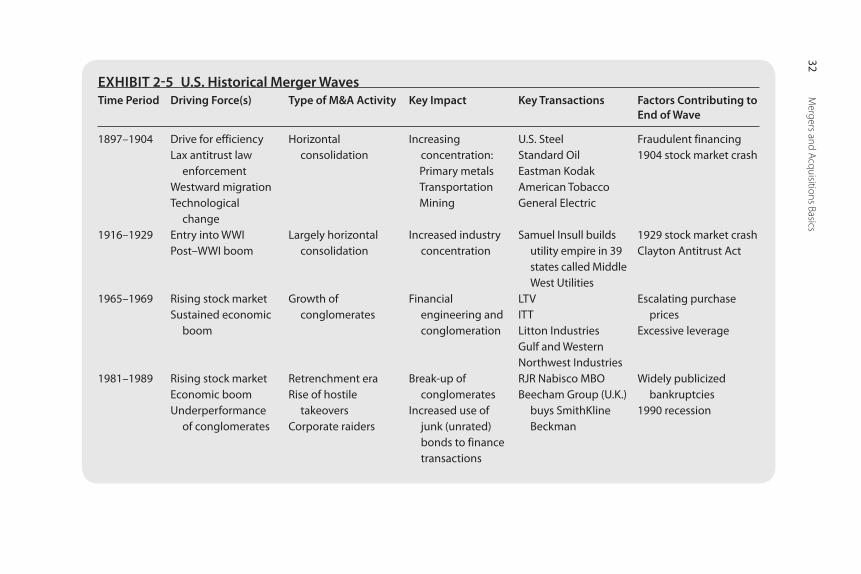

T�e� followin�� sec�ions� �iscuss� ��e� �e�erminan�s� of� M&�� waves��� ��e� six��iscre�e�perio�s�in�w�ic����ey��ave�occurre����an��w�y�i��is�impor�an���o�an�icipa�e�suc��waves.

Why M&A Waves OccurM&�� ac�ivi�y� in� ��e� Uni�e�� S�a�es� �as� �en�e�� �o� clus�er� in� mul�iyear�waves���wi���six�suc��waves�occurrin��since���e�la�e�1��0s.�T�ere�are��wo�compe�in�� explana�ions� for� ��is� p�enomenon.� �ne� ar�ues� ��a�� mer�er�waves�occur�w�en�firms�in�in�us�ries�reac���o�“s�ocks”�in���eir�opera�in��environmen�s��1� suc�� as� from� �ere�ula�ion;� ��e� emer�ence� of� new� �ec��nolo�ies��� �is�ribu�ion� c�annels��� or� subs�i�u�e� pro�uc�s;� or� a� sus�aine�� rise�in�commo�i�y�prices.�T�e�size�an�� len����of� ��e�M&��wave��epen�s� �o�

2

1� Brealey�an��Myers�(200�);�Mar�ynova�an��Renneboo��(200�);�an��Mi�c�ell�an��Mul�erin�(1��6).

Mergers and Acquisitions Basics24

a� lar�e�par��on��ow�many�in�us�ries�are�affec�e��by���ese�s�ocks���as�well�as� ��e�ex�en��of� ��e� impac�.�Some� s�ocks��� suc�� as� ��e�emer�ence�of� ��e�In�erne���� are� pervasive� in� ��eir� impac�;� o��ers� are� more� specific��� suc�� as��ere�ula�ion� of� financial� services� an�� u�ili�ies� or� rapi�ly� escala�in�� com�mo�i�y� prices.� In� response� �o� s�ocks��� firms� wi��in� ��e� in�us�ry� of�en�acquire�ei��er�all�or�par�s�of�o��er�firms.

T�e� secon�� ar�umen�� is� base�� on� ��e� misvalua�ion� i�ea� (�iscusse�� in�C�ap�er�1)�an��su��es�s���a��mana�ers�use�overvalue��s�ock��o�buy���e�asse�s�of�lower�value��firms.�For�M&�s��o�clus�er�in�waves����oes���e�ar�umen����valu�a�ions�of�many�firms�(measure��by���eir�price��o�earnin�s�or�marke���o�book�ra�ios� compare�� �o� o��er� firms)� mus�� increase� a�� ��e� same� �ime.� Mana�ers�w�ose� s�ocks� are� believe�� �o� be� overvalue�� move� concurren�ly� �o� acquire�companies�w�ose�s�ock�prices�are�lesser�value�2�an����reflec�in����e�influence�of�overvalua�ion�����e�me��o��of�paymen��woul��normally�be�s�ock.�

Experience�su��es�s���a����e�“s�ock”�ar�umen��is�a�s�ron�er�one���espe�cially� if� i�� is�mo�ifie�� �o� inclu�e� ��e� effec�s� of� ��e� availabili�y� of� capi�al�in� causin�� an�� sus�ainin��mer�er�waves.�Capi�al� availabili�y� plays� a� cri�i�cal� role� in� �e�erminin�� mer�er� waves.� S�ocks� alone��� wi��ou�� sufficien��liqui�i�y� �o� finance� ��e� �ransac�ions��� will� no�� ini�ia�e� a� wave� of� mer�er�ac�ivi�y.�Moreover���rea�ily�available��� low�cos��capi�al�may�cause�a�sur�e�in�M&��ac�ivi�y�even�if�in�us�ry�s�ocks�are�absen�����an����is�was�par�icularly�impor�an��in���e�mos��recen��M&��boom.

First Wave (1897–1904): Horizontal ConsolidationM&��ac�ivi�y� in� ��is� firs��wave�was� spurre��by�a��rive� for�efficiency��� lax�enforcemen��of���e�S�erman��n�i�rus���c����wes�war��mi�ra�ion���an���ec��nolo�ical�c�an�e.�Mer�ers��urin����is�perio��were�lar�ely��orizon�al�an��resul�e��in�increase��concen�ra�ion�in�primary�me�als��� �ranspor�a�ion���an��minin�.�Lar�e�companies�absorbe��small�ones.�In�1�01���J.�P.�Mor�an�cre�a�e���merica’s� firs��billion��ollar�corpora�ion���U.S.�S�eel—forme��by� ��e�combina�ion�of���5�separa�e�companies�����e�lar�es��of�w�ic��was�Carne�ie�S�eel.����er��ian�s�forme���urin����is�era�inclu�e�S�an�ar���il���Eas�man�Ko�ak����merican�Tobacco���an��General�Elec�ric.�Frau�ulen��financin��an����e�1�0��s�ock�marke��cras��en�e����e�boom.

2� R�o�es�Kropf�an��Viswana��an�(200�);�S�leifer�an��Vis�ny�(200�).�� Numerous�s�u�ies�confirm���a��lon���erm�fluc�ua�ions�in�marke��valua�ions�an����e�number�of�

�akeovers�are�posi�ively�correla�e�.�See��n�ra�e�e��al.�(2001);��n��an��C�en��(2006);��aniel�e��al.�(1���);�an���on��e��al.�(2006).�However���w�e��er��i���valua�ions�con�ribu�e��o��rea�er��akeover�ac�ivi�y�or�increase��M&��ac�ivi�y�boos�s�marke��valua�ions�is�less�clear.

�� Harfor��(2005).

What History Tells Us about M&A Performance 25

Second Wave (1916–1929): Increasing Concentration�c�ivi�y��urin����is�perio��was�a�resul��of���e�en�ry�of���e�Uni�e��S�a�es�in�o�Worl��War�I�an����e�pos�war�economic�boom.�Mer�ers�also��en�e���o�be� �orizon�al� an�� fur��er� increase�� in�us�ry� concen�ra�ion;� for� example���Samuel�Insull�buil��an�empire�of�u�ili�ies�wi���opera�ions�in����s�a�es.�T�e�s�ock�marke�� cras��of� 1�2���� alon��wi���passa�e�of� ��e�Clay�on��n�i�rus���c����a��fur��er��efine��monopolis�ic�prac�ices���brou������is�era��o�a�close.

Third Wave (1965–1969): The Conglomerate EraT�is�perio��of�M&��ac�ivi�y�was�c�arac�erize��by���e�emer�ence�of�finan�cial�en�ineerin��an��con�lomera�ion.���risin��s�ock�marke��an����e�lon��es��perio��of�unin�errup�e���row���in�U.S.��is�ory��o���a���ime�resul�e��in�recor��price��o�earnin�s�(P/E)�ra�ios.�Companies��iven��i���P/E�ra�ios�by�inves�ors�learne���ow��o��row�earnin�s�per�s�are�(EPS)���rou���acqui�si�ion���ra��er���an���rou���reinves�men�.�Companies�wi����i���P/E�ra�ios�woul��of�en�acquire�firms�wi���lower�P/E�ra�ios�an��increase���e�EPS�of���e� combine�� companies��� w�ic�� in� �urn� boos�e�� ��e� s�are� price� of� ��e�combine��companies—so�lon��as���e�P/E�applie���o���e�s�ock�price�of���e�combine�� companies��i��no�� fall� below� ��e�P/E�of� ��e� acquirin�� com�pany� before� ��e� �ransac�ion.�To� main�ain� ��is� pyrami�in�� effec���� ��ou������ar�e��companies��a�� �o��ave�earnin�s��row���ra�es� sufficien�ly�a��rac�ive��o�convince�inves�ors��o�apply���e��i��er�mul�iple�of���e�acquirin��com�pany� �o� ��e� combine�� companies.� In� �ime��� ��e� number� of� �i����row�����rela�ively� low� P/E� companies� �ecline���� as� con�lomera�es� bi�� up� ��eir�P/Es.�T�e��i��er�prices�pai�� for� ��e� �ar�e�s���couple��wi��� ��e� increasin��levera�e�of���e�con�lomera�es���cause����e�“pyrami�s”��o�collapse.

Fourth Wave (1981–1989): The Retrenchment EraT�e�1��0s���a��eca�e���a��saw���e�rise�of���e�corpora�e�rai�er���were�c�ar�ac�erize�� by� ��e� breakup� of�many�major� con�lomera�es� an�� a� prolifera��ion�of�financial�buyers�usin����e��os�ile��akeover�(rarely�use��previously)�an�� ��e� levera�e�� buyou�� (LB�)� as� ��eir� primary� acquisi�ion� s�ra�e�ies.�Mana�emen��buyou�s�an���akeovers�of�U.S.�companies�by�forei�n�acquirers�became�more�common.�Con�lomera�es�be�an��o��ives��unrela�e��acquisi��ions�ma�e�in���e�1�60s�an��early�1��0s;�in�fac����of�acquisi�ions�ma�e�ou��si�e� ��e� acquirer’s� main� line� of� business� be�ween� 1��0� an�� 1��2��� some��60�percen���a��been�sol��by�1���.5�In�1��������e�me�a�railroa��Burlin��on�Nor��ern� spun� off� i�s� ener�y� proper�ies��� Burlin��on� Resources��� for��5� Wassers�ein�(1���).

Mergers and Acquisitions Basics26

$�.2�billion.�T�e�same�year���Mobil��il�sol��re�ailer�Mon��omery�War��for�$�.�� billion.� In� 1������ Paramoun���� formerly� Gulf� an��Wes�ern� In�us�ries���sol��i�s�finance�company����ssocia�es�Firs��Capi�al���for�$�.��billion.

For� ��e� firs�� �ime��� �akeovers� of� U.S.� companies� by� forei�n� firms�excee�e��in�number�an���ollars���e�acquisi�ions�by�U.S.�firms�of�compa�nies� in� Europe��� Cana�a��� an�� ��e� Pacific� Rim� (exclu�in�� Japan).� Forei�n�purc�asers�were�mo�iva�e��by� ��e� size�of� ��e�marke���� limi�e�� res�ric�ions�on� �akeovers��� ��e� sop�is�ica�ion� of�U.S.� �ec�nolo�y��� an�� ��e�weakness� of���e��ollar�a�ains��major�forei�n�currencies.�Forei�n�companies�also��en�e���o� pay� subs�an�ial� premiums� for�U.S.� companies��� because� ��e� s�ren���� of���eir�currencies�lowere����e�effec�ive�cos��of�acquisi�ions.�Moreover���favor�able�accoun�in��prac�ices�allowe��forei�n�buyers��o�wri�e�off��oo�will� in���e�year�in�w�ic��i��occurre����unlike�U.S.�firms���a���a���o�c�ar�e��oo��will� expense� a�ains�� earnin�s� for� many� years.6�T�e� lar�es�� cross�bor�er��eals� in� ��is�perio�� inclu�e� ��e�Beec�am�Group�PLC�(UK)�purc�ase�of���e�Smi��Kline�Beckman�Corpora�ion� for� $16.1�billion� in�1������Bri�is��Pe�roleum�Corpora�ion’s�1����acquisi�ion�of���e�remainin���5�percen��of�S�an�ar���il�Corpora�ion�for�$�.��billion���an��Campeau�Corpora�ion�of�Cana�a’s�1����purc�ase�of�Fe�era�e���epar�men��S�ores�for�$6.5�billion.

T�e� for�unes� of� LB�s� wane�� �urin�� ��e� �eca�e’s� secon�� �alf.� RJR�Nabisco� exemplifie�� ��e� c�allen�es� face�� by� LB�s� �urin�� ��is� perio�.�Ko�lber����Kravis�&�Rober�s�(KKR)�pai��$2�.5�billion�for���e�company�in�1������a�recor��purc�ase�price�a����e��ime.��espi�e��oin��public�in�1��1���RJR�Nabisco�s�ru��le��un�er���e�bur�en�of�i�s�massive��eb��un�il���e�mi��1��0s���w�en�improvin��cas��flow�enable����e�firm��o�pay�off�a�si�nifican��por�ion.����er�LB���ransac�ions�also�fell�on��ar���imes.�Towar����e�en��of���e�1��0s�����e�level�of�mer�er�ac�ivi�y��apere��off�in�line�wi���a�slowin��economy�an��wi�ely�publicize��LB��bankrup�cies.�Moreover�����e�junk�bon��marke���rie��up�as�a�major�source�of�financin��wi�����e��emise�of��rexel�Burn�am�����e�lea�in��un�erwri�er�an��“marke��maker”�for��i���yiel��securi�ies.

6� Goo�will�represen�s���e�excess�of���e�purc�ase�price�pai��by���e�acquirer�for���e�ne��asse�s�acquire��(i.e.���asse�s�purc�ase��revalue���o���eir�curren��marke��values�less�acquire��liabili�ies).�Concep�ually���i��represen�s�in�an�ible�value�suc��as�bran��names�an��o��er�forms�of�in�ellec�ual�proper�y.�Prior��o��ecember�15���2001�����e�value�of��oo�will�on���e�acquirer’s�balance�s�ee���a���o�be�wri��en�off�(i.e.���amor�ize�)�over�as�lon��as��0�years.�T�is�is�no�lon�er�require����bu��i��mus��be�c�ecke��for�impairmen��in���e�wake�of�any�si�nifican��even����a��may�re�uce���e�value�of���e��oo�will��o�less���an�w�a��is�s�own�on���e�acquirer’s�balance�s�ee��(suc��as���e�loss�of�key�cus�omer�con�rac�s�or�pa�en��or�copyri����pro�ec�ion���or�any��iminu�ion�in���e�value�of���e�bran��of�pro�uc�s�acquire��from���e��ar�e��firm).�W�enever���is�occurs�����e�value�of���e��oo�will�mus��be�revise���ownwar���o�reflec����ese�even�s�wi�����e�amoun��of���e��ownwar��revision�c�ar�e��a�ains����e�firm’s�curren��earnin�s.

What History Tells Us about M&A Performance 27

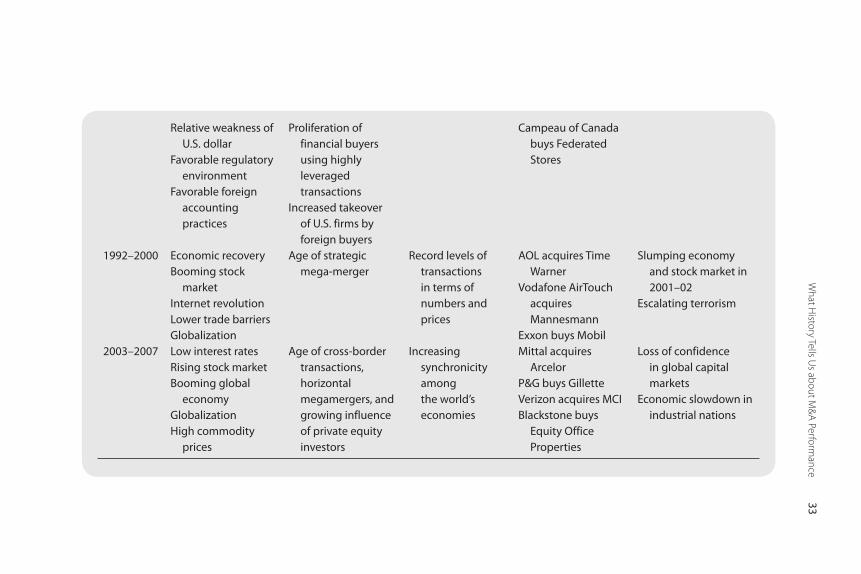

Fifth Wave (1992–2000): The Age of the Strategic Mega-MergerMany�believe����a����e�M&�s��urin����e�1��0s�were� lar�ely�overprice��an��overlevera�e����an��junk�bon��or��i���yiel��financin��was�consi�ere��unlikely� �o� recover� from� ��e� pummelin�� i�� �a�� �aken� a�� ��e� en�� of� ��e��eca�e.�Consequen�ly���many�assume�� ��a�� �akeovers�woul��no�� re�urn� �o���eir�levels�of���e�la�e�1��0s.

�l��ou��� M&�� ac�ivi�y� �i�� �iminis�� �urin�� ��e� 1��0� recession��� ��e�number� of� �ransac�ions� an�� ��e� �ollar� volume� reboun�e�� s�arply� be�in�nin��in�1��2.�T�e�lon�es��economic�expansion�an��s�ock�marke��boom�in�U.S.��is�ory���unin�errup�e��by�recession���was�powere��by�a�combina�ion�of���e�informa�ion��ec�nolo�y�revolu�ion���con�inue���ere�ula�ion���re�uc�ions�in��ra�e�barriers���an����e��lobal��ren���owar��priva�iza�ion.�Bo�����e��ollar�volume�an��number�of� �ransac�ions� con�inue�� �o� se�� recor�s� ��rou��� ��e�en��of���e�1��0s�before�con�rac�in��s�arply�w�en���e�In�erne��bubble�burs����a�recession��i����e�Uni�e��S�a�es�in�2001���an���lobal��row���weakene�.

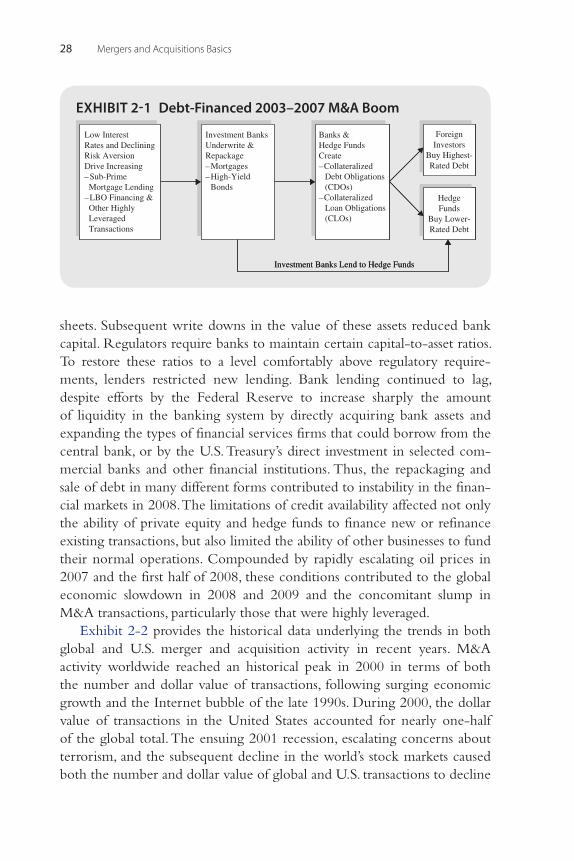

Sixth Wave (2003–2007): The Rebirth of LeverageU.S.�financial�marke�s��urin����is�six���wave���especially�from�2005���rou���200����were�c�arac�erize��by�an�explosion�of��i��ly�levera�e��buyou�s�an��priva�e� equi�y� inves�men�s� (i.e.��� �akeovers� finance�� by� limi�e�� par�ner�s�ips)�an����e�prolifera�ion�of�complex�securi�ies�colla�eralize��by�pools�of��eb��an��loan�obli�a�ions�of�varyin��levels�of�risk.�Muc��of���e�financin��of� ��ese� �ransac�ions���as�well� as�mor��a�e�backe�� securi�y� issues��� �ook� ��e�form�of�syn�ica�e���eb��(i.e.����eb��purc�ase��by�un�erwri�ers�for�resale��o���e�inves�in��public).

T�e�syn�ica�ion�process��isperses�suc���eb��amon��many��ifferen��inves��ors.�T�e� issuers� of� ��e� �eb�� �isc�ar�e� muc�� of� ��e� responsibili�y� for� ��e�loans� �o�o��ers� (excep��w�ere� inves�ors��ave� recourse� �o� ��e�ori�ina�ors� if��efaul��occurs�wi��in�a�s�ipula�e���ime).�Un�er�suc��circums�ances��� len�ers��ave�an�incen�ive��o�increase���e�volume�of�len�in���o��enera�e�fee�income�by�re�ucin����eir�un�erwri�in��s�an�ar�s��o�accep��riskier� loans.��f�er�suc��loans�are�sol���o�o��ers���loan�ori�ina�ors�are�likely��o�re�uce���eir�moni�orin��of���em.�T�ese�prac�ices���couple��wi���excee�in�ly�low�in�eres��ra�es�ma�e�possible�by�a�worl��awas��in�liqui�i�y���con�ribu�e���o�excessive�len�in��an��encoura�e�� acquirers� �o� overpay� si�nifican�ly� for� �ar�e�� firms.� Ex�ibi�� 2�1�illus�ra�es��ow���ese�fac�ors�sprea��risk���rou��ou����e��lobal�cre�i��marke�s.

Because� i�� is� �ifficul�� �o� �e�ermine� ��e� ul�ima�e� �ol�ers� of� ��e� �eb��af�er�i��is�sol�����eclinin���ome�prices�an��a�rela�ively�few��i��ly�publicize���efaul�s� in�200���ri��ere��concerns�amon��len�ers���a����e�marke��value�of� ��eir� asse�s� was� ac�ually� well� below� ��e� value� lis�e�� on� ��eir� balance��

Mergers and Acquisitions Basics28

s�ee�s.�Subsequen��wri�e��owns�in���e�value�of���ese�asse�s�re�uce��bank�capi�al.�Re�ula�ors�require�banks��o�main�ain�cer�ain�capi�al��o�asse��ra�ios.�To� res�ore� ��ese� ra�ios� �o� a� level� comfor�ably� above� re�ula�ory� require�men�s��� len�ers� res�ric�e�� new� len�in�.� Bank� len�in�� con�inue�� �o� la�����espi�e� effor�s� by� ��e� Fe�eral� Reserve� �o� increase� s�arply� ��e� amoun��of� liqui�i�y� in� ��e� bankin�� sys�em�by� �irec�ly� acquirin�� bank� asse�s� an��expan�in����e��ypes�of�financial�services�firms���a��coul��borrow�from���e�cen�ral�bank���or�by���e�U.S.�Treasury’s��irec��inves�men��in�selec�e��com�mercial� banks� an��o��er� financial� ins�i�u�ions.�T�us��� ��e� repacka�in�� an��sale�of��eb��in�many��ifferen��forms�con�ribu�e���o�ins�abili�y�in���e�finan�cial�marke�s�in�200�.�T�e�limi�a�ions�of�cre�i��availabili�y�affec�e��no��only���e�abili�y�of�priva�e�equi�y�an���e��e�fun�s��o�finance�new�or�refinance�exis�in���ransac�ions���bu��also�limi�e����e�abili�y�of�o��er�businesses��o�fun����eir�normal�opera�ions.�Compoun�e��by� rapi�ly�escala�in��oil�prices� in�200��an����e�firs���alf�of�200������ese�con�i�ions�con�ribu�e���o���e��lobal�economic� slow�own� in� 200�� an�� 200�� an�� ��e� concomi�an�� slump� in�M&���ransac�ions���par�icularly���ose���a��were��i��ly�levera�e�.

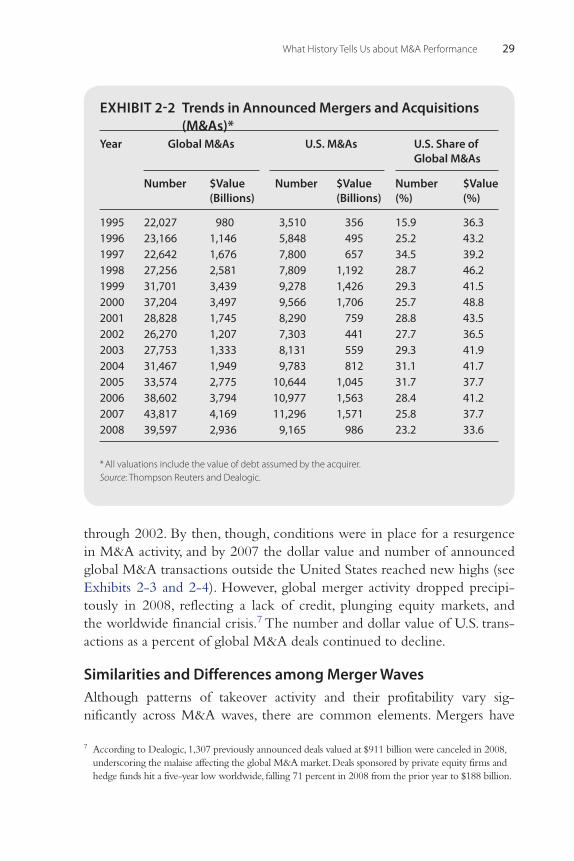

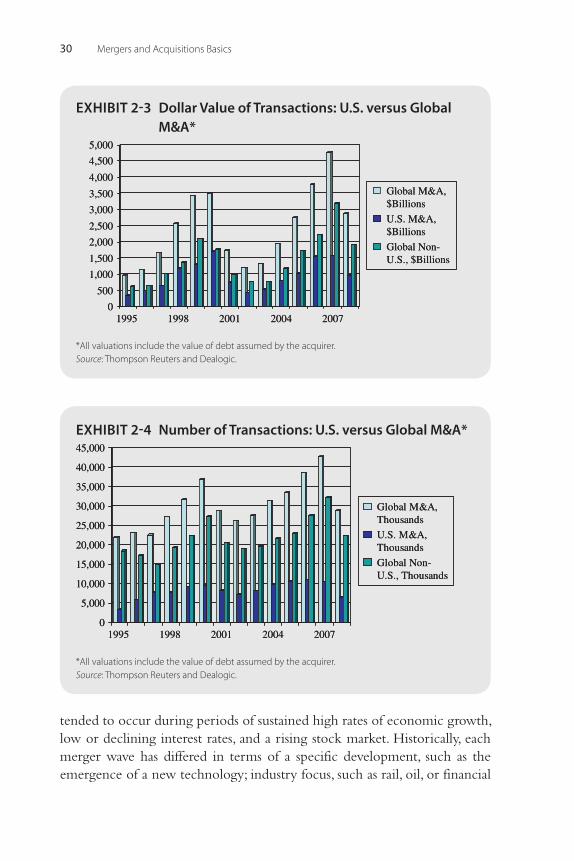

Ex�ibi��2�2�provi�es���e��is�orical��a�a�un�erlyin����e��ren�s�in�bo����lobal� an�� U.S.� mer�er� an�� acquisi�ion� ac�ivi�y� in� recen�� years.� M&��ac�ivi�y� worl�wi�e� reac�e�� an� �is�orical� peak� in� 2000� in� �erms� of� bo�����e�number�an���ollar�value�of� �ransac�ions��� followin��sur�in��economic��row���an����e�In�erne��bubble�of���e�la�e�1��0s.��urin��2000�����e��ollar�value� of� �ransac�ions� in� ��e�Uni�e�� S�a�es� accoun�e�� for� nearly� one��alf�of���e��lobal��o�al.�T�e�ensuin��2001�recession���escala�in��concerns�abou���errorism���an����e�subsequen���ecline�in���e�worl�’s�s�ock�marke�s�cause��bo�����e�number�an���ollar�value�of��lobal�an��U.S.��ransac�ions��o��ecline�

EXHIBIT 2-1 Debt-Financed 2003–2007 M&A Boom

Low InterestRates and DecliningRisk AversionDrive Increasing–Sub-Prime Mortgage Lending–LBO Financing & Other Highly Leveraged Transactions

Investment BanksUnderwrite &Repackage–Mortgages–High-Yield Bonds

Banks &Hedge FundsCreate–Collateralized Debt Obligations (CDOs)–Collateralized Loan Obligations (CLOs)

ForeignInvestors

Buy Highest-Rated Debt

HedgeFunds

Buy Lower-Rated Debt

Investment Banks Lend to Hedge Funds