Embed Size (px)

Citation preview

EXECUTIVE SUMMARY

Mergers and acquisition will be now new step in takeover marriages of two different but

allied corporate companies on Indian Business scenario, due to global recession. It is

necessity of both companies to come, unite & amalgamate for mutual survival and

benefit to boost the turnover. It is also a boon to investors and shareholders of both

companies.

Here I take pleasure to present my project study on recent merger of HLL & Ponds (I)

Ltd. as a case study because this amalgamation of two giant corporate companies have

shown significant growth in sales turnover compared to their previous singular existence

two years back.

Two years successful joint involvement proves their mutual unification for their

committed goals. This can be example and lesson for other merger aspirant companies

and it has also set a milestone for collapsing or shaking industries. On the background

of ‘liquidity Crunch’, it is oxygen. It is also catalyst to enhance and accelerate the mutual

growth. Indian business atmosphere should welcome this promontory strategy.

In this study you will find miraculous transfer of seen from before to aftermath of

merging. Here I have elaborated the wide effect on joint range of products of both

companies, increase in sales figures and increase in their sales value. It is a productivity

analysis of the merger between HLL and PIL.

1

I observed the factors they consider, to get merge with each other. What was the

objective behind this merge? Have all the shareholders and creditors approved this

merge? What procedures took place at the time of merge? & What was the fruit of

that merge?

After observing all the data collected, I came to conclusion that, this merger was really

fruitful for both companies & mutually beneficial.

2

CHAPTER 1

1.1 RATIONALE

This project on acquisitions and mergers has been selected by me basically out

of the curiosity to know the reasons for which companies go in for acquisitions

and mergers and also about the after effects of the same.

I have focused mainly on HLL and Ponds merger, which took place in March

1998 and had created much furore in the market. This project is an effort to study

how these businesses get attracted to merge with each other’s? What factors

they consider for merging? What is the objective behind such mergers? Is

everyone including shareholders, creditors, employees and others happy with

such mergers? What procedures take place at the time of mergers? & What is

the fruit of such mergers and acquisitions taking place round the globe?

1.2 AIMS AND OBJECTIVES IN DOING THIS PROJECT

The prime motto in doing this project is to know in depth about mergers and

acquisitions and their effects on companies undergoing the same. Also an effort

has been taken to differentiate among mergers and acquisitions. A case study on

the merger between HLL and Ponds has been put to practically understand such

happenings going on in the business world every next day. The objectives of

my study are as under –

1. To find out the reasons for which HLL and PONDS merged with each

other.

3

2. To learn the external growth of HLL through PONDS merger. i.e. the after

effects of this merger

3. To learn the applications of my knowledge of mergers and acquisitions.

1.3 METHOD OF DATA COLLECTION

I have collected primary data as well as secondary data. I have adopted the

following methodology of study through out the project –

1. I visited Hindustan lever Limited, 165/166-lever house, Back Bay

Reclamation, Mumbai 400 020 several times.

2. I interviewed the top -level executives i.e. finance officer of the company

and collected the primary information about the merger and required data.

3. I telephonically interviewed Mr. Rajprakash who is from Finance

department in HLL Company.

4. Then from websites of HLL as well as some corporate sector websites I

collected some required material regarding legal policies of merger. From

strategic planting’s books I got brief theoretical notes regarding mergers.

5. Data was also collected from secondary sources such as various leading

newspapers, magazines, Internet, TV etc.

1.4 LIMITATIONS IN DOING THIS PROJECT

Certain difficulties were faced by me while doing this project, which became

limitations in the completion of this project.

1. Most of the times in quo with the policy of keeping the data ‘confidential’

HLL refuse to give data in detail.

4

2. As Ponds India limited Company is in Madras I could not meet any person

from Ponds India Limited, as it was not possible physically to go there.

3. Because of unavailability of main executive officers who were really on the

panel of that merger I could not get appointment of such officers.

The success story of this merger is explained in brief in the project report, which I

had undertaken. I started my data collection work on 2, January 2002. I required

30 days to complete this project. First I started by collecting adequate basic

material from websites. Then I took appointment of HLL financial officers and I

discussed about my project in detail with them and they gave me required

material.

5

CHAPTER 2

2.1 INTRODUCTION

Today’s world is on the urge of industrial growth. No one is standing behind.

Everybody wants to flow off with success. Every one wants value added benefits

for survival.

Our Indian industry sector is also not behind in this case. I, personally feel that

our country is going to be one good example for other countries. But when I think

about, by what means we can achieve such success I get attracted by our

industrial growth rate, which is hardly below 2%. Instead of thinking on, what

factors are responsible for this slow rate of growth, we have to think upon our

strategy, which we are going to implement. If we are lagging in any case we

always take help of other in somewhat same manner our industries are taking co-

operation in corporate sector for mutual benefits from other companies.

On observation it was found that such business combinations, which may take

forms of mergers, acquisitions, amalgamations and takeovers, are important

features of corporate structural changes. They have played an important role in

external growth also.

6

2.2 MERGER MANIA

1993 will go down in business almanac as the year in which corporate India

experienced a merger mania. For, freed of the economic shackles that had

chained them for decades, transnationals and big business houses have since

displayed a voracious appetite for parts - or the whole - of their rivals.

The figures speak for themselves. During the '80s the total number of Mergers &

Acquisitions (M&As) that India witnessed was only 84 (32 mergers & 52

takeovers), but in 1993 alone there were 114 M&As. What's more, in the coming

years this figure is bound to rise further. In 1995 there were 426 M&A

announcements, more than half of which are bound to go through. This

translates more than one merger / acquisition every three days.

To be sure, this is by no means the first time that the M & A game are being

played in recent times. The first wave was between 1977 & 1985, kicked off by

the imposition of FERA & the industrial license-permit raj. The second wave

began in 1989-90, triggered off by the first changes of liberalization. This time

round, the difference is that the game is no longer dominated by a single player.

Firms and businessmen, small & large, low profile & high profile, Indian & foreign

are into M & A. The time is not far off when M&A will become the mainstay of

corporate developments.

7

2.3 FACTORS WHICH GAVE A SUDDEN IMPETUS TO M & A

The main reasons for the sudden impetus to M&A in India are the deshackling of

the restrictive provisions of various laws & regulations like the MRTP Act, FERA,

Industrial Licensing Policy, etc. Moreover, in a protected economy, there was

little incentive to contemplate acquisitions, hog limelight & get into complicated

legal & financial problems. The entry of multinationals and the integration of India

into the global market has also made it necessary for Indian corporates to own

companies of a truly global scale for the sake of economies. Divestures and sell-

offs, earlier considered a sign of failure, are also becoming commonplace as

organizations learn to focus on core competence.

CHAPTER 3

3.1 DESCRIPTION OF THE TERMS MERGER / AMALGAMATION AND

ACQUISITION / TAKEOVERS

1. MERGER

Merger means combination of two or more companies wherein only one

company survives and others cease to exist. The merger takes place for a

consideration, which the acquiring company either pays in cash or by offering its

shares. The survivor acquires the assets as well as liabilities of the merged

company or companies. Thus combination of two or more firms is known as

merger. It may be brought about in two ways -

1. Acquisition of one business unit by another or,

2. Creation of a new company by complete consolidation of two or more units.

8

2. AMALGAMATION

Ordinarily, amalgamation means merger. Amalgamation can be described as a

blending of two or more existing undertakings into one undertaking. The

shareholders of each blending company which is to carry on the blended

undertaking.

3. ACQUISITION

Acquisition in general sense is acquiring the ownership in the property. In the

context of business combinations, an acquisition is the purchase by one

company of a controlling interest in the share capital of another existing

company. An acquisition may be affected by -

1. Agreement with the persons holding majority interests in the company

management like members of the board or major shareholders commanding

majority of voting power.

2. Purchase of shares in open market.

3. To make takeover offer to the general body of shareholders.

4. Purchase of new shares by private treaty.

5. Acquisition of share capital of one company may be by either all or one of the

following forms of consideration viz. Means of cash, issuance of loan capital

or insurance of share capital.

4. TAKEOVER

A takeover is acquisition and both the terms are used interchangeably. Takeover

differs from merger in approach to business combination. Transactions involved

9

in takeover, determination of the share exchange or cash price and the fulfillment

of goals of combination all are different in takeovers than in mergers.

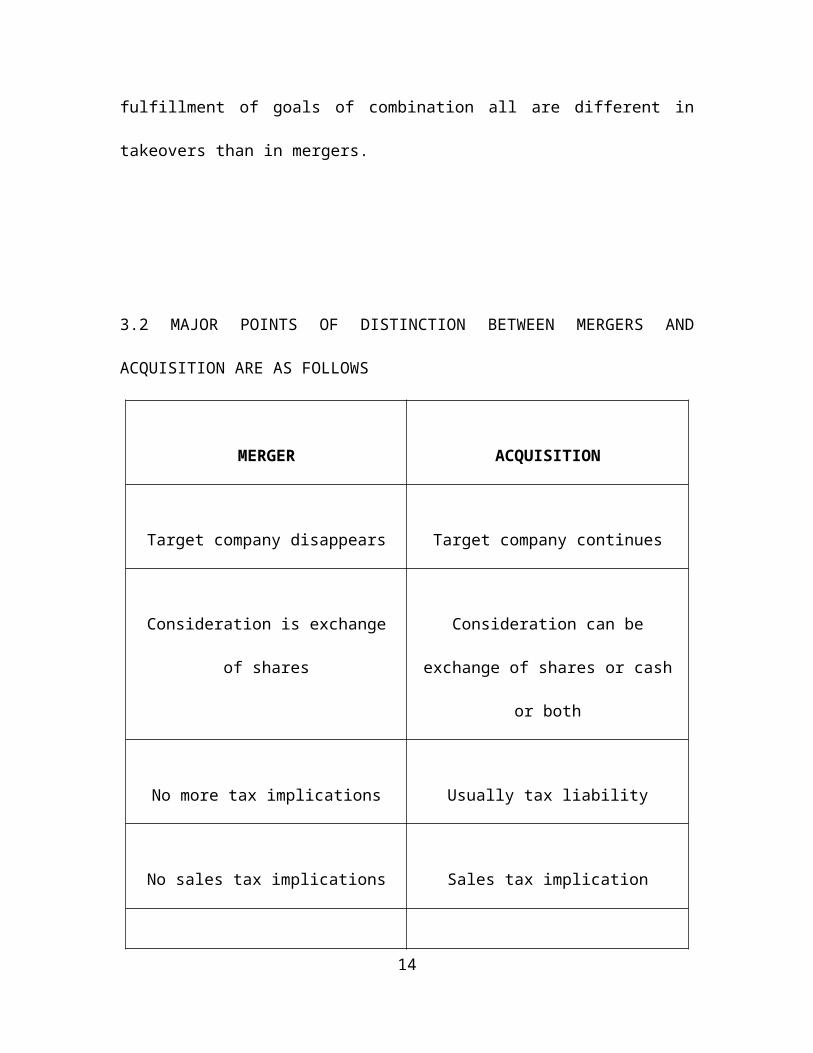

3.2 MAJOR POINTS OF DISTINCTION BETWEEN MERGERS AND ACQUISITION

ARE AS FOLLOWS

MERGER ACQUISITION

Target company disappears Target company continues

Consideration is exchange of shares Consideration can be exchange of

shares or cash or both

No more tax implications Usually tax liability

No sales tax implications Sales tax implication

No out flow of funds by acquiring

company

Outflows of funds may take place

Cannot acquire part Can acquire part

10

3.3 TYPES OF MERGERS

The basis for classification of mergers is the business in which the companies

are involved. Different motives underlie different types of mergers. Different types

of mergers are –

1. HORIZONTAL MERGER

It is a merger of two competing firms, which are at the same stage of industrial

process. The acquiring firm belongs to the same industry as the target company.

The main motives behind this are to obtain economies of scale in production by

eliminating duplication of facilities and operations, elimination of competition,

increase in market segments and exercise of better control over the market.

There is little evidence to dispute the claim that properly executed horizontal

mergers lead to a significant reduction in costs. A horizontal merger brings about

all the benefits that accrue with an increase in the scale of operations. Apart from

the cost reduction it also helps firms in industries like pharmaceuticals, cars, etc

where huge amounts are spent on R&D to achieve a critical mass and reduce

unit development costs.

11

2. VERTICAL MERGER

It is a merger of one company with another, which is involved, in a different stage

of the production and/or distribution process thus espousing backward integration

to assimilate the sources of supply and/or forward integration towards market

outlets. The main motives are to ensure ready take off of the materials, gain

control over product specifications, increase profitability by gaining the margins of

the previous supplier/distributor, gain control over scarce raw material supplies

and in some cases to avoid sales tax.

3. CONGLOMERATE MERGER

It is an amalgamation of two companies engaged in unrelated industries. The

motive is to ensure a better utilization of financial resources, enlarge debt

capacity, and to reduce risk by diversification.

Conglomerate merger has evinced particular interest among researchers

because of the general curiosity about the nature of gains arising out of them.

Economic gain arising out of a conglomerate merger is not clear. Much of the

traditional analysis relating to economies of scale in production, research,

distribution and management is not relevant for conglomerates. The argument in

its favour is that inspite of the absence of economies of scale and

complimentaries, they may cause stabilization in profit stream.

4. CONCENTRIC MERGER

12

This is a mild form of conglomeration. It is the merger of one company with

another which is engaged in the production / marketing of an allied product.

Concentric merger is also called product extension merger. In such a merger, in

addition to the transfer of general management skills, there is also a transfer of

specific management skills, as in production, research, marketing, etc, which

have been hitherto used in a different line of business. A concentric merger

brings all the advantages of conglomeration without the side effects i.e. with a

concentric merger it is possible to reduce risk without venturing into areas that

the management is not competent in.

5. CONSOLIDATION MERGER

It involves a merger of a subsidiary company with its parent. Reasons behind

such a mergers are to stabilize cash flows & to make funds available for the

subsidiary.

In consolidation economic gain is not readily apparent because the merging firms

are under the same management even before the merger. Still the flow of funds

between a parent & the subsidiary is obstructed by a lot of other considerations

like taxation, etc. Therefore, consolidation can smoothen cash flows and also

make it easier to infuse funds for the revival of sick subsidiaries.

3.4 TYPES OF ACQUISITIONS

1. NEGOTIATED / FRIENDLY

13

This is organized by the incumbent management with a view to part with the

control of management to another group through negotiations. The terms and

conditions of takeover are mutually settled by the groups.

2. OPEN MARKET / HOSTILE

They are also referred to as raid on the company in order to takeover the

management of, or acquire controlling interest in, the target company, a

person /group of persons acquire shares from the open market / financial

institutions/mutual funds/ willing shareholders at a price higher than the prevailing

market price.

3. BAILOUT

When a profit earning company takes over a financially sick company it is a bail –

out type of takeover.

3.5 STAGES IN MERGERS & ACQUISITION

The complexity of mergers & acquisitions requires skills, which are not often

needed, in a day-to- day business. A typical merger or acquisition involves the

following stages -

1. Strategic review of opportunities.

2. Target identification and evaluation.

14

3. Confidential approaches.

4. Tax-efficient financial structuring.

5. Transaction securing and closing.

3.6 ANALYSIS OF MERGERS AND ACQUISITIONS

There are three important steps involved in the analysis of mergers and

acquisitions –

1. PLANNING

The acquiring firm should review its objective of acquisition in the context of its

strengths and weaknesses, and corporate goals. This will help in indicating the

product-market strategies that are appropriate for the company. It will also force

the firm to identify business units that should be dropped and those that should

be added.

The planning of acquisition will require the analysis of industry-specific and the

firm-specific information. The acquiring firm will need industry data on market

growth, nature of competition, ease of entry, capital and labour intensity, degree

of regulation etc. About the target firm the information needed will include the

quality of management, market share, size, capital structure, profitability,

production and marketing capabilities etc.

15

2. SEARCH AND SCREENING

Search focuses on how and where to look for suitable candidates for acquisition.

Screening process short-lists a few candidates from many available. Detailed

information about each of these candidates is obtained.

Merger objectives may include attaining faster growth, improving profitability,

improving managerial effectiveness, gaining market power and leadership,

achieving cost reduction etc. These objectives can be achieved in various ways

rather than through mergers alone. The alternatives to merger include joint

ventures, strategic alliances, elimination of inefficient operations, cost reduction

and productivity improvement, hiring capable managers etc. If merger is

considered as the best alternative, the acquiring firm must satisfy itself that it is

the best available option in terms of its own screening criteria and economically

most attractive.

3. FINANCIAL EVALUATION

Financial evaluation of a merger is needed to determine the earnings and cash

flows, areas of risk, the maximum price payable to the target company and the

best way to finance the merger. The acquiring firm must pay a fair consideration

to the target firm for acquiring its business. In a competitive market situation with

capital market efficiency, the current market value is the correct and fair value of

the target firm. The target firm will not accept any offer below the current market

value of its share. The target firm may, in fact, expect the offer price to be more

than the current market value of its share since it may expect that merger

16

benefits will accrue to the acquiring firm. A merger is said to be at a premium if it

thinks that it can increase the target firm’s after merger by improving its

operations and due to synergy. It may have to pay premium as an incentive to

the target firm’s shareholders to induce them to sell their shares so that the

acquiring firm is enabled to obtain the control of the target firm.

CHAPTER 4

4.1 MOTIVES AND BENEFITS OF MERGERS

Why do mergers take place? It is believed that mergers and acquisitions are

strategic decisions leading to the maximization of a company’s growth by

enhancing its production and marketing operations. They have become popular

in the recent times because of the enhanced competition, breaking of trade

barriers, free flow of capital across countries and globalization of business as a

number of economies are being deregulated and integrated with other

economies. A number of reasons are attributed for the occurrence of mergers

and acquisitions. For example, in a nutshell it is suggested that mergers and

acquisition are intended to -

1. To attain a higher growth rate than is possible through internal growth

strategy;

2. To bring about an increase in the price-earnings ratio and market price of

shares;

3. To purchase a unit for better use of investible funds;

17

4. To have quick access to resources already developed by another firm

through R & D and innovative management;

5. To reduce competition by acquiring competing firms and limit competition;

6. To fill the gap in the existing product line;

7. To add new products (diversify) when the existing product has reached

the peak in its life cycle;

8. To secure tax advantage by acquiring other firms with accumulated losses

which can be set off against the current or future profits;

9. To improve the efficiency of operations and attain higher profitability

through potential synergistic effects;

10. Overcome the problem of slow growth and profitability in one’s own

industry;

11. Gain economies of scale and increase income with proportionately less

investment;

12. Establish a transnational bridgehead without excessive start-up costs to

gain access to a foreign market;

13. Utilize under-utilized resources – human and physical and managerial

skills and market power;

14. Displace existing management;

15. Circumvent government regulations;

16. Create an image of aggressiveness and strategic opportunism, empire

building and to amass vast economic powers for the company.

18

4.2 ARE THERE ANY REAL BENEFITS OF MERGERS AND ACQUISITIONS?

A number of benefits of mergers are claimed. All of them are not real benefits.

Based on the empirical evidence and the experience of certain companies, the

most common motives and advantages of mergers and acquisitions are

explained below -

1. ACCELERATED GROWTH

Growth is essential for sustaining the viability, dynamism and value enhancing

capability of a company. A growth-oriented company is not only able to attract

the most talented executives but it would also be able to retain them. Growing

operations provide challenges and excitement to the executives as well as

opportunities for their job enrichment and repaid career development. This helps

to increase managerial efficiency. Being the same all other things, growth lead to

higher profits and increase in the shareholders’ value. A company can achieve its

growth objective by -

Expending its existing markets.

Entering in new markets.

A Company may expand and/or diversify its markets internally or externally. If the

company cannot grow internally due to lack physical and managerial resources, it

can grow externally by combining its operations with other companies through

mergers and acquisitions. Mergers and acquisitions may help to accelerate the

pace of a company’s growth in a convenient and inexpensive manner.

19

Internal growth requires that the company should develop its operating facilities-

manufacturing, research; marketing etc. internal development of facilities for

growth also requires time. Thus, lack or inadequacy of resources and time

needed for internal development constraints a company’s pace of growth. The

company can acquire production facilities as well as other resources from outside

through mergers and acquisitions. Specially, for entering in new

products/markets, the company may lack technical skills and may require special

marketing skills and/or a wide distribution network to access different segments

of markets. The company can acquire existing company or companies with

requisite infrastructure and skills and grow quickly. Mergers and acquisitions,

however, involve cost. External growth could be expensive if the company pays

an excessive prince for merger. Benefits should exceed the cost of acquisition for

realizing.

A growth, which adds value to shareholders - In practice, it has been found that

the management of number of acquiring companies paid an excessive price for

acquisition to satisfy their urge for high growth and large size of their companies.

It is necessary that price may be carefully determined and negotiated so that

merger enhances the value of shareholders.

20

2. ENHANCED PROFITABILITY

The combination of two or more companies may result in more than the average

profitability due to cost reduction and efficient utilization of resources. This may

happen because of the following reasons -

Economies of scale

Operating economies

Synergy

3. ECONOMIES OF SCALE

Economies of scale arise when increase in the volume of production leads to a

reduction in the cost of production per unit. Merger may help to expand volume

of production without a corresponding increase in fixed costs. Thus, fixed costs

are distributed over a large volume of production causing the unit cost of

production to decline. Economies of scale may also arise from other

indivisibilities such as production facilities, management functions and

management resources and systems. This happens because a given function,

facility or resource is utilized for a larger scale of operation. For example, a given

mix of plant and machinery can produce scale economies when \its capacity

utilization is increased. Economies in the use of the marketing function can be

achieved by covering wider markets and customers using a given sales force and

promotion and advertising efforts. Economies of scale may also be obtained

21

from the optimum utilization of management resource and systems resulting in

economies of scale.

4. REDUCTION IN TAX LIABILITY

In a number of countries, a company is allowed to carry forward its accumulated

loss to set off against it future earnings for calculating its tax liability. A loss

making or sick company may not be in a position to earn sufficient profits in

future to take advantage of the carry forward provision. If it combines with a

profitable company, the combined company can utilize the carry forward loss and

save taxes. In India, a profitable company is allowed to merge with a sick

company to set off against its profits the accumulated loss and unutilized

depreciation of that company. A number of companies in India have merged to

take advantage of this provision.

5. FINANCIAL BENEFITS

There are many ways in which a merger can result into financial synergy and

benefits. A merger may help in -

Eliminating the financial constraint;

Deploying surplus cash;

Enhancing debt capacity;

Lowering the financial costs.

22

6. OVERCOME FINANCIAL CONSTRAINTS

A company may be constrained to grow through internal development due to

shortage of funds. The company can grow externally by acquiring another

company by the exchange of shares and thus, realize the financing constraint.

7. SURPLUS CASH

A Cash rich company may face a different situation. It may not have enough

internal opportunities to invest its surplus cash. It may either distribute its surplus

cash to its share holders or use it to acquire some other company. The share

holders may both really benefit much if surplus cash is returned to them since

they would have to pay tax at ordinary income tax rate. Their wealth may

increase through an increase in the market value of their shares if surplus cash is

used to acquire another company. If they sell their shares, they would pay tax at

a lower, capital gains tax rate. The company would also be enabled to keep

surplus funds and grow through acquisition

8. DEBT CAPACITY

A merger of two companies, with fluctuating, but negatively correlated, cash

flows can bring stability of cash flows of the combined company. The stability of

cash flow s reduce the risk of insolvency and enhances the capacity of the new

entity to service a larger amount of debt. The increased borrowing allows a

higher interest tax shield, which adds to the shareholders wealth.

4.3 URGE TO MERGE & ACQUIRE

23

Following are the apparent reasons why companies are attracted towards

merging & acquiring -

1. BIG IS BEAUTIFUL

From sugar to cement, white goods to pharmaceuticals, the compulsions for

consolidation i.e. to merge & acquire is increasing by the day. And due to the

strict patent regime looming, companies need the critical mass to be able to set-

up research.

Instances -

Consider Pharmaceuticals - 20,000 units with even the market leader having only

a 5% market share.

The Indian Cement Sector comprises hundreds of units. The top 20 players

control 80% in Southeast Asia. Cement prices are dropping fast and the only way

to grow is to get better and faster efficiencies of production and distribution.

2. DESPERATE SELLERS

Even elite business groups are today desperate to sell off non-core businesses

as profitability & margins are under squeeze in every industry.

Instances -

Tatas exited cosmetics & pharmaceuticals in a fortnight. Raymonds sold off its

steel division to Thyssen of Germany. Voltas is shifting focus from white goods to

engineering & air-conditioning. Indian promoters grew big by gorging on licences,

cheap loans & diversifying madly. They promoted their children as heirs

irrespective of talent. Now many of them have neither the capital, technology nor

24

managerial skills to cope with the new competitive reality. The downturn is

forcing them to sell peripheral business to raise cash for focus areas.

3. EAGER BUYERS

The concept of replacement cost is fast taking root in the Indian pysche.

Companies are realizing that it is far cheaper to expand by acquiring other

companies in a downturn than by setting up Greenfield projects. Thus any

company with margins superior to the sector average and able to withstand the

recessionary trend is looking for expansion through mergers & acquisitions.

Instances -

Cement industry- a greenfield project of million tonnes would cost Rs.400 crores

whereas companies with the same capacity can be bought out for Rs.150-200

crores. So it makes sense for Indian Cements to catapult itself to second largest

cement company status by trying to buy other low key players in the same

sector.

4. FRESH THINKING

The present day business tycoons realized that being sentimentally attached to

their business does not pay off in the corporate jungle and so, they don't mind

acquiring or merging.

Instances -

"I am not emotional about any business" says Ajay Piramal, who has built a huge

pharmaceutical business primarily through acquisition.

25

"It has been a long and highly satisfactorily association…but there is no place for

sentimentality since shareholder's interests are paramount to one's feelings."

said Simone Tata last month as she bid adieu to Lakme.

Now many a new boss like Kumarmangalam Birla is looking to the overseas

acquisition route to grow.

5. TRANSPARENT LAW

Adding to all this is the great facilitator- the takeover code. Now anyone is free to

buy up to 10% of a company's paid up capital. He must make an open offer for at

least 20% more then & if shareholders bite the bait, the company can't block the

transfer of shares and the predator can force the existing management out.

6. DITHERING FIs

The success of M & A strategies is largely dependent on which way the big five -

UTI, LIC, ICICI, IDBI and IFCI swing in a takeover bid. So far there is little

change in their dithering ways.

Instances -

The Indian Cements Offer -The FIs, as 20% shareholders of Raasi Cements,

have been saying that they would subscribe to the offer, as the price was too

good to be true. But as shareholders of India Cements, they are talking of

blocking the offer, as the price being paid is too high and therefore detrimental

to ICL shareholder's interest. The reasoning is that ICL should have picked up

any other smaller unit for half the price. "It's a classic case of wanting to run with

26

the hare and hunt with the hound and could blow the whole takeover attempt in

ICL's face, says an investment banker.

7. INCREASES THE MARKET SHARE

It helps to eliminate competition and protect the existing market. Thus the market

share can be enhanced.

Instances -

When Coca Cola acquired Parle Products it reduced competition thus increasing

its market share.

8. STRENGTHENS THE MARKET POSITION

It helps to strengthen the market position in the following ways –

By obtaining new market outlets in position of the offeree -

Instances -

When McLeod Russel (India) Ltd. Merged with Eveready Industries India Ltd.,

`McLeod Russel could use Eveready’s five lakh strong direct retail outlets to

market its product.

By controlling patents and copyrights -

Instances -

When pharmaceutical companies like Hoechst, Marion and Russel merged to

form HMR the result was that the patent rights were in control of the single

existing company - the HMR.

27

4.4 DRAWBACKS OF MERGERS AND ACQUISITIONS

Negative Side Of Merger

However mergers and acquisitions are not always successful.

According to Harry Levinson many mergers have been

disappointing with their results and painful to their participants

primarily due to psychological reasons arising out of the neurotic

wish to become big by all means and because of the

condescending attitude of the senior partner towards the junior

organization.

Research studies on the value of mergers have shown that the

growth rate and profitability of the combined organization tend to

decline as competed with the performance of the combining firms.

Executives of the acquired firm often lose their status, authority and even their

jobs. From the social point of view mergers give rise to monopolistic conditions

with increased concentration of economic and political power, higher prices,

restricted supply, and other abuses of monopoly. Some other drawbacks include

–

1. MONOPOLY

All mergers decrease competition. The resulting oligopoly and monopoly can

lower output and raise prices. While monopolies give rise to economies of scale,

the lower output reduces economic efficiency.

Those who framed India’s industrial policy took the view that the net effect of this

would be a loss in social welfare. For this reason the MRTP act of 1969

28

contained a lengthy provision to prevent monopolies and by extension, mergers

from coming into being.

Instances -

Recently there were rumours, that with a large market share assured, Brooke

Bond was dumping low quality tea. This was the consequence of monopoly

power, which was clearly overlooked by the MRTPA amendments. In the soft

drinks market, when Coca-Cola acquired Parle products thus becoming the

monopolist of the market, it increased the prices of the soft drinks in a short span

of time.

Take the examples of Hindustan Lever and TOMCO merger, the takeover of

Damania airways by NEPC Airlines, the acquisition of mosquito repellent

products like Goodnight, etc. by the Godrej Group, the recently announced joint

venture between HLL and Lakme, the acquisition spree of the HLL group in ice-

creams (Dollops, Kwality,..), etc. In most of these & many other cases, it is

apparent that large market shares have now been concentrated in the hands of a

single company / group. Questions arise as to the monopolistic practices, which

could arise as a result. It also necessary to consider whether such an extent of

total decontrol is desirable.

2. NO EARNINGS ENHANCEMENT

The factors which drove corporate interest in buying up other firms was none

other than low capital costs, strong cash flows and robust balance sheets in a

29

low interest rate environment. Unfortunately the cost of financing an acquisition is

neither low in this country nor have the managers been able to produce

something that is earnings enhancing.

3. CULTURE CONFLICT

Cultural integration is a much-misunderstood term. In a majority of companies’

culture tend to be viewed as a single, overarching and immutable entity –

corporate culture. Even in the biggest corporations of the world, it is impossible to

say that there is only one corporate culture.

Instance -

IBM tried for years to impose its Big Blue culture on its employees. But people

from the same technical background, educational system and social background

doing the same type of job, were doing things differently. Especially, when they

were from different nationalities. Thus the employees of the smaller organisation

are frustrated, as they have to adapt to the alien culture of the dominant

organisation.

Most management in India particularly the more traditional baggage-laden

organisations, simply ignore this problem till it is too late.

4. INVOLVES LARGE TRANSACTION COST

30

Large transactional costs are involved in hostile takeovers-resources that are

spent by the Target Company in fending off the bid and by the acquirer too in

pushing through its strategy.

5. TRADE UNION PROBLEMS

One of the major problems in mergers and acquisitions faced by companies is

that when they try to reduce the work force, the trade union of all the involved

companies oppose.

Instance -

Trade Union filed a case against HMR on technical grounds.

CHAPTER 5

5.1 GUIDELINES FOR EFFECTIVE MERGERS

Mergers and acquisitions involve a complex set of decisions to be made as

regards financial arrangements, organizational changes and adjustments of

different kinds. On the basis of his own experience with mergers, an American

executive has suggested the following guidelines for carrying through the

process of merger or acquisition effectively -

1. Specify clearly the merger objectives, especially earnings objectives;

2. Work out and specify the gains of shareholders of both the combining

units;

31

3. Be sure that the management of the acquired company is or can be made

competent;

4. Note the existence of important dovetailing resources but do not expect

perfect compatibility;

5. Initiate the process of merger with active involvement of the chief executive;

6. Clearly define the business that the company is in;

7. Identify and check on the strengths, weaknesses and key performance

factors for both the combining units;

8. Anticipate problems and discuss them early with the other company so as to

create a climate of trust;

9. Be sure that the merger does not pose a threat to the present management

team;

10. People should be of prime consideration in planning for merger and

structuring the organization.

5.2 LEGAL & PROCEDURAL ASPECT OF MERGER

The procedure of amalgamation or merger is long-drawn and involves some

important legal dimensions. Following steps are taken into procedure -

1. Analysis of proposal by the companies -

Whenever the proposal of amalgamation or merger comes up the

management of the concern companies looks in pros and cons of the

scheme. The likely benefits such as economies of scale, operational

economies, improvement in efficiency, reduction in costs, benefits of mergers

32

etc are clearly evaluated. The likely reactions of shareholders, creditors and

others are also assessed. The taxation implication is also studied. After going

through whole analysis work, it is seen the whole scheme s beneficial or not.

It is perused further only if it will benefit the interested parties otherwise the

scheme is shelved.

2. Determining exchange ratio -

The amalgamation or merger schemes involve exchange of shares. The

shareholders of amalgamated companies are given shares of amalgamated

companies. It is very important that the rational ratio of exchange of share

should be decided. Normally a number of factors like book value per share,

potential earnings, value of assets are taken over are considered for

determining exchange ratios.

3. Approval of board of directors -

After discussing amalgamation scheme throughly and negotiating the

exchange ratio, it is put before the respective board of directors for approval

4. Approval of shareholder –

After the approval of scheme by the respected BOD, it must be put before

the shareholders. According to section 391 of Indian Companies Act, the

amalgamation scheme should be approved at the meeting of the members or

class of the members, as the case may be, of the respected companies

33

representing three-fourth of value and majority of numbers, whether present

in person or by proxies. In case the scheme involves the exchange of shares

it is necessary that is approved by not less than 90% of the share holders (in

value) of the transferor company to deal effective with the dissenting

shareholder.

5. Consideration of the interest of the creditors –

The views of creditors should also be taken into consideration. According to

section 391, amalgamation scheme should be approved by majority of

creditors in numbers and value.

6. Approval of the court -

After getting the scheme approved, an application of scheme should be filed in

the court for its sanction. The court will consider the viewpoints of all parties

appearing, it any, before it, before giving its consent. It will see that the interest

of all parties are protected amalgamation scheme and pass orders accordingly.

However, it is up to shareholder, whether to accept the modified scheme or not.

It may be noted that no scheme of amalgamation can go through unless the

registrar of companies send the report to court to the effect that the affairs of

the company have not been conducted as to be prejudicial to the interest of its

members or to the public interest.

7. Clearance under MRTP Act –

34

Every scheme of amalgamation or merger requires the court government

under MRTP Act. The idea behind is that to see that it does not result in control,

ownership & management of important undertakings into a few hands, which is

not likely to be in public interest. The government does not allow any scheme of

amalgamation or merger leading to concentration of economic power.

CHAPTER 6

6.1 A CASE STUDY ON THE MERGER OF HLL AND PONDS

It was found that the proposed merger would not be a surprise to the Indian

stock market because it’s only a consolidation by a parent company. ‘If one

examines the history of Unilever, Hindustan Lever and Pond’s (India)

Limited, one would find an important role of mergers, acquisition and

corporate restructuring in their growth.’

35

6.1.1 MERGERS, ACQUISITION AND CORPORATE RESTRUCTURING IN

HISTORY OF UNILEVER

UNILEVER ROOTS

Few would have thought that the merger of two companies in 1929 would

develop into one of the world’s most progressive, fast-moving, consumer goods

businesses but that is what Unilever is today. But Unilever’s origins stretch

backs much further than 1929 when the Company was formed. Other

entrepreneurs whose businesses have become part of Unilever have helped the

business to grow and prosper.

LEVER BROTHERS

William Hesketh Lever, later Lord Leverhulme, founded Lever Brothers in 1885

after working in his father’s wholesale grocery business. He introduced Sunlight,

the world’s first packaged, branded laundry soap, backing it with a large-scale

advertising campaign. He soon established soap factories in Europe, North

America, Australia and the Far East, and oil mills at Port Sunlight in the UK and

Balmain, Sydney in Australia. After 1917 he moved into the food trade, acquiring

fish shops, as well as canned foods, meat and ice cream businesses. Port

Sunlight is the site of William Lever’s factory in the UK and houses a thriving

detergents plant and research laboratory. Here too is the model village, which

William Lever began to build for his workforce and their families in 1888. He

provided them with decent affordable housing and pioneered welfare schemes,

36

recreational facilities and many other benefits. The houses in this attractive

village, complete with its own church, hotel and school, are now sold on the open

market. But the village stands as a monument to its founder’s philanthropic

principles.

UNILEVER WAS CREATED IN 1929 WHEN MARGARINE UNIE

MERGED WITH LEVER BROTHERS LIMITED.

The Dutch established the first margarine factories in the 1870s and 1880s,

although margarine was invented in France. In 1872 both Jurgens and Van den

Bergh began commercial production of margarine, which came to be known as

Margarine Unie.

Both Margarine Unie and Lever were in the business of supplying goods for

household needs but were competing for supplies of oils and fats. The merger

made sound commercial sense. Margarine Unie’s strengths were in mainland

Europe, while Lever Brothers were market leaders in the United Kingdom. At the

time of its creation, Unilever already had an international presence - William

Lever had plantations and trading activities in Africa and there were also

business operations in the US and Asia.

FAMOUS FOUNDERS

Here is the brief about the founder of various businesses who had started their

business in 18th century and prospered. They had come under the umbrella of

Unilever afterwards.

37

Clarence Birdseye 1886-1956

Clarence Birdseye changed the eating habits of millions and founded a new

industry in frozen foods. Inspired by the fresh taste of frozen fish when he worked

in the Arctic north of Canada, he developed the technology to quick-freeze food

on a commercial scale. The business made great progress in the 1930s and

in 1943 Unilever obtained the right to manufacture and sell frozen foods

under the Birds Eye name in the UK.

Thomas J Lipton 1850-1930

After a spell working in the US, Thomas Lipton opened his first provisions store in

his hometown of Glasgow, Scotland at the age of 21. The number of stores

expanded and he began to buy tea direct to get cheaper and better-flavored pre-

packed teas. In 1890 he bought his first tea plantations in Ceylon (now Sri

Lanka). In 1898 Queen Victoria knighted him. His company became

associated with Unilever in the 1920s.

Arthur Brooke 1845-1918

Taking over his father’s small tea wholesale business in the north of England,

Arthur Brooke opened his own shops under the Brooke Bond name and became

part of Unilever. In the 1880s Arthur Brooke began to sell tea wholesale and

a century later, when Unilever acquired the company in 1984, it was

employing 76,000 people and operating on all continents.

38

Chesebrough and Pond’s

Robert Augustus Chesebrough was a New York chemist who in the 1860s

developed the first petroleum jelly that was pure, colourless, odourless and safe.

He called it Vaseline. In 1955 the company merged with the Pond’s Extract

Company founded by Thereon Pond to create Chesebrough Pond’s Inc,

USA. His first success was Pond’s Extract, using the healing powers of the

hamemelis tree. The introduction of Pond’s Vanishing Cream and Cold Cream in

the early 1900s provided the first mass-produced, low-cost beauty and skincare

products. Unilever acquired this company in 1986.

Schicht

Bohemia, in central Europe, was the home of the Schicht family, founders of a

soap business that prospered during the latter half of the 19th century under the

watchful eye of Johann Schicht. He was a pioneer of branding and an

enlightened employer. Trading problems and an acute shortage of raw

materials and able-bodied staff during the First World War, combined with

the subsequent loss of sales territory, led the company to enter into an

agreement with Jurgens and Van den Bergh’s. In 1929 the company

merged with Margarine Union, shortly before Unilever was formed.

6.1.2 UNILEVER HISTORY AFTER ITS CREATION IN 1929

1930 GREAT DEPRESSION

39

The economic slump of the 1930s affected every aspect of the operation from the

manufacturing of detergents, personal products, edible fats and foods, to the

buying and processing of more than a third of the world’s commercial oils and

fats.

Despite the severe downturn, Unilever prospered. Branded products offering

added variety and quality were skillfully marketed. Margarine, toilet soaps and

foods such as sausages, pies and ice cream were sold.

At this time a new form of leadership was created. A Special Committee or

‘inner cabinet’ was formed, consisting of three directors, usually the

chairmen of the two parent companies and a vice-chairman. This ‘inner

cabinet’, which defined broad policies and gave strategic direction,

remained an important part of Unilever’s organizations for the next 65

years.

SECOND WORLD WAR

The Second World War interrupted the natural development of the company, as

many manufacturing operations were diverted to the war effort. The Company

helped produce tank periscopes and packs of soldiers’ rations. By 1945 a

number of Unilever’s businesses in Central and Eastern Europe and in Asia

had been cut off and remained in isolation for many years.

NEW PRODUCTS NEW MARKETS

40

In 1930 soap and edible fats had accounted for 90 per cent of Unilever’s profits.

By 1980 they contributed no more than 40 per cent. But sales of frozen foods, ice

cream, packaged soup; tea and personal products had all increased significantly.

The geographical emphasis was changing as well. In 1930 only 20 per cent of

net profit came from outside Europe. Fifty years later this had doubled to 40 per

cent, mainly through expansion in South America, Africa and Asia. In the 1980s

Unilever undertook a massive restructuring program. A decision was made to

concentrate on core businesses, those in which it had a critical mass and a

promising future. Detergents, foods, toiletries, specialty chemicals and

agribusiness were selected.

CONCENTRATING ON CORE BUSINESSES

Restructuring was costly but it improved profitability. By 1986 the company had

sold most of its service and ancillary businesses. At the beginning of the 1990s

Unilever pruned down its core businesses still further. The packaging

companies and the major part of its agribusiness interests were sold,

leaving four core product groups – home, personal care, foods, and specialty

chemicals - which by 1991 accounted for 96 per cent of sales.

The Company also embarked on an aggressive acquisition program. Between

1984 and 1988, around 80 companies were bought up. Valuable new prizes were

secured: the Brooke Bond Group in 1984 and Chesebrough-Pond’s in the US in

1987.

41

Unilever was strengthening its position in personal products around the world.

After the acquisition of Chesebrough-Pond’s, Unilever acquired the

Faberge/Elizabeth Arden and Calvin Klein fragrance businesses in the late

1980s. It now had a firm base in the prestige sectors where margins and growth

rates were attractive.

Unilever has maintained a presence in almost every region of the world over the

years, through local companies or export operations. It is investing an increasing

proportion of its resources in emerging economies. In 1996, 27 per cent of total

Unilever investments were made in emerging markets.

1996 A NEW STRUCTURE FOR UNILEVER

In 1996 Unilever changed the organisation of its top management for the first

time since the Company was formed. Under the new structure, the chairmen of

Unilever PLC and Unilever NV, together with directors responsible for Foods,

Home & Personal Care, Finance, Personnel and Strategy & Technology form an

Executive Committee or ExCo. On behalf of the Company’s various boards, Ex

Co is responsible for taking key decisions and planning long-term strategy.

Twelve business group presidents have operational responsibility for

implementing this strategy throughout the business.

The two category directors for Foods and HPC provide central resources and

strategic direction for the corporate categories.

42

Acquisition plays a continuing role. Over 100 purchases were made between

1992 and 1997, including Helene Curtis (hair care) and Diversey (industrial

cleaning) in 1996 and Kibon (ice cream) in 1997.Unilever is expanding further

throughout the world. In doing so, it faces tough competition. But with its

understanding of the consumer, its technical expertise and its strong brands, it is

well placed to meet the opportunities and challenges of the 21st century.

UNILEVER IN INDIA

In 1888, less than four years after William Hesketh Lever launched Sunlight Soap

in England, his newly founded company, Lever Brothers, started exporting the

revolutionary laundry soap to India.

By the time the company merged with the Netherlands-based Margarine Unie in

1930 to form Unilever, it had already carved a niche for itself in the Indian

market. Coincidentally, Margarine Unie also had a strong presence in India, to

which it exported Vanaspati (hydrogenated edible fat).

A year after the merger, Unilever set up the Hindustan Vanaspati Manufacturing

Company, its first subsidiary in India and went on to strengthen its position by

establishing two more subsidiaries, Lever Brothers India Limited and United

Traders Limited, soon afterwards. The three companies, which marketed Soaps,

Vanaspati and Personal Products, merged in 1956 to form Hindustan Lever, in

which Unilever has a 51% stake.

6.1.3 HISTORY OF HLL

43

1888 - Lever soap, ‘Sunlight’, introduced in India through Imports

1918 - Vanaspati (hydrogenated edible fat) launched through imports

1930 -Unilever created through the merger of Lever Brothers, UK, and Margarine

Unie, Netherlands

1931 - Unilever registers company in India: Hindustan Vanaspati Manufacturing

Company (HVM) for local manufacture of Vanaspati.

1933 - Lever Brothers India Limited (LBIL) incorporated in India to manufacture

Soaps.

1935 - United Traders Limited (UTL) incorporated in India to market Personal

Products.

1956 - The three subsidiaries, HVM, LBIL and UTL, merge to form Hindustan

Lever Limited (HLL)

1958 - Hindustan Lever Research Center starts functioning

1979 - Chemicals complex commissioned at Haldia, West Bengal.

1993 - HLL’s largest competitor, Tata Oil Mills Company (TOMCO) merges with

the company

Erstwhile Brooke Bond India acquires Kissan Business from the UB

Group and Dollops ice-cream business from Cadbury. Doom Dooma

44

and Tea Estates Plantation divisions merged with Brooke Bond -

Brooke Bond and erstwhile Lipton India merge to form Brooke Bond

Lipton India Limited

1994 - HLL and US-based Kimberley-Clark Corporation form 50:50 joint venture,

Kimberley-Clark Lever Ltd.

1995 -HLL and Indian cosmetics major, Lakme Ltd, form 50:50 joint venture,

Lakme Lever Ltd.

HLL acquires Quality and Milkfood 100% brand names and

distribution assets.

HLL and US-based S.C. Johnson & Son Inc. form 50:50 joint venture,

Lever Johnson (Consumer Products) Pvt. Ltd.

1996 -HLL and Associate Company, Brooke Bond Lipton India Limited, India’s

biggest in Food and Beverages, merge.

1997 - HLL and Gist Brocades BV form 50:50 joint venture, Lever Gist Brocades,

to market ‘Gold Seal Fermipan Instant Yeast’ for baking industry.

1998 - Group Company, Pond’s India Ltd., merges with HLL.

HLL acquires Lakme brand, factories and Lakme Ltd’s 50% equity in

Lakme Lever Ltd. HLL acquires manufacturing rights of Kwality ice cream.

6.1.4 HLL BUSINESSES

45

HLL’s core business comprises of soaps (18%), detergents (16%), personal

products (19%), Tea (16%), coffee (2%), Oils, vanaspati and dairy products (6%),

branded staples (2%), Ice-cream (1%), culinary products (1%). Animal Feed,

specialty chemicals and other small businesses contribute to the balance 18% of

HLL’s turnover.

6.1.5 PONDS INC

Chesebrough - Pond's Inc, USA, manufacturer of cosmetics and toiletry products,

set up an Indian branch in 1947 in Bombay. The first plant was set up at

Bangalore in 1956. In 1968 all operations were integrated and shifted to Madras.

In May 1977, an Indian company Pond's (India) Pvt. Ltd. was incorporated

to take over the cosmetics and toiletries business of the Indian branch of

Chesebrough-Pond's to comply with the provisions of FERA.

In July 1978 the company became a public limited company following a public

issue, also thereby reducing foreign equity holding in the company to 40%. A

new manufacturing unit was set up at Tindivanam (T.N.) in 1981. Plants were put

up at Pondicherry(T.N.) for soaps and shoe uppers.

During 1983-84 the undertakings at Kodaikanal and Kandla of Pond's Exports

were taken over by the company. In 1982 the first joint venture with Sri Lanka

was signed. In 1983 a 100% EOU to manufacture clinical thermometers was set

up in Kodaikanal (T.N.). The R & D center in Madras came up in 1982. The

company diversified into processing and canning mushrooms and commissioned

46

a 100% EOU in Nilgiris in 1991. During 1986 Pond's introduced its own

toothpaste and tooth brushes, manufactured by International Dental Care

Products and marketed by Pond's.

In December 1986 Unilever acquired Chesebrough Pond's Inc. and with this

Pond's (India) came under Unilever fold. Quest International India Ltd. (with

Unilever holding 73% and Pond's and Hindustan Lever holding 27% in the

company) was merged with Pond's (India) from November 1993. After the

amalgamation Unilever’s stake in Pond's went up from 40% to 52.5% and

Pond’s (India) became subsidiary of Unilever.

6.2 THE HLL - PONDS POST MERGER SCENARIO

The two companies had significant overlaps in Personal Products, Speciality

Chemicals and Exports businesses, besides a common distribution system since

1993 for Personal Products. The two also had a common management pool and

a technology base. The amalgamation was done to ensure for the Group benefits

from scale economies both in domestic and export markets and enable it to fund

investments required for aggressively building new categories, such as

deodorants and other Personal Products.

(For more detail please, refer Annexure A & B)

SEGMENT WISE SALES OF PRODUCTS

47

Soaps, Detergent & Household Care

Personal Products

Foods

Chemicals Agriculture fertilizers & Animal feed

Others

It is observed that, compared to yr 1997 there is increase in personal care

product sales in the yr 1998 by 10 % indicated by color yellow, which is the effect

of merger. From 1994 to 1997 total % of sales of personal care products were 10

% but after merger it got increased by 10 % and so this sales has become 20 %

of the total product profile.

TOTAL NET SALES

48

This graph clearly indicates that there is a growth in the total net sales, going in

an upward direction from 1998 (i.e. after merger) indicating that this merger has

also become fruitful for HLL.

ASSETS TURNOVER

49

After merger working capital T/O ratio suddenly increased. This fact can be seen

from above graph that, from 1997 there was down ward slope of graph and

suddenly after merger in 1998 it get raised. In 1995 after the merger of Lakme

India with HLL, working Capital Turnover get pulled upward and in 1997 it again

reduce down but this ponds merger pulls up this Working Capital turnover

drastically.

CHAPTER 7

7.1 CONCLUSION

50

The magic of economic liberalization worked wonderfully with its positive impact

on the economy till 1995 - 96. The Indian economy has been having a testing

time since the middle of 1996. The performance of some major industries has not

been encouraging, but the software, plantation, pharmaceutical and select

chemical industries have acquitted themselves well. Worldwide recession and

slowdown in world trade also contributed to the problems. Therefore mergers and

acquisitions are going to play an important role not only in India but also

everywhere in the world.

Many companies are realizing at an increasing speed the need to merge and

grow big .The small ones are being swallowed by the bigger ones and they in

turn are being gulped by the still bigger ones. Above study reviews one important

derivation – Merger & Acquisition has given special boost to the overall progress

of both – HLL & Ponds (I) Limited -surpassing their previous individual turnover

marks. Graphically it also indicates their substantial growth in earnings and

dividend per share, sales figures and assets turnover ratio.

From 1992, Hindustan Lever Limited has been adopting a strategy of growth

through the mergers & acquisition route. This strategic direction is highly

influenced by its parent company, which is also pursuing the same strategy.

Between 1992 and 1997, HLL adopted a strategy of growth by acquisition. Over

this period of five years, net sales grew 4.5 times Rs 7737 crore. Gross fixed

assets rose 3 times to Rs 1035 crore and more significantly, net profit (net of

non-recurring transactions) grew 5.9 times to Rs 573 crore.

51

Herewith I conclude that the merger between HLL & Ponds (I) Limited is

successful and also mutually beneficial in the long term. This can be an ideal

example & milestone in the history of Indian business.

So next time when you think to merge with any company first, determine if a

merger or acquisition is necessary. This is the most important step, as a poorly

handled merger or acquisition can damage even a strong firm. Could your need

for employees be solved in another way? For instance, if you would like to

increase your presence in the market, you could hire a marketing contact or a

small team to work in that specific area. If this would not be enough, you may

want to consider an acquisition or merger. If you have experienced a merger or

acquisition before, this is the time to assess how it went last time, whether it

helped your firm, and how you feel it could help your current situation.

Take your time and determine whether a merger or acquisition will really help

your current situation or simply exacerbate existing problems.

BIBLIOGRAPHY

BOOKS

1. Financial management – I M Pande

Page No.1098 – 1105

2. Strategic Planning & management – P. K. Ghosh

52

Page No.234- 241

3. Strategic planning - Formulation of corporate strategy

V. S. Ramaswamy & S. Namkumari.

Page No- 367- 410

ARTICLES / NEWS PAPERS

1. ‘ Altogether now ’ - The Telegraph (Calcutta), May 10 1996

- Kaustubh Ghosh

2. A disaster called merger ’ -The Economic Times, January 17 1998

- Rajiv Handa

3. ‘ The cultural cauldron ’ - Business Standard, March 17 1998

- Indrajeet Gupta

4. ‘ Wrong Priorities ’ -The Economic Times, April 4 1998

- Ram Manohar Reddy

5. ‘ The urge to merge ’ -Outlook, April 6, 1998 – Neeraj Jetley

6. ‘ McLeod merges, Eveready emerges ’ - Calcutta Bureau, Sep 24 1998

7. ‘ Lakme, HLL launch 50:50 marketing venture ’ -The ET, Nov 13

8. ‘ Motives behind mergers ’ -The ET, April 28

53

9. ‘ Mergers are a good alternative ’ – Rashid J

WEBSITES

1. www.hll.com

2. www.corporateinformation.com

3. www.indiainfoline.com

4. www.indiainformer.com

5. www.khoj.com

54

Graph A

Earnings per share Vs dividend per shares

From 1998 slope of EPS suddenly gets raised.Accordingly DPS also got an uplift.

In 1997 – Rs. 28.14 and in 1998- Rs. 36.70

Graph B

Profit after tax in %

In 1997 it was7.42% in 1998 it got raised by 8.83 & in 1999 it got uplifted up to 10.55 %

Graph CReturn on capital employed (%)Return on net worth (%) In 1998 return on capital employed is increased up to 61.84 which was in previous yr at 58.65

Graph DInterest covered in 1997 26.09 times In 1998 it was 39.61 timesIn 1999 it was 63.00 times

55

Annexure B

Tables –

Table1: Audited results

Audited Results for 1998 Rs. Crores

1998 1997

Gross Turnover (including excise) 10215.2

4

8342.75

Turnover (net of Excise) 9481.85 7819.71

Profit Before Tax, before exceptional items 1130.44 850.25

Profit After Tax, before exceptional items 837.44 580.25

Net Profit, after exceptional items 805.71 560.37

Earnings Per Share (EPS) Rs.36.70 Rs.28.14

56

Table 2:

Category

Wise

Turnover

Rs. Crores

Category1998 1997

Soaps & Detergents 3565 3360

Personal Products 1526 884

Beverages 1799 1544

Processed triglycerides, Oils &

Vanaspati

653 542

Dairy Products 79 87

Ice Cream & Frozen Desserts 155 153

Canned & Processed Fruits &

Vegetables

119 97

Branded Staple Foods 160 112

Speciality Chemicals 227 156

Animal Feeding Stuffs 278 272

Others 921 613

Total 9,482 7,820

57

58