Embed Size (px)

Citation preview

1

2

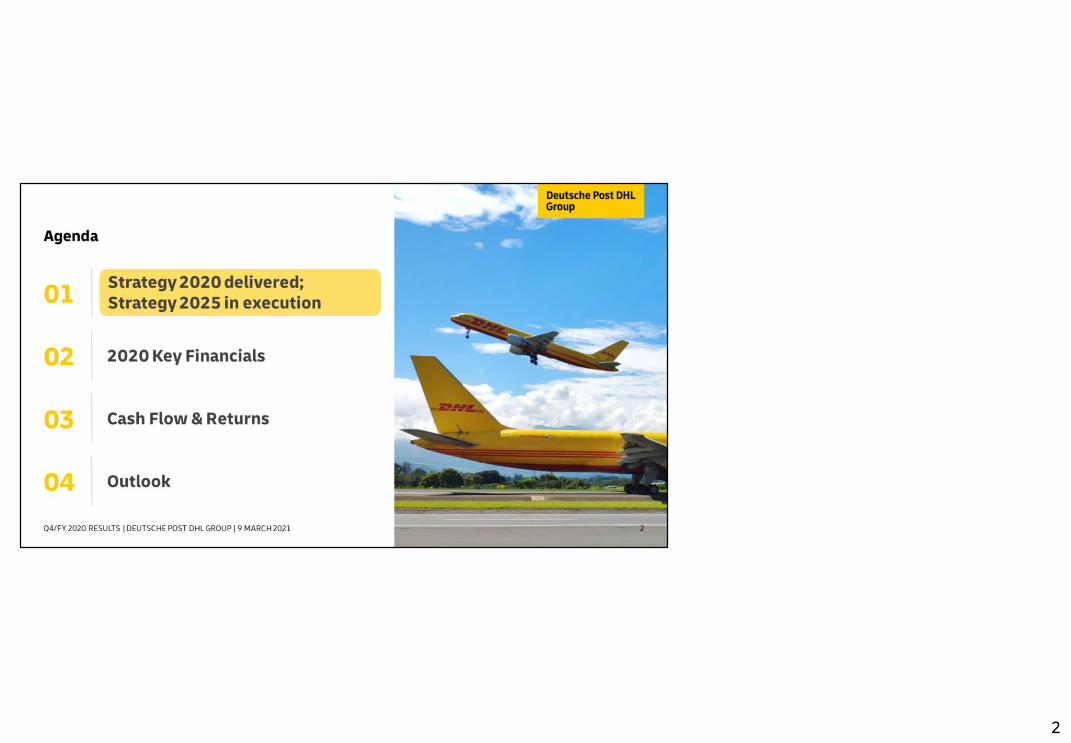

Management Comments:2020 was an exceptional year with unseen circumstances.For DPDHL, 2020 also marks the completion of ourStrategy 2020, introduced in 2014. This strategic journeyhas tackled internal and external challenges over theseyears. Based on our long standing purpose “ConnectingPeople. Improving Lives“, as well as our clear mission andbottom lines, Strategy 2020 has delivered - in terms offinancial results, as well as in regards to making DPDHLtoday a different and better company.

In terms of financial performance, the reported €4.8bnEBIT for 2020 delivers on our targeted 8% CAGR over theperiod. Excl. 2020 one-offs, e.g. €163m bonus paid to allDPDHL employees for their outstanding 2020 efforts,EBIT was above €5bn, with a fully adjusted EBIT of€5.4bn.

What is even more important is that these achievementsset a strong base for further profitable growth as shownwith our new mid-term guidance for EBIT growth out to2023. As detailled later (p. 10), the four identified keylong-term strategic trends remain fully valid and are atthe core of our strategic actions – also for the now up andrunning Strategy 2025.

The success of Strategy 2020 benefits all DPDHLstakeholders. We created 90,000 jobs over the period andreached record high employee engagement, and thestrong financial performance has been the basis forattractive returns for DPDHL shareholders, see next pagefor details.

3

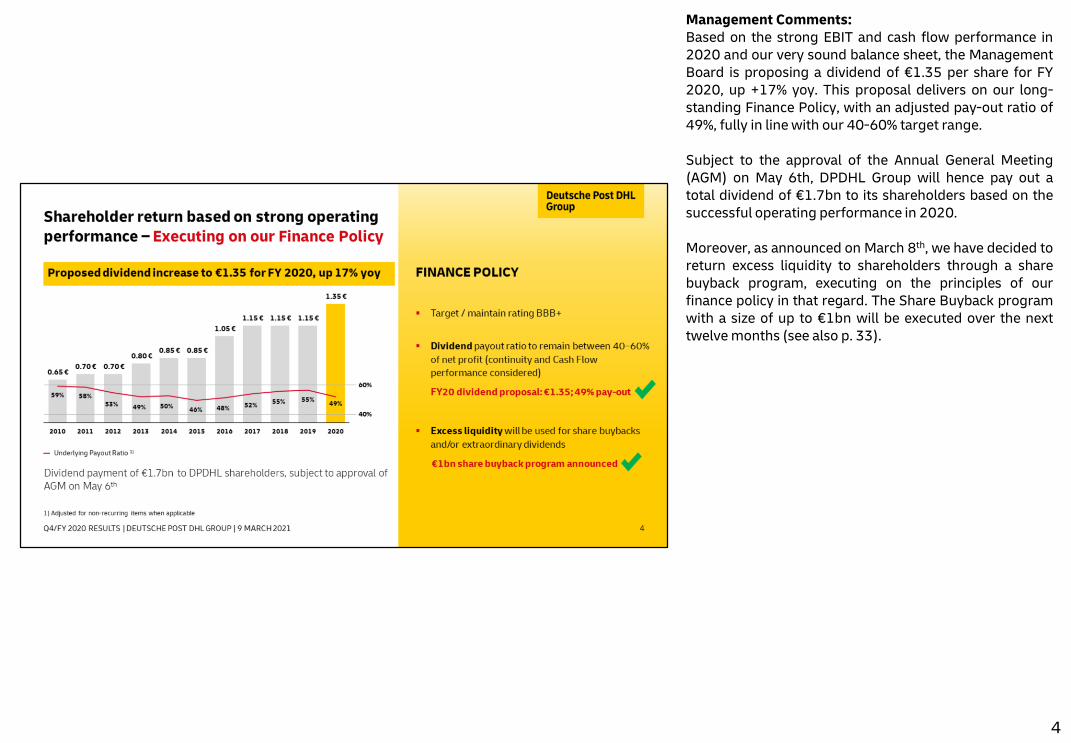

Management Comments:Based on the strong EBIT and cash flow performance in2020 and our very sound balance sheet, the ManagementBoard is proposing a dividend of €1.35 per share for FY2020, up +17% yoy. This proposal delivers on our long-standing Finance Policy, with an adjusted pay-out ratio of49%, fully in linewith our 40-60% target range.

Subject to the approval of the Annual General Meeting(AGM) on May 6th, DPDHL Group will hence pay out atotal dividend of €1.7bn to its shareholders based on thesuccessful operating performance in 2020.

Moreover, as announced on March 8th, we have decided toreturn excess liquidity to shareholders through a sharebuyback program, executing on the principles of ourfinance policy in that regard. The Share Buyback programwith a size of up to €1bn will be executed over the nexttwelvemonths (see also p. 33).

4

Management Comments:The next pages provide a short financial recap of ourStrategy 2020 journey, and – more importantly – showhow these achievements and the strategic focus on theright long-term topics also form the basis for furthersignificant progress targeted under Strategy 2025.

As a summary of Strategy 2020 communication to theCapital Markets:• Launch of Strategy 2020 at our Capital Markets Day in

April 2014• In addition to ongoing updates in our regular quartertly

reporting, Half-Time Report on Strategy 2020 in May2017

• Launch of Strategy 2025 at our Capital Markets Day inOctober 2019

5

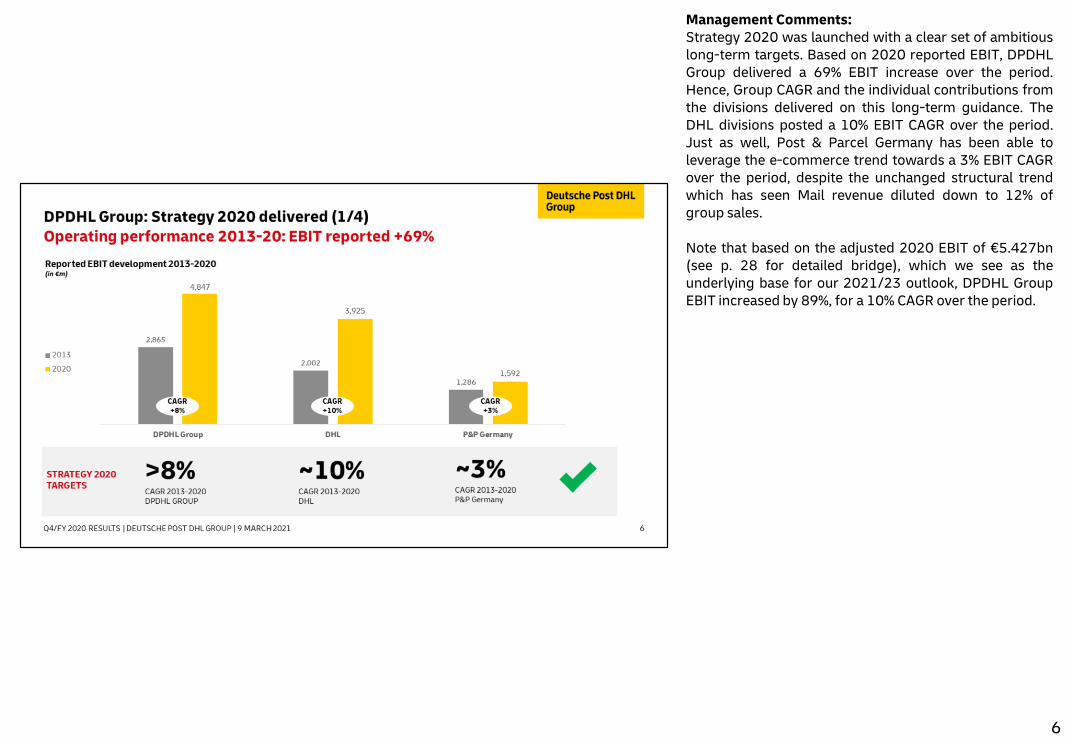

Management Comments:Strategy 2020 was launched with a clear set of ambitiouslong-term targets. Based on 2020 reported EBIT, DPDHLGroup delivered a 69% EBIT increase over the period.Hence, Group CAGR and the individual contributions fromthe divisions delivered on this long-term guidance. TheDHL divisions posted a 10% EBIT CAGR over the period.Just as well, Post & Parcel Germany has been able toleverage the e-commerce trend towards a 3% EBIT CAGRover the period, despite the unchanged structural trendwhich has seen Mail revenue diluted down to 12% ofgroup sales.

Note that based on the adjusted 2020 EBIT of €5.427bn(see p. 28 for detailed bridge), which we see as theunderlying base for our 2021/23 outlook, DPDHL GroupEBIT increased by 89%, for a 10% CAGR over the period.

6

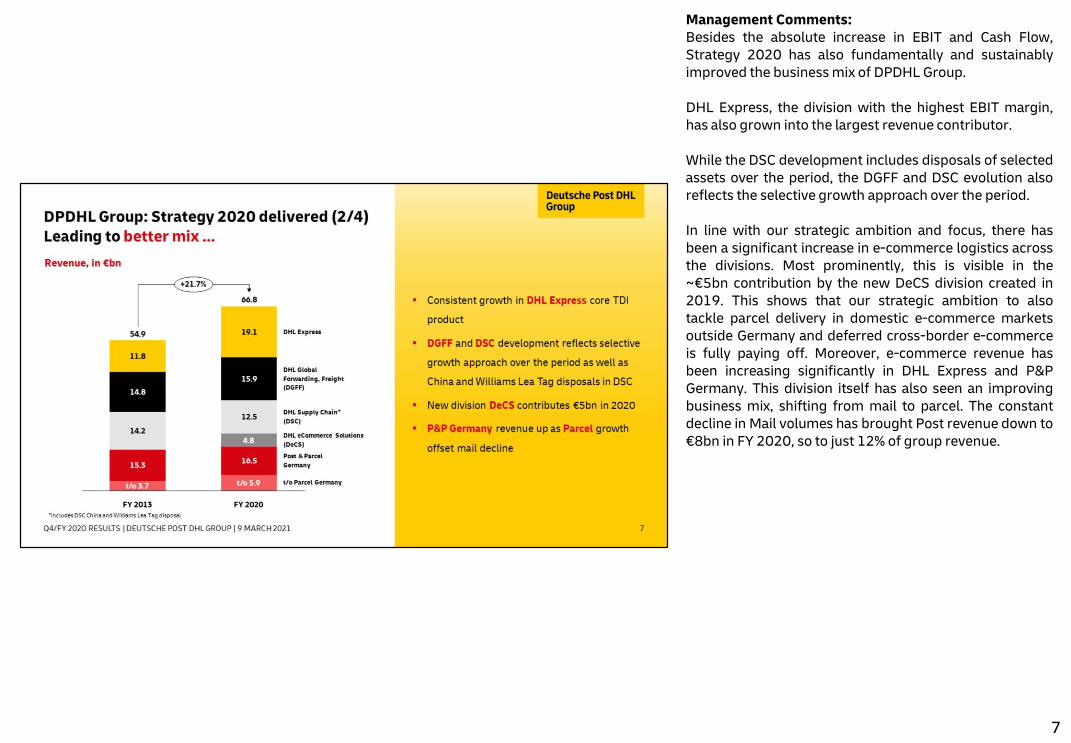

Management Comments:Besides the absolute increase in EBIT and Cash Flow,Strategy 2020 has also fundamentally and sustainablyimproved the businessmix of DPDHL Group.

DHL Express, the division with the highest EBIT margin,has also grown into the largest revenue contributor.

While the DSC development includes disposals of selectedassets over the period, the DGFF and DSC evolution alsoreflects the selective growth approach over the period.

In line with our strategic ambition and focus, there hasbeen a significant increase in e-commerce logistics acrossthe divisions. Most prominently, this is visible in the~€5bn contribution by the new DeCS division created in2019. This shows that our strategic ambition to alsotackle parcel delivery in domestic e-commerce marketsoutside Germany and deferred cross-border e-commerceis fully paying off. Moreover, e-commerce revenue hasbeen increasing significantly in DHL Express and P&PGermany. This division itself has also seen an improvingbusiness mix, shifting from mail to parcel. The constantdecline in Mail volumes has brought Post revenue down to€8bn in FY 2020, so to just 12% of group revenue.

7

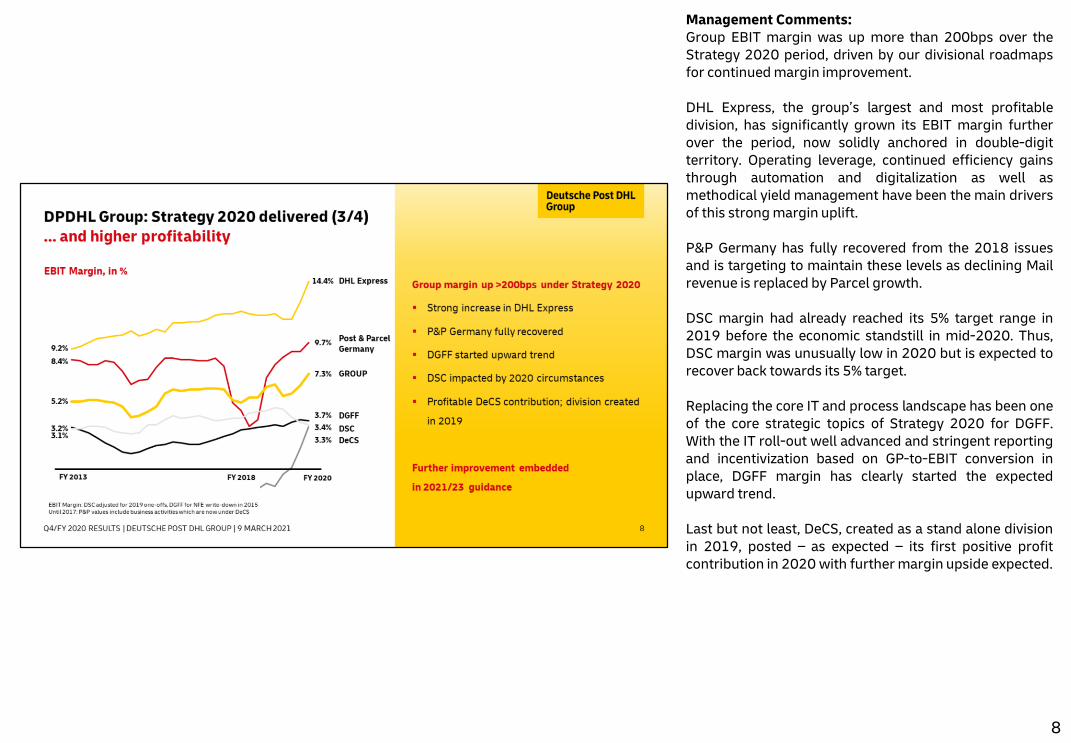

Management Comments:Group EBIT margin was up more than 200bps over theStrategy 2020 period, driven by our divisional roadmapsfor continuedmargin improvement.

DHL Express, the group’s largest and most profitabledivision, has significantly grown its EBIT margin furtherover the period, now solidly anchored in double-digitterritory. Operating leverage, continued efficiency gainsthrough automation and digitalization as well asmethodical yield management have been the main driversof this strongmargin uplift.

P&P Germany has fully recovered from the 2018 issuesand is targeting to maintain these levels as declining Mailrevenue is replaced by Parcel growth.

DSC margin had already reached its 5% target range in2019 before the economic standstill in mid-2020. Thus,DSC margin was unusually low in 2020 but is expected torecover back towards its 5% target.

Replacing the core IT and process landscape has been oneof the core strategic topics of Strategy 2020 for DGFF.With the IT roll-out well advanced and stringent reportingand incentivization based on GP-to-EBIT conversion inplace, DGFF margin has clearly started the expectedupward trend.

Last but not least, DeCS, created as a stand alone divisionin 2019, posted – as expected – its first positive profitcontribution in 2020with furthermargin upside expected.

8

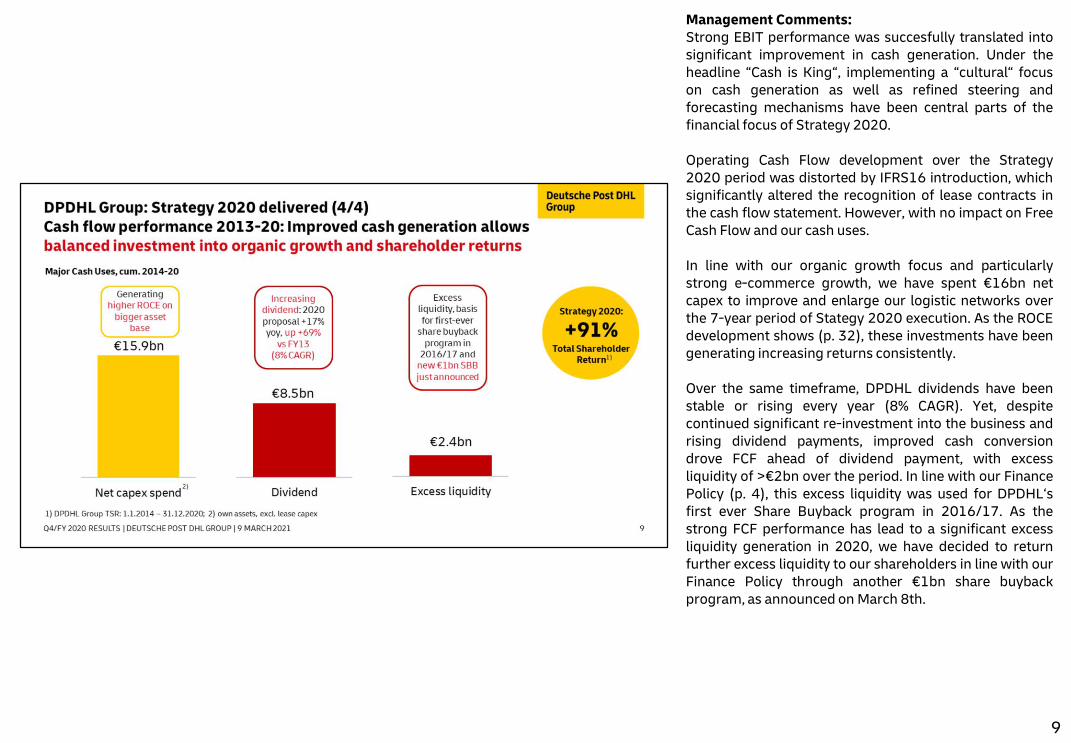

Management Comments:Strong EBIT performance was succesfully translated intosignificant improvement in cash generation. Under theheadline “Cash is King“, implementing a “cultural“ focuson cash generation as well as refined steering andforecasting mechanisms have been central parts of thefinancial focus of Strategy 2020.

Operating Cash Flow development over the Strategy2020 period was distorted by IFRS16 introduction, whichsignificantly altered the recognition of lease contracts inthe cash flow statement. However, with no impact on FreeCash Flow and our cash uses.

In line with our organic growth focus and particularlystrong e-commerce growth, we have spent €16bn netcapex to improve and enlarge our logistic networks overthe 7-year period of Stategy 2020 execution. As the ROCEdevelopment shows (p. 32), these investments have beengenerating increasing returns consistently.

Over the same timeframe, DPDHL dividends have beenstable or rising every year (8% CAGR). Yet, despitecontinued significant re-investment into the business andrising dividend payments, improved cash conversiondrove FCF ahead of dividend payment, with excessliquidity of >€2bn over the period. In line with our FinancePolicy (p. 4), this excess liquidity was used for DPDHL‘sfirst ever Share Buyback program in 2016/17. As thestrong FCF performance has lead to a significant excessliquidity generation in 2020, we have decided to returnfurther excess liquidity to our shareholders in line with ourFinance Policy through another €1bn share buybackprogram, as announced onMarch 8th.

9

Management Comments:Strategy 2020 has been a financial success and deliveredon financial targets. More importantly, Strategy 2020 hascreated a strong basis for future success by focussing thewhole organization on the relevant long-term trends.

One of the key inputs into our new, now up and runningStrategy 2025 has therefore been the confirmation thatthe key four trends are still fully intact and valid.

Therefore, based on Strategy 2020 accomplishments,DPDHL Group will also further improve its contribution toall stakeholders by orientating all strategic actions alongthese fundamental trends.

10

Management Comments:DPDHL Group has been steered along integrated bottomlines since 2009. As part of Strategy 2015, managementaction and progressively also incentivization have indeedbeen oriented by the virtuous circle of Employer-,Provider- and ultimately Investment of Choice.

Financial results have been shown in this investorpresentation on the previous pages, but Strategy 2020has also delivered multi-year achievements onmanymoredimensions.

With DPDHL employees at the basis of everything weachieve for our customers around the globe everyday, ourfinancial performance has been based on a constantgrowth in our employee base, coupled with record highemployee engagement as measured by our yearlyemployee opinion survey (EOS).

Measurement of customer satisfaction has been and iscontinuously refined as it is the base for our long-termsuccess. Our NPS showed further improvement in 2020.Of course, in the unusual circumstances, DPDHL Group’spurpose of “Connecting People. Improving Lives.” hasbeen more valid than ever for our employees, ourcustomers as well as their clients.

The impact on our broader stakeholder base and theenvironment has been reported in detail since many yearsas well. Our CO2 efficiency index uses 2007 as base yearand showed a 37% improvement by 2020. We will providean updated roadmap on the broad range of ESG topics onMarch 22nd.

11

Management Comments:DPDHL Group’s successful Strategy 2020 – and any futureaccomplishments – are delivered by DPDHL’s employees,which are now 570,000, all over the world. The successfulbusiness growth, not at least by realizing e-commercegrowth opportunities across the group, has comealongside a continuous increase in the overall number ofcolleagues working for and earning their living fromDPDHL Group.

At the origin of any of our group’s achievements are theskills and engagement of all DPDHL employees. Wetherefore invest employee and management time as wellas significant budget in training programs, notably ourinternally-run Certified Program.

Furthermore, measuring anonymous but relevantemployee feedback is at the core of our management andsteering processes. To that purpose, a dedicatedEmployee Opinion Survey (EOS) is run every year inautumn across DPDHL Group, with part of management’sbonus linked to the results. The core KPI measures“Employee Engagement” and the 2013-2019-2020progression shows how the continued performanceimprovement – for our customers and investors – is basedon a continuously rising engagement by the increasingnumber of DPDHL colleagues across the globe.

12

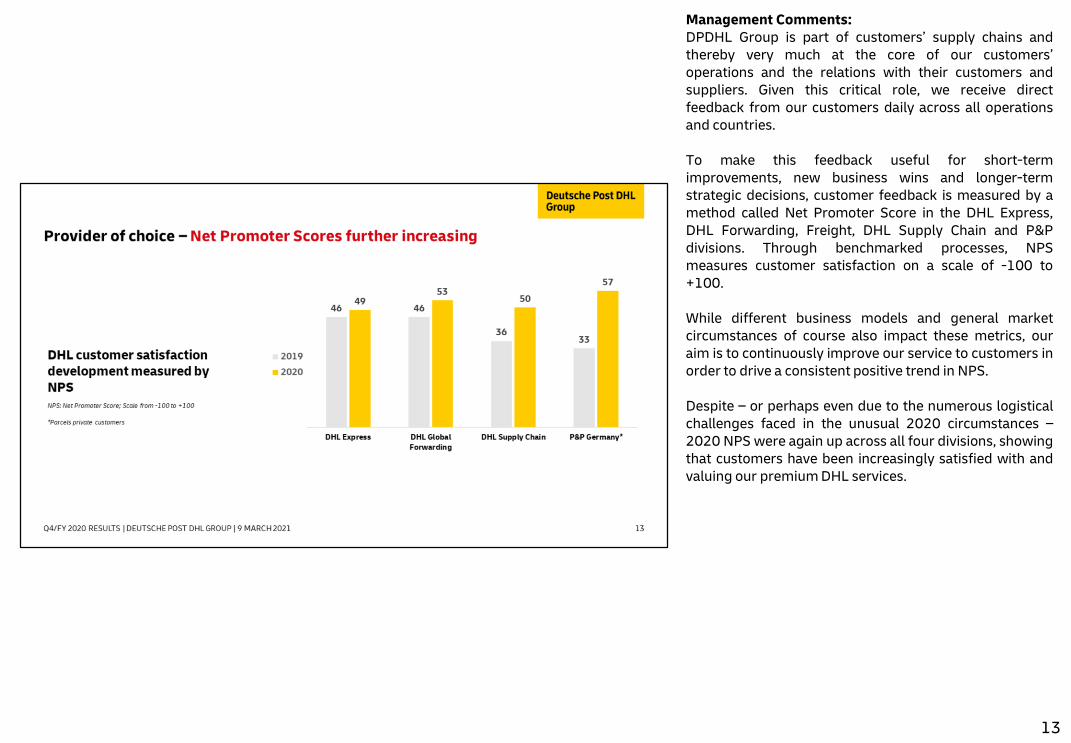

Management Comments:DPDHL Group is part of customers’ supply chains andthereby very much at the core of our customers’operations and the relations with their customers andsuppliers. Given this critical role, we receive directfeedback from our customers daily across all operationsand countries.

To make this feedback useful for short-termimprovements, new business wins and longer-termstrategic decisions, customer feedback is measured by amethod called Net Promoter Score in the DHL Express,DHL Forwarding, Freight, DHL Supply Chain and P&Pdivisions. Through benchmarked processes, NPSmeasures customer satisfaction on a scale of -100 to+100.

While different business models and general marketcircumstances of course also impact these metrics, ouraim is to continuously improve our service to customers inorder to drive a consistent positive trend in NPS.

Despite – or perhaps even due to the numerous logisticalchallenges faced in the unusual 2020 circumstances –2020 NPS were again up across all four divisions, showingthat customers have been increasingly satisfied with andvaluing our premiumDHL services.

13

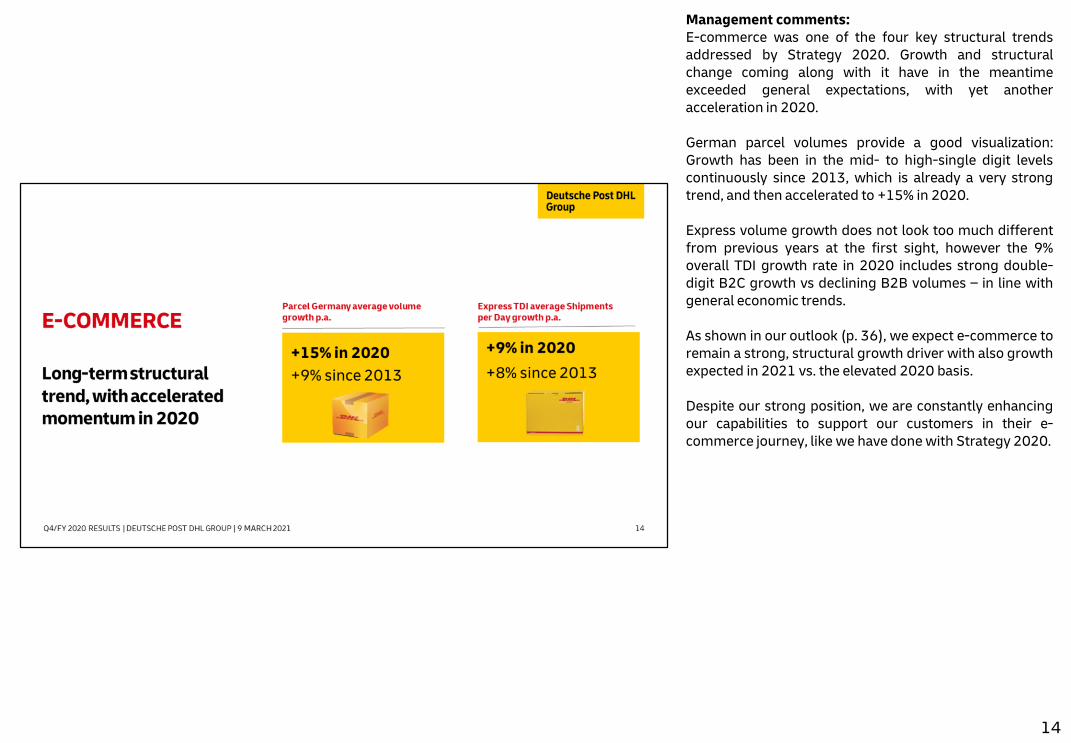

Management comments:E-commerce was one of the four key structural trendsaddressed by Strategy 2020. Growth and structuralchange coming along with it have in the meantimeexceeded general expectations, with yet anotheracceleration in 2020.

German parcel volumes provide a good visualization:Growth has been in the mid- to high-single digit levelscontinuously since 2013, which is already a very strongtrend, and then accelerated to +15% in 2020.

Express volume growth does not look too much differentfrom previous years at the first sight, however the 9%overall TDI growth rate in 2020 includes strong double-digit B2C growth vs declining B2B volumes – in line withgeneral economic trends.

As shown in our outlook (p. 36), we expect e-commerce toremain a strong, structural growth driver with also growthexpected in 2021 vs. the elevated 2020 basis.

Despite our strong position, we are constantly enhancingour capabilities to support our customers in their e-commerce journey, like we have donewith Strategy 2020.

14

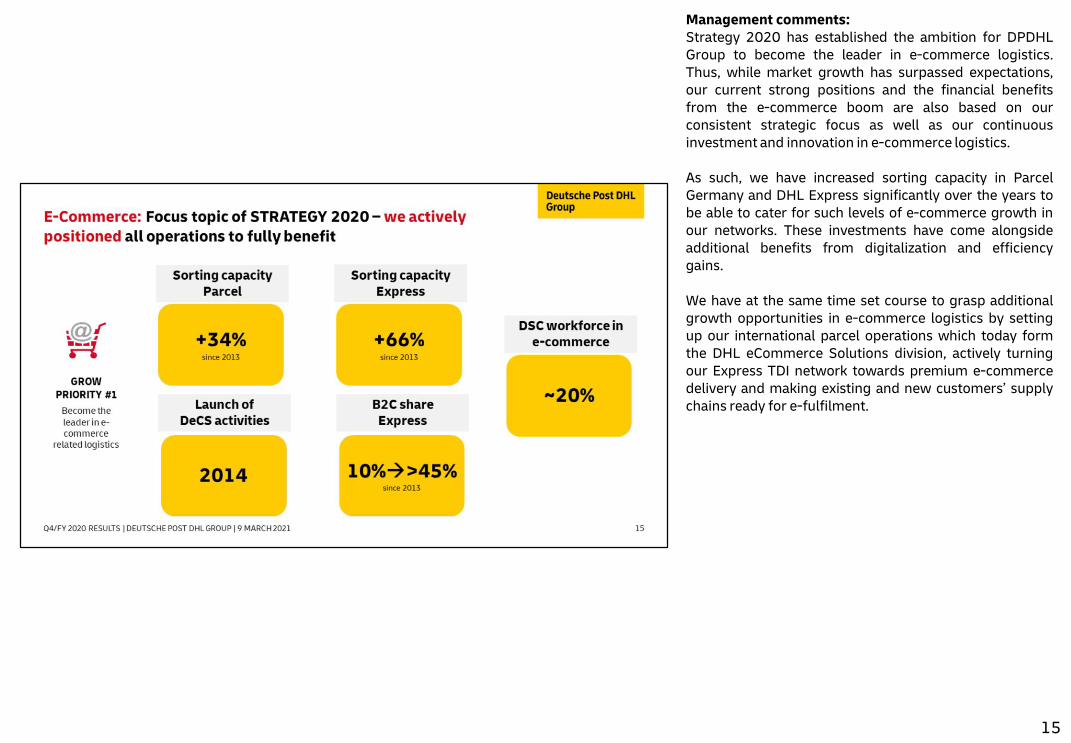

Management comments:Strategy 2020 has established the ambition for DPDHLGroup to become the leader in e-commerce logistics.Thus, while market growth has surpassed expectations,our current strong positions and the financial benefitsfrom the e-commerce boom are also based on ourconsistent strategic focus as well as our continuousinvestment and innovation in e-commerce logistics.

As such, we have increased sorting capacity in ParcelGermany and DHL Express significantly over the years tobe able to cater for such levels of e-commerce growth inour networks. These investments have come alongsideadditional benefits from digitalization and efficiencygains.

We have at the same time set course to grasp additionalgrowth opportunities in e-commerce logistics by settingup our international parcel operations which today formthe DHL eCommerce Solutions division, actively turningour Express TDI network towards premium e-commercedelivery and making existing and new customers’ supplychains ready for e-fulfilment.

15

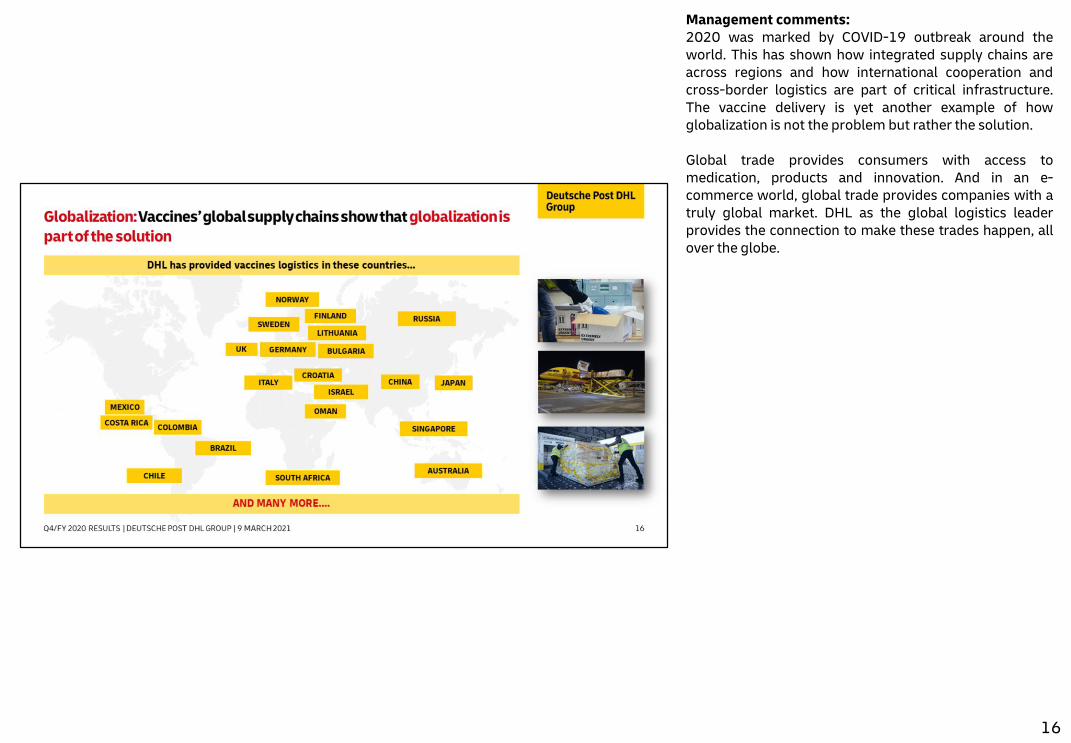

Management comments:2020 was marked by COVID-19 outbreak around theworld. This has shown how integrated supply chains areacross regions and how international cooperation andcross-border logistics are part of critical infrastructure.The vaccine delivery is yet another example of howglobalization is not the problem but rather the solution.

Global trade provides consumers with access tomedication, products and innovation. And in an e-commerce world, global trade provides companies with atruly global market. DHL as the global logistics leaderprovides the connection to make these trades happen, allover the globe.

16

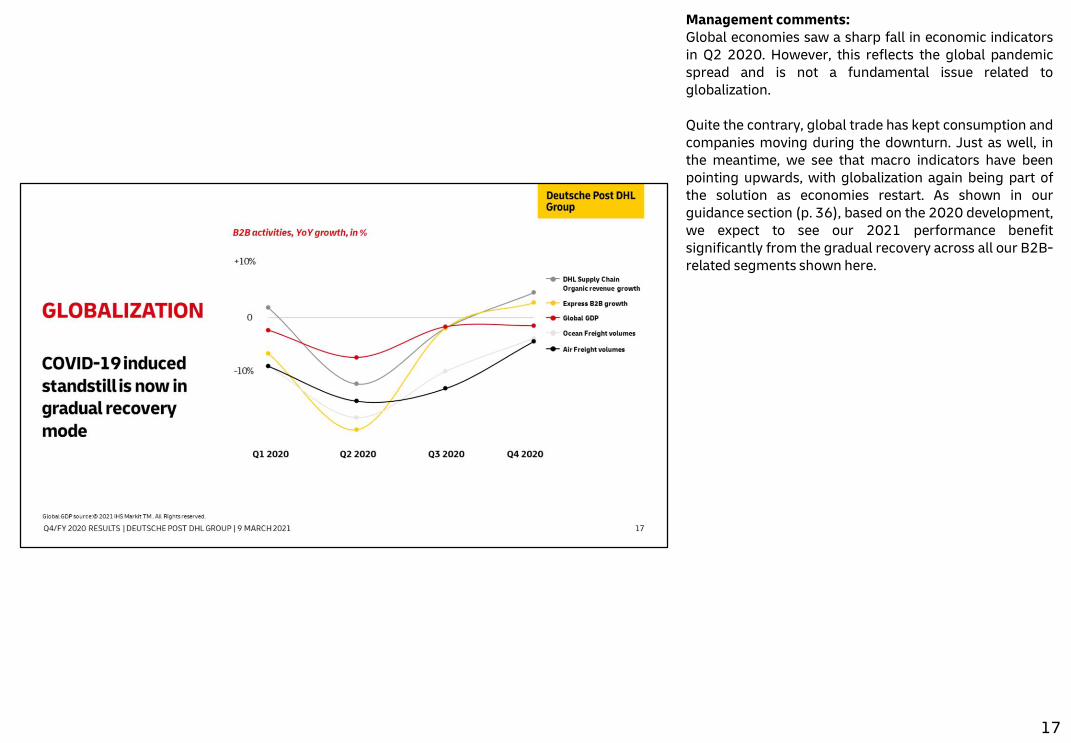

Management comments:Global economies saw a sharp fall in economic indicatorsin Q2 2020. However, this reflects the global pandemicspread and is not a fundamental issue related toglobalization.

Quite the contrary, global trade has kept consumption andcompanies moving during the downturn. Just as well, inthe meantime, we see that macro indicators have beenpointing upwards, with globalization again being part ofthe solution as economies restart. As shown in ourguidance section (p. 36), based on the 2020 development,we expect to see our 2021 performance benefitsignificantly from the gradual recovery across all our B2B-related segments shown here.

17

18

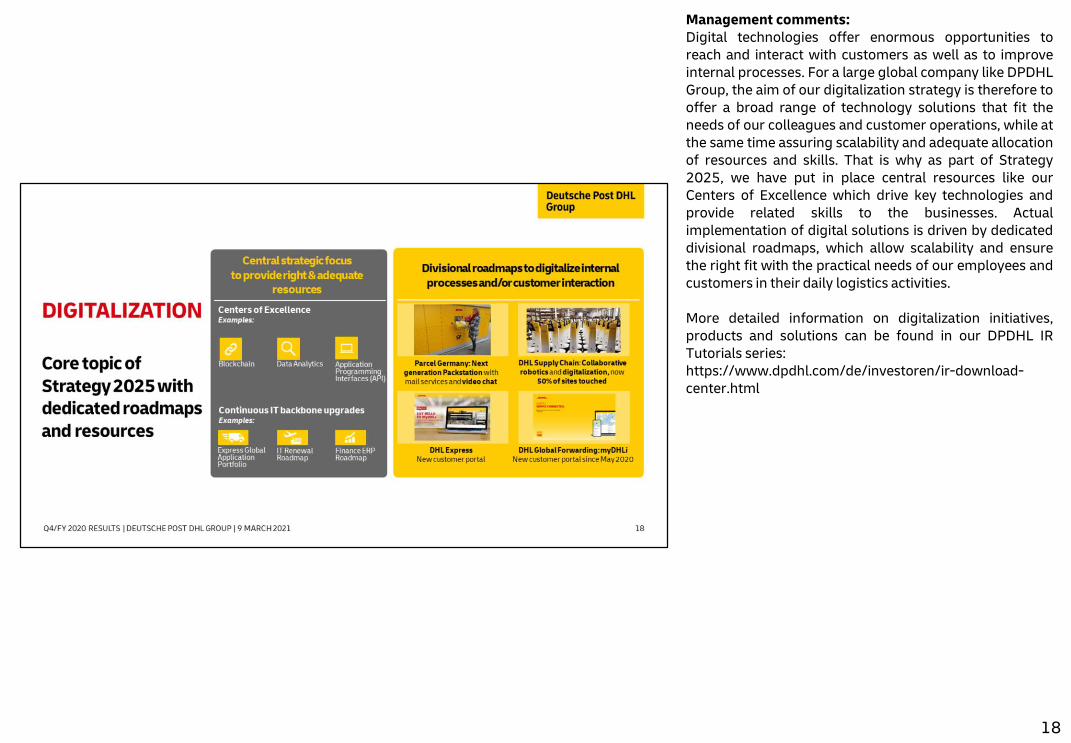

Management comments:Digital technologies offer enormous opportunities toreach and interact with customers as well as to improveinternal processes. For a large global company like DPDHLGroup, the aim of our digitalization strategy is therefore tooffer a broad range of technology solutions that fit theneeds of our colleagues and customer operations, while atthe same time assuring scalability and adequate allocationof resources and skills. That is why as part of Strategy2025, we have put in place central resources like ourCenters of Excellence which drive key technologies andprovide related skills to the businesses. Actualimplementation of digital solutions is driven by dedicateddivisional roadmaps, which allow scalability and ensurethe right fit with the practical needs of our employees andcustomers in their daily logistics activities.

More detailed information on digitalization initiatives,products and solutions can be found in our DPDHL IRTutorials series:https://www.dpdhl.com/de/investoren/ir-download-center.html

19

20

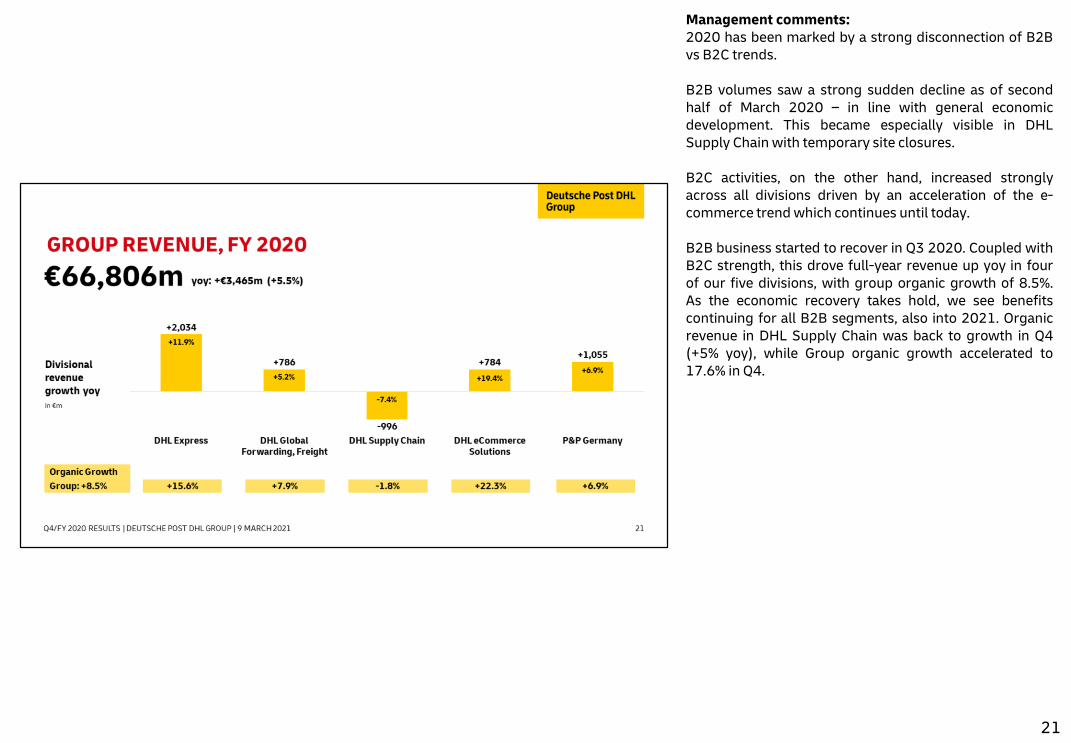

Management comments:2020 has been marked by a strong disconnection of B2Bvs B2C trends.

B2B volumes saw a strong sudden decline as of secondhalf of March 2020 – in line with general economicdevelopment. This became especially visible in DHLSupply Chain with temporary site closures.

B2C activities, on the other hand, increased stronglyacross all divisions driven by an acceleration of the e-commerce trendwhich continues until today.

B2B business started to recover in Q3 2020. Coupled withB2C strength, this drove full-year revenue up yoy in fourof our five divisions, with group organic growth of 8.5%.As the economic recovery takes hold, we see benefitscontinuing for all B2B segments, also into 2021. Organicrevenue in DHL Supply Chain was back to growth in Q4(+5% yoy), while Group organic growth accelerated to17.6% in Q4.

21

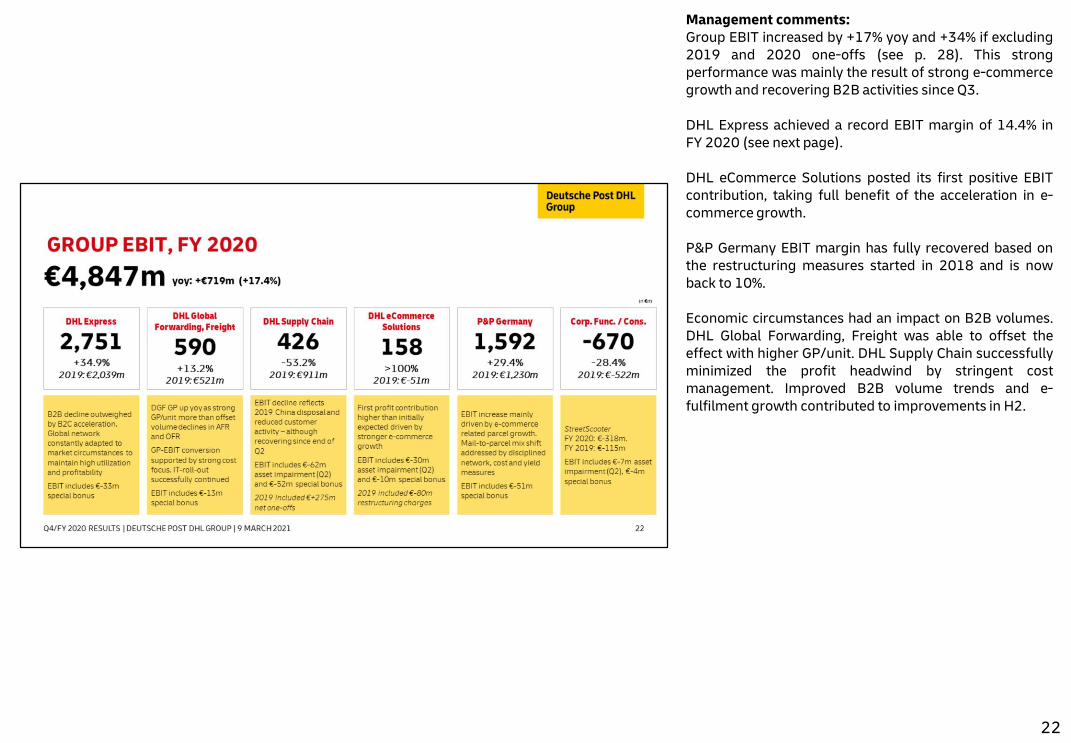

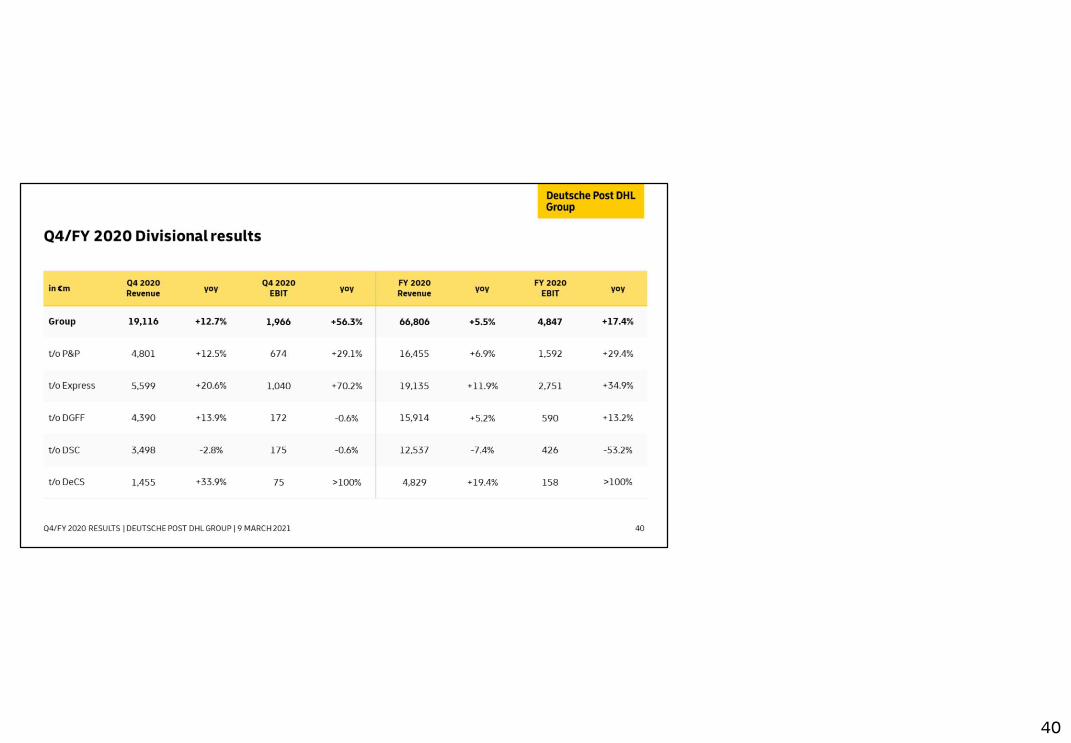

Management comments:Group EBIT increased by +17% yoy and +34% if excluding2019 and 2020 one-offs (see p. 28). This strongperformance was mainly the result of strong e-commercegrowth and recovering B2B activities since Q3.

DHL Express achieved a record EBIT margin of 14.4% inFY 2020 (see next page).

DHL eCommerce Solutions posted its first positive EBITcontribution, taking full benefit of the acceleration in e-commerce growth.

P&P Germany EBIT margin has fully recovered based onthe restructuring measures started in 2018 and is nowback to 10%.

Economic circumstances had an impact on B2B volumes.DHL Global Forwarding, Freight was able to offset theeffect with higher GP/unit. DHL Supply Chain successfullyminimized the profit headwind by stringent costmanagement. Improved B2B volume trends and e-fulfilment growth contributed to improvements in H2.

22

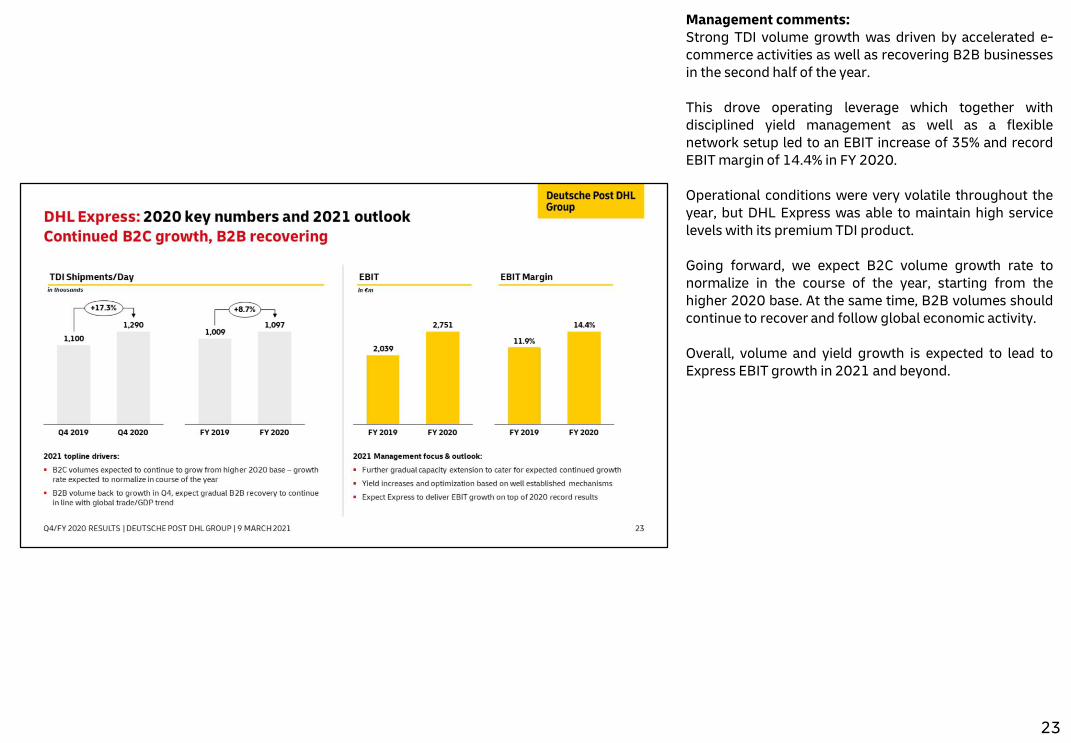

Management comments:Strong TDI volume growth was driven by accelerated e-commerce activities as well as recovering B2B businessesin the second half of the year.

This drove operating leverage which together withdisciplined yield management as well as a flexiblenetwork setup led to an EBIT increase of 35% and recordEBITmargin of 14.4% in FY 2020.

Operational conditions were very volatile throughout theyear, but DHL Express was able to maintain high servicelevels with its premiumTDI product.

Going forward, we expect B2C volume growth rate tonormalize in the course of the year, starting from thehigher 2020 base. At the same time, B2B volumes shouldcontinue to recover and follow global economic activity.

Overall, volume and yield growth is expected to lead toExpress EBIT growth in 2021 and beyond.

23

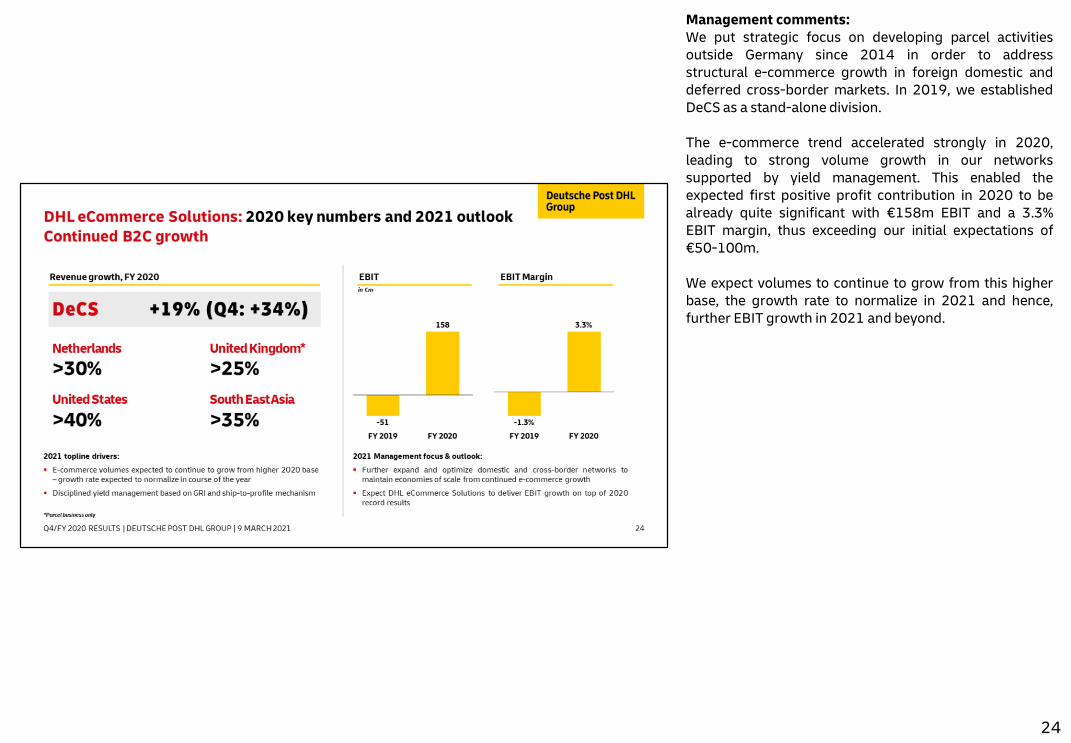

Management comments:We put strategic focus on developing parcel activitiesoutside Germany since 2014 in order to addressstructural e-commerce growth in foreign domestic anddeferred cross-border markets. In 2019, we establishedDeCS as a stand-alone division.

The e-commerce trend accelerated strongly in 2020,leading to strong volume growth in our networkssupported by yield management. This enabled theexpected first positive profit contribution in 2020 to bealready quite significant with €158m EBIT and a 3.3%EBIT margin, thus exceeding our initial expectations of€50-100m.

We expect volumes to continue to grow from this higherbase, the growth rate to normalize in 2021 and hence,further EBIT growth in 2021 and beyond.

24

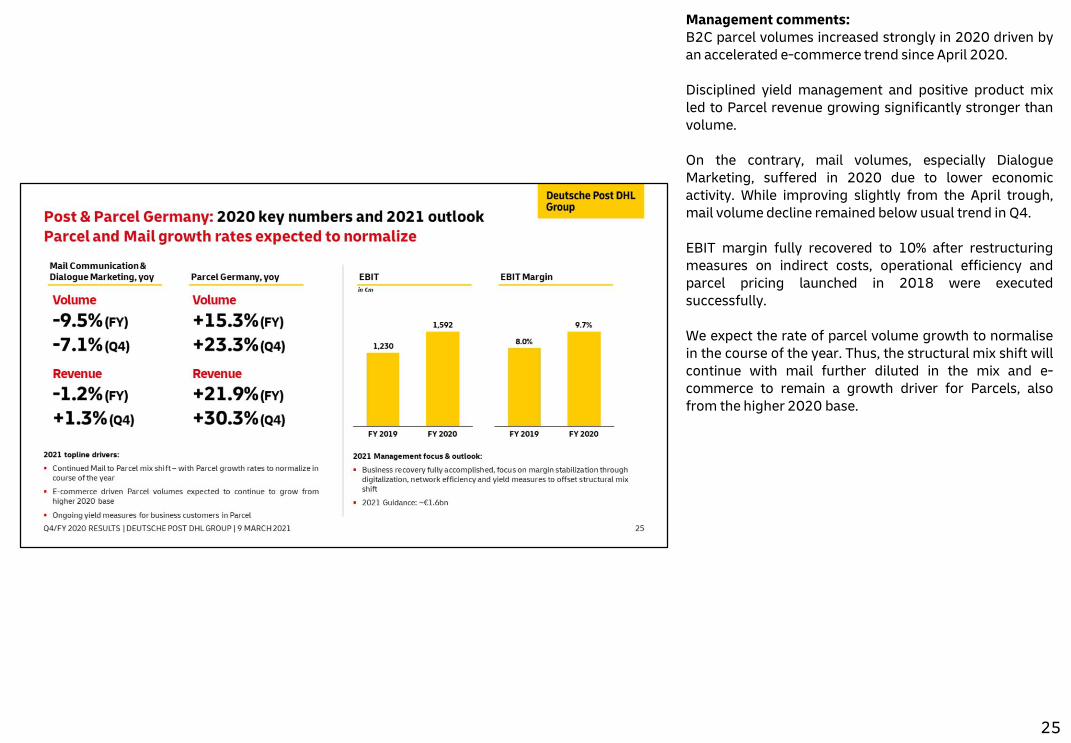

Management comments:B2C parcel volumes increased strongly in 2020 driven byan accelerated e-commerce trend since April 2020.

Disciplined yield management and positive product mixled to Parcel revenue growing significantly stronger thanvolume.

On the contrary, mail volumes, especially DialogueMarketing, suffered in 2020 due to lower economicactivity. While improving slightly from the April trough,mail volume decline remained below usual trend in Q4.

EBIT margin fully recovered to 10% after restructuringmeasures on indirect costs, operational efficiency andparcel pricing launched in 2018 were executedsuccessfully.

We expect the rate of parcel volume growth to normalisein the course of the year. Thus, the structural mix shift willcontinue with mail further diluted in the mix and e-commerce to remain a growth driver for Parcels, alsofrom the higher 2020 base.

25

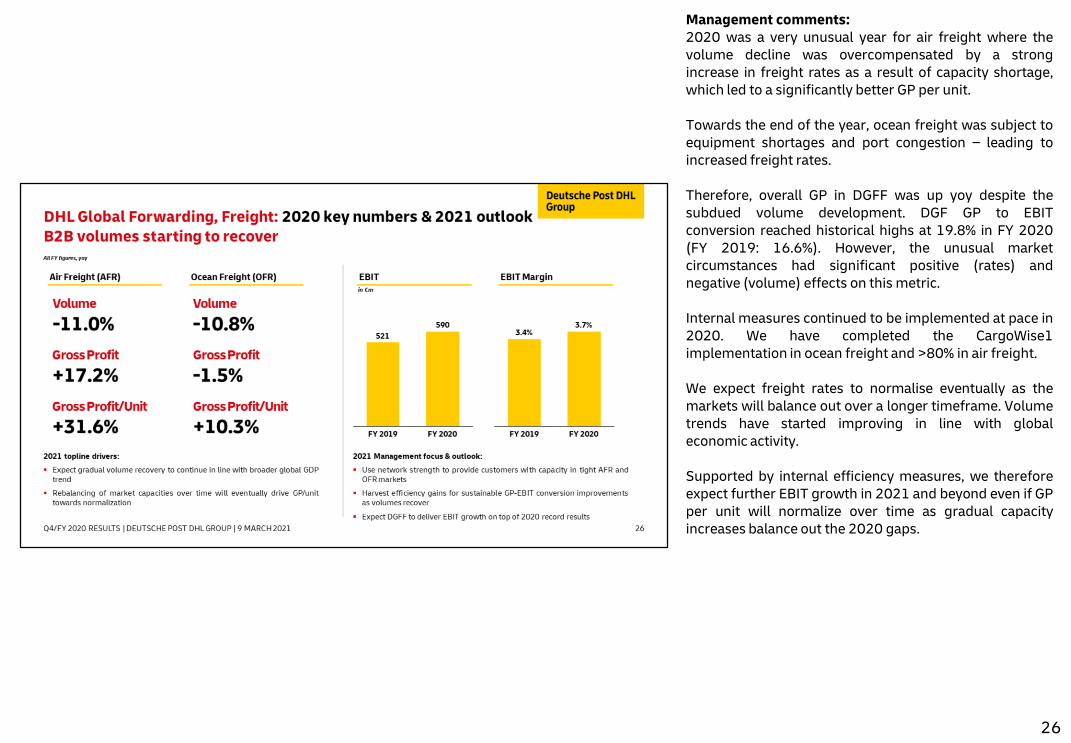

Management comments:2020 was a very unusual year for air freight where thevolume decline was overcompensated by a strongincrease in freight rates as a result of capacity shortage,which led to a significantly better GP per unit.

Towards the end of the year, ocean freight was subject toequipment shortages and port congestion – leading toincreased freight rates.

Therefore, overall GP in DGFF was up yoy despite thesubdued volume development. DGF GP to EBITconversion reached historical highs at 19.8% in FY 2020(FY 2019: 16.6%). However, the unusual marketcircumstances had significant positive (rates) andnegative (volume) effects on this metric.

Internal measures continued to be implemented at pace in2020. We have completed the CargoWise1implementation in ocean freight and >80% in air freight.

We expect freight rates to normalise eventually as themarkets will balance out over a longer timeframe. Volumetrends have started improving in line with globaleconomic activity.

Supported by internal efficiency measures, we thereforeexpect further EBIT growth in 2021 and beyond even if GPper unit will normalize over time as gradual capacityincreases balance out the 2020 gaps.

26

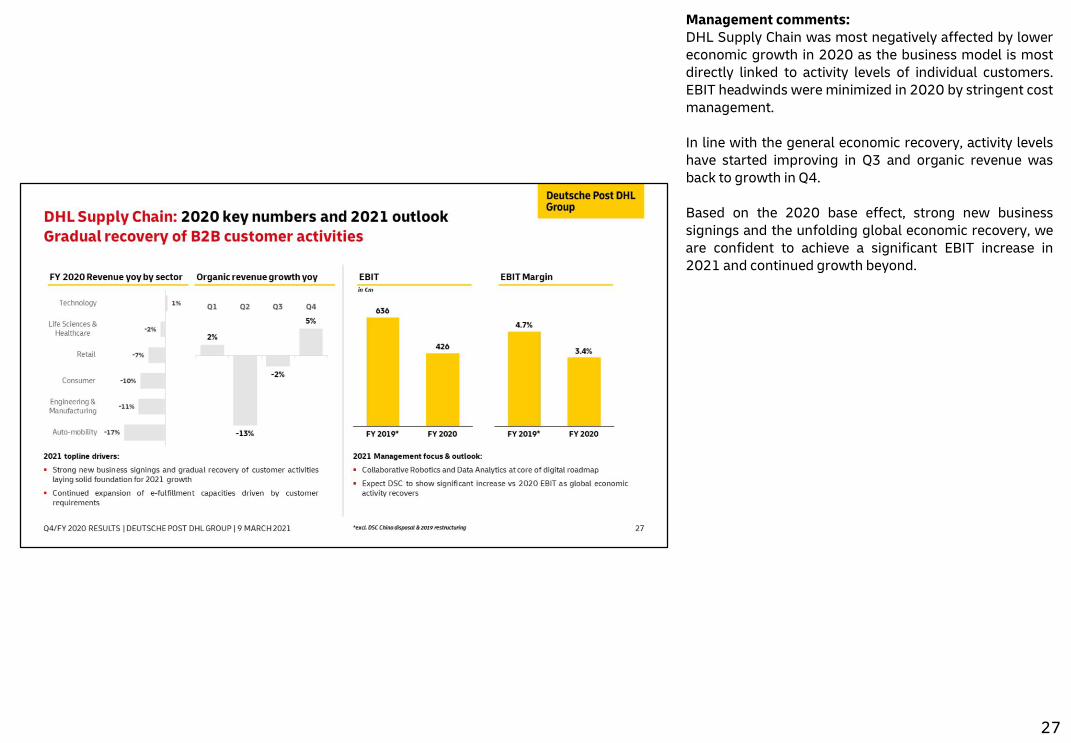

Management comments:DHL Supply Chain was most negatively affected by lowereconomic growth in 2020 as the business model is mostdirectly linked to activity levels of individual customers.EBIT headwinds wereminimized in 2020 by stringent costmanagement.

In line with the general economic recovery, activity levelshave started improving in Q3 and organic revenue wasback to growth in Q4.

Based on the 2020 base effect, strong new businesssignings and the unfolding global economic recovery, weare confident to achieve a significant EBIT increase in2021 and continued growth beyond.

27

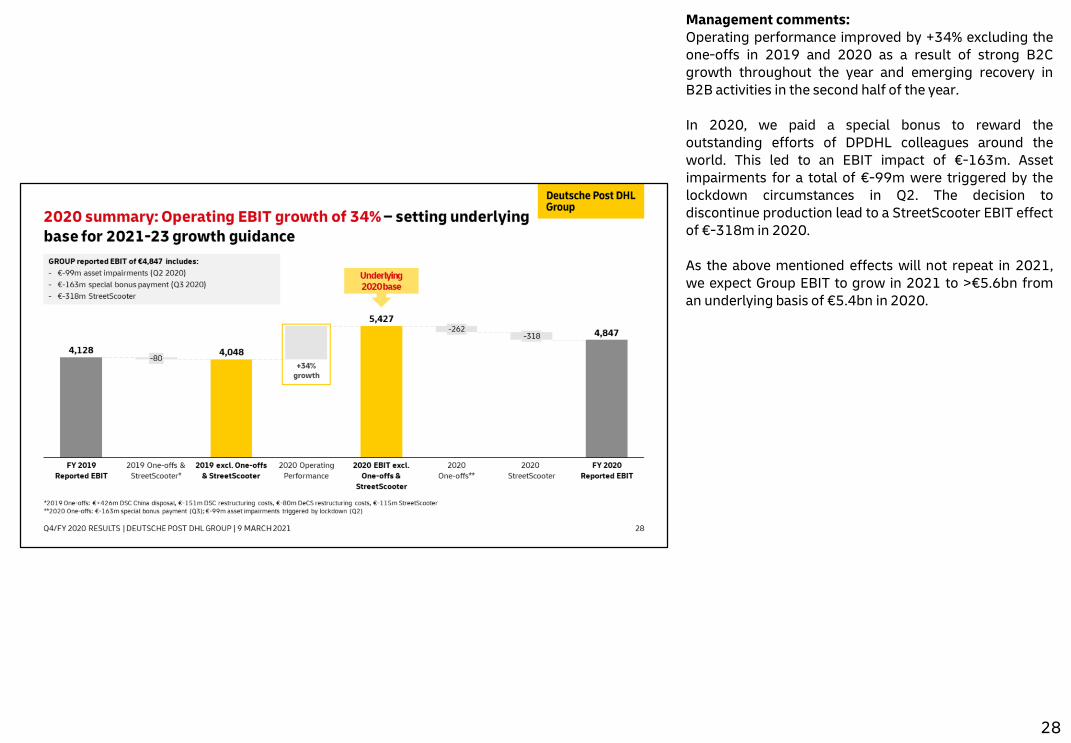

Management comments:Operating performance improved by +34% excluding theone-offs in 2019 and 2020 as a result of strong B2Cgrowth throughout the year and emerging recovery inB2B activities in the second half of the year.

In 2020, we paid a special bonus to reward theoutstanding efforts of DPDHL colleagues around theworld. This led to an EBIT impact of €-163m. Assetimpairments for a total of €-99m were triggered by thelockdown circumstances in Q2. The decision todiscontinue production lead to a StreetScooter EBIT effectof €-318m in 2020.

As the above mentioned effects will not repeat in 2021,we expect Group EBIT to grow in 2021 to >€5.6bn froman underlying basis of €5.4bn in 2020.

28

29

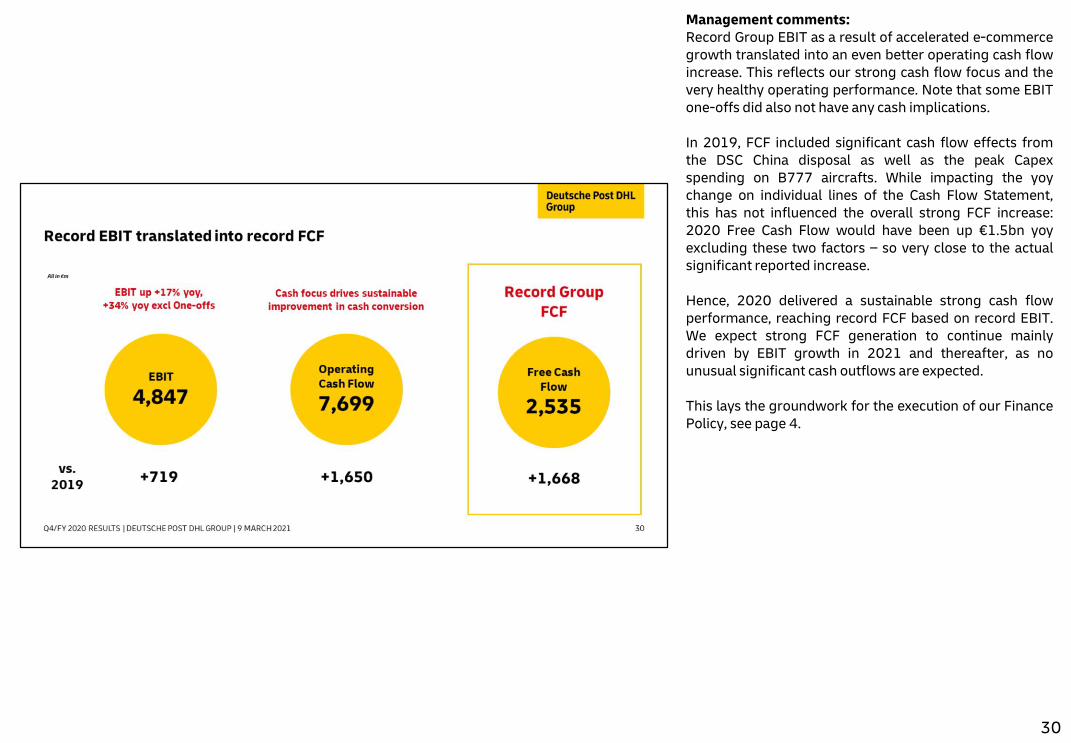

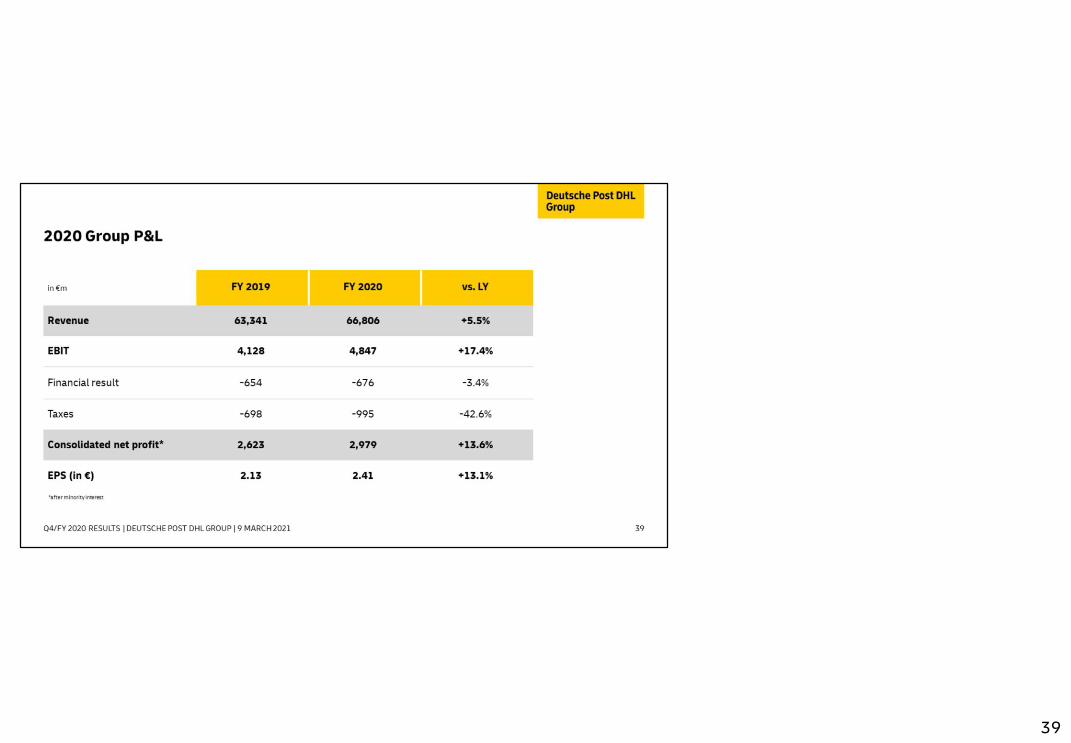

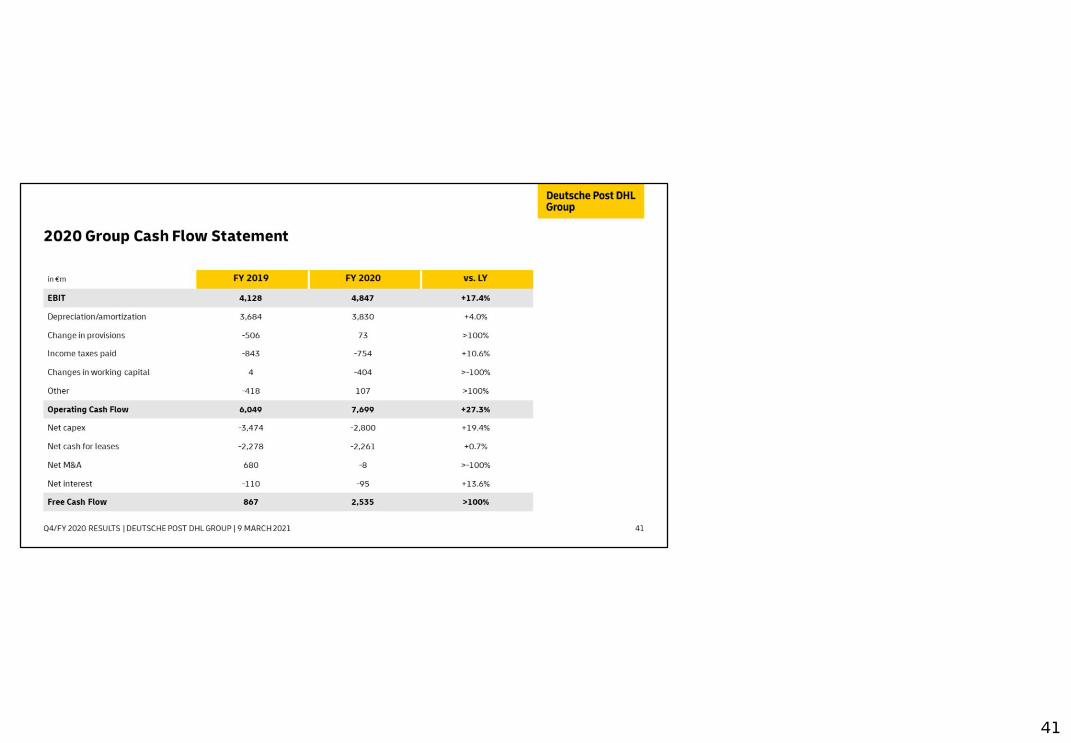

Management comments:Record Group EBIT as a result of accelerated e-commercegrowth translated into an even better operating cash flowincrease. This reflects our strong cash flow focus and thevery healthy operating performance. Note that some EBITone-offs did also not have any cash implications.

In 2019, FCF included significant cash flow effects fromthe DSC China disposal as well as the peak Capexspending on B777 aircrafts. While impacting the yoychange on individual lines of the Cash Flow Statement,this has not influenced the overall strong FCF increase:2020 Free Cash Flow would have been up €1.5bn yoyexcluding these two factors – so very close to the actualsignificant reported increase.

Hence, 2020 delivered a sustainable strong cash flowperformance, reaching record FCF based on record EBIT.We expect strong FCF generation to continue mainlydriven by EBIT growth in 2021 and thereafter, as nounusual significant cash outflows are expected.

This lays the groundwork for the execution of our FinancePolicy, see page 4.

30

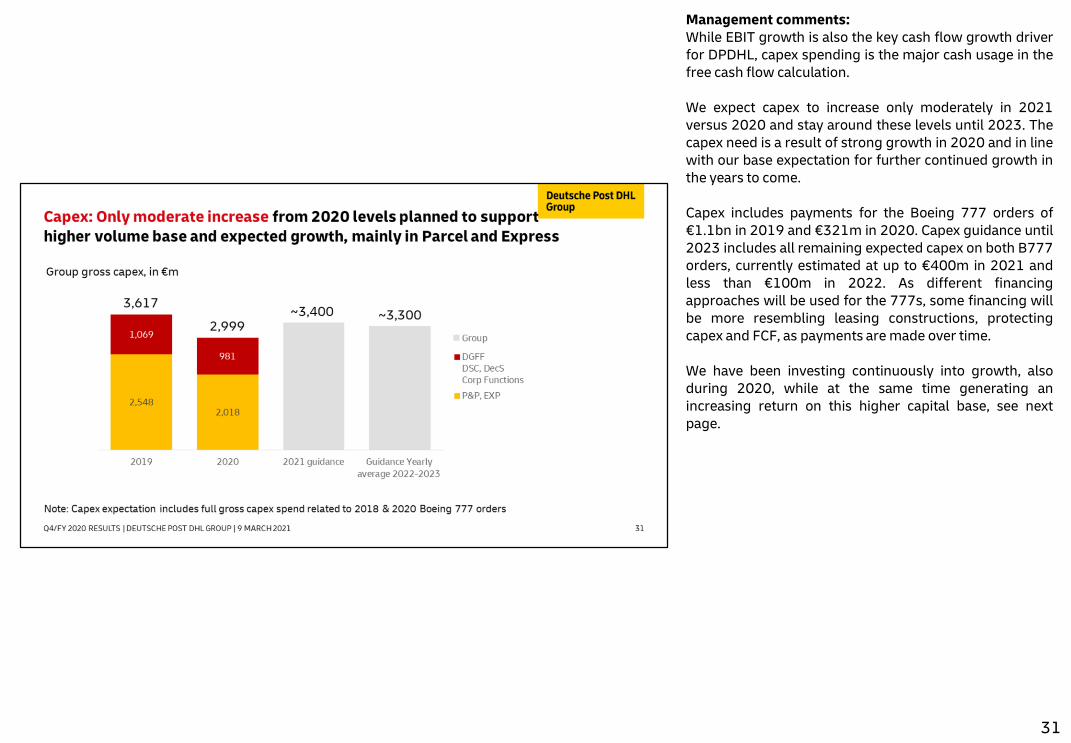

Management comments:While EBIT growth is also the key cash flow growth driverfor DPDHL, capex spending is the major cash usage in thefree cash flow calculation.

We expect capex to increase only moderately in 2021versus 2020 and stay around these levels until 2023. Thecapex need is a result of strong growth in 2020 and in linewith our base expectation for further continued growth inthe years to come.

Capex includes payments for the Boeing 777 orders of€1.1bn in 2019 and €321m in 2020. Capex guidance until2023 includes all remaining expected capex on both B777orders, currently estimated at up to €400m in 2021 andless than €100m in 2022. As different financingapproaches will be used for the 777s, some financing willbe more resembling leasing constructions, protectingcapex and FCF, as payments aremade over time.

We have been investing continuously into growth, alsoduring 2020, while at the same time generating anincreasing return on this higher capital base, see nextpage.

31

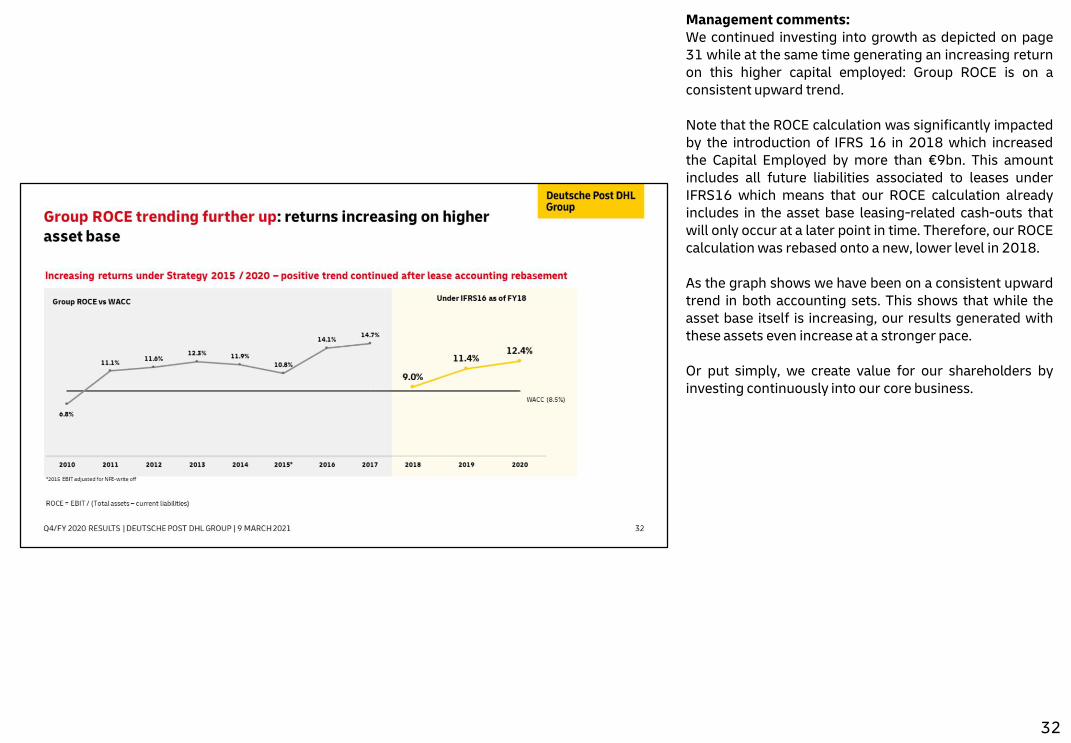

Management comments:We continued investing into growth as depicted on page31 while at the same time generating an increasing returnon this higher capital employed: Group ROCE is on aconsistent upward trend.

Note that the ROCE calculation was significantly impactedby the introduction of IFRS 16 in 2018 which increasedthe Capital Employed by more than €9bn. This amountincludes all future liabilities associated to leases underIFRS16 which means that our ROCE calculation alreadyincludes in the asset base leasing-related cash-outs thatwill only occur at a later point in time. Therefore, our ROCEcalculationwas rebased onto a new, lower level in 2018.

As the graph shows we have been on a consistent upwardtrend in both accounting sets. This shows that while theasset base itself is increasing, our results generated withthese assets even increase at a stronger pace.

Or put simply, we create value for our shareholders byinvesting continuously into our core business.

32

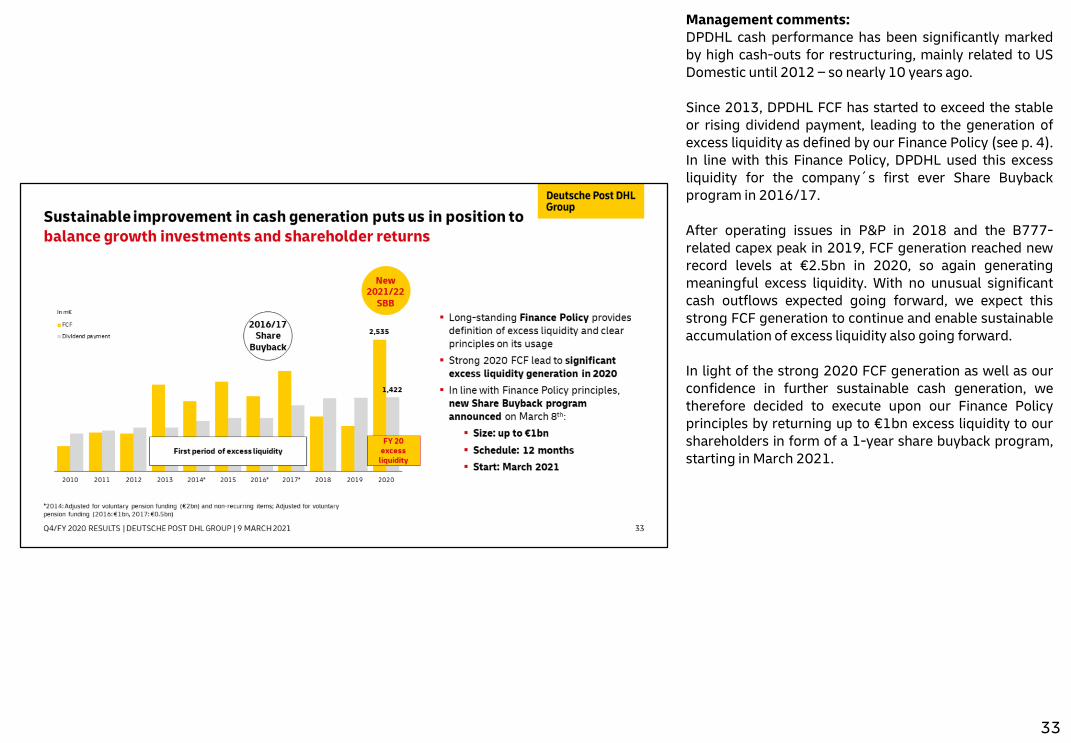

Management comments:DPDHL cash performance has been significantly markedby high cash-outs for restructuring, mainly related to USDomestic until 2012 – so nearly 10 years ago.

Since 2013, DPDHL FCF has started to exceed the stableor rising dividend payment, leading to the generation ofexcess liquidity as defined by our Finance Policy (see p. 4).In line with this Finance Policy, DPDHL used this excessliquidity for the company´s first ever Share Buybackprogram in 2016/17.

After operating issues in P&P in 2018 and the B777-related capex peak in 2019, FCF generation reached newrecord levels at €2.5bn in 2020, so again generatingmeaningful excess liquidity. With no unusual significantcash outflows expected going forward, we expect thisstrong FCF generation to continue and enable sustainableaccumulation of excess liquidity also going forward.

In light of the strong 2020 FCF generation as well as ourconfidence in further sustainable cash generation, wetherefore decided to execute upon our Finance Policyprinciples by returning up to €1bn excess liquidity to ourshareholders in form of a 1-year share buyback program,starting in March 2021.

33

34

35

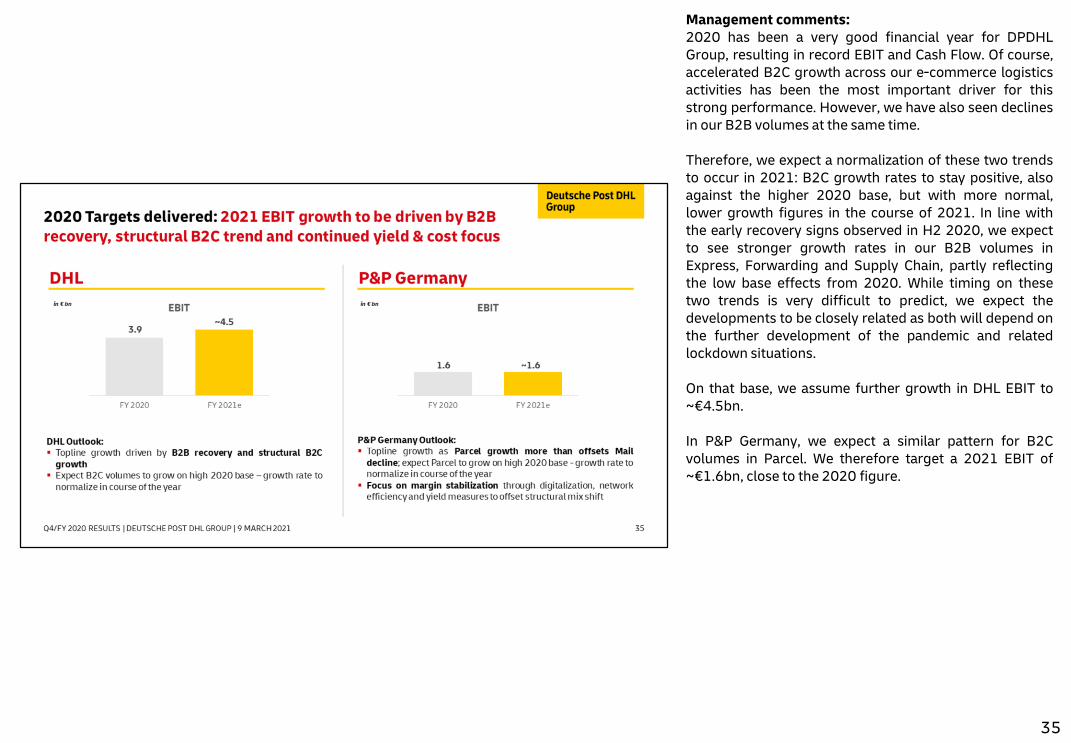

Management comments:2020 has been a very good financial year for DPDHLGroup, resulting in record EBIT and Cash Flow. Of course,accelerated B2C growth across our e-commerce logisticsactivities has been the most important driver for thisstrong performance. However, we have also seen declinesin our B2B volumes at the same time.

Therefore, we expect a normalization of these two trendsto occur in 2021: B2C growth rates to stay positive, alsoagainst the higher 2020 base, but with more normal,lower growth figures in the course of 2021. In line withthe early recovery signs observed in H2 2020, we expectto see stronger growth rates in our B2B volumes inExpress, Forwarding and Supply Chain, partly reflectingthe low base effects from 2020. While timing on thesetwo trends is very difficult to predict, we expect thedevelopments to be closely related as both will depend onthe further development of the pandemic and relatedlockdown situations.

On that base, we assume further growth in DHL EBIT to~€4.5bn.

In P&P Germany, we expect a similar pattern for B2Cvolumes in Parcel. We therefore target a 2021 EBIT of~€1.6bn, close to the 2020 figure.

36

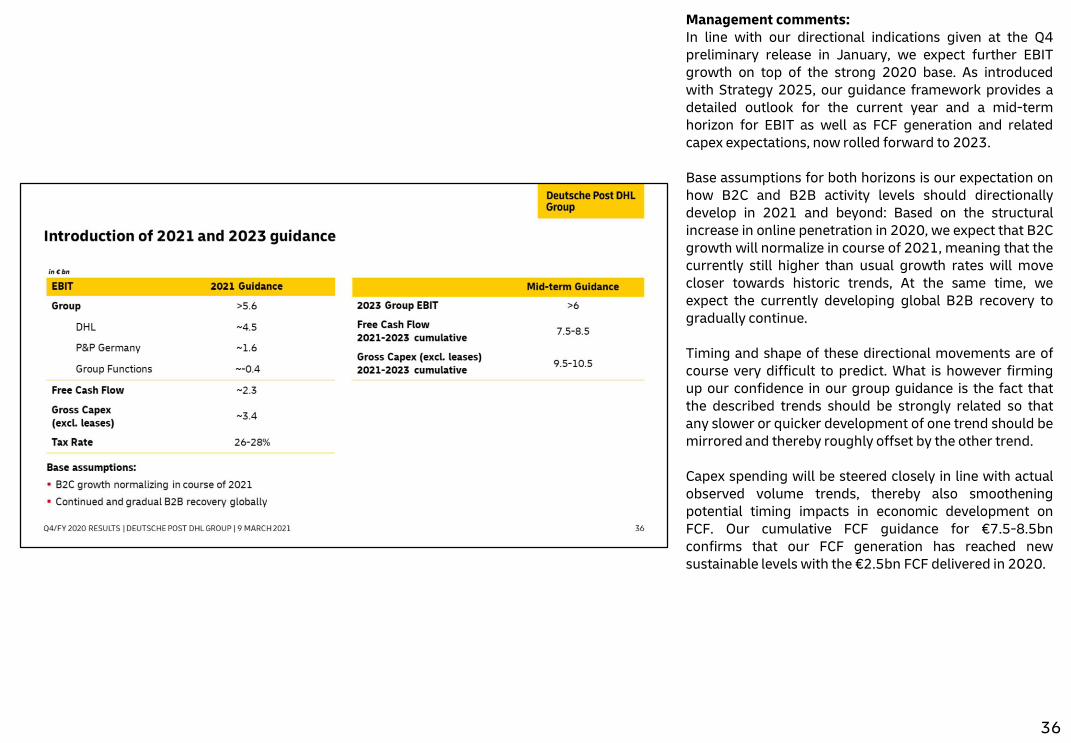

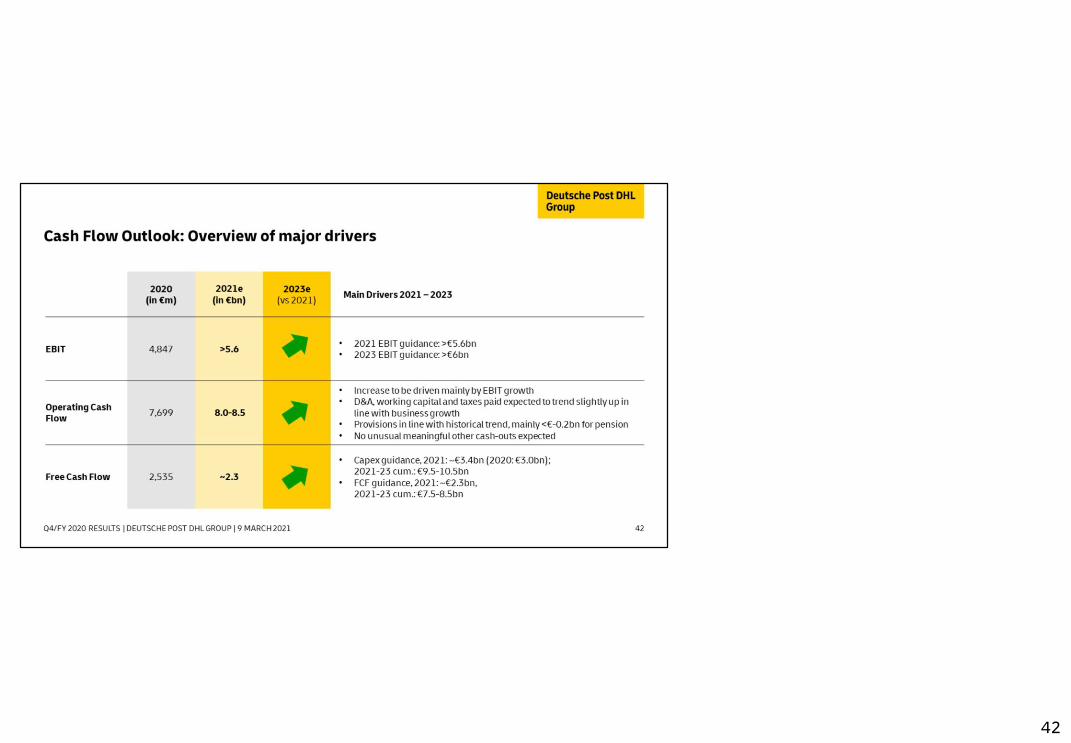

Management comments:In line with our directional indications given at the Q4preliminary release in January, we expect further EBITgrowth on top of the strong 2020 base. As introducedwith Strategy 2025, our guidance framework provides adetailed outlook for the current year and a mid-termhorizon for EBIT as well as FCF generation and relatedcapex expectations, now rolled forward to 2023.

Base assumptions for both horizons is our expectation onhow B2C and B2B activity levels should directionallydevelop in 2021 and beyond: Based on the structuralincrease in online penetration in 2020, we expect that B2Cgrowth will normalize in course of 2021, meaning that thecurrently still higher than usual growth rates will movecloser towards historic trends, At the same time, weexpect the currently developing global B2B recovery togradually continue.

Timing and shape of these directional movements are ofcourse very difficult to predict. What is however firmingup our confidence in our group guidance is the fact thatthe described trends should be strongly related so thatany slower or quicker development of one trend should bemirrored and thereby roughly offset by the other trend.

Capex spending will be steered closely in line with actualobserved volume trends, thereby also smootheningpotential timing impacts in economic development onFCF. Our cumulative FCF guidance for €7.5-8.5bnconfirms that our FCF generation has reached newsustainable levels with the €2.5bn FCF delivered in 2020.

37

38

39

40

41

42