Embed Size (px)

Citation preview

LONGMEAD CROSSING COMMUNITYSERVICE ASSOCIATION

INDEPENDENT AUDITOR'S REPORT

DECEMBER 31,2007

SCHREINER1 LEGGE& COMPANY

A Professional Accounting & Consulting Corporation'RECEIVED Sf? 04 ¡COO

INEPENDENT AUDITOR'S REPORT

June 29, 2008

Board of DirectorsLongiead Crossing CommunitySerce Association

Silver Spring, Marland 20874

We have audited the accompanying statement of fiancial condition of Longiead CrossingCommunty Serice Association as of December 31, 2007, and the related statements of revenueand expenses, changes in fud balance, and cash flows for the year then ended. These fiancialstatements are the responsibilty of the Association's management. Our responsibilty is toexpress an opinion on these fiancial statements based on our audit.

We conducted our audit in accordance with U.S. generally accepted auditing standards. Thosestandards require that we plan and perorm the audit to obtain reasonable assurance aboutwhether the financial statements are free of materal misstatement. An audit includes examining,on a test basis, evidence supporting the amounts and disclosures in the financial statements. Anaudit also includes assessing the accounting principles used and signficant estimates made bymanagement, as well as evaluating the overall financial statement presentation. We believe thatour audit provides a reasonable basis for our opinion.

In our opinion, the financial statements refered to above present fairly, in all material respects,the financial position of Longiead Crossing Communty Serice Association as ofDecember 31, 2007, and the results of its operations and its cash flows for the year then ended inconformity with U.S. generally accepted accounting principles.

Information for the year ended December 31, 2006, is presented for comparative purposes only,and was extracted from the financial statements on which an unqualified opinion, dated June 28,2007, was expressed.

.;Ã"~~1 ,lf'Y ,I ~/(JSCHREINER, LEGGE & COMPANYCERTIFIED PUBLIC ACCOUNTANTS

DA VID R. lEGGE.ClAKENNETH M. WElCHClA

AUDRY POMERENING Cl

2800 Eisenhower Avenue

Suite 100Alexandria, VA 22314

703.329.800800.800.7520

fax 703329.9040

ic:CPi-\

infoiislc-cp.comwww.slc-cpa.com

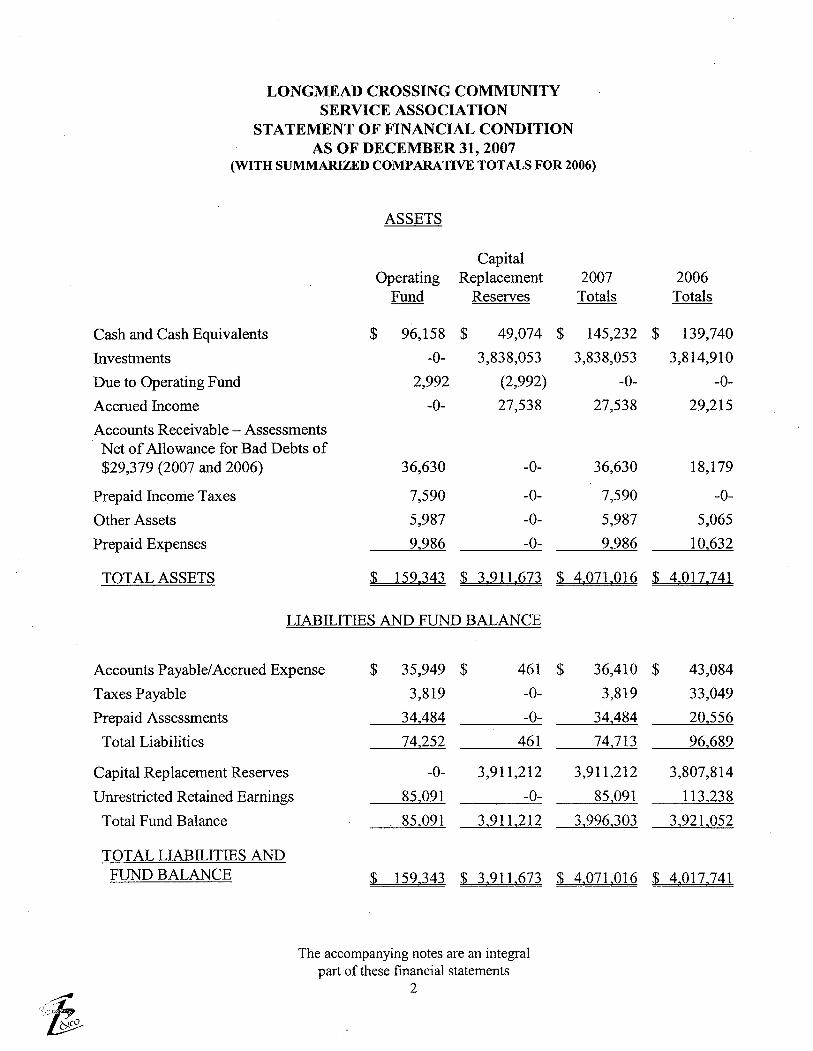

LONGMEAD CROSSING COMMUNITYSERVICE ASSOCIATION

STATEMENT OF FINANCIAL CONDITIONAS OF DECEMBER 31, 2007

(WITH SUMMARZED COMPARTIVE TOTALS FOR 2006)

ASSETS

CapitalOperating Replacement 2007 2006

Fund Reserves Totals Totals

Cash and Cash Equivalents $ 96,158 $ 49,074 $ 145,232 $ 139,740

Investments -0- 3,838,053 3,838,053 3,814,910

Due to Operating Fund 2,992 (2,992) -0- -0-

Accrued Income -0- 27,538 27,538 29,215

Accounts Receivable - AssessmentsNet of Allowance for Bad Debts of$29,379 (2007 and 2006) 36,630 -0- 36,630 18,179

Prepaid Income Taxes 7,590 -0- 7,590 -0-

Other Assets 5,987 -0- 5,987 5,065

Prepaid Expenses 9,986 -0- 9,986 10,632

TOTAL ASSETS $ 159.343 $ 3,91 1.673 $ 4,071.016 $ 4,017,741

LIAILITIES AN FUN BALANCE

Accounts Payable! Accrued Expense $ 35,949 $ 461 $ 36,410 $ 43,084

Taxes Payable 3,819 -0- 3,819 33,049

Prepaid Assessments 34,484 -0- 34,484 20,556

Total Liabilities 74,252 461 74,713 96,689

Capital Replacement Reserves -0- 3,911,212 3,911,212 3,807,814

Unrestricted Retained Earings 85,091 -0- 85,091 113,238

Total Fund Balance 85,091 3,911,212 3,996,303 3,921,052

TOTAL LIAILITIES ANDFUN BALANCE $ 159,343 $ 3.911.673 $ 4,071.016 $ 4,017,741

~"~The accompanying notes are an integral

part of these financial statements2

LONGMEAD CROSSING COMMUNITY SERVICE ASSOCIATIONSTATEMENT OF REVENUE AND EXPENSES,

AND CHANGES IN FUND BALANCEFOR THE YEAR ENDED DECEMBER 31,2007

(WITH SUMMARZED COMP ARTIVE TOTALS FOR 2006)

Capital

Operating Replacement 2007 2006Fund Reserves Totals Totals

REVENUOwners' Assessments $ 883,878 $ 130,000 $ 1,013,878 $ 985,272

Investment Income 3,105 178,694 181,799 172,061

Pool, Late Fees, andOther Miscellaneous Income 58,418 -0- 58,418 68,153

Total Revenue 945,401 308,694 1,254,095 1,225,486

EXPENSES

Management Fees 136,066 -0- 136,066 132,103

Professional Services 19,599 -0- 19,599 55,897

Insurance 11,232 -0- 11,232 13,248

General Administrative Expense 50,911 311 51,222 35,867

Trash Removal 108,289 -0- 108,289 108,289

Snow Removal 113,252 -0- 113,252 36,240

Ground Contract and Maintenance 336,925 -0- 336,925 351,012

RecreationlSociallPrinting 6,237 -0- 6,237 7,508

Pool Operations 144,768 -0- 144,768 128,077

Federal and State Income Taxes 46,269 -0- 46,269 45,666

Bad Debt Expense -0- -0- -0- 1,726

Capital Replacement ReserveExpenditures -0- 204,985 204,985 91,557

Total Expenses 973,548 205,296 1,178,844 1,007,190

Excess (Deficiency) of Revenue

Over Expenses (28,147) 103,398 75,251 218,296

Balance - Beginning of Year 113,238 3,807,814 3,921,052 3,702,756

Balance - End of Year $ 85,091 $ 3,911.212 $ 3,996.303 $ 3.921.052

-~..\,;t-lb

The accompanying notes are an integralpart of these financial statements

3

LONGMEAD CROSSING COMMUNITY SERVICE ASSOCIATIONSTATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31,2007(WITH SUMMARZED COMPARTIVE TOTALS FOR 2006)

CapitalOperating Replacement 2007 2006

Fund Reserve Totals Totals

Reconciliation of Excess (Deficiency) ofRevenue Over Expenses to Net CashProvided by (Used in) Operating Activities:

Excess (Deficiency) of Revenue Over Expenses $ (28,147) $ 103,398 $ 75,251 $ 218,296

Adjustments to Reconcile Excess (Deficiency)of Revenue Over Expenses to Net CashProvided by (Used in) Operating Activities:

Interfund ReceivablelPayable (9,464) 9,464 -0- -0-Bad Debt Expense -0- -0- -0- 1,726Decrease (Increase) in:

Assessments Receivable (18,451) -0- (18,451) 1,226Other Assets (7,866) 1,677 (6,189) 4,433

Increase (Decrease) in:Accounts Payable!Other Expense (33,126) (2,317) (35,443) 26,891Prepaid Assessments 13,928 -0- 13,928 (17,305) .

Total Adjustments (54,979) 8,824 (46,155) 16,971

Net Cash Provided by (Used in)Operating Activities (83,126) 112,222 29,096 235,267

Cash Flows from Investing ActivitiesInflows:Maturity of Investments 60,556 501,625 562,181 210,530

Outflows:Purchase of Investments -0- (585,785) (585,785) (510,967)

Net Cash Provided by (Used in)Investing Activities 60,556 (84,160) (23,604) (300,437)

Net Increase (Decrease) in Cash andCash Equivalents (22,570) 28,062 5,492 (65,170)

Cash and Cash Equivalents - Beginning of Year 118,728 21,012 139,740 204,910

Cash and Cash Equivalents - End of Year $ 96.158 $ 49.074 $ 145,232 $ 139,740

Supplemental Disclosure of Cash Flow Information:Cash Paid for Income Taxes $ . 86.846 $ 21.626

The accompanying notes are an integralpart of these financial statements

..~ 4''''""'~

lb

LONGMEAD CROSSING COMMUNITY SERVICE ASSOCIATIONNOTES TO FINANCIAL STATEMENTS

DECEMBER 31,2007

ORGANIZATION

The Association was established in 1984 to provide trash and snow removal, lawn maintenance,and preservation and repair and replacement ofthose elements of common areas of the plannedresidential community located in Silver Spring, Marland, known as Longiead Crossing. As ofDecember 31, 2007, its membership totaled 1,292 units.

The Association is charged with the maintenance and upkeep of the common areas and is alsoconcerned with ensuring that the original plan for the design and use ofthe land and homeswithin the community is not altered or changed.

The Association's principal source of income is from community unit owners' assessments. Italso receives income from other user fees and late payment fees, as well as interest earned oninvestments.

NOTE 1- SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A summar of the major accounting policies followed by the Association is setfort below:

Accounting Basis

The Association maintains its records on the accrual basis of accounting inaccordance with U.S. generally accepted accounting principles.

Fund Accounting

The Association uses fund accounting which requires that funds, such as operatingfunds, and restricted funds designated for future major repairs and replacements,be classified separately for accounting and reporting purposes. Disbursementsfrom the operating fund are generally at the discretion of the Board of Directorsand property manager. Disbursements from the replacement fund may be madeonly for designated purposes. Appropriated cash transfers between funds areaccomplished through interfund receivables and payables in the statement offinancial condition.

Assessments and Allowance for Bad Debts

Assessments are recorded as revenue when billed; unit owners are assessedmonthly. An allowance for bad debts in the amount of$29,379 has beenestablished for 2007, as the Association currently does not anticipate the full

'lb'~

~%~ .&eO

5

NOTE 2-

,,;:t'j~

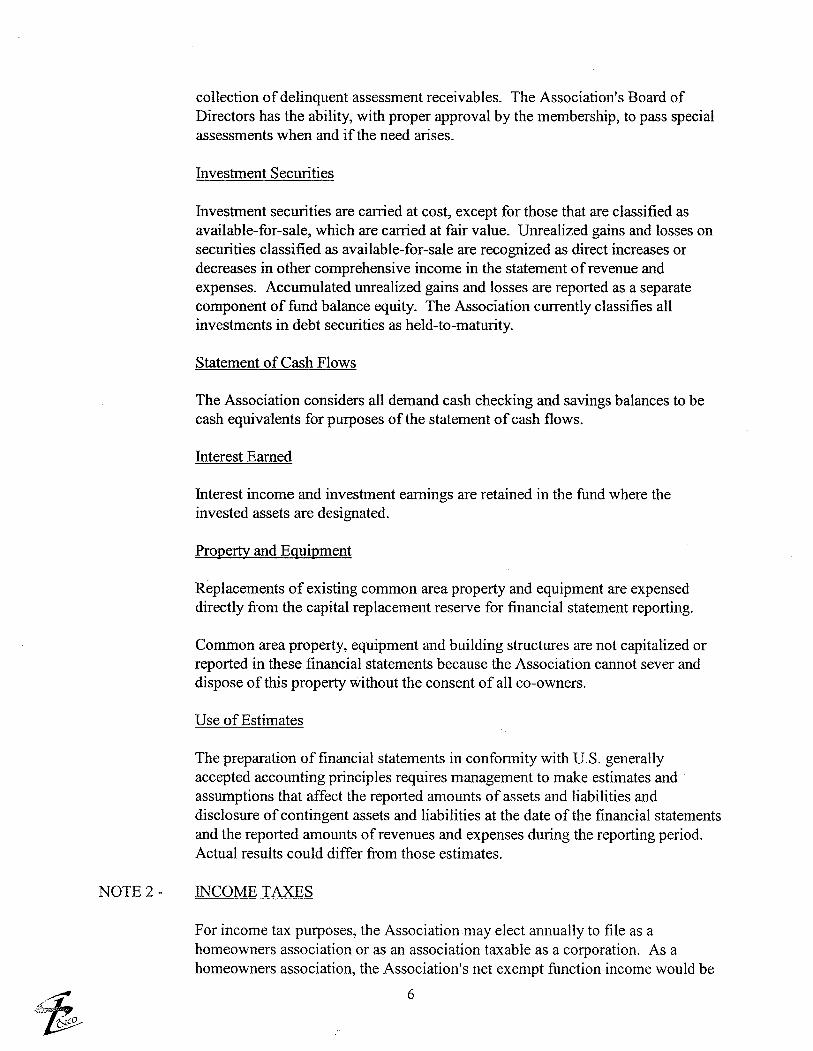

collection of delinquent assessment receivables. The Association's Board ofDirectors has the ability, with proper approval by the membership, to pass specialassessments when and if the need arses.

Investment Securities

Investment securities are cared at cost, except for those that are classified asavailable-for-sale, which are cared at fair value. Unrealized gains and losses onsecurities classified as available-for-sale are recognized as direct increases ordecreases in other comprehensive income in the statement of revenue andexpenses. Accumulated unrealized gains and losses are reported as a separatecomponent of fund balance equity. The Association currently classifies allinvestments in debt securities as held-to-maturity.

Statement of Cash Flows

The Association considers all demand cash checking and savings balances to becash equivalents for purposes of the statement of cash flows.

Interest Eared

Interest income and investment earings are retained in the fund where theinvested assets are designated.

Property and Equipment

Replacements of existing common area property and equipment are expenseddirectly from the capital replacement reserve for financial statement reporting.

Common area property, equipment and building structures are not capitalized orreported in these financial statements because the Association cannot sever anddispose of this property without the consent of all co-owners.

Use of Estimates

The preparation of financial statements in conformity with U.S. generallyaccepted accounting principles requires management to make estimates andassumptions that affect the reported amounts of assets and liabilities anddisclosure of contingent assets and liabilities at the date of the financial statementsand the reported amounts of revenues and expenses during the reporting period.Actual results could differ from those estimates.

INCOME TAXES

For income tax purposes, the Association may elect annually to fie as ahomeowners association or as an association taxable as a corporation. As ahomeowners association, the Association's net exempt function income would be

6

NOTE 3-

NOTE 4-

,ti;;..~

exempt from income tax, but its net non-exempt income would be taxed. Electingto file as a corporation, the Association is taxed on its net income from all sources(to the extent not capitalized or deferred) at normal corporate rates after corporateexemption, subject to the limitation that operating expenses are deductible only tothe extent of income from members. The financial statements reflect the incometax expense calculated as a corporation. The total federal and state tax liability for2007 was $46,269.

FUTURE MAJOR REPAIRS AN REPLACEMENTS

The Association's governing documents do not require that funds be accumulatedfor future major repairs and replacements. If funds are needed, the Associationmay increase regular assessments, pass special assessments, or delay major repairsand replacement until funds are available.

The Association has elected to set aside funds in a capital replacement reserve.Accumulated funds in this account wil generally not be available for normaloperations. Interfund receivables/payables have been established to maintain theallocation of capital replacement funds. The Association's replacement reservefund owes the operating fund $2,992 as of December 31, 2007. There are nodefinite plans to liquidate this interfund obligation in the coming year.

During 2007, $205,296 was expended from the capital reserve fund as follows:

Repair/Maintenance Item Amount

Asphalt/Concrete $ 89,318

Tot Lot 21,875

Pool Furniture 1,988

Pool Repair 61,405

Tennis CourtOther 3,569

Retaining Wall 26,830

Administration 311

TOTAL $ 205,296

OWNERS' ASSESSMENTS

Monthly assessments to community unit owners ranged from $32 to $57 per unitin 2007. Of the total assessment, $130,000 was designated to the capitalreplacement reserve.

The annual budget and owners' assessments are determined by the Board ofDirectors and are approved by the owners. The Association retains excessoperating funds at the end of the operating year, if any, for use in future operatingperiods.

7

NOTE 5- INESTMENTS

The average final maturities of the investments in the Association's portfolio atDecember 31, 2007 and 2006, were as follows:

2007 2006

Federal Agency Debt Securities 59 Months 69 Months

Certificates of Deposit 58 Months 51 Months

The composition of investments as of December 31, 2007 and 2006, is shownbelow:

2007 2006

Federal Agency Debt Securities $ 1,523,012 $ 1,483,786

Certificates of Deposit 2,315,041 2,331,24

Total Investments $ 3,838,053 $ 3,814,910

Held-to-maturity debt securities consist of the following:

December 31, 2007

Gross GrossAmortized Unrealized Unrealized Fair

Cost Gains Losses Value

Federal Agency Debt Securities $ 1.523,012 $ 44,494 $ (93) $ 1.67,413

Total Debt Securities $ 1.523,012 $ 44.494 $ (93) $ 1.567.413

i December 31, 2006

Gross GrossAmortized Unrealized Unrealized Fair

Cost Gains Losses Value

Federal Agency Debt Securities $ 1,483,786 $ 4,1 17 $ (24,874) $ 1,463,029

Total Debt Securities $ 1.483,786 $ 4,117 $ (24,874) $ 1.463,029

4~:¡~8

The following is a summar of matuties for debt securties held-to-matuty as ofDecember 31, 2007 and 2006.

2007 2006

Securties Held-to-Matuty Securties Held-to-MatutyAmounts Matug in: Amortzed Cost Fair Value Amortzed Cost Fair Value

One Year or Less $ 176,866 $ 178,255 $ 54,360 $ 55,075

Afer One Year Through Five Years 413,952 429,223 449,558 450,533

Greater than Five Years 932,194 959,935 979,868 957,421

TOTAL $ 1.523,012 $ 1.567.413 $ 1.483.786 $ 1.463,029

Debt securties temporarly impaired as of December 31, 2007 and 2006, consist

of the following:

December 31, 2007

Less Than 12 Months 12 Months or Longer Total

Gross Gross Gross# Unrealized # Fair Unrealized # Fair Unrealized

Fair Value Losses Value Losses Value LossesU.S. Governent andFederal Agencies 0 $ -0- $ -0- 1 $ 49,907 $ (93) 1 $ 49,907 $ (93)

Tota Temporarly

Impaired Securties 0 $ -0- $ -0- 1 $ 49,907 $ (93) 1 $ 49.907 $ (93)

December 31. 2006

Less Than 12 Months 12 Months or Longer Total

Gross Gross Gross# Unrealized # Fair Unrealized # Fair Unrealized

Fair Value Losses Value Losses Value LossesU.S. Governent and

Federal Agencies 4 $ 184,912 $ (2,287) 19 $ 853,827 $ (22.587) 23 $1,038,739 $ (24,874)

Total TemporarlyImpaired Securties 4 $ 184,912 $ (2.287) 19 $ 853,827 $ (22.587) 23 $1.038.739 $ (24.874)

U.S. Government and Federal Agency Securities - The unealized losses on theAssociation's investments in U.S. Treasur obligations and direct obligations ofagencies created by the U.S. Government were caused by interest rate increases.The contractual terms of these investments do not permit the issuer to settle thesecurities at a price less than the amortized cost of the investments. Because theAssociation has the ability and intent to hold these investments until a recovery offair value, which may be maturity, the Association does not consider theseinvestments to be other-than-temporarily impaired at December 31, 2007 and2006.

9

fè;:..~

SCHREINER1 LEGGE& COMPANY

A Professionol Accounting & Consulting Corporation'

INEPENDENT AUDITOR=S REPORT

June 29, 2008

Board of DirectorsLongiead Crossing Communty

Service AssociationSilver Spring, Marland

The supplementar information on futue major repais and replacements on page 11 is not arequired par of the basic financial statements but is supplementar information required by theAmerican Iistitute of Cerified Public Accountants. We have applied cerain limited procedures,which consisted principally of inquiries of management regarding the methods of measurementand presentation of the supplementar information. However, we did not audit the information

. and express no opinion on it.

~~I L'Y/c:~SCHREINER, LEGGE & COMPANY (JCERTIFIED PUBLIC ACCOUNTANTS

DAVID R. lEGGE.ClAKENNETH M. WElCHClA

AUDRY POMERENING.ClA

2800 Eisenhower Avenue

Suite 100

Alexandrio, VA 22314

10

7033298008008007520

fox 7033299040

.._-_.. -.-,.--.. .--,-'~h.ìï: :(;1 CPt), F'l:Tr::~_

infoiislc-cpa.comwww.slc-cpa.com

LONGMEAD CROSSING COMMUNITY SERVICE ASSOCIATIONSUPPLEMENTARY INFORMATION ON

FUTURE MAJOR REPAIRS AND REPLACEMENTSDECEMBER 31,2007

(UNAUDITED)

The Association's Board of Directors had a study performed in 2003 by Miller DodsonAssociates to estimate the remaining useful lives and the replacement costs of the components ofcommon property. Replacement costs were based on the estimated costs to repair or replace thecommon property components at the date of the study. The study did not account for the effectsof inflation between the date of the study and the date that the components will require repair orreplacement.

The following information is based on the study and presents significant information about thecomponents of common property.

EstimatedComplete Current

Useful Lives ReplacementComponents (Years) Costs

Concrete Components 30 $ 1,070,708

Storm BasinIonds 40-50 585,998

Asphalt 6-20 1,000,296

EntrancelF encing 2-30 696,484

Tennis!Basketball Courts 7-20 60,200

Pool 1 1-50 503,250

Pool 2 1-34 601,180

Tot Lots 2-30 243,785

Retaining Walls 1-5 364,000

TOTAL, $ 5.125,901

The total unallocated capital replacement reserve fund balance as of December 31,2007, was$3,911,212. This balance includes $2,992 due to the operating fund.

The annual recommended minimum contribution using the cash flow method is $132,699. TheAssociation budgeted a contribution of$130,000 and capital replacement reserve investmentsearned an additional $178,694 in 2007.

cf~~'''..&CO,

11

Acct, #

6310632763286329633063336335633863506360638064006910592063156997

71007101714071307160716272807430744075507560787078807890791083019941

7600

Longmead Crossing Community Services Association2008 Approved Budget

Assessments (per unit per month): 2008

Cluster 8 (36 homes)Rest of Homes (1,256 homes)Wintergate at Longmead (456 homes)Longmead Crossing Condos (240 homes)

$32.15$56.65$17.50$17.50

INCOME

Assessment Income

Assessment Biling-WintergateAssessment Income - LCCSAAssessment Income - Other Co.Clubhouse Rental IncomePool Guest Pass IncomeRegistration Fee IncomeSecurity Contract ReimbursementLegal Fees ReimbursementCertified/Lien/NSF IncomeMisc. Homeowner IncomeIncome Tax RefundInterest Income - OperatingMiscellaneous IncomeResale Package IncomeDebt Recovery

TOTAL INCOME

867,71895,76050,400

7507,000

7504,5008,435

24,00017,000

500o

3,500ooo

1,080,313

EXPENSESGeneral and AdministrativeManagement FeesArchitectural EnforcementAudit FeesICC ExpenseLegal Expenses - HomeownerLegal Fees - AssociationInsuranceTaxesPersonal Propert TaxesStreet Light ElectricityRecreation Fee ExpenseResale Package ReimbursementsMisc, Homeowner Admin. FeesMisc. General & AdministrativeCommission on Common OwnershipCommunity Website

Consulting Fees/Reserve StudySub-Total

138,7886,0002,150

o29,00010,00010,50038,000

6,50037,0004,500

o17,000

7502,907

9003,200

307,195

PersonnelContract - Maintenance Man

Sub-Total26,52026,520

74107500

Newsletter/SocialNewsletterSocial & Recreation

Sub-Total

1,000400

1,400

Pool8200 Pool Contract - Pool I

36,650

8201 Pool Contract Pool II67,825

8210 Pool Repairs/Maint - Pool I3,500

8211 Pool Repairs/Maint - Pool II6,000

8220 Pool Supplies - Pool I1,000

8221 Pool Supplies - Pool II1,500

8230 Pool Telephone - Pool I 360

8231 Pool Telephone - Pool II 900

8250 Pool Water & Sewer - Pool I 8,000

8251 Pool Water & Sewer - Pool II 11,500

8350 Electricity - Pool I6,171

8351 Electricity - Pool II20,056

8270 Guard Bonuses750

Sub-Total164,212

Community Room/Building8310 Repairs and Maintenance

2,000

8315 Carpet Cleaning2,520

8330 Improvements1,000

8340 Telephone900

9860 Janitorial Services3,900

9850 Social Director3,600

Sub-Total13,920

Reserve Contributions6999 Reserve Contributions - Replacements

130,000

Sub-Total130,000

Site Maintenance and Repairs9010 Tree Maintenance

12,000

9020 Pond Maintenance Contract3,200

9090 Street Light Repair6,000

9110 Site Maintenance10,000

9115 Improvements - Landscaping8,029

9116 Improvements - Other4,000

9118 Street Cleaning0

9150 HVAC Maintenance1,105

Sub-Total44,334

Contract Services9610 Lawn Contract

177,608

9650 Security System Monitoring1,500

9660 Covenant Patrol40,925

9700 Trash Removal108,289

9705 Trash Patrol4,160

9750 Extermination250

9800 Snow Removal60,000

Sub-Total392,732

TOTAL EXPENSES1,080,313

NET INCOME/(LOSS)°

LONGMEAD CROSSING COMMUNITYSERVICE ASSOCIATION

MAAGEMENT LETTER

DECEMBER 31, 2007

SCHREINER, LEGGE& COMPANY

A Professional Accounting & Consulting Corporotion

May 14, 2008

Board of DirectorsLongmead Crossing Community

Service Associationc/o The Management Group Associates, Inc.20440 Centu Boulevard, Suite 100Germantown, MD 20874

Dear Board Members:

We have completed our audit of the financial statements ofLongmead Crossing CommunityService Association as of December 31, 2007, and have issued an unqualified opinion thereon.

. As a result of our audit, we would like to bring the following comments to your attention.

AUDITING STANDARDS

An audit performed in accordance with U.S. generally accepted auditing standards certainlyaddresses many matters of interest to your Board, such as internal control, adherence to operatingpractices and whether the financial statements are free of material misstatement. It is importantfor the Board to understand that an audit conducted in accordance with U.S. generally acceptedauditing standards is designed to obtain reasonable, rather than absolute, assurance about thefinancial statements being fairly presented in accordance with U.S. generally accepted accountingprinciples, Because of the concept of reasonable assurance and because we did not perform a

detailed examination of all transactions there is a risk that material errors, irregularties, or ilegalacts including fraud and defalcations, may exist and not be detected by us.

As part of our audit, we considered the internal control of Longmead Crossing CommunityService Association. Such considerations were solely for the purpose of determining our auditprocedures and not to provide any assurance concerning such internal control.

DA VID R. lEGGE.ClA

KENNETH M. WElCH.ClAAUDRY POMERENING.ClA

2800 Eisenhower Avenue

Suiie 100

Alexondrio, VA 22314

703.329.800800.80.7520

fox 7033299040

infoiislc'cp.comwww.slc-ca.com

Board of DirectorsLongmead Crossing Community

Service AssociationPage 2 May 14,2008

SIGNIFICANT ACCOUNTING POLICIES

Management has the responsibility for selection and use of appropriate accounting policies. Inaccordance with the terms of our engagement letter, we wil advise management about theappropriateness of accounting policies and their application. The significant accounting policiesused by Longmead Crossing Community Service Association are described in Note 1 to thefinancial statements. No new accounting policies were adopted. We noted no transactionsentered into by the Association durng the period that were both significant and unusual, and ofwhich, under professional standards, we are required to inform you, or transactions for whichthere is a lack of authoritative guidance or consensus.

ACCOUNTING ESTIMATES

Accounting estimates are an integral par of the financial statements prepared by managementand are based on management's knowledge and experience about past and curent events, andassumptions about future events, Certain accounting estimates are paricularly sensitive becauseof their significance to the financial statements, and because of the possibility that futue eventsaffecting them may differ significantly from those expected.

The process management uses to formulate parcularly sensitive accounting estimates, includingthe allowance for bad debts, and the basis concerning the reasonableness of these managementestimates have been reviewed by us.

SIGNIFICANT AUDIT ADJUSTMENTS

Professional standards define a significant audit adjustment as a proposed correction of thefinancial statements that, in our judgment, may not have been detected except through ourauditing procedures. These adjustments may include those proposed by us but not recorded bythe Association that could potentially cause futue financial statements to be materially misstated,even though we have concluded that such adjustments are not material to the current financialstatements.

INTERFUND RECEIVABLE

As of December 31,2007, the capital replacement reserve fund "owes" the operating fund$2,992. Interfund payables should be liquidated anually or additional funding should be

formally approved.

~è~

Board of DirectorsLongiead Crossing CommuntySerice Association

Page 3 May 14, 2008

ADJUSTING ENTRIS

Adjusting entres have been recorded for income taxes payable, accrued income eared, andaccounts payable. We have provided the management company with copies of these adjustmentsand an adjusted tral balance,

IR REVENUE RULING 70-604

Attached to ths report is a sample motion regarding IRS Revenue Ruling 70-604, dealing withexcess operating income and the Association's refud or rollover election requirements, Thsmotion is typically presented at an anual meeting where such an election would be made,

Please ensure that this election is made before filing the 2007 income ta retu and documentthis election in the Board of Directors' minutes. We were unable to locate any documentation ofthis critical approval in 2007. Failure to follow this election correctly could subject theAssociation to additional taxes and penalties.

Because the Association pays a considerable amount in income taxes, the financial penalty forfailure to properly document ths election could be signficant. We canot over-emphasize thecrtical need to complete ths election.

DISTRIBUTION

We than the Board of Directors of Longiead Crossing Community Serce Association forletting us be of serce to you. If we can be of fuher assistance, or if there are any questions

concerning this report, please let us know.

~~/L'Y/~. SCHREINER, LEGGE & COMPANYCERTIFIED PUBLIC ACCOUNTANTS

;è5;;..~.;..."~

~:~~

HQMl5-139

APPENDIX 5C...

ASSOCIATION RESOLUTION FOR REVENUE RULING 70-604 ELECTION-EXCESS INCOME APPLIED TO THE FOLLOWING YEAR'S ASSESSMENT

RESOLUTION OF THE

ASSOCIATION

RE: .EXCESS INCOME APPLIED TO THE FOLLOWING YEA'S ASSESSMENTSREVENUE RULING 70-

WHEREAS, theis à (Name of Stte)ofthe.Stte of

Associationcorporation duly organized and existng under the laws

and

WHEREAS, the members desire that the corporation shall act in full accordance wi the rulings anèlregulations of the Intern Revenue Servce;

.NOW, THEREFORE, the members hereby adopt the following resolution by and on behalf otthe. Asociation:''RESOLVED, that any excess of membership income O\lef membership 'expenses fOf the year ended

,19 , shan be applied against the subsequent ta year member assessment

as provided by IRS Revenue Ruling 70-.

This resolution Is adopted and made a part of the minutes of the meeting of

BYPresident

ATIST:Secreta

Appendix SC-1

c.\

C'.....:. ."/

(

(~.~-:,".-0~

HO8I 5-47~

75-370 and 75-371 (HTL-Appendixes SP and SO)) to either (a) apply the excess net member-ship income to the following year or (b) refund the excess net membership income to theassociation's members. .Excess membership deductions-The excess membership deductons must be carried forwardto offet net membership income in future years, Under the provisions of IRC Secon 2n, it maynot be carried back nor may it be offet against net nonmembership income.

Nonmembership Activities

Net nonmembership income-Net nonmembership income is taed at regular corporate rates.

Net nonmembership lossNet nonmembership losses are treated as net operating losses underIRC Section 172.

503.21 Net Nonmembership Loss When No Profit Motive Exists. Portland Golf Club v. Commissioner(HTL-Appendix 4A) raises an interesting quesion about the nature of a loss from än act for which profimotive cannot be documented,8 The income and expense of the activ meet neither the defniton ofexempt income or expense for an exempt organization nor membership incOme or expns for a nonexemptmembership organization. The Portland case prohibits combining such. a loss wit profi-motiated non-memberShip activities (such as investing activities)' to reduce or eliminate taxble income, The autors donot recommend combining the loss with membership activites because the asociation might conclude ithad an IRC Secon 2n carryover when, in fact, the. loss might be masking table membership income.Consequently, the authors recommend treating the loss as a net operating loss from a specifc activit thatthe association could carr forward,

Using Revenue Ruling 70-604 to Defer Tax on Net Membership Income

503.22 Basic Provisions. Revenue RUling 70- (HTL-Appendix SH) allows asociations to remove anyexcess membership assessments from taxable income by effectively refunding the excess assessments tothe members. (Te authors believe that "excess membership assessments" and "net membership Income"may be used interchangeably and have used them that way In this Guide.) Under the revenue ruling,asociations n:ay make an annual election to exempt or defer net membership income from taation by,lneffect, returning the excess to its members, As stated in the revenue ruling, associations have the followingoptions: .

· Apply the excess of membership income over membership expenses to the following year'sassessments,

· Refund the excess of membership income over membership expenses to the association'smembers.9

503,23 The authors recommend using caution in applying Revenue Ruling 70- beuse the IRS is

currently reconsidering Revenue Ruling 70-S04. The IRS has also specifically stated that the ruling allowsonly a one-year carryover of excess membership income. (See paragraph 503.24.) In addition, the excesassessments discussion in section 803 states the IRS has suggested that Revenue Ruling 70- may notbe used by time-share associations. That ruling may have implications beyond the time-share industr if theIRS applies it in audits of other CIAAs, such as condominium and homeowners' associations, (See para-graph 503.27.)

8 The nature of a loss from an activity for which a profit motive cannot be documented is not an issue forassociations that file Form 1120-H because IRC Section 528 does not allow net operating loss deductions.Thus, the loss would simply be terminated and would be a concern only if the activity were to becomeprofitable at a later date.

The authors do not recommend this alternative, and it may conflict with certain state statutes.9

503.23

~..- - .._..- .-.. .".~.~~..

HOA8/

5-4

503.24 Making the Election. There is virtually no authoritative guidance about how associations mayproperl make a 7() elecon alough the reue ruling ha ben in efct since 1970. Freueny r.. .encountd isses abou making th eleion an the auors' recomendations ar discd belo. ~ . .

....-J.

a. The 70-604 election should be made by the members.

Recent audit act indicates that IRS agents are requiring the elecon to be made by the members,

Absent clarifcation, the authors recommend that associations interpret the wording

of Revenue

Ruling 70- literally and make the electon in the form of a resoluton adopted by the membership,(See Appendix 56.)

b~ The 70-604 election must be made before the tax retum is fied.

Revenue Ruling 70-604 simply states, "A meeting is held each year. . . ."it doe not specif

whether

the meetng should be held before year end or merely before the ta return is filed. Tax rules do notestablish a consistent time for making ta elecons; rather, the timing of most ta elecons is spelledout either in the Internal Revenue Code, regulations,revenue rulings, or other authoritative ta .sources. The timing of the 70- elecion is not addressed, however, Thus, to minimize the risk of

losing the benef of the elecon, the autors recmmend that associations make the elecon befrethe end of the fiscal year for which it is to apply. The election must be made before the ta return isfiled,

c. It is not necessary to state the specifc dollar amount of excess membership income in the election;

Since the 70-604 election should preferably be made before year end and the excess membershipincome cannot be determined until after the end of the year when separate calculations ofmembership and nonmembership income are made, some accountants recommend thatassociations make the elecon, but leave a blank for the amount to be filled in later. When the speifc C-. -. '.amount is determined, it could be documented in the minutes of an asociation meeng and addedto the resolution, In the authors' opinion, however, a

specific dollar amount need not be

included

in the resoluton becuse Revenue Ruling 70- literally states that "any excess asesmen" maybe carred over or refunded, Some accountats also believe that it is prudent not to specif a dollaramount in the election, Thus, if an association is audited and a

capital contribution denied or the

allocation of expenses questioned, a blanket 70-604 election serves to keep the membershipincome untaxed,

d, Thé 70-604 carrover of excess membership income over membership expenses that is applied tothe following year's assessments should be included on Schedule M-1 (or M-3) on the association'stax return,

The autors believe that the carrover should be shown as a SChedule M-1 (or M-3) adjustent sinc

(as a ta-only elecion) it is not recorded in the financial statements. Asociations that file Form 1120wil have either a Revenue Ruling 70-604 net membership income carryover (70-6 carrover) or

an IRC Secon 277 net membership loss caover (277 caover) at the end of each ta year. Onlyif the association had net membership income equal to zero at the end of the tax year could adiferent situation result. Since that situation is highly unlikely to occur at any given year end, eithera 70-604 carryover or a 277 carryover wil generally result. The two carryovers cannot coexist atyear-end, as the larger carryover wil offet (or use up) the other carryover. For example, a 70-604carryover from Year 1 gets carried into Year 2. It may remain unchanged (if the net membershipincome equals zero, which is unlikely), it may increase as the result of additional net membershipincome generated in Year 2 (and assuming that you subscribe to the theory that 70- carroverscontinue indefinitely (see point e.)), or it may decrease as a result of being offet (reduced) by netmembership losses generated in Year 2. If the IRC 277 losses generated in Year 2 exceed the 70-carrover frm Ye 1. then a 277 los carer will exis at the end of Year 2 an will ca (N to (

Year 3. (See Exhibit 5-11 for a graphic presentation of the treatment of 70-604 and 277 carrovers.) _.

,':i 503.24/0-