Embed Size (px)

Citation preview

J. K. Dietrich - FBE 532 – Spring, 2006

Module II: Private Equity Financing

Week 4 –February 2, 2006

J. K. Dietrich - FBE 532 – Spring, 2006

Objectives of this Lecture

Contrast venture capital, hedge funds, and other sources of private equity

Discuss the role of venture capitalists in providing capital to new firms and to companies attempting to go private

Understand why leveraged buyouts are profitable and how LBOs are done

Analyze the impact of LBOs

J. K. Dietrich - FBE 532 – Spring, 2006

Private Equity Managed pools of capital not subject to

SEC review or regulation Major types are venture capital, hedge

funds, and other limited partnerships Most funds are managed by specialized

experts who are general partners Funds are raised in “rounds” and have

specified goals and time limits Efforts to regulate hedge funds by SEC

J. K. Dietrich - FBE 532 – Spring, 2006

Venture Capital Venture capital is a global phenomenon

although it is largest in the United States Venture capitalists invest in firms started by

entrepreneurs They are a temporary source of financing

with a limited time horizon They provide entrepreneurs with more than

money– Management advice and strategic planning– Personnel services– Additional financing

J. K. Dietrich - FBE 532 – Spring, 2006

Venture Capital

Venture capital is early stage financing of new and young firms looking to grow quickly

Venture capitalists are an important source of funds for these firms

Venture capital is also critical when a company goes private.

J. K. Dietrich - FBE 532 – Spring, 2006

Types of Venture Capitalists

Venture capitalists supply capital; there are several types:– High Net Worth Individuals (“Angels”) and

Families– Private Partnerships and Corporations

» Arthur Rock & Co.

– Large Industrial or Financial Corporations» Example: Citicorp Venture Capital

J. K. Dietrich - FBE 532 – Spring, 2006

Venture Capital Financing Stages

Several distinct stages– Seed money: to “prove” the product or concept– Start-up: Funds for marketing and product

development for new firms– First-Round Financing: Supplements to

start-up funds to begin sales and manufacturing

J. K. Dietrich - FBE 532 – Spring, 2006

Venture Capital Financing Stages

– Second-Round Financing: Funds earmarked for working capital beyond first-stage financing

– Mezzanine Financing: Financing for a profitable firm contemplating expansion

– Bridge Financing: Funds for firms likely to go public within a year.

J. K. Dietrich - FBE 532 – Spring, 2006

Venture Capital

In IPO situations, venture capitalists often require rates of return of 25-50% on an annualized basis

To achieve this with loans, they usually demand and get warrants (“equity kickers”) that effectively give them an equity stake as well.

J. K. Dietrich - FBE 532 – Spring, 2006

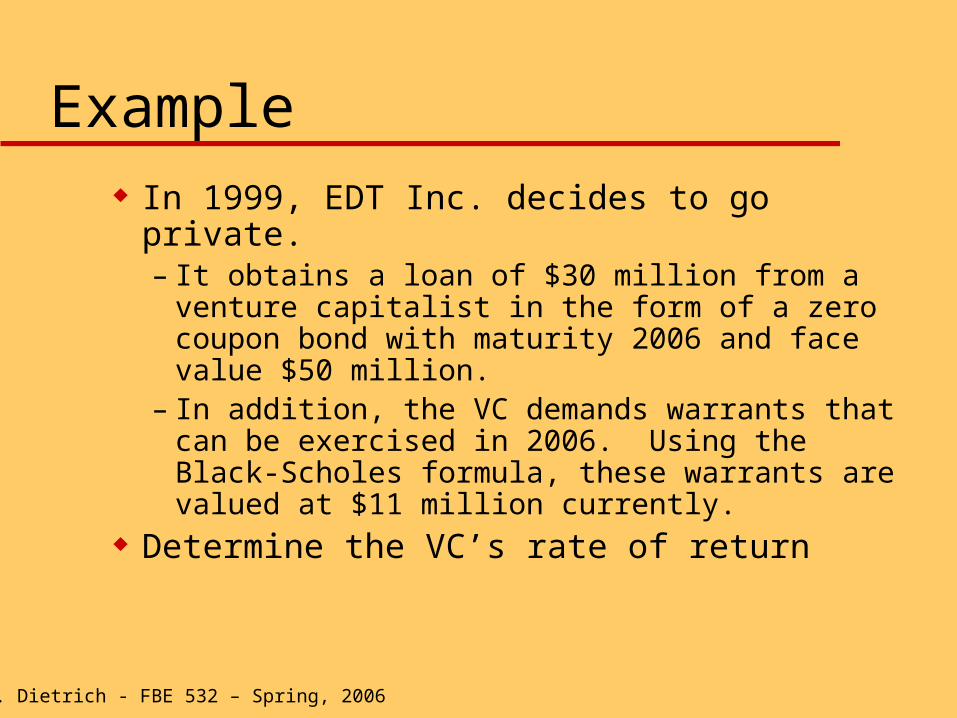

Example

In 1999, EDT Inc. decides to go private. – It obtains a loan of $30 million from a venture

capitalist in the form of a zero coupon bond with maturity 2006 and face value $50 million.

– In addition, the VC demands warrants that can be exercised in 2006. Using the Black-Scholes formula, these warrants are valued at $11 million currently.

Determine the VC’s rate of return

J. K. Dietrich - FBE 532 – Spring, 2006

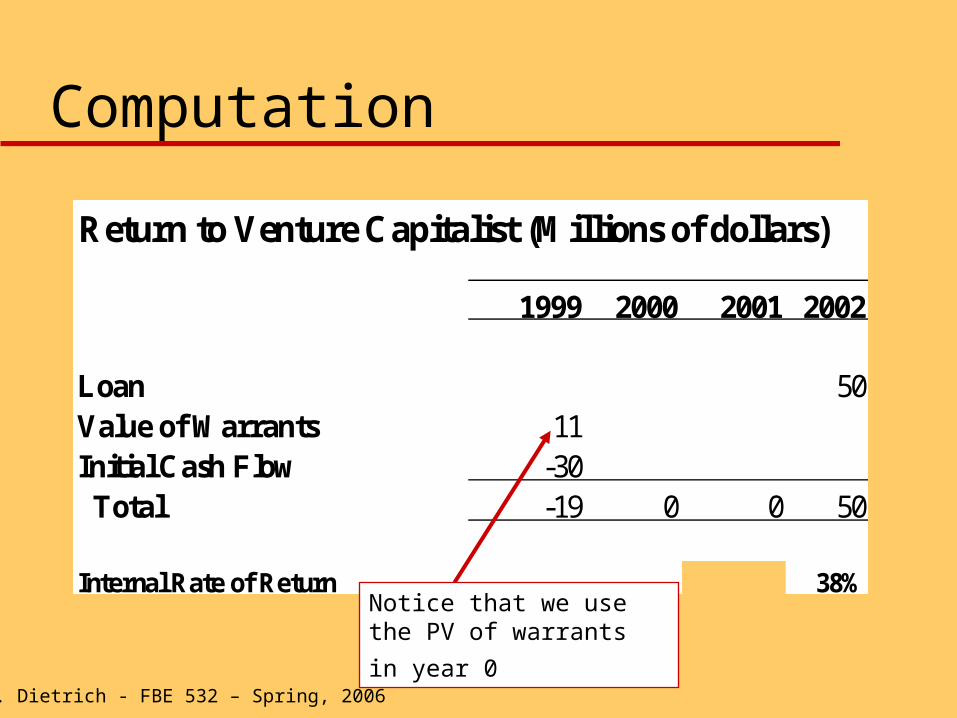

Return to Venture Capitalist (Millions of dollars)

1999 2000 2001 2002

Loan 50Value of Warrants 11Initial Cash Flow -30 Total -19 0 0 50

Internal Rate of Return 38%

Computation

Notice that we use the

PV of warrants in year 0

J. K. Dietrich - FBE 532 – Spring, 2006

Issues in LBOs

Why do LBOs occur? How are such deals structured? How can venture capitalists obtain their

required rates of return? What is the source of value?

Do LBOs represent an expropriation of shareholder wealth by management? Do they hurt minority shareholders?

J. K. Dietrich - FBE 532 – Spring, 2006

Hedge Funds

Name comes from “short-long” strategies and use of hedging strategies

Subject of intense interest globally and in U.S. because of failure of LTCM

Hedge funds are evolving– Multiple strategies– Active role in management– Assuming credit risk and others in hedged

portfolios

J. K. Dietrich - FBE 532 – Spring, 2006

Types of LBOs

Going Private: This occurs if the entire public stock interest of the firm is bought by management exclusively; this is sometimes known as a management buyout

LBO: Ownership in the subsequent private firm is shared by management and third-party investors and some (often large) financing in the form of debt

J. K. Dietrich - FBE 532 – Spring, 2006

Anatomy of Going Private

Merger: Management forms a shell that merges with the original firm, paying with cash or securities; requires shareholder approval.

Asset Sales: Similar in that a vote is required, and assets are purchased by a shell corporation owned by management

J. K. Dietrich - FBE 532 – Spring, 2006

Anatomy of Going Private

Tender Offer: No vote required, and minority shareholders are not required to involuntarily surrender their shares

Reverse Stock-Split: requires holders of fractional shares to sell their ownership back to the firm -- rare

J. K. Dietrich - FBE 532 – Spring, 2006

Anatomy of an LBO

Leveraged buyouts involve purchase of the entire public stock interest of the firm

Typically, the transaction is heavily debt financed; additional sources of funds are often found in the cash reserves of the firm itself

J. K. Dietrich - FBE 532 – Spring, 2006

Financing an LBO

LBOs are often financed with several layers of non-equity financing such as senior debt, subordinated debt, convertible debt, and preferred stock.

Mezzanine level financing refers to the securities between senior debt and common stock, e.g., subordinated and convertible debt

J. K. Dietrich - FBE 532 – Spring, 2006

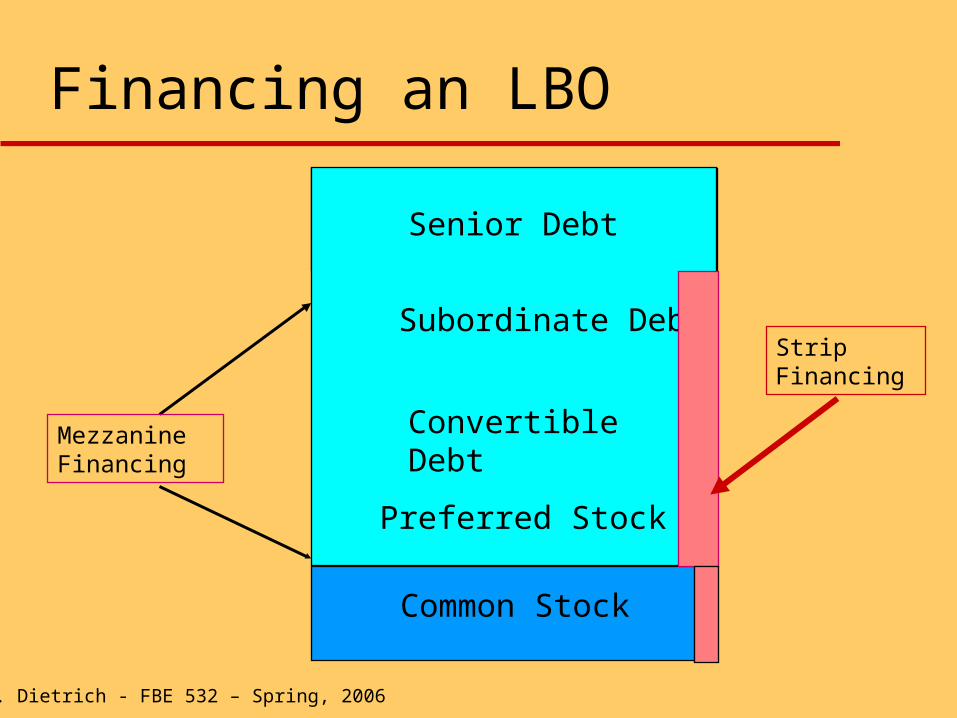

Financing an LBO

Subordinate Debt

Preferred Stock

Convertible Debt

Senior Debt

Common Stock

Strip Financing

Mezzanine Financing

J. K. Dietrich - FBE 532 – Spring, 2006

Financing an LBO

Strip financing is common in LBOs This requires that a buyer purchasing, say,

12% of any mezzanine level security must also purchase 12% of all mezzanine level securities and some equity

J. K. Dietrich - FBE 532 – Spring, 2006

Financing an LBO

Strip Financing has two advantages– As each level of financing senior to equity goes

into default, the strip holder automatically gets new rights to intercede in the organization.

– Eliminates conflicts between senior and junior claim holders

J. K. Dietrich - FBE 532 – Spring, 2006

Sources of Financing

Senior Debt: Usually banks Equity: Venture capitalists (up to 80%)

and management; venture capitalists usually get warrants attached to bonds

Mezzanine: Third-party financiers, holding strips and maybe equity as well

J. K. Dietrich - FBE 532 – Spring, 2006

LBO Targets

Firms with large cash flows Firms in less risky industries with stable

profits Firms with unutilized debt capacity Example

– O. M. Scott

J. K. Dietrich - FBE 532 – Spring, 2006

Gains from LBOs

Reduced regulatory and listing costs:– Exchange registration and listing costs and

shareholder servicing costs are eliminated– If costs are, say, $200,000 annually, the present

value at 10% is $2 million, which may be significant for small firms

– For large firms, these gains may be insignificant.

J. K. Dietrich - FBE 532 – Spring, 2006

Gains from LBOs

Reduction in agency costs: – LBOs align the interests of management and

shareholders, increasing management performance

– Management has strong incentives to cut costs given the high ratio of interest expense to cash flow -- this may lead to “downsizing” that hurts other stakeholders

J. K. Dietrich - FBE 532 – Spring, 2006

Gains from LBOs

Increased monitoring: – High debt provides strong incentives for

outside auditing by the lenders and venture capitalists

– The conflicts between stockholders and bondholders may be reduced; strip financing allows quick replacement of management

J. K. Dietrich - FBE 532 – Spring, 2006

Free Cash Flow Argument

When the firm’s actual growth rate is less than its sustainable growth rate, cash accumulates within the corporation:– Although this belongs to shareholders, it is

controlled by management– Jensen observes that managers may waste

shareholder wealth High debt places limits on such managerial

“excess”

J. K. Dietrich - FBE 532 – Spring, 2006

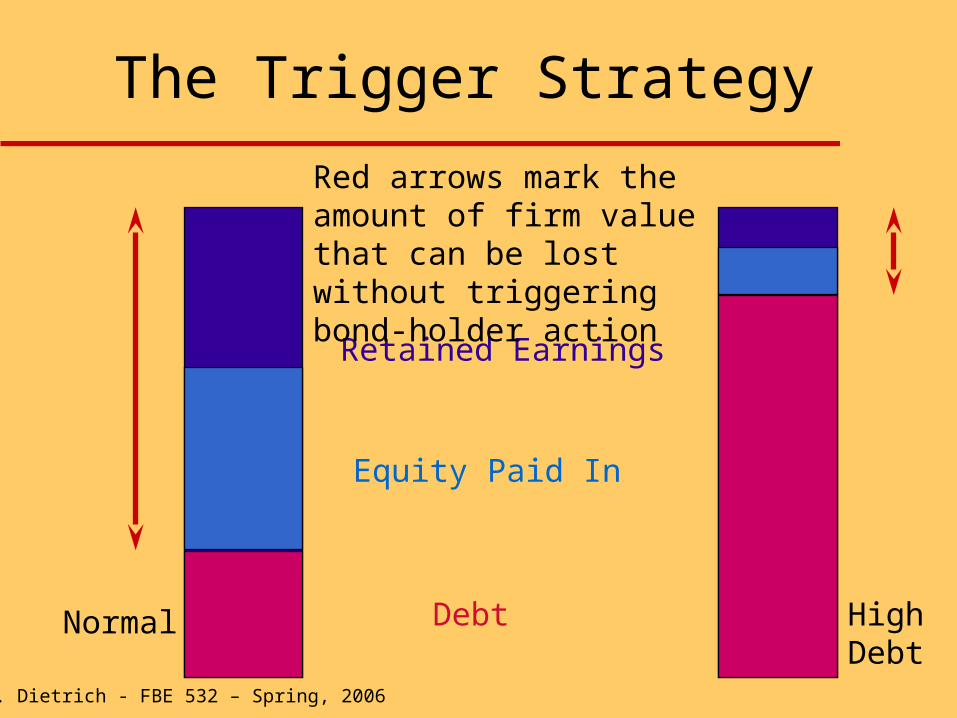

The Trigger Strategy

Debt

Equity Paid In

Retained Earnings

Red arrows mark the amount of firm value that can be lost without triggering bond-holder action

Normal HighDebt

J. K. Dietrich - FBE 532 – Spring, 2006

The Trade-Off

The costs of financial distress may be reduced as reorganization is triggered earlier.

But the commitment of free cash flow to service debt reduces management discretion.

J. K. Dietrich - FBE 532 – Spring, 2006

Evaluation

The free cash flow argument will work for companies that derive value from assets in place rather than discretionary investment

For companies with high R&D costs and high capital expenditures, you may cut muscle with the fat.

J. K. Dietrich - FBE 532 – Spring, 2006

Example of O.M. Scott

O.M. Scott was a division of ITT; in 1986, there was a divisional LBO

Venture capitalists were Clayton and Dublier, with 70% of equity

Post-buyout leverage was 90%

J. K. Dietrich - FBE 532 – Spring, 2006

O.M. Scott

Operating performance increased in 1986-1988– EBIT rose 56% (Baker and Wruck)

Organizational changes focused on incentives– Bonuses for top managers increased dramatically

– There was increased monitoring because of covenants

J. K. Dietrich - FBE 532 – Spring, 2006

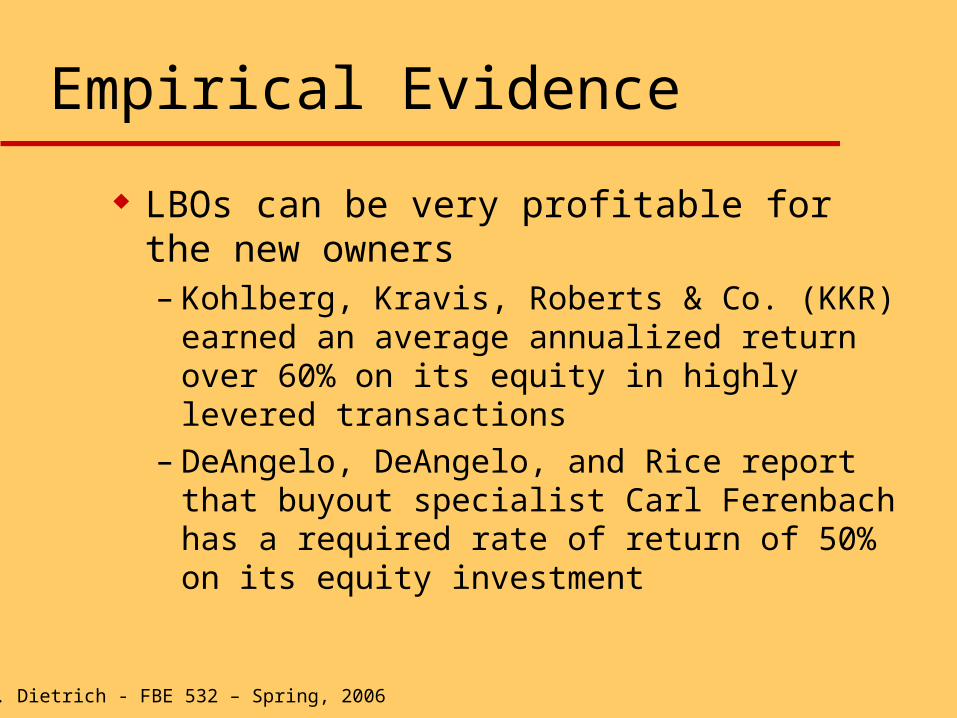

Empirical Evidence

LBOs can be very profitable for the new owners– Kohlberg, Kravis, Roberts & Co. (KKR) earned

an average annualized return over 60% on its equity in highly levered transactions

– DeAngelo, DeAngelo, and Rice report that buyout specialist Carl Ferenbach has a required rate of return of 50% on its equity investment

J. K. Dietrich - FBE 532 – Spring, 2006

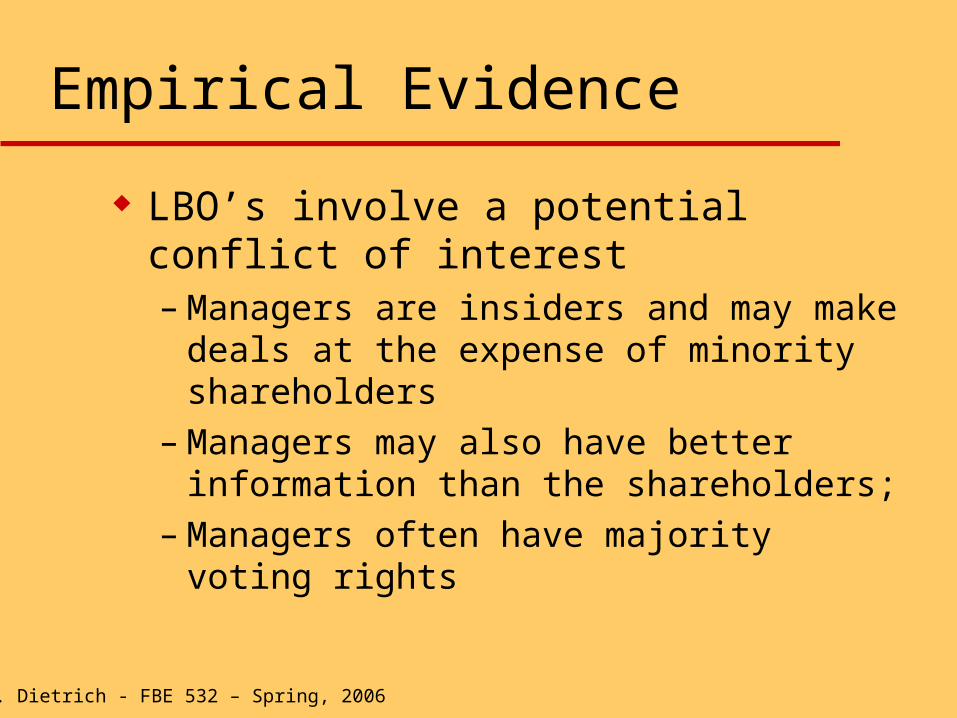

Empirical Evidence

LBO’s involve a potential conflict of interest– Managers are insiders and may make deals at

the expense of minority shareholders– Managers may also have better information

than the shareholders; – Managers often have majority voting rights

J. K. Dietrich - FBE 532 – Spring, 2006

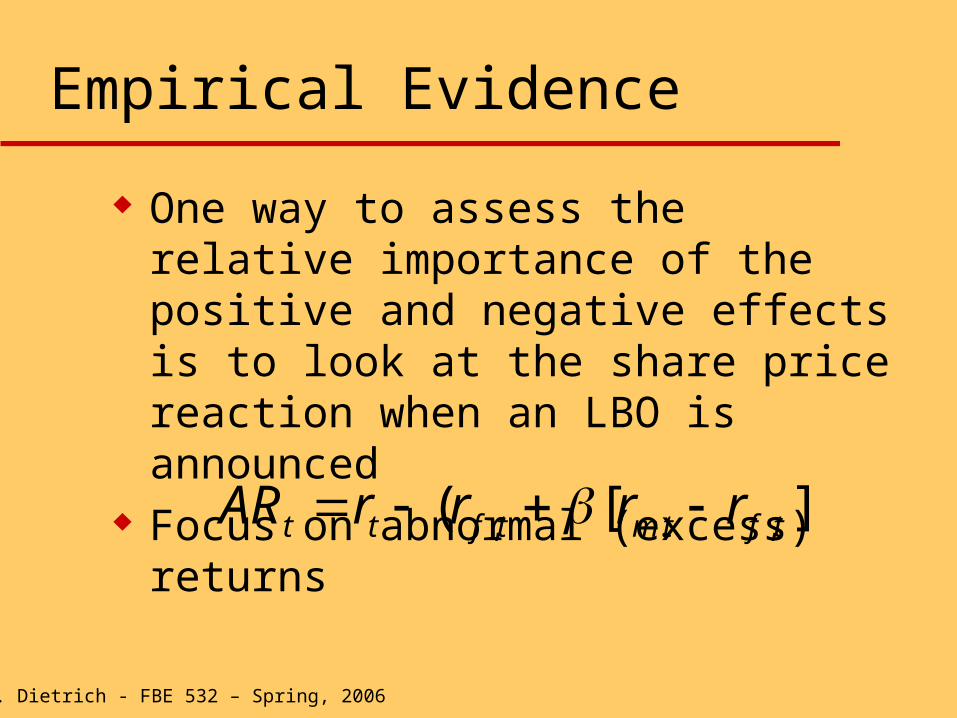

Empirical Evidence

One way to assess the relative importance of the positive and negative effects is to look at the share price reaction when an LBO is announced

Focus on abnormal (excess) returns

][( ,., tftmtftt rrrrAR

J. K. Dietrich - FBE 532 – Spring, 2006

Empirical Evidence

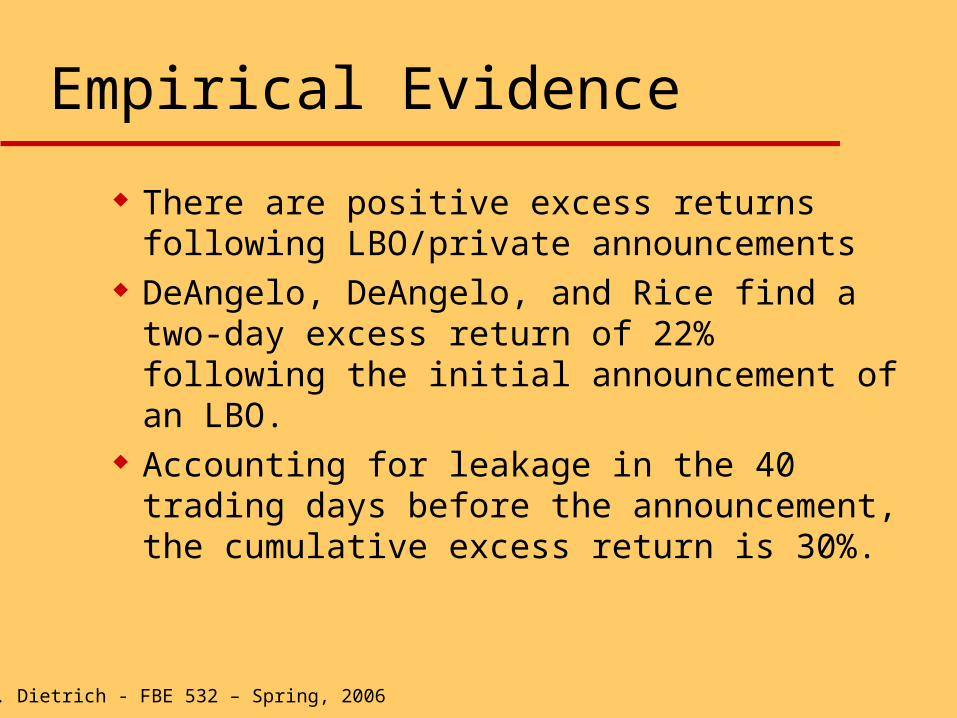

There are positive excess returns following LBO/private announcements

DeAngelo, DeAngelo, and Rice find a two-day excess return of 22% following the initial announcement of an LBO.

Accounting for leakage in the 40 trading days before the announcement, the cumulative excess return is 30%.

J. K. Dietrich - FBE 532 – Spring, 2006

Empirical Evidence

However, these returns are below the 56% average premium offered in LBO transactions

The difference is explained by the high percentage of offers (23%) withdrawn following announcement

J. K. Dietrich - FBE 532 – Spring, 2006

Problems

The problem is that we cannot separate the effect of good insider information from the other benefits such as the reduction in agency costs

Accordingly, research has focused on whether minority shareholders win or lose

J. K. Dietrich - FBE 532 – Spring, 2006

Minority Shareholders

For offers that are subsequently withdrawn, prices Spring by 9%

Clearly, even minority shareholders benefit from LBOs

The division of the gains is still an open question

J. K. Dietrich - FBE 532 – Spring, 2006

Alternatives to LBOs

Cost-cutting associated with LBOs often gives them a bad name

One option is a voluntary restructuring Donaldson discusses the case of General

Mills

J. K. Dietrich - FBE 532 – Spring, 2006

Restructuring and General Mills

In the 1980s, the company was over-diversified and lacked focus

They decided to concentrate on core areas Change in incentive compensation to focus

on ROE

J. K. Dietrich - FBE 532 – Spring, 2006

Results

In 1980, General Mills had a ROE of 16.7% By 1989, ROE had risen to 56.6% Positive stock Market response

J. K. Dietrich - FBE 532 – Spring, 2006

Caveats

Debt also increased: The leverage ratio rose from 27% to 74%

Orderly implementation “LBO-like” But, did it take too long?

J. K. Dietrich - FBE 532 – Spring, 2006

Conclusions

Highly levered transactions are a source of value; restructurings may do the same

Although they can be highly profitable, the evidence is difficult to interpret

There is no evidence that minority shareholders are hurt as a result of LBOs - the same cannot be said of other stakeholders

J. K. Dietrich - FBE 532 – Spring, 2006

Next Week – February 9

Review RWJ, Chapter 22 to 24 Read Term Sheet Negotiations for

Trendsetter Inc. case and begin to think about the issues