Embed Size (px)

Citation preview

Investor DayApril 2015

2

Disclaimer

The information contained herein has been prepared for the use in this Presentation (the “Presentation”) and has not been independently verified. Such information is confidential

and is being provided to you solely for your information and may not be reproduced, retransmitted, further distributed to any other person or published, in whole or in part, for any

purpose.

The opinions presented herein are based on general information gathered at the time of writing and are subject to change without notice. Certain industry, market and competitive

position data contained in this Prospectus come from official or third party sources believed to be reliable but ALROSA does not guarantee its accuracy or completeness.

This Presentation contains statements about future events and expectations that are forward-looking statements. Any statement in this Presentation that is not a statement of

historical fact is a forward-looking statement that involves known and unknown risks, uncertainties and other factors which may cause the ALROSA’s actual results, performance

or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Past performance

should not be taken as an indication or guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance. ALROSA

assumes no obligation to update, supplement or revise forward-looking or any other statements contained herein to reflect actual results, changes in assumptions or changes in

factors affecting these statements. ALROSA does not intend or have any duty or obligation to update or to keep current any information contained in this Presentation.

The diamond resources and reserves estimates provided in this Presentation have been prepared and presented in accordance with the standards and classifications of the

JORC Code (the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves as promulgated by the Australasian Joint Ore Reserves

Committee), which differ in significant respects from the standards and classifications applicable to the disclosure of mineral resources and reserves under the laws and

regulations of certain other jurisdictions, including the regulations of the U.S. Securities Exchange Commission (the “SEC”) with respect to registration statements and other

documents filed with the SEC. Among other things, in accordance with the JORC Code, this Presentation provides certain mineral resources estimates classified as “inferred”,

“indicated” or “measured”, which differ in significant respects from “probable” and “proven” mineral reserves estimates and are not disclosed in certain jurisdictions, including in

SEC filings. There can be significant uncertainty as to whether mineral resources can ever be feasibly and commercially mined. For further explanation of the JORC Code, see

the JORC website at www.jorc.org.

This Presentation does not constitute an offer to sell, or any solicitation of any offer to subscribe for or purchase, any securities. No part of this Presentation, nor the fact of its

distribution, should form any basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever.

The information in this Presentation is subject to verification, completion and change. No representation or warranty or undertaking, express or implied, is made as to, and no

reliance should be placed on, the accuracy or completeness of the information or opinions contained in this Presentation. None of ALROSA nor any of its shareholders, directors,

officers or employees, affiliates, advisors, representatives nor any other person accepts any liability whatsoever for any loss howsoever arising from any use of this Presentation

or its contents or otherwise arising in connection therewith.

This Presentation is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other

jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such

jurisdiction.

This Presentation is not for distribution, directly or indirectly, to the public in the United States (including its territories and possessions, any State of the United States and the

District of Columbia). These materials are not an offer or solicitation to purchase or subscribe for securities in the United States or any other jurisdiction. Securities may not be

offered or sold in the United States absent registration with the U.S. Securities and Exchange Commission or an exemption from registration under the U.S. Securities Act of

1933, as amended. ALROSA does not intend to register any part of any offering in the United States or to conduct a public offering of any of its securities in the United States.

By attending a meeting where this Presentation is made or reviewing this Presentation you acknowledge and agree to be bound by the foregoing.

3

Presenting team

Ilya Ryashchin

Igor Kulichik

Sergei Mezhokh

Acting CEO, First Vice President

CFO, Vice President

Head of IR

4

Content

ALROSA at a glance1 5

Diamond Industry2 7

Production3 14

Marketing4 20

Financial Performance5 25

ALROSA Tomorrow6 32

Appendix7 40

5

ALROSA at a glance

6

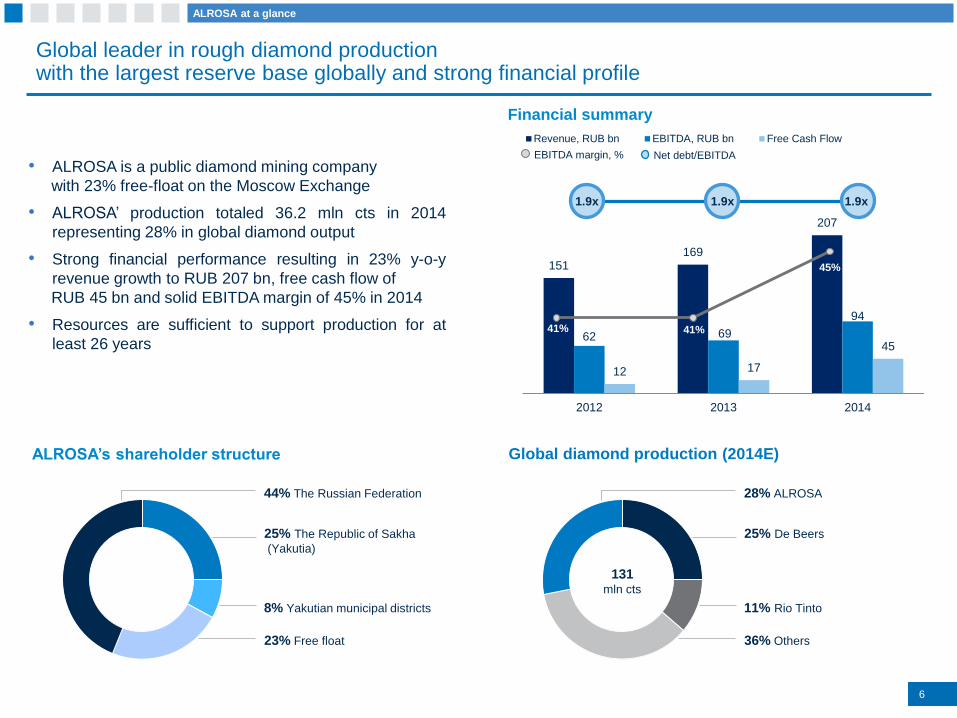

Global leader in rough diamond production with the largest reserve base globally and strong financial profile

44% The Russian Federation

25% The Republic of Sakha

(Yakutia)

8% Yakutian municipal districts

23% Free float

ALROSA’s shareholder structure

151169

207

62 69

94

12 17

45

0

50

100

150

200

2012 2013 2014

Revenue, RUB bn EBITDA, RUB bn Free Cash Flow

Financial summary

Global diamond production (2014E)

• ALROSA is a public diamond mining company

with 23% free-float on the Moscow Exchange

• ALROSA’ production totaled 36.2 mln cts in 2014

representing 28% in global diamond output

• Strong financial performance resulting in 23% y-o-y

revenue growth to RUB 207 bn, free cash flow of

RUB 45 bn and solid EBITDA margin of 45% in 2014

• Resources are sufficient to support production for at

least 26 years

ALROSA at a glance

28% ALROSA

25% De Beers

11% Rio Tinto

36% Others

131mln cts

41% 41%

45%

EBITDA margin, %

1.9x 1.9x 1.9x

Net debt/EBITDA

7

Diamond Industry

8

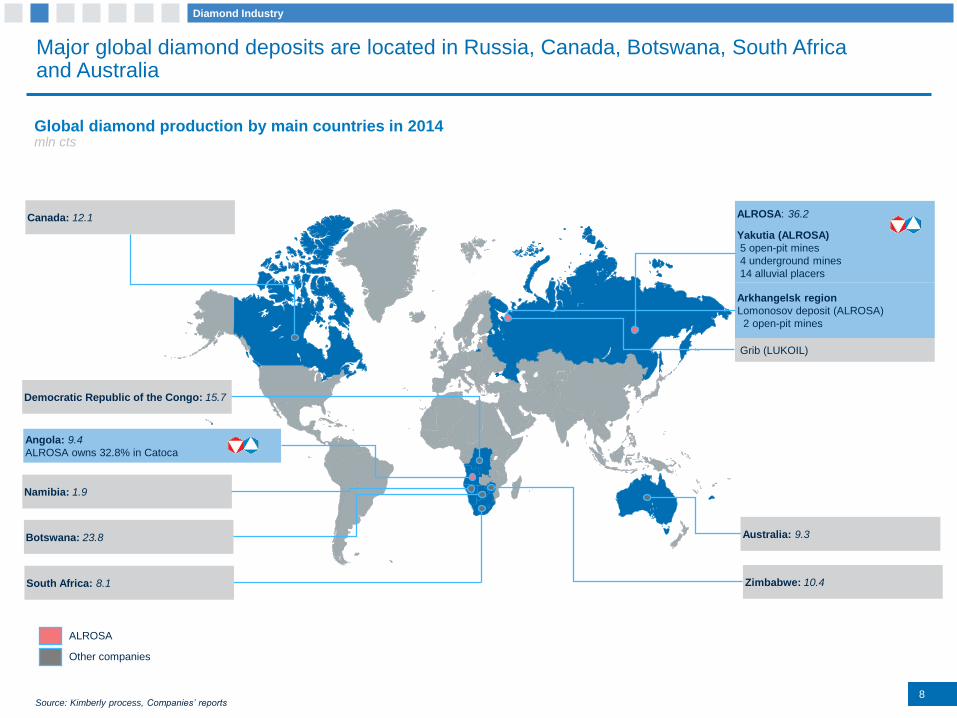

Major global diamond deposits are located in Russia, Canada, Botswana, South Africa and Australia

Australia: 9.3

ALROSA

Other companies

Yakutia (ALROSA)

5 open-pit mines

4 underground mines

14 alluvial placers

Botswana: 23.8

Angola: 9.4

ALROSA owns 32.8% in Catoca

Canada: 12.1

Democratic Republic of the Congo: 15.7

Arkhangelsk region

Lomonosov deposit (ALROSA)

2 open-pit mines

Grib (LUKOIL)

Zimbabwe: 10.4

Namibia: 1.9

mln cts

ALROSA: 36.2

Global diamond production by main countries in 2014

Diamond Industry

South Africa: 8.1

Source: Kimberly process, Companies’ reports

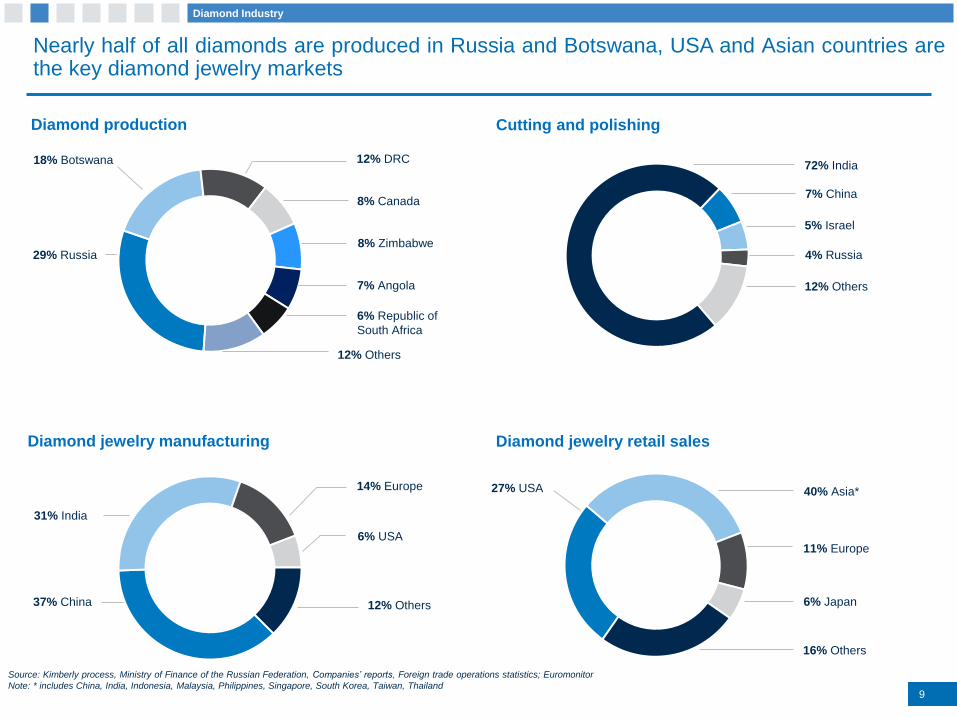

Diamond jewelry manufacturing

Nearly half of all diamonds are produced in Russia and Botswana, USA and Asian countries arethe key diamond jewelry markets

Source: Kimberly process, Ministry of Finance of the Russian Federation, Companies’ reports, Foreign trade operations statistics; Euromonitor

Note: * includes China, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan, Thailand

Diamond production

9

Cutting and polishing

Diamond jewelry retail sales

72% India

12% Others

7% China

5% Israel

4% Russia

27% USA

16% Others

11% Europe

40% Asia*

6% Japan37% China 12% Others

14% Europe

6% USA

31% India

29% Russia

18% Botswana

8% Zimbabwe

8% Canada

12% DRC

12% Others

7% Angola

6% Republic of

South Africa

9

Diamond Industry

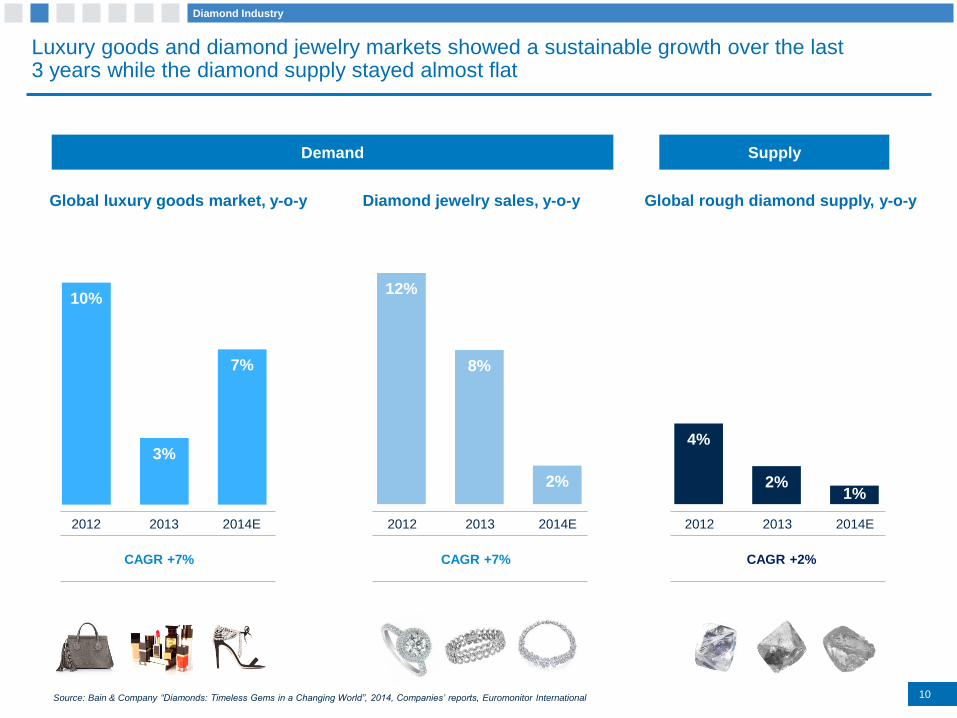

Luxury goods and diamond jewelry markets showed a sustainable growth over the last 3 years while the diamond supply stayed almost flat

Source: Bain & Company “Diamonds: Timeless Gems in a Changing World”, 2014, Companies’ reports, Euromonitor International

Diamond jewelry sales, y-o-yGlobal luxury goods market, y-o-y

10%

3%

7%

12%

8%

2%

2012 2013 2014E 2012 2013 2014E

Global rough diamond supply, y-o-y

4%

2%1%

2012 2013 2014E

Demand Supply

10

CAGR +7% CAGR +7% CAGR +2%

Diamond Industry

11

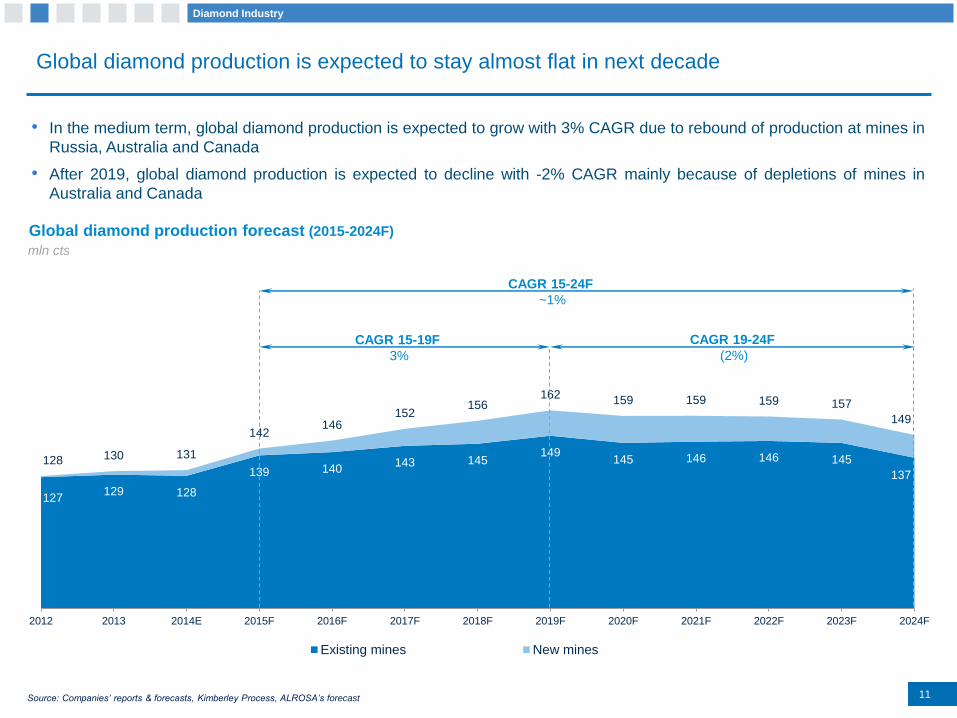

Global diamond production is expected to stay almost flat in next decade

• In the medium term, global diamond production is expected to grow with 3% CAGR due to rebound of production at mines in

Russia, Australia and Canada

• After 2019, global diamond production is expected to decline with -2% CAGR mainly because of depletions of mines in

Australia and Canada

Source: Companies’ reports & forecasts, Kimberley Process, ALROSA’s forecast

127129 128

139 140143 145

149145 146 146 145

137

128 130 131

142146

152156

162159 159 159 157

149

2012 2013 2014E 2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2024F

Existing mines New mines

Global diamond production forecast (2015-2024F)

CAGR 15-19F

3%

CAGR 19-24F

(2%)

CAGR 15-24F

~1%

mln cts

Diamond Industry

35

77

133

0,00

50,00

100,00

150,00

2006 2010 2014

9.8

10.2

11.2

9,09 9,10 9,10 9,10 9,11 9,11 9,11 9,11 9,12 9,12 9,12 9,13 9,13 9,13 9,14 9,14 9,14 9,14 9,15 9,15 9,15 9,16 9,16 9,16 9,17 9,17 9,17 9,17 9,18 9,18 9,18 9,19 9,19 9,19 9,20 9,20 9,20 9,20 9,21 9,21 9,21 9,22 9,22 9,22 9,23 9,23 9,23 9,23 9,24 9,24 9,24 9,25 9,25 9,25 9,26 9,26 9,26 9,27 9,27 9,27 9,27 9,28 9,28 9,28 9,29 9,29 9,29 9,30 9,30 9,30 9,30 9,31 9,31 9,31 9,32 9,32 9,32 9,33 9,33 9,33 9,33 9,34 9,34 9,34 9,35 9,35 9,35 9,36 9,36 9,36 9,36 9,37 9,37 9,37 9,38 9,38 9,38 9,39 9,39 9,39 9,39 9,40 9,40 9,40 9,41 9,41 9,41 9,42 9,42 9,42 9,42 9,43 9,43 9,43 9,44 9,44 9,44 9,45 9,45 9,45 9,45 9,46 9,46 9,46 9,47 9,47 9,47 9,48 9,48 9,48 9,49 9,49 9,49 9,49 9,50 9,50 9,50 9,51 9,51 9,51 9,52 9,52 9,52 9,52 9,53 9,53 9,53 9,54 9,54 9,54 9,55 9,55 9,55 9,55 9,56 9,56 9,56 9,57 9,57 9,57 9,58 9,58 9,58 9,58 9,59 9,59 9,59 9,60 9,60 9,60 9,61 9,61 9,61 9,61 9,62 9,62 9,62 9,63 9,63 9,63 9,64 9,64 9,64 9,64 9,65 9,65 9,65 9,66 9,66 9,66 9,67 9,67 9,67 9,67 9,68 9,68 9,68 9,69 9,69 9,69 9,70 9,70 9,70 9,71 9,71 9,71 9,71 9,72 9,72 9,72 9,73 9,73 9,73 9,74 9,74 9,74 9,74 9,75 9,75 9,75 9,76 9,76 9,76 9,77 9,77 9,77 9,77 9,78 9,78 9,78 9,79 9,79 9,79 9,80 9,80 9,80 9,80 9,81 9,81 9,81 9,82 9,82 9,82 9,83 9,83 9,83 9,83 9,84 9,84 9,84 9,85 9,85 9,85 9,86 9,86 9,86 9,86 9,87 9,87 9,87 9,88 9,88 9,88 9,89 9,89 9,89 9,89 9,90 9,90 9,90 9,91 9,91 9,91 9,92 9,92 9,92 9,93 9,93 9,93 9,93 9,94 9,94 9,94 9,95 9,95 9,95 9,96 9,96 9,96 9,96 9,97 9,97 9,97 9,98 9,98 9,98 9,99 9,99 9,99 9,99 10,00 10,00 10,00 10,01 10,01 10,01 10,02 10,02 10,02 10,02 10,03 10,03 10,03 10,04 10,04 10,04 10,05 10,05 10,05 10,05 10,06 10,06 10,06 10,07 10,07 10,07 10,08 10,08 10,08 10,08 10,09 10,09 10,09 10,10 10,10 10,10 10,11 10,11 10,11 10,11 10,12 10,12 10,12 10,13 10,13 10,13 10,14 10,14 10,14 10,15 10,15 10,15 10,15 10,16 10,16 10,16 10,17 10,17 10,17 10,18 10,18 10,18 10,18 10,19 10,19 10,19 10,20 10,20 10,20 10,21 10,21 10,21 10,21 10,22 10,22 10,22 10,23 10,23 10,23 10,24 10,24 10,24 10,24 10,25 10,25 10,25 10,26 10,26 10,26 10,27 10,27 10,27 10,27 10,28 10,28 10,28 10,29 10,29 10,29 10,30 10,30 10,30 10,30 10,31 10,31 10,31 10,32 10,32 10,32 10,33 10,33 10,33 10,34 10,34 10,34 10,34 10,35 10,35 10,35 10,36 10,36 10,36 10,37 10,37 10,37 10,37 10,38 10,38 10,38 10,39 10,39 10,39 10,40 10,40 10,40 10,40 10,41 10,41 10,41 10,42 10,42 10,42 10,43 10,43 10,43 10,43 10,44 10,44 10,44 10,45 10,45 10,45 10,46 10,46 10,46 10,46 10,47 10,47 10,47 10,48 10,48 10,48 10,49 10,49 10,49 10,49 10,50 10,50 10,50 10,51 10,51 10,51 10,52 10,52 10,52 10,52 10,53 10,53 10,53 10,54 10,54 10,54 10,55 10,55 10,55 10,56 10,56 10,56 10,56 10,57 10,57 10,57 10,58 10,58 10,58 10,59 10,59 10,59 10,59 10,60 10,60 10,60 10,61 10,61 10,61 10,62 10,62 10,62 10,62 10,63 10,63 10,63 10,64 10,64 10,64 10,65 10,65 10,65 10,65 10,66 10,66 10,66 10,67 10,67 10,67 10,68 10,68 10,68 10,68 10,69 10,69 10,69 10,70 10,70 10,70 10,71 10,71 10,71 10,71 10,72 10,72 10,72 10,73 10,73 10,73 10,74 10,74 10,74 10,74 10,75 10,75 10,75 10,76 10,76 10,76 10,77 10,77 10,77 10,78 10,78 10,78 10,78 10,79 10,79 10,79 10,80 10,80 10,80 10,81 10,81 10,81 10,81 10,82 10,82 10,82 10,83 10,83 10,83 10,84 10,84 10,84 10,84 10,85 10,85 10,85 10,86 10,86 10,86 10,87 10,87 10,87 10,87 10,88 10,88 10,88 10,89 10,89 10,89 10,90 10,90 10,90 10,90 10,91 10,91 10,91 10,92 10,92 10,92 10,93 10,93 10,93 10,93 10,94 10,94 10,94 10,95 10,95 10,95 10,96 10,96 10,96 10,96 10,97 10,97 10,97 10,98 10,98 10,98 10,99 10,99 10,99 11,00 11,00 11,00 11,00 11,01 11,01 11,01 11,02 11,02 11,02 11,03 11,03 11,03 11,03 11,04 11,04 11,04 11,05 11,05 11,05 11,06 11,06 11,06 11,06 11,07 11,07 11,07 11,08 11,08 11,08 11,09 11,09 11,09 11,09 11,10 11,10 11,10 11,11 11,11 11,11 11,12 11,12 11,12 11,12 11,13 11,13 11,13 11,14 11,14 11,14 11,15 11,15 11,15 11,15 11,16 11,16 11,16 11,17 11,17 11,17 11,18 11,18 11,18 11,18 11,19 11,19 11,19 11,20 11,20 11,20 11,21 11,21 11,21 11,22 11,22 11,22 11,22 11,23 11,23 11,23 11,24 11,24 11,24 11,25 11,25 11,25 11,25

2006 2010 2014

12

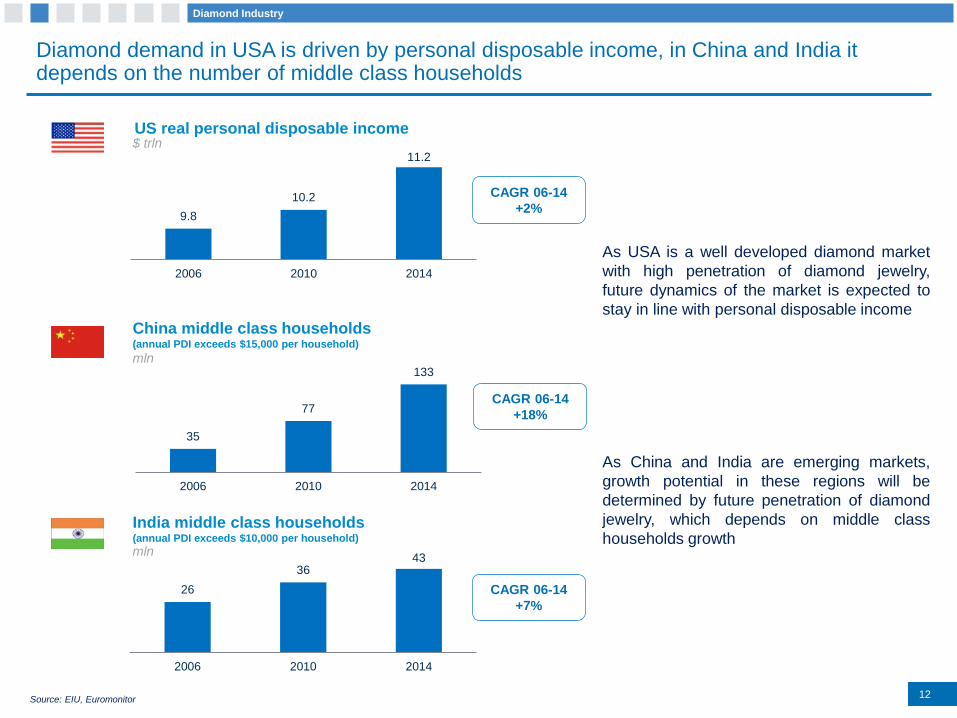

Diamond demand in USA is driven by personal disposable income, in China and India it depends on the number of middle class households

US real personal disposable income

India middle class households(annual PDI exceeds $10,000 per household)

mln

China middle class households(annual PDI exceeds $15,000 per household)

mln

26

3643

0,00

10,00

20,00

30,00

40,00

50,00

2006 2010 2014

Source: EIU, Euromonitor

$ trln

CAGR 06-14

+2%

CAGR 06-14

+18%

CAGR 06-14

+7%

Diamond Industry

As USA is a well developed diamond market

with high penetration of diamond jewelry,

future dynamics of the market is expected to

stay in line with personal disposable income

As China and India are emerging markets,

growth potential in these regions will be

determined by future penetration of diamond

jewelry, which depends on middle class

households growth

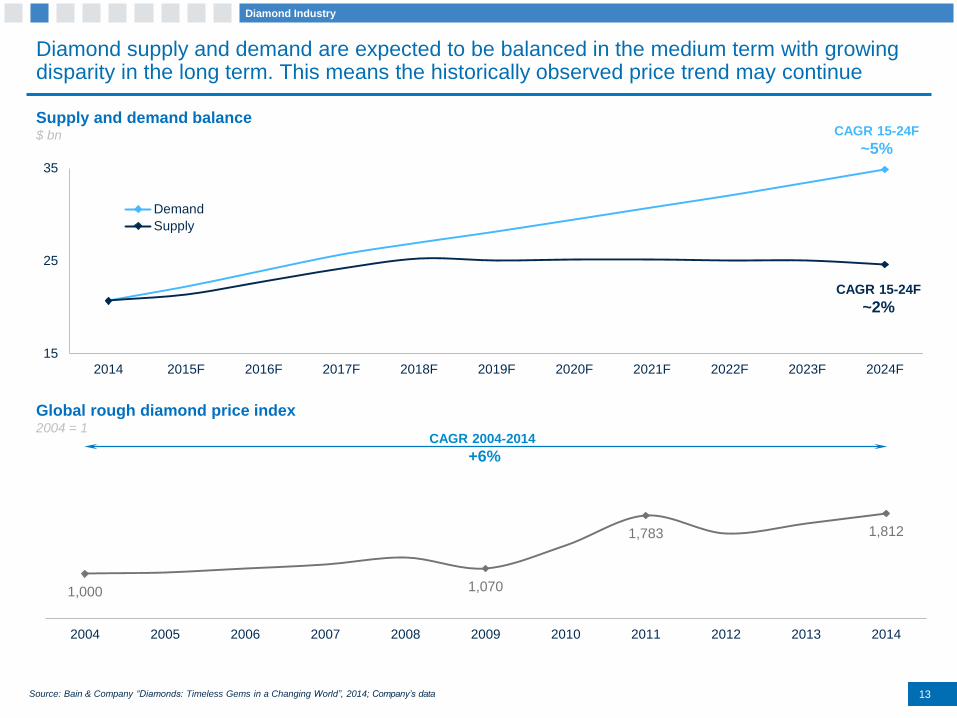

1,000 1,070

1,783 1,812

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

15

25

35

2014 2015F 2016F 2017F 2018F 2019F 2020F 2021F 2022F 2023F 2024F

Demand

Supply

Diamond supply and demand are expected to be balanced in the medium term with growing disparity in the long term. This means the historically observed price trend may continue

Source: Bain & Company “Diamonds: Timeless Gems in a Changing World”, 2014; Company’s data

Global rough diamond price index 2004 = 1

Supply and demand balance$ bn

CAGR 2004-2014

+6%

Diamond Industry

13

CAGR 15-24F

~5%

CAGR 15-24F

~2%

14

Production

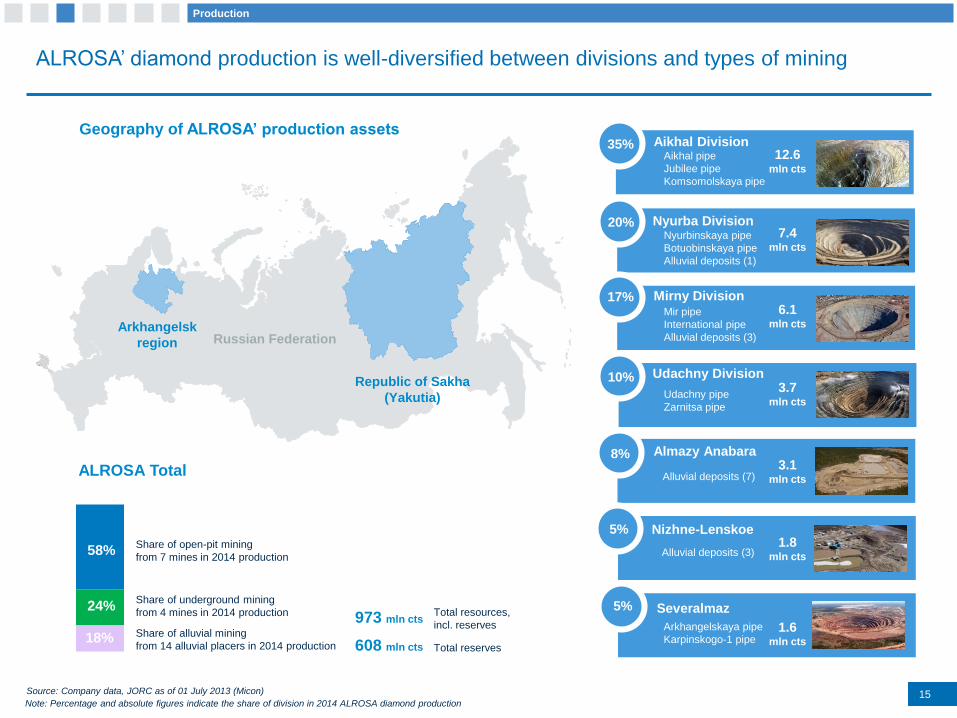

15Source: Company data, JORC as of 01 July 2013 (Micon)

ALROSA’ diamond production is well-diversified between divisions and types of mining

Severalmaz

1.6mln cts

Note: Percentage and absolute figures indicate the share of division in 2014 ALROSA diamond production

ALROSA Total

Production

Aikhal Division

17%

10%

8%

5%

Nyurba Division

Mirny Division

Udachny Division

Almazy Anabara

Nizhne-Lenskoe

12.6mln cts

7.4mln cts

6.1mln cts

3.7mln cts

3.1mln cts

1.8mln cts

Aikhal pipe

Jubilee pipe

Komsomolskaya pipe

Nyurbinskaya pipe

Botuobinskaya pipe

Alluvial deposits (1)

Mir pipe

International pipe

Alluvial deposits (3)

Udachny pipe

Zarnitsa pipe

Alluvial deposits (7)

Alluvial deposits (3)

Arkhangelskaya pipe

Karpinskogo-1 pipe

973 mln ctsTotal resources,

incl. reserves

608 mln cts Total reserves

Share of open-pit mining

from 7 mines in 2014 production

Share of underground mining

from 4 mines in 2014 production

Share of alluvial mining

from 14 alluvial placers in 2014 production

35%

20%

5%

58%

24%

18%

Geography of ALROSA’ production assets

Republic of Sakha

(Yakutia)

Arkhangelsk

region Russian Federation

16

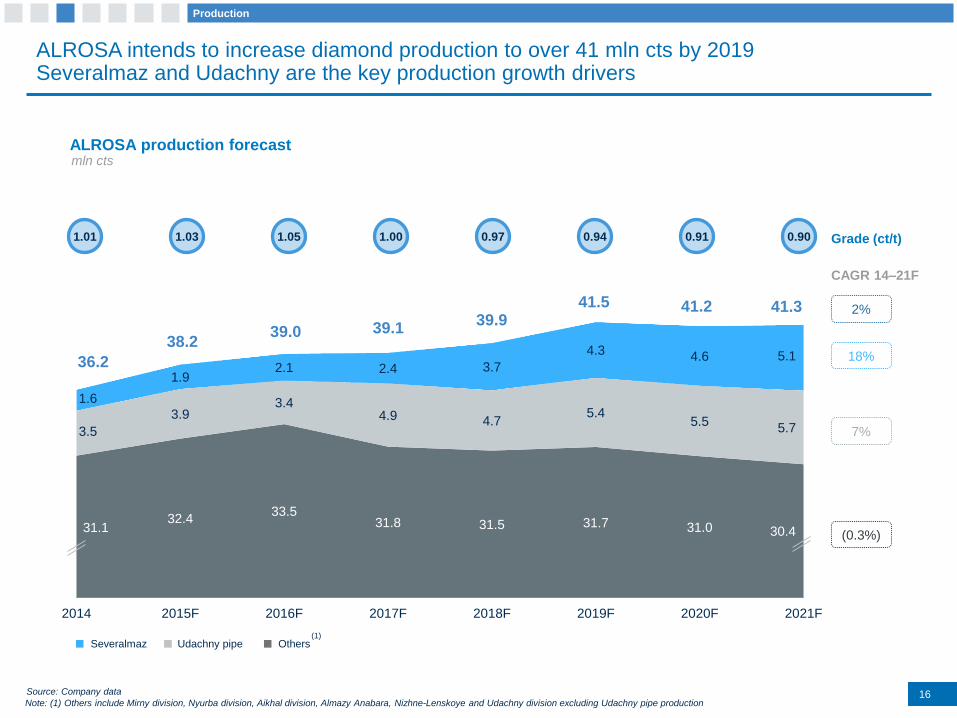

ALROSA intends to increase diamond production to over 41 mln cts by 2019Severalmaz and Udachny are the key production growth drivers

ALROSA production forecastmln cts

CAGR 14–21F

18%

7%

(0.3%)31.1

32.433.5

31.8 31.5 31.7 31.0 30.4

3.5

3.93.4

4.9 4.75.4

5.55.7

1.6

1.92.1 2.4 3.7

4.3 4.6 5.1

2014 2015F 2016F 2017F 2018F 2019F 2020F 2021F

38.2

36.2

39.0 39.1

41.341.241.539.9

2%

Source: Company data

Note: (1) Others include Mirny division, Nyurba division, Aikhal division, Almazy Anabara, Nizhne-Lenskoye and Udachny division excluding Udachny pipe production

(1)

1.01 1.03 1.05 1.00 0.97 0.94 0.91 0.90 Grade (ct/t)

Severalmaz Udachny pipe Others

Production

17

Capex will be decreasing as Severalmaz and Udachny underground mine reach their designed capacity

Planned Capex by mining complex

Source: Company data

Production

11.0

7.55.5 5.3

6.9 7.2

11.1

2.5

2.3

1.6 1.3

2.8 2.2

1.4

9.9

8.0

8.8 10.9

11.9

7.8

6.7

10.2

10.9

8.63.7

3.0

4.62.1

2.0

1.0 1.2

2.41.5

2015F 2016F 2017F 2018F 2019F 2020F 2021F

22.7

RUB bn

24.1

25.8

29.0

35.6

25.4

21.8

0.4

0.5

Severalmaz Udachny division Mining projects in the Republic of Sakha (Yakutia) Alluvial deposits Industrial infrastructure and other

1.0

18

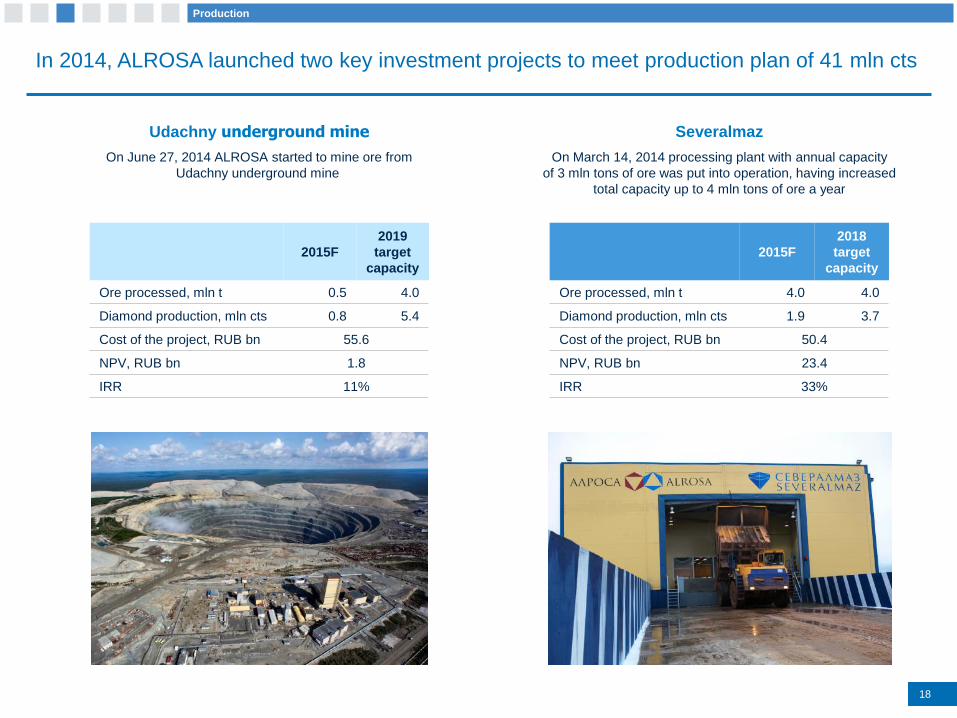

Udachny underground mine

On June 27, 2014 ALROSA started to mine ore from

Udachny underground mine

Severalmaz

On March 14, 2014 processing plant with annual capacity

of 3 mln tons of ore was put into operation, having increased

total capacity up to 4 mln tons of ore a year

2015F

2019

target

capacity

Ore processed, mln t 0.5 4.0

Diamond production, mln cts 0.8 5.4

Cost of the project, RUB bn 55.6

NPV, RUB bn 1.8

IRR 11%

2015F

2018

target

capacity

Ore processed, mln t 4.0 4.0

Diamond production, mln cts 1.9 3.7

Cost of the project, RUB bn 50.4

NPV, RUB bn 23.4

IRR 33%

In 2014, ALROSA launched two key investment projects to meet production plan of 41 mln cts

Production

19

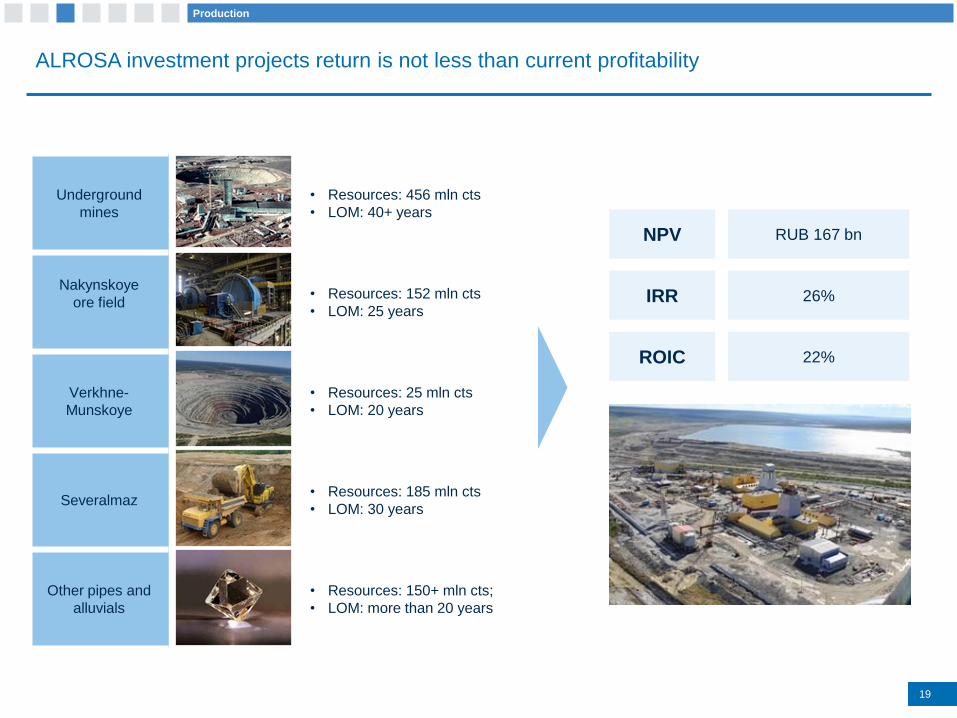

ALROSA investment projects return is not less than current profitability

Underground

mines

• Resources: 456 mln cts

• LOM: 40+ years

Nakynskoye

ore field• Resources: 152 mln cts

• LOM: 25 years

Verkhne-

Munskoye

• Resources: 25 mln cts

• LOM: 20 years

Severalmaz• Resources: 185 mln cts

• LOM: 30 years

Other pipes and

alluvials

• Resources: 150+ mln cts;

• LOM: more than 20 years

NPV

IRR

RUB 167 bn

26%

Production

ROIC 22%

2020

Marketing

21

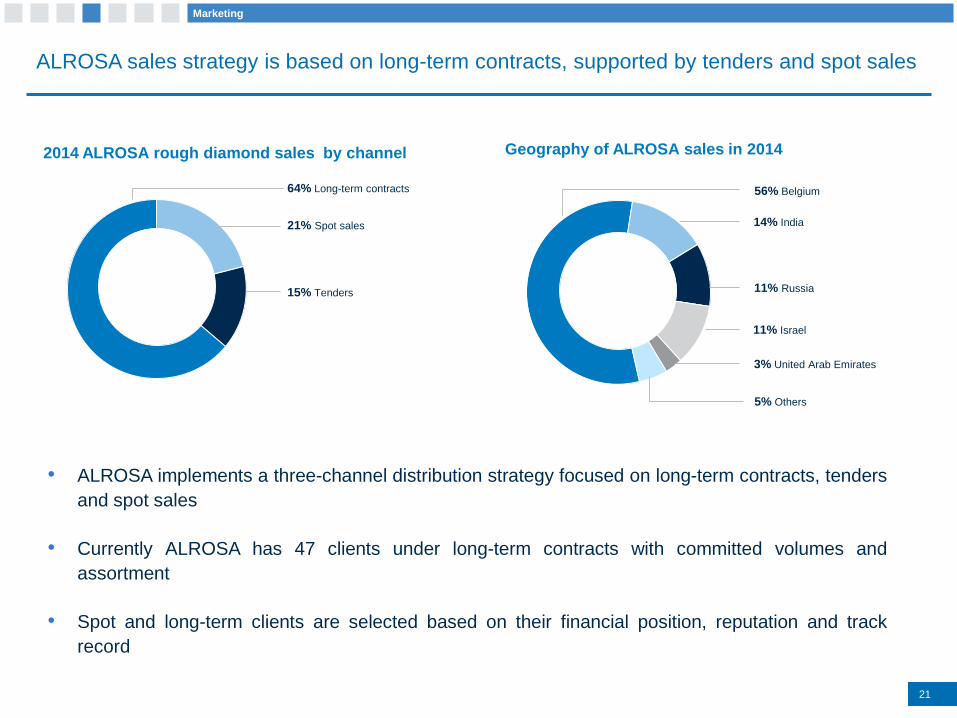

ALROSA sales strategy is based on long-term contracts, supported by tenders and spot sales

2014 ALROSA rough diamond sales by channel

• ALROSA implements a three-channel distribution strategy focused on long-term contracts, tenders

and spot sales

• Currently ALROSA has 47 clients under long-term contracts with committed volumes and

assortment

• Spot and long-term clients are selected based on their financial position, reputation and track

record

Geography of ALROSA sales in 2014

64% Long-term contracts

15% Tenders

56% Belgium

14% India

11% Israel

3% United Arab Emirates

5% Others

21% Spot sales

11% Russia

Marketing

30%

3%

45%

22%

15%

16%

5%

14%

5%

34%

11%

by sales volume by sales value

22

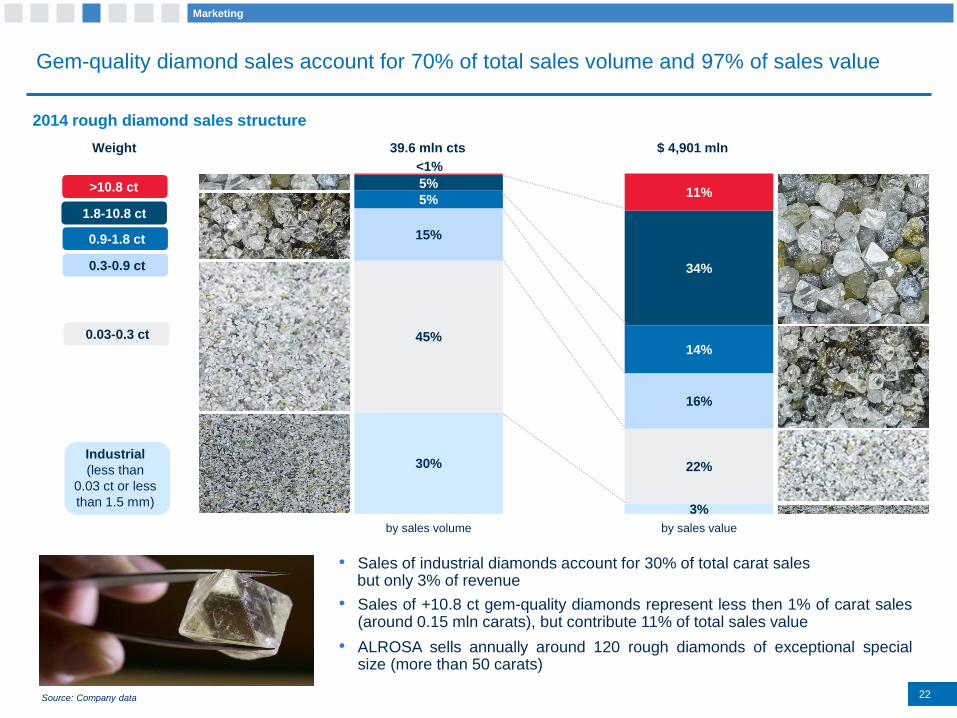

Gem-quality diamond sales account for 70% of total sales volume and 97% of sales value

Source: Company data

2014 rough diamond sales structure

• Sales of industrial diamonds account for 30% of total carat salesbut only 3% of revenue

• Sales of +10.8 ct gem-quality diamonds represent less then 1% of carat sales(around 0.15 mln carats), but contribute 11% of total sales value

• ALROSA sells annually around 120 rough diamonds of exceptional specialsize (more than 50 carats)

>10.8 ct

<1%

1.8-10.8 ct

0.9-1.8 ct

0.3-0.9 ct

0.03-0.3 ct

Industrial

(less than

0.03 ct or less

than 1.5 mm)

39.6 mln cts $ 4,901 mlnWeight

Marketing

23

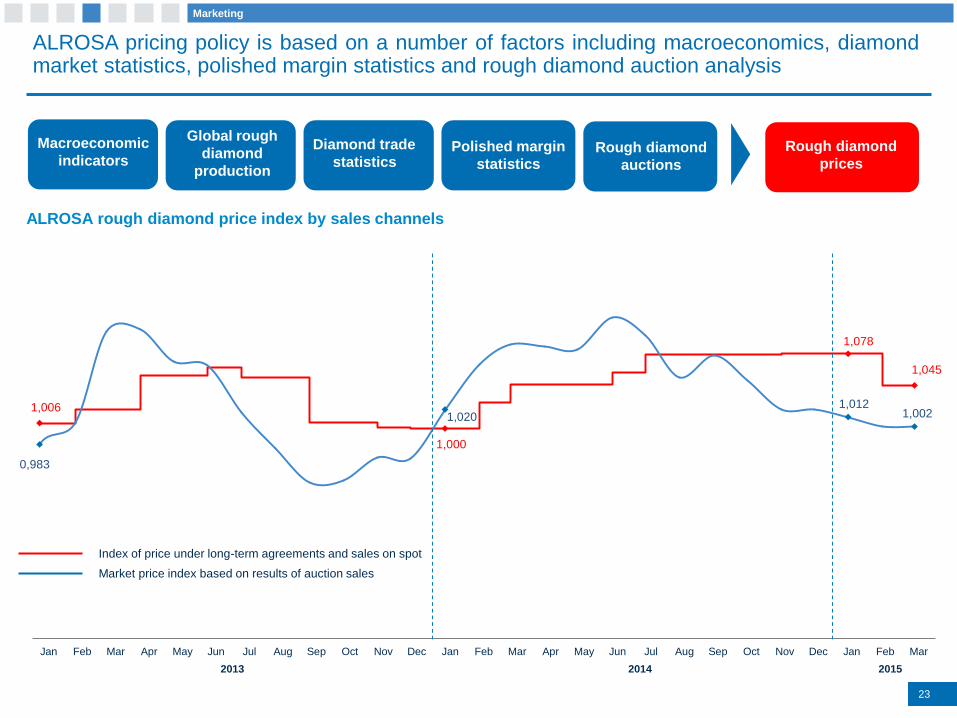

1,006

1,000

1,078

1,045

0,983

1,0201,012

1,002

2013/1 2013/22013/3 2013/42013/5 2013/62013/7 2013/8 2013/92013/102013/112013/122014/1 2014/22014/3 2014/42014/5 2014/62014/7 2014/8 2014/92014/102014/112014/122015/1 2015/22015/3

Index of price under long-term agreements and sales on spot

Market price index based on results of auction sales

Rough diamond

prices

ALROSA rough diamond price index by sales channels

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

ALROSA pricing policy is based on a number of factors including macroeconomics, diamondmarket statistics, polished margin statistics and rough diamond auction analysis

Macroeconomic

indicators

Global rough

diamond

production

Diamond trade

statisticsPolished margin

statisticsRough diamond

auctions

2013 2014 2015

Marketing

• ALROSA currently has 15 mln cts of diamonds in inventory

and plans to reduce inventory turnover from 6 to 4 months

• ALROSA intends to optimise inventory turnover

by developing automated sorting machines

• ALROSA is on track to sell around 2 mln cts from inventory

in 2015 and the same amount in 2016

24

Sales strategy under lack of significant price growth in mid-term is based on additional sales volumes from inventory

ALROSA diamond stockpilemln cts

Current diamond inventory turnover is around 6 months

As of Jan 1, 2014 As of Mar 1, 2015

Gem-quality rough diamonds 12 9

Industrial rough diamonds 6 6

Total 18 15

Mining and processing

2-5 weeks

Sorting and valuation

9 weeks

Aggregation and sale

4-7 weeks

Marketing

25

Financial Performance

26

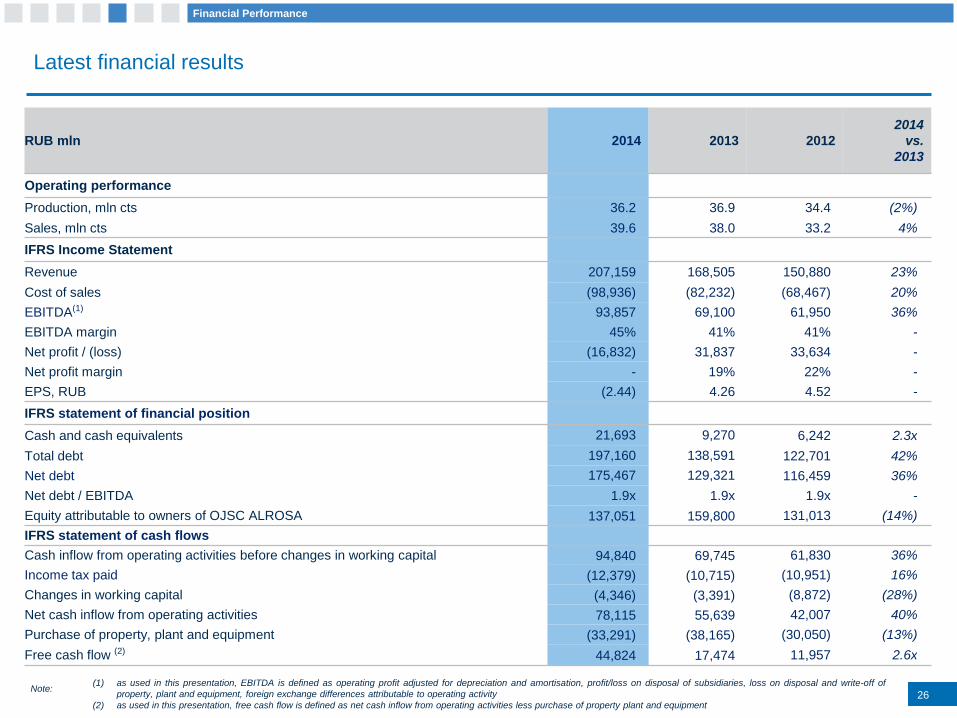

Latest financial results

RUB mln 2014 2013 2012

2014

vs.

2013

Operating performance

Production, mln cts 36.2 36.9 34.4 (2%)

Sales, mln cts 39.6 38.0 33.2 4%

IFRS Income Statement

Revenue 207,159 168,505 150,880 23%

Cost of sales (98,936) (82,232) (68,467) 20%

EBITDA(1) 93,857 69,100 61,950 36%

EBITDA margin 45% 41% 41% -

Net profit / (loss) (16,832) 31,837 33,634 -

Net profit margin - 19% 22% -

EPS, RUB (2.44) 4.26 4.52 -

IFRS statement of financial position

Cash and cash equivalents 21,693 9,270 6,242 2.3x

Total debt 197,160 138,591 122,701 42%

Net debt 175,467 129,321 116,459 36%

Net debt / EBITDA 1.9x 1.9x 1.9x -

Equity attributable to owners of OJSC ALROSA 137,051 159,800 131,013 (14%)

IFRS statement of cash flows

Cash inflow from operating activities before changes in working capital 94,840 69,745 61,830 36%

Income tax paid (12,379) (10,715) (10,951) 16%

Changes in working capital (4,346) (3,391) (8,872) (28%)

Net cash inflow from operating activities 78,115 55,639 42,007 40%

Purchase of property, plant and equipment (33,291) (38,165) (30,050) (13%)

Free cash flow (2) 44,824 17,474 11,957 2.6x

(1) as used in this presentation, EBITDA is defined as operating profit adjusted for depreciation and amortisation, profit/loss on disposal of subsidiaries, loss on disposal and write-off of

property, plant and equipment, foreign exchange differences attributable to operating activity

(2) as used in this presentation, free cash flow is defined as net cash inflow from operating activities less purchase of property plant and equipment

Note:

Financial Performance

27

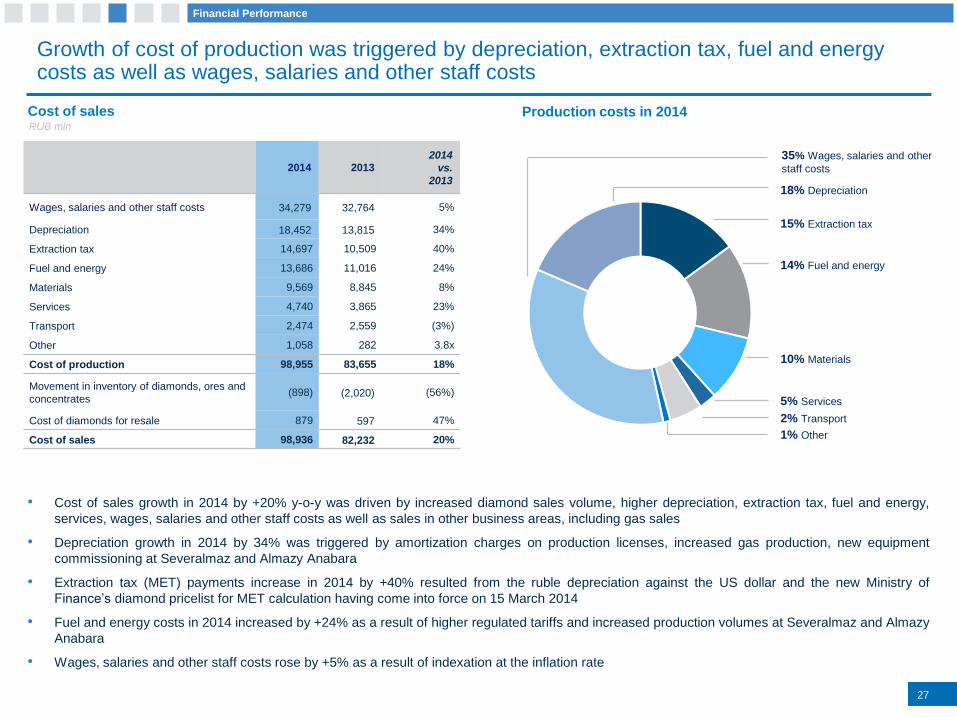

Growth of cost of production was triggered by depreciation, extraction tax, fuel and energy costs as well as wages, salaries and other staff costs

2014 20132014

vs.

2013

Wages, salaries and other staff costs 34,279 32,764 5%

Depreciation 18,452 13,815 34%

Extraction tax 14,697 10,509 40%

Fuel and energy 13,686 11,016 24%

Materials 9,569 8,845 8%

Services 4,740 3,865 23%

Transport 2,474 2,559 (3%)

Other 1,058 282 3.8x

Cost of production 98,955 83,655 18%

Movement in inventory of diamonds, ores and

concentrates(898) (2,020) (56%)

Cost of diamonds for resale 879 597 47%

Cost of sales 98,936 82,232 20%

• Cost of sales growth in 2014 by +20% y-o-y was driven by increased diamond sales volume, higher depreciation, extraction tax, fuel and energy,

services, wages, salaries and other staff costs as well as sales in other business areas, including gas sales

• Depreciation growth in 2014 by 34% was triggered by amortization charges on production licenses, increased gas production, new equipment

commissioning at Severalmaz and Almazy Anabara

• Extraction tax (MET) payments increase in 2014 by +40% resulted from the ruble depreciation against the US dollar and the new Ministry of

Finance’s diamond pricelist for MET calculation having come into force on 15 March 2014

• Fuel and energy costs in 2014 increased by +24% as a result of higher regulated tariffs and increased production volumes at Severalmaz and Almazy

Anabara

• Wages, salaries and other staff costs rose by +5% as a result of indexation at the inflation rate

Production costs in 2014Cost of salesRUB mln

15% Extraction tax

35% Wages, salaries and other

staff costs

14% Fuel and energy

18% Depreciation

2% Transport

10% Materials

5% Services

1% Other

Financial Performance

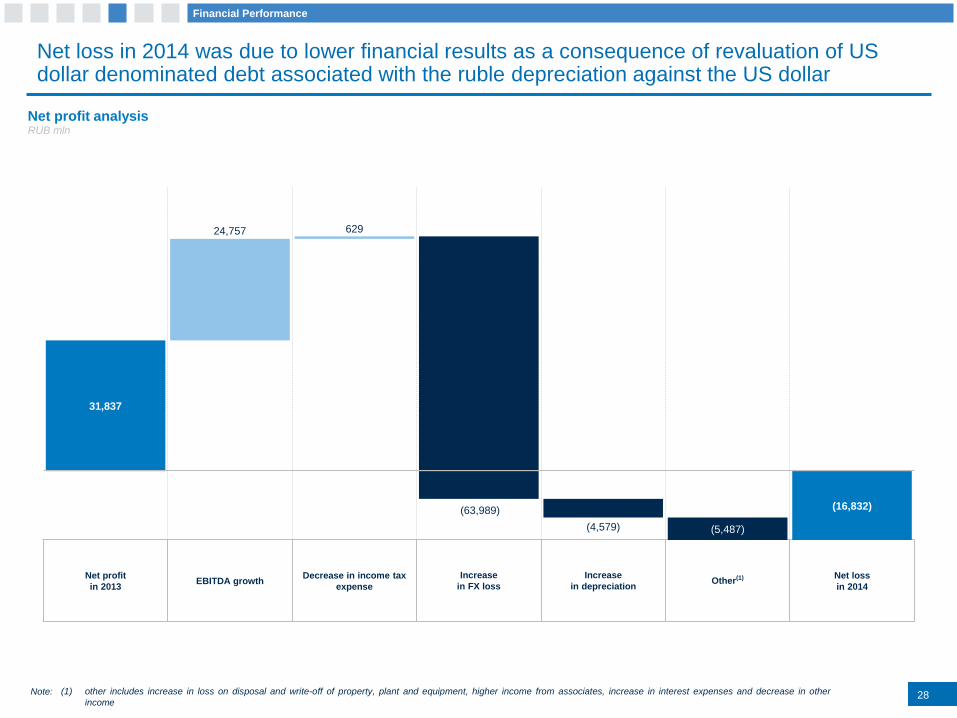

Net loss in 2014 was due to lower financial results as a consequence of revaluation of US dollar denominated debt associated with the ruble depreciation against the US dollar

Net profit

in 2013EBITDA growth

Decrease in income tax

expense

Increase

in FX loss

Increase

in depreciationOther(1) Net loss

in 2014

28

Net profit analysisRUB mln

(1) other includes increase in loss on disposal and write-off of property, plant and equipment, higher income from associates, increase in interest expenses and decrease in other

income

Note:

31,837

24,757 629

(63,989)

(4,579) (5,487)

(16,832)

Financial Performance

29

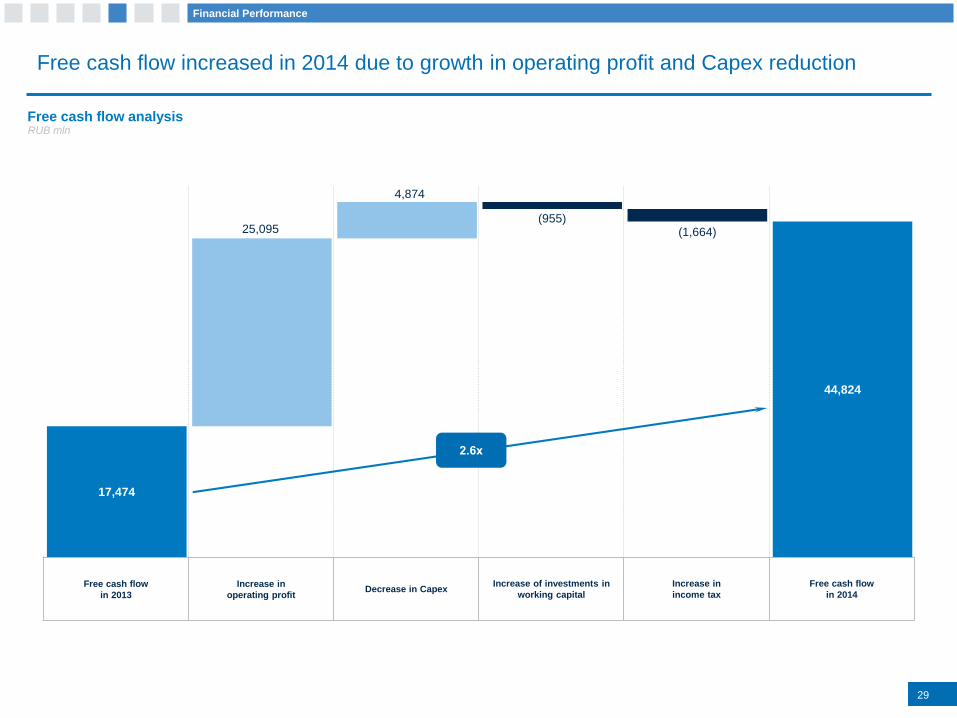

Free cash flow increased in 2014 due to growth in operating profit and Capex reduction

Free cash flow

in 2013

Increase in

operating profitDecrease in Capex

Increase of investments in

working capital

Increase in

income tax

Free cash flow

in 2014

Free cash flow analysisRUB mln

17,474

25,095

4,874

(955)(1,664)

44,824

2.6х

Financial Performance

30

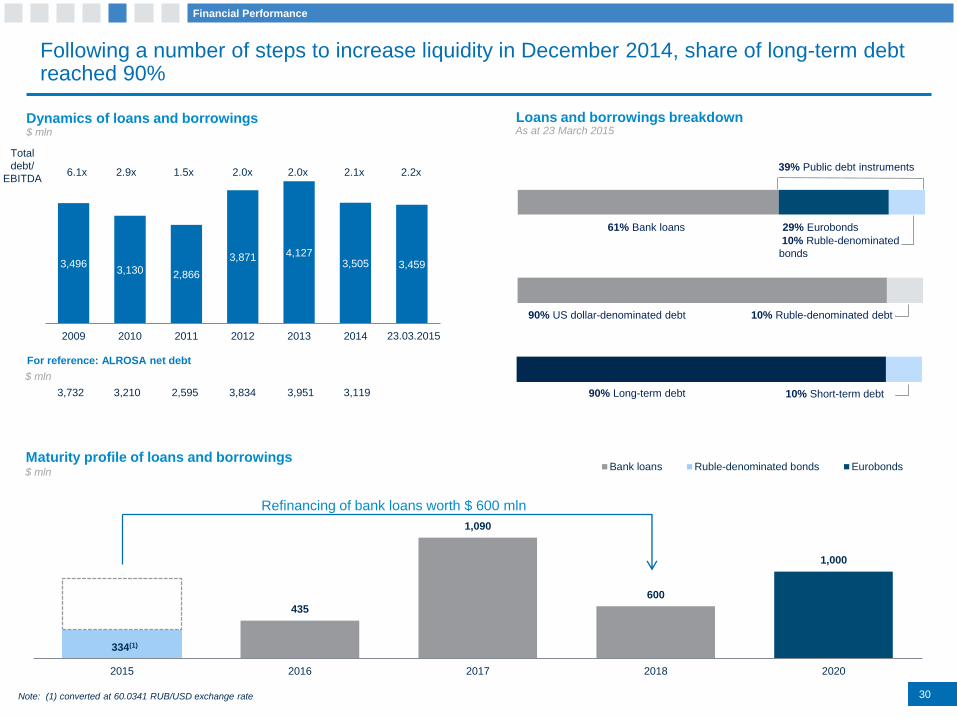

Following a number of steps to increase liquidity in December 2014, share of long-term debt reached 90%

334(1)

435

1,090

600

1,000

2015 2016 2017 2018 2020

Bank loans Ruble-denominated bonds Eurobonds

3,8342,5953,732

$ mln

3,951

39% Public debt instruments

61% Bank loans 29% Eurobonds

10% Ruble-denominated

bonds

10% Ruble-denominated debt90% US dollar-denominated debt

90% Long-term debt 10% Short-term debt

3,4963,130 2,866

3,871 4,1273,505 3,459

2009 2010 2011 2012 2013 2014 17.03.2015

3,210 3,119

23.03.2015

Total

debt/

EBITDA6.1x 2.9x 1.5x 2.0x 2.0x 2.1x 2.2x

Dynamics of loans and borrowings Loans and borrowings breakdown$ mln As at 23 March 2015

For reference: ALROSA net debt

Maturity profile of loans and borrowings$ mln

Note: (1) converted at 60.0341 RUB/USD exchange rate

Refinancing of bank loans worth $ 600 mln

Financial Performance

31

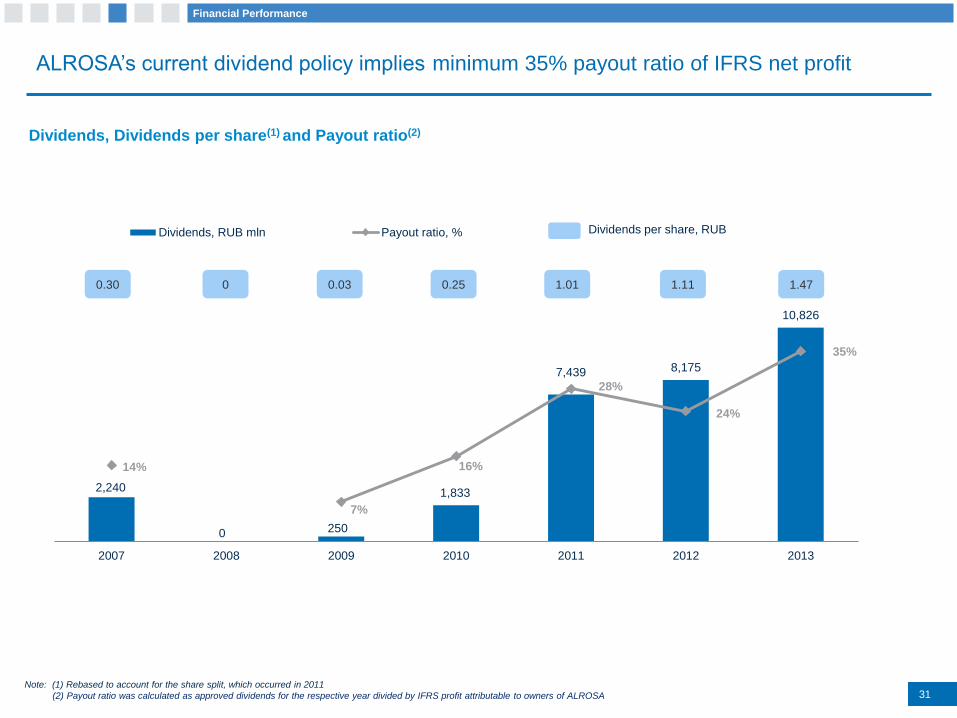

ALROSA’s current dividend policy implies minimum 35% payout ratio of IFRS net profit

Dividends, Dividends per share(1) and Payout ratio(2)

2,240

0 250

1,833

7,439 8,175

10,826

14%

7%

16%

28%

24%

35%

0

0,05

0,1

0,15

0,2

0,25

0,3

0,35

0,4

2007 2008 2009 2010 2011 2012 2013

Dividends, RUB mln Payout ratio, % Dividends per share, RUB

0.30 0 0.03 0.25 1.01 1.11 1.47

Note: (1) Rebased to account for the share split, which occurred in 2011

(2) Payout ratio was calculated as approved dividends for the respective year divided by IFRS profit attributable to owners of ALROSA

Financial Performance

32

ALROSA Tomorrow

Strategic directions for development

33

ALROSA Tomorrow

Focus on most profitable segment in the industry

Geological exploration

Operational efficiency

Marketing and brand

Non-core assets divestment

ALROSA

IS

ABOUT

33

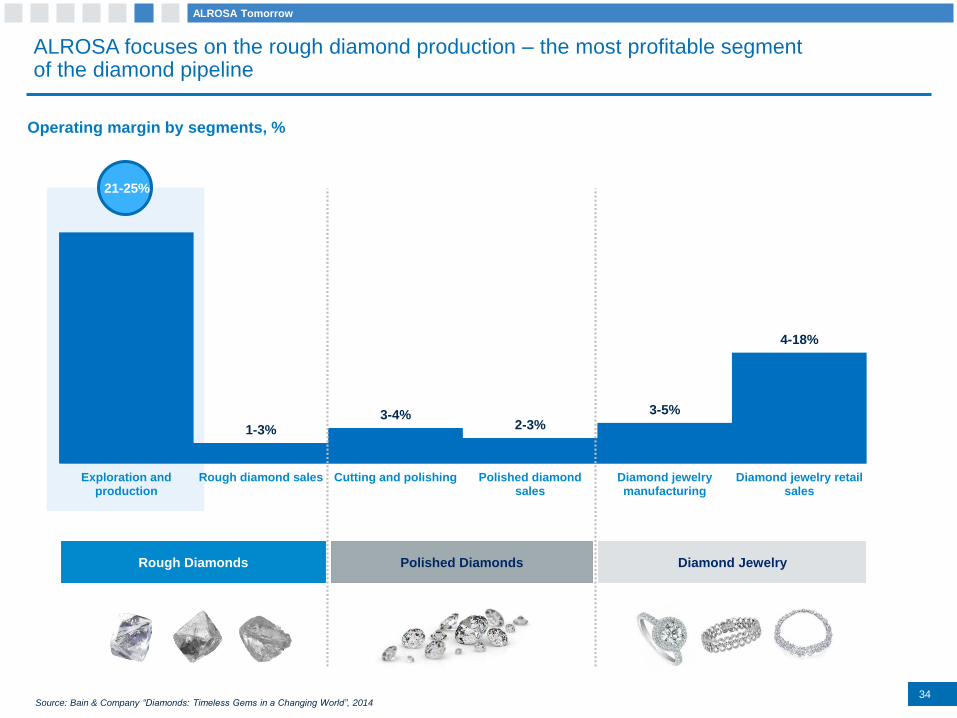

1-3%3-4%

2-3%3-5%

4-18%

Exploration andproduction

Rough diamond sales Cutting and polishing Polished diamondsales

Diamond jewelrymanufacturing

Diamond jewelry retailsales

ALROSA focuses on the rough diamond production – the most profitable segment of the diamond pipeline

Source: Bain & Company “Diamonds: Timeless Gems in a Changing World”, 201434

Rough Diamonds Polished Diamonds Diamond Jewelry

Operating margin by segments, %

21-25%

ALROSA Tomorrow

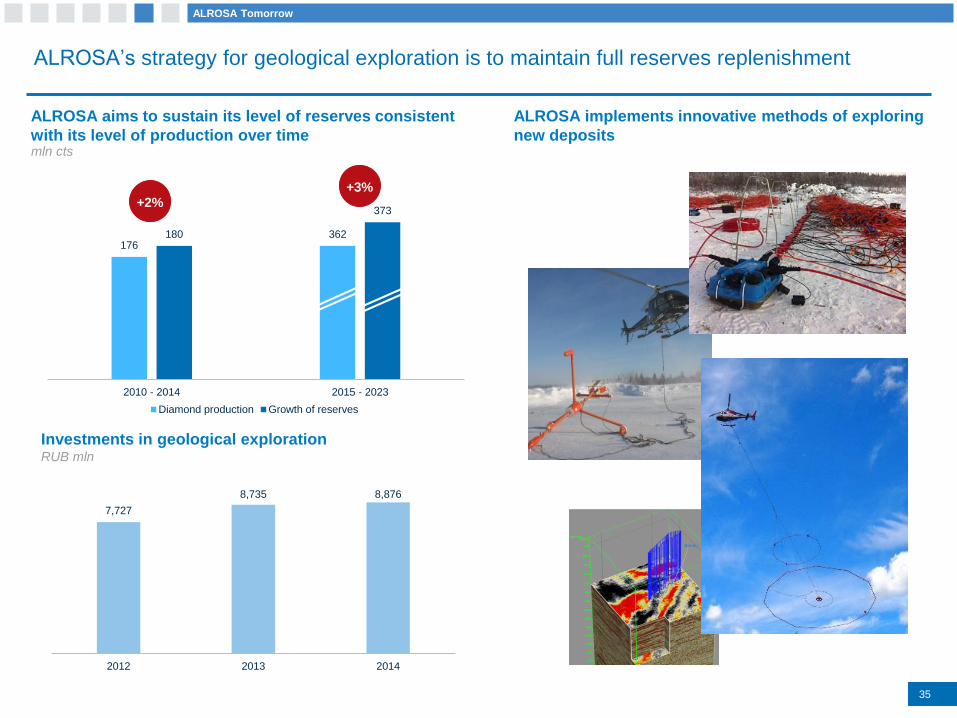

ALROSA’s strategy for geological exploration is to maintain full reserves replenishment

ALROSA aims to sustain its level of reserves consistent

with its level of production over timemln cts

ALROSA implements innovative methods of exploring

new deposits

35

176362180

373

2010 - 2014 2015 - 2023

Diamond production Growth of reserves

7,727

8,735 8,876

2012 2013 2014

Investments in geological explorationRUB mln

+2%+3%

ALROSA Tomorrow

Supply and marketing strategy

The structure of supply and marketing in ALROSA implies the following:

Speedier inventories turnover for rough diamonds, reduced from 6 to 4 months due to automation of sorting

process

Improved sorting quality in accordance with the requirements asserted by the producers of polished

diamonds

Promotion of “ALROSA ALLIANCE” brand in order to improve reputation and recognition of ALROSA in all

sectors of the diamond market

Development of trade and marketing relationships with leading jewelry retailers through direct sales of

diamonds and joint ventures for selling polished diamonds

36

ALROSA Tomorrow

70

62

5347

39

31

20

2010 2011 2012 2013 2014 2015E 2020E

ALROSA is to focus on diamond mining

Number of subsidiaries

• In 2012, social assets in monocities in Yakutia, occupied mostly by

ALROSA workers, were transferred to the Republic of Sakha (Yakutia) and

ALROSA committed to cover the maintenance costs in Udachny (until

2014), Aikhal (until 2015) and Mirny (until 2016)

• 6 airports, located nearby ALROSA production area in Yakutia, are in the

process of transferring to the federal authorities

• ALROSA receives annually around RUB 2 bn of subsidies from the

Republic of Sakha (Yakutia) to compensate partially from current social

costs, including housing maintenance and utilities infrastructure

37

ALROSA Tomorrow

ALROSA continues transferring its social facilities and

infrastructure to the Republic of Sakha (Yakutia)

38

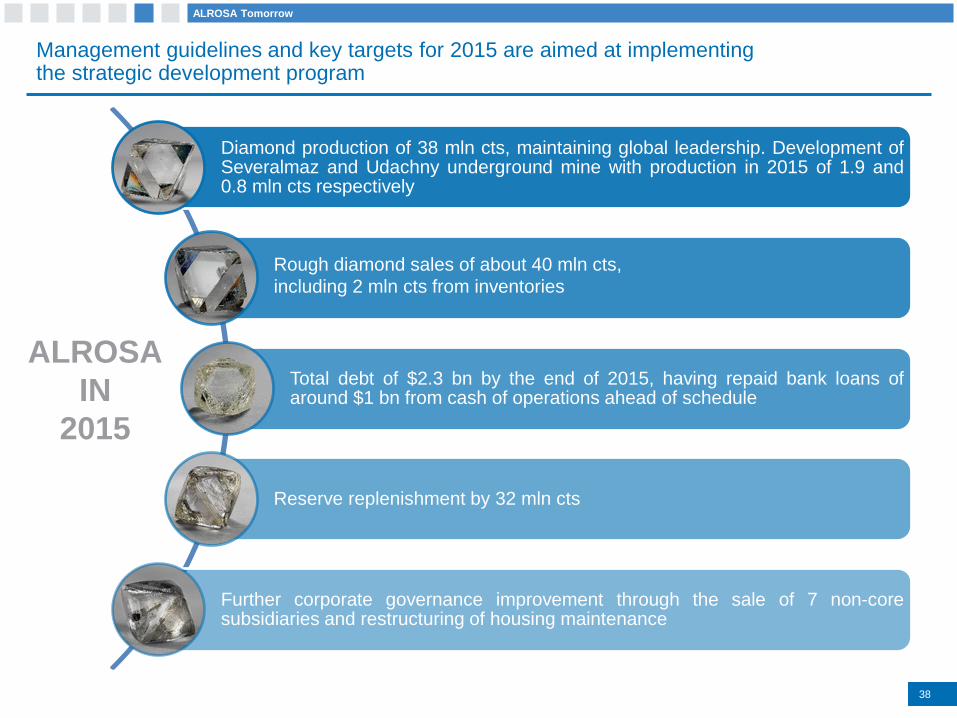

Management guidelines and key targets for 2015 are aimed at implementing the strategic development program

Diamond production of 38 mln cts, maintaining global leadership. Development ofSeveralmaz and Udachny underground mine with production in 2015 of 1.9 and0.8 mln cts respectively

Rough diamond sales of about 40 mln cts,

including 2 mln cts from inventories

Total debt of $2.3 bn by the end of 2015, having repaid bank loans ofaround $1 bn from cash of operations ahead of schedule

Reserve replenishment by 32 mln cts

Further corporate governance improvement through the sale of 7 non-coresubsidiaries and restructuring of housing maintenance

ALROSA

IN

2015

ALROSA Tomorrow

3939

Thank you!

4040

Appendix

41

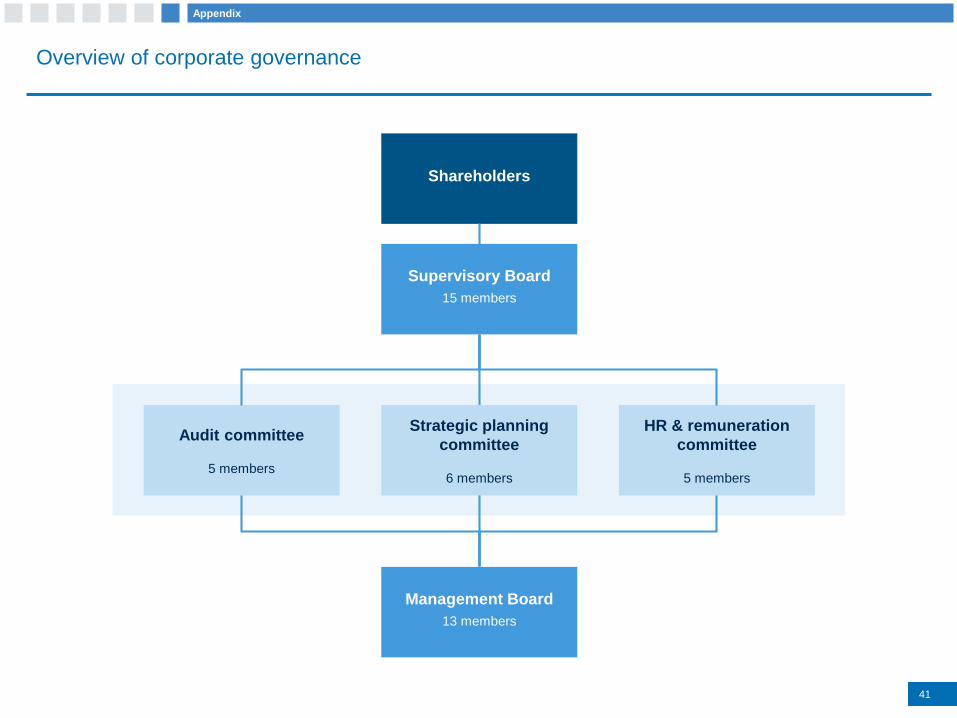

Overview of corporate governance

Appendix

Shareholders

Supervisory Board

15 members

Management Board

13 members

HR & remuneration

committee

5 members

Audit committee

5 members

Strategic planning

committee

6 members

42

Management team overview

Operational Team

Mikhail Lopatinsky

Director, Mirny Mining and Processing Division

• Joined the Company in 1992

• Over 20 years of industry experience

Mir

ny

Ud

ac

hn

y

Alexander Makhrachev

Director, Udachny Mining and Processing Division

• Joined the Company in 1979

• Over 33 years of industry experience

Ravil Sanatulov

Director, Aikhal Mining and Processing Division

• Joined the Company in 1986

• Over 28 years of industry experience

Aik

ha

l

Igor Uvarov

Director, Nyurba Mining and Processing Division

• Joined the Company in 1989

• Over 24 years of industry experience

Nyu

rba

Matvey Yevseev

CEO OJSC Almazy Anabara

• Joined the Company in 1997

• Over 16 years of industry experience

Alm

azy

An

ab

ara

Sergey Gerasimov

CEO Severalmaz

• Joined the Company in 1977

• Over 36 years of industry experienceSe

ve

ralm

az

Executive Team

Appendix

Fin

an

ce

an

d e

co

no

my

Ilya Ryashchin

First Vice-President for Finance and Economy, acting CEO

• Joined the Company in 2012

• Head of Planning and Budgeting Department at OJSC Russian

Railways (since 2006)

• Deputy Head of Finance Department, Ministry of Railways of

Russia (since 2001)

CO

O

Igor Sobolev

First Vice-President – Chief Operating Officer

• Joined the Company in 2007

• Head of Capital Construction Division, Mining & Metallurgical

directorate, OJSC MMC Norilsk Nickel (2000-2007)

CF

O

Igor Kulichik

Vice-President - Chief Financial Officer

• Joined the Company in 2002

• Vice-president and CFO of ALROSA since August 2009

Sa

les

Yuri Okoyomov

Vice-President for Sales

• Joined the Company in 1993

• Vice-President of ALROSA for marketing and sales since August

2009

43

Ilya Yuzhanov

Chairman of the Board of

directors, Polyus Gold

International Limited

Sergey Mestnikov

First Deputy Minister of

Property and Land Relations

of Republic of Sakha (Yakutia)

Sergey Barsukov

Director, Financial Policy

Department, Ministry of Finance

of the Russian Federation

Andrey Sharonov

Dean, Moscow School of

Management SKOLKOVO

Nominated by: Russian Federation Nominated by: Republic of Sakha (Yakutia) Nominated by: Russian Federation Nominated by: Russian Federation

Previously held positions include

2008–2012 – Chairman of the Board of

Directors, OJSC Polymetal

2012–2014 – Board Member, Board of

Directors, OTKRITIE Financial

Corporation JSC

2009–2011 – Member of the

Supervisory Board, OJSC ALROSA

Since 2013 – Chairman of the Board of

Directors, Polyus Gold International

Limited.

Previously held positions include

2010–2012 – Deputy Head, Head,

Secretariat of Chairman of the

Government of the Republic of Sakha

(Yakutia)

Since 2012 – Republic of Sakha

(Yakutia) First Deputy Minister of

Property and Land Relations

Previously held positions include

2007–2008 – First Deputy General

Director, Agency for Housing Mortgage

Lending (OJSC “AHML”)

2008–2010 – Assistant to Vice

Chairman of the Russian Federation

Government – Russian Federation

Minister of Finance

Since 2010 – Director, Financial Policy

Department, Ministry of Finance of the

Russian Federation

Previously held positions include:

2007-2010 – Managing Director, CJSC

Investment Company Troika Dialog

2010-2013 – Deputy Mayor of Moscow

for Economic Policy, Government of

Moscow

Since 2013 – Dean, Moscow School of

Management SKOLKOVO

Igor Lozhevsky

Vice-Chairman for Eastern

Europe, Deutsche Bank AG

Sergey Dubinin

Chairman of the Supervisory

Council, VTB Bank, Member of

the Board of Directors, CJSC

VTB Capital

Oleg Fedorov

Adviser to the Head of the

Federal Agency for State

Property Management

Denis Morozov

Representative of the Russian Federation in the Board of Directors of the European Bank for Reconstruction and Development, Executive Director for Russian Federation, Belarus and Tajikistan

Nominated as an independent director

Independent

Nominated by: Russian Federation Nominated by: Russian Federation Nominated as an independent director

Independent

Previously held positions include

2007–2008 – Chairman of Global

Banking and Capital Markets for Russia

and CIS, Dresdner Bank, Moscow

2008–2012 – Chief Executive Officer,

Deutsche Bank for Russia and CIS,

Moscow

Previously held positions include

2005–2008 – member of the Board of

Directors, Financial Director, Corporate

Centre, RAO UESR (Unified Energy

System of Russia)

Since 2008 – member of the Board of

Directors, CJSC VTB Capital

Since 2011 – Chairman of the

Supervisory Council, VTB Bank

Previously held positions include:

2009–2012 – Head, Department for

cooperation with Governmental

authorities and companies with

government participation, Department

of Investment and Banking on Global

Markets, CJSC VTB Capital

Since 2012 – Adviser to the Head of the

Federal Agency for State Property

Management

Previously held positions include

2010 – CEO, General Director,

Chairman of the Management Board,

Board of Directors member, OJSC

UralkaliSince 2011 – Representative of the Russian Federation in the Board of Directors of the European Bank for Reconstruction and Development, Executive Director for Russian Federation, Belarus and Tajikistan

1 3

6 7 8

2

5

4

Supervisory board overview (1/2)

Appendix

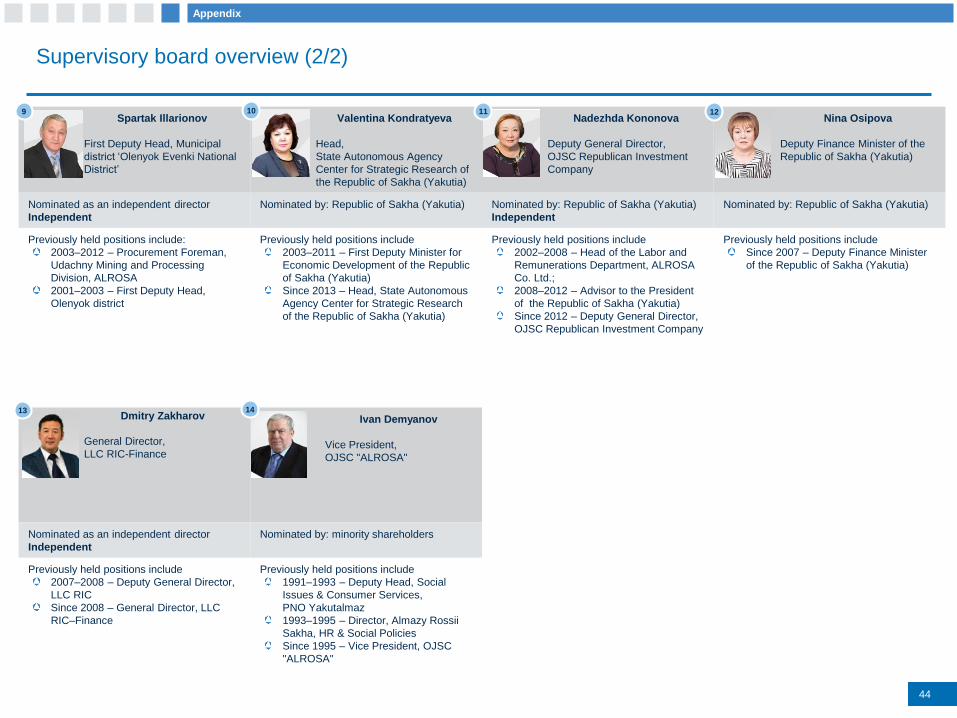

Spartak Illarionov

First Deputy Head, Municipal

district ‘Olenyok Evenki National

District’

Valentina Kondratyeva

Head,

State Autonomous Agency

Center for Strategic Research of

the Republic of Sakha (Yakutia)

Nadezhda Kononova

Deputy General Director,

OJSC Republican Investment

Company

Nina Osipova

Deputy Finance Minister of the

Republic of Sakha (Yakutia)

Nominated as an independent director

Independent

Nominated by: Republic of Sakha (Yakutia) Nominated by: Republic of Sakha (Yakutia)

Independent

Nominated by: Republic of Sakha (Yakutia)

Previously held positions include:

2003–2012 – Procurement Foreman,

Udachny Mining and Processing

Division, ALROSA

2001–2003 – First Deputy Head,

Olenyok district

Previously held positions include

2003–2011 – First Deputy Minister for

Economic Development of the Republic

of Sakha (Yakutia)

Since 2013 – Head, State Autonomous

Agency Center for Strategic Research

of the Republic of Sakha (Yakutia)

Previously held positions include

2002–2008 – Head of the Labor and

Remunerations Department, ALROSA

Co. Ltd.;

2008–2012 – Advisor to the President

of the Republic of Sakha (Yakutia)

Since 2012 – Deputy General Director,

OJSC Republican Investment Company

Previously held positions include

Since 2007 – Deputy Finance Minister

of the Republic of Sakha (Yakutia)

Dmitry Zakharov

General Director,

LLC RIC-Finance

Ivan Demyanov

Vice President,

OJSC "ALROSA"

Nominated as an independent director

Independent

Nominated by: minority shareholders

Previously held positions include

2007–2008 – Deputy General Director,

LLC RIC

Since 2008 – General Director, LLC

RIC–Finance

Previously held positions include

1991–1993 – Deputy Head, Social

Issues & Consumer Services,

PNO Yakutalmaz

1993–1995 – Director, Almazy Rossii

Sakha, HR & Social Policies

Since 1995 – Vice President, OJSC

"ALROSA"

44

10 11 12

1413

9

Supervisory board overview (2/2)

Appendix

45

2014 cash costs and production

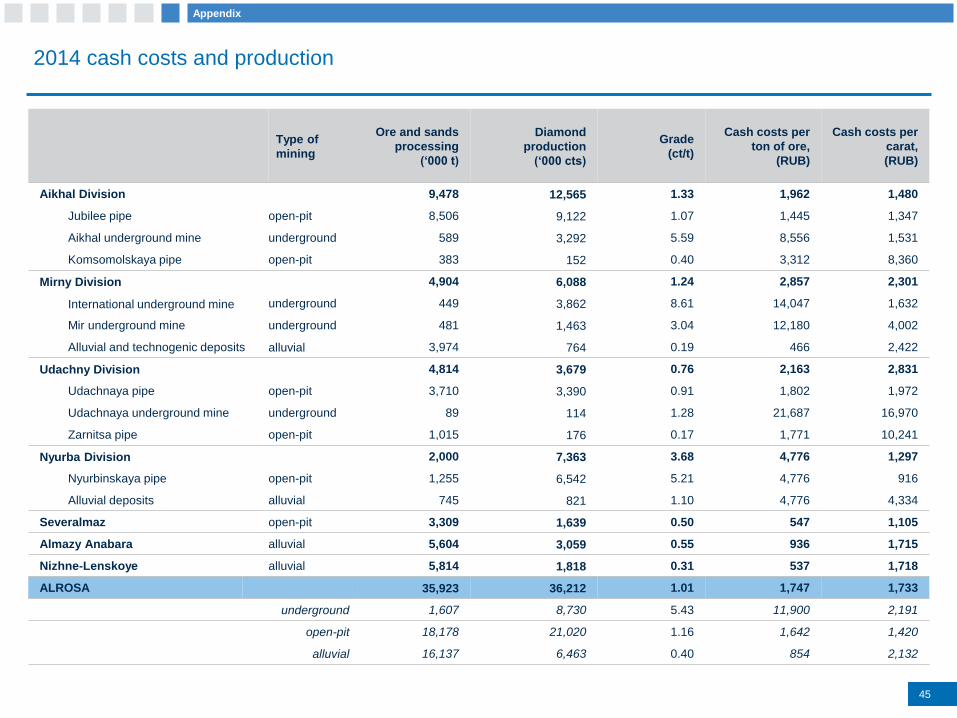

Type of

mining

Ore and sands

processing

(‘000 t)

Diamond

production

(‘000 cts)

Grade

(ct/t)

Cash costs per

ton of ore,

(RUB)

Cash costs per

carat,

(RUB)

Aikhal Division 9,478 12,565 1.33 1,962 1,480

Jubilee pipe open-pit 8,506 9,122 1.07 1,445 1,347

Aikhal underground mine underground 589 3,292 5.59 8,556 1,531

Komsomolskaya pipe open-pit 383 152 0.40 3,312 8,360

Mirny Division 4,904 6,088 1.24 2,857 2,301

International underground mine underground 449 3,862 8.61 14,047 1,632

Mir underground mine underground 481 1,463 3.04 12,180 4,002

Alluvial and technogenic deposits alluvial 3,974 764 0.19 466 2,422

Udachny Division 4,814 3,679 0.76 2,163 2,831

Udachnaya pipe open-pit 3,710 3,390 0.91 1,802 1,972

Udachnaya underground mine underground 89 114 1.28 21,687 16,970

Zarnitsa pipe open-pit 1,015 176 0.17 1,771 10,241

Nyurba Division 2,000 7,363 3.68 4,776 1,297

Nyurbinskaya pipe open-pit 1,255 6,542 5.21 4,776 916

Alluvial deposits alluvial 745 821 1.10 4,776 4,334

Severalmaz open-pit 3,309 1,639 0.50 547 1,105

Almazy Anabara alluvial 5,604 3,059 0.55 936 1,715

Nizhne-Lenskoye alluvial 5,814 1,818 0.31 537 1,718

ALROSA 35,923 36,212 1.01 1,747 1,733

underground 1,607 8,730 5.43 11,900 2,191

open-pit 18,178 21,020 1.16 1,642 1,420

alluvial 16,137 6,463 0.40 854 2,132

Appendix