Embed Size (px)

Citation preview

Inspiring consumer confidence in

challenging economic times

Graham Pickett

Lead Partner – Travel, Hospitality & Leisure

June 2013

© 2013 Deloitte LLP

Inspiring consumer confidence in challenging economic timesAgenda

Overcoming

barriers to

growth

Prospects for

the UK

consumer

economy

The crisis

continues

Europe in a global

context

Europe in a global context

© 2013 Deloitte LLP

Developing nations remain key driversAs developing nations remain key to global economic growth, prevailing Eurozone crisis continues

to threaten Europe’s role in the global economy.

2.2%

-0.2% -0.5%

0.6%

7.8%

5.5% 5.3%

3.1%

5.5%

3.7% 3.6%

1.6%

0.3% 0.1%0.8%

7.5%

4.7% 5.0%

3.0%

2.2%

4.2%

2.9%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

US Europe(EU27)

Euro Area Japan China India Otherdeveloping

Asia

LatinAmerica

MiddleEast

Africa Russia,Central

Asia, andSoutheast

Europe

Global growth of Gross Domestic Product (%)

2012 2013(Projected)

Source: The Conference Board Global Economic Outlook 2013

© 2013 Deloitte LLP

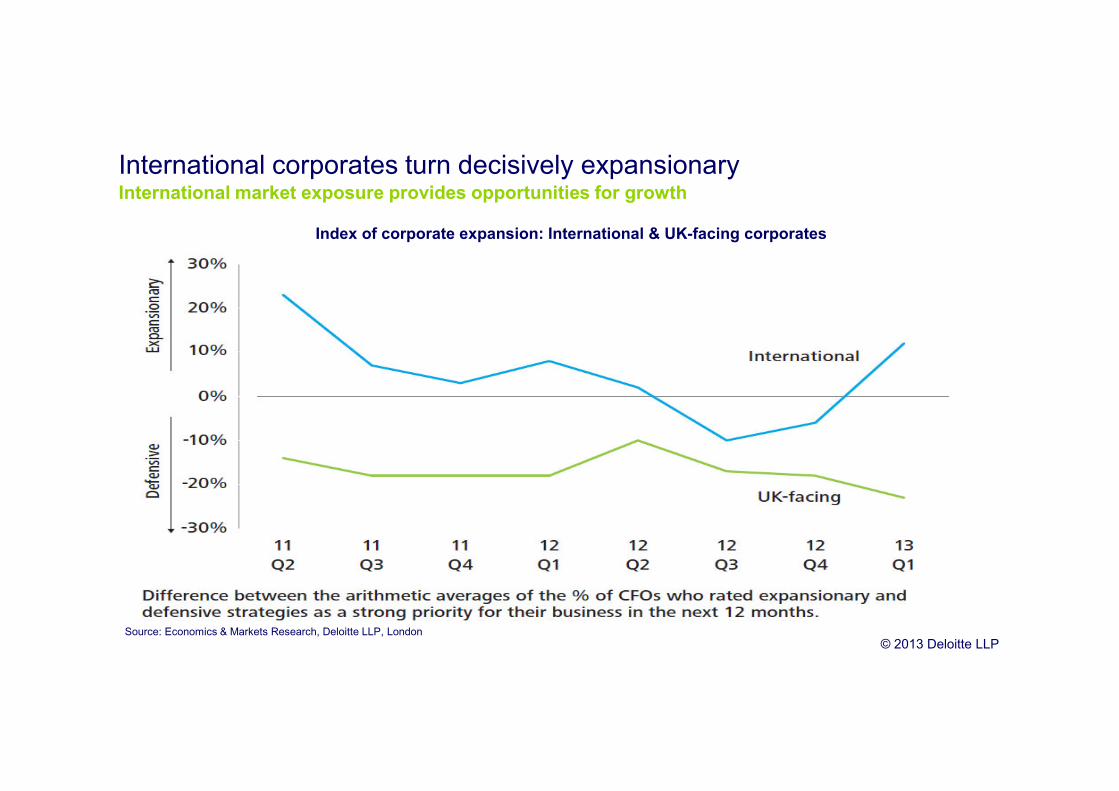

International corporates turn decisively expansionaryInternational market exposure provides opportunities for growth

Source: Economics & Markets Research, Deloitte LLP, London

Index of corporate expansion: International & UK-facing corporates

Europe remains on the edge

© 2013 Deloitte LLP

Support for European unity on declineWhile support for Euro is still strong in major European countries, favourability for the European

Union continues to decline, thus putting stress on political will to keep EU together.

52%

60%

66%

71%

69%

64%

67%

66%

69%

63%

0% 20% 40% 60% 80%

Italy

Spain

Germany

Greece

France

Support for Euro currency (% Keep the Euro)

2013

2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2007 2009 2010 2011 2012 2013

EU Favourability (% Favourable)

Germany United Kingdom Spain France

Source: Pew Research Center (The New Sick Man of Europe: the European Union)

© 2013 Deloitte LLP

Euro breakup fears easing, but risks remain

Source: Economics & Markets Research, Deloitte LLP, London

37%

26%

36%

27%

22%18%

2011 Q4 2012 Q1 2012 Q2 2012 Q3 2012 Q4 2013 Q1

Average probability of euro secession

Probability assigned by UK CFOs to the likelihood of any of the existing members of the euro area not being in the single currency

in the next 12 months (%)

© 2013 Deloitte LLP

Eurosystem imbalances narrow but remain wide

Source: Institute of Empirical Economic Research - Osnabrück University

-600

-400

-200

0

200

400

600

800

1000

Jan-0

3

Apr-

03

Jul-0

3

Oct-

03

Jan-0

4

Apr-

04

Jul-0

4

Oct-

04

Jan-0

5

Apr-

05

Jul-0

5

Oct-

05

Jan-0

6

Apr-

06

Jul-0

6

Oct-

06

Jan-0

7

Apr-

07

Jul-0

7

Oct-

07

Jan-0

8

Apr-

08

Jul-0

8

Oct-

08

Jan-0

9

Apr-

09

Jul-0

9

Oct-

09

Jan-1

0

Apr-

10

Jul-1

0

Oct-

10

Jan-1

1

Apr-

11

Jul-1

1

Oct-

11

Jan-1

2

Apr-

12

Jul-1

2

Oct-

12

Jan-1

3

Apr-

13

Net Balance with the Eurosystem/Target (EUR billions)

Germany Greece Spain France Italy

© 2013 Deloitte LLP

Europe’s unemployment woes continueBenefiting from its education and skill development policies, Germany continues to maintain a

lower unemployment rate than its European peers.

Source: Eurostat

Germany

United Kingdom

Spain

France

Italy

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010 2011 2012 2013

Unemployment rate (%)

Germany United Kingdom Spain France Italy

© 2013 Deloitte LLP

Europe remains a key destination for UK travellers

Source: ONS

Spain19.7%

France15.5%

USA5.3%

Irish Republic5.0%Italy

4.7%Germany

4.1%Portugal

3.4%

Netherlands3.4%

Greece3.2%

Belgium2.9%

Rest of the World32.9%

Countries visited by UK residents in 2012 (as % of total overseas visits)

Prospects for the UK consumer?

© 2013 Deloitte LLP

Prospects for the UK consumer?Three key issues

1

2

3

© 2013 Deloitte LLP

Impacts on consumer spending

© 2013 Deloitte LLP

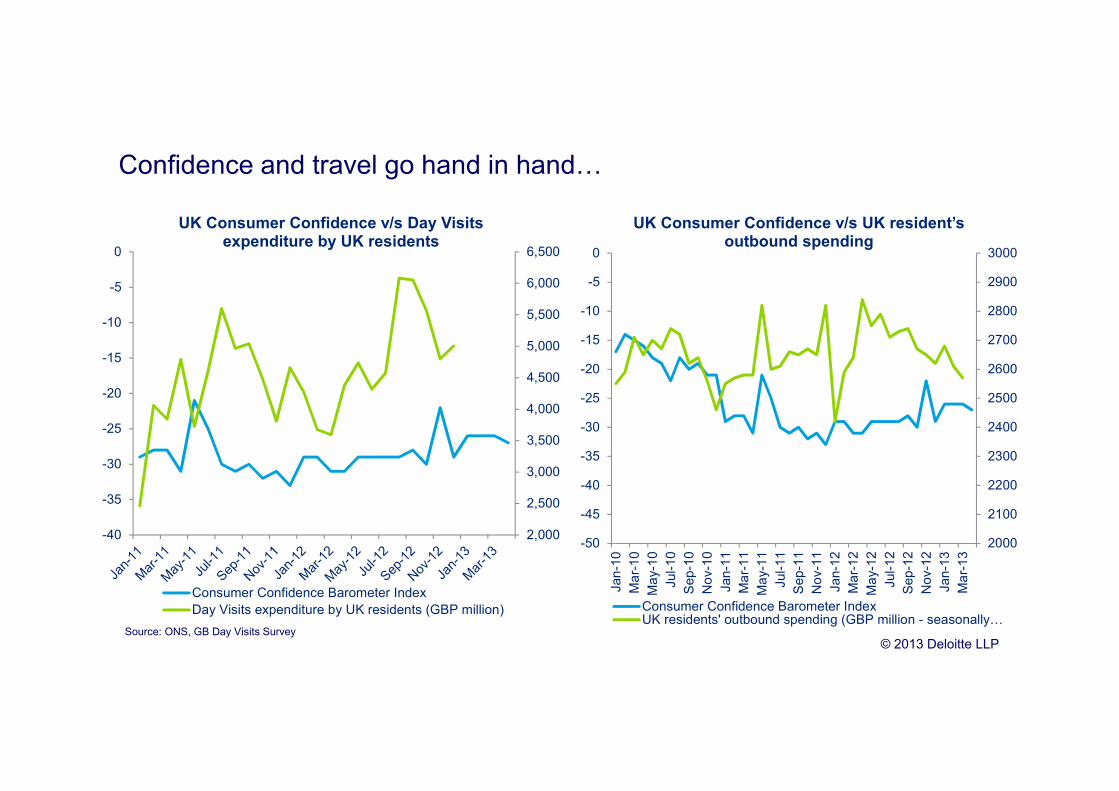

Confidence and travel go hand in handG

Source: ONS, GB Day Visits Survey

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

-40

-35

-30

-25

-20

-15

-10

-5

0

UK Consumer Confidence v/s Day Visits expenditure by UK residents

Consumer Confidence Barometer Index

Day Visits expenditure by UK residents (GBP million)

2000

2100

2200

2300

2400

2500

2600

2700

2800

2900

3000

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Jan-1

0

Ma

r-1

0

Ma

y-1

0

Jul-1

0

Sep-1

0

No

v-1

0

Jan-1

1

Ma

r-1

1

Ma

y-1

1

Jul-1

1

Sep-1

1

No

v-1

1

Jan-1

2

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Sep-1

2

No

v-1

2

Jan-1

3

Ma

r-1

3

UK Consumer Confidence v/s UK resident’s outbound spending

Consumer Confidence Barometer IndexUK residents' outbound spending (GBP million - seasonallyG

© 2013 Deloitte LLP

Consumers taking control of their debt

Source: BBA - Credit Card Statistics

60%

62%

64%

66%

68%

70%

72%

74%

76%

78%

80%

50,000

52,000

54,000

56,000

58,000

60,000

62,000

64,000

66,000

68,000

70,000

Jan '0

8

Apr

'08

Jul '0

8

Oct '0

8

Jan '0

9

Apr

'09

Jul '0

9

Oct '0

9

Jan '1

0

Apr

'10

Jul '1

0

Oct '1

0

Jan '1

1

Apr

'11

Jul '1

1

Oct '1

1

Jan '1

2

Apr

'12

Jul '1

2

Oct '1

2

Jan '1

3

UK Credit card debt outstanding and % of outstanding balances bearing interest

Credit outstanding (GBP million)

Percentage of outstanding balances bearing interest (%)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

UK Credit cards in issue v/s Active card accounts

Number of cards in issue (thousands)

Number of active accounts (thousands)

© 2013 Deloitte LLP

Private sector hiring, offsets job losses in public sector

© 2013 Deloitte LLP

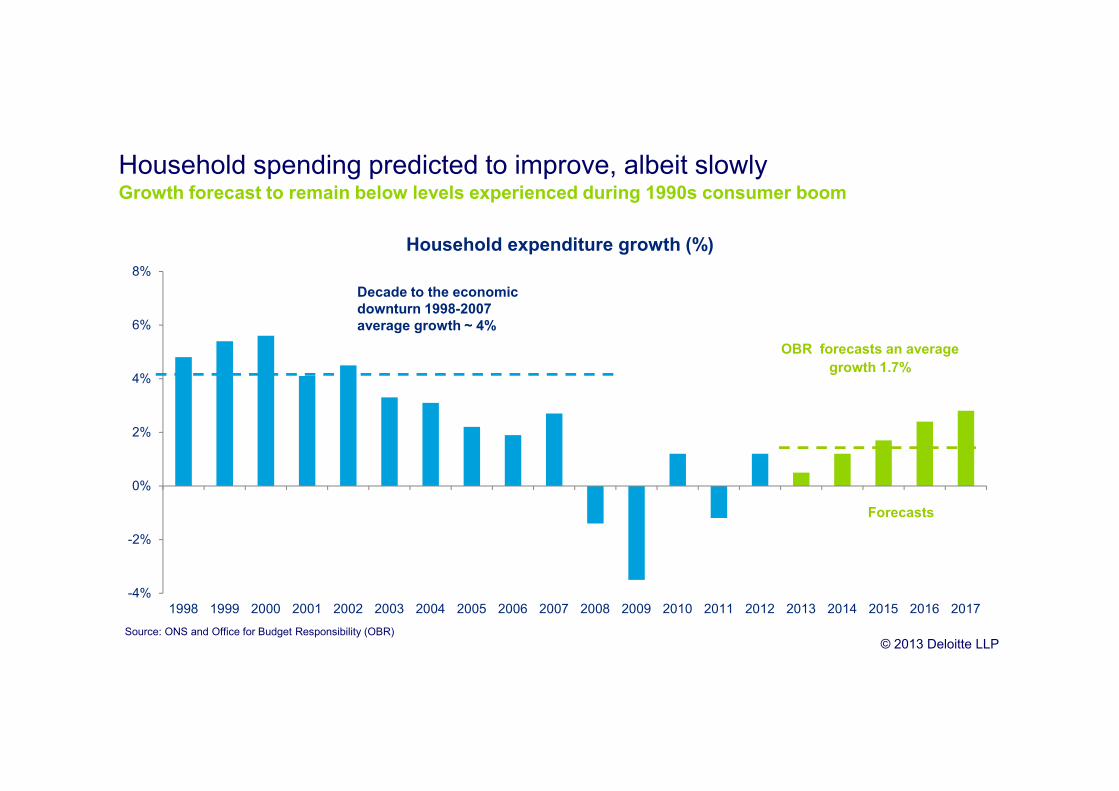

Household spending predicted to improve, albeit slowlyGrowth forecast to remain below levels experienced during 1990s consumer boom

Source: ONS and Office for Budget Responsibility (OBR)

-4%

-2%

0%

2%

4%

6%

8%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Household expenditure growth (%)

OBR forecasts an average

growth 1.7%

Decade to the economic

downturn 1998-2007

average growth ~ 4%

Forecasts

© 2013 Deloitte LLP

3% 3%2%

5% 5%

8%9%

20%

3% 3% 3%

5% 5%

7%

9%

19%

0%

5%

10%

15%

20%

25%

Selling anexpensive

electrical item

Downsizing:moving into asmaller home

Upgrading:moving into alarger home

Buying a car Buying a majorhome

appliance

Buying anexpensive

electrical item

Homeimprovements

Long breakholiday

UK consumers major purchases for the next three months

Q1 2012 Q1 2013

Consumers will still not compromise on their holidaysUK Consumer spending expectations for major purchases

Source: Deloitte Consumer Tracker (Q1 2013)

© 2013 Deloitte LLP

Majority of corporates now focused on growthImproving situation allows business to switch out of survival mode

© 2013 Deloitte LLP

Business leadership seen as key for the new growthAs consumers and government are unable to kick start the economy

© 2013 Deloitte LLP

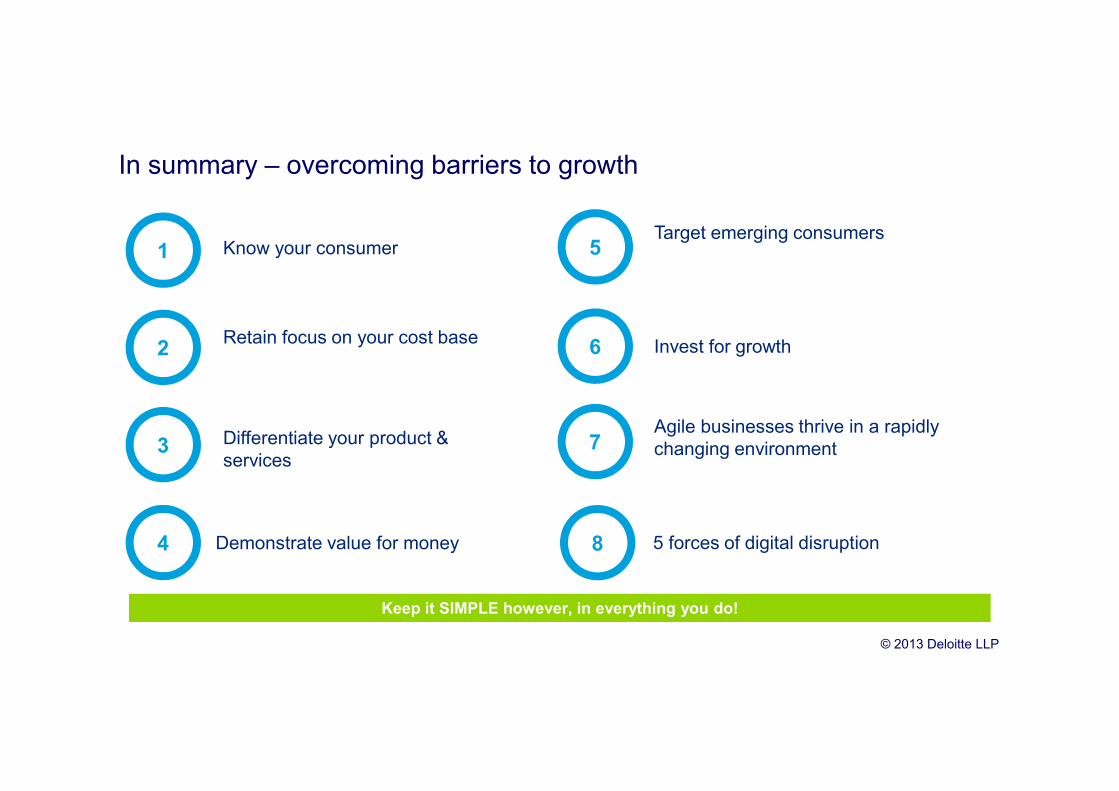

In summary – overcoming barriers to growth

Keep it SIMPLE however, in everything you do!

Know your consumer1

2

3

4

Retain focus on your cost base

Differentiate your product &

services

Demonstrate value for money

5Target emerging consumers

6

7

Invest for growth

Agile businesses thrive in a rapidly

changing environment

8 5 forces of digital disruption

© 2013 Deloitte LLP

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms,

each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and

its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will

depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of

the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific

circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any

material in this publication.

© 2013 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street

Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

Member of Deloitte Touche Tohmatsu Limited