-

Gazprom in the European Gas Market

by Valery Nemov

OOO Gazprom Export

Deputy Head Contract Structuring and Pricing Directorate

Novy Urengoy, June 19, 2017

-

1 Gazprom in the European Gas Market

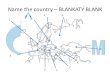

Poland, 11.1

France, 11.5

United Kingdom

17.9

Italy, 24.7

Turkey, 24.8

Germany, 49.8

Deliveries by Gazprom Group

to Far Abroad in 2016 (under OOO Gazprom export and GAZPROM

Schweiz AG contracts)

• In 2016, total gas

deliveries reached

unprecedented

179.3 bcm

• Annual growth totaled

in 19.9 bcm

(+12.5%)

• In 2016, the biggest

customers were

Germany, Turkey and

Italy with the former

having received

record-breaking 49.8

bcm

-

2

583 598 564 602

551 542 540 485 507

542

26% 27% 25% 23% 27% 26% 30% 30% 31% 33%

0

100

200

300

400

500

600

700

800

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Consumption Gazprom Group deliveries*, bcm Gazprom Group's

share*

150,5

Gazprom in Europe

bcm

* Volumes sold under Gazprom Export and Gazprom Schweiz

contracts to European Far Abroad

Gazprom Group’s* Share in the European Consumption

158,8 140,6 138,6 150,3 139,9 162,7 147,6 159,4

179,3

158,8 140,6 138,6 150,3 139,9 162,7 147,6 159,4 179,3 150,5

Gazprom in the European Gas Market

-

3

Gazprom Group’s* Share in the European Imports**

271 273 257 280 274

248 255 225 240

273

56% 58% 55% 50% 55% 56% 64% 66% 66% 66%

0

100

200

300

400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Consumption, bcm Gazprom Group deliveries*, bcm Gazprom Group's

share*

139,9 162,7 147,6 159,4

179,3

bcm

* Volumes sold under Gazprom Export and Gazprom Schweiz

contracts to European Far Abroad

** Difference between consumption and domestic production

158,8 150,5 140,6 138,6 150,3

Gazprom in Europe

Gazprom in the European Gas Market

-

4

Gas Consumption in Europe, 2011-2015

European Gas Consumption in 2013 – 2017

In Q1 2017 natural gas

consumption in Europe

exceeded the volumes

of Q1 2016 by 4 bcm or

2.2%, amounting to

183.3 bcm. It is

remarkable that

consumption volumes

were higher in January

(+11.0 bcm or +16.0%)

but lower in February

and especially in March

(-0.4 bcm or -0.7% and -

6.6 bcm or -12.0%

respectively), reflecting

the impact of the

weather factor.

Monthly Gas Consumption (Accumulated Values)

Gazprom in the European Gas Market

-

5

Medium-Term Gas Consumption Forecast

Medium-Term Forecasts by Leading Industry Consultants

(Consumption in 2012 = 100%)

CERA and PIRA industry

consultants as well as IEA

experts expect adjustment of

gas demand in 2017 after

perceptible growth in 2016.

However, afterwards the

expectations about future

demand differ significantly.

These differences are

explained mainly by different

assumptions about gas

demand in power generation.

Whereas the PIRA consultants

assume a negative trend in

gas-fired power generation

until 2020, the CERA experts

on contrary forecast a

continuing growth of demand

as early as 2018.

Gazprom in the European Gas Market

-

6

Major Factors Affecting Gas Consumption in

Europe in Q1 2016 and Q1 2017*

Q1 2016 Q1 2017

1.Favorable weather conditions

(cold and long winter, hot summer)

2. Economic recovery

3. Use of gas in power generation

4. Base period effect

Total consumption dynamics, YoY: +2.7% +2.2%

* Factors are defined in comparison with long-term averages.

Factors could affect consumption in a bidirectional way. Changes in

volumes

made on year-on-year and quarter-on-quarter basis.

Gazprom in the European Gas Market

-

7

Gas-fired Power Generation Projected Growth

Power generation is

the key area for gas

consumption growth in

Europe.

Even the ‘greenest’,

heavily subsidisied

scenario envisages

more electricity to be

produced from gas.

By 2025 ‘basic’

scenario foresees

30%+ growth in the EU

gas generation against

2015 figures.

‘Basic’ scenario* ‘Strategy 2030’**

* 21% energy efficiency rise by 2030, 33% CO2 emissions cut by

2030 against the 1990 level, renewables reaching 24.4% in primary

energy consumption by 2030

** 27% energy efficiency rise by 2030, 40% CO2 emissions cut by

2030 against the 1990 level, renewables reaching 27% in primary

energy consumption by 2030

Source: European Commission, ENTSO-E

438

473

489

505

521

537

554

570

586

602

618

634

650

666

682

698

714

0

500

1000

1500

2000

2500

3000

3500

4000

2014

2016

2018

2020

2022

2024

2026

2028

2030

ТWh

33.3

%

33.6

%

Gazprom in the European Gas Market

438

473

476

478

481

484

487

489

492

495

497

500

503

505

508

511

513

0

500

1000

1500

2000

2500

3000

3500

4000

2014

2016

2018

2020

2022

2024

2026

2028

2030

Oil

Natural Gas

Coal

Wind

Solar, tidal etc.

Biomass

Hydro

Nuclear

ТWh

26.4

%

40.1

%

-

8

Demand for Natural Gas in Power Generation

Q1 2016 Q1 2017 ∆, bcm ∆, %

Total gas consumption 179.4 183.3 4.0 2.2%

Gas consumption in power generation 43.4 45.3 2.0 4.6%

Share of power generation in gas consumption 24.2% 24.7% 0.6

pp

Gas consumption in other sectors 136.0 138.0 2.0 1.5%

Demand for Natural Gas in Power Generation in European Far

Abroad

Demand for natural gas in power generation in European Far

Abroad in Q1 2017 increased by 4.6%, outrunning the growth of

demand in other sectors, which amounted to only 1.5% compared to

Q1 2016.

The share of power generation in total demand for natural gas

grew up to 24.7% in Q1 2017 (Q1 2016 – 24.2%).

Sources: Eurostat, International energy agency (IEA), ENTSOG,

IHS, PIRA, National Statistical Agencies as of April 2017.

Given values may differ from the calculated ones as they are

rounded.

Gazprom in the European Gas Market

-

9

Gas/coal Competition in Power Generation

(Germany and the UK) (1)

Source: based on Bloomberg, Department of Energy and Climate

Change of the UK’s Government (DECC)

Germany UK*

Increase of natural gas price on NCG in Q1 2017 accompanied by

adjustment of coal prices reduced attractiveness of gas-fired power

plants against coal-

based power generation in Germany. According to forward curves,

coal price decrease until 2018 accompanied by stabilization of gas

prices will lead to

deterioration of market conditions for gas demand in German

power generation.

Meanwhile the Carbon Price Support mechanism in the UK provides

higher margins for gas-fired power plants than coal-fired ones.

However, as forward

indicates, the competitiveness of gas power generation will

decline in winter periods.

*Including UK Carbon Price Support

Gazprom in the European Gas Market

-

10

Gas/coal Competition in Power Generation

(Germany and the UK) (2)

Source: based on Bloomberg, Department of Energy and Climate

Change of the UK’s Government (DECC)

Gas-Coal Switching Price in Power Generation in Germany and the

UK*

*Difference between gas-coal switching prices is due to

different efficiencies of power plants on German and British

markets and due to UK Carbon Price Support as addition to EU

ETS.

** Gas price - TTF Day-ahead. *** Coal price - CIF ARA

Decline of natural gas prices on European hubs in 2015, increase

of coal price in 2016 and introduction of Carbon Price Support

mechanism in the UK boosted

a competitiveness of gas-fired power plants significantly in

2016 and in Q1 2017. In the UK the price difference supported

switch from coal to gas, while on the

German market only the most effective gas-fired power plants

became more competitive. Forward prices for deliveries in 2017-2018

indicate an expected

decline of coal prices and insignificant seasonal increase of

gas prices during winter peak-loads. It might make gas less

attractive in power generation.

However, gas will remain more competitive than coal in the

UK.

Gazprom in the European Gas Market

-

11 11

Deliveries to the European* market by foreign and domestic

producers, bcm

*European countries with Turkey (excluding CIS and Baltics) **

Iranian supplies to Turkey

*** Including pipeline and LNG deliveries from Norway to the

European market, but not LNG to Asia and America

Source: Eurostat, IEA, IHS, National Statistics, PJSC Gazprom,

PIRA

Major Suppliers to the European Market

159,4

37,6 28,4

7,9 8,1

124,5

44,6 48,9

179,3

51,2

24,0 9,8 8,0

124,0

46,4 45,4

0

50

100

150

200

GAZPROM JSC ALGERIA

(INCL. LNG)

QATAR NIGERIA IRAN** NORWAY*** UNITED

KINGDOM

NETHERLANDS

2015 2016

Gazprom in the European Gas Market

-

12

Supply Dynamics to Europe

by Major Foreign Producers (Q1’2017)

Sources: Eurostat, IEA, ENTSOG, Bloomberg, National Statistical

Agencies as of April 2017.

Given values may differ from the calculated ones as they are

rounded.

Comparison of supply dynamics in Q1 2017 with range of

deliveries in 2010–

2016 demonstrates a record level of supplies by PJSC Gazprom, as

well as

close to the average level of supplies from Algeria and a low

level of LNG

supplies from Qatar.

Gazprom in the European Gas Market

-

13

Supply Dynamics to Europe

by Major Domestic Producers (Q1’2017)

Sources: Eurostat, IEA, ENTSOG, Bloomberg, National Statistical

Agencies as of April 2017.

Given values may differ from the calculated ones as they are

rounded.

Comparison of supply dynamics in Q1 2017 with range of

deliveries in 2010 –

2016 demonstrates a high level of supplies from Norway, which in

January

and March were higher than those of previous years, as well as a

low level of

supplies from the Netherlands and the UK.

Gazprom in the European Gas Market

-

14

TurkStream

• TurkStream – a direct (bypassing transit countries) gas

pipeline project from

Russia under the Black Sea to Turkey and to the Turkish border

to neighboring

countries

• The first line (15.75 bcm/y) will be aimed for the Turkish

market, the second (of

the same capacity) — for supplies to the EU

• RUS-TUR Intergovernmental Agreement signed October 10,

2016

• Offshore project is pursued by South Stream Transport B.V. —

PAO Gazprom

100% subsidiary

• Pipelaying started May 7, 2017

• TurkStream is to be phased in by the end of 2019

Gazprom in the European Gas Market

-

15

Nord Stream 2

• Following the success of the first Nord Stream,

the Nord Stream 2 project provides for a twin

pipeline to go from Russia under the Baltic Sea

to Germany carrying additional 55 bcm/y

• Along with higher security of supplies Nord

Stream 2 supports European drive for energy

security and emissions cut

• Project is handled by Nord Stream 2 AG

• Agreements to finance the project have been

signed by Nord Stream 2 AG with energy

majors ENGIE, OMV, Shell, Uniper и Wintershall

Gazprom in the European Gas Market

-

16

Underground Storages: Getting Supplies More

Reliable and Flexible

Rehden

Banatski Dvor

Katharina

Bergermeer

Haidach

Dambořice

In 2016/2017, Gazprom Group companies had

access to 5 bcm storage capacity in European gas

storages.

In 2016/2017, the maximum daily withdrawal rate

In Western Europe topped 83,3 mcm.

The two recently commissioned storage projects of Gazprom Group

in Europe are UGS Katharina and UGS Dambořice:

• Katharina operates six caverns, with the total active capacity

of 315 mcm and the maximum daily production rate of 23.2

mcm.

• On June 1, 2016 Czech UGS Dambořice with the designed active

capacity of 456 mcm was phased in. Currently Gazprom

Group has access to the active capacity of 156 mcm with the

daily production rate up to 3.7 mcm.

Gazprom in the European Gas Market

Etzel

Jemgum

http://www.ugs-katharina.de/http://www.gasstoragebergermeer.com/http://www.gsa-services.ru/http://www.gasstoragebergermeer.com/

-

17

• In 2013-2016, the number of Gazprom Group natural gas filling

stations in Europe went from 23 to 69

• In 2016 Gazprom Group entered the Serbian gas motor fuel

market

• The volume of CNG/LNG supplied to own and third party NGV

filling stations rose from 4.8 mcm to 14.6 mcm

• The Gazprom NGV Europe company together with local partners

implements first European projects on municipal LNG-powered

buses introduction in Poland

• By 2025 the capacity of the European gas motor fuel market

might amount to as much as 27 bcm in additional demand*

Natural Gas as Motor Fuel

* ACER (Agency for the Cooperation of Energy Regulators)

forecast.

0

5

10

15

20

2013 2014 2015 2016

Serbia

Czech Rep.

Poland

Germany

Sales of gas for NGV through own and third party stations ,

mcm/y

Gazprom in the European Gas Market

-

18

Source: adapted Timera

Energy periodization given

in article “The next phase

of global gas pricing”

See: http://www.timera-

energy.com/the-next-

phase-of-global-gas-

pricing/

European Gas Pricing History by Periods

1) ‘Global gas glut’ (Jun ‘08 – Dec ‘10) only strengthened

European gas prices despite the LNG flood. European gas prices just

followed oil price

recovery prior to Fukushima.

2) ‘Fukushima tightness’ (Mar ‘11 – Dec ‘14) gave no special

momentum to gas price developments: erratic fluctuations of gas

prices completely

ignored outflow of large LNG volumes from Europe.

3) ‘Oversupply and price convergence’ (Dec ’14 – current):

although gas prices start to weaken prior to September 2014 due to

abnormally warm Q1

2013, their collapse coincided with oil price drop on the market

which has already rebalanced itself.

Gazprom in the European Gas Market

-

19

Ceiling

Floor

Oil/Oil products

parity

Coal parity

Source: Gazprom Export

Inter-Fuel Competition Defines Upper and Lower

Price Range Levels for Natural Gas

Gazprom in the European Gas Market

-

20

Oil-p

ari

ty Co

al-p

arity

Loose market Tight market

Buoy 1

Buoy 2

Buoy 3

LTCs

prices

Gas price as

derivative of shale oil

breakeven costs

Price of shale

gas full costs of

deliveries to Europe

Pri

ce

Up

Pric

e

Do

wn

Hub Natural Gas Price Navigation in Europe

Gazprom in the European Gas Market

-

21

Bouy #1. Extreme Weather Conditioned Pushed

TTF Prices above BAFA for Nearly Two Months

Sources: BAFA, Bloomberg

In January – February 2017 natural gas on the most liquid

European hub TTF was traded with a premium to average import price

in Germany (BAFA), reflecting the higher demand for natural gas as

a consequence of weather impact. However, in March prices declined

due to a lower gas demand at the end of the winter season. Gas

futures with delivery in Summer 2017 are traded at a level of

$175/Mcm, whereas the winter futures – at a level of $190/Mcm.

Thus, the seasonal spread is about $15/Mcm.

Gazprom in the European Gas Market

-

22

Bouy #2. Correlation and Regression Analysis

Indicates

that TTF Price Dependence on Oil Prices is

Increasing Correlation (TTF MA, USD/mcm)

Time period Brent,

USD/barrel

Oil Price:

Six month moving

average

Oil Price:

Nine month moving

average

2008-2016 76.6% 85.5% 83.3%

2008-2013 69.9% 84.7% 81.9%

2014-2016 79.5% 87.3% 88.7%

R Squared

(TTF MA, USD/mcm)

2008-2016 58.6% 73.1% 69.4%

2008-2013 48.9% 71.8% 67.1%

2014-2016 63.2% 76.3% 78.6%

This effectively means that NA shale breakeven costs which

emerged as the major determinant for

global oil prices are setting price rage for European hub

prices

Gazprom in the European Gas Market

-

23

Bouy#3. Outlook for NA LNG Export to Europe

In current

circumstances,

prices of European

Futures do not

cover full cycle

costs of US LNG,

which are indexed

to Henry Hub prices

Estimated Costs* of US LNG Deliveries to Europe vs. Prices of

European Gas Futures**

* Based on Henry Hub-related contract price, P = 115% *

Henry Hub + X, where X are costs of liquefaction, shipping

and regasification

** Historical NBP 1st Month and current NBP Futures

*** Historical price of Russian gas deliveries to Germany

(based on World Bank data) and projected price based on

current Brent and TTF Futures

Source: Bloomberg, Cheniere Energy, Wood Mackenzie,

World Bank

Gazprom in the European Gas Market

-

24

Thank you!

Gazprom in the European Gas Market