Embed Size (px)

Citation preview

ICEX Seminar

Working with the European Bank

for Reconstruction and Development (EBRD)

May 2016

Madrid, Spain

1. INTRODUCTION TO EBRD

2. EBRD’S INFRASTRUCTURE BUSINESS GROUP (IBG)

3. SEMED, TURKEY AND KAZAKHSTAN – OPPORTUNITIES AND CHALLENGES

4. CASE STUDIES

5. CONTACTS

2

Contents

The EBRD is an international, AAA-rated financial

institution, which promotes transition to market economies

3

EBRD is an international financial

institution that promotes transition to

market economies.

Owned by 65 countries and 2

inter-governmental institutions (EU, EIB).

Recent “new” countries: 2014 Cyprus,

2015 Greece, 2016 Lebanon.

China most recent shareholder (Jan

2016).

Capital base of around EUR 38 billion.

SHAREHOLDING STRUCTURE WHO WE ARE

The EBRD has a triple-A rating from all three main

rating agencies (S&P, Moody’s and Fitch)

(1) Includes European Community and European Investment Bank (EIB) each

at 3%. Among other EU countries: France, Germany, Italy, and the UK each

holds 8.6%

(2) Russia at 4%

EU 27 Countries (1); 59%

EBRD region excluding EU;

14%

USA; 10%

Japan; 9%

Others; 9%

Russia

Kazakhstan Mongolia

—Kyrgyz Republic

—Tajikistan

—Moldova

—Jordan

Azerbaijan

—Morocco

Belarus

Ukraine

—Romania —Serbia

—Kosovo Georgia—

Armenia—

Tunisia—

Croatia— Bosnia and Herzegovina—

Montenegro—

Albania—

FYR Macedonia

—Turkmenistan

—Bulgaria

Estonia—

Latvia—

Lithuania—

Poland

Slovenia—

Czech Republic—

—Slovakia

—Hungary

Uzbekistan—

Central

Eastern Europe SEMED Western Balkans Turkey

Armenia,

Azerbaijan,

Belarus,

Georgia,

Moldova,

Ukraine

Central Asia

(incl. Mongolia)

Egypt—

Where we invest

Greece

Cyprus

The EBRD is active in 37 countries

5

Projects in 37 countries across various

sectors.

Aim to promote transition to market

economies by investing mainly in the

private sector.

Mobilise significant foreign direct

investment.

Support privatisation, restructuring and

better municipal services to improve

people’s lives.

Encourage environmentally sound and

sustainable development

EBRD TOP 10 COUNTRIES (ABI IN EUR M) OUR OBJECTIVES

2013 2015

1 RUSSIAN

FEDERATION 1,816 1 TURKEY 1,904

2 TURKEY 920 2 UKRAINE 997

3 UKRAINE 798 3 EGYPT 780

4 POLAND 756 4 KAZAKHSTAN 709

5 ROMANIA 508 5 POLAND 647

6 SERBIA 424 6 SERBIA 478

7 KAZAKHSTAN 328 7 MONGOLIA 467

8 CROATIA 288 8 MOROCCO 431

9 BELARUS 255 9 GREECE 320

10 SLOVAK

REPUBLIC 237 10 AZERBAIJAN 269

The EBRD has invested over EUR 105 billion across a wide

range of projects

6

EBRD invested over EUR 105 billion

in around 4,500 projects since 1991.

Loan, equity and guarantees for well-

structured, financially robust projects

of all sizes (incl. many small

businesses).

Close policy dialogue with

governments, civil society and other

stakeholders.

Targeted technical assistance.

Focus on working with the private

sector to foster innovation and open-

market economies.

EBRD SECTORS WHAT WE DO AND WHERE WE ARE

Transport Municipal & Environmental

Infrastructure

Property & Tourism

Financial Institutions Natural Resources Telecommunications,

Informatics & Media

Industry, Commerce

& Agribusiness

Manufacturing

& Services

Power & Energy

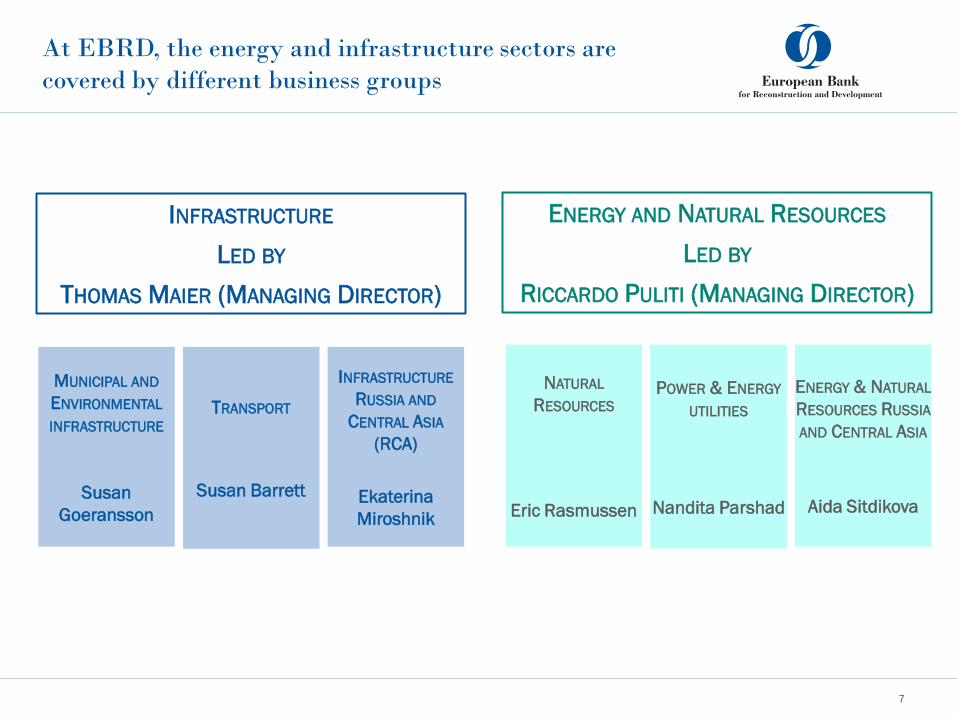

At EBRD, the energy and infrastructure sectors are

covered by different business groups

7

ENERGY AND NATURAL RESOURCES

LED BY

RICCARDO PULITI (MANAGING DIRECTOR)

INFRASTRUCTURE

LED BY

THOMAS MAIER (MANAGING DIRECTOR)

MUNICIPAL AND

ENVIRONMENTAL

INFRASTRUCTURE

Susan

Goeransson

TRANSPORT

Susan Barrett

INFRASTRUCTURE

RUSSIA AND

CENTRAL ASIA

(RCA)

Ekaterina

Miroshnik

NATURAL

RESOURCES

Eric Rasmussen

POWER & ENERGY

UTILITIES

Nandita Parshad

ENERGY & NATURAL

RESOURCES RUSSIA

AND CENTRAL ASIA

Aida Sitdikova

In 2015, EBRD invested a total of EUR 9.5 billion in 380

projects across a wide range of sectors

8

2015 INVESTMENTS:

Debt 82%, Equity 14% and

Guarantee 4%.

Capital market transactions ~20%.

Net profit expected at

EUR 0.8 billion.

Local currency: Tenge, Lira, Rouble,

etc.

Both, direct investments and through

holding companies.

Amid economic and political turbulence,

EBRD remains a strong, resilient and

trusted partner.

0

20

40

60

80

100

120

0

1

2

3

4

5

6

7

8

9

10

11

12

Net c

um

ula

tive b

usin

ess in

vestm

ent

Annual busin

ess investm

ent

(AB

I) in E

UR

bn

1)

Debt ABI Equity ABI Net Cumulative ABI

(1) Annual Bank investment (ABI) is the volume of commitments made by

the Bank during the year

ANNUAL BANK INVESTMENT1) 2011-2015

EBRD financing with Spanish Companies

9

VALUE OF JOINT SPAIN-EBRD INVESTMENT

EUR 4.0 billion as of December 2015:

• EUR 2.3 billion from EBRD

• EUR 1.6 billion from Spain

Major target regions: Poland, Romania and Hungary.

Dominant investment sectors:

• Energy: EUR 1.9 billion

• Industry, Commerce and Agribusiness: EUR 1.2 million

• Infrastructure: EUR 0.3 billion

• Financial Institutions: EUR 0.6 billion

1. INTRODUCTION TO EBRD

2. EBRD’S INFRASTRUCTURE BUSINESS GROUP (IBG)

3. SEMED, TURKEY AND KAZAKHSTAN – OPPORTUNITIES AND CHALLENGES

4. CASE STUDIES

5. CONTACTS

10

Contents

EBRD’s infrastructure business group exemplified

continuous growth

11

EBRD INFRASTRUCTURE YE2015

Number of projects to date 640

Net cumulative Bank investment EUR 19.7bn

Non-sovereign Share 50 per cent

EBRD’s infrastructure business group as engaged partner

to facilitate investments across sectors

12

TRANSPORT MUNICIPAL /ENVIRONMENTAL INFRASTRUCTURE

In 2015: Investments of over EUR 0.7

billion in 45 transactions.

Since 1994: Over 360 transactions and

commitment of EUR 5.8 billion.

Sector focus: Water and sewage, solid

waste, district heating, urban transport

and roads.

Since 2006: total of 15 PPP transactions

with over EUR 680 million in finance

In 2015: Investments of over EUR 1.0

billion in over 25 transactions.

Since 1994: Over 275 transactions and

commitment of EUR 13.9 billion.

Sector focus: Roads, aviation, ports,

shipping, rail and intermodal / logistic

service.

Since 2006: total of 12 PPP

transactions with over EUR 1.2 billion in

finance

EBRD infrastructure investments 2015: over EUR 1.7 billion in 70 operations.

Supported privatisation, restructuring and better infrastructure service delivery.

Promoted policy dialogue with regards to investment climate business environment and policies.

EBRD as catalyst to access additional equity, debt and trade finance.

Creating the Environment for Private Sector Participation

13

EBRD VALUE ADDED FOR

PRIVATE SECTOR PARTICIPATION

Broad product range to engage with the

public sector with the aim to create

commercial principles for future private

sector participation.

Regulatory and legal reforms to support

the private sector and a clear

understanding and allocation of risks

between the public and private sectors.

Commercialisation of public entities:

Cost recovery tariffs / user fees

Improved cash flow and cost monitoring

Outsourcing of (non-) core activities

Public service/ management contracts

Key technical cooperation:

Financial/ operational improvement

programmes (FOPIPs)

Assistance with PPP tendering

Key tool: IPPF

1. INTRODUCTION TO EBRD

2. EBRD’S INFRASTRUCTURE BUSINESS GROUP (IBG)

3. SEMED, TURKEY AND KAZAKHSTAN – OPPORTUNITIES AND CHALLENGES

4. CASE STUDIES

5. CONTACTS

14

Contents

EBRD Snapshot in SEMED

• Permanent offices were opened in Tunis and Amman in 2013, in Egypt in 2014 and in

Morocco in 2015.

• To date, over 90 projects have been signed for a total value of EUR 3.5 billion.

• Local currency financings are available in the four countries.

15

49% Egypt

27% Morocco

16% Jordan

8% Tunisia

~1%

0% 0% 0% 0%

Egypt (49%) - EUR 1.7 billion (33 projects)

Morocco (27%) - EUR 0.9 billion (26 projects)

Jordan (16%) - EUR 0.6 billion (22 projects)

Tunisia (8%) - EUR 0.3 billion (20 projects)

SHARE OF EBRD’S PORTFOLIO IN SEMED BY REGION

Note: as at 31 March 2016

24% FI

25% Corporate 21%

Infrastructure

30% Energy

SHARE OF EBRD’S PORTFOLIO IN SEMED BY SECTOR

Note: as at 31 March 2016

• Continued strong centralization of the decision-making

processes

• Limited financial resources of the government and

broader economy

• High standards of basic utilities since the end of the

Revolution

• Heavily subsidized and non-

market oriented tariff systems

• Environmental challenges

• S&P credit rating - Morocco

(BBB-), Tunisia (BB-)

Tunisia and Morocco: Reforms have initiated but

challenges persist

Morocco and

Tunisia

Opportunities Challenges

EBRD Added Value

• Decentralization / reforms initiated but still in early

phase

• Investments needed urgently (due to demography and

urbanization)

• New PPP law in Morocco

Private Sector Development (IPPs, PPPs)

Technical assistance, adoption of best practices (i.e. ONEE)

Support for more efficient uses of energy resources (E2C2)

Promoting commercialization by improving regulation and reforming the tariff system (i.e. ONEE Water

project)

Funding of projects in rural areas and securing sustainability of supply

16

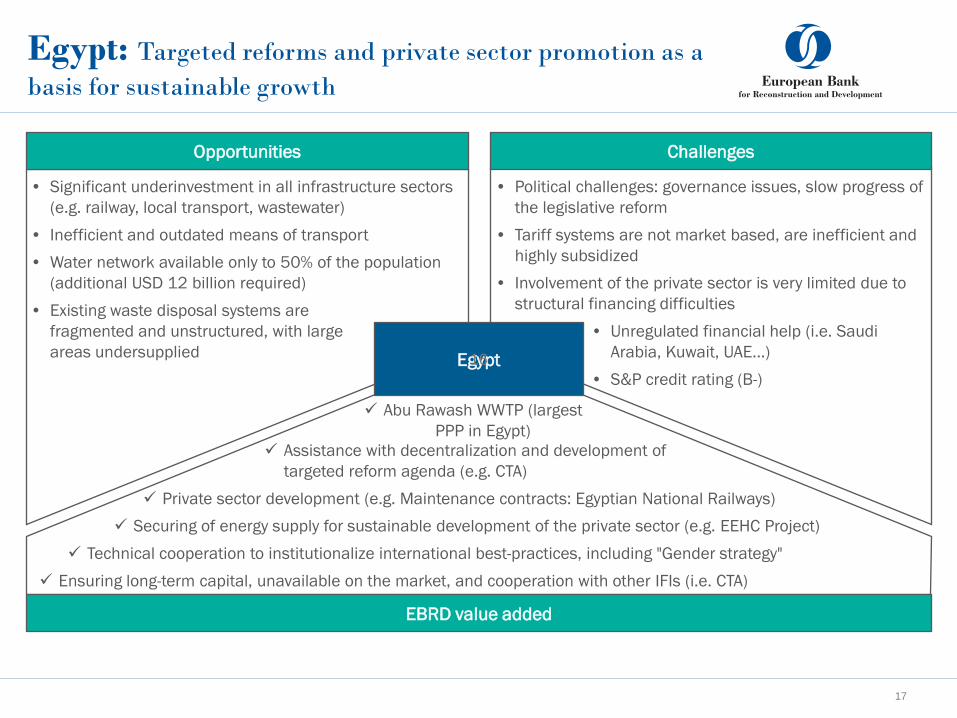

Egypt

Opportunities Challenges

EBRD value added

• Significant underinvestment in all infrastructure sectors

(e.g. railway, local transport, wastewater)

• Inefficient and outdated means of transport

• Water network available only to 50% of the population

(additional USD 12 billion required)

• Existing waste disposal systems are

fragmented and unstructured, with large

areas undersupplied

Egypt: Targeted reforms and private sector promotion as a

basis for sustainable growth

• Political challenges: governance issues, slow progress of

the legislative reform

• Tariff systems are not market based, are inefficient and

highly subsidized

• Involvement of the private sector is very limited due to

structural financing difficulties

• Unregulated financial help (i.e. Saudi

Arabia, Kuwait, UAE…)

• S&P credit rating (B-)

Assistance with decentralization and development of

targeted reform agenda (e.g. CTA)

Private sector development (e.g. Maintenance contracts: Egyptian National Railways)

Securing of energy supply for sustainable development of the private sector (e.g. EEHC Project)

Technical cooperation to institutionalize international best-practices, including "Gender strategy"

Ensuring long-term capital, unavailable on the market, and cooperation with other IFIs (i.e. CTA)

Abu Rawash WWTP (largest

PPP in Egypt)

16

17

EBRD in Turkey (1) Key EBRD figures

18

The EBRD has been investing in Turkey since 2009 with EUR 7.2 billion investments and

over 180 projects signed

Today, Turkey is the biggest country of EBRD operations

In the resident offices in Istanbul, Ankara and Gaziantep, EBRD employs 50 professionals

In 2015, EBRD invested EUR 1.9 billion for over 40 projects in Turkey

EBRD Snapshot in Turkey

EBRD INVESTMENT IN TURKEY

SHARE OF EBRD’S PORTFOLIO IN TURKEY BY SECTOR

Note: as of 31 March 2016

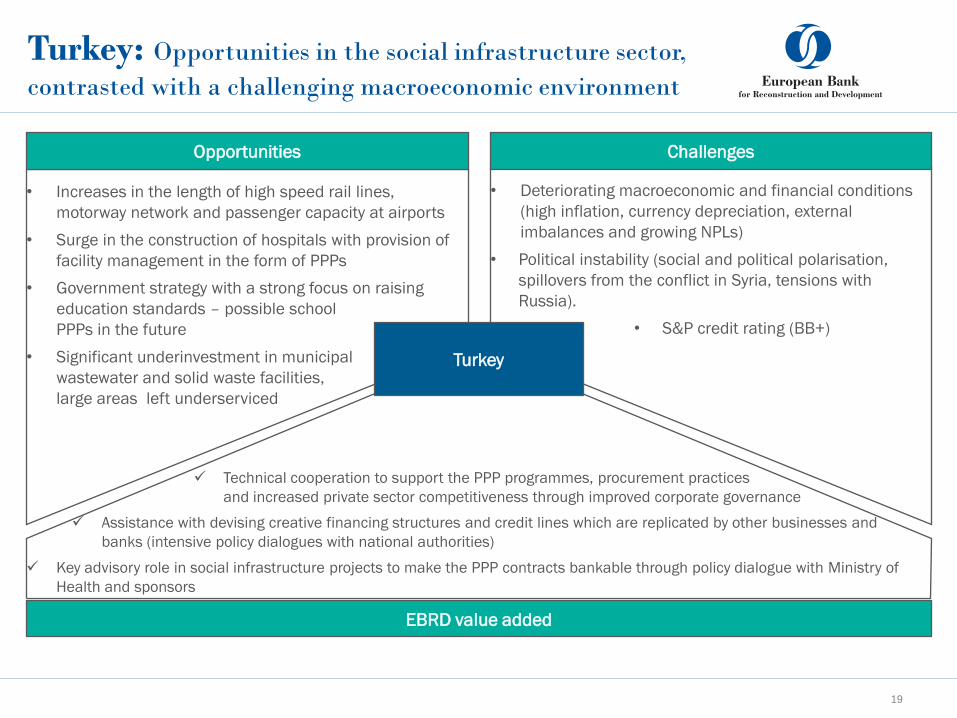

• Increases in the length of high speed rail lines,

motorway network and passenger capacity at airports

• Surge in the construction of hospitals with provision of

facility management in the form of PPPs

• Government strategy with a strong focus on raising

education standards – possible school

PPPs in the future

• Significant underinvestment in municipal

wastewater and solid waste facilities,

large areas left underserviced

Technical cooperation to support the PPP programmes, procurement practices

and increased private sector competitiveness through improved corporate governance

Assistance with devising creative financing structures and credit lines which are replicated by other businesses and

banks (intensive policy dialogues with national authorities)

Key advisory role in social infrastructure projects to make the PPP contracts bankable through policy dialogue with Ministry of

Health and sponsors

• Deteriorating macroeconomic and financial conditions

(high inflation, currency depreciation, external

imbalances and growing NPLs)

• Political instability (social and political polarisation,

spillovers from the conflict in Syria, tensions with

Russia).

• S&P credit rating (BB+)

Turkey

Opportunities Challenges

EBRD value added

Turkey: Opportunities in the social infrastructure sector,

contrasted with a challenging macroeconomic environment

19

EBRD in Turkey (1) Key EBRD figures

20

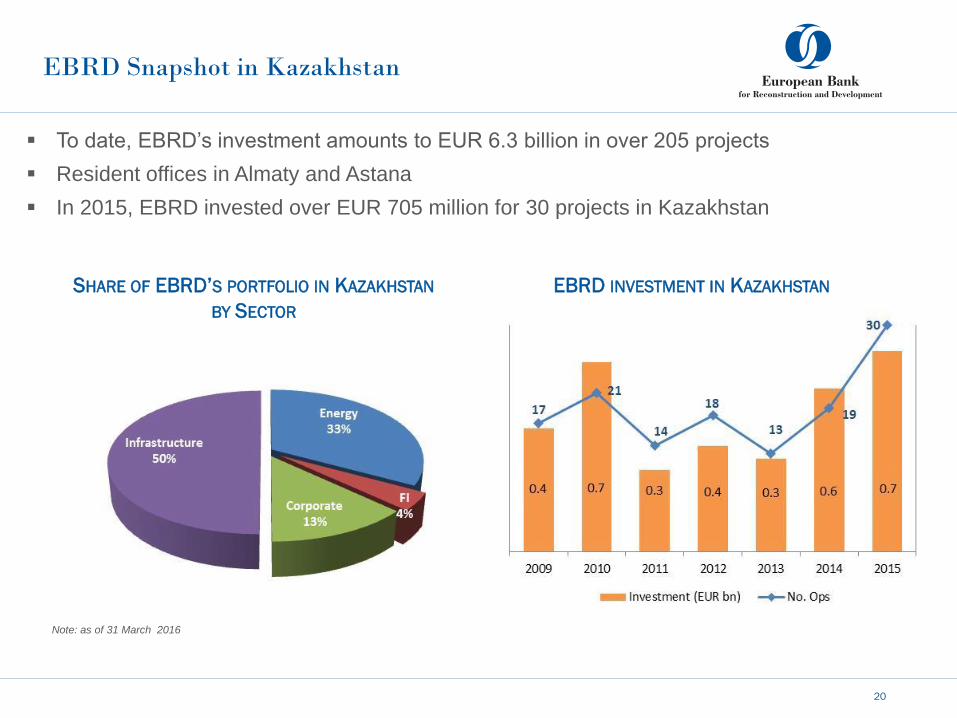

To date, EBRD’s investment amounts to EUR 6.3 billion in over 205 projects

Resident offices in Almaty and Astana

In 2015, EBRD invested over EUR 705 million for 30 projects in Kazakhstan

EBRD Snapshot in Kazakhstan

EBRD INVESTMENT IN KAZAKHSTAN

SHARE OF EBRD’S PORTFOLIO IN KAZAKHSTAN

BY SECTOR

Note: as of 31 March 2016

Amended legislation on PPPs was

developed with the participation of EBRD and WB

Advisory on the preparation of the PPP structure, following international best

practice (e.g. BAKAD ring road project) and technical cooperation to support selection

of qualified advisors

Assisting the authorities in balancing the roles of the state and the market by supporting growth of private sector

enterprises (commercialising of public enterprises and appropriate risk sharing the private and public sectors)

• Growing population and raising standard of living

• Improved investment climate due to a set of systematic

reforms taken by the government

• Infrastructure development as a cornerstone of the

government’s new economic policy (modernisation of

utilities and social infrastructure)

• New PPP law adopted in 2015, aimed

at expanding the breath of PPPs

• Privatisation programme of state

infrastructure assets

(airports and ports)

• Uncertain macroeconomic prospects (low oil prices,

depreciating currency, deteriorating external

environment, budget deficit…), S&P credit rating: BBB

• Poor institutional environment and slow diversification

of the economy (reliance on oil)

• Slow progress of the privatisation programme

• S&P credit rating (BBB)

Kazakhstan

Opportunities Challenges

EBRD value added

Kazakhstan: Growing market with a strong state support

for public-private partnerships

21

22

Contents

1. INTRODUCTION TO EBRD

2. EBRD’S INFRASTRUCTURE BUSINESS GROUP (IBG)

3. SEMED, TURKEY AND KAZAKHSTAN – OPPORTUNITIES AND CHALLENGES

4. CASE STUDIES

5. CONTACTS

Project

Summary

Cross regional: Aqualia Investment Venture

Client

Aqualia New Europe (“ANE”) is an investment vehicle created in 2009, in which EBRD has 49% and FCC Aqualia has the remaining 51%.

The vehicle was created to promote investments in the water and wastewater sector in EBRD’s countries of operations.

EBRD Finance

An equity investment of up to EUR 30 million

Aqualia New Europe’s investment:

In February 2015, ANE completed its first investment through the acquisition of Aqualia’s 45 per cent stake in the New Cairo WWTP in Egypt. The New Cairo WWTP was a PPP awarded in 2008 to Orasqualia, a 50/50 joint venture between Aqualia and OCI. The contract is a 20 year concession to build, own and operate a 250,000 m3/day WWTP.

Abu Rawash WWTP PPP

In August 2015, ANE was awarded the contract for the Abu Rawash WWTP PPP. The PPP contract is the largest awarded since the start of the PPP programme in Egypt in 2006. The project is a 25 year to build, own and operate a 1.6 million m3/day WWTP. Total project costs are EUR 500 million.

6 May, 2016 23

2009 Signed in

Project

Summary

6 May, 2016 24

Client

ADN PPP Saglik Yatirim, a special purpose vehicle

Objective

Construction of an integrated hospital campus in Adana (population of 1.66 million), under an infrastructure facilities management PPP, including sustainable energy investments

EBRD finance:

• A/B loan of up to EUR 225 million (EBRD loan EUR 125 million and a ‘B loan’ tranche of up to 100 million syndicated)

• Co-financed by the International Finance Corporation (IFC), bilateral agencies (DEG/Proparco) and commercial bank

EBRD value added/impact:

• Demonstration effect for commercial financing for privately financed, procured and operated hospital infrastructure;

• Implementation of value for money assessment and strengthening of the monitoring function for hospital facilities management PPP projects

Turkey: Adana Hospital PPP Project

Signed in

2015

Project

Summary

6 May, 2016 25

Turkey: EBRD as an anchor investor in a

Turkish corporate bond

Signed in

2016

Client:

Rönesans Holding A.S., a joint stock conglomerate with activities in construction, real estate and energy

EBRD financing:

An anchor investor in Rönesans’ TRY 200 million bond issue in the amount of up to TRY 100 million.

EBRD value added/impact:

EBRD’s participation principally utilised for the equity needs in the Elazig Hospital PPP project.

• Facilitating development of the non-financial corporate bond market by increasing bond maturities;

• Encouraging companies to raise financing from the bond markets;

• Promoting a level of transparency sufficient to attract investor participation both internationally or locally.

Project

Summary

Tunisia: Clean-up of Lake Bizerte

Client

Office National de l’Assainissement (ONAS), ONAS, is the national sanitation utility created in 1974 to manage wastewater in Tunisia reporting to the Ministry of Environment and Sustainable Development. It provides sewerage services to 170 municipalities totalling over 6.6 million people.

EBRD Finance

A €20 million direct loan to ONAS and technical assistance, guaranteed by the Republic of Tunisia with a 18 years tenor, inclusive of a 4 years grace period.

Use of proceeds

To support the expansion and rehabilitation of the sewage network of the Bizerte’s region and the rehabilitation of three wastewater treatment plants located near the Lake of Bizerte.

EBRD value added / impact The operation will improve sanitation services to approximately 400,000 inhabitants in the Bizerte Governorate. Improvement in the water quality of the lake will also have a positive impact on the development of tourism and aquaculture.

6 May, 2016 26

2015 Signed in

Project

Summary

Morocco: Nador West Med

Client

Nador West Med is a Moroccan public company under private law, created and charged by the government for implementation, development, planning, promotion and management of the industrial port complex.

EBRD Finance

EBRD financing EUR 200 million. Total cost of the project EUR 943 million.

Use of proceeds

Financing the construction of basic port infrastructure for a greenfield port in Nador, Morocco.

EBRD added value / impact

• Expanding competitive market interactions by attracting FDI investors with subsequent market linkages to creating a local industry.

• Promoting private ownership by awarding all commercial port operations to third parties under concession contracts, including container handling and operation of a hydrocarbon terminal.

• Setting standards for corporate governance and business conduct for infrastructure projects in Morocco through implementation of environmental and climate-related measures.

6 May, 2016 27

2015 Signed in

Project

Summary

6 May, 2016 28

Egypt: Cairo Metro

Client

the Arab Republic of Egypt. The beneficiary is a state owned National Authority for Tunnels (NAT).

EBRD Finance

A sovereign loan of up to EUR 175 million to the Government of Egypt. The loan will consist of a committed tranche (EUR 100 million) and an uncommitted tranche (EUR 75 million, utilised only in the event the EIB financing does not come through).

Use of proceeds:

Procurement of new train sets for Cairo Metro Line II, improvement of metro’s services and lower carbon emissions.

EBRD value added/impact

The project will improve and reform public transport services in Cairo (greater commercialisation of services, enhanced private sector participation, improved regulation and opportunities for on the job training and use of carbon monetisation mechanisms).

Signed in

2015

Project

Summary

Hungary: Iberdrola Magyar Wind

6 May, 2016 29

Client Iberdrola Renovables Magyarország (“IBR Magyar”) is a fully-owned Hungarian subsidiary of Iberdrola Renovables, a world leading developer in the renewable energy industry.

EBRD Finance 25% equity investment in IBR Magyar of the HUF equivalent to up to EUR 50 million, by subscribing for shares following a capital increase.

Use of Proceeds Proceeds of the investment will fund the development, construction, and operation of the Company’s current portfolio of wind power projects in Hungary.

EBRD value added By financing one of the most visible wind farm portfolios in Hungary, EBRD’s investment will provide comfort to project developers and other private investors and will demonstrate confidence in Hungary’s renewable energy framework.

2010 Signed in

Project

Summary

Cross regional: Gestamp

Client Gestamp, a global leader in the design and manufacture of automotive metal components and a key supplier to the world’s leading automotive producers.

EBRD Finance A loan facility consisting of a EUR 100 million.

Syndicated amortized A/B loan and a EUR 50 million loan with bullet repayment

Use of Proceeds to partially finance the expansion of Gestamp Automocion in the EBRD Countries of Operations, namely in Russia, Turkey, Hungary and Poland.

EBRD value added The loan support implementation of Gestamp’s strategy of increasing its production capacities in the countries where its customer OEMs are moving their car assembly facilities. As a supplier of metal components, further expansion of Gestamp will create a critical mass of demand for the locally produced automotive steel that itself shall trigger the investment into the high quality automotive steels by major local steel manufacturers.

Signed in

2013

30

Project

Summary

Poland: Golice Wind Farm

6 May, 2016 31

Client Golice Wind Farm - fully owned by Acciona Energy Poland, itself a subsidiary of Acciona Energía

EBRD Finance Senior loan of PLN 97.2 million (EUR 22 million equivalent) and representing up to 50 per cent of the total debt financing, and up to 35 per cent of the total Project cost.

Use of Proceeds Develop the 38 MW Golice wind farm in Poland

EBRD value added Setting standards for business conduct, through communicating the viability of renewable energy financing in Poland to the market; expansion of renewable energy sector in Poland, through supporting Acciona’s participation in this and other renewable energy projects in the country

2011 Signed in

32

Contents

1. INTRODUCTION TO EBRD

2. EBRD’S INFRASTRUCTURE BUSINESS GROUP (IBG)

3. SEMED, TURKEY AND KAZAKHSTAN – OPPORTUNITIES AND CHALLENGES

4. CASE STUDIES

5. CONTACTS

Contact

33

Thomas Maier

Managing Director, Infrastructure

Tel: +44 20 7338 7924

Email: [email protected]

EBRD

One Exchange Square

London, EC2A 2JN

UK

www.ebrd.com