Embed Size (px)

Citation preview

1

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Introduction to Emissions Introduction to Emissions TradingTrading

Paul VickersPaul VickersManaging DirectorManaging Director

NatsourceNatsource

2

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Background…Government and Background…Government and Business leaders in Canada have done Business leaders in Canada have done

muchmuch GERT and PERT…establishing standards for project based

reductions VCR…establishing reporting process …could evolve into

registry

GEMCo…driving supply and innovative contract structures

Leading companies have built portfolios of emission reduction credits

Buyers are building legal, due diligence and other skills Leading suppliers are also building skills and financing needed

3

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Why emissions trading? The driver is Why emissions trading? The driver is regulation !regulation !

GHG Canada:– Kyoto: non zero obligation, compliance not strategic, duty of care obligation,

‘covenant ‘ negotiations beginning– Covenants will differentiate amongst sectors and subsectors – BAU efficiency gains will be built into targets - will likely be larger than 15% reduction

GHG Provincial : new power faces GHG permit requirements in Quebec, Alberta, BC; Bill 32 discussions beginning with other sectors

GHG USA: state by state regulations on new power and existing power. Permit negotiations at local siting Boards. Federal regulations on reporting. Federal proposals for cap-and-trade. “Mandatory-Voluntary” agreements in Oil, Chemicals and Power sectors

RPS requirements in USA; likely in Canada

USA Clear skies: new reductions in So2 and Nox etc…applies to most emitting sources across the USA

Importers of commodities in Europe and Japan beginning to seek concessions and / or ‘bundled’ product

4

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Cement Power Chemicals Pulp & Paper

Steel

Co2 Intensity

(t / unit of product)

0.8 1.0 0.7 0.3 1.8

BAT Intensity 0.53 0.78 0.56 0.2 1.2

Production

(t or other per year)

1,000,000 1,000,000 1,000,000 1,000,000 1,000,000

Target Reduction (%)

15 15 15 15 15

Emissions (t) 800,000 1,000,000 700,000 300,000 1,800,000

Allocation (t) 450,000 663,000 476,000 170,000 1,020,000

Shortfall (t) 350,000 337,000 224,000 130,000 780,000

An Example of possible regulatory Obligations

5

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

There are two distinct markets emerging There are two distinct markets emerging world wide…what will Canada do ?world wide…what will Canada do ?

Emission allowances and / or credits

Renewable energy and demand side management credits

6

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

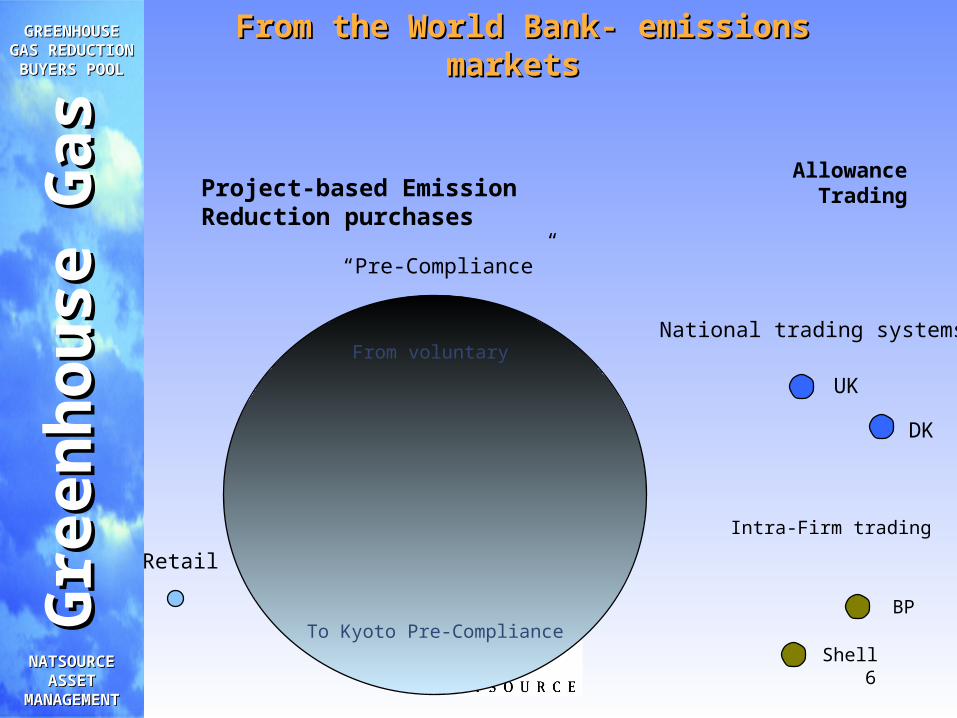

From the World Bank- emissions markets From the World Bank- emissions markets

Project-based Emission Reduction purchases

Allowance Trading

National trading systems

Intra-Firm trading

Retail

UK

DK

Shell

BP

“Pre-Compliance”

From voluntary

To Kyoto Pre-Compliance

7

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Data show emissions market is growingData show emissions market is growing( From the World Bank)( From the World Bank)

The past year has been the most active GHG market to date

– volume traded in first half of 2002 already exceeds overall 2001 volume(24 MtCo2e transacted, 103 deals).

Based on closed and pending deals, total 2002 volume could be in the range of 60-70 MtCo2e.

– Conservatively, this could represent a manifold increase in volume over the previous year’s volume of 12 MtCo2e.

This is significant compared to 157 MtCO2e transacted overall since 1996 (190 MtCO2e if post-2012 vintages are counted).

8

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Canada

USA

Netherlands

Other WEU

Japan PCF

Australia

Canada

USA

Other WEU

Japan

Australia

PCF

Netherlands

From the World Bank: Evolution of buyers’ shares of marketFrom the World Bank: Evolution of buyers’ shares of market

(in % of total volume purchased through projects(in % of total volume purchased through projects))

1996-2000 2001-2002

Other Europe

Other Europe

9

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

GHG instrument 2002 Prices ($ CAN/mt CO2e)

Project-based reductions that could be converted to Kyoto compliance instruments

Developing country VERs, vintage years 2000-12 (candidate CERs) $4.00 - $5.00 (current bid-ask spread; one transaction reported in 2002 for $3.82)

Developed country project-based VERs, vintage years 2008-12 (candidate ERUs)

No transactions reported, see also Dutch ERUPT anticipated prices.

Project-based reductions that could be converted to domestic compliance instruments

Developed country emission reductions, vintage years 2002-12 $2.88 - $3.88

Developed country emission reductions, vintage years before 2002 $0.73 - $3.88

Other Kyoto compliance instruments

AAUs of vintage year 20052007 (for future delivery) 2 transactions with prices undisclosed

National and regional compliance instruments

UK allowances $10.50 - $30

Danish allowances $2.73 - $4.33

Other ghg instruments

Dutch ERUPT candidate ERUs and CER’s $6.91 (anticipated)

Renewable Energy Credits (REC’s) $1.50-$ 7.00 / Mw-Hr

Current GHG / REC market prices

10

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Emission / REC Sales IssuesEmission / REC Sales Issues

RISKS

Supplier Default Risk – Project Delivery

Supplier Default Risk – Credit Risk

Price Risk

Validity Risk –

Quality of Reductions

Validity Risk – Regulatory Certainty

Risk of Fraud

11

Gre

enh

ou

se G

asG

reen

ho

use

Gas

GREENHOUSE GREENHOUSE GAS GAS

REDUCTION REDUCTION BUYERS POOLBUYERS POOL

NATSOURCE NATSOURCE ASSET ASSET

MANAGEMENTMANAGEMENT

Further InformationFurther Information

www.natsource.comwww.natsource.com

www.gcsi.cawww.gcsi.ca

Ottawa Doug Russell150 Isabella Street, Suite 305, Ottawa, Ontario, Canada K1S 1V7 1 613 232 7979 1 613 232 3993 faxEmail;:[email protected]

Calgary Paul Vickers615 3rd Avenue, S. W.Suite 300Calgary, Alberta,Canada T2P 0G61 403 215 55871 403 215 5510 faxEmail:[email protected]

Washington D.C. Rich Rosenzweig1120 19th Street, NWSuite 730Washington D.C.,U.S.A. 200361 202 496 14231 202 496 1416 faxEmail:[email protected]

With offices in Vancouver, Edmonton, Toronto , Tokyo and London