Embed Size (px)

Citation preview

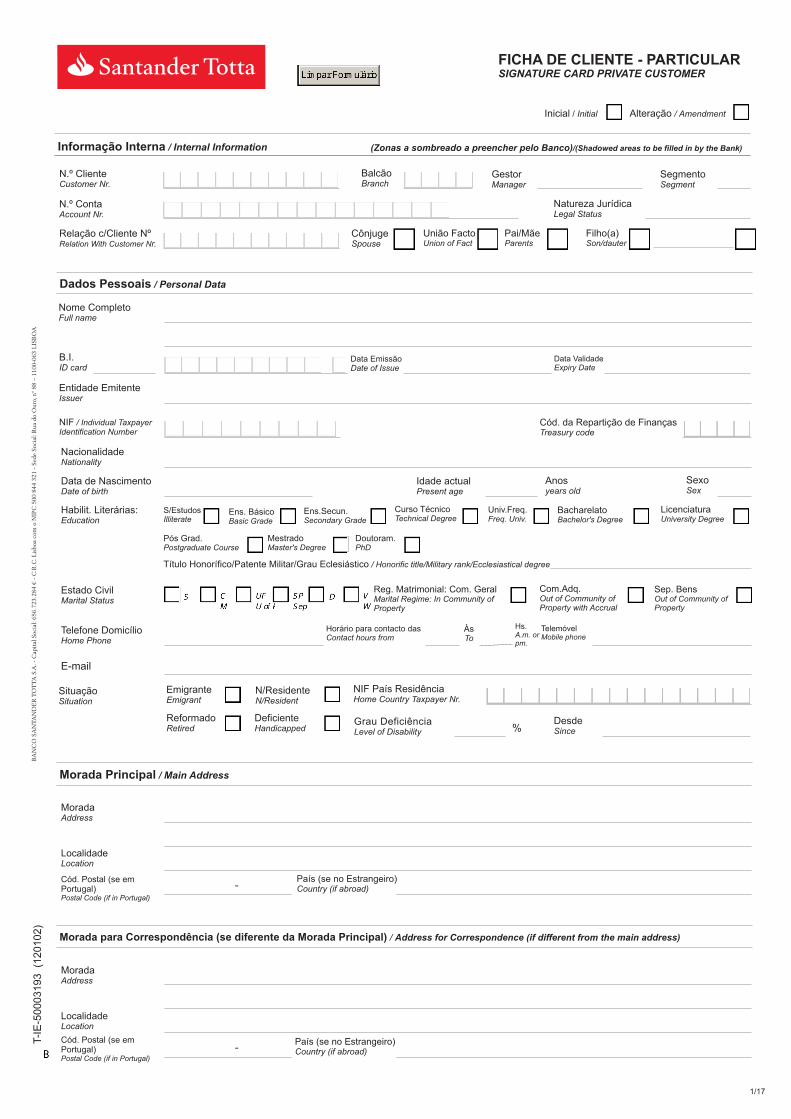

FICHA DE CLIENTE - PARTICULARSIGNATURE CARD PRIVATE CUSTOMER

BS

T-I

E-5

0003193 (1

20102)

Inicial / Initial Alteração / Amendment

GestorManager

Informação Interna / Internal Information (Zonas a sombreado a preencher pelo Banco)/(Shadowed areas to be filled in by the Bank)

BalcãoBranch

N.º ClienteCustomer Nr.

Natureza JurídicaLegal Status

SegmentoSegment

N.º ContaAccount Nr.

Morada Principal / Main Address

MoradaAddress

LocalidadeLocation

-

Morada para Correspondência (se diferente da Morada Principal) Address for Correspondence (if different from the main address)/

Cód. Postal (se emPortugal)Postal Code (if in Portugal)

-País (se no Estrangeiro)Country (if abroad)

Nome CompletoFull name

Dados Pessoais / Personal Data

Sep. BensOut of Community ofProperty

Com.Adq.Out of Community ofProperty with Accrual

Reg. Matrimonial: Com. GeralMarital Regime: In Community ofProperty

Habilit. Literárias:Education

S/EstudosIlliterate

Ens. BásicoBasic Grade

Ens.Secun.Secondary Grade

Pós Grad.Postgraduate Course

LicenciaturaUniversity Degree

BacharelatoBachelor's Degree

Univ.Freq.Freq. Univ.

Curso TécnicoTechnical Degree

Título Honorífico/Patente Militar/Grau Eclesiástico / Honorific title/Military rank/Ecclesiastical degree

B.I.ID card

Data EmissãoDate of Issue

Data ValidadeExpiry Date

NIF / Individual TaxpayerIdentification Number

Cód. da Repartição de FinançasTreasury code

Data de NascimentoDate of birth

NacionalidadeNationality

SexoSex

Idade actualPresent age

Anosyears old

MestradoMaster's Degree

Doutoram.PhD

Telefone DomicílioHome Phone

Hs.A.m. orpm.

ÀsTo

Horário para contacto dasContact hours from

TelemóvelMobile phone

Estado CivilMarital Status

Entidade EmitenteIssuer

Grau DeficiênciaLevel of Disability %

DesdeSince

NIF País ResidênciaHome Country Taxpayer Nr.

SituaçãoSituation

ReformadoRetired

EmigranteEmigrant

N/ResidenteN/Resident

DeficienteHandicapped

BA

NC

O S

AN

TA

ND

ER

TO

TT

A S

.A. -

Cap

ital

Soci

al: 6

56.7

23.2

84

€-

C.R

.C. L

isboa

com

o N

IPC

500 8

44 3

21 -

Sed

e Soci

al: R

ua

do O

uro

, nº

88

–1100-0

63 L

ISB

OA

Cód. Postal (se emPortugal)Postal Code (if in Portugal)

País (se no Estrangeiro)Country (if abroad)

MoradaAddress

LocalidadeLocation

Relação c/Cliente NºRelation With Customer Nr.

CônjugeSpouse

União FactoUnion of Fact

Pai/MãeParents

Filho(a)Son/dauter

1/17

InvestimentoInvestment

Dados Profissionais / Profession Data

Situação ProfissionalProfession Status

Profissional LiberalLearned Profession

Empresário em Nome IndividualSelf-employed

Entidade PatronalEmployer

Telefone (Empresa)Phone (Company)

Hs. / a.m.or p.m

Àsto

Horário para contactodasContact hours from

Fax

ProfissãoProfession

DenominaçãoDesignation

Morada SedeHead Office Address

ObjectoCorporate Purpose

Empresário em Nome Individual / Self-employed

CAECEA

Cargo PúblicoPublic post

Qual?Whichpost?

ExerceIs he inoffice?

ExerceuWas he inoffice?

Assinatura do Cliente (tal como consta no Documento de Identificação)Customer Signature (as in the Identity Card)

Conferido por: (Assinatura / Nº Empregado)Checked by: (Signature/ Employee Nr.)

DataDate

DataDate

Trabalhador por conta de outremEmployed by a third party

- País (se no Estrangeiro)Country (if Abroad)

LocalidadeLocation

Cód. Postal (se emPortugal)Postal Code (if in Portugal)

Declaro que tomei conhecimento, me foi explicado, aceitei e me foi entregue um exemplar, assinado neste acto pelo Banco, das “Condições Gerais –Cliente – Particular”

I hereby declare that I am aware, I was clarified, I accepted and it was delivered to me a set of documents, signed in this act by the Bank, of the - General Conditions - Customer - PrivateCustomer”, that include the contractual provisions which govern the performance of financial brokering services.

, que incluem as disposições contratuais que disciplinam a prestação dos serviços de intermediação financeira.

Declaração / Statement

2/17

Finalidade e Natureza da Relação de Negócio / Purpose And Nature Of Business Relationship

Familiar / Pessoal / IndividualFamiliar / Personal / Individual

Empresarial / ProfissionalCompany I Business

I. PARTE GERALObjectoI.1.

ÂmbitoI.2.

Dados Pessoais - Consulta e Tratamento Informático de Dados Pessoais eComunicação de alterações de elementos de identificação do ClienteI.3.

I.4.

I.5.

I.6.

Correspondência e ComunicaçõesI.7.

I.8.

I.9.

I.10.

I.11.

I.12.

As presentes Condições Gerais regulam, em tudo o que não for contrariado porcondições particulares acordadas entre as partes, a relação estabelecida entre o BANCOSANTANDER TOTTA, S.A. - doravante simplesmente designado por Banco - e o Cliente -como tal identificado na Ficha de Cliente que assinou - decorrente desta abertura de contade depósito à ordem nos termos abaixo indicados.

Sem prejuízo das Condições Gerais e Particulares, que tenham sido acordadaspontual e especificamente com cada um, as presentes Cláusulas Gerais são aplicáveis atodos os Clientes PARTICULARES e abrangem todos os produtos e serviços nelasreferidos.As condições particulares revestirão a forma escrita ou qualquer outra que, respeitados osrespectivos requisitos, lhe seja legalmente equiparada, nomeadamente a electrónica,sendo bastante a troca de correspondência, salvo disposição imperativa em contrário.

O Cliente autoriza expressamente o Banco a proceder, nos limites da lei, aoarmazenamento, tratamento informático ou não, comunicação e interconexão dos seusdados pessoais, quer os que lhe haja voluntariamente fornecido, quer outros que o Bancotenha legalmente obtido, destinando-se tais dados exclusivamente ao estabelecimento emanutenção das relações comerciais entre o Cliente e o Banco ou sociedades que com oBanco estejam, directa ou indirectamente, em relação de domínio ou de Grupo, podendo osreferidos dados ser facultados ao conhecimento e utilização dessas sociedades para osfins acima indicados. O Cliente igualmente autoriza o Banco a, em caso de mora ouincumprimento de qualquer das obrigações que lhe incumba, comunicar tais factos aempresas que estejam autorizadas pela Comissão Nacional da Protecção de Dados aproceder ao tratamento de dados pessoais para centralização e troca de informações sobreriscos de crédito, nos limites da correspondente autorização.

Com a ressalva que resulta do número anterior, o Banco manterá sigilo sobre os dadospessoais do Cliente e sobre as relações com ele mantidas, nos termos da Lei vigente.Igualmente nos termos e nos limites da Lei, o Cliente tem, a todo o tempo, acesso àinformação e actualização dos dados armazenados e tratados informaticamente peloBanco, devendo para tanto dirigir-se ao seu Balcão, ou ligar para a Superlinha, e solicitar asinformações referidas.

O Cliente igualmente autoriza o Banco a, sempre que venha a solicitar-lhe crédito porqualquer forma e dentro dos limites da lei, consultar toda e qualquer informação na Base dedados do Banco de Portugal que diga respeito ao Cliente, quer se trate de confirmarinformação por ele voluntariamente oferecida, quer se trate de obter outro tipo deinformação relevante para o estabelecimento e manutenção das relações comerciais entreas partes ou sociedades que com o Banco estejam directa ou indirectamente em relação dedomínio ou de Grupo.

O Cliente fica obrigado a, imediatamente, comunicar ao Banco toda e qualqueralteração aos elementos de identificação que lhe haja fornecido, comprovando-asdocumentalmente nos termos da lei.

Toda a correspondência a dirigir ao Cliente poderá ser-lhe enviada em formato digitalatravés do NetBanco se for utilizador deste meio de comunicação, ou para o endereçoelectrónico indicado na Ficha de Cliente, a não ser que o Cliente não seja utilizador doNetBanco nem tenha fornecido endereço electrónico ou o envio da correspondência emformato em papel tenha sido acordado com o Banco, caso em que será enviada ao Clientepor via postal para o domicilio indicado. O Cliente e o Banco podem, porém, a todo o tempo,acordar a alteração do formato da informação e o domicílio de destino.O Cliente tem disponível para receber as suas comunicações a rede de Balcões do Banco,as linhas telefónicas Superlinha (707 21 24 24 ou +351 217 807 364, se estiver noestrangeiro), Linha NetBanco Empresas (217 807 130) ou os canais comuns como fax, aWeb (www.santandertotta.pt) e o correio. Para efeitos de prestação de serviços deintermediação financeira e de pagamento as comunicações e informações serão feitas porescrito ou através da Internet em língua portuguesa, se outro idioma ou endereço ou canalde comunicação não tiver sido acordado com o Banco.

Quando se trate de Cliente pluripessoal e salvo o que em contrário possa resultarimperativamente da Lei ou das condições específicas do produto ou serviço a que respeite,as comunicações do Banco consideram-se devidamente efectuadas quando feitas aqualquer um dos membros titulares da conta de depósito à ordem, ainda que esta sejaconjunta ou mista.

Sem prejuízo do que em contrário possa resultar das condições específicas dosprodutos ou serviços a que respeite, a correspondência a dirigir pelo Cliente ao Banco deveser endereçada preferencialmente para o Balcão onde está sedeada a conta de depósitos àordem ou, alternativamente, para a sede social.

Quando se trate de Cliente pluripessoal, a correspondência a dirigir ao Banco deve sersubscrita por quem tiver poderes de movimentação da conta de depósitos à ordem, salvo aque seja de mero expediente ou respeite exclusivamente a algum dos titulares semquaisquer reflexos sobre a situação jurídica dos demais a qual pode ser exclusivamentesubscrita pelo interessado.

O Banco remeterá periodicamente ao Cliente extractos dos movimentos efectuadosnas suas contas. Além disso, sempre que a lei o imponha ou quando o entenderconveniente, o Banco remeterá avisos relativos à realização de operações efectuadas. Anão ser que a lei imponha outra solução, a periodicidade dos extractos é definida peloBanco podendo ser alterada a todo o tempo.

Os extractos e avisos a que se refere a cláusula anterior poderá ser enviados emformato digital ao Cliente utilizador do NetBanco onde serão disponibilizados, ou para oendereço electrónico indicado na Ficha de Cliente ou fornecido e registado no Banco, se oenvio em formato em papel não tiver sido acordado com o Banco ou o Cliente não forutilizador do Net Banco ou não tenha fornecido ao Banco o endereço electrónico, caso emque lhe serão enviados por via postal para o domicilio indicado, implicando ou não opagamento de portes e comissões conforme estiver determinado no preçário do Bancoaplicável à generalidade dos Clientes para os mesmos actos.

CONDIÇÕES GERAIS - CLIENTE - PARTICULAR / GENERAL CONDITIONS - CUSTOMER - PRIVATE

Clie

nte

N.º ContaAccount nr.

Esta abertura de conta está condicionada à verificação da suficiência da documentação edeclarações apresentadas.No caso de se concluir por alguma irregularidade ou insuficiência, não sanada como forsolicitado, o Banco, sem dependência de outro aviso, cancelará a conta e os meios depagamento disponibilizados que não poderão então ser utilizados. A verificação será feitapelo Banco no prazo de quarenta e cinco dias a contar da data da subscrição destasCondições Gerais.The opening of this account is subject to checking the sufficiency of documentation and statementssubmitted.If any irregularity or insufficiency is found, not resolved as required, the Bank, not depending upon anothernotice, may cancel the account and the means of payment offered that may not be then used. Conferenceshall be made by the Bank within forty-five days from the date of subscription of these General Conditions.

I.ObjectI.1.

ScopeI.2.

Personal Data Query and Automatic Treatment of Personal Data and Communicationof changes in the Customer's elements of identificationI.3.

I.4.

I.5.

I.6.

Correspondence and CommunicationsI.7.

I.8.

I.9.

I.10.

I.11

I.12

GENERAL

In every matter not covered by the particular conditions agreed between the parties,these General Conditions govern the relationship established between BANCOSANTANDER TOTTA, S.A. hereinafter the “Bank” and the Customer identified as such inthe Signature Card arising from this current account opening under the terms set outhereunder.

Without prejudice to such General and Particular conditions as occasionally andspecifically agreed with each of them, these General Conditions are applicable to allCustomers PRIVATE CUSTOMER and cover all products and serves referred to herein.The particular conditions shall be in writing or any other form that, satisfying the respectiverequirements, shall be legally equivalent, namely the electronic means, being sufficient theexchange of correspondence, except for imperative disposition to the contrary.

Within the limits of the law, the Customer expressly authorises the Bank to store, whetherin computers or otherwise, communicate and inter-connect his/her personal data, boththose which were provided voluntarily and such other as the Bank may have lawfullyobtained, such data to be exclusively used to establish and maintain commercial relationsbetween the Customer and the Bank or companies with which the Bank is directly orindirectly in a controlling or Group position, and the said data may be provided for theknowledge of or use by such companies for the above mentioned purposes. The Customeralso authorises the Bank, in the event of default or breach of any of its obligations, tocommunicate such facts to companies authorised by the National Data ProtectionCommission to process personal data to centralise and exchange information on creditrisks, within the limits of the corresponding authorisation.

With the exception arising from the aforementioned clause, the Bank shall maintainconfidential the Customer's personal data and its relations with the Customer, under theterms of the law. Likewise, under the terms and within the limits of the law, the Customershall have from time to time access to the data information and its updating which is storedand processed automatically by the Bank and, for that purpose, the Customer shouldcontact Superlinha and request the said information. You can access Superline 24 hours aday, 365 days a year. It also provides Personalised Attendance every day, from 8 in themorning to 11 at night.

The Customer likewise authorises the Bank, whenever it requires credit in any way andwithin the limits of the law, to consult any information concerning the Customer at the Bank ofPortugal database, either to confirm information voluntarily provided by it or to obtainanother type of relevant information to set up and maintain commercial relations betweenthe parties or companies that, with the Bank, are directly or indirectly in a controlling orGroup position.

The Customer is obliged to immediately notify the Bank of any change occurred in theidentification elements supplied, by presenting documental proof of those changes in theterms of the law.

All correspondence to be addressed to the Client may be sent in digital support throughNetBanco if the former is an user of this communication method, or to the email stated in theClient Form, unless the Client is not a NetBanco user and has not provided an emailaddress, or he has agreed with the Bank the correspondence to be sent in paper, in whichcase it shall be sent to the Client by post to the stated address. However, the Client and theBank may, at any time, agree on changing the support for the provided information and thedestination address.The Client may receive its communications at the Bank's Branches network, telephone linesSuperlinha (707 21 24 24 or +351 217 807 364, if he is abroad), Linha NetBanco Empresas(Netbanco line companies) (217 807 130) or the normal channels such as the fax, the Web(www.santandertotta.pt) and the mail. For the purpose of providing financial intermediationand payment services the communications and information shall be carried out, in writing, orthrough the internet in the Portuguese language, if no other language, address orcommunication channel has been agreed with the Bank.

In the case of a Multi-person Customer and except for any imperative provision of the lawor of the specific conditions of the product or service to which it refers, the Bank'scommunications shall be deemed to have been duly made when made to any of the holdersof the current account, even tough the account might be a joint collective signature or a jointmixed signature account.

Without prejudice to what may arise from the specific conditions of the products orservices to which it refers, all correspondence to be sent by the Customer to the Bank shallbe addressed preferably to the branch where the current account is open or, alternatively, tothe Bank's head office.

In the case of a Multi-person Customer, the correspondence to be addressed to theBank shall be signed by those empowered to operate the current account, except in the caseof ordinary correspondence or that exclusively concerns any of the holders with norepercussion on the legal situation of the others and which may be signed by the interestedparty alone.

The Bank shall periodically send to the Customer statements with the transactions in itsaccounts.Additionally, whenever required by law or when it so deems fit, the Bank shall sendnotices concerning transactions made. Unless otherwise required by law, the frequency ofthe statements is defined by the Bank and may be changed from time to time.

The statements and notices mentioned in the previous clause may be sent in digitalsupport to the Client using NetBanco, or to the email address stated in the Client Form orprovided to and registered in the Bank, if the Bank and the Client have not agreed on sendingthose communications in paper, or the Client does not use NetBanco or has not provided thebank with his email address, in which case the former shall be sent to him by post to thestated address, whether involving or not the payment of postage and commissionsaccording to what is established in the Price List of the Bank applying to most Clients for thesame actions.

BA

NC

O S

AN

TA

ND

ER

TO

TT

A S

.A. -

Cap

ital

Soci

al: 6

56.7

23.2

84

€-

C.R

.C. L

isboa

com

o N

IPC

500 8

44 3

21 -

Sed

e Soci

al: R

ua

do O

uro

, nº

88 1100-0

63 L

ISB

OA

,au

tori

zado p

ara

a p

rest

ação

da

acti

vidad

e de

inte

rmed

iaçã

o f

inan

ceir

a em

29 d

e Ju

lho d

e 1991 e

reg

ista

do s

ob o

nº

130 n

a C

om

issã

o d

e M

erca

do d

eV

alore

s M

obiliá

rios

(ww

w.c

mvm

.pt)

3/17

BS

T-I

E-5

0003193 (1

20102)

I.13.

I.14.

CópiasI.15.

I.16.

I.17.

ReclamaçõesI.18.

I.19.

I.20.

Rendimentos e Remunerações do ClienteI.21.

I.22.

Impostos, Taxas e ContribuiçõesI.23.

EstornosI.24.

Compensação VoluntáriaI.25.

I.26.

I.27.

I.28.

PreçárioI.29.

I.30.

I.31.

I.32.

I.33.

Despesas Judiciais e ExtrajudiciaisI.34.

I.35.

Pagamentos ao BancoI.36.

I.37.

I.38.

O Cliente pode, porém, suportando os custos correspondentes, solicitar ao Banco oenvio de extractos com periodicidade inferior à geralmente praticada, bem como solicitarextractos avulsos.

O Cliente autoriza o Banco a, por qualquer meio, comunicar com o Cliente,nomeadamente por via electrónica, postal, telecópia ou telefone, com a utilização ou não desistemas automáticos com mensagens vocais pré-gravadas, promovendo directa ouindirectamente a comercialização de quaisquer bens ou serviços objecto da sua actividadecomercial e, bem assim, transmitindo factos decorrentes das suas relações negociais ou deiniciativas do Banco conexas com a sua actividade comercial.

O Cliente pode solicitar ao Banco, suportando o custo respectivo, fotocópia dosdocumentos que lhe respeitem e que estejam em poder do Banco.

O Banco procurará corresponder o mais solicitamente que lhe for possível mas nãoestá obrigado ao cumprimento de nenhum prazo para o efeito.

O preço a pagar pelo Cliente é o que for praticado pelo Banco e aplicável àgeneralidade dos Clientes em situações equivalentes.

Salvo quando ocorra justo motivo devidamente demonstrado ou quando a lei imponhaprazos mais longos, toda a reclamação de actos do Banco deve ser apresentada no prazode quinze dias contados do envio do extracto, aviso, ou qualquer outro documento onde aprática do acto em questão esteja evidenciada, sem o que não poderá ser atendida. Areclamação deve, à escolha do Cliente, ser dirigida ao Balcão onde se encontra domiciliadaa conta ou à Direcção de Qualidade.

Quando o acto não seja objecto de informação documental ao Cliente o prazo referidona cláusula anterior conta-se a partir do respectivo conhecimento por ele.

O Banco dispõe de um serviço destinado a receber as reclamações do Cliente noâmbito da prestação dos seus serviços, incluindo os de intermediação financeira, quefunciona em dias úteis no período compreendido entre as 8.30 e as 16.30 na Rua daMesquita, nº 6, Torre B, telefone 808 241 206, com o endereço www.santandertotta.pt. OCliente pode dirigir a sua reclamação ao Banco de Portugal ou à Comissão de Mercado deValores Mobiliários, cujos contactos poderá encontrar nos endereços Internet:www.bportugal.pt e www.cmvm.pt. As reclamações dirigidas ao Banco que possuam todosos elementos necessários à sua análise serão respondidas num prazo máximo que seestima em 10 dias.

Os juros, dividendos, rendimentos e qualquer outro tipo de remuneração que o Clientetenha direito a receber do Banco ser-Ihe-á pago pelo crédito do valor respectivo na suaconta de depósitos à ordem.

O disposto na cláusula anterior não prejudica o recurso a outras formas de pagamento,nomeadamente através da capitalização, quando tal decorra de imperativo legal, dascaracterísticas específicas do produto gerador do rendimento ou remuneração devida, oude condições particulares acordadas com o Cliente.

Todas as quantias devidas pelo Banco ao Cliente ser-Ihe-ão pagas líquidas deimpostos, taxas ou contribuições que o Banco deva reter.

O Banco fica expressamente autorizado a estornar quaisquer movimentosindevidamente efectuados nas contas do Cliente, designadamente em caso de erro, lapsoe em todas as demais circunstâncias em que tal estorno se justifique, sendo o movimentoefectuado com a data-valor do movimento originário.

Quando seja credor do Cliente por dívida vencida, o Banco pode, sem prejuízo dasdemais faculdades que lhe caibam nos termos da Lei ou do título de onde a dívida emerge,reter e utilizar, para o seu reembolso, todos e quaisquer fundos provenientes de saldos,contas ou valores detidos pelo Cliente no Banco, compensando o respectivo montante comdébitos de igual valor, e independentemente da verificação dos requisitos da compensaçãolegal.

Para os efeitos da cláusula anterior pode, designadamente, o Banco proceder àmobilização antecipada de depósitos ou aplicações financeiras a prazo, sem necessidadede outra autorização ou de pré-aviso, fazendo-o na medida do necessário ao reembolso doque lhe seja devido.Sendo as contas utilizadas para a compensação constituídas em moeda diferente das dadívida a compensar, far-se-á a respectiva conversão ao câmbio praticado pelo Banco paraa compra da moeda em que a conta se acha constituída, e até ao montante necessário parasaldar a dívida em questão.

No caso de Cliente pluripessoal, o disposto na cláusula anterior é aplicável, nos limitesda lei, aos saldos, fundos e valores que qualquer dos membros que compõem o Clientepossua no Banco individualmente ou conjuntamente com outrém.

Sendo vários os créditos do Banco, compete-lhe em exclusivo determinar os que ficamextintos por recurso ao mecanismo previsto nas cláusulas anteriores.

O Cliente poderá, a todo o tempo, consultar, em qualquer agência do Banco, o preçárioonde constam as taxas de juro em vigor, indexantes, comissões e preços cobrados peloBanco em contrapartida dos serviços por si efectuados, ou o modo de os determinar.

Salvo quando a lei disponha imperativamente de outro modo, o Banco pode, a todo otempo, alterar qualquer rubrica do preçário.

As alterações a que se refere a cláusula anterior terão efeitos imediatos salvo se oBanco fixar dilação para a sua entrada em vigor, e sem prejuízo do disposto nas cláusulasseguintes.

No caso de serviços continuados, em curso ou a iniciar, o novo preço aplica-seimediatamente após a sua entrada em vigor. No caso de serviços pontuais só se aplica aserviços ainda não acordados à mesma data. As alterações do preçário não se aplicam,porém, a períodos de contagem já decorridos ou em curso nem a serviços já prestados.

Quando proceda a alterações no preçário, o Banco advertirá os Clientes do factoatravés de referência a inserir ou acompanhar o extracto de movimentos de contaimediatamente posterior à decisão.

Quando haja mora ou incumprimento por qualquer das partes de alguma das suasobrigações perante a outra, seja ela resultante do presente contrato ou de qualquer outrotítulo, a parte faltosa é responsável pelos custos judiciais e extrajudiciais em que a outracomprovadamente incorrer para obter a reparação da situação.

Sem prejuízo do disposto no número anterior, as partes poderão acordar, no título deonde emerge a obrigação em falta ou noutro qualquer, o estabelecimento de comissões asuportar pela parte faltosa e destinadas a compensar custos extrajudiciais incorridos pelaoutra no caso de mora ou incumprimento de obrigações pecuniárias de qualquer delas.

Salvo quando o contrário resulte das condições particulares acordadas ou decondições específicas dos produtos ou serviços a que respeitam, os pagamentos devidosao Banco pelo Cliente, seja a que título for, são feitos através do débito dos montantescorrespondentes na conta de depósito à ordem, que o Cliente se obriga a ter suficiente eatempadamente provisionada para o efeito, ficando o Banco irrevogavelmente autorizado aproceder aos débitos em causa sem necessidade de pré-aviso.

Os débitos a que se refere o número anterior não podem ser feitos anteriormente aovencimento das obrigações correspondentes, mas podem sê-lo posteriormente com data-valor do dia em que os pagamentos eram devidos.

Quando haja lugar à extinção da conta de depósito à ordem por qualquer que seja acausa e se mantenham obrigações pecuniárias do Cliente perante o Banco, o respectivopagamento deverá ser feito por crédito da conta que o Banco, para tanto, indicar ao Cliente.

4/17

I.13.

I.14.

CopiesI.15.

I.16.

I.17.

ClaimsI.18.

I.19.

I.20.

Customer's Income and RemunerationI.21.

I.22.

Taxes, Duties andAmounts OwedI.23.

Reverse entriesI.24.

Voluntary CompensationI.25.

I.26.

I.27.

I.28.

Price-listI.29.

I.30.

I.31.

I.32.

I.33.

Legal and Extrajudicial CostsI.34.

I.35.

Payments to the BankI.36.

I.37.

I.38.

However, the Customer may, by bearing the respective costs, request the Bank to sendstatements within shorter periods than usual as well as request isolated statements.

The Client authorizes the Bank to, by any means, get in touch with him, namely byelectronic means, post, fax or telephone, using or not automatic systems with pre-recordedverbal messages, for the direct or indirect promotion of the marketing of any goods orservices pertaining to its business as well as, to convey facts resulting from the Bank'sbusiness relations or initiatives in connection with its commercial activity.

The Customer may request from the Bank, bearing the respective cost, photocopies ofthe documents that concern the Customer and which are in the Bank's possession.

The Bank shall try to comply as quickly as possible but it is not obliged to do so within apredetermined period of time.

The price to be paid by the Customer is the general price charged by the Bank to all theCustomers in similar situations.

Unless in the case of just cause, or when the law requires longer delays, every claimconcerning Bank's acts must be lodged within fifteen days from the date when thestatement, notice or any other document where the act in question is confirmed wasdespatched. Otherwise it shall not be taken into consideration. The claim should, at theCustomer's discretion, be addressed to the Branch where the account is domiciled or to theDepartment of Quality.

In the case of an act not originating a document to the Customer, the above mentioneddelay shall start on the date the Customer takes knowledge of the fact.

The Bank has a designated department for clients' complaints relating to its services,including financial brokering services, which is open on working days between 8:30 a.m. and4:30 p.m. at Tower B, Rua da Mesquita, no. 6, Lisbon (or which can be contacted by phoneon 808 241 206 or via the Internet on www.santandertotta.pt). The Client may also direct hiscomplaints to the Portuguese Central Bank (Banco de Portugal) or the PortugueseSecurities Market Commission (Comissão de Mercado de Valores Mobiliários), whoserespective contact details can be found at www.bportugal.pt and www.cmvm.pt. Complaintsaddressed to the Bank, which contain all the necessary information for the purpose ofanalysis, will be replied to within a maximum period of 10 days.

Interest, dividends, income and any other type of remuneration the Customer is entitledto receive from the Bank shall be paid by depositing the respective amount in its currentaccount.

The aforementioned clause does not affect other forms of payment, namely throughcapitalisation, when legally mandatory, or arising from the specific characteristics of theproduct generating the income or remuneration owed, or from particular conditions agreedwith the Customer.

All amounts due by the Bank to the Customer shall be paid net of taxes, duties or anyamounts owed that the Bank has to withhold.

The Bank is expressly authorised to reverse any entries unduly made in the Customer'saccount, namely in case of error, fault and any other circumstances when a reverse entry isjustified, the entry to be made with the value date of the original entry.

If the Bank is a creditor of the Customer for an amount overdue, it may, withoutprejudice to any other power under the Law or the security from which the debt arises, retainand use, for its repayment, any funds from balances, accounts or securities held by theCustomer at the Bank, offsetting the respective amount with debits of the same amount,regardless of the lawful requirements for legal offsetting.

For the purposes of the aforementioned clause, the Bank may proceed to the earlycancellation of term deposits or investments, with no need for further authorisation or priornotice, up to the amount needed for the repayment of the amount due. If the accounts usedfor offsetting the amounts are in a currency other than that of the debt to be paid, thetranslation at the Bank's exchange rate will be made to buy the currency of the account up tothe amount needed to pay the amount due.

In the case of a Multi-person Customer, the provision of the aforementioned clause isapplicable, within the limits of the law, to balances, funds and assets that any of the personswho compose the Customer holds at the Bank severally or jointly with others.

Should the Bank have several credits, it shall at its own discretion, determine which areextinguished through recourse to the mechanism foreseen in the aforementioned clauses.

From time to time, the Customer may consult at any branch of the Bank the price-listwith the prevailing interest rates, indices, commissions and prices charged by the Bank forits services or the method of determining them.

Unless when the law otherwise imperatively stipulates, the Bank may, from time to time,change any item of its price-list.

Changes referred to in the aforementioned clause shall take effect immediately unlessthe Bank sets a delay for them to become effective, and without prejudice to the provisions ofthe following clauses.

In the case of ongoing services, under way or yet to be started, the new price shall beimmediately applied after it comes into effect. In the case of occasional services it shall applyonly to services not yet agreed on the same date. However, changes to the price-list shall notbe applied to terminated or yet in progress computation periods and to services alreadyprovided.

When the price-list is changed, the Bank shall so advise its Customers by sending anote to be included in or go together with the bank statement immediately following itsdecision.

In the case of default or breach by either of the parties of their obligations towards theother, arising from this agreement or from any other document, the defaulter shall be liablefor the proven legal and extrajudicial costs incurred by the other party to redress thesituation.

Without prejudice to the provisions of the aforementioned clause, the parties mayagree, in the document from which the breached obligation arises or in any other, to set upcommissions to be borne by the defaulter and to offset extrajudicial costs incurred by theother in the case of default or breach of the pecuniary obligations by either party.

Unless when the opposite happens from the particular conditions agreed or from thespecific conditions of products or services to which they refer, payments due to the Bank bythe Customer, for whatever reason, shall be made by debiting the respective amounts to thecurrent account, which the Customer undertakes to keep timely with funds, the Bank beingirrevocably authorised to make the above mentioned debits with no need of prior notice.

Debits referred to in the aforementioned clause may not be made prior to the maturity ofthe corresponding obligations, but they may be made later with the correct value date.

When the current account is cancelled for any reason whatsoever and the Customerstill has pecuniary obligations towards the Bank, the payment shall be made by crediting theaccount that the Bank shall indicate to the Customer for that purpose.

PrazoI.39.

Denúncia e ResoluçãoI.40.

I.41.

I.42.

I.43.

I.44.

I.45.

I.46.

I.47.

I.48.

I.49.

I.50.

I.51.

Exercício de direitosI.52.

ReduçãoI.53.

Conflito de CláusulasI.54.

Branqueamento de CapitaisI.55.

I.56.

O contrato estabelecido entre o Banco e o Cliente a que se aplicam as presentescláusulas gerais durará por tempo indeterminado, sem prejuízo do disposto nas cláusulasseguintes.

O Banco pode proceder ao cancelamento imediato da conta de depósitos aberta nostermos das presentes Condições Gerais e dos meios de pagamento disponibilizados, semdependência de qualquer aviso, no caso de concluir por alguma irregularidade ouinsuficiência, não sanada, nas declarações produzidas e nos documentos apresentadospelo Cliente na sua abertura, e denunciar o contrato estabelecido com o Cliente a quemnotificará com, pelo menos, trinta dias de antecedência relativamente à data em que adenúncia deva produzir efeitos.Cancelada a conta de depósitos à ordem, não pode o Cliente fazer qualquer uso de nenhumdos meios de pagamento que tenha em seu poder e que devolverá ao Banco,nomeadamente cheques e cartões de débito ou crédito, nem pode emitir novas ordens ouinstruções ao Banco.Nestes casos o Banco entregará ao Cliente o valor depositado, em numerário ou porrecâmbio para a Instituição de Crédito donde veio transferido, do mesmo modo como tenhasido recebido para depósito pelo Banco.

O Cliente pode, a todo o tempo e com efeitos imediatos, denunciar o contratoestabelecido com o Banco, notificando-o do facto. No caso de Cliente pluripessoal adenúncia só procede se feita por quem tem poderes de movimentação da conta dedepósitos à ordem.

A notificação não prejudica, todavia, as operações já em curso ou que, tendo sidoordenadas ou solicitadas, não possam ser paralisadas, nem impede ao Banco a prática dosactos adequados ao exercício dos direitos que Ihe cabem.

A notificação faz, porém, cessar as ordens de pagamento que tenham sido emitidaspelo Cliente, permanentes ou não, e que devessem ser cumpridas depois do quinto diapassado sobre o conhecimento da denúncia.

Recebida a notificação e realizadas as operações e praticados os actos a que se referea cláusula anterior, o Banco procederá ao encerramento da conta de depósito à ordem edará aos fundos nela existentes, que não sejam necessários para o reembolso de dívidasvencidas, bem como a outros eventuais valores que lhe estejam confiados e que possamser imediatamente movimentados, o destino ordenado pelo Cliente.Os demais valores serão disponibilizados quando puderem ser movimentados, quer emfunção das suas características ou da dos produtos financeiros em que se enquadram, querem razão dos ónus que sobre eles eventualmente impendam.

O disposto na cláusula anterior quanto à entrega de valores ao Cliente não terá lugarquando o Banco esteja impedido de a ela proceder, por determinação da lei ou autoridadejudicial ou administrativa competente, sendo então aplicável o que resulte da Lei.

O Banco pode, porém, optar por não proceder ao encerramento da conta de depósito àordem no caso de continuarem a vigorar relações com o Cliente, contratuais ou outras, deonde emerjam para este obrigações de carácter pecuniário que ele deva futuramentecumprir.

No caso previsto na cláusula anterior o Banco pode, no entanto, bloquear a conta atodos os movimentos a débito que não sejam para realizar pagamentos devidos peloCliente ao Banco, não sendo aplicável o regime das cláusulas I.44ª e I.45ª, sem prejuízo dodireito do Cliente à movimentação dos fundos que lhe pertençam, com respeito pelascaracterísticas próprias de cada um.

Em qualquer caso, uma vez denunciado o contrato nos termos da cláusula I 41ª, nãopode o Cliente fazer qualquer uso de nenhum dos meios de pagamento que tenha em seupoder, nomeadamente cheques e cartões de débito ou crédito, nem pode emitir novasordens ou instruções ao Banco que, se isso ocorrer, pode, livremente, recusá-las oucumpri-las, conforme melhor entender.

O Banco pode, a todo o tempo, resolver o contrato estabelecido com o Cliente, comefeitos imediatos, quando se verifique alguma das seguintes circunstâncias:a) mora ou incumprimento de alguma das obrigações do Cliente;b) inexistência de quaisquer fundos depositados ou confiados ao Banco pelo Cliente:c) O Cliente tenha denunciado o Contrato de Serviço de Pagamentos constante dasCondições VI.

Para além do disposto no número anterior, tem também o Banco a faculdade de, a todoo tempo, denunciar o contrato estabelecido com o Cliente, notificando a denúncia aoCliente com, pelo menos, trinta dias de antecedência relativamente à data em que devaproduzir efeitos. Tendo o Banco procedido à denúncia ou resolução, são aplicáveis com asnecessárias adaptações as cláusulas anteriores que regulam os efeitos da denúnciaoperada pelo Cliente.

Se, uma vez notificado da resolução ou da denúncia, o Cliente não instruir validamenteo Banco, no prazo de trinta dias, sobre o destino a dar aos fundos e valores neledepositados ou a ele confiados, pode o Banco, alternativa ou cumulativamente, conformemelhor lhe aprouver:a) transferir os fundos ou valores para uma conta transitória interna, até à movimentaçãodefinitiva;b) remeter para o domicílio do Cliente cheque bancário no valor que o Cliente tem direitoa receber;c) proceder à consignação em depósito.Enquanto o Banco não usar das faculdades a que se referem as alíneas b) e c), o Clientemantém o direito de o instruir sobre o destino a dar aos valores.

O exercício por qualquer das partes de algum dos direitos que lhe assista nãoprejudica, em caso algum, a possibilidade de, concomitante ou posteriormente, exerceroutros direitos de que igualmente disponha e que com ele não sejam incompatíveis. Semprejuízo das regras da prescrição e da caducidade, o não exercício, pontual ou continuado,por qualquer das partes, de um direito que lhe assista não pode, em caso algum, serentendido como renúncia implícita ao direito em causa, nem, decorrendo esse direito demora ou incumprimento de alguma obrigação da outra parte, autoriza o infractor apermanecer na infracção ou repeti-la.

A eventual declaração judicial de invalidade ou ineficácia de alguma das presentescondições gerais não prejudica a validade e eficácia das demais que continuarão a regulara relação entre o Banco e o Cliente.

Em caso de eventual conflito ou discrepância entre cláusulas que respeitem emparticular a certo produto ou serviço e outras de carácter geral ou relativas a outro produtoou serviço, as primeiras prevalecem sobre as segundas.

O Banco está vinculado ao cumprimento do normativo legal sobre a prevenção e lutacontra o branqueamento de capitais e o financiamento do terrorismo. Neste domínio,impõem-se ao Banco, na relação com os seus clientes, vários deveres consagradoslegalmente, destacando-se o dever da completa identificação dos seus clientes,representantes e, em certas situações, o dever de identificação do beneficiário efectivo dapessoa colectiva, ou do centro de interesses colectivos sem personalidade jurídica.

Neste contexto, o Cliente obriga-se perante o Banco a fornecer todos os elementos deverificação de identidade solicitados pelo Banco, quer no momento de abertura de conta,quer em qualquer momento posterior à abertura de conta, independentemente de taiselementos serem relativos ao próprio Cliente, ao seu representante, ou ao beneficiárioefectivo.

5/17

TermI.39.

TerminationI.40.

I.41.

I.42.

I.43.

I.44.

I.45.

I.46.

I.47.

I.48.

I.49.

I.50.

I.51.

Exercise of rightsI.52.

ReductionI.53.

Conflict of ClausesI.54.

Money LaunderingI.55. The Bank is bound to the compliance with the legal provisions about preventionand

.I.56.

.

The agreement entered into by the Bank and the Customer to which these generalclauses apply shall last for an indefinite period, without prejudice to the provisions of thefollowing clauses.

The Bank may with immediate effect cancel the current account opened under theterms of the General Conditions herein and the means of payment provided, with no need offurther notice, if the Bank finds any irregularity or insufficiency, not solved, in the statementsmade and documents submitted by the Customer when opening the account, and terminatethe agreement made with the Customer who will be notified with at least thirty days noticeprior to the date when the termination must become effective. Following cancellation of thecurrent account, the Customer may not use any of the means of payment in his/herpossession which it shall return to the Bank, namely cheques and debit or credit cards, normay he/she issue new orders or instructions to the Bank. In the cases hereunder, the Bankshall deliver to the Customer the amount deposited, in cash or by transfer to the CreditInstitution from where it was transferred, in the same way as it was received to be depositedby the Bank.

From time to time, the Customer may with immediate effect terminate the agreementmade with the Bank, by notifying it to that effect. In the case of a Multi-person Customertermination only becomes effective if made by whoever is empowered to handle the currentaccount.

However, this notice shall not affect those operations already in progress or that, havingbeen instructed or requested, may not be stopped, nor shall it prevent the Bank fromcarrying out such acts as may be adequate to exercise its rights.

However, this notice shall stop such payment orders as have been issued by theCustomer, permanent or otherwise, and that should have been fulfilled after the fifth dayfrom the acknowledgement of termination.

Once such notice has been received and the transactions and the acts mentioned in theprevious clause carried out, the Bank shall close the current account and give the fundswhich exist therein and which are not necessary to repay overdue amounts as well as othersuch assets entrusted to the Bank that may be immediately transacted, the destination asinstructed by the Customer. The other assets shall be made available when they can betransacted, either due to their characteristics or those of such financial products they arepart of, or to any occasional lien.

The provisions of the aforementioned clause concerning the delivery of assets to theCustomer shall not apply when the Bank is prevented from doing so, subject to the law orcompetent judicial or administrative authority, in which case the law shall apply.

However, the Bank may choose not to close the current account before 30 (thirty) dayshave elapsed from the settlement of the linked term deposits or if the Customer and the Bankcontinue to do business, through agreements or other forms, from where pecuniaryobligations emerge for the Customer which he shall comply with in the future.

In the case foreseen in the aforementioned clause, the Bank may however block theaccount to every debit entry not for the purpose of making payments due by the Customer tothe Bank, the provisions of clauses I.44 and I.45 not being applicable, without prejudice tothe Customer's right to handle such funds belonging to him/her, with due respect for thecharacteristics of each one.

In any case, once the contract is terminated following the provisions of clause I.41., theCustomer may neither use any of the means of payment in its possession, namely chequesand debit or credit cards, nor issue new orders or instructions to the Bank, which, should thatoccur, may freely refuse them or comply with them, as it may deem fit.

The Bank may, at any time, terminate the contract signed with the Client, withimmediate effects, when any of the following circumstances occur:a) delay or default regarding any of the Client's obligations;b) lack of any funds deposited or entrusted to the Bank by the Client;c) The Client has terminated the Payment Services Contract included in Conditions VI.

Besides the provisions of the aforementioned clause, the Bank is entitled at any time toterminate the agreement made with the Customer, giving at least a prior notice of thirty daysfrom the date it becomes effective. The agreement having been terminated by the Bank, theaforementioned clauses that govern the termination by the Customer shall apply with thenecessary adjustments.

If, once the Customer has been given notice of termination, it does not validly instructthe Bank, within thirty days, as to what to do with the funds and assets deposited therein orentrusted to it, the Bank may, alternatively or cumulatively, as it may deem fit:a) transfer the funds or assets to an internal temporary account until their ultimate

transaction;b) send to the Customer's address a banker's cheque for the amount the Customer is

entitled to receive;c) to deposit in escrow.While the Bank does not use such powers as referred to in b) and c), the Customer has aright to instruct on the destiny of the assets.

The exercise by either party of any of its rights shall not affect, in any case, thepossibility of concomitantly or at a later date exercising such other rights as it may have andthat are not incompatible with it. Without prejudice to the rules of the statute of limitation anforfeiture, the occasional or continued non-exercise, by any of the parties, of a right to whichit is entitled may neither be understood, in any case, as an implied waiver of the said right,nor, if the right arises from default or breach of any obligation by the other party, does itauthorise the party at fault to continue the infringement or to repeat it.

The probable judicial declaration of the invalidity or inefficacy of any of the generalconditions herein shall not affect the validity and efficacy of the others which shall continue togovern the relationship between the Bank and the Customer.

In the event of a probable conflict or discrepancy between clauses that relate inparticular to a certain product or service and others of a general nature or relating to anotherproduct or service, the former shall prevail over the latter.

combating money laundering and financing of terrorism. In this field the Bank has,regarding its customers, various duties provided for in the law, such as the duty of fullidentification of its customers, their representatives and, under certain circumstances, alsothe duty of identification of the actual beneficial owner of the corporate body, or the centre ofcollective interests without independent legal status

In this context, the Customer undertakes the obligation before the Bank to provide allidentity check details required by the former, both at the moment the account is opened andany other subsequent moment, whether or not those details have concern the customeritself, his representative or the actual beneficial owner

I.57.

a)

b)

c)

I.58. Caso o cliente não cumpra com todos os requisitos de verificação da identidade,ou o

II.CONTADE DEPÓSITOS À ORDEMII.1.

II.2.

II.3.

II.4.

II.5.

II.6.

II.7.

II.8.

II.9.

II.10.

II.11.

II.12.

II.13.

II.14.

II.15.

II.16.

II.17.

Sempre que, no âmbito da sua relação com o Banco, o Cliente actue por conta deoutrém, nomeadamente seus clientes, o Cliente obriga-se igualmente a colaborar com oBanco em tudo o que for necessário para que este possa cumprir as suas obrigaçõesdecorrentes do normativo legal sobre a prevenção e luta contra o branqueamento decapitais e o financiamento do terrorismo, em particular o seguinte:

facilitar ao Banco, num prazo máximo de 24 horas após o respectivo requerimento, osdados e documentos completos de identificação dos seus próprios clientes, sempre queestes sejam beneficiários efectivos de alguma das operações registadas nas suas contas;

facilitar ao Banco, num prazo máximo de 24 horas após o respectivo requerimento,qualquer outra informação, incluindo os documentos que justifiquem a origem dos fundos ea natureza da transacção ou negócio subjacente, na medida em que estes permitam umcabal conhecimento do seu conteúdo, alcance e legitimidade.

abster-se de canalizar para o Banco quaisquer operações susceptíveis de estarrelacionadas com a prática dos crimes de branqueamento ou de financiamento aoterrorismo, bem como novas operações relacionadas com o cliente que tenha originadouma comunicação de operativa suspeita, ao abrigo da legislação aplicável.

utras informações solicitadas, no momento de abertura de conta, ou em qualquermomento posterior quando questionado pelo Banco para o efeito, o Banco não poderáestabelecer a relação de negócio pretendida pelo cliente, quer seja a abertura de conta dedepósito bancário, ou a realização de qualquer transacção ocasional, e, caso a conta jáesteja aberta, o Banco resolverá o presente contrato e procederá ao encerramento daconta.

A abertura da Conta de Depósito à Ordem depende de proposta do Clientesubscrevendo e preenchendo completamente a Ficha de Cliente, da prestação pelo Clientede informação sobre todos os elementos de identificação previstos na referida ficha, daapresentação e entrega ao Banco dos adequados documentos comprovativos doselementos de identificação assegurando o Cliente a veracidade de todas as informações eelementos fornecidos ao Banco, da subscrição destas Condições Gerais, do depósito domontante mínimo fixado em cada momento no preçário do Banco e disponível nos seusBalcões, e da verificação pelo Banco da regularidade e suficiência das declaraçõesproduzidas e documentação apresentada.

A falta de prestação pelo Cliente de informação sobre todos os elementos deidentificação constantes da ficha de cliente ou a falta de apresentação e entrega ao Bancodos respectivos documentos comprovativos, é impeditiva da realização de quaisquermovimentos a débito ou a crédito na respectiva conta de depósitos à ordem subsequentesao depósito inicial e disponibilização pelo Banco de quaisquer instrumentos de pagamentosobre aquela conta ou a alteração da sua titularidade, se a falta cometida não for impeditivada abertura ao Cliente da conta de depósitos à ordem.

Se a Ficha de Cliente não se encontrar devidamente preenchida ou não estiverinstruída com os documentos adequados à prova dos factos declarados, pode o Banconotificar o Cliente para a supressão da falta, no prazo que lhe indicar, sob pena doencerramento da conta.

Presume-se que a Ficha de Cliente se encontra devidamente preenchida e instruídacom os documentos adequados à prova dos factos declarados, decorridos 45 dias após asubscrição destas Condições Gerais sem que o Banco tenha notificado o cliente parasuprimir qualquer falta ou deficiência nas declarações produzidas e nos documentosapresentados.

A conta será identificada por um número atribuído pelo Banco que, todavia, por actounilateral do mesmo, pode ser modificado a todo o tempo, tendo designadamente em contarazões de carácter operacional, informático ou de segurança. A modificação do número daconta será atempadamente comunicada ao Cliente, obrigando-se o Banco, a expensasexclusivamente suas, a operar eventuais modificações nos meios de pagamento ou demovimentação da conta confiados ao Cliente que se tornem necessárias.

A conta será individual ou plural conforme o Cliente seja uma pessoa única ouconstituída por mais do que uma pessoa, caso em que a conta é aberta na titularidade detodas as pessoas que constituem o Cliente.

As Contas plurais serão, conforme os casos:a) Solidárias - quando movimentáveis isolada e indistintamente por qualquer um dosTitulares;b) Conjuntas - quando movimentáveis apenas com a intervenção de todos os Titulares;c) Mistas - quando movimentáveis em termos diferentes, com a intervenção dos Titularesindicados na ficha de cliente.

A modalidade da conta plural obedecerá ao que for indicado pelo Cliente no impressode abertura de conta.

Sem prejuízo do que mais resulta das cláusulas que regulam a Banca à Distância, aconta é movimentável pelo Cliente por meio de cheques, ordens de pagamento, cartões dedébito ou quaisquer outros meios de pagamento emitidos ou admitidos pelo Banco, desdeque, conforme os casos, os instrumentos utilizados contenham a assinatura do Cliente compoderes de movimentação, ou operem mediante a utilização de códigos pessoais secretosatribuídos e aceites pelo Banco.

Quando o instrumento de movimentação seja documento que contenha a assinaturado Cliente, o Banco conferi-la-á por semelhança com a constante da sua ficha deassinaturas.

Para o efeito do disposto na cláusula anterior, com a subscrição do impresso deabertura de conta todas as pessoas que integram o Cliente preencherão também uma fichaonde aporão a assinatura que utilizarão nos instrumentos de movimentação da conta.Quando pretendam utilizar indiscriminadamente mais do que um modelo de assinatura, aspessoas em causa aporão todos eles na ficha em causa. No caso de pretender alterar aassinatura a utilizar, o interessado procederá à prévia substituição da ficha de assinaturas.

Salvo expressa indicação em contrário, a alteração da ficha de assinaturas apenasreleva quanto a instrumentos de pagamento datados e apresentados dez dias úteis após adata em que tenha tido lugar.

Sem prejuízo do sigilo a que está obrigado, o Banco fica expressamente autorizadoa reproduzir, nos termos que entender, a ficha de assinaturas, nomeadamente com vista apoder certificar-se da genuinidade das assinaturas constantes dos instrumentos demovimentação da conta.

A conta pode também ser movimentada por procuradores do Cliente devidamenteconstituídos por procuração outorgada nos termos da Lei, e segundo o que dela constar.Para o efeito, o Procurador deverá preencher ficha de assinaturas nos termos da cláusulaII.1., prestar informação sobre todos os elementos da sua identificação nela previstos eentregar ao Banco os adequados documentos comprovativos dos elementos da suaidentificação.

O Banco, porém, só está obrigado a reconhecer e aceitar a procuração quando severifique um dos seguintes factos:a) O original ou cópia certificada seja entregue ao Banco;b) Seja entregue ao Banco fotocópia autenticada de procuração arquivada em CartórioNotarial.

Quando proceda à revogação da procuração, o Cliente deverá notificarespecificamente o facto ao Banco. Salvo disposição imperativa da lei em contrário, arevogação, no que ao Banco respeita, só é eficaz após a notificação referida.

Havendo mudança do seu representante o Cliente obriga-se a notificarimediatamente o facto ao Banco, que não pode, em circunstância alguma, ser responsávelpor movimentações da conta feitas com a intervenção do anterior representanteanteriormente à referida notificação, e sem prejuízo do disposto na cláusula II.19.

6/17

I.57.

a)

b)

c)

.I.58.

II.CURRENTACCOUNTII.1.

II.2.

II.3.

II.4.

II.5.

II.6.

II.7.

II.8.

II.9.

II.10.

II.11.

II.12.

II.13.

II.14.

II.15.

II.16.

II.17.

Whenever, within the scope of its relation with the bank, the Customer, acts on behalf ofanother party, especially its customers, the Customer undertakes also the obligation tocooperate with the Bank in everything deemed necessary to enable the later to comply withits obligations deriving from the legal provisions about prevention and combating moneylaundering and financing of terrorism, especially the following:

to provide the Bank, within a maximum of 24 hours after being required to do so, with theirown customers' full identification data and documents, whenever these are the beneficialowners of some of the transactions recorded in their accounts;

to provide the Bank, within a maximum of 24 hours after being required to do so, with anyother information, including documents showing the source of the funds and the nature ofthe transaction or underlying business, to the extent that the later may enable a fullawareness of their contents, scope and legitimacy.

refrain from directing to the Bank any operations likely to being related with moneylaundering and financing of terrorism crimes, as well as new operations related to the clientwhich has originated a suspicious operation, according to the applicable legislation

If the Customer does not comply with the requirements of the identification check, orother information required by the Bank at the moment of opening an account or any othersubsequent moment when required by the Bank to do so, the Bank may not enter thebusiness relationship the Customer wants, whether it is the opening of a deposit account, orany other occasional transaction and if the account has already been opened, the Bankshould terminate the current contract and close the account

The opening of a Current Account depends on a Customer's proposal by signing andcompleting the Signature Card, giving information about every identification elementforeseen in the above mentioned card, submitting and delivering to the Bank adequatedocuments to prove his/her identification and confirming the truthfulness of everyinformation and element given to the Bank, subscribing the General Conditions herein,depositing the minimum amount stipulated at any time in the Bank's price-list and availableat its Branches, and the Bank has to confirm the reliability and sufficiency of the statementsproduced and documentation submitted.

If the Customer does not provide information on every identification element in theSignature Card or if the documents confirming the information given are not submitted anddelivered to the Bank, no debits or credits shall be made in the Customer's current accountfollowing the initial deposit, and the Bank shall not make available any payment instrumentson that account nor shall its holder be changed, if the fault is not impeditive of the opening ofthe current account for the Customer.

If the Signature Card is not dully completed or is not joined by such adequate documentsas to prove the declared statements, the Bank may notify the Customer to correct the faultwithin the delay it shall specify, under penalty of closing the account.

The Signature Card is presumed to be duly filled in and joined by such adequatedocuments that shall confirm the declared statements, after forty five days of the signature ofthe General Conditions herein with no notice from the Bank to the Customer to correct anyfault or deficiency in the statements produced and documents submitted.

The account shall be identified by a number assigned by the Bank which, however, theBank may unilaterally modify from time to time, taking specifically into account any reasonsof operational, information technology or security nature.Any change in the account numbershall be communicated to the Customer on time, and the Bank, at its own expenses, shall berequired to implement any changes in such means of payment or handling of the accountentrusted to the Customer and considered necessary.

The account shall be individual or a joint account depending on whether the Customer isa single person or more than one person, in which case the account is held in the name ofevery person that make up the Customer.

The JointAccounts shall be, as applicable:a) Joint Single Signature Accounts when handled with the individual signature of any of the

account holders;b) Joint Collective Signature Accounts when handled with the signature of all the account

holders;c) Joint Mixed Signature Accounts when handled under different terms, with the

intervention of such Holders as shown in the Signature Card.The joint account type shall comply with the Customer's instructions in the account

application form.Without prejudice of what arises from the clauses that govern the Home Banking, the

Customer shall handle the account by means of cheques, payment orders, debit cards orany other means of payment issued or allowed by the Bank, provided that, as applicable, theinstruments used contain the signature of the Customer with powers to handle the account,or use secret personal codes allocated and accepted by the Bank.

When the handling instrument is a document with the Customer's signature, the Bankshall confirm it by comparison with the one in the Signature Card.

For the purpose of the provisions of the aforementioned clause, when signing theaccount application form, all the persons that compose the Customer shall also fill in a cardwhere they shall affix the signature they shall be using in the account handling instruments.In the event of wanting to be able to indiscriminately use more than one type of signature,these persons shall affix them on the above mentioned card. Should any of them wish tochange the signature to be used, the interested party shall previously replace the signaturecard.

Unless otherwise expressly indicated, any change in the signature card shall onlyapply to payment instruments dated and submitted ten business days after the date whenthe change was made.

Without prejudice to the confidentiality to which it is bound, the Bank is expresslyauthorised to reproduce the signature card under such terms as it may deem fit, namely tobe sure that the signatures in the account handling instruments are legitimate.

The account may also be handled by the Customer's attorneys duly appointed bymeans of a power of attorney issued under the terms of the Law and of the power of attorney.For the purpose, the attorney shall fill in the signature card under the terms of clause II.1.,provide information on every element of his identification therein foreseen and deliver to theBank the adequate documents confirming his identification.

However, the Bank must recognise and accept the power-of-attorney when one offollowing two facts occurs:a) the original or certified copy is delivered to the Bank;B) a certified copy of a power-of-attorney filed at a notary public is delivered to the Bank.

When revoking a power-of-attorney, the Customer must notify the Bank specificallythereof. Except for an imperative legal provision to the contrary, and as far as the Bank isconcerned, the revocation is effective only following the aforesaid notice.

The Customer undertakes to immediately notify the Bank of any changes of itsrepresentatives, and in no circumstance can the Bank be held responsible for a formerrepresentative handling the account prior to the said notification, and without prejudice to theprovisions of clause II.19.

II.18.

II.19.

II.20.

II.21.

II.22.

II.23.

II.24.

II.25.

II.26.

II.27.

II.28.

II.29.

II.30.

II.31.

II.32.

II.33.

II.34.

II.35.

II.36.

II.37.

III. DEPÓSITOS A PRAZO E APLICAÇÕES DE FUNDOS EM PRODUTOSFINANCEIROSIII.1.

III.2.

III.3.

III.4.

III.5.

Sem embargo do disposto na cláusula anterior, o Banco pode recusar amovimentação da conta se, não obstante não ter sido notificado pelo Cliente do facto, tiverconhecimento, por outro meio, da alteração do seu representante.

Salvo quando receba expressas indicações em contrário, feita com a indicação dosnovos representantes do Cliente, o Banco autorizará todas as movimentações de contafundadas em documento subscrito pelos anteriores representantes com data anterior à danotificação ou em ordem por eles comprovadamente dada antes da mesma data, ainda queo movimento em causa só deva ocorrer no futuro.

O disposto nas cláusulas anteriores não prejudica o poder de revogação das ordensdadas pelos novos representantes, o qual pode ser exercido nos termos gerais de direito.

A manutenção da conta de depósitos à ordem pode implicar a manutenção de umsaldo médio mínimo, ou, sendo inferior, o pagamento de custos de manutenção fixado peloBanco, podendo este cobrar também uma comissão por cada operação efectuada. O saldomínimo, os custos de manutenção e a comissão são os que constarem do preçáriodisponível nos Balcões do Banco, que podem ser alterados a todo o tempo.

O Cliente pode, a todo o tempo, solicitar ao Banco a emissão de cheques, cartões dedébito ou outros meios específicos de movimentação da conta, obrigando-se em todos oscasos a fazer devida utilização dos meios que venham a ser facultados, nos termos da Lei.

Compete, porém, ao Banco o poder discricionário de decidir se faculta ou não aoCliente - e em caso afirmativo nos termos, condições e quantidades pedidas - os meios porele solicitados.O facto de o Banco ter atendido um pedido ou mesmo atender regularmente os pedidosformulados pelo Cliente não implica a obrigação de satisfazer solicitações futuras.

Sempre que aceite a requisição de cheques e os emita, o Banco entregá-Ios-ádirectamente ao Cliente ou a representante ou procurador autorizado ou com poderes demovimentação da conta, sendo a entrega feita no Balcão onde a conta está domiciliada ounoutro pretendido pelo Cliente, sempre contra recibo, que pode consistir na simplesassinatura do receptor no verso ou em local próximo da requisição.

O Cliente pode, porém, solicitar a remessa dos cheques pelo correio, suportandoentão o respectivo custo de acordo com o que se encontra fixado no preçário. Nestes casos,os cheques são enviados na situação de activos podendo ser de imediato utilizados peloCliente.

De acordo com a legislação aplicável e com a regulamentação emitida pelasautoridades de supervisão bancária, nomeadamente o Banco de Portugal, pode o Cliente,em caso de utilização indevida, ser incluído na lista de utilizadores de cheques queoferecem risco, bem como suportar as demais consequências legais apropriadas àsituação.

Mesmo quando a conta não se encontrar devidamente provisionada para suportar opagamento de qualquer valor devido ao Banco, pode este debitar o correspondentemontante a descoberto.Igual faculdade cabe ao Banco no caso de pagamentos a favor do próprio Cliente ou a favorde Terceiros, por ele ordenados.O disposto nesta cláusula constitui unicamente uma faculdade do Banco, não podendo, emcaso ou circunstância alguma, ser considerado como uma obrigação.

Ainda que o Banco tenha já autorizado pagamentos ou débitos a descoberto oumesmo os autorize com regularidade, tem sempre a faculdade de, a seu único critério,recusar novos pagamentos ou débitos, salvo quando, por contrato específico estabelecidopor escrito com o Cliente, se tenha obrigado de outra forma.

A entrega de cheques, outros títulos de crédito ou outros valores para depósito emconta é sempre considerada à cobrança, pelo que os montantes respectivos apenas sãodisponibilizados ao Cliente após a verificação da boa cobrança dos valores entregues ou deoutra circunstância que a ela seja legal ou regulamentarmente equiparada, sendo aplicávelo disposto nas cláusulas anteriores relativamente à eventual disponibilização antecipadade fundos correspondentes a valores à cobrança.

Salvo acordo escrito em contrário, quando tenha antecipado os fundos relativos avalores entregues pelo Cliente para depósito, o Banco tem o direito a reembolsarimediatamente os montantes não cobrados, procedendo ao respectivo débito na conta dedepósito à ordem.

O Banco obriga-se a avisar o Cliente dos valores que, tendo-lhe sido entregues paracobrança de acordo com as cláusulas anteriores, não hajam sido cobrados.

Salvo acordo escrito das partes em contrário, os pagamentos sobre valoresautorizados pelo Banco, que não tenham contrapartida em dinheiro efectivamentedisponível na conta, são considerados pagamentos a descoberto para os efeitos dodisposto na cláusula seguinte.

Sobre os descobertos gerados na conta são devidos juros ao Banco à taxaconstante do preçário e aplicável à generalidade dos Clientes.

Sem prejuízo de acordo escrito em contrário, os juros dos descobertos são apuradose pagos mensalmente pelo Cliente.

Em qualquer caso, os descobertos verificados devem ser regularizados pelo Clientemediante o depósito de dinheiro correspondente, no mais curto prazo possível após arespectiva verificação e, no limite, à simples interpelação do Banco.

Salvo acordo em contrário estabelecido entre as partes, os saldos positivos da contaserão ou não remunerados nos termos publicitados pelo Banco, aplicáveis à generalidadedos Clientes e disponíveis em todos os Balcões, podendo o Banco alterar as condições deremuneração a todo o tempo e com efeitos imediatos.A contagem e pagamento de juros, quando devidos, far-se-á igualmente nos termospublicitados pelo Banco, que também os pode unilateralmente alterar a todo o tempo.O Cliente pode, em qualquer momento, obter em qualquer Balcão informação sobre ascondições e termos de remuneração dos saldos de contas à ordem praticados pelo Bancopara a generalidade dos Clientes.

O encerramento da conta terá lugar nos casos de denúncia ou resolução do contratoa que se aplicam as presentes Condições Gerais e nos termos a propósito indicados. Aconta pode também ser encerrada ou suspensa por ordem de autoridade judicial ouadministrativa competente.

Os depósitos constituídos serão identificados por um número ou código e ficarãonormalmente agregados à conta de depósito à ordem, podendo, no entanto, o Banco, porrazões operacionais, informáticas, de segurança ou outras modificar a todo o tempo onúmero ou código atribuído.Os prazos, montantes mínimos, se os houver, e demais condições de constituição, vigênciae mobilização de depósitos a prazo são os determinados pelo Banco e aplicáveis àgeneralidade dos Clientes.

Respeitadas as condições fixadas, o Cliente pode, a todo o tempo, ordenar aconstituição de depósitos a prazo, a qual terá sempre lugar por débito do montantecorrespondente na conta de depósito à ordem devida e previamente provisionada para oefeito, ficando o Banco autorizado a efectuar todas as operações correspondentes.

Os depósitos ordenados serão constituídos com data-valor do primeiro dia útilseguinte ao da ordem, salvo quando, pelas próprias características do depósito em causa,deva ele ser constituído em data posterior.

O Banco emitirá um documento probatório da constituição do depósito no qualconstarão o respectivo montante, prazo e remuneração aplicável.

Salvo instruções do Cliente em contrário ou imposição das características específicasdo depósito constituído, os depósitos a prazo são de renovação automática por períodoidêntico ao da constituição e à taxa de remuneração praticada à data pelo Banco para ageneralidade dos depósitos do mesmo tipo.

7/17

II.18.

II.19.

II.20.

II.21.

II.22.

II.23.

II.24.

II.25.

II.26.

II.27.

II.28.

II.29.

II.30.

II.31.

II.33.

II.34.

II.35.

II.36.

II.37.

III. TERM DEPOSITSAND INVESTMENTS IN FINANCIAL PRODUCTSIII.1.

III.2.

III.3.

III.4.

III.5.

Notwithstanding the provisions of the aforementioned clause, the Bank may refuse tohandle the account if, despite not having been so notified by the Customer, it is aware of thechange of the Customer's representative by some other means.

Unless it receives express indication to the contrary by instruction of the newCustomer's representatives, the Bank shall authorise every account transaction based ondocuments signed by the former representatives dated prior to the notification or on aninstruction given by them prior to the said date, although the transaction shall only take placein the future.

The provisions of the above mentioned clauses do not prejudice the power to revokethe instructions given by the new representatives, which can be exercised under the generalterms of the law.

The subsistence of the current account may imply keeping a minimal average balance,or, in case of a lower balance, the payment of account maintenance costs as determined bythe Bank, who shall also be allowed to charge a fee for each transaction made. Theminimum balance, the maintenance costs and the fee are those included in the price-listavailable at the Bank's Branches, which can be changed from time to time.

From time to time, the Customer may request the Bank to issue cheques, debit cardsor other specific means to handle the account, undertaking in all such cases to make properuse of the means with which it shall be provided, subject to the terms of the law.

However, the Bank shall have the discretionary power to decide if it shall provide theCustomer and if so, under the requested terms, conditions and quantities with therequested means.The fact of the Bank having satisfied one request or even having regularly satisfied therequests made by the Customer does not imply the obligation to satisfy future requests.

Whenever the Bank accepts the cheque requisition and issues them, it shall deliverthem directly to the Customer or to a representative or authorised attorney with powers tohandle the account. The delivery shall take place at the Branch where the account isdomiciled or such other as requested by the Customer, always against receipt notice, whichcan be simply the receptor's signature on the backside or close of the requisition.

The Customer may however request that the cheques be sent by mail, bearing therespective cost according to the Bank's price-list. In these cases, the cheques are sent inthe active status enabling the Customer to start using them immediately.

Subject to the law and with the regulations issued by the banking supervisionauthorities, namely the Bank of Portugal, the Customer may, in the event of improper use, beincluded in the list of risky cheque users, as well as suffer other legal consequences arisingtherefrom.

Even when the account has insufficient funds to pay any sum owed to the Bank, theBank may debit such sum as an overdraft.The Bank may do the same in the case of payments to the Customer or to Third Parties,instructed by the Customer.This provision is merely an option of the Bank and can in no circumstance whatsoever beconsidered an obligation.

Even if the Bank may have authorised an overdraft facility to cover payments or debits,or even if it regularly authorises them, it shall be entitled, at all times, at its own discretion, torefuse new payments or debits, except if it is otherwise bound by a specific contract made inwriting with the Customer.

The delivery of cheques, other credit securities or other assets to be deposited shallalways be subject to collection, therefore their respective amounts are only made availableto the Customer following due collection of the assets deposited or any other circumstancedeemed equivalent under the law or any regulation, the provisions of the aforementionedclauses being applicable regarding any advance of funds in respect of assets pendingcollection.

Unless there is a written agreement to the contrary, if the Bank has advanced funds inrespect of assets delivered by the Customer to be deposited, it shall be entitled to thereimbursement of any sums not collected, by debiting the current account accordingly.

The Bank undertakes to notify the Customer of any assets that, having been deliveredto it for collection under the aforementioned clauses, have not been collected.II.32. Unless there is a written agreement between the parties to the contrary, payments onassets to be collected authorised by the Bank not covered by cash actually available in theaccount, shall be considered overdraft payments for the purposes of the provisions of thefollowing clause.