Embed Size (px)

Citation preview

YORK HOUSING ASSOCIATION LIMITED

FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 MARCH 2017

Registered under the Co-operative and Community Benefit Societies Act 201416826R

YORK HOUSING ASSOCIATION LIMITED

CONTENTS

Page

Corporate information 1

Report of the Board 2 – 17

Independent Auditor’s Report 18

Statement of Comprehensive Income 19

Statement of Financial Position 20

Statement of Changes in Reserves 21

Statement of Cash Flows 22

Notes to the Financial Statements 23 – 45

YORK HOUSING ASSOCIATION LIMITED

CORPORATE INFORMATION

Co-operative & Community Benefit Society Registered Number: 16826R

Homes and Communities Agency number: L1019

Secretary: Julia Histon

Registered office: 2 Alpha CourtMonks Cross DriveHuntingtonYorkYO32 9WN

Bankers: Lloyds Bank plcSME Banking Yorkshire and North East1st Floor, Lisbon House116 Wellington StreetLeedsLS1 4LT

Auditors: External Beever and StruthersSt. George’s House215 – 219 Chester RoadManchesterM15 4JE

Internal MazarsTower Bridge HouseSt Katharine's WaySt Katharine's & WappingLondonE1W 1DD

Solicitors: Corporate Trowers & Hamlins LLP3 Bun Hill RowLondonEC1Y 8YZ

Property Crombie Wilkinson Solicitors LLP19 Clifford StreetYorkYO1 9RJ

Members of the National Housing Federation

1

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

The Board is pleased to present its report and financial statements for the year ended 31 March 2017.

Principal activity

The principal activities of the Association are: The provision and management of housing; Assistance to help house people; Provision of associated facilities and amenities or services for vulnerable people.

Results

The results for the year show a surplus of £1,132k, (2015/16 surplus: £1,546k).

Statement of the responsibilities of the Board for the report and financial statements

The Board is responsible for preparing the report and financial statements in accordance with applicable law and United Kingdom Generally Accepted Accounting Practice.

The Co-operative and Community Benefit Societies Act 2014 and Social Housing Provider legislation in the United Kingdom require the Board to prepare financial statements for each financial year which give a true and fair view of the state of affairs of the Association at the end of the year and of the surplus or deficit of the Association for the year then ended.

In preparing these financial statements the Board is required to:

Select suitable accounting policies and then apply them consistently;

Make judgments and accounting estimates that are reasonable and prudent

State whether applicable UK Accounting Standards and the Housing SORP 2014 have been followed, subject to any material departures disclosed and explained in the financial statements;

Prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Association will continue in business

The Board is responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the Association and enable it to ensure that the financial statements comply with the Co-operative and Community Benefit Societies Act 2014, the Housing and Regeneration Act 2008 and the Accounting Direction for Private Registered Providers of Social Housing 2015. It is also responsible for safeguarding the assets of the Association and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The Board is responsible for ensuring that the Report of the Board is prepared in accordance with the Statement of Recommended Practice: Accounting by Registered Social Housing Providers: Update 2014.

Status

The Association is registered with the Financial Conduct Authority under the Co-operative and Community Benefit Societies Act 2014 and registered with the Homes and Communities Agency as a Registered Provider of Social Housing under the Housing and Regeneration Act 2008.

The Association is an exempt charity and accordingly is not liable to taxation on either revenue surpluses or any surplus on sale of freehold property.

2

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

Summary review of the business

The Board is pleased to report that the past year, 2016/17, has been one of continued achievement for York Housing Association with key service performance targets being exceeded and a strong financial outturn being delivered in this set of results. In summary:

- Net Surplus to Reserves £1,132k (2016: £1,546k); - Operating Margin 25.1% before property sales surplus (2016: 27.3%); - Current Tenant Arrears 1.09% (Target 1.80%);- Former Tenant Arrears 1.14% (Target 1.10%); - Bad Debts 0.58% (Target 1.00%);- Void Properties 1.16% (Target 1.60%);- Development – new properties completed 9 (2016: 18).

Highlights of 2016/17 in addition to the above key statistics include:

- Full integration of the 57 units that York Housing Association (YHA) acquired through a transfer of engagements from Family Housing Association (FHA) in September 2015. This enabled YHA to enhance the services to existing FHA tenants, and create more headroom for further development of new homes for future tenants by realising economies of scale;

- Continued work on developing and maintaining a comprehensive Asset and Liabilities Register so that we are clear what stock we own, what liabilities are held against that stock, and where there may be capacity to provide further security for future development finance;

- During the year YHA acquired 9 homes for affordable rent, completed 3 outright sales and handed back 25 units to City of York Council that were previously managed on behalf of the Council;

- The Association put in place the Government’s statutory 1% per annum reduction in rents for its core stock and we are working closely with tenants to mitigate any negative impact from the full rollout of Universal Credit arising from the Government’s Welfare Reform programme;

- YHA handed back the leases on Scarcroft Road, Melbourne Street and St. Marys to York City Council to allow them to enter into a new lease with the successful support provider;

- YHA has continued to review potential merger opportunities and is currently in advanced discussions that would see the Association retain its identity but be part of a group structure. If successfully completed the merger will add greater efficiencies for the future and enable the Association to further its ambitions to use its assets to continue to build more new affordable homes. Legal completion date for the merger is December 2017 with a go live date of April 2018;

- The Association continues to invest in our existing stock in line with the Board’s agreed asset management plan; and

- The Association continues to remain committed to using its surpluses to develop new homes, where the future financial climate enables us to do this without putting at risk existing homes.

1. Our approach to VFM

1.1 What we mean by VFM

York Housing Association’s (YHA) definition of value for money is rooted in its mission and vision.

In order to achieve the mission and vision, as much value as possible must be produced from the money and resources available to YHA, and our objectives must be delivered in the most cost-effective way possible.

The value YHA produces is directly related to its strategic objectives, laid out in the 2016/21 Corporate Plan. These are:

- To remain a strong and viable provider of excellent homes and services to our existing and future customers;

- To grow the business and develop the organisation;- To be an excellent service provider to all our customers;- To remain open to exploring strategic partnerships; and- To be an employer of choice.

3

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

For YHA therefore, value for money is about achieving the highest levels of excellence possible, being the best partner possible, providing the most new properties possible and supporting as many customers as possible with the resources we have. YHA will do this mindful of the legitimate and sometimes competing demands of its key stakeholders, customers, local partner organisations, service commissioners, funders and the taxpayer.

The Association remains committed to using its surpluses to develop new homes, where the future financial climate enables this to be done without putting at risk existing homes.

Going forward, YHA has decided that the maximisation of its objectives is best achieved through joining a Group structure (more below).

1.2 VFM strategy

Our latest VfM Strategy was approved by the Board in November 2014 and confirms the Association’s commitment to delivering VfM. As well as underpinning the business plan it is also linked inextricably to other key corporate strategies and plans. Its aims and objectives are:

- VfM Culture – to fully embed within YHA and to underlie the resource allocation process;- Financial Capacity – to optimise the use of YHA’s asset value to deliver further housing;- Assets – robust ongoing management to achieve financial, social and environmental benefits;- Tenant Satisfaction – to improve landlord and neighbourhood services by targeting resources;- Performance – to achieve continuous improvement and benchmark against sector peers;- Procurement – to drive value from YHA’s purchasing activities;- Operating Costs – to control and improve operating costs and to monitor against peers;- VfM Self-Assessment – meeting regulatory requirements and publish annual review.

We seek to embed the concept of VfM into the heart of the organisation by maintaining a balanced service and cost conscious culture – all staff (particularly budget holders) and Board members endeavour to improve the quality and scope of the services we offer but recognise the need for constant stewardship of the limited resources available as a smaller housing association. We actively encourage ideas and innovation in developing new and different ways to deliver more efficient and effective services to our customers.

Despite the financial challenges YHA has committed to continue its pipeline development programme and offers a wide and complex range of services to its customers. We recognise the value that our development programme can potentially deliver to our existing customers through economies of scale and contributions from commercial activities but also acknowledge the inherent risks involved. As such we work with partners where they are able to bring relevant skills and experience, and maintain a prudent approach so that we can remain ‘strong and viable’.

A revised VfM strategy will be devised once the forthcoming merger takes place. The governance and assurance arrangements for driving and overseeing VfM performance will be considered at the same time.

2. Our performance in 2016-17

2.1 Responding to a changing operating environment

The Board Risk Appetite statement is as follows:

“YHA risk appetite is to remain a strong and viable provider of excellent homes and services to our existing and future customers. To achieve this YHA will seek to grow the business and develop the organisation, including through exploring strategic partnerships, but will regularly test these proposals against market conditions and the Business Plan to ensure that we do not place our core services or homes at risk.”

4

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

The Board recognised at an early stage the potential impact of changes in Government policies particularly:

- Rents to be reduced by 1% per year for 4 years- Welfare reform and its impact on tenants - Application of the Local Housing Allowance Cap and subsequent inclusion of supported housing- Pressures on funding social care within local authorities and their consequent reviews of

commissioning arrangements- Financial pressures within the NHS, which changes the support arrangements for some of YHA’s

more vulnerable customers- Right to Buy- Greater emphasis on home ownership

In view of a fast changing environment, YHA reflects material changes in its business plan when required. The last revision was effected in February 2017.

During 2016/17 YHA undertook an in depth review of all supported housing provision. This incorporated changes in the commissioning of some YHA properties by City of York Council, decommissioning certain properties which were no longer appropriate in the new environment, and identifying schemes which would need to operate at lower costs by April 2019 in order to be financially viable under the new Local Housing Allowance Cap provisions.

In order to achieve the required efficiencies and to create a more effective staffing leadership structure, better able to deal with the increasingly challenging external environment, a comprehensive organisational structure review was carried out during the 2015/16 year. During 2016/17 this new structure was being implemented and an Organisational Development Programme was procured in order to support the process.

In order to accommodate the Government changes referred to above, either through TUPE transfers or managed exits, the staffing numbers have reduced further from 43 in April 2016 to 32 in April 2017.Arising from the latest valuation by SHPS, the Board carefully considered, using external professional advice from KPMG, the risks associated with continuing to offer Defined Benefit Schemes. It concluded that with effect from the 1 April 2016 existing Defined Benefit Schemes would be closed and replaced with a Defined Contribution Scheme to lessen future liabilities. This was extensively discussed with staff, including providing consultation with an Independent Financial Advisor.

Whilst the Board has confidence in the financial viability of YHA over the medium term, it recognises that in order to embrace the new environment, additional specialist skills and organisational capacity is required. It also appreciates that current financial capacity can only support a lower level of new property developments. Accordingly a merger strategy has been developed.

The Board held an “away day” to review this strategy. After considering a number of proposals, it decided to progress discussions on a merger and become a subsidiary within a group structure.

Following a rigorous selection process, supported by external consultants, YHA’s Board has identified a preferred merger partner, North East based Karbon Homes. As a result, the Association is currently in advanced discussions that would see YHA retain its identity as a subsidiary in the Karbon Group. Subject to the necessary process being achieved during 2017, legal completion is expected to be achieved by the end of December 2017, with a ‘go live’ date of April 2018 for IT and Finance services to be moved across to the Group.

5

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

To maintain the integrity of our mission and vision, the Board agreed a set of business drivers against which the merger business case will be appraised. They are:

- Growth and development – increasing our output of new homes - Service improvements – improvements to the quality and breadth of services provided to residents,

including those tenants requiring care and support- Social value – whilst many organisations have withdrawn from social interventions (employment,

health, etc.) it is proposed to strengthen the offer in this important area, deriving benefit from sharing skills, expertise and capacity within the group

- Efficiency savings – merger presents an opportunity to deliver efficiencies through economies of scale

- Relevance and impact – larger scale will enable the drive to better and more productive relationships with key stakeholders such as, for example, City of York Council. The importance of this is likely to increase as stakeholders become larger and cover wider area.

- Building resilience and enhancing risk management capability – as the external world becomes less certain, scale and diversity will play an increasingly important part in the ability to manage risk and improve resilience to external shocks.

- People and Diversity – larger organisations can offer more opportunity for progression and attracting/retaining staff in an increasingly competitive market and reduce the dependency on key individuals.

The Board has made clear that whist the financial drivers are important, they should not take precedence over other opportunities that might be created by the merger.

2.2 Key cost data

The following table sets out YHA’s key costs over the last 3 years against the median for a range of smaller Housing Associations:

Performance Measure 2014/15 2015/16 2016/17 SPBM median

Accounts-based metricsHeadline Social Housing Cost £/Unit N/A 4,160 3,477 4,378.5Av Weekly Operating Cost/Unit £ 97.72 102.30 99.06 88.97Operating Costs as % of Turnover * 70.07 65.47 75.63 74.06Av Weekly Management Cost / Unit £ 18.24 16.45 14.95 17.50

Note * Turnover in 2015/16 includes impact of donated income (£1.285m) from FHA Transfer of Engagements

SPBM metricsCost per property for housing management N/A N/A 386 411.89Cost per property for responsive repairs and void works

N/A N/A 463 659.11

Cost per property for major and cyclical works

N/A N/A 984 908

Overhead costs as percentage of turnover N/A N/A 17.5 15.24

SPBM (Small Providers Bench Marking) cost metrics adhere to a cost apportionment methodology to ensure consistency across providers. The accounts-based metrics, with the exception of the Headline Social Housing Indicator, are subject to a degree of local variation in terms of accounting practice and should be used cautiously when comparing to others. They are helpful however to understand trends. The SPBM benchmark figure is the median value for a range of smaller housing associations across England which have collected data for the specific indicator in question.

6

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

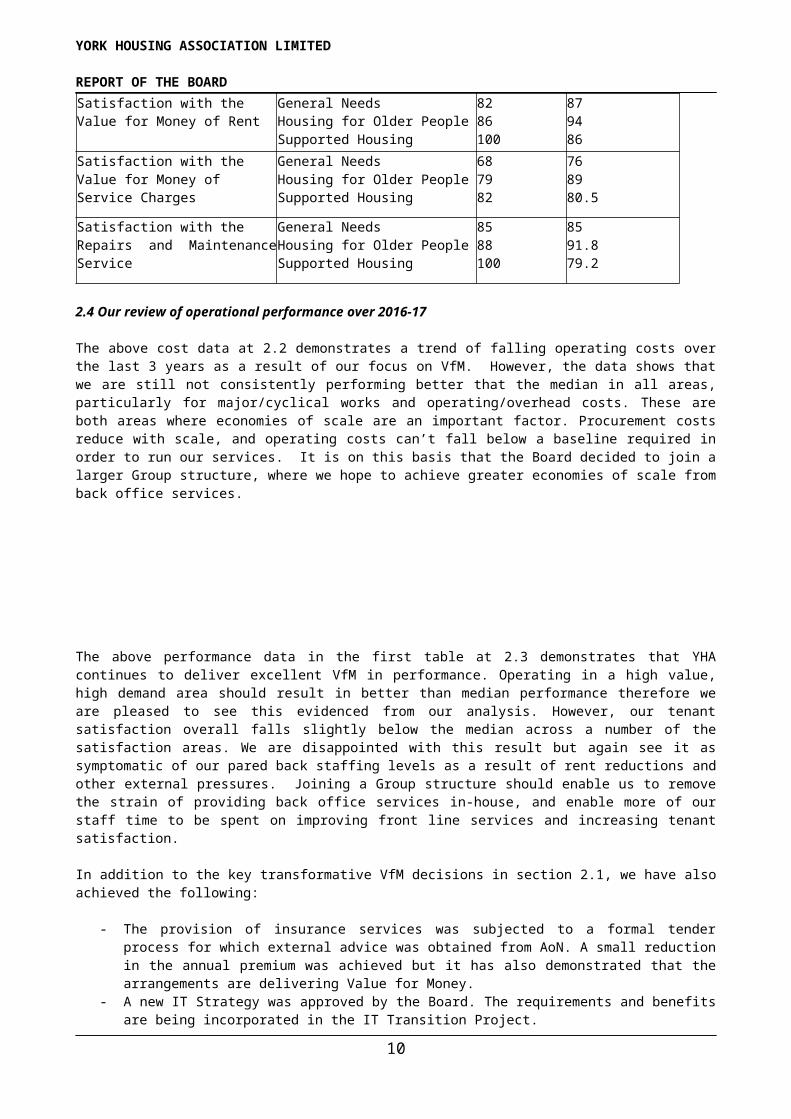

2.3 Key performance and satisfaction data

Performance Measure 2014/15 2015/16 2016/17 SPBM median

Current Tenant Arrears % GN 3.1 2.56 1.82 2.4Current Tenant Arrears % Supported 0.62 1.05 0.51 4.98

Current Tenant Arrears % HfOP 0.62 0.17 0.4 0.98

Rent lost due to Voids % GN 0.59 0.18 0.75 0.48Rent lost due to Voids % Supported 1.96 3.73 1.46 3.18Rent lost due to Voids % HfOP 0.59 0.45 1.16 0.91Average re let time (days) GN 27.3 7.9 14.29 17Average re let time (days) Supported 21 28 26 17Average re let time (days) HfOP 15.4 6.3 7.64 23.4Repairs Completed Right First Time % 97 96.7 94 93.02Residents Satisfied with Repair % 96 94.47 94 96.5Dwellings with Valid Gas Certificate % 100 100 100 100

Satisfaction Measure Tenure YHA2016/17%

SPBM2016/17%

Satisfaction with OverallService Provided byLandlord

General NeedsHousing for Older PeopleSupported Housing

879191

8992.590

Satisfaction with OverallQuality of the Home

General NeedsHousing for Older PeopleSupported Housing

888982

899589

Satisfaction with theValue for Money of Rent

General NeedsHousing for Older PeopleSupported Housing

8286100

879486

Satisfaction with theValue for Money ofService Charges

General NeedsHousing for Older PeopleSupported Housing

687982

768980.5

Satisfaction with theRepairs and Maintenance Service

General NeedsHousing for Older PeopleSupported Housing

8588100

8591.879.2

2.4 Our review of operational performance over 2016-17

The above cost data at 2.2 demonstrates a trend of falling operating costs over the last 3 years as a result of our focus on VfM. However, the data shows that we are still not consistently performing better that the median in all areas, particularly for major/cyclical works and operating/overhead costs. These are both areas where economies of scale are an important factor. Procurement costs reduce with scale, and operating costs can’t fall below a baseline required in order to run our services. It is on this basis that the Board decided to join a larger Group structure, where we hope to achieve greater economies of scale from back office services.

7

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

The above performance data in the first table at 2.3 demonstrates that YHA continues to deliver excellent VfM in performance. Operating in a high value, high demand area should result in better than median performance therefore we are pleased to see this evidenced from our analysis. However, our tenant satisfaction overall falls slightly below the median across a number of the satisfaction areas. We are disappointed with this result but again see it as symptomatic of our pared back staffing levels as a result of rent reductions and other external pressures. Joining a Group structure should enable us to remove the strain of providing back office services in-house, and enable more of our staff time to be spent on improving front line services and increasing tenant satisfaction.

In addition to the key transformative VfM decisions in section 2.1, we have also achieved the following:

- The provision of insurance services was subjected to a formal tender process for which external advice was obtained from AoN. A small reduction in the annual premium was achieved but it has also demonstrated that the arrangements are delivering Value for Money.

- A new IT Strategy was approved by the Board. The requirements and benefits are being incorporated in the IT Transition Project.

- Work of the Tenant scrutiny panel continued and in particular value for money improvements were made in relation to voids and estate services.

- The life cycles of the housing property components were reviewed in the context of past experience and the timescales adopted by peers. This will further inform future investment in planned maintenance.

- A review of service charges has been carried out during the year and the next steps will be to review with the tenants the services currently provided and their requirements for the future.

- Bad debts reduced by no longer carrying out repairs for which YHA is not responsible.- A tender was conducted for the Internal Audit Service and Mazars were appointed. Their approach

and work completed during the year has provided additional assurance to the Audit Committee.- A new contract for IT infrastructure support commenced which has improved data security and whole

system reliability. Following development of an IT strategy progress has been made on procuring replacement software to enhance integration of management information, create efficiencies in staff time, and provide more reliability of the data.

- Purchasing of the freehold of a property surplus to requirements and held for sale at the year end which enhanced its marketability and resale value.

- Further improved performance on rent collection and turn round of void properties.- Contractors incurring additional expenditure through the Living Wage requirements were supported

and encouraged to reduce costs and avoid additional charges to YHA.- The approach and costs of undertaking repairs following a property becoming void was undertaken

and it was concluded that utilising multi trade contractors provided the best value for money.

2.5 Our review of asset performance over 2016-17

2.5.1 Development Programme

During 2016/17 York Housing Association completed the following properties:

Scheme AffordableRent

SharedOwnership

TotalUnits

Phoenix Park, Whitby 9 - 9

These homes have been purchased from Barratt under a S106 Agreement and are targeted at people already living in the town. In common with many desirable seaside locations, Whitby is a particularly difficult place for local people to get on the property ladder or purchase their first home. By YHA targeting its resources at areas of highest need we continue to get greatest value for money for our investment and for customers. A further 17 affordable rent and 6 shared ownership homes will be acquired during 2017/18 to complete this scheme.

8

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

YHA have also entered into a contract for the design and build of 12 properties at Sherriff Hutton and completion is expected by April 2018.

Sherriff Hutton AffordableRent

SharedOwnership

TotalUnits

2 Bedroom 4 2 6

3 Bedroom 2 4 6

2.5.2 Existing Assets

YHA’s Asset Management Strategy incorporates the following objectives:

- Strengthening the Association’s Business and Financial Planning processes by annually updating our 30 year investment plan, and the more detailed 5 year planned investment programme. This will enable the Business Plan to confidently support the development of more new homes when the external environment is right, and the protection of existing homes.

- Maintaining 100% stock condition surveys of the Association’s stock on a 5 year rolling programme to identify properties which need further investment to maintain them into the longer term. This will not just look at the physical investment requirements, but will also assess the social and environmental value of our assets.

- Delivering an annual planned investment programme, based on sound asset data and knowledge, and prepared with tenant involvement. This programme will ensure all YHA’s properties continue to meet the Decent Homes Standard.

- Interrogating our planned investment programmes to ensure they are effective in reducing demand for responsive repairs, and delivering greater value for money through joined up procurement between our planned investment and responsive maintenance programmes.

YHA’s stock condition database (Lifespan) provides essential information for reporting Decent Homes Standard requirements, energy ratings and for informing future investments. This means that YHA has a rich source of up to date property data.

YHA has an ongoing planned investment programme which is, among other things, designed to protect the value of the property.

The expenditure over the last 6 years has been as follows:

Year Annual Expenditure£’000

2016/17 4232015/16 5262014/15 4182013/14 4102012/13 3762011/12 321

9

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

Over the last few years the following investment works have been carried out:

- Installation of new kitchens;- Installation of new gas central heating;- Installation of new windows & doors;- Installation of new doors & frames;- Installation of new windows only ;- Installation of new Velux roof windows;- Installation of new bathrooms;- Installation of new gas central heating boilers;- Installation of new modern electric heating systems;- Installation of new fire alarms & emergency lighting systems;- Installation of new smoke alarms;- Electrical upgrades;- Extensive structural works;- Re-roofing works;- New driveways.

These planned works ensure that our existing homes remain in good condition, are in high demand, and cost less to maintain through day to day repairs.

Three properties were identified during 2014/15 as not representing VfM to our core business; two of these remain to be sold in 2017/18. The resulting proceeds will be applied to our development programme which offers better value for money for both existing and new customers.

Potential property impairment in 2016/17 has been considered from the following perspectives:

- Properties Identified for Sale;- Asset Management – Planned Investment Programme;- Indicative Evidence of Impairment Requirement;- Government Policy Changes;- General Core Housing Stock.

The conclusion was that none of these triggered the requirement to make any impairment charges against the Association’s housing stock in 2016/17.

In relation to the planned investment programme YHA continues to be part of a collaboration with a number of other smaller Housing Associations in the region who are seeking to jointly procure their planned investment programmes to achieve greater economies of scale and therefore reduce costs. We are working with Procurement for Housing to ensure that we can package the works in such a way as to attract the best possible prices.

YHA is a member of the Northern Housing Consortium and works with Procurement for Housing, both of which provide a procurement service that enables members to obtain professional advice, savings through joint buying, and procurement compliance. During the last year the following estimated savings were achieved:

- Assisted living – product £5,071- Heating systems £11,641

3. Our plans for 2017-18

Looking Ahead to 2017/18

A key focus for the Association’s VfM work in 2017/18 will be completing the process required to achieve a merger into a larger Group structure. Following a rigorous selection process, supported by external consultants, YHA’s Board has identified a preferred merger partner, North East based Karbon Homes. As a

10

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARDresult, the Association is currently in advanced discussions that would see YHA retain its identity as a subsidiary in the Karbon Group.

The primary aim of the merger is to generate greater efficiencies for the future, particularly through the buying-in of back office services from the Group; which will create efficiencies to protect the Association’s future in uncertain economic times. The efficiency savings generated from this move will be used to realise YHA’s ambition to develop more new affordable homes, protect its existing services to tenants, and investment in existing homes. In addition, Karbon Homes will invest 50, rising to 100 new homes per annum in the YHA area of operation which YHA will manage on their behalf.

However, there is much work to be done in 2017/18 to finalise this proposal. During the early part of the year, Heads of Terms will be negotiated and agreed with Karbon Homes. Following this, an outline Business Case will be developed to capture the scale of efficiencies achievable and produce a projected business plan to ensure that additional new development is achievable. Once both Boards are satisfied that there is a strong business case to proceed, consultation will take place over the summer with tenants, Local Authorities, lenders and other key stakeholders to obtain their views. At the same time, a formal due diligence process will take place by each party on the other. In autumn 2017, all of this information will be pulled together and if positive, the regulator will be notified of the proposal, with final approval sought from both Boards to proceed to legal completion.

Legal completion is expected to be achieved by the end of December 2017, with a ‘go live’ date of April 2018 for IT and Finance services to be moved across to the Group.

In looking back to how this fits with our VfM Strategy agreed by the Board in November 2014, this covered a 3 year period to November 2017. As such, 2017/18 will be the final year of delivery against our original VfM targets, after which it is expected that we will review our VfM Strategy as a subsidiary within a larger group structure.

We are still in the process of identifying the full anticipated future VfM efficiencies as a result of joining the Karbon Group, however the initial headline efficiencies anticipated are:

Action Anticipated VFM gain WhenNet efficiency savings from procuring back office services from the Group

£350k per annum From Yr 2, 2018/19

Reduction in procurement costs of major/cyclical works

10% or £60k per annum From Yr 3, 2019/20

Potential sharing of telephony services

£12k per annum From Yr 2, 2018/19

New affordable homes to be built 60 additional new affordable homes in next 5 years by YHA

From Yr 2, 2018/19

Particular areas of VfM focus were originally identified as set out below, with a summary on key activities planned during 2017/18:

1. VfM Culture

Aim – Promote and embed a culture of value for money and continuous improvement, integrating value for money principles into all the day to day activities of the organisation.

Objective – Ensure YHA’s budget setting and management processes are robust and challenging in terms of resource allocation decisions.

The Board have been actively involved in budget setting for 2017/18 and monitor progress against budget quarterly to ensure that efficiency savings identified are being achieved.

2. Financial Capacity

Aim – Maximise the resources available to meet future customer demand.

11

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARDObjective – Use YHA’s capacity for the delivery of further social housing. By utilising YHA’s borrowing capacity, increasing gearing and making use of unencumbered assets, YHA will aim to maximise delivery of new homes.

YHA has sufficient finance in place to complete all of its current developments in 2017/18. Beyond this, the Association will need to seek further borrowing to realise its ambition to continue to develop more new affordable homes. During 2017/18 the Association’s Treasury Strategy will be reviewed and Business Plan refreshed to enable the Association to proceed with its next tranche of borrowings.

3. Assets

Aim – Maximise the resources available to meet current customer requirements.

Objective – Actively manage YHA’s assets. Bring together YHA’s understanding of its stock condition and associated investment needs; maintenance costs; demand and the communities and markets it operates in; and return on assets in financial, social and environmental terms. Use this understanding to inform intelligent asset management that aims to improve returns and intelligent business decisions around YHA’s housing stock (i.e. hold, invest, dispose, convert), investing only where returns (financial, social and environmental) are clear.

2017/18 will see us complete option appraisals on assets that do not perform strongly, and seek to reach a decision to invest, remodel or dispose. Much of this work is already underway on our Supported Housing stock as future Government proposals to cap rents and service charges at Local Housing Allowance levels render the vast majority of YHA’s Supported Housing stock financially unviable. A number have been decommissioned by Local Authority partners, and are being sold on the open market.

4. Tenant Satisfaction

Aim – Wherever possible target resources to priorities that have been identified by customers and ensure improvement in services where customer feedback indicates concern with quality, cost or performance.

Objective – Maintain and improve upon YHA’s current performance on tenant satisfaction (median or upper quartile performance), particularly focussing on:

- Overall service provided by the landlord- Repairs and maintenance- Quality of the home- Neighbourhood- Value for money of rent and service charges

During 2017/18 there will be a number of specific tenant satisfaction exercises. A survey of tenants’ views of VfM from service charges will take place to influence and shape a wider review of service charged from 2018 onwards. A consultation around tenant involvement will also take place to explore how we can better engage our tenants in shaping services through the review of our Tenant Engagement Strategy. Finally, the Association recognised the importance of providing excellent Customer Service and as such has sought to be re-assessed again for the Customer Service Excellence (CSE) Award, and was delighted to have this confirmed in June 2017.

5. Performance

Aim – To perform at the sector benchmarks, or better for all areas of operation.

Objectives – Ensure YHA’s operational activities focus on income, and hence resource maximisation. Monitor YHA’s performance over time against the national benchmarks for smaller associations (through membership of the SPBM benchmarking club). Achieve targets for:

- Current and former tenant arrears and bad debts- Voids

12

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD- ASB- Repairs and maintenance- HR

The VfM Strategy was written prior to Government requirements to reduce rents by 1% per annum to 2020. As a result, the Board have already had to set appropriate and stretching efficiency targets to mitigate the loss of income that this has created. In 2017/18, further stretch targets have been set in key areas of operational performance, and are monitored by the Board quarterly.

6. Procurement

Aim – Ensure that value for money drives the organisation’s procurement processes.

Objective – Evidence that YHA’s procurement processes, as laid down in YHA’s Procurement Strategy, continue to drive value from YHA’s purchasing activities.

During 2017/18 we will start procuring some of our major works contracts in conjunction with two other smaller Housing Associations, in an attempt to achieve greater economies of scale. An organisation called Procurement for Housing is supporting this process to ensure that the procurement is undertaken in line with legislation and good practice, and that we achieve the greatest possible benefits from the way in which we package the works.

7. Operating Costs

Aim – Deliver value for money by operating at costs comparable with sector peers.

Objective – Ensure YHA’s cost base is not significantly misaligned with the rest of the sector, by working towards the Homes and Communities Agency’s Global Accounts performance, in relation to percentage of turnover allocated to:

- Management costs per unit- Maintenance costs per unit- Investment per unit- Operating surplus

The biggest area of work during 2017/18 is around YHA joining the larger Group structure of Karbon Homes. This is described in more detail at the start of this section. However, the primary aim of this move is to generate efficiencies that YHA can’t achieve as a small independent organisation operating on its own. This move is therefore a pivotal decision in our drive to achieve VfM for the organisation and therefore its customers.

8. VfM Self- Assessment

Aim – Meet regulatory requirements.

Objective – Produce a robust Value for Money Self- Assessment, published in YHA’s annual financial statements, and on YHA’s website.

This VfM Self -Assessment is written by YHA and owned by the YHA Board. However, we have also sought external advice of smaller Housing Association benchmarking organisation, Acuity, to ensure that it meets Regulatory requirements and follows best practice developed in the sector. Further comments and advice from Acuity are therefore contained in this VfM Statement.

Value for Money – the Regulators perspective

In 2016 the Homes and Communities Agency took the unprecedented step of writing to all Registered Housing Providers with over 1,000 homes in ownership, to set out its understanding of the organisation’s cost data, alongside some key contextual information it holds on each organisation based on its statistical

13

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARDreturns. Both the cost data and contextual information was presented alongside the upper, median and lower quartile results taken from the Global accounts 2015. The letter called upon organisations to understand their results and be able to explain any key variations in costs.

YHA did not receive one of these letters as the Association did, and still does, have just under 1,000 homes in ownership. However, we recognise the importance of understanding YHA’s cost data in this format and being able to explain this in the context of YHA’s contextual information.

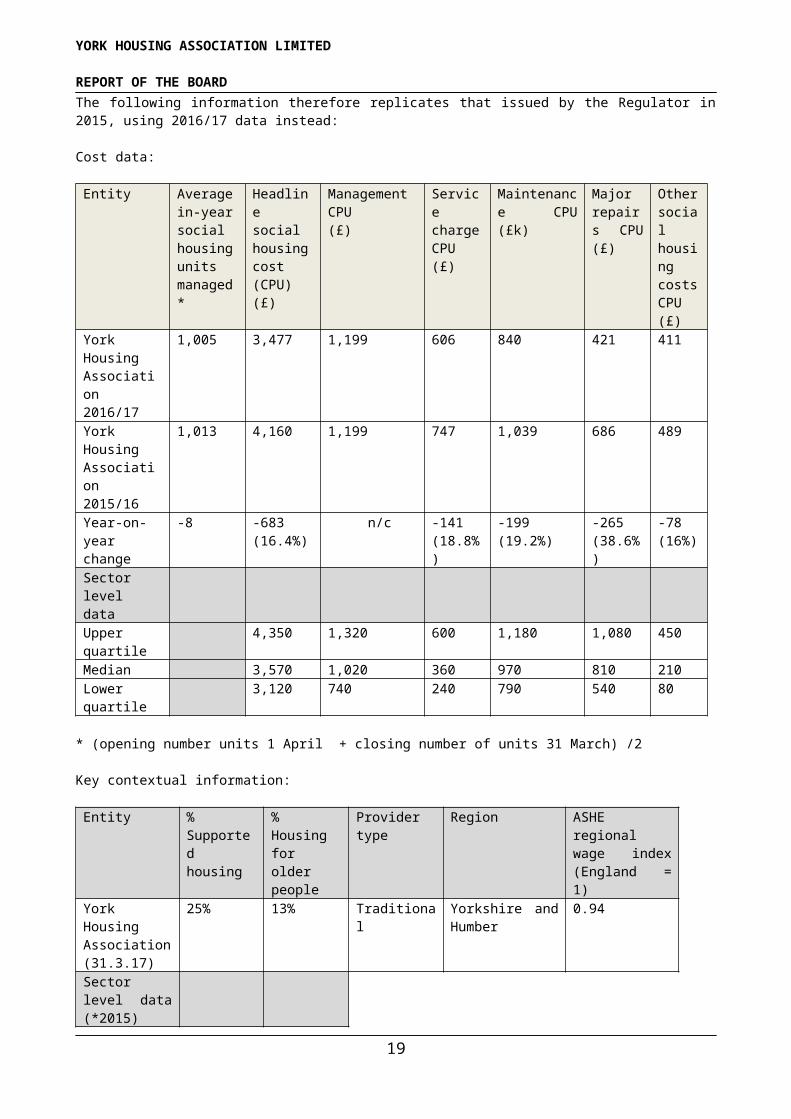

The following information therefore replicates that issued by the Regulator in 2015, using 2016/17 data instead:

Cost data:

Entity Average in-year social housing units managed*

Headline social housing cost (CPU) (£)

Management CPU(£)

Service charge CPU (£)

Maintenance CPU (£k)

Major repairs CPU (£)

Other social housing costs CPU (£)

York Housing Association 2016/17

1,005 3,477 1,199 606 840 421 411

York Housing Association 2015/16

1,013 4,160 1,199 747 1,039 686 489

Year-on-year change

-8 -683 (16.4%)

n/c -141 (18.8%)

-199 (19.2%)

-265 (38.6%)

-78 (16%)

Sector level dataUpper quartile

4,350 1,320 600 1,180 1,080 450

Median 3,570 1,020 360 970 810 210Lower quartile

3,120 740 240 790 540 80

* (opening number units 1 April + closing number of units 31 March) /2

Key contextual information:

Entity % Supported housing

% Housing for older people

Provider type Region ASHE regional wage index (England = 1)

York Housing Association(31.3.17)

25% 13% Traditional Yorkshire and Humber

0.94

Sector level data (*2015)Upper quartile 4% 15%

Median 1% 8%

Lower quartile 0% 4%

Source: HCA Global Accounts 2016: https://www.gov.uk/government/publications/2016-global-accounts-of-private-registered-providers

14

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

Context – YHA is a small specialist housing association with a long history of providing Supported housing and related Support services to the most vulnerable people in our area of operation. As a result, our stock profile of 26% Supported housing is well above the sector Upper quartile of 4%. Supported housing has significantly higher costs than General Needs properties and this has a detrimental impact on our costs per unit. Costs vary considerably depending on the type of accommodation and support offered, but in the majority of cases, our Supported housing will not be financially viable if the Government proceeds with plans to cap rents and service charges at Local Housing Allowance levels. As a result the Association is remodelling its Supported housing stock in conjunction with our Local Authority partners. Properties that are no longer fit for purpose are

being decommissioned, remodelled, or sold; whilst the costs of those homes which provide statutory housing provision for adult social care are being reviewed and commitments sought from Local Authority partners to ‘top up’ the future funding required. The result of this exercise is likely to be a reduction in our overall Supported housing and the associated exposure to this higher cost form of provision. This review and remodelling work is being overseen by a Board working group, and a specialist Supported housing consultant has been co-opted onto the Board to assist with the process.

In conclusion, YHA understands the reasons for its higher cost per unit being due to its high proportion of Supported housing. We are satisfied that the strategy outlined will protect specialist Supported housing for the most vulnerable customers, whilst reducing the financial risks to the Association overall.

In addition to Supported housing, YHA has 13% Housing for Older People again in the region of the Upper quartile of the sector as a whole. Additional costs associated with housing for older people are much more modest than for other supported housing, however they still contribute to our higher costs per unit. Whilst the priority is to remodel Supported housing in the first instance, we have already begun working with the Local Authority to decommission some sheltered housing and re-categorise as General Needs with floating support services where appropriate.

Asset and Liabilities Register

During 2016/17 the Association completed its asset and liabilities register and now maintains this as a live document. In terms of its use, this provides the Association with a comprehensive register of all the organisation’s assets and liabilities. It assists in the Board having an overview of all the assets at its disposal, and helps us to consider whether we are achieving best value from use of those assets.

In summary, at 31 March 2017 the Association has assets of 1,025 homes in ownership and management, of which 101 are managed on behalf of others. In addition it has 1 main office at its headquarters Alpha Court in York, and a further 10 small offices within schemes where staff can base themselves to meet tenants and deliver services. YHA also generates income through the provision of services to others, but which are also contractual commitments. These include a management agreement with Thirteen Group to manage some housing stock on their behalf; and an Agreement to maintain 600 homes on behalf of Broadacres.

In terms of liabilities, the Association has 5 loan agreements, against which 512 properties are secured. 10 Supported housing Management Agreements are in place with specialist managing agents, and one Service Level Agreement to provide Supported Housing services. Finally, there are 5 contracts in place for the delivery of goods and services.

The total of net assets at 31 March 2017 is £9,052k however, whilst they could not be realised, this summary is provided to demonstrate that the Association is clear about where its assets and liabilities sit and has a strategic overview of their use and importance

SurplusThe Association’s surplus for the financial year of £1,132k exceeded its target by £842k including property sales surplus of £111k. The annual surplus will be reinvested to support achievement of the Association’s Business Plan objectives.

AssuranceThe Association’s Board seeks and gains assurance of the robustness of this self-assessment of value for money through the Association’s Performance Management Framework, business planning processes, and

15

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARDinternal audit reviews. The Association continues to implement tenant scrutiny which will provide the Board with further assurance.

SharesAt 31 March 2017 there were 26 shareholders of the Association, each having one £1 share.

GovernanceThe Board has adopted and believes it fully complies with the National Housing Federation's Code of Governance (Promoting Board excellence for Housing Associations 2015).

Internal controls assuranceThe Board acknowledges its overall responsibility for establishing and maintaining the whole system of internal control and for reviewing its effectiveness.

The system of internal control is designed to manage, rather than eliminate, the risk of failure to achieve business objectives, and to provide reasonable, and not absolute, assurance against material misstatement or loss.

The process for identifying, evaluating and managing the significant risks faced by the Association is ongoing and has been in place throughout the year commencing 1 April 2016 up to the date of approval of the report and financial statements.

Key elements of the control framework include:

- Board approved terms of reference and delegated authorities for Audit and HR & Governance Committees;

- clearly defined management responsibilities for the identification, evaluation and control of significant risks;

- robust strategic and business planning processes, with detailed financial budgets and forecasts;- formal recruitment, retention, training and development policies for all staff;- established authorisation and appraisal procedures for all significant new initiatives and

commitments;- regular reporting on key business objectives, targets and outcomes;- Board approved whistle-blowing and anti-fraud and bribery policies;- Audit Committee regularly reporting to the Board on Risk Management controls and mitigations;- Stress testing to understand potential financial resilience to multiple adverse events.

The Board cannot delegate ultimate responsibility for the system of internal control, but it can, and has, delegated authority to the Audit Committee to regularly review the effectiveness of the system of internal control. The Board receives regular reports from the Audit Committee together with minutes of Audit Committee Meetings.

The Board has received the Chief Executive's annual review of the effectiveness of the system of internal control for the Association. The Audit Committee has received the annual report of the Internal Auditor, and has reported its findings to the Board.

Going concernAfter making enquiries, the Board has a reasonable expectation that the Association has adequate resources to continue in operational existence for the foreseeable future, being a period of twelve months after the date on which the report and financial statements are signed. For this reason, it continues to adopt the going concern basis in the financial statements.

Annual General MeetingThe annual general meeting will be held on 7 September 2017.

Grenfell Tower

16

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARDIn June 2017 a terrible fire destroyed Grenfell Tower, a social housing high rise tower block in London, resulting in multiple fatalities. In line with all social housing providers, YHA has since reviewed its Fire Risk Assessment (FRA) procedures and management arrangements across its housing stock, including with the Fire Service, and awareness raising with tenants.

YHA has no high rise accommodation of six stories or more, and no properties clad in the material now understood to have contributed to the rapid spread of fire at Grenfell. However, YHA has adopted a sharpened focus on Fire Risk and also wider Health and Safety compliance areas to ensure our tenants and homes are safe. Internal Audit now undertake a twice yearly rolling compliance review which includes an audit that FRAs are up to date and actions identified from them are being carried out.

BoardThe members of the Board who served during the year were:

- Kevin McAleese – Chair from 11/09/2014 (left 25/04/2016)- Janet Whipps – Deputy Chair from 21/05/2015 (Chair of the Board from 19/05/2016)- Juliette Clark – New Board Co-Optee Jan 2017- Pat Southgate – New Board Co-Optee Feb 2017 – Board Member March 2017- Mike Leonard – Deputy Chair of Audit Committee- Pat Walton- Sue Walters Thompson- Kelly Shaw – Chair of HR & Governance Committee (left April 2017)- Michael Newbury – Chair of Audit Committee and Deputy Chair- Alison Rusdale- Ian Simpson – Chair of HR Governance Committee (May 2017)- Mike Wills

Executive Directors

- Julia Histon – Chief Executive- Derrick Palmer – Resources Director- Kate Spencer – Operations Director

Governance and Financial ViabilityThe Board confirms that the Association complies with the Homes & Communities Agency’s Governance and Financial Viability Standard.

Merger CodeThe Board adopted the NHF Merger Code on 18 February 2016 and is currently in advanced discussions that would see YHA retain its identity as a subsidiary in the Karbon Group (see page 5).

Disclosure of Information to auditorsAt the date of making this report each of the Association's Board members, as set out above, confirm the following:

- So far as each Board member is aware, there is no relevant information needed by the Association's auditors in connection with preparing their report of which the Association's auditors are unaware.

- Each Board member has taken all the steps that they ought to have taken as a Board member in order to make themselves aware of any relevant information needed by the Association's auditors in connection with preparing their report and to establish that the Association's auditors are aware of that information.

AuditorsThe auditors, Beever and Struthers, are willing to remain in office and a resolution to re-appoint them as auditors to the Group was approved by the Board on 7 September 2017. During the forthcoming year, a procurement exercise will be undertaken to appoint external auditors for the Karbon Homes Group. If the merger proceeds this procurement exercise will include York Housing Association. Beever and Struthers have stated that they will resign as external auditors if required to do so.

17

YORK HOUSING ASSOCIATION LIMITED

REPORT OF THE BOARD

Approval of the Report of the BoardThe Report of the Board was approved on 7 September 2017 and signed on its behalf by:

……………………………..Janet WhippsChair of York Housing Association Limited

18

INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS OF YORK HOUSING ASSOCIATION LIMITED

We have audited the financial statements of York Housing Association Limited for the year ended 31 March 2017 which comprise the Statement of Comprehensive Income, Statement of Financial Position, Statement of Changes in Reserves, Statement of Cash Flows and the related notes. The financial reporting framework that has been applied in their preparation is applicable law and United Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting Practice) including FRS 102 “The Financial Reporting Standard applicable in the UK and Republic of Ireland”.

This report is made solely to the Association’s members, as a body, in accordance with Section 87(2) of the Co-operative and Community Benefit Societies Act 2014. Our audit work has been undertaken so that we might state to the Association’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Association and the Association’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective Responsibilities of the Board and the auditor

As explained more fully in the Statement of Board’s Responsibilities set out on page 2, the Board is responsible for the preparation of the financial statements which give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Financial Reporting Council’s (FRC’s) Ethical Standards for Auditors.

Scope of the audit of the financial statements

A description of the scope of an audit of financial statements is provided on the FRC’s website at www.frc.org.uk/auditscopeukprivate.

Opinion on financial statements

In our opinion the financial statements:

give a true and fair view of the state of the Association’s affairs as at 31 March 2017 and of its income and expenditure for the year then ended; and

have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice; and

have been prepared in accordance with the requirements of the Co-operative and Community Benefit Societies Act 2014, the Housing and Regeneration Act 2008 and the Accounting Direction for Private Registered Providers of Social Housing 2015.

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Co-operative and Community Benefit Societies Act 2014 require us to report to you if, in our opinion:

a satisfactory system of control over transactions has not been maintained; or the Association has not kept proper accounting records; or the financial statements are not in agreement with the books of account; or we have not received all the information and explanations we need for our audit.

Beever and StruthersStatutory AuditorSt George's House215-219 Chester RoadManchester M15 4JE

19

YORK HOUSING ASSOCIATION LIMITED

STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 MARCH 2017

Notes 2017 2016£’000 £'000

Turnover 2 7,189 8,434

Cost of sales 2 (310) (609)

Operating expenditure 2 (5,076 ) (5,522 )

Operating surplus 2 1,803 2,303

Gain on disposal of housing properties 12 111 70

Interest receivable and similar income 4 21 18

Interest payable and similar charges 5 (803 ) (845 )

Surplus before taxation 1,132 1,546

Taxation - -

Surplus for the year 1,132 1,546

Total comprehensive income for the year 1,132 1,546

All of the above results derive from the continuing operations of the Association.

The notes on pages 23 to 45 form an integral part of these financial statements.

The financial statements on pages 19 to 45 were approved and authorised for issue by the Board on 7 September 2017 and were signed on its behalf by:

…………………………………….. ………………………………..……..Janet Whipps - Chair xxxxxx - Board Member

……………………………………… ……………………………………....xxxxxx - Board Member Julia Histon - Chief Executive and Secretary

20

YORK HOUSING ASSOCIATION LIMITED

STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH 2017

Notes 2017 2016£’000 £'000

Tangible fixed assetsHousing properties 12 43,190 43,720Other tangible fixed assets 13 1,047 1,143

44,237 44,863 Current assetsProperties held for sale 14 810 816Stock 15 5 5Trade and other debtors 16 501 509Investments 17 3,020 2,966Cash and cash equivalents 18 1,760 1,549

6,096 5,845 Less Creditors: Amounts falling due within one year 19 (2,133 ) (2,786 )

Net current assets 3,963 3,057

Total assets less current liabilities 48,200 47,922

Creditors: Amounts falling due after more than one year 20 (39,003) (39,877)

Provisions for liabilities 23 (145 ) (125 )

Total net assets 9,052 7,920

ReservesIncome and expenditure reserve 9,052 7,920

The notes on pages 23 to 45 form an integral part of these financial statements.

The financial statements on pages 19 to 45 were approved and authorised for issue by the Board on 7 September 2017 and were signed on its behalf by:

…………………………………….. ………………………………..……..Janet Whipps - Chair xxxxxx - Board Member

……………………………………… ……………………………………....xxxxxx - Board Member Julia Histon - Chief Executive and Secretary

21

YORK HOUSING ASSOCIATION LIMITED

STATEMENT OF CHANGES IN RESERVES FOR THE YEAR ENDED 31 MARCH 2017

Income and expenditure

reserve£'000

Balance at 1 April 2015 6,374

Total comprehensive income for the year 1,546

Balance at 31 March 2016 7,920

Total comprehensive income for the year 1,132

Balance at 31 March 2017 9,052

The notes on pages 23 to 45 form an integral part of these financial statements.

22

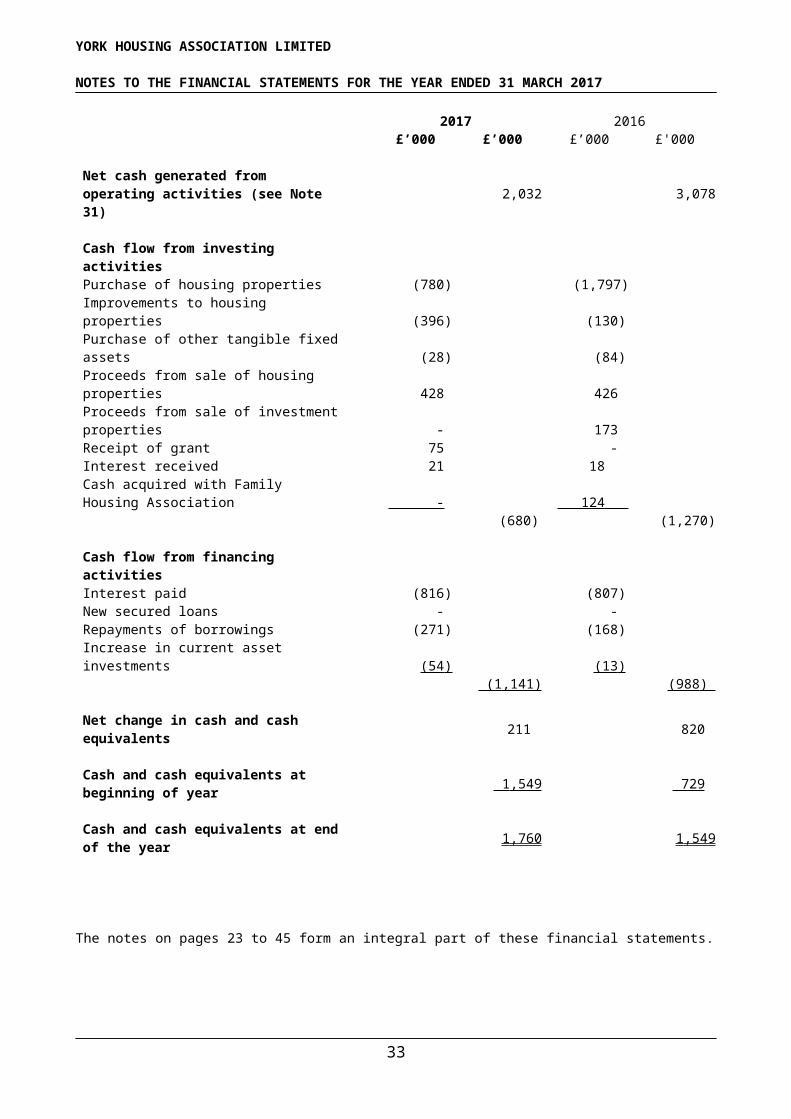

YORK HOUSING ASSOCIATION LIMITED

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017

2017 2016£’000 £’000 £’000 £'000

Net cash generated from operating activities (see Note 31) 2,032 3,078

Cash flow from investing activitiesPurchase of housing properties (780) (1,797)Improvements to housing properties (396) (130)Purchase of other tangible fixed assets (28) (84)Proceeds from sale of housing properties 428 426Proceeds from sale of investment properties - 173Receipt of grant 75 -Interest received 21 18 Cash acquired with Family Housing Association - 124

(680) (1,270)

Cash flow from financing activitiesInterest paid (816) (807)New secured loans - -Repayments of borrowings (271) (168)Increase in current asset investments (54 ) (13 )

(1,141 ) (988 )

Net change in cash and cash equivalents 211 820

Cash and cash equivalents at beginning of year 1,549 729

Cash and cash equivalents at end of the year 1,760 1,549

The notes on pages 23 to 45 form an integral part of these financial statements.

23

YORK HOUSING ASSOCIATION LIMITED

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017

1. Principal Accounting Policies

a) Legal statusThe Association is incorporated in England under the Co-operative and Community Benefit Societies Act 2014 and is registered with the Homes & Communities Agency as a Private Registered Provider of Social Housing.

The registered office is 2 Alpha Court, Monks Cross Drive, Huntington, York, YO32 9WN.

b) Basis of accounting The financial statements have been prepared in accordance with applicable United Kingdom Generally Accepted Accounting Practice (UK GAAP) and the Statement of Recommended Practice for registered housing providers: Housing SORP 2014.

The financial statements comply with the Co-operative and Community Benefit Societies Act 2014, the Housing and Regeneration Act 2008 and the Accounting Direction for Private Registered Providers of Social Housing 2015. The accounts are prepared on the historical cost basis of accounting and are presented in £ sterling (rounded to the nearest £’000).

The financial statements have been prepared in compliance with FRS 102. The Association meets the definition of a public benefit entity (PBE).

c) Going concernThe Association’s financial statements have been prepared on a going concern basis which assumes an ability to continue operating for the foreseeable future.

Following the Government’s announcements in July 2015 impacting on the future income of the Association a reassessment was carried out of the Association’s business plan as well as an assessment of imminent or likely future breach in borrowing covenants. No breaches are anticipated.

The Chancellor set out in the November 2015 Comprehensive Spending Review that all new tenancies would have their Housing Benefit capped to Local Housing Allowance from April 2018. The Association has adapted accordingly, and also sought assurances to ensure that where possible, Local Authority funding remains unaffected.

We consider it appropriate to continue to prepare the financial statements on a going concern basis.

d) Judgements and key sources of estimation uncertaintyThe preparation of the financial statements requires management to make judgements, estimates and assumptions that affect the amounts reported for assets and liabilities as at the balance sheet date and the amounts reported for revenues and expenses during the year. However, the nature of estimation means that actual outcomes could differ from those estimates. The following judgements (apart from those involving estimates) have had the most significant effect on amounts recognised in the financial statements.

i. Categorisation of assets The Association has undertaken a detailed review of the intended use of all housing properties. In determining the intended use, the Association has considered if the asset is held for social benefit or to earn commercial rentals. Student Accommodation is held as housing property assets, as the creation of YHA was for the initial purpose of creating accommodation for mature students with their families.

ii. Impairment A review has been undertaken as set out in note 1 l.

iii. Categorisation of debt The Association’s debt has been treated as “basic” in accordance with paragraphs 11.8 and 11.9 of FRS 102. The Association has some fixed rate loans which have a two-way break clause (i.e. in addition to compensation being payable by a borrower to a lender if a loan is prepaid where the prevailing fixed rate is lower than the existing loan’s fixed rate, compensation could be payable by the lender to the borrower in the event that a loan is prepaid and the prevailing fixed rate is higher than the existing loan’s fixed rate).

24

YORK HOUSING ASSOCIATION LIMITED

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017

The Financial Reporting Council (FRC) issued a statement on 2 June 2016 in respect of such loans with no prescriptive direction as to whether they should be classified as “basic” or “non-basic”. On the grounds that the Association believes the recognition of each debt liability at cost provides a more transparent and understandable position of the Association’s financial position and that each loan still satisfies the requirements of paragraphs 11.8 and 11.9 of FRS 102, the Association has retained its “basic” treatment of its debt following the FRC announcement.

iv. Provision for bad debts An estimate has been made regarding the potential for write off of bad debts relating to the sales ledger and to rent debts. Every effort is made to locate former tenants to seek payment of their debt.

e) Turnover and revenue recognitionTurnover comprises rental income, net of voids, including student accommodation, receivable in the year, income from shared ownership first tranche sales, sales of other properties developed for outright sale, other income included at the invoiced value (excluding VAT) of goods and services supplied in the year, amortised capital grant and revenue grants from local authorities and the Homes and Communities Agency, receivable in the year.

Rental income is recognised from the point when properties under development reach practical completion or otherwise become available for letting.

Income from first tranche sales and sales of properties built for sale is recognised at the point of legal completion of the sale.

f) Interest payableInterest payable is charged to the Statement of Comprehensive Income in the year.

g) Supporting people income and costsSupporting People contract income received from Administering Authorities is accounted for as Supporting People income in the Turnover as per note 2. The related support costs are matched against this income in the same note. Support charges included in the rent are included in the Statement of Comprehensive Income from social housing lettings note 3 and matched against the relevant costs.

h) Social Housing Grant (SHG) and Other Government GrantsWhere developments have been financed partly or wholly by social housing and other grants, the amount of the grant received has been included as deferred income and recognised in Turnover over the estimated useful life of the associated asset structure under the accruals model. SHG received for items of cost written off in the Statement of Comprehensive Income is included as part of Turnover.

SHG received in respect of revenue expenditure is credited to the Statement of Comprehensive Income in the same period as the expenditure to which it relates.

SHG is subordinated to the repayment of loans by agreement with the Homes and Communities Agency.

SHG must be recycled by the Association under certain conditions, if a property is sold, or if another relevant event takes place. In these cases, the SHG can be used for projects approved by the Homes and Communities Agency and the relevant Local Authority. However, SHG may have to be repaid if certain conditions are not met. If grant is not required to be recycled or repaid, any unamortised grant is recognised as Turnover. In certain circumstances, SHG may be repayable, and, in that event, is a subordinated unsecured repayable debt.

25

YORK HOUSING ASSOCIATION LIMITED

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017

i) Revenue and other grantsGrants received from non-government sources are recognised under the performance model. If there are no specific performance requirements the grants are recognised when received or receivable. Where grant is received with specific performance requirements it is recognised as a liability until the conditions are met and then it is recognised as Turnover.

Revenue grants are payable to the Association at the discretion of Local Authorities, the Department for Communities and Local Government or the Homes and Communities Agency. The grants are credited to the Statement of Comprehensive Income when the conditions are met for their recognition.

Grants are also made by Local Authorities and Health Authorities for special purposes, and where it relates to the acquisition or refurbishment of a property the grant has been deducted from the cost of the property. The grants are repayable in full following the sale of the property.

j) Service charges Service charge income and costs are recognised on an accruals basis. The Association operates fixed service charges on a scheme by scheme basis in full consultation with residents.

Where periodic expenditure is required a provision may be built up over the years, in consultation with the residents; until these costs are incurred this liability is held in the Statement of Financial Position within long term creditors.

k) Tangible fixed assets and depreciation

Housing propertiesHousing properties are stated at cost less accumulated depreciation, which includes the following:-

i) Cost of acquired land and buildings.ii) Development expenditure.

All invoices and architects certificates relating to capital expenditure incurred in the year at net value after retentions, are included in the accounts for the year, provided that the dates of issue or valuation are prior to the year end. Related mortgage advances receivable from lending authorities are also included.

Expenditure on schemes which are subsequently aborted is written off in the year in which it is recognised that the schemes will not be developed to completion.

Schemes are classified in the relevant note as being “complete” or “under construction”. Schemes are transferred to completed schemes on the relevant date, which is the date of issue of the certificate of practical completion under the building contract. Housing properties under construction are stated at cost and are not depreciated.

Works to existing propertiesWorks to existing properties which replace a component that has been treated separately for depreciation purposes, along with those works that result in an increase in net rental income over the lives of the properties, thereby enhancing the economic benefits of the assets, are capitalised as improvements.

Capitalisation of administration costs Administration costs relating to development activities are capitalised only to the extent that they are incremental to the development process and directly attributable to bringing the property into their intended use.

Shared ownership propertiesThe costs of shared ownership properties are split between current and fixed assets on the basis of the first tranche portion. The first tranche portion is accounted for as a current asset and the sale proceeds shown in turnover. The remaining element of the shared ownership property is accounted for

26

YORK HOUSING ASSOCIATION LIMITED

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017as a fixed asset and subsequent sales treated as sales of fixed assets.

Leasehold propertiesAlterations to leasehold properties are stated at cost less accumulated amortisation.

Other tangible fixed assetsOther tangible fixed assets are stated at cost less accumulated depreciation.

Depreciation

i) Freehold landThere is no depreciation on freehold land.

ii) Freehold housing propertiesProperties are depreciated over their expected economic lives in equal instalments. The depreciation is calculated on the cost of properties less cost of land and major components. Properties are grouped in accordance to their expected economic lives as follows:

Post-1919 houses with easy conversion at a minimum cost 100 years

Pre-1988 housing within City Centre location 100 years

Post-1988 single person housing except City Centre location 60 years

Post-1988 family housing and City Centre single person housing 100 years

Shared general needs, student housing and supported housing 30 years

Pre-1988 housing in Leeds 60 years

Shared housing in City Centre location with difficult conversion 30 years

Mix of self-contained and shared housing outside City Centre locationwith difficult conversion 40 years

Major components are treated as separable assets and depreciated over their expected economic lives, or the lives of the properties to which they relate, if shorter, in equal instalments.

The Association reviewed the useful economic lives (UELs) of its components and increased its estimate of the UELs of boilers and heating systems, kitchens, bathrooms and wiring. The impact of the change was a reduction in the annual depreciation charge of £202k.

The expected economic lives of each major component are as follows:

Roofs 50 years

Windows and external doors 30 years

Boilers and heating systems (previously 15 years) 23 years

Kitchens (previously 15 years) 20 years

Bathrooms (previously 20 years) 30 years

Ground works 100 years

Wiring (previously 30 years) 40 years

iii) Freehold office buildings

Freehold office buildings 100 years

27

YORK HOUSING ASSOCIATION LIMITED

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017

iv) Leasehold housing propertiesAlterations to leasehold housing properties are written off by way of amortisation over the period of the leases.

v) Other fixed assets

Office furniture and equipment 5 years

Furniture and equipment in dwellings 5 years

Computer equipment and software 4 years

Fire alarm upgrades 15 years

Depreciation is charged monthly from the month following acquisition until the point of disposal or full depreciation.

A de minimis threshold has been set of £500 for non-property assets.

l) ImpairmentHousing properties which are depreciated over a period, usually in excess of 50 years, are subject to an impairment review annually in accordance with FRS 102. Other assets are reviewed for impairment if there is an indication that impairment may have occurred e.g. when a decision is made to sell a property and a value is professionally assessed. Impairment is recognised where the carrying value exceeds the higher of its net realisable value or its value in use.

Where there is evidence of impairment, fixed assets are written down to their recoverable amount. Any such write down is charged to the Statement of Comprehensive Income.

The Association has undertaken an impairment review for the current year and considers that there have not been any triggers to warrant generating any impairment charges against its assets.

m) Properties held for saleFixed assets and associated liabilities are classified as held for sale when their carrying amount will be recovered principally through a sale transaction rather than continuing use and a sale is highly probable.

Assets designated as held for sale are held at the lower of carrying amount at designation and fair value less costs to sell.

Depreciation is not charged against property classified as held for sale.

n) Stocks of materialsStocks of materials are valued at the lower of cost and net realisable value, after making due allowance for obsolete and slow moving stock.

o) Operating leasesRentals paid under operating leases are charged to the Statement of Comprehensive Income on a straight line basis over the lease term.

p) Loan and Bond Finance - Issue Costs and PremiumsThese are amortised over the life of the related loan. Loans and bonds are stated in the Statement of Financial Position at the amount of the net proceeds after issue, plus increases to account for any subsequent amounts written off. Bond premiums are written back over the life of the product and are credited to the interest payable account. Where loans are redeemed during the year, any redemption penalty and any connected loan finance issue costs are recognised in the income and expenditure account in the year in which the redemption took place.

28

YORK HOUSING ASSOCIATION LIMITED

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2017

q) Recycled Capital Grant FundAs described in (h) above, Capital Grant (i.e. Social Housing Grant) can be recycled by Registered Providers after the sale of properties. The SHG is credited to a fund which appears as a creditor until spent. The fund is used for the provision of new Social Housing for rent and re-improvements to existing eligible housing stock.

r) Non-monetary government grantOn disposal assets for which non-monetary government grants are held as liabilities in the Statement of Financial Position, the unamortised amount in creditors is derecognised and recognised as income in the Statement of Comprehensive Income.

s) Pension costsThe Association participates in the Social Housing Pension Scheme (SHPS), a group scheme for housing associations operated by TPT Retirement Solutions. There is a defined benefit scheme, providing retirement benefits based on pensionable pay and a defined contribution scheme. The defined benefit scheme was closed to all future contributions from 1 April 2016. Future payments will be to a defined contribution scheme. Payments to the defined benefits scheme continue to be made in accordance with periodic valuations of consulting actuaries and are based on pension costs applicable across the various participating employers taken as a whole. Contributions payable under an agreement with SHPS to fund past deficits are recognised as a liability in the financial statements calculated by the repayments known, discounted to the net present value at the year ended using a market rate discount factor of 1.92% at 31 March 2015, 2.06% at 31 March 2016 and 1.33% at 31 March 2017. The unwinding of the discount is recognised as a finance cost in the Statement of Comprehensive Income in the period incurred.

Contributions made by the Association to the defined contribution scheme are recognised as a finance cost in the Statement of Comprehensive Income in the period incurred.

t) Holiday pay accrualA liability is recognised to the extent of any unused holiday pay entitlement which has accrued at the date of the Statement of Financial Position and carried forward to future periods. This is measured at the undiscounted salary cost of the future holiday entitlement so accrued at the date of the Statement of Financial Position.

u) Properties managed by agentsThe Association owns or leases properties which are managed by other agencies. The assets and associated liabilities are included in the financial statements.

Where the Association carries the majority of the financial risk, all the income and expenditure arising from the property is included in the Statement of Comprehensive Income.

Where the agency carries the majority of the financial risk, the Statement of Comprehensive Income includes only that income and expenditure which relates solely to the Association.

The financial statements do not include income and expenditure incurred by the agencies.