Embed Size (px)

Citation preview

Elasticity of Demand

Chapter 5

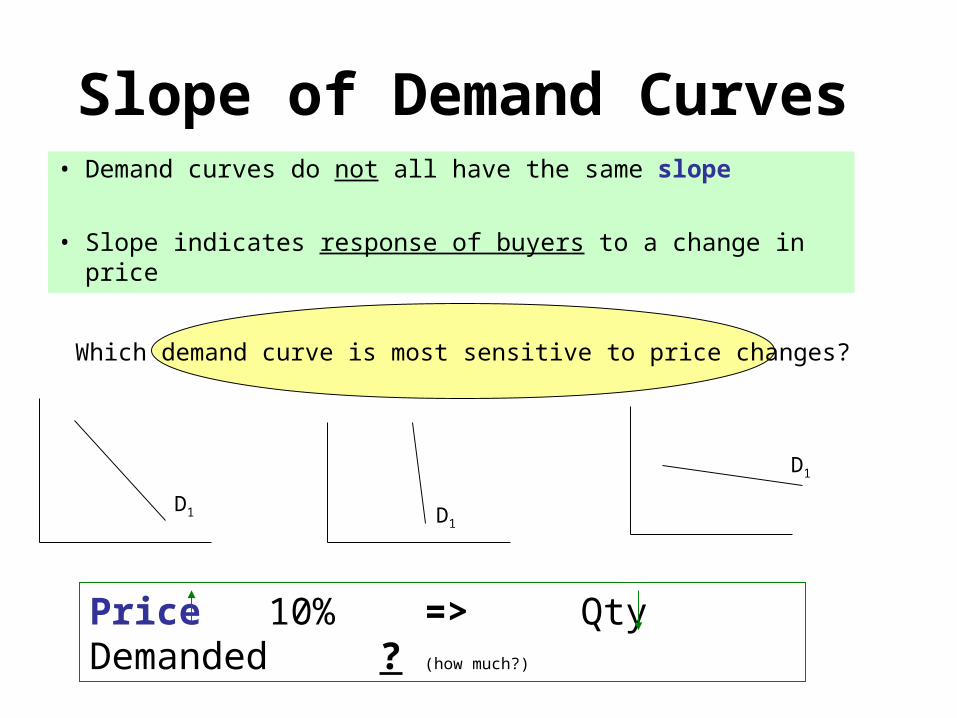

Slope of Demand Curves• Demand curves do not all have the same slope

• Slope indicates response of buyers to a change in price

D1

D1

D1

Price 10% => Qty Demanded ? (how much?)

Which demand curve is most sensitive to price changes?

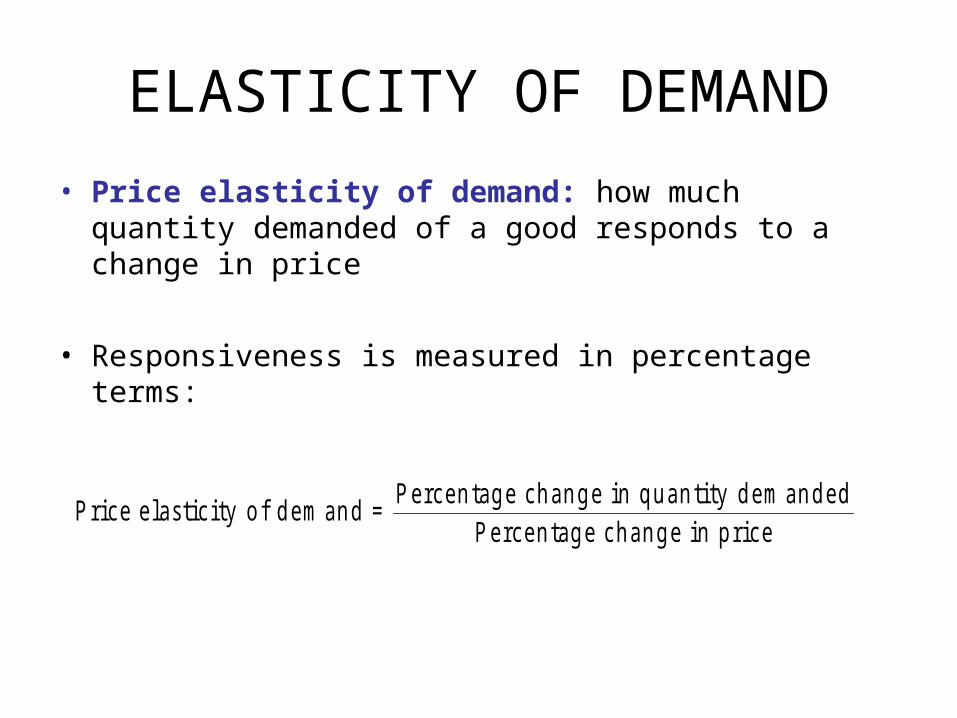

ELASTICITY OF DEMAND

• Price elasticity of demand: how much quantity demanded of a good responds to a change in price

• Responsiveness is measured in percentage terms:

P rice e las tic ity o f d em an d =P ercen tag e ch an g e in q u an tity d em an d ed

P ercen tag e ch an g e in p rice

Determinants of Elasticity of Demand

• Availability of Close Substitutes

• Necessities versus Luxuries

• Proportion of Income

• Time Horizon

Demand is more elastic:

• the larger the number of close substitutes

• if the good is a luxury

• Good is a larger percent of budget

• the longer the time period

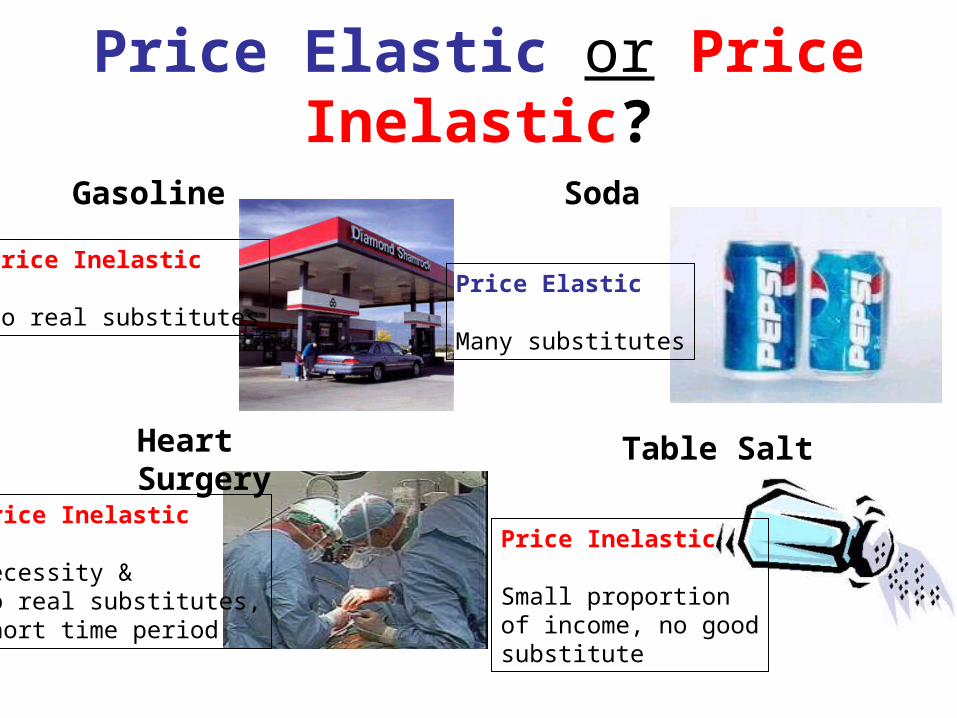

Price Elastic or Price Inelastic?

Soda

Heart Surgery Table Salt

Gasoline

Price Inelastic

No real substitutes

Price Inelastic

Necessity &No real substitutes,Short time period

Price Elastic

Many substitutes

Price Inelastic

Small proportionof income, no goodsubstitute

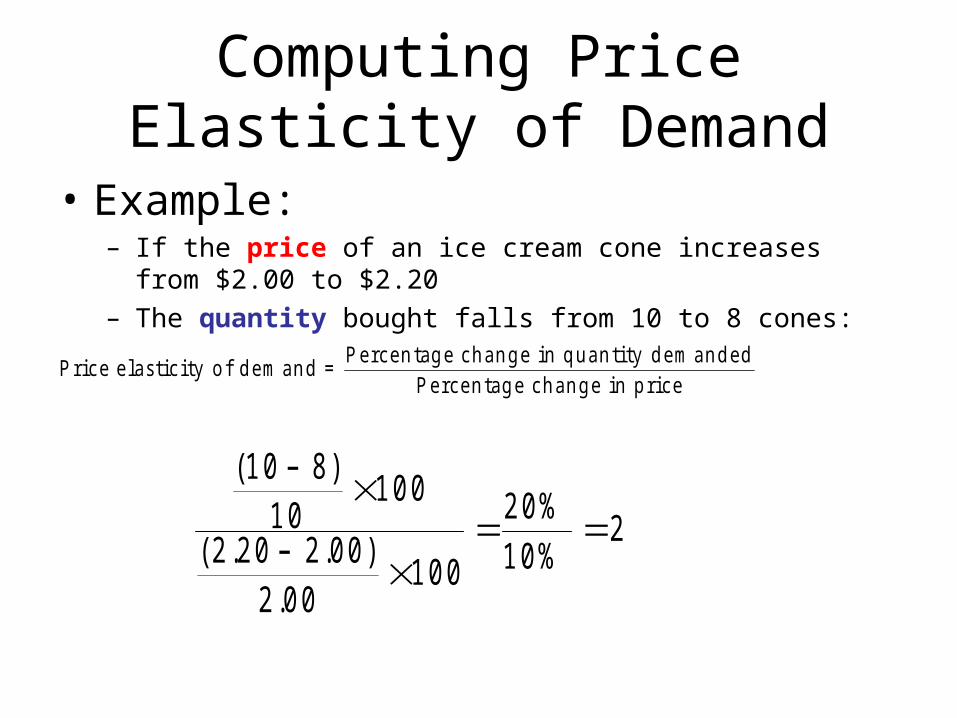

Computing Price Elasticity of Demand

• Example: – If the price of an ice cream cone increases from $2.00 to $2.20 – The quantity bought falls from 10 to 8 cones:

( )

( . . ).

1 0 81 0

1 0 0

2 2 0 2 0 02 0 0

1 0 0

2 0 %

1 0 %2

P rice e las tic ity o f d em an d =P ercen tag e ch an g e in q u an tity d em an d ed

P ercen tag e ch an g e in p rice

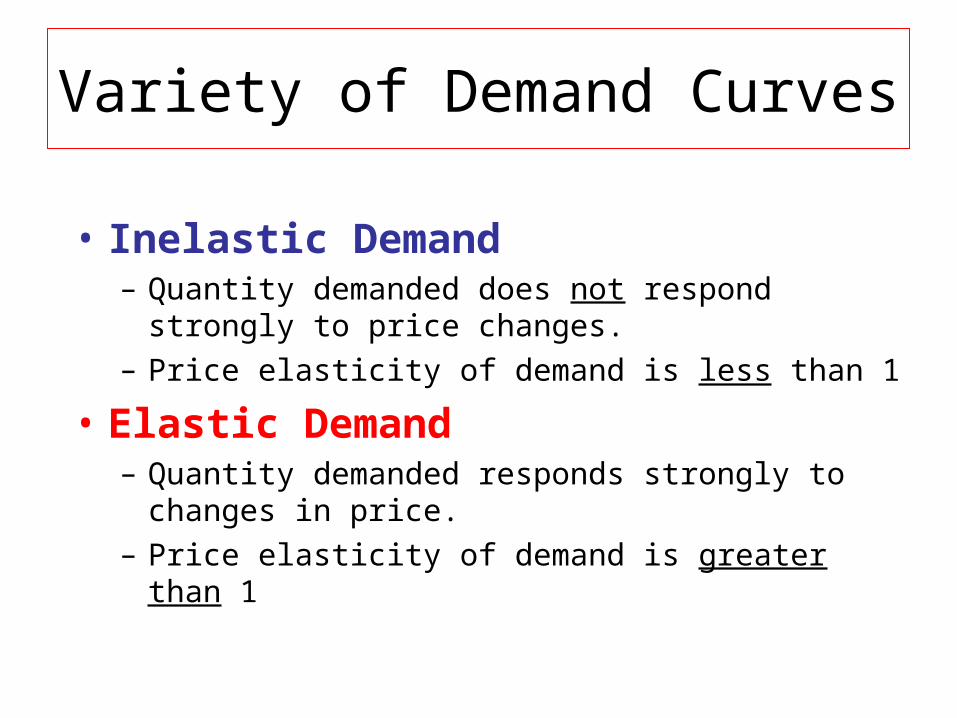

Variety of Demand Curves

• Inelastic Demand– Quantity demanded does not respond strongly to

price changes.– Price elasticity of demand is less than 1

• Elastic Demand– Quantity demanded responds strongly to changes in

price.– Price elasticity of demand is greater than 1

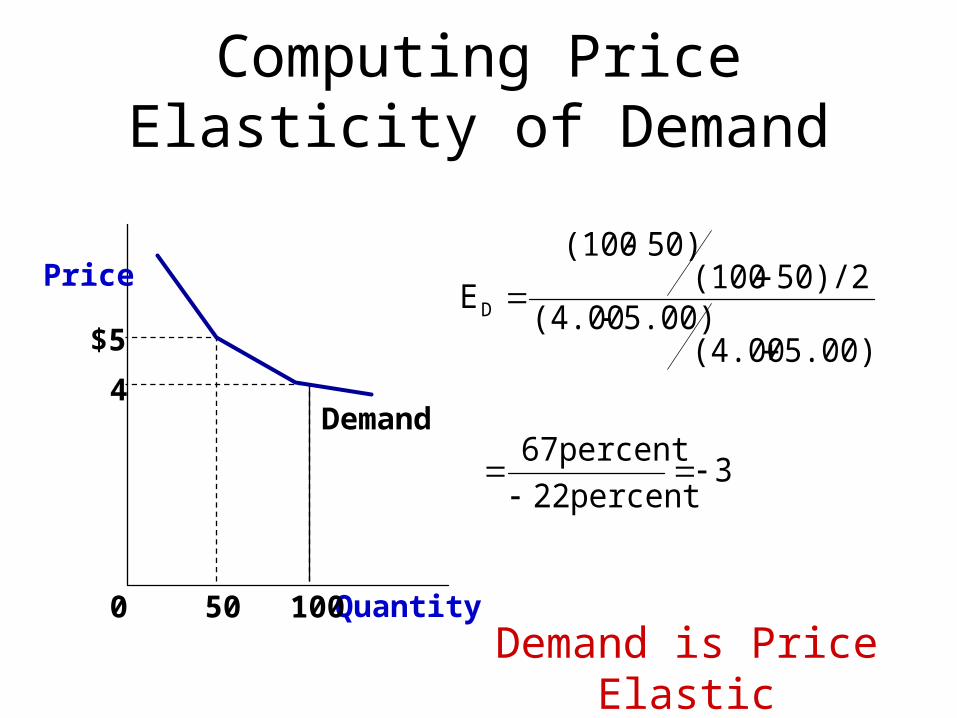

Computing Price Elasticity of Demand

Demand is Price Elastic or Greater than 1---(use absolute values)

$5

4Demand

Quantity1000 50

3percent 22

percent 67

5.00)/2(4.005.00)(4.00

50)/2(10050)(100

ED

Price

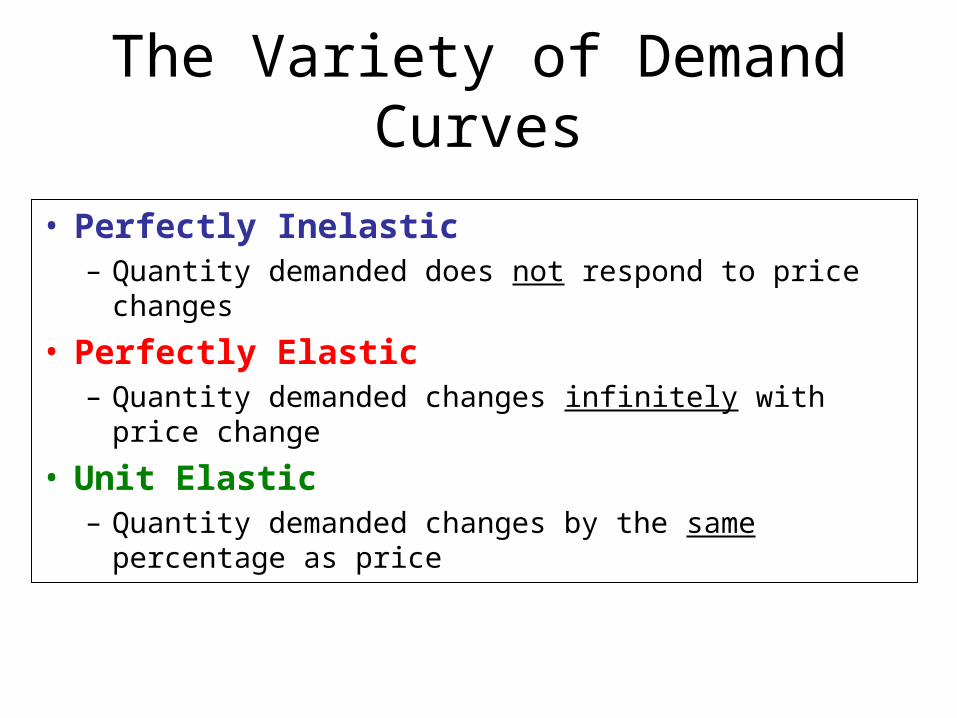

The Variety of Demand Curves

• Perfectly Inelastic– Quantity demanded does not respond to price changes

• Perfectly Elastic– Quantity demanded changes infinitely with price change

• Unit Elastic– Quantity demanded changes by the same percentage

as price

The Variety of Demand Curves

• Price elasticity of demand is closely related to the slope of the demand curve.

• But it is not the same thing as the slope!

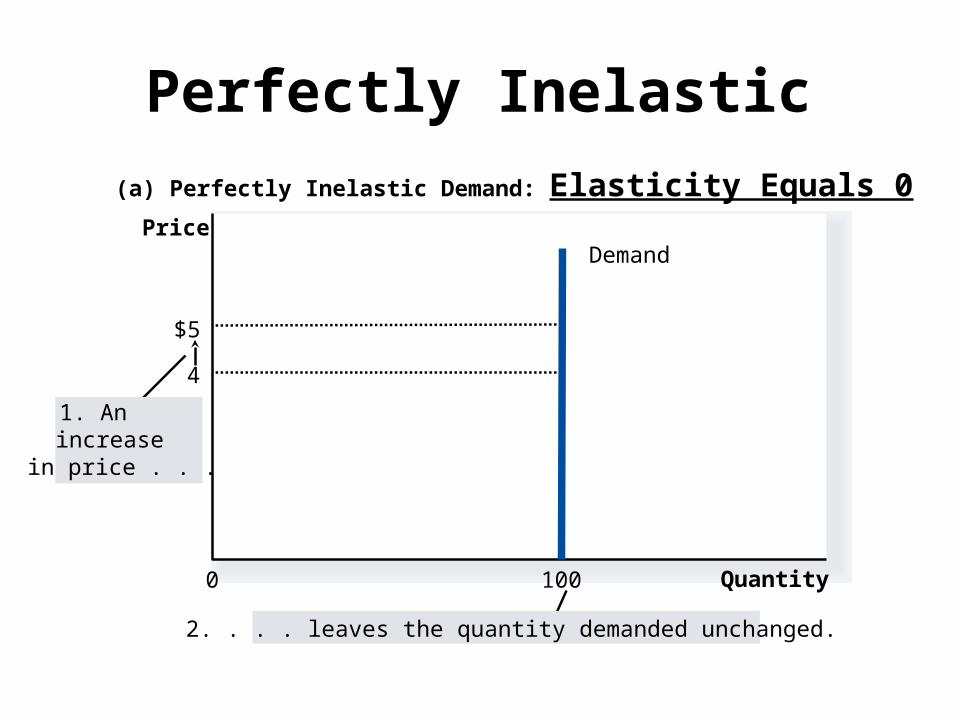

Perfectly Inelastic

(a) Perfectly Inelastic Demand: Elasticity Equals 0

$5

4

Quantity

Demand

1000

1. Anincreasein price . . .

2. . . . leaves the quantity demanded unchanged.

Price

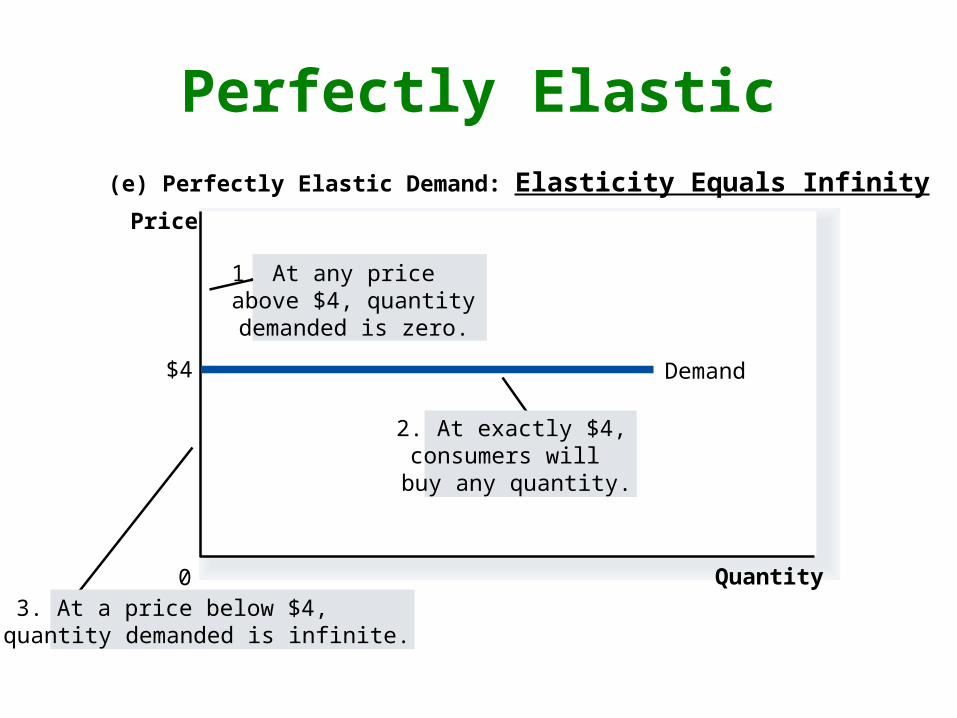

Perfectly Elastic(e) Perfectly Elastic Demand: Elasticity Equals Infinity

Quantity0

Price

$4 Demand

2. At exactly $4,consumers willbuy any quantity.

1. At any priceabove $4, quantitydemanded is zero.

3. At a price below $4,quantity demanded is infinite.

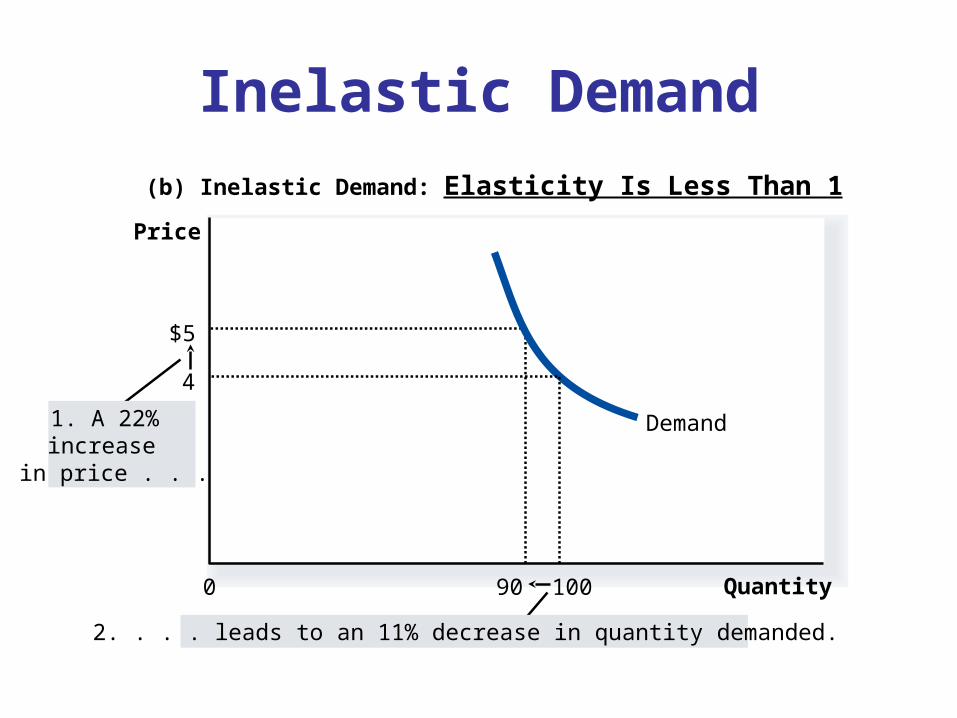

Inelastic Demand

(b) Inelastic Demand: Elasticity Is Less Than 1

Quantity0

$5

90

Demand1. A 22%increasein price . . .

Price

2. . . . leads to an 11% decrease in quantity demanded.

4

100

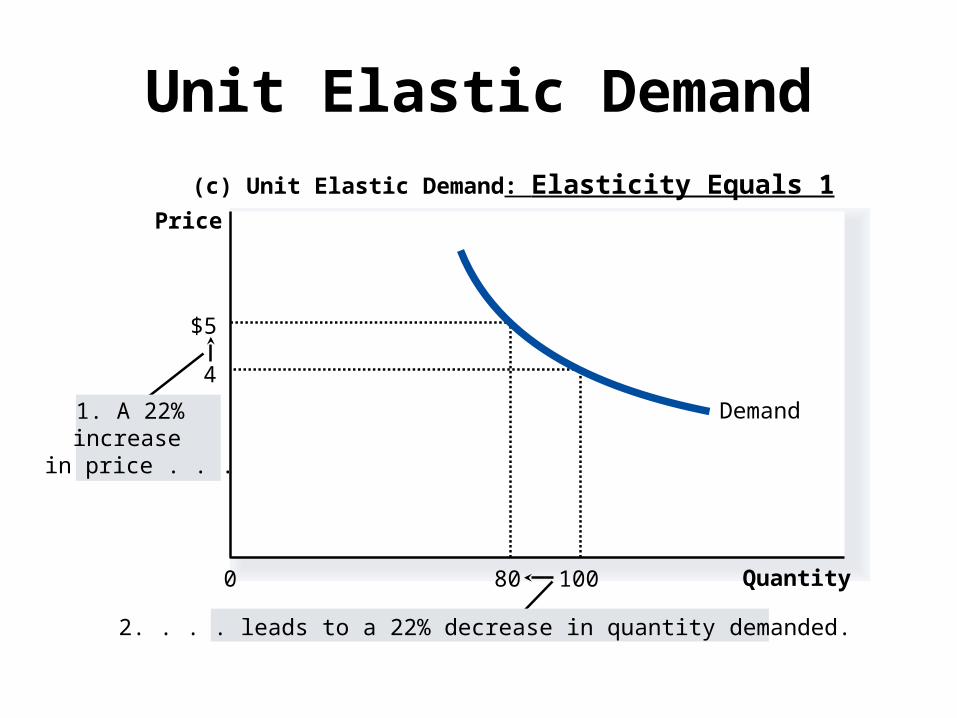

Unit Elastic Demand

2. . . . leads to a 22% decrease in quantity demanded.

(c) Unit Elastic Demand: Elasticity Equals 1

Quantity

4

1000

Price

$5

80

1. A 22%increasein price . . .

Demand

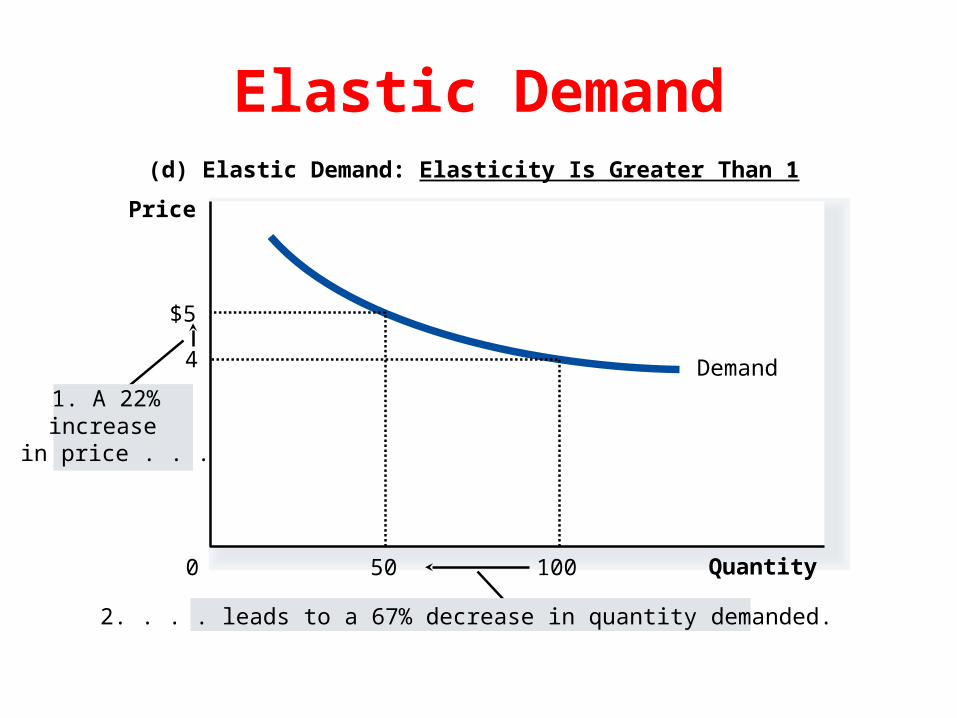

Elastic Demand(d) Elastic Demand: Elasticity Is Greater Than 1

Demand

Quantity

4

1000

Price

$5

50

1. A 22%increasein price . . .

2. . . . leads to a 67% decrease in quantity demanded.

Elasticity & Total Revenue

Chapter 5

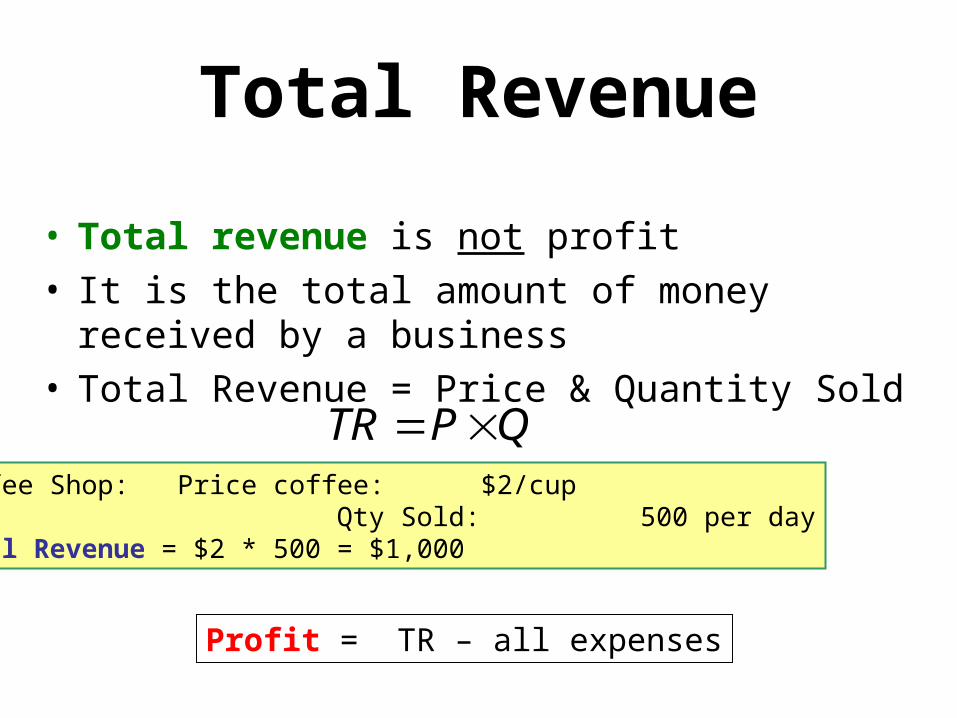

Total Revenue

• Total revenue is not profit• It is the total amount of money received by a

business• Total Revenue = Price & Quantity Sold

QPTR Coffee Shop: Price coffee: $2/cup Qty Sold: 500 per dayTotal Revenue = $2 * 500 = $1,000

Profit = TR – all expenses

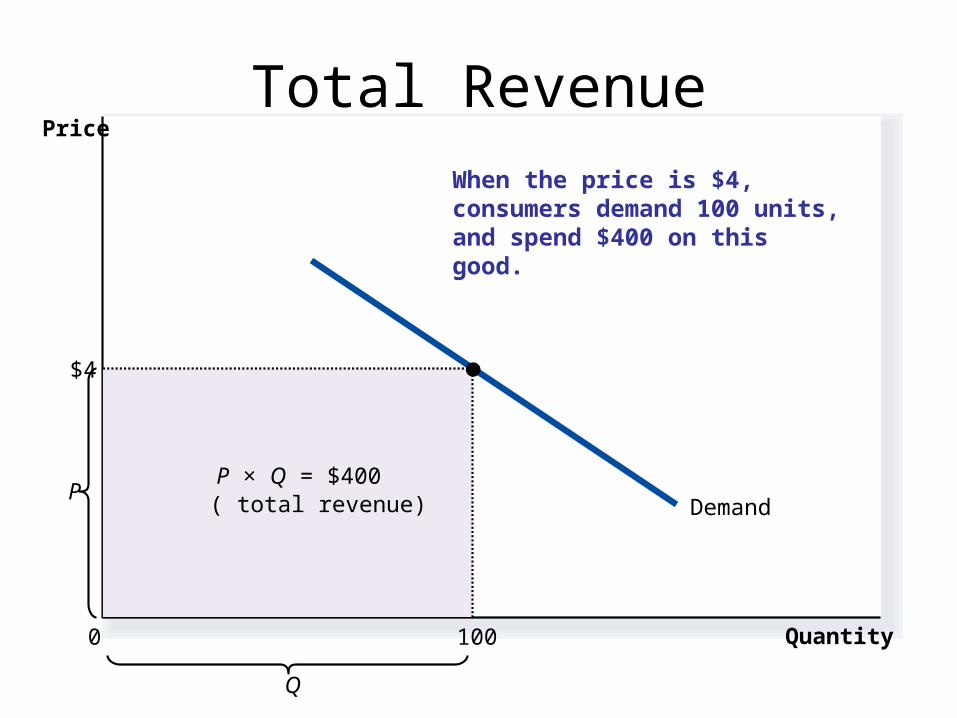

Total Revenue

Demand

Quantity

Q

P

0

Price

P × Q = $400( total revenue)

$4

100

When the price is $4, consumers demand 100 units, and spend $400 on this good.

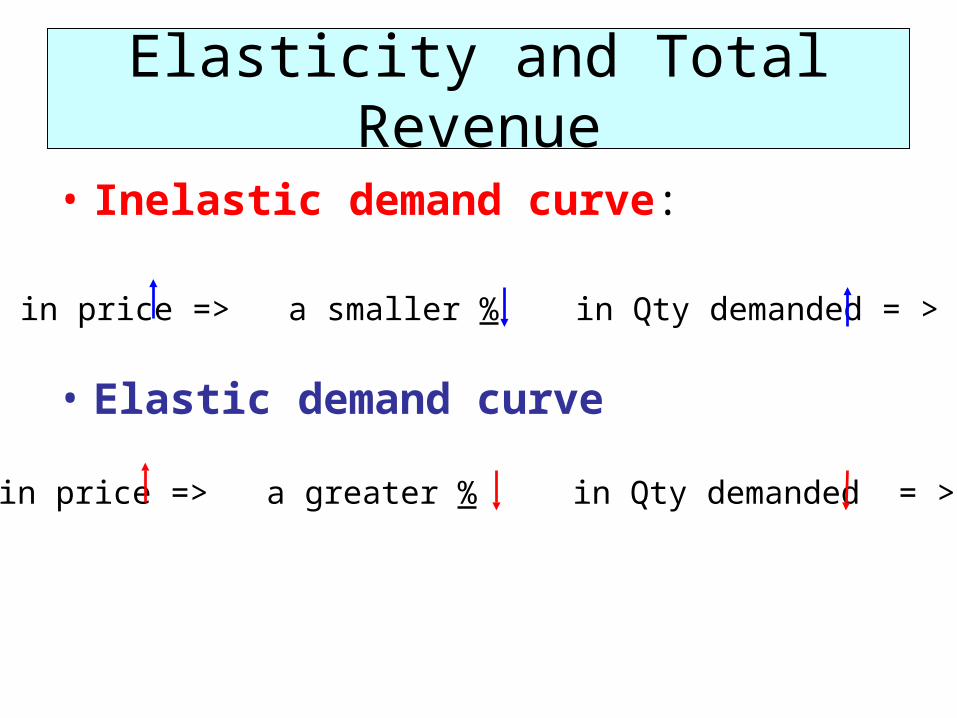

Elasticity and Total Revenue

• Inelastic demand curve:

• Elastic demand curve

in price => a smaller % in Qty demanded = > TR

in price => a greater % in Qty demanded = > TR

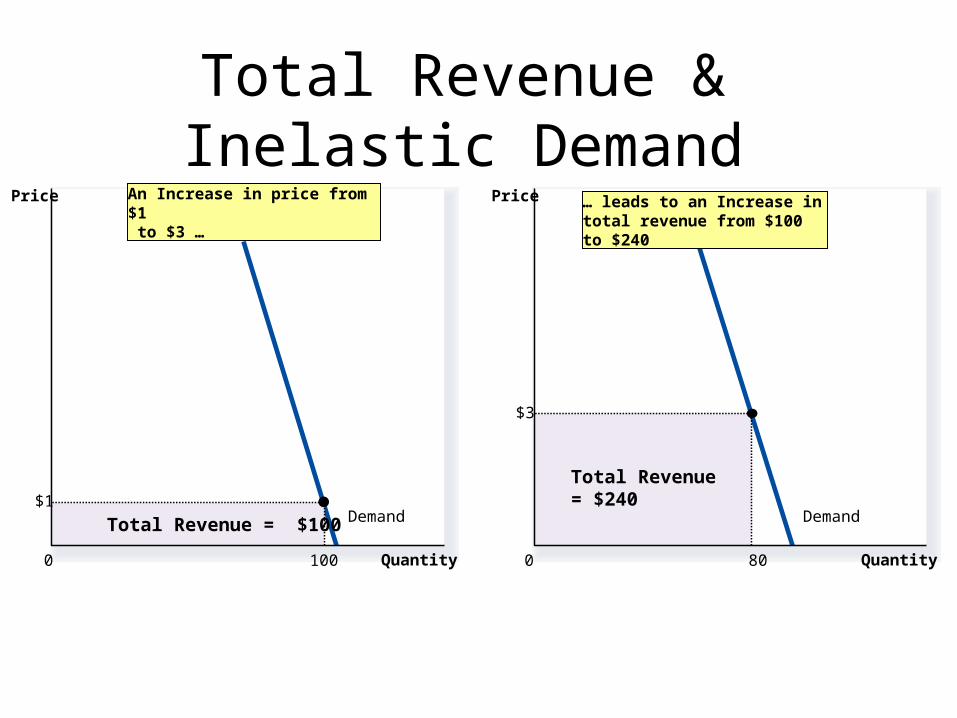

Total Revenue & Inelastic Demand

Demand

Quantity0

Price

Total Revenue = $100

Quantity0

Price

Total Revenue = $240

Demand$1

100

$3

80

An Increase in price from $1 to $3 …

… leads to an Increase in total revenue from $100 to $240

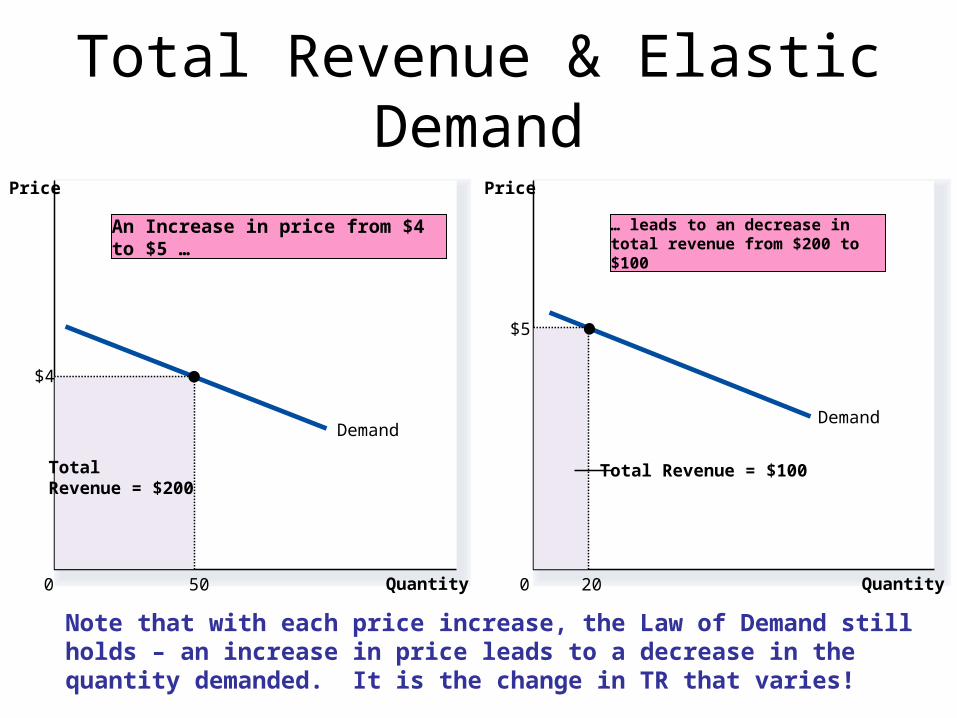

Total Revenue & Elastic Demand

Demand

Quantity0

Price

TotalRevenue = $200

$4

50

Demand

Quantity0

Price

Total Revenue = $100

$5

20

An Increase in price from $4 to $5 … … leads to an decrease in total revenue from $200 to $100

Note that with each price increase, the Law of Demand still holds – an increase in price leads to a decrease in the quantity demanded. It is the change in TR that varies!

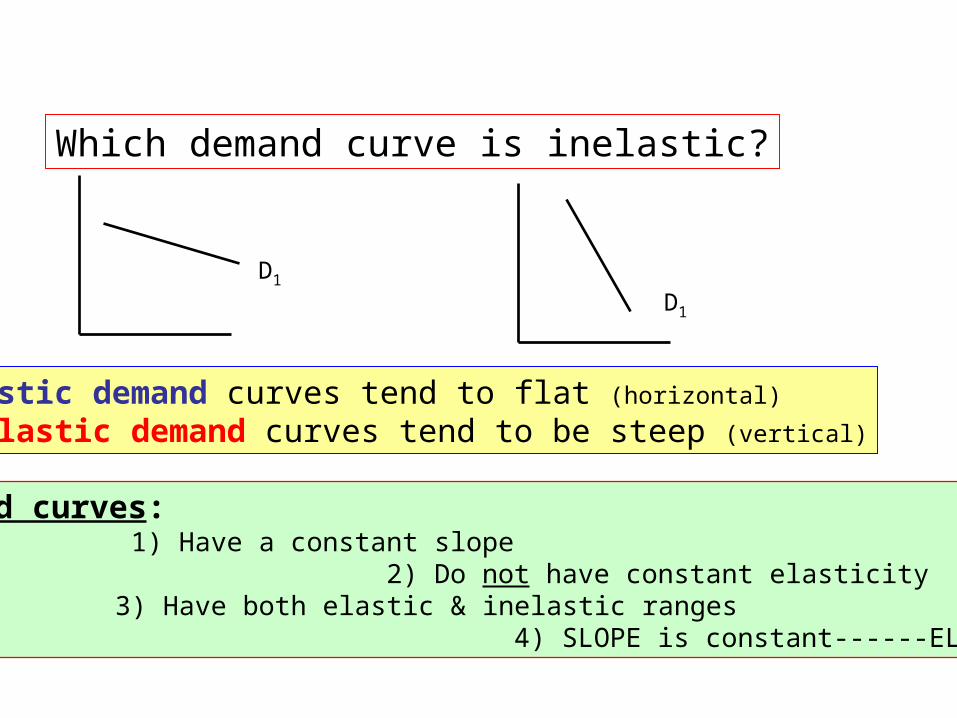

D1

D1

Which demand curve is inelastic?

Elastic demand curves tend to flat (horizontal)

Inelastic demand curves tend to be steep (vertical)

Linear demand curves: 1) Have a constant slope

2) Do not have constant elasticity 3) Have both elastic & inelastic ranges

4) SLOPE is constant------ELASTICITY changes

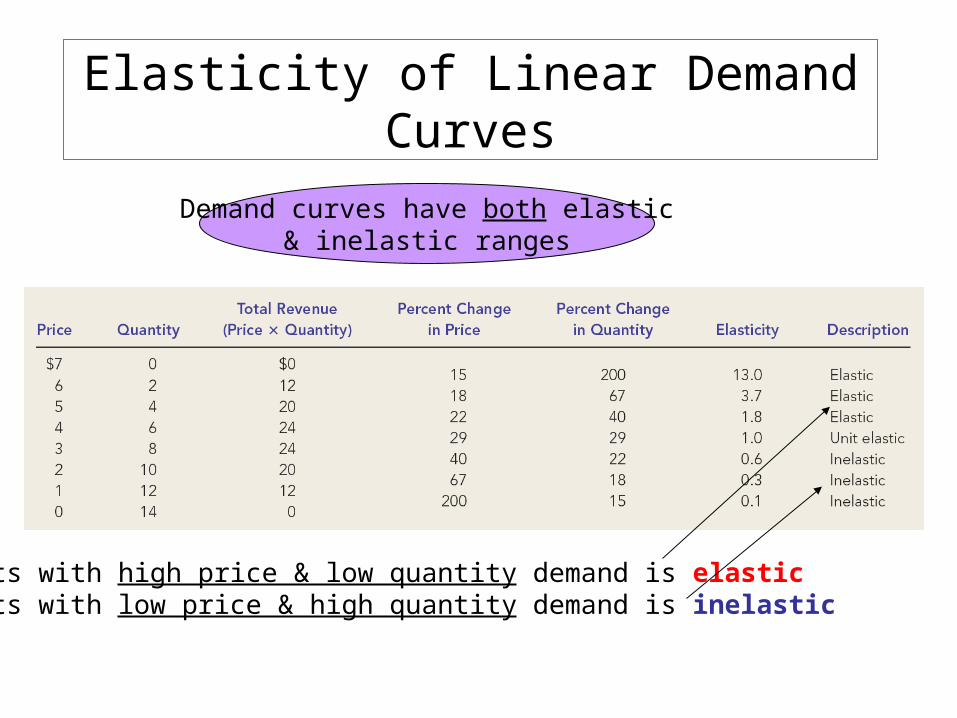

Elasticity of Linear Demand Curves

Demand curves have both elastic& inelastic ranges

Points with high price & low quantity demand is elasticPoints with low price & high quantity demand is inelastic

0 2 64 108 12 14

2

1

4

3

5

6

$7

Elastic Range: Elasticity > 1

Inelastic Range: Elasticity < 1

Price

Quantity

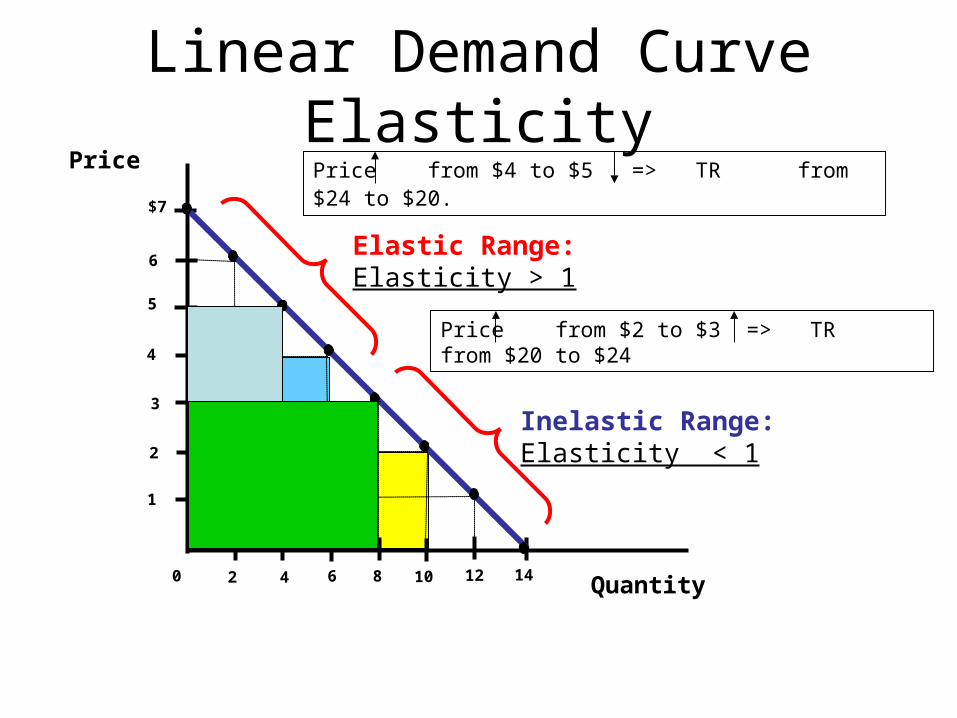

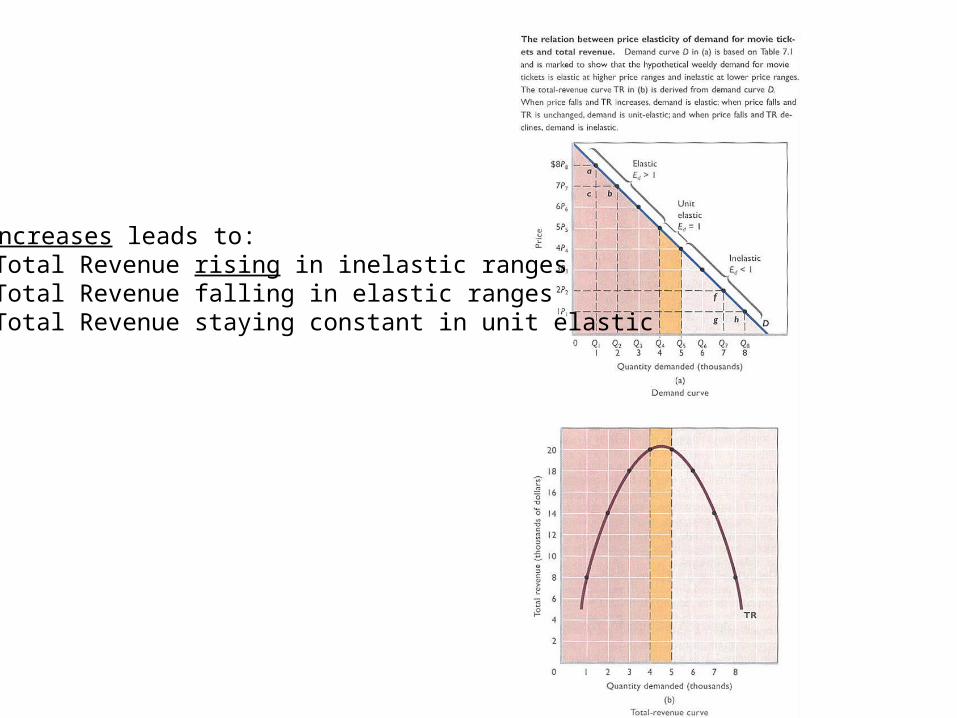

Linear Demand Curve Elasticity

Price from $4 to $5 => TR from $24 to $20.

Price from $2 to $3 => TR from $20 to $24

Price increases leads to:Total Revenue rising in inelastic rangesTotal Revenue falling in elastic rangesTotal Revenue staying constant in unit elastic

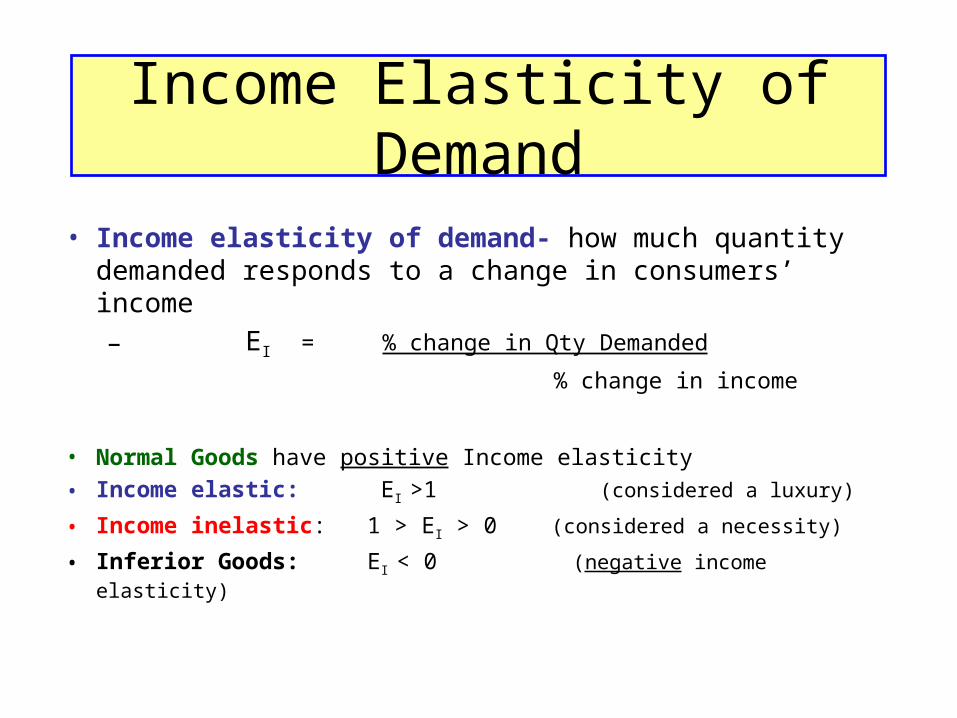

Income Elasticity of Demand

• Income elasticity of demand- how much quantity demanded responds to a change in consumers’ income

– EI = % change in Qty Demanded

% change in income

• Normal Goods have positive Income elasticity

• Income elastic: EI >1 (considered a luxury)

• Income inelastic: 1 > EI > 0 (considered a necessity)

• Inferior Goods: EI < 0 (negative income elasticity)

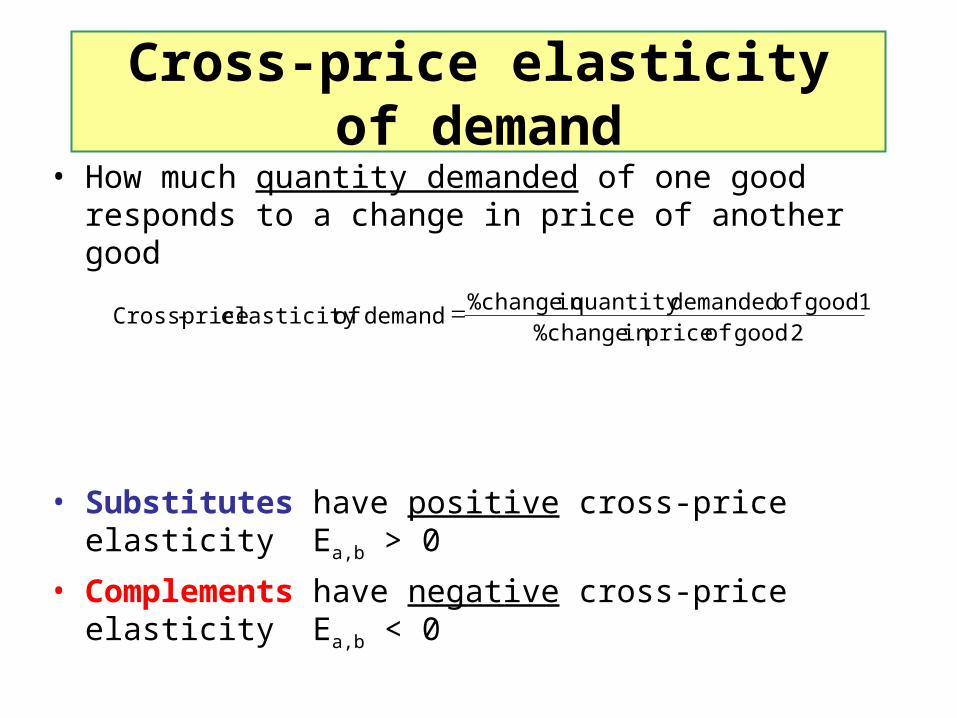

Cross-price elasticity of demand

• How much quantity demanded of one good responds to a change in price of another good

• Substitutes have positive cross-price elasticity Ea,b > 0

• Complements have negative cross-price elasticity Ea,b < 0

2 good of pricein %change1good of demandedquantity in %change

demand of elasticity price-Cross

Summary

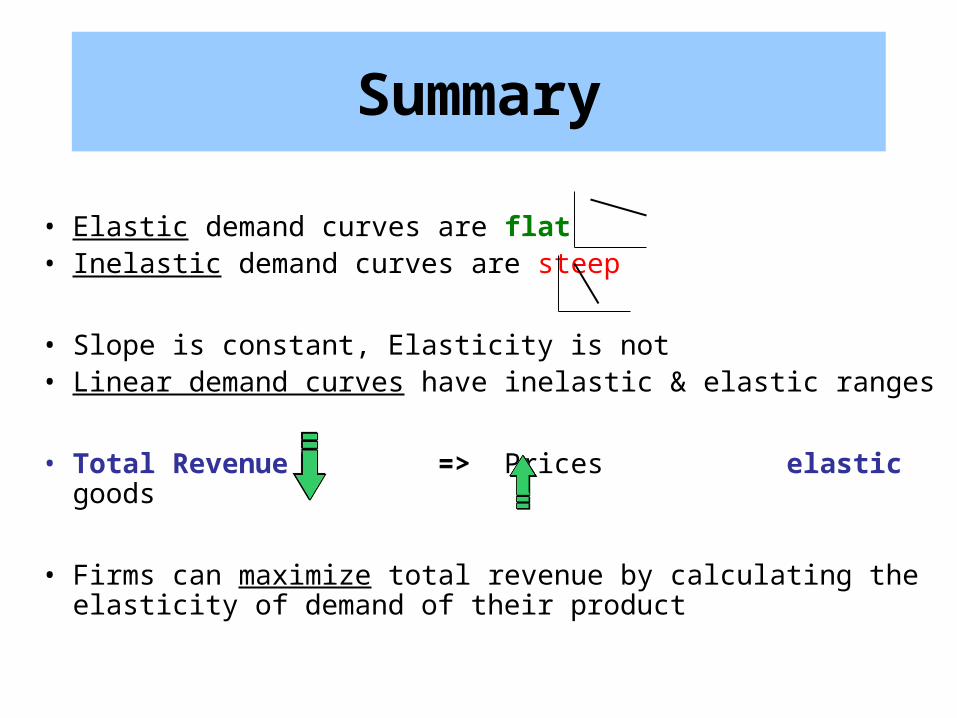

• Elastic demand curves are flat • Inelastic demand curves are steep

• Slope is constant, Elasticity is not • Linear demand curves have inelastic & elastic ranges

• Total Revenue => Prices elastic goods

• Firms can maximize total revenue by calculating the elasticity of demand of their product

Taxes & Market Equilibrium

Chapter 6

How Taxes on Buyers (and Sellers) Affect Market Outcomes

• When a good is taxed, the quantity sold is smaller • Buyers and sellers both share the tax burden

• Types of Taxes:– Sales Tax: tax on most goods

– Excise Tax: taxes on specific goods (ex: cigarettes, gasoline, etc…)

• Why tax?– To raise Government Revenue or– To decrease consumption of a good (cigarettes)

Elasticity & Tax Incidence

• Tax incidence is the study of who bears the burden of a tax

• Taxes result in a change in market equilibrium

• Buyers pay more & sellers receive less – regardless of whom the tax is levied on

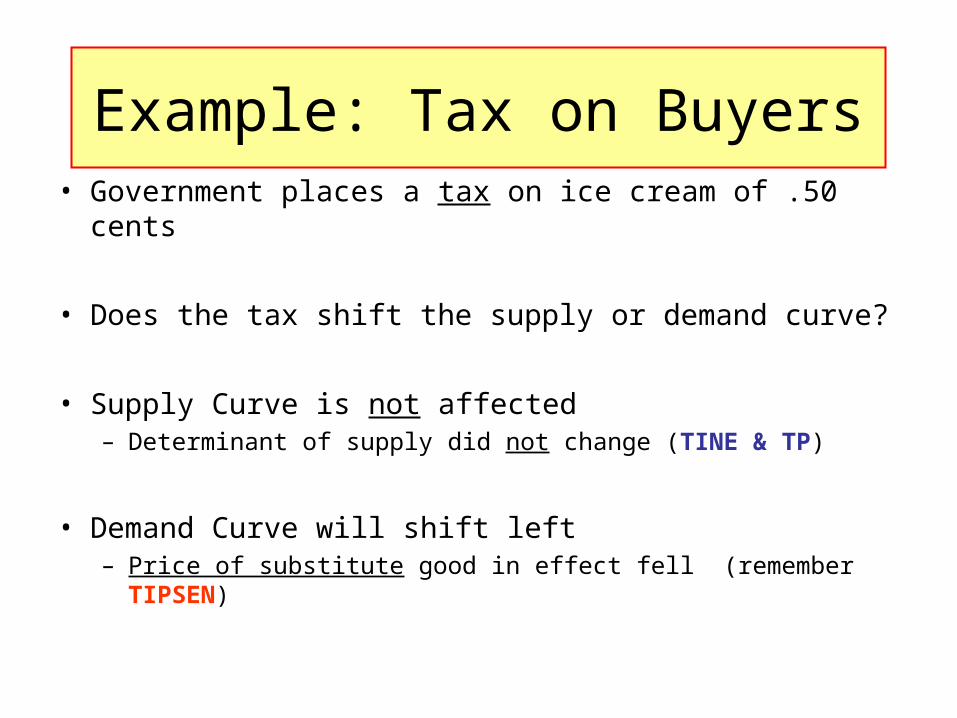

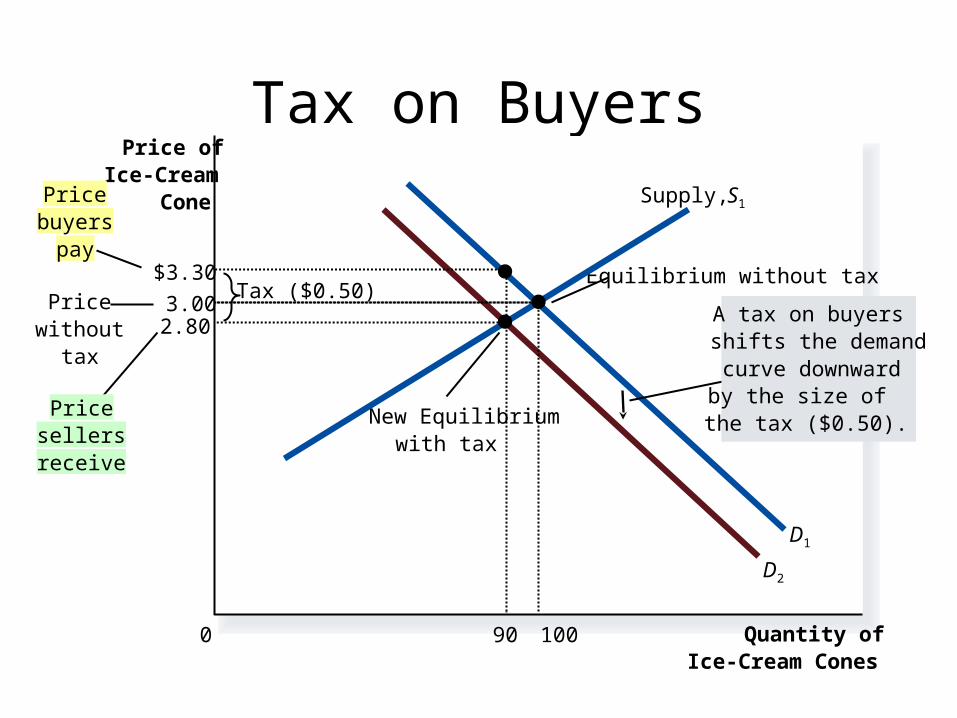

Example: Tax on Buyers• Government places a tax on ice cream of .50 cents

• Does the tax shift the supply or demand curve?

• Supply Curve is not affected – Determinant of supply did not change (TINE & TP)

• Demand Curve will shift left– Price of substitute good in effect fell (remember TIPSEN)

Tax on Buyers

Quantity ofIce-Cream Cones

0

Price ofIce-Cream

Cone

Pricewithout

tax

Pricesellersreceive

Equilibrium without taxTax ($0.50)

Pricebuyers

pay

D1

D2

Supply, S1

A tax on buyersshifts the demandcurve downwardby the size ofthe tax ($0.50).

$3.30

90

New Equilibriumwith tax

2.803.00

100

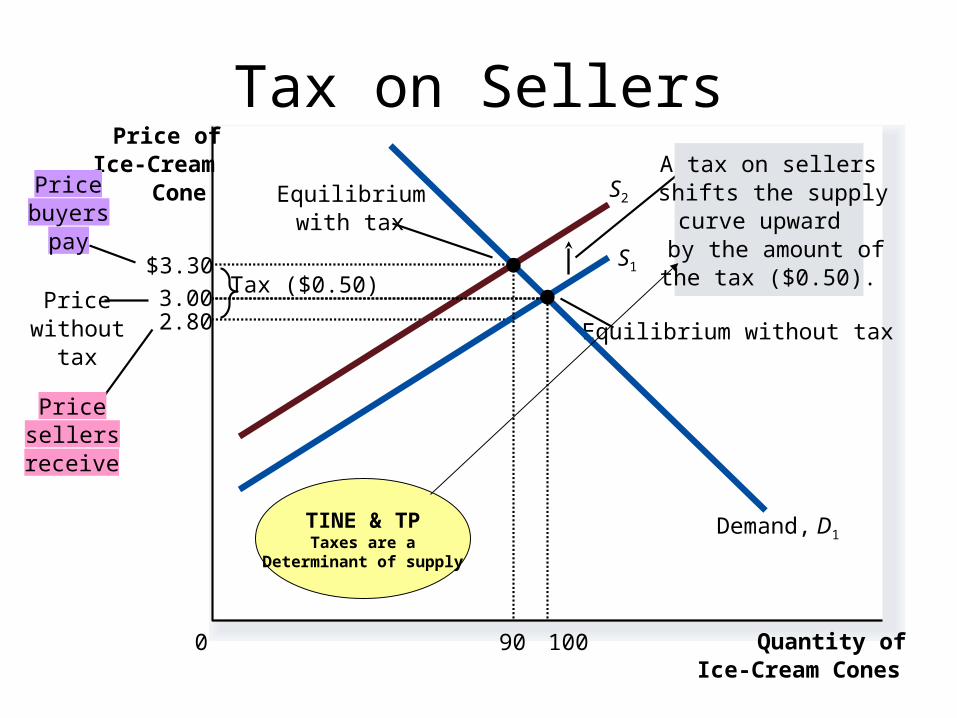

Tax on Sellers

2.80

Quantity ofIce-Cream Cones

0

Price ofIce-Cream

Cone

Pricewithout

tax

Pricesellersreceive

Equilibriumwith tax

Equilibrium without tax

Tax ($0.50)

Pricebuyers

payS1

S2

Demand, D1

A tax on sellersshifts the supplycurve upwardby the amount ofthe tax ($0.50).

3.00

100

$3.30

90

TINE & TPTaxes are a

Determinant of supply

Elasticity and Tax Incidence

• In what proportions is the burden of the tax divided?

• How do the effects of taxes on sellers compare to those levied on buyers?

• It depends on the elasticity of demand & the elasticity of supply.

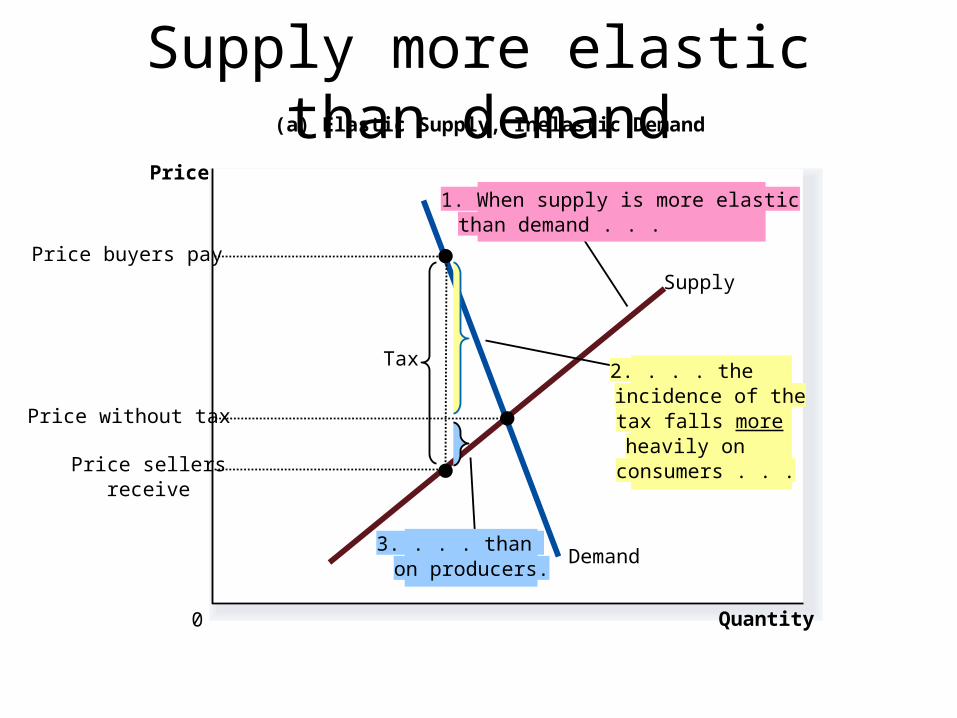

Supply more elastic than demand

Quantity0

Price

Demand

Supply

Tax

Price sellersreceive

Price buyers pay

(a) Elastic Supply, Inelastic Demand

2. . . . theincidence of thetax falls moreheavily onconsumers . . .

1. When supply is more elasticthan demand . . .

Price without tax

3. . . . than on producers.

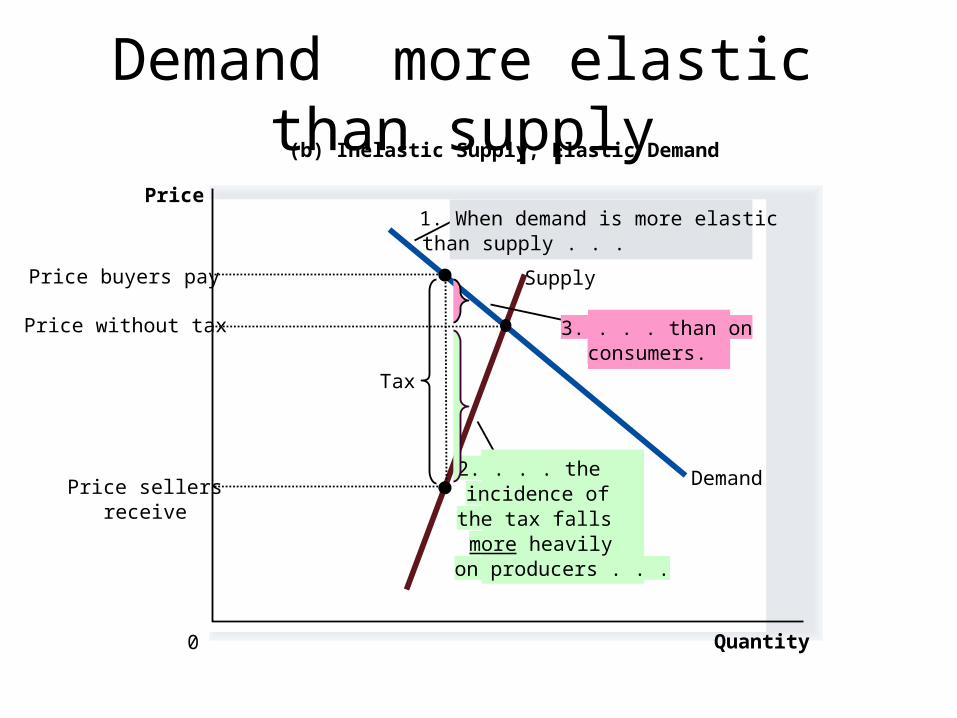

Demand more elastic than supply

Quantity0

Price

Demand

Supply

Tax

Price sellersreceive

Price buyers pay

(b) Inelastic Supply, Elastic Demand

3. . . . than onconsumers.

1. When demand is more elasticthan supply . . .

Price without tax

2. . . . theincidence of the tax falls more heavily on producers . . .

So, how is the burden of the tax divided?

The burden of a tax falls more heavily on the side of the market that is less elastic.

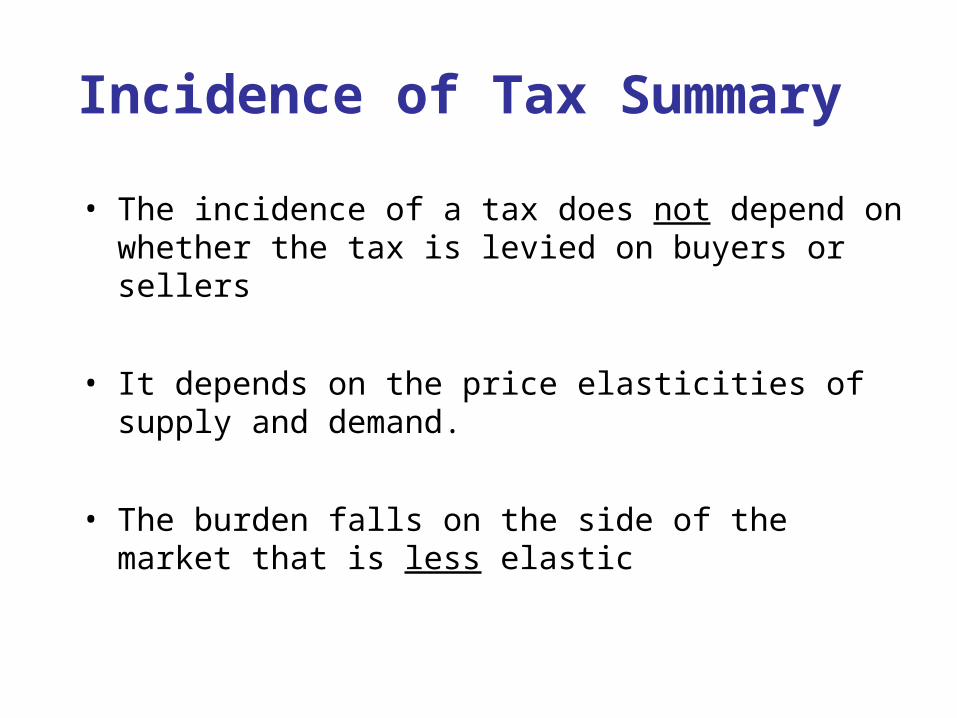

• The incidence of a tax does not depend on whether the tax is levied on buyers or sellers

• It depends on the price elasticities of supply and demand.

• The burden falls on the side of the market that is less elastic

Incidence of Tax Summary

Welfare Economics

Chapter 7: Consumer Surplus

Consumers, Producers & Efficiency of Markets

• Market equilibrium reflects the way markets allocate scarce resources

• Whether the market allocation is desirable can be addressed by welfare economics

• Welfare economics is the study of how the allocation of resources affects economic well-being

Welfare Economics

• Equilibrium- results in maximum total welfare for consumers & producers

• Consumer surplus measures economic welfare from the buyer’s side

• Producer surplus measures economic welfare from the seller’s side

CONSUMER SURPLUS

• Willingness to pay- the maximum amount that a buyer will pay for a good

• It measures how much the buyer values the good or service

• Consumer surplus- the buyer’s willingness to pay for a good minus the amount the buyer actually pays for it

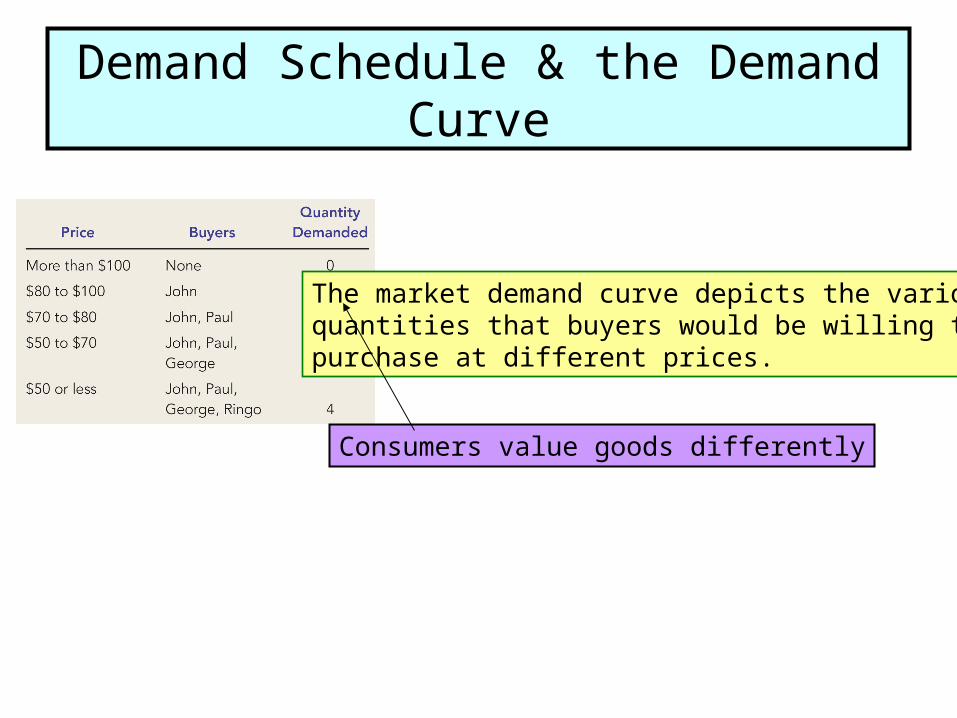

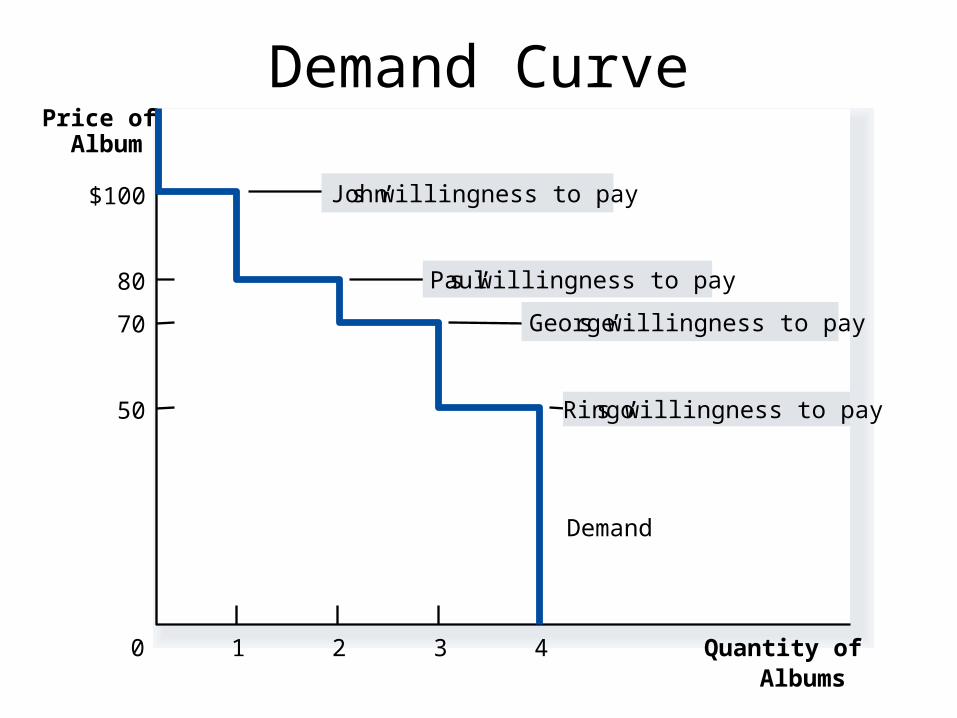

Demand Schedule & the Demand Curve

The market demand curve depicts the various quantities that buyers would be willing to purchase at different prices.

Consumers value goods differently

Demand CurvePrice of

Album

0 Quantity ofAlbums

Demand

1 2 3 4

$100 John’s willingness to pay

80 Paul’s willingness to pay

70 George’s willingness to pay

50 Ringo’s willingness to pay

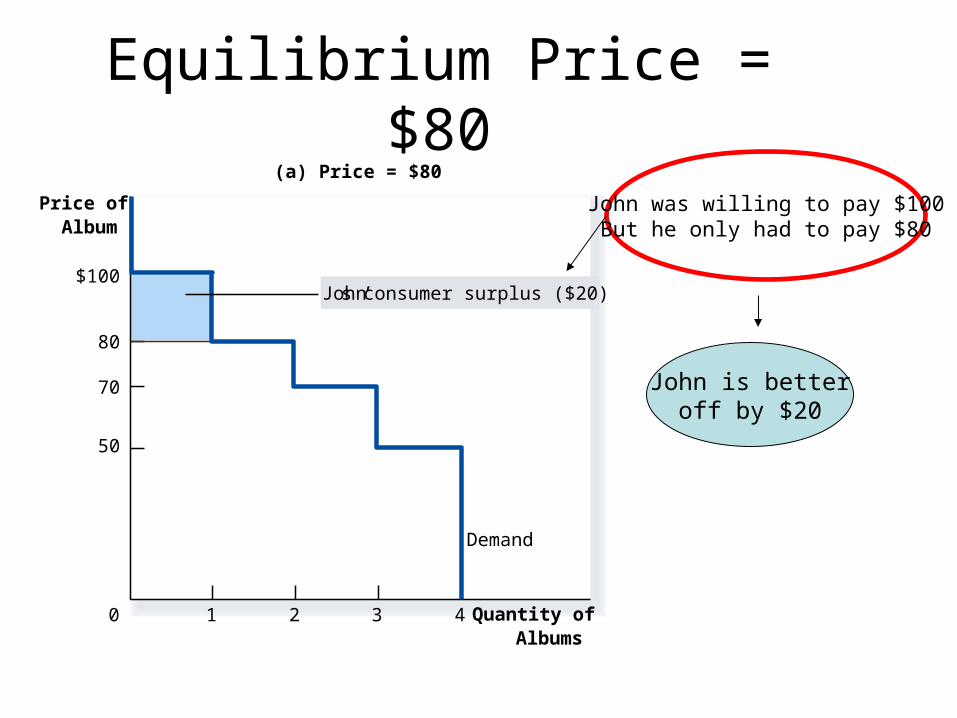

Equilibrium Price = $80(a) Price = $80

Price ofAlbum

50

70

80

0

$100

Demand

1 2 3 4 Quantity ofAlbums

John’s consumer surplus ($20)

John was willing to pay $100But he only had to pay $80

John is betteroff by $20

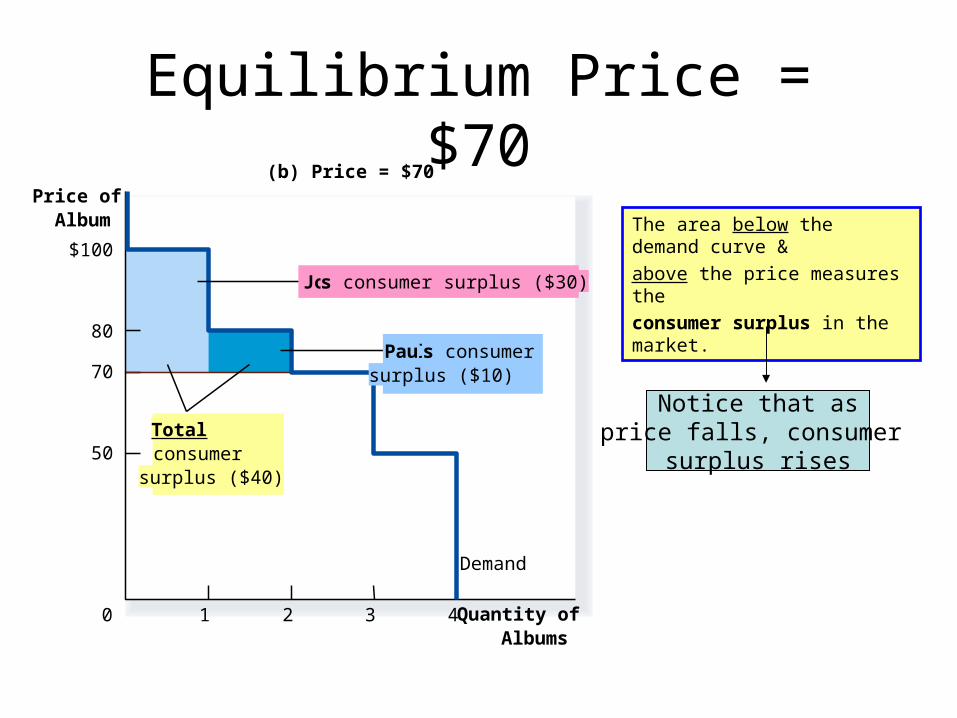

Equilibrium Price = $70(b) Price = $70

Price ofAlbum

50

70

80

0

$100

Demand

1 2 3 4

Totalconsumersurplus ($40)

Quantity ofAlbums

John’s consumer surplus ($30)

Paul’s consumersurplus ($10)

The area below the demand curve &

above the price measures the

consumer surplus in the market.

Notice that asprice falls, consumer

surplus rises

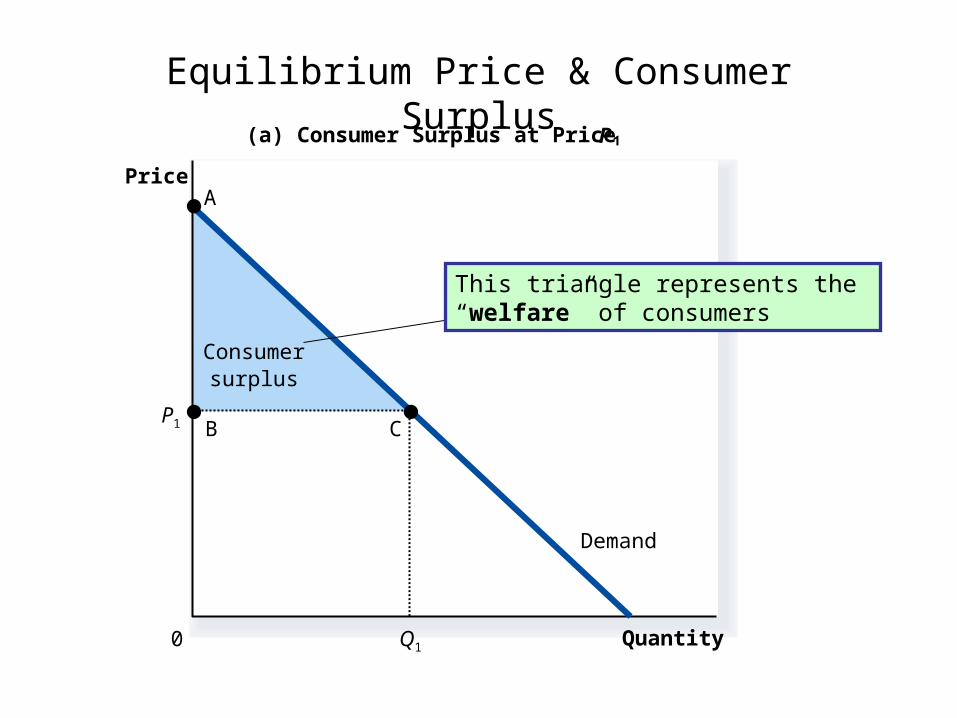

Equilibrium Price & Consumer Surplus

Consumersurplus

Quantity

(a) Consumer Surplus at Price P

Price

0

Demand

P1

Q1

B

A

C

This triangle represents the “welfare” of consumers

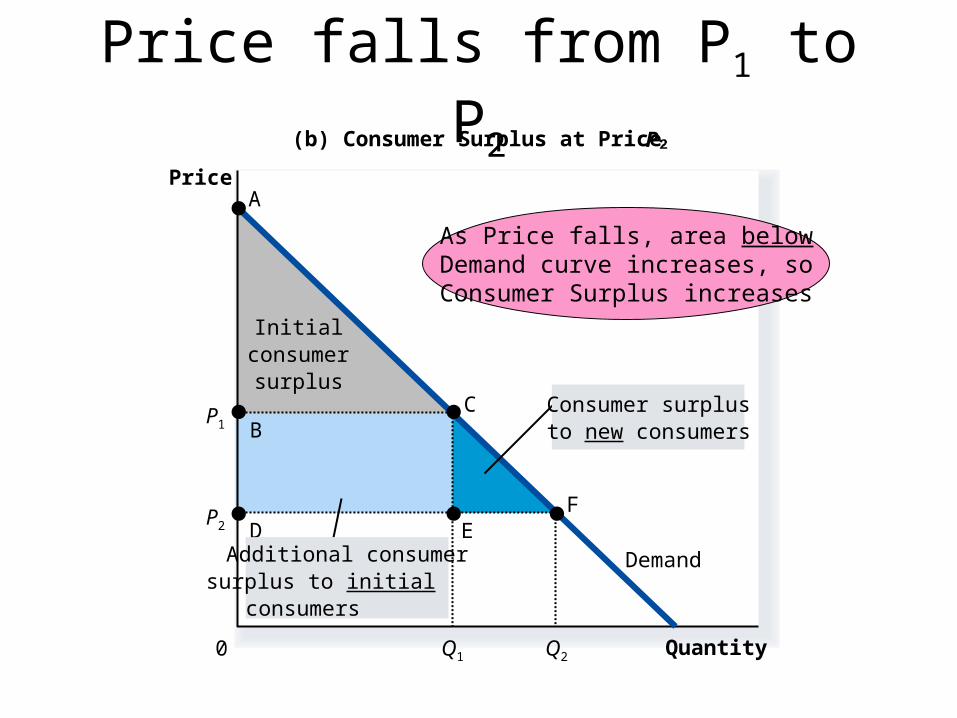

Price falls from P1 to P2

Initialconsumer

surplus

Quantity

(b) Consumer Surplus at Price P

Price

0

Demand

A

BC

D EF

P1

Q1

P2

Q2

Consumer surplusto new consumers

Additional consumersurplus to initial consumers

As Price falls, area belowDemand curve increases, soConsumer Surplus increases

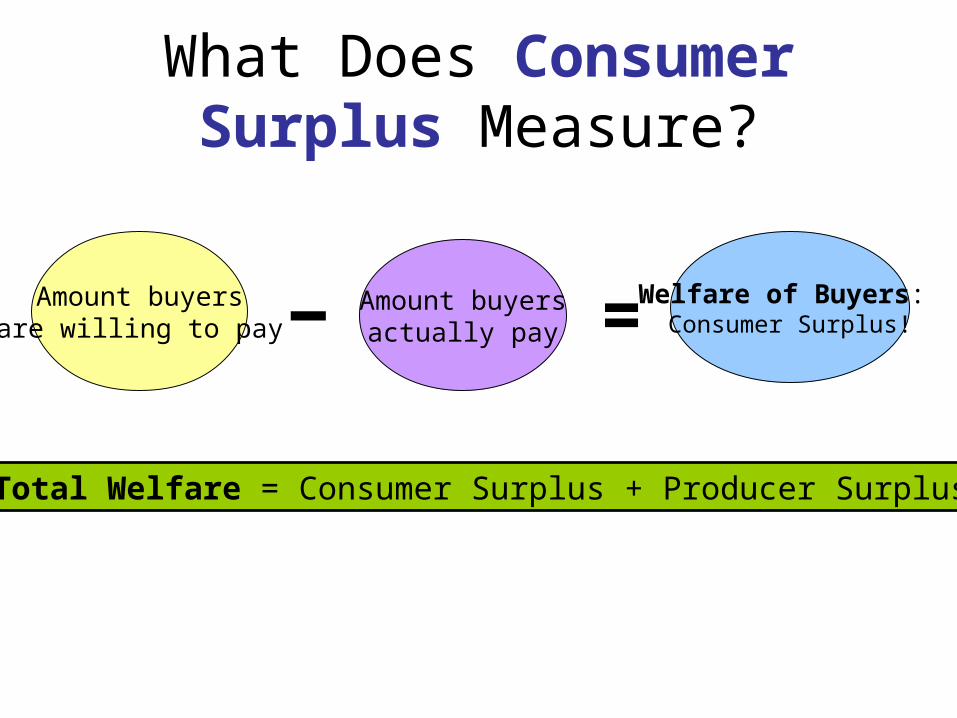

What Does Consumer Surplus Measure?

Amount buyersare willing to pay

Amount buyersactually pay

Welfare of Buyers: Consumer Surplus!- =

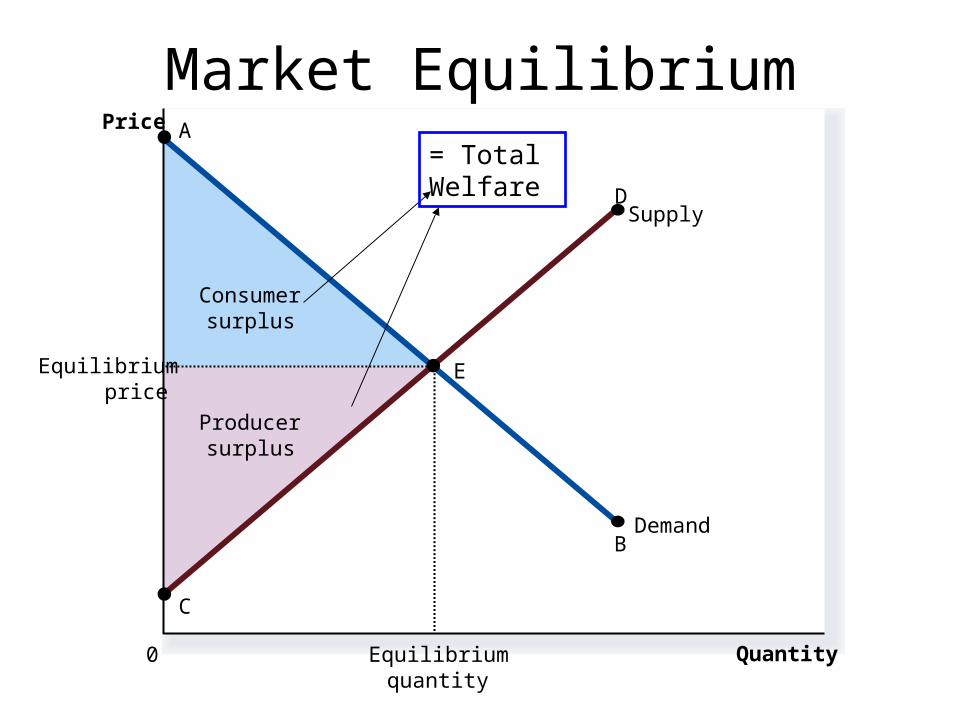

Total Welfare = Consumer Surplus + Producer Surplus

Welfare Economics Part II

Chapter 7: Producer Surplus

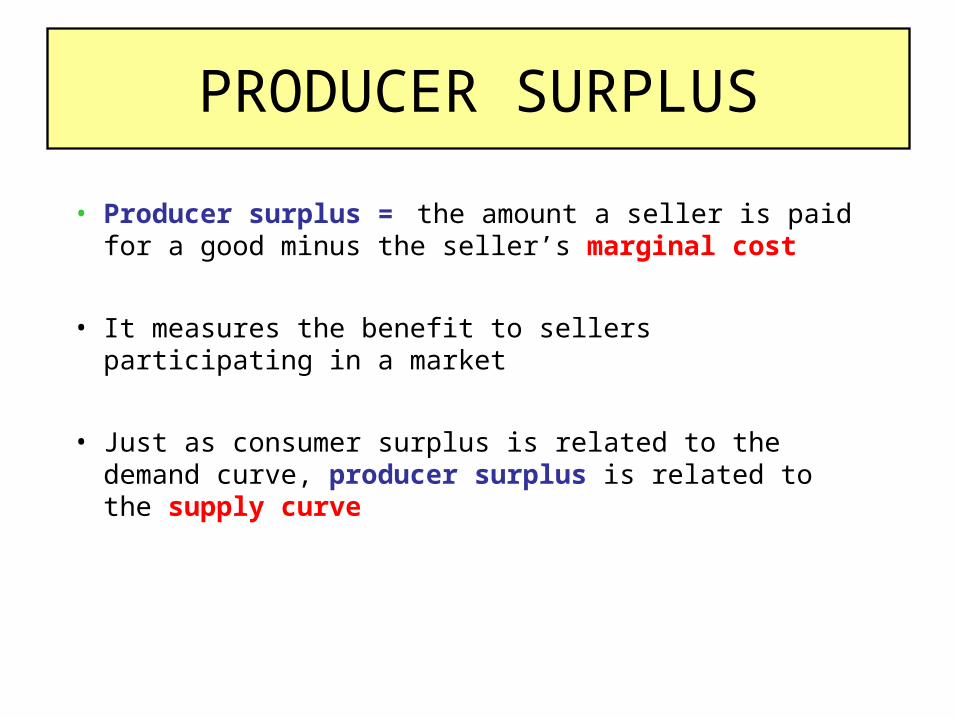

PRODUCER SURPLUS

• Producer surplus = the amount a seller is paid for a good minus the seller’s marginal cost

• It measures the benefit to sellers participating in a market

• Just as consumer surplus is related to the demand curve, producer surplus is related to the supply curve

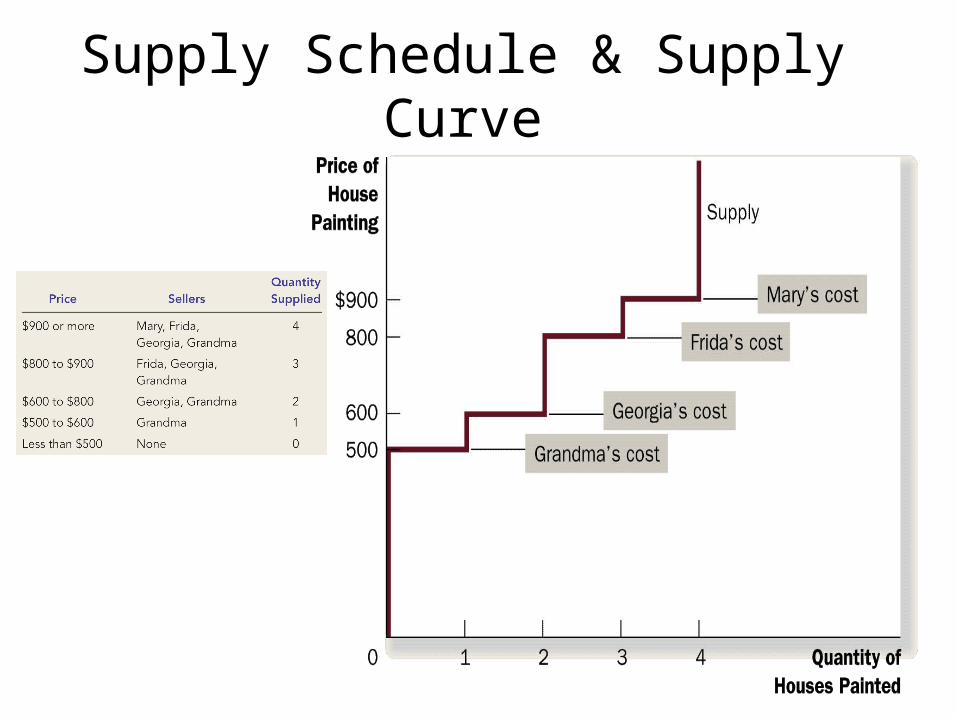

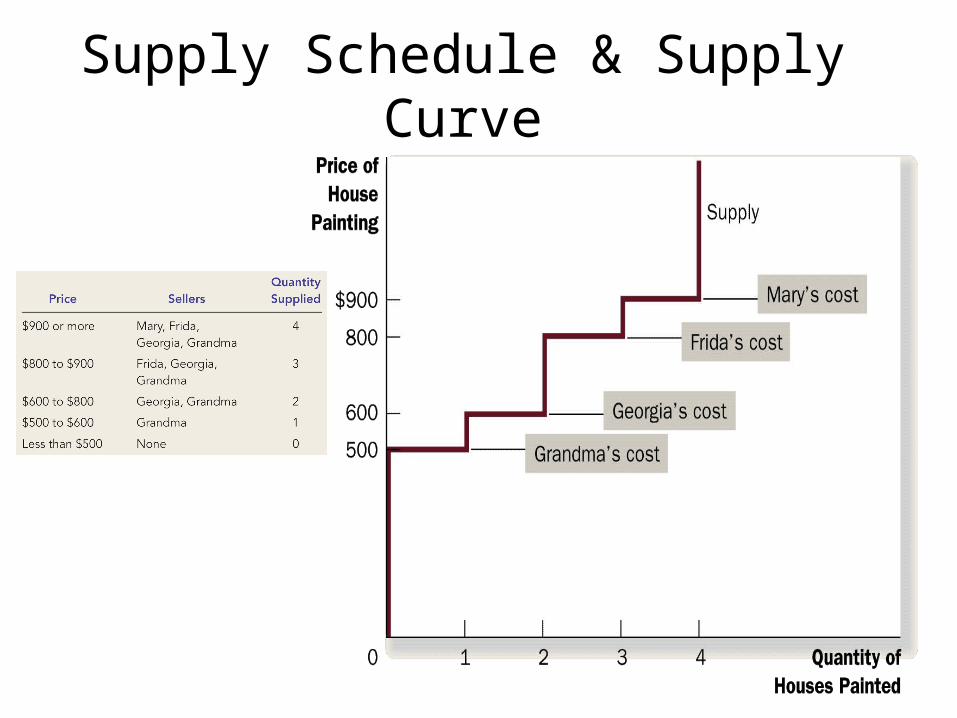

Supply Schedule & Supply Curve

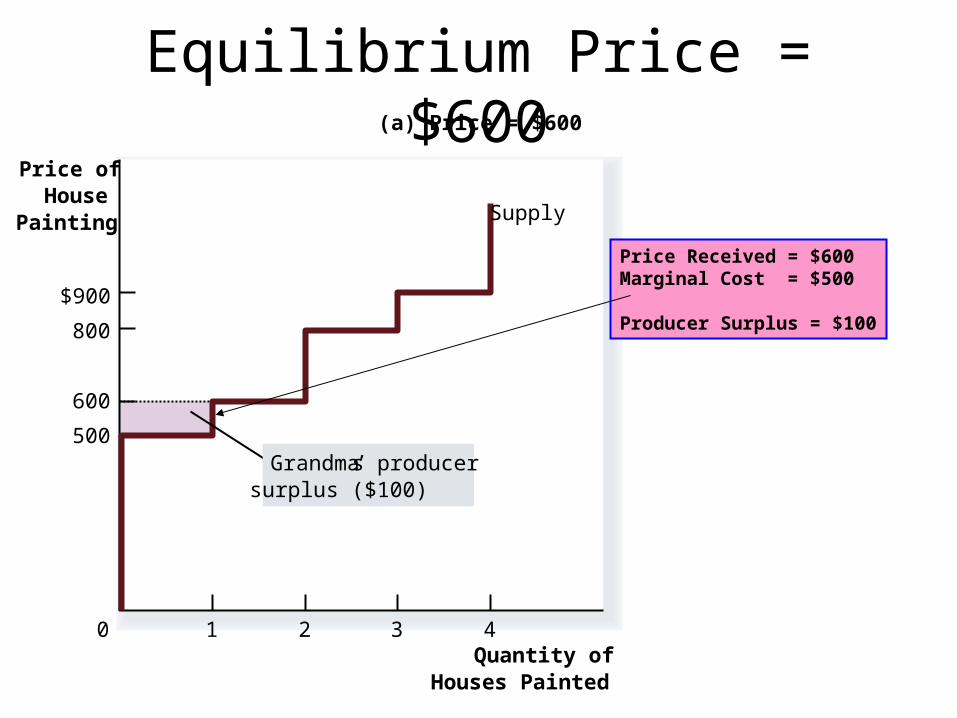

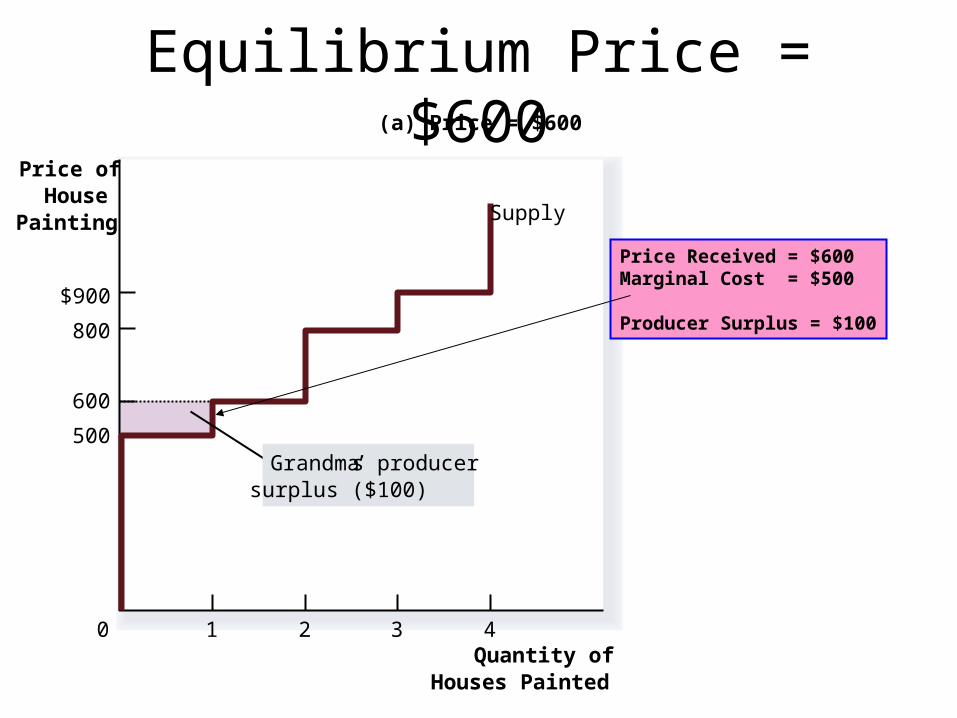

Equilibrium Price = $600

Quantity ofHouses Painted

Price ofHouse

Painting

500

800

$900

0

600

1 2 3 4

(a) Price = $600

Supply

Grandma’s producersurplus ($100)

Price Received = $600Marginal Cost = $500

Producer Surplus = $100

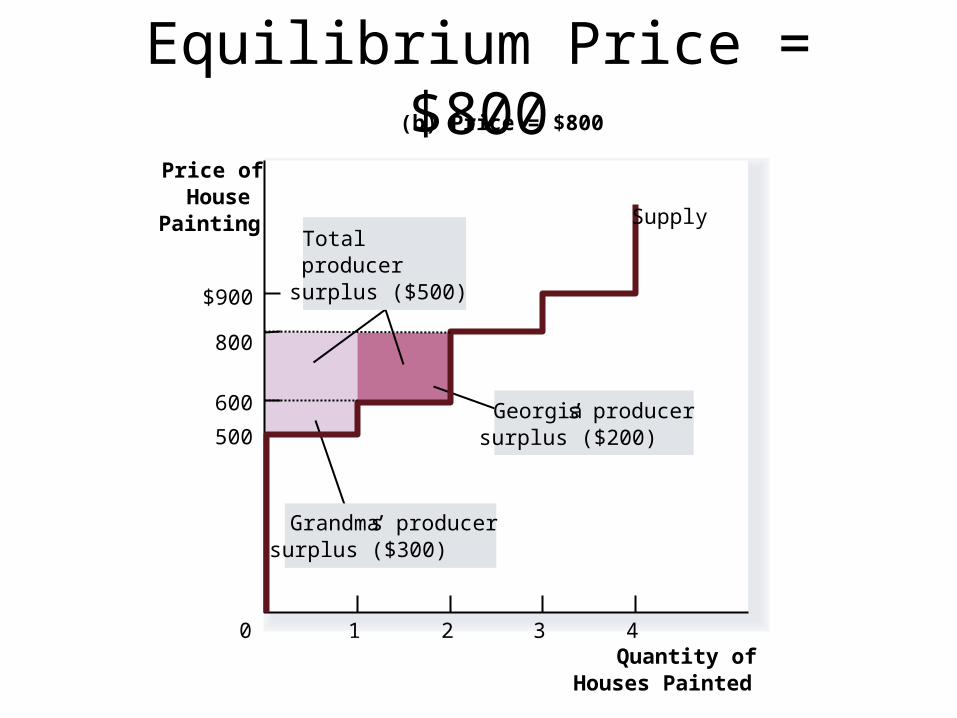

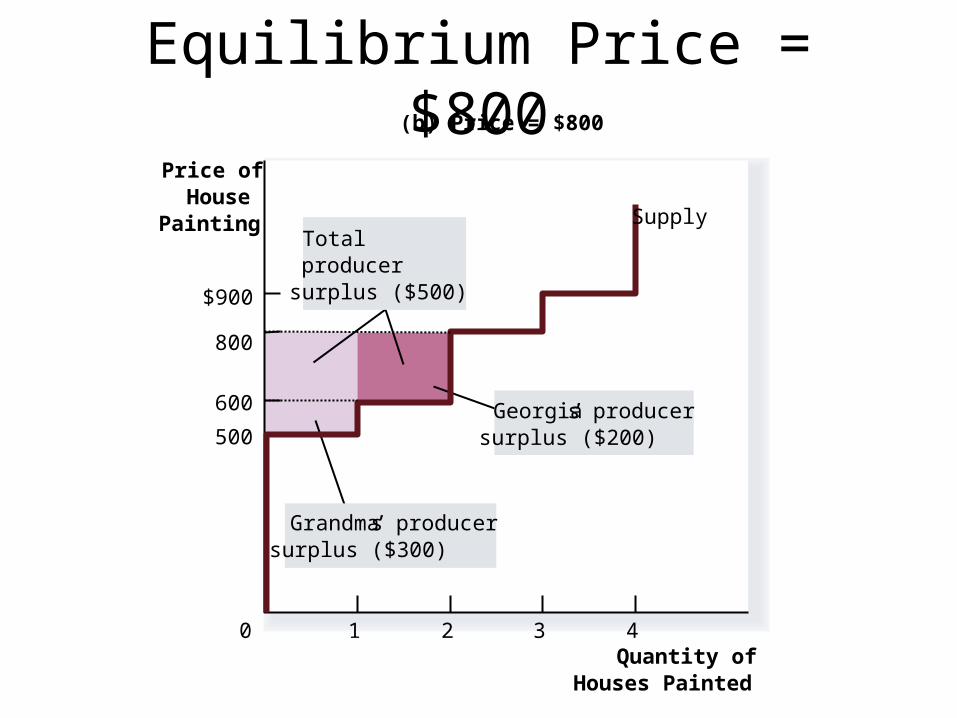

Equilibrium Price = $800

Quantity ofHouses Painted

Price ofHouse

Painting

500

800

$900

0

600

1 2 3 4

(b) Price = $800

Georgia’s producersurplus ($200)

Totalproducersurplus ($500)

Grandma’s producersurplus ($300)

Supply

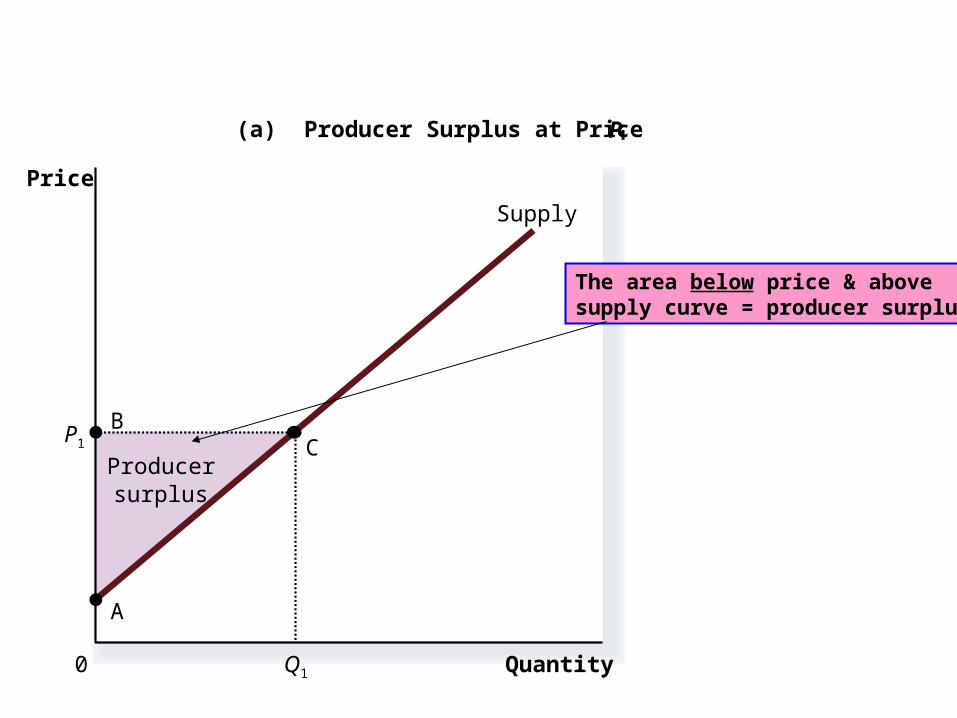

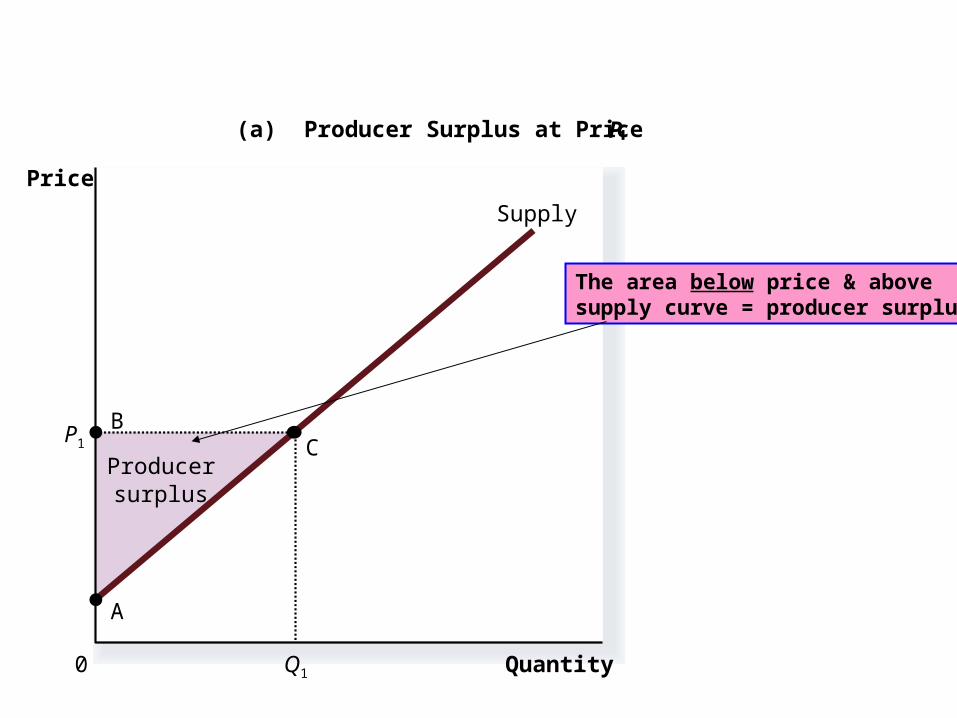

Producersurplus

Quantity

(a) Producer Surplus at Price P

Price

0

Supply

B

A

C

Q1

P1

The area below price & abovesupply curve = producer surplus

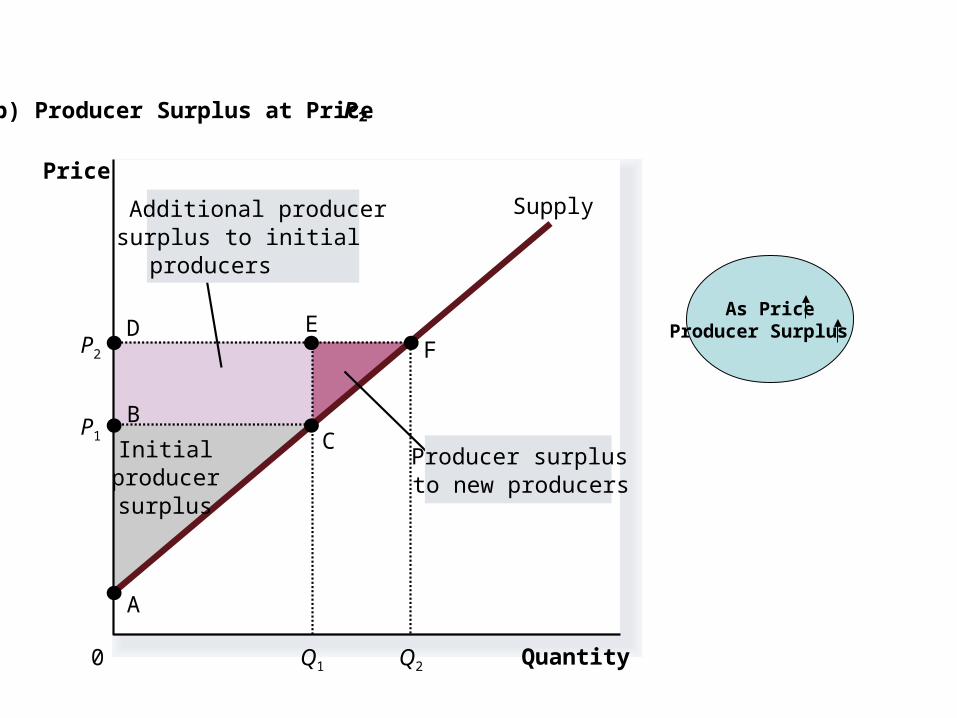

Quantity

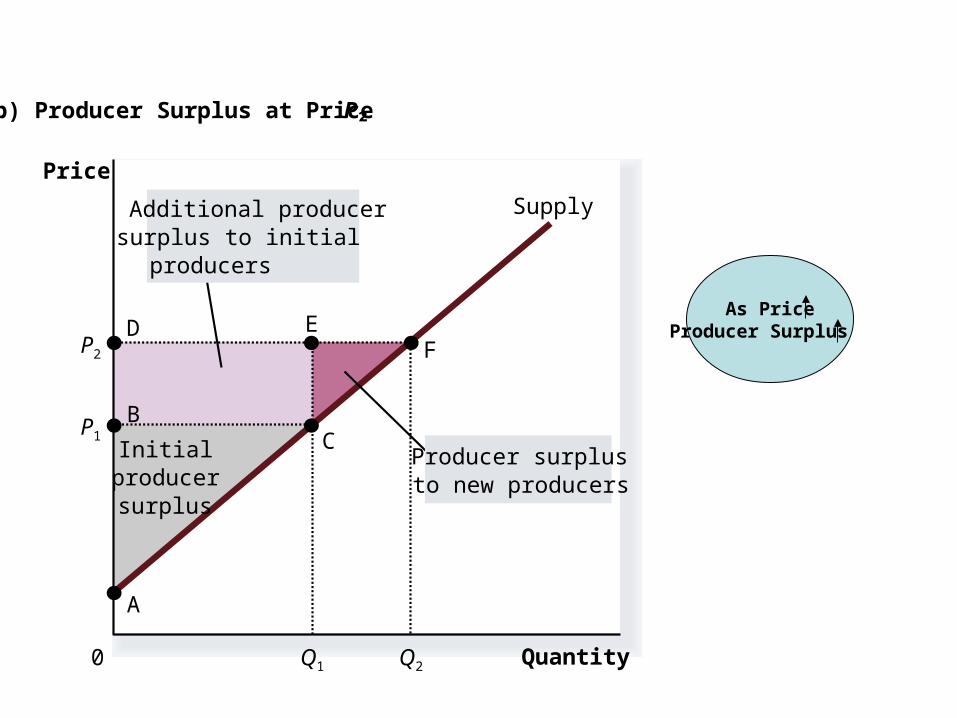

(b) Producer Surplus at Price P

Price

0

P1B

C

Supply

A

Initialproducersurplus

Q1

P2

Q2

Producer surplusto new producers

Additional producersurplus to initialproducers

D EF

As PriceProducer Surplus

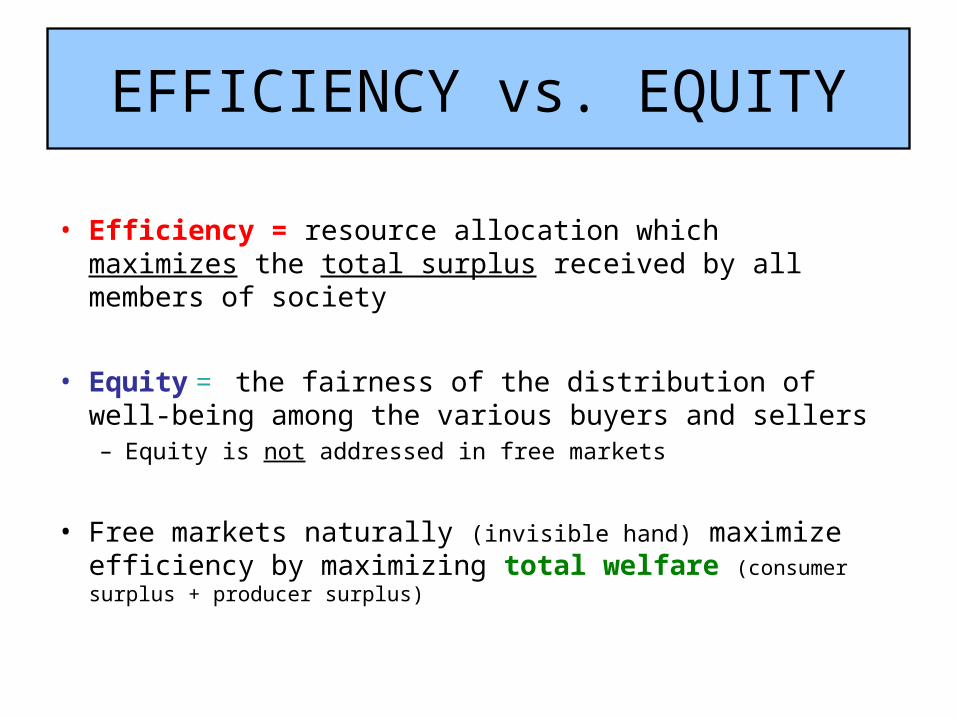

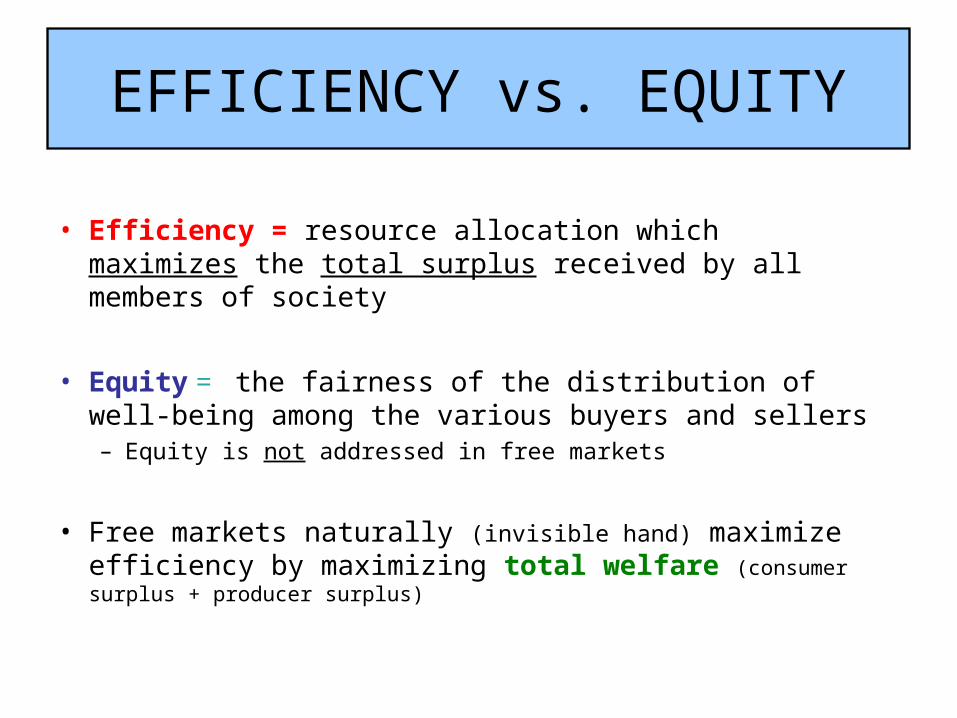

EFFICIENCY vs. EQUITY

• Efficiency = resource allocation which maximizes the total surplus received by all members of society

• Equity = the fairness of the distribution of well-being among the various buyers and sellers – Equity is not addressed in free markets

• Free markets naturally (invisible hand) maximize efficiency by maximizing total welfare (consumer surplus + producer surplus)

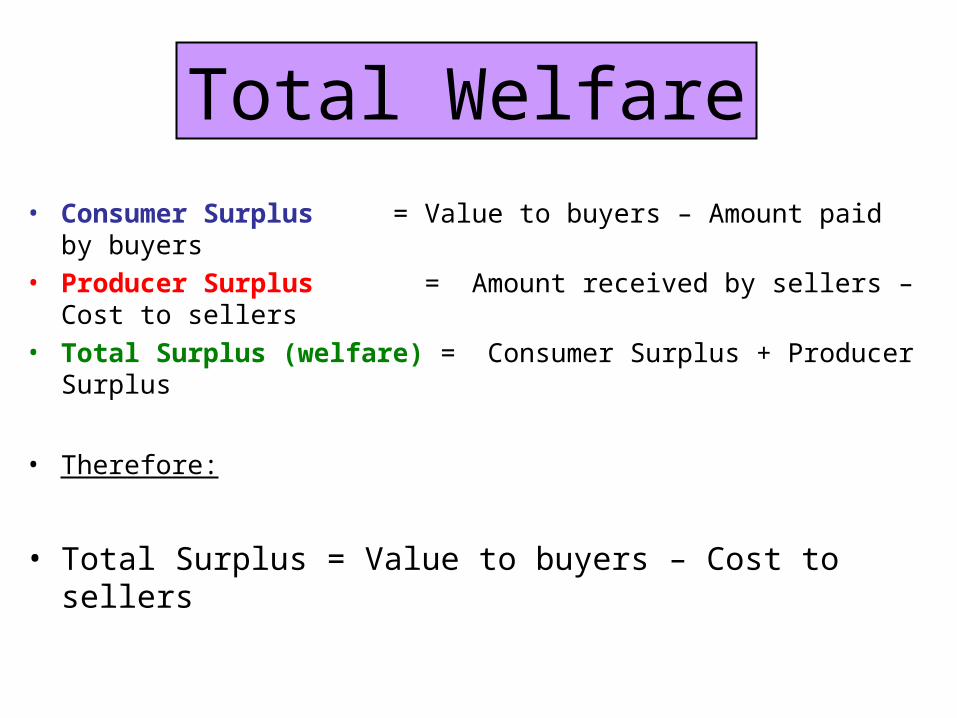

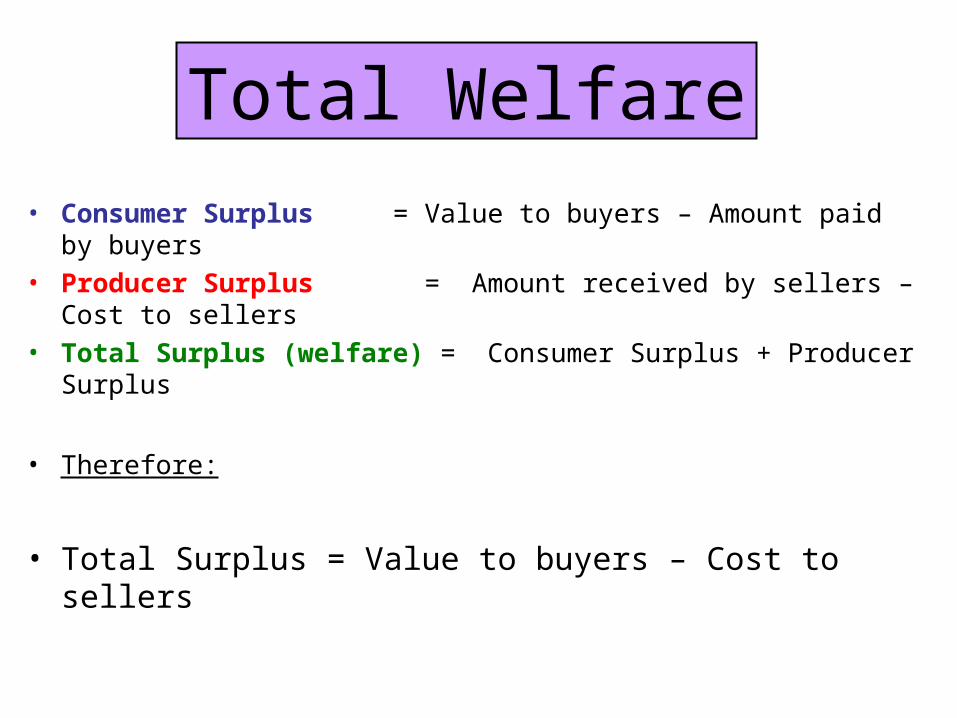

• Consumer Surplus = Value to buyers – Amount paid by buyers• Producer Surplus = Amount received by sellers – Cost to sellers• Total Surplus (welfare) = Consumer Surplus + Producer Surplus

• Therefore:

• Total Surplus = Value to buyers – Cost to sellers

Total Welfare

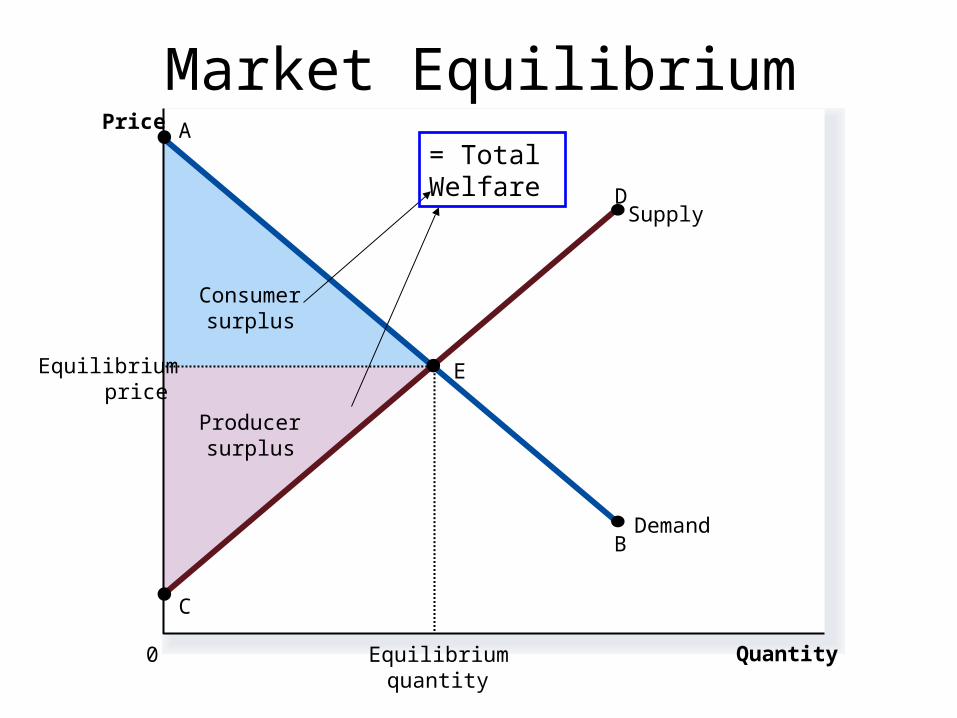

Market Equilibrium

Producersurplus

Consumersurplus

Price

0 Quantity

Equilibriumprice

Equilibriumquantity

Supply

Demand

A

C

B

D

E

= Total Welfare

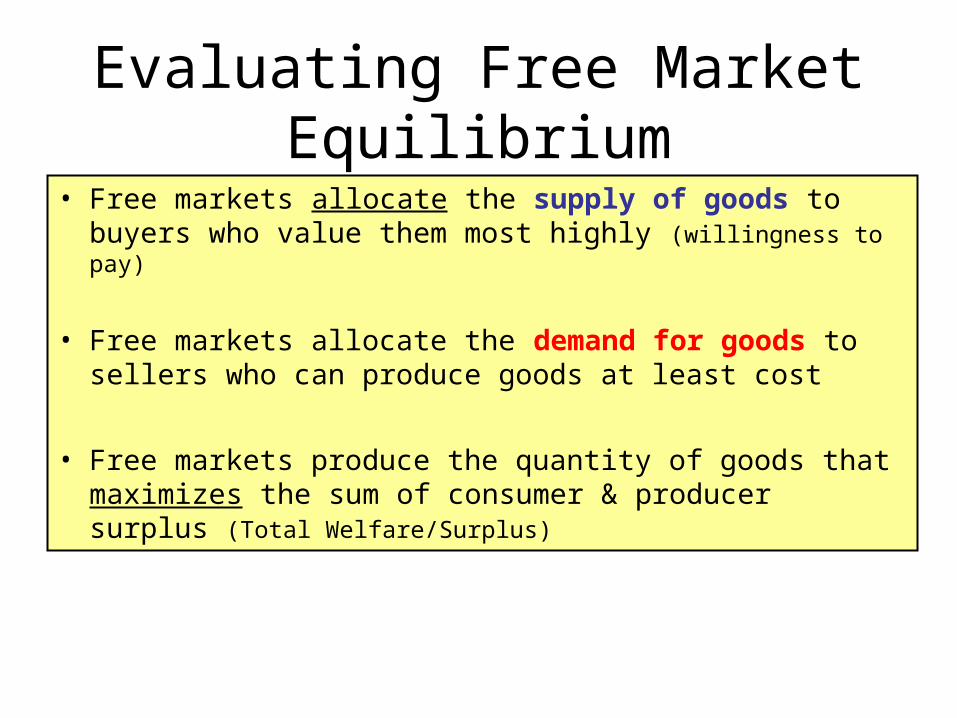

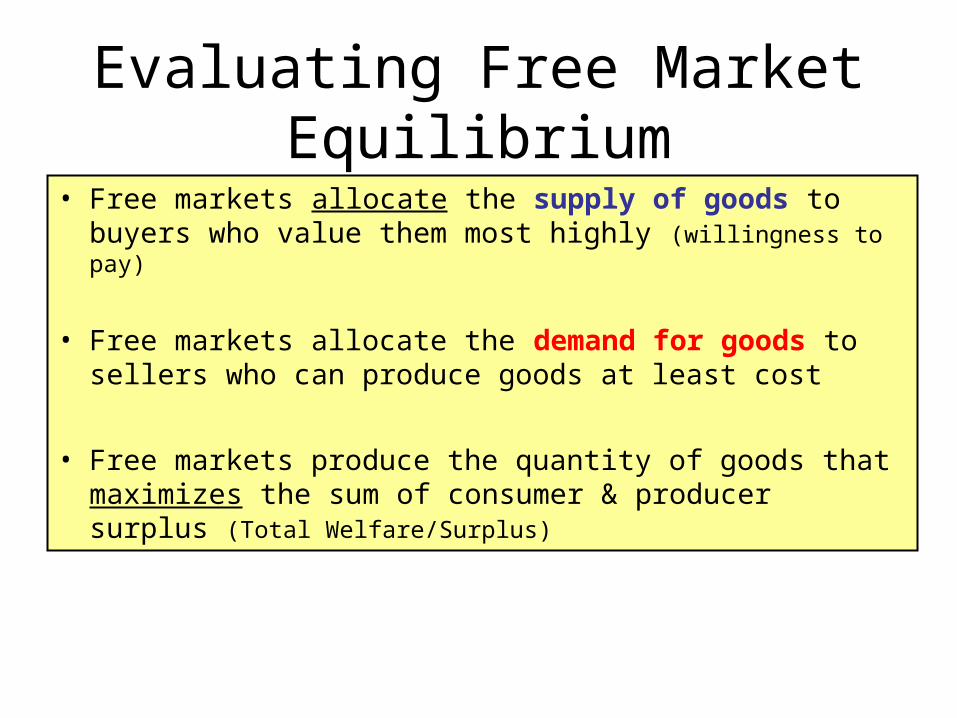

Evaluating Free Market Equilibrium

• Free markets allocate the supply of goods to buyers who value them most highly (willingness to pay)

• Free markets allocate the demand for goods to sellers who can produce goods at least cost

• Free markets produce the quantity of goods that maximizes the sum of consumer & producer surplus (Total Welfare/Surplus)

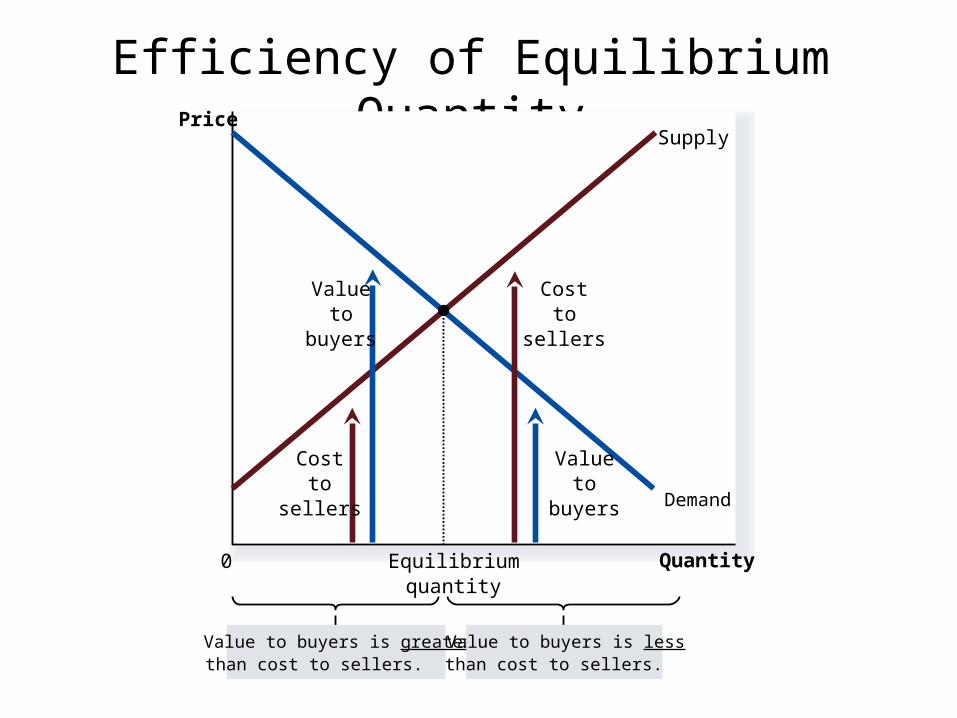

Efficiency of Equilibrium Quantity

Quantity

Price

0

Supply

Demand

Costto

sellers

Costto

sellers

Valueto

buyers

Valueto

buyers

Value to buyers is greaterthan cost to sellers.

Value to buyers is lessthan cost to sellers.

Equilibriumquantity

Worksheet: Lesson 1, Activity 9

• Please complete side 2 of the Consumer/Producer Surplus worksheet

Welfare Economics Part II

Chapter 7: Producer Surplus

PRODUCER SURPLUS

• Producer surplus = the amount a seller is paid for a good minus the seller’s marginal cost

• It measures the benefit to sellers participating in a market

• Just as consumer surplus is related to the demand curve, producer surplus is related to the supply curve

Supply Schedule & Supply Curve

Equilibrium Price = $600

Quantity ofHouses Painted

Price ofHouse

Painting

500

800

$900

0

600

1 2 3 4

(a) Price = $600

Supply

Grandma’s producersurplus ($100)

Price Received = $600Marginal Cost = $500

Producer Surplus = $100

Equilibrium Price = $800

Quantity ofHouses Painted

Price ofHouse

Painting

500

800

$900

0

600

1 2 3 4

(b) Price = $800

Georgia’s producersurplus ($200)

Totalproducersurplus ($500)

Grandma’s producersurplus ($300)

Supply

Producersurplus

Quantity

(a) Producer Surplus at Price P

Price

0

Supply

B

A

C

Q1

P1

The area below price & abovesupply curve = producer surplus

Quantity

(b) Producer Surplus at Price P

Price

0

P1B

C

Supply

A

Initialproducersurplus

Q1

P2

Q2

Producer surplusto new producers

Additional producersurplus to initialproducers

D EF

As PriceProducer Surplus

EFFICIENCY vs. EQUITY

• Efficiency = resource allocation which maximizes the total surplus received by all members of society

• Equity = the fairness of the distribution of well-being among the various buyers and sellers – Equity is not addressed in free markets

• Free markets naturally (invisible hand) maximize efficiency by maximizing total welfare (consumer surplus + producer surplus)

• Consumer Surplus = Value to buyers – Amount paid by buyers• Producer Surplus = Amount received by sellers – Cost to sellers• Total Surplus (welfare) = Consumer Surplus + Producer Surplus

• Therefore:

• Total Surplus = Value to buyers – Cost to sellers

Total Welfare

Market Equilibrium

Producersurplus

Consumersurplus

Price

0 Quantity

Equilibriumprice

Equilibriumquantity

Supply

Demand

A

C

B

D

E

= Total Welfare

Evaluating Free Market Equilibrium

• Free markets allocate the supply of goods to buyers who value them most highly (willingness to pay)

• Free markets allocate the demand for goods to sellers who can produce goods at least cost

• Free markets produce the quantity of goods that maximizes the sum of consumer & producer surplus (Total Welfare/Surplus)

Efficiency of Equilibrium Quantity

Quantity

Price

0

Supply

Demand

Costto

sellers

Costto

sellers

Valueto

buyers

Valueto

buyers

Value to buyers is greaterthan cost to sellers.

Value to buyers is lessthan cost to sellers.

Equilibriumquantity