Embed Size (px)

Citation preview

Drillsearch Energy Limited ABN 73 006 474 844

Telephone +61 2 9249 9600 Facsimile +61 2 9249 9630 [email protected]

www.drillsearch.com.au Level 16, 55 Clarence Street

Sydney NSW 2000

29 August 2013 FY 2013 Full Year Results Drillsearch in the black – Record net profit of $45.1 million Drillsearch Energy Limited (ASX: DLS) is pleased to announce its results for the 2013 financial year including a net profit after tax of $45.1 million; a significant increase on the 2012 financial year result of $10.0 million. The record financial performance was on the back of the Company’s highest ever total production and sales revenues, which are attributed to the ramp up in oil production from the Western Flank Oil Fairway and the resumption of wet gas production from the Western Cooper Wet Gas project. Drillsearch Managing Director, Brad Lingo said, “We are very proud to announce a second consecutive year of profitability for the Company as we continue to pursue our focused strategy and become a significant Cooper Basin oil and gas producer”. “Our ongoing strategic focus of increasing Reserves, production and cash flow has been the key to our positive growth across the Company, with record levels of production and sales revenues achieved during the year, as well as a 157% increase in 2P Reserves, as announced earlier this month”. “The excellent operational and financial results for the 2013 Financial year have established a strong platform from which Drillsearch will continue to grow in the coming year and beyond, evidenced by the almost doubling of our 2014 production guidance to 2.3–2.5 mmboe”. “We are well placed to add to the major achievements of the 2013 Financial year and reinforce our strong position as a high-growth Cooper Basin oil and gas explorer and producer.” FY 2013 RESULTS BRIEFING WEBCAST Managing Director, Brad Lingo and Chief Financial Officer, Ian Bucknell will host a results teleconference briefing that will take place at 11am (AEST) today. The briefing will also be streamed live on our website, through our BRR Media page which can be found with the following link http://www.drillsearch.com.au/page/brr-media

• Drillsearch delivers record net profit after tax of $45.1 million

• Sales revenue up 356% to $102.2 million

• Earnings up 147% to 11.1 cents per share

• Total production up 173% to 1.1 mmboe

• 2P Reserves up by 157% to 28.5 mmboe

• FY 2014 production guidance of 2.3–2.5 mmboe

For

per

sona

l use

onl

y

Teleconference dial-in details: All participants will be asked for their full name, company and passcode when joining the call. Pass code: 3033182 Australia: 1800 801 825 or +61 2 8524 5042 Hong Kong: 800 905 927 Malaysia: 1800 816 107 Singapore: 800 616 3222 UK: 0800 015 9725 US: 1855 298 3404 Yours faithfully, Brad Lingo Managing Director [email protected] Or visit the website www.drillsearch.com.au and register for email alerts Media enquiries to: Rebecca Lawson, Mercury Consulting, P: +61 2 8256 3332 E: [email protected] About Drillsearch Energy Limited (ASX: DLS), which listed on ASX in 1987, explores and develops conventional and unconventional oil and gas projects. Drillsearch has a strategic spread of petroleum exploration and production acreage in Australia’s most prolific onshore oil and gas province, the Cooper-Eromanga Basins in South Australia and Queensland. The company’s focus is on ‘brownfields’ exploration where geological risk is reduced and there is access to existing infrastructure, ensuring that any discoveries can be brought into production. Competent Person Statement Any reference to Reserves and Contingent Resources in this release follows guidelines set forth by the Society of Petroleum Engineers – Petroleum Resource Management System (SPE - PRMS). Information on the Reserves and Resources in this ASX Announcement have been compiled by Mr David Evans, Chief Technical Officer of Drillsearch Energy Limited, who is a qualified person as defined under ASX Listing Rule 5.11 and has given his consent as of the date of this ASX Announcement to the inclusion of these statements and the information in the form and the context in which it appears in this ASX Announcement. The Reserves and Contingent Resources used in this ASX Announcement were taken by Mr Evans from Independent Audited Reserve and Contingent Resource reports dated 30 June 2013 and prepared by DeGolyer and MacNaughton under the supervision of R. Michael Shuck, Senior Vice President and RISC under the supervision of Mr Geoffrey J Barker, Partner, both being qualified persons as defined in the ASX Listing Rule 5.11. RISC RISC is an independent advisory firm who works in partnership with companies to support their interests in the oil and gas industry. RISC offers the highest level of technical, commercial and strategic advice to clients around the world. RISC services include the preparation of independent reports for listed companies in accordance with regulatory requirements. RISC is independent with respect to Drillsearch in accordance with the Valmin Code, ASX listing rules and ASIC requirements." Information on the Reserves and Resources in this release relating to the PEL91, PRL14, 17, 18 and PEL101 assets is based on an independent review and audit conducted by RISC Operations Pty Ltd (RISC) and fairly represents the information and supporting documentation reviewed. The review and audit was carried out in accordance with the SPE Reserves Auditing Standards and the SPE-PRMS guidelines under the supervision of Mr. Geoffrey J Barker, a Partner of RISC, a leading independent petroleum advisory firm. Mr. Barker is a member of the SPE and his qualifications include a Master of Engineering Science (Petroleum Engineering) from Sydney University and more than 30 years of relevant experience. Mr. Barker meets the requirements of qualified petroleum reserve and resource evaluator and consents to the inclusion of this information in this report. DeGolyer and MacNaughton The information contained in our report entitled “Report as of December 31, 2012 on Reserves and Contingent Resources of Certain Fields in the PEL 106A, 106B, and 107 Permits of the Cooper Basin with interests owned by Drillsearch Energy Limited” has been prepared under the supervision of R. Michael Shuck, Senior Vice President of DeGolyer and MacNaughton. Mr. Shuck holds a Bachelor of Science degree in Chemical Engineering from the University of Houston, has in excess of 35 years of relevant experience in the estimation of reserves and contingent resources, is a member of the Society of Petroleum Engineers, and is a Registered Professional Engineer in the State of Texas. Mr. Shuck is a qualified person as defined in the ASX Listing Rule 5.11.

For

per

sona

l use

onl

y

FULL YEAR REPORT

Drillsearch Energy LimitedABN 73 006 474 844

For the year ended 30 June 2013 including Appendix 4E, Directors’ Report and Annual Financial Report

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Contents

Contents

Appendix 4E 1

Directors’ report 2

Remuneration report 14

Auditor’s independence declaration 27

Independent auditor’s report 28

Directors’ declaration 30

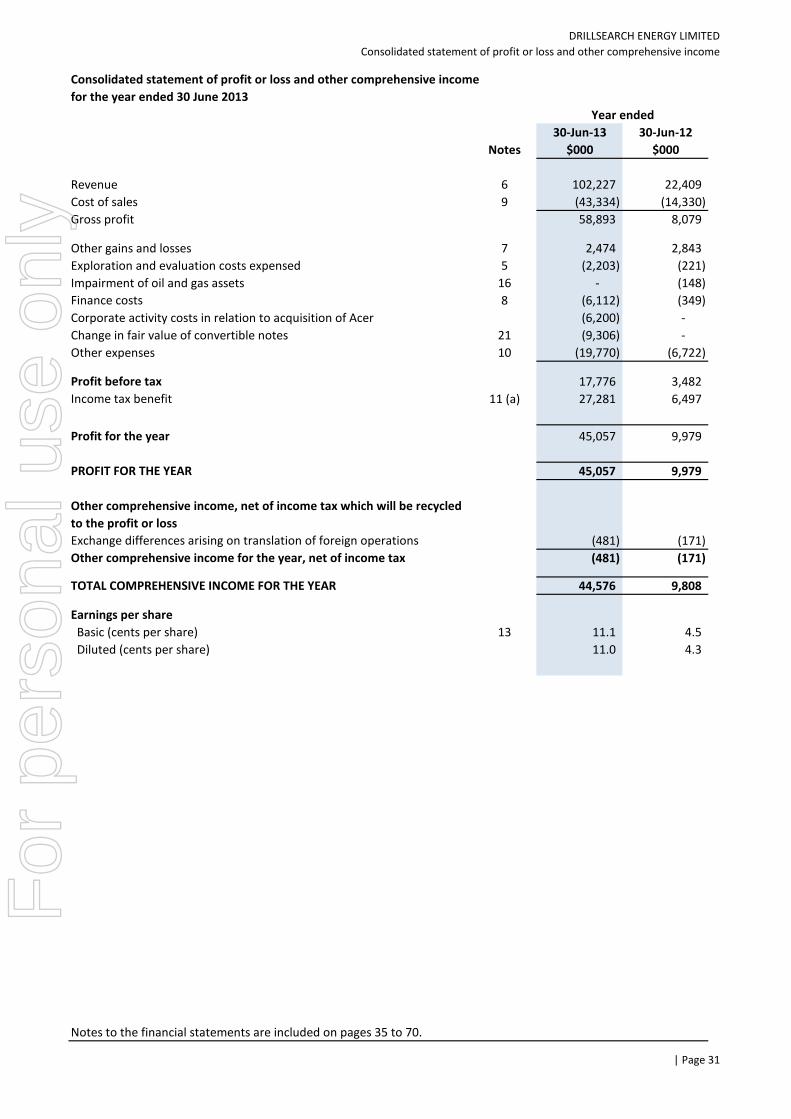

Consolidated statement of comprehensive income 31

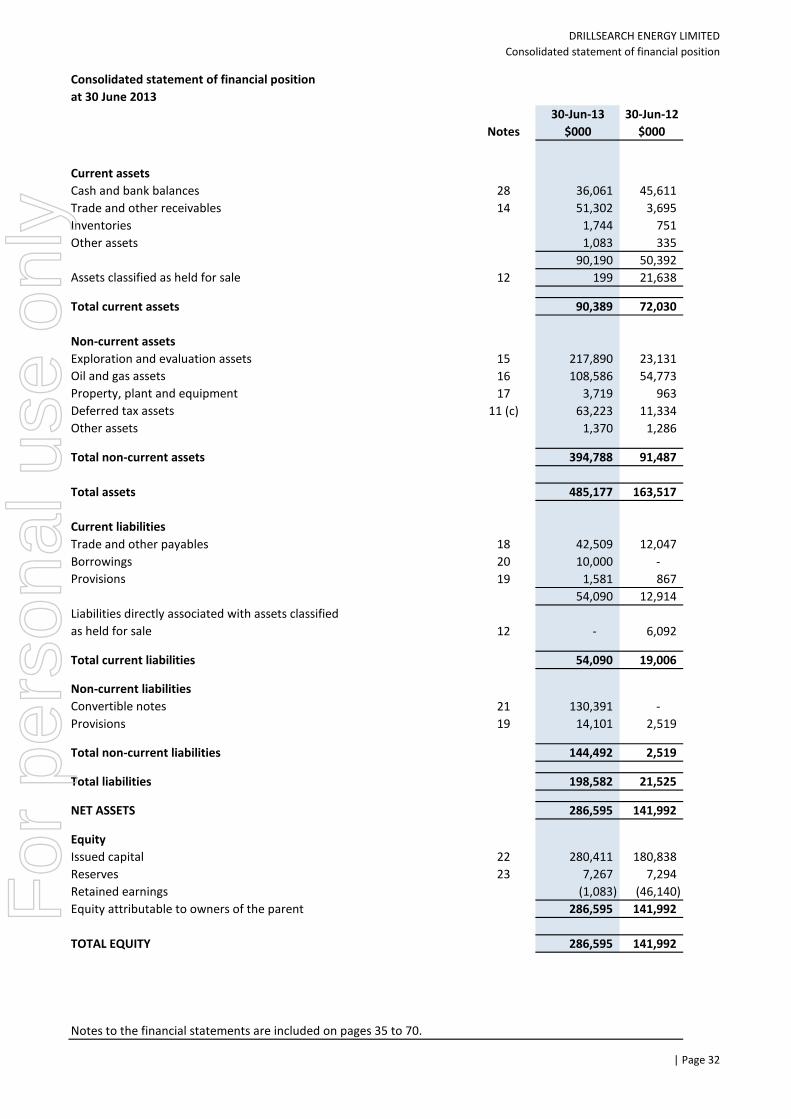

Consolidated statement of financial position 32

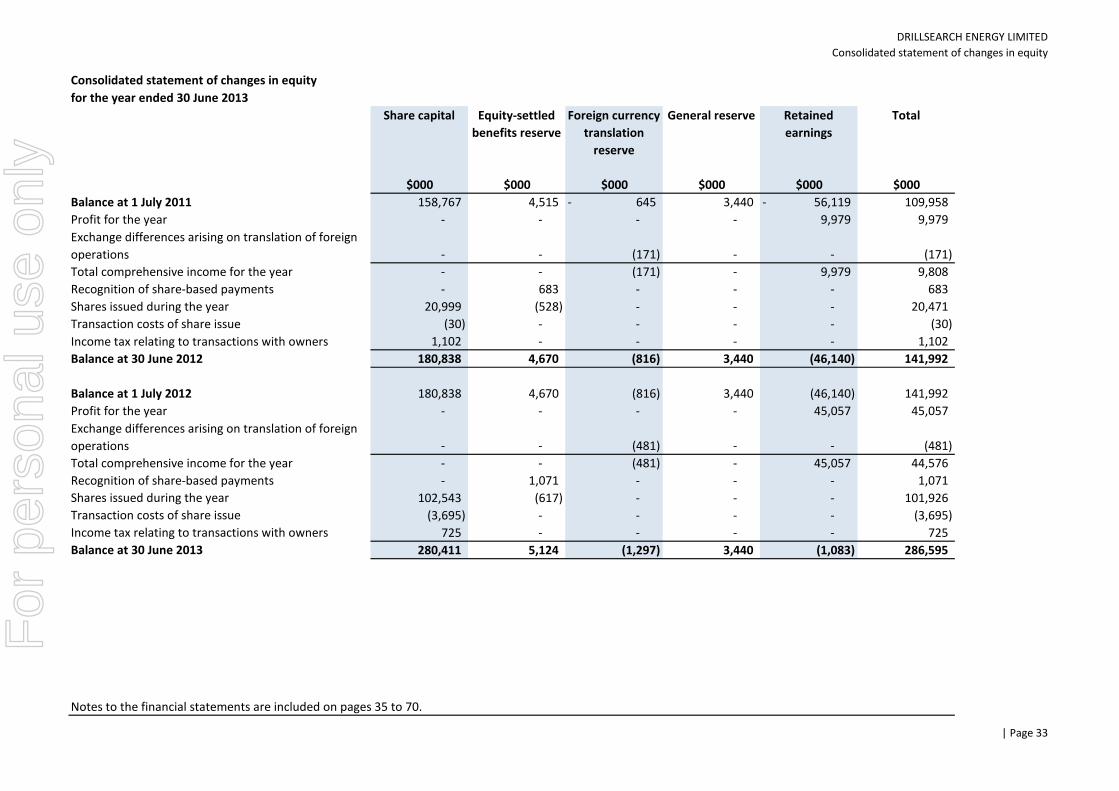

Consolidated statements of changes in equity 33

Consolidated statements of cash flows 34

Notes to the financial statements 35

Additional stock exchange information 71

Schedule of tenements 73

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

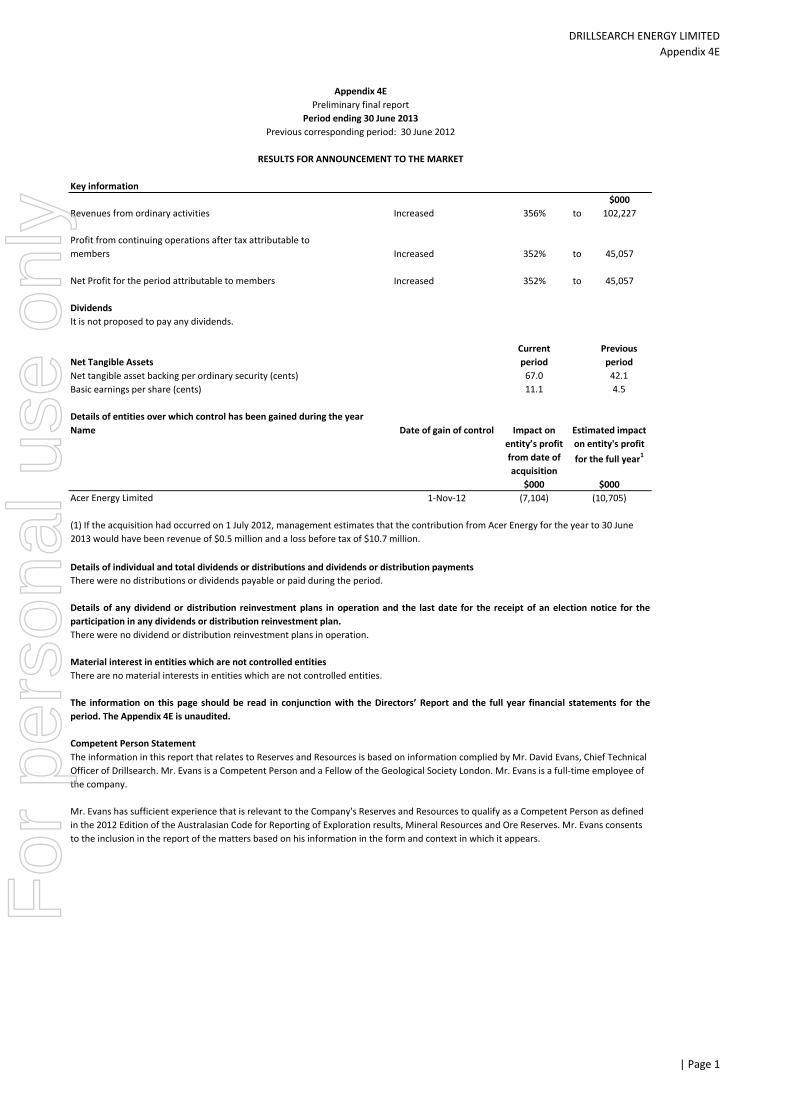

Appendix 4E

Key information

$000

Revenues from ordinary activities Increased 356% to 102,227

Profit from continuing operations after tax attributable to

members Increased 352% to 45,057

Net Profit for the period attributable to members Increased 352% to 45,057

Dividends

It is not proposed to pay any dividends.

Net Tangible Assets

Current

period

Previous

period

67.0 42.1

11.1 4.5

Details of entities over which control has been gained during the year

$000

Acer Energy Limited 1-Nov-12 (7,104)

There were no dividend or distribution reinvestment plans in operation.

Material interest in entities which are not controlled entities

There are no material interests in entities which are not controlled entities.

Competent Person Statement

Appendix 4E

Period ending 30 June 2013

Previous corresponding period: 30 June 2012

RESULTS FOR ANNOUNCEMENT TO THE MARKET

Preliminary final report

Mr. Evans has sufficient experience that is relevant to the Company's Reserves and Resources to qualify as a Competent Person as defined

in the 2012 Edition of the Australasian Code for Reporting of Exploration results, Mineral Resources and Ore Reserves. Mr. Evans consents

to the inclusion in the report of the matters based on his information in the form and context in which it appears.

(10,705)

Name

Details of any dividend or distribution reinvestment plans in operation and the last date for the receipt of an election notice for the

participation in any dividends or distribution reinvestment plan.

$000

The information on this page should be read in conjunction with the Directors’ Report and the full year financial statements for the

period. The Appendix 4E is unaudited.

Date of gain of control Impact on

entity’s profit

from date of

acquisition

Estimated impact

on entity's profit

for the full year1

There were no distributions or dividends payable or paid during the period.

(1) If the acquisition had occurred on 1 July 2012, management estimates that the contribution from Acer Energy for the year to 30 June

2013 would have been revenue of $0.5 million and a loss before tax of $10.7 million.

Details of individual and total dividends or distributions and dividends or distribution payments

Basic earnings per share (cents)

The information in this report that relates to Reserves and Resources is based on information complied by Mr. David Evans, Chief Technical

Officer of Drillsearch. Mr. Evans is a Competent Person and a Fellow of the Geological Society London. Mr. Evans is a full-time employee of

the company.

Net tangible asset backing per ordinary security (cents)

| Page 1

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

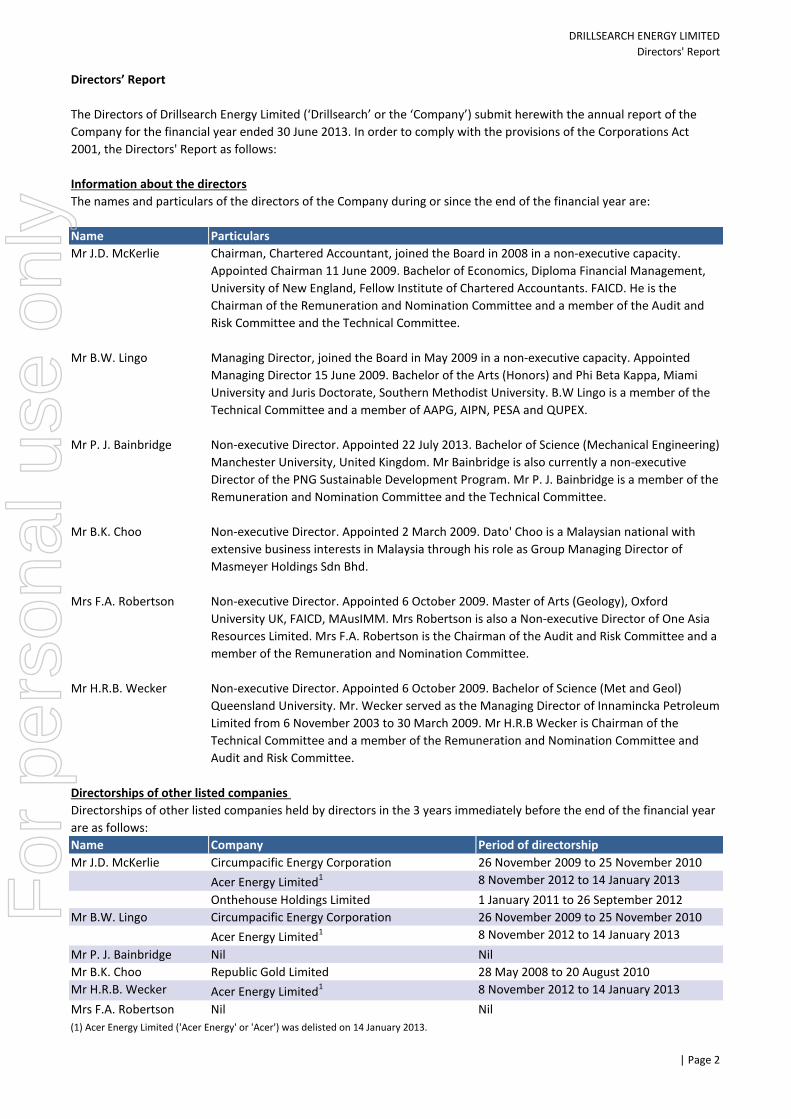

Directors' Report

Directors’ Report

Information about the directors

The names and particulars of the directors of the Company during or since the end of the financial year are:

Name Particulars

Mr J.D. McKerlie

Mr B.W. Lingo

Mr P. J. Bainbridge

Mr B.K. Choo

Mrs F.A. Robertson

Mr H.R.B. Wecker

Directorships of other listed companies

Name Company Period of directorship

Mr J.D. McKerlie Circumpacific Energy Corporation 26 November 2009 to 25 November 2010

Acer Energy Limited1 8 November 2012 to 14 January 2013

Onthehouse Holdings Limited 1 January 2011 to 26 September 2012

Mr B.W. Lingo Circumpacific Energy Corporation 26 November 2009 to 25 November 2010

Acer Energy Limited1 8 November 2012 to 14 January 2013

Mr P. J. Bainbridge Nil Nil

Mr B.K. Choo Republic Gold Limited 28 May 2008 to 20 August 2010

Mr H.R.B. Wecker Acer Energy Limited1 8 November 2012 to 14 January 2013

Mrs F.A. Robertson Nil Nil

(1) Acer Energy Limited ('Acer Energy' or 'Acer') was delisted on 14 January 2013.

Managing Director, joined the Board in May 2009 in a non-executive capacity. Appointed

Managing Director 15 June 2009. Bachelor of the Arts (Honors) and Phi Beta Kappa, Miami

University and Juris Doctorate, Southern Methodist University. B.W Lingo is a member of the

Technical Committee and a member of AAPG, AIPN, PESA and QUPEX.

The Directors of Drillsearch Energy Limited (‘Drillsearch’ or the ‘Company’) submit herewith the annual report of the

Company for the financial year ended 30 June 2013. In order to comply with the provisions of the Corporations Act

2001, the Directors' Report as follows:

Chairman, Chartered Accountant, joined the Board in 2008 in a non-executive capacity.

Appointed Chairman 11 June 2009. Bachelor of Economics, Diploma Financial Management,

University of New England, Fellow Institute of Chartered Accountants. FAICD. He is the

Chairman of the Remuneration and Nomination Committee and a member of the Audit and

Risk Committee and the Technical Committee.

Non-executive Director. Appointed 2 March 2009. Dato' Choo is a Malaysian national with

extensive business interests in Malaysia through his role as Group Managing Director of

Masmeyer Holdings Sdn Bhd.

Non-executive Director. Appointed 6 October 2009. Master of Arts (Geology), Oxford

University UK, FAICD, MAusIMM. Mrs Robertson is also a Non-executive Director of One Asia

Resources Limited. Mrs F.A. Robertson is the Chairman of the Audit and Risk Committee and a

member of the Remuneration and Nomination Committee.

Non-executive Director. Appointed 6 October 2009. Bachelor of Science (Met and Geol)

Queensland University. Mr. Wecker served as the Managing Director of Innamincka Petroleum

Limited from 6 November 2003 to 30 March 2009. Mr H.R.B Wecker is Chairman of the

Technical Committee and a member of the Remuneration and Nomination Committee and

Audit and Risk Committee.

Directorships of other listed companies held by directors in the 3 years immediately before the end of the financial year

are as follows:

Non-executive Director. Appointed 22 July 2013. Bachelor of Science (Mechanical Engineering)

Manchester University, United Kingdom. Mr Bainbridge is also currently a non-executive

Director of the PNG Sustainable Development Program. Mr P. J. Bainbridge is a member of the

Remuneration and Nomination Committee and the Technical Committee.

| Page 2

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

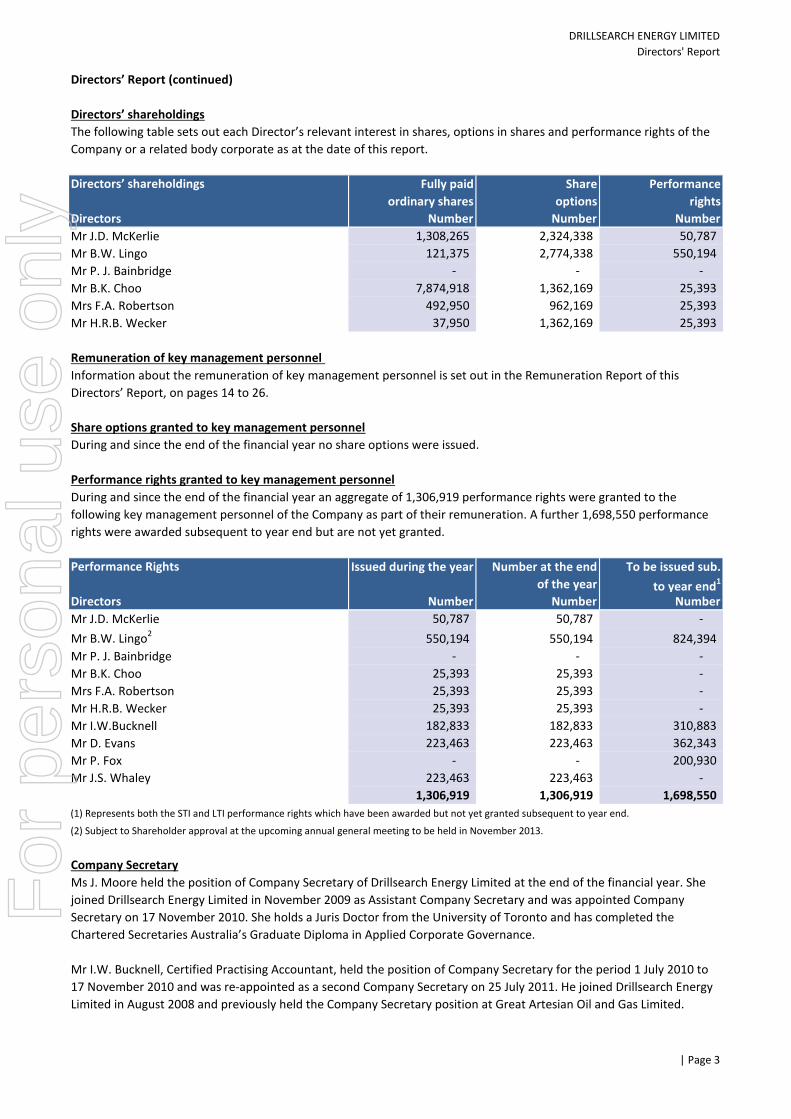

Directors’ shareholdings

Directors’ shareholdings

Directors

Mr J.D. McKerlie

Mr B.W. Lingo

Mr P. J. Bainbridge

Mr B.K. Choo

Mrs F.A. Robertson

Mr H.R.B. Wecker

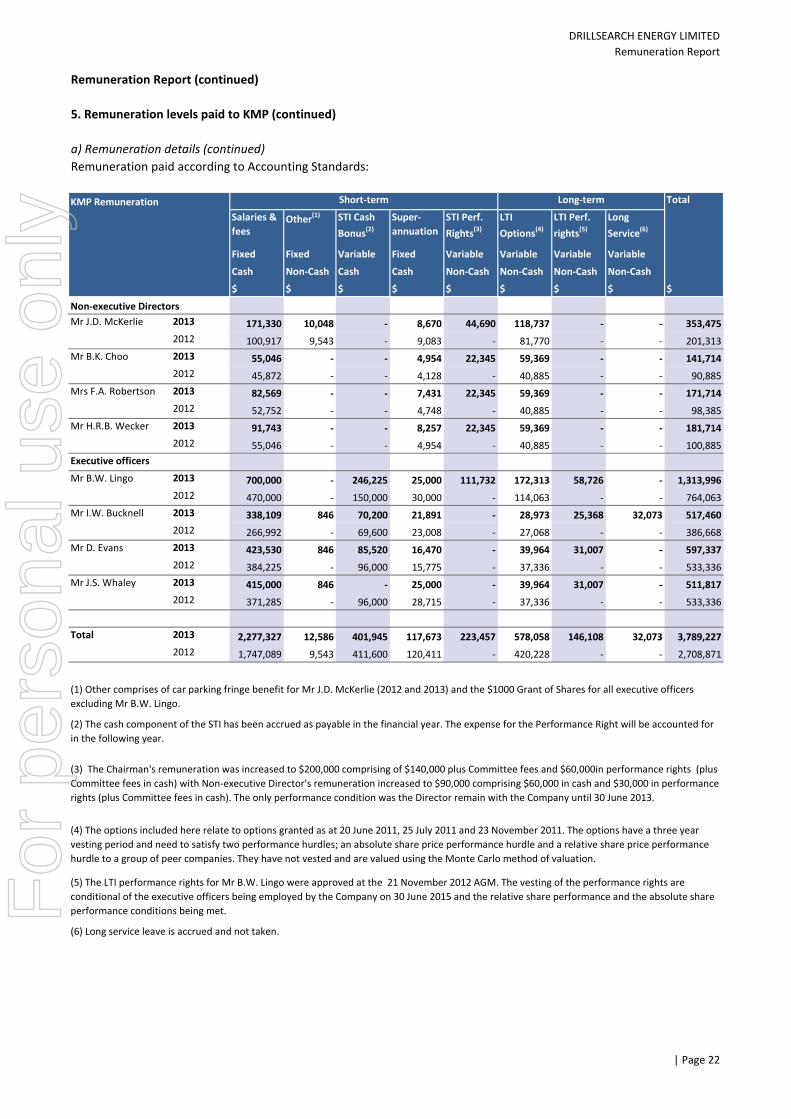

Remuneration of key management personnel

Share options granted to key management personnel

During and since the end of the financial year no share options were issued.

Performance rights granted to key management personnel

Performance Rights

Directors

Mr J.D. McKerlie

Mr B.W. Lingo2

Mr P. J. Bainbridge

Mr B.K. Choo

Mrs F.A. Robertson

Mr H.R.B. Wecker

Mr I.W.Bucknell

Mr D. Evans

Mr P. Fox

Mr J.S. Whaley

(1) Represents both the STI and LTI performance rights which have been awarded but not yet granted subsequent to year end.

(2) Subject to Shareholder approval at the upcoming annual general meeting to be held in November 2013.

Company Secretary

The following table sets out each Director’s relevant interest in shares, options in shares and performance rights of the

Company or a related body corporate as at the date of this report.

1,308,265 2,324,338 50,787

121,375 2,774,338 550,194

Fully paid

ordinary shares

Number

Share

options

Number

Performance

rights

-

25,393 25,393

- -

Information about the remuneration of key management personnel is set out in the Remuneration Report of this

Directors’ Report, on pages 14 to 26.

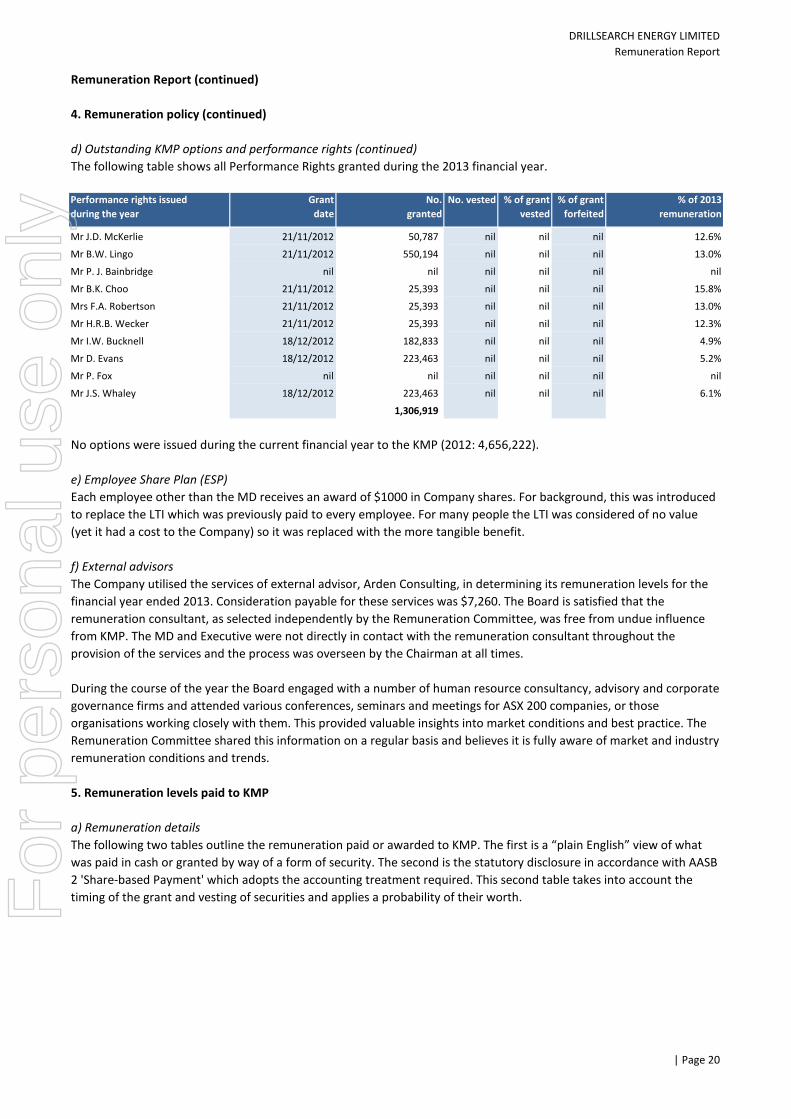

During and since the end of the financial year an aggregate of 1,306,919 performance rights were granted to the

following key management personnel of the Company as part of their remuneration. A further 1,698,550 performance

rights were awarded subsequent to year end but are not yet granted.

50,787 50,787

37,950 1,362,169 25,393

492,950 962,169

824,394

-

-

25,393

Issued during the year Number at the end

of the year

Number Number

- -

Number

-

7,874,918 1,362,169 25,393

550,194 550,194

182,833 182,833

223,463 223,463

223,463 223,463

25,393 25,393

25,393 25,393

To be issued sub.

to year end1

Number

- - 200,930

-

-

-

362,343

310,883

1,698,550

Ms J. Moore held the position of Company Secretary of Drillsearch Energy Limited at the end of the financial year. She

joined Drillsearch Energy Limited in November 2009 as Assistant Company Secretary and was appointed Company

Secretary on 17 November 2010. She holds a Juris Doctor from the University of Toronto and has completed the

Chartered Secretaries Australia’s Graduate Diploma in Applied Corporate Governance.

Mr I.W. Bucknell, Certified Practising Accountant, held the position of Company Secretary for the period 1 July 2010 to

17 November 2010 and was re-appointed as a second Company Secretary on 25 July 2011. He joined Drillsearch Energy

Limited in August 2008 and previously held the Company Secretary position at Great Artesian Oil and Gas Limited.

1,306,919 1,306,919

| Page 3

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

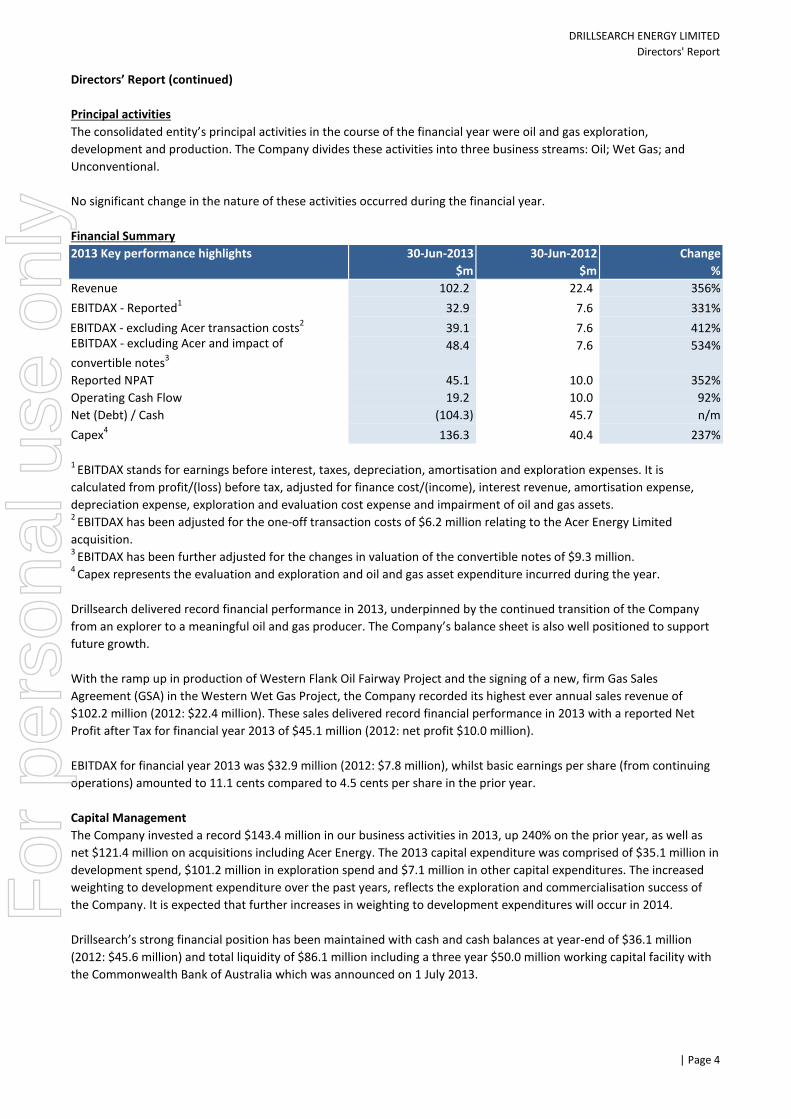

Principal activities

No significant change in the nature of these activities occurred during the financial year.

Financial Summary

2013 Key performance highlights

Revenue

EBITDAX - Reported1

EBITDAX - excluding Acer transaction costs2

Reported NPAT

Operating Cash Flow

Net (Debt) / Cash

Capex4

Capital Management

EBITDAX - excluding Acer and impact of

convertible notes3

3 EBITDAX has been further adjusted for the changes in valuation of the convertible notes of $9.3 million.

356%

The consolidated entity’s principal activities in the course of the financial year were oil and gas exploration,

development and production. The Company divides these activities into three business streams: Oil; Wet Gas; and

Unconventional.

2 EBITDAX has been adjusted for the one-off transaction costs of $6.2 million relating to the Acer Energy Limited

acquisition.

136.3 40.4 237%

1 EBITDAX stands for earnings before interest, taxes, depreciation, amortisation and exploration expenses. It is

calculated from profit/(loss) before tax, adjusted for finance cost/(income), interest revenue, amortisation expense,

depreciation expense, exploration and evaluation cost expense and impairment of oil and gas assets.

102.2 22.4

Change

%

10.0 352%

32.9 7.6 331%

39.1 7.6 412%

n/m45.7 (104.3)

92%10.0 19.2

Drillsearch delivered record financial performance in 2013, underpinned by the continued transition of the Company

from an explorer to a meaningful oil and gas producer. The Company’s balance sheet is also well positioned to support

future growth.

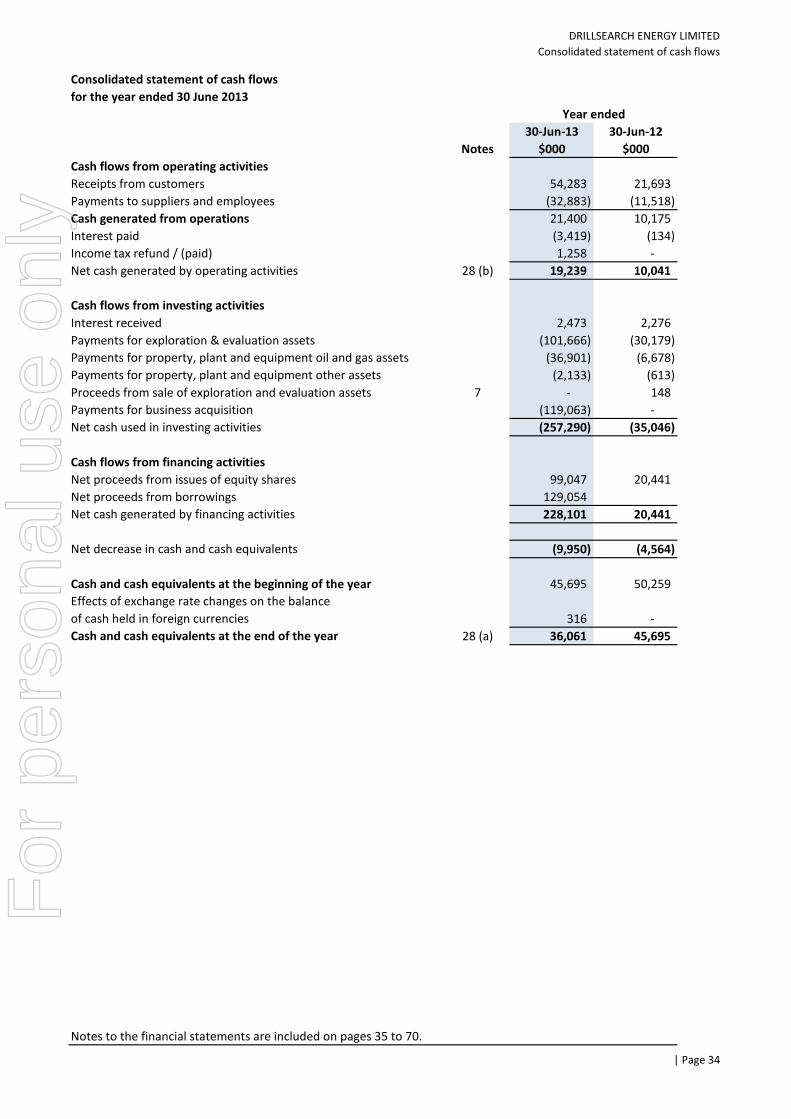

Drillsearch’s strong financial position has been maintained with cash and cash balances at year-end of $36.1 million

(2012: $45.6 million) and total liquidity of $86.1 million including a three year $50.0 million working capital facility with

the Commonwealth Bank of Australia which was announced on 1 July 2013.

48.4 7.6 534%

30-Jun-2013 30-Jun-2012

$m $m

The Company invested a record $143.4 million in our business activities in 2013, up 240% on the prior year, as well as

net $121.4 million on acquisitions including Acer Energy. The 2013 capital expenditure was comprised of $35.1 million in

development spend, $101.2 million in exploration spend and $7.1 million in other capital expenditures. The increased

weighting to development expenditure over the past years, reflects the exploration and commercialisation success of

the Company. It is expected that further increases in weighting to development expenditures will occur in 2014.

With the ramp up in production of Western Flank Oil Fairway Project and the signing of a new, firm Gas Sales

Agreement (GSA) in the Western Wet Gas Project, the Company recorded its highest ever annual sales revenue of

$102.2 million (2012: $22.4 million). These sales delivered record financial performance in 2013 with a reported Net

Profit after Tax for financial year 2013 of $45.1 million (2012: net profit $10.0 million).

EBITDAX for financial year 2013 was $32.9 million (2012: $7.8 million), whilst basic earnings per share (from continuing

operations) amounted to 11.1 cents compared to 4.5 cents per share in the prior year.

4 Capex represents the evaluation and exploration and oil and gas asset expenditure incurred during the year.

45.1

| Page 4

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Financial Summary (continued)

Capital Management (continued)

Review of operations

Corporate Strategy

Our vision is to become a leading Australian mid-tier oil and gas exploration and production company.

To achieve this vision we will:

2013 in review

On the corporate front financial year 2013 has been an extremely busy time. The Company has:

2014 – The year ahead

A summary of consolidated revenues and results of significant segments is set out in Note 6 of the financial report.

Working capital has increased during the year by $8.6 million to $46.6 million (2012: $38.0 million) due to a net increase

of $17.0 million in trade receivables and payables at year end offset by the movement in cash. Cash and bank balances

at year end decreased to $36.1 million (2012: $45.6 million). The increase in trade receivables reflects the significant

ramp up in production as a result of the commissioning of the Bauer-to-Lycium Oil Export Pipeline in May and increased

oil sales in the closing month of the period. This was offset by an increase in trade payables due to the high degree of

capital activity occurring over the close of the period.

• Pursue attractive opportunities to expand our acreage position either through the acquisition of assets directly or

through mergers throughout Central Australia complementary to the Company’s existing Cooper Basin holdings.

• Successfully completed two $50 million equity raisings;

• Completed an all-cash takeover offer of Acer Energy significantly expanding the Company’s position in the

Western Flank Oil Fairway and delivering a new growth project now identified as the Northern Wet Gas Project;

• Put in place a $100 million acquisition bridge facility with the Commonwealth Bank of Australia ('CBA');

• Develop and commercialise the Company’s significant unconventional gas potential resource; and

• Explore and develop the Company’s Cooper Basin acreage for conventional oil and gas;

The net assets of the consolidated group have increased by $143.6 million from 30 June 2012 to $256.1 million (2012:

$142.0 million). This increase is mainly the result of the acquisition of Acer Energy and capitalised exploration and

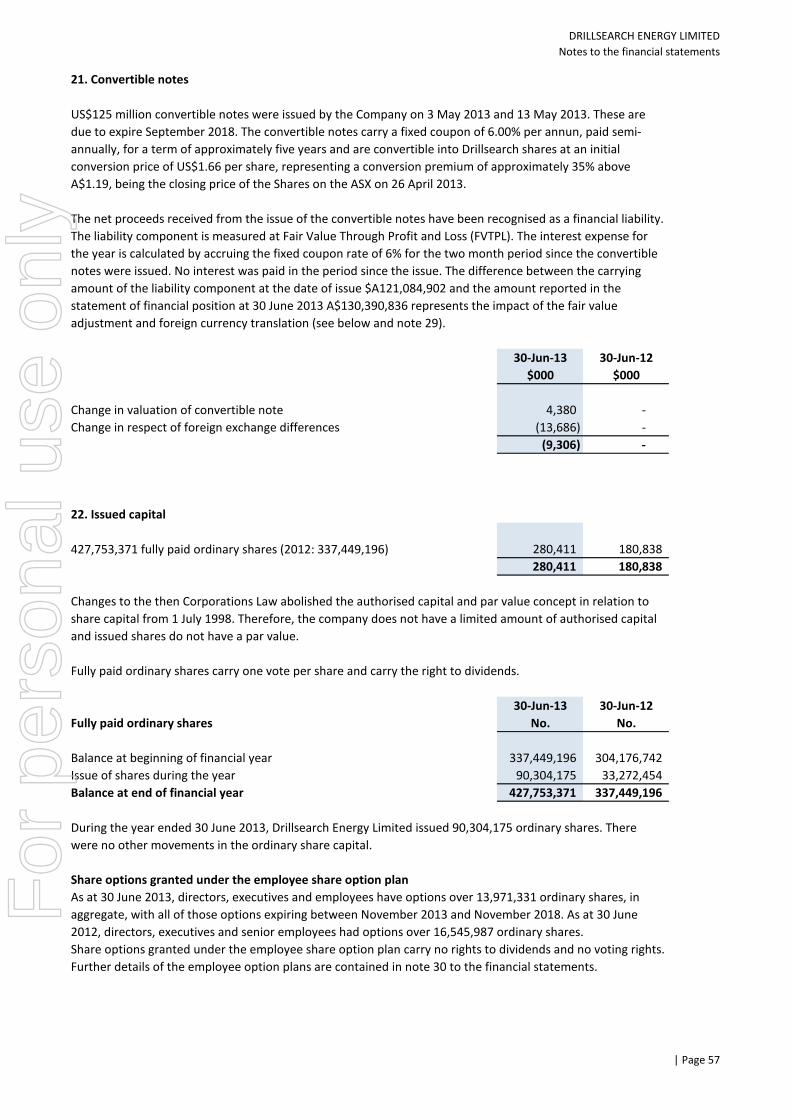

development expenditure. This was offset by US$125 million convertible notes which were issued by the Company (on 3

May 2013 and 13 May 2013). The convertible notes carry a fixed coupon of 6.00% per annum, paid semi-annually, for a

term of approximately five years and are convertible into Drillsearch shares at a conversion price of US$1.66 per share.

This represents a conversion premium of approximately 35% above $1.19, being the closing price of the Shares on the

ASX on 26 April 2013.

Cash flows generated from operating activities amounted to $19.2 million, a 92% increase compared to the prior year

(2012: $10.0 million). Drillsearch also raised a further $100 million through the issue of equity shares which was utilised

to fund the Company’s significant 2013 financial year investment activities.

• Executed a US$125 million convertible note to help refinance the acquisition bridge;

• Established a long term $50 million working capital facility; and

• Subsequent to year end announced a series of binding transactions with Santos Limited ('Santos') to accelerate

Western Cooper Wet Gas commercialisation and expanding Drillsearch’s Cooper Basin Oil Reserves and production.

We believe that we have a strong balance sheet and liquidity capable of supporting organic opportunities within our

portfolio. We will continue to look to deliver on our vision.

| Page 5

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Review of operations (continued)

Oil Business

Strategy

We do this by:

2013 in review

The overall focus of the Oil Business is to rapidly grow conventional oil reserves, production and cash flow generated

within this business. This focus is based on the exploration, development and production of conventional oil in proven

fairways within Central Australia.

The financial year has seen continued success for the Western Flank Oil Fairway Project where the Company has

substantial permit holdings in PEL 91 and PEL 182. This success can be measured by the Company’s delivery of strong

growth in 2P Oil Reserves and oil production from the Western Flank Oil Fairway. These increases were driven by

extensive appraisal/development and exploration drilling programs in the PEL 91 permit with seven successful

appraisal/development wells in the Bauer Oil Field and four new oil discoveries in PEL 91. Drilling programme success

rates continued to be high in the financial year with 100% success in appraisal/development drilling and 80% success in

exploration drilling.

Of the seven appraisal/development wells drilled in PEL 91 during the financial year, all were cased and suspended as

future oil producers in the Bauer Oil Field. Currently eight wells, Bauer-1 to Bauer-8, are connected and producing into

the Bauer Central Oil Production Facility. Four Bauer development wells - Bauer 9 to 11 and Bauer North-1 - have been

completed and are awaiting connection to the Bauer Central Oil Production Facility. Throughout the financial year,

production from the Chiton and Hanson oil fields was trucked directly to Moomba.

Of the five exploration wells drilled in the Western Flank Oil Fairway PEL 91 permit area, four wells - Pennington-1,

Kalladeina-2, Sceale-1 and Congony-1 - are new oil discoveries and each was cased and suspended as a future

production well. Smoky-1, an exploration well in PEL 91, was plugged and abandoned after encountering water in the

primary and secondary targets. All wells were drilled on 3D seismic and continue to highlight the benefits of utilising 3D

seismic acquisition to help unlock the potential of this play.

The Oil Business is comprised of three main project areas, the Western Flank Oil Fairway Project (PELs 91 and 182), the

Eastern Margin Oil Fairway Project (Tintaburra Block Joint Venture ('JV') and ATP 783P) and the Inland-Cook Oil Fairway

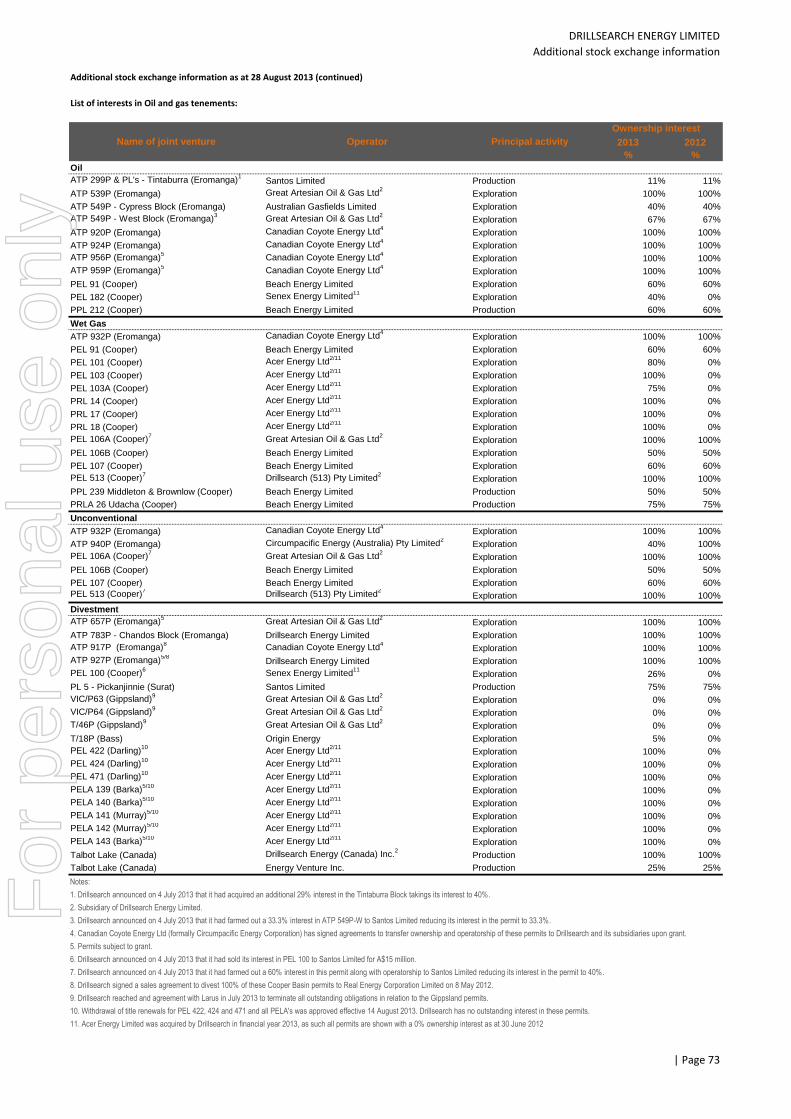

Project (ATPs 539P, 549P, 920P and 924P). In the Western Flank Oil Fairway Project, PEL 91 is held in joint venture

between the Company (60%) and Beach Energy Limited ('Beach Energy')(40% and operator) and PEL 182 is held in joint

venture between the Company (40%) and Senex Energy Limited (52. 5% and operator).

In the Eastern Margin Oil Fairway Project, the Tintaburra Block JV is held in joint venture between the Company (11%)

and Santos (89% and operator). In the Tintaburra Block JV the Company announced on 4 July 2013 that it had entered

into a binding agreement with Santos to increase its interest in the JV to 40% through acquiring an additional 29%

working interest in the JV for $38 million.

• Holding acreage positions in those fairways and building off of our existing positions to look to secure additional

acreage;

• Systematically exploring in proven fairways through the application of advanced 3D seismic and other

technologies;

• Fast tracking the development of discoveries through fit for purpose development solutions and once scale is

achieved committing to centralised production and transportation infrastructure to deliver secure, low cost

production on a long-term basis.

During the year the Company as part of the PEL 91 JV also completed the 485km2 Caseolus 3D seismic survey. The data

set is currently being processed. This 3D seismic data set together with those previously acquired by the PEL 91 JV now

means that 59% of the block has been covered in 3D seismic providing an extensive seriatim of 3D defined prospects

and leads.

| Page 6

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Review of operations (continued)

Oil Business (continued)

2013 in review (continued)

Oil Reserves and production

2014 – The year ahead

Wet Gas Business

Strategy

In the Eastern Margin Oil Fairway Project the Company is focusing on further field development and exploration

activities. These include:

Work program activities also continued in other permits. In the Eastern Margin Oil Fairway Project, the Company as part

of the Tintaburra Block JV, drilled four wells during the financial year - one exploration well, two appraisal wells and one

development well. Two wells were cased and suspended as future oil producers with the other two plugged and

abandoned. In the Inland-Cook Oil Fairway Project , the Company acquired the 600km2 Kaden 3D seismic survey

covering the southern portion of ATP 539P and the northern portion of the adjacent ATP 549P permit. Based on the

Kaden 3D, the Company drilled two permit commitment wells in ATP 539P (Triclops-1 and Tibor- 1). Minor oil shows

were encountered in poor quality reservoir in the Tibor-1 well. Both exploration wells were plugged and abandoned.

• Completion of the previously announced acquisition of an additional 29% interest in the Tintaburra Block JV from

Santos;

In the Western Flank Oil Fairway Project, following the success of 2013, the Company is embarking on further appraisal,

development and exploration activities. These include the:

• Drilling of seven exploration wells and seven appraisal/development wells in the PEL 91 Permit;

The overall focus of the Wet Gas Business is to rapidly grow conventional wet gas Reserves, production and cash flow

within this Business. This focus is based on the exploration, development and production of conventional wet gas in

proven fairways within Central Australia.

• Development of existing new oil discoveries in the Western Flank Oil Fairway in the PEL 91 Permit;

• Acquisition, processing and interpretation of additional 3D seismic in the PEL 182 Permit.

• Upgrade and expansion of the Bauer Central Oil Production Facility to maintain current production levels and to

accommodate increased production from the Bauer Oil Field; and

• Development drilling and the reinstatement of long-term inactive production wells with a focus on maintaining

and increasing oil production in the Tintaburra Block JV;

• Upgrading, expansion and refurbishment of production facilities in the Tintaburra Block; and

• Securing joint venture partners in the Eastern Margin Oil Fairway Project ATP 783 Permit area and commencing a

focused 3D seismic acquisition program across the northern area of the permit in the vicinity of the Chandos and

Chandos South oil exploration wells which successfully drill stem tested oil in earlier exploration programs.

On 15 August 2013, Drillsearch announced its 30 June 2013 Reserves. They included a 145% increase in the 2P Reserves

for the combined PEL 91 Oil Fields in the Western Flank Oil Fairway increasing to 7.6 mmboe (net) (30 June 2012 – net

3.1 mmboe). 2P Reserves in the Eastern Margin Oil Fairway decreased by 0.05 mmboe as a result of production in the

period.

For most of the financial year oil production from the Bauer, Hanson and Chiton oil fields was constrained to available

trucking capacity. Construction of the Bauer-to-Lycium Oil Export Pipeline commenced in December 2012 and the

pipeline was commissioned to increase overall oil production and ensure production reliability. Completion of this

pipeline has helped to significantly remove the earlier transportation constraints on production from the Bauer Oil Field

and dramatically increase oil export capacity. Commercial operation commenced in May 2013 and the pipeline is

currently operating at its nameplate capacity of 10,000 bbls per day (gross). Chiton and Hanson oil field production

continues to be exported to Moomba by truck with additional production volumes from the Bauer oil field, in excess of

pipeline capacity, also being exported by truck.

| Page 7

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Review of operations (continued)

Wet Gas Business (continued)

Strategy (continued)

We do this by:

• Utilising our corporate capability to appraise, develop and commercialise Wet Gas; and

2013 in review

During the year, the PEL 106B JV successfully conducted extended production testing (EPT’s) of the Coolawang and

Haslam Wet Gas discoveries in PEL 106B and the Southend Wet Gas discovery in PEL 107. All three wells were part of

the successful Western Wet Gas Fairway Project exploration program undertaken during the 2012 financial year.

During the financial year, the Company pursued an active exploration drilling and seismic acquisition program in the

100% owned and operated areas within the Western Wet Gas Project. The Company drilled three exploration wells in

PEL 106A (Wamberal-1, Moruya-1 and Narrabeen-1). The Wamberal-1 exploration well was plugged and abandoned

after failing to intersect commercial quantities of wet gas in conventional or tight gas sands. Moruya-1 was cased and

suspended for further evaluation as a new wet gas discovery after intersecting gas and liquids saturated tight sands.

Narrabeen-1 was also cased and suspended for future appraisal and development as a new wet gas discovery after

intersecting gas and liquids saturated in conventional and tight sands. In PEL 106A and PEL 513 work programs

continued with Santos acquiring the 385km2 Andree Leleptian 3D seismic survey and in PEL 513 Drillsearch acquired the

320km2 Munathiri 3D seismic survey.

In January 2013, the Company successfully completed the compulsory acquisition of Acer Energy which subsequently

became a wholly-owned subsidiary of Drillsearch. One of the primary drivers of the acquisition was the prospectivity of

Acer’s Wet Gas assets, including the existing wet gas discoveries in PEL 101, PEL 103 and PRLs 14, 17 and 18. The

acquisition of these permit areas, formed the basis for the Company establishing the Northern Wet Gas Project. Acer

commenced the drilling of the Cypress-1 wet gas exploration well in December 2012 in PEL 103. Upon gaining control of

Acer, the Company took over supervision of the Cypress drilling program and suspended drilling of the well due to

downhole issues.

In the Northern Wet Gas Project area, as part of focusing on accelerating development and exploration in the PEL 101

permit, the Company also undertook the 478km2 Coolabah 3D seismic program covering the majority of the PEL 101

permit area and the Ginko, Crocus and Crocus South Wet Gas discoveries as well as ten wet gas exploration leads and

prospects previously identified in PEL 101.

The PEL 106B JV also drilled four wet gas exploration wells in the period. Coorabie-1 was cased and suspended for

future technical studies to assess the potential for unconventional gas. The Rosetta-1, Destress-1 and Euler-1

exploration wells all encountered gas in tight sands and associated with deep coal seams but failed to encounter

significant gas quantities in conventional reservoir quality sands. All of these wells were plugged and abandoned.

• Holding acreage positions in those fairways and building off of our existing positions to look to secure additional

acreage;

• Systematically exploring in proven fairways through the application of advanced 3D seismic and other

technologies;

• Developing key joint venture and customer relationships that secure long-term gas commercialisation pathways.

The Wet Gas Business is comprised of two main project areas, the Western Wet Gas Project (PELs 106A, 106B, 107 &

513) and the Northern Wet Gas Project (PELs 101, 103 and PRLs 14, 17 and 18). In the Western Wet Gas Project, the PEL

106B and PEL 107 permit area are held in JV between the Company (PEL 106B- 50% / PEL 107- 60%) and Beach Energy

(PEL 106B-50% / PEL 107- 40% and operator). The PEL 106B JV also contains the Middleton Gas Project. During the

financial year the PEL 106A and 513 permit areas of the Western Wet Gas Project were held 100% by the Company. On

4 July 2013 the Company announced that it had entered into a binding agreement with Santos to joint venture this

acreage (Drillsearch 40%, Santos 60% and operator) in order to accelerate the exploration potential and

commercialisation of existing discoveries in these permits. In the Northern Wet Gas Project, the Company operates and

holds the PEL 103 and PRLs 14, 17 and 18 on a 100% basis and operates and holds an 80% interest in the PEL 101

permit.

| Page 8

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Review of operations (continued)

Wet Gas Business (continued)

Wet Gas Reserves and Production

2014 – The year ahead

Unconventional Business

Strategy

Subsequent to the year end, Drillsearch announced on 4 July 2013 that it had entered into a series of binding

transactions with Santos Limited to accelerate Western Cooper Wet Gas development and commercialisation. Santos

will acquire a 60% interest and operatorship for the PEL 106A and PEL 513 permit areas of the Western Cooper Wet Gas

project (PEL 106A and PEL 513) through committing to fund a work program valued by Drillsearch at $100-120 million.

These include:

• PEL 106A – funding a $75 million firm work program of exploration, appraisal and field development works; and

On 15 August 2013, Drillsearch announced its 30 June 2013 Reserves. They included a 170% increase in the combined 2P

Reserves for the Wet Gas Business increasing to 20.3 mmboe (net) (30 June 2012 – net 7.5 mmboe). This increase has

been driven by Reserves additions in the Middleton and Brownlow Wet Gas Fields based on continuing field production

results and by the conversion of 2C Resources to 2P Reserves for the wet gas discoveries in PEL 106A. The independent

Reserve audit as of 30 June 2013, upgraded all of the wet gas discoveries in PEL 106A to Reserves from their previous

classification as Contingent Resources based on the Company securing new gas sale arrangements with the South

Australian Cooper Basin JV ('SACBJV') and Santos accepting the commerciality of these discoveries.

The Middleton Gas Project in PEL 106B was in continuous production from early January 2012 until 1 October 2012

when the field was shut-in. This was due to constraints as a result of ongoing gathering system pipeline expansion works

by the SACBJV associated with the development of the Greater Tindilpie Gas Field Complex.

• Processing and interpretation of 3D seismic.

• PEL 513 – funding a firm work program valued by Drillsearch at $45 million covering all of the outstanding firm

permit work commitments including acquiring 100km2 3D seismic, and drilling six firm commitment exploration

wells.

Production re-commenced from the field on 17 March 2013 when a new three-year firm Gas Sales Agreement (GSA)

with the SACBJV was signed. The GSA provides for the sale of 10 BCF of raw gas on a firm basis for a three-year term

with a Maximum Daily Quantity (MDQ) up to 35 mmscfd of raw gas. Under the GSA the Joint Venture sells untreated

raw gas consisting of condensate, LPG and sales gas, and is paid for each component. Condensate and LPG pricing is

linked to international product pricing, less specific transport and processing charges. Gas sales are priced on a

confidential fixed price basis, reflecting transport and processing costs of the SACBJV in producing sales gas quality for

onward sale. The additional gas sales underpin the expansion of the Western Cooper Wet Gas Project to increase overall

production capacity via the completion and connection of the Canunda Wet Gas Field (completed in June 2013).

• Completing, testing and commencing production from wet existing gas discoveries in the PEL 106A permit area of

the Western Wet Gas Project;

• Expansion of the Western Wet Gas Project through the development and commencement of production from the

Coolawang wet gas discovery by connecting it to the Middleton Gas Plant;

• Reinstatement of production in the Northern Wet Gas Project from the Flax Field and commencing the

development of the Yarrow wet gas discovery through connection to the Flax Production Plant; and

• Drilling of exploration, appraisal and development wells across both the Western and Northern Wet Gas Project

areas;

The overall focus of the Unconventional Business is to prove within the Company’s existing conventional acreage

positions the presence, prevalence and producibility of unconventional oil and gas resources of known hydrocarbons

within Central Australia. Our approach is the systematic exploration and appraisal of known hydrocarbons in our

existing acreage with a view to establishing the presence of substantial Contingent Resources and ultimately that these

resources can be produced on a commercially sustainable basis.

| Page 9

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Review of operations (continued)

Unconventional Business (continued)

Strategy (continued)

We do this by:

2013 in review

2014 – The year ahead

Active Portfolio management

Drillsearch and its JV partners are embarking on further appraisal, development and exploration activities. These

include:

In the Wet Gas Business, the Company formed a new JV with Santos to accelerate the exploration and development of

the Western Wet Gas Project through farming down a portion of the Western Wet Gas Project area (PEL 106A and PEL

513) and entering into a long-term gas sale agreement providing for sale of production from the project area through

2025.

The ATP 940P JV has agreed on well locations for the first four exploration wells to be drilled. Site preparations are well

underway for the multi-well drilling program expected to start during the December 2013 quarter.

• Developing and executing work programs targeted at proving the presence, magnitude and producibility of these

resources; and

The Central Cooper Unconventional Resource Project is focused on the ATP 940P permit which is located within the

Nappamerri Trough Shale Gas Fairway in Southwest Queensland. Drillsearch has formed a JV with QGC Pty Limited (BG

Group) to explore, appraise and develop these unconventional resources within ATP 940P. The Company holds a 40%

interest in the Project and is operator and the remaining 60% interest is held by QGC. The ATP 940P block is located

immediately adjacent to Beach Energy and Chevron’s unconventional resource project in PEL 218 and ATP 855P where

their drilling exploration and appraisal testing programs are currently underway.

• Drilling, coring, testing and completing unconventional exploration wells in the Central Unconventional Fairway to

define both shale gas and tight basin centred gas resources;

• Processing and interpretation of the Winnie 3D seismic survey;

• Determine if the Company should also establish a new unconventional project within the Northern Cooper Wet

Gas Project in the PEL 101 permit.

• Re-entry and stimulation of tight sands and deep coals in the Western Cooper Unconventional Project area; and

The Unconventional Business is comprised of two main project areas, the Central Cooper Unconventional Resource

Project (ATP 940P and ATP 932P) and the Western Unconventional Resource Project (PEL 106A and PEL 513). The

potential for additional unconventional resources have also been identified in association with the Northern Cooper

Wet Gas Project principally within the PEL 101 permit area but the Company has not yet formally established a separate

project based on this identified unconventional resource potential.

• Specifically targeting identified shale, tight gas and basin centred gas as well as liquids rich Unconventional

resource plays;

• Securing appropriate JV Partners that deliver commercialisation pathways, access to technology and technical

expertise and capital necessary to fully explore, appraise and develop these resources.

During the year, the Company’s focus in the Unconventional Business was in the Central Cooper Unconventional

Resource Project. As a first step in this project, the Company conducted the 1,050km2 Winnie 3D seismic survey across

the western half of ATP 940P. The primary objective of the Winnie 3D seismic survey is to delineate the Nappamerri

Trough REM (Roseneath - Epsilon - Murteree) Shale and deeper tight gas play fairway. The survey is also targeting early

identification of shale and tight gas sweet spots within the Nappamerri Trough Unconventional Play Fairway.

Drillsearch has continued to actively manage its asset portfolio through financial year 2013. An on-market acquisition of

Acer Energy was completed in January 2013 which provided additional Cooper Basin acreage complementing the Oil,

Wet Gas and Unconventional Businesses. Shortly after the year end, Drillsearch announced a series of transactions with

Santos that significantly advance both the Wet Gas and Oil businesses.

| Page 10

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Active Portfolio management

Outlook

The key objectives for the Company with regard to the finance and capital management in 2014 are to ensure that:

• growth programs of each of the Company’s businesses are appropriately and fully funded;

• capital management is optimized supporting this growth - both organic and transactional; and

• disciplined cost management is applied and delivered to this growth.

Changes in state of affairs

There was no significant change in the state of affairs of the consolidated entity during the financial year.

Subsequent events

Subsequent to balance date the following material events have occurred:

• On 15 August 2013, Drillsearch announced a 157% increase in reported 2P Reserves as at 30 June 2013.

Environmental regulations

Dividends

During the year no dividends were paid. No dividend is proposed for the current year (2012: nil).

• On 1 August 2013, the Company entered into oil price options for a portion of its audited 12 month 1P production

profile. The Company will manage its position on options on an ongoing basis. See note 29 for further information

on the Company’s financial risk management objectives, strategy and the options currently undertaken.

The parent entity is subject to significant environmental regulation in respect of its operated and non-operated joint

venture interests in petroleum exploration, development and production. Its oil production interests in the state of

Queensland are operated by Santos, who is required to comply with all relevant environmental legislation. The

Company's oil and the Western Wet Gas Project production interests in the state of South Australia are operated by

Beach Energy, who is required to comply with all relevant environmental legislation. The Northern Wet Gas Project

production and exploration interests in South Australia are operated by the Company and the Company’s Queensland

exploration interests are largely operated by the Company. In connection with these activities, the Company complies

with all relevant environmental legislation.

• On 1 July 2013 the Company announced that it had secured a $50 million credit facility with the Commonwealth

Bank of Australia subject to the satisfaction of the usual conditions precedent. These conditions precedent have now

been met although the facility remains undrawn to date.

In the Oil Business, the Company expanded its existing equity position, reserves and oil production in the Eastern

Margin Oil Fairway of the Cooper Basin through the acquisition of an additional working interest in the Tintaburra Block

JV and sold its minority interest in the PEL 100 oil exploration permit which was a non-core asset acquired as part of the

Acer takeover.

• On 22 July 2013, the Company announced the appointment of Philip Bainbridge as a new Non-executive Director.

Capital investment expenditure for financial year 2014 is expected to be $90-$110 million, which is broadly in-line with

guidance previously provided to the market. Of this 50-60% is expected to be spent on development activities and 40-

50% invested in exploration work programs.

• On 4 July 2013 the Company announced that it had entered into a series of binding agreements with Santos.

Under this transaction, Santos will earn a 60% interest and Operatorship in PEL 106A and PEL 513 by funding future

work programs and providing further field development assistance to export production from these permits.

Additionally, the Company has entered into a long-term GSA covering production from PEL 106A and PEL 513

through 2025. Drillsearch will also acquire from Santos a further 29% interest in the Tintaburra Block JV Oil Project,

increasing its holding from 11% to 40% for $38 million and Santos will acquire the Company's interest in PEL 100 of

25.8% for $15 million. Overall, transaction completion is expected to take place by the end of September 2013.

| Page 11

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Shares under option or issued on exercise of options

Details of unissued shares or interests under option as at the date of this report are:

Class

Issuing Entity of shares

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Class

Issuing Entity of shares

Drillsearch Energy Limited Ordinary $nil

Shares which may be issued on exercise of performance rights

Details of shares or interests which may be issued on exercise of performance rights as at the date of this report are:

Class

Issuing Entity of shares

Drillsearch Energy Limited Ordinary

Drillsearch Energy Limited Ordinary

Class

Issuing Entity of shares

Drillsearch Energy Limited nil nil $nil $nil

Indemnification of officers and auditors

Number of

performance rights paid for shares unpaid on shares

1,541,172

The holders of these performance rights do not have the right, by virtue of the performance right, to participate in any

share issue or interest issue of the company or of any other body corporate or registered scheme.

Number of

shares under Amount Amount

shares under Peformance

performance rights period end date

253,934 30 June 2013

1,287,238 30 June 2015

$0.376 10 November 2013

Expiry

date of options

1,200,000

1,000,000 $0.853 15 March 2015

500,000 $0.701 3 January 2016

3,200,000 $0.700 30 November 2013

1,000,000 $0.600 30 September 2014

Number of

shares under option

Exercise price

of option

13,913,139

1,199,597 $0.596 20 June 2018

2,627,956 $0.596 25 July 2018

The Company has not otherwise, during or since the end of the financial year, except to the extent permitted by law,

indemnified or agreed to indemnify an officer or auditor of the Company or of any related body corporate against a

liability incurred as such an officer or auditor.

During the financial year, the Company paid a premium in respect of a contract insuring the directors of the Company

(as named above), the Company Secretary, Ms J. Moore, and all executive officers of the Company and of any related

body corporate against a liability incurred as such a director, secretary or executive officer to the extent permitted by

the Corporations Act 2001. The contract of insurance prohibits disclosure of the nature of the liability and the amount

of the premium.

The holders of these options do not have the right, by virtue of the option, to participate in any share issue or interest

issue of the company or of any other body corporate or registered scheme.

Number of

shares under option

Amount

paid for shares

Amount

unpaid on shares

3,185,586 $0.596 23 November 2018

Details of shares or interests issued during and since the end of the financial year as a result of exercise of options are:

Details of shares or interests issued during and since the end of the financial year as a result of exercise of performance

rights are:

2,500,000 $1,509,600

| Page 12

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Directors' Report

Directors’ Report (continued)

Directors’ meetings

Directors Held Attended Held Attended Held Attended Held Attended

Mr J.D. McKerlie 22 22 5 5 8 8 6 6

Mr B.W. Lingo 22 22 n/a n/a n/a n/a 6 6

Mr B.K. Choo 22 19 n/a n/a n/a n/a n/a n/a

Mrs F.A. Robertson 22 21 5 5 8 8 n/a n/a

Mr H.R.B. Wecker 22 22 5 5 8 8 6 6

Legal matters

Non-audit services

Rounding off of amounts

Auditor’s independence declaration

The auditor’s independence declaration is included on page 27 of the annual financial report.

The Company is a company of the kind referred to in ASIC Class Order 98/100, dated 10 July 1998, and in accordance

with that Class Order amounts in the Directors’ Report and the financial statements are rounded off to the nearest

thousand dollars, unless otherwise indicated.

The following table sets out the number of Directors’ meetings (including meetings of committees of directors) held

during the financial year and the number of meetings attended by each Director (whilst they were a Director or

committee member). During the financial year, twenty-two board meetings, five remuneration and nomination

committee meetings, eight audit and risk committee meetings and six technical committee meetings were held.

Details of amounts paid or payable to the auditor for non-audit services provided during the year by the auditor are

outlined in Note 33 to the financial statements.

The Directors are satisfied that the provision of non-audit services, during the year, by the auditor (or by another person

or firm on the auditor’s behalf) is compatible with the general standard of independence for auditors imposed by the

Corporations Act 2001.

The Directors are of the opinion that the services as disclosed in Note 33 to the financial statements do not compromise

the external auditor’s independence, based on advice received from the Audit Committee, for the following reasons;

• all non-audit services have been reviewed and approved to ensure that they do not impact the integrity and

objectivity of the auditor; and

Board of Directors Remuneration &

Nomination

committee

Audit & risk

committee

Technical

committee

During the year, the Company was not involved in any legal proceedings of a material nature against Drillsearch or its

subsidiaries of which the Directors are aware.

• none of the services undermine the general principles relating to auditor independence as set out in Code of

Conduct APES 110 Code of Ethics for Professional Accountants issued by the Accounting Professional & Ethical

Standards Board, including reviewing or auditing the auditor’s own work, acting in a management or decision-

making capacity for the Company, acting as advocate for the Company or jointly sharing economic risks and

rewards.

| Page 13

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Remuneration Report

Remuneration Report

This Remuneration Report covers the following areas:

1. People covered by this report (KMP)

2. Remuneration, corporate strategy and Company performance

3. Remuneration governance

4. Remuneration policy

a) Fixed pay

b) Short term incentives (STI)

c) Long term incentives (LTI)

d) Outstanding KMP options and performance rights

e) Employee Share Plan (ESP)

f) External advisors

5. Remuneration levels paid to KMP

a) Remuneration details

b) Key terms of employment contracts

6. Non-executive Directors remuneration arrangements

7. Diversity

8. Changes in remuneration policy for 2014.

1. People covered by this report (KMP)

• Mr J.D. McKerlie (Chairman)

• Mr B.W. Lingo (Managing Director)

• Mr P. J. Bainbridge (Non- Executive Director) - appointed 22 July 2013

• Mr B.K. Choo (Non- Executive Director)

• Mrs F.A. Robertson (Non- Executive Director)

• Mr H.R.B. Wecker (Non- Executive Director)

• Mr I.W. Bucknell (Chief Financial Officer)

• Mr D. Evans (Chief Technical Officer)

• Mr P. Fox (Chief Commercial Officer) - appointed 1 July 2013

• Mr J.S. Whaley (Chief Operating Officer)

2. Remuneration, corporate strategy and Company performance

This Remuneration Report, which forms part of the Directors’ Report, sets out information about the remuneration of

Drillsearch Energy Limited’s key management personnel (KMP) for the financial year ended 30 June 2013. It outlines the

remuneration arrangements of the Company in accordance with section 300A of the Corporations Act 2001 (‘Act’) and

its regulations. The information has been audited as required by section 308(3C) of the Act.

The following were key management personnel of the consolidated entity during or since the end of the financial year:

Except as noted, the named persons held their position for the whole of the financial year and remain in position at the

time of this report.

The Company has experienced substantial growth over the last five years during which time the number of employees

has grown from less than ten to approximately 80, with approved hires to bring headcount to 100 people in the near

future. A substantial effort has gone into the recruitment of this talent, and a commensurate effort has also gone into

developing the necessary people management systems to ensure the productivity and development of the Drillsearch

team. The Board has also looked at longer term retention strategies by ensuring the Company is an employer of choice.

| Page 14

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Remuneration Report

Remuneration Report (continued)

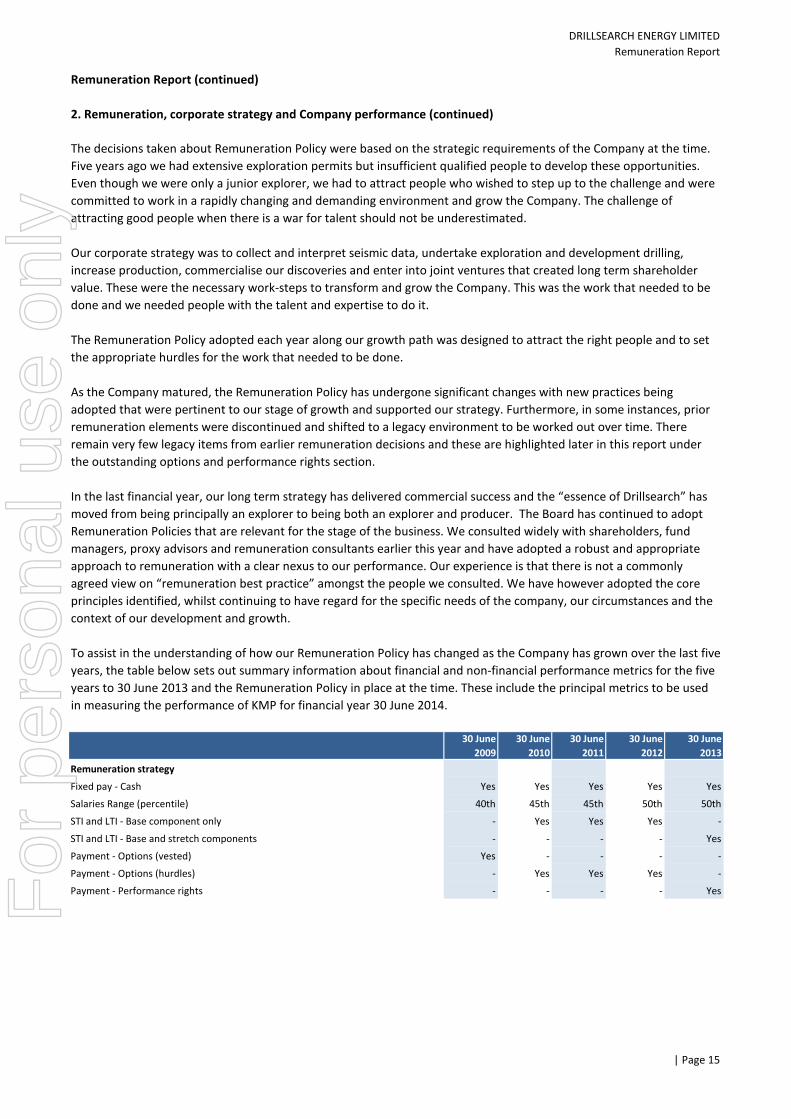

2. Remuneration, corporate strategy and Company performance (continued)

30 June

2009

30 June

2010

30 June

2011

30 June

2012

30 June

2013

Remuneration strategy

Fixed pay - Cash Yes Yes Yes Yes Yes

Salaries Range (percentile) 40th 45th 45th 50th 50th

STI and LTI - Base component only - Yes Yes Yes -

STI and LTI - Base and stretch components - - - - Yes

Payment - Options (vested) Yes - - - -

Payment - Options (hurdles) - Yes Yes Yes -

Payment - Performance rights - - - - Yes

The decisions taken about Remuneration Policy were based on the strategic requirements of the Company at the time.

Five years ago we had extensive exploration permits but insufficient qualified people to develop these opportunities.

Even though we were only a junior explorer, we had to attract people who wished to step up to the challenge and were

committed to work in a rapidly changing and demanding environment and grow the Company. The challenge of

attracting good people when there is a war for talent should not be underestimated.

Our corporate strategy was to collect and interpret seismic data, undertake exploration and development drilling,

increase production, commercialise our discoveries and enter into joint ventures that created long term shareholder

value. These were the necessary work-steps to transform and grow the Company. This was the work that needed to be

done and we needed people with the talent and expertise to do it.

The Remuneration Policy adopted each year along our growth path was designed to attract the right people and to set

the appropriate hurdles for the work that needed to be done.

As the Company matured, the Remuneration Policy has undergone significant changes with new practices being

adopted that were pertinent to our stage of growth and supported our strategy. Furthermore, in some instances, prior

remuneration elements were discontinued and shifted to a legacy environment to be worked out over time. There

remain very few legacy items from earlier remuneration decisions and these are highlighted later in this report under

the outstanding options and performance rights section.

In the last financial year, our long term strategy has delivered commercial success and the “essence of Drillsearch” has

moved from being principally an explorer to being both an explorer and producer. The Board has continued to adopt

Remuneration Policies that are relevant for the stage of the business. We consulted widely with shareholders, fund

managers, proxy advisors and remuneration consultants earlier this year and have adopted a robust and appropriate

approach to remuneration with a clear nexus to our performance. Our experience is that there is not a commonly

agreed view on “remuneration best practice” amongst the people we consulted. We have however adopted the core

principles identified, whilst continuing to have regard for the specific needs of the company, our circumstances and the

context of our development and growth.

To assist in the understanding of how our Remuneration Policy has changed as the Company has grown over the last five

years, the table below sets out summary information about financial and non-financial performance metrics for the five

years to 30 June 2013 and the Remuneration Policy in place at the time. These include the principal metrics to be used

in measuring the performance of KMP for financial year 30 June 2014.

| Page 15

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Remuneration Report

Remuneration Report (continued)

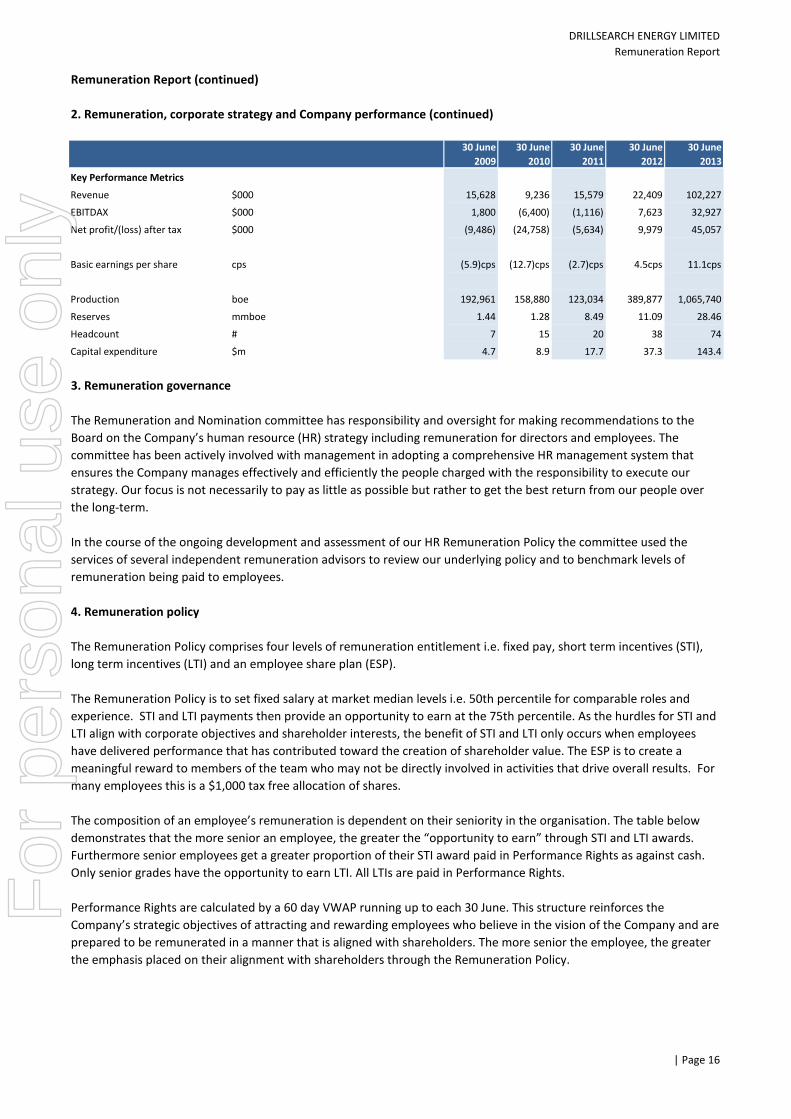

2. Remuneration, corporate strategy and Company performance (continued)

30 June

2009

30 June

2010

30 June

2011

30 June

2012

30 June

2013

Key Performance Metrics

Revenue $000 15,628 9,236 15,579 22,409 102,227

EBITDAX $000 1,800 (6,400) (1,116) 7,623 32,927

Net profit/(loss) after tax $000 (9,486) (24,758) (5,634) 9,979 45,057

Basic earnings per share cps (5.9)cps (12.7)cps (2.7)cps 4.5cps 11.1cps

Production boe 192,961 158,880 123,034 389,877 1,065,740

Reserves mmboe 1.44 1.28 8.49 11.09 28.46

Headcount # 7 15 20 38 74

Capital expenditure $m 4.7 8.9 17.7 37.3 143.4

3. Remuneration governance

4. Remuneration policy

The Remuneration and Nomination committee has responsibility and oversight for making recommendations to the

Board on the Company’s human resource (HR) strategy including remuneration for directors and employees. The

committee has been actively involved with management in adopting a comprehensive HR management system that

ensures the Company manages effectively and efficiently the people charged with the responsibility to execute our

strategy. Our focus is not necessarily to pay as little as possible but rather to get the best return from our people over

the long-term.

In the course of the ongoing development and assessment of our HR Remuneration Policy the committee used the

services of several independent remuneration advisors to review our underlying policy and to benchmark levels of

remuneration being paid to employees.

The Remuneration Policy is to set fixed salary at market median levels i.e. 50th percentile for comparable roles and

experience. STI and LTI payments then provide an opportunity to earn at the 75th percentile. As the hurdles for STI and

LTI align with corporate objectives and shareholder interests, the benefit of STI and LTI only occurs when employees

have delivered performance that has contributed toward the creation of shareholder value. The ESP is to create a

meaningful reward to members of the team who may not be directly involved in activities that drive overall results. For

many employees this is a $1,000 tax free allocation of shares.

The composition of an employee’s remuneration is dependent on their seniority in the organisation. The table below

demonstrates that the more senior an employee, the greater the “opportunity to earn” through STI and LTI awards.

Furthermore senior employees get a greater proportion of their STI award paid in Performance Rights as against cash.

Only senior grades have the opportunity to earn LTI. All LTIs are paid in Performance Rights.

Performance Rights are calculated by a 60 day VWAP running up to each 30 June. This structure reinforces the

Company’s strategic objectives of attracting and rewarding employees who believe in the vision of the Company and are

prepared to be remunerated in a manner that is aligned with shareholders. The more senior the employee, the greater

the emphasis placed on their alignment with shareholders through the Remuneration Policy.

The Remuneration Policy comprises four levels of remuneration entitlement i.e. fixed pay, short term incentives (STI),

long term incentives (LTI) and an employee share plan (ESP).

| Page 16

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Remuneration Report

Remuneration Report (continued)

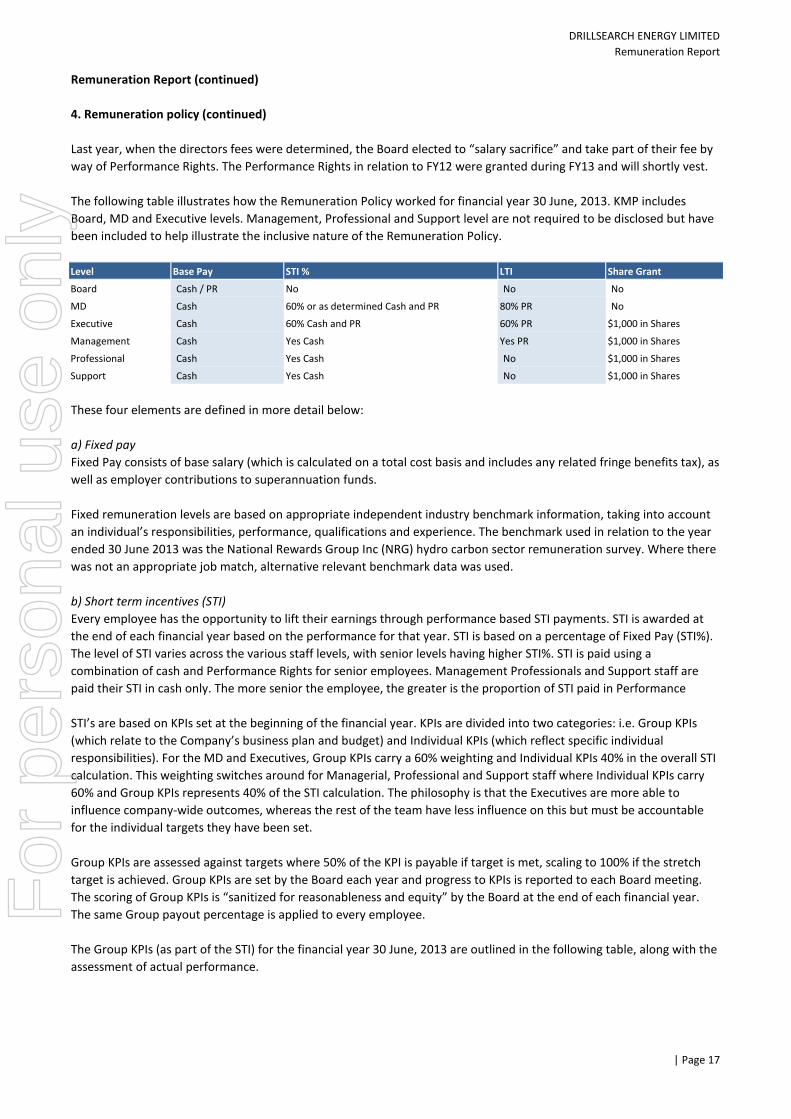

4. Remuneration policy (continued)

Level Base Pay STI % LTI Share Grant

Board Cash / PR No No No

MD Cash 60% or as determined Cash and PR 80% PR No

Executive Cash 60% Cash and PR 60% PR $1,000 in Shares

Management Cash Yes Cash Yes PR $1,000 in Shares

Professional Cash Yes Cash No $1,000 in Shares

Support Cash Yes Cash No $1,000 in Shares

These four elements are defined in more detail below:

a) Fixed pay

b) Short term incentives (STI)

Fixed Pay consists of base salary (which is calculated on a total cost basis and includes any related fringe benefits tax), as

well as employer contributions to superannuation funds.

Fixed remuneration levels are based on appropriate independent industry benchmark information, taking into account

an individual’s responsibilities, performance, qualifications and experience. The benchmark used in relation to the year

ended 30 June 2013 was the National Rewards Group Inc (NRG) hydro carbon sector remuneration survey. Where there

was not an appropriate job match, alternative relevant benchmark data was used.

Last year, when the directors fees were determined, the Board elected to “salary sacrifice” and take part of their fee by

way of Performance Rights. The Performance Rights in relation to FY12 were granted during FY13 and will shortly vest.

The following table illustrates how the Remuneration Policy worked for financial year 30 June, 2013. KMP includes

Board, MD and Executive levels. Management, Professional and Support level are not required to be disclosed but have

been included to help illustrate the inclusive nature of the Remuneration Policy.

Every employee has the opportunity to lift their earnings through performance based STI payments. STI is awarded at

the end of each financial year based on the performance for that year. STI is based on a percentage of Fixed Pay (STI%).

The level of STI varies across the various staff levels, with senior levels having higher STI%. STI is paid using a

combination of cash and Performance Rights for senior employees. Management Professionals and Support staff are

paid their STI in cash only. The more senior the employee, the greater is the proportion of STI paid in Performance

STI’s are based on KPIs set at the beginning of the financial year. KPIs are divided into two categories: i.e. Group KPIs

(which relate to the Company’s business plan and budget) and Individual KPIs (which reflect specific individual

responsibilities). For the MD and Executives, Group KPIs carry a 60% weighting and Individual KPIs 40% in the overall STI

calculation. This weighting switches around for Managerial, Professional and Support staff where Individual KPIs carry

60% and Group KPIs represents 40% of the STI calculation. The philosophy is that the Executives are more able to

influence company-wide outcomes, whereas the rest of the team have less influence on this but must be accountable

for the individual targets they have been set.

Group KPIs are assessed against targets where 50% of the KPI is payable if target is met, scaling to 100% if the stretch

target is achieved. Group KPIs are set by the Board each year and progress to KPIs is reported to each Board meeting.

The scoring of Group KPIs is “sanitized for reasonableness and equity” by the Board at the end of each financial year.

The same Group payout percentage is applied to every employee.

The Group KPIs (as part of the STI) for the financial year 30 June, 2013 are outlined in the following table, along with the

assessment of actual performance.

| Page 17

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Remuneration Report

Remuneration Report (continued)

4. Remuneration policy (continued)

b) Short term incentives (STI) (continued)

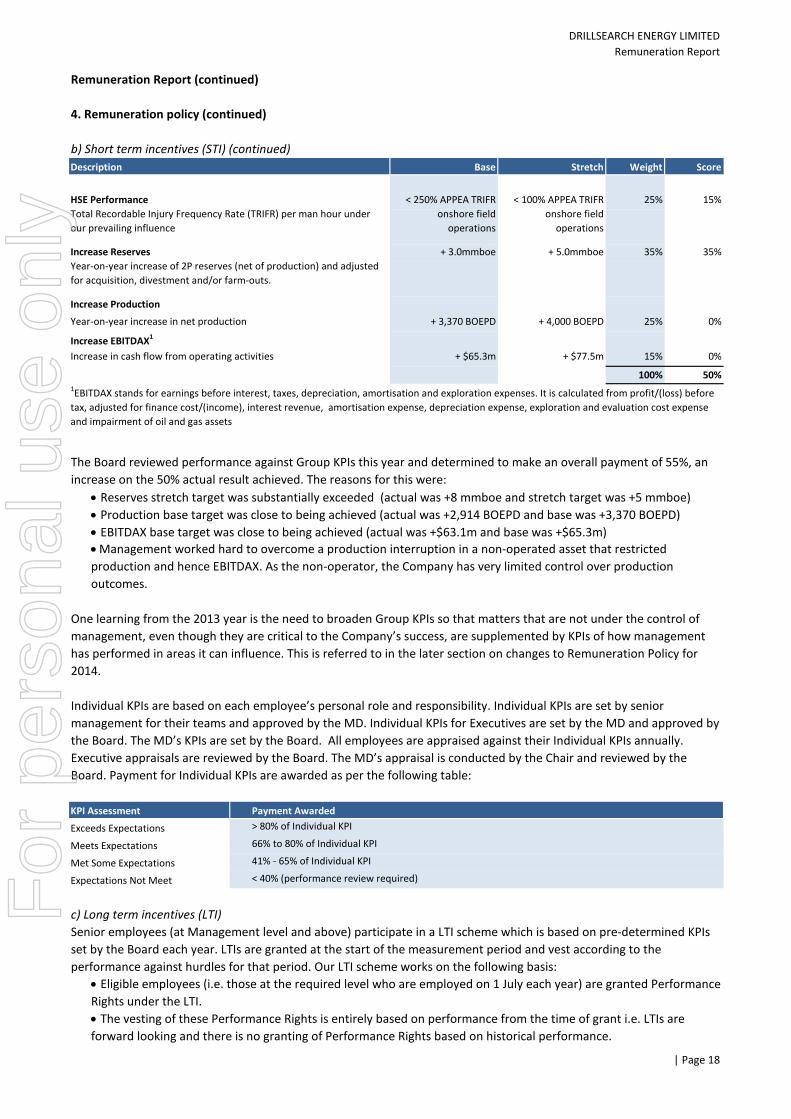

Description Weight Score

25% 15%

35% 35%

Increase Production

25% 0%

Increase EBITDAX1

15% 0%

100% 50%

Reserves stretch target was substantially exceeded (actual was +8 mmboe and stretch target was +5 mmboe)

Production base target was close to being achieved (actual was +2,914 BOEPD and base was +3,370 BOEPD)

EBITDAX base target was close to being achieved (actual was +$63.1m and base was +$65.3m)

KPI Assessment Payment Awarded

Exceeds Expectations > 80% of Individual KPI

Meets Expectations 66% to 80% of Individual KPI

Met Some Expectations 41% - 65% of Individual KPI

Expectations Not Meet < 40% (performance review required)

c) Long term incentives (LTI)

One learning from the 2013 year is the need to broaden Group KPIs so that matters that are not under the control of

management, even though they are critical to the Company’s success, are supplemented by KPIs of how management

has performed in areas it can influence. This is referred to in the later section on changes to Remuneration Policy for

2014.

Individual KPIs are based on each employee’s personal role and responsibility. Individual KPIs are set by senior

management for their teams and approved by the MD. Individual KPIs for Executives are set by the MD and approved by

the Board. The MD’s KPIs are set by the Board. All employees are appraised against their Individual KPIs annually.

Executive appraisals are reviewed by the Board. The MD’s appraisal is conducted by the Chair and reviewed by the

Board. Payment for Individual KPIs are awarded as per the following table:

Senior employees (at Management level and above) participate in a LTI scheme which is based on pre-determined KPIs

set by the Board each year. LTIs are granted at the start of the measurement period and vest according to the

performance against hurdles for that period. Our LTI scheme works on the following basis:

Base

1EBITDAX stands for earnings before interest, taxes, depreciation, amortisation and exploration expenses. It is calculated from profit/(loss) before

tax, adjusted for finance cost/(income), interest revenue, amortisation expense, depreciation expense, exploration and evaluation cost expense

and impairment of oil and gas assets

Year-on-year increase in net production

Increase in cash flow from operating activities

< 250% APPEA TRIFR

onshore field

operations

+ 3.0mmboe

+ $65.3m

Eligible employees (i.e. those at the required level who are employed on 1 July each year) are granted Performance

Rights under the LTI.

+ 5.0mmboe

+ 4,000 BOEPD

+ $77.5m

HSE Performance

Total Recordable Injury Frequency Rate (TRIFR) per man hour under

our prevailing influence

Increase Reserves

Year-on-year increase of 2P reserves (net of production) and adjusted

for acquisition, divestment and/or farm-outs.

+ 3,370 BOEPD

Stretch

< 100% APPEA TRIFR

onshore field

operations

The Board reviewed performance against Group KPIs this year and determined to make an overall payment of 55%, an

increase on the 50% actual result achieved. The reasons for this were:

Management worked hard to overcome a production interruption in a non-operated asset that restricted

production and hence EBITDAX. As the non-operator, the Company has very limited control over production

outcomes.

The vesting of these Performance Rights is entirely based on performance from the time of grant i.e. LTIs are

forward looking and there is no granting of Performance Rights based on historical performance.

| Page 18

For

per

sona

l use

onl

y

DRILLSEARCH ENERGY LIMITED

Remuneration Report

Remuneration Report (continued)

4. Remuneration policy (continued)

c) Long term incentives (LTI) (continued)

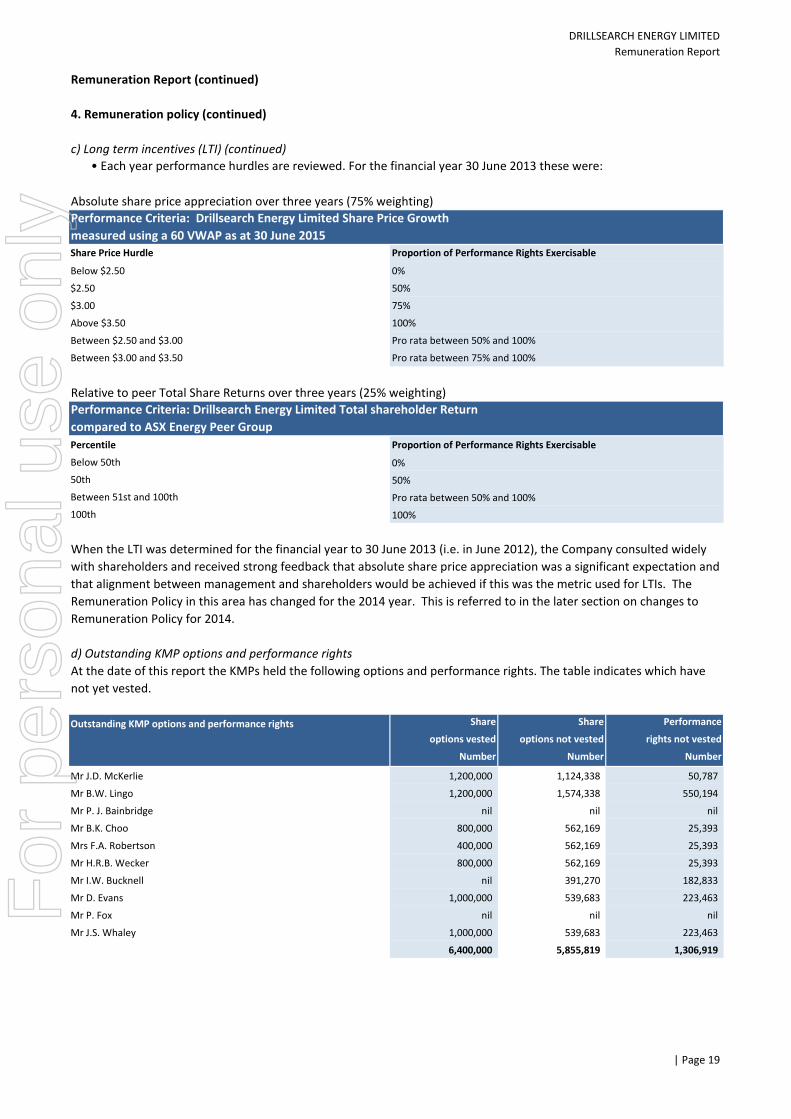

Absolute share price appreciation over three years (75% weighting)

Below $2.50 0%

$2.50 50%

$3.00 75%

Above $3.50 100%

Between $2.50 and $3.00 Pro rata between 50% and 100%

Between $3.00 and $3.50 Pro rata between 75% and 100%

Relative to peer Total Share Returns over three years (25% weighting)

Percentile Proportion of Performance Rights Exercisable

Below 50th 0%

50th 50%

Between 51st and 100th Pro rata between 50% and 100%

100th 100%

d) Outstanding KMP options and performance rights

Outstanding KMP options and performance rights

Mr J.D. McKerlie

Mr B.W. Lingo

Mr P. J. Bainbridge

Mr B.K. Choo

Mrs F.A. Robertson

Mr H.R.B. Wecker

Mr I.W. Bucknell

Mr D. Evans

Mr P. Fox

Mr J.S. Whaley

nil

1,306,919

Share Performance

options vested options not vested rights not vested

Number Number

1,200,000 1,574,338

nil nil nil

800,000 562,169

400,000 562,169

223,463

1,000,000 539,683 223,463

6,400,000 5,855,819

1,124,338

Share

800,000 562,169

nil 391,270

1,000,000 539,683

nil nil

Number

25,393

25,393

25,393

182,833

50,787

550,194

1,200,000

Performance Criteria: Drillsearch Energy Limited Total shareholder Return

compared to ASX Energy Peer Group

When the LTI was determined for the financial year to 30 June 2013 (i.e. in June 2012), the Company consulted widely

with shareholders and received strong feedback that absolute share price appreciation was a significant expectation and

that alignment between management and shareholders would be achieved if this was the metric used for LTIs. The