Embed Size (px)

Citation preview

DELAWARE JOURNAL OF CORPORATE LAW

towards the plaintiff."'' 42 The Court distinguished the plaintiffs claim inBig Lots Stores, Inc. from the Production Resources defendant's debt on theground that the credit agreement benefiting the plaintiff in Big Lots Stores,Inc. consisted of an unsecured note "due eight years after the 2002transaction was set to close."'43 Moreover, the Court emphasized that,while, in Production Resources, "all the challenged transactions occurredin the context of an already insolvent company,"' 44 in Big Lots Stores, Inc.,the complained-of breaches of fiduciary duty were alleged to have causedthe insolvency, which the Court found to be "classically derivative." 145 TheCourt concluded that such claims "do not become direct simply becausethey are raised by a creditor, who alleges that the breaches of fiduciary dutycaused it specific harm by preventing it from recovering a debt outside ofbankruptcy."'' 46 Assuming, arguendo, that a direct claim may potentiallybe asserted in these circumstances, the Court follows this approach inanalyzing NACEPF's claim.

The analysis employed by the Court in Big Lots Stores, Inc. effec-tively limits direct claims, assuming arguendo that they are cognizable, bycreditors of insolvent firms for breach of fiduciary duty to allegations offact substantially similar to those pleaded by the plaintiff in ProductionResources. Indeed, Big Lots Stores, Inc. suggests a two-step approach fordetermining whether a creditor has properly asserted a direct claim forbreach of fiduciary duty in the insolvency context. First, the Court mustdetermine whether the plaintiff-creditor has pleaded facts demonstrating,with a high degree of certainty, that the creditor is entitled to payment andthat the entitlement is either currently or imminently due. 147 If the Courtconcludes that the pleadings satisfy the demanding burden set forth by thisinitial requirement, the Court must then consider whether the claimant'sallegations satisfy the second step of the analysis, which asks whether adirect claim implicating invidious conduct or, in the words of ProductionResources, "such a marked degree of animus" has been properly pleaded.

In this instance, NACEPF has failed to allege facts satisfying the firststep of the above analysis. Put simply, the pleadings neither identify anentitlement to payment that is clearly and immediately due nor do theypermit a reasonable inference to that effect. As a consequence, the Court

1421d.1431d.144id.1451d.1461d"147See also Production Resources, 863 A.2d at 798 (positing that a direct claim might

exist when directors display "marked degree of animus towards a particular creditor with aprovenentitlement to payment" (emphasis added)).

[Vol. 32

UNREPORTED CASES

need not consider whether the Complaint properly sets forth allegationssatisfying the second element of the analysis. 4

First, NACEPF has failed to allege the existence of an entitlementthat is "clearly" due. Instead, NACEPF's theory of the case assumes apriori the existence of a fiduciary duty, upon Clearwire's entry intoinsolvency, requiring that the Defendant Directors variously preservecertain assets or relinquish Clearwire's claimed rights in those assets. Thisassumption is made without first carefully delineating the nature ofClearwire's obligations which make NACEPF a creditor holding a clear andimmediate claim.'49 For their part, the Defendants have vigorously deniedthat NACEPF should be considered a "creditor" at all for purposes of thislitigation. In Production Resources, the plaintiff-creditor was a judgmentcreditor. In this instance, in support of its status as a "creditor" ofClearwire, NACEPF merely identifies a clause of the Master Agreementproviding:

WHEREAS, Clearwire is prepared, and the Alliance Membersare prepared to accept, as royalties, the payments ... foraccess to the Commercial Spectrum Capacity of the Channels... which payments and transfers are intended to generate anaggregate value, as of Initial Closing, of $0.90 for eachChannel POP through a combination of cash commitment

118Because of its conclusion below, the Court does not attempt to define "animus" in thiscontext. "Animus," of course, is only a convenient (and, one hopes, helpful) label for a conceptthat likely will require iterative development. More specifically, the Court need not resolve thequestion, posed in Production Resources, of whether "pure self-dealing is the only fiduciarily-invidious reason that might justify a direct claim by a disadvantaged creditor." 863 A.2d at 798.The Court notes that this question is likely to be answered affirmatively-i.e., that in determiningwhether the second-step of the analysis in this context has been satisfied, the Court shouldexamine whether, during the period of insolvency and for self-dealing purposes, collection of theentitlement at issue has been wrongfully made more difficult or other creditors have beenwrongfully preferred. Cf Production Resources, 863 A.2d at 800 (noting the unique and"suspicious pattern of dealing" alleged permitting an inference of preferential treatment benefitinginsiders and the "de facto controlling stockholder" over plaintiff-creditor).

It should also be noted that, although the Court uses the term "self-dealing" for con-venience, this claim would conceivably also extend to wrongful preferences by directors for thebenefit of persons controlling the directors. Additionally, there is the possibility that a directclaim might lie for "acts committed in contemplation of insolvency." McDonald, 174 U.S. at 404-05 (applying principles of so-called "trust fund doctrine"). Of course, this notion is very distinctfrom (and substantially more limited than) the broader "zone of insolvency." The Court only notesthe possibility that this narrow exception might apply in very limited circumstances, given ourcase law's previous, intermittent citation to McDonald.

149It may be that NACEPF considers itself a creditor simply because of the obligationsthat flow in both directions between NACEPF and Clearwire under the Master Agreement.

2007]

DELAWARE JOURNAL OF CORPORATE LAW

royalty, equity in Clearwire, an earn-out, use agreementexecution and usage royalties. 5 '

NACEPF argues that " [t]his shows that Clearwire had financial obligationstowards NACEPF and Alliance members, rendering NACEPF a creditor ofClearwire with a right to demand its monetary dues for license usage."151

NACEPF also seeks to rely on financial projections prepared for theClearwire board of directors that projected certain outlays payable toNACEPF and Alliance members. 52

As an initial matter, the financial projections referenced by NACEPFare not contained within the allegations of the Complaint and therefore lieoutside the scope of matters that may be considered by the Court.Moreover, even if the Court could consider them, the budgets of anticipatedfuture expenditures fail here to demonstrate a clear entitlement to payment,much less one that is currently due. Significantly, the Defendants arguethat NACEPF recites the "WHEREAS" clause of the Master Agreement,in its answering brief, "[p]resumably [in order to] draw[] the conclusionthat [P]laintiff 'had a right to payment' under the terms of the MasterAgreement." 153 The Defendants rightly point out that NACEPF has failedto demonstrate, through the facts pleaded in the Complaint or even in itsbrief, that "it was not paid what it was owed under the Master Agreement,or that [NACEPF] performed under the terms of the Master Agreement insome way that triggered an unfulfilled obligation of Clearwire to pay[Pllaintiff."154 As a consequence, the Court cannot, based on the argumentsadvanced by NACEPF, conclude that NACEPF has met its burden ofalleging a clear entitlement to payment.155

IS'Master Agreement at 2.15 'Ans. Br. at 28.1521d

'"53Reply Br. at 12.'541d. at 12-13. On February 12, 2004, NACEPF voluntarily dismissed a separate action,

filed on November 20, 2003, against Clearwire for breach of contract. See N. Am. Catholic Educ.Programming Found., Inc. v. Clearwire Holdings, Inc., C.A. No. 03C-11-172 (RRC) (Del.Super.).

155The Court notes that, at oral argument, NACEPFs counsel only briefly stated: "At thetime when we get to 2002 .... the agreements with Sprint and WorldCom, some of them hadexpired or come to their end. At that point, there was an immediate cash obligation on the partof Clearwire." Tr. 41:1-5; see also Tr. 40:1-7 (citing Master Agreement, Preamble Clause (a));Tr. 40:7-14. As an initial matter, it does not appear that the Complaint sets forth facts supportingthis particular proposition-nor was it referenced in NACEPFs answering brief. The Complaint'sprincipal allegations related (perhaps only tangentially, at best) to this proposition state, inter alia,that the market for wireless spectrum "collapsed" in June 2002 and that Clearwire "thereafter"entered into negotiations with Alliance members to "end Clearwire's obligations to the members."Compl. 91 34-35. The Complaint also provides that Clearwire ultimately settled with HITN and

[Vol. 32

UNREPORTED CASES

Indeed, it appears that the best argument in NACEPF's favor, giventhe allegations contained in the Complaint, would be that Clearwirebreached its implied duty of good faith and fair dealing in failing to pursueaggressively build-out of the envisioned wireless internet network. Sucha claim would not, on these facts, give rise to a clear entitlement to paymentsatisfying the first prerequisite for a cognizable direct claim in this context.NACEPF is one party to a contract, and its frustration is perhaps-indeed,likely-better characterized as a claim under contract or tort law.'15 6

Perhaps NACEPF has a colorable claim that Clearwire failed to abide, ingood faith, by the terms of the Master Agreement;' 57 however, this is the

ITF and that, "by October 2003," Clearwire "effectively went out of business;" but the Complaintnever alleges that a monetary obligation of Clearwire to NACEPF, coming due under the termsof the Master Agreement, actually arose and was left unpaid. Certainly, it is difficult to view thesesuppositions as satisfying the requirement that allege a clear entitlement to payment.

By scouring the terms of the Master Agreement, the Court, of its own accord, is able topick up a basis from which an obligation to pay potentially could have arisen. See, e.g., MasterAgreement, §§ 1.2(a) (describing a process by which "Individual Use Agreements" would besubsequently entered into upon the occurrence of an "Availability Event," as those terms aredefined in the Master Agreement); § 9.3. NACEPF, however, has failed to place this argumentbefore the Court, instead making only general references to obligations for payment, as describedabove. Indeed, it is unclear precisely when these obligations may have arisen, if ever. Forexample, NACEPF has identified no information which the Court may consider for purposes ofthis motion to dismiss regarding whether an "Availability Event" occurred during the relevantperiods, whether obligations arising pursuant to such an occurrence were left unmet by Clearwire,and, most importantly, the extent to which Clearwire may have had discretion in entering intoadditional agreements. Even assuming that an obligation to enter into additional "Individual UseAgreements" (or any other unidentified obligation) arose, the bare pleadings of NACEPF (and itsreferences, in briefing and at oral argument, to the introductory provisions of the MasterAgreement) leave the Court unable to infer that any of those obligations was not fulfilled. At best,NACEPFs arguments in this regard could be described as only conclusory allegations (if they areallegations, at all), which do not aid in making the necessary inferences in NACEPFs favor.

Additionally, even assuming that a clear entitlement were shown, NACEPFs claim in thisrespect would ultimately be derivative. The Court is required to make all reasonable inferencesin favor of the plaintiff on a motion to dismiss under Court of Chancery Rule 12(b)(6); however,the only reasonable inference that may be drawn, based on the allegations, regarding non-paymentof this obligation, assuming it existed and was adequately pleaded, was that no funds (or onlyinadequate funds) were available. NACEPF premises its claims on the theory that the Defendantsfailed to pursue adequately the ostensible business plan of Clearwire, which resulted in its coffersbeing empty. Thus, the harm was to the corporation, and the benefit of any remedy would flowto the corporation.

156 Cf. Production Resources, 863 A.2d at 801 (citing RGC Int'l Investors, LDC v. GrekaEnergy Corp., 2001 WL 312454, at *10 n.45 (Del. Ch. Mar. 7, 2001) ("Equity historically'follows the law' and does not create remedies where the parties' behavior is already closelyregulated by the law.")); Production Resources, 863 A.2d at 801 n.88 ("In general .... thereseems to be utility in applying fiduciary duty law quite cautiously, to avoid unduly benefitingcreditors by enabling them to recover in equity when they could not prevail on legal tort orcontract claims.").

157But see supra note 154.

2007]

DELAWARE JOURNAL OF CORPORATE LAW

subject of legitimate debate and therefore fails to constitute a "clear" debtobligation of the ftrm."'

Second, given the Court's analysis above that NACEPF has failed todemonstrate a clear entitlement to payment, NACEPF has also necessarilyfailed to demonstrate that the alleged entitlement on which it seeks topremise its claim has the immediacy necessary to maintain a direct claimin this context. As in Big Lots Stores, Inc., no claim of NACEPF has beenreduced to judgment, even assuming that a breach of contract has occurred.Judgment creditor status might not be necessary in the face of anentitlement that is otherwise clearly and currently due. 5 9 In this instance,however, the pleadings fail to allege facts from which the existence of sucha debt can be reasonably inferred.

The two-step approach followed here with respect to direct claimscomports with the principal policy considerations that underlie analysis inthis context. Foremost among these is the notion that directors of insolventcorporations must retain the freedom to engage in vigorous, good-faithnegotiations with their creditors for the benefit of the firm.160 To holdotherwise would, in the context of insolvency, not only cast a cloud ofuncertainty over directors' ordinary discretion to exercise freely theirrational business judgment, but arguably also would diminish the potential

'"58Similarly, NACEPF has not argued that Count I of the Complaint, for fraudulentinducement, is a proper basis for creditor status in this context. The bulk of its arguments withrespect to that claim are directed toward allegedly fraudulent conduct of the Defendants, notClearwire. Therefore, to the extent NACEPF might have a claim (regardless of its viability), itis against the Defendants. The Court notes, however, that NACEPF has briefly mentionedconduct that might be charged to Clearwire-principally, if not entirely, in reference to statementsof intention contained in the Preamble of the Master Agreement. See Compl. 38. Thisargument, although not advanced by NACEPF in support of its creditor status, would, inter alia,obviously fail to set forth a clearly held entitlement to payment and therefore could not serve asthe basis of a direct fiduciary duty claim in this context-assuming such a claim exists.

Additionally, to the extent that Count III arguably, might theoretically serve as the basisfor claiming creditor status in this context-an argument NACEPF has not advanced-such anargument fails, inter alia, for similar reasons in this context. Moreover, the "nexus" between theclaimed breach of fiduciary duty and such an entitlement, even if it were adequately alleged, isnot readily apparent.

"59This is an issue that the Court need not resolve, however, given the other inadequaciesof NACEPFs allegations described above. But cf Johnston v. Wolf, 487 A.2d 1132, 1135-37(Del. 1985) (holding that plaintiff was not a "creditor" (of pre-merger corporation) grantedstanding under 8 Del.C. § 174 to pursue claims against pre-merger directors for unlawfulredemption of stock where plaintiffs claim had not been reduced to judgment prior to merger).

'60Cf Production Resources, 863 A.2d at 797 ("[D]irectors of an insolvent corporationmust retain the right to negotiate in good faith with creditors and to strike fair bargains for thefirm."); id. at 800 ("I do not rest my decision in any manner on the proposition that it is a breachof fiduciary duty for the board of an insolvent company to engage in vigorous, good-faithnegotiations with a judgment creditor. That, in fact, might be the duty of a board, whichnecessarily has to balance the interests of all those with a claim to the firm's inadequate assets.").

[Vol. 32

UNREPORTED CASES

that an insolvent corporation might emerge from insolvency on its own.Moreover, to some extent, albeit neither easily defined nor universallypraised, the so-called "trust fund doctrine" may, however, inform analysisin this context.'6 1 Assuming the so-called "trust fund doctrine" does, tosome degree, apply, 62 the initial requirement that a debt be both clearly andimmediately due arguably achieves a workable balance between thecomplex realities of serving as a director of an insolvent firm and theconcerns implicit in "trust fund doctrine." 163

Additionally, although NACEPF argues that Clearwire was insolventor in the vicinity of insolvency from the moment the Master Agreement wasentered into, when the Complaint is "shorn of excess verbiage," it becomesclear that the alleged conduct of the Defendants challenged by NACEPF isbetter viewed as the cause of Clearwire's approach to the brink ofinsolvency and, perhaps, slide into actual insolvency. The allegations inthe Complaint suggest that, as of the time of contract, Clearwire had beenprovided with funds that, although not sufficient for the long-term, appearto have been sufficient for the purpose of developing the "intended"business opportunity in the short-term."6 As in Big Lots Stores, Inc.,"claims of this type are classically derivative. "165

161In conceding that a direct claim for "animus" might exist, Production Resourcessuggests that, to some extent, semi-analogous trust principles might require that creditors not, incertain circumstances (e.g., for self-dealing purposes), be wrongfully disadvantaged vis-a-visother creditors. See 863 A.2d at 798 n.77. Cf supra note 118.

162But cf. Asmussen, 156 A. at 181. The Court, in Production Resources, acknowledgedthat venerable case law holds that directors of an insolvent corporation may generally prefer onecreditor over another. See 863 A.2d at 792, 798 (citing Asmussen, 156 A. 180). This line of caselaw, however, imposes the limitation that directors may not exercise this discretion for self-dealing purposes. See Penn. Co. for Ins. on Lives & Granting Annuities, 174 A. 112. Thislimitation would also most likely extend to preferences for the benefit of persons or entities bywhich the directors are controlled.

It may bear repeating that the analysis contained in the text above only assumes theexistence of a direct claim which may be asserted by creditors for "animus." The venerable lineof case law discussed above, however, arguably addresses only distributions of corporateassets-i.e., dissipating the corporation's pool of available assets, which would presumablyconstitute a derivative claim under the modem test enunciated in Tooley. See, e.g., Penn. Co.forIns. on Lives & Granting Annuities, 174 A. at 116 (suggesting, through its "lifeboat" example,that recognition of claims for preference implicating directorial self-dealing may be limited toinstances in which injury to the corporation occurs and that this doctrine is perhaps better viewedas flowing from "applied common honesty" than "so-called 'trust fund theory").

'It should be noted that this Memorandum Opinion does not reach the applicability ofthe presumptions of the business judgment rule, because the Court concludes that NACEPF hasfailed, as an initial matter, to set forth allegations satisfying the elements of the underlyingclaim--assuming, arguendo, such a claim exists.

"See supra note 97 and accompanying text.1652006 WL 846121, at *7 (quoting Production Resources, 863 A.2d at 776). It is not

as easy to fault Clearwire's directors as NACEPF suggests it should be for failing to relinquish

20071

DELAWARE JOURNAL OF CORPORATE LAW

Unlike in Production Resources, Clearwire's alleged debt obligation,as alleged in the Complaint, to NACEPF was neither clear norimmediate."6 Therefore, even assuming that a limited direct claim mightbe asserted by a creditor of an insolvent corporation in this context, theCourt concludes that NACEPF has failed to allege facts which set forthsuch a claim. NACEPF may not now recover for its own benefit what itperhaps could not have recovered through contract or tort by transformingits claims into one claim for breach of a fiduciary duty that it can directlypursue.

IV. CONCLUSION

Accordingly, Count II of the Complaint fails to state a claim uponwhich relief can be granted and must be dismissed. Therefore, for reasonsalso set forth above, the Court is without personal jurisdiction over theDefendants with regard to Counts I and III, which must be dismissed.Accordingly, the Defendants' Motion to Dismiss is granted. Animplementing order will be entered.

IN RE PNB HOLDING CO. SHAREHOLDERS LITIGATION

No. 28-N

Court of Chancery of the State of Delaware, New Castle

August 18, 2006

Clearwire's claim to license rights under the Master Agreement-conduct which forms theprincipal basis for NACEPFs alleged breach of fiduciary duty claim-when that was the onesignificant asset Clearwire appears to have had.

'6As noted above, because NACEPFs claim fails to satisfy the foundational requirementsfor a direct claim for breach of fiduciary duty in this context, the Court does not consider whetherthe pleadings properly allege facts supporting the second step of the analysis. Therefore, theCourt also does not reach the issue of whether "animus," see supra note 148, can supply the finalingredient for a direct claim for breach of fiduciary duty in this context.

[Vol. 32

UNREPORTED CASES

Ronald A. Brown, Jr., Esquire, and Bruce E. Jameson, Esquire, of Prickett,Jones & Elliott, P.A., Wilmington, Delaware; and Arthur T. Susman,Esquire, John R. Wylie, Esquire, Matthew T. Heffner, Esquire, andMatthew Hurst, Esquire, of Susman, Watkins & Wylie, LLP, Chicago,Illinois, of counsel, for plaintiffs.

Thomas A. Beck, Esquire, of Richards, Layton & Finger, P.A.,Wilmington, Delaware; and W. Scott Porterfield, Esquire, Annaliese F.Fleming, Esquire, and Barack Ferrazzano Kirschbaum, Esquire, of Perlman& Nagelberg LLP, Chicago, Illinois, of counsel, for defendants.

STRINE, Vice Chancellor

This post-trial opinion addresses the claims of stockholders of a ruralIllinois bank holding company, PNB Holding Company, who were cashedout in a merger that had the purpose and effect of allowing PNB toreclassify itself as a subchapter S corporation (the "Merger"). To have thateffect, the Merger had to reduce the number of PNB stockholdersremaining after the Merger to no more than seventy-five. The stockholdersof PNB were offered $41.00 per share in the Merger. Several stockholdersdissented from the Merger and perfected their appraisal rights. Theremaining stockholders accepted the Merger consideration but throughclass counsel now complain that the directors of PNB breached theirfiduciary duties and that the Merger was unfair. That is, this opinionresolves both an appraisal claim and an equitable challenge to the Merger.

A major issue decided in this opinion is whether the Merger issubject to entire fairness review. The plaintiffs claim that it is subject toheightened review because the PNB directors, and many members of theirfamilies, remained in the "golden circle" of PNB ownership after itsconversion into an S corporation while the numerical majority of PNBstockholders were cashed-out. Because the directors and their familymembers who would remain collectively held 59.5% of the stock, theplaintiffs claim the Merger was destined to receive the required vote. Asa result, the plaintiffs argue that this case should be analyzed as acontrolling stockholder merger, governed by Kahn v. Lynch Communi-cations Systems, Inc.1 I reject that argument, however, because the largestbloc held by any PNB director was 10.6%, and the directors were notbound together by voting agreements or other material, economic bonds tojustify treating them as a unified group.

'638 A.2d 1110 (Del. 1994) (hereinafter, "Lynch").

2007]

DELAWARE JOURNAL OF CORPORATE LAW

Although I do not believe Lynch governs review of the Merger, I dofind that the Merger is presumptively subject to entire fairness review. Bydeciding to embark on the Merger, the PNB directors created a zero-sumgame. Each of them (and their family members) stood to gain by paying aslittle as possible to the departing PNB stockholders. The Merger contem-plated only sixty-eight of PNB's more than 300 stockholders remaining inthe new S corporation. The reality, then, was that the PNB directors wereassured of remaining in this golden circle and far more than half of theremaining PNB stockholders would be on the outside. In this conflictedsituation, the PNB directors are bound to show that the Merger was fair tothe departing stockholders or to point to the presence of a cleansing device,such as approval by a special committee of independent directors or aninformed majority-of-the-minority vote, in order to justify review under thebusiness judgment rule. The first device was not employed here, and amajority of the minority was not obtained. Therefore, the entire fairnessstandard applies.

The question then becomes whether certain members of the equitableclass are precluded from recovery. I conclude that those stockholders whovoted for the Merger are barred from recovery. The PNB directors, I find,despite the plaintiffs' arguments to the contrary, disclosed all material factsin connection with the Merger. Thus, these plaintiffs are barred by thedoctrine of acquiescence from challenging the fairness of the Merger. Bycontrast, I conclude that those stockholders who did not vote for theMerger, but who simply forewent appraisal and accepted the Mergerconsideration, are not barred from recovery. The consequence of thatruling is that those members of the plaintiff class will receive the differencebetween the fair value of PNB's shares on the Merger date and theconsideration paid to them in the Merger. That is, the recovery of thestockholders who did not seek appraisal will track the recovery of theplaintiffs who perfected their appraisal rights. After performing anindependent valuation, I conclude that the fair value of a share of PNB onthe date of the Merger was $52.34, which is $11.34 per share higher thanthe consideration offered in the Merger. Therefore, the appraisal plaintiffsare entitled to $52.34 per share, while the remaining plaintiffs (all of whomaccepted the Merger consideration) will receive $11.34 - the damagesresulting from the unfair Merger. Those awards will be subject to pre-judgment interest at the legal rate, compounded quarterly.

I. Factual Background

These are the facts as I find them after trial.

[Vol. 32

UNREPORTED CASES

A. The Parties

The respondent in the appraisal portion of this combinedappraisal/equitable action is PNB Holding Company. PNB is a bankholding company that, at all relevant times, owned only one bank -Pontiac National Bank. For the sake of simplicity, I refer to PNB and theBank interchangeably.

The defendants in the equitable action were PNB's directors at thetime of the challenged Merger. Defendant H. Edward Vogelsinger was theonly PNB board member in management, and served both as Chairman andChief Executive Officer of PNB. The remaining defendant-directors areAlonzo W. Clay, John G. Dargan, Richard Y. Dievendorf, Henry J. Eppel,Thomas W. Ewing, J. Alan Gschwendtner, John J. Kelly, and Stephen W.Snyder.2

The parties seeking recovery consist of two groups. The class ofappraisal petitioners is comprised of eighteen stockholders, representing5,846 shares of PNB, who voted against the PNB conversion and perfectedtheir appraisal rights (the "Appraisal Class"). There is a dispute, resolvedlater, about whether 3,000 other shares are in the Appraisal Class. TheAppraisal Class seeks an appraisal of the fair value of PNB as of the dateof the Merger by which PNB converted into an S corporation. The secondgroup seeking recovery consists of the plaintiffs in the equitable action.The plaintiffs' counsel seeks recovery on behalf of all former PNBstockholders who were cashed out in the Merger (the "Plaintiff Class").That Class, which was certified on February 23, 2006, has "roughly 159members" who represent 85,896 shares.'

The Plaintiff Class alleges that the Merger is subject to the entirefairness standard and that the defendant-directors caused PNB to cash outtheir shares at an inadequate price. As this court has become accustomedto in combined appraisal/equitable actions, the actual relief sought by theAppraisal Class and the Plaintiff Class is identical, consisting of the gapbetween what the complaining Classes believed was the fair value of theirshares and the Merger price. Because of this identity in interests, I willrefer to the two Classes collectively as the plaintiffs, for the sake of givingthem a simple moniker.

2For reasons that are not apparent, one director, Ralph B. Mandell, was not named as adefendant in this action.

3Order Certifying Class at 1.

2007]

DELAWARE JOURNAL OF CORPORATE LAW

B. PNB And The Vogelsingers

PNB is headquartered in, and its original operations were located in,Livingston County, Illinois. The parties describe Livingston County as aplace lifted from a Grant Wood painting. According to them, LivingstonCounty consists of farming communities located in north central Illinoiswith a population of approximately 40,000 people, though the county hasexperienced "almost no population growth... in nearly 150 years."'4 Infact, the plaintiffs contend that they primarily consist of "farmers and theirwives.., who held shares... for a long time and had a sense of pride inownership of a local business."5 PNB was started as a small communitybank in 1934 after its predecessor, National Bank of Pontiac, became acasualty of the Great Depression in 1933. It was formed by the grandfatherof defendant Vogelsinger and other members of the Pontiac businesscommunity. After serving in World War II, Vogelsinger's father took overthe reins of PNB from his grandfather in 1948. Vogelsinger's father retiredfrom his role as president of the bank in 1982.

During his father's tenure, Ed Vogelsinger was not involved in theaffairs of PNB. Instead, he pursued a career in accounting in Chicago andMilwaukee. A year after his father retired, however, Ed Vogelsingerjoinedthe board of the Bank.

In 1994, Vogelsinger returned to live in Livingston County and tookover as Chairman of the Bank. Upon his arrival in 1994, the Bank'soperations were confined to the town of Pontiac. Although PNB was awell-capitalized institution, it was not an impressive performer. WithVogelsinger at the helm, PNB's board embarked on plans to change that byexpanding PNB to markets adjacent to Pontiac and Livingston County.

Despite the lengthy involvement of the Vogelsinger family in PNB,Ed Vogelsinger's ascendancy to the Chairmanship did not result from theexercise of voting control. At no time did the Vogelsinger family haveanything approaching voting control. Rather, the Vogelsinger family wasjust one of many area families that owned shares in PNB, and the largerstockholder families had representatives on the board.

C. The Expansion Of PNB

PNB opened its first non-Livingston County branch in 1995 inBloomington, Illinois, which is located in McLean County. In contrast toLivingston County, McLean County had a rising population, more wealthy

4Def. Op. Post-Trial Br. at 2.'P1. Op. Post-Trial Br. at 1.

[Vol. 32

UNREPORTED CASES

residents, a younger population base, and "one of the strongest economiesin Illinois outside of Chicago."6 The expansion into McLean enabled PNBto rapidly expand its lending in 1996 and 1997. Unfortunately, thatexpansion was tainted by imprudent practices.

In 1997, as a result of bad loans made at the Bloomington branch, theOffice of the Comptroller of the Currency (the "OCC") declared PNBunsafe and unsound. In addition, around this same time, the OCC gave thetrust department of the Bank an unsatisfactory rating.

As one of the steps taken in 1997 to address these regulatory issues,PNB hired Thomas Criswell, an experienced commercial banker andhospital CFO, to become the chief lending officer of the Bank. Vogelsingeralso expanded his own role at PNB and the Bank, assuming the topmanagerial role of CEO at both as well as becoming President of PNB, theholding company. In addition, the Bank hired a new trust officer andincreased its allowance for loan losses in order to adequately handle the badloans made at the Bloomington branch. In 1998, as a result of the increasedloan loss reserve, PNB reported negative earnings of $145,000 - only thesecond annual loss in its operating history.

PNB began to recover in 1999, reporting annual earnings of $1.2million, which was lower than PNB's earnings of $1.686 million in 1996,the year before the regulatory issues began to affect earnings. The next twoyears saw continued earnings growth, with net income of $1.635 million in2000 and $1.917 million in 2001. As a result of the improvement, PNBdecided to continue its expansion into McLean County. In 2001, PNBpurchased a bank in order to establish a branch in Gridley, which is asuburb of Bloomington. PNB also decided to lease office space in abuilding known as the Brickyard in order to establish a second branch inBloomington (the "Brickyard Branch").7

In addition to leasing space for the Brickyard Branch, PNBconvinced the real estate investors who owned the Brickyard building tobecome investors in PNB. Initially, those real estate investors intended toopen their own bank, but PNB negotiated with the group to instead investin PNB and to allow PNB to open its new branch in their building. Usingprojections compiled by the investors that detailed their forecasted cost ofstarting a bank, PNB offered the investors the opportunity to purchase PNBshares at the price of $38.75 per share.

61d. at 3.7Around this time, PNB also purchased the right to use the name "People's Bank" for its

McLean County branches because that had been the name of a former bank with a strong presencein that county.

2007]

DELAWARE JOURNAL OF CORPORATE LAW

When the board of PNB was considering this expansion into Gridleyand the opening of the Brickyard Branch, Criswell created a set of five-yearprojections for the Bank (the "Criswell Projections"). By this time,Criswell had become the Bank's Chief Financial Officer and had assumedthe title of Bank President.

Criswell created the projections in December 2000 and presentedthem to the PNB board in February 2001. The Criswell Projections in-volved a forecast of the Bank's future earnings based on its existingbusiness and the addition of the Gridley and Brickyard branches. Theprojections initially were created by Criswell, but, after PNB secured thenew investors who had been planning on opening a bank in McLean Countythemselves, Criswell incorporated some of their initial projections into hisown. The final projections that were presented to the board were compre-hensive and presented a detailed five-year forecast for PNB's income,beginning in 2001. According to the Criswell Projections, the expected netincome for PNB was $1.708 million in 2001, $2.011 million in 2002,$2.408 million in 2003, $2.753 million in 2004, and $3.132 million in 2005.In 2001, the first year of the Criswell Projections, PNB reported a netincome of $1.917 million, which exceeded the Criswell Projections byapproximately 12%. In 2001, then, PNB was expanding and managed toachieve income greater than forecast in the Criswell Projections.

D. PNB Decides To Convert Into An S Corporation

In July 2002, even with the success of the McLean Countyexpansion, the PNB board began considering more fundamental strategicoptions than simple expansion. At a board meeting on July 11, 2002,Vogelsinger outlined a variety of strategic possibilities that PNB mightpursue, including merging with another bank of similar size, acquiringsmaller banks, converting to a so-called "S corporation," or continuing tooperate PNB under its current business plan. The board decided to"continue to evaluate all strategic options in future meetings and have afinal decision by the end of the third quarter of 2002."8

In order to help the board in its deliberations, Vogelsinger drafted aJuly 22, 2002 memorandum to the board that provided more detail withrespect to the options mentioned at the July 11 meeting. That memodiscussed two options: "the sell option" and "the grow to $500MMoption."' The issues raised concerning the sell option involved the universeof potential buyers and how an appraiser would value PNB. The issues

88JX2at 3.9JX 16 at 2-3.

[Vol. 32

UNREPORTED CASES

raised concerning the growth option involved whether PNB could achievethat level of assets through acquisitions or, potentially, a merger withanother bank, and whether achieving an asset level of $500 million wouldallow PNB to continue to operate efficiently. As to either of the two basicoptions that involved a sale of the Bank or a stock-for-stock merger,Vogelsinger expressed concern about whether "CONTROL passed from thecurrent Board to another group and will we have been paid for that changeof control." 0 That memo promises "more to come" about the possibility ofan S corporation conversion."1 The essence of an S corporation conversionis simple: by converting to the S corporation form, PNB would be relievedof the duty to pay corporate level taxes and its stockholders would bedirectly taxed, at individual rates, for income earned by the company.' 2

Additional information about conversion to an S corporation camein the form of a presentation by Vogelsinger to the PNB board at its nextmeeting on August 30, 2002. Vogelsinger listed the advantages of Scorporation status, including the increased return that would result tocontinuing stockholders through the elimination of double taxation ondistributions, and the disadvantages, including the requirement to reducethe number of PNB stockholders to seventy-five to attain eligibility as wellas the inability to use PNB stock for future acquisitions. 3 Vogelsinger alsobriefly addressed the option of seeking out a merger of equals with anothersmall, regional bank and informed the board that the Bank's returns likelywould not be enhanced by that type of business combination. The boardthen had a "lengthy and meaningful discussion," and a motion carried toallow Vogelsinger to "take such steps as may be necessary to position theCompany for conversion to a Subchapter S company, while at the sametime continuing to look at possible stock mergers with banks located inNorthern Illinois." 14

Given this authorization from the board, Vogelsinger sent a letter toPNB stockholders on September 23, 2002, informing them that a series ofinformal dinners would be held where he would present information onPNB and its "future direction."'" At those dinners, Vogelsinger gave aPowerPoint presentation to the stockholders titled "Controlling OurDestiny" that discussed the S corporation structure and the benefits it wouldprovide to PNB, including a higher return on equity and the ability for PNB

l° Id. at 4 (emphasis in original).'lid. at 5.12See Delaware Open MRI Radiology Assoc., P.A. v. Kessler, 898 A.2d 290, 328 (Del.

Ch. 2006).13JX 3 at 2.141d.

115 JX 25.

2007]

DELAWARE JOURNAL OF CORPORATE LAW

to remain an "independent institution."' 6 Vogelsinger also presentedinformation to the stockholders concerning the implementation of anemployee stock ownership plan ("ESOP"). Vogelsinger touted the ESOPas a benefit to the Bank's staff and a way to infuse PNB with cash as theESOP purchased shares from PNB.' 7 Finally, Vogelsinger informed thestockholders that a necessary consequence of converting PNB to an Scorporation would be reducing the number of stockholders to a maximumof seventy-five.

On November 18, 2002, Vogelsinger sent out a letter to PNB stock-holders who were unable to attend the informal dinners that essentiallyprovided a recap of the presentation he gave at the dinners and stated that"the S Corporation model reduces taxes, makes your Bank morecompetitive and results in a more attractive investment to shareholders."' 8

Shortly after sending this letter, the PNB board formed an "S CorporationConversion Committee" on November 12,2002 to "work with.., attorneysand advisers on the conversion to S Corporation Status."' 9 PNB thenretained Prairie Capital Services, Inc. to appraise PNB and determine the"fair value" of PNB common stock.2 °

The Prairie Capital valuation was dated as of December 31,2002 andarrived at a value of $40.74 per share of PNB common stock.21 The PrairieCapital conclusion, which is described in more detail later, was based ona weighting of three major valuation analyses: 1) a discounted cash flowvaluation (20% weight); 2) a comparable companies valuation (40%weight); and 3) a comparable acquisitions valuation (40% weight). ThePrairie Capital DCF used projections Prairie Capital developed afterconsidering PNB's business plans and results, the Criswell Projections anda set of draft projections given to them by Vogelsinger, which PrairieCapital revised to come up with its own estimates.

The S Corporation Conversion Committee next met on February 6,2003 to discuss the Prairie Capital report and to determine whatrecommendations it would make to the PNB board. Relying on thevaluation work done by Prairie Capital, and the fact that the Merger wouldtake place months after the date of the Prairie Capital report, the Committeerecommended payment of $41.00 per share to stockholders cashed out inthe conversion.22 The Committee further stated that the proxy materials

'6JX 26 at 1.171d.18JX 27.19JX 31 at 1.20JX 29.21JX 38 at 13.22JX 34 at 2.

[Vol. 32

UNREPORTED CASES

would be distributed to stockholders in early April and recommended thata shareholder meeting take place on April 30. The full PNB board met fourdays later, on February 10, 2003, and representatives of Prairie Capitalwere present to discuss the valuation report. After discussion and apresentation by Prairie Capital, the board voted to accept the appraisal andconcluded that $41.00 per share would be fair to the cashed-out stock-holders.23

Before going on with the rest of the story, let me put to rest oneargument made in a cursory fashion by the plaintiffs. That is the notionthat the record reflects that the PNB board ruled out options like a sale ofthe Bank in order to entrench itself. The plaintiffs did not bother to presentany director other than Vogelsinger as a witness. As will be discussed,Vogelsinger is the only director also involved in management. Almost allof the directors own sizable blocs of PNB stock. Nothing in the recordindicates that they chose to turn their backs on attractive merger oracquisition options to preserve their board positions, which the plaintiffsdo not even argue provide them with material fee income. In fact, the largestock ownership of the independent board majority suggests that they hada healthy incentive to pursue a sale or merger of the Bank if that promisedto benefit stockholders. The mere fact that Vogelsinger's July 22, 2002memorandum notes the reality that, in certain types of mergers, the existingboard could lose control of the Bank's destiny, and raises the question ofwhether the stockholders would receive an appropriate premium for thattransfer of control, does not, in itself, come close to convincing me that theboard acted to entrench itself. The Merger price may be tainted, but therecord does not support the inference that the board fixated on the Scorporation conversion, and rejected other options, because those otheroptions would risk the loss of their board seats.

E. The Proxy Materials

After the board voted in February to approve the Merger at a priceof $41.00 per share, PNB sent the proxy materials to stockholders onApril 9, 2003. The proxy statement scheduled a special meeting ofstockholders to occur on April 30, 2003 to "elect ten directors and to voteon an Agreement and Plan of Reorganization."24 The proxy statementfurther stated that "the Board of Directors unanimously recommends thatyou vote for the directors and for the approval of the reorganization" 25 and

23JX 33 at 2.24 jX 12 ("Proxy").251d.

2007]

DELAWARE JOURNAL OF CORPORATE LAW

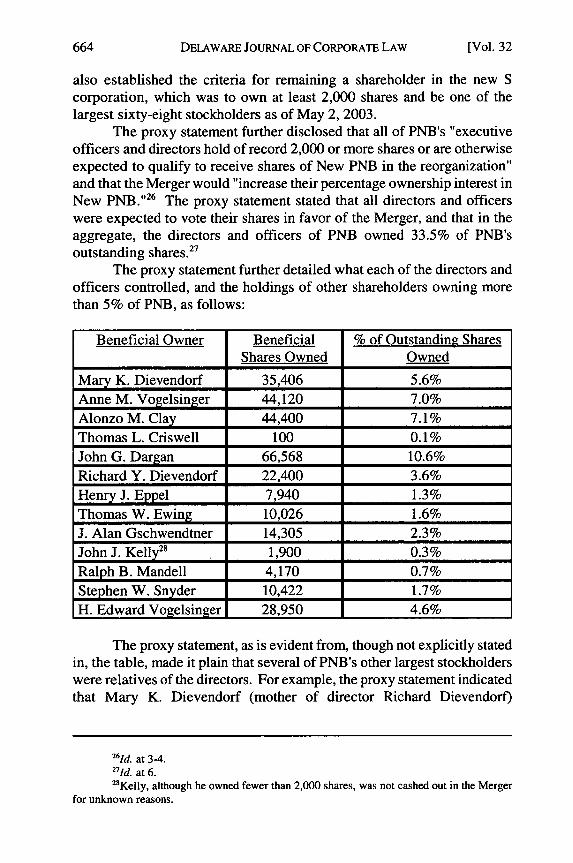

also established the criteria for remaining a shareholder in the new Scorporation, which was to own at least 2,000 shares and be one of thelargest sixty-eight stockholders as of May 2, 2003.

The proxy statement further disclosed that all of PNB's "executiveofficers and directors hold of record 2,000 or more shares or are otherwiseexpected to qualify to receive shares of New PNB in the reorganization"and that the Merger would "increase their percentage ownership interest inNew PNB. '26 The proxy statement stated that all directors and officerswere expected to vote their shares in favor of the Merger, and that in theaggregate, the directors and officers of PNB owned 33.5% of PNB'soutstanding shares.27

The proxy statement further detailed what each of the directors andofficers controlled, and the holdings of other shareholders owning morethan 5% of PNB, as follows:

Beneficial Owner Beneficial % of Outstanding SharesShares Owned Owned

Mary K. Dievendorf 35,406 5.6%Anne M. Vogelsinger 44,120 7.0%Alonzo M. Clay 44,400 7.1%Thomas L. Criswell 100 0.1%John G. Dargan 66,568 10.6%Richard Y. Dievendorf 22,400 3.6%Henry J. Eppel 7,940 1.3%Thomas W. Ewing 10,026 1.6%J. Alan Gschwendtner 14,305 2.3%John J. Kelly 28 1,900 0.3%Ralph B. Mandell 4,170 0.7%Stephen W. Snyder 10,422 1.7%H. Edward Vogelsinger 28,950 4.6%

The proxy statement, as is evident from, though not explicitly statedin, the table, made it plain that several of PNB's other largest stockholderswere relatives of the directors. For example, the proxy statement indicatedthat Mary K. Dievendorf (mother of director Richard Dievendorf)

261d. at 3-4.271d. at 6.28Kelly, although he owned fewer than 2,000 shares, was not cashed out in the Merger

for unknown reasons.

[Vol. 32

UNREPORTED CASES

controlled 5.6% of the shares, and that Anne Vogelsinger (mother ofdirector Ed Vogelsinger) controlled 7.0% of the shares. That table alsoincludes the shares owned by the spouses of the directors and otherstockholders.

Aside from information on the criteria to remain a shareholder andinformation about the directors, the proxy materials also included thePrairie Capital report. Notably, that report included the projections foryears 2003-2007 that Prairie Capital utilized in its discounted cash flowanalysis. The proxy statement did not disclose the Criswell Projections,which had been prepared in 2000.

The proxy statement also contained other PNB financial information.The proxy statement provided the consolidated financial statements ofPNB, including its income statements, balance sheets, and return on assetsand equity data, for 1998-2002. The Prairie Capital report contained PNB'sfinancial statements for the years 1996-2002. The proxy statement alsoprovided the unaudited income and balance sheet data from the first quarterof 2003 and offered a comparison with the financial results from the samequarter of 2002. It listed the book value per share of PNB stock as $36.50as of December 31, 2002 and the high market value for 2002 as $38.75 pershare.29 That is, the $41.00 per share offered to cashed-out stockholdersrepresented approximately a 12% premium over PNB's book value and a6% premium over market value. As to market value, it is worth observinghere that PNB's stock did not trade on a stock exchange; rather, when itsshares traded, they did so sporadically through transfers within thecommunity or as a result of over-the-counter or broker-to-broker trades onthe pink sheets.

F. The Shareholder Vote

As of March 1, 2003, PNB had approximately 360 stockholders ofrecord and 629,452 shares outstanding.3° As mentioned, the directors held33.5%, or 211,181, of the outstanding shares. According to an affidavitfiled by Vogelsinger later that month, on March 31, 2003, there wereactually 630,097 shares authorized to vote on the conversion.3' Of theoutstanding shares, 582,293 returned a proxy or attended the shareholdermeeting on April 30, 2003, and the remaining 47,804 neither returned aproxy nor attended the shareholder meeting.32 Of the 582,293 shares that

291d. at 5.30Id. at 19.3 1Vogelsinger Aff. 3.3 2

1d

20071

DELAWARE JOURNAL OF CORPORATE LAW

were actually voted, 538,951 shares (92.6%) voted in favor of the Merger,30,872 (5.3%) shares voted against the Merger, and 12,470 (2.1%) sharesabstained.33

Those figures represent the aggregate vote of all PNB stockholders,including the directors and other stockholders who would remain in the Scorporation. When looking at a vote of only those PNB stockholders whowere not eligible to remain stockholders after the Merger, who held a totalof 94,742 shares, 35,346 shares (37.3%) did not return a proxy, 46,224shares (48.8%) voted in favor of the Merger, 5,846 (6.2%) dissented andsought appraisal, 4,066 shares (4.3%) voted against the Merger, and 3,260shares (3.4%) abstained. 4 By a margin of 1,147 shares, then, PNB failedto get a majority of the outstanding shares to be cashed-out to vote in favorof the Merger. Following the vote, though, the owners of all the shares thatfailed to return a proxy, abstained, or voted against the Merger exchangedtheir shares for the $41.00 per share consideration except the 5,846 sharesrepresented in the Appraisal Class and the 3,000 disputed shares.

II. The Equitable Claim

As noted, this is a consolidated equitable/appraisal action. Atbottom, both the equitable claim and the appraisal claim rest on the notionthat the $41.00 per share paid in the Merger was unfair. Before theplaintiffs in the equitable action can proceed to a value determination,however, they have to do some convincing that the appraisal petitionersneed not. In view of that reality, I therefore consider the key issues uniqueto the equitable claim first.

The thrust of the plaintiffs' argument in the equitable action issimple. They contend that the Merger is subject to stringent entire fairnessreview under two alternative theories. The first is that the PNB boardshould be considered as a monolith and that given the board's voting powerand board control, the Merger should be analyzed as if it were a squeeze-out merger proposed by a controlling stockholder and subjected to the ruleof Lynch.35 Alternatively, the plaintiffs argue that the PNB board wascomprised of large PNB stockholders, who would remain as stockholdersafter the Merger and, therefore, had a financial interest in ensuring thatPNB paid as little as possible to the departing stockholders. Having

331d. at 4.'This figure counts the 3,000 disputed shares of Ethel Carlson Hoerner in the category

of shares that did not return a proxy, rather than as members of the Appraisal Class who dissented.5638 A.2d 1110.

[Vol. 32

UNREPORTED CASES

devised and implemented an "us versus them" business strategy, the board,the plaintiffs argue, must prove that they were fair to the "them."

A. Is The PNB Merger Presumptively Subject To Entire FairnessReview?

One important threshold question is whether the Merger by whichPNB converted into an S corporation should, as a presumptive matter, bereviewed under the deferential business judgment standard or whether itshould be reviewed under the more exacting entire fairness standard.

The plaintiffs advance two theories why entire fairness reviewshould apply. One of them can be disposed of easily. That is the theorythat the PNB directors could be conceived of singularly, as comprising a"controlling stockholder" group. That the plaintiffs would like to charac-terize this situation as involving a squeeze-out merger of minoritystockholders by a controlling stockholder is not surprising. Absent clarify-ing guidance from our Supreme Court, after Lynch, it is difficult for thiscourt to subject such a merger to anything but entire fairness review,regardless of whether the proponents of the transaction employed all theprocedural protections necessary to replicate an arms-length merger, bynegotiating the transaction with a special committee of independentdirectors and conditioning the transaction on a non-waivable majority-of-the-minority vote."

The problem for the plaintiffs here is that they did not prove that thePNB board may be conceived of as a single, monolithic controller.Remember that the Delaware case law in this area (that is, the Lynch lineof jurisprudence) has been premised on the notion that when a controllerwants the rest of the shares, the controller's power is so potent thatindependent directors and minority stockholders cannot freely exercisetheir judgment, fearing retribution from the controller.37 For this reason(which is in great tension with other aspects of our law),38 thejurisprudencehas required that such transactions always be subject to fairness review.

The present context is far removed from that which gave rise to theLynch line of cases. Under our law, a controlling shareholder exists when

36See Lynch, 638 A.2d 1110. The evolution of this body ofjurisprudence is detailed in,among other decisions: In re Pure Resources, 808 A.2d 421 (Del. Ch. 2002); In re CysiveS'holders Litig., 836 A.2d 531 (Del. Ch. 2003); In re JCC Holding Co., Inc., 843 A.2d 713 (Del.Ch. 2003); In re Cox Commc'ns S'holders. Litig., 879 A.2d 604 (Del. Ch. 2005).37See In re Pure Resources, 808 A.2d at 443-45.

38E.g., Aronson v. Lewis, 473 A.2d 805, 814 (Del. 1984); see also Leo E. Strine, Jr., TheInescapably Empirical Foundation of the Common Law of Corporations, 27 DEL. J. CORP. L.499, 506-07 (2002) (describing this tension).

20071

DELAWARE JOURNAL OF CORPORATE LAW

a stockholder: 1) owns more than 50% of the voting power of acorporation; or 2) exercises control over the business and affairs of thecorporation.39 Here, neither test is satisfied.

For starters, even taken together, the directors and officers of PNBdid not control a majority of the company's voting power. Thus, the firsttest is not met without considering other individuals in addition to thedirectors themselves.

Nor is the second test met. The second test exists to allow the lawto impose fiduciary obligations on stockholders who, although lacking aclear majority, have such formidable voting and managerial power thatthey, as a practical matter, are no differently situated than if they hadmajority voting control. But the second test is not an easy one to satisfyand stockholders with very potent clout have been deemed, in thoughtfuldecisions, to fall short of the mark.' Nonetheless, it is clear that there isno absolute percentage of voting power that is required in order for thereto be a finding that a controlling stockholder exists; in Lynch itself, thecontroller owned 43.3% of the shares.4

Here, though, the plaintiffs start from an overall level of ownershipthat is relatively low. Taken as a group, the directors and officers owned33.5% of PNB's outstanding shares. At that level of ownership, a singlestockholder would not be deemed a controller without additional factssupplementing his clout.42 For example, in Cysive, a person holding 35%,and an option to purchase another 0.5% to 1.0%, of the stock was deemedto be a controller because he was also Chairman and Chief ExecutiveOfficer, and his brother and brother-in-law, who were both employed by thecompany, held another 0.5% of the stock.43 In addition, after trial, he wasdeemed to wield influence over another director who owned 1% of thecompany's shares with an option to purchase 3-4% of the shares.' Givenhis managerial clout over his siblings and the fact that he brought them intothe company, his overall managerial dominance, and the practical blockingpower he had over other transactions, that person was deemed a controller

3 9Lynch, 638 A.2d at 1113-14.4°E.g., In re Western Nat'l Corp. S'holders Litig., 2000 WL 710192 (Del. Ch. May 22,

2000); Citron v. Steego, 1988 WL 94738 (Del. Ch. Sept. 9, 1988).4 'Lynch, 638 A.2d at 1112.42E.g., Kaplan v. Centex Corp., 284 A.2d 119, 122-23 (Del. Ch. 1971) ("Stock ownershipalone, at least when it amounts to less than a majority, is not sufficient proof of domination orcontrol."); In re Western Nat. Corp. S'holders Litig., 2000 WL 710192, at *6 (Del. Ch. May 22,2000) (same).431n re Cysive, 836 A.2d 531, 535 (Del. Ch. 2003).

"Id. at 552.

[Vol. 32

UNREPORTED CASES

in the context of a challenge to his merger proposal to acquire the rest ofthe company."5

Here, the facts are strikingly different. The CEO of PNB, EdVogelsinger, owned only 4.6% of the stock. Except for Vogelsinger, noneof the PNB directors was a member of PNB management. The largest bloc,10.6%, was held by another director, John Dargan. All told, some twentypeople (directors, officers, spouses, children, and parents) comprise thesupposed controlling stockholder group. The record, though, does notsupport the proposition that these various director-stockholders and theirfamily members were involved in a blood pact to act together. To thatpoint, there are no voting agreements between directors or family member.Rather, it appears that each had the right to, and every incentive to, act inhis or her own self-interest as a stockholder. 6

To find that this board was a unified controlling stockholder wouldbe unprincipled and create a negative precedent. As a general matter, it isuseful to have directors with, as Ross Perot was wont to say, skin in thegame. Such directors have a personal interest in ensuring that the companyis managed to maximize returns to the stockholders. Glomming share-owning directors together into one undifferentiated mass with a singlehypothetical brain would result in an unprincipled Frankensteinian versionof the already debatable 800-pound gorilla theory of the controllingstockholder that animates the Lynch line of reasoning. Precisely becauseeach director of PNB had a personal self-interest in the firm's performanceas a stockholder, but none had enough shares to control the corporation andemploy herself, PNB's board was arguably comprised in an ideal manner.47

451d."Evidence in the record indicates that as some of the board began focusing on converting

PNB to an S corporation, at least one director wanted to keep open the option of "stock for stockmergers with banks in the northern part of [Illinois]." JX 3 at 2. That director, Dargan, happenedto own a larger bloc of PNB stock, 10.6%, than any other director or individual PNB stockholder.Proxy at 41. Vogelsinger, referring to Dargan, also recalled that "one director in particular...wanted to see the bank sold in a stock transaction." Tr. at 697. Dargan also favored an attemptby PNB to grow to an asset size of $500 million rather than convert to an S corporation. Tr. at698. 47For a sampling of thoughtful views favoring the ownership of equity by non-management directors, see Charles M. Elson, Enron and the Necessity of the Objective ProximateMonitor, 89 CORNELL L. REV. 496, 499 (2004) ("It is important to note that while equityownership provides the incentive to monitor, it alone does not provide the proper objectivity tofoster effective oversight. Independence creates this objectivity, and that is why moderngovernance theory demands both equity ownership and independence. Independent directorswithout equity ownership may be objective, but they have little incentive to engage in activeoversight. Equity ownership provides the incentive to exercise objective oversight. On the otherhand, equity-holding directors who are not independent may have the proper incentive but lackthe necessary objectivity. Independence and equity ownership, acting in tandem, are the keys toeffective corporate governance."); R. Franklin Balotti, Equity Ownership and the Duty of Care:

2007]

DELAWARE JOURNAL OF CORPORATE LAW

There is no factual basis to ascribe to the individual PNB stockholder-directors a lack of autonomy or a cult-like devotion to Vogelsinger. Thebest that the plaintiffs can do is to point to the fact that director Dievendorf,who owned 3.6% of the shares, is a cousin of Vogelsinger. That simplefact does not come close to demonstrating that they should be consideredpart of a unified bloc.

I also reject another related aspect of the plaintiffs' controllingstockholder argument. At an inexcusably late stage, the plaintiffs attemptedto argue that any PNB stockholder with the same name and some of thesame blood as a PNB director must be deemed one and the same with them.The plaintiffs did that without fair notice before trial and without puttingthis issue in play in discovery. There was no reason for the defendant-directors to believe they had to confront the notion that their cousins ornieces, etc. should be deemed under their command and control. Moreover,the idea that children and parents always see eye-to-eye is not a premise ofour law. One can have a healthy family relationship and still feel free tovote one's stock differently than a parent. Absent some reason to believethat the vote would work a serious injury on the close relative - forexample, a vote that would ask a child to unseat her CEO father in favor ofanother director candidate, knowing that the loss of his seat would mean theloss of his job - the mere fact that relatives both own stock means little.Rather, what is critical is whether there is a reason to believe that thefamilial relationship, coupled with other important facts, is so thick that thestockholders should be treated as essentially a voting group.48 In this case,the plaintiffs have simply advanced the notion that all the relatives of PNBstockholder-directors, none of whom owns anywhere near a controllinginterest and only one of whom is a manager, would necessarily vote as

Convergence, Revolution, or Evolution?, 55 BUS. LAW. 661, 692 (2000) ("The intuitive andexperiential foundations for these principles now find additional support in empirical research thatshows that substantial equity holdings in fact promote superior board monitoring and effectivecorporate decision making. To the extent corporations respond to an equity-based presumptionof care by increasing the equity holdings of board members, the result should be improvedcorporate performance and the creation of greater wealth for the economy as a whole."); R.William Ide, Post-Enron Corporate Governance Opportunities: Creating a Culture of GreaterBoard Collaboration and Oversight, 54 MERCER L. REv. 829, 840-41 (2003) (".... the lack ofincentive to question the judgment of the CEO is exacerbated by a lack of financial interest byboard members in the corporations on whose boards they serve. There is a sense that in the longrun, it is not their money at stake. Without an equity stake in the corporation to align theirinterests with those of the shareholders, directors have less personal incentive to ensure positivecorporate performance.").

48See, e.g., Harbor Finance Partners v. Huizenga, 751 A.2d 879, 889 (Del. Ch. 2003)(discussing that a familial relationship coupled with a history of investing in, starting, andmanaging companies together was sufficient to show that a director was not able to impartiallyconsider suing his brother-in-law) (hereinafter, "Huizenga").

[Vol. 32

UNREPORTED CASES

those who share their surname suggest. Our law does not embrace thatidea.

The plaintiffs' alternative argument has more potency, although it isby no means doubtless. That argument consists in the notion that theMerger presented a situation when the stockholder-directors' personal self-interest left them disabled from disinterestedly setting the transaction price.The economics of this argument are simple. Through the Merger, the sixty-eight remaining stockholders of PNB would gain the advantages of beingstockholders in an S corporation.49 Any upside in PNB's future wouldbelong to them, exclusive of their departing brethren. To the extent that theprice paid in the Merger was lower, rather than higher, the stockholder-directors stood to benefit as all but one of them was expected to remain inthe golden circle of sixty-eight and share in the excess value retained byPNB. Even defendant-director Snyder, the exception, was not necessarilyan exception because trusts for which he served as trustee were expectedto remain. Interestingly, because the corporation was paying theconsideration, the PNB board did not face a situation where they were atodds with the entity. Rather, the conflict they faced was between them-selves, as major stockholders who would remain, and the more numerousPNB stockholders who would be cashed-out. This conflict does not dependon believing that the stockholder-directors were an undifferentiated mass,without independent perspectives on many things, but rather it arises fromthe obvious fact that they stood to benefit personally if the price PNB paidwas lower rather than higher.

Although the question is not free from doubt, on this record Iconclude that this conflict is sufficient to invoke the entire fairness standardof review. In Aronson v. Lewis,5° in the context of demand futility, ourSupreme Court stated that the business judgment rule would protect only"disinterested directors whose conduct otherwise meets the tests of businessjudgment,"5 which occurs only when directors "neither appear on bothsides of a transaction nor expect to derive any personal financial benefitfrom it in the sense of self-dealing, as opposed to a benefit which devolvesupon the corporation or all stockholders generally."52 The Supreme Courtlater refined the language of Aronson and determined that director self-interest exists "whenever divided loyalties are present, or a director hasreceived, or is entitled to receive, a personal financial benefit from the

49See Delaware Open MRI, 879 A.2d at 328.50473 A.2d 805 (Del. 1984).5"Id. at 812.521d"

20071

DELAWARE JOURNAL OF CORPORATE LAW

challenged transaction which is not equally shared by the stockholders."53

This analysis "flows from . . . the factual allegations pertaining to theinfluences upon the directors' performance of their duties generally, andmore specifically in respect to the challenged transaction."54 This court hasemployed the Rales analysis of whether a director received a personalfinancial benefit not shared equally by stockholders in making thedetermination whether a transaction is subject to entire fairness or businessjudgment review.55 Therefore, when determining whether the PNBdirectors were financially interested in the Merger, I must determinewhether they had divided loyalties or received a financial benefit notavailable to stockholders equally.

The type of financial benefit that the defendants received from theMerger is not a paradigmatic example of a benefit that is not equally sharedby the stockholders. For example, in Gentile v. Rossette, the stockholdersalleged that a director, who was also the company's controlling shareholder,conditioned approval of the merger on his receipt of a special benefit,namely a put agreement, that was not made available to the otherstockholders at all.56 Similarly, in Orman, shareholders cashed out in amerger alleged that two of the company's directors received benefits, oneallegedly received fees from a consulting contract while the other director'scompany stood to receive $3.3 million in fees if the merger closed, thatclearly were unavailable to the stockholders of the target company.57

What is different here is that the defendant-directors created, bydefinition, a transactional context that created subclasses of the PNBcommon stockholders.58 One class would remain; the other would go. The

53Rales v. Blasband, 634 A.2d 927, 933 (Del. 1993) (internal emphasis omitted).54 1d.55See Orman, 794 A.2d at 29; see also Feldman v. Cutaia, 2006 WL 920420, at *6 (Del.

Ch. Apr. 5, 2006) (discussing interestedness in the context of a motion to dismiss under Rule12(b)(6) and Rule 23.1); Gentile v. Rossette, 2005 WL 2810683, at *8 n.79 (Del. Ch. Oct. 20,2005) (addressing director interestedness at the summaryjudgment stage), rev'don other grounds,No. 573,2005, slip op., _ A.2d _ (Del. 2006); In re Freeport-McMoran Sulphur, Inc. S'holdersLitig., 2005 WL 1653923, at *7 (Del. Ch. June 30, 2005) (same).56Gentile, 2005 WL 2810683, at *5.

5 7Orman, 794 A.2d at 29-31.5 8The predicament that the PNB directors faced is analogous to, but more serious than,

the situation that a board faces in a self-tender offer, where "the interest of the corporate offeror... is to pay the lowest price possible; the interest of the stockholders... is to receive as high aprice as possible." Eisenberg v. Chicago Milwaukee Corp., 537 A.2d 1051, 1057 (Del. Ch.1987). Here, the structure of the Merger also "gives rise to a potential conflict of the directors,which calls for procedural protections for the stockholders whose interests may not be adequatelyrepresented." Id. In Eisenberg, then-Vice Chancellor, now Justice, Jacobs went on to concludethat adequate disclosure was an adequate safeguard of the shareholders' interest because a self-tender is voluntary. Here, though, the Merger contemplated that shareholders would be cashed-outinvoluntarily. That is, shareholders would be cashed out regardless of their vote so long as a

[Vol. 32

UNREPORTED CASES

class that would remain would profit, at the other's expense, if it underpaidthose departing.

On the facts here, I conclude that the defendants' status as majorstockholders who were eligible to remain rendered them conflicted. Asfiduciaries for all the common, they were obliged to treat all stockholdersfairly. That does not mean that they could not propose a transactionwhereby certain common stockholders would be cashed-out against theirwill. Of course, they could. The question is how the board could dischargeits obligation to the departing stockholders in a situation when the board'sown self-interest conflicted with the interests of stockholders generally. Insuch a circumstance, the core insight of the entire fairness standard comesinto play: to wit, even when acting in subjective good faith, a person whostands on one side of a transaction may not act fairly towards the person onthe other side.

That insight is relevant here. Unlike the defendants, I cannotconclude that the defendant-directors did not have a material interest in theMerger. Most of them had significant blocs of stock in PNB, ownershipthat seems to have preceded and inspired their willingness to serve asdirectors. The stock was not an after-the-fact indicia of ownership resultingfrom board service.59 Given what the defendants have said about thecommunity in which PNB operates, and given what one knows about themedian income in this nation,' it would be difficult to call the annualdividends received by the directors trivial. Notably, one of the purposes ofthe transaction was to reduce the effective taxation of those dividends.Upon consummation of the Merger, the directors and officers of PNB stoodto capture nearly 42% of those dividends for themselves, and wouldcomprise ten of the sixty-eight eligible stockholders.6 ' In concluding thatthe directors faced a conflict, I do not wish to be exaggerative. It was notas if they were selling their homes to the corporation in the Merger andsetting the price. But nor was this an every day transaction; it was a majortransaction for PNB and its directors were among the company's largest

majority of shareholders, which included 33.5% ownership by the directors, approved thetransaction.

59In other words, these directors were not given stock as an emolument for service on apublic company board in a hoped-for attempt to make them think like owners. These directors,I infer, came to the board because they were owners.

The median household income in Livingston County in 2002 was $44,712. JX 22 at 9.Nationally, the median household income was $51,742. See UNITED STATES CENSUS BUREAU,MEDIAN FAMiLY INCOME (IN 2002 INFLATION-ADJUSTED DoLLARs) (2002), available athttp://www.census.gov/acs/www/Products/Ranking/2002/R 14T040.htm.

61 Proxy at 3-4.

2007]

DELAWARE JOURNAL OF CORPORATE LAW

stockholders. On this record, I cannot conclude that the pricing of thetransaction was immaterial to these directors.

In this context, the family ties between the directors and non-directorstockholders are relevant. Although I cannot conclude that the PNB boardcan be considered a single mind, comprised of all shares owned byindividuals related in any way by blood, there is evidence in the record thatdirectors communicated with certain family members and aided them inremaining within the PNB stockholder family.62 Although the defendantssay that any PNB stockholder could have sought out to buy up enoughshares to make it to the golden circle, PNB shares did not trade regularly.To get them, one had to find someone in the community willing to sell.

In that respect, it appears that several of the directors actuallytransferred some shares to family members in order to help them gaineligibility. To put this in perspective, of the sixty-nine stockholders 63

remaining after the Merger, twenty-seven are related to the directors.'Many of those relatives held in excess of 2,000 shares well in advance ofthe Merger, but testimony from Vogelsinger himself indicated that severalof the relatives, specifically the children of directors Gschwendtner,Dargan, and Clay, were able to survive the fate of being cashed out byreceiving "shares as a gift from their parents., 65 In fact, the stockholderslist as of March 28, 2003 indicates that Michael Spence, Dargan's stepson,increased his PNB ownership from 300 shares to 2,532 shares as a result ofa transfer of shares from Dargan.6 Similarly, the shareholder list indicatesthat Virginia Clay Welch, Clay's daughter, owned only 1,500 shares as ofMarch 28, 2003, but Vogelsinger testified that she remained a shareholderin PNB after the Merger.67 In the quest to remain a PNB stockholder, thefamilies of PNB directors were more equal than others. When the raceended, the results were that of the hundreds of PNB stockholders before theMerger who were not related to a member of the board, only thirtyremained after the Merger. Put simply, a majority of the individuals whoowned PNB stock before the Merger ended up on the outside looking in.That the directors of PNB took steps to include members of their family inthe class of remaining stockholders is indicative of the importance they

62Tr. at 774-77.63As discussed earlier, the proxy materials indicated that the largest sixty-eight

shareholders would remain shareholders, but after the vote and Merger, sixty-nine shareholdersremained.

'Def. Ltr. at 2 (June 30, 2006).65Tr. at 775.66JX 54.671d.; Tr. at 777.

[Vol. 32

UNREPORTED CASES

ascribed to continued ownership in PNB. Given that, I find it impossibleto infer that the economics of the Merger were immaterial to them.

In view of all the facts, the PNB board majority was not positionedto make a judgment about the Merger consideration that is entitled, as apresumptive matter, to business judgment rule protection.68 Rather, theconflict they faced requires that they prove the fairness of the price paid,unless they can point to some other circumstance relieving them of thatburden. Those circumstances traditionally include approval of thetransaction by disinterested directors, preferably constituting a boardmajority or as a special committee.69 But the PNB board all suffered thesame conflict and made no attempt to add directors representing thestockholders to be cashed-out. At best, the board employed an investmentbank to give them an opinion about the price to be paid. But that move, initself, does nothing to invoke the business judgment rule.

Therefore, the only basis for the defendants to escape entire fairnessreview is by showing that an informed majority of the departing PNBstockholders approved the Merger. I turn to that issue next.